intellectual property rights, strategic technology ...home.tm.tue.nl/rbekkers/bekkers duysters...

TRANSCRIPT

Research Policy 31 (2002) 1141–1161

Intellectual property rights, strategic technologyagreements and market structure

The case of GSM

Rudi Bekkersa, Geert Duystersa,∗, Bart Verspagenba Eindhoven Centre for Innovation Studies (ECIS), Eindhoven University of Technology, P.O. Box 513,

NL-5600 MB Eindhoven, The Netherlandsb ECIS and MERIT, Maastricht University, Maastricht, The Netherlands

Received 14 November 2000; received in revised form 15 May 2001; accepted 6 November 2001

Abstract

This paper investigates the role of intellectual property rights (IPRs) in shaping the GSM (global system for mobilecommunications) industry. This industry is an example of a high-tech industry in which standards play a large role. In theprocess of designing the GSM standard, a lot of attention has been given to IPRs, mainly to avoid a situation in which a single IPRholder could hamper or even totally block the development of the standard. Nevertheless, the ultimate GSM standard containsa large amount of so-called ‘essential IPRs’, i.e. IPRs without which the implementation of GSM products is impossible.

The GSM case provides an interesting example of how (essential) IPRs ownership and alliance networks influence eachother, and how both of them affect market structure and market shares. The play with the essential GSM IPRs, and the strategyof Motorola in particular, is found to have dramatically changed the standardization processes in the telecommunicationsindustry. Where IPR was considered a non-issue in this sector for many decades, it is now among the main issues to beresolved for any new standard, as has recently been shown with the standardization of third-generation mobile networks. Ourfindings with respect to alliances reveal that timing of the emergence of strong network positions is in line with the findingson essential IPRs. We found for three of the four dominant network players that their position in the network is based onownership of essential IPRs. The relationship between market power (inclusion in the top-5 equipment suppliers) and thetwo variables of our main interest (essential IPRs and network centrality) is found to be a positive one with some notableexceptions. © 2002 Elsevier Science B.V. All rights reserved.

Keywords: Innovation strategies; Strategic alliances; Patents; Telecommunications

1. Introduction

The notion of the knowledge economy implies thatknowledge has become a firm’s primary means of

∗ Corresponding author. Fax:+31-40-2474646.E-mail addresses: [email protected] (R. Bekkers),[email protected] (G. Duysters),[email protected] (B. Verspagen).

generating profits. The large body of literature on thesubject (for an overview see, e.g. Boisot, 1998) seemsto point to the important conclusion that the extent towhich a firm can generate and exploit economicallyuseful knowledge depends on factors that include(strategic) management decisions as well as externalfactors. How these factors influence the link between(un)successful knowledge accumulation and marketexploitation differs greatly between technology fields

0048-7333/02/$ – see front matter © 2002 Elsevier Science B.V. All rights reserved.PII: S0048-7333(01)00189-5

1142 R. Bekkers et al. / Research Policy 31 (2002) 1141–1161

or sectors, however. It is the aim of this paper toinvestigate, analyze and describe this link betweenknowledge generation in firms and external factorsin the specific context of mobile telecommunications,more specifically the development of the GSM (globalsystem for mobile communications) system.1

We chose the GSM industry because it providesan example of a successful technological and mar-ket standard. With the increasingly important roleof standards in the telecommunications industry (wewill discuss this in more detail below), the under-standing of how a successful standard can be set alsobecomes increasingly important. The crucial aspect inthe standard setting process with regard to knowledgelies in intellectual property rights (IPRs). Especiallyso-called essential IPRs (without which products ad-hering to the standard cannot be manufactured), playan important but complicated role. Obviously, there issome tension between the private character of IPRs,and the public interest that a standard wants to foster.2

As will be argued in the next section, this gives riseto a complicated process of negotiations, of whichthe GSM case was one of the first to take place inEurope within the information age. Drawing lessonson the relation between ownership of essential IPRsand other technology-related intangible assets thusseems to be of importance, both from a policy andscientific point of view.

With multiple firms owning (essential) IPRs em-bodied in a standard, strategic technology alliances areof crucial importance. Holders of essential IPRs maycross-license to each other, or engage in (partly) otherthan licensing agreements. Firms without the access toessential IPRs may use strategic technology alliancesin order to gain access to such knowledge, althoughthey may be in a relatively bad position to do so. How-ever, (essential) IPRs are obviously not the only factorhaving an impact on strategic alliances. Manufacturing

1 Originally, the acronym GSM stood forGroupe Special Mobile,named after an early group concerned with developing the standard.

2 GSM has been the first case where a serious clash betweenIPR and standards occurred. Later, other clashes have followed,like those with the VESA local bus (VL-bus) for PC graphic cards,the MPEG2 compression standard for storing and transmittingvideo and audio content, with the DVD standard for storing videocontent and, more recently, with UMTS. For MPEG2 problems,see Iversen, 1999, p. 96. For the VESA local bus, see Bekkersand Liotard, 1999, p. 65 and Iversen, 1999, p. 96.

capabilities, (tacit) knowledge not laid down in IPRs,or previously obtained market positions are all exam-ples of other factors that may influence the degree towhich a firm is able to attract partners.

Although relatively neglected in the traditional lit-erature, co-operative agreements have now becomean important and recurrent issue in strategic man-agement, international business, industrial economicsas well as in organization studies. Scholars in thefield of innovation studies (e.g. Nooteboom, 1999;Hagedoorn and Schakenraad, 1993, Archibugi andPianta, 1996) have observed a declining importanceof large in-house R&D laboratories, and a simulta-neous increase in interfirm co-operation. Although,the innovation literature has been rather neglectingthe ex-post innovative performance effects of strate-gic alliances, an increasing number of publicationshas shown that strategic alliances do indeed con-tribute significantly to the innovative performance ofcompanies (for an overview see e.g. Duysters andHagedoorn, 2000). Innovation can therefore, no longerbe seems as the sole outcome of internal accumulationof know-how. In today’s turbulent business environ-ment innovation comes about by the interplay of twodistinct but related factors: endogenous R&D effortsand (quasi) external acquisition of technology andknow-how. It is often noted that a firm’s capability toabsorb externally generated knowledge by means ofstrategic alliances is to a large degree dependent onthe degree of knowledge in a specific field. Therefore,we might argue that if the core of a company’s tech-nology base is not sufficiently developed or adaptedto the new technology, then the absorption of newlyacquired external technological knowledge within thetechnological core of a company is very difficult.

The research question that we are therefore inter-ested in with regard to the GSM industry can thusbe formulated as follows. How do the ownership ofessential IPRs, the position of a firm in the overallstructure of the network of strategic technology al-liances, and the market position of a firm interact?From the answer to this question, we are interested indrawing more general conclusions for the process oftechnological standardization and the relationship be-tween technology assets and firm success in high-techmarkets where standards are important.

The main variables in our research question areinterwoven in a complex pattern of causality. For

R. Bekkers et al. / Research Policy 31 (2002) 1141–1161 1143

Table 1

Supplier Market shareswitching (%)

Market share basestations (%)

Market share mobileterminals, world-wide (%)

Rank on totalGSM market

Ericsson 48 37 25 1Nokia 14 22 24 2Siemens 21 2 9 3Motorola 1 13 20 4Alcatel 10 10 6 5Lucent 2 4 6Matra 2 3 7Italtel 0 5 8Nortel 1 0 3 9Philips 0 2 10Orbitel 0 2 11Other 1 0 13 –

Source: Bekkers and Liotard, 1999, pp. 123–124. Ranking is based on the average of all three subsystems market share, assuming thatall subsystems are roughly equally important in the total sales GSM suppliers. Recent market shares are not very different from those in1996, although for mobile terminals Nokia seems to have won a higher share at the cost of Ericsson.

example, at one level of analysis, we find that owner-ship of essential IPRs may strengthen a firm’s positionin the alliances network, and this in turn leads to mar-ket power. But at the same time, market success willenhance the firm’s technological capability (learningeffects as well as through availability of resources forR&D investment), and the same can be said aboutknowledge capital gained through networking. Hencethere is a feedback from alliances and market suc-cess to knowledge capital and patents (ownership ofIPRs). Our intention in this paper is not to disentangleall these causal links in a precise and final way, butrather to provide a narrative interpretation that is wellfounded in quantitative data and historical analysis ofthe GSM industry.

