integrated accounting systems sage 50 accounts · pdf fileintegrated accounting systems sage...

TRANSCRIPT

1

Integrated Accounting Systems Sage 50 Accounts

Republic of Ireland

Exam Paper 2016/2017

2nd Year Examination: Exam Paper 2016/2017

Paper: Integrated Accounting Systems (Republic of Ireland)

INSTRUCTIONS TO CANDIDATES

PLEASE READ CAREFULLY

For candidates answering in accordance with the law and practice of the Republic of Ireland. Candidates should answer the paper in accordance with the appropriate provisions up to and including the Finance Act 2016. The provisions of the Finance Act 2017 should be ignored. All names and addresses mentioned are entirely fictitious. This examination paper is copyright and may not be reproduced. Candidates should allocate their time carefully. On completion of this examination: 1. Ensure that you have correctly completed the examination cover sheet and any other

documentation provided by the invigilator. 2. Ensure that all printouts (Payroll, Accounts and Excel) are in the order requested in each

section and are correctly submitted to the invigilator. 3. Ensure that PDF reports have been correctly saved and submitted to the invigilator. 4. Ensure that there is a folder (created in the location as indicated by the invigilator)

showing your examination number * as the folder name. Ensure that you have saved a backup of your Sage Micropay, Sage 50 Accounts and Excel data into the created folder.

It is the student’s responsibility to ensure that all work is saved and submitted as required above. Accounting Technicians Ireland cannot be held responsible for any marks lost as a result of the above not being completed correctly.

* NB: Ensure that you use your exam number; you must not use your student registration number or college registration number.

- 3 - -

Integrated Accounting Systems Examination 2016/2017 (ROI)

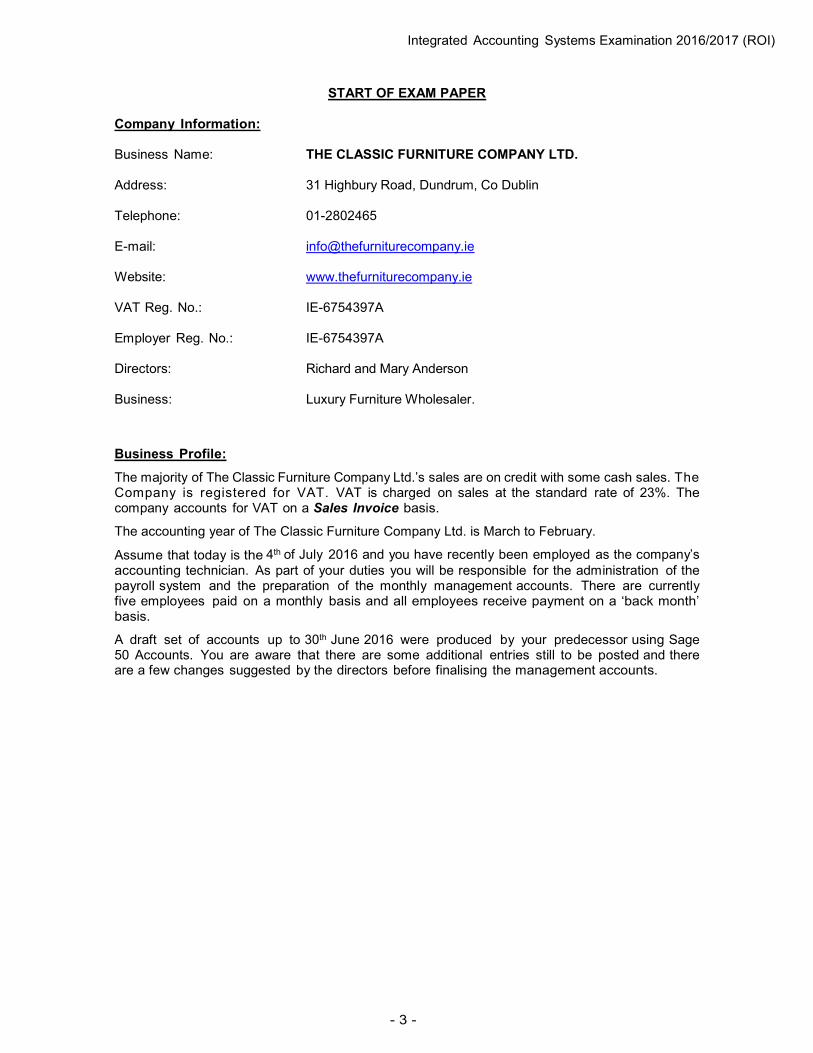

START OF EXAM PAPER

Company Information: Business Name: THE CLASSIC FURNITURE COMPANY LTD.

