insurance journal west 2015-09-07

DESCRIPTION

Surplus Lines: State of the Market / NAPSLO Issue. Lloyd's Syndicate SpotlightTRANSCRIPT

WEST EDITIONUber’s Employee Status Headache

Geico’s $6M Practices Settlement

Supreme Court Rules Against Hartford

ACTION-READY

With our unique blend of products and

a skilled multi-line underwriting team,

we are building value, enhancing

relationships, and responding to our

customers’ needs. And as a wholly

owned subsidiary of Nationwide® , with an

A.M. Best rating of A+ (Superior) FSC XV,

all the pieces are in place to make great

things happen.

The iron is hot. Now is the time to strike.

Scottsdale Insurance Company and design is a federally registered service mark of Scottsdale Insurance Company.

a Nationwide Insurance® company

A.M. Best Rating of A+ (Superior), FSC XV

www.scottsdaleins.com

SCOTT16754.indd 1 2/7/15 4:51 PM

®™

MVP.EarthquakeAuthority.com

CEAUT16337.indd 1 7/18/15 11:55 AM

Applied UnderwritersEquity Comp Construction Spread Ad

Bleed: 17” x 11.125”Trim: 16.75” x 10.875”Live: 16.25” x 10.375”

Applied Underwriters 2015_EC_Construction_IJ.indd

Contact: Sheila Gallagher P: 707-395-0645 Email: [email protected] Experience. Applied Intelligence.

©2015 Applied Underwriters, Inc., a Berkshire Hathaway company. Rated A+ (Superior) by A.M. Best. Insurance plans protected U.S. Patent No. 7,908,157.

IT PAYS TO GET A QUOTE FROM APPLIED®

Accepting large workers’ compensation risks. Most classes. All states, all areas,

including New York City, Boston, and Chicago. Few capacity and concentration restrictions.

Simplified financial structure covers all exposures.

EXPECT THE WINNING DEAL ON LARGE WORKERS’ COMPENSATION.

Call (877) 234-4450 or visit auw.com to get a quote.

APPLIED PROTECTS THE TITANS OF INDUSTRY.®

AUDIRECT16752.indd 1 8/21/15 6:37 AM

Applied UnderwritersEquity Comp Construction Spread Ad

Bleed: 17” x 11.125”Trim: 16.75” x 10.875”Live: 16.25” x 10.375”

Applied Underwriters 2015_EC_Construction_IJ.indd

Contact: Sheila Gallagher P: 707-395-0645 Email: [email protected] Experience. Applied Intelligence.

©2015 Applied Underwriters, Inc., a Berkshire Hathaway company. Rated A+ (Superior) by A.M. Best. Insurance plans protected U.S. Patent No. 7,908,157.

IT PAYS TO GET A QUOTE FROM APPLIED®

Accepting large workers’ compensation risks. Most classes. All states, all areas,

including New York City, Boston, and Chicago. Few capacity and concentration restrictions.

Simplified financial structure covers all exposures.

EXPECT THE WINNING DEAL ON LARGE WORKERS’ COMPENSATION.

Call (877) 234-4450 or visit auw.com to get a quote.

APPLIED PROTECTS THE TITANS OF INDUSTRY.®

AUDIRECT16752.indd 1 8/21/15 6:37 AM

6 | INSURANCE JOURNAL-WEST September 7, 2015 www.insurancejournal.com

InsideThisIssue

WEST

September7,2015•Vol.93No.17•West

10 Auto Insurance Affordability Improves in Most States: IRC

10 Insurers Look to Cyber, M&A Coverage as Prices Decline: Marsh

14 MGAs Next to Feel Impact of Capital Markets: AmWINS’ DeCarlo

15 Cyber Risk Insurers Lag in Buying Cyber

24 Survey Examines Agents’ Views of Agency Aggregators

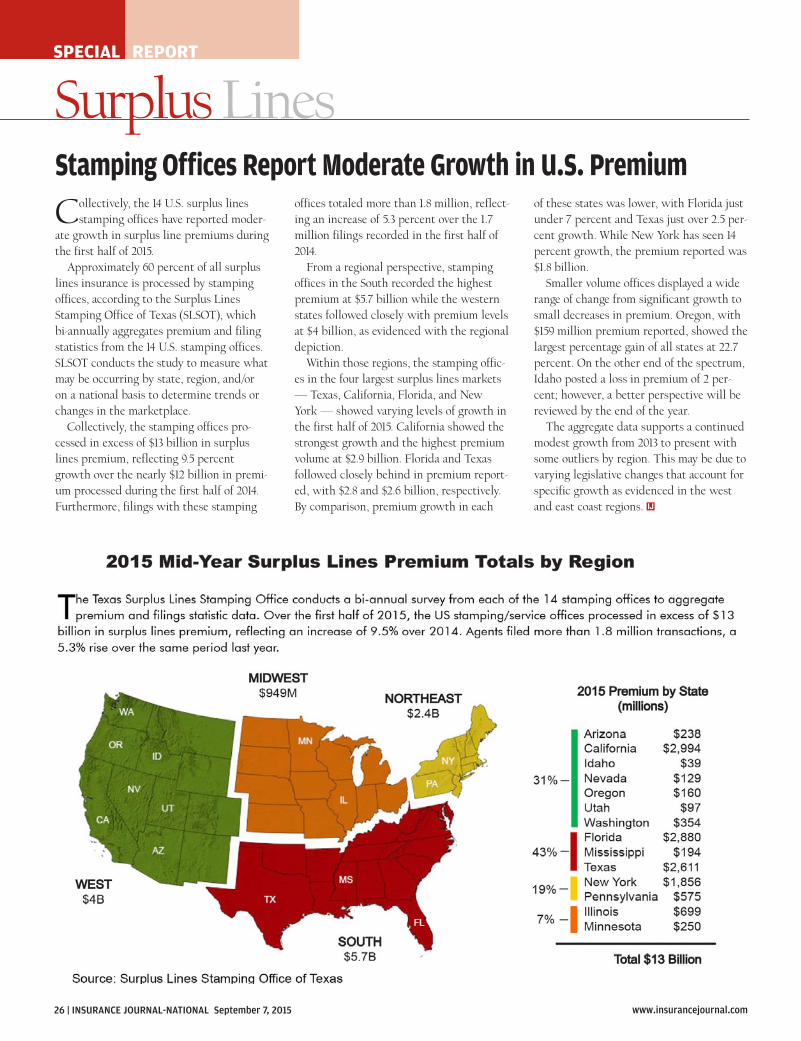

26 Special Report: Stamping Offices Report Moderate Growth in U.S. Surplus Lines Premium

28 Special Report: 10 Drivers of Surplus Lines Growth

32 Special Report: Lloyd’s & Its Syndicates 2015 – Adapting to Changing Times

37 Spotlight: Marketers Have Lost Control of Insurance Buying Process

NATIONAL COVERAGE

42 The Competitive Advantage: Chris Burand

48 The Hard Market That Wasn’t

54 Minding Your Business: Catherine Oak & Bill Schoeffler

58 Managers as Employee Engagement Ambassadors

62 Closing Quote: Making Strides for Gender Equality

IDEA EXCHANGE

DEPARTMENTSW4 People12 Declarations12 Figures18 Business Moves52 MyNewMarkets

W2 W10

W2 California Commissioner Applauds Supreme Court Decision Against Hartford

W2 Study: Ventura, Oxnard in California Could Be at Greater Tsunami Risk

W6 California WCIRB Proposes Premium 7.8% Below 2015 Average

W6 Geico Agrees to $6M Settlement over Business Practices in California

W8 Former California Probation Officer Nabbed for Fraud While on Probation

W10 Uber Headache if More Drivers Want Full-Time Status

WEST COVERAGE

3224

On The CoverSpecial Report:

10 Drivers of Surplus Lines Growth

IMPATIENCE IS A VIRTUE.

Clear your desk. Your mind, too.Quote and order standalone personal umbrellas online in 3 minutes100% direct billNo MVRsNo signed applicationsAdmitted, rated A+ XV by A.M. Best

Family-owned and operated. Proudly dog-friendly. Available nationally. Underwriting criteria varies by state. Visit us online for guidelines. California Insurance License 0D08438A.M. Best rating effective August 2015. For the latest rating, visit ambest.com.

PERSONALUMB16635.indd 1 8/21/15 6:48 AM

8 | INSURANCE JOURNAL-NATIONAL September 7, 2015 www.insurancejournal.com

NATIONAL COVERAGE

FOR QUESTIONS REGARDING SUBSCRIPTIONS: Call: 855-814-9547 or you may subscribe or change your address online at:

insurancejournal.com/subscribeInsurance Journal, The National Property/Casualty Magazine (ISSN: 00204714) is published semi-monthly by Wells Media Group, Inc., 3570 Camino del Rio North, Suite 200, San Diego, CA 92108-1747. Periodicals Postage Paid at San Diego, CA and at additional mailing offices. SUBSCRIPTION RATES: $7.95 per copy, $12.95 per special issue copy, $195 per year in the U.S., $295 per year all other countries. DISCLAIMER: While the information in this publication is derived from sources believed reliable and is subject to reasonable care in preparation and editing, it is not intended to be legal, accounting, tax, technical or other professional advice. Readers are advised to consult competent professionals for application to their particular situation. Copyright 2014 Wells Media Group, Inc. All Rights Reserved. Content may not be photocopied, reproduced or redistributed without written permission. Insurance Journal is a publication of Wells Media Group, Inc.

POSTMASTER: Send change of address form to Insurance Journal, Circulation Department, PO Box 708, Northbrook, IL 60065-0708

ARTICLE REPRINTS: For reprints of articles in this issue, contact: Ly Nguyen at 1-800-897-9965 ext. 125 or [email protected] Visit insurancejournal.com/reprints/ for more information.

Opening Note

Andrea WellsEditor-in-Chief

By offering more relaxed terms and conditions, the market could be repeating historical mistakes.

