institutional presentation -...

TRANSCRIPT

Institutional Presentation

This presentation may contain forward-looking statements which are inherently difficult to predict. Actual results could

differ materially for a variety of reasons. Forward-looking statements speak only as of the date they are made and the

Company does not assume any obligation to update them in light of new information or future developments.

This material is published solely for informational purposes and is not to be construed as a solicitation or an offer to buy

or sell any securities or related financial instruments. Likewise it does not give and should not be treated as giving

investment advice. It has no regard to the specific investment objectives, financial situation or particular needs of any

recipient.

No representation or warranty, either express or implied, is provided in relation to the accuracy, completeness or reliability

of the information contained herein. It should not be regarded by recipients as a substitute for the exercise of their own

judgment.

Certain percentages and other amounts included in this document have been rounded to facilitate its presentation. Thus,

numbers presented as total in some tables may not represent the arithmetic sum of the numbers that precede them and

may differ from those presented in the financial statements.

Disclaimer

2

Section 1

Camil at a Glance

4

Purpose and Values

We believe that each person can make a difference in others lives and we exist to nurture

relationships that bring more flavor to the everyday life.

Our Purpose

Our Values

TrustWe honor our commitments with seriousness and discipline. We value transparency in our relationships, and

for that, we aim to gain respect and trust.

EntrepreneurshipWe believe in those who dream with the effort and courage of who realize their dreams. This is the driving

force for entrepreneurship and growth with profitability.

EnthusiasmWe express joy, vitality and energy in our everyday life.

Therefore, we inspire people.

ResponsibilityWe prioritize ethics and high quality standards in everything we do. This way we seek to ensure the

sustainability of our business and of the environment, going beyond results.

ProximityWe build strong partnerships as a way of establishing deep lasting relationships with all stakeholders:

consumers, customers, employees and suppliers.

5

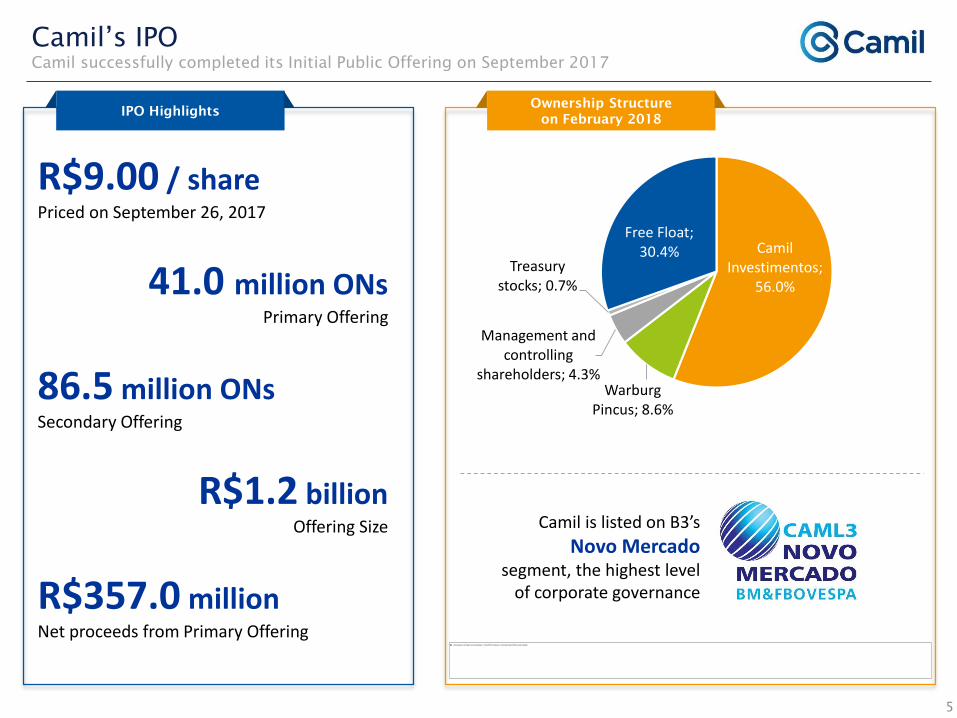

Camil’s IPO

Camil successfully completed its Initial Public Offering on September 2017

Ownership Structure

on February 2018IPO Highlights

Camil is listed on B3’s

Novo Mercado segment, the highest level

of corporate governance

R$9.00 / sharePriced on September 26, 2017

41.0 million ONs Primary Offering

86.5 million ONsSecondary Offering

R$1.2 billionOffering Size

R$357.0 millionNet proceeds from Primary Offering

Camil Investimentos;

56.0%

Warburg Pincus; 8.6%

Management and controlling

shareholders; 4.3%

Treasury stocks; 0.7%

Free Float; 30.4%

Main Brands and Segments

Leading position in all operating markets

– #1 processor and distributor of rice in Brazil (Camil brand)

– #1 processor and distributor of rice in Uruguay (Saman brand)

– #1 processor and distributor of rice in Chile (Tucapel brand)

– #1 processor and distributor of rice in Peru (Costeño brand)

– #1 player in refined sugar in Brazil (União brand)

– #1 player in the canned sardine and #2 in the canned tuna market in Brazil (Coqueiro and Pescador brands)

29 processing facilities and 18 distribution centers distributed throughout LatAm

Reaches more than 20,000 direct and 285,000 indirect sales points in Brazil

Exports to more than 50 countries

6

Camil at a Glance

Founded in 1963, Camil is a leading food company in Latin America with a diversified portfolio

of several brands in rice, beans, canned fish and sugar

Highlights

Grains Sugar Canned Fish

Leadership positioning in all segments and countries in which it operates,

Camil is one of the largest food companies in Brazil

Notes:

(1) Santa Cruz plant produces both rice and sugar

(2) Considers both plants operated by Raízen

(3) Market shares referring to total Camil Company brands

(4) Company’s market share in the Rice Market only

(5) Nielsen Retail Index – Apr17 - Mar18

(6) Comisión Sectorial del Arroz – Mar17 - Feb18. Local Internal Market Share. Export Market Share is 48% (#1 player)

(7) Nielsen Chile – Mar17 - Feb18

(8) Top of mind – Sugar Kantar Nov16 / Rice and Fish Ipsos Nov17

(9) Kantar Worldpanel Peru – Apr17 - Mar18

Processing and Distribution Platform

Rice Processing Facilities: 23 (81

in Brazil)

Fish Processing Facilities: 2

Sugar Packaging Facilities: 41,2

Distribution Centers: 18 (8 in Brazil)

Rice Producing Regions

Beans Producing Regions

Grains Sugar Fish

Brazil3 Uruguay Chile Peru

Grains

Business Divisions Overview

Brands

Market Share1st

8.1%4,5

1st

35.2%5

2nd

40.5%6

2nd

43.8%5

2nd

24.3%5

Sardine Tuna

1st

49.1%9

1st

32.9%7

Net Revenue

(Feb-18)

Facilities

Top of

Mind860% 84%

47%

Sardine

37%

Tuna

n.a. 50% 72%

EBITDA

(Feb-18)