Address: 31 Highbury Road, Dundrum, Co Dublin

Telephone: 01-2802465

E-mail: [email protected]

Website: www.thefurniturecompany.ie

VAT Reg. No.: IE-6754397A

Employer Reg. No.: IE-6754397A

Directors: Richard and Mary Anderson

Business: Luxury Furniture Wholesaler.

Business Profile:

The majority of The Classic Furniture Company Ltd.’s sales are on credit with some cash sales. The Company is registered for VAT. VAT is charged on sales at the standard rate of 23%. The company accounts for VAT on a Sales Invoice basis.

The accounting year of The Classic Furniture Company Ltd. is March to February.

Assume that today is the 4th of July 2016 and you have recently been employed as the company’s

accounting technician. As part of your duties you will be responsible for the administration of the payroll system and the preparation of the monthly management accounts. There are currently five employees paid on a monthly basis and all employees receive payment on a ‘back month’ basis.

A draft set of accounts up to 30th June 2016 were produced by your predecessor using Sage 50 Accounts. You are aware that there are some additional entries still to be posted and there are a few changes suggested by the directors before finalising the management accounts.

- 4 - -

Integrated Accounting Systems Examination 2016/2017 (ROI)

Section A – Payroll: Log in to Sage Micropay and restore the setup Sage Micropay dataset from the location indicated by the invigilator. (The user name is USER1, the payroll name is ATI, and both passwords are PASS). You have been advised that (unless stated otherwise) all employees are entitled to 1.67 days holidays per month worked and on average an employee will work 260 days in a year. You are required to: 1. Adjust the company narrative (in Company details) to include your examination number. You do

not need to change the company name. Update the payroll period to June 2016 and record all payroll information provided below, setting up any new pay elements that may be required. You are to assume all other employees NOT mentioned below, but on the payroll of the company, earned their usual monthly salary value.

(1 Mark)

2. Set yourself up as a new employee identified by your examination number only. Insert your exam number in the first name field and complete the surname field with the word ‘student’. You commenced employment on Friday 24th June 2016. You have not yet received a copy of your P45 from your previous employer; your PPS number is 2604621R, standard PRSI code A applies and you may assume that you are paid by cheque. You will be paid at a standard rate of €12.00p/h. Overtime will be paid at time and a quarter. You are to be paid for 37.5 standard hours and overtime of 2.5 hours worked in June and you should adjust your insurable weeks for June to 1 PRSI week.

(3 Marks)

3. Michael Jackson was made redundant on the 30th June 2016. He has been employed with the company since May 31st 2010. He is to be paid a tax free statutory redundancy payment of 2 weeks pay for every year of service, plus one bonus week, up to a maximum of €600 per week. He is to receive his full month’s salary for June.

(3 Marks)

4. Mary Anderson is to receive an annual car allowance of €9,000 per annum commencing June 1st 2016 and payable monthly. She is also to be reimbursed for vouched postage expenses totalling €70.00.

(2 Marks) 5. In June 2016, Amanda Carter travelled 740 business kilometres bringing her total business

kilometres in 2016 to 6,739km. She is to be reimbursed for this expense based on current civil service rates (refer to the table below) assuming engine capacity is 1,800cc.

(2 Marks)

6. Gary Jones has opted to contribute €175 per month into the company pension scheme effective

from the 1st June 2016. The company has agreed to contribute €60 per month on his behalf. (2 Marks)

7. Print the Gross to Net report, a payslip for the new employee only, and the Control Summary report.

When you have completed processing the payroll for June 2016 ensure that you backup the Sage Micropay dataset into a folder, created in the location indicated by the invigilator, which should be titled with your examination number.

(2 Marks)

Section A Total: (15 Marks)

- 5 - -

Integrated Accounting Systems Examination 2016/2017 (ROI)

