insights from m & a survey 2016-17 - knav - home...

TRANSCRIPT

Insights fromM & A Survey 2016-17

Presented by

Vaibhav ManekPartner, Business Advisory Services

29-30 June 2017

• Key drivers for M&A

• Global M&A Overview

• Sectors for M&A in 2017

• Case studies

M & A Insights 2017

Key drivers for M&A

• Market share expansion

• Acquisition of new technology/intellectual properties close second

• Product portfolio enhancement ranked third most important

• Consolidation of competition and backward/forward integration complete the top 5 drivers

Market share expansion

Select deals

Acquisition of technology/intellectual properties

4

$ 300mn $ 70mn

$ 54mn

$ 130mn

$ 50mn

$ 26.2 bn

Select deals

Enhancing product portfolioConsolidation of competition

$ 13.6 Bn.

$ 66 Bn.

$ 14 Bn.

$ 1 Bn.

$ 19 Bn.

$ 382 mn.

• Get skills or technologies faster or at lower cost than they can be built:

• Amazon’s 2017 acquisition of Whole Foods for USD 14 Bn.

• to expand their product portfolio faster at lower prices

• access to new fancier grocery options such as fruits and vegetables

• Exploit a business’s industry-specific scalability:

• For instance, the cost to develop a new car platform is enormous, so auto companies try to minimize the

number of platforms they need. The combination of Volkswagen, Audi, Skoda & Porsche allows all these

companies to share common platforms

• Pick winners early and help them develop their businesses:

• Johnson & Johnson pursued this strategy in its early acquisition of orthopedic-device manufacturer DePuy,

when DePuy had revenues of $900 mn. In 10 years, DePuy’s revenues had grown to $5.6 bn (17% CAGR).

Strategic rationale behind acquisitions globally

Strategic rationale behind acquisitions globally

• Improve the target company’s performance: Google’s acquisition of Android and YouTube gave these

targets Google’s reach and interlinked ecosystem to boost their growth;

• Consolidate to remove excess capacity from industry: Flipkart’s acquisition of Myntra and Jabong to

consolidate its capacity and market share in fashion e-tailing and gain from its scale of operations – today it

enjoys 75% market share in India

• Accelerate market access for the target’s (or buyer’s) products:

• IBM between 2010 and 2013, acquired over 30 companies for an average of $350 mn each.

• IBM’s global sales force was successfully leveraged and it was able to accelerate the acquired

companies’ revenues, sometimes by more than 40% in the first two years after each acquisition.

