inland waterways and port modernization project...

TRANSCRIPT

E- /ApVio. 3

VIETNAM INLAND WATERWAY INTERNATIONAL BANK FORDEPARTMENT / PMU-SW RECONSTRUCTION

AND DEVELOPMENT

INLAND WATERWAYS ANDPORT MODERNIZATION PROJECT

REHABILITATION AND MODERNIZATION OFTHE PORT OF CAN THO

FINAL REPORT

JUNE 1996

INEDECOQNetherlands Engineering Consultants

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

LIST OF REPORTS

VOLUME I : EXECUTIVE SUMMARY

VOLUME II : INLAND WATERWAYS IMPROVEMENT PROJECT(Main Report)

Annex II - 1 Design ReportAnnex II - 2: Navigation AidsAnnex il - 3: Soil Report

VOLUME III RESETTLEMENT ACTION PLAN

VOLUME IV : ENVIRONMENTAL IMPACT ASSESSMENT &ENVIRONMENTAL MANAGEMENT PLAN

VOLUME V : TOPOGRAPHIC MAPS (scale 1:5000)

Book 1: Ho Chi Minh City - Cho Gao (PI/O to PI/l 3)Cho Gao - Sa Dec (PIl/OtoPIV/21)

Book 2: Sa Dec - Lap Vo (PIIl/Oto PIIl/14)Rach Gia - Ha Tien (PIV/O to PIV/1 9)Rach Soi - Ha Giang (PIV/20 to PIV32)

Book 3: Cho Lach - Mang Thit (PV/O to PV/20)Can Tho - Ca Mau (PVI/O to VI/38)

CONTENTS

1. INTRODUCTION 1A. Study Organisation 1B. The Terms of Reference 2

2. THE EXISTING PORT 3A. Fixed Facilities 3B. Equipment 7C. Management 9D. Manning 10E. Access to the Port 12

3. PORT TRAFFIC 14A. Historical Traffic 14B. Port Traffic in the South of Vietnam 18C. Present Cargo Trends 25D. Forecast of future cargo volumes 29

4. CARGO HANDLING 42A. Present Practice 42B. Improvements 44C. Equipment Requirements 45

5. BERTH OCCUPANCY 48A. The Main Berth 48B. The Mooring Buoys 48

6. FUTURE DEVELOPMENT 49A. Fixed Facilities 49B. Equipment 49C. Environmental Impacts 49

7. ECONOMIC ANALYSIS 53A. Background 53B. The With the Project Case 53C. The Without the Project Case 54D. Calculation of Economic Return 55E. Sensitivity Analysis 56

8. THE FINANCIAL FUTURE OF THE PORT 59

9. CONCLUSIONS 61

June 1996/5K9012.C1875.21/R005/SPE/tb

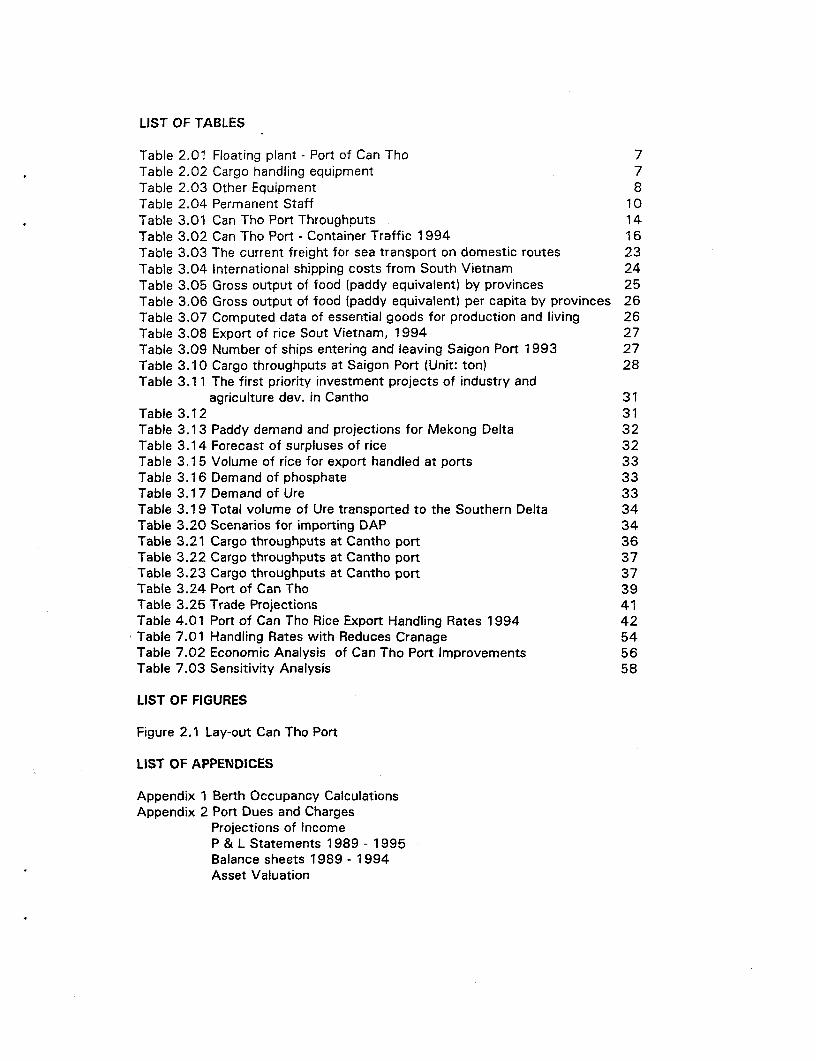

LIST OF TABLES

Table 2.01 Floating plant - Port of Can Tho 7Table 2.02 Cargo handling equipment 7Table 2.03 Other Equipment 8Table 2.04 Permanent Staff 10Table 3.01 Can Tho Port ThroughDuts 14Table 3.02 Can Tho Port - Container Traffic 1994 16Table 3.03 The current freight for sea transport on domestic routes 23Table 3.04 International shipping costs from South Vietnam 24Table 3.05 Gross output of food (paddy equivalent) by provinces 25Table 3.06 Gross output of food (paddy equivalent) per capita by provinces 26Table 3.07 Computed data of essential goods for production and living 26Table 3.08 Export of rice Sout Vietnam, 1994 27Table 3.09 Number of ships entering and leaving Saigon Port 1993 27Table 3.10 Cargo throughputs at Saigon Port (Unit: ton) 28Table 3.11 The first priority investment projects of industry and

agriculture dev. in Cantho 31Table 3.12 31Table 3.13 Paddy demand and projections for Mekong Delta 32Table 3.14 Forecast of surpluses of rice 32Table 3.15 Volume of rice for export handled at ports 33Table 3.16 Demand of phosphate 33Table 3.17 Demand of Ure 33Table 3.19 Total volume of Ure transported to the Southern Delta 34Table 3.20 Scenarios for importing DAP 34Table 3.21 Cargo throughputs at Cantho port 36Table 3.22 Cargo throughputs at Cantho port 37Table 3.23 Cargo throughputs at Cantho port 37Table 3.24 Port of Can Tho 39Table 3.25 Trade Projections 41Table 4.01 Port of Can Tho Rice Export Handling Rates 1994 42Table 7.01 Handling Rates with Reduces Cranage 54Table 7.02 Economic Analysis of Can Tho Port Improvements 56Table 7.03 Sensitivity Analysis 58