By the mid-1990s, the largest GSM networks byfar were deployed in Europe. To determine mar-ket structure for GSM infrastructure equipment, thisstudy focuses on all European GSM networks thathad 100,000 or more subscribers by the end of 1997.Market shares for the two main subsystems, calledswitching and base stations, are calculated indepen-dently and weighted against the size of each of the 33included networks. Market shares for GSM mobileterminals are world-wide figures for 1996. The resultsfor the 11 largest suppliers are shown in Table 1.3

Overall, there are five players (Ericsson, Nokia,Siemens, Motorola and Alcatel) that dominate the

3 Unfortunately, we do not have time series data on marketshares.

market. In each of the three segments that are distin-guished in Table 1, these five players hold approx-imately 85% of the market or more. Also, each ofthe five firms generally has at least a market share of10% in each of the three segments (with only threemajor exceptions: Motorola in switching, Siemens inbase stations and mobile terminals, and Alcatel in ter-minals). Other firms in the Table typically hold muchsmaller shares. Given the formulation of our researchquestion above, we will attempt to provide an answerto the question how these five firms have come todominate the market, on the basis of two major (in-teracting factors): the ownership of essential IPRs (asa result both of technological competencies of firms,and strategic management decisions), and the positionof the firm in the network of strategic alliances.

The main thread of our story is an historicaloverview4 of the GSM industry, with the processof standard setting as the most important element ofthis process. This history will be discussed in twoparts. First, Section 2 will discuss the role of IPRs inthe telecommunication sector in general, and in theprocess of GSM standard setting in general. Giventhat GSM will be described as a case in this section,the broad history of the standard will be illustrated.Section 3 will focus on essential IPRs in GSM, by

4 The historical treatment is drawn from a detailed case studypresented in full in Bekkers (2001). The sources for this casestudy consist of interviews and (secondary) literature. See Bekkers(2001) for details.

1144 R. Bekkers et al. / Research Policy 31 (2002) 1141–1161

introducing some descriptive statistics from a databaseon essential IPRs. Given that the data on essentialIPRs are firm-level data, we will illustrate the historyof GSM from the point of view of individual com-panies in this section. Among other things, we willmake a sub-division into periods: a pre-standard pe-riod that is characterized by uncertainty about futuredevelopments; a period of development of the basicstandard immediately following the decision for theGSM standard; and a final period of enhancements tothe standard combined with large scale diffusion ofthe basic technology in the market. As we will try toshow, individual firm strategies with regard to R&Dand the management of (essential) IPRs are a crucialfactor in shaping both the overall market structure inthe industry, and the structure of the alliances network.This is the second part of our story, told in Section 4.The final Section 5 will bring together the main piecesof the story and draw some general conclusions.

2. The role of IPRs in telecommunicationsand GSM

In the earliest days, of the telecommunicationssector, the ownership of IPRs largely determined itsstructure. The American Bell Telephone Company(later AT&T) owed its dominant market positionlargely to the patent of Alexander Graham Bell, andalso the ownership of IPRs for major inventions suchas the Pupin coil and the Strowger switch turned outto be of prime importance for the success of firms(Brooks, 1975). However, after the early phase ofthe life cycle of the industry, the role of IPRs in thetelecommunications sector waned with the emergenceof the state-owned monopolist networks operators,the PTTs (Post, Telegraphy and Telephony operators).This market model not only took away all effectivecompetition between telecommunications services,but also much of the competition between the equip-ment suppliers in this sector. The PTTs’ procurementprocedures usually favored national suppliers, andnational industrial policy determined which firmsreceived long-term supply contracts (Noam, 1992).

Research, a possible source for the generation ofproperty rights, was not only carried out by manu-facturers but also by the national operators, who allmaintained extensive research laboratories. For the

manufacturers, applying for IPRs had little value be-cause it would not result in larger sales, given thatthe market was largely divided by national procure-ment policies. Also, manufacturers could be forced tolicense patents to other suppliers at no costs by op-erators with multi-supplier policies (see, e.g. Noam,1992). An additional difficulty was that much of theresearch work of manufacturers was fully paid for bythe operator, resulting in questions with regard to theownership of the resulting IPRs. Operators, in turn,faced no competition from each other, and thereforefelt little need to protect their research results. It wasalso in their interest that the results of their researchwere incorporated in the equipment they purchased.

To summarize, neither operators nor supplierswould benefit widely from protecting research results.The mutual interests of operators and suppliers didnot call for comprehensive arrangements of propertyrights. A culture emerged in which it was consideredto be improper for manufacturers to demand licensingfees to operators, and this also applied to a certain ex-tent also to other manufacturers (see, e.g. Granstrand,1999).

However, starting in the 1980s, competition be-tween both network operators and equipment suppli-ers grew substantially. In Europe, this developmentwas brought about by the policy of the EuropeanCommunity, but the liberalization of this sector wasby no means restricted to the member states of theEC. In the US, the liberalization was brought aboutby technological developments, including that ofmicrowave transmission. This type of transmissionmade it possible to build long-distance links withoutthe need to run cables in public ground, which hadbeen one of the foundations of the exclusive positionof the incumbent network operators. This world-wideliberalization strongly increased the importance ofIPRs in the telecommunication sector.

At the same time, the importance of technical stan-dards for telecommunication system was growing.There were several reasons behind this develop-ment. First, the increasing demand for internationalcommunications required common standards to in-terconnect such networks. Second, the introductionof data communications between computer systems,calling for standard interfaces. This argument also ap-plied for other services, such as fax communication.Finally, the increasing complexity of terminals and

R. Bekkers et al. / Research Policy 31 (2002) 1141–1161 1145

infrastructure and the growing R&D costs associatedwith digital systems called for economies of scale, thatonly could be achieved by having common standards.

IPRs and standards obviously have a troublesomerelation (Bekkers and Liotard, 1999). While it is in theinterest of any party that wants to promote a standardto have the technological knowledge that is needed toimplement the standard diffused widely, the main aimof IPRs, on the contrary is to restrict diffusion. Theconflict is most outspoken in cases of a (semi-)publicstandard, when the formal standardization body willaim to give all interested parties equal access to thestandards they produce. Individual firms contributingto the standard and holding IPRs on their knowledgewill, on the contrary, want to enforce their exclusiverights for parts of the technologies used. Still, althoughIPRs and standards are often at odds with each other,they need to be combined, as was the case for GSM.

When IPRs get incorporated into a standard, twocases can be distinguished: essential and non-essentialIPRs. An IPR is non-essential to the standard whenother implementations are available, while the knowl-edge described in an IPR is essential to the standard ifit is the only way of ‘doing things’ while adhering tothe standard. Obviously, an essential IPR for a certainstandard has a great strategic value. During the phasewhen the standard is negotiated, such an IPR may beused as a means of blocking the standard (Granstrand,1999). After the standard has been established, an es-sential IPR has great value in negotiations about theexchange of technology, or in licensing negotiations.

There are several reasons why telecommunicationsstandards are increasingly covered by IPRs, and alsoby essential IPRs. In Bekkers and Liotard (1999,pp. 115–116), seven of such reasons are discussed.The most important ones are: (1) the high R&D in-vestments and patent intensity in this sector; (2) thedevelopment into a truly open, world-wide marketfor standardized equipment, which increases the needto protect the results of research efforts; (3) telecom-munications standards are most often compatibilitystandards, requiring that the interfaces are describedin a very detailed and conscientious way; and (4) thefact that most standards are based on proposals thatare developed by manufacturers.

The strategic value of an essential IPR is espe-cially large when there is an obligation to use thestandard, and users cannot opt for alternatives. This

obligatory situation is, in fact, the case for GSM.5 Insuch cases, owners of essential IPR know that theirlicenses are indispensable for anyone that wants tobuild products or wants to operate networks for thatparticular application.6 This makes it possible to de-mand a high fee for such licenses. Alternatively, theIPR holder could refuse monetary compensations anddemand cross-licenses instead, thus gaining access totechnology that might otherwise be difficult or im-possible to get. A licenser could also require others tolicense a whole bundle of IPRs of which only a feware actually essential to the standard. Licensees haveno choice but to buy the rights for this complete set.Also, the licenser could demand other types of com-pensations, such as the common development and/ormarketing of systems. Finally, granting licenses onlyto a limited number of other firms could relieve theactual competition on the supply market.

