· pdf filethe insurance generally covers all the warranties given by the seller as well as...

TRANSCRIPT

Aon Risk Solutions

LifecycLe of a cLaim

Core financial lines policies

Aon Risk Solutions 1

PARt 1: iNtRODUCtiON 2

PARt 1: CORe FiNANCiAl liNeS POliCieS 3

PARt 2: PRe-lOSS ChAlleNgeS 9

PARt 3: WheN A ClAim OCCURS 12

PARt 4: POSt-ClAim: leARNiNg leSSONS 16

PARt 5: the AON ADvANtAge 18

TaBLe of coNTeNTS

2 lifecycle of A Claim

iNTRoDUcTioN

this eBook will guide you through the lifecycle of a financial lines claim, providing an insight into the many challenges which insured parties face, the responsibilities of a broker, the claims handling process, and how optimal outcomes can be ensured.

Businesses and individuals purchase insurance policies for the purpose of benefitting from their protection in the event of a loss. When the worst happens, you expect your policy to respond in a timely and fair manner, indemnifying you or offering protection when you need it.

however, selection of the wrong insurer, inappropriate policy limits or deductibles, and the breach of important conditions in insurance policies, can all result in unsatisfactory claims outcomes that could directly impact the financial health of your organisation. As the regulatory environment continues to evolve in europe and as society becomes progressively more litigious, achieving positive claims outcomes becomes increasingly important.

Claims can be complex and the investigation process can be lengthy. When dealing with Professional indemnity (Pi) or Directors and Officers (D&O) insurance, you may be investigated by an authority scrutinising possible criminal, administrative, or regulatory misdemeanours. Furthermore, in complex cases, it may not always be immediately clear whether particular types of losses are covered under your existing insurance policies, and insurers can and do raise legal defences in order to attempt to deny claims which they believe are not covered.

how policies respond in the event of a claim is the true test of insurers and insurance brokers. the final outcome of whether a claim is paid in full, partially paid, or declined is affected by a number of factors. Before a policy incepts and before a loss occurs, it is vital to have a clear understanding of your risk profile and how any insurance will respond in various loss scenarios. there is no international standard for claims handling, as each client’s needs vary considerably, along with the nature, severity, and frequency of losses they will

experience. however, in order to have peace of mind, you must have confidence in the quality of the insurance programme your broker has placed for you, your broker’s technical knowledge and claims handling ability, and the quality and professionalism of the insurers underwriting your risk.

the role of a broker in representing their clients in the event of a loss may need to extend far beyond a simple notification of a claim in some cases. Complex claims may require a broker to project manage the claims process and advocate your interests at each step of the process. their role may include:

Providing help and guidance in the investigation of losses and claims

Assisting with negotiations on your behalf, liaising with insurers and their representatives

Facilitating face-to-face meetings between you and your insurers

managing relationships that become fractured and exploring amicable resolutions to prevent protracted and expensive litigation

Utilising specialist claims advocacy services from in-house coverage counsel experienced in dispute resolution

Reviewing the claims strategy, challenging insurers and lawyers

Being focused on getting the best outcome for their client

Offering consultancy support, analysis, and guidance where required

Providing litigation management to assist in the selection of outside counsel, development of procedural guidelines, case monitoring, and internal claims team interface

Aon Risk Solutions 3

Part

1

CoreFinancial linesPoliCies

4 lifecycle of A Claim

Core financial lines policies

this ebook focusses on the life cycle of financial lines claims and so, before entering into a discussion on some of the challenges which you may encounter as a result of financial lines claims; below, we provide an overview of some of the core financial lines policies:

Professional indemnity (Pi)

/ errors & omissions(e&o)

insurance

Coverage

Pi insurance covers the insured company against liability (by reason of judgments against them, settlements, or costs of legal defence) through actual or alleged acts, errors and omissions committed during the provision of, or in relation to the failure to provide, professional services, by the insured or by another party acting on the insured’s behalf, to their customers or clients. An example of a loss which would typically be covered is liability resulting from a claim against an insured institution for mis-selling a financial product.

Who should buy Pi/e&O?

Any company which provides services to clients or owes a duty of care to a class of persons, as these companies may be exposed to claims for compensation. those claims, particularly where litigated, can result in costly settlements or judgments against the insured company, and inevitably involve significant legal costs.

Organisations which provide advice or services in relation to sensitive or complex issues, or matters of significant value are particularly exposed (e.g. investment advisors, lawyers, and accountants) and should ensure that adequate Pi/e&O protection is in place. For many of these professionals, such insurance is mandatory.

What best-in-class cover looks like

Arguably the most important clause in a Pi/e&O policy is the definition of the Professional Services (in some cases “Financial Services”) provided by the insured company. the policy’s insuring clause is constructed around this definition, so it is critical that the scope of the services provided by the company is drafted broadly enough to capture all claims, and ideally to capture work performed which is related or incidental to those services.