LIST OF FIGURES

Figure 2.1 Lay-out Can Tho Port

LIST OF APPENDICES

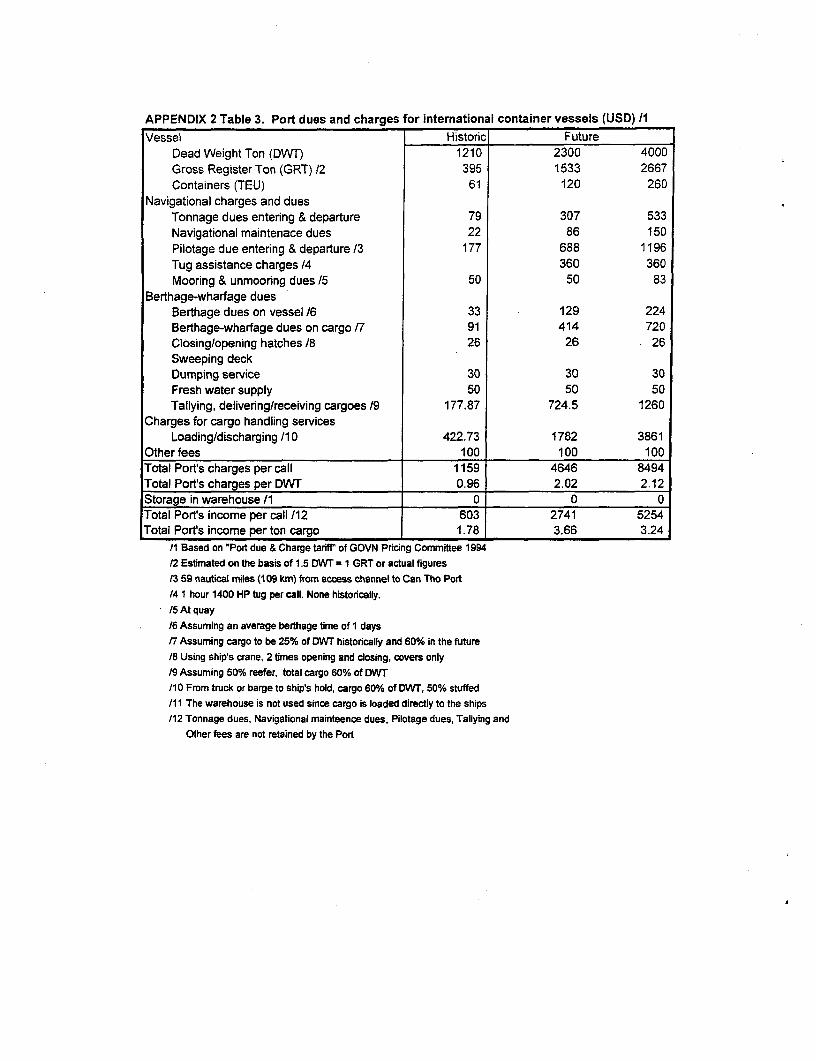

Appendix 1 Berth Occupancy CalculationsAppendix 2 Port Dues and Charges

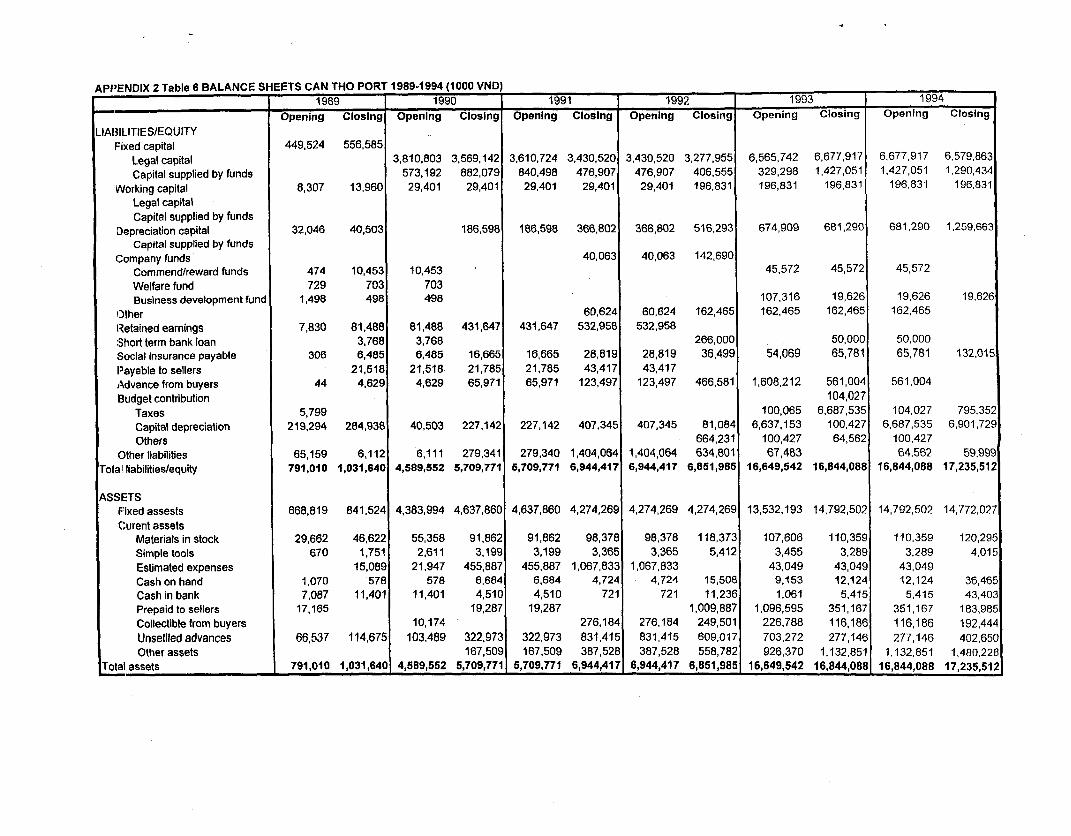

Projections of IncomeP & L Statements 1989 - 1995Balance sheets 1989 - 1994Asset Valuation

EXECUTIVE SUMMARY

The Nature of the Study

This study was commissioned to produce a set of cargo forecasts and toassess whether the throughput of the Port of Can Tho could be increased tohandle the predicted cargo over a reasonable time span. The parameters of thestudy were set so as to exclude the effect of any future deepening of the DinhAn Channel at the mouth of the Bassac River and to not include the option ofbuilding extensive new fixed facilities.

The study was carried out by staff from NEDECO and the PMU assisted bysome input from TESI South.

The Present Situation

The Port of Can Tho is at present a port which is performing at a fraction of itscapacity. This appears to be mainly because the port has not managed to breakthe shipping community's long established practice of servicing the MekongDelta through the ports of Ho Chi Minh City. This is partly because manyshippers have established facilities in HCMC but also it is because the true levelof service and facilities at Can Tho have never really been brought to theshippers' attention. The apparent state of dilapidation of parts of the port doesnot help its marketing effort.

The Findings of the Study

The study concluded that the traffic through the Port of Can Tho was likely togrow very quickly to reach approximately 500,000 Tonnes per year by the year2000. The port at present handles only one quarter of this trade but itsthroughput has doubled in the last year.

In reality, the port can handle almost 4 times its 1994 throughput (or twice its1995 traffic) with its present equipment and some adjustments to the shiftpatterns. With the addition of a US$ 1.8 million investment split betweenremedial works to the existing structures, some handling equipment and sometraining, the port should be able to handle its likely cargo throughput up to theyear 2000 or 2001. At that point a further investment of US$ 0.8 million inhandling equipment will be needed. This expenditure leaves the port financiallyviable and it shows economic rates of return in excess of 30%.

Shortly after the year 2000, the port will need additional quay space if it isattracting cargo in line with the projections. At present there are plans to buildtwo other separate international ports within an 8 km radius of the Port of CanTho. If this happens it is extremely unlikely that any of them will be successfulso it is important that a single site is selected for development.

1

1. INTRODUCTION TO THE STUDY

A. Study Organisation

1 .01 The Mekong Delta Master Plan Study, completed in 1993,identified the possibility of developing the Port of Can Tho to become aninternational port carrying a substantial part of the cargo exported from theDelta to other parts of Vietnam and to foreign destinations. The benefits of thiswere seen to be reduction in transport costs, greater wealth generation withinthe Delta and a reduction of pressure on the infrastructure of Ho Chi Minh Cityand its surroundings.

1.02 The study forms part of the Inland Waterways and PortModernisation Project which is funded by a grant from the JapaneseGovernment and administered by the World Bank. The study started inSeptember 1995 and is to be completed in March 1996. The object of thestudy is to define the expenditure which is required to help the Port of Can Thoboost its traffic from the present low levels to a substantial proportion of thegoods entering and leaving the Delta. The planned expenditure will form phase1 of the project with phase 2 being undertaken once the proposed study of theBassac river entrance (the Dinh An channel) has been completed.

1.03 The original Terms of Reference for the appointment ofConsultants for this project were written in terms of the work being carried outby the Project Management Unit of the Southern Waterways (PMU) and theTransport Economic Science Centre in the South (TESI) with the Consultantsproviding technical assistance and advice.

1.04 Following the World Bank visit to Ho Chi Minh City in lateSeptember 1995, the structure of the project was changed such that theproject is to be carried out by the Project Management Unit working with theteam from NEDECO. TESI are to be contracted by the Project Management Unitto carry out specific tasks on the project.

1.05 The main work for the study was under taken by the followingstaff .-

Richard Clarke - Port planner, engineer and operations specialist, NEDECO.Alexander Mueller - Financial and economic analyst, NEDECO.Tran Doan Phi An - Transport Economist, Transport and Economic ScienceCentre in the South (TESI).

Richard Clarke and Alexander Mueller each made two visits to Vietnam underthe project, the first being in September/October 1995 and the second inJanuary/February 1996. The majority of TESI's work was done between thesetwo visits.

1.06 An Inception Report for the study was written in October 1995and it was published as part of the Inland Waterways and Port ModernizationProject Phase 1 Report.

2

B. The Terms of Reference

1.07 The full Terms of Reference (TOR) for the study are set out inAppendix I. Below are summarised the major points from the TOR:-

- Assume that the Dinh An channel remains as at present;- No Major Expansion of Existing Wharves;- Produce traffic Forecasts for years 2000 and 2015;- Survey existing facilities and equipment;- Examine port operations, management practices, accountancy procedures;- Propose improvements to facilities, equipment, operations, management

and training;- Evaluate environmental impact of proposed measures;- Economic evaluation of the proposed measures;- Financial evaluation of the proposed measures.

1.08 Although the Terms of reference were written very much in termsof an engineering study, the situation on the ground turned out to be a portwhich was basically in sound condition but which was under performingbecause it failed to attract cargo. Part of the study resources were thereforeused to investigate why cargo was not using the port and what mechanismdecided the distribution of cargo between the various ports of the southern partof Vietnam.

3

2. THE EXISTING PORT

A. Fixed Facilities

a) General Description

2.01 The port is located approximately 8 km north of the city of CanTho and approximately 3 km south of the Can Tho Export Processing Zone(EPZ). Immediately to the south of the port the land is occupied by a militaryinstallation whilst to the north is an open area used by a local constructioncompany.

2.02 The site is approximately rectangular with an average width parallel tothe road of 200 m and an average depth back from the waterfront of 135 m. Itis basically level with an elevation of approximately 2.8 m above survey datum.(see figure 2.1)

2.03 During his visit, the Port Planner carried out an inspection of theport's fixed facilities and equipment.

2.04 For the fixed facilities, the inspection took the form of a visualinspection recorded as notes and photographs. It included an inspection of theunderside of the jetty from a boat. No materials testing was undertaken.

2.05 The plant and equipment survey took the form of an externalinspection, watching most of the plant in operation and a discussion withmanagement about the problems encountered with each item. The two lorrieshave been rented out to another enterprise and were away from the port onboth visits. The two barges were also away from the port having been rentedout.

2.06 These surveys are sufficient to assess the likely load capacity andlife of the port structures but they would have been much more effective haddrawings of the structures been available. For the plant, they are adequate toassess the useful life and availability of the individual items. On both counts,the port management seemed to take a realistic and practical view.

b) The Main Jetty

2.07 The main quay is a piled platform with a 144 m berthing face anda width of 18 m. It is connected to the shore by four access bridges each 6 mwide. Its surface is at an elevation of 3.0 m above datum. The publishedminimum depth of water alongside is 10.0 m.

2.08 The southern section of the quay, with a frontage of 61 m (200')was built by the US military before liberation. It consists of H section steel pilessupporting in situ cast concrete beams. These in turn support precast concretepanels with in situ infills. At the front of this section of berth there is afendering grillage on the berthing face. This structure consists of a steel grillageof the same section as the bearing piles but it is damaged and has no timberingattached. It is not evident whether the grillage originally had fender rubbersbetween it and the jetty. Apart from this damage and a small area of soffit

fZ71~~

U-)~ ~~

LU.

4 4~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~1

Fiur,.J Lyou CnTh Pr

4

spalling, this area of the quay is in excellent condition and appears to havebeen well built. The port has no drawings or loading data for this part of thequay and they report that no data exists in Vietnam. The study team isattempted to obtain copies of the drawings and loading data from the USmilitary without success. In the absence of any loading criteria, the port takesthe sensible view that this section is stronger than the newer section. Certainlythe construction appears more substantial than the newer part and shows nosign of distress from overloading.

