information for students in math 329 2005 01

TRANSCRIPT

McGILL UNIVERSITY

FACULTY OF SCIENCE

DEPARTMENT OFMATHEMATICS AND STATISTICS

MATH 329 2005 01

THEORY OF INTEREST

Information for Students(Winter Term, 2004/2005)

Pages 1 - 10 of these notes may be considered theCourse Outline for this course.

W. G. Brown

April 12, 2005

Information for Students in MATH 329 2005 01

Contents

1 General Information 11.1 Instructor and Times . . . . . 11.2 Course Description . . . . . . 1

1.2.1 Calendar Description . 11.2.2 Syllabus (in terms of sec-

tions of the text-book) 11.2.3 “Verbal” arguments . 4

1.3 Evaluation of Your Progress . 41.3.1 Term Mark . . . . . . 41.3.2 Assignments. . . . . . 41.3.3 Class Test . . . . . . . 41.3.4 Final Examination . . 51.3.5 Supplemental Assessments 51.3.6 Machine Scoring . . . 51.3.7 Plagiarism . . . . . . . 5

1.4 Published Materials . . . . . 61.4.1 Required Text-Book . 61.4.2 Website . . . . . . . . 61.4.3 Reference Books . . . 6

1.5 Other information . . . . . . 71.5.1 Prerequisites . . . . . 71.5.2 Calculators . . . . . . 71.5.3 Self-Supervision . . . . 71.5.4 Escape Routes . . . . 71.5.5 Showing your work; good

mathematical form; sim-plifying answers . . . . 7

2 Timetable 9

3 First Problem Assignment 11

4 Second Problem Assignment 13

5 Solutions, First Problem Assign-ment 16

6 Third Problem Assignment 22

7 Solutions, Second Problem As-signment 25

8 Class Tests 348.1 Class Test, Version 1 . . . . . 348.2 Class Test, Version 2 . . . . . 408.3 Class Test, Version 3 . . . . . 468.4 Class Test, Version 4 . . . . . 52

