insurance erm sweepstakes: who’s winning: risk management or the risks? neil t. strausssoa erm...

TRANSCRIPT

INSURANCE ERM SWEEPSTAKES: WHO’S WINNING:RISK MANAGEMENT OR THE RISKS?

NEIL T. STRAUSS SOA ERM APRIL 20 2012

2

It’s Been Quite Risky Recently

Eurozone

U.S. Budget Stand-off

Equity Market Volatility

Interest Rates to Unprecedented Low Rates

Financial Crisis Recovery ? / Bumpiness

Regulatory Debate related to Financial Companies

MF Global

… And much, much more

3

Life Insurance Sector: The Good, The Bad, The Mixed?

The Good – Investments – Bond and Mortgage Risk Management

The Bad – Interest Rate Risk Management

The Mixed – Product Risk: Variable Annuities

4

The Good: Investment Risk – Risk Management Wins!

5

Investment Losses Normalizing; 2011: Down, but Above-Avg

ACLI CML Delinquency Rate

CML Losses* : Moody’s Universe

Bond / Pfd Stock Credit Losses* : Moody’s Universe

*Data source: Highline Data

RMBS, CMBS remain elevated

CML: ~ 60bp remaining next couple yrs

Bonds/Pfd stock: ~ 25-40 bp annualized

Peripheral Eurozone sov/bank exposure minimal

2011 Credit Loss Expectations

2Q11:

12 bp

6

The Bad: Interest Rate Risk – Risk Management Loses!

7

Interest Rates: Risk from Flat/Down or Spike Up

Flat/Down:

Next 3-5 years: modest, growing earnings drag

Longer-term: material earnings/capital impact

At risk: long-tail liabilities and unhedged VA “rho”

Risk management: do nothing, limited hedges, or wait for a higher-rate entry point

Spike Up:

Disintermediation risk

Fixed income investments underwater

Significant block written at low rates

Risk management: caps and market value adjustment feature

Best scenario for industry: gradually rising interest rates – likely?

8

Interest Rates: Risk from Flat/Down

Few insurers have bought protection against lower interest rates, either because of the high cost of doing so or because they deem the risk to be remote (editor’s addition: Risk management using the old technique of ‘crossing one’s fingers’ Humans will be humans – the biggest risk of all). Exceptions are the minority of companies that have bought interest rate floors, insurers with interest rate hedging programs for variable annuity lifetime income guarantees, and companies that have locked in interest rates on the investment of future premiums for products such as no-lapse universal life and long-term care.

Moody’s Investors Service, August 19, 2011 (excluding insert)

9

The Mixed: Product Risk (Tie: Risk/Risk Management)

10

Life Insurer Product Risk: Variable Annuity (VA)?

What is a variable annuity?

Insurance product allowing customer to invest deposits in a range of investment options

Insurer agrees to make future periodic payments to the customer

Includes a death benefit

Funds accumulate tax-deferred

Investment Risk is the policyholder’s, not the insurance companies

… that is until the Advent of guaranteed living benefits

Insurance company takes investment risk in certain scenarios

10

11

Variable Annuity Risk Management Evolution

First RM for VA’s - “Head in the sand” – i.e., no risk management

Actuarial analysis – 1999 - 2000 Borrowed techniques used for more traditional products

Goals – simplicity; limiting reserves required

Hampered by lack of robust technology

Could not get actuaries and investment people in the same room – “you just don’t understand”

Stochastic modeling – beginning mid-2000’s

Availability of computer power

Development of modeling techniques

Regulatory pressure

VA Guarantee Arms Race repeated itself: 2002/3 and then 2008/9\

Conclusion – it takes > a near-death experience to change – need a death experience!

Even in 2011, the risk/growth equation hard to navigate – current market

11

12

VA’s Add Earnings/Capital Volatility Hedging-related issues

Competing hedge goals: economics, GAAP and Stat

Limited rho hedging

Liquidity risk from collateral posting

Earnings and capital volatility from VA book

Captive reinsurance masks capital shortfalls

Includes 28 rated companies; operating income = net income – net realized cap gains

ex derivatives

GAAP Income Volatility

13

Some Key VA Issues

How de-risked are the new products? Tail risk improving

More equity and interest rate risk passed back to customers Low vol funds, automatic equity reallocation, interest rate-dependent withdrawal rates, etc.

Which companies’ VA business have better credit profiles? Sound product design

Comprehensive (including static) hedging of economics

Transparency

How does Moody’s evaluate VA risk? Examine capital post-stress event (30% drop in equities)

Compare results with Moody’s view of required capital

Incorporate transfer of risk and capital to reinsurance captive

Review greeks hedged versus exposure (including f/x, interest rate, etc.)

14

Assessing Risk Management

It starts with assessing risk tolerance

It only then moves onto analyzing risk management

Board of Directors – oversight

Executive Management – top down management of risks

Business Line Management – bottom up management of risks

What is the right breakdown?