Furthermore, in the telecommunications industry,strong network externalities are present, leading tovery dominant standards. In some regions, the use ofcertain standards is even obligatory. This makes theconsequences of a certain strategic behavior possiblemore damaging. The first case where IPRs were ofprime importance was indeed the development of thesecond-generation European standard for mobile tele-phony, called GSM. The development of this standardstarted around 1982. At that time, the European PTTsperceived a need for a common European standardfor high-capacity mobile telephony networks. Thisnew standard could be the successor to the variousincompatible technologies that were being introducedin Europe. GSM, compared to its predecessors, wouldhave to be an improvement in a number of ways. First,

5 The standards laid down at the European TelecommunicationsStandards Institute (ETSI), including GSM, are formally voluntary.Nevertheless, there are a number of reasons why European networkoperators have virtually no choice but to use GSM for mobiletelephony networks. For example, national licenses for buildingsuch networks often refer to the GSM standard. Also, virtually allfrequency bands that are allocated by the ITU for mobile telephonyapplications in Europe are exclusively reserved for GSM networks.Furthermore, GSM is the only second-generation standard forwhich Common Technical Regulations (CTR) are available, greatlyfacilitating the procedures for bringing products on the market.

6 Many network operators pass on all possible risks associatedwith IPR infringements to their suppliers by clauses in the purchasecontracts. As a result, most licenses have to be negotiated amongmanufacturers.

1146 R. Bekkers et al. / Research Policy 31 (2002) 1141–1161

the new standard had to profit from real economies ofscale (resulting in lower equipment prices) and have alarge system capacity. Second, it would have to makeoperators less dependent on their suppliers by meansof increased competition, and by defining not only theair-interface but also other, intra-network interfaces.Third, it would also have to support lucrative roamingservices.7

The initiative for GSM was taken in the so-calledConférence Européenne des Administrations desPostes et des Télécommunications (CEPT), an or-ganization that comprised all European incumbenttelephone operators. Manufacturers initially regardedthis development with fear. They dreaded the risks as-sociated with the high development costs, and fearedJapanese competition if a common standard wouldbe defined. Network operators therefore realized thatthey needed to reduce the perceived uncertainties ofthe suppliers. Fourteen network operators then signedthe so-called GSM Memorandum of Understanding(MoU), committing themselves to procure GSM net-works. As a result, the reluctance of manufacturerschanged into enthusiasm when the potential marketsize of this standard became apparent.

Research indicated that digital technology wouldbest fulfil the capacity and cost/performance demandsof the operators, although the final decision for a dig-ital system was repeatedly postponed. Germany andFrance strongly subsidized the development of suitabletechnology, hoping to ensure a leading position fortheir national industry. In an attempt to create a headstart for their national industries, Germany, Franceand Italy signed an agreement for the adoption of anidentical, digital standard. This way, they were forc-ing the CEPT to adopt a digital standard, and theyexpected that such a standard would be based on oneof the technologies developed by German and Frenchsuppliers.

7 Roaming means that a subscriber can obtain services via guestnetworks (e.g. where the own network does not provide coverage,like abroad) via its own terminal. The user will be billed byher own operator for these services. Up to the mid-1990s, tariffsfor international telephone traffic were much higher than actualcosts. When there was roaming, also mobile network could enjoythis high margin. In the late 1990s, international tariffs for fixedtelephony dropped dramatically, but those for international mobilecalls remained high.

However, actors from other countries presentedtechnically less challenging designs that better suitednetworks in areas with medium traffic densities,whereas the German–French proposals were designedwith high traffic densities in mind. After laborioustechnical discussion, comparing various proposals,the operators finally rejected the German–French pro-posals, and decided upon a system that was largelybased on a proposal that had been submitted by Eric-sson. However, this choice was difficult to accept forthe governments of Germany and France, and politicaltalks on the highest level were held to prevent thosetwo countries from stepping out from the GSM projectaltogether. These talks, and diplomatic arrangementsbetween suppliers that secured that certain Germanand French suppliers could also play an importantrole in the selected technology eventually made thetechnology choice acceptable for these two countries.

During the period of the development of the varioustechnical proposals, actors became increasingly awareof the imminent danger of IPRs. One of the reasonsfor the rejection of the German–French proposal wasindeed that it was considered to be ‘too proprietary’.8

In 1988, under great pressure from the EC, the GSMproject was transferred from the CEPT to the newlyestablished European Telecommunications StandardsInstitute (ETSI).9 ETSI aimed for a general policyconcerning IPRs, but this came too late to serve theGSM project.

Aware of the risks that IPRs could constitute forthem, the main European operators issued an invi-tation to equipment suppliers in 1988 to tender fornetwork equipment. These operators, acting together

8 Cattaneo (1994, p. 63). It is not clear whether she refers toproperty rights owned by members of the SEL/Alcatel consortium,or more generally to the head start that consortium members wouldhave if this technology was selected. Nevertheless, both situationswere undesirable for other actors (see also Iversen, 1999, p. 93).

9 The European Community recognized that the GSM standardwould greatly facilitate the strongly wished harmonization in thissector, but regarded the CEPT not as the most appropriate bodyto set such a standard. One reason was that the CEPT was onlyopen for network operators, not for other actors involved in GSMsuch as manufacturers and candidate privately owned operators.The CEPT and its member states reacted by transferring the stan-dardization to the ETSI: a newly established standards body thatmeets all the requirements of the EC. With this new body, theGSM standardization moved to a more institutionalized and moretransparent environment.

R. Bekkers et al. / Research Policy 31 (2002) 1141–1161 1147

in the GSM MoU, produced a draft procurementprocedure in which manufacturers were essentiallyforced to give up all their IPRs and to providefor free world-wide licenses for essential patents(Garrard, 1998, p. 139, Cattaneo, 1994, p. 64, Good,1991, p. 402, and Wilkinson, 1991, p. 97). This ar-rangement was found to be unacceptable by manymanufacturers and resulted in a dispute that threat-ened the entire GSM program. Especially Motorolafrom the US, which was heavily involved in the de-velopment of GSM, stood up against the attemptedimposition (Garrard, 1998, p. 140, Wilkinson, 1991,p. 197). Under pressure of the manufacturers, theintended provisions of the operators were dropped.However, in a Musketeer’s Oath approach, a numberof operators required the suppliers of their networkto sign a declaration in which they agreed to servethe whole GSM community, both suppliers and op-erators, on fair, reasonable and non-discriminatoryconditions. Companies that decided not to accept thiscondition, as Motorola did, were not entitled to supplyequipment to those operators, but thereby prevented arestriction of their rights.

In the early 1990s, however, when the first net-works were being supplied to the operators, the IPRsproblem peaked when Motorola refused to grantnon-discriminatory licenses for its sizeable portfolioof essential patents that turned out to be essential forGSM. Motorola was only prepared to enter into alimited number of cross-licenses with selected par-ties, and also limited the geographic scope of suchlicenses to Europe. For the companies involved inthese agreements, this cross-licensing reduced marketrisks. However, for those not involved, it created bar-riers to enter the market. Several companies, includingMatra from France and Dancall from Denmark, madeunsuccessful attempts to secure licenses. Of the manyJapanese companies that showed very promising pro-totypes of GSM terminals around 1992, almost nonesucceeded to get all the necessary licenses withinthe first few years of commercial success of theGSM standard.

The behavior of Motorola strongly influenced thesupply market structure in the sector, but could notobstruct the success of the standard. European reg-ulations resulted in two or more GSM operators ineach EC member state, and GSM subscribers grewtremendously in all countries, especially from 1994

onwards. On the supply side, virtually all equipmentwas supplied by the companies that took part in thecross-licensing scheme: Ericsson, Nokia, Siemens, Al-catel, and Motorola. Many countries world-wide ex-pressed their preference for GSM, and this forced Mo-torola to lift the regional restrictions in its licenses.With the use of IPRs, Motorola succeeded in having aninteresting revenue stream even though it could not of-fer switching subsystems and even though it knew thatits market prospects were restricted. With the inter-nationalization of GSM, non-European suppliers suchas Lucent (former AT&T) and Nortel started to playa more active role, but never surpassed the successof the five champions. In the late 1990s, a numberof non-European firms (especially from Japan) finallymanaged to obtain all the necessary licenses to buildGSM terminals, but it will be difficult for them to catchup. For suppliers, the participation in cross-licensesturns out to be essential to obtain a strong market posi-tion. First of all, companies that do not succeed in se-curing all the necessary licenses simply cannot marketproducts. It is generally held that this kept many po-tential Japanese and smaller European suppliers fromthe GSM handset market. This is also the case formany smaller European suppliers.10 Secondly, thosefirms that do succeed in getting all the necessary li-censes, could be forced to pay a premium price forthem. Sometimes, IPR holders are only prepared to sella full bundle of patents that in fact only contain a fewessential ones. Our own research has indicated that thecumulative fee paid for GSM handset licenses is veryhigh, and this was recently confirmed by the actor di-rector of the ETNO,11 who revealed that royalty feesmake up to 29% of the costs of GSM handset.12 Suchprices make competing very difficult for those com-panies that are not participating in the cross-licensefees.