Aon Risk Solutions 5

Directors & officers

(D&o) liability

insurance

Coverage

D&O liability insurance provides cover for claims made against directors and officers for “Wrongful Acts” in their capacity as such of the company. Where the organisation is permitted by law to indemnify such individuals, the policy will reimburse the company for such amounts, subject to deductibles. Where the insured company is not permitted to indemnify directors and officers, the policy will pay such amounts directly on behalf of the individuals with no deductible applied. D&O policies cover claims against directors and officers arising from:

Regulators investigations for breaches of regulatory conduct

employees actions for alleged wrongful termination of employment, discrimination, and sexual harassment

Customers, clients & consumer groups actions where a director or officer is held personally liable in a similar manner to the company for product liability

Competitors actions for alleged breach of copyright and patent breaches

government bodies actions in respect of the legal environment of a company, this would involve fraud, civil rights violations, and licensing issues

Shareholders actions arising out of mergers, takeovers, financial disclosure, acquisitions, and divestitures

Who should buy D&O?

Before considering taking a role as a director, individuals should ensure that their organisation has sufficient D&O coverage. D&O insurance is a financial safety net for directors and officers and a backstop to corporate indemnification. the true value of D&O insurance to an individual is the ability of the insurance to respond to situations where the individual is accused of wrong-doing and is unable to recover his or her legal expenses from the company. Companies may not be able to indemnify for a variety of reasons including legal restrictions, financial constraints, public policy considerations or plain company unresponsiveness. Directors and officers do not want to find themselves in a position of footing the bill for their own defence, which can be very costly, particularly involving cross-jurisdiction claims. Companies want to ensure they have adequate insurance so they can attract high quality individuals to serve on their board. individuals will want to benchmark the level and terms of insurance their employer holds against peer companies, while at the same time considering the financial strength of the company and its ability to indemnify them if required.

What best-in-class cover looks like

Basic D&O insurance will include components of coverage for individuals where no indemnification from the company is forthcoming (A-side), as well as coverage for the company itself to the extent it does indemnify (B-side). it is common to see the company also named as an insured for securities claims (C-side). Companies may also want to consider a separate dedicated A-side tower of insurance to provide individuals with peace of mind that insurance will be available for them alone and which cannot be eroded by claims against the entity assumed to be an asset of the company in a bankruptcy situation.

6 lifecycle of A Claim

Cyberinsurance

Coverage

A standalone cyber insurance policy offers broad cover for both the first party costs incurred by a company and its liability to third parties in the event of a cyber-attack, data breach, or system disruption. Cover includes:

Breach event notification and management costs including forensic investigations, public relations expenses, credit monitoring services, and legal advice

Network business interruption: loss of income and extra expenses due to a system disruption

the costs to restore or recreate data or software

third party claims arising from network security failures that result in unauthorised access to data, dissemination of confidential information, and damage to third-party systems

Regulatory proceedings and investigations, including associated fines and penalties as well as legal expenses

Cyber extortion payments and expenses where permissible by law

Who should buy Cyber?

Cyber risk exposure is directly proportional to technological reliance. Accordingly, the more an organisation processes or stores sensitive data or relies on digital automation or connectivity, the more pressing the need for a cyber risk transfer insurance solution. high-risk industries include financial services, healthcare, hospitality, aviation, e-commerce, and telecommunications.

What best-in-class cover looks like

Cyber insurance policies, when compared to more traditional policies, are in a relative state of flux, allowing insureds and their brokers to craft policies which respond to specific exposures. there are numerous levers to be pulled within a typical cyber policy, so organisations should seek to expand cover for non-malicious events (e.g. operator error or system failure), expert engagement (e.g. public relations) in the event of a system disruption and system repair, and improvement coverage.

Aon Risk Solutions 7

Warranty & indemnity

(W&i) insurance

Coverage

W&i insurance protects either the buyer or seller in a merger & acquisition (m&A) transaction from financial loss arising from a breach of the representations and warranties or claims against the tax indemnity given by the seller in the transaction under a sale and purchase agreement (SPA).

the insurance generally covers all the warranties given by the seller as well as the tax indemnity or tax deed, with the intent being that the W&i policy will mirror as closely as possible the terms of the SPA.

these insurance policies have certain limited exclusions from coverage. the position varies between insurers, but generally speaking, they include the following topics:

matters which the insured is aware of and which would give rise to a claim under the warranties

Forward looking warranties

Pension underfunding

transfer pricing

Certain tax liabilities

Criminal fines and penalties uninsurable at law

Fraud of the insured

Anti-bribery/corruption matters

Who should buy W&i?

W&i insurance provides the buyer with the certainty that they will receive compensation for post-closing claims (that fall within the scope of the policy), and the seller with the knowledge that the insurer would not look to the seller to recover such payments (except under certain circumstances such as fraud by the seller). As such, W&i insurance is often used strategically by industry players to lower purchase prices (buyers), reduce escrows (buyers), distinguish buyers’ bids, achieve clean exits (sellers), or incentivise more participants in an auction (sellers).

What best-in-class cover looks like

Known or fairly disclosed breaches or specific indemnities are generally not covered under a standard W&i policy. that said, there are specialist insurance products and extensions available in the market that provide additional coverage.