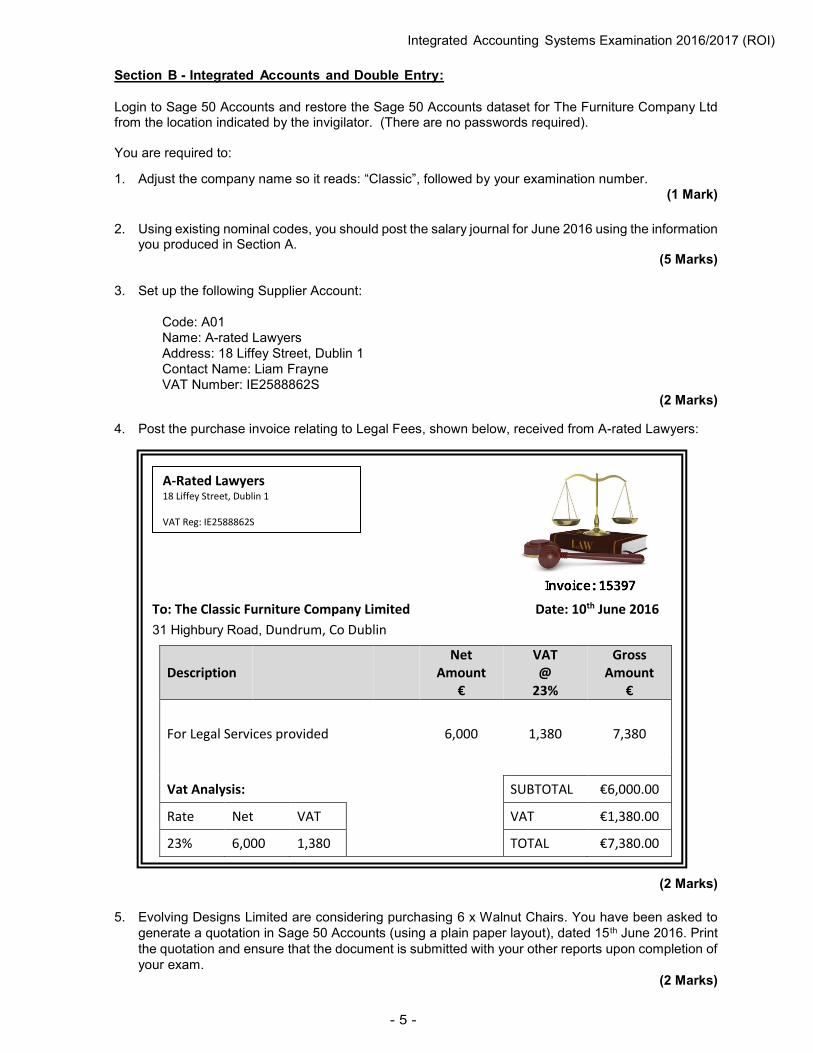

Section B - Integrated Accounts and Double Entry:

Login to Sage 50 Accounts and restore the Sage 50 Accounts dataset for The Furniture Company Ltd from the location indicated by the invigilator. (There are no passwords required). You are required to:

1. Adjust the company name so it reads: “Classic”, followed by your examination number. (1 Mark)

2. Using existing nominal codes, you should post the salary journal for June 2016 using the information

you produced in Section A. (5 Marks)

3. Set up the following Supplier Account:

Code: A01

Name: A-rated Lawyers

Address: 18 Liffey Street, Dublin 1

Contact Name: Liam Frayne

VAT Number: IE2588862S (2 Marks)

4. Post the purchase invoice relating to Legal Fees, shown below, received from A-rated Lawyers:

THANK YOU FOR YOUR BUSINESS!

(2 Marks)

5. Evolving Designs Limited are considering purchasing 6 x Walnut Chairs. You have been asked to

generate a quotation in Sage 50 Accounts (using a plain paper layout), dated 15th June 2016. Print

the quotation and ensure that the document is submitted with your other reports upon completion of

your exam.

(2 Marks)

To: The Classic Furniture Company Limited Date: 10th June 2016

31 Highbury Road, Dundrum, Co Dublin

Description Net

Amount €

VAT @

23%

Gross Amount

€

For Legal Services provided 6,000 1,380 7,380

Vat Analysis: SUBTOTAL €6,000.00

Rate Net VAT VAT €1,380.00

23% 6,000 1,380 TOTAL €7,380.00

A-Rated Lawyers 18 Liffey Street, Dublin 1 VAT Reg: IE2588862S

- 6 - -

Integrated Accounting Systems Examination 2016/2017 (ROI)

6. On the 15th of June 2016, the directors sent a US dollar draft for $10,660 (issued from the current

account) to The Californian Redwood Co. costing €10,036.75 for payment of invoice number 20915.

A bank charge of €12.50 is included in this figure and the difference is the currency gain/loss. Post

these transactions through the Purchase ledger and allocate the payment against the invoice and

related charges.

(3 Marks)

7. The company entered into a new lease agreement on 1st June 2016 purchasing new office

equipment at a cost of €12,480. Interest of €1,542 in total will be charged over 3 years. Ignoring

VAT implications, and assuming that lease interest accrues evenly over the life of the lease, you are

required to:

(i) Set up any required nominal accounts and post an appropriate journal at the date of acquisition to capitalise the new asset and record the lease liability at 1st June 2016.

