institutional structures of financial sector supervision, their drivers and historical benchmarks

TRANSCRIPT

Ia

Ma

b

a

ARRAA

KFIPBPO

1

utassoidtbt

v

eIig

U

(

1h

Journal of Financial Stability 9 (2013) 428– 444

Contents lists available at ScienceDirect

Journal of Financial Stability

journal homepage: www.elsevier.com/locate/jfstabil

nstitutional structures of financial sector supervision, their driversnd historical benchmarks�

artin Meleckya,b,∗, Anca Maria Podpieraa,b

World Bank, G-5-141, 1818 H Street, NW 20433, United StatesTechnical University of Ostrava, Sokolska 33, Ostrava, Czech Republic

r t i c l e i n f o

rticle history:eceived 10 August 2012eceived in revised form 23 January 2013ccepted 18 March 2013vailable online 26 March 2013

a b s t r a c t

This paper studies institutional structures of prudential and business conduct supervision of financialservices in 98 high and middle income countries over the past decade. It identifies possible drivers ofchanges in these supervisory structures using the panel ordered probit analysis. The results show that (i)more developed, small open economies with better public governance tend to integrate their supervision,especially the prudential one; (ii) more financially developed countries integrate more their supervision;however, greater development of the non-bank financial system leads to less integrated prudential super-

eywords:inancial servicesntegrated supervisionrudential supervisionusiness conduct supervisionanel data analysis

vision but not business conduct supervision; (iii) the lobbying power of concentrated and highly profitablebanking sectors significant hinders business conduct integration; (vi) countries that experienced finan-cial crises integrate their supervisory structure relatively more and (v) greater central bank independencecould cause less integration of prudential supervision, but not necessarily of business conduct supervision.

fieesttslmcgos

rdered probit

. Introduction

How the institutions for financial services supervision are setp and structured is important, because this can crucially affecthe quality of financial services supervision, financial stability andlso financial development. But do similar countries choose similarupervisory structures for financial services? Why do supervisorytructures differ so much across United States, Germany, Japan andther developed countries in their degree of integration, the prox-mity of microprudential and macroprudential supervision, and theevelopment of business conduct supervision? What models havehe developing countries chosen to follow and why? And, can someenchmark models be identified so that countries can implement

hem based on their financial system typology?Several factors can influence the choice of a particular super-isory structure for a given financial system. These could be the

� The findings, interpretations, and conclusions expressed in this paper arentirely those of the authors. They do not necessarily represent the views of thenternational Bank for Reconstruction and Development/World Bank and its affil-ated organizations, or those of the Executive Directors of the World Bank or theovernments they represent.∗ Corresponding author at: World Bank, G-5-141, 1818 H Street, NW 20433,nited States. Tel.: +1 2024731924.

E-mail addresses: [email protected], [email protected]. Melecky).

duePDuslfftt

572-3089/$ – see front matter © 2013 Elsevier B.V. All rights reserved.ttp://dx.doi.org/10.1016/j.jfs.2013.03.003

© 2013 Elsevier B.V. All rights reserved.

nancial system’s size, development or structure, as well as pres-nce of financial groups, strong industry lobby and other politicalconomy factors. But also more general variables can play role,uch as the overall quality and governance of public institutions, orhe experience of past financial crises. The importance of each fac-or varies across countries. Developing countries observe diverseupervisory structures in advanced economies and could find chal-enging selecting the role model to follow. The global financial crisis

ade countries reform their supervisory structures and this pro-ess is to continue for some time. Preliminary evidence points toreater integration of prudential supervisory structures in smallpen economies, and growing importance of business conductupervision in overall supervisory efforts.

The literature discusses extensively the different models of pru-ential supervision, the arguments for and against supervisorynification, and the role of central bank in the supervision andventual unification (De Luna-Martinez and Rose, 2003; Cihak andodpiera, 2006; Masciandaro and Quintyn, 2007; Di Giorgio andi Noia, 2007; Herring and Carmassi, 2008). The main reasons fornified supervision are related to changes in the financial industrytructure – the emergence of financial conglomerates and regu-atory challenges posed by this – and to the aim of supervisors

or a more effective and harmonized oversight. The argumentsor supervisory unification have been traditionally presented fromhe microprudential perspective. In addition, a better informa-ion flow and coordination among supervisors can also allow for a

l of Fin

belrpfm

pfi2tMMiaTebcwsoasm

vbcipasawm(ttpccBsbam

dot(aclbtrB

af

spsd

lswiclatcImtcbiciwlgps

ttoo5cc

2

2

(t9d(swfiv9obituF

M. Melecky, A.M. Podpiera / Journa

etter systemic risk monitoring and management, and thusnhance macroprudential supervision and financial stability. Theiterature is equally concerned with potential disadvantages andisks associated with the process of supervisory integration. A mainractical concern is the actual feasibility of unifying the objectivesor supervision of several different financial subsectors. A great

onopoly powers of the unified supervisor is another concern.Several studies attempt to establish a relationship between the

erformance of supervisors and their degree of unification acrossnancial sectors (Arnone and Gambini, 2006; Cihak and Podpiera,006). Other studies analyze the relevance of country characteris-ics for the type of the chosen supervision structure (Shen, 2006;

asciandaro, 2006, 2007, 2009; Masciandaro and Quintyn, 2008;asciandaro et al., 2008). Masciandaro et al. (2012) estimate the

mpact of changes in supervisory architectures (greater unification)nd in supervisory governance on resilience to economic crises.hey find that increased supervisory unification and improved gov-rnance are negatively correlated with economic resilience. To theest of our knowledge, all existing empirical studies are based onross-sectional data sets, and thus analyze the supervisory frame-orks at a certain point in time. In addition, most of the reviews of

upervisory regimes and related empirical studies focus primarilyn microprudential supervision. These studies pay only marginalttention to the proximity of microprudential and macroprudentialupervision, and to business conduct supervision and its comple-entary function to prudential supervision.This paper studies changes and cross-country variation in super-

isory structures for financial services, focusing on prudential andusiness conduct1 supervision as two separate aspects of finan-ial sector supervision. It identifies possible drivers of changesn the supervisory structures using an ordered probit model foranel data. We have collected a new dataset covering 98 highnd middle income countries over 1999–2010 that enables us totudy changes and differences in supervisory structures over times well as across countries. We are interested in investigatinghich factors made countries choose (i) integrated over frag-ented microprudential supervision across financial sub-sectors,

ii) placement of an integrated prudential supervisor within a cen-ral bank instead a stand-alone financial supervisory agency––andhus opt for higher proximity of microprudential and macro-rudential supervisors––(iii) integrated over fragmented businessonducts supervision, and (iv) single out the mandate for businessonduct supervision over adding it to the prudential supervisor.ased on the results of the analysis, the paper compares the existingupervisory structures of our sample countries with the predictedenchmark, and discusses the main outliers concerning prudentialnd business conduct supervisory structures vis-à-vis the bench-arks.The considered determinants of supervisory structures can be

ivided into four groups: (i) countries’ general and economic devel-pment indicators; (ii) political and governance indicators, such ashe quality of governance and the autonomy of the central bank;iii) financial sector development indicators, such as the depthnd complexity of the financial system, including banking sectorharacteristics such as concentration, efficiency, profitability, andiquidity, and (iv) the number of past financial crises experiencedy a country. In addition to the baseline ordered probit, we employ

he binomial probit and multinomial logit models, and the pooledegression analysis to test robustness of our baseline estimates.uilding on the identified significant determinants of changes in1 The business conduct supervision here includes financial consumer protectionnd market integrity supervision, and we will use this term as an integrating conceptor these slightly distinct areas throughout the paper.

g

l

an

ancial Stability 9 (2013) 428– 444 429

upervisory structures over time and across countries, the paperredicts country benchmark models. This forward-looking per-pective is enabled by the time-series dimension of our panelataset.

We find that, as countries develop and improve their pub-ic governance, they tend to integrate more their financial sectorupervisory structures. Greater independence of the central bank,hich is often involved in supervision of banks, could entail less

ntegrated prudential supervision, but not necessarily businessonduct supervision. In this regard, our results provide some qua-ifications to those obtained by Masciandaro (2006, 2007, 2009)nd Masciandaro et al. (2008). Further, small open economiesend to integrate prudential supervision, while greater opennessould coincide with less integrated business conduct supervision.ncreasing financial depth makes countries integrate supervision

ore. But strong development of the non-bank financial sec-ors, including capital markets and the insurance industry, makesountries opt for less integrated prudential supervision but not theusiness conduct supervision. Higher concentration of the bank-

ng sector, associated with higher monopolistic pricing powers,hronic inefficiencies and often stronger industry lobby, hindersntegration of business conduct supervision. Moreover, countries

ith banking sectors that have been more exposed to aggregateiquidity risk, because of greater external funding, tend to inte-rate more their prudential supervision. Finally, the experience ofast crises makes countries choose more integrated supervisorytructures.