Processing

& Packaging

8 plants

4

packing

plants

2 plants 8 plants 3 plants 3 plants

Diversification across 3 products categories

R$1,3 bi

(29% of total)

7

(Uruguay)

(Argentina)(Chile)

(Peru)

R$3,3 bi

(71% of total)

R$142 mn

(29% of total)

R$347 mn

(71% of total)

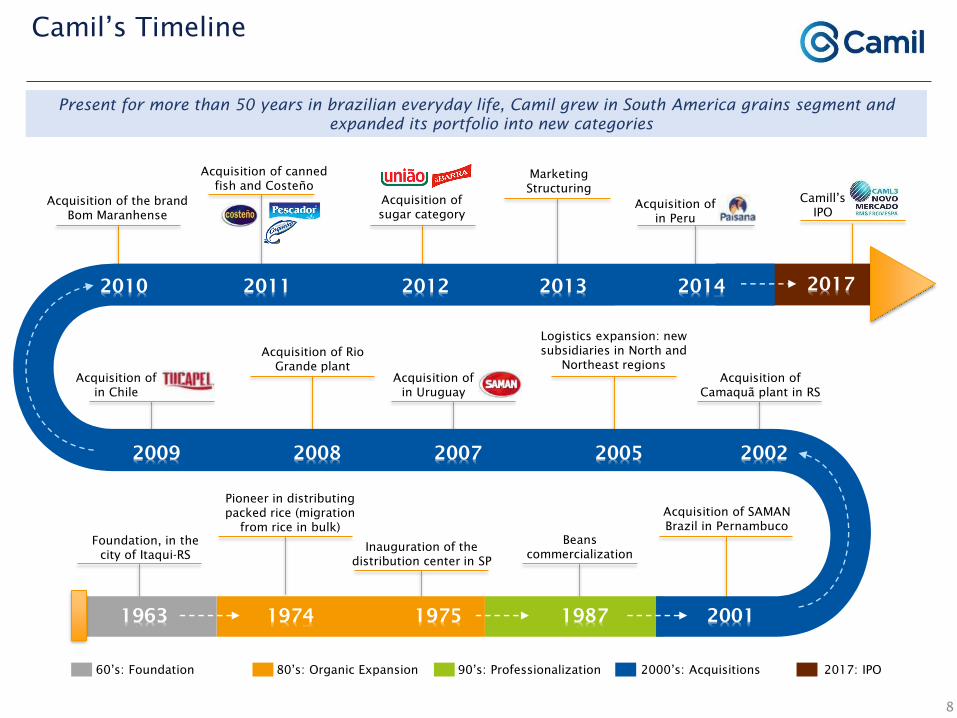

Foundation, in the

city of Itaqui-RS

1963

Pioneer in distributing

packed rice (migration

from rice in bulk)

1974

Inauguration of the

distribution center in SP

1975

Beans

commercialization

1987

Acquisition of SAMAN

Brazil in Pernambuco

2001

Acquisition of

Camaquã plant in RS

2002

Logistics expansion: new

subsidiaries in North and

Northeast regions

2005

Acquisition of

in Uruguay

2007

Acquisition of Rio

Grande plant

20082009

Acquisition of

in Chile

Acquisition of the brand

Bom Maranhense

2010 2011 2012 2013

Marketing

Structuring

2014

Acquisition of

in Peru

60’s: Foundation 80’s: Organic Expansion 90’s: Professionalization 2000’s: Acquisitions

8

Camil’s Timeline

Present for more than 50 years in brazilian everyday life, Camil grew in South America grains segment and

expanded its portfolio into new categories

2017

Camill’s

IPO

2017: IPO

Acquisition of canned

fish and Costeño

Acquisition of

sugar category

FishSugar

Grains - InternationalGrains - Brazil

9

Complementary product portfolio composed of high value

added items

Value addedBiscuits

Core

Main products across the segments that Camil operates

Notes:

(1) Considers 12 months ended on February for 2010 and 2017

(2) Market share figures for Camil as a Company for the Brazilian market

(3) Nielsen Retail Index – Apr17 - Mar18

(4) Nielsen Scantrack - Apr17 - Mar18

(5) Top of mind – Sugar Kantar Nov16 / Rice and Fish Ipsos Nov17

20101

20171

R$1,407 million

R$142 million

n.a.

R$4,663 million

R$490 million

Rice: 8.1%3

Beans: 6.8%4

Sugar: 35.2%3

Sardine: 43.8%3

Tuna: 24.3%2

2

4

5

1 Net Revenue

EBITDA

Market Share2

Top of Mind (Brazil)5

Rice: 60%

Beans: 53%

Sugar: 84%

Sardine: 47%

Tuna: 37%

Rice: n.a.

Beans: n.a.

Sugar: n.a.

Sardine: n.a.

Tuna: n.a.

10

Iconic performance supported by the creation of a leading

brand portfolio

Since its IPO attempt in 2011, Camil expanded its portfolio to the sugar and canned fish categories,

and more than tripled its revenue and EBITDA

9.9% 15.7%3 ROIC

Despite the slowdown in the Brazilian economy, Camil posted solid results maintaining EBITDA margin over +10%

Even in a challenging environment,

Camil was able to post double-digit

growth, maintaining profitability

11

Solid Business Model with Stable and Resilient Margins

Net Revenue by Segment

CAGR+15%

Camil: Net Revenue (R$mn)

EBITDA Evolution (R$mn) Net Profit Evolution (R$mn)

168,6

126,6 141,7

209,1

312,7

375,3 360,1

422,9

547,0 489,9 22,9% 23,0%

24,2%

27,1%

24,1% 24,5%23,2%

24,5% 24,7% 24,7%

11,1%

9,6% 10,1%

11,7% 11,3%10,5%

9,8% 10,0%11,1% 10,5%

R$50

R$150

R$250

R$350

R$450

R$550

R$650

12M08 12M09 12M10 12M11 12M12 12M13 12M14 12M15 12M16 12M17EBITDA Gross Margin EBITDA Margin

Net Profit Evolution (R$mn)

5874

5674

137124

105 111

202

2513,8%

5,6%

4,0% 4,1%4,9%

3,5%2,9% 2,6%

4,1%

5,4%

11,1%

9,6% 10,1%

11,7% 11,3%10,5%

9,8% 10,0%11,1%

10,5%

R$0

R$50

R$100

R$150

R$200

R$250

R$300

R$350

R$400

R$450

12M08 12M09 12M10 12M11 12M12 12M13 12M14 12M15 12M16 12M17Net Income Net Margin EBITDA Margin

R$20

R$40

R$60

R$80

R$100

R$120

R$140

R$160

R$180

CAGR+20%

CAGR+14%

Notes:

Company fiscal year begins in March and ends in February of the following year (inclusive).