Specialist products include transaction liability insurances for tax liabilities, litigation liabilities, contingent liabilities, and environmental liabilities. examples of insurable tax risks include diligence issues, transaction structure (tax free structuring, reorganisation, spin-offs etc), real estate tax, unwinding fiscal unity, employment benefits/deferred compensation issues, and net operation loss carry forwards.

Other bespoke extensions include cover for new known breaches (coverage for breaches occurring and discovered post-signing but pre-completion) and Committee of Foreign investment in the United States (CFiUS) reverse break fee (coverage for break fee to be paid by the buyer to the seller in the event that the m&A transaction falls through due to failure to obtain approval from the CFiUS).

8 lifecycle of A Claim

Bankers’ Blanket Bond / Crime (BBB/Crime)

Coverage

BBB/Crime policies provide cover for the direct financial loss an organisation suffers as a result of employee or third party theft and fraud.

these policies typically provide broad cover in respect of a range of fidelity losses; but the primary cover is for the dishonest or fraudulent acts of the insured’s employee.

Coverage is also provided on a specified basis for external criminal acts, including forgery or fraudulent alteration of securities or other financial instruments, and fraudulent manipulation of data, computer programmes, and instructions (including the introduction of malware). BBB/Crime policies also protect companies against the physical loss of, damage to, or disappearance of, securities or other valuable financial instruments or property which the insured owns, or for which it is legally liable.

Who should buy BBB/Crime?

BBB/Crime policies are made specifically for financial institutions, and are a critical risk transfer pillar for those organisations which are most susceptible to direct financial loss.

For other organisations, similar cover can be achieved through robust commercial crime policies.

What best-in-class cover looks like

interpol has named “social engineering fraud” as one of the world’s key emerging fraud trends, reflecting Aon’s experience in claims in 2016 and 2017.

in a typical attack, a malicious third party poses as a commercial supplier, either by infiltrating that party’s systems and sending emails from a legitimate account, or creating a fake, but similar email address. New account details are provided for payment, and the victim only realises a loss has been suffered when the legitimate vendor enquires as to their unpaid bills.

Coverage for these losses varies, subject to the precise circumstances of the loss and the wording of the policies. We recommend that companies seek affirmative cover for this loss, usually by extension, ensuring that the terms and sub-limits applied do not unduly restrain the cover.