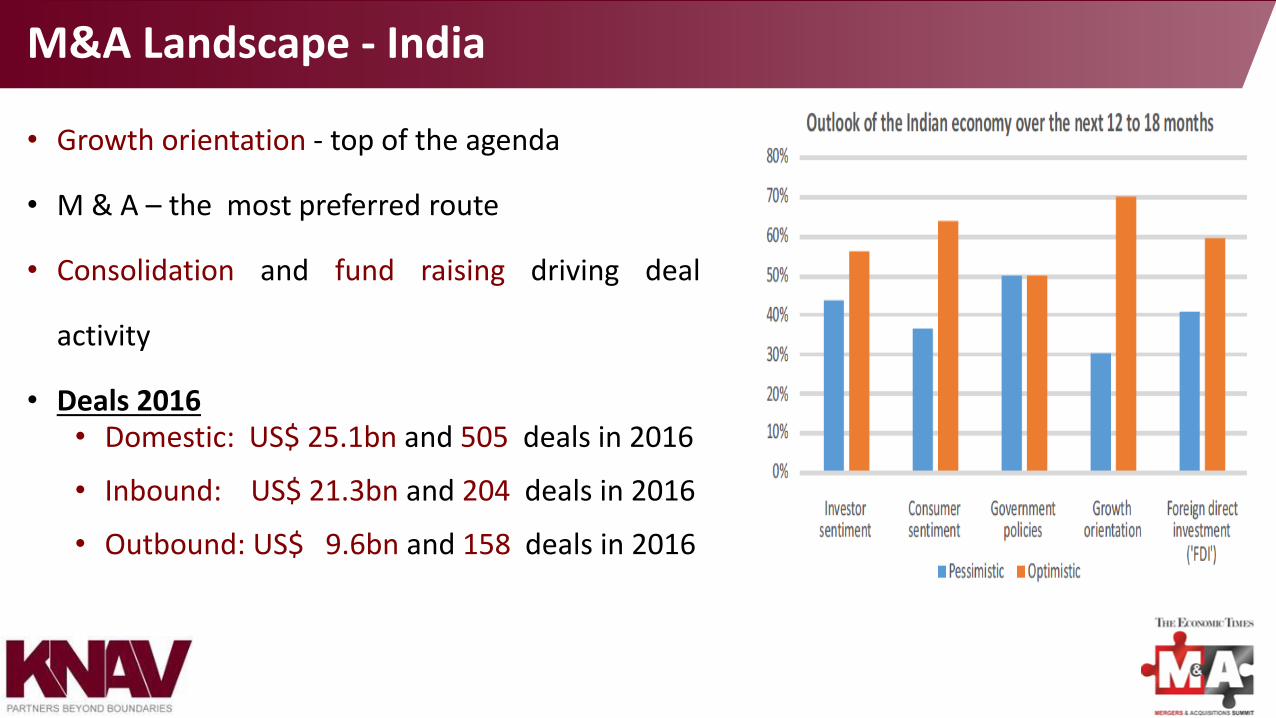

• Growth orientation - top of the agenda

• M & A – the most preferred route

• Consolidation and fund raising driving deal

activity

• Deals 2016• Domestic: US$ 25.1bn and 505 deals in 2016

• Inbound: US$ 21.3bn and 204 deals in 2016

• Outbound: US$ 9.6bn and 158 deals in 2016

M&A Landscape - India

• Most active cross-border countries for M & A with India:

• USA: 50 Inbound 43 Outbound

• UK: 21 Inbound 23 Outbound

• Singapore: 16 Inbound 8 Outbound

• Focus of companies to harness the growth potential of new & disruptive technologies

• Restructuring and consolidation of businesses of global conglomerates to focus on key areas and spin off

or divest non core businesses

• Current modest global GDP growth trend - regulatory uncertainty persists in 2017

Global M&A Overview

Top sectors for M&A in 2017

Technology 22%

Manufacturing 15%

Media & Entertainment

10%

Health & Life sciences 9%

Energy 8%

Cross Border M&A – Inbound & Outbound

• Indian investors have been focused on developed markets seeking :

o new technologies

o establishing a business reputation in developed markets

o expand customer base & geographic reach

• Indian investors for strategic reason are exploring emerging markets like South

America, African countries, Middle East, ASEAN countries.

• US continues to be the most active cross-border partner along with Japan.

• Radical regulatory changes in FDI policy for real estate, defence and civil aviation

• GST regime will generate and unleash higher growth over next 2-3 years.

• Technology, pharmaceutical and infrastructure were the most active sectors for M&A activity in terms of value and count

• Radical changes in the FDI policy under the automatic approval route supported inbound M&A

• Social, mobile, analytics and cloud (SMAC) solutions have ensured a high deal volume in the technology space

• Post demonetization - ‘Digital Economy’ boom

• Inbound activity in the insurance sector, post easing of the FDI cap to 49% from 26%

Deal Tracker FY 16-17KNAV Deal Tracker analysis for FY16-17 showcases:

28

4439

68

0

20

40

60

80 Number of transactions

6978

4078

1768

2520

0

2000

4000

6000

8000

Transaction size (in USD Mn)

• Hailed as a significant development that paves path for consolidation in

the banking sector in India

• Benefits include:

• a combined treasury will perform better

• lower cost of deposits will boost margins

• Better costs management—the cost-to-income ratio can reduce by

almost 100 basis points (bps).

• Deal Challenges include:

• related to human resources.

• associate banks with stressed balance sheets

• 5 banks have a higher share of restructured loans than SBI, while

non-performing assets being at par.