24.5%23.2%

24.5% 24.7% 24.7%

941.6 1,075.2

1,293.6

1,264.5

1,331.5

2,639.9 2,600.6 2,935.3

3,683.3 3,331.4

R$800

R$1,300

R$1,800

R$2,300

R$2,800

R$3,300

R$3,800

R$4,300

R$4,800

R$5,300

12M13 12M14 12M15 12M16 12M17

Food Products Brasil Food Products International Gross Margin

Section 2

Investment Highlights

Iconic Brand Recognition… …Leading to a Leadership Position in all Sectors & Regions1

13

Brazil – RICE2

#1 8.1%

#2 Player 2 5.1%

#3 Player 3 4.5%

Peru – RICE3

#1 49.1%

#2 Player 2 5.1%

#3 Player 3 4.5%

Chile – RICE5

#1 32.9%

#2 Player 2 17.2%

#3 Player 3 (PLs) 43.5%

Brazil – REFINED SUGAR2

#1 35.2%

#2 Player 2 18.5%

#3 Player 3 12.0%

Brazil – SARDINE2

#1 Player 1 45.4%

#2 43.8%

Brazil – TUNA2

#1 Player 1 58.6%

#2 24.3%

Uruguay – RICE4

#1 48.0%

#2 Player 2 40.5%

Percentage values indicate market

share in terms of volume.

Market leader in São Paulo City:

Rice 36.2% market share

Rice: 65% Top of Mind in São Paulo

One of the most complete line of

products: More than 10 variations of

grains, including ready to eat

One of the most complete line of

products: traditional and new

segments (i.e. “Fit” sugar, Sucralose,

Naturals)

Top of Mind leader (84%)

“Top-5 Suppliers” Award (#1)

Complete line of products: Tuna,

Sardines, Tuna Sauces and Pâtés

47% Top of Mind in Sardine and

37% in Tuna

“Top-5 Suppliers” Award

(Sardine #1; Tuna #2)

Market Leader with Iconic Brand Recognition

Notes:

(1) Market shares referring to total Camil Company brands

(2) Nielsen Retail Index – Apr17 - Mar18

(3) Kantar Worldpanel – Apr17 - Mar18

(4) Comisión Sectorial del Arroz – Mar17 - Feb18. 40,5% for Local Internal Market Share (#2 player)

(5) Nielsen – Mar17 - Feb18. Player 3 includes private label volumes

União: Brand of strong emotional bond, preferred by consumers and with greater perception of value!

35.2%

72%

Unique Footprint

150,000 points of sale

reaching big part of the

population

Wide presence across all

States of Brazil

Pricing Power3

"Brand of sugar": higher

prices compared to the

main competitors³

Market Leadership Absolute Leadership

Total Company refined

sugar brands have 35%¹

market share

Unique Brand One of the most

traditional and valuable

brands in Brazil

84%² of Top of Mind

Market Share(1)

14

Sugar | Case Study

Notes:

(1) Nielsen | Retail Index – Apr17 – Mar18

(2) Top of mind – Kantar – Nov16

(3) União Refinado 1kg. Source Nielsen | Retail index – Feb/Mar18

+14%

114

100

Main Competitor

Sugar price

One of the most recognized

brands in Brazil

One of the 30 most loved brands

in 2013

1º

15

Unique

Marketing

Efforts

Innovation

Strategy and

Execution in

the POS

A

B

C

Relevant brand positioning

Powerful consumer engagement

platforms

Impactful Live marketing/

promotional initiatives

Clear Price-Portfolio Strategy

Brand leverage through culinary

programs and specialists

Sell-out Incentives:

High Visibility,

Promotions, MPOS;

Execution:

New Shopper

Experience

Brand value creation

Halo Effect on the Core Brand

Margin accreative

Improved Go-to-Market Strategy

8.1

5.14.5

3.5

Camil Player 1 Player 2 Player 3

105,2

100

Camil Others

Premium Price Compared to Competitors2SP

26%

MG

11%

RJ

10%BA

6%

RS

5%

Others

42%

National

Grains

Market

Camil is Market Leader in Brazil

Camil has 8.1%1

of

the Brazilian rice

market, which is

highly fragmented

Notes:

(1) Nielsen Retail Index - Apr17 - Mar18

(2) Nielsen Retail Index - Mar18. Considers only non-premium brands16

Market share of rice in the Brazilian market (%)

Camil's unique brand awareness leads to a

Unusual combination of market leadership and pricing power

+5,2%

Rice price in Brazil (base 100)

Rice | Case Study

17

Rice | Broad Product Portfolio

Tailored product offering for targeted consumer segments across Brazil

Premium

Uppermainstream

Mainstream

Value Priced Products

Notes:

(1) White rice price index Nielsen Retail Index - Mar18

(2) Nielsen Scantrack - Mar18

(3) Price index for Pop brand only Mar18

Avg. national prices

Avg. regional prices

95³

111 100

112

129²

Portfolio Camil¹Product Portfolio - Breakdown

Avg market

selling price

129

Avg market

selling price

111

Avg market

selling price

101

Avg market

selling price

93

Product Shelving

18

Unique Distribution Platform

36%

100%

36%

24%

4%

Key Accounts Grocery Stores Wholesales Distributors Total Sales

Selected Accounts / Retailers

Selected Wholesale Stores

Sales Breakdown per Distributors (2017)

Despite its long-standing relationship with the main Brazilian

retailers (key accounts) and wholesalers, Camil distribute 40% of its

sales through grocery stores and distributors

Grain

s

Brand

Su

gar

Fish

Production 19

Agriculture

Processing

Packing

Distribution

Marketing

Origination

Solid Business Model

–

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

100.0%

-

10.00

20.00

30.00

40.00

50.00

60.00

70.00

80.00

90.00

100.00

jan-06

set-0

6

mai-07

jan-08

set-0

8

mai-09

jan-10

set-1

0

mai-11

jan-12

set-1

2

mai-13

jan-14

set-1

4

mai-15

jan-16

set-1

6

mai-17

Since 2006, Camil maintained gross margin of 22.5% - 28.0%,

mainly due to its weekly pricing capacity

Business Model: Proven Cost Transfer Capability (rice case)

Notes:

(1) Adjusted by the monthly inflation of the period (Jan/2006 – Feb/2017)

(G

ro

ss m

arg

in

)

Average

sale price

(R$/30kg)

Average

cost

(R$/30kg)

Sale / CostGross

marginYear

2006

37.0 22.3 1.7x 25.4%

2007

39.4 22.7 1.7x 27.9%

2008

42.0 24.8 1.7x 25.9%

2009

53.9 34.2 1.6x 24.9%

2010

51.0 30.8 1.7x 24.6%

2011

50.5 28.6 1.8x 25.1%

2012

45.5 25.1 1.8x 27.2%

2013

55.8 34.4 1.6x 26.3%

2014

59.2 35.5 1.7x 22.8%

2015

63.5 36.9 1.7x 24.2%

2016

67.3 37.4 1.8x 24.5%

80.5 46.5 1.7x 24.7%

20

Solid Business Model with Stable and Resilient Margins

Subtitle

Average purchase price (CIF - R$/30kg)

Gross margin (% net revenue)Average selling price (CIF - R$/30kg)

Adjusted selling price (1)

(CIF - R$/30kg)

2005

25%

11%10%

6%5% 5%

4% 4% 4%3%

23%

SP MG RJ BA RS PR PE CE GO PA Others

Distribution of Grain Sales by Brazilian State (% value)

Metropolitan regions – expansion to countryside

Minas

Gerais

São

Paulo

High potential to consolidate leadership towards

countryside

Expansion to white areas……Coupled with consolidation of the Brazilian grains

market

Unique opportunity to consolidate the fragmented Brazilian rice market....