Repeating Mistakes

Lloyd’s international casualty reinsurance underwriters are running the risk of repeating the same mistakes that have placed the market in difficulty in

the past, according to a new poll of Lloyd’s reinsurance specialists. The survey conducted by the Lloyd’s Market Association (LMA), revealed that 68 percent of casualty treaty underwriters believe that by offering more relaxed terms and conditions, the market could be repeating historical mis-takes. Ninety-five percent of respondents said that they had seen softening of terms and conditions in the international casualty market and 39 percent believed that more than half of those changes were having a material impact on underwriters’ exposures. Worryingly for the market, 71 percent of those surveyed thought that differ-ential terms across a placement were becoming more prevalent at Lloyd’s, the LMA survey revealed. (Differential terms are when some following carriers on a reinsurance slip or on a different layer underwrite the risk on terms and con-ditions different to those agreed by the slip’s lead carrier.) In terms of market conditions, underwriters felt that rates were at the bottom of the cycle, or were approaching bottom. The vast majority felt that current prices were unsus-tainable. Considering these conditions, underwriters were surprised that clients were not buying more international casualty reinsurance protection. Two-thirds of underwriters said they had declined more renewal business in 2015 than the previous year. Broadening terms and conditions was the rea-son most commonly cited for their decision not to renew, followed by pricing considerations and poor loss experience.

“This is a fairly informal survey but its results point strongly towards a buyer’s market in which traditional under-writer discipline is under considerable pressure,” said Patrick Davison, the LMA’s senior executive – underwriting. “The growth in the prevalence of differential terms is particularly disturbing. These create headaches for the mar-ket’s back office and the efficiency with which claims in a subscription market can be managed. Differential terms might be one indicator that some reinsurers have concluded further amendments to coverage or retentions are unsustainable,” Davison said. “This view is supported by the clear perception in the market that the bottom of the cycle is approaching, as

highlighted by the increasing number of underwriters declining business.” The LMA’s survey of members of its international casualty treaty business panel took place during August 2015. Respondents represented three-quarters (by gross written premium) of the interna-tional casualty treaty market in Lloyd’s.

Publisher Mark Wells | [email protected]

EDITORIALChief Content OfficerAndrew Simpson | [email protected] Wells | [email protected] EditorYoung Ha | [email protected] EditorAmy O’Connor | [email protected] Central Editor/Midwest EditorStephanie K. Jones | [email protected] EditorDon Jergler | [email protected] EditorCharles E. Boyle | [email protected] EditorSusanne Sclafane | [email protected] EditorDenise Johnson | [email protected] Chris Burand, Catherine Oak, Bill Schoeffler Contributing Writers David Coons, Rudy Dimmling, Greg Hoeg, Betsy Myatt

SALESChief Marketing Officer Julie Tinney (800) 897-9965 x148 | [email protected] Manager Lauren Knapp (800) 897-9965 x161 | [email protected] Dena Kaplan (800) 897-9965 x115 | [email protected] Steinkamp (800) 897-9965 x172 | [email protected] Whalen (800) 897-9965 x180 | [email protected] Central Mindy Trammell (800) 897-9965 x149 | [email protected] (NY, PA and CT only) Dave Molchan (800) 897-9965 x145 | [email protected] & East (except for NY, PA and CT) Howard Simkin (800) 897-9965 x162 | [email protected] Markets Sales Manager Kristine Honey | [email protected], Jobs, Agencies Wanted/For SaleKelly De La Mora (800) 897-9965 x125 | [email protected]

MARKETING/NEW MEDIAMarketing Administrator Gayle Wells | [email protected] Coordinator Erin Burns (619) 584-1100 x120 | [email protected] Media ProducerBobbie Dodge | [email protected]

DESIGN/WEBChief Technology Officer/Chief Innovation OfficerJoshua Carlson | [email protected]. of Design Guy Boccia | [email protected] Development Elizabeth Duffy | [email protected] Director Derence Walk | [email protected] Developer Jeff Cardrant | [email protected] Developer Tim Layer | [email protected]

IJ ACADEMY OF INSURANCEV.P. of EducationChris Boggs | [email protected] ExecutiveRomeo Valdez | [email protected] Training CoordinatorBarbara Whiffen | [email protected]

ADMINISTRATION Chief Executive OfficerMitch Dunford | [email protected] Financial Officer Mark Wooster | [email protected]

PROFESSIONAL LIABILITY

Take your professional liability business to new heights.

At Burns & Wilcox, our expertise becomes your expertise. Whether it is cyber liability or medical malpractice, EPLI or fiduciary liability, we will ensure your clients avoid any gaps in coverage. Raise the level of your professional liability expertise with Burns & Wilcox.

800.521.1918 | burnsandwilcox.comCommercial | Professional | Personal | Brokerage | Binding | Risk Management Services

36175_Burns_Prof.Lia_Ad_InsJournal_Aug2015_APPROVED.indd 1 8/18/15 4:51 PMBURNWIL16628.indd 1 8/21/15 6:42 AM

10 | INSURANCE JOURNAL-NATIONAL September 7, 2015 www.insurancejournal.com

NATIONAL COVERAGE

News & Marketspercentage of the average consumer’s budget and lower-to-moderate income consumer’s budget. It also has had unprecedented affordability improvements over time. The auto insurance expenditure-to-in-come ratio was calculated using insur-ance expenditure data from the National Association of Insurance Commissioners and the Bureau of Labor Statistics Consumer Expenditure Survey. Currently, about 1.5 percent to 1.6 percent of income is spent on auto insurance in the U.S. by the average consumer, which represents much lower figures than seen in previous decades, according to IRC. Low-to-moderate income consumers have also witnessed similar trends, the researchers said. “There is a lot of interest in the afford-ability of auto insurance .... This report adds to the discussion, showing that auto insurance is becoming more and more affordable,” said Elizabeth Sprinkel, senior vice president of the IRC.

Auto Insurance Affordability Improves in Most States: IRC

Personal auto insurance has become more affordable over time for all income

groups, including low-to-moderate income groups, and in most states, according to a report from the Insurance Research Council (IRC). The industry group says the study also shows that the degree of improvement in auto insurance affordabil-ity is not being witnessed in other industries. The study includes state estimates indi-cating that auto insurance affordability has also been improving in most states. All but five experienced improved affordability from the 1990s to the 2000s, and all but four have shown an improvement in affordability between the 2000s and the present. Affordability does vary across states, however. According to the report, auto insurance was least affordable in Louisiana (2.85 percent of income), Florida (2.45 per-

cent), New York (2.42 percent), Delaware (2.18 percent) and Michigan (2.10 percent). The most affordable states were found

to be North Dakota (1.03 percent of income), Iowa (1.05 percent),

New Hampshire (1.06 per-cent), Virginia (1.07 percent) and Wyoming (1.08 per-cent). The study, “Trends in Auto Insurance

Affordability,” used an auto insurance expenditure-to-income ratio to analyze auto insurance affordability. The report does not prescribe a specific thresh-old at which auto insurance may be consid-ered affordable. Instead, it examines trends in affordability. The report compares affordability trends for auto insurance to the affordability trends for other industries whose products or services are considered necessities. Auto insurance was found to represent a smaller

Insurers Look to Cyber, M&A Coverage as Prices Decline: MarshCommercial insurance rates continued

their global decline in the second quarter of 2015, a trend driven by an abun-dance of global capacity and a lack of large insured loss activity, Marsh said in its latest Global Insurance Market Quarterly Briefing. At the same time, property/casualty insurers are looking to specialty coverages including cyber and transactional risk insurance for mergers and acquisitions (M&A) as a way to grow, the report says. As of Q2, there have been nine consecu-tive quarters of overall rate declines. Globally, natural catastrophe losses are at historic lows, which is helping profitability but also reducing the drive for rate increas-es, according to Marsh.

Pricing Marsh said the Asia-Pacific region saw the largest overall rate decreases, followed by the U.K., Continental Europe, Latin America and then the U.S.

Commercial casualty rates dipped at a more moderate rate than property, ranging from flat to a 5 percent decline dependent on the market. Property insurance dipped more than 5 percent on average, Marsh said. The Asia-Pacific region saw renewal rate declines greater than 7.5 percent on average. In Continental Europe, the average declines ranged from 5 percent to 7.5 percent, with the U.K. coming in at slightly worse aver-ages. In Latin America and the Caribbean, rate declines varied on average from 2.5 percent to 5 percent. The U.S. saw the least declines, with renewal rates staying flat or dip-ping to 2.5 percent on average.

Specialized Coverages One exception to the price declines — specialized coverag-es — is led by a cyber insurance market that continues to firm up, Marsh reports.

Another bright spot: transactional risk insurance, particularly for M&A deals. Demand for the specialty coverage contin-ued to grow through the first six months of 2015, jumping by 15 percent overall com-pared to the same period last year in terms of limits placed by Marsh. “The demand for transactional risk insurance on M&A transactions continues to grow rapidly, as competition among acquirers continues to remain intense,” says Karen Beldy Torborg, global practice leader

for Marsh’s private equity and M&A sales practice. Dealmakers in the pri-vate equity and corporate space are “increasingly using insurance capital to get deals over the line, and we don’t see this trend subsiding anytime soon.” In Europe, real estate deals are driv-ing the demand for transactional insurance and U.S. and Asia-Pacific corporations involved in buying and

selling are buying it.

Chubb - 153026Project: Vegas Lady

Campaign: February

Creative: 153026_CHUBB_VegasLady_InsuranceJrnl_Feb28

AE: Dave Wood

Publication: Insurance Journal

IO #: None

Issue: February 28th 2015

Ad Type: single

bleed = 8.625” X 11.125”

trim = 8.375” X 10.875”

safety = 7.875” X 10.375”

Insurance Journal

3570 Camino del Rio North

Suite 200

San Diego, CA 92108

Attn: Production Dept

t: 800.897.9965 f: None

Ship Info:

Contact Ad Production with any questions regarding these materialsph: (973) 952-8273 email: [email protected]

TM

Chubb Group of Insurance Companies (“Chubb”) is the marketing name used to refer to the insurance subsidiaries of The Chubb Corporation.

For a list of subsidiaries, please visit our website at www.chubb.com. Actual coverage is subject to the language of the policies as issued.

Chubb, Box 1615, Warren, NJ 07061-1615. © 2015 Chubb & Son, a division of Federal Insurance Company.