10 For example, one of the first companies to develop a GSMhandheld phone, Dancall from Denmark, is reported to have filed acomplaint with the Commission of the EC, in a desperate attemptto eliminate its competitive disadvantages. Pelkmans (2001). TheGSM standard: explaining a success story. Manuscript submittedfor publication.11 ETNO: European public Telecommunications Network

Operators’ Association.12 3G patent initiative devised to avoid ‘Qualcomm-type’ disputes.

(19 June 2000). TotalTele. Retrieved 4 July 2000 from the WorldWide Web:www.totaltele.com.

1148 R. Bekkers et al. / Research Policy 31 (2002) 1141–1161

3. Essential patents in GSM

Above, we have stressed the importance of es-sential IPRs in telecommunication standards, espe-cially GSM. This is why we turn now to a statisticaloverview of essential patents in GSM. Patents arethe predominant form of IPRs in telecommunica-tion. ETSI requires its members to notify essentialIPRs, and publishes these in the form of a writtenand electronic document that is regularly updated(ETSI, 1998). We used the ETSI list published inJune 1998 to get an overview of essential patentsin GSM.

The list contains 380 entries, the large majorityof which are individual patents. However, compa-nies use largely different practices in both the filingof patents and the notification to ETSI. For exam-ple, some companies apply for national patents ina few countries (usually countries with large GSMnetworks), others apply for international patents (Eu-ropean patents or PCT applications filed either atEuropean patent office (EPO) or WIPO). Some com-panies report only patents in Europe or the US, othersalso report patents in Asian countries such as China,India and Singapore. In all of these cases, what isone invention may in fact appear as several patents,because of the filing of applications in multiplecountries.

We used the EspaceNet webserver of the EPO toeliminate such ‘double counts’.13 The EspaceNetdatabase is aimed at identifying so-called patent fam-ilies, which are exactly the multiple filings of one andthe same invention. One may look up a patent docu-ment in the database by searching on features such asthe applicant or the patent number (we mostly usedthe patent numbers supplied in the ETSI list). Thedatabase will supply a list of all patent documentsfrom other patent offices (and sometimes of the samepatent office) that are equivalent to the original hit.Most of the returned patent documents can then beviewed online.

In this way, we were able to reduce the 380 entriesin the ETSI list to 140 patents. In the process, wedecided to take into account three types of patentsonly in the final list: European patents, US patents and

13 We did our searches in the database during the period January2000–April 2000.

International patents (issued with a WO number).14

The large majority of the original 380 entries can betraced back to an application in one or more of thesethree systems. The patents from the original list wedid not include (89) were patents that were not presentin the EspaceNet database (mostly patents in a fewAsian countries other than Japan), or French (sevencases) or German (three cases) patents that appearednot to be granted, although they had been filed a longtime ago. It is our impression that most of the Asianpatents are in fact covered by equivalent applicationsunder the European or US system, for two reasons.First, most of the titles of these Asian patents given inthe ETSI database are equal to patents we identified asEuropean, US or International (PCT) patents. Second,patenting in a number of Asian markets only and not inthe major GSM market (Europe) would not constitutesensible protection for a firm.

By focusing on the three most important patentsystems in the world generally, and for GSM in par-ticular, we feel that the list of 140 patents we have isa fair representation of essential IPRs in GSM. Onemay argue that the ETSI essential patent databaseis constructed from notifications of members, and itis therefore not guaranteed that all essential patentsare indeed listed in the database, neither that patentspresent in the database are actually essential to thestandard. However, we feel that it is unlikely that afirm that holds essential IPRs in GSM would concealthese IPRs from ETSI, and that therefore the proba-bility that there are essential patents for GSM that arenot in the database is small.

Additionally, we have analyzed a version of thedatabase that was published in July 1996. The latterdatabase is largely restricted to the patents that are es-sential to what we would call ‘basic GSM services’,i.e. the ones that are now implemented in virtually allterminals and infrastructure.15 Patents added to this

14 The order given in the text is also out preferred order, in thesense that if a patent has equivalents in more than one of thesethree systems, we will preferably note it as a European patent,than a US patent.15 To prevent excessive delays in the standardization process, it

was decided to publish those parts that are needed for basic speechservices first. This standard is called GSM Phase 1. Around 1994,a number of new services was finalized including circuit-switcheddata, fax, and short messages. This whole set of services is whatwe call ‘basic GSM’.

R. Bekkers et al. / Research Policy 31 (2002) 1141–1161 1149

Fig. 1. Shares of firms in essential IPRs in GSM.

list in a later stage are usually essential only for lateradditions to the standard, such as the improved voicecompression algorithmEnhanced Full Rate (EFR) andthe packet-switched data serviceGeneral Packet Ra-dio Service (GPRS). Such new services can be option-ally be implemented by manufacturers and operators.

Of the 140 patents in our database, 107 are identi-fied by an EP number (European patents), 20 are USpatents, and the remaining 13 are WO patent num-bers (International patents filed under PCT). The 140patents are held by 23 firms. Fig. 1 gives an overviewof the shares of these firms, where we have groupedall firms with only 1 or 2 patents under ‘others’. Interms of sheer numbers, Motorola is the largest, with27 patents. Nokia (19), Alcatel (14), Philips (13) andTelia (10) are the next largest holders of essential IPRsin GSM. It is notable that although operators clearlytook the lead in the GSM development and controlledthe process, they only hold a minority of the patents(BT, NTT, not shown in the figure are France Telecom,Vodafone and Nortel, who each have one patent). Thisis somewhat paradoxical given the usually extensiveresearch facilities they own.

Not all firms have applied for the patents they pos-sess by themselves. In some cases, the original appli-cants of the patents are subsidiaries, which may havebeen acquired after the original patent applications.For example, the four Ericsson patents are in fact

Fig. 2. Shares of technical fields in essential IPRs in GSM.

owned (and applied for) by Orbitel, which was lateracquired by Ericsson. Nokia owns patents that wereoriginally applied for by Voicecraft (1 patent) and theUniversity of Sherbrooke (4 patents). Philips holdspatents that were applied for by Felten & GuilleaumeFernmeldeanlagen (1 patent), and by TRT (1 patent).The patents owned by Bull were applied for by CP8Transpac (in fact, these patents were also registeredby CP8 Transpac at ETSI, we have assigned them tothe mother company Bull).

On the basis of the International Patent Classes(IPC) to which the patents were assigned by the patentexaminers, we have grouped the data into five techni-cal fields: encryption, radio transmission, speech cod-ing, switching, and other. Fig. 2 gives the shares ofthese technical classes in the total amount of patents.Switching is the largest field in terms of the numberof patents, with almost half of all patents (in fact, 61)in this field. The ‘other’ field only has 4 patents. Theother three categories are roughly similar in size, withbetween 20 and 29 patents.

The priority dates of the 140 patents range fromFebruary 1977 to December 1997, i.e. a period of morethan 20 years. In light of the history of the GSM stan-dard that we briefly reviewed above, this period can besplit into three sub periods. The first sub period runsup to the moment when the choice for the basic tech-nology was made, i.e. February 1987. In this period,different technologies and proposals were being de-veloped, at first without a clear vision of a Europeanmobile communications standard, but later on clearlywith such a goal in mind. The second sub period runs

1150 R. Bekkers et al. / Research Policy 31 (2002) 1141–1161

Fig. 3. Cumulative share of essential patents in GSM as a functionof time.

from February 1987 to roughly 1991. During this timespan, the exact implementation of the standard wasdecided upon, and product development took place inparallel. Third, during the period after 1991, new ser-vices and other additions to the standard were devel-oped and standardized.

Fig. 3 shows the total (cumulative) number ofpatents developed over the whole period. For almostthe complete period, the line is below the 45 degreesline, which indicates that there is a tendency for thenumber of patents realized in a certain time periodto increase over time. Generally, however, the de-velopment is quite smooth over time, with no majordiscontinuities that could represent sudden increasesor decreases in the speed of technological change.The only point in time where one might speak of aslight increase in the rate of patenting is the periodfrom early 1994 onwards, when somewhat of a sud-den jump is seen. This can possibly be explained bythe increased consciousness of firms of the value ofowning essential patents, if not for the basic GSMstandard, then for future, optional additions. Between1991 and 1993, the consequences of the rigorouspatent licensing strategy of Motorola16 became ap-parent, as explained above. This increased the aware-ness of firms that it was of vital importance to secure

16 The discussion of Motorola’s strategy is based on Cattaneo(1994), Garrard (1998), Hansen and Søndergård (1993), Pelkmans(2001), Granstrand (1999), Bekkers and Liotard (1999), Liotard(1999), and Iversen (1999).

access to essential patents, and that this could befacilitated by owning essential patents. Another fac-tor may be the fact that with the enormous growthof GSM subscribers, the potential revenue stream oflicenses became a more attractive prospect.