2.09 The northern 83 m of the quay was built in 1980. It uses 350 mmsquare precast concrete piles supporting cast in situ beams. These in turnsupport precast slabs with an in situ topping and infills. There are no fendersapart from irregular bundles of vehicle tyres hung over the berthing edge. Atthe inshore edge of the slab there is a plate which shows a design loading of3.0 T/m. This section of the deck is constructed to very poor standards withconsiderable honeycombing of the concrete and some crude in situ makinggood around the top of the piles. Despite this the structure has suffered littlevisible deterioration. No copies of the construction drawings are held in the portand, at the time of writing, copies had not been located in the Ministry ofTransport. Since the design criteria have not been established, no absoluteview can be taken on the actual strength of the structure. It is understood thatlow concrete strengths have been assumed for the design and it is likely thatthe quay achieves the design strengths.

2.10 In September 1995 a project was started to infill the gaps betweenthe bridges at the back of the quay. These sections are similar in design to thenorthern quay area. The port planner watched the piles being cast and some ofthe early piles being driven. The standards of workmanship were reasonableeven if the cosmetic finish was rather poor. The piles were being driven to aset at a length of approximately 36 m below the finished deck level. The portstaff stated that the thinking behind filling in these gaps was that the narrowdeck and bridges made manoeuvring trucks difficult when loading large ships.They also wanted the ability to stuff and unstuff containers on the back edgeof the jetty. The infill sections have been designed for the same loading as thenorthern section of the jetty. This work is scheduled to be completed in May1996.

2.11 The jetty has a small water supply (75 mm) surface run along thejoint between the two sections. Behind the berth edge upstand this pipe has atee fitting to feed two hose connectors. This arrangement is used to supplywater to the ships although the port did not seem to know the rate at whichwater could be supplied. Otherwise the jetty has no services.

2.12 On the shore, some 23 m back from the jetty there are five lightpoles approximately 10 m high. Each pole carries two or three fittings severalof which have no bulb. It is understood that for night working the port relies onthe ship providing lighting.

5

c) Onshore Facilities

2.13 The two main cargo handling facilities on shore are a bitumensurfaced open storage area approximately 95 m x 60 m and a shed with anarea of 4,500 m2 . There are other areas available in the port but they are notsurfaced or drained.

2.14 The construction of the surfaced open storage area is not knownbut it was used for container handling for a year and appeared to have sufferedlittle damage. The area is drained by shallow perimeter ditches which againappears to work reasonably well. The entry and exit points across these ditchesis not well defined and this aspect needs further investigation and upgrading.

2.1 5 The cargo shed was built in 1982 but it is apparently never used.The metal roof has perforated over some of its area but otherwise the structureappears sound. The floor of the shed is concrete paved but the strength of thepaving is unknown. For modern port use, the doors on the shed are rather smalland would have to be widened if the shed were to be used for the handling ofbulky cargoes.

2.16 There is general area lighting for the perimeter road around theopen storage area. This is just about adequate for security purposes but not forsafe working.

d) Offices

2.17 At the road edge of the port there is a row of buildings which areoffices, workshops, rest rooms and a workers' hostel.

2.18 The largest of the office buildings houses the Port Director's officeand the main meeting room. This is in good condition with good qualityfurnishings and effective air conditioning.

2.19 The other three office buildings are of prefabricated constructionand need new roof sheeting. At present they are kept weather tight by acollection of odd sheets and tarpaulins. This gives this area of the port a ratherrun down appearance. These offices are not air conditioned but they aredesigned with a verandah and hence provide a comfortable workingenvironment.

2.20 Departments housed in these offices are

- Planning and Stevedoring;- Finance and Accounting;- Dock Office;- Material and Technical;- Transportation and General Dockers;- Medical Services.

7

B. Equipment

a) Port Equipment

2.28 Investment in equipment for the port is minimal and appears tohave occurred in a series of discrete packages rather than as a plannedprogramme. The newest items of plant on the port are the forklift trucks whichare 1 0 years old. Despite this, and a general lack of spare parts, most of theequipment is in serviceable condition.

2.29 The port does not appear to keep a definitive list of the equipment itowns but the lists given below are as discussed with the port management.This differs in some respects from the list giving the assets of the port and,since not all the equipment was present in the port during the study team'svisit, it has not been possible to verify which is correct.

b) Floating Craft

2.30 The port owns the following floating plant

Table 2.01 Floating plant - Port of Can Tho

Item Size Condition:Tug 1400 HP American built,scuttled in 1975. Refloated and in

sound but basic condition. A single screw tractor tug.Tug 135 H P Built 1982. Poor condition.

Barge 300 T Built 1982. Not inspected.

Barge 500T Built 1990. Not Inspected.

Floating Crane 15 T approx Age unknown. Reasonable condition.

This list corresponds closely with the port assets list.

c) Cargo HandlinQ Equipment

2.31 The Port owns the following cargo handling equipment

Table 2.02: Cargo handling equipment

Item Size Age . Co<mnents: :

Rubber Tyred Mobile Crane 25 T lift approx More than 20 years Moto-Crane Lorrain. Good Condition.

Rubber Tyred Mobile Crane ZOT lift approx More than 20 years Unknown make. Reasonable condition.

Rubber Tyred Mobile Crane Unknown Unknown Derelict.

2 No fork lift trucks 5 T 10 years Bulgarian made. Moderate condition. No______________ parts available. Substitute parts used.

2 Tractors 50 HP approx 10 years Czech manufacture. Moderate condition.

4 Trailers 20 T capacity Unknown 2 Usable but poor condition.2 Derelict

2 Lorries 30 T approx Unknown Russian Mars type.Not inspected.

The port asset list shows a further two lorries but these were not present atthe port during the study.

8

2.32 In addition to these items of equipment, the port owns a range ofcargo slings, nets and three grabs of approximately 1.5 m3 each. The conditionof the nets and slings is very variable. Two of the grabs are in moderatecondition and a third is in the process of being rebuilt.

d) Other Equipment

2.33 Besides the cargo handling equipment listed above, the port ownstwo cars, one van and one 12 seat minibus. All appear in good condition andare reported to cover quite small annual milages.

2.34 In addition to the usual tables, chairs and desks, the officeequipment consists of the following:-

Table 2.03: Other Equipment

tenm Age Comments

Various typewriters Unknown Used mostly by the traffic department and forcorrespondence.

Various Desk Calculators Less than 5 years

A3 size photocopier New Adequate for general office use

Intel 486 based desk top New Used mainly by the accounts departmentcomputer I_I

Laser printer New As above.

Fax machine New Frequently switched off and hence not available.

2.35 For the present level of operations this sis satisfactory but furtheroffice equipment will be needed to keep up with management functions if theport traffic increases.

9

C. Management

a) The Control of the Port

2.36 The port of Can Tho was until recently controlled by the provincialgovernment. Approximately two years ago the port was designated as aninternational port and control was passed to the Ministry of Transport. Thischange appears to have had little impact on the running of the port with thesame management team being retained.

b) The Management Structure

2.37 The port is managed by the Director assisted by two ViceDirectors. These staff have been in place for a number of years and they appearto have the present operations and manning arrangements. One consequenceof their period in office is that many of the present practices have evolved andare not fully documented. This makes any study such as this slightly difficult asmost information has to be derived from discussions rather than being availablein tabulated form. As an example, the team's requests for an organisation chartwere acknowledged politely but no chart was ever forthcoming. Evidently themanagement knew how responsibilities were divided and saw no need for suchdocumentation.

2.38 Below this upper layer of management, the port is split into thefollowing departments :-

- Planning and Stevedoring (Port Operations);- Finance and Accounting (Finance);- Dock Office (Services to ships);- Material and Technical (Maintenance);- Transportation and General Dockers (Personnel).

As described above, the exact split of responsibility between thesedepartments is poorly defined and any future management training must startwith a review of present roles and a documentation of responsibilities. Adiscussion with the managers indicated that these departments seem to covermost of a port's normal functions with some overlaps. There are however anumber of functions which are not covered :-

- There is no marketing department. At present the port's only promotion ofits capabilities are occasional advertisements in trade and local journals.This clearly shows the port's history as part of a planned economy. Thismust be addressed if the port is to take its share of the traffic in the Delta.

- There is very little financial planning in the port. This is shown by the porthaving the same planned trade in each of the last four years, in none ofwhich years has it achieved anything like the target. Similarly budgets forthe year are set in a purely nominal way with little regard for the definedneeds of the port. The tariffs for the port are set centrally and do notreflect the costs of the port.

10

- The technical department concerns itself purely with the equipment of theport, not even holding any drawings of the port's structures and buildings.If greater use is to be made of the port's facilities, the management musthave a better grasp of how they can be loaded and adapted to suitcustomers' requirements.

2.39 To cover these requirements will need some training of themanagement team and the addition of an experienced port engineer. The realneed is however for the management to be convinced that it is now operatingin a market environment and to be trained to handle the changes and pressureswhich this requires. The introduction of a genuinely performance basedincentive scheme would be very likely to provide most of the motivationneeded.

c) Customer Reactions to Management

2.40 A number of the port's customers were interviewed to find theirviews on the management of the port. All those interviewed commented thatthe port management was helpful, responsive and easy to deal with. Thecomment did however come out that the initiative for changes to operatingpatterns tended to come from the customers rather than the port staff.

D. Manning

a) Permanent Staff

2.41 In addition to the three directors and vice directors, the port isreported to have the following full time employees. No documents verifyingthese numbers have been found.

Table 2.04: Permanent Staff

Depermem Staff Numbers

Planning and Stevedoring 1 manager2 supervisors23 tally clerks

Finance and Accounting 1 manager6 clerks

Dock Office 1 supervisor3 clerks

Materials and Technical 1 manager2 supervisors3 clerks3 technicians6 part time technicians

Transportation 2 supervisors24 operators

At the present traffic levels, it would appear that these staff are generallyunder utilised and that they could deal with at least a doubling of throughput.

1 1

b) Casual Labour

2.42 The labourers working in the port are employed on a casual basisbeing drawn from a pool of about 300 registered workers. They are employedalmost entirely on a piece work basis with no guaranteed minimum payment.On this basis a man could report for work but if it rains all day, he will get nopayment. On average the labourers work in the port for approximately 1 2 daysper month, most being farmers for the rest of the time. The labourers areresponsible for their own transport to work and most seem to walk or travel bybicycle.

2.43 This system has of casual labour has many advantages for the portbut at present the labour pool is probably too small to handle a higherthroughput or true multi shift working. With the high population density in theDelta, there should be no problem increasing the labour pool so that anincreased throughput can be achieved without disrupting the workers' otheractivities.

c) Skill Levels

2.44 During a few days observation, the work of the port appeared tobe carried out with good personal skills and the loading gangs achieved goodthroughputs for the technology used.