The rest of the paper is organized as follows. Section 2 describeshe new panel data set and discusses the developments in pruden-ial and business conduct supervision in our sample of 98 countriesver the past decade. Section 3 describes the estimation methodol-gy. Section 4 presents and discusses the empirical results. Section

benchmarks the actual supervisory structures of our sampleounties to those predicted by our estimated model. Section 6 con-ludes and presents some policy implications.

. Panel data

.1. A new database of supervisory structures

To study the changes from sectoral (institutional) to integratedfunctional) supervisory structures, including the role of the cen-ral banks in supervision, we collected a new dataset covering8 countries over 1999–2010. Institutional supervision involvesifferent rules and supervisors for each type of intermediarybanks, insurance or capital market),2 while functional supervi-ion has common rules for similar financial activities regardless ofhich intermediary performs them. We compiled two datasets ofnancial sector supervisory structures, one for prudential super-ision and the other for business conduct supervision, covering8 countries over 1999–2010. In collecting the data, we drewn the 1999–2010 editions of “How countries supervise theiranking, insurers and securities markets” and on on-line official

nformation from country authorities concerning supervisory insti-utions. Among the 98 countries, there are 40 high-income, 34pper-middle income, and 24 lower-middle income economies.or illustrative purposes, we divide these countries into two sub-roups according to their financial depth.

The prudential supervision dataset distinguishes among the fol-owing structures:

2 We thus abstract from other possibly relevant subsectors that could have sep-rate supervisors such as pension funds, non-bank credit institutions or otheron-bank financial institutions.

4 l of Fin

(

(

(

(

(

rpttsaPNto

cdtahdpstsae(c

n

(

(

o

i

g

(

(

(

pe

2

adcm

2

dkfts1fgFe

vfispbppspsi

tmmss

30 M. Melecky, A.M. Podpiera / Journa

1) sectoral (institutional) supervision with the banking supervi-sion in an agency other than the central bank;

2) sectoral (institutional) supervision with the banking supervi-sion in the central bank;

3) partial integration, where two financial sectors are supervisedby the same institution, either the central bank or an agencyoutside of the central bank;

4) integration of supervision for financial subsectors in a FinancialSupervisory Authority (FSA)3;

5) integration of supervision for financial subsectors into the cen-tral bank4.

Compilation of the business conduct supervision datasetequired a more judgmental approach. Many countries have inlace a legislative framework concerning transparency of opera-ions and consumer protection. Nevertheless, some of them lackhe enforcement mechanism, especially in regards to financial con-umer protection. Pursuing transparency and disclosure is on thegenda of many prudential supervisors––the Codes of Bankingractices often set the standards for financial consumer protection.evertheless, the investigation, resolution, and arbitration of cus-

omer complaints (in particular banking customers) are pursuednly in some countries.

We include in the group of countries which pursue businessonduct supervision, all those that have in place, in addition toirectives on the pursuit of transparency and consumer protec-ion, an enforcement mechanism for financial consumer regulationnd dispute resolution. Hence, we account for (i) countries thatave specialized agencies looking after all aspects of business con-uct across financial subsectors (i.e., the “twin peak” model, orrudential supervisors that are assigned also business conductupervision), as well as for (ii) countries where there are no insti-utions with statutory responsibility for overall business conductupervision of the banking sector, but they progressed towardsn adequate consumer protection in all financial subsectors andstablished institutions, such as a financial consumer protectionFCP) agency, Financial Ombudsman, or special departments foronsumer finance within the consumer protection agency.

Following the outlined approach, we classify the following busi-ess conduct supervisory structures:

1) No business conduct – supervision not all financial sectors haveassigned business conduct supervision. Typically, the pruden-tial supervisors of the insurance sector and capital markets arealso mandated to oversee business conduct. Hence, in mostcases, no business conduct is mandated for the banking sector.5

2) Separate institution(s) for financial consumer protection – thiscategory comprises those countries in which no agency isassigned with the statutory responsibility for business conductsupervision of the banking sector. However there exist insti-tutions or specialized departments in the national consumerprotection agency that oversee the protection of financial con-sumers, including consumers of banking services. Namely, this

category includes those countries in which the prudentialsupervisors do not have statutory responsibility for FCP butthere exist either a FCP agency (e.g., Canada or Mexico), or spe-cialized complaint boards within an economy-wide consumer3 FSA also stands for Financial Supervision Authority, Financial Services Authority,r Financial Services Agency.4 The main financial subsectors that we consider are: the banking sector, the

nsurance sector and the capital markets sector.5 In this way, we stress the importance of business conduct in the banking sector,

iven the dominance of banks in financial sectors of most countries.

oiogtetwiot

ancial Stability 9 (2013) 428– 444

agency (e.g., Denmark), or a Financial Ombudsman Bureau (e.g.,Greece).

3) Sectoral supervision – prudential supervisor of each financialsubsector is assigned with the business conduct supervision inaddition to prudential supervision.

4) Business conduct supervision is integrated and assigned eitherto the central bank or to the FSA, which act as an integratedprudential supervisor.

5) The “twin peak” model – there exists an institution solelyfocused on supervising business conduct in provision of allfinancial services.

Table A1 in Appendix provides a summary of the regimes forrudential and business conduct supervisions as of end-2010 forach country in our sample.

.2. Descriptive statistics of the new database

Figs. A1, A2 and Table A2 in Appendix describe, through plotsnd summary statistics, changes in institutional structures for pru-ential supervision, and Fig. A3 and Table A3 in Appendix describehanges in business conduct supervision over 1999–2010. We sum-arize the main points revealed by these descriptive statistics next.

.2.1. Prudential supervisionOver the past decade, there has been a tendency to unify pru-

ential supervision (see Fig. A1). The proportion of countries thatept the traditional model of institutional supervision decreasedrom 62 percent in 1999 to 44 percent in 2010. At the same time,he proportion of countries that adopted a FSA or integrated theirupervision under the central bank increased substantially: from1 percent in 1999 to 25 percent in 2010 (FSA integration), androm three percent in 1999 to 8 percent in 2010 (central bank inte-ration). The proportion of countries that chose to integrate in aSA outpaced those that integrated in the central bank, both inconomies with high and low financial depth.

The prevalence of central banks in prudential banking super-ision has diminished (see Fig. A2). Among economies with highnancial depth, the central banks were responsible for bankingupervision in 58 percent of countries in 2010, down from 66ercent in 1999. In economies with low financial depth, centralank responsibility for banking supervision has decreased from 70ercent to 67 percent. However, the proportion of countries withartial integration of supervision in the central bank did not changeignificantly. At the same time, the proportion of countries withartial integration outside of the central bank decreased becauseome of them chose to unify supervision of all financial subsectorsn a FSA.

Important changes in prudential supervisory struc-ures occurred between 1999 and 2010 (see the transition

atrix in Table A2). The number of economies with frag-ented supervision––separate supervision for each financial

ubsector––decreased. Further, the number of a FSA integratedupervisors increased from 10 in 1999 to 24 in 2010, regardlessf countries’ financial development. Half of the economies thatntegrated in a FSA had initially partial prudential integrationutside of the central bank. The number of countries that inte-rated prudential supervision in the central bank increased fromhree in 1999 to eight in 2010. Four of these changes happened inconomies with lower financial depth. Central bank integrationypically occurred in economies with initially sectoral supervision,

ith the central bank supervising banks. Economies that hadnitially sectoral supervision, with the banking supervision outsidef the central bank, and those with partial integration outside ofhe central bank typically maintain their supervisory structure

l of Fin

osi

2

citsclf

osgppfist

3

fis1vfibt

3

mvssas

vsp

(

(

((

ttiotbdf

fioiopipiamiiTsbp

dvtmu

((

((

(

giavtabcdwtdaons

M. Melecky, A.M. Podpiera / Journa

r integrate in a FSA. Also, countries that have sectoral supervi-ion with the central bank supervising banks are more likely tontegrate into the central bank than into a FSA.

.2.2. Business conduct supervisionAn increased proportion of countries implemented business

onduct supervision––from 20 percent of the total pool of countriesn 1999 to 50 percent in 2010––as the awareness of its impor-ance has been rising (see Fig. A3). The percentage of countriesupervising business conduct increases with the countries’ finan-ial deepening (63 percent versus 41 percent). But economies withow financial depth have been also adopting increasingly someorm of business conduct supervision.

The transition matrix in Table A3 in Appendix shows that in 15ut of the 33 countries that adopted or integrated business conductupervision during 1999–2010, the change occurred through inte-ration either in a FSA or the central bank, or adoption of a “twineak” model. The rest of countries introduced business conduct asart of prudential supervision or founded outside agencies to fosternancial consumer protection. The twin peak type of supervisiontructures is still very limited. Countries that adopted this modelypically show high financial development.