Fig. 4 shows a similar indicator for the separatetechnical fields, with the exception of the small ‘other’field. Several interesting issues arise from this figure.First, it is clear that encryption was the field that de-veloped first. In fact, the inventions in this field wereoriginally developed for a completely different fieldof application, i.e. bankcards, and were subsequentlyapplied to GSM, where they were used for the Sub-scriber Identification Module (‘SIM-card’). This ex-plains why this field shows a strong rise of the numberof essential IPRs in the early period, while the otherthree fields lag behind. Second, while developments inthis field more or less flattened out after the first waveof inventions (until 1981), a strong impulse occurredfrom 1995 onwards. Third, developments in the otherthree fields are more or less parallel. The lines ofthese three fields are remarkably similar, and are neververy wide apart. This may indeed indicate that thethree major fields of the GSM technology developedas an intertwingled set of technology, rather than asthree separate fields. Because new services and otherparts were gradually added to the standard, it alsoshows that standardization work and patenting wereiterative processes; once more services were added,more patents were applied for that relate to theseservices.

The fact that the cumulative number of essentialIPRs in GSM developed relatively smoothly over timedoes not imply that there are no differences with re-gard to timing between firms. Fig. 5 gives an indica-tion of this. The bars, which are displayed on the leftaxis, give the number of patents for each firm. Thedots give the mean priority dates of the patents by thefirm, where time is measured in months. This variableis displayed on the right axis. The vertical lines thatsurround the dots indicate a range of plus/minus twostandard deviations around the mean timing. A long(short) line thus indicates a broad (narrow) period oftechnical activity of the firm. The two horizontal linesin the figure indicate the subdivision into three periodsthat we introduced above. The part below the bottomline corresponds to the pre-standard era. The part inbetween the two lines refers to the period in which

R. Bekkers et al. / Research Policy 31 (2002) 1141–1161 1151

Fig. 4. Cumulative share of essential IPRs in GSM as a function of time, broken down by technical fields.

Fig. 5. Timing of firms with regard to essential IPRs in GSM.

1152 R. Bekkers et al. / Research Policy 31 (2002) 1141–1161

the basic choice for the standard had been made anddevelopment took place.

The part above the top line refers to the period inwhich additional services were developed. The resultsfound here largely confirms a more qualitative inter-pretation of the role of the various firms in the historyof GSM. Bull and Philips are clearly earlier than anyother firm. All their patents date from the period beforethe basic choice for the GSM standard was made, andtheir inventive activity at the time was therefore clearlymade without knowledge of the future standard. ForBull, this is related to the phenomenon that we sig-naled earlier for the encryption field. Bull, through itssubsidiary CP8 Transpac, held a number of patents re-lated to bankcards, which later became relevant for theGSM standard. Philips was initially strongly involvedin the GSM development. But Philips did not patentwith a very clear intention to exploit essential IPRsonce the standard was established, as is illustrated bythe fact that it made the licenses for its most valuablepatents (the GSM speech coder) available at no costs.

Motorola has its mean timing value right at thepoint in time when the standard emerged. Motorolawas the only non-European firm that was allowed toparticipate in the GSM project and one of the firstnon-European companies to enroll in the ETSI. Thefirm owed this special position to its significant sharein the European supply market for first-generationmobile telephony and mobile radio systems, and itsextensive European research and production facilities.As we have already argued above, however, its strat-egy turned out to be rather different than those of theother suppliers involved (see also Granstrand, 1999).

Motorola had the advantage that it already hadsome of its work from the pre-standard period laiddown in essential GSM patents. But unlike Philipsand Bull, it turned this advantage into a strong posi-tion after the standard had been decided upon. Whereother firms refrained from patenting once the basictechnical decisions were taken (i.e. during the earlyphases of the development period), Motorola intensi-fied its patenting activities. In parallel with the gradualwork of drawing up the standard and early productdevelopment, Motorola applied for numerous patentsthat turned out to be essential to the standard. It waseven accused of stealing ideas of others and applyingfor patents on them subsequently (Granstrand, 1999,p. 204). Others, in contrast, were also highly involved

in the standardization work but did not apply forpatents. They were still stuck to the traditional roleof IPRs in telecommunications, and believed therewas a ‘Gentlemen’s agreement’, in which “the de-velopers were generous to each other when it cameto potential patents” (Granstrand, 1999, p. 204). Thelicensing strategy that Motorola adopted once GSMproducts came to the market showed that this firmhad two aims with its intensive patenting activities.First, its licenses enabled it to prevent GSM frombeing adopted in other world regions in which it haddifferent interests. Second, it could set specific licenseconditions, such as cross-licensing, enabling accessto other firms’ technology and dictating the structureof the supply market.

There are four other companies with patenting ac-tivity concentrated in the second period (1987–1991):NEC, NTT, AT&T and Ericsson (Orbitel). It is strikingthat the majority (three out of four) of these companiesis non-European, and that they are all small in termsof the total number of patents. In addition, for NEC,NTT and AT&T, the patents were not primarily aimedat securing a strong position in GSM. The patentsowned by these companies were primarily developedfor application in other mobile telephony standardssuch as D-AMPS and PDC,17 and just happened tobe essential to GSM as well. In fact, none of thesecompanies showed particular interest in the GSMstandard at the time. NTT and AT&T were planningto use different technologies in their home markets.Although NEC did show some interest in developingGSM terminals (NEC announced GSM products bothat the Telecom 91 and CEBIT 92 fair), its interest inthis market seems to have waned afterwards. We thusconclude that the in period right after the decision forthe basic GSM standard had been taken, Motorolawas able to build up a strong position in essentialpatents, with other firms lagging behind considerably.

In the third period, several of the ‘lagging behind’companies strongly increased their inventive activi-ties and the patenting thereof. Especially Nokia andAlcatel were able to gain a large portfolio of essen-tial patents in GSM. For these two companies, the

17 D-AMPS: Digital Advanced Mobile Phone System, aUS-developed second-generation mobile telephony standard. PDC:Pacific Digital Cellular, a second-generation mobile telephony stan-dard developed in Japan.

R. Bekkers et al. / Research Policy 31 (2002) 1141–1161 1153

‘Gentlemen’s agreement’ not to patent inventionsthat was in force during the period 1987–1991 wasnot the most important reason behind their relativelylate entry in the patenting field. For Nokia, the mainreason is the fact that up to the early 1990s, mobiletelecommunications were only a small activity ofthis firm. In fact, telecommunications and electronicsplayed only a minor role in Nokia up till this period,and strategic research did not have a very high pri-ority. For Alcatel, the explanation is rather different.Alcatel and its predecessors (of which SEL from Ger-many is of particular importance here) have been veryactive in R&D for digital mobile telephony systems.Their first projects date from around 1981 (e.g. thegovernment-subsidized ‘Autotel’ study from 1981).The Alcatel technology for mobile communicationsbecame the basis for the German–French proposal fora standard in the field that was discussed above, andwhich became rejected in the negotiations. Alcatelwas therefore forced to make a technological re-start,in which the company had to focus on product devel-opment and not on the more fundamental mechanismsunderlying the technology. The data show that de-spite this late re-entry, Alcatel made up its lag withan impressive range of patents that turned out to beessential to new GSM services.

Going back to our main research question on thedeterminants of market dominance, what can we sayabout the relationship between the numbers of es-sential IPRs that a firm holds, and the question ofwhether or not it belongs to the ‘dominant five’ ofTable 1? Motorola, Alcatel and Nokia are the threefirms that hold the most essential IPRs according toFig. 1. Thus, for these three firms, the evidence isconsistent with the hypothesis that market dominanceis (at least partially) caused by the possession of es-sential IPRs. However, there are two firms among thedominant five (Siemens and Ericsson) that do not holdlarge amounts of essential IPRs. Also, Philips and toa lesser extent Telia and Bull have a relatively largeamount of essential IPRs, but do not enter the groupof five dominant market players. How can we explainthese cases in which the link between ownership ofessential IPRs and market shares is less clear?

