insecurity, inequality and the labour … inequality and the labour market ... inquiry clerks 95.9...

TRANSCRIPT

INSECURITY, INEQUALITY AND THE LABOUR MARKET

PRESENTATION TO JOBS AUSTRALIA CONFERENCE

HOTEL GRAND CHANCELLOR, HOBART – 2ND NOVEMBER 2017

It’s widely believed that robots, artificial intelligence, ‘big data’, machine learning etc will lead to mass unemployment

2

Carl B. Frey

Michael Osborne

One very widely-quoted study seeks to estimate the probability of each of 702 different

occupations being replaced by computers, robots or algorithms based on an

assessment of the capacity for the tasks undertaken by each occupation ‘to be

performed by state-of-the-art computer-controlled equipment’, and the existence or

otherwise of ‘bottlenecks’ to computerization

(social perceptiveness,negotiation, persuasion, assisting & caring for others)

(originality, fine arts)

(finger dexterity, manual dexterity, working in cramped spaces or awkward positions)

Source: Carl Frey & Michael Osborne, The Future of Employment: How Susceptible are Jobs to Computerization, Oxford Martin School,

University of Oxford, September 2013.

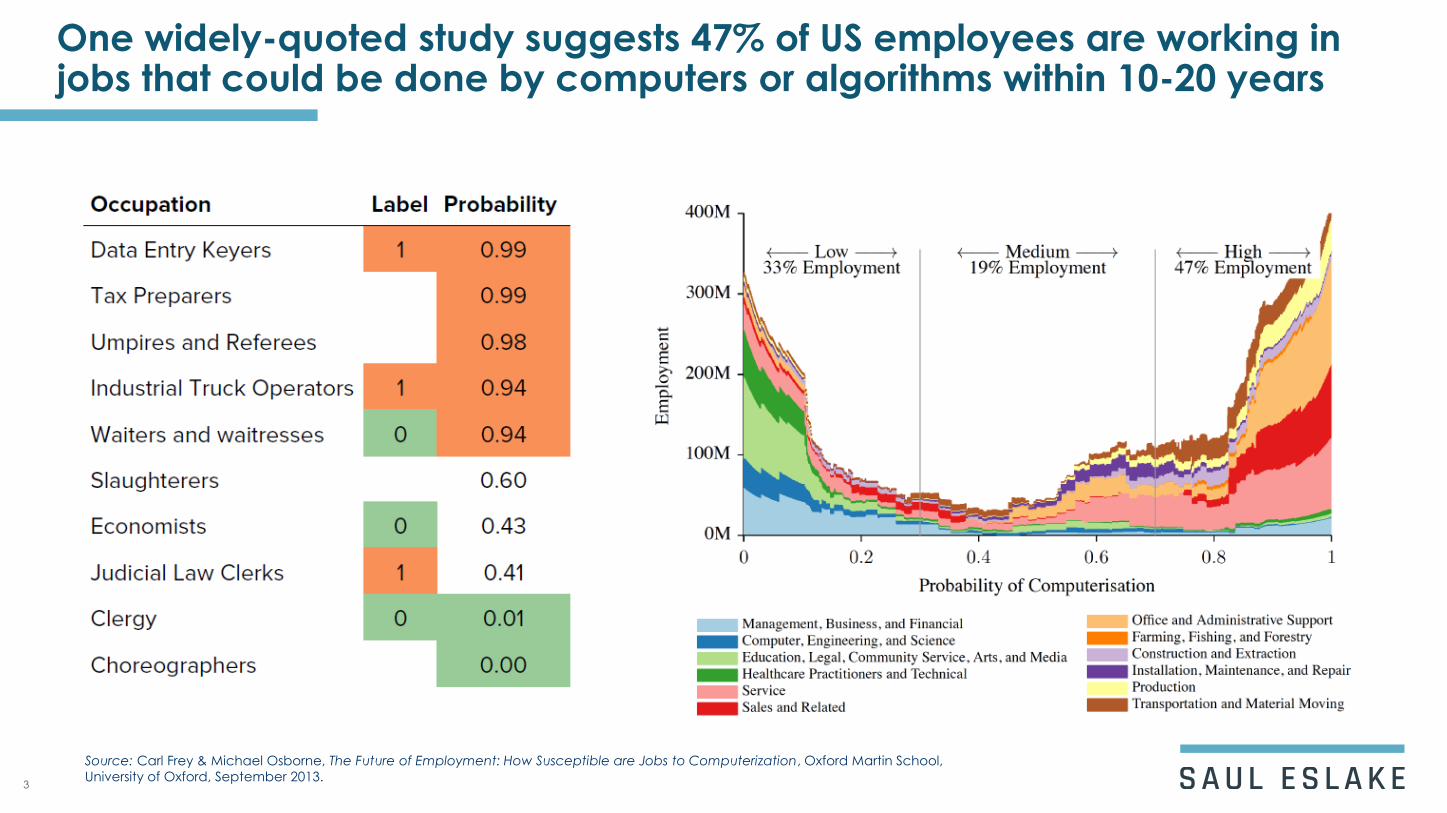

One widely-quoted study suggests 47% of US employees are working in jobs that could be done by computers or algorithms within 10-20 years

3

Source: Carl Frey & Michael Osborne, The Future of Employment: How Susceptible are Jobs to Computerization, Oxford Martin School,

University of Oxford, September 2013.

The same framework has been used to suggest that 40% of Australian jobs could be lost to computerisation or automation in the next 10-15 years …

4

Source: Hugh Durrant-Whyte et al, ‘The impact of computerisation and automation on future employment’, in Committee for the

Economic Development of Australia (CEDA), Australia’s Future Workforce?, June 2015.

… or that the proportion of jobs ‘at risk’ could even be as high as 44%

5

Source: Daniel Edmonds and Timothy Bradley, Mechanical boon: will automation advance Australia?, Research Paper 7/2015, Office of the Chief

Economist, Australian Department of Industry, Innovation and Science, October 2015.

20 highest automation scores 20 lowest automation scores

Occupation Automation

score

Occupation Automation

score

Telemarketers 99.0 Dietitians 0.4

Bank workers 97.8 Hotel managers 0.4

Bookkeepers 97.7 Education advisers 0.4

Accounting clerks 97.2 Psychologists 0.5

Product quality 97.0 Dental practitioners 0.5

Payroll clerks 97.0 Speech professionals 0.6

Checkout operators 96.9 Education managers 0.7

Other clerical workers 96.7 School principals 0.7

Insurance investigators 96.6 ICT business analysts 0.7

Library assistants 96.3 Secondary teachers 0.8

Other sales assistants 96.2 Podiatrists 0.8

Switchboard operators 96.1 Occupational therapists 0.8

General clerks 96.0 Chiropractors 0.8

Inquiry clerks 95.9 Special educ. teachers 1.1

Secretaries 95.4 Agricultural scientists 1.1

Product assemblers 95.2 Pharmacists 1.2

Keyboard operators 95.1 Ministers of religion 1.3

Jewellers 95.0 ICT trainers 1.4

Debt collectors 95.0 Training professionals 1.4

Garden labourers 95.0 Office managers 1.4

0

5

10

15

20

25

30

1 2 3 4 5 6 7 8 9 10

Pe

rce

nta

ge

of

lab

ou

r m

ark

et

Automation score decile

Australia

US

Top and bottom 20 occupations, by

automation susceptibility, 2014

Distribution of Australian and US jobs by

susceptibility to automation 44% of Australian jobs

have high (>70%)