(3 Marks)

(ii) Calculate, set up and post a recurring bank payment for the monthly lease repayment starting on June 5th and to be processed monthly. You are instructed to use your examination number as the reference on the recurring journal.

(3 Marks)

(iii) Create a new nominal account for lease interest and then calculate, set up and post an appropriate recurring journal to charge the appropriate value for monthly lease interest to the Profit and Loss Account on the same date as (ii) above. You should use your examination number as the reference on the recurring journal.

(3 Marks)

8. The following business expenses were paid personally by the director, Richard Anderson. Enter the appropriate adjustments in Sage 50 Accounts to reflect the expenses incurred and the outstanding liability.

Date Details Analysis Net VAT Total

€ € €

04/06/2016 Taxi Receipts Travelling 24.00 0.00 24.00

21/06/2016 Sundry Purchases Cleaning 17.50 0.00 17.50

(2 Marks) 9. Enter the following supplier payment, allocating the payment to invoices 7690 and 7710, and write

off any remaining value on the Creditor’s account to Discount (you may ignore VAT implicat ions):

PREMIER BANK PLC

4 Town Centre, Main Street, Dundrum Date 30/06/2016

Pay: Best Furniture Ever Ltd

Four thousand, seven hundred and forty-seven euro only €4,747.00

Cheque number: 50019 Richard Anderson

The Classic Furniture Co. Ltd.

(2 Marks)

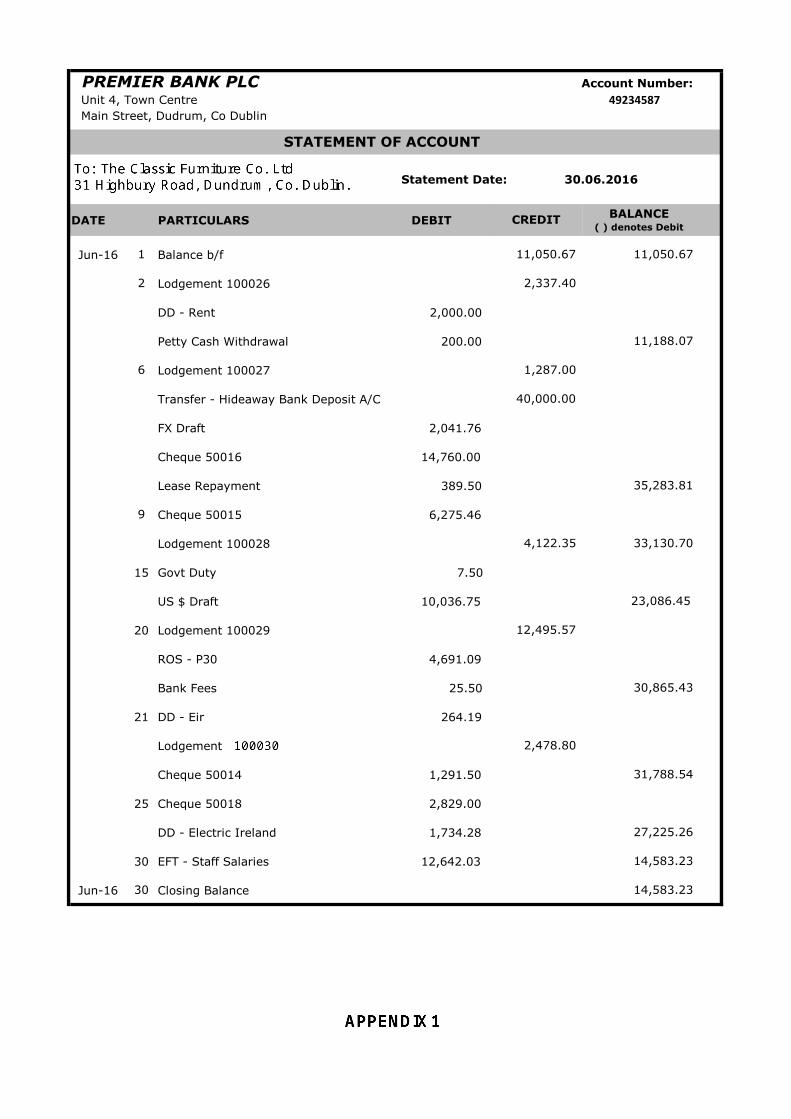

10. You are instructed to reconcile the bank account:

(i) Enter any amounts from the attached bank statement (refer to Appendix 1) that may not

have been recorded. (4 Marks)

(ii) Print the Bank Reconciliation Report (using the Report facility) available in the Bank Reconciliation Window and then reconcile the account to the bank statement for June.