. Estimation methodology

We estimate the determinants of institutional structures fornancial prudential supervision and business conduct supervi-ion, respectively using a panel data covering 98 countries during999–2010. We aim to explain the choice of a particular super-isory structure using a country’s general, economic, political, andnancial sector indicators, and to find which of the indicators coulde the most important. The choice of a particular supervisory struc-ure thus represents the dependent variable in the model.

.1. The modeled (dependent) variable

In the case of prudential supervision, we aim to distinguishainly between sectoral supervision and fully integrated super-

ision while accounting for the proximity of microprudentialupervision to the central bank (the macroprudential supervi-or). Partial prudential integration, in which two financial sectorsre supervised by a single agency, are thus classified as sectoralupervision.6

Because of our interest in understanding the drivers of super-isory integration and the choice of placing microprudentialupervision closer to macroprudential supervision, we order therudential supervisory structures into the following categories:

1) sectoral supervision, with the banking sector supervised by anagency outside of the central bank;

2) sectoral supervision, with the central bank supervising the

banking sector;3) unified supervision in a FSA; and4) unified supervision in the central bank.

6 In an initial regression analysis that accounted separately for partial integra-ion, no strong cut off points were identified between sectoral and partial integrationypes of prudential supervision. The two categories that we merge cannot be empir-cally distinguished using our data sample and the set of variable that we conditionn. Since we use a comprehensive set of development and financial indicators,he two categories, while theoretically and qualitatively distinguishable, may note empirically distinguishable using our modeling approach even with larger panelata sample and even broader set of conditioning variables. We leave this challengeor future research.

3

aa

l

y

wtv

ancial Stability 9 (2013) 428– 444 431

Category 1 thus represents cases when supervision of eachnancial subsector is delegated to a separate supervisor. More-ver, microprudential supervision of banks, the most systemicallymportant financial subsector, is delegated to a government agencyutside of the central bank, the macroprudential supervisor. Micro-rudential and macroprudential supervision of banks, the most

mportant financial subsector, are thus separated, increasing therobability of silos between these two supervisors. Category 2

ncludes also fragmented microprudential supervision, but banksre supervised by the central bank––with microprudential andacroprudential supervision of the systemically important bank-

ng sector closely cooperating. Category 3 groups countries withntegrated microprudential supervision outside of the central bank.his structure still separates microprudential and macroprudentialupervision. Category 4 comprises countries in which the centralank, the macroprudential supervisor, is also the integrated micro-rudential supervisor.

For business conduct supervision, the ordering focuses on theegree of integration and whether (or not) business conduct super-ision is the attached (subsumed) to prudential supervision. Wehus order the “twin peak” structure as the highest given the single

andate assigned to the integrated business conduct supervisornder this arrangement.

1) No business conduct.2) An agency for financial consumer protection exists but there

is no integrated business conduct supervisor and prudentialsupervisors have no responsibility for business conduct.

3) Sectoral business conduct.4) FSA or central bank as integrated supervisors are also assigned

the task of business conduct supervision.5) “Twin peak” model, i.e., there is a unified authority with a single

mandate for business conduct supervision.

The specific logic of the ordering is as follows. Category 1roups countries with no business conduct supervision. Category 2ncludes countries where financial consumer protection agenciesre established, but no comprehensive business conduct super-ision exists. Recall that business conduct supervision is broaderhan financial consumer protection, including other elements suchs market integrity. Category 3 comprises countries with sectoralusiness conduct supervision. Here we do not separate out theases when a sectoral prudential supervisor is also business con-uct supervisor or otherwise. Category 4 involves countries inhich integrated business conduct supervision exists but is not

he sole mandate of the government agencies. In practice, the man-ate of prudential supervision has a longer history in these casesnd business conduct supervision is, at least implicitly, a secondarybjective. Category 5 then includes counties with integrated busi-ess conduct supervision in an agency that has business conductupervision as the sole mandate (objective).

.2. The applied regression model

We model the changes in supervisory structures over time andcross countries using ordered probit model and condition on

broad set of explanatory variables.7 Given our ordering crite-

7 The general ordered choice model, a latent variable regression, takes the fol-owing form:

∗ = x′ ̌ + ε (1)

here y* is the unobserved variable, x is a vector of explanatory variables, ε ishe random disturbance normally distributed across observations, with mean andariance normalized to one and zero, respectively

4 l of Fin

rtpratlmcioi

3

efircpmoiib(C

ctatfaseaildd

t

ia

wa

cNwCcifila1ta

ttcwcfiiMnpctadbattgena

32 M. Melecky, A.M. Podpiera / Journa

ia for the dependent variable and the interest in understandinghe determinants of supervisory integration, ordered probit is ourreferred methodology.8 The ordered probit model is a latentegression model. The latent (unobserved) variable in our caseccounts for the existing variations among countries and acrossime within each ordered category. It quantifies how a particu-ar legal framework––that governs the institutional arrangement,

andates, powers and tools––concerning prudential (businessonduct) supervision in a country provides for greater/smallerntegration of supervisory functions and their governance. Thebserved dependent variable is the classification of each countryn one of the ordered choices.

.3. The considered explanatory variables

We consider four groups of explanatory variables: general andconomic development indicators, political economy indicators,nancial sector development indicators, and financial crises expe-ience. The general country characteristics include the populationount, GDP per capita, and the degree of openness (total trade as aercentage of GDP). To characterize a country’s political environ-ent that is relevant to our investigation, we focus on the quality

f governance and the independence of the central bank. The qual-ty of governance is based on the average of the six governancendicators9 constructed by Kaufmann et al. (2010). For the centralank independence indicator, we use the central bank autonomyCBA) index estimated in Arnone et al. (2007), which assesses theBA at the end of 2003.

The financial sector development indicators that we consideromprise private credit as a percentage of GDP, stock market capi-alization as a percentage of GDP, the number of listed companies,nd the non-life insurance premium as a percentage of GDP. Fur-her, to characterize specifically a country’s banking sector, weocus on banking concentration, efficiency, profitability, liquidity,nd performance. The banking concentration is measured by thehare of the three largest banks in total banking sector assets. Thefficiency is approximated by the cost-to-income ratio. Countries’verage net interest margin and the proportion of the non interestncome in total income describe banking sector profitability. The

iquidity indicator is measured by the ratio of liquid assets overeposits and short-term funding, and the ratio of private credit overeposits. Additional financial soundness indicators for banks that8 We, use the multinomial logit and other alternative estimation approaches toest the robustness of our results in Section 4.3.

9 The six governance indicators are the following: voice and accountability, polit-cal stability no violence, government effectiveness, regulatory quality, rule of law,nd control of corruption.

3

Supervisory structureit(2) = populationit−1 + GDP per capitait−1 + tra

+(

private creditGDP

)it−1

+ market capitaliz

+ financial crisesit−1 + banking concentr

+(

noninterest incometotal income

)it−1

+(

privat crdepos

+(

capitalassets

)it−1

+ εit

Apo

zn1ct

ancial Stability 9 (2013) 428– 444

e consider include the non-performing loans ratio (NPL), capitaldequacy ratio (CAR), and capital to assets ratio.

Finally, we consider the effect of past financial crises on thehoice to integrate. Charmichael et al. (2004) note that in someordic or Asian countries the creation of integrated supervisorsas prompted by a recent financial sector crisis. On the other hand,ihak and Podpiera (2006), based on the visual inspection of aross-section of countries as of 2004, claim that this relationships far from straightforward. We aim to capture the effect of pastnancial crises by their cumulative count as of 1996.10 The cumu-

ative number of financial crises was constructed based on Laevennd Valencia’s (2008) financial crisis database, covering the period970–2007. The database was updated using the same criteria forhe period 2008–2010. Table A4 in Appendix lists data sources forll explanatory variables employed in our regression analysis.

The choice of explanatory variables in our study is motivated byhe existing literature, but also augmented by additional variableshat further elaborate on the development stage of and finan-ial structure in our sample countries. Many of the variables thate consider (e.g., GDP per capita, population, good governance,

entral bank independence, banking assets as percentage of GDP,nancial market capitalization, concentration effect) are employed

n related studies (Shen, 2006; Masciandaro, 2006, 2007, 2009;asciandaro et al., 2008). Generally, GDP per capita, public gover-

ance, banking assets, and financial market capitalization impactositively (not always significantly) on supervisory unification. Inontrast, population size and central bank independence are nega-ively related to supervisory integration. Masciandaro (2009) alsoccounts for the influence of past financial crises by including aummy that signals whether a crisis has occurred up to five yearsefore the last reform of the supervisory architecture. We choose toccount for the cumulative impact of financial crises, expecting thathe more often a country as been confronted with a financial crisis,he stronger the incentive to reform and unify its supervision. Weo beyond the usual set of variables employed in the literature andnrich it with variables that further elaborate on countries’ eco-omic and institutional development, as well as the developmentnd characteristics of their financial sector.