PROPERTY / LIABILITY / EXECUTIVE PROTECTION / WORKERS COMPENSATION / MARINE

SURETY / HOMEOWNERS / AUTO / YACHT / JEWELRY / ANTIQUES / ACCIDENT & HEALTH

www.chubb.com

INSURANCE AGAINST REGRETTALK TO YOUR CLIENTS ABOUT CHUBB.

S:7.875”S:10.375”

T:8.375”T:10.875”

B:8.625”B:11.125”

153026_CHUBB_Vegaslady_InsuranceJrnl_Feb28.indd 1 1/29/15 11:45 AMCGMLV16502.indd 1 2/7/15 4:54 PM

12 | INSURANCE JOURNAL-NATIONAL September 7, 2015 www.insurancejournal.com

NATIONAL COVERAGE

FIGURES DECLARATIONS

$8.9 Million

$2 Million 6 Years

$71 MillionThe amount in the latest round of fund-ing that the New Jersey Transit is getting

from the federal government to pay for rebuilding and replacing equipment dam-

aged by Superstorm Sandy. New Jersey’s Congressional delegation announced the

award Aug. 21. The money comes from the Federal Transit Administration and is part

of a $3.7 billion second round of funding for Superstorm Sandy relief.

The amount of a jury award favoring Michael Jordan in a civil trial focused on the

market value of the former Chicago Bulls basketball star’s identity. The now-defunct grocery store chain Dominick’s Finer Foods

has been ordered to pay Jordan for using his name in a steak ad without his permis-sion. Jordan has said the lawsuit was about

protecting the name he has worked hard for and not about the money. He plans to give

the award amount to charity.

The amount of damage caused by a fire that ripped through a 14th floor pool deck at

The Cosmopolitan hotel-casino on the Las Vegas Strip in late July, according to fire

officials, who say the cause of the fire is still unknown.

Crop Insurance“The lack of insurance for malt barley is pre-

venting farmers from planting this crucial crop.”

— U.S. Sen. Charles Schumer, D-N.Y., during his Aug. 20 speech at the Empire Farmstead Brewery in Madison County, N.Y. Schumer called on the

USDA to establish a new crop insurance program for Central New York farmers who grow malt

barley, a crop that is crucial to the growth of the area’s burgeoning craft beer industry.

Much Better and Much Worse

“You’re going to hear a lot of folks say things are so much better, the economy is so improved, and other people are going to say

it is so much worse.” — Allison Plyer, with the New Orleans-based think tank, The Data Center, comments on the

state of her city 10 years after it was devastated by Hurricane Katrina. Much of New Orleans has rebounded but many areas still struggle, partic-ularly African-American neighborhoods and the

chronically neglected Lower 9th Ward.

Biometric Identifier?“I support technological innovation.

Innovation, however, does not give compa-nies a license to mislead consumers about

issues affecting their safety.”— San Francisco District Attorney George Gas-con and another prosecutor filed a revised lawsuit in late August against Uber saying its background checks rely only on personal information, and the firm can’t ensure information is associated with

an applicant without a “unique biometric identifi-er” — fingerprints, in other words.

A Strong Relationship“We know, at least based on the spatial and temporal relationship between these earth-

quakes and brine disposal operations in Harper and Sumner counties, that these two are certainly linked. … There’s definitely a

strong relationship between the two.”— Kansas Geological Survey scientist Tandis Bidgoli, on the link between an uptick in the

number of earthquakes in two southern Kansas counties and the injection into wells of saltwater

used in oil and natural gas drilling.

Sinkhole Crisis“We’re completely reactionary. We don’t

have the resources to be proactive.” — Lou Akers, executive director of the Hunting-ton, W. Va., Water Quality Board, said in regards to a dramatic increase in sinkholes in the city. The

Huntington Water Quality Board is reportedly getting at least three sinkhole-related calls a week.

The amount of time a Florida man was sentenced to prison for after staging car

crashes. Guillermo de la Vega of Jacksonville pleaded guilty to two counts of participating

in an intentional motor vehicle crash and two counts of false insurance claims. The Florida Times Union reported the fraud-ulent personal injury protection claims

originated at a Jacksonville rehabilitation clinic that authorities say provided bogus treatment for nonexistent injuries. De la

Vega paid those who participated in the fake crashes after the clinic received the money.

The number of seasonally adjusted nonag-ricultural jobs added in Texas in July. The Texas Workforce Commission (TWC) says the state has added jobs in 57 of the last 58

months. The seasonally adjusted unemploy-ment rate remained at 4.2 percent in July,

the lowest monthly unemployment rate since July 2007. The state’s unemployment rate continues to trend well below the national

rate of 5.3 percent and is down from 5.0 per-cent a year ago.

31,400

© 2015 Vertafore, Inc. and its subsidiaries. All rights reserved. Trademarks contained herein are owned by Vertafore, Inc.

Rating, reference, and agency management in one

integrated solution. That’s the power of the Platform.

Learn more: www.vertafore.com/ChoosePlatform

“All the tools we use every day. On one screen. That’s powerful.”

Michelle MorganGeneral Manager Gene Morgan Insurance Agency

The Vertafore Agency Platform™

VFORP16725.indd 1 8/26/15 5:16 AM

14 | INSURANCE JOURNAL-NATIONAL September 7, 2015 www.insurancejournal.com

NATIONAL COVERAGE

News & Markets

got disintermediated in that transaction?” he asked the audience, quickly answering his own question. “Frankly, MGAs — because if I can do it myself without going through that big frictional cost, we’re going to save everybody money,” he said.

Analytics AmWINS had the ability to do this because they had analytics to share with Nephila, he added. “We had the analytics where they could see through our book of business, [which] we distribute through to 600 markets … “They got comfortable with that big data. That’s one of our core skills,” he said. Summing up, DeCarlo said, “The reality of the Nephila transaction is [this]: If I had 600 direct insurance companies before, now I have 601. It’s the MGA and the Lloyd’s platforms that potentially could be impact-ed,” he concluded.

MGAs Next to Feel Impact of Capital Markets: AmWINS’ DeCarlo

Now that traditional reinsurers are adjusting to the idea that third-party

capital providers have moved into their space, managing general agents (MGA) may be next to feel the negative impact of new capital, the leader of a specialty broker said. Speaking at the Standard & Poor’s 2015 Insurance Conference in June, Steven DeCarlo, the chief executive officer of AmWINS Group, provided details of a deal between AmWINS and Nephila, an invest-ment manager specializing in reinsurance risk, which is helping Nephila plow into new territory — the direct insurance mar-ketplace. It’s the MGAs that were disintermediat-ed in the deal, DeCarlo asserted during a session on trends in the specialty insurance market. DeCarlo made the remark after going over his rationale for accepting almost no commission under terms of a deal. Basically, he said the deal gives Nephila access to a vast retail distribution network without 10 points of commission going to an MGA to get there. (AmWINS has both MGA and wholesale brokerage operations.)

AmWINS and Nephila Deal The background and basics of the arrangement are these, according to DeCarlo: “Nephila is a well-known brand, and they obviously have been on the reinsurance side for years. [But] more and more as they had seen less opportunity to acquire rein-surance, it was not lost on a lot of us that they weren’t going to sit there — that they were going to figure out a way to distribute their capital directly into the [insurance] marketplace … “They did it originally through some facil-ities at Lloyd’s, through some MGAs in the U.S. And then we struck a relationship. “They wanted to get access to insureds. They cannot manage 20,000 retail brokers. There are just too many …So they’ve hired us to do that on their behalf.”

In addition, DeCarlo noted that AmWINS handles a large book of property insurance business — $2.5 billion overall, including a $1.6 billion program of shared and layered premium. Nephila wanted to participate on that shared and layered premium. The issue was how, he said. To solve the problem, “what Nephila did was give us the ability to put their capital out on these property placements country-wide” — small, medium and large. “They follow form, basically like Lloyd’s. They follow terms and conditions and pricing established by somebody else.” Another underwriter establishes the layer’s pricing, and they participate on that pricing. “What people have missed on this is typ-ically that looks like an MGA, and I would make an extra 10 points. [But] instead, I took a half a point. I took basically noth-ing,” DeCarlo said. “The reason I took it is because I want to sell exclusive product — because if I can get retailers to call me, I’m going to get more opportunities,” he explained. “I’m willing to distribute product that’s exclusive without the additional fric-tional cost.” “Nephila’s happy, less friction. We’re happy, exclusive product. That’s the distri-bution game that’s going on …We’re manag-ing retailers with less frictional cost to the capital markets. And it was a quick way for Nephila to participate on a very, very big book of excess property business,” DeCarlo said. “Will they do it in [workers] comp? Will they do it in GL? I don’t know their strate-gy. That’s their choice,” he added. DeCarlo also explained that Nephila needed a fronting company to get this done, revealing that Allianz is the risk transfer agent in this arrangement. The specialty broker executive also revealed that he took a lot of heat from car-rier executives “because it looks like we’re underwriting. We’re not. We’re distributing,” he stated. Carriers shouldn’t be upset, he said. “Who

‘We’re managing retailers with less frictional cost to

the capital markets.’

Steven DeCarlo AmWINS’ CEO

Marty HacalaFitness Enthusiast General Star President & CEO

“Rolling out of bed at 5am every morning to work out requires discipline. It’s my way of getting the very most out of my busy day.

“At General Star, we strive to get the very most out of our wholesale broker relationships. As a member of the Berkshire Hataway family of companies, our financial strength is unsurpassed. But it’s our disciplined approach to building and maintaining profitable partnerships with a select group of brokers that drives us.

“Discipline: Whether sticking with an early morning exercise regimen or standing firm with a limited number of valuable wholesale broker relationships, it remains the cornerstone of our success.”

To locate the General Star broker nearest you, visit our website at www.generalstar.com.

Beyond Security®

“It Takes Discipline”

© 2015 General Star National Insurance Company is licensed in the District of Columbia, Puerto Rico and all states. General Star National Insurance Company has its principal place of business in Stamford, CT and operates under NAIC Number 0031-11967. Insurance is placed with General Star National Insurance Company by licensed producers. General Star Indemnity Company is an eligible surplus lines insurer in all states, the District of Columbia, Puerto Rico, and the Virgin Islands. It has the status as an unlicensed insurer in California and operates

under NAIC Number 0031-37362. Insurance is placed with the General Star Indemnity Company by licensed producers and, for risk that qualify, by licensed surplus lines brokers.