(2 Marks)

- 7 - -

Integrated Accounting Systems Examination 2016/2017 (ROI)

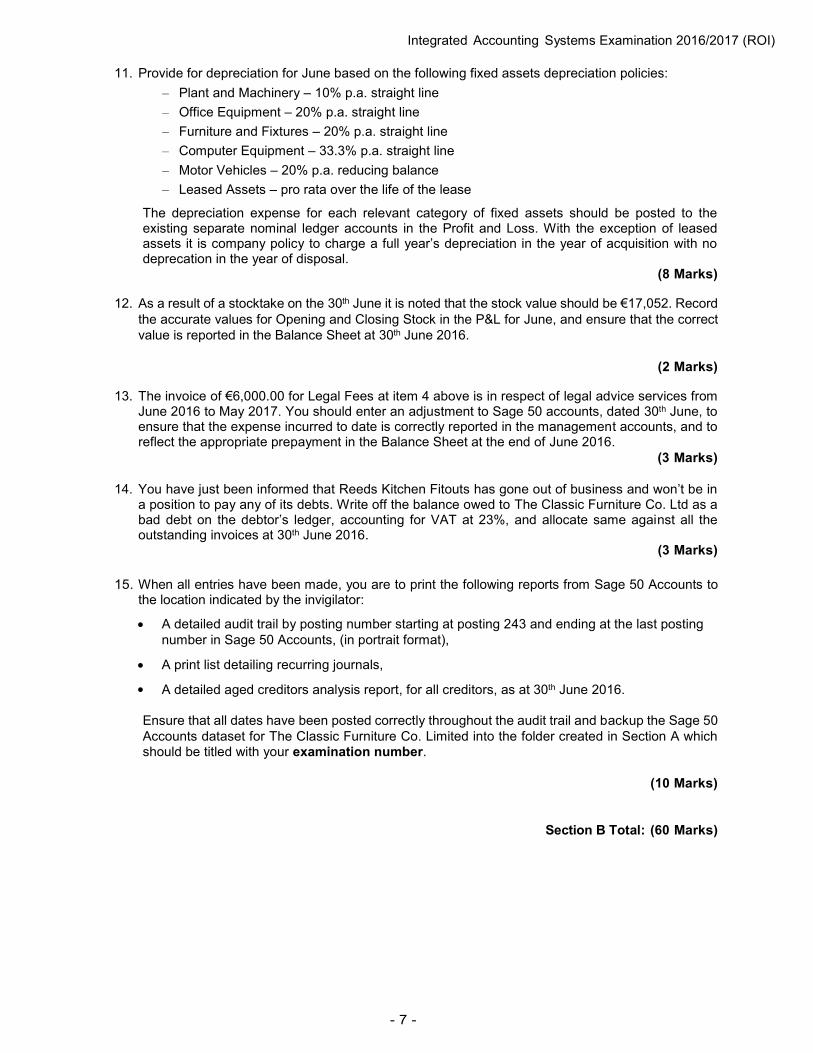

11. Provide for depreciation for June based on the following fixed assets depreciation policies:

– Plant and Machinery – 10% p.a. straight line

– Office Equipment – 20% p.a. straight line

– Furniture and Fixtures – 20% p.a. straight line

– Computer Equipment – 33.3% p.a. straight line

– Motor Vehicles – 20% p.a. reducing balance

– Leased Assets – pro rata over the life of the lease

The depreciation expense for each relevant category of fixed assets should be posted to the existing separate nominal ledger accounts in the Profit and Loss. With the exception of leased assets it is company policy to charge a full year’s depreciation in the year of acquisition with no deprecation in the year of disposal.

(8 Marks) 12. As a result of a stocktake on the 30th June it is noted that the stock value should be €17,052. Record

the accurate values for Opening and Closing Stock in the P&L for June, and ensure that the correct

value is reported in the Balance Sheet at 30th June 2016.

(2 Marks)

13. The invoice of €6,000.00 for Legal Fees at item 4 above is in respect of legal advice services from June 2016 to May 2017. You should enter an adjustment to Sage 50 accounts, dated 30th June, to ensure that the expense incurred to date is correctly reported in the management accounts, and to reflect the appropriate prepayment in the Balance Sheet at the end of June 2016.

(3 Marks)

14. You have just been informed that Reeds Kitchen Fitouts has gone out of business and won’t be in

a position to pay any of its debts. Write off the balance owed to The Classic Furniture Co. Ltd as a bad debt on the debtor’s ledger, accounting for VAT at 23%, and allocate same against all the outstanding invoices at 30th June 2016.