9 Solutions, Third Problem Assign-ment 58

10 Fourth Problem Assignment 67

11 Solutions to Problems on the ClassTest 7011.1 Problems on rates of interest and

discount . . . . . . . . . . . . 7011.2 Problems on the values of annu-

ities and perpetuities with con-stant payments . . . . . . . . 73

11.3 Problems on increasing and de-creasing annuities and perpetu-ities . . . . . . . . . . . . . . 76

11.4 Problems on combinations of an-nuities and perpetuities . . . 78

11.5 Problems on drop and balloonpayments . . . . . . . . . . . 79

12 Fifth Problem Assignment 82

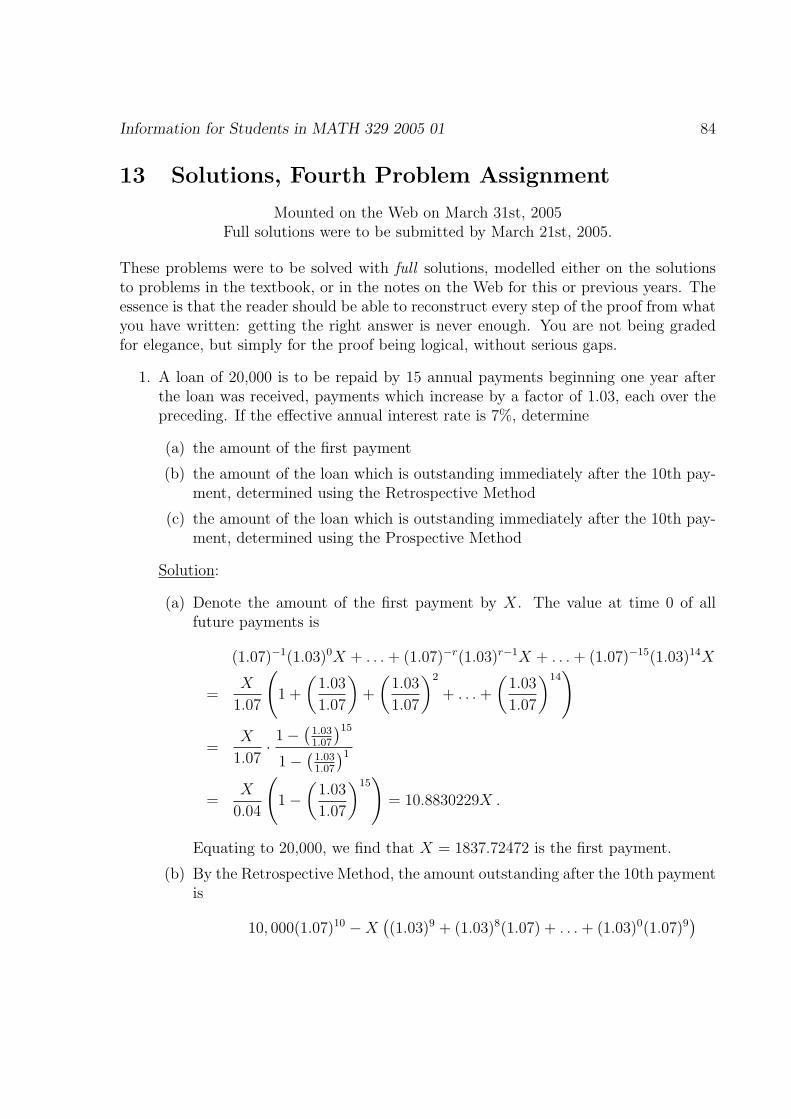

13 Solutions, Fourth Problem Assign-ment 84

14 Solutions, Fifth Problem Assign-ment 92

15 References 901

A Supplementary Lecture Notes 2001A.1 Supplementary Notes for the Lec-

tures of January 4th and Janu-ary 5th, 2005 . . . . . . . . . 2001A.1.1 These notes . . . . . . 2001A.1.2 §1.1 INTRODUCTION 2001

Information for Students in MATH 329 2005 01

A.1.3 §1.2 THE ACCUMULA-TION AND AMOUNTFUNCTIONS . . . . . 2002

A.2 Supplementary Notes for the Lec-ture of January 7th, 2005 . . 2007A.2.1 §1.2 THE ACCUMULA-

TION AND AMOUNTFUNCTIONS (conclusion) 2007

A.2.2 §1.3 THE EFFECTIVERATE OF INTEREST 2007

A.3 Supplementary Notes for the Lec-ture of January 10th, 2005 . . 2009A.3.1 §1.3 THE EFFECTIVE

RATE OF INTEREST (con-clusion) . . . . . . . . 2009

A.3.2 §1.4 SIMPLE INTEREST 2010A.3.3 §1.5 COMPOUND INTER-

EST . . . . . . . . . . 2012A.4 Supplementary Notes for the Lec-

ture of January 12th, 2005 . . 2018A.4.1 §1.6 PRESENT VALUE 2018

A.5 Supplementary Notes for the Lec-ture of January 14th, 2005 . . 2021A.5.1 §1.7 THE EFFECTIVE

RATE OF DISCOUNT 2021A.5.2 §1.8 NOMINAL RATES

OF INTEREST AND DIS-COUNT (barely begun 2025

A.6 Supplementary Notes for the Lec-ture of January 17th, 2005 . . 2026A.6.1 §1.8 NOMINAL RATES

OF INTEREST AND DIS-COUNT (continued) . 2026

A.6.2 §1.9 FORCES OF INTER-EST AND DISCOUNT(barely begun) . . . . 2030

A.7 Supplementary Notes for the Lec-ture of January 19th, 2005 . . 2031A.7.1 §1.9 FORCES OF INTER-

EST AND DISCOUNT 2031A.7.2 §1.10 VARYING INTER-

EST . . . . . . . . . . 2032

A.7.3 §1.11 SUMMARY OF RE-SULTS . . . . . . . . 2032

A.7.4 §2.1 INTRODUCTION 2033A.7.5 §2.2 OBTAINING NUMER-

ICAL RESULTS . . . 2033A.8 Supplementary Notes for the Lec-

ture of January 21st, 2005 . . 2036A.8.1 §2.2 OBTAINING NUMER-

ICAL RESULTS (contin-ued) . . . . . . . . . . 2036

A.8.2 §2.3 DETERMINING TIMEPERIODS . . . . . . . 2037

A.8.3 §2.4 THE BASIC PROB-LEM . . . . . . . . . . 2039

A.8.4 §2.5 EQUATIONS OF VALUE 2039A.9 Supplementary Notes for the Lec-

ture of January 24th, 2005 . . 2041A.9.1 §2.5 EQUATIONS OF VALUE

(continued) . . . . . . 2041A.9.2 §2.6 UNKNOWN TIME 2042

A.10 Supplementary Notes for the Lec-tures of January 26th, 2005 . 2045A.10.1 §2.7 UNKNOWN RATE

OF INTEREST . . . . 2045A.10.2 §2.8 PRACTICAL EX-

AMPLES . . . . . . . 2046A.10.3 §2.9 MISCELLANEOUS

PROBLEMS . . . . . 2049A.10.4 §3.1 INTRODUCTION 2050

A.11 Supplementary Notes for the Lec-ture of January 28rd, 2005 . . 2052A.11.1 §3.2 ANNUITY-IMMEDIATE 2052

A.12 Supplementary Notes for the Lec-ture of January 31st, 2005 . . 2056A.12.1 §3.3 ANNUITY-DUE 2056

A.13 Supplementary Notes for the Lec-ture of February 2nd, 2005 . . 2058A.13.1 §3.3 ANNUITY-DUE (con-

tinued) . . . . . . . . 2058A.