Aon Risk Solutions 9

Part

2Pre-lossChallenges

10 lifecycle of A Claim

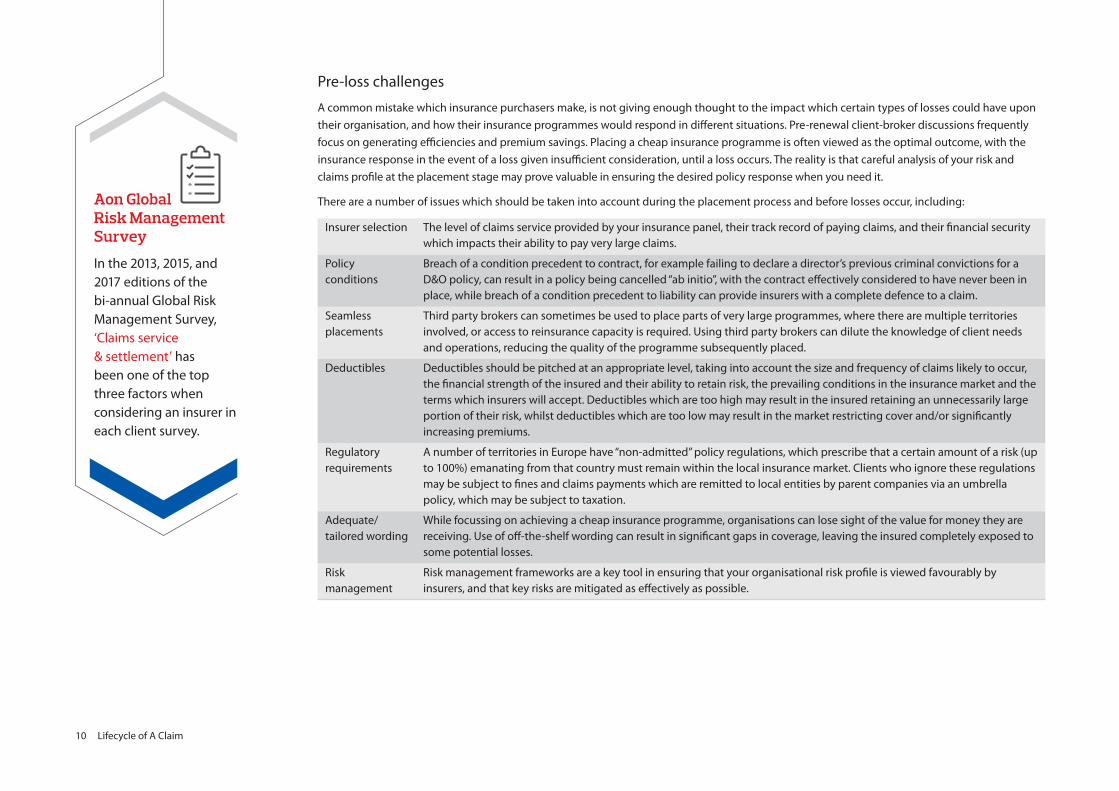

Pre-loss challenges

A common mistake which insurance purchasers make, is not giving enough thought to the impact which certain types of losses could have upon their organisation, and how their insurance programmes would respond in different situations. Pre-renewal client-broker discussions frequently focus on generating efficiencies and premium savings. Placing a cheap insurance programme is often viewed as the optimal outcome, with the insurance response in the event of a loss given insufficient consideration, until a loss occurs. the reality is that careful analysis of your risk and claims profile at the placement stage may prove valuable in ensuring the desired policy response when you need it.

there are a number of issues which should be taken into account during the placement process and before losses occur, including:

insurer selection the level of claims service provided by your insurance panel, their track record of paying claims, and their financial security which impacts their ability to pay very large claims.

Policy conditions

Breach of a condition precedent to contract, for example failing to declare a director’s previous criminal convictions for a D&O policy, can result in a policy being cancelled “ab initio”, with the contract effectively considered to have never been in place, while breach of a condition precedent to liability can provide insurers with a complete defence to a claim.

Seamless placements

third party brokers can sometimes be used to place parts of very large programmes, where there are multiple territories involved, or access to reinsurance capacity is required. Using third party brokers can dilute the knowledge of client needs and operations, reducing the quality of the programme subsequently placed.

Deductibles Deductibles should be pitched at an appropriate level, taking into account the size and frequency of claims likely to occur, the financial strength of the insured and their ability to retain risk, the prevailing conditions in the insurance market and the terms which insurers will accept. Deductibles which are too high may result in the insured retaining an unnecessarily large portion of their risk, whilst deductibles which are too low may result in the market restricting cover and/or significantly increasing premiums.

Regulatory requirements

A number of territories in europe have “non-admitted” policy regulations, which prescribe that a certain amount of a risk (up to 100%) emanating from that country must remain within the local insurance market. Clients who ignore these regulations may be subject to fines and claims payments which are remitted to local entities by parent companies via an umbrella policy, which may be subject to taxation.

Adequate/ tailored wording

While focussing on achieving a cheap insurance programme, organisations can lose sight of the value for money they are receiving. Use of off-the-shelf wording can result in significant gaps in coverage, leaving the insured completely exposed to some potential losses.

Risk management

Risk management frameworks are a key tool in ensuring that your organisational risk profile is viewed favourably by insurers, and that key risks are mitigated as effectively as possible.

aon Global Risk management Survey

in the 2013, 2015, and 2017 editions of the bi-annual global Risk management Survey, ‘Claims service & settlement’ has been one of the top three factors when considering an insurer in each client survey.

Aon Risk Solutions 11

What to expect from your broker

in the event that you experience one of the common challenges outlined earlier in this section, you may need your broker to assist:

Claims issue Appropriate approach/solutions

insurer selection

Your broker should select an insurer or panel of insurers who are able to - and have - a track record of paying claims quickly and fairly, and avoid:

• Insurers who may not have the financial strength to pay large claims

• Insurers who are known to attempt to find reasons why a claim should not be paid, often instructing lawyers

• Poor claims leaders not respected in the market who will cause delays in settlement, and increase the level of involvement required by following markets and claims agreement parties. this can be avoided by pre-agreeing with recognised and seasoned claims leaders who have a strong track record in the market.

Your broker’s market knowledge and analysis of insurers’ willingness to pay will help you to establish the right claims framework and select the appropriate claims leader for your organisation.

Policy conditions

Your broker should explain any conditions which are precedent in your policy to you, and negotiate favourable terms, so you are not exposed to the position of accidently breaching your policy’s conditions. if conditions precedent cannot be avoided altogether, they should be clearly worded, reasonable, and relevant. evidencing compliance with them should be easily achievable. Non-compliance could mean that claims are not paid or that the entire policy is voided. A policy which includes a long list of conditions is not to be encouraged.

Seamless placement

the payment of claims may be put at risk when a third party wholesale broker is used to access international markets by a retail broker, rather than one broking house being used through the chain of placement. Your broker should maintain the same standards of compliance and service protocols throughout the placement.

Deductibles Your broker may assist you to decide on the appropriate level of your deductible. this can be determined by comparing the financial impact on your organisation of the losses which you have previously suffered at various deductible levels. the deductible level will then also be affected by your broker’s ability to broke your risk to the market and what the insurance market is willing to accept, based upon the prevailing conditions and their assessment of your risk.

Regulatory requirements

Your broker should be well versed in the local regulations of the countries you operate in. Using a global broker with owned offices in these territories, rather than going through third parties, ensures the optimal outcome for clients. Policy management it systems can also be used to manage local policies and the renewal process, and update you on regulatory and legislative updates which affect your business and insurance programme.