(3 Marks)

15. When all entries have been made, you are to print the following reports from Sage 50 Accounts to

the location indicated by the invigilator:

A detailed audit trail by posting number starting at posting 243 and ending at the last posting

number in Sage 50 Accounts, (in portrait format),

A print list detailing recurring journals,

A detailed aged creditors analysis report, for all creditors, as at 30th June 2016.

Ensure that all dates have been posted correctly throughout the audit trail and backup the Sage 50

Accounts dataset for The Classic Furniture Co. Limited into the folder created in Section A which should be titled with your examination number.

(10 Marks)

Section B Total: (60 Marks)

- 8 - -

Integrated Accounting Systems Examination 2016/2017 (ROI)

Section C - Excel: You are required to: 1. Prepare a month by month budget for the 3 months from 1st June 2016 to 31st August 2016 based

on the actual figures for March 2016.

Export the Profit and Loss Report for March 2016 from the Sage 50 Accounts dataset into an Excel worksheet and save the file as an Excel workbook:

All nominal account descriptions should appear in column A,

Ensure all the figures for March 2016 appear in column B, delete any YTD information,

Column B should be titled “Mar-16”

Insert narratives for total sales, total purchases and total overheads,

Ensure that there is a blank row inserted after each ‘total’ line.

(3 Marks)

2. Based on the information shown below you are asked to indicate the anticipated variances for Jun-

Aug in Column C. These should be shown as a percentage (e.g. +/- 5%) or fixed value (e.g. +/- €). In columns D-F you should then prepare the month by month budget for Jun-Aug, calculating your formulas using the variances indicated in Column C. Ensure each column is appropriately named.

Because of recent marketing initiatives it is anticipated that all Sales and Cost of sales will increase progressively by 5% each month from June onwards,

As a result of a recent redundancy and other payroll adjustments, payroll costs will decrease by 5% from 1st June 2016.

All other expenses have increased by 3% since April 2016 and it’s expected that these increases will hold for the foreseeable future, with the exception of rent & rates and depreciation,

Further to a review of rent & rates in mid-June, a 15% increase will apply in the monthly expense for same from July onwards,

Depreciation should be based on the March 2016 figures, while also taking into account the additional depreciation for the new leased asset addition as outlined in Section B. (Refer to the company’s fixed assets depreciation polices in Section B). Indicate this additional charge on a new line in the budget spreadsheet,

The monthly lease interest on the new leased asset addition (as indicated in Section B) should be accounted for in the budget for Quarter 2.

* Where no specific instruction is given you may use any appropriate Excel formula of your choice.

(6 Marks)

3. In the same worksheet, in a new column:

Insert formulas to show the total value for the 3 months ending 31st August 2016 for all nominal accounts, and name this column “Total Budget Values”.

Insert formulas to show the updated totals for gross profit and net profit in each month and in the total values column.

(2 Marks)

- 9 - -

Integrated Accounting Systems Examination 2016/2017 (ROI)

4. Format the whole spreadsheet in the following way:

All text and figures should be in Verdana style, italics and in font size 12,

Format all monetary values to ensure they have a “€” sign,

Bold all gross profit and net profit information,

Ensure all information is visible,

Using any Word Art, title the page “Budget for The Classic Furniture Company” in font size 20,

Insert today’s date as a footer on the right section and your examination number on the left side section. Both should be in bold and italics.

(4 Marks)

5. In a new worksheet, create a cashflow projection for September 2016, linking your values to the

original budget spreadsheet, to present the following information:

Assume an opening Bank balance of €15,000,

Debtors are given 30 days credit. (i.e. pay 1 month in arrears),

All cost of sale creditors give us 60 days credit (i.e. we pay 2 months in arrears),

All salary related costs, including taxes, are paid one month after they are incurred,

All other expenses are paid two months after they are incurred,

Provision should also be made for the repayments of the lease asset addition as outlined in Section B,

All text and figures should be in Verdana style, italics and in font size 12,

Using any Word Art, title the page “Cashflow for Sept 2016 (followed by your examination number) in font size 20.

Indicate the values for Cash Inflows, Cash Outflows and Net Cash Movement during September and indicate the projected bank balance as at 30th September 2016.

(You may ignore VAT implications and any VAT refunds/payments to the Revenue.)

(6 Marks)

6. Print the following reports:

One printout of the budget worksheet showing figures as normal,

One printout of the budget worksheet adjusted to show formulas instead of figures,

One printout of the cashflow worksheet showing figures as normal,

One printout of the cashflow worksheet adjusted to show formulas instead of figures.