SBI Merger

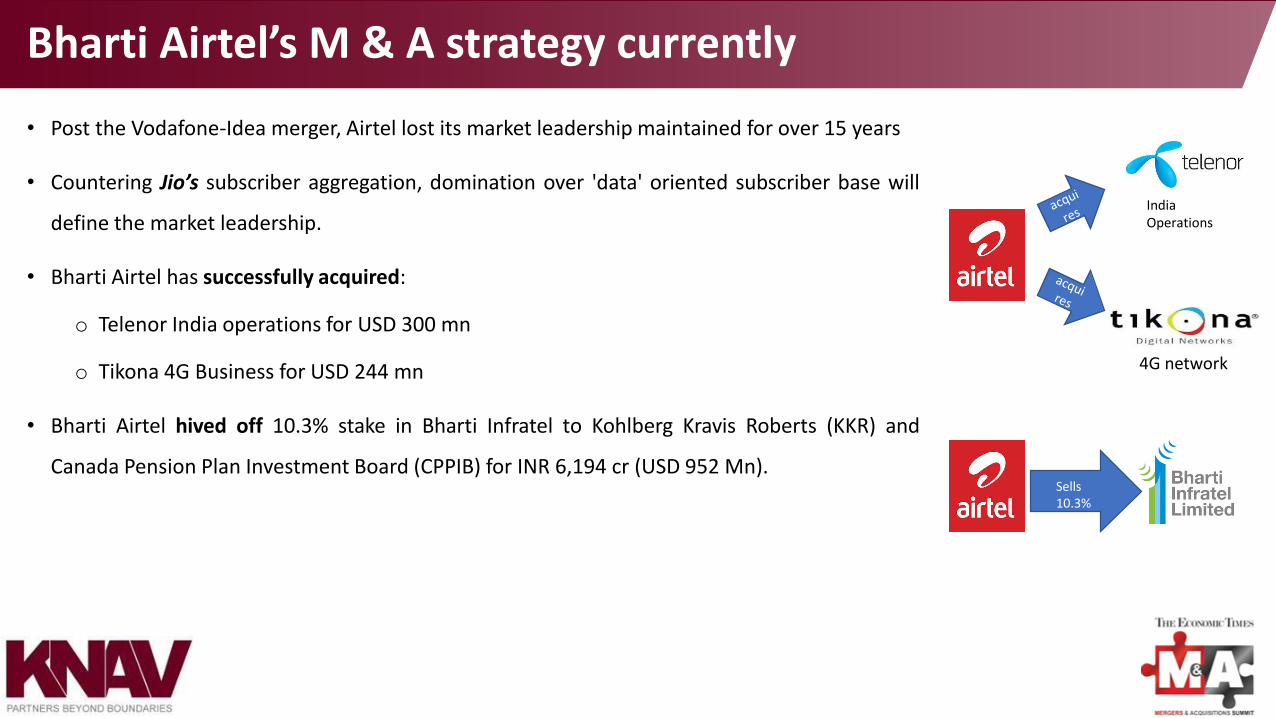

• Post the Vodafone-Idea merger, Airtel lost its market leadership maintained for over 15 years

• Countering Jio’s subscriber aggregation, domination over 'data' oriented subscriber base will

define the market leadership.

• Bharti Airtel has successfully acquired:

o Telenor India operations for USD 300 mn

o Tikona 4G Business for USD 244 mn

• Bharti Airtel hived off 10.3% stake in Bharti Infratel to Kohlberg Kravis Roberts (KKR) and

Canada Pension Plan Investment Board (CPPIB) for INR 6,194 cr (USD 952 Mn).

Bharti Airtel’s M & A strategy currently

India Operations

4G network

Sells 10.3%

• Havells India has acquired white goods and electronics business of Lloyd

Electrical and Engineering Ltd for a value of USD 230 mn.

• Lloyd’s 12% market share in the air conditioners industry gives access into the

white goods segment.

• Havells’ core business — switchgears — was facing problems on volume

& profitability fronts; and with onset of summer and monsoon, white goods

like air conditioners and refrigerators were expected to drive the sales.

• Lloyd is expected to utilise the net proceeds from sale to partially bring down

the debt and for investments in its other interests.

Havells’ acquisition of white goods business of Lloyd

White Goods Business

Acq

uires

© 2017 KNAV All rights reserved

Content

Our offices:

Vaibhav ManekPartner – Business Advisory ServicesMob:+91 98676 70620Email: [email protected]

We would be delighted to answer any questions

Thank you

16

Amsterdam | WTC Amsterdam, Strawinskylaan 925, 1077XX Amsterdam

Atlanta | One Lakeside Commons, Suite 850, 990 Hammond Drive NE, Atlanta, GA 30328

Geneva | Rue du Rhone 114, 1204 Geneva

Hyderabad | 402, Moghul's Court, Basheerbagh, Hyderabad - 500 001

London | Kajaine House, 57-67 High Street, Edgware, Middlesex, HA8 7DD

Lyon | 74 Rue Maurice Flandin 69003 Lyon

Mumbai | 303, OIA House, 470 Cardinal Gracious Road, Andheri East, Mumbai, Maharashtra 400099

New Delhi | 220 & 221, Square One Building, Saket, New Delhi 110017

Singapore | 71 Ubi Crescent, Excalibur Center, #08-0, Singapore 408571

Toronto | 55 York Street, Suite 401, Toronto, Ontario, M5J 1R7