8.1%

5.1%4.5%

3.5%

Player 2 Player 3 Player 4

1º

…with additional expansion opportunities in the also fragmented bean market

Even in regions where it is the absolute

leader, there is still potential for

expansion as brand penetration is not

homogeneous in each state

Notes:

(1) Rice Nielsen Retail Index Apr17 - Mar18

(2) Beans Nielsen Scantrack Apr17 - Mar18 21

1

Rice

Bean

s

IV III

II

VI

I

V

36%

15%

2%

10%

1%

10%

IV III

II

VI

I

V

19%

7%

1%

2%

0,2%

7%

8.0%

6.8%

5.3%4.9%

Player 1 Player 3 Player 4

2º

Unique position to consolidate Brazilian rice and beans markets

Backed by

Private Equity

Acquisitions

history

Player 2

Player 3

Player 4

% of total rice market share1

Rice Market Share

Beans Market Share

Clear and Tangible Avenues for Expansion

VII

1%

VII

3%

Source: Camil - Considers the amounts accumulated in the 12-month period up to the highlighted date.

% of total beans market share1

22

Clear recovery opportunities in the sugar and fish markets

and expansion to new categories in South America

Consolidation in

the Fish Market in

Brazil

3

International

Geographic

Expansion

5

Entry into new markets

and long-term opportunity

for entry into new

categories Focus Regions for

Expansion

New Markets

5.4%

2.5% 1.9%

Solid Growth Perspective

Rice sales CAGR 2016-2021

ArgentinaPeru ColômbiaNotes:

(1) Bimonthly Nielsen Retail Index

Expansion to

New Categories

4

Pasta - R$8.1 billion

Coffee - R$19.7 billion

Flour- R$12.5 billion

Additional Potential Market Rated

at + R$40 billion

2%

6%

4%

88%

Pasta Coffee Farinaceous

Camil's unique

distribution network

enables products to

expand into other

growing markets

Total Market Packaged Foods

R$342bi

Market share - actual

Tuna Market Share1

(%)Sardine Market Share1

(%)

Fine Sugar Market Share Evolution1

(%)

Recovery in the

Sugar Market in

Brazil

2

Clear and Tangible Avenues for Expansion

39.7% 34.3% 34.0% 36.5% 36.1% 37.7% 40.2% 36.7% 36.2% 34.8% 34.5% 37.0% 36.0% 33.0%

Dec/Jan'16 Feb/Mar'16 Apr/May'16 Jun/Jul'16 Aug/Sep'16 Oct/Nov'16 Dec/Jan'17 Feb/Mar'17 Apr/May'17 Jun/Jul'17 Aug/Sep'17 Oct/Nov'17 Dec/Jan'18 Feb/Mar'18

43.4% 43.5% 42.1%22.6% 22.7% 22.9%

Camil record share was 25.9% in Nov 2017. Camil expects to reduce

share gap to its main competition, reaching 34.7% until 2020, which

represents an additional volume of 5 thousand tones per year

Camil record share was 45,5% in May 2017. Camil expects to reach

46.5% market share until 2020, consolidating its leadership position

with an additional volume of 10 thousand tones per year

Market Share

23

Solid Corporate Governance

Jairo Quartiero

(Chairman)

Piero

Minardi

Alain

Belda

Thiago

Quartiero

Jacques

Quartiero

José Fay

(Board Member at J.Macedo

former CEO of BRF)

Carlos Júlio

(Former CEO of Tecnisa

and HSM do Brasil)

Founding

Family

Warburg

Pincus

Independent

Members

Corporate Governance

Camil has high levels of controls and corporate governance, being supported by

independent board members for +10 years and being audited for +15 years (big 4)

Listing on Novo Mercado, highest

Corporate Governance standard at

B3

Common voting shares only

100% Tag along

2 or 20% of independent Board

Members

Minimum Free Float of 25%

OPA by fair value

Evaluation of Board of Directors,

Management, and Committees

Board of Directors

Since 2008, the Board of Directors

is responsible for general strategic

policies

2 independent Board Members

12 meetings/year on average

Election for unified terms of 2

years

Re-election is permitted.

Election date: June 2017

End of office: June 2018

24

All Camil's directors have

experience in their respective areas of expertise

25 25

Luciano Quartiero

CEO

Ex-CFO of Camil Alimentos

Post-Graduate in Finance from the University of California, USA and

MBA at IBMEC, Brazil

Graduated in Business Administration from PUC / SP, Brazil

3 23

Andréa Martins 1

Marketing Director

Former Director of the North-Northeast Business Unit at Mondelez

do Brasil Ltda.

Former General Manager of Kraft Foods Ecuador Ltd and different

positions in marketing at Kraft Foods Brasil Ltda.

Postgraduate in Business Administration from the University of

California, USA

Graduated in Social Communication from ESPM, Brazil

1 29

Pérsio Pinheiro 1

HR Director

Former Director of People, Management and Innovation Processes -

Ypê (Química Amparo)

Former Director of Organizational Development and HR

International - BRF S / A

MBA in Human Resources by FIA / USP

Graduated in Business Administration from FEA / USP

k

9 30

Previous experience in Casarin, Saman and Josapar companies in

the areas of sales and supplies

Graduated in Agricultural Engineering from Federal University

MBA FGV in Business Management and Marketing Management

André Ziglia

Supply Director

5 22

Max Sommerhauzer Vaz da Silva 1

Commercial Director

Former Commercial Director of Cosan S.A.

Former Commercial Manager and Marketing of Agricultural

Machines Jacto S.A.

Post-Graduate in Business Administration from FIA / USP

Graduated in Agronomy from Universidade Estadual Paulista UNESP

- Jaboticabal

Years of experience in Camil

Legend

Years of experience in the market

18 36

Jaime Ghisi

Logistics Director

Former Commercial Manager Mercosul Ferrovia ALL

Former Regional Superintendent of AGEF - General Warehouse

Customs Brokers

Graduated in Civil Engineering from PUC / RS, Brazil

Flavio Vargas, CFA

CFO and IR Director

Ex-CFO of Smiles S.A.

Ex-Director of Fleet and Treasury of Gol Linhas Aéreas S.A.

MBA, with honors, in Finance from NY University, Stern, EUA

Graduated in Mechanical Engineering from Escola Politécnica,

Universidade de SP, Brazil

1 20

Renato Gastaud1

LatAm Director

Former Superintendent and Industrial Director of Josapar

He has relevant experience in rice, market in which it has been

inserted for 39 years, of which 15 in Camil

Graduated in Agricultural Engineering at UFPEL / RS

15 39

Renato Costa 1

Industrial Director

Former Industrial Director of Kraft Heinz

He has relevant experience in the industrial area, having passed

through Suzano and Ambev, where for 16 years he held various

positions in logistics and management

Graduated in Mechanical Engineering from UMC and holds an MBA

in Marketing from FGV and in business management from IBMEC /

SP1 19

Notes:

(1) Non statutory directors.