probability of being

automated in next

10-15 years

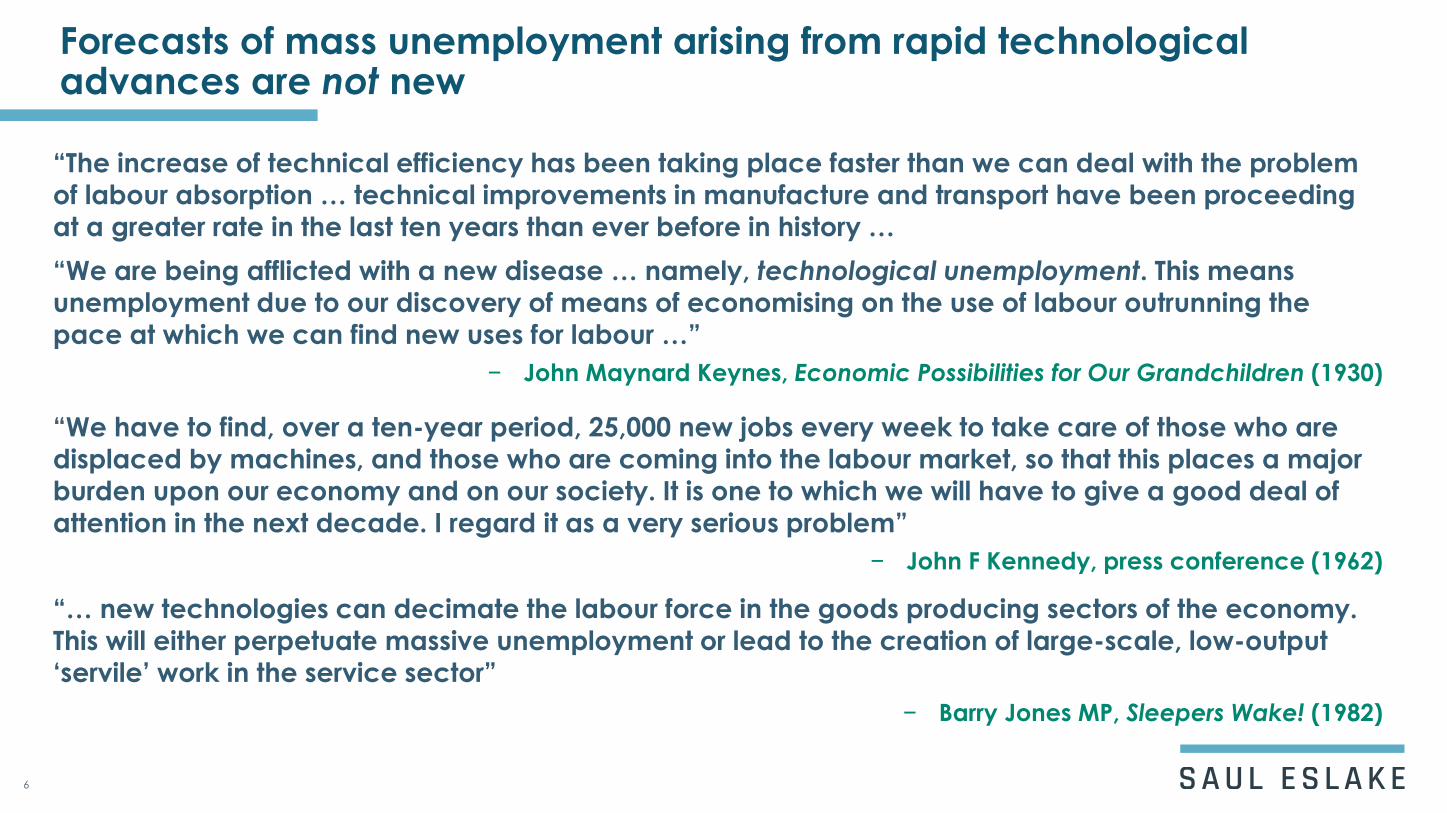

Forecasts of mass unemployment arising from rapid technological advances are not new

6

“The increase of technical efficiency has been taking place faster than we can deal with the problem

of labour absorption … technical improvements in manufacture and transport have been proceeding

at a greater rate in the last ten years than ever before in history …

“We are being afflicted with a new disease … namely, technological unemployment. This means

unemployment due to our discovery of means of economising on the use of labour outrunning the

pace at which we can find new uses for labour …”

− John Maynard Keynes, Economic Possibilities for Our Grandchildren (1930)

“We have to find, over a ten-year period, 25,000 new jobs every week to take care of those who are

displaced by machines, and those who are coming into the labour market, so that this places a major

burden upon our economy and on our society. It is one to which we will have to give a good deal of attention in the next decade. I regard it as a very serious problem”

− John F Kennedy, press conference (1962)

“… new technologies can decimate the labour force in the goods producing sectors of the economy.

This will either perpetuate massive unemployment or lead to the creation of large-scale, low-output

‘servile’ work in the service sector”

− Barry Jones MP, Sleepers Wake! (1982)

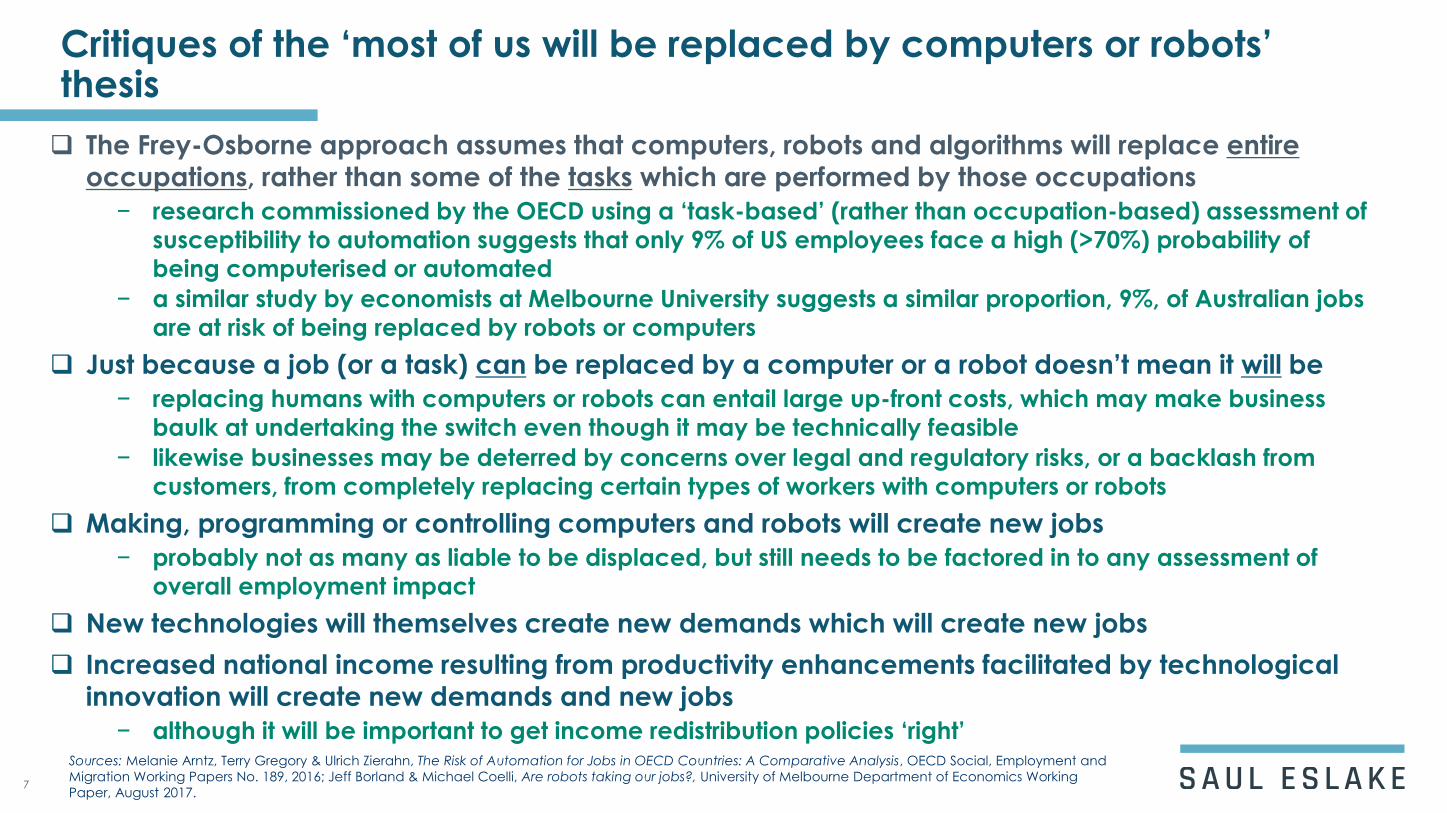

Critiques of the ‘most of us will be replaced by computers or robots’ thesis

7

The Frey-Osborne approach assumes that computers, robots and algorithms will replace entire

occupations, rather than some of the tasks which are performed by those occupations

− research commissioned by the OECD using a ‘task-based’ (rather than occupation-based) assessment of

susceptibility to automation suggests that only 9% of US employees face a high (>70%) probability of

being computerised or automated

− a similar study by economists at Melbourne University suggests a similar proportion, 9%, of Australian jobs

are at risk of being replaced by robots or computers

Just because a job (or a task) can be replaced by a computer or a robot doesn’t mean it will be

− replacing humans with computers or robots can entail large up-front costs, which may make business

baulk at undertaking the switch even though it may be technically feasible

− likewise businesses may be deterred by concerns over legal and regulatory risks, or a backlash from

customers, from completely replacing certain types of workers with computers or robots

Making, programming or controlling computers and robots will create new jobs

− probably not as many as liable to be displaced, but still needs to be factored in to any assessment of

overall employment impact

New technologies will themselves create new demands which will create new jobs

Increased national income resulting from productivity enhancements facilitated by technological

innovation will create new demands and new jobs

− although it will be important to get income redistribution policies ‘right’Sources: Melanie Arntz, Terry Gregory & Ulrich Zierahn, The Risk of Automation for Jobs in OECD Countries: A Comparative Analysis, OECD Social, Employment and

Migration Working Papers No. 189, 2016; Jeff Borland & Michael Coelli, Are robots taking our jobs?, University of Melbourne Department of Economics Working

Paper, August 2017.