Atlanta 404 239 6777 Chicago 312 267 8600 Los Angeles 213 630 1930 New York 212 859 3950 Stamford 203 328 5700

A.M. Best A++ XV S&P AA+ A Berkshire Hathaway Company

GENSTA16332.indd 1 8/26/15 5:15 AM

W2 | INSURANCE JOURNAL-WEST September 7, 2015 www.insurancejournal.com

WEST COVERAGE

News & Markets

Thefederalstatuteoflimitationsforfiresissixyears,comparedwiththestateofCalifornia’sthree. AnEdisonspokesmansaidtheutilitycompany’spolicyisnottocommentonpendinglitigation. Copyright2015AssociatedPress.

Federal Government Suing Southern California Edison over 2009 Fire

Justdaysbeforethefederalstatuteoflimitationswouldhaverunout,the

governmenthasfiledalawsuitagainstSouthernCaliforniaEdisoninconnectiontoa2009firethatprimarilyburnedtheSanBernardinoNationalForesteastofHemet. Accordingtothelawsuit,anequipmentmalfunctionsparkedthefirethatburnedalmost4squaremiles,about3ofwhichwerenationalforestland. ThefirestartedAug.27,2009andwascontainedfourdayslater. Itcostmorethan$2.65milliontosup-press.

California Commissioner Applauds Supreme Court Decision Against Hartford

CaliforniaInsuranceCommissionerDaveJonespraisedarecentunanimous

CaliforniaSupremeCourtdecisionthathesaidensurespolicyholdersareprotectedfrominsurersrefusingtocoverthird-partyliabilityclaimswhentheinsuredtransferstheinsurancebene-fitsaftertheeventstriggeringcoveragehaveoccurredbutbeforeclaimsarefullyresolved. TheCourtinitsdecisioninAugustinFluorv.SuperiorCourt(HartfordAccident&IndemnityCo.)reliedheavilyontheamicusbrieffieldbyJones,whicharguedthatonceaninsureracceptspremiumforariskandthecoveredeventsoccurduringthepolicyperiod,theinsurer’sobligationisfixedanditmustdefendtheinsuredagainstsubsequentthird-partyclaimseveniftheinsurancebenefitsaretransferredtoanotherentitybeforeclaimsarefullyresolved.

Thisiscodifiedininsurancecode,andisaquintessentialconsumerprotectionthatrequiresinsurancecompaniestodeliverontheirpromisetopayclaimsthatarisefromeventsthatoccurduringthepolicyperiod,

Jonessaid. “Thecourtmadetherightdecisioninfind-ingthatonceaninsureracceptspremiumtocovercertainrisks,andthoserisksactuallyoccur,theinsur-

er’sobligationsarefixedregardlessofanysubsequenttransferoftheinsurancebene-fits,”Jonessaidinastatement.“Thestatuteisclear.Insurersshouldnotbeabletoavoidtheirobligations.” IntheFluorv.SuperiorCourtcase,theissuewaswhetherHartfordcouldwalkawayfromcoverageobligationswhenFlourtransferredtheinsurancebenefittoanotherentity,aftertheeventstriggeringtheinsur-

Study: Ventura, Oxnard in California Could Be at Greater Tsunami Risk

AstudysaystwoCaliforniacoastalcitiesareatgreaterriskfromtsunamisthan

previouslythought. ThestudyreleasedinAugustbytheAmericanGeophysicalUnionexaminedthefloodingriskifearthquakefaultsintheSantaBarbaraChannelarearuptured. Coastalbuildingsdirectlyoppositethefaultswouldnaturallybeatrisk. Butacomputersimulationofamagni-tude-7.7quakesuggeststheresultingwavewouldsplit,turnandmovemuchfartherinlandthanpreviouslythought—perhapsmorethanamile. VenturaandOxnardcouldbehitwithawave23feethigh. Thestudy’sleadauthor,KennyRyanoftheUniversityofCalifornia,Riverside,saysthetsunamimightpenetratetwiceasfarasthelinestatedintheofficialstatetsunamiplan—whichmayneedtobeupdated. Copyright2015AssociatedPress.

ancecoveragehavealreadyoccurred. Inthiscase,Fluortransferreditsinsur-ancecoveragetoanothercompanyandaliabilityclaimwaslaterfiled.Thecourtupheldtheexistingconsumerprotectionslong-codifiedininsurancecodesection520andrequiredtheinsurertomeetitscover-ageobligationsregardlessofthetransfer.

Whoever heard of a $2,500 Earthquake Deductible? We have.

Our revolutionary Equity Protector Earthquake product makes people rethink how they buy earthquake insurance. Instead of buying a policy that covers the entire cost of rebuilding a home in the unlikely event of a total loss, why not buy the amount of coverage needed to repair the damage most likely to occur? Your customer can choose the amount of coverage desired (from $25,000 to $500,000) and the deductible is 10% of the amount selected. When your customer needs a more traditional earthquake product, we’ve got that covered, too. Our popular stand-alone Comprehensive Earthquake policy and Mini-Policy are also available on our exclusive on-line system, where coverage can be quoted and a policy issued in a snap.

Give us a call or visit our website to learn more about our suite of competitive products and apply to become a producer.

800.733.0880, ext. 2576 | www.cnico.com

HOMEOWNER’S EARTHQUAKE MOBILE HOME COMMERCIAL AUTO PERSONAL AUTO UMBRELLA

Our best earthquake protection is groundbreaking.

CNIQuakeAd4a.indd 1 7/15/14 6:18 PMCENNAT16804.indd 1 8/21/15 6:43 AM

W4 | INSURANCE JOURNAL-WEST September 7, 2015 www.insurancejournal.com

WEST COVERAGE

PeoplewithDaVitaHealthCarePartnersInc. Cantlonisresponsiblefordevelopingnewbusinessrelationships,andretainingandservicingexistingclients. ShewasmostrecentlyaprivatebankerwithMutualofOmahaBankinReno. Reno,Nev.-basedLPspecializesinproperty/casualty,surety,workers’compensation,employeebenefits,medi-cal/professionalpractice,personalandriskmanagementservices.

King InsuranceinCaliforniahasnamedLaura Fondarellaasvicepresidentofmarketingandproductdevelopment. Fondarellahasbeeninvolvedinthedevelopmentandmerchandisingofvariouspersonallinesandcommercialnicheproductsservingthehomeowners,mobilehomeparkandprofessionalliabilityspecialties. Shewaspreviouslyafieldrepresentativeandmarketingmanager. Fondarellahasbeenwiththefirmfor18years. KingInsuranceisaspecialtyprogrammanagerhead-quarteredinSanJuanCapistrano.

NewportBeach,Calif.-basedAlliant Insurance ServiceshasnamedRobert BennetsentoleaditsAlliantAmericasdivisionasexecutivevicepresidentandseniormanagingdirector. BennetsenwillspearheadAlliant’sefforttoexpanditspresenceinthemiddlemarketthroughstrategicacquisi-tionsandorganicgrowth. Bennetsenhasexperienceonthecarrierandbrokeragesidesofthebusiness. HepreviouslyservedasexecutivevicepresidentandmanagingdirectorofAlliantEmployeeBenefits. Alliantisalargeinsurancebrokeragethatprovidesproperty/casualty,workers’compensation,employeebene-fits,surety,andfinancialproductsandservices.

Alfred W. BottalicohasjoinedLocke Lord LLP’sglobalregulatoryandtransactionalinsurancepracticegroupinLosAngeles,Calif.,asaninsurancespecialist. Bottalicoisaformerdeputycommissionerforthefinan-cialsurveillancebranchoftheCaliforniaDepartmentofInsurance. Bottalicohas38yearsofregulatoryexperienceinallaspectsoffinancialregulationandexaminationofinsur-ancecompanies,includingstatutoryaccounting,auditingandCaliforniaInsuranceCode Dallas,Texas-basedLockeLordisaninternationallawfirm.

TheIMA Financial Group Inc.hasnamedRobin HelleritschieftechnologyandoperatingofficerinDenver,Colo. Inthenewlycreatedrole,Hellerwilloverseestrategictechnologydevelopment. PriortoIMAHellerwaspresidentandCEOofTheLeadershipInvestment,aColoradononprofit. HerexperienceincludesleadingtechnologyteamsforAmericanExpress,FirstDataandWesternUnion. IMAisafinancialservicescompanyspecializinginriskmanagement,insurance,suretyandemployeebenefitssolutions.

Peggy DrewhasjoinedCrystal & Co.’s commercialproperty/casualtydepartmentasmanagingdirector. Drewwillalsoserveastheteamleaderforthefirm’sLosAngeles,Calif.,office. Herresponsibilitiesincludethedevelopment,admin-istrationandexecutionofaccountservicestrategiesforavarietyofindustriesincludingmanufacturinganddistribu-tion,restaurantsandnonprofitorganizations. Drewhasmorethan25yearsofexperienceintheinsur-anceindustry.PriortoCrystal&Co.,DrewwasaseniorvicepresidentwithWellsFargoInsuranceServices.ShebeganherinsurancecareerwithMarsh. NewYork-basedCrystal&Co.isariskandinsuranceadvisorandinsurancebrokerage.

Berkshire Hathaway Guard Insurance Cos.hasnamedMark Martinez seniorfieldrepresentative. MartinezwillhelppromotegrowthinSouthernCalifornia.Inthiscapacity,heisresponsibleforidentifyingprospectsforappointmentswhileprovidinginformationaboutavailableresourcesandnewdevelopmentstoexist-ingmembersofthedistributionnetwork. Healsofunctionsasagents’fieldliaisonwithBerkshireHathawayGuard’sunderwriting,losscontrolandclaimsstaff. Martinezhasmorethan25yearsofexperience,primari-lyrepresentingnationalcarriers. InOctober2012,GuardInsuranceGroupwasacquiredbyNationalIndemnityCo.,awhollyownedsubsidiaryofBerkshireHathaway.