2.45 The checking and monitoring procedures seemed to be wellorganised and worked in a smooth but very labour intensive manner.

2.46 The ability of the maintenance technicians to look after an elderly,if lightly used, collection of equipment is impressive. They are obviously wellpractised at repairing and rebuilding components with whatever materials cometo hand. With new plant, these technicians may well have to learn some newskills and the introduction of proper lighting and reefer power supplies willrequire the port to take on a full time electrician.

2.47 The finance department seemed to produce rather erratic figuresbut it is difficult to tell whether this was a function of the individuals or thesystems in use. The introduction of a new accounting system this year shouldaddress this issue.

2.48 As described above, the main skill deficiencies can be identified asbeing in the areas of marketing, operations planning and budgeting. These areall functions carried out at a senior level in the organisation and it is at managerlevel and above that the training effort should be concentrated.

12

E. Access to the Port

a) Access by Road

2.49 The port is situated adjacent to the main road north-west out ofCan Tho and this is able to handle considerable volumes of traffic. Like allmajor roads in the Delta it suffers from the many bridges having very poortransitions and not being able to carry trucks above 1 8 or 25 Tonnes. Thismakes it impossible to carry full 40' containers more than a few kilometresfrom the port. There is a programme of upgrading bridges but this will takemany years to complete.

2.50 The proposed bridge across the Bassac River just downstream ofthe port will make it much easier to bring cargo from the east and north butother trunk road improvements will also make it more attractive to take thiscargo to Ho Chi Minh City.

2.51 The immediate entrance into the port is rather sharp with very littlerun off area from the main road. This is readily corrected by small changes tothe layout and safety would be greatly improved.

b) Access by Barae

2.52 At present, more than half the port's cargo arrives by barge orcountry boat. This is a very efficient form of transport and is encouraged byCan Tho's position at the centre of the Delta waterways system. Inlandwaterways access to Can Tho will be improved by the upgrading of thewaterways proposed elsewhere in this study.

2.53 One problem with the present fleet of inland waterways craftwhich serve Can Tho is the layout of the typical wooden country boat. Thiscraft has developed around loading and discharge by manual labour andgenerally the hatches are.too small to allow the use of full sized cargo nets andslings when handling bagged cargo. As more of the rice mills developmechanised loading docks, the country boats will be adapted to have largerhatches. Also with time, it is likely that there will be more steel built barges inthe fleet and these are likely to have modern hatch arrangements.

c) Shivoina Access

2.54 The published information about Can Tho shows it to be accessibleto ships of 3,000 DWT at all states of tide and 5,000 DWT at high tide. Thesefigures have led to the perception that Can Tho is a small port only suitable forcoastal trades.

2.55 In fact these published figures are highly misleading since accessto the port is fixed by the water depths available in the Dinh An channel at themouth of the Bassac River. The charting of this channel is not good withinsufficient soundings being available to determine the true water depthsavailable at different seasons. There is a planned study of the regime of theBassac entrance and this is very important for the future of the port.

1 3

2.56 It would appear from the available information that there issufficient depth in the entrance to allow ships with a draft of 7.0 m to transitthe channel and it is known that vessels of up to 7.5 m have used the river.Given the tidal range of 3.0 - 3.5 m, this would equate to full tide access forvessels of up to 4.0 m draft. Appendix II gives details of typical general cargoand container ships in this size range.

2.57 These shipping lists clearly show that there are many vessels of upto 7,000 DWT able to access the Dinh Ahn channel and that careful choice ofship gives up to 1 2,000 DWT. These figures assume that the vessel is laden tofull draft but often cargo densities leave a ship at less than her maximum drafteven when fully laden. A recent example of this was the call at Can Tho by an11,000 DWT ship which left with 8,000 T of cargo at a draft of 7.2 m.

2.58 If the ability to take ships of up to 7.5 m draft were more widelypublicised, it would make the port much more attractive to shippers evenwithout the planned deepening of the Dinh An channel.

2.59 The Port of Can Tho has a minimum alongside depth of 10 m sothe capacity of the quay is not a constraint on ship size.

14

3. PORT TRAFFIC

A. Historical Traffic

a) Overall Traffic Handled

3.01 The traffic through the port of Can Tho has varied widely over thelast few years. Full historical cargo data for the years 1 990-94 and preliminarydata for 1995 were obtained from the port and have been analysed.

3.02 The statistics kept are reasonably comprehensive for the size ofport but they suffer somewhat from the headings changing year to year. It hastherefore been found necessary to modify the cargo groups in order to give aconsistent picture of the cargo passing through the port. Table 3.01 shows themodified version of the same table.

Table 3.01: Can Tho Port Cargo Throughputs (Tl

Year 1990 1991 1992 1993 1994 1995

Cargo Total 92,689 105.827 59,419 53,903 65,870 123,277

Exports 43,758 46,101 30,570 9,710 44,106 98.774

Rice, food, Agri products 33,253 20,683 10,889 9,107 26,081 98,774

Seafood 7,992

Wood 19,406 603 10.032

Miscellaneous 10,505 25,418 275

Imports 43,818 55,034 6,210 28,533 13,607 8.201

Construction Materials 7,937 3,261 6,300 8,685 2,756

Fertiliser 15,507 15,555 5,501 20,807

Flour, sugar 11,921 28.233 203

Miscellaneous 8.453 7,985 506 1,426 4,922 5,445

Domestic Cargo 5,113 4,692 22.639 15,660 8,158 16.302

Fertiliser 979 721 726 399

Cement 2,498 2,603 17,107 13,385 15,392

Food 1,080 1,412 693 1,513 5,527

Wood 298 589

Coal 163 450 910

Agricultural Products 1,193

Miscellaneous 556 216 4,118 36

Ship Calls 137 68 64 63 94 86

Foreign 50 42 22 21 59

Vietnamese 57 23 36 39 29 86

Barges 30 3 6 3 6

Working Days 257 203 217 181 169 ?

Weather Delays 16 12 18 8 18 ?

Holidays 10 10 10 12 12 7

No Ship 82 140 121 164 166 ?

3.03 Domestic cargo in the above tables is defined as being importcargo from within Vietnam. This may have arrived by sea from northernVietnam or it may have arrived by barge from a more local source.

1 5

These changes in throughput are demonstrated below.

Can Tho Port Cargo Throughputs

140,000123,27

120,000- 105, 827

10, 000- 92,89

s0,0000 9 65,870

60, 0001 . b4 303

40,00e 111 11

1.990 1991 ±992 1993 1394 1995

Yea

As can be seen, the total throughput of the port has almost doubled between1994 and 1995.

b) Changes in Traffic Patterns

3.04 The cargo traffic using the port has seen quite substantial changesover the last few years. This is not unusual in small ports but the presence ofthe competing Ho Chi Minh ports close by makes the trade through Can Thoparticularly volatile.

3.05 One example of the irregular pattern of trade is the container tradethrough the port. In November 1 993, Maersk started a container servicebetween Can Tho and Singapore. This service was operated by the small(1,210 DWT, 61 TEU) container vessel Marie Riis following a triangular routeSingapore - Vung Tau - Can Tho - Singapore. In the second half of 1994, thisroute was varied to be sometimes direct Singapore - Can Tho - Singapore andsome times calls in Thailand were included. In late November 1994, the largerMekong Harmony (3061 DWT) took over the route but the service wascancelled with one month's notice at the end of 1994. Despite its short periodof operation and slightly irregular scheduling, (intervals varied from 7 to 17days with a 9 day mean) this service attracted regular business from the frozenfood export market, a field which is otherwise not addressed by Can Tho Port.Table 3.02 shows the cargo types and tonnages carried by the service.

16

Table 3.02: Can Tho Port - Container Traffic 1994

Call Vessel Arrival DepartLsre Cargo in Torks Cargo Out Tons

Number Misc Agricultural Reefer Wood Rice

4 Marie Riis 31-Dec 01-Jan 13 11 136

6 Marie Riis 07-Jan 10-Jan 8 90

7 Marie Riis 17-Jan 17-Jan 7 32 402

9 Marie Riis 03-Febi 03-Feb 26 13 241

10 Marie Riis 14-Feb 14-Feb 183

11 Marie Riis 23-Feb 23-Feb 180 158

14 Marie Riis 03-Mar 04-Mar 9 251 310

18 Marie Riis 11-Mar 11-Mar 48 181 149

19 Marie Riis 19-Mar 19-Mar 29 96 159

20 Marie Riis 26-Mar 26-Mar 8 21 335

21 Marie Riis 11-Apr 11-Apr 20 49 343

22 Marie Riis 19-Apr 19-Apr 21 64 196

23 Marie Riis 03-Apr 03-Apr 16 98 101

25 Marie Riis 27-Apr 27-Apr 145 83 252

26 Marie Riis 03-May 03-May 103 59 252

28 Marie Riis 13-May 1 3-May 159 232

29 Marie Riis 20-May 20-May 44 30 162

33 Marie Riis 28-May 29-May 14 8 306

35 Marie Riis 05-Jun 05-Jun 4 25 284

37 Marie Riis 13-Jun 13-Jun 39 156 185

39 Marie RAis 21-Jun 22-Jun 85 242 27

41 Marie Ails 29-Jun 30-Jun 596 23 132

43 Marie Riis 08-Jul 08-Jul 30 1 31

47 Marie Riis 14-Jul 16-Jul 296 86 110

49 Marie Riis 21-Jul 22-Jul 370 126

52 Marie Riis 2 27-Jul 27-Jul 413 86

55 Marie Riis 05-Aug 05-Aug 121 16 93

59 Marie Riis 20-Aug 20-Aug 63 139 377

60 Marie Riis 26-Aug 27-Aug 66 116 67

65 Marie Riis 01-Sep 01-Sep 51 46 56

67 Marie Riis 07-Sep 08-Sep 464 19 17

69 Marie Riis 13-Sep 13-Sep 76 80 99

70 Marie Riis 19-Sep 19-Sep 37 28 116

74 Marie Aiis 25-Sep 25-Sep 13 100 113

75 Marie Riis 03-Oct 03-Oct 46 6 168

77 Marie Riis 11 -Oct 11 -Oct 102 193

78 Marie Riis 19-Oct 19-Oct 132 159 137

82 Marie Riis 27-Oct 27-O0t 73 68 155

83 Marie Riis 05-Nov 05-Nov 7 146 107

84 Marie Riis 14-Nov 1 5-Nov 36 267 265

86 M e k o n g 25-Nov 25-Nov 240 86 279Harmony _

88 Mekong 15-Dec 15-Dec 119 240 238Harmony

Totals 4154 3404 7282 0 101

Averages 106.51 92 182.05 101

1 7

Call Vessel j Arrival Departure Cargo In Tons Cargo Out Tons

Number Misc Agricultural Reefer Wood Rice

N o o f Imports ExportVoyages

full empty full empty

42 358 474E596 255

Average cargo weight per container Imports 11.60

l___________ __________ Exports 18.10

Average box exchange per call Full 22.71

(Total on and off) Empty 17.36 _

3.06 Without a container service from Can Tho it is going to be verydifficult for the port to diversify away from the shipment of bagged agriculturalproducts. The full reasons for the Maersk service closing have not yet beenestablished but the fact that a service has already been seen to fail will make itmuch more difficult for the port to attract a replacement service. It is mostlikely from the figures that the main reason for the closure was simple lack oftrade.