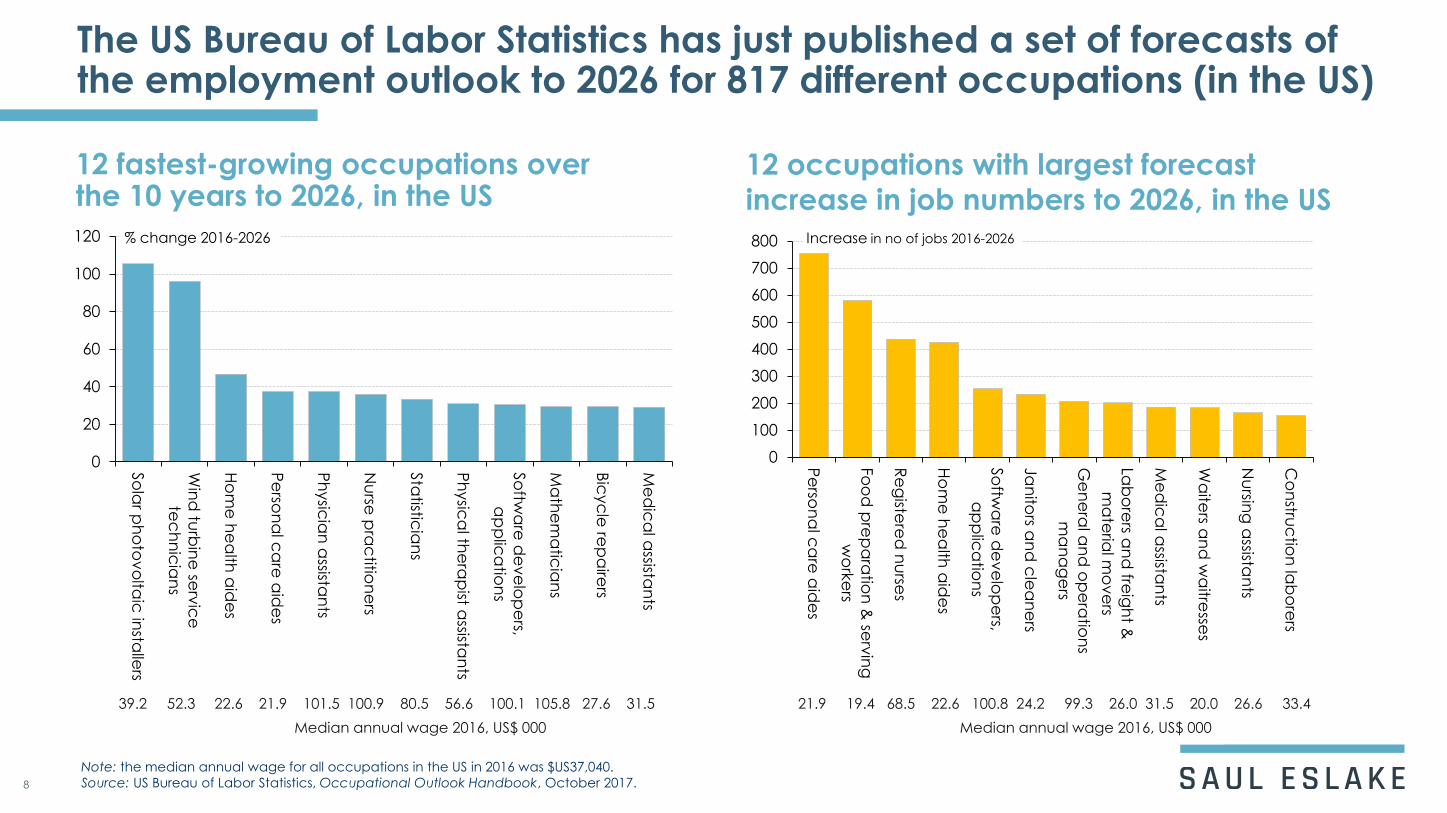

The US Bureau of Labor Statistics has just published a set of forecasts of the employment outlook to 2026 for 817 different occupations (in the US)

12 fastest-growing occupations over the 10 years to 2026, in the US

12 occupations with largest forecast

increase in job numbers to 2026, in the US

Note: the median annual wage for all occupations in the US in 2016 was $US37,040.

Source: US Bureau of Labor Statistics, Occupational Outlook Handbook, October 2017. 8