Leadership with Wide Experience in the Sector…

25

Consolidated platform uniquely positioned for sustained organic growth

Camil has a consolidated and scalable distribution platform, positioning the company to leverage on the development of new segments and change in

consumers habits

8

High potential for inorganic growth

Leadership position across all segments the Company operates, coupled with its distribution platform, enabling fast and efficient integration of new

operations and capacity to capture synergies

9

Growth Avenues

Camil

Market leader with unique brand awareness4

Wide distribution network reaching close to 20k customers 5

Clear and tangible avenues for expansion and consolidation6

Seasoned management team backed by top-notch sponsorship7

Key Messages

Market

Resilient demand

The Company’s main market proves resilient to economic downturns as the consumption of rice and beans has a strong cultural appeal, being a pillar of

the Brazilians’ typical diet

1

Low exposure to fluctuations in commodities prices

The market dynamics differ materially from the general commodity market, as the quality perception and brand awareness are key factors in customers’

buying decision process

2

Weekly price pass-through

The grains and sugar retail markets present active price dynamics, with weekly price pass-through, ensuring stability of margins. The canned fish market

is going through a change in its price dynamics, in which price pass-through is becoming more frequent

3

Section 4

Financial highlights

27

Historical Financial highlights

Camil Consolidated Profitability Evolution

Notes:

Company fiscal year begins in March and ends in February of the following year (inclusive).

Profitability Evolution (R$mn)EBITDA Evolution (R$mn)

Net Profit Evolution (R$mn) Margin Profitability Evolution (% of Net Rev.)

168.6

126.6 141.7

209.1

312.7

375.3 360.1

422.9

547.0 489.9 22.9% 23.0%

24.2%

27.1%

24.1% 24.5%23.2%

24.5% 24.7% 24.7%

11.1%

9.6% 10.1%

11.7% 11.3%10.5%

9.8% 10.0%11.1% 10.5%

R$50

R$150

R$250

R$350

R$450

R$550

R$650

12M08 12M09 12M10 12M11 12M12 12M13 12M14 12M15 12M16 12M17EBITDA Gross Margin EBITDA Margin

11.1%9.6% 10.1%

11.7% 11.3% 10.5% 9.8% 10.0%11.1% 10.5%

3.8%5.6%

4.0% 4.1% 4.9%3.5% 2.9% 2.6%

4.1%5.4%

R$0

R$100

R$200

R$300

R$400

R$500

R$600

12M08 12M09 12M10 12M11 12M12 12M13 12M14 12M15 12M16 12M17

EBITDA Net Income EBITDA Margin Net Margin

22.9% 23.0%24.2%

27.1%

24.1% 24.5%23.2%

24.5% 24.7% 24.7%

11.1%

9.6% 10.1%

11.7% 11.3%10.5%

9.8% 10.0%11.1% 10.5%

3.8%

5.6%

4.0% 4.1%4.9%

3.5%2.9% 2.6%

4.1%5.4%

0%

5%

10%

15%

20%

25%

30%

12M08 12M09 12M10 12M11 12M12 12M13 12M14 12M15 12M16 12M17

Gross Margin EBITDA Margin Net Margin

5874

5674

137124

105 111

202

2513.8%

5.6%

4.0% 4.1%4.9%

3.5%2.9% 2.6%

4.1%

5.4%

11.1%

9.6% 10.1%

11.7% 11.3%10.5%

9.8% 10.0%11.1%

10.5%

R$0

R$50

R$100

R$150

R$200

R$250

R$300

R$350

R$400

R$450

12M08 12M09 12M10 12M11 12M12 12M13 12M14 12M15 12M16 12M17Net Income Net Margin EBITDA Margin

28

4Q17 and FY2017 Results

Financial Highlights

Notes:

(1) Comparisons refer to results ended on Feb 28, 2017 (4Q16 and 2016)

4Q17 Financial Highlights

Comparisons refers to 4Q16¹

R$1.1 billion Net Revenue ( -11.6%)

R$767 million Brazil Food Segment ( -18.6%)R$349 million International Food Segment ( +9.1%)

R$4.7 billion Net Revenue ( -5.8%)

R$3.3 billion Brazil Food Segment ( -9.6%)R$1.3 billion International Food Segment ( +5.3%)

R$285 million Gross Profit ( +1.6%)

25.% Gross Margin ( +3.3pp)

R$1.2 billion Gross Profit ( -5.8%)

24.7% Gross Margin (stable vs. 2016)

R$119 million EBITDA ( +21.9%)

10.7% EBITDA Margin ( +2.9pp)

R$490 million EBITDA ( -10.5%)

10.5% EBITDA Margin ( -0.6pp)

R$77 million Net Income ( +286.6%)

6,9% Net Margin ( +5.3pp)

R$251 million Net Income ( +24.4%)

5.4% Net Margin ( +1.3pp)

2017 Financial Highlights

Comparisons refers to 2016¹

29

Brazil Food Segment | Rice

4Q17 and FY2017 Results

Main

str

eam

We reviewed our pricing strategy and our product’s composition to

adjust the Company to a new market reality

Volume:

• 128.4 thousand tons on 4Q17 (-13.0%)

• 596.1 thousand tons on 2017 (-0.6%)

Raw material acquisition - average market prices:

• R$36.61/bag on 4Q17 (-25.7%)

• R$38.40/bag on 2017 (-18.6%)

Lower decrease in Camil’s gross prices vs. market prices:

• R$2.33 on 4Q17 (-11.3%)

• R$2.37 on 2017 (-8.3%)

Decrease in value priced brands volume

Increase in Camil’s brand volume

Rice Brazil – Market vs. Camil’s pricesRice prices – Brazilian Market (in R$/50kg)

Source: Esalq Senar Source: Esalq Senar, Company

Rice – Camil’s PortfolioRice – Main Highlights

The reduction in gross prices was lower than the decrease of market prices, as a result of Camil’s strategy to preserve profitability and

brand positioning in the market

Valu

e

Bra

nd

s

Notes:

(1) Comparisons refer to results ended on Feb 28, 2017 (4Q16 and 2016)

30

Brazil Food Segment | Beans

4Q17 and FY2017 Results

Beans – Camil’s PortfolioBeans – Main Highlights

Beans value priced category: distribution similar to rice

Beans Brazil – Market vs. Camil’s pricesBeans prices – Brazilian Market (in R$/60kg)

Source: Agrolink Source: Agrolink, Company

Volume:

• 16.4 thousand tons on 4Q17 (-14.9%)

• 72,4 thousand tons on 2017 (-4.7%)

Raw material acquisition - average market prices:

• R$98.90/bag on 4Q17 (-40.9%)

• R$132.13/bag on 2017 (-50.3%)

Lower decrease in Camil’s gross prices vs. market prices:

• R$3.23 on 4Q17 (-22.9%); and

• R$3.86 on 2017 (-31.9%).