15

Shampoo: The endless loop of rinse, repeat

Risk identification

Risk measurement

Risk Mitigation

Risk Prioritization

Risk Monitor – Repeat

16

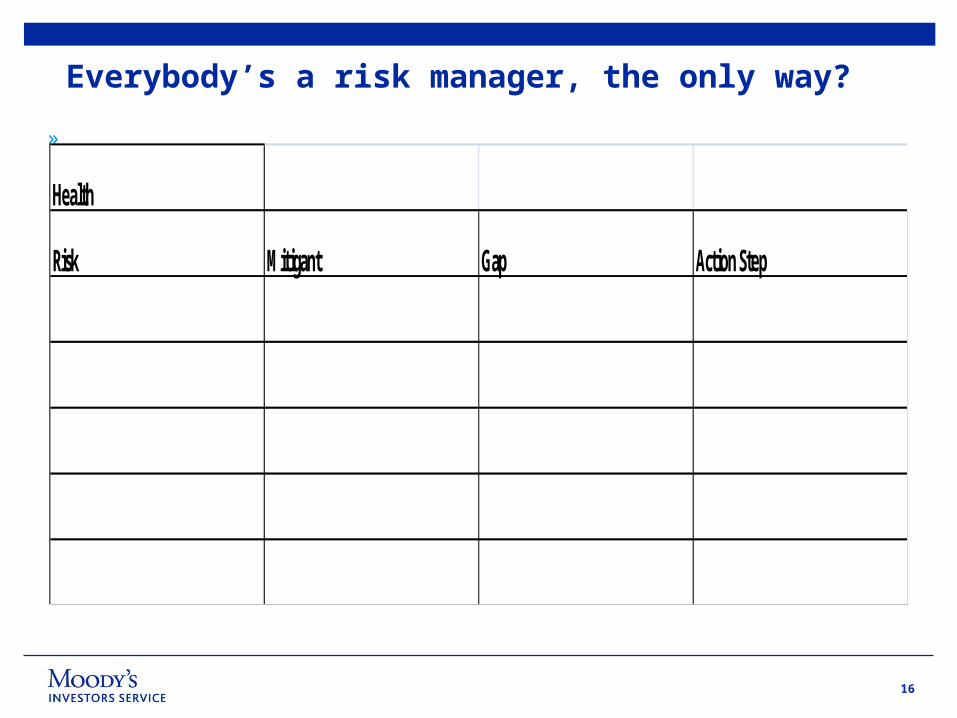

Everybody’s a risk manager, the only way?

»

Health

Risk Mitigant Gap Action Step

17

Risk Management Quotable Quotes

“What’s a Chief Risk Officer?”

Heard at one of the first financial companies to implode in 2008, 3 months prior

“Everybody’s sub-optimizing in the enterprise for their business/function except for the CEO, CFO and CRO who are optimizing for the whole”

Heard from one of the first CROs in the insurance industry (paraphrased)

“If money isn’t loosened up, this sucker could go down”

George Bush, October 2008

18

Risk Management Quotable Quotes

Is this ERM enough for the financial sector?: Can regulation/government

ever catch up to the private sector: Imagine the police without the ability to

speed or carry weapons?

Anonymous

“There are known knowns. These are things we know that we know.

There are known unknowns. That is to say, there are things that we

know we don't know. But there are also unknown unknowns. There are

things we don't know we don't know.”

Donald Rumsfeld

19

Background – Neil Strauss

Vice President - Senior Credit Officer in Financial Institutions Group of Moody’s Investors Service – responsible for a portfolio of U.S. ratings within the Life Insurance Group.

Prior, worked for about 30 years in a variety of roles both in the insurance industry and as a senior credit rating agency insurance and reinsurance sector analyst.

Held actuarial, risk management, and credit roles at New York Life, AXA-Equitable and AIG, respectively. Consulted for Promontory Financial Group and Neil T. Strauss Associates, LLC. on insurance, risk management and rating agency related engagements.

Adjunct professor in the Graduate Division of New York University’s School of Professional and Continuing Studies. Currently teaches a course that he developed on Enterprise Risk Management for the Insurance Sector, both online and onsite.

A graduate of Johns Hopkins University.

Professional designations as an actuary and as a chartered enterprise risk analyst, both from the Society of Actuaries.

20

© 2011 Moody’s Investors Service, Inc. and/or its licensors and affiliates (collectively, “MOODY’S”). All rights reserved.