0

20

40

60

80

100

120

So

lar p

ho

tov

olta

ic in

stalle

rs

Win

d tu

rbin

e se

rvic

e

tec

hn

icia

ns

Ho

me

he

alth

aid

es

Pe

rson

al c

are

aid

es

Ph

ysic

ian

assista

nts

Nu

rse p

rac

tition

ers

Sta

tisticia

ns

Ph

ysic

al th

era

pist a

ssistan

ts

So

ftwa

re d

ev

elo

pe

rs,

ap

plic

atio

ns

Ma

the

ma

ticia

ns

Bic

yc

le re

pa

irers

Me

dic

al a

ssistan

ts

% change 2016-2026

39.2 52.3 22.6 21.9 101.5 100.9 80.5 56.6 100.1 105.8 27.6 31.5

Median annual wage 2016, US$ 000

0

100

200

300

400

500

600

700

800

Pe

rson

al c

are

aid

es

Fo

od

pre

pa

ratio

n &

serv

ing

wo

rke

rs

Re

giste

red

nu

rses

Ho

me

he

alth

aid

es

So

ftwa

re d

ev

elo

pe

rs,

ap

plic

atio

ns

Ja

nito

rs an

d c

lea

ne

rs

Ge

ne

ral a

nd

op

era

tion

s

ma

na

ge

rs

Lab

ore

rs an

d fre

igh

t &

ma

teria

l mo

ve

rs

Me

dic

al a

ssistan

ts

Wa

iters a

nd

wa

itresse

s

Nu

rsing

assista

nts

Co

nstru

ctio

n la

bo

rers

Increase in no of jobs 2016-2026

21.9 19.4 68.5 22.6 100.8 24.2 99.3 26.0 31.5 20.0 26.6 33.4

Median annual wage 2016, US$ 000

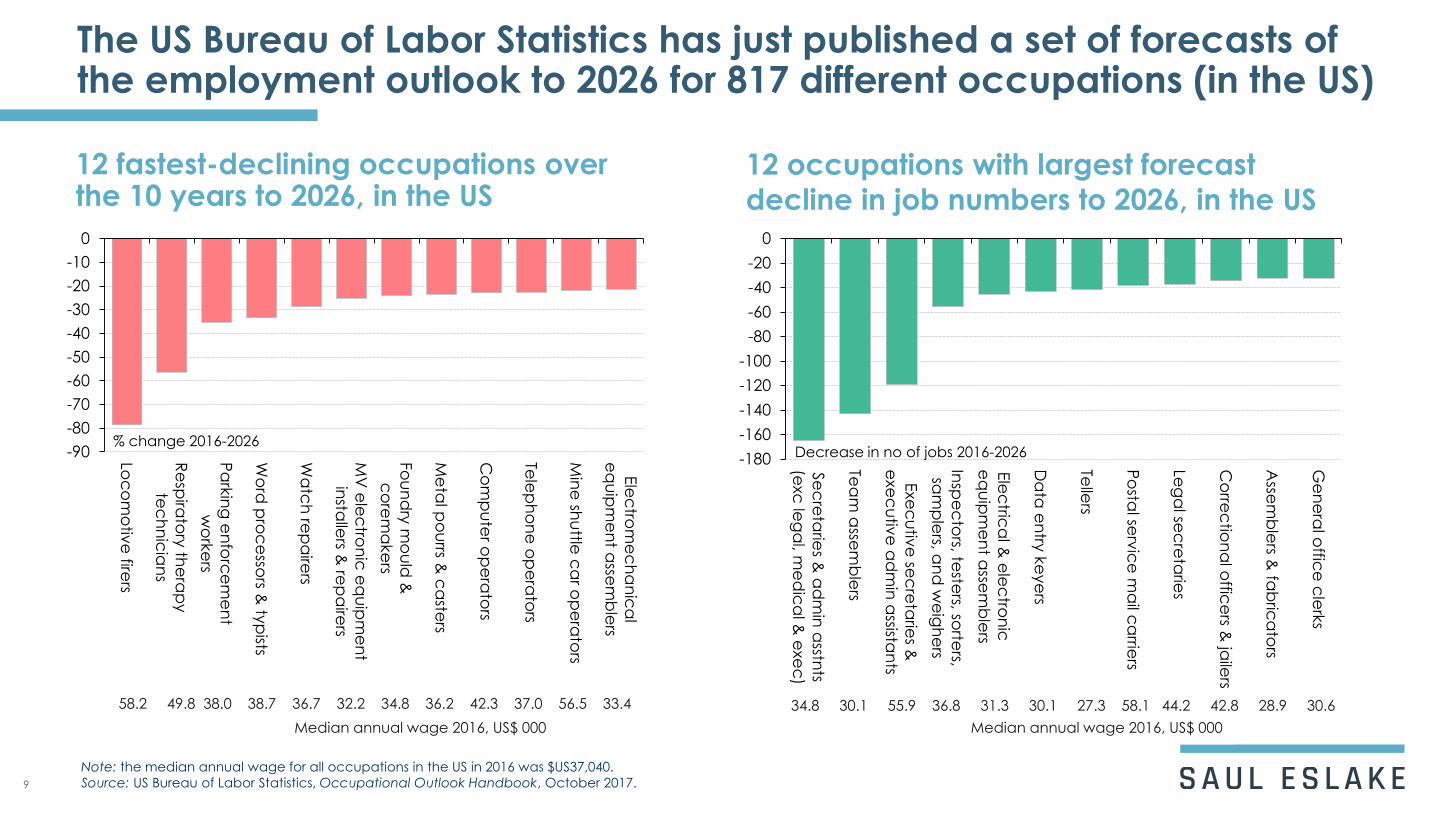

The US Bureau of Labor Statistics has just published a set of forecasts of the employment outlook to 2026 for 817 different occupations (in the US)

12 fastest-declining occupations over the 10 years to 2026, in the US

12 occupations with largest forecast

decline in job numbers to 2026, in the US

Note: the median annual wage for all occupations in the US in 2016 was $US37,040.

Source: US Bureau of Labor Statistics, Occupational Outlook Handbook, October 2017. 9

58.2 49.8 38.0 38.7 36.7 32.2 34.8 36.2 42.3 37.0 56.5 33.4

Median annual wage 2016, US$ 000

-90

-80

-70

-60

-50

-40

-30

-20

-10

0

Loc

om

otiv

e fire

rs

Re

spira

tory

the

rap

y

tec

hn

icia

ns

Pa

rkin

g e

nfo

rce

me

nt

wo

rke

rs

Wo

rd p

roc

esso

rs & ty

pists

Wa

tch

rep

aire

rs

MV

ele

ctro

nic

eq

uip

me

nt

insta

llers &

rep

aire

rs

Fo

un

dry

mo

uld

&

co

rem

ake

rs

Me

tal p

ou

rrs & c

aste

rs

Co

mp

ute

r op

era

tors

Tele

ph

on

e o

pe

rato

rs

Min

e sh

uttle

ca

r op

era

tors

Ele

ctro

me

ch

an

ica

l

eq

uip

me

nt a

ssem

ble

rs

% change 2016-2026

34.8 30.1 55.9 36.8 31.3 30.1 27.3 58.1 44.2 42.8 28.9 30.6

Median annual wage 2016, US$ 000

-180

-160

-140

-120

-100

-80

-60

-40

-20

0

Se

cre

tarie

s & a

dm

in a

sstnts

(exc

leg

al, m

ed

ica

l & e

xe

c)

Tea

m a

ssem

ble

rs

Exe

cu

tive

sec

reta

ries &

exe

cu

tive

ad

min

assista

nts

Insp

ec

tors, te

sters, so

rters,

sam

ple

rs, an

d w

eig

he

rs

Ele

ctric

al &

ele

ctro

nic

eq

uip

me

nt a

ssem

ble

rs

Da

ta e

ntry

ke

ye

rs

Telle

rs

Po

stal se

rvic

e m

ail c

arrie

rs

Leg

al se

cre

tarie

s

Co

rrec

tion

al o

ffice

rs & ja

ilers

Asse

mb

lers &

fab

rica

tors

Ge

ne

ral o

ffice

cle

rks

Decrease in no of jobs 2016-2026

Substantial increases in the use of IT by Australian businesses have not so far resulted in massive net job losses

Australia’s information technology business capital stock

Australian employment,

by skill type

Note: Skill types based on occupational categories in labour force statistics.

Sources: ABS, Australian System of National Accounts 2016-17 (5204.0), Table 69; Labour Force, Australia, Detailed, Quarterly, August 2017 (6291.0.55.003).

Based on ideas in Jeff Borland & Michael Coelli, Are robots taking our jobs?, University of Melbourne, August 2017; and Alex Heath, ‘The Changing Nature of the

Australian Workforce’, Speech to a CEDA Conference, Brisbane, 21st September 2016. 10

0

5

10

15

20

25

30

35

40

45

87 90 93 96 99 02 05 08 11 14 17

% of total

Non-routine cognitive

Non-routine manual

Routine cognitive

Routine manual

Financial years ended 30 June

0

10

20

30

40

50

60

81 86 91 96 01 06 11 16

$ bn (2015-16 chain volumes)