Ericsson’s weak patent position can be explainedby the relative lack of importance that was given bythe company to IPRs in the 1980s and early 1990s(see, e.g. Granstrand, 1999). Although GSM was

actually based on a proposal by Ericsson, the firmholds only four essential patents, and all of these werenot developed within Ericsson itself but became itsproperty when Ericsson bought the British firm Orbi-tel. The weak patent position of Siemens is explainedby the fact that this company initially chose not to beinvolved in the GSM project at all. It entered the fieldas late as 1987 and then decided it would give prior-ity to product development instead of R&D aimed atthe fundamental mechanisms underlying GSM. As isevident from Table 1, this led to a strong focus on theproduction of GSM switches. Obviously, these two is-sues explain why Ericsson and Siemens did not buildup a strong position in essential IPRs, but they do notaddress the issue as to how these firms were able toenter the group of five dominant market parties. Wewill postpone this issue until the next section, wherewe introduce data on strategic technology agreements.

The bad market position of Philips in Table 1 is atcontrast with the relatively strong position in terms ofthe number of essential patents in Fig. 1. This can beexplained by the decision of Philips to withdraw fullyfrom the GSM field in the early 1990s, i.e. during astill relatively early stage of the market. At the time,the substantial research and product development ac-tivities carried out by Philips’ German subsidiary PKI(which was the major source of Philips’ activities inmobile communications) lead to large losses. The cor-porate Philips management did not regard telecommu-nications as one of its core activities at the time, anddecided it was no longer willing to accept the lossesincurred in these activities. PKI was thus forced towithdraw fully from the GSM industry, regardless ofthe fact that PKI had recently succeeded to win a sub-stantial amount of infrastructure orders (Metze, 1991,pp. 297–198). Years later, Philips tried to enter thetop-3 in the GSM handset market by force, but failed.

Telia and Bull are the other major firms in terms ofpatenting that do not hold substantial market share.The specific character of both firms provides a rea-sonable explanation for this discrepancy. Bull gotinvolved in the development of GSM by accident, be-cause its patents on bankcards turned out to be usefulfor SIM cards. By nature of this product, Bull nevertook an interest in producing GSM equipment, butinstead licensed out its technology. Telia still is essen-tially an operator, and hence not primarily interestedin manufacturing of equipment either.

1154 R. Bekkers et al. / Research Policy 31 (2002) 1141–1161

We are thus left with the impression that there mayindeed be a relationship between a strong positionin the ownership of essential IPRs and a dominantmarket position, but that this is certainly not a rela-tionship without exceptions. Although we are ableto explain in a reasonable way why some firms thathold many essential IPRs did not become dominantmarket parties, we have not yet been able to explainhow other firms that did become dominant marketplayers (Siemens and Ericsson) were able to do thiswithout owning a large number of essential IPRs. Aswe will argue in the next section, the answer can befound in the field of strategic technology agreements.

4. Strategic technology agreements in GSM

The data on strategic alliances used in this paper arebased on the MERIT-CATI database. We selected fromthis database the 60 strategic technology alliances thatare related to GSM technology. The expression inter-firm co-operation is used to refer to those co-operativeagreements between partners that are not connectedthrough (majority) ownership at the outset of the pe-riod under study. As it happens, some of the firmsin our analysis are merged or taken over by otherfirms in the sample during the period under study (e.g.the above example of Orbitel that gets taken over byEricsson). In principle, when this happens, we willstill treat these firms as separate entities, but make

Fig. 6. The cumulative number of strategic alliances and essential patents in GSM.

separate calculations for the situation where the twofirms are merged in the alliances data.

In this paper, we will limit our analysis to tech-nology inclined agreements. In order to safeguardthe strategic element in our sample we will studyonly those alliances that are undertaken for strategicreasons. We will refer to alliances as being strate-gic if they can reasonably be assumed to effect thelong-term product market positioning of at least onepartner. Because alliances between government oracademic institutions and private companies are oftenundertaken for different reasons than the alliancesbetween two or more private companies (see e.g.Hacklish, 1986), we will restrict our attention to thosealliances that are established between private compa-nies. For the same reason we do not pay attention togovernment initiated or EC-wide R&D cost-sharingprograms such as ESPRIT, EUREKA or JESSI.

Fig. 6 shows the cumulative total number of newlyestablished strategic technology alliances in the GSMmarket (right axis), along with the cumulative numberof essential patents that were the subject of analysisin the previous section (left axis). During the secondhalf of the 1970s and early 1980s co-operative activityremained at a rather modest level in the GSM sec-tor. It was not until the late1980s that the rise in thenumber of alliances really took off. This take-off tookplace largely in parallel with the steady increase inthe number of essential patents (priority date), whichindeed suggests a close relationship between the two

R. Bekkers et al. / Research Policy 31 (2002) 1141–1161 1155

variables. Apart from 2 years of stabilization in 1990and 1995, growth in the number of alliances persisteduntil the end of the period. Thus, strategic alliancesseem to have become an essential vehicle for technol-ogy transfer in the GSM market.

After having identified the basic trends in tech-nology partnering, we will now turn to the analysisof co-operative networks. Our main goal is to studythe changes in the overall structure of the alliancesnetwork over time, and to study the emergence offocal players in the co-operative networks of theGSM sector. The use of network analysis as a toolto analyze complex social systems was introduced inthe 1970s (see, e.g. Burt, 1976; Freeman, 1979) andfurther developed in the 1980s (see, e.g. Bonachich,1987). As argued by Nohria (1992, p. 2) “. . . networkanalysis has grown from the esoteric interest of a fewmathematically inclined sociologists to a legitimatemainstream perspective”. Network analysis can beused to analyze complex flows of information, and thesimultaneous analysis of all the relationships betweenindividual organizations may result in the descriptionof a social system that closely resembles the structureof a specific organizational field (Barley et al., 1992).

We will analyze the role of individual firms inthe GSM alliance network. For this, we will use theconcept of ‘network centrality’, which is in a way ameasure of the importance of particular players. Cen-trality in a network context refers to the importanceof a specific organization for the overall structure of anetwork. Centrality in information networks was firstintroduced by Bavelas in 1948 to assess the relation-ship between centrality and power within networks(Freeman, 1979). Advances in graph theory in lateryears have significantly broadened the use of centralitymeasures as a tool to assess the importance of a spe-cific point (or actor) in a network. In this paper we willuse three basic measures of centrality as put forwardby Freeman (1979): degree centrality (CD), between-ness centrality (CB) and closeness centrality (CC).18

The most straightforward measure of centrality isthe so-called degree centrality (CD). Degree centralityis measured by summing the total number of actors towhich a specific player is adjacent in the matrix. Thedegree of an actor is therefore equal to the total numberof direct links of a particular actor to other actors.

18 See also, Duysters and Vanhaverbeke, 1996.

The measure is standardized by dividing through bythe maximum possible number of connections (n − 1,where n is the number of firms, i.e. 48). In formalterms, degree centrality of firmk is equal to (rememberthat a is a binary variable)

CD(k) =∑

i

aik

n − 1,

actors that are represented by a high degree of degreecentrality share the ability to access a large stock ofpotential information sources.

The second centrality measure that was put forwardby Freeman is the so-called betweenness centrality(CB). Betweenness refers to the number of times anactor is located on the shortest path (‘geodesic’) be-tween two other actors. If a certain actor is directlylinked to two other actors who are not directly linkedto each other, then the first actor is said to be ‘between’the two other actors. In formal terms:

CB(k) =∑

i

∑

j<i

gij(k)

gij,

where gij represents the number of geodesic pathsbetweeni andj, andgij (k) is the number of these pathson which firmk is present.

In an information network a company that hasa high degree of betweenness centrality has a po-tential to control the flows of information betweenthose other companies (Freeman, 1979; Knoke andKuklinski, 1982). In this paper we will therefore useCB as an indicator of the ability to control flows ofinformation within a network.

Finally, closeness centralityCC is associated withthe distance between the location of a certain playerand the location of the other players in the network.Distance is measured as the length of geodesics (num-ber of firms on the geodesic). Formally, closenesscentrality is defined as follows:

CC(k) = n − 1∑idgik

,

wheredgij represents the length of the geodesic fromfirm i to firm k.

If a company has high closeness centrality in anetwork, this means that it is close to most of theother players, and hence is able to avoid the controlof others (Freeman, 1979).