Adequate/tailored wordings

As a key facet of their service to you, your broker must develop a deep understanding of your risk, business strategy, and risk financing goals. Policies must then be tailored to your organisation to provide coverage which is fit for purpose, provides the protection you need, and responds as expected.

Reporting requirements

Reporting requirements should be clearly explained to you by your broker at inception, and assistance should be provided in preparing and submitting a claim. Reporting requirements are often technical and require careful consideration. in the event of a loss, some policies will have reporting requirements around the period of time in which and the manner of how a claim must be submitted in order to be valid. generally, policies may state that claims should be reported “as soon as practicable”, “immediately” or “as soon possible.” there may be a question as to who must have the knowledge of the claim within your organisation. For claims made policies, reporting must be made within the policy period, or any applicable extended reporting period.

Risk management

Your broker should advise you on how to embed risk management best practice across your organisation, explain how this can have a positive impact on your risk, and drive optimal total Cost of insurable Risk outcomes.

What is covered?

it’s important that you understand the coverages available prior to any losses occurring in your business. Your broker can provide advice and guidance on cover, as well as coordinating pre-loss workshops, to include your lead insurer, where the Policy can be tested. examples of different incidents can be discussed and your broker and insurer can guide you through what aspects would be indemnified, ensuring you understand the full extent of coverage available.

12 lifecycle of A Claim

Part

3when aClaim oCCurs

Aon Risk Solutions 13

When a claim occurs

When a loss occurs, you should reasonably expect your claim to be handled in a transparent, accurate, and timely manner. however, there are a number of challenges which could significantly impact your balance sheet, cash flow, and reputation. examples of hurdles in claims payment include:

Complex claims can give rise to coverage issues where policy language may be subject to differing views on construction and application. this can lead to delays, especially if the insurer seeks external legal advice.

Without a clear process or claims procedure and a clear line of communication, actions which should be expedited can drag on unnecessarily.

You must always obtain consent from the insurer before you instruct your defence counsel, and must provide details of the firm‘s competence and charging rates.

Sometimes insurers may rely on a general reservation of rights for up to 12 months, leading to uncertainty and significant delays in claims settlements, although insurers in the UK should be mindful of the reforms allowing damages for the late payment of claims following the enterprise Act 2016.

these are time consuming and will often involve exposure to specialised areas of practice and jurisdiction for example, US Class Actions.

Without proper management of the various moving parts of a claim and active project management, final settlement of a claim can be delayed unnecessarily.

Coverage response

Clarity of claims

procedure

appointment of defence

counsel

reservation of rights

Complex & contentious

claims

expediting prompt

settlement

14 lifecycle of A Claim

in the event that you experience one of the common challenges outlined earlier in this section, you may need your broker to assist:

Claims issue Appropriate approach / solutions

Uncertainty of coverage

Your broker’s claims advocates may need to be engaged to review the insurance policy wording at the placement stage to ensure that it reflects your needs. this should create seamless cover, ensuring gaps and overlaps are removed.

Clarity of claims procedure

Your broker should create a tailored claims procedure to meet your individual needs. Joint discussions should lead to an agreed claims handling process, along with contact details. this procedure document should then be distributed to all parties involved in the process.

Claims handling procedure

Your broker should hold discussions with the insurer’s claims leaders and any experts involved, ensuring that they deliver the service standards expected.

Complex and controversial claims

the ability to resolve complex and controversial claims without damaging relationships is key. Your broker must be able to achieve an optimal outcome once a claim is made, whilst ensuring that you are not penalised at your next renewal. this depends on their skill, relationships, and leverage.

Claims tracking and recording

Claims tracking and recording is essential in the overall management and handling of any claim. information should be kept up-to-date, reports from external experts should be issued in a timely manner, and most importantly, claim collections should be pursued with the utmost urgency.

expediting prompt settlement

Your broker should hold regular claims review meetings with you, ensuring open claims are regularly reviewed, resulting in action plans with set deadlines for achieving targets.

Aon undertakes a twice yearly internal claims survey, which is completed globally by all

1,200 claims colleagues to gauge their perception of insurer performance.

What to expect from your broker

When a claim occurs, your broker must consider:

All relevant policies which may respond, particularly if more than one policy may be triggered

the applicable policy period

the applicable deductible

Whether a claim has been made or whether circumstances have arisen which may give rise to a claim

When the claim was first made

the reporting conditions under the applicable policy(ies)

the claims handling procedure and contacts between the insurer, broker, and client

Any technical elements of the claim, for example interrelated wrongful acts or any aggregation issues

Any applicable policy exclusions

Aon Risk Solutions 15

if cover is accepted, the broker will continue to monitor as claim progresses, ensuring updates are relayed and any indemnity

payments are processed quickly

ORDiNARY

if cover, in whole or part is not agreed and this is not accepted by broker and client,

broker will contend insurers position, putting forward reasons as to why cover should be afforded. Broker to engage its

escalation and governance procedures if an agreement cannot be reached by the claims

advocate.