Financial years ended 30 June

Computers &

peripherals

Software

Electrical &

electronic

equipment

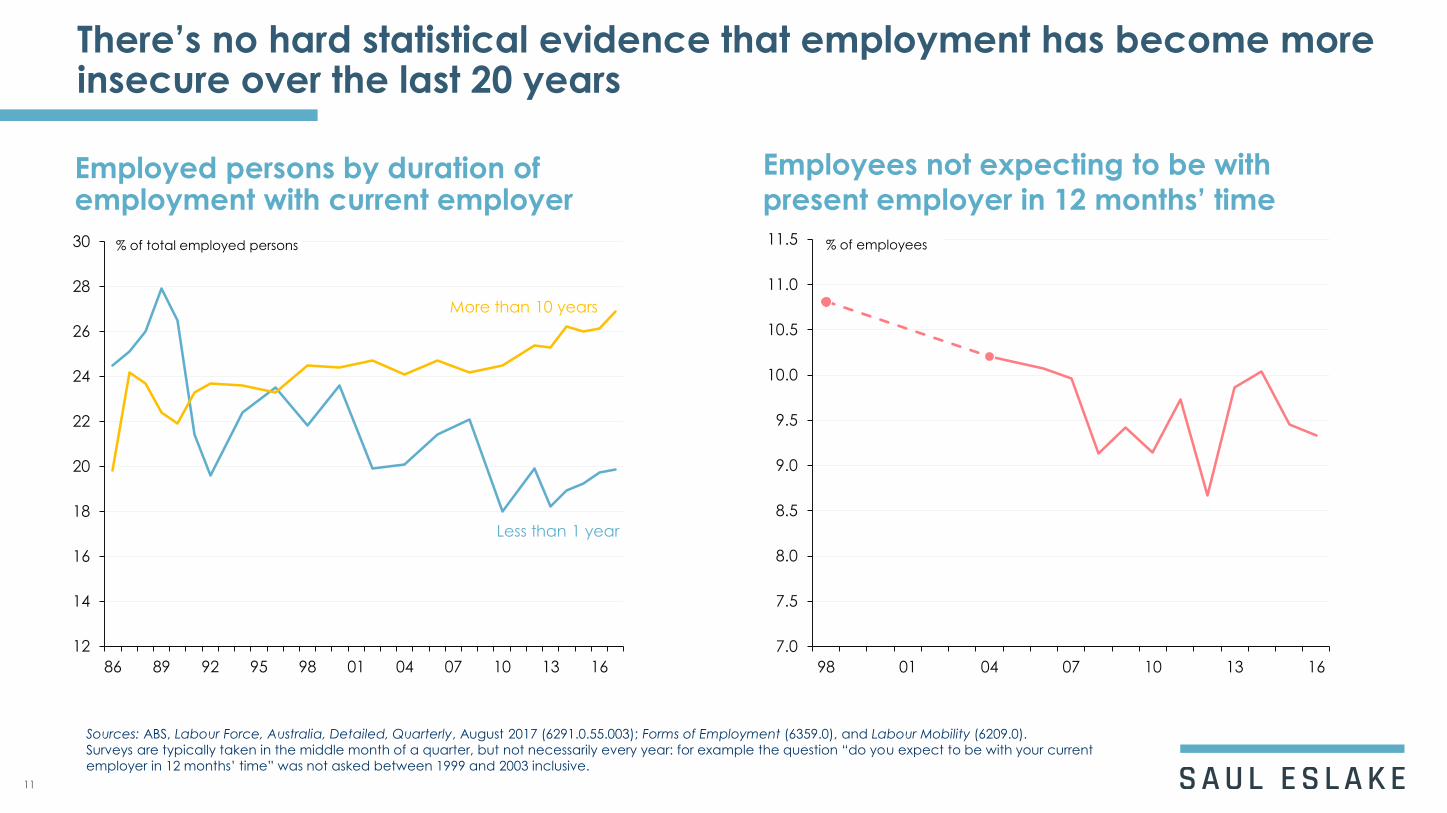

There’s no hard statistical evidence that employment has become more insecure over the last 20 years

Employed persons by duration of employment with current employer

Employees not expecting to be with

present employer in 12 months’ time

Sources: ABS, Labour Force, Australia, Detailed, Quarterly, August 2017 (6291.0.55.003); Forms of Employment (6359.0), and Labour Mobility (6209.0).

Surveys are typically taken in the middle month of a quarter, but not necessarily every year: for example the question “do you expect to be with your current

employer in 12 months’ time” was not asked between 1999 and 2003 inclusive.

11

12

14

16

18

20

22

24

26

28

30

86 89 92 95 98 01 04 07 10 13 16

% of total employed persons

Less than 1 year

More than 10 years

7.0

7.5

8.0

8.5

9.0

9.5

10.0

10.5

11.0

11.5

98 01 04 07 10 13 16

% of employees

Casual employment is becoming more commonplace, but not as dramatically as is widely believed

Employees with and without paid leave entitlements

Employees with paid leave entitlements,

by gender

Note: The ABS uses 'employees without paid leave entitlements' as the primary measure of casual employment. This is an objective measure that can be collected

consistently. An employee with paid leave entitlements has access to either paid holiday leave or paid sick leave, or both. Sources: ABS, Characteristics of

Employment, August 2016 (6333.0) and Australian Labour Market Statistics, July 2013 (6105.0). Surveys are in either August or November of each year. 12

20

21

22

23

24

25

26

27

73

74

75

76

77

78

79

92 95 98 01 04 07 10 13 16

% of total

With paid leave

(left scale)

Without paid leave

(right scale)

68

70

72

74

76

78

80

82

84

86

88

92 95 98 01 04 07 10 13 16

% of total

Females

Males

A steadily increasing proportion of people are working part-time – and while that suits many, it is not always by choice

Part-time employment as a pc of total, by gender

Part-time workers who would like more

hours, as a pc of total, by gender

Source: ABS, The Labour Force, Australia, September 2016 (6202.0) .

13

34

36

38

40

42

44

46

48

50

4

6

8

10

12

14

16

18

20

80 83 86 89 92 95 98 01 04 07 10 13 16

% of total

Males

(left scale)

Females

(right scale)

% of total

Financial years ended 30 June

0

2

4

6

8

10

12

30

35

40

45

50

55

60

80 83 86 89 92 95 98 01 04 07 10 13 16

% of total

Males

(left scale)

Females

(right scale)

% of total

Financial years ended 30 June

There is thus more ‘spare capacity’ in the labour market than suggested by the conventional unemployment rate

‘Heads-based’ alternative measures of ‘spare capacity’ in the labour market

‘Hours-based’ alternative measures of

‘spare capacity’ in the labour market

Sources: ABS, The Labour Force, Australia, September 2016 (6202.0)14

0

2

4

6

8

10

12

14

16

18

20

80 83 86 89 92 95 98 01 04 07 10 13 16

% of the labour force

'Under-utilization' rate

Unemployment rate

'Under-

employment'

rate

Note: The ‘under-employment’ rate is the number of people working part-time who are willing and able to work more hours (including those who normally work full-

time but are working part-time for ‘economic reasons’) as a percentage of the labour force. The ‘under-utilization’ rate is the number of unemployed and under-

employed as a percentage of the labour force. The ‘heads-based’ measures take no account of the number of additional hours ‘under-employed’ people would

like to work, nor of whether they have been ‘actively looking’ for additional hours (as is required of people not working in order to be counted as ‘unemployed’.

; Reserve Bank of Australia, Statement on Monetary Policy, February 2017, Box B.

0

1

2

3

4

5

6

7

8

9

04 05 06 07 08 09 10 11 12 13 14 15 16

'Under-utilization' rate

Unemployment rate

'Under-employment‘ rate

% of the labour force

Leading indicators of the labour market are pointing to an ongoing gradual decline in unemployment

National Australia Bank monthly survey measure of employer hiring intentions

NAB hiring intentions measure as a leading

indicator of changes in unemployment

Source: National Australia Bank, Monthly Business Survey, September 201715

; ABS, The Labour Force, Australia, September 2017 (6202.0).

-30

-25

-20

-15

-10

-5

0

5

10

15

20

01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17

Net balance (%)

Trend

-25

-20

-15

-10

-5

0

5

10

15-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17

Percentage points (trend)

Change in unemploymentrate from 12 mths earlier(inverted; left scale)

NAB surveyhiring intentions(4 mths forward;right scale)

Net balance (trend, % )

However long-term unemployment seems to be becoming more entrenched

Median duration of unemployment

Long-term unemployed as a share of total

unemployed

Source: ABS, The Labour Force, Australia, September 2017 (6202.0).16

70

80

90

100

110

120

130

5

10

15

20

25

30

92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17

Weeks

All unemployed(left scale)

Financial years ended 30 June

Weeks

Unemployed for more than 1 year(left scale)

0

5

10

15

20

25

30

35

40

92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17

More than 2 years

1 -2 years

% of total unemployed

Financial years ended 30 June

Unemployed for -

New Zealand seems to be doing better in dealing with long-term unemployment than Australia

Long-term unemployment rates (pc of labour force), Australia and NZ

Long-term unemployed as pc of total

unemployed, Australia and NZ

Source: ABS, The Labour Force, Australia, September 2017 (6202.0); Statistics New Zealand Infoshare, Household Labour Force Survey.17