3.07 To establish a new service, a sustained marketing campaign will beneeded and it may be necessary for the port to provide additional facilities insupport of the operation. With the earlier service, virtually all the containerswere taken from the ship's side by trailer and put down in the container yard.there they were emptied and the cargo loaded onto lorries. Outgoing cargoesarrived by lorries and were stuffed in the port. This is a relatively inefficientway to use containers but it is dictated by very few of the end customershaving facilities to handle containers on their own premises. This could beaddressed by the *port operating a container delivery service using selfdischarging container lorries helping to boost traffic. Ideally the port shouldstick to its core business but it may be difficult to persuade an outside operatorto invest in the necessary plant.

3.08 In a similar way, there may be scope for the port to operate a coldstore facility to assist in the groupage of refrigerated cargoes. Alternatively, anexisting cold store operator may be able to provide this service, possibly inconjunction with the container delivery service described above.

3.09 One feature of the earlier service was the very high proportion ofempty containers (43% of imports, 30% of exports) carried. This is quitecommon with small container services and is a result of differing patterns oftrade inbound and outbound. In this case most of the inbound trade ismiscellaneous cargo shipped in plain containers whilst most exports arerefrigerated cargo in reefer containers. Unless there is an increase inconsumption of frozen food in the delta, which is unlikely, there seems no wayof correcting the imbalance for reefer containers. When Can Tho develops as aregional distribution centre, more goods should be shipped in direct bycontainer and hopefully this can be balanced by the development of newindustries exporting manufactured goods.

18

B. Port Traffic in the South of Vietnam

a) The Network of Ports

3.10 At present, together with the development of Saigon port complex,a system of sea and river /sea ports has been developed from the southern areaof the Middle Region to the South Region such as : Cat Lo port (Ba Ria - VungTau), Go Dau port (Dong Nai), My Tho (Tien Giang), Tran Quoc Toan (DongThap), Vinh Thai (Vinh Long), Can Tho port (Can Tho), My Thoi (An Giang),Hon Chong (Kien Giang), Nam Can (Minh Hai). These are small scale ports withthe accessibility for 1,000 - 5,000 DWT ships and the capability of 50 -250,000 T / year. The main reasons for these low trade levels are inability toattract cargo and shallow access channels.

3.11 As shown in National Transport Development Strategy, 3 MaritimeTrade Centers will be developed in the South in near future. They are: HCMCport complex, Thi Vai - Vung Tau port complex and Can Tho port.

1. HCMC port complex:

Though there will be many changes of the cargo flows from Mekong Delta tooutside provinces; a proportion of agricultural products, foodstuff, agriculturalmaterials and some other cargoes will not be trans-shipped to HCMC area.HCMC still takes the key role as the main gateway to the South. HCMC has andominant position of trade, service, industry and socio - economic advantages.It would take at least 20 years and the investment of about 2 billion dollars todevelop a port with equipment to match the HCMC port complex. Hence theHCMC port complex will continue to be upgraded, improved and developed inparallel with other ports.

2. Vung Tau - Thi Vai port complex:

At the end of the 20th c.entury, the international deep sea shipping market hasmade may changes, especially in transporting container, bulk cargo, liquidcargo and over-length, over -weight cargoes. With the tendency of using large-size vessels worldwide, there should be deep-water ports with modernequipment to facilitate the cargo handling. The HCMC port complex accesschannel along the Long Tau river has restrictions of width and depth. Therehabilitation of this access channel needs much of investment and effort. As aresult a deep-water port complex will be developed in Vung Tau - Thi Vai areafor large vessels in case as a more effective option.

Functions of Vung Tau - Thi Vai deep-water port complex:

- Handling bulk cargo : bauxite and alumina.- Specialized berth for oil exploitation in the South.- Specialized berth for paper materials from eucalyptus wood.- Specialized berth for Go Dau industrial park, Long Thanh phosphate

fertilizer factory.- Trans-shipment berth for cargo and raw materials from other provinces for

export.- Berth for International Maritime Services.

1 9

3. Can Tho port:

The Mekong Delta Master Plan indicated that Can Tho will become a majorcentre in the economy of Mekong Delta. Can Tho port will be a major port forhandling bulk, bagged cargoes and container in Mekong Delta. Once theimprovement ot the Dinh An access channel is completed and the Bassac riverbecomes the major navigation route, Can Tho port should be upgraded tobecome the trans-shipment port for Saigon, Vung Tau ports and internationalports such as Singapore and Hong Kong. It will also be the port for transferringcargo between the Mekong Delta and Cambodia. Can Tho port will be thegateway for cargo transport to the 5 provinces in the southern area of Bassacriver (An Giang, Can Tho, Soc Trang, Minh Hai, Kien Giang) and a part of theprovinces: Vinh Long, Tra Vinh, Dong Thap. At present, cargo from the Northand foreign countries transported to these provinces must be transferredthrough the ports in HCMC. The upgrading of Can Tho port will share the hugevolume of cargo at these ports, and concurrently push up the production, thusmaking an important contribution to the economy of the above provinces andchanging Can Tho into a trade center of domestic and internationalsignificance.

3.12 The access channels:

1. Saigon - Vung Tau access channel:

The present Saigon - Vung Tau access channel runs along Nga Bay river,reaches to Long Tau, Nha Be rivers and goes into Saigon river. The bed riverhas the width of 800 m at some widest places and about 200 m at thenarrowest place. The bed channel elevation is about 8.2 -9.6 m except somehard clay shallow places. There are several bending sections with small bendradii on the channel line that makes difficulties for vessel passage (especially atL'EST point). The 95 km long of the access channel is divided into 7 parts

Part 1: From the beginning to Bai Yen (Ganh Rai)+ Channel width : 200 m+ Smallest channel depth : 9.6 m / OTS

Part 2 : From Bai Yen to Bon Mat river ( Stand N°13)+ Channel width : 400 m+ Smallest channel depth : 10 m / OTS

Part 3: From Bon Mat river to An Thanh point (Stand N°1 5):+ Channel width : 200 m+ Smallest channel depth : 8.2 m /OTS

Part 4 : From an Thanh point to Dong Tranh river (Stand No1 6):+ Channel width : 150 m+ Smallest channel depth : 7.0 m/OTS

Part 5 : From Dong Tranh river to Pha Mi point (light stand No1 8):+ Channel width : 200 m+ Smallest channel depth : 9.6 m/OTS

20

Part 6: From Pha Mi point to Den Do point:-+ Channel width : 200 m+ Smallest channel depth : 8.5 m/OTS

Part 7 : From Den Do point to Saigon port:+ Channel width : 150 m+ Smallest channel depth : 8.5 m/OTS

3.13 To provide the accessibility for large vessels, the Maritime Bureauhas approved the channel improvement project. After being rehabilitated theshoals then have the depth of about - 8.4 m deep. With little dredging workand unchanged natural conditions the channel can provide the accessibility forfully - laden ships of 18,000 DWT at high tide (> + 1.30 m).

3.14 There are 5 segments that have the depth of under - 8.4 m onchannel alignment from Vung Tau to the port:

- Can Gio mouth : about 3.5 km- Dan Xay area : about 1.0 km- Keverlla point area : about 1.5 km- LEst point area : about 3.5 km- The area near red light : about 1.5 km.

3.15 The dredging volume at 11 km of shoals is 1,350,000 m3. Somesections with bending radius R = 1,000 m will be widened with B = 250 m,so that bending radius will be 5,000 m. From 2000 forward, according to thestudy on the changes of current, the L'Est point and bending sections will bestraightened for safe passage of vessels. The volume of dredging and bendingis about 2,000,000 m3 .

3.16 Beside, with urgent requirements to widen the field of action tomeet the demand of international shipping route, the People's Committee ofHCMC has decided to carry out the study on dredging of Soai Rap river toprovide surface for the urbanization and industrial development. Soai Rap riveris the second navigation channel for foreign vessels going in and out of theHCMC port complex. The present depth of Soai Rap river is less than that ofLong Tau river but it is short and straight with the width of 1,000 m.

3.17 The purposes of the dredging of Soai Rap river:

- Forming a new, safe and short navigation channel for foreign ships goinginto / out of the HCMC port complex;

- Taking sand from the shoals, transferring to the lowlands in the south ofHCMC to provide the surface for the construction of the new urban andindustrial areas such as the Hiep Phuoc Industrial Zone;

- Developing a new berth to meet the increasing demand of exporting inHCMC and the Southern region.

21

3.18 The natural resources and environmental condition at the mouth ofSoai Rap river have been surveyed by the Tan Thuan Industrial DevelopmentCompany belonging to the People's Committee of HCMC in association withexperts and specialized agencies such as Professor Tran Kim Thach - Doctor ofGeology, Southern Hydraulics Science Institute (Ministry of Hydraulics) to studythe possibility of developing the channel for large - size vessels. The studyconsists of

- Positioning the channel alignment and planning the dredging of the channelon Soai Rap river, study on the stability of the channel;

- Bending the Nha Be - Long Tau T-junction to improve the navigationcapacity at present natural condition;

- Evaluating the effect and influence of the dredging work on the meteo-hydraulics behaviour of the downstream river network of Dong Nai - Saigonrivers and changes of saline intrusion.

3.19 The feasibility study was due to be completed at the end of 1995.If the technical features and economical effects are feasible, the HCMC portcomplex new access channel will be at the same grade with Thi Vai - Vung Tauaccess channel and it's potential will be beyond the present predictions.

2. Thi Vai access channel:

3.20 The operating access channel of Thi Vai with the length of about40 km including 12 km from channel dividing buoy to the mouth of Cai Mepriver and 28 km from Cai Mep river to Go Dau port is divided as follows

Part 1: From channel dividing buoy to buoy N°5+ Channel width :150 m+ Smallest channel depth :10.5 m / OTS.