1156 R. Bekkers et al. / Research Policy 31 (2002) 1141–1161

Table 2Network centrality scores, 26 firms with highest degree centrality

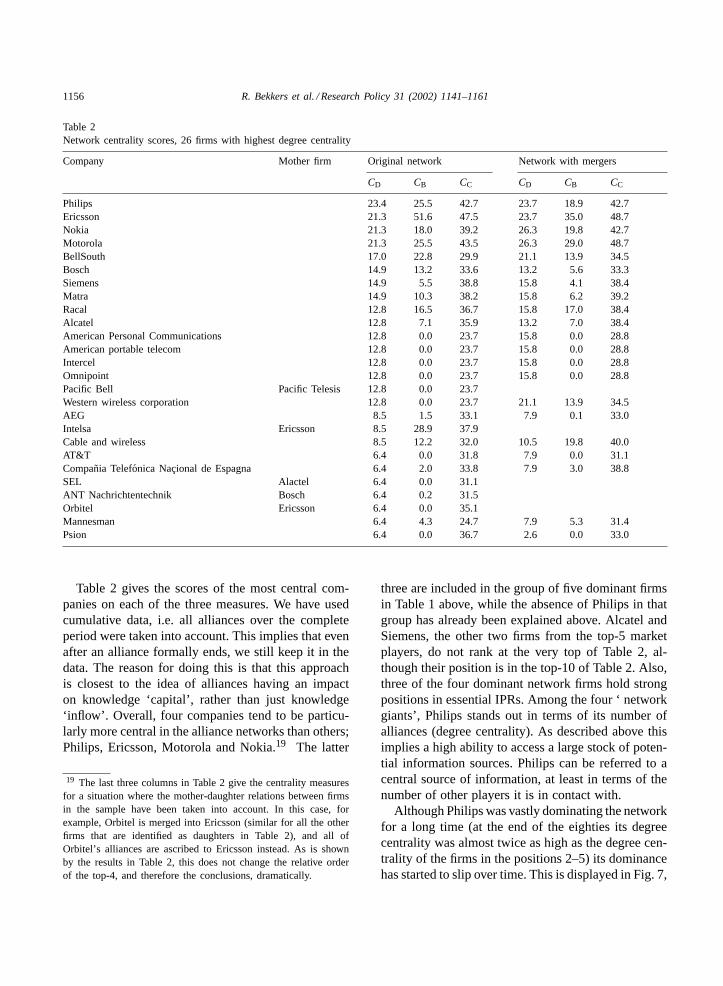

Company Mother firm Original network Network with mergers

CD CB CC CD CB CC

Philips 23.4 25.5 42.7 23.7 18.9 42.7Ericsson 21.3 51.6 47.5 23.7 35.0 48.7Nokia 21.3 18.0 39.2 26.3 19.8 42.7Motorola 21.3 25.5 43.5 26.3 29.0 48.7BellSouth 17.0 22.8 29.9 21.1 13.9 34.5Bosch 14.9 13.2 33.6 13.2 5.6 33.3Siemens 14.9 5.5 38.8 15.8 4.1 38.4Matra 14.9 10.3 38.2 15.8 6.2 39.2Racal 12.8 16.5 36.7 15.8 17.0 38.4Alcatel 12.8 7.1 35.9 13.2 7.0 38.4American Personal Communications 12.8 0.0 23.7 15.8 0.0 28.8American portable telecom 12.8 0.0 23.7 15.8 0.0 28.8Intercel 12.8 0.0 23.7 15.8 0.0 28.8Omnipoint 12.8 0.0 23.7 15.8 0.0 28.8Pacific Bell Pacific Telesis 12.8 0.0 23.7Western wireless corporation 12.8 0.0 23.7 21.1 13.9 34.5AEG 8.5 1.5 33.1 7.9 0.1 33.0Intelsa Ericsson 8.5 28.9 37.9Cable and wireless 8.5 12.2 32.0 10.5 19.8 40.0AT&T 6.4 0.0 31.8 7.9 0.0 31.1Compañia Telefonica Naçional de Espagna 6.4 2.0 33.8 7.9 3.0 38.8SEL Alactel 6.4 0.0 31.1ANT Nachrichtentechnik Bosch 6.4 0.2 31.5Orbitel Ericsson 6.4 0.0 35.1Mannesman 6.4 4.3 24.7 7.9 5.3 31.4Psion 6.4 0.0 36.7 2.6 0.0 33.0

Table 2 gives the scores of the most central com-panies on each of the three measures. We have usedcumulative data, i.e. all alliances over the completeperiod were taken into account. This implies that evenafter an alliance formally ends, we still keep it in thedata. The reason for doing this is that this approachis closest to the idea of alliances having an impacton knowledge ‘capital’, rather than just knowledge‘inflow’. Overall, four companies tend to be particu-larly more central in the alliance networks than others;Philips, Ericsson, Motorola and Nokia.19 The latter

19 The last three columns in Table 2 give the centrality measuresfor a situation where the mother-daughter relations between firmsin the sample have been taken into account. In this case, forexample, Orbitel is merged into Ericsson (similar for all the otherfirms that are identified as daughters in Table 2), and all ofOrbitel’s alliances are ascribed to Ericsson instead. As is shownby the results in Table 2, this does not change the relative orderof the top-4, and therefore the conclusions, dramatically.

three are included in the group of five dominant firmsin Table 1 above, while the absence of Philips in thatgroup has already been explained above. Alcatel andSiemens, the other two firms from the top-5 marketplayers, do not rank at the very top of Table 2, al-though their position is in the top-10 of Table 2. Also,three of the four dominant network firms hold strongpositions in essential IPRs. Among the four ‘ networkgiants’, Philips stands out in terms of its number ofalliances (degree centrality). As described above thisimplies a high ability to access a large stock of poten-tial information sources. Philips can be referred to acentral source of information, at least in terms of thenumber of other players it is in contact with.

Although Philips was vastly dominating the networkfor a long time (at the end of the eighties its degreecentrality was almost twice as high as the degree cen-trality of the firms in the positions 2–5) its dominancehas started to slip over time. This is displayed in Fig. 7,

R. Bekkers et al. / Research Policy 31 (2002) 1141–1161 1157

Fig. 7. The evolution of network centrality for the four most central firms in the network.

which gives for the (network) dominating four firmsthe evolution of the network centrality measures overtime (calculation for the cumulative set of strategic al-liances up to and including the year on the horizontalaxis). The first part of the figure shows how Philipsgradually lost its central role in terms of degree cen-trality, and how the other three firms catch up. Whatis most the interesting feature in Fig. 7 with regard toour research question is that Motorola is the first tocatch up, i.e. during the period immediately after theacceptance of the basic GSM standard (1988–1992).Nokia and Ericsson catch up much later, i.e. towardsthe end of the period.

This relative timing of the emergence of strong net-work positions is in line with the findings on essential

IPRs in Fig. 5. There it was shown that Motorola’spatent position was built up earlier than that of Nokia,and that the Philips dominant patent position was builtup exclusively during the earliest GSM phase. Obvi-ously, Ericsson is an exception to the close connec-tion between ownership of essential IPRs and a strongnetwork position.

The picture is somewhat different for the two other,more sophisticated measures of centrality. The onlything that the dynamic movement of these indicatorsclearly shares with the first one (degree centrality) isthe increase of the score of Motorola during the late1980s and early 1990s. The movement and relativeposition for Ericsson and Nokia differs quite a bit be-tween the three parts of Fig. 7. The movements of

1158 R. Bekkers et al. / Research Policy 31 (2002) 1141–1161

these two firms are rather erratic, and jumps or falls20

are mostly related to a single year, i.e. one or twoisolated alliances.

Thus, while it is possible to argue for three of thefour dominant network players that their position inthe network is based on ownership of essential IPRs,Ericsson emerges as the major exception to this rela-tionship. Despite its relatively weak position in termsof essential patents, Ericsson is a very well positionedcompany in the GSM network. Because of its strate-gic position, it is not dependent on other companiesfor its information flow, and it holds a position as agatekeeper for the flow between other companies inthe network. We attribute this exception to the factthat the basic GSM technology is based on an Eric-sson proposal, as pointed out above. Consequently,this company had a technological head start. Further-more, during the period of GSM product development(1988–1992), Ericsson set up numerous co-operationswith suppliers from different countries, thus openingup entry into many national markets (Meurling andJeans, 1994). Thus, although Ericsson did not emergewith very many essential IPRs, it definitely was asmart networker.