Decrease in value priced brands volume

Increase in Camil’s brand volume

The reduction in gross prices was lower than the decrease of market prices, as a result of Camil’s strategy to preserve profitability and

brand positioning in the market

Main

str

eam

V

alu

e

Bra

nd

s

Notes:

(1) Comparisons refer to results ended on Feb 28, 2017 (4Q16 and 2016)

31

Brazil Food Segment | Sugar

4Q17 and FY2017 Results

The reduction in gross prices was lower than the decrease of market prices, as a result of Camil’s strategy to preserve profitability and

brand positioning in the market

União: absolute leadership with greater perception of value translated

in premium prices

Sugar – Camil’s PortfolioSugar – Main Highlights

Sugar Brazil – Market vs. Camil’s pricesSugar prices – Brazilian Market (in R$/50kg)

Source: Esalq Senar Source: Esalq Senar, Company

Volume:

• 118.0 thousand tons on 4Q17 (-5.9%)

• 541.3 thousand tons on 2017 (-2.2%)

Raw material acquisition - average market prices:

• R$60.92/bag on 4T17 (-30.6%)

• R$64.24/bag on 2017 (-25.4%)

Lower decrease in Camil’s gross prices vs. market prices:

• R$2.11 on 4Q17 (-18.9%)

• R$2.22 on 2017 (-12.5%)

Decrease in value priced brands volume

Increase in Camil’s brand volume

The reduction in gross prices was lower than the decrease of market prices, as a result of Camil’s strategy to preserve profitability and

brand positioning in the market

Main

str

eam

V

alu

e

Bra

nd

s

Notes:

(1) Comparisons refer to results ended on Feb 28, 2017 (4Q16 and 2016)

32

Brazil Food Segment | Canned Fish

4Q17 and FY2017 Results

Continued challenge of sardine and tuna fishing in the Brazilian coast resulted in record levels of imports by the industry

Pescados Brasil - Volume de Vendas Camil

8,08 8,30 9,21

14,02

7,55 6,18

10,92 11,39

39,62

36,05

0

5

10

15

20

25

30

35

40

45

1Q16 2Q16 3Q16 4Q16 1Q17 2Q17 3Q17 4Q17 2016/17 2017/18

Canned Fish – Camil’s Gross Prices (R$/kg)Canned Fish – Camil’s Volume (‘000 ton)

Source: Company Source: Company

Canned Fish – Camil’s PortfolioCanned Fish – Main Highlights

Volume:

• 11.4 thousand tons on 4Q17 (-18.7%)

• 36.1 thousand tons on 2017 (-9.0%)

2017: Raw material reached record levels of imports

Camil’s gross prices:

• R$20.92 on 4Q17 (+22.9%)

• R$19.42 on 2017 (+13.5%)

Improved industrial performance + efficiency gains from the

canned fish operations concentration at Navegantes (SC)

Main

str

eam

V

alu

e

Bra

nd

s

Notes:

(1) Comparisons refer to results ended on Feb 28, 2017 (4Q16 and 2016)

33

International Food Segment

4Q17 and FY2017 Results

We continue to present a better operational performance: the combined effect of volume growth and price increase in local currency

offset the exchange devaluation in each country we operate.

Chile

Uruguay

Production

mainly for

domestic market

Production

mainly for

domestic market

Production

mainly for export

Peru

Volume reached 143.2 thousand tons on 4Q17 (-7.6%)

and 547.8 thousand tons (+3.4%) on 2017.

Price in US$ per ton increased by 1.5% on 4Q17 and

decreased by 2.8% on 2017.

4.3% dollar exchange devaluation

Volume reached 18.3 thousand tons on 4Q17 (+3.7%)

and 75.8 thousand tons (+4.8%) on 2017.

Price in CLP per ton increased 3.7% on 4Q17 and 4.8%

on 2017.

0,2% Chilean peso exchange devaluation.

Volume reached 22.8 thousand tons on 4Q17

(+19.1%) and 94.1 thousand tons (+9.5%) on 2017.

Price in PEN per ton decreased 8,2% on 4Q17 and

4,7% on 2017.

1,4% Peruvian soles exchange devaluation

Operational Highlights - International International Operational Performance – Quarterly Evolution (‘000 ton)

International Operational Performance – Annual Evolution (‘000 ton)

Source: Company

Source: Company

Notes:

(1) Comparisons refer to results ended on Feb 28, 2017 (4Q16 and 2016)

34

Financial Results

4Q17 and FY2017 Results

Net Financial Expense (in R$mn)

2017 Liability Management

Net Financial Expenses decrease

Decrease of average market tax rate (SELIC)

Net Debt reduction (-43.7%)

o from R$1,014 million (feb/17) to R$571 milhões (feb/18)

Reduction of debt cost

o R$973 million issuance of Agribusiness Receivables

Certificate over the past months at a remuneration

interest lower than the Interbank Deposit Rate (DI).

The Company concluded its important initiatives to improve its capital structure, including the reduction of the cost of debt and

better amortization profile.

Statements (in R$ millions) 4Q17 3Q17 4Q16 4Q17 vs 4Q17 vs 2017 2016 2017 vs.

Closing Date 28-feb-18 30-nov-17 28-feb-17 3Q17 4Q16 28-feb-18 28-feb-17 2016

EBIT 96.1 105.7 77.0 -9.0% 24.9% 399.6 460.4 -13.2%

(+/-) Finacial Result (13.0) (12.6) (39.3) 3.7% -66.9% (74.4) (158.0) -52.9%

(-) Debt Interest Expense (33.6) (40.4) (62.3) -16.9% -46.0% (181.1) (224.2) -19.2%

(+) Interest Income 20.6 27.9 23.0 -26.1% -10.3% 106.7 66.2 61.2%

Pre-Tax Income 83.1 93.1 37.6 -10.7% 120.8% 325.2 302.4 7.5%

(-) Total Income Taxes (5.8) (21.2) (17.7) -72.4% -66.9% (74.5) (100.8) -26.1%

Net Income 77.3 71.9 20.0 7.5% 286.6% 250.7 201.6 24.4%

Notes:

(1) Comparisons refer to results ended on Feb 28, 2017 (4Q16 and 2016)

Appendix

Additional information

Rice Market | Market Share

Rice is the main element in Brazilians’ diet, with resilient consumption and stable production

levels

36

The rice industry in Brazil is characterized by a resilient demand based on cultural identity

Notes:

(1) Company’s Volumes / USDA

(2) Nielsen Retail Index - Apr17 - Mar18

Rice Brazil - Consumption Evolution USDA

Rice Brazil - Market Share Evolution

40%

45%

50%

55%

60%

65%

70%

75%

80%

7.200

7.400

7.600

7.800

8.000

8.200

8.400

8.600

8.800

9.000

9.200

99/00 01/02 03/04 05/06 07/08 09/10 11/12 13/14 15/16 17/18E 19/20E

Milled Rice Consumption Brasil (mn ton) % Milled Rice Cons./Prod.