.4. Putting it all together in the estimation

Formally, the estimated panel regression is specified as:

deit−1 + governanceit−1 + central bank autonomyi

ationit−1 +(

nonlife insuranceGDP

)t−1

+ listed companiesit−1

ationit−1 +(

costincome

)it−1

+ net interest marginit−1

editits

)it−1

+(

liquid assetsfunding

)it−1

+ NPLRit−1 + CARit−1

(2)

ll variables in Eq. (2) are lagged by one period in order to avoidossible endogeneity problems, except for the “central bank auton-my” (which is a constant for each country).

10 We consider also other statistics related to financial crisis experience, namely,ero-one variable indicating simply whether a country has experienced a crisis orot, a measure of whether country experienced a single or repeated crises in last5 years, and the time from the last crisis (in years). Only the cumulative number ofrises was kept in the baseline regression for its best performance and behavior inhe regression.

l of Fin

4

odfetRatacraaed

4

ltntepctimtismc(

ognsbsgfistca

cgiftifbb

s

apt

tfttvsisvansfmafio

iiTadapiNpl

ettctfi

4

vticfiiimpresumably ensure holistic and consistent oversight of businessconduct in the provision of financial services. The degree of open-ness is significant in the regression but with a negative sign,suggesting a higher probability of existence and greater integration

M. Melecky, A.M. Podpiera / Journa

. Estimation results

Tables 1 and 2 present our baseline regression results usingrdered probit model for prudential supervision and business con-uct supervision, respectively. The tables show estimation resultsor selected explanatory variables (columns 1–9), as well as for allxplanatory variables (column 10). Column (11) presents results ofhe parsimonious regressions based on adjusted R2 maximization.esults for the full specification, presented in column (11), do notccount for the effect of bank soundness indicators (NPL, CAR, andhe capital to assets ratio), because data for these variables arevailable only as of 2003. The results for the subgroup of finan-ial soundness indicators are thus only showed separately. As aobustness check for the main regression results, Table 3 reportsdditional estimation results using alternative model specificationnd estimation approaches. Namely, the robustness is tested bystimating the pooled ordered probit model, binary choice panelata model, and multinomial panel data model.

.1. Prudential supervision

Table 1 shows the country characteristics that influence theikelihood that a country would integrate prudential supervision:he country size, openness, level of development, quality of gover-ance, central bank’s autonomy, financial sector development, andhe number of past financial crises. Based on the estimates, smallconomies are more likely to integrate prudential supervision. Theopulation size has a negative and significant coefficient both whenonsidered in a subgroup regression as well as in the full specifica-ion. Typically, a small economy has a small financial sector; hencentegrating supervisory institutions of financial subsectors could be

ore feasible and practical than in the case of a large economy. Fur-her, in small economies with relatively small financial sectors, thentegration is likely to enhance cost efficiency, especially throughupervisory staff reduction, and economizing on the fixed invest-ents (IT infrastructure and systems, training facilities, etc.) that

an be consolidated in the case of unified prudential supervisionErbenova, 2006).

A country’s level of development (GDP per capita) and tradepenness positively influence the likelihood of prudential inte-ration. More developed countries could easily mobilize resourcesecessary for developing and implementing the strategy for tran-ition from a less to more integrated supervisory structure. Also,anking systems of more developed countries are relatively moreophisticated and characterized by the presence of financial con-lomerates. Hence, integrated prudential supervision of mainnancial subsectors could increase the effectiveness of prudentialupervision. Further, a country’s openness is positively related tohe probability of integrating prudential supervision, as increasedapital flows in and out of the country need a holistic monitoringnd managing of exposures to capital flow reversals.

Regarding political economy variables, both governance andentral bank autonomy play an important role. The quality ofovernance stays significant in all specifications, underlying themportance of good governance for the decision to integrate (asound also in Masciandaro, 2006, 2007). The significant and nega-ive coefficient estimate for central bank’s autonomy suggests thatntegration of prudential supervision is a less preferred outcome

rom the point of view of an independent central bank. This coulde because integration of prudential supervision in the central bankrings additional responsibilities for the central bank.11 One may11 Highly autonomous central banks might have preferred to keep theirtrong independence that primarily came from the mandate of monetary policy

idc

tp

ancial Stability 9 (2013) 428– 444 433

lso argue that the integration process itself could jeopardize thereviously established independence of the central bank’s mone-ary policy.

Although the evidence from the subgroup regressions showshat several financial development indicators are significant, in theull specification, only the coefficient of stock market capitaliza-ion comes out significant. In the subgroup regressions, the credito GDP ratio impacts positively the probability of integration, whileariables related to other financial sectors (non-life premium, andtock market capitalization) have negative impacts. A large bank-ng sector is more likely to be interconnected with other financialubsectors. Hence there is a synergy effect that a unified super-ision can induce (see De Luna-Martinez and Rose, 2003; Cihaknd Podpiera, 2006; Herring and Carmassi, 2008). However, if theon-banking financial subsectors are relatively large, a sectoralupervision might be more appropriate as the drawbacks comingrom an oversized institution conducting prudential supervision

ight be higher than the synergetic benefits of integration (seelso Cihak and Podpiera, 2006; Herring and Carmassi, 2008). In theull specification, only the coefficient on the stock market capital-zation turns out significant, revealing a negative impact of the sizef securities market on the probability to integrate.12

Among the banking sector characteristics, the aggregate liquid-ty risk exposure (private credit to deposit ratio) appears the mostmportant drivers of supervisory integration in the prudential area.he estimated positive effect suggests that an increased exposure toggregate liquidity risk has prompted changes towards unified pru-ential supervision. The results from subgroup regressions reveallso a negative significant coefficient on the net interest margin, aroxy for banking sector profitability that could be related to the

nfluence of the banking sector lobby on the decision to integrate.amely, the higher the banking sector profitability, the higher is itsreference for status quo in prudential supervision, and hence the

ower is the probability of integrating prudential supervision.The cumulative number of financial crises, which a country has

xperienced, has clearly brought about an increase in the incen-ives to integrate prudential supervision. This is consistent withhe hypothesis that an integrated supervisor, which provides forlose proximity of micro- and macro-prudential supervision, is bet-er prepared to prevent, or cope with, episodes of system-widenancial distress than sectoral supervisors.

.2. Business conduct supervision

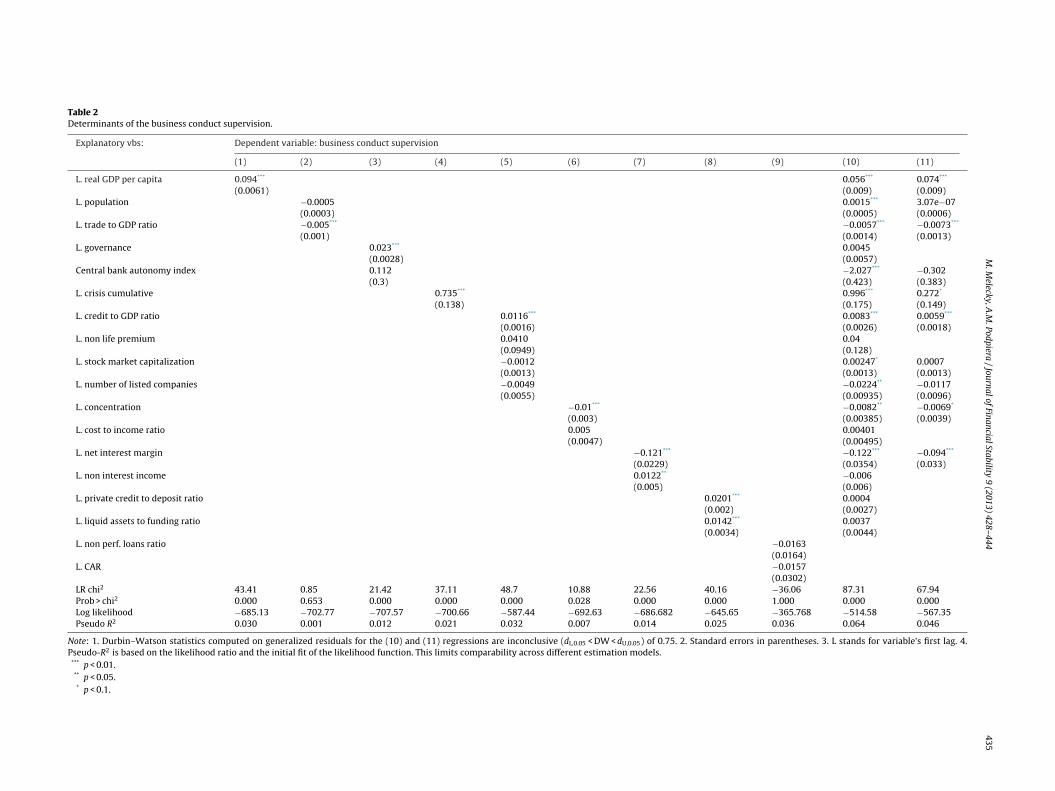

The estimation results in Table 2 reveal which of the consideredariables could significantly affect the probability that a coun-ry established and integrated business conduct supervision: thencome level, degree of openness, financial depth, banking sectoroncentration, aggregate liquidity exposure (the share of foreignnancing), and the number of past financial crises. The income level

s a robust explanatory variable, maintaining sign and significancen all regressions. The results thus suggest that as countries develop,

ore integration of business conduct supervision is desired to

mplementation. Nevertheless, recent events have shown that integration of pru-ential outside the central bank (in a FSA) could prohibit the synergies between theonduct of monetary policy and banking supervision.12 The loss of significance of the other financial depth variables is probably dueo the presence of colinearity as the credit to GDP ratio and the GDP per capita areositively correlated (see the correlation matrix in Appendix).