This purely quantitative analysis of the strategictechnology agreements network does not, however,tell the complete story with regard to the importanceof networking, although in combination with the storywe have told in connection with Fig. 5 it does providean important hint. The crucial aspect that remains hid-den in the quantitative representation of the networkis the special importance of a number of strategicalliances, more specifically a limited number of bi-lateral cross-licensing agreements between Motorolaand some other firms, all of which together (includingMotorola) have become the top-5 dominant marketplayers in Table 1. These agreements are part of theagreements that initiated the catch up of Motorolain terms of network centrality in the late 1980s andearly 1990s. The reason why these agreements havebecome so important is the strong position of Mo-torola in the field of essential IPRs as has been shownin Figs. 1 and 5. Firms that were not allowed accessto this set of Motorola essential IPRs have not beenable to enter the market in a major way.

20 Falls of the index are possible because new firms enter thenetwork, and because other firms change their position.

The catch up of Motorola in terms of networkingposition was thus largely based on the aggressivepatenting strategy the company had followed duringthe early phase of development of the GSM standard.The strategic agreements Motorola was able to strikein this way were of prime importance to the company,which was the only non-European firm that was in-volved in the development of the standard. Althoughthis different national background could be seen as acertain disadvantage, it also, however, implied someadvantages.21 Specifically, companies from the US atthe time were better aware of the value of IPRs, espe-cially after the demonstration effect of the lawsuits ofKodak versus Polaroid, and the successful defence ofTexas Instrument’s ‘Kilby’ patent before court, bothin 1985/1986.22 This resulted in a very pro-patent at-titude of US companies, and Motorola was among theAmerican companies with a relatively aggressive IPRpolicy. Additionally, Motorola always showed a tradi-tion of having to fight hard for its market share. In itsdomestic telecommunications supply sector, it had tocompete with AT&Ts vertically integrated manufac-turing company, whereas in the foreign telecommuni-cations sector it had to fight against procurement prac-tices that favored national suppliers. Motorola is alsoactive in electronics and microprocessors, and in boththese markets it had strong (domestic) competitors(e.g. Intel). Finally, Motorola’s (initial) lack of mar-ket share in Europe and its fears that GSM contractswould be awarded to European suppliers contributedto its aggressive GSM licensing practices.23

The inclusion of Nokia and Alcatel in the bilat-eral cross-licensing agreements with Motorola is inline with the relatively strong position of these firmsin the technological field, as indicated by their own-ership of substantial amounts of essential IPRs. Forother firms with a strong position in essential IPRs(Philips, Bull, Telia), it has already been explainedwhy they were not interested in manufacturing GSM

21 See Iversen (1999) for a more elaborate treatment of many ofthe points made in this paragraph with regard to Motorola.22 In Polaroid’s infringement suit against Kodak, the latter had

to pay almost US$ 1 billion for damages and was barred from theinstant-film camera market. With its so-called ‘Kilby’ patent, TexasInstrument was able to demand high royalty fees to all companiesmanufacturing integrated circuits. See Hall and Ziedonis, 2000,p. 11–12.23 Iversen (1999, p. 94).

R. Bekkers et al. / Research Policy 31 (2002) 1141–1161 1159

equipment, and the same reasons apply to the questionwhy these firms did not enter into agreements withMotorola. The inclusion of the other two parties in thebilateral cross-licensing deals, Siemens and Ericsson,need some more explanation, however.

Motorola had strong experience in developing basestation products and mobile terminals, but did not havea switching platform on which GSM switching prod-ucts could be based. Thus, it tried to strike allianceswith other suppliers that did have such a platform. Thefirm was thus in need for a partner in order to be ableto offer complete systems on the market. This is howSiemens was able to enter the deal with Motorola.As is evident from Table 1, Siemens is specializedstrongly in switching. Ericsson succeeded in securinga cross-license agreement with Motorola by virtueof having developed the selected technical proposalfor GSM. This, and its ‘smart networking’ behaviordescribed above, secured this firm an indispensableposition in the network. Additionally, Ericsson wasalready one of the largest global players on the marketfor analogue mobile telephony, and, without doubt,would have done anything within its capabilities tofight an eventual refusal of Motorola to license IPRs.

5. Conclusions and discussion

The GSM case provides an interesting example ofhow (essential) IPRs ownership and alliance networksinfluence each other, and how both of them affect mar-ket structure and market shares. We have shown howthe GSM market has become dominated by five majorfirms in the late 1990s: Ericsson, Nokia, Siemens, Mo-torola and Alcatel. Together, these five firms controlmore than 85% of the European GSM market (whichis the largest in the world). We have shown how twoof these firms (Motorola and Nokia) are characterizedby both a strong position with regard to the owner-ship of essential IPRs and a central position in thenetwork of strategic technology agreements in mo-bile communications. Two other firms score relativelyhigh on at least one of these two variables: Ericssonwith regard to network centrality (but not essentialIPRs) and Alcatel with regard to essential IPRs (butnot network centrality). Siemens has neither a strongposition in essential IPRs not in network centrality.

The relationship between market power (inclusionin the top-5 equipment suppliers) and the two vari-ables of our main interest (essential IPRs and networkcentrality) is thus at best a positive one with some ma-jor exceptions. One is thus tempted to conclude that apure quantitative analysis of the relationship betweenthese three variables leaves important parts of thestory of how these five companies came to dominatethe GSM market untold. The key to understandingthese ‘missing links’ largely lie in the activities ofone company, Motorola, during the period just afterthe technical GSM standard had been set.

We identified three periods in the history of GSM.The first is a pre-standard period (until February1987). In this period, there was huge technologicaluncertainty on which of the competing technologieswould be adopted as the standard. Thus, what laterbecame ‘essential’ IPRs (patents) to the GSM stan-dard from this period, were at the time just one of anumber of options for the future. A high number of(with hindsight, essential) patents during this perioddid not necessarily lead to later dominance in theindustry, as is shown by the evolution of the marketposition of Motorola and Philips.

Philips was the company with most essential patentsfrom the pre-standard period. However, it did not playa major role in the production and sales of GSM equip-ment afterwards, mainly because of strategic choicesof the management. Its strong early position in termsof technology and patents did, however, lead to earlydominance of the technology alliances network. Butthis position waned when other players started to de-velop the GSM standard later on.

Motorola, on the other hand, was able to use its rel-atively strong position in the pre-standard age in theperiod in a more vigorous way afterwards. During theperiod until 1991, which we characterize as the periodin which the basic standard was developed, Motorolabuilt up a strong portfolio of essential patents inGSM. Other firms, including those in Europe mostinvolved with the development of GSM (e.g. Erics-son, Siemens, Alcatel), did not follow an aggressivepatenting strategy, basically because they were usedto manners of conduct in a pre-liberalization Euro-pean market (Ericsson), or simply because they didnot have the inventions yet (Alcatel, Nokia).

By using the negotiation power that came with itspatent portfolio, Motorola could dictate its licensing

1160 R. Bekkers et al. / Research Policy 31 (2002) 1141–1161

conditions to all firms. The company thus imposed amarket structure by conducting exclusive cross-licenseagreements with a selected number of other partieson the market. These parties were selected becausetheir IPRs were valuable to Motorola (not only essen-tial patents, but also others), or because their productline complemented that of Motorola. Also Motorolatook the position of firms in the alliance network intoaccount when selecting its cross-licensing partners(Ericsson). As a result, the importance of Motorola inthe network of strategic alliances increased drasticallyin the late 1980s.

Firms that took part in the cross-licensing agree-ments (i.e. Ericsson, Nokia, Siemens, Motorola, andAlcatel) dominate the market for GSM infrastructureand terminals. They hold well above 85% of the to-tal market, which is estimated to be worth more than100 billion US$.24 Only 5 years after the first com-mercial products were introduced on the market, othercompanies, including those from the far east and fromthe American continent, gradually succeed in captur-ing some part of this huge market. In the field oftechnology and essential patenting, this process ofcatching-up took the form of a number of additionsto the standard in the form of more enhanced equip-ment or services. We denote this as the third phasein the history of GSM. This is the period when someof the major European firms (most notably Alcatel,Nokia and Telia) took out large amounts of essentialpatents in GSM. This is also the period during whichNokia and Ericsson greatly improved their position inthe alliances network.

The play with the essential GSM IPRs, and thestrategy of Motorola in particular, appears to havedramatically changed the standardization processesin the telecommunications industry. From 1992 on,many firms have intensified their patenting activities,hoping to obtain essential IPR for future standards oradditions to existing standards. Where IPR was con-sidered a non-issue in this sector for many decades,it is now among the main issues to be resolvedfor any new standard, as has recently been shownwith the standardization of third-generation mobile

24 Note 1, Communication from the Commission on strategyand policy orientations with regard to the further developmentof mobile and wireless communications (UMTS), COM(97)513,Brussels.