4,8% 4,8%4,9%

5,2%

6,0%

6,6% 6,6%

6,3%6,5%

7,6%7,5%

3,0%

3,5%

4,0%

4,5%

5,0%

5,5%

6,0%

6,5%

7,0%

7,5%

8,0%

300

350

400

450

500

550

600

650

700

07/08 08/09 09/10 10/11 11/12 12/13 13/14 14/15 15/16 16/17 17/18E

Rice - Volume Sold (k ton) Rice - Market Share

Highlights

Large and resilient marketP

Fragmented marketP

Strong consolidation

potentialP

8.1

5.14.5

3.5

Camil Player 1 Player 2 Player 3

Rice Brazil – Consumption Evolution USDA¹Rice Brazil - Consumption Evolution USDA

Rice Brazil - Market Share Evolution

40%

45%

50%

55%

60%

65%

70%

75%

80%

7.200

7.400

7.600

7.800

8.000

8.200

8.400

8.600

8.800

9.000

9.200

99/00 01/02 03/04 05/06 07/08 09/10 11/12 13/14 15/16 17/18E 19/20E

Milled Rice Consumption Brasil (mn ton) % Milled Rice Cons./Prod.

4,8% 4,8%4,9%

5,2%

6,0%

6,6% 6,6%

6,3%6,5%

7,6%7,5%

3,0%

3,5%

4,0%

4,5%

5,0%

5,5%

6,0%

6,5%

7,0%

7,5%

8,0%

300

350

400

450

500

550

600

650

700

07/08 08/09 09/10 10/11 11/12 12/13 13/14 14/15 15/16 16/17 17/18E

Rice - Volume Sold (k ton) Rice - Market Share

Rice Brazil – Market Share Evolution¹

Rice Brazil – Market share of rice in the Brazilian market (%)

141.0

105.2

45.0

11.7 2.1 1.0 0.1

135.0

77.7

69.2 65.1

39.9

12.4 12.0 8.6

11.6 11.8 12.1 12.4

10.6

12.1

11/12 12/13 13/14 14/15 15/16 16/17E

Per capita Consumption by Country1

Notes:

(1) OECD, FAO and CONAB/ Average of 2013 and 2015 figures

(2) Rice husk represents ~32% of the grain’s total weight

11.7 12.6

12.0 11.5 11.4 11.5

11/12 12/13 13/14 14/15 15/16 16/17E

Industry Overview | Rice

Rice is the main element in Brazilians’ diet, with resilient consumption and stable production

levels

Largest Producers in the World1

Ton mm

National Production

Ton mm

World’s 9th

largest rice producer

China India Indonesia Peru Uruguay Chile

9º

Brazil

kg/year

Indonesia China India Peru Brazil USA Chile Uruguay

National Consumption of Paddy2

Ton mm

Rice is highly penetrated in Brazil, being part of the country’s

cultural identity

37

Consumption Historically Stable

Production Historically Stable

The rice industry in Brazil is characterized by a combination of (i) resilient demand based on cultural identity

and (ii) high and stable production levels

Rice Market | Historical Crop Data

Rice is the main element in Brazilians’ diet, with resilient consumption and stable production

levels

38

The rice industry in Brazil is characterized by a resilient demand based on cultural identity

Rice Brazil - Long Term Market (in R$/50kg) Rice Brazil - Long Term - Market vs. Camil

Rice Brazil - Prices per Crop (in R$/50kg) Rice Brazil - Supply vs. Consumption Evolution

18,0

22,0

26,0

30,0

34,0

38,0

42,0

46,0

50,0

54,0

Mar-07 Mar-08 Mar-09 Mar-10 Mar-11 Mar-12 Mar-13 Mar-14 Mar-15 Mar-16 Mar-17

Rice Brazil Average +1 STDV -1 STDV

1,20

1,40

1,60

1,80

2,00

2,20

2,40

2,60

2,80

18,0

22,0

26,0

30,0

34,0

38,0

42,0

46,0

50,0

fev-07 fev-08 fev-09 fev-10 fev-11 fev-12 fev-13 fev-14 fev-15 fev-16 fev-17 fev-18

Cam

il -

Pre

ço B

ruto

(R

$/kg

)

Pre

ço A

rro

z -

Esal

q S

en

ar (

RS/

50kg

)

Brazil - Rice Price Camill - Gross Price

26,0

28,0

30,0

32,0

34,0

36,0

38,0

40,0

42,0

44,0

46,0

48,0

50,0

52,0

Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb

2012/13 2013/14 2014/15 2015/16 2016/17 2017/18 Average

10.000

10.500

11.000

11.500

12.000

12.500

13.000

13.500

14.000

00/01 01/02 02/03 03/04 04/05 05/06 06/07 07/08 08/09 09/10 10/11 11/12 12/13 13/14 14/15 15/16 16/17 17/18E

mn

to

n

Production (mn ton) Consumption Brasil (mn ton)Notes:

Source: Conab, Esalq Senar and Company

Rice Market | Historical Crop Data

Rice is the main element in Brazilians’ diet, with resilient consumption and stable production

levels

39

The rice industry in Brazil is characterized by a resilient demand based on cultural identity

Rice Brazil - Production and Area Rice Brazil - Production Area vs. Productivity Evolution

Rice Brazil - Consumption vs. Production Evolution Rice Brazil - International Trade Evolution

1.000

2.000

3.000

4.000

5.000

6.000

7.000

1.800

2.800

3.800

4.800

5.800

6.800

7.800

76/77 81/82 86/87 91/92 99/97 01/02 06/07 11/12 16/17

Pro

du

tivi

dad

e (k

g/h

a)

Áre

a (h

a)

Brazil - Planted Area Rice (ha) Brazil - Rice Productivity (kg/ha)

1.500

2.000

2.500

3.000

3.500

4.000

10.000

10.500

11.000

11.500

12.000

12.500

13.000

13.500

14.000

99/00 01/02 03/04 05/06 07/08 09/10 11/12 13/14 15/16 17/18E

Production (mn ton) Planted Area (ha)

10.000

11.000

12.000

13.000

14.000

15.000

16.000

99/00 01/02 03/04 05/06 07/08 09/10 11/12 13/14 15/16 17/18E

Consumption Brasil (mn ton) Supply Brasil (mn ton)

0

500

1.000

1.500

2.000

2.500

99/00 01/02 03/04 05/06 07/08 09/10 11/12 13/14 15/16 17/18E

Import (mn ton) Export (mn ton)Notes:

Source: Conab, Esalq Senar and Company

0.9 0.9

1.0 1.1

0.9

1.1

11/12 12/13 13/14 14/15 15/16 16/17E

Notes:

(1) CONAB; Agrolink; 15/16 crop registered significant drop in productivity due to rainfall scarcity during the period40

0.00

100.00

200.00

300.00

400.00

500.00

Jul-07 Jul-09 Jul-11 Jul-13 Jul-15 Jul-17

2.9 2.8

3.53.2

2.5

3.3

11/12 12/13 13/14 14/15 15/16 16/17E

1

CAGR09/10-16/17E: 2.2%

National Production

Ton mm

Average Productivity

Ton/hectare

3 annual crops in Brazil and only 1 in other producing countries

Price volatility due to beans perishability

Historical Price

R$/60 Kg sack

National Consumption

Ton mm

3.53.3 3.4 3.4

2.8

3.4

11/12 12/13 13/14 14/15 15/16 16/17E

Consumption Historically Stable

Production Historically Stable

With stable production levels, the beans market in Brazil are characterized by a combination of: (i) resilient

demand based on cultural identity and (ii) supply stability

Industry Overview | Beans

Beans are also one of the main elements in Brazilian’s diet

11.6 11.0

21.3

3.4 2.8 3.4

2014 2015 2016

Sales (R$ bn) Volume (ton mm)