LP Insurance Services Inc. hasnamedBridget BrundigeandAndrea CantlontoitsnorthernNevadasalesteam. Brundigeisresponsiblefordevelopingnewbusinessrelationshipsaswellasretainingandservicingexistingclients. Brundigewasmostrecentlyapatientaccountspecialist

Robin Heller

Peggy Drew

Mark Martinez

Bridget Brundige

Andrea Cantlon

You’ll Get the Royal Treatment

Watch our videos at MonarchExcess.com

La Crescenta 818-249-0100 • Simi Valley 805-577-6800 • San Diego 619-521-2170 • Rancho Mirage 760-779-5555Novato 415-883-1411 • Fresno 559-226-0200 • Arizona 877-406-8026 • Hawaii 818-425-9847 • License 0697233

At Monarch, Honor Is a Way of Life

One Who Serves

Derek BorisoffChief Executive [email protected]

Doth yonder standard market betray thee? Fear not. Monarch E&S shall write all thine risks! CEO Derek Borisoff pledges his honor and his knowledge to your business.

• Commercial Lines• Personal Lines• Special Risk• Professional Liability• Brokerage

Come hither and ye shall receive the Royal Treatment!

MONARCH16801.indd 1 5/4/15 3:35 PM

W6 | INSURANCE JOURNAL-WEST September 7, 2015 www.insurancejournal.com

WEST COVERAGE

News & Markets

ancecompanies;includingtheirboardmanagementstructure,codeofconductand

risk-managementprocesses. Preservednationalsystemofstate-basedinsuranceregulationbyclarifyingtheroleofstateinsurancedepartmentsasgroup-widesuper-visorsovermulti-nationalinsurancegroups,aspartoftheInsuranceHoldingCompanySystemRegulatorAct. “Asthelargestinsurancemarketinthecountry,Californiaisagainleadingthewayinimprovingtheregulationofinsurancecompa-nies,”Jonessaidinastatement.“AB553includesanurgencyclausesoCaliforniacanhavethesenew

consumerprotectiontoolsinplaceassoonaspossible.I’dliketothankAssemblyMemberDalyforauthoringthisimportantbill.” AB553wasapprovedbytheAssemblyandSenateunanimously.Thebilltookeffectimmediatelyaftersigning.

California Insurance Company Oversight Law Signed

CaliforniaGov.JerryBrowninlateAugustsignedAssemblyBill553,

whichestablishesnewoversightaimedatreducingthenumberofinsurancecompanyinsolvencies. AB553wasauthoredbyAssemblymanTomDaly,D-Anaheim,andwasspon-soredbyInsuranceCommissionerDaveJonesandbyinsuranceindustrystakeholders. AB553improvesoversightofthecor-porategovernanceofinsurersbyaligningstatelawwithnewandimprovedstandardsdevelopedbytheNationalAssociationofInsuranceCommissionersintwokeyareas: Improvedoversightofthecorporategovernancepoliciesandpracticesofinsur-

California WCIRB Proposes Premium 7.8% Below 2015 Average

TheWorkers’CompensationInsuranceRatingBureauhassubmitteditsJan.

1,2016,purepremiumratefilingtotheCaliforniaDepartmentofInsurancepro-posingadvisorypurepremiumratesthataverage$2.45per$100ofpayroll. ThatWCIRBfigureis7.8percentlessthanthecorrespondingindustryaveragefiledpurepremiumrateof$2.66asofJuly1,2015,and0.8percentlessthantheaverageapprovedJuly1,2015advisorypurepremiumrateof$2.47. TheproposedfurtherreductionintheadvisorypurepremiumratelevelforJan.1,2016,followsa10.2percentreductionapprovedbytheCaliforniaInsuranceCommissionereffectiveJuly1,2015.Thepri-marydriversofthereductioninclude:

• Medicallossescontinuetodevelopfavor-ably;

• Recentseveritygrowthcontinuestoemergebelowprojections;

• IncreasesinprojectedwagegrowthinCaliforniaduetoeconomicexpansion.

However,thefilingcautionedthathis-toricallyhighlevelsoflossadjustmentexpenses,persistentlyhighratesofindem-nityclaimfrequency,anincreasingnumberofindependentmedicalreviewrequests,aspikeinlienfilingsinearly2015andper-sistentincreasesintemporarydisabilitydurationrequirecontinuedmonitoringastheymaydriveincreasedcostsinthefuture. TheDepartmentofInsurancewillsched-uleapublichearingtoconsiderthefiling.

Geico Agrees to $6M Settlement over Business Practices in California

Geicohasagreedtopay$6milliondollarsandimplementseveral

changestotheirbusinesspracticesaspartofasettlementwiththeCaliforniaDepartmentofInsurance,CDIannouncedlatelastmonth. Thesettlementstemsfromapeti-tioninwhichConsumerFederationofCaliforniaallegedGeico’sonlinepremiumquotingsystemwasdiscriminatoryandmisleadingtoconsumers. BasedoninformationobtainedthroughtestingoftheGeicowebsite,theconsum-ergroupdiscoveredtheinsurermisrepre-senteda$100,000/$300,000limitquoteasbeingalowest-limitsquote,whenitwasnot,accordingtoCDI. ConsumerFederationofCaliforniaallegedintheirpetitionthatthesehigherpolicylimitswereonlyquotedtocertainconsumers,basedontheireducationlevel,occupationandgender. Thoughinsurersmayalsoofferandsellpolicieswithhigherlimits,Californialawrequiresinsurerstoofferaminimumlimitspolicyof$15,000/$30,000.Geico’sonlinepremiumquotingsystemwasinaccuratelydescribingquotesforhigherlimitsasthelowestlimits,accordingtoCDI. InsuranceCommissionerDaveJonesissuedanorderapprovingthesettlementagreementandrequiringGeicotodiscon-tinueusingconsumers’educationleveloroccupationtoquotecoveragelimits,andtoofferaquotefora$15,000/$30,000policytocertainconsumersforthenextthreeyears.Theinsurerhasalsoagreedtosubmittotwice-yearlyauditsoftheirwebsiteforthenextthreeyears,toensuretheyarecomplyingwiththelaw.

GOLDBEA15088.indd 1 5/9/11 1:44 PM

W8 | INSURANCE JOURNAL-WEST September 7, 2015 www.insurancejournal.com

WEST COVERAGE

News&Markets Palmerwasarrestedwhileservingfiveyears’probationfollowingacon-victionon14felonycountsofinsurancefraud,forgery,wirefraudandgrandtheftin2014forillegallycol-lectingdisabilitybenefitsfromAllstateInsurance. CaliforniaDepartmentofInsurancedetectiveswerecontactedbyAmericanFamilyLifeInsuranceCo.aftertheinsureridentifiedsus-pectedfraudbyPalmer.AninvestigationrevealedthatPalmerwasallegedlycollectingdisabilitybenefitstotal-ing$24,000fromAFLACwhilebeingprose-cutedforthefirstcrimeagainstAllstateandcontinuedtodosoafterherconvictionandwhileonprobation. Ifconvicted,Palmercouldbesentencedtofiveyearsinstateprison.

Former California Probation Officer Nabbed for Fraud While on Probation

AformerLosAngelesCountyprobationofficer,RobynPalmer,29,ofLong

Beach,Calif.,wasarrestedinlateAugustonsixfelonycountsofinsurancefraudfor

allegedlyforgingdocumentstoillegallycol-lectdisabilityinsurancebenefitswhileserv-ingprobationforanotherinsurancefraudconviction.

ABRAM16741.indd 1 8/26/15 11:53 AM

Calif. Man Hurt in Trolley Station Fall Gets $21.5M Insurance Settlment

AnImperialBeach,Calif.,manwhowasinjuredwhenhetrippedandfellon

trolleytracksisreceivinga$21.5millioninsurancesettlement. Fifty-seven-year-oldDavidLongwasinjuredinMay2013whenhesteppedoffthetrolleyandtrippedoverapieceoftrack.Hehithisheadandsufferedinjuriestohisneckandspinalcord,whichhislawyerssaylefthimquadriplegic.LongfiledalawsuitagainstHMSConstructionInc.,AsphaltandConcreteEnterprisesInc.,SanDiegoTransitCorp.,SanDiegoTrolleyInc.andotheragenciesinJanuary2014. Hislawyersaidsurveillancevideoshowedasmanyas10peopletrippingovertheexposedtrack. ThecasesettledinlateJuly. Copyright2015AssociatedPress.

Robyn Palmer, A former Los Angeles County probation officer, was arrested on six felony counts of insurance fraud for allegedly forging doc-uments to collect disabil-ity insurance benefits while on probation for another fraud conviction.

As one of the premiere managing general agents in the excess & surplus

arena of insurance products, we are committed to providing leading edge

products and services in today’s chaotic, global environment.

CALL ON US FOR YOUR:

Casualty • Garage • Homeowners • Professional Liability

Property • Transportation • Umbrella • Workers’ Compensation

Proprietary On Line Quoting Available

(800) 437- 6616

w w w . g o r s t c o m p a s s . c o mLic. #0359417/0443957

NO MATTER WHERE YOU ARE, WE ARE HERE FOR YOU...

15_11158_Gorst_Insurance_Journal_Ad_V3.indd 1 6/15/15 2:18 PMGCOMP16765.indd 1 6/22/15 1:49 PM

W10 | INSURANCE JOURNAL-WEST September 7, 2015 www.insurancejournal.com

WEST COVERAGE

News & Markets

tor.TherulingorderedUbertoreimburseBerwick$3,878formileageandtollsplus

$274ininterest. Inasimilarmatter,theFloridaDepartmentofEconomicOpportunitydecidedinMaythatfor-merUberdriverDarrinMcGillishadbeenan

employee,whichentitledhimtounemploy-mentbenefits. Bothdecisionsapplyonlytotheindi-

Uber Headache if More Drivers Want Full-Time StatusBy Don Jergler

Thousandsofnewfull-timeworkerswouldspringintoexistenceifUberis

forcedtostoptreatingsomeofitsdriverslikecontractworkers,andthebenefitsthatcomewiththatemployeestatusmayenticepart-timeridesharedriverstobeefuptheirhoursofoperation. ArecentstudyfromtheconsumerfinancesiteNerdWalletshowsUberdriversinsixmajorU.S.citieswouldreceivepaidholidaysandhealthcarebenefitsworthan

averageof$5,500ayear,plusthousandsofdollarsmoreinmileagereimbursement,iftheSanFrancisco-basedfirmprovidedthemwiththesamebenefitsasitsfull-timeemployees. ThecatalystforthestudyisaCaliforniaLaborCommissioner’srulinginJunethatUberdriverBarbaraBerwickwasanemployeeofthecompanyandnotacontrac- continued on page W12

‘Eighty-seven percent of drivers say the main reason to use Uber is because they love being their own boss.’