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

92 95 98 01 04 07 10 13 16

% of labour force

New Zealand

Financial years ended 30 June

Australia

0

5

10

15

20

25

30

35

40

92 95 98 01 04 07 10 13 16

% of total unemployed

New Zealand

Financial years ended 30 June

Australia

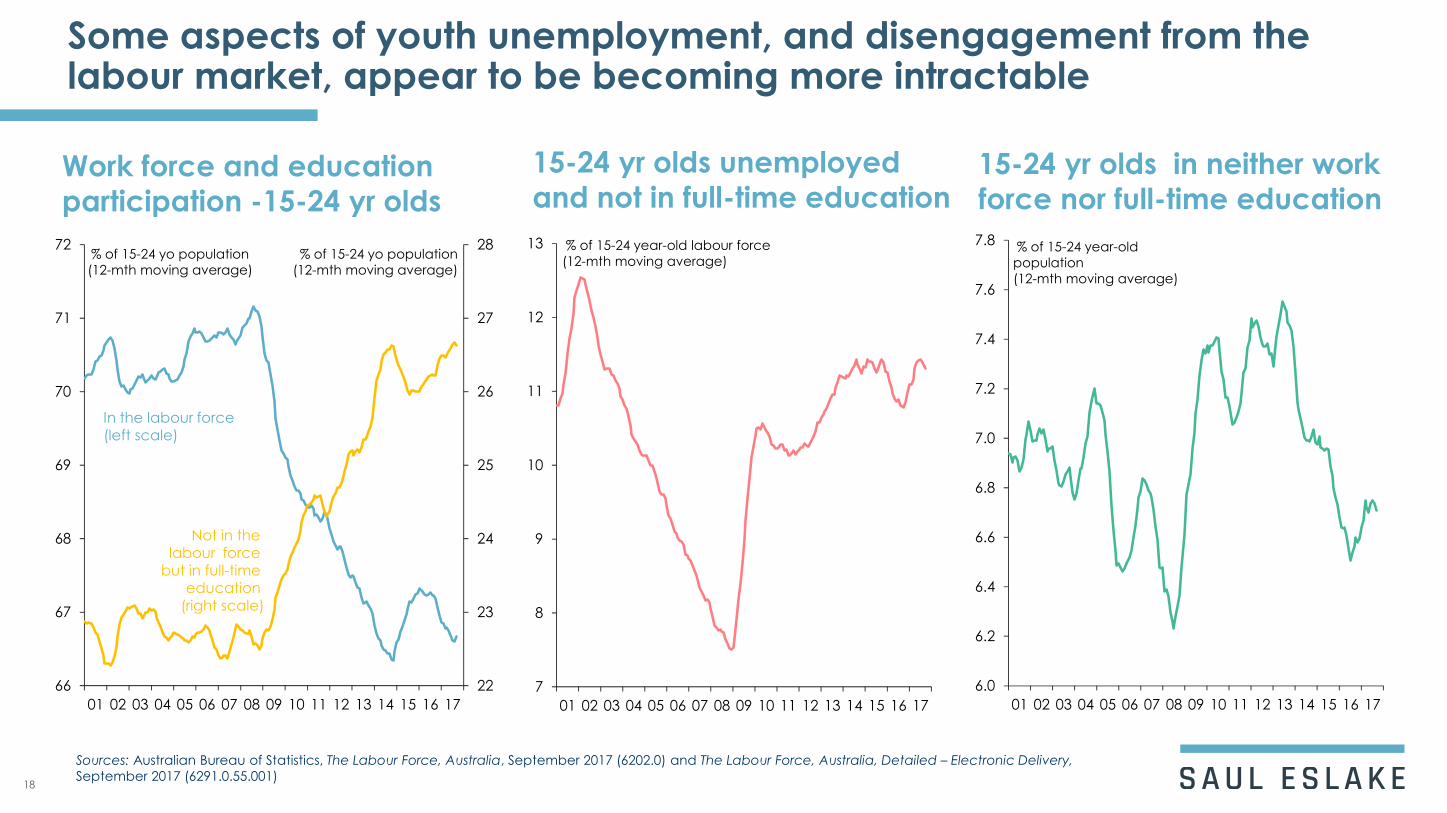

Some aspects of youth unemployment, and disengagement from the labour market, appear to be becoming more intractable

15-24 yr olds unemployed

and not in full-time education

Sources: Australian Bureau of Statistics, The Labour Force, Australia, September 2017 (6202.0) and The Labour Force, Australia, Detailed – Electronic Delivery,

September 2017 (6291.0.55.001)

15-24 yr olds in neither work

force nor full-time educationWork force and education

participation -15-24 yr olds

18

22

23

24

25

26

27

28

66

67

68

69

70

71

72

01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17

% of 15-24 yo population

(12-mth moving average)

In the labour force(left scale)

Not in the labour force

but in full-time education

(right scale)

% of 15-24 yo population

(12-mth moving average)

7

8

9

10

11

12

13

01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17

% of 15-24 year-old labour force

(12-mth moving average)

6.0

6.2

6.4

6.6

6.8

7.0

7.2

7.4

7.6

7.8

01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17

% of 15-24 year-old

population

(12-mth moving average)

The higher a person’s level of educational attainment, the more likely he or she is to be working – and to be working full-time

Employment as a pc of population, by level

of educational attainment

Full-time work as a pc of total employment, by

level of educational attainment

Source: ABS, Education and Work, Australia, May 2016 (6227.0).

19

Labour force experience by level of educational attainment – Australia, May 2016

30

40

50

60

70

80

90

Yr 10 or

below

Yr 11 Yr 12 Cert III/IV Dip /

Adv Dip

Under-

grad

degree

Post-grad

degree

% of civilian populationaged 15-74

Average

30

40

50

60

70

80

90

Yr 10 or

below

Yr 11 Yr 12 Cert III/IV Dip /

Adv Dip

Under-

grad

degree

Post-grad

degree

% of civilian populationaged 15-74

Average

And while more Australians are getting more education …

Australians with some kind of post-

secondary school qualificationAustralians with no formal educational

qualification beyond Year 10

Source: ABS, Education and Work, Australia, May 2016 (6227.0).

16

18

20

22

24

26

28

30

05 06 07 08 09 10 11 12 13 14 15 16

% of population

Diploma,

adv. diploma

or Cert III/IV

Bachelor's degree

or higher

Population

aged 15+

Population

aged 15-64

Population

aged 15-74

16

18

20

22

24

26

28

30

05 06 07 08 09 10 11 12 13 14 15 16

% of population

Population

aged 15+

Population

aged 15-64

Population

aged 15-74

… they may not be getting better education

Australia’s average PISA scores compared

with OECD averageHigh and low performers in Australia

Note: Scores are averaged across reading (2000 onwards), mathematical literacy (2003 onwards) and scientific literacy(2006 onwards).

Source: Sue Thomson, Lisa De Bortoli and Catherine Underwood, PISA 2015: A first look at Australian student’s [sic] performance, Australian Council for Educational

Research, December 2016.

480

490

500

510

520

530

540

550

560

2000 2003 2006 2009 2012 2015

Average score

OECD average

Australia

20 15 10 5 0 5 10 15 20

2000

2003

2006

2009

2012

2015

Pc of students

PISA

cycleLow performers High performers

Wages growth is now slower than at any time since the early 1990s

Measures of growth in wages

Employment by industry, according to

average earnings

Sources: ABS, Wage Price Index, June quarter 2017 (6345.0); Average Weekly Earnings, May 2017 (6302.0)

22

0

1

2

3

4

5

6

7

8

91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17

% change from year earlier

Average weekly ordinary time earnings (AWOTE) - full timeadult employees (4-qtr moving average)

Wage price index (WPI)

(excl. bonuses)

75

85

95

105

115

125

135

01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17

Level of employmentin 2007-08 = 100

Sectors with ‘average’earnings (± 15% of all-

Industry average)

Sectors with ‘below-average’earnings (<85% of national average)

Sectors with ‘above-average’earnings (>115% of national average)

− but not because jobs growth has been concentrated in low-paying sectors

; The Labour Force, Australia, Detailed, Quarterly, August

2017 (6291.0.55.003).

Rather, it’s because wage increases have become smaller, and rarer

Frequency and size of wage changes

Share of jobs that experience a wage

change of given size

Source: James Bishop and Natasha Cassidy, ‘Insights into Low Wage Growth in Australia’, Reserve Bank of Australia Bulletin, March Quarter 2017.23