Ensure that all Excel printouts are in Landscape format and that each report prints on one page only. On completion of your activity ensure that you have saved the Excel Workbook into the folder created in Section A which should be titled with your examination number.

(4 Marks)

Section C Total: (25 Marks)

TOTAL EXAM MARKS: (100 MARKS)

- 10 - -

Integrated Accounting Systems Examination 2016/2017 (ROI)

On completion of your examination:

Ensure that you have correctly completed the examination cover sheet and any other

documentation provided by the invigilator.

Ensure that all printouts (Payroll, Accounts and Excel) are in the order requested in each

section and are correctly submitted to the invigilator.

Ensure that PDF reports have been correctly saved and submitted to the invigilator.

Ensure that there is a folder, created in the location indicated by the invigilator, showing

your examination number as the folder name. Confirm that you have saved a backup of your

Sage Micropay, Sage 50 Accounts and Excel data into this folder.

It is the student’s responsibility to ensure that all work is saved and submitted as required above.

Accounting Technicians Ireland cannot be held responsible for any marks lost as a result of the

above not being completed correctly.

END OF EXAM

49234587

DATE PARTICULARS DEBIT

Jun-16 Balance b/f

Lodgement 100026

DD - Rent 2,000.00

Petty Cash Withdrawal 200.00

Lodgement 100027

Transfer - Hideaway Bank Deposit A/C

FX Draft 2,041.76

Cheque 50016 14,760.00

Lease Repayment 389.50

Cheque 50015 6,275.46

Lodgement 100028

15 Govt Duty 7.50

US $ Draft 10,036.75

20 Lodgement 100029

ROS - P30 4,691.09

Bank Fees 25.50

21 DD - Eir 264.19

Lodgement

Cheque 50014 1,291.50

25 Cheque 50018 2,829.00

DD - Electric Ireland 1,734.28

30 EFT - Staff Salaries 12,642.03

Jun-16 Closing Balance

BALANCE ( ) denotes Debit

CREDIT

4,122.35

2,337.40

1,287.00

40,000.00

1

31,788.54

27,225.26

23,086.45

30

2,478.80

14,583.23

Account Number:

Unit 4, Town Centre

9

35,283.81

11,188.07

6

11,050.67

2

STATEMENT OF ACCOUNT

PREMIER BANK PLC

Statement Date: 30.06.2016

Main Street, Dudrum, Co Dublin

14,583.23

33,130.70

30,865.43

11,050.67

12,495.57

These pages are supplied to facilitate Workings.

Students should note that no marks will be awarded for workings shown on these pages.

END OF EXAM PAPER

These pages are supplied to facilitate Workings.

Students should note that no marks will be awarded for workings shown on these pages.

2nd Year Examination: April 2017

Integrated Accounting Systems ROI

Examiner’s Comments

Statistical Analysis – By Question

Question No. 1 2 3

Average Mark

(%)

86% 82% 81%

Nos. Attempting 611 611 611

Statistical Analysis – Overall

Pass Rate 84%

Average Mark 82%

Range of Marks Nos. of Students

0-59 64

60-69 36

70 and over 511

Total No. Sitting Exam 611

Total Absent 42

Total Approved Absent 16

Total No. Applied for Exam 669

General Comment:

The results of the Summer examinations in Integrated Accounting Systems 2017 indicated that many candidates had prepared well for each of the three integrated modules of Payroll, Accounts and Excel, and it was noted the confident demonstration of Excel skills was maintained.

Candidates should continue to pay close attention to the requirements of printing, file management and data integrity. Candidates are reminded, as always, that the following items should be considered:

All exam material submitted for correction is be well presented and in the requested order i.e. Payroll, Accounts and Excel.

Computerised reports will be marked on their own merits, no handwritten detail will be reviewed or marked.

All reports should be produced according to the specific instruction provided (e.g. Detailed, Landscape etc.) and marks will be deducted if alternative reports are submitted.

Students do not have to write their student number on each report. The use of highlighters is also strongly discouraged in the IAS examination.

Backups of all completed material (i.e. a solution Payroll dataset, solution Accounts dataset, and solution Excel workbook) must be submitted to the invigilator.

Payroll:

In general, candidates scored well in the Payroll section with only a few items presenting challenges:

Students should pay careful attention to the calculations involved in order to identify weekly, and daily, salary values. A few candidates are making errors in these calculations e.g. incorrectly dividing an employees’ monthly wage value by 4 to get the weekly value. The correct methods of calculation should be reviewed (e.g. multiply by 12 and divide by 52).