Part 2 : From buoy N°5 to buoy N1 5+ Channel width :150 m+ Smallest channel depth : 9.8 m / OTS

From buoy N° 5 to Go Dau port+ Channel width :80 m+ Smallest channel depth : 6.5 m / OTS

VEDAN access channel part : from buoy N020 to VEDAN berth+ Channel length :1,400 m+ Channel width :80 m+ Smallest channel depth : 6.2 m / OTS

3.21 The Thi Vai river system consists of Thi Vai river, Go Gia river andCai Mep river. Thi Vai - Cai Mep river, 40 km long, runs in South - Northdirection almost in parallel to the National road N051. The average depth is 15 -20 m, the deepest place (Thi Vai-Go Gia - Cai Mep junction) is 30 m deep. It'saverage width is 500 -600 m and on Cai Mep river there are some placeshaving a width of 1,000 m. With little volume of dredging the access channelof Thi Vai and Cai Mep river can accommodate 30,000 DWT vessels at hightide.

22

3.22 At present, there is a bending segment with bending radius R =300 m from Ganh Rai bay to Go Dau whose accessibility only for 3,000 DWTvessel; if using tug - boat, the 5,000 DWT vessel can go through. There shouldbe measures of dredging and bending at Go Dau access channel for 10,000DWT vessel passage.

3. Dinh An access channel

3.23 Dredging through the outer bar in 1 981 and again in 1983 failed tosustain improved depths of 4.2 m below chart datum (= Lowest Low Water)and the channel was lost after a few months. However, in July 1991 a channelwith a bottom width of 75 m was dredged to -4.5 m over a 75 km reach on adifferent more northerly alignment, again with the intention of permitting highwater access for ships of 5,000 DWT or more. This dredging was moresuccessful and the latest bathymetric survey in September 1993 shows a leastdepth of 3.5 m below chart datum along the channel and generally channellevels are in excess of 4.0 m. Since the last dredging it is reported that severalvessels with drafts up (equivalent in government tables to fully laden cargoships of 5,000 DWT) have made the passage to Can Tho and in someinstances to Phnom Penh. However, the pilots had to time the crossing of thebars to make entry to the Bassac river on the Higher High Water of SpringTides i.e when water levels were at least 3.0 m above chart datum.

3.24 The operating access channel to Can Tho port is 110 km long (59miles) including 31 km of Dinh An access channel (from buoy 0 to the stand13) with the channel width of 150 m and the average depth of 3.9 m / OTS.

b) Comparative Shiwoina Costs from Can Tho

3.25 In considering future trade from Can Tho, the most importantsingle factor is the competition between Ho Chi Minh City and Can Tho. Sincethe main Vietnamese shipping industry is based in HCMC, and has all itsstorage facilities there, the natural tendency is to ship through that port. Only ifCan Tho shows a significant voyage cost advantage will it gain a significantmarket share. Set out below are the significant shipping cost differencesbetween Can Tho and HCMC.

1. Current transport costs for different categories of cargo HCM City toCantho and vice-versa ( rice, fertilizer, container, general cargo, refrigeratedcargo).Transport costs:By waterways

Rice 3.60 USD/TFertilizer 4.10 USDITContainer 3.64 USD/T

By road:General cargo 7.60 USD/TRefrigerated cargo 29.10 USD/T

The above are the bare freight costs between the two centres. It isunderstood from shippers that there are other costs associated withshipping delays which push the total costs above US$ 6 per Tonne.

23

2. Storage charges for the above mentioned cargoes in Saigon and CanthoPorts are based on the same port dues issued by the State Committee ofPricing.

3. The differences between port charges in Cantho port and those in Saigonport are caused by the following reasons:

- The length of access channelAccess channel of Saigon port 51 miles.Access channel of Cantho port 59 miles.

- Pilotage dues:Saigon port: 0.003 USD / GRT. mile.Cantho port: 0.0038 USD / GRT. mile.

4. Table 3.03: The current freight for sea transport on domestic routes

Cargo/lSizeofship iSaigon-Maiphong Cantho4iaiphgng.

Rilce O100000

5000 115,000 125,000

10000

15000

Ger eral 3000

5000 135,000 145,000

10000

15000

Ge~neral 30~00~

5000 135,000 145,000

10000

15000

The Vietnamese government sets these internal transport rates such that thenormal economies of scale in shipping do not operate on this route. Theconsistent freight differential of VND 10,000 per Tonne (US$ 0.91/T) is easilyexceeded by the transport costs to get goods to HCMC. While this tariffpersists, there is a US$ 2.60 per Tonne saving by shipping goods for the Norththrough Can Tho.

5. International shipping costs.

The following are comparative to various representative internationaldestinations

24

Table 3.04 International shipping costs from South Vietnam

Destination Distance Ship Size Speed Alongside Time Shipping Cost per T

[Nautical Miles] IDWTI [Knots] [Days] [US$1

Manila 907 3,000 11 4 8.09

5,000 12 4 5.82

10,000 14 6 4.11

15,000 16 8 3.31

Jakarta 1,032 3,000 11 4 8.68

5,000 12 4 6.24

10,000 14 6 4.33

15,000 16 8 3.44

Dubai 4,076 3,000 11 4 23.29

5,000 12 4 16.39

10,000 14 6 9.68

15,000 16 8 6.66

Rotterdam 8,934 3,000 11 4 46.60

I ____________ ______________X 5,000 12 4 32.58

10,000 14 6 18.21

15,000 16 8 11.81

Los Angeles 7,190 3,000 11 4 38.23

5,000 12 4 26.77

10,000 14 6 15.15

15,000 16 8 9.96

Miami 11,061 3,000 11 4 56.80

5,000 12 4 39.67

10,000 14 6 21.94

.___ __ _ 15,000 16 8 14.06

From the above it can be seen that, even if Can Tho is restricted to 5,000 DWTships, there is a clear cost saving for all shipping to South East Asia. Shipmentsto the Arabian Gulf region only become viable if the extra costs through HCMCexceed US$ 6 per Tonne or if 10,000 DWT ships can be used.

25

C. Present Cargo Trends

3.26 Evaluation on production and consumption capacity of the majorcommodities in the attractive areas

The southern area of the Bassac river has an area of 23,51 2km2, i.e 54.42% ofthe total area of the Delta. In 1994, the Mekong Delta provided about 12million tons of paddy, i.e 50% of the total national output, in which 6 milliontons came from the southern area of the Bassac river. This is where 8.1 millionpeople settle, that is 51.12% of the whole Mekong Delta population. Theproducts by whom play an important role in export, especially rice andprocessed aquatic products export. This has been shown through the followingstatistical data:

Table 3.05: Gross output of food (paddy equivalent) by provinces (1,000 T)

ID11 i::0$070 0 i;Region 1.990 J 1991 11992 1993 1 994

WHOLE COUNTRY 21,488. 21,989.5 24,214.6 25,501.7 26,198.5

A NORTH 8,448.4 7,834.6 9,701.2 10,797.8 9,882.8

1 North mountain and midland 2,349.6 2,367.4 2,832.9 3,162.1 2,955.8

2 Red river delta 4,100.7 3,456.7 4,693.1 5,388.1 4,619.1

3 North central coast 1,998.1 2,010.5 2,175.2 2,247.6 2,307.9

B SOUTH 13,040. 14,154.9 14,513.4 14,703.9 16,315.7

1 South central coast 1,875.6 2,027.3 1,853.9 1,732.2 2,034.3

2 Central Highlands 581.0 606.9 618.6 634.2 664.4

3 North East South 975.7 1,056.7 974.3 1,135.6 1,327.7

4 Mekong river delta 9,607.8 10,464.0 11,066.6 11,201.9 12,289.3

5 Southern region of Bassac river 5,025.6 5,578.6 6,124.6 6,106.3 6,699.6

a An Giang - 1,498.4 1,539.4 1,760.7 1,848.9 1,898.8

b Can Tho 1,112.3 1,215.0 1,371.7 1,237.6 1,481.5

c Soc Trang 629.3 778.2 833.0 701.7 1,002.3

d Kien Giang 879.1 944.3 1,022.1 1,120.0 1,223.9

e Minh Hai 906.5 1,101.7 1,137.1 1,198.1 1,093.1

5/4 (5) 52.31 53.31 55.34 54.51 54.52

3.27 In 1994, the Mekong Delta exported nearly 1.8 million tons of rice,which means it has an enormous potential for agricultural production. Theagricultural products contribution of the southern area of the Bassac river isvery important because its surplus of food (paddy equivalent) is highest incomparison with that of the whole country. The food average output percapita in 1994 was 769.8 kg, i.e 2.14 times and 1.07 times as much as thoseof the whole country and the Mekong Delta respectively.

26

Table 3.06: Gross output of food (kg paddy equivalent) per capita by provinces

ID Region 1990 1991 1992 . 1993

WHOLE COUNTRY 324.4 *245 35

A NORTH 255.0 231.3 271.4 312.7

1 North mountain and midland 230.0 200.0 239.2 261.0

2 Red river detta 294.5 256.5 346.4 389.8

3 North central coast 226.0 222.1 233.7 236.4

B SOUTH 406.7 418.7 431.1 402.9

1 South central coast 274.0 289.8 257.4 234.7

2 Central Highlands 223.7 225.7 220.6 217.4

3 North East South 160.5 129.0 115.3 130.4

4 Mekong river delta 658.2 703.1 727.3 721.3

5 Southern region of Bassac river 674.3 733.1 788.3 769.8

a An Giang 811.1 832.1 928.2 956.3

b Can Tho 631.5 714.6 787.5 695.6

c Soc Trang 693.2 726.6 599.0

d Kien Giang 712.0 714.6 788.3 844.3

e Minh Hai 564.8 745.9 675.9 696.5

| 5/4 102.44 104.27 108.39 106.72

3.28 In 1993, with the population of 7.9 million and the agricultural land usearea of about 1.550 million ha, the southern area of the Bassac river generated54.51 % of the total food output (paddy equivalent) of the Mekong Delta. Inthat condition, the surplus food volume and the consumption demand of somemajor commodities in the southern area of the Bassac river are to be estimatedas follows

Table 3.07: Computed data of essential goods for production and livingdemand in the Southern provinces of Bassac river in 1993 (1,000 T)

ID , Region Uc Fertilizer .Ceivent Sted Constructin Totamateel-ms

A Mekong Delta nver ,632 932 23 ' 3172 5

B The Southern provinces of Bassac 2,479 661 476 119 1,904 5,639river

1 An Giang 776 154 116 29 464 1,539

2 Can Tho 542 135 107 27 427 1,238

3 Soc Trang 374 98 70 18 281 842

4 Kien Giang 481 132 80 20 318 1,031

5 Minh Hai 306 142 103 26 413 990

8/A (°h) 1 41% 5 i Yo 51% 5S2%

27

3.29 Along the southern bank of the Bassac river, there are 2 ports CanTho and My Thoi that can receive ocean ships. Cargo is still handled at theabove mentioned ports but these ports have not been able to attract the cargoflow to achieve their potential and the transport demand of the region. Thereare many reasons leading to such a situation. The main reason results from thesedimentation at the Dinh An mouth which creates obstacles to navigation oflarge sea-going vessels. In many cases this is more a perceived than actualproblem. In addition, the subjective reasons that cause the little attraction ofCantho port to the ship-owners and cargo-owners are:

- The port's infrastructure like quay, storage, warehouse, handling facilities,etc are perceived to be in poor condition.