0

0.5

1

1.5

2

2.5

3

3.5

4

4.5

4.0 5.0 6.0 7.0 8.0 9.0

Q1 1992 -

Q2 2008

Unemployment rate lagged 2 quarters

Wa

ge

s gro

wth

%

% change fromyear earlier

Q3 2008 -

Q1 2017

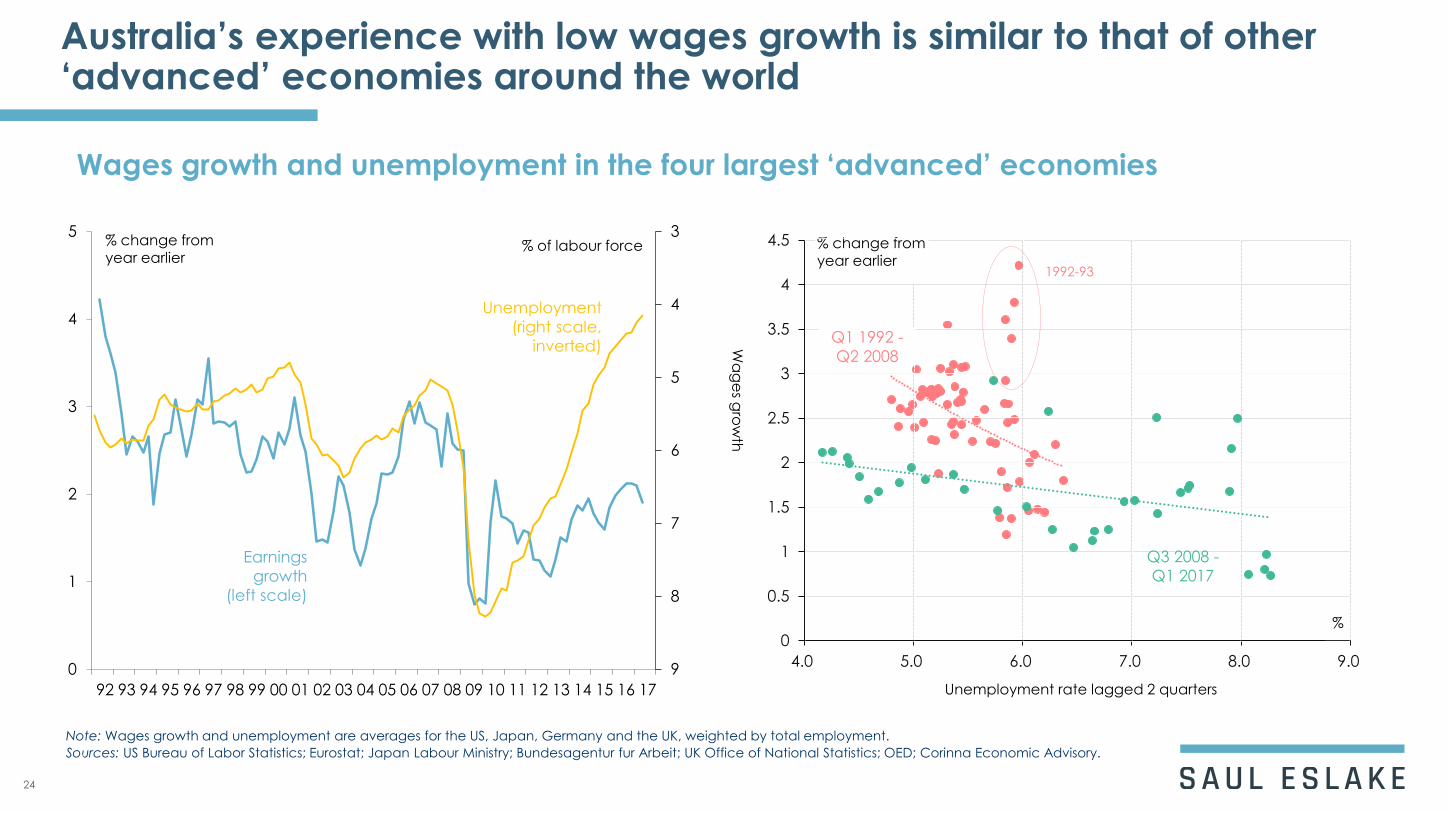

Australia’s experience with low wages growth is similar to that of other ‘advanced’ economies around the world

Wages growth and unemployment in the four largest ‘advanced’ economies

Note: Wages growth and unemployment are averages for the US, Japan, Germany and the UK, weighted by total employment.

24

Sources: US Bureau of Labor Statistics; Eurostat; Japan Labour Ministry; Bundesagentur fur Arbeit; UK Office of National Statistics; OED; Corinna Economic Advisory.

3

4

5

6

7

8

90

1

2

3

4

5

92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17

Earnings

growth

(left scale)

Unemployment

(right scale,

inverted)

% change from year earlier

% of labour force

1992-93

Income inequality widened in the years before the global financial crisis but has narrowed a bit since then

Shares of total gross household income, by quintile, 1994-95 to 2015-16

Shares of equivalized household disposable

income, by quintile, 1994-95 to 2015-16

Note: Quintiles are five equally-sized groups each comprising 20% of the population, ranked (in this case) by income. Gross household income is income from all

sources (including pensions and benefits) before income tax and Medicare levy.

25

0

5

10

15

20

25

30

35

40

45

50

Lowest Second Third Fourth Highest

94-95 95-96 96-97 97-98 99-00 00-01 02-03

03-04 05-06 07-08 09-10 11-12 13-14 15-16

% of total

Income quintile

0

5

10

15

20

25

30

35

40

45

50

Lowest Second Third Fourth Highest

94-95 95-96 96-97 97-98 99-00 00-01 02-03

03-04 05-06 07-08 09-10 11-12 13-14 15-16

% of total

Income quintile

‘Equivalized’ disposable income means after adjusting for differences in household

composition and size (number of adults and children) and after deducting income tax and Medicare levy.

Source: Australian Bureau of Statistics, Household Income and Wealth, Australia, 2015-16 (6523.0).

Although Australia is a low-tax country by ‘advanced’ economy standards …

Source: Organization for Economic Co-operation and Development (OECD), Revenue Statistics – OECD Countries: Comparative Tables, 2017.

Taxation revenue as a share of GDP – OECD countries, 2014

26

10

15

20

25

30

35

40

45

50 %

… Australia’s tax system is in some important respects more ‘progressive’ than many of those which collect a bigger share of GDP in tax

Source: Organization for Economic Co-operation and Development (OECD), Revenue Statistics – OECD Countries: Comparative Tables, 2017.

Personal income taxation revenue as a

share of GDP – OECD countries, 2014

27

0

5

10

15

20

25

30%

Goods & services taxation revenue as

a share of GDP – OECD countries, 2014

0

2

4

6

8

10

12

14

16

18%

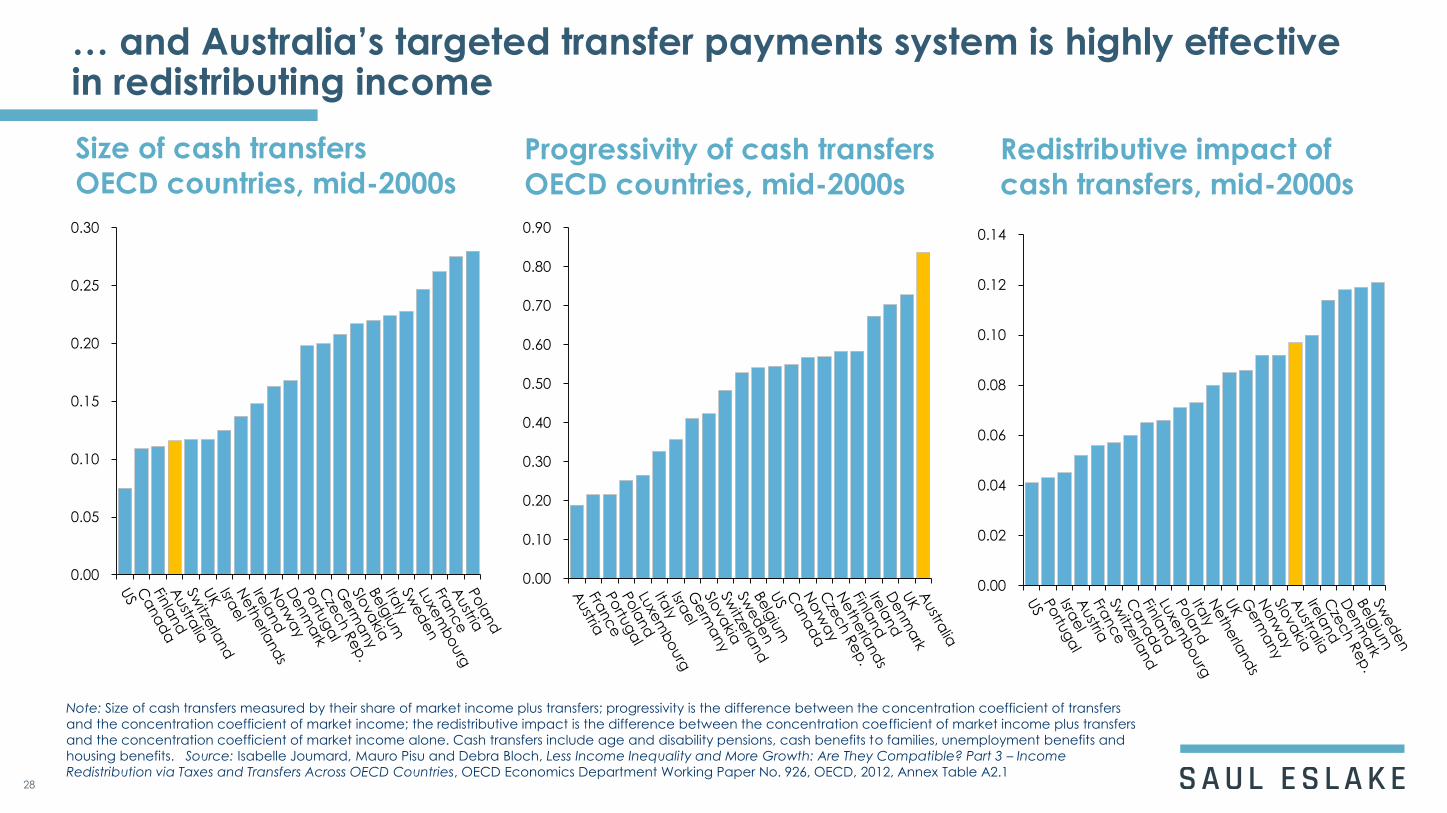

… and Australia’s targeted transfer payments system is highly effective in redistributing income