Additionally, it is crucial to be familiar with which pay elements should, and should not be, subject to tax, PRSI, USC etc. The statutory redundancy payment (Classic paper) was frequently taxed, while the bank holiday payment (Antique paper) was occasionally included as a non-taxable payment.

Students should pay close attention when printing the requested payroll reports, and ensure that all employees have been recorded and paid appropriately. It was noted that timesheets were occasionally not “saved”, particularly for the employee that did not require any adjustment.

Accounts:

Adequate preparation for this section of the paper meant that students were well rewarded for their studies and revision. A small number of items continue to pose difficulties and can result in lost marks, so careful attention should be paid to the following items.

Regarding Presentation:

The company name should be adjusted according to the specific instruction given on the face of the paper so that each report can be easily identified.

Any recurring journals should be referenced with an exam number, as requested.

A detailed audit trail (as requested, in Section B), in portrait format, is mandatory and candidates will lose a number of marks if the incorrect report is submitted. The audit trail should run from the indicated audit trail transaction, and no limit should be applied in respect of dates.

If debtor or creditor reports are requested, it is necessary to have an starting date (which often defaults in the software) and an ending date (i.e. at the end of the reporting period), so that all details can be viewed.

All dates should fall within the management accounting period.

It should be noted that nominal ledger journals can now be edited in Sage 50 Accounts and therefore it is no longer necessary to post reversing journals if errors are made; the original transaction can be directly amended.

When posting transactions:

The salary journal affords the opportunity to gain 5 marks and students should pay close attention when preparing and inputting the payroll details. Students are reminded to post the salary journal in a way that distinguishes each pay element i.e. Director’s remuneration, Staff salaries, pension costs and contributions etc. It was noted that a significant number of candidates omitted the salary journal entirely.

Students should note that they should NOT use the suspense account unless specifically requested to do so. They are reminded that the correct use of this account is examinable i.e. for recording opening balances etc.

A few candidates demonstrated confusion between the differences between accounting for a lease, and accounting for a loan. There are nine marks typically available for any finance agreements so very close attention should be paid to this topic.

The adjustment for depreciation was particularly well handled this year. However, several students continue to calculate the incorrect value for the reducing balance motor vehicle depreciation; the correct approach should be considered carefully i.e. using the cost and accumulated depreciation values at the start of the accounting

year. Additional marks were awarded for the leased asset depreciation, where applicable. For transparency, candidates are encouraged to post the value for the leased asset as a separate item in the depreciation journal i.e. they should not combine it with the value for depreciation for other similar assets.

The bank reconciliation exercise still poses problems and results in easy marks being lost; common mistakes include:

o Treating Supplier payments as Expense outlays (e.g. recording a payment for a telephone expense, rather than a creditor payment to Eircom),

o Posting P30 and Net wage payments to expense accounts, instead of liability accounts,

o Not printing the correct Bank Reconciliation Report, or not printing the report at all.

Period end adjustments again proved to be difficult for a significant number of candidates (Prepaid expenses and bad debt write off in the Classic paper, and Rent accrual and bad debt provision in the Antique paper) with discomfort and confusion frequently present; it is therefore very likely that adjustments of this type will be under the spotlight in upcoming examinations.

Excel:

In general, students were either well prepared for the Excel section and scored highly; or struggled with the requirements and sacrificed a significant number of marks. However, it is noted that the overall performance in Excel is showing substantial improvement every year and this is an extremely positive and pleasing trend.

Some frequent errors in Excel included the following:

Adjusting for the increase in rent in the wrong month (Classic & Antique papers)

Including depreciation in the cashflow statement (Classic paper)

Indicating the lease interest as an additional expense in the cashflow (Classic paper)

Not linking the values in the cashflow to the original budget spreadsheet (Classic paper)

Using the “Sum” instead of “Average” total for the three-month period (Antique paper)

Selecting the wrong expense codes for the column chart (Antique paper)

Not adjusting the series title in the chart correctly (Antique paper)

It should also be noted that all the Excel reports in this sitting were requested in landscape format and marks were sacrificed if portrait format was applied, or if reports printed on more than one page each.

Conclusion:

As always, students are reminded that the following activities are fundamental to success in the IAS examination:

1. Practice, 2. Performance, and 3. Presentation.

Students reap the rewards when they devote sufficient time and attention to the subject of IAS and are therefore strongly encouraged to start on their studies with the IAS manual and software as early as possible in the academic period. Adequate practice in all sections of the syllabus translates into a confident performance on the day of the examination. Excellent performance is then supported by the submission of clean, well presented financial documents and candidates who appreciate the value of all these activities should do very well indeed in the final examination.