SIAA.Helping independent

insurance agents soar to new heights.

2020celebrating years

[email protected] | www.siaa.net

ACCESS TO COMPANIES

LOCAL &NATIONAL

INCENTIVES

BUSINESSINSURANCE RESOURCES

AGENCYDEVELOPMENT

MARKETINGASSISTANCE

SIAAJL16316.indd 1 2/7/15 4:49 PM

W12 | INSURANCE JOURNAL-WEST September 7, 2015 www.insurancejournal.com

WEST COVERAGE

News & Marketsleftoutothercostfactors,suchasworkers’compensationinsurance,whichwoulddependonUber’sbusinessmodelgoingfor-wardifsomeofitsdriverswereconsideredfull-time. Hethinksthefiguresinthestudyareenoughtoenticesomedriverstoconsideruppingtheirridesharedrivingeachweek.

“IfUberprovidedfull-timebenefits,thatwouldmotivatemoredriverstobecomefull-time,”Chusaid. Uberhasarguedthat

manyridesharedriversdon’twanttobefull-time,becausetheydrivetoaugmenttheirexistingincomeandtheydon’twanttogiveuptheirflexibilityandindepen-dence. AccordingtoapollbyUberofitsowndrivers:85percentofrespondentscitedmoreflexibilityintheirscheduleandbal-ancetheirworkwithlifeandfamilyasamajorreasontoworkwithUber;50per-centofU.S.Uberdriver-partnersdriveonaveragefewerthan10hoursperweek;and65percentofdriver-partnerschangedthenumberofhourstheyworkedbymorethan25percentfromoneweektothenext. Campbellbelievessomecompromiseintheemployeevs.contractorissuecouldbefoundthatbenefitsbothfull-timedriversandUber “Ithinkthere’salotofroomforcompro-miseormiddle-groundswhereUbercouldprovidemorebenefits,”hesaid. Hebelievesacompromiseinwhichcertainbenefitswereofferedtofull-timedriverswouldenableUbertoalsobenefitbyallowingitmorecontroloverthosedrivers,suchasenablingthefirmtoensurethatfeweraredriversarebunchedtogethertoofferridesfromthe9a.m.-to-5p.m.mid-weekslowtimeandthatmoredriverswereavailableduringtheprimetimeoperatinghours. “IthinkthatUberhasthemindsetthatthesituationisallornothing,”Campbellsaid.“Ithinkthat’sprettymisleading.” LindaT.Pierce,anattorneyandareaexecutivevicepresidentwithglobalbroker-

vidualsinvolved,anddonotsetlawsorregulationsthatUbermustfollowwiththerestofitsemployeesinthosestates.Uberisappealingthosedecisions. Initsappeal,UbernotedthatinCalifornia,apreviousrulingbythesamecommissionconcludedin2012thatadriverperformedservicesasanindependentcon-tractorandnotasabonafideemployee. Inacasethatcouldbeturnedintoaclass-actionsuitandcoverallofUber’sdrivers,threedriverstookUbertoafederalcourtinSanFrancisco,contendingtheyareemployeesandentitledtoreimbursementforexpenses,includinggasandvehiclemaintenance.ThecaseinU.S.DistrictCourt,NorthernDistrictofCaliforniaisDouglasO’Connoretalvs.UberTechnologiesInc. Uberprovidedastatementonthatsuit: “Eighty-sevenpercentofdriverssaythemainreasontouseUberisbecausetheylovebeingtheirownboss.Asemployees,driverswoulddrivesetshifts,earnafixedhourlywage,andlosetheabilitytodriveusingotherridesharingappsaswellasthepersonalflexibilitytheymostvalue.TherealityisthatdriversuseUberontheirownterms:theycontroltheiruseoftheapp.It’swhythere’snotypicaldriver—thekeyquestioninthiscase.Andwhynothreepeoplecaneverrepresenttheinterestsofsomanydifferentdriv-ers.” Asidefromthepossibilityofaclass-actionsuit,shouldtheexist-inglabordecisionsbeupheld,somebelievemoreridesharedriverscouldbemotivatedtoseekstatusasfull-timeemployees. Justhowmanyemployeesthisaffectsisn’tclear,butifallUberdriverswerecon-sideredfull-timeemployeesthefirmwouldrankamongthetop50U.S.employersbysize—somewhereaboveBoeingCo.andStarbucks,andbelowSafewayandBankofAmerica. UberinJanuaryreportedthatnearly

14percentofits160,000-and-countingU.S.driversworkedatleast35hoursaweek.Thefirmalsoreporteddriversearned$17.56onaverage. TherearenospecificfiguresforthenumbersofUberdriversineachstate,butHarryCampbell,whoblogsforForbesonthetopicofridesharing,believesCaliforniahasalargerpercentageofridesharedriverswhoarefull-time. Hisreasoningisthatthestateiswheretheridesharingcrazefirstexploded,andasignificantportionofCaliforniaisthinonmasstransitandheavilyautomobilereliant. Campbell,whooftenpollsridesharedriv-ersonhiswebsite,TheRideShareGuy.com,estimatesthatroughly30percentofUber

driversspend40hoursormoreperweekscouringthestreetsforridesandtakingpassengerstoandfro. “Idothinkthere’salotofdriversthatthiswouldaffect,”Campbellsaid. Askedtoputanumberonthetotalnumberoffull-timeUberdrivers,hepostulatedthatasmanyas15,000couldbeconsideredfull-timeemployees. TheNerdWalletstudyoutlinedthebenefitscostsforthoseemployeesinpaidholidays,healthinsurance,mile-agereimbursementandautoinsurance. BasedonUber’sstatedaveragehourlywageforfull-timedrivers,thechangeinemploymentstatusaddsupto$1,264.32forninepaidholidayseachyear.Healthinsurancecostsvarybyarea,butinLosAngelesit’s$2,859peryearandNewYorkit’s$3,585peryear,accordingtoNerdWallet.

Tocalculateestimatedmileagereim-bursementthestudyusesBerwick’sdrivingtotals,whichifextrapolatedtofullyearwouldaddupto38,808miles.Anemployeedrivingthosemileswouldget$22,315inreimbursement. Autoinsuranceratesalsovarybylocale,butinLosAngelesit’s$1,175.61andinNewYorkit’s$1,614.71,thestudyshows. JeffreyChu,theauthorofthestudy,saidhestucktoabarebonescomparisonand continued on page W14

continued from page W10

‘I do think there’s a lot of drivers that this would affect.’

www.mjhallandcompany.com

WORLDS OF EXPERIENCE

SURPLUS LINES BROKER GENERAL AGENT

Since our inception in 1973, M.J. Hall and Company, Inc. has earned aname for dependable surplus lines insurance. As one of California’s mostexperienced general agents, the M.J. Hall team of insurance professionalssets the standard for customer service, product knowledge and reliability.

(209) 948-8108

COMMERCIAL PROFESSIONAL BINDING BROKERAGE

LICENSE #04889001

MJHALLCO16800.indd 1 2/10/15 1:23 PM

W14 | INSURANCE JOURNAL-WEST September 7, 2015 www.insurancejournal.com

WEST COVERAGE

News & Marketssuchasallowingemployeestoworkremotely,andreducingoverheadbycut-tingdownonneededofficespacewhileincreasingemployeeflexibility,Methenysaid. “Therulesaremakingitevenmorechal-lengingforemployerstomovewiththe

trends,”hesaid. Thereversalofthesetrends,possiblyforcingsomeemployerstobringworkersbackintotheofficeandinsistontightercontrolsandlessflexibility,couldmakeforsomeunhappyemployer-employeerela-tionships.

“We’regoingtoseelotsofwageandhoursuits,”hesaid. MethenycountsemploymentpracticesliabilityinsuranceasamongtheinsuranceimplicationsforUberiftheBerwickcaseisupheldandmoreemployeesseekfull-timestatus. Anexampleisanemployerthattreatsallofitsemployeesasindependentcontrac-tors,andthenthere’sanincidentinwhichoneindependentcontractorisaccusedofharassinganother. Becausetheemployerconsidersthemindependentcontractors,theytake“ahandsoff”approach. “Butiftheyfailtoinvestigatethecom-plaint,andtotryandremedythesituation,thatopensthemuptoexposuresthatwouldbepassedontotheinsurerinthetraditionalEPLIpolicy,”Methenysaid. Thisiswhathappenedtoanemployerherepresentedinacaseayearago.Theemployermisunderstoodtheindependentclassificationruleandtreatedhundredsofworkersasindependentcontractorsdespitemanyoftheputtingin50hoursaweek,hesaid. Afewemployeeswereallegedlyharassedbysomeonetheyconsideredtheirsupervi-sor,yetwhowasalsobeingtreatedasanindependentcontractor,andtheemployertoldtheworkerstohandleitbetweenthemselves,accordingtoMetheny. That“handsoff”policydidn’tworkoutsowell. “Itblewuponthem,”Methenysaid.