Note: Size of cash transfers measured by their share of market income plus transfers; progressivity is the difference between the concentration coefficient of transfers

and the concentration coefficient of market income; the redistributive impact is the difference between the concentration coefficient of market income plus transfers

and the concentration coefficient of market income alone. Cash transfers include age and disability pensions, cash benefits to families, unemployment benefits and

housing benefits. Source: Isabelle Joumard, Mauro Pisu and Debra Bloch, Less Income Inequality and More Growth: Are They Compatible? Part 3 – Income

Redistribution via Taxes and Transfers Across OECD Countries, OECD Economics Department Working Paper No. 926, OECD, 2012, Annex Table A2.1

Size of cash transfers

OECD countries, mid-2000s

28

0.00

0.05

0.10

0.15

0.20

0.25

0.30

Progressivity of cash transfers

OECD countries, mid-2000s

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

Redistributive impact of

cash transfers, mid-2000s

0.00

0.02

0.04

0.06

0.08

0.10

0.12

0.14

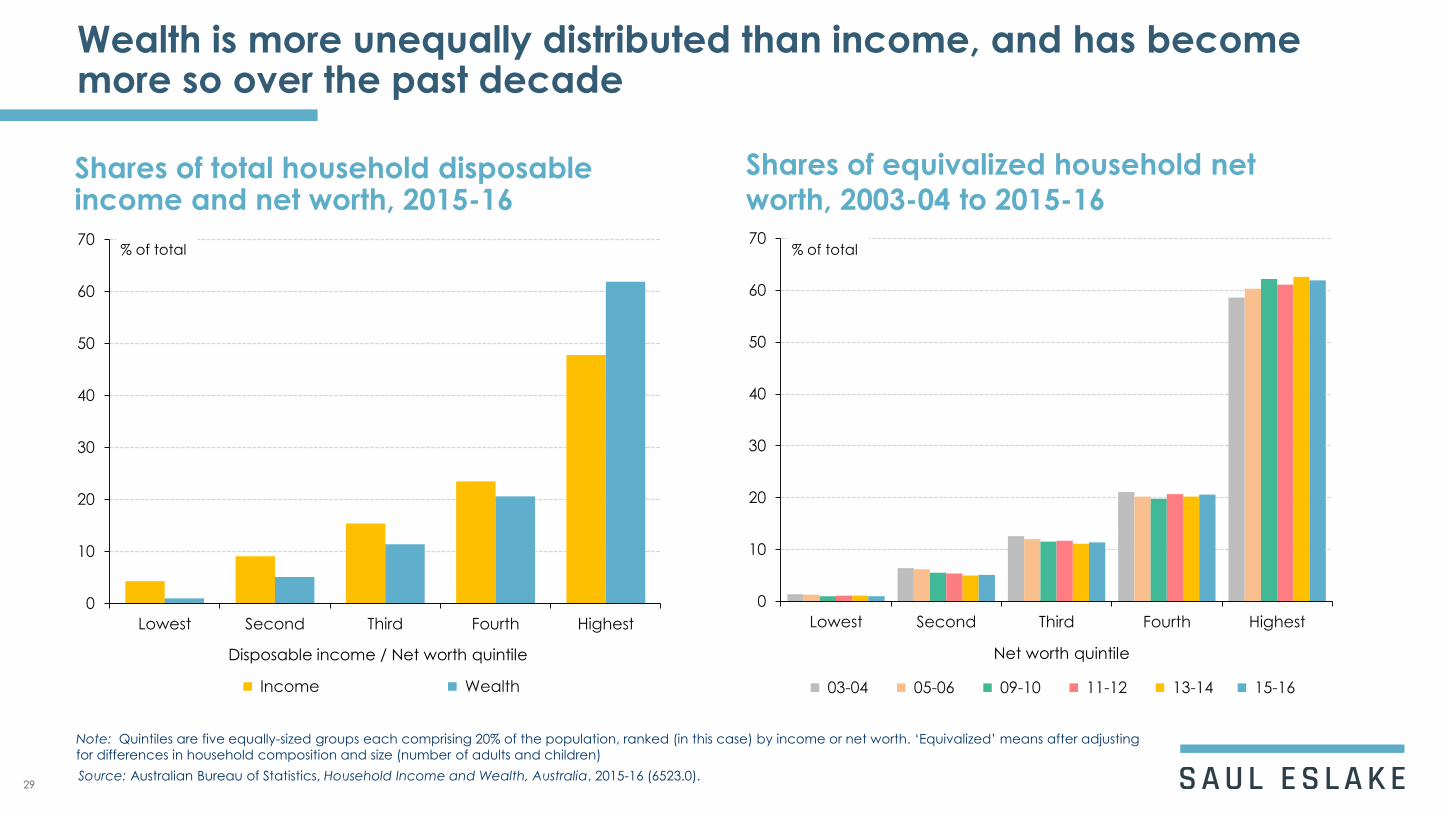

Wealth is more unequally distributed than income, and has become more so over the past decade

Shares of total household disposable income and net worth, 2015-16

Shares of equivalized household net

worth, 2003-04 to 2015-16

Note: Quintiles are five equally-sized groups each comprising 20% of the population, ranked (in this case) by income or net worth. ‘Equivalized’ means after adjusting

for differences in household composition and size (number of adults and children)

29Source: Australian Bureau of Statistics, Household Income and Wealth, Australia, 2015-16 (6523.0).

0

10

20

30

40

50

60

70

Lowest Second Third Fourth Highest

Income Wealth

% of total

Disposable income / Net worth quintile

0

10

20

30

40

50

60

70

Lowest Second Third Fourth Highest

03-04 05-06 09-10 11-12 13-14 15-16

% of total

Net worth quintile

Unemployment benefits have fallen relative to other social security payments

Single rate unemployment benefit / ‘Newstart’ Allowance vs age pension

Single rate unemployment benefit /

’Newstart’ allowance vs minimum wage

30

Sources: Australian Government, Department of Social Security, Guide to Social Security Law, Version 1.237, October 2017, Section 5.2 – Historical rates;

200

250

300

350

400

450

90 93 96 99 02 05 08 11 14 17

$ per week (2017 $)

Single rate age pension

Single rate UB/JSA/NSA

200

300

400

500

600

700

800

90 93 96 99 02 05 08 11 14 17

$ per week (2017 $)

Single rate UB/JSA/NSA

Federal minimum wage

Reg Hamilton, The history of the Australian Minimum Wage, Fair Work Commission, Sir Richard Kirby Archives, March 2016.

and by comparison with the minimum wage

Some concluding suggestions

31

Don’t set too much store by exaggerated claims regarding the impact of technology on jobs

− yes, advances in information technology, ‘big data’, machine learning, etc. will lead to a range of tasks

(and some jobs) disappearing

− but those and other advances, demographic and other changes, will also create new tasks and new jobs

− as has always been the case, down the ages

Continue to emphasize the importance of education to improving employment outcomes

− and, in particular, in improving educational participation and attainment of people from lower-income

and otherwise socio-economically disadvantaged backgrounds

Challenge the notions that there is something inherently more noble or worthy about manufacturing

jobs than other areas of employment, and that services jobs are all about “flipping hamburgers” or

“taking in each others’ laundry”

− and similarly challenge traditional gendered views about “men’s” and “women’s” work

Consider how the New Zealand ‘investment’ approach to long-term unemployment can be adapted

to Australian circumstances

Give consideration to ways in which the Government might more directly address the problem of

stagnant wages growth

− for example in its submissions to FWC minimum wage cases

Continue to advocate for increases in the level of Newstart Allowances

And so to your question …

32

What strategies will you use to counter the challenges and

changes in the availability of work for you, your organisation and

the people you work with?