Broker will chase insurer regularly to ensure

delivered in a timely manner

Your broker can advise as to whether the matter

should be notified as a claim or circumstance

Broker liaises with client as to whether insurer’s comments are agreed

Broker assembles necessary claims documentation and requests any further

information from client, where appropriate. Broker to comment on coverage and any

clauses that may be applicable

Broker receives notice of a claim from the client

Notice of claim is drafted by broker and sent to primary and excess insurers

insurer provides acknowledgement of notification

insurer sends substantive coverage position or any requests for information so they can

provide coverage position

Broker forwards coverage position to client and provides comment around the same

the claims process

Complex claims may require your broker to meticulously project manage the entire claims process, taking into account your concerns and expectations, as well as being aware of any risk management issues and initiatives you are undertaking. Planning, execution, and tracking outcomes are pivotal to delivering the right support to you. here, we outline what a typical broker’s claims handling procedure would look like:

16 lifecycle of A Claim

Part

4Post-claim:learning lessons

Aon Risk Solutions 17

What to expect from your broker

Following a large or complex claim, particularly if specific challenges are encountered, it is vital that lessons are learnt and changes are implemented. As part of this process, your broker should arrange routine reviews of your insurance panel’s claims performance, capabilities, and procedures, including an evaluation of your satisfaction. information feedback sessions and annual surveys are important and provide you, the client, with an opportunity to provide your input on performance. Review meetings should be established to discern lessons learnt, as well as to review the policy wording. Furthermore, claims reports and analysis can help to pave the way for future improvements. Your broker can assist you to this end in the following ways:

risk management

review

review of any challenges

thrown up by current

wording

Post loss, if policy language or restrictions to coverage imposed by the existing wording have resulted in unsatisfactory claims outcomes or the delay in achieving a satisfactory outcome, your broker should work with you to improve the existing wording at next renewal, to secure positive future outcomes.

Following any loss, it is essential to undertake a review to understand if steps can be taken to avoid similar claims. the results of this review and go-forward steps should then be communicated to internal stakeholders and highlighted to insurers at your next renewal.

Your broker should work with you to examine the adequacy of your existing limits and appropriateness of your existing deductibles. Since last renewal, your risk profile may have changed, or large or unforeseen losses may have raised issues which were not previously accounted for and must be carried through into next renewal.

the performance of your incumbent insurance panel should be periodically reviewed by your broker to highlight any shortcomings or consistent underperformance by certain insurer(s). insurer performance on your risk can also be benchmarked by your broker against their experience across similar accounts which they service to give a broader view of performance trends. Underperformance by any particular insurer should then be addressed at renewal, with alternative capacity sought if required.

review of limits and

deductibles

review insurer

performance

Post-claimreview activity

aPProPriateaPProach

18 lifecycle of A Claim

Part

5

theaon advantage

Aon Risk Solutions 19

A bespoke solution with you in mind

We understand the critical importance in providing a claims service that does not duplicate, but one that compliments and enhances. Aon’s proposition sits both pre- and post-loss, enabling optimal claims planning processes and focussing on risk mitigation, if and when, claims occur. these services interlink in order to provide synergy and overall claims efficiency and are delivered in a two pronged approach:

inside out: We will author a plan to define how we will work together during the year and outline our commitments to you. We will develop an understanding of your business, including the organisational structure and risks. We will work in partnership with you and the carrier to identify the best way of working amongst all parties and the right people to get involved when a claim arises. Based on our evaluation, we will define and implement claims handling procedures and protocols bespoke to your business.

Outside in: We work for you, advising in improvements to policy language and drafting and negotiating bespoke wordings to ensure that the terms are legally and operationally sound. this requires an in-depth understanding of your business, an appreciation of the specific exposures faced and, in addition, the wider legal and industry-specific liabilities. Wordings are developed in conjunction with learned experience from yourselves and your peers and in the knowledge of what the market will bear. We work closely with Account executives in the design of insurance programmes, ensuring consistency of wordings and avoiding any gaps in coverage across the various lines of business.