ageArthurJ.GallagherinGlendale,Calif.,viewsworkers’compasamajorconsider-ationforUbergoingforwardiftheBerwickdecisionisupheldandotherdriversseekthesamestatus. Piercebelievesworkers’compjudgesoverseeingdisputesinvolvingUberdriverscouldusetheLaborCommissioner’srulingasguidance. “Itwouldlikelybeatestawork-ers’compjudgewoulduse,”Piercesaid.“Ithinkthat’sarealpossibili-ty.” TheBerwickcasefitsanexistingmoldinwhichforyearspeoplehavebeenclassifiedasanindependentcontrac-torandhavebroughtacasetogetworker’scompbenefits,unemploymentbenefitsordisabilitybenefits. “There’sallsortsofdifferentagenciesthatarepitfallsforCaliforniaentitiesthatuseindependentcontractors,”Piercesaid. AssoonasenoughUberdriversarehurtonthejobandtheybeginseekingworkers’compbenefits,that’swhentroublemayarisebetweenUberanditsinsurer,sheadded. “Iftheygetclaimsputin,theyruntheriskofbeingauditedbytheircarrierandbeingassessedahugepremium,”Piercesaid,addingthatthere’salsodangerthecar-rierwouldjustrescindthepolicy. BobKing,anattorneyandfounderofLegallyNanny,aCalifornialawfirmthatspecializesinhouseholdemployment,seesthedecisionintheBerwickcaseasfar-reachingand“verydangerousforUber.” TheLaborCommissionermadethefind-ingsintheBerwickcasebasedonlevelofcontrolUberexercisesoveritsdrivers.Sounlessthedecisionisoverruled,therewillbeplentyofsavvyplaintiffs’lawyersarmedwiththisdecisionasanargumentwhowillgooutandfindotherUberdriverstomakethesameclaim,Kingsaid. “BasicallywhattheLaborCommissionerhasdoneissay‘Here’swhatyouhavetosayinyourcomplainttoprevail,’”hesaid.“They’vegivenemployeesaroadmapagainstUber.” Kingtypicallyrepresentsfirmsthat

providenannies,eldercaregiversandothersimilarservicesthatoftensendpeopleouttohomes,butthoseoperationssometimesmisclassifytheiremployeesasindependentcontractors,hesaid. HebelievestheLaborCommissioner’srulingcanbeusedasastandardotherin

otherindustriesoutsideofridesharingtoshowthatcaregiversareemployeesandnotcontractors. “Thisrulingisactuallyabigdealformyindustryaswell,”Kingsaid.“Thisrulingputsanothernailthecoffintoconfirmthatworkersareinfactemployees.WhatthisLaborCommissionerhasdoneisprovidethisroadmapforemployeestosaytherightthinginthehearingtowin.” Headded,“It’snotbindingprecedent,butitispersuasive.” BryanceMetheny,apartnerandchairofthelaborandemploymentpracticegroupatBurr&FormanBurr&FormaninBirmingham,Ala.,alsobelievessuchrulingsaren’tgoingtobelimitedtooneindustry. “Thefutureisgoingtorevealit’snotgoingtobelimitedtoridesharing,”Methenysaid. OvertimepaycouldincreasinglybeanotherconsiderationUberandotherswhooperatewithindependentcontractorswillhavetodealwithifnewrulesproposedbytheU.S.DepartmentofLaborareenacted,hesaid. TheDepartmentofLaborrecentlypro-posedupdatestotheFairLaborStandardsActthatwouldextendovertimepaytoanestimated4.6millionworkerswhoarecurrentlyexemptfromundercurrentregu-lations. Theserules,alongwithdecisionslikethoseintheBerwickmatter,goagainstongoingemploymenttrendsthatbothemployersandemployeesseemtofavor,

continued from page W12

We offer a wide variety of commercial auto, garage, property, packageand general liability products.

All backed by an A++ financial rating by AM Best.

27200 Tourney Rd Suite 360 Phone: (800) 354-4844 - Fax (661) 257-5988 Valencia, CA 91355 www.pgiainsurance.com - License #: 0C04869

PACIFIC GATEWAY INSURANCE AGENCY

NopePass

Sorry

Decline

Huh?

JOHNSO001.indd 1 1/15/14 11:33 AM

Strike up some fun in San Diego at the 8th Annual Insurance Industry Charitable Foundation Bowling Charity Event. It’s a great way to build team morale while supporting local charities. Register today!

Register by Oct 1 $550 per team of four people

(includes food, drink, and raffle) Additional sponsorships available

Thursday Oct 8, 2015 2-5pm • Kearny Mesa Bowl • 7585 Clairemont Mesa Blvd. San Diego, CA

Visit bit.ly/iicfsdbowling2015 or contact Bryan Anderson at 619.686.2900 for more info.

Untitled-3 1 7/16/15 4:43 PM

September 7, 2015 INSURANCE JOURNAL-NATIONAL | 15www.insurancejournal.com

NATIONAL COVERAGE

News & Marketsof competition” in the middle market. “Insurance carriers realize that they can make money as long as they have a diversi-fied portfolio of risk and that the insured meets minimum standards.” In larger, high-risk categories, some car-riers have pulled out from being primary, resulting in less competition. Kalinich reports that there is a greater focus on retention than on pricing among carriers, with retentions that were once $1 million rising to $5 million or $10 million. “Some of the exclusions have expanded and restrictions [have increased]. Unencrypted laptops — we’re not going to cover that,” carriers say. Or “we might cover business interruption for an entity, but we’re not going to cover business interruption if it’s a third party that is disrupted and now it affects your business interruption. Those are the types of coverage issues that are being introduced into the larger risks,” he said.

How Carriers Price Cyber Insurance Standard & Poor’s released a report at the conference applauding insurers for their restraint in offering cyber coverage — a positive from a credit ratings perspective. “Even insurers with a larger market share are guarded enough to use low limits and a whole slew of exclusions (such as excluding damages resulting from data handled by an external contractor), which we believe is sensible. The need for risk-averse under-writing is heightened considering the lack of actuarial data, potential systemic conse-quences, loss creep and clash risk,” rating agency analysts wrote in “Look Before They Leap: U.S. Insurers Dip Their Toes Into the Cyber Risk Pool.” The report highlights the fact that pro-viding cyber risk coverage presents “a huge area of opportunity” for insurers, with a $10 billion potential market size seen as a real possibility within the next five to 10 years. The challenges inherent in pricing a cov-erage for which reliable actuarial is not yet available and probabilistic models are sus-

Cyber Risk Insurers Lag in Buying Cyber CoverBy Susanne Sclafane

As recently as two years ago, only half of the top 10 carriers writing cyber insur-

ance had purchased cyber coverage them-selves, a broker specialist said recently. During an interview at the Standard & Poor’s 2015 Insurance Conference, Kevin Kalinich, global practice leader for cyber insurance at Aon, told Carrier Management that the number buying cyber insurance for their own companies is up to seven of the top 10 carriers, and that two more are in the process of purchasing insurance. (Kalinich defined the top carriers as the 10 that write the most premium volume in the cyber insurance market, noting that Aon is the broker for a number of the top carriers.) “It’s over a majority, but it’s still not unan-imous that they all buy cyber insurance, the same product they’re selling,” he said. Kalinich also reported that 67 insurance companies write some form of standalone

cyber insurance today. Among market par-ticipants, “the appetite has changed but not necessarily expanded,” he said when asked if a soft market for commercial insurance has broadened carrier appetites or prompt-ed price declines. “After the large data breaches, what has happened is that many of the insurance companies that jumped in with both feet suffered their first cyber losses and are reevaluating their commitment to cyber insurance. They have either contracted, or are reducing the limits that they’ll offer from a particular risk — from $20 mil-lion to $10 million or from $10 million to $5 million. Or they have moved from the large risks of retail, hospitality, financial institutions and healthcare into more mid-dle-market risks that they view as [having] a smaller probability of a catastrophic loss.” Kalinich separates larger, higher-risk classes from lower-risk, middle-market categories, noting that there’s ”quite a bit

continued on page 16

16 | INSURANCE JOURNAL-NATIONAL September 7, 2015 www.insurancejournal.com

pect (mainly because of “the unpredictable behaviors associated with cyber attacks”). So how are insurers pricing coverage? Kalinich said insurers rely on a combina-tion of methods. “Initially, they were using a number of personal identifiable information records and then multiplying it by a number — between $175 and $225 per record.” But insurers realized “there was differentiation depending on the type of information. Social Security number and patient information in healthcare is worth more than credit card information from a retailer.” “As you increase the number of records, the cost per record goes down dramatically to be below $5 per record.”

NATIONAL COVERAGE

News & Markets In addition to getting better at bifurcat-ing the risks related to PII, insurers are get-ting better at differentiating risks beyond PII exposures. “An entity that is dependent on manufacturing, transportation, logistics, they’re looking at those types of risks now compared to what losses they’ve seen, doing modeling based on what they want to get for their return on the capital and adjusting as they get more claims and adjusting as they see more entities,” he said. “The second thing they’re doing different is partnering with modeling companies and rating companies — not rating agencies like the S&P but the equivalent for cyber risks.” “These entities now can assess their

cyber exposures and give them ratings in various categories to determine both the fre-quency and severity of a potential loss. The insurance companies reward those compa-nies that embrace those assessments and make changes, and mitigate and remediate vulnerabilities,” Kalinich said. “Four or five years ago, the insured may have paid for an IT security assessment. Now, insurance companies are not only including some of those as part of their service offering, but they’re demanding that you take on this type of antivirus software or intrusion detection or the equivalent. They still let you do the equivalent.” “It’s actually a tremendous benefit, more so for the small and middle-market com-panies that might not have that expertise,” he said, distinguishing them from larger insureds who want to have direct relation-ships with third-party vendor partners instead of having those controlled by the insurance company. Kalinich said pricing differentials between carriers are decreasing as the use of these assessments are not becoming more widespread. “You would think that they would converge and come closer together based on their assessments. We have seen tremendous divergence in pricing and retention,” he said More typically, there are coverage vari-ations among carriers. “Cyber insurance is not a homogeneous product,” S&P analysts said in their report — a situation that is not bothersome to Kalinich. “It’s okay to have the nuances in the pol-icies to differentiate the coverages,” he said, when asked if a standardized offering might benefit insurers. “Where I think there needs to be more commonality is all carriers look-ing at some of the same type of factors that go into the risk,” he added, reasoning that “if they start taking into account the import-ant factors on a more macro level, that will improve risk management in totality.” “So you can’t have an organization use adverse selection to go to a carrier that doesn’t understand the [right] questions [to ask]. It actually would improve the whole risk management if they have a baseline of the factors that they consider,” he said.

continued from page 15

S&P: U.S. Insurers Cautious to Respond to Soaring Cyber Demand

Standard & Poor’s predicts a major jump in demand for cyber insurance

in the coming years, with interest initial-ly outstripping supply. U.S. insurers will respond gradually, however, entering the market with caution, allowing for breath-ing room to develop knowledge and experience about the fast-evolving risk, the rating entity found in a new report. Insurers remain hesitant to embrace cyber risk quickly because it is “fast mov-ing, impossible to predict, and difficult to understand and model, but change can be immense,” S&P noted. Another concern: aggregation risk and clash with other policies. S&P outlined these and other insur-ance-related cyber trends/concerns in its newly-released report: “Looking Before They Leap: U.S. Insurers Dip Their Toes In The Cyber-Risk Pool.” The report says cyber insurance demand will grow “as management teams utilize both offensive and defen-sive capabilities,” and perception of cyber risk and its financial costs grows due to increasing media coverage. Attacks will increase in both frequen-cy and sophistication as losses grow. Lloyd’s estimates that there are around

$400 billion in annual losses due to cyber hackings, only a small number are insured, S&P said. With that in mind, cyber insurance is gaining more promotion and regulators are encouraging companies to buy it to help manage their risks and minimize the cost of a breach. Cyber breaches can dam-age an organization’s reputation, and that could spur the growth of the cyber mar-ket. More regulations passed in response to hackings should also trigger interest in cyber coverage, according to the report. “Cyber insurance is a sellers’ market, unlike more developed/traditional busi-ness lines,” S&P said. However, insurers aren’t exactly jumping in “with both feet” for a number of reasons. “Due to the changing nature of tech-nology and hacking strategies, insurers don’t have an accurate loss history,” S&P noted. “Whereas traditional liability products may use revenue and industry as particularly important drivers of risk assessment, it is much more difficult to determine a company’s ability to defend itself from a very determined hacker.” S&P said it expects cyber insurance capacity to increase as experience in the sector grows.