CREDIT RATINGS ARE MOODY'S INVESTORS SERVICE, INC.'S (“MIS”) CURRENT OPINIONS OF THE RELATIVE FUTURE CREDIT RISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES. MIS DEFINES CREDIT RISK AS THE RISK THAT AN ENTITY MAY NOT MEET ITS CONTRACTUAL, FINANCIAL OBLIGATIONS AS THEY COME DUE AND ANY ESTIMATED FINANCIAL LOSS IN THE EVENT OF DEFAULT. CREDIT RATINGS DO NOT ADDRESS ANY OTHER RISK, INCLUDING BUT NOT LIMITED TO: LIQUIDITY RISK, MARKET VALUE RISK, OR PRICE VOLATILITY. CREDIT RATINGS ARE NOT STATEMENTS OF CURRENT OR HISTORICAL FACT. CREDIT RATINGS DO NOT CONSTITUTE INVESTMENT OR FINANCIAL ADVICE, AND CREDIT RATINGS ARE NOT RECOMMENDATIONS TO PURCHASE, SELL, OR HOLD PARTICULAR SECURITIES. CREDIT RATINGS DO NOT COMMENT ON THE SUITABILITY OF AN INVESTMENT FOR ANY PARTICULAR INVESTOR. MIS ISSUES ITS CREDIT RATINGS WITH THE EXPECTATION AND UNDERSTANDING THAT EACH INVESTOR WILL MAKE ITS OWN STUDY AND EVALUATION OF EACH SECURITY THAT IS UNDER CONSIDERATION FOR PURCHASE, HOLDING, OR SALE.

ALL INFORMATION CONTAINED HEREIN IS PROTECTED BY LAW, INCLUDING BUT NOT LIMITED TO, COPYRIGHT LAW, AND NONE OF SUCH INFORMATION MAY BE COPIED OR OTHERWISE REPRODUCED, REPACKAGED, FURTHER TRANSMITTED, TRANSFERRED, DISSEMINATED, REDISTRIBUTED OR RESOLD, OR STORED FOR SUBSEQUENT USE FOR ANY SUCH PURPOSE, IN WHOLE OR IN PART, IN ANY FORM OR MANNER OR BY ANY MEANS WHATSOEVER, BY ANY PERSON WITHOUT MOODY’S PRIOR WRITTEN CONSENT. All information contained herein is obtained by MOODY’S from sources believed by it to be accurate and reliable. Because of the possibility of human or mechanical error as well as other factors, however, all information contained herein is provided “AS IS” without warranty of any kind. Except as expressly stated otherwise, MOODY’S has not verified, audited or validated independently any information received in the rating process, nor will it do so. Under no circumstances shall MOODY’S have any liability to any person or entity for (a) any loss or damage in whole or in part caused by, resulting from, or relating to, any error (negligent or otherwise) or other circumstance or contingency within or outside the control of MOODY’S or any of its directors, officers, employees or agents in connection with the procurement, collection, compilation, analysis, interpretation, communication, publication or delivery of any such information, or (b) any direct, indirect, special, consequential, compensatory or incidental damages whatsoever (including without limitation, lost profits), even if MOODY’S is advised in advance of the possibility of such damages, resulting from the use of or inability to use, any such information. The ratings, financial reporting analysis, projections, and other observations, if any, constituting part of the information contained herein are, and must be construed solely as, statements of opinion and not statements of fact or recommendations to purchase, sell or hold any securities. Each user of the information contained herein must make its own study and evaluation of each security it may consider purchasing, holding or selling. NO WARRANTY, EXPRESS OR IMPLIED, AS TO THE ACCURACY, TIMELINESS, COMPLETENESS, MERCHANTABILITY OR FITNESS FOR ANY PARTICULAR PURPOSE OF ANY SUCH RATING OR OTHER OPINION OR INFORMATION IS GIVEN OR MADE BY MOODY’S IN ANY FORM OR MANNER WHATSOEVER.

MIS, a wholly-owned credit rating agency subsidiary of Moody’s Corporation (“MCO”), hereby discloses that most issuers of debt securities (including corporate and municipal bonds, debentures, notes and commercial paper) and preferred stock rated by MIS have, prior to assignment of any rating, agreed to pay to MIS for appraisal and rating services rendered by it fees ranging from $1,500 to approximately $2,500,000. MCO and MIS also maintain policies and procedures to address the independence of MIS’s ratings and rating processes. Information regarding certain affiliations that may exist between directors of MCO and rated entities, and between entities who hold ratings from MIS and have also publicly reported to the SEC an ownership interest in MCO of more than 5%, is posted annually at www.moodys.com under the heading “Shareholder Relations — Corporate Governance — Director and Shareholder Affiliation Policy.”

Any publication into Australia of this document is by MOODY’S affiliate, Moody’s Investors Service Pty Limited ABN 61 003 399 657, which holds Australian Financial Services License no. 336969. This document is intended to be provided only to “wholesale clients” within the meaning of section 761G of the Corporations Act 2001. By continuing to access this document from within Australia, you represent to MOODY’S that you are, or are accessing the document as a representative of, a “wholesale client” and that neither you nor the entity you represent will directly or indirectly disseminate this document or its contents to “retail clients” within the meaning of section 761G of the Corporations Act 2001.