- The operational management of the port has not caught the marketmechanism.

- The Government's policy has not encouraged the state cargo-owners toimport and export cargo through Cantho port to reduce costs.

- The other services for the importation and exportation at Cantho port arenot synchronous.

3.30 Perhaps because of the above said subjective causes, the exportrice from the Mekong Delta to the ports in South East Asia (accounting forabout 58.38%) is transported mainly through Saigon port. These maritimeroutes do not require large-size ships (up to 10,000 DWT). The following is theoutline statistical data of rice from the South of Vietnam exported to thevarious areas in the world in 1994.

Table 3.08: Export of rice from the South Vietnam, 1994

Totl ii: Africa APera 4Astlia[ i4Eupe SE-Asia NE-Asia Midde- Other

1,212,349.45 (T) 752.50 74,342 18,640 298,984.25 718,172.65 87,665 13,015.75 18,600.30

Density % 10.000611 0.06043 10.01515 0.24304 0.58380 0.07126 0.01058 0.01512

3.31 The consulting data of ships entering and going from Saigon port in1 993 shows that there are 1,788 ships up to 10,000 DWT in the total numberof 2,464; accounting for 72.56%. If almost of these ships transport import andexport cargo from the southern area of Bassac river through Cantho port, andthe Vietnamese importers and exporters endeavour to export and import cargothrough Cantho port, the cargo throughput at Cantho port in recent years willnot the fore-mentioned figures. The following is the number of ships enteringand leaving Saigon port in 1993.

Table 3.09: Number of ships entering and leaving Saigon Port 1993

Sizeofsip Qhuanty i Totalf.DWT .Total IofGRT Rateofshp :RateofDWT

DWT= < 10000 1.788 6,768,499 5,175,009 72.56% 34.31%

DWT> 10000 676 12,958,885 8,701.729 27.44% 65.69%

Total 2,464 19.727,384 13,876,738 100.00% 100.00%

28

3.32 Due to the present limitations of the ports in the Delta, especially CanTho port, the biggest sea port on the Southern bank of the Bassac river, thecirculation of goods between the Mekong Delta and its outside areas has beendone mainly through ports in Ho Chi Minh city.About 85-90% of the totalvolume of the Delta's export cargoes have been handled at the HCMC portcomplex, most of which at Saigon port. Rice produced in the Mekong Delta hasbeen transported to Ho Chi Minh city for export, and fertilizers, steel, machineshave been imported via Ho Chi Minh city for the Mekong Delta.

Table 3.10: Cargo throughputs at Saigon Port (T)

Year 1990 1991 1992 1993 1994

Total 47, f5,003,986 5 5 6,438,577

1. Export 2,085,582 1,625,781 2,495,953 2,359,659 2,551,758

Rubber 5 10707 X867 1,675

Rice 1,345,821 964,069 1,674,339 1,514,698 1,679,989

Agro-products 101.106 102,697 162,786 88,261 78,568

Fruits 38,271 12.624 3,106

Timber 274.127 261,863 143,532 16,967 5,250

Foodstuff 17,579 18.534 3,809

Frozen products 49,291 31,194 16,118 15,546 1,878

General cargoes 138,018 172,261 347,291 498,919 505,979

Others 67,976 51,832 142,105 223,593 280,094

2. Import 1,789,889 1,883,028 1,911,537 2,727,781 3,468,257

Foodstuff 1,77 15761 23T75 1 2,Cement 334.079 88,805 111,048 141,767 328,482

Clinker 34,419 267,196 438,954

Fertilizer 656.702 1,081,477 757.584 460,720 643,051

Machinery 82,435 74,575 16,510 93,818 107,313

Equipment 166,100 82,345 154,434 499,790 360,446

Chemicals 47,923 23,505 46,218 77,464 127,269

Asphalt 219 4,035 20,258 28,488

Cotton 16,174 10.603

Paper 13.450 7.184 8,212 24,314 20,887

General cargoes 215.201 237,401 453.308 723,467 866,506

Others 102,529 91,372 90,864 242,841 323,789

3. Domestic 471,684 650,810 596,496 421,185 418,562

Coal 67,2 47,75 78,17 6,023 3897Fice 244,029 322,439 170,550 86,240 158,415

Cement 59,049 65,063 203,020 125,557 19,431

Clinker 22,878 125.146 2,381

General cargoes 13,268 14,762 17,271 17,678

Fertilizer

Others 78.528 77,219 129.547 123,094 182,060

4. Container

Number of containers 29,101 7, 7874 137,662 7,- Export 13,669 17,376 34,407 68,638 77,305

(Empty) 1,679 4,320 6,548 18,192 19,304

- Import 15,432 20,060 44,338 69,024 80,378

(Empty) 1,438 1,625 4,767 5,404 7,067

In tons 291.619 321,400 863.671 1,426,091 1,628,318

- Export 122,235 143,496 396,253 621,502 687,752

- Import 169,384 177,904 467,418 804,589 940,566

29

D. Forecast of future cargo volumes

a) Socio - economic development orientation in attractive areas

1. General

3.33 The direct attractive area behind Can Tho port includes theWestern provinces such as: An Giang, Kien Giang, Can Tho, Soc Trang, MinhHai and part of the provinces : Vinh Long, Tra Vinh, Dong Thap. Theseprovinces are rich of natural resources and contribute large share of agricultural,forestry, aquaculture products for consuming needs and export to the MekongDelta. Moreover, this is a large consumption market.

3.34 In the coming years and in future, with the development of themarket economy and foreign trade, accordance with the 'open' investmentpolicy having the attraction of domestic and foreign investment, the tradingwith international market will help the regional economy develop.

3.35 The Vietnam socio - economic development strategy to the year of2000 has indicated that agriculture will still play an important role in thenational economy. The provinces in the southern area of Bassac river with thearea of 15,499 km2 of agricultural land(59% of the total agricultural land areain Mekong Delta), potential natural resources are favourable for developing anall-sided tropical agriculture, especially paddy.

3.36 Forest development orientation is protecting forest and growingthe upstream forest, making full use of acid sulphate soils in the South - Westregion to grow new-origin eucalyptus according to the program of exportingpaper material in co - operation with France, Japan and Taiwan.

3.37 The light industry will concentrate on consuming goods, accuratemechanics, electronic assembly, transport mechanics and export agriculturalproducts.

2. Potentiall/rosoect of socio-economic development in Canthocity

3.38 Cantho city has the natural geographical area of 14,100 ha and isdivided into 22 villages and wards. In which, the urban area is 5,530 haconsisting of 15 urban wards.

3.39 The population is now up to 300, 400 inhabitants (female takes52%) with the population density on average being 2,130 inhabitants/km2 . Theethnic groups : Vietnamese 95%, Chinese 4,25, the remainder is of otherraces. The-age-labour force takes 58% of population, working mainly in thestate economic fields : agriculture 33,000 persons.

3.40 Industry 21,400 persons, commerce 25,700 persons,transportation 7,400 persons. Among the remainder, approximately 30,000persons are unemployed.

30

3.41 The labour force quality is that over 5,200 persons are Universitygraduates and post graduates, 5,200 persons of Vocationals, 7,700 skilledmechanics.

3.42 The economic development strategy of the South West hasconfirmed"Cantho city will be enlarged, developed in many fields to becomethe Mekong Delta centre. Here will develop the science, technology researchcentres, the concentrated industrial Zone, the export -processing zone, airports,seaports concurrently with the development needs of the whole region.

3.43 To get ability to develop the Mekong Delta completely as intentionand to get the certain positions, Cantho needs to carry out the strategicfeasible study and urgently calls for investment to speed up the development ofdomestic totals products

- Feasible study of the Hau River Bridge;- Study the development for the Capital town and plan the infrastructure

consisting of: The export processing Tra Noc Airport scape Dinh Anchannel and enlarge Seaport.Have the Plan for Cantho's total surface.

3.44 Having got the decree by the Prime Minister for the approval ofCantho as being the second- type city, the leaders of all fields in Canthoprovince and Cantho city have prepared the developing projects basing on thenew planning. From now on, Cantho will be the centre for economy, culture,science and technology of the Mekong Delta and the projects such as :CanthoProcessing Zone, Tra Noc Airport rehabilitation for the civil transport, upgradingCantho International port to receive the 10,000 DWT container ships will haveconditions to be developed.

3.45 On 28 October 1995, the State Council of Investment ProjectApproval agreed to approve the Master Plan of Socio-Economic Development ofCantho in the period of 1996-2000. According to that 28 Economic Zones willbe established in CanthQ province and its economic structure will be transferredfrom agriculture-industry-service to industry-service-agriculture. To the year2000, the growth rate GNP is planned to reach to 10-11% per year. There are3 main socio-economic zones among 28 of that:

- Tra Noc Export Processing-industry Zone (500 ha) is invested toconcentrate on processed agricultural and aquatic products, garmentindustry, electronic products, and steel. Presently, there are several joint-venture and foreign companies operating and leasing land here;

- The Industrial Zone in southern area of Cantho city (860 ha) : After theconstruction of Cantho bridge is completed, the Cantho port will be builthere for large-size ships, a port industrial area and a system of warehousefor trans-ship cargo will also established. Besides, the construction materialproduction and agricultural and aquatic products processing industry areaalso developed;

- Vi Thanh Zone (150 ha) focuses mainly on agricultural and aquaticproducts processing.