SeeYourself

as a

CPCU

Why CPCU?With The Institutes’ Chartered Property Casualty Underwriter (CPCU®) designation you

transform learning opportunities into career success.

• 85% of CPCUs believe earning the designation accelerated their career.

• 90% of CPCU designees say their job opportunities increased.

• 74% of CPCUs say the designation helped them gain a promotion or salary increase.

• Join a network of 22,000 CPCU Society members dedicated to professionalism.

Commit to Your Success—Order Course Materials Today!

www.TheInstitutes.org/CPCU

© 2015, American Institute For Chartered Property Casualty UnderwritersCPCU is a registered trademark of The Institutes. All rights reserved.Statistics are based on a 2008 survey of CPCU program completers. www.TheInstitutes.org

INSTBRA16785.indd 1 7/22/15 6:43 AM

18 | INSURANCE JOURNAL-NATIONAL September 7, 2015 www.insurancejournal.com

NATIONAL COVERAGE

Business Moveshealthcare organizations and pro-viders. Dan Nissi, DISNE’s president, will join Hub as president of Healthcare Solutions for Hub New England, a Hub International subsidiary, and report to Charles Brophy, CEO of Hub New England. In a separate deal, Hub also acquired the assets of Triangle Insurance Services Inc., an inde-pendent insurance agency based in Raleigh, N.C. Terms of the acquisition were not disclosed. Triangle Insurance specializes in providing property/casualty insurance services to clients in the Cary/Raleigh area. Cleve and Linda Folger, the founders

and owners of Triangle Insurance, are joining the Hub Carolinas division of Hub International Southeast. Hub International is an insurance broker-age that provides property/casualty, life and health, employee benefits, investment and risk management products and services.

Beneficial Insurance, PKA Beneficial Insurance Services, a subsid-iary of Beneficial Bank in Philadelphia, acquired Pye Karr Ambler & Co. Inc. (PKA), an independent insurance agency in Jenkintown, Pa. Terms of the transaction were not disclosed. Under the transaction, PKA President and CEO Lou Karr and the agency’s two staff members will join Beneficial Insurance. PKA’s Jenkintown office will continue to be used for the immediate future, Beneficial Insurance said. Beneficial Insurance is an insurance bro-kerage offering commercial, personal, and benefit products.

Union Insurance, McLaughlin Co. Union Insurance Group, a Chicago-based commercial insurance agency specializing in property/casualty and professional liabili-ty products for labor organizations, acquired The McLaughlin Co., an insurance agency in Rockville, Md. Terms of the transaction

Distinguished, Fulcrum Distinguished Programs Holdings LLC announced the pending acquisition of Bellevue, Wash.-based Fulcrum Insurance Programs. The businesses will be combined and rebranded as Distinguished Specialty. Fulcrum principals Dusty Rowland and Eric Arthur will be joining Distinguished Specialty as senior executives and Rowland will join Distinguished’s board of advisors when the deal is concluded. Brooks Chase will become president of Distinguished Specialty. The deal is expected to close at the end of October. New York-based Distinguished is a port-folio of businesses serving the insurance industry. Fulcrum is a program administrator focused on real estate and hospitality.

Hub International, DISNE, Triangle Insurance Hub International Limited acquired the assets of Doctors Insurance Services of New England (DISNE). Terms of the acquisition were not disclosed. Based in the Boston suburb of Holliston, Mass., DISNE specializes in providing per-sonal and professional liability, including medical malpractice insurance services, to

were not disclosed. Union Insurance Group provides com-mercial insurance including property/casu-alty and professional liability coverage to labor organizations of various sizes.

AAdvantage Insurance Group, Premier Insurance Associates AAdvantage Insurance Group in Glen Carbon, Ill., led by founder Dave Viox, recently announced a merger with Premier Insurance Associates located in Edwardsville, Ill. Vince and Deb Valesano, former owners of Premier Insurance Associates, will also join AAdvantage Insurance Group. AAdvantage specializes in farm, com-mercial, home, auto and life insurance and serves clients in the Metro-East/St. Louis area, as well as throughout Illinois and Missouri.

Meadowbrook Insurance, Mackinaw Administrators Meadowbrook Insurance Group Inc., based in Southfield, Mich., has acquired Mackinaw Administrators LLC (Mackinaw). Mackinaw is a Michigan-based program and claims administrator that provides tai-lored insurance and risk management pro-grams and other related services for both group and individual clients. Under the terms of the transaction, Mackinaw will operate as an independent subsidiary within Meadowbrook. Mackinaw will maintain its present headquarters in Brighton, Mich., and continue to be led by its current management team, including the company’s president, Stephen Flechsig.

Higginbotham, Commercial Global Insurance Higginbotham, based in Fort Worth, and Commercial Global Insurance (CGI), based in Deer Park, Texas, are merging their oper-ations in Friendswood, Texas. Higginbotham’s union with CGI is its second merger in the Friendswood area and brings its total number of employees to 660 in 22 offices. Higginbotham provides property, lia-

continued on page 20

Fujitsu iX500 silhouette-printAgency contact: Jon Miwaphone: 926-642-3053email: [email protected]

Incredibly fast

Intuitively smart

One button simple

http://ez.com/insj

wireless desktop scanner

© 2015 Fujitsu Computer Products of America, Inc. All rights reserved. Fujitsu and the Fujitsu logo are registered trademarks of Fujitsu Ltd. All other trademarks are the property of their respective owners.

Own productivity

FUJITPFU16719.indd 1 7/15/15 1:35 PM

20 | INSURANCE JOURNAL-NATIONAL September 7, 2015 www.insurancejournal.com

NATIONAL COVERAGE

Business Movesbility, life and health insurance, risk man-agement and employee benefit services to businesses and individuals. CGI is a boutique agency that provides commercial insurance and bonds to businesses and investors primarily in the industrial, environmental and construction industries. CGI founder Blake Barnes will serve as a managing director of the combined firm.

TIA-TCOR TCOR Management, based in New Braunfels, Texas, has formed a new insur-ance agency, TIA-TCOR LLC, dba Texas Insurance Agency. With Ben Reedy as principal, San Antonio-based TIA-TCOR provides insur-ance, risk management, surety and employ-ee benefits to organizations across Texas and the nation. The firm maintains a focus on the energy, construction, manufacturing, healthcare, life sciences, non-profit, real estate, retail and wholesale trade, and technology indus-tries.

Marsh & McLennan,Tequesta Insurance Advisors Marsh & McLennan Agency LLC (MMA), the middle market agency subsidiary of Marsh, has acquired Tequesta Insurance Advisors, a personal, commercial, and employee benefits insurance provider in Florida. Terms of the transaction were not disclosed. With approximately $10 million in annual revenues and 50 employees, Tequesta adds additional property/casualty capabilities and personal lines expertise to MMA’ s Florida region. All of Tequesta’s employees are joining MMA and will continue to oper-ate out of the agency’s Tequesta, Fla. office. According to Shannon Alfonso, president of MMA’s Florida region, MMA now has more than 220 colleagues in eight offices throughout Florida.

Marsh, Dovetail Insurance Marsh has signed a definitive agreement to acquire Dovetail Insurance, a provider of

insurance technology services tailored to the U.S. small commercial market. Terms of the transaction, which is expected to close in the third quarter, were not disclosed. Based in Columbia, S.C., Dovetail has developed a cloud-based technology plat-form that enables independent insurance agents, on behalf of their small business clients, to obtain online quotes from multi-ple insurance providers and bind insurance policies in real-time. Upon closing, Steve Francis, CEO of Dovetail, and the entire Dovetail team, will join Marsh. Dovetail will be part of Marsh’s Global Risk & Specialties segment.

Johnson & Johnson, John Handel & Associates Managing general agency Johnson & Johnson Inc. (J&J) has acquired John Handel & Associates Inc. (JHA), located in St. Petersburg, Fla. John Handel & Associates was estab-lished in 1983 as a full service multi-line E&S brokerage agency serving Florida. The company will continue to serve its agents and insureds from JHA’s office in St. Petersburg and from the current J&J office in Melbourne, Fla. The entire JHA team will join the organization. Based in Charleston, S.C., J&J is a full-service MGA offering E&S markets, standard markets, and premium financing to independent insurance agents.

Patriot National, RCA Patriot National Inc., a workers’ com-pensation outsourcing services firm based in Fort Lauderdale, Fla., acquired R.C.A. Insurance Group (RCA), a Clifton, N.J.-based property and liability program administrator to the hospitality industry. Terms of the transaction were not dis-closed. RCA provides preferred insurance pro-grams designed for restaurants, bars and taverns nationwide. RCA will become part of Trigen Insurance Solutions, Patriot National’s operating subsidiary focused on expansion into broader commercial insur-ance lines.

continued from page 18

ENER

GYR

ISK

S