434M

. M

elecky, A

.M.

Podpiera /

Journal of

Financial Stability

9 (2013) 428– 444

Table 1Determinants of prudential supervision.

Explanatory vbs: Dependent variable: prudential supervision

(1) (2) (3) (4) (5) (6) (7) (8) (9) (10) (11)

L. real GDP per capita 0.014*** 0.0595*** 0.0545***

(0.0038) (0.0092) (0.0093)L. population −0.0036*** −0.0021*** −0.002***

(0.0003) (0.0004) (0.0003)L. trade to GDP ratio 0.0064*** 0.0104*** 0.0097***

(0.0016) (0.0015) (0.0014)L. governance 0.0399*** 0.0150** 0.0096*

(0.0027) (0.0059) (0.0054)Central bank autonomy index −0.831** −3.861*** −3.978***

(0.381) (0.425) (0.418)L. crisis cumulative 1.653*** 0.673*** 0.652***

(0.152) (0.144) (0.134)L. credit to GDP ratio 0.00368** −0.0017

(0.00145) (0.0023)L. non life premium −0.280*** −0.188

(0.0889) (0.119)L. stock market capitalization −0.005*** −0.0088*** −0.009***

(0.0012) (0.0013) (0.0012)L. number of listed companies −0.0071 0.0041

(0.0052) (0.0068)L. concentration 0.0020 0.0013

(0.0023) (0.004)L. cost to income ratio 0.00035 −0.003

(0.0026) (0.0039)L. net interest margin −0.032* 0.0424

(0.0176) (0.0363)L. non interest income −0.0034 −0.0034

(0.0031) (0.0049)L. private credit to deposit ratio 0.0024* 0.0102*** 0.0098***

(0.0014) (0.0022) (0.0019)L. liquid assets to funding ratio 0.0014 −0.0034

(0.0024) (0.0036)L. non perf. loans ratio −0.0065

(0.0137)L. CAR 0.0129

(0.0219)LR chi2 75.5 8.6 25 14.2 20.3 63.2 63.5 52.6 32.02 80.3 77.3Prob > chi2 0.000 0.0136 0 0.0002 0.0004 0.0000 0.0000 0.0000 0.0000 0.0000 0.000Log likelihood −673.8 −703.15 −697.911 −706.08 −587.41 −674.19 −669.47 −644.66 −327.46 −515.1 −538.2Pseudo R2 0.042 0.005 0.014 0.008 0.014 0.036 0.036 0.031 0.032 0.065 0.064

Note: 1. Durbin–Watson statistics computed on generalized residuals for the (10) and (11) regressions are inconclusive (dL,0.05 < DW < dU,0.05) of 0.74. 2. Standard errors in parentheses. 3. L stands for variable’s first lag. 4.Pseudo-R2 is based on the likelihood ratio and the initial fit of the likelihood function. This limits comparability across different estimation models.

*** p < 0.01.** p < 0.05.* p < 0.1.

M.

Melecky,

A.M

. Podpiera

/ Journal

of Financial

Stability 9 (2013) 428– 444

435

Table 2Determinants of the business conduct supervision.

Explanatory vbs: Dependent variable: business conduct supervision

(1) (2) (3) (4) (5) (6) (7) (8) (9) (10) (11)

L. real GDP per capita 0.094*** 0.056*** 0.074***

(0.0061) (0.009) (0.009)L. population −0.0005 0.0015*** 3.07e−07

(0.0003) (0.0005) (0.0006)L. trade to GDP ratio −0.005*** −0.0057*** −0.0073***

(0.001) (0.0014) (0.0013)L. governance 0.023*** 0.0045

(0.0028) (0.0057)Central bank autonomy index 0.112 −2.027*** −0.302

(0.3) (0.423) (0.383)L. crisis cumulative 0.735*** 0.996*** 0.272*

(0.138) (0.175) (0.149)L. credit to GDP ratio 0.0116*** 0.0083*** 0.0059***

(0.0016) (0.0026) (0.0018)L. non life premium 0.0410 0.04

(0.0949) (0.128)L. stock market capitalization −0.0012 0.00247* 0.0007

(0.0013) (0.0013) (0.0013)L. number of listed companies −0.0049 −0.0224** −0.0117

(0.0055) (0.00935) (0.0096)L. concentration −0.01*** −0.0082** −0.0069*

(0.003) (0.00385) (0.0039)L. cost to income ratio 0.005 0.00401

(0.0047) (0.00495)L. net interest margin −0.121*** −0.122*** −0.094***

(0.0229) (0.0354) (0.033)L. non interest income 0.0122** −0.006

(0.005) (0.006)L. private credit to deposit ratio 0.0201*** 0.0004

(0.002) (0.0027)L. liquid assets to funding ratio 0.0142*** 0.0037

(0.0034) (0.0044)L. non perf. loans ratio −0.0163

(0.0164)L. CAR −0.0157

(0.0302)LR chi2 43.41 0.85 21.42 37.11 48.7 10.88 22.56 40.16 −36.06 87.31 67.94Prob > chi2 0.000 0.653 0.000 0.000 0.000 0.028 0.000 0.000 1.000 0.000 0.000Log likelihood −685.13 −702.77 −707.57 −700.66 −587.44 −692.63 −686.682 −645.65 −365.768 −514.58 −567.35Pseudo R2 0.030 0.001 0.012 0.021 0.032 0.007 0.014 0.025 0.036 0.064 0.046

Note: 1. Durbin–Watson statistics computed on generalized residuals for the (10) and (11) regressions are inconclusive (dL,0.05 < DW < dU,0.05) of 0.75. 2. Standard errors in parentheses. 3. L stands for variable’s first lag. 4.Pseudo-R2 is based on the likelihood ratio and the initial fit of the likelihood function. This limits comparability across different estimation models.

*** p < 0.01.** p < 0.05.* p < 0.1.

436M

. M

elecky, A

.M.

Podpiera /

Journal of

Financial Stability

9 (2013) 428– 444

Table 3Robustness analysis.

Explanatory vbs: Ordered probit pooled regression Binary choice panel regression Multinomial logit panel regressions

Prudential supervision Business conduct supervision

Prudentialsupervision

Businessconductsupervision

Prudentialsupervision

Businessconductsupervision

Prob 2/Prob1a

Prob 3/Prob1a

Prob 4/Prob1a

Prob 2/Prob1a

Prob 3/Prob1a

Prob 4/Prob1a

L. real GDP per capita 0.0194*** 0.0228*** 0.330*** 0.307*** 1.021*** 1.207*** 1.228*** 0.147** 0.221*** 0.210***

(0.00622) (0.00656) (0.0770) (0.0636) (0.302) (0.303) (0.304) (0.0588) (0.0495) (0.0473)L. population −0.00092*** −0.00048 −0.0141 −0.00204 −0.033*** −0.059*** −0.059*** −0.017*** −0.0023 −0.010***

(0.00027) (0.00035) (0.0265) (0.00605) (0.008) (0.01) (0.021) (0.0061) (0.0018) (0.0034)L. trade to GDP ratio 0.00351*** −0.00113 0.011 0.0151 0.0265 0.0342** 0.0564*** −0.062*** −0.029*** −0.0092

(0.00085) (0.000864) (0.008) (0.0109) (0.0173) (0.0173) (0.0181) (0.0102) (0.00695) (0.00678)L. governance 0.0146*** 0.0212*** 0.0110 0.0188 −0.688*** −0.653*** −0.536*** −0.0217 −0.096*** −0.0336

(0.0035) (0.00410) (0.0281) (0.0402) (0.176) (0.176) (0.179) (0.0244) (0.0228) (0.0232)Central bank autonomy index −1.368*** −0.502* 1.241 −2.336 −54.43*** −52.45*** −56.93*** −8.319*** −4.773*** −7.661***

(0.260) (0.287) (3.100) (3.938) (13.63) (13.65) (13.72) (1.850) (1.808) (1.736)L. crisis cumulative 0.586*** 0.411*** 1.479 1.959** −0.618 0.875 3.088* −2.248** 1.836*** 2.976***

(0.0980) (0.111) (1.076) (0.958) (1.752) (1.758) (1.865) (0.969) (0.597) (0.591)L. credit to GDP ratio −0.0059*** 0.00019 −0.0134 0.0295** 0.0975*** 0.0905*** 0.0953*** 0.0810*** 0.0667*** 0.0567***

(0.00148) (0.00154) (0.0124) (0.0129) (0.0338) (0.0339) (0.0353) (0.0145) (0.0110) (0.0105)L. non life premium −0.219*** −0.143* −0.115 −0.564 −4.799** −5.176** −7.824*** −2.333*** 0.575 0.295

(0.0771) (0.086) (0.623) (0.585) (2.298) (2.300) (2.411) (0.898) (0.680) (0.652)L. stock market capitalization −0.0052*** 0.00137 −0.0155*** −0.0236* −0.00314 −0.0180 −0.0309** 0.0444*** 0.0441*** 0.0194**

(0.0009) (0.00091) (0.00559) (0.0137) (0.0129) (0.0130) (0.0149) (0.0087) (0.0076) (0.0077)L. number of listed companies 0.0220*** 0.000167 −0.109 −0.0439 0.0422 0.0926 −0.235 0.127*** −0.0423 0.121***

(0.00463) (0.00529) (0.117) (0.0769) (0.121) (0.122) (0.209) (0.0355) (0.0361) (0.0329)L. concentration 0.00735*** −0.00571** −0.0357** −0.0516** 0.268*** 0.240*** 0.193*** 0.0211 −0.073*** −0.055***

(0.00246) (0.00277) (0.0159) (0.0206) (0.0661) (0.0664) (0.0680) (0.0178) (0.0176) (0.0174)L. cost to income ratio −0.00960*** −0.00260 −0.0306** −0.00177 0.00882 0.0118 0.0162 0.0319 −0.0226 0.0117

(0.00292) (0.00327) (0.0149) (0.0156) (0.0225) (0.0217) (0.0258) (0.0253) (0.0190) (0.0163)L. net interest margin −0.0922*** 0.0127 −0.122 −0.195 −0.701 −0.610 −0.0681 0.0880 −0.190** −0.0715

(0.0223) (0.0252) (0.129) (0.206) (0.488) (0.494) (0.506) (0.129) (0.0919) (0.0941)L. non interest income −0.000922 −0.00239 −0.0326** −0.0307 −0.0668 −0.0301 −0.0554 0.0395 −0.00375 0.0139

(0.00338) (0.00392) (0.0164) (0.0223) (0.0485) (0.0489) (0.0529) (0.0250) (0.0208) (0.0202)L. private credit to deposit ratio 0.00938*** 0.00507*** 0.0217*** 0.0124 0.0665*** 0.0881*** 0.0869*** −0.067*** 0.000418 0.0206**

(0.00146) (0.00162) (0.00822) (0.00960) (0.0236) (0.0239) (0.0255) (0.0156) (0.00884) (0.00902)L. liquid assets to funding ratio 0.00940*** 0.00130 −0.00520 −0.00824 0.0262 −0.00883 0.0418 0.0440** 0.0445** 0.0423**

(0.00255) (0.00297) (0.0138) (0.0162) (0.0240) (0.0244) (0.0285) (0.0186) (0.0179) (0.0172)LR chi2/Wald chi2 215.31 207.05 50.16 126.46 966.53 661.122Prob > chi2 0.0000 0.0000 0.0000 0.0000 0.000 0.000Log likelihood −790.95 −791.5 −144.95 −91.8249 −363.94 −392.18Pseudo R2 0.12 0.116 0.148 0.47 0.88 0.59

Note: 1. Durbin–Watson statistics computed on generalized residuals are inconclusive (dL,0.05 < DW < dU,0.05) of 0.79 (prudential) and 0.74 (business conduct) for the pooled regression; 0.84 and 0. 74 (prudential and businessconduct) for the binomial regression. 2. Standard errors in parentheses. 3. L stands for variable’s first lag. 4. Pseudo-R2 is based on the likelihood ratio and the initial fit of the likelihood function. This limits comparability acrossdifferent estimation models.

a The reference structure for prudential supervision is “sectoral supervision, with the banking sector supervised by an agency outside of the central bank”. The reference structure for business conduct supervision is “nobusiness conduct”.

*** p < 0.01.** p < 0.05.* p < 0.1.

l of Fin

oOsvIpv

gtfgsr

dniiidigdds

cgimmcttoslccs

4b

npbtAbtspbpno

ponit

fimbtwra

igbvvta

4

twmsd(

rgctrtstaodeg

tssinwfm

easocmIrtioi

M. Melecky, A.M. Podpiera / Journa

f business conduct supervision in relatively less open economies.pen economies are subject to high capital inflows and prudential

upervisors in conjunction with monetary policy have to be extraigilant in managing the volumes and allocation of capital inflows.n the past, this may have diverted the focus of open economies torudential supervision at the expense of business conduct super-ision implementation or improvements.

As for the political characteristics, the quality of a country’sovernance is an important factor for business conduct integra-ion in the subset regression, but it loses its significance in theull regression, likely due to the significant correlation between theovernance and income. The central bank autonomy Index is notignificant both in the subset regression and in the parsimoniousegression.

Concerning the financial development indicators, financialeepening (private credit to GDP) is the only variable staying sig-ificant and positive in all regressions. The greater the financial

nclusion of household and firms in credit provision, the highers the probability that the country will establish and integratets business conduct supervision. We can conjecture that greaterevelopment of the banking sector (higher credit to GDP) increases

nter-linkages with other financial subsectors, and leads to emer-ence of financial conglomerates. This could then prompt theecision to integrate business conduct supervision to a greateregree to eliminate possible loopholes in fragmented sectoralupervision.

Banking sector characteristics, such as net interest margins andoncentration have persistently significant negative effects on inte-ration of business conduct supervision. The negative effect of netnterest margins could stem from the negative influence of greater

arket monopolistic power, which allows for sustained high profitargins, on business conduct supervision. Similarly, highly con-

entrated banking sectors typically show greater lobbying powerhat could be used against the introduction of and a more holis-ic approach to business conduct supervision. In addition, severalther characteristics of the banking sector appear significant in theubset regressions but lose their significance in the full regression,ikely due to present colinearities. Finally, the number of finan-ial crises experienced in the recent past positively influenced aountry’s decision to implement and integrate business conductupervision.

.3. Comparison of the empirical results for prudential andusiness conduct supervision

Several variables influence integration of prudential and busi-ess conduct supervision in a similar direction. The increasedrobability of greater integration in both structures is promptedy higher economic development, greater financial deepening andhe size of the banking sector, and the experience of financial crises.lso, development of country’s governance and greater centralank autonomy increase the probability of integration of pruden-ial as well as business conduct supervision. For business conductupervision, however, the latter variables lose their explanatoryower when economic development is accounted for. Althoughusiness conduct supervision is younger in its implementation thanrudential supervision, the above common drivers seem to alertational policymakers to act in similar ways on both these aspectsf financial services supervision.

Some variables have contrasting impact on prudential com-ared with business conducts supervision. One of them is trade

penness that positively impacts prudential integration but has aegative impact on business conduct integration. This result is intu-tive for the prudential supervision where countries get exposedo larger capital flows, so that supervisory harmonization across

tis

ancial Stability 9 (2013) 428– 444 437

nancial subsectors and closer cooperation of microprudential andacroprudential supervision are needed. The negative impact on

usiness conduct integration is somewhat puzzling. Our conjec-ure is that the greater need to focus on prudential supervisionhen country opens up could take away some of the focus and

esources from business conduct supervision and its integration,t least initially.

Finally, there are a number of significant drivers of prudentialntegration that do not affect significantly business conduct inte-ration and vise versa. Although we have started from a common,road set of possibly relevant explanatory variables for both super-isory regimes, we have expected the final parsimonious models toary. This expectation has proven right and the aspects of institu-ional structures for prudential and business conduct supervisionre indeed distinct.

.4. Robustness analysis

We employ different model structures and estimation methodso test the robustness of our baseline estimation results. Namely,e use the ordered probit pooled regression, the binary choiceodel, and the multinomial model to test the impact of the cho-

en functional form, and the classification and ordering of theependent variables. Table 3 reports the results of these regressionsrobustness tests).

Overall, the pooled regressions results support the main panelesults. Specifically, the effects of income, openness, population,ood governance, central bank autonomy, the number of pastrises, and banking concentration, liquidity, and profitability fromhe baseline estimations hold. The only puzzling estimation resultelates to the effect of financial depth. The coefficient of the credito GDP ratio turns out significant and negative for prudentialupervision estimation. Nevertheless, for the same regressions,he coefficient of stock market capitalization and non-life insur-nce as percentage of GDP are negative and significant, as in therdered probit regressions. Hence, the interpretation that greaterevelopment of financial subsectors other than the banking one,ncourages countries to opt for more sectoral rather than inte-rated supervision, still holds.

The binary choice regressions test the effect of the explana-ory variables on less granular classification of the supervisorytructures that distinguishes only among unified and non-unifiedupervision. For prudential supervision, the unified structurencludes FSA and unified supervision in the central bank. For busi-ess conduct supervision, the unified structures include those,here FSA or central banks have the statutory responsibility

or business conduct supervision, and the twin peak supervisoryodel.Consider the regression results for prudential supervision. The

ffects of income, stock market capitalization, and banking liquidityppear crucial for the decision to integrate prudential supervi-ion. It seems that other significant explanatory variables of therdered probit regression (population, trade, public governance,entral bank autonomy, and the number of past crises) could beore important in describing the type of supervisory structures.

n addition, the binary choice regression for prudential supervisioneveals other significant explanatory variables behind the decisiono integrate. Bank concentration, the proxy for efficiency (cost toncome ratio), and the ratio of non-interest income to total incomef the banking sector have a significantly negative influence onntegration.

All of these variables can be related to the lobbying power ofhe banking sector which may act as a negative force against thentegration of prudential supervision. This is presumably to pre-erve capital and other profit-driven arbitrage opportunities across

4 l of Financial Stability 9 (2013) 428– 444

fibtmptser

ovsFapApisiFepcomc

olwcirsGi“btoccppv

5s

to

bc

ac

tst

Source: Authors‘ Cal culation

ARGARM

AUS

AUTBEL

BOL

BWA

BRA

BGRCAN

CHL

CHN

COLCRI

HRV

CYPCZE

ECU

EGY

SLV

FINFRAGEO

DEU

GRC

HKGHUN

IND

IDN

IRN

ISR

ITA

JPN

JORKAZ

KOR

LBN

LTU

LUX

MKD

MYSMLTMUS

MEX

APR

NAM NLD

NZL

NGA

PAN

PER

PHLPOL

PRTROMRUSSAU

SGP

SVK

SVN

ZAFESPLKA

SWE

CHE

THATTOTUN

TUR

UKR

ARE

GBR

USAURY

VNM

0

0.5

1

1.5

2

2.5

3

0 0. 5 1 1. 5 2 2. 5 3 3. 5

Fit

ted

Actual

sotAbst

5

ripSolstie

bmltUpc

38 M. Melecky, A.M. Podpiera / Journa

nancial subsectors within financial groups. The results of theinary choice regression for business conduct supervision supporthe estimated effects of income, the number of past crises, stock

arket capitalization, and bank concentration from the orderedrobit regression. Further, the binary choice regression indicateshat the remaining significant variables from the ordered regres-ion (trade and net interest margin) have more relevance forxplaining the particular type of business conduct supervisionather than its overall integration.

We also employ the multinomial logit model to test the effectf explanatory variables on the probability of choosing one super-isory structure over the probability of choosing a referenceupervisory structure (this is the first category of our ranking13).or the dependent variable characterizing prudential supervision,ll three sets of results – corresponding to the three ratios ofrobabilities14 – are generally supportive of the baseline results.n increase in the income level, the credit to GDP ratio and therivate credit to deposit ratio seem to characterize environments

n which countries opt for relatively more integrated supervisorytructures. The population, CBA index, and the ratio of non-lifensurance premium over GDP affect this preference negatively.or other variables, the coefficients turn out significant only whenxplaining some of the probability ratios. The openness impactsositively only the preference towards unified structures (FSA orentral bank unification). In the same manner, the positive effectf the number of past crises and the negative effect of the stockarket capitalization appear to influence only the preference for

entral bank unification.Albeit supporting the baseline results in general, the results

f multinomial regressions for business conduct supervision areess uniform across the three reported probability ratios, compared

ith those for prudential supervision.15 At the same time, they areonveying interesting information as to which probability ratio isnfluenced by the changes in explanatory variables, given that theeference supervisory structure is “no business conduct supervi-ion”. The effects of the income level, CBA index, and credit overDP ratio hold for all three probability ratios. Openness negatively

nfluences only probability ratios pertaining to the change fromno business conduct” to “sectoral business conduct” and “partialusiness conduct with some consumer finance protection”, but nothe change to “unified business conduct supervision”. The numberf past crises positively impacts only the probability ratios con-erning partial and unified business conduct supervision. Bankingoncentration, on the other hand, affects negatively the latter tworobability ratios. The profitability indicators affect negatively therobability ratio of a change to the partial business conduct super-ision with enforcement of financial consumer protection.

. Actual and benchmark (predicted) supervisorytructures

In this section, we benchmark the existing supervisory struc-ures of our sample countries against the model predicted degreef supervisory integration. This is to illustrate whether a country’s

13 For prudential supervision the first category is “sectoral supervision, with theanking sector supervised by an agency outside of the central bank”. For the businessonduct the first category is “no business conduct”.14 1. Probability of choosing category 2/probability of choosing category 1; 2. Prob-bility of choosing category 3/probability of choosing category 1; 3. Probability ofhoosing category 4/probability of choosing category 1.15 There are three sets of results (corresponding to three probability ratio). In ordero be able to run the regressions, we had to merge the last ranked supervisorytructure, the “twin peaks model”, to the “unified in FSA or central bank” and givenhe very small number of countries with a “twin peak model”.

5

coct

megtfi

Fig. 1. Actual and model predicted values of prudential supervision integration.

upervisory structure followed the prevailing global trend basedn its typology, and to identify countries with supervisory struc-ures notably less or more integrated than predicted by our model.lthough each country and its financial system are unique, the com-ination of relevant country indicators identified in our estimationshould be able to capture the country specifics for the purpose ofhis benchmarking exercise reasonably well.

.1. Prudential supervision

Using the parsimonious estimates of the ordered probit modeleported in Table 1 (column 12), we derive the model’s predictedntegration of prudential supervision for each country and com-are it with the actual degree of integration (ranked 1–4, seeection 4), constructed as an average over 2008–2010. The resultf such a comparison is depicted in Fig. 1 along with the regressionine showing in the north-west corner countries with supervisorytructures less integrated than predicted by our model and, inhe south-east corner, countries with supervisory structures morentegrated than predicted by our models based on internationalxperience.

Fig. 1 shows that a number of countries, in particular Luxem-urg, Panama, Costa Rica, Canada, and Chile, are expected to haveore integrated prudential supervision by 2010, given their typo-

ogy and historical experience of their peers. On the other hand,here are several countries including Armenia, Czech Republic,ruguay, Netherlands, Slovakia and Poland that integrated theirrudential supervisory structures more than predicted by theirountry and financial system characteristics.16

.2. Business conduct supervision

Again, using the estimates of our model reported in Table 2 weompare the model’s predicted values with the actual structures

f business conducts supervision (averaged over 2008–2010). Theomparison of existing versus model-predicted supervisory struc-ures is shown in Fig. 2.16 For some of the countries in the over-performing category, a “fashion effect”aybe at work. The literature (see Masciandaro et al., 2008) refers to the fashion

ffect (or bandwagon effect) if reformers were inspired by the type of changes inovernance arrangements introduced by earlier reformers rather than the effec-iveness of an integrated supervisory structure based on their economic system andnancial sector characteristics.

M. Melecky, A.M. Podpiera / Journal of Fin

Source: Authors‘ Cal culati on

ARG

ARM

AUSAUT

BEL

BOL BWA

BRA

BGR

CAN

CHL

CHN

COL

CRI

HRV

CYP

CZE

DNK

EGY

SLVEST

FIN

FRA

GEO

DEU

GRC

HKG

HUNIND

IDNIRN

IRL

ISR

ITA

JAM

JPN

JORKAZ

KOR

LVALBN

LTU

LUX

MKD

MYSMLT

MUS MEXAPR

NAM

NLD

NZL

NGA PANPERPHL

POL

PRT

ROM

RUSSAU

SGPSVK

SVN

ZAF

ESP

LKA

SWE

CHE

THATTOTUN

TURUKR

ARE

GBR

USA

URY

VNM0

0.5

1

1.5

2

2.5

3

0 0. 5 1 1. 5 2 2. 5 3 3. 5 4 4. 5

Fit

ted

Act ual

Ft

tiNIfstSasws

6

aonpotoio1cb

otttalntgtpiit

sbiitbcce

utcsmtivmlcgsKt

trptdpatscmlmabms

A

MmCFC

A

Table A2

ig. 2. Actual and model predicted values of business conduct supervision integra-ion.

This comparison suggests that implementation and integra-ion of business conduct supervision, including mechanisms forts enforcement, in countries such as USA, Austria, Cyprus, andew Zealand is much less advanced than predicted by our model.

n contrast, there are no notable over-performers pointing to theact that implementation of holistic business conduct supervi-ion and consumer finance protection is relatively new area inhe focus of policymakers. Nevertheless, some countries includingingapore, Czech Republic, Hungary, Poland, Uruguay, Kazakhstan,nd Malta showed greater tendency to address business conductupervision and consumer finance protection in a more holisticay than their country and financial sector characteristics would

uggest.

. Conclusion

This paper presents and studies a new dataset of the prudentialnd business conduct supervisory structures and their evolutionver 1999–2010 for a panel of 98 countries. We show that theumber of integrations of prudential supervision in a FSA out-aced those in a central bank: there were 14 new unificationsf prudential supervision in a FSA and five unifications in a cen-ral bank since 1999. Regarding business conduct supervision, webserved an important increase in the proportion of countries thatntroduced its enforcement over 1999–2010. Almost fifty percentf the countries that did not have business conduct supervision in999, have adopted it during the past decade. In half of the cases, thehange was accomplished by integration either in a FSA or centralank, or by adoption of the “twin peak” model.

We analyzed our panel dataset on supervisory structures usingrdered probit regressions to identify drivers behind the integra-ion of prudential and business conduct supervision. We foundhat as countries develop they tend to integrate both pruden-ial and business conduct supervision. The size and opennessffect supervisory integration. Small open economies are moreikely to integrate their prudential supervision. Integration of busi-ess conduct supervision is not influenced by country size, andrade openness shows a negative impact on integration. Publicovernance is positively related to prudential supervisory integra-ion, while greater central bank’s autonomy could hinder greater

rudential supervisory integration. Financial development is anmportant driver of supervisory integration. A larger banking sectorncreases the probability of supervisory integration, both pruden-ial and business conduct ones. Development of non-bank financial

ancial Stability 9 (2013) 428– 444 439

ubsectors, however, favors less integrated prudential supervision,ut nor business conduct one. Regarding banking sector character-

stics, higher aggregate liquidity exposures seem make countriesntegrate prudential supervision. Higher banking sector concen-ration and profitability decrease the probability of integratingusiness conduct supervision. Finally, the experience of finan-ial crises makes countries integrate both prudential and businessonduct supervision, as integrated supervisors could be betterquipped to manage systemic financial distress.

We benchmarked the actual supervisory structure of individ-al countries against the model predicted supervisory integrationo identify outliers in supervisory integration taking into accountountry typology. Considering prudential supervision, countriesuch as Luxemburg, Panama, Costa Rica, Canada, and Chile imple-ented less-integrated prudential supervisory structures vis-à-vis

he international historical benchmark. In contrast, countriesncluding Armenia, Czech Republic, Uruguay, Netherlands, Slo-akia and Poland integrated their prudential supervisory structuresore than predicted by their country and financial system typo-

ogy. Regarding business conduct supervision implementation,ountries such as USA, Austria, Cyprus, and New Zealand inte-rated less than predicted by our benchmark. In contrast, countriesuch as Singapore, Czech Republic, Hungary, Poland, Uruguay,azakhstan, and Malta were more progressive considering their

ypology.Our results have important policy implications. Based on

he lessons from the 2008 financial crisis, many countries areethinking their supervisory structures for financial services. Arominent example is the UK that has been a role model inhis area for many small open economies, both developed andeveloping. The UK is reforming the FSA by integrating micro-rudential supervision into the Bank of England, the monetaryuthority and macroprudential supervisor. At the same time,he UK is setting up an integrated, business conduct supervi-ory authority as a self-standing institution, which will haveonsumer protection among its responsibilities. We thus recom-end that, at least those countries, which appear to have much

ess integrated supervisory structures compared with our esti-ated historical benchmarks, consider integrating their prudential

s well as business conduct supervision. Moving closer to suchenchmark structure should provide a basis for further improve-ents in the quality and efficiency of their financial services

upervision.

cknowledgements

We thank Martin Cihak, the editors Iftekhar Hasan, and Donatoasciandaro, as well as the anonymous referee for helpful com-ents on an earlier draft of the paper. Financial support from the

zech Science Foundation 13-20613S “Institutional Structures ofinancial Services Supervision and Monitoring of Systemic Risk inentral Europe” is gratefully acknowledged.

ppendix.

Fig. A1Fig. A2Fig. A3Table A1

Table A3Table A4Table A5

440 M. Melecky, A.M. Podpiera / Journal of Fin

Note: Sectoral supervision — proporti on of coun tries with different supervisors foror an agency outside of the central bank; Partial integration — propo rti on of councentral bank or an agency outside of the central bank; CB inte grati on — propo rproporti on of countries with unified superv isor in an FSA.

0

10

20

30

40

50

60

70

% All Economies

CB integration FSA integration

Sect oral Supe rvision Partial Integration

0

10

20

30

40

50% High financial depth ec onomies

CB integration FSA integration

Sect oral Supe rvision Partial Integration

Fig. A1. Evolution of prudential supervision structures, 1999–2010:

0

10

20

30

40

50

60% All Economies

Partial Integration in the Cen tral Ban k

Partial Integration outs ide the Ce ntral Ban k

Sect oral Supe rvision , Ban king Supe rvision within the Ce ntral Ban kSect oral Supe rvision , Ban king Supe rvision outs ide the Ce ntral Ban k

0

5

10

15

20

25

30

35

40

45% High financial de

Partial Integration in the C Partial Integration outs ide

Sect oral Supe rvision, Ban Central Ban kSect oral Supe rvision, Ban the Ce ntral Ban k

Fig. A2. Sectoral supervision and partial integration v

Note: Inte grate d business conduct — propo rti on of coun tries where the business co

act as an integrated supervisor; The “twin peak” model — proportion of countries

of all financial servic es; Business conduct in plac e — proportion of countries

supervision or specialized agencies that oversee the protection of the financial consu

0

10

20

30

40

50

60

% All Economies

Integrated bu siness conduct

Business conduct in place

Twin pea ks

0

10

20

30

40

50

60

70

% High financial depth economies

Integrated business conduct

Business conduct in place

Twin pea ks

Fig. A3. Evolution of business conduct supervision, 1999–2010: p

ancial Stability 9 (2013) 428– 444

each type of inte rmedia ry, the banking supervision eit her in the central bank tries with two financial sectors supervised by the same insti tution, eit her the ti on of coun tries with unified supervision in the CB; FSA integration —

0

10

20

30

40

50

60

70

80

90% Low financial depth ec onomies

CB integration FSA integration

Sect oral Supe rvision Partial Integration

proportion of countries with a specific supervisory structure.

pth economies

entral Ban k

the Ce ntral Ban k

king Supe rvision within the

king Supe rvision outs ide

0

10

20

30

40

50

60

70

80% Low financial depth economies

Partial Integration in the Central Bank

Partial Integration outs ide the Ce ntral Ban k

Sect oral Supe rvision, Ban king Supe rvision within the Ce ntral Ban kSect oral Supe rvision, Ban king Supe rvision outs ide the Ce ntral Ban k

is-a-vis central bank: proportion of countries.

nduct supervision is as signed eit her to the central bank or to the FSA, whic h

that have an institution exclusively supervising business conduct in provision

that have insti tuti ons with sta tutory responsibili ties for business conduct

mers, including banking product consumers.

0

5

10

15

20

25

30

35

40

45% Low financial depth economies

Integrated bu siness conduct

Business conduct in place

Twin pea ks

roportion of countries with a specific supervisory structure.

M. Melecky, A.M. Podpiera / Journal of Financial Stability 9 (2013) 428– 444 441

Table A1Prudential and business conduct supervisory structures in 98 countries as of end-2010.

Country Prudentialsupervision

Business conduct supervision

Albania Sectoral, BSBCB NBCAlgeria Sectoral, BSBCB NBCArgentina Sectoral, BSBCB SectoralArmenia CB CBAustralia FSA TPAustria FSA NBCAzerbaijan Sectoral, BSBCB SectoralBelarus Sectoral, BSBCB NBCBelgium FSA FSAa

Bolivia FSA NBCBosnia andHerzegovina

Sectoral, BSOCB NBC

Botswana Sectoral, BSBCB The office of the bankingadjudicator

Brazil Sectoral, BSBCB NBCBulgaria PI: IS + SS, BSBCB NBCCanada PI: BS + IS OCB Financial consumer protection

agency in charge with thesupervision of the businessconduct of federally regulatedinstitutions (banks andinsurances)