31

Table 3.11: The first priority investment projects of industry and agriculturedevelopment in Cantho

Name of projects Description of projects1. AGRICULTURE TOGETHER WITH PROCESSING

INDUSTRY1. Product, preserve, process , export rice Processing capacity 5 tons /hour, export rice

volume 200,000-300,000 tons /year1. Process frozen-meat for export Building up the raw material section

processing capacity of 10,000 tons /year1. Upgrade the Hau Giang refreshment drink factory Capacity 5 million litres of soft drink, 10

million litres of beer per year1. Plant and process tropical fruit Reorganize the unplanned orchards, process

capacity 100 tons /day1. Process products from coconut Raw oil 100 tons /day1. Animal foodstuff process Capacity 10,000 tons per year1. Plant and process Eucalyptus Capacity of raw wood 300,000 tons /year,

paper powder 50,000 tons /year1. Process Children's nutritious flour Capacity 120 tons /year1. Plant sugar cane and process sugar Capacity 1,000 tons /yearII. MECHANIC INDUSTRY1. Manufacture spare parts for engines Capacity 100,000 products /yearIll. STANDARD CHEMICAL INDUSTRY1 Packing and manufacture inorganic fertilizer Capacity 200.000 tons /yearI. Manufacture veterinary medicine Capacity 100 tons medicine of all kinds1. Manufacture hard PVC hard water pipe Capacity 500 tons PVC hard water pipe per

year

Table 3.12:

IV. UGHT INDUSTRY14. Develop leather sewing for export Capacity 2.5-3 million products per year1, INFORMATIC, ELECTRONIC INDUSTRIES _15. Develop informatic, electronic industries Capacity 10.000 products per year1. SMALL-SCALE HANDICRAFT INDUSTRIES1. Develop small-scale handicraft industries On scale of 50,000 products per yearVIl. AGRICULTURE17. P ant and export banana Building-up every banana mono-cultivated

section, scale 500 ha18. Produce fresh water fish breeds MCapacity 100 million breeds per year

b) Forecasts on the volume of cargoes handled at Can Tho port:

1. Rice

3.46 The Mekong Delta with its rich natural resource base has a highagricultural potential. Today it accounts for 40% of the agricultural productionin the country and produces 50% of its rice. The Delta has the potentiality tokeep its role as surplus producer of rice and at the same time to diversify intohigher value non-rice crops. Recently, agricultural production in the MekongDelta has considerably developed. In the period of 1991-1995, the averagegrowth of food output has increased over 1 million tons annually. According tothe target mentioned in the forecast of Ministry of Agriculture and RuralDevelopment, in the next 5 years, the paddy output of 13 million tons in 1995will be increased to 15.5-16 million tons. Hence, with the average growth rate,in the year 2000 the output of the Mekong Delta will coincide with the outputof 1 6 million tons projected for the year 201 5.

32

3.47 Following FAO estimates, average rice consumption should be ofthe order of 1 58 kg per year on the medium to long-term. This assumes that ofa desirable intake of around 2,200 calories per capita per day, 70-75% is metby rice. The volumes projected for export would probably form sufficientcushion to compensate for drops in domestic supply in poor agricultural year.

Table 3.13: Paddy demand and projections for Mekong Delta.

Udtt 2000 201 !Population min 17.9 23.7Rice consumption per capita kg 1T61PaddV demand for mln t 15 16

- Domestic consumption min t 4.65 5.74- Export min t 4.65 4.98- Provision for other areas min t 3.45 3.68- On-farm losses' min t 1.50 0.80- Seed requirement mln t U.75 0.80

1 Conversion paddy to rice: + domestic consumption 65 %2 On-farm losses: 10% of production in 2000, dropping to 5% in 2010 and

thereafter3 Seed: 5% of production

3.48 The forecasted surpluses of food in the Delta which will betransported to the other regions in Vietnam and exported are given in Table3.14.

Table 3.14 : Forecast of surpluses of rice

Unit Year 2000 Year 2015To South-East areas 1.000 t 1,300 1,400To other regions 1,000 t 900 1,000Export 1,000 t 2,800 3,000Total ,&0i00 0 5,400

Note: Conversion paddy to rice: + domestic consumption 65 %;+ export 60 % -

3.49 There will be 3 proposed major ports for exporting rice in the SouthRegion: Saigon port, Can Tho port, and Thi Vai-Vung Tau port. The possibilityof using these ports for exporting rice depends on their transport line andthroughput capacity.

3.50 Because of the poor accessibility of the channel from the SouthChina Sea, Can Tho port has been accessible only for vessels between 5,000DWT - 10,000 DWT. Hence, Can Tho port has been reserved for cargotransport to the neighbouring countries like : Indonesia, The Philippines,Malaysia .... Cargo transport to Europe, Africa, America requires large - sizevessels. According to the source from Ministry of Trade, The PhilippinesGovernment has intended to import 300,000 T of rice from Vietnam. Thenegotiation procedure has just initiated but this volume of rice is expected to betransported to The Philippines by the beginning of 1996. The volume of rice forexport handled at the ports in the period of 2000 - 2015 is forecasted in Table3.1 5.

33

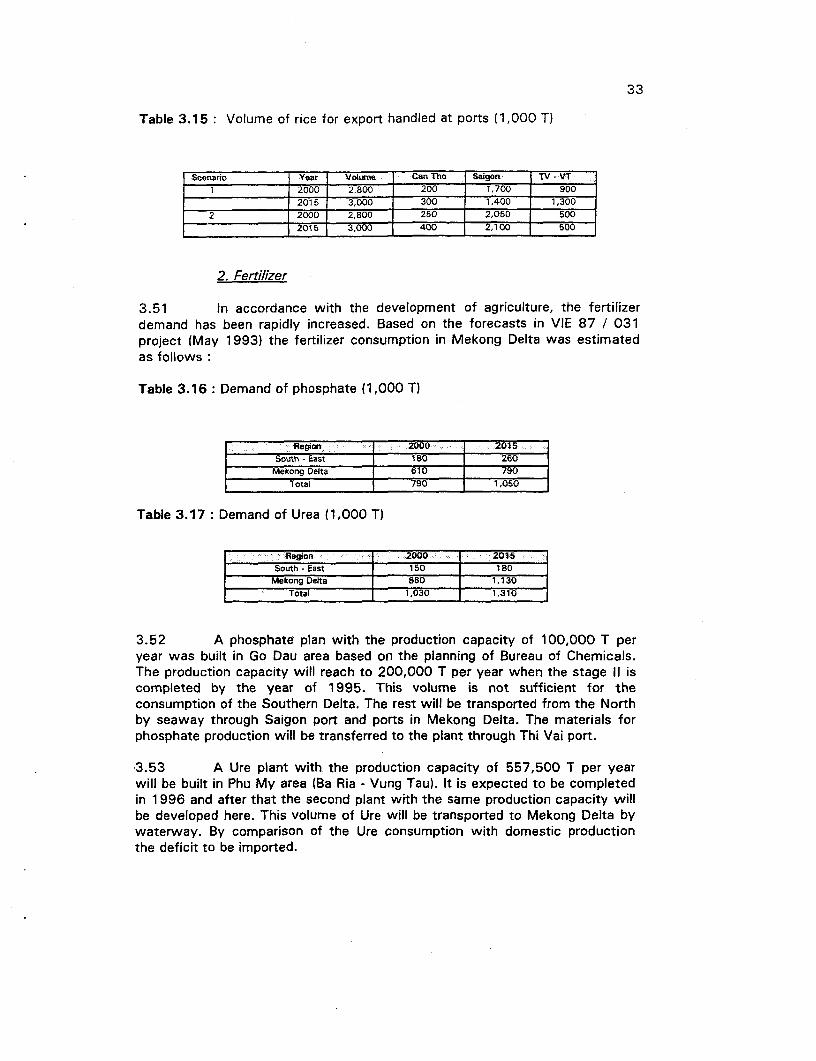

Table 3.15 : Volume of rice for export handled at ports (1,000 T)

Scenario Year Voi Vne: Can Tho Saigont TV - VT1 2000 2,800 200 1,700 900

2015 3,000 300 1,400 1,3002 2000 2,800 250 2,050 500

2015 3,000 400 2,100 500

2. Fertilizer

3.51 In accordance with the development of agriculture, the fertilizerdemand has been rapidly increased. Based on the forecasts in VIE 87 / 031project (May 1993) the fertilizer consumption in Mekong Delta was estimatedas follows:

Table 3.16: Demand of phosphate (1,000 T)

Region 2000 2015South - East 180 260 l

Mekong Delta 610 790Total 790 1,050

Table 3.17: Demand of Urea (1,000 T)

Region 2000 j 2015,South - East j 150 j 180 _

Mekong Delta 880 1,130Total 1,030 1,31

3.52 A phosphate plan with the production capacity of 100,000 T peryear was built in Go Dau area based on the planning of Bureau of Chemicals.The production capacity will reach to 200,000 T per year when the stage 11 iscompleted by the year of 1995. This volume is not sufficient for theconsumption of the Southern Delta. The rest will be transported from the Northby seaway through Saigon port and ports in Mekong Delta. The materials forphosphate production will be transferred to the plant through Thi Vai port.

3.53 A Ure plant with the production capacity of 557,500 T per yearwill be built in Phu My area (Ba Ria - Vung Tau). It is expected to be completedin 1 996 and after that the second plant with the same production capacity willbe developed here. This volume of Ure will be transported to Mekong Delta bywaterway. By comparison of the Ure consumption with domestic productionthe deficit to be imported.

34

3.54 The total volume of Ure that will be imported and transported fromthe North is shown in Table 3.19.

Table 3.19: Total volume of Ure transported to the Southern Delta (1,000 T)

Items 2000 2015Phosphate 590 850

Urea 502 186

DAP fertilizer will be imported in bulk and then bagged into bags of 50 kg eachand transported to Mekong Delta by waterway.

Table 3.20 Scenarios for importing DAP (1,000 T)

Scenrios i 2000 2015Scenario1 1 200 200Scenario 2 400 400

(Source :"Economic Data - Planning of Thi Vai - Vung Tau Deep - water PortComplex)

3. Coal

Coal transported to the South from the North is mainly used forconstruction materials production. In recent years, the amount of coal handledat Saigon port is about 100,OOOT. The volume of coal consumption in theSouth is estimated at 1 50,000 T in 2000 and 250,000 T in 2015.

4. Steel

3.56 Today, construction industry has developed rapidly. In addition tothe large - scale works like :Thac Mo Hydroelectric Plant, Yaly HydroelectricPlant...etc., other civil ones like: hotels, building of offices, residential housingare in need of enormous amount of steel. In the coming years, the steeldemand will be increased with higher speed because of more foreigninvestment.

3.57 The steel consumption in the period of 2000 - 201 5 in the area isestimated as below:

Year of 2000 : 830,000 TYear of 2015 : 1,790,000 T