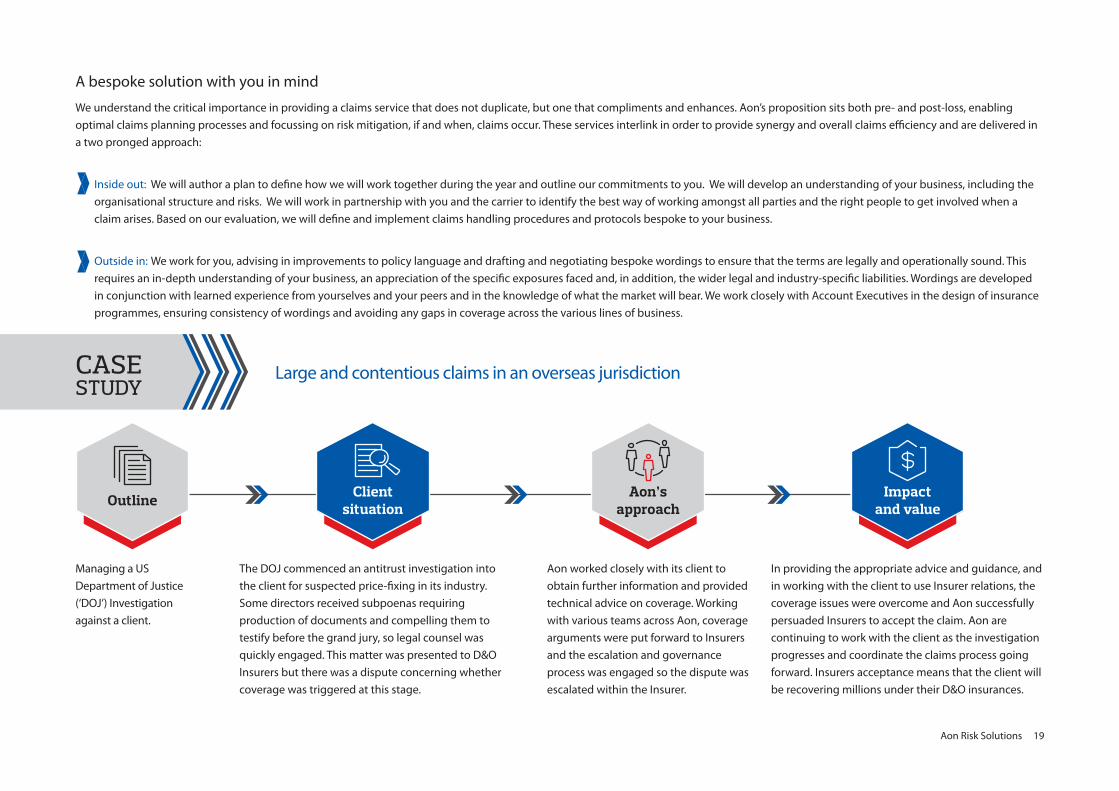

large and contentious claims in an overseas jurisdictionCasestudy

impact and value

in providing the appropriate advice and guidance, and in working with the client to use insurer relations, the coverage issues were overcome and Aon successfully persuaded insurers to accept the claim. Aon are continuing to work with the client as the investigation progresses and coordinate the claims process going forward. insurers acceptance means that the client will be recovering millions under their D&O insurances.

aon’s approach

Aon worked closely with its client to obtain further information and provided technical advice on coverage. Working with various teams across Aon, coverage arguments were put forward to insurers and the escalation and governance process was engaged so the dispute was escalated within the insurer.

Client situation

the DOJ commenced an antitrust investigation into the client for suspected price-fixing in its industry. Some directors received subpoenas requiring production of documents and compelling them to testify before the grand jury, so legal counsel was quickly engaged. this matter was presented to D&O insurers but there was a dispute concerning whether coverage was triggered at this stage.

outline

managing a US Department of Justice (‘DOJ’) investigation against a client.

20 lifecycle of A Claim

Structured support at every stage of the process

good broking processes lead to positive claims outcomes, which in turn lead to positive future broking outcomes. therefore, our involvement starts with the negotiation phase of a policy, even before its inception. We work collaboratively with you, the Aon network, the placement team, and insurers to bring you bespoke solutions and products, as well as expanding on traditional post-loss activities.

stages of the Claims

ProCessadvisory services

reporting & analytics

Claims managementPrior to loss

tailor the claims proposition to meet your needs

Provide insight on insurer willingness to pay claims

Develop a claims handling procedure bespoke to meet your business needs

Recommend claims experts to enable early response

insurer relationship management

Review legacy claims and recommend actions

in-house expertise to provide specialist advice and support

effective and strategic preparation and presentation of the claim to insurers

legally qualified liability claims team

Review all coverages available and identify any possible defences and possible solutions

Support throughout the journey of the claim from notification to settlement

establish a claims strategy and provide guidance and strategic input in all claim phases

Open dialogue with insurance managers, offering guidance at each step

Proactive representation of your interests with insurers to maximise policy response and benefits

Drive confirmation of coverage and prompt settlement

trending and risk management reporting

Bespoke claims benchmarking on industry or product-related claims trends

loss scenario modelling

in-house training

Claim review and audit programmes to ensure insurer performance and efficient closure

Aon Risk Solutions 21

leading technical expertise, resources, and leveragein the UK, our 30 claims experts deal with more than 3,000 new financial and professional lines claims a year leading to over £27 million collected on behalf of our clients.

At a local, regional and global level, Aon’s claim personnel have extensive experience of handling financial lines claims. Our local claims experts are well versed in the nuances of doing business in their home country and are experts in local law, regulation and insurance practices. they are supported at a regional level by a team of legally trained specialists with a background in handling particularly large, complex and contentious claims. At a global level, we are able to draw upon the niche product and sector expertise of our 1,200 strong claims team in order to ensure optimal claims settlements for our clients.

the combined technical knowledge boasted by our team is not only leveraged to resolve complex and demanding claims but also to advise on coverage issues and negotiate bespoke policy wordings with insurers at placement.

We understand the issues that need to be addressed and the benefits of claim resolutions; approaching claims management methodically to reduce unnecessary delays. A key component of our role is to act as the strategic driving force of claims resolution, avoiding and overcoming delay from insurers and counsel.