Notes:

(1) CONAB and Nielsen/ Considers average sales price in accordance to Nielsen data

(2) Stores with over 4,000 sqm of sales area

(3) Stores with 1,000 sqm to 4,000 sqm of sales area

(4) Stores with less than 1,000 sqm of sales area

(5) Beans Nielsen Scantrack Apr17 - Mar18

National Beans Sales

41

Industry Overview | Beans (cont’d)

Beans market with future growth perspectives

Highlights

Large and resilient marketP

Fragmented marketP

Strong consolidation

potentialP

CAGR14-16

(Sales): 35.3%

CAGR14-16

(Volume): 0.0%

R$ bi; Ton mm

The beans market is still very fragmented, mainly due to the producers fragile distribution structure

1

Market Share (in volume)

Beans Industry Market Share5

18.3%

57.6%

24.1%

Retail Beans Distribution

% of volume

Hypermarkets2

Supermarkets3

Neighborhood4 8.0%

6.8%

5.3%4.9%

Player 1 Player 3 Player 4

2º

58 57 5754

50

40 39 39 37

21

Cuba Australia Brazil Guatemala European

Union

South

Africa

Mexico Colombia Tailand Global

Median

39.2

21.9

16.5

10.0 9.58.0

6.6 6.1 6.0 5.1

Brazil India European

Union

Tailand China United

States

Mexico Russia Pakistan Australia

Notes:

(1) USDA; CONABT/ Average between 2013 and 2015

(2) Considers consumption of industrialized products 42

Industry Overview | Sugar

Brazil is the largest producer and exporter of sugar in the world, also being one of the largest

consumers

CAGR05/06-17/18E: 3,2%

Per Capita Consumption1

kg/year

National Consumption2

Ton mm

Largest Producers in the World1

Ton mm

National Production

Ton mm

Largest producer in the world

1º

Brazil is one of the largest sugar consumers in the world

11,2 11,3 11,410,9 10,9 11,0

12/13 13/14 14/15 15/16 16/17E 17/18E

38,3 37,935,6

33,5

38,7 38,7

12/13 13/14 14/15 15/16 16/17E 17/18E

Production Historically Stable

Consumption Historically Stable

Brazil has a leading position in sugar production and consumption, presenting: (i) resilient demand and (ii)

supply stability

2.52.6

3.6

1.3 1.4 1.3

2014 2015 2016

Sales (R$ bn) Volume (ton mm)

Notes:

(1) Nielsen; Sales and volume in accordance to Nielsen data

(2) 2016 data

(3) Nielsen | Retail Index – Apr17 – Mar18

Industry Overview | Sugar (cont’d)

The retail sugar market in Brazil is highly concentrated, with small players facing difficulties due

to high indebtedness levels

National Refined Sugar Sales1

43

Highlights

Large and resilient marketP

Highly concentrated

marketP

Strengthening of Camil's

positioningP

Retail Sugar Distribution2

% do volume Market Share (em volume)

Refined Sugar Industry Market Share3,4

47.9%

21.9%

20.5%

9.7%

CAGR14-16

(vendas): 20.8%

CAGR14-16

(volume): (0.8%)

R$ bi; Ton mm

In Brazil, the sugar market is still: (i) wide, (ii) resilient and (iii) highly concentrated

Supermarkets

(+10 checkouts)

Small retail

(5-9 checkouts)

Neighborhood

(1-4 checkouts)

Traditional retail

(mom-and-pop)

35.2%

72%

Absolute Leadership

Total Company refined sugar brands have 35%¹ market share

1º

Notes:

(1) IBGE; ABPA; ABIEC; FAO; Euromonitor/ In 2015

(2) 2013 data 44

Industry Overview | Fish

The fish industry in Brazil is consistently growing, driven by the trend of the diversification of protein

sources and increase in the consumption of food with higher nutritional value

Total Brazil production: 483.2 thousand tons1

1.4%

1.8%

2.1%

4.0%

Pork

Beef

Poultry

Fish

1st - Rondônia

3rd - Mato Grosso

1.5321.622

1.745

1.893 1.933 1.967

2011 2012 2013 2014 2015 2016

65.5

37.933.5

25.522.0 21.5 20.8

13.29.7

7.5

19.7

Hong

Kong

China France Italy Peru United

States

United

Kingdom

Chile Brazil Uruguay Global

Median

2nd - ParanáMain producers

Per Capita Consumption2

National Production Per Capita Protein Consumption Growth

CAGR 09-13

(%)

kg/year

National Sales

Ton ‘000

Wide space to increase penetration Strong growth in the last years

Fish protein in Brazil still has low penetration levels, but with high growth rates

0.7 0.8 0.8

25.728.0 27.7

2014 2015 2016

Sales (R$ bn) Volume (ton '000)

1.8 1.9 2.0

84.6 88.8 89.3

2014 2015 2016

Sales (R$ bn) Volume (ton '000)

45

Industry Overview | Fish (cont’d)

Concentrated market with strong growth potential

Notes:

(1) Nielsen; Sales and volume in accordance to Nielsen data

(2) 2016 data

(3) Bimonthly Nielsen Retail Index

National Preserve Sardine and Tuna Sales1

Highlights

Market with high

expansion potentialP

Highly concentrated

marketP

Strengthening of Camil's

positioningP

% do volume Market Share (volume)

Preserved Fish Industry Market Share3

CAGR14-16

(Sales): 6.0%

CAGR14-16

(Volume): 2.8%

R$ bi; Ton ‘000

Retail Preserved Fish Distribution2

In Brazil, the fish market has high potential for expansion and is highly concentrated

CAGR14-16

(Sales): 9.0%

CAGR14-16

(Volume): 3.7%

Sardine Tuna

Supermarkets

(+10 checkouts)

Small retail

(5-9 checkouts)

Neighborhood

(1-4 checkouts)

Traditional retail

(mom-and-pop)

31.7%

16.2%30.4%

21.7%

Sardine

59.1%18.5%

17.1%5.3%

Tuna

Tuna Market Share (%)

Sardine Market Share (%) 43.4% 43.5% 42.1%

22.6% 22.7% 22.9%

Camil record share was 25.9% in Nov 2017. Camil expects to reduce

share gap to its main competition, reaching 34.7% until 2020, which

represents an additional volume of 5 thousand tones per year

Camil record share was 45,5% in May 2017. Camil expects to reach

46.5% market share until 2020, consolidating its leadership position

with an additional volume of 10 thousand tones per year

Flavio Vargas

Chief Finance and IR Officer

Guilherme Salem

IR and Financial Planning

Investor Relations

Phone:

+55 11 3039-9238

+55 11 3039-9237

E-mail: [email protected]