As we regularly interact with key industry members, we are able to leverage our good working relationships with insurers and legal counsel to resolve issues and avoid bottlenecks that may beset claims.

globally,

our 1,200 claims experts deal with more than

8,500 new claims a year.

large and contentious claims in an overseas jurisdictionCasestudy

impact and value

Following this claim, Aon performed a review of all the client’s policy wordings to ensure that the scope of cover was suitable in these types of scenarios. this post-loss consultancy resulted in the client implementing a number of operational changes to ensure a smoother claims process going forward and an effective insurance programme.

aon’s approach

Aon facilitated meetings and dialogue directly with insurers in order to reduce legal communications between the lawyers. this defused an already fractured claim, and culminated in successfully negotiating a seven figure settlement for the client.

Client situation

Our client acquired a firm which had an ongoing cyber data breach claim. With limited resources, they turned to Aon for key Claims Advocacy services. the insurer had raised a lot of coverage questions with regards to prior handling and the client had also engaged its own counsel to defend the claim, prior to consultation with insurers.

outline

global UK-based client, occupying key space in cyber, technology and government defence contract works, faced a data breach. An investigation was commenced by the UK industry body.

22 lifecycle of A Claim

Who caN heLp?For more information about how Aon can support you across the lifecycle of a claim, please contact:

Claire is an experienced lawyer specialising in drafting and advising on insurance wordings and coverage issues, with a particular emphasis on financial institution clients. She assists clients with complex claims, particularly where there is a coverage dispute involving D&O, Pi, gPl, Fidelity and BBB policies. Prior to joining Aon, Claire was a Senior Associate in the insurance team at Debevoise & Plimpton llP and a major loss Adjuster in the Financial lines Claims department at Aig. She is also an admitted attorney in the State of New York.

Claire Sales - Coverage Counsel | [email protected] | 020 7086 4176

Karen is a highly experienced lawyer with many years’ experience of acting on complex, high value insurance and reinsurance claims often with a multi-jurisdictional element. Karen has particular expertise in the areas of Pi, D&O and ePli claims. Prior to joining Aon, Karen was a partner in the global Professional & Financial lines team at DAC Beachcroft llP.

Karen Cargill - Coverage Counsel | [email protected] | 020 7086 6038

Angus has over 23 years in the insurance industry. the majority of this has been working at specialty insurers. Angus joined Aon in February 2017 as head of F&PS Claims in the global Broking Centre and then, in may 2017, he became head of Claims. he has a proven track record in senior claims management and operational roles having managed functional teams, processes and systems across the UK, USA, europe, Australia, Asia and South Africa. Angus has extensive experience in managing claims strategies for large complex losses and volume claims functions for all major classes of business.

Angus Watson - Head of Claims | [email protected] | 020 7086 0203

Sam has over 7 years of experience in handling insurance claims (initially working within a law firm before joining a specialised insurer for 3 years prior to joining Aon). Sam joined Aon’s Claims Advocacy team, specialising in Financial and Professional Services, in march 2015. She is responsible for the active management of claims from a wide portfolio of clients, primarily handling complex D&O, FiPi, ePl, Crime and Ptl claims. this entails providing advice on policy coverage, negotiating settlement and delivering both pre and post loss consultancy services, ensuring that clients maximise coverage under their insurances.

Samantha Ellis - Senior Claims Advocate | [email protected] | 020 7086 4113

Future proofing your organisation

there are a number of trends that will continue to impact the claims environment in europe in the coming years, but the two most significant are the continued regulatory pressure in the region, and the increasingly litigious landscape. the increased regulatory scrutiny is changing the liability landscape, as governments globally further clamp down on bribery, corruption, and market conduct abuses. Penalties for offenders are increasing and enforcement is noticeably more active around trading errors and breaches of sanctions. Shareholder activism across europe has increased. While there is no direct comparison to US class actions, various jurisdictions across europe have similar mechanisms in place to allow for group representative actions (including group litigation Orders in the UK, “group actions” in France and two collective redress mechanisms in holland for class actions by shareholders). moreover, changes in the way that litigation may be funded is likely to have a tangible effect on litigation patterns, with an increase in after the event insurance and the targeting of europe by third party litigation funders.

As these dynamics play out across europe, Aon continues to invest in leading claims resources and technology in key strategic locations across the region, to support you in future proofing your organisation. As the frequency of claims increases, the severity of losses rise and the nature of claims become more complex; it will become ever more important to partner with a leading broker in this area.

About Aon Aon plc (NYSe:AON) is a leading global professional services firm providing a broad range of risk, retirement and health solutions. Our 50,000 colleagues in 120 countries empower results for clients by using proprietary data and analytics to deliver insights that reduce volatility and improve performance.

For further information on our capabilities and to learn how we empower results for clients, please visit http://aon.mediaroom.com.

© Aon plc 2017. All rights reserved.the information contained herein and the statements expressed are of a general nature and are not intended to address the circumstances of any particular individual or entity. Although we endeavor to provide accurate and timely information and use sources we consider reliable, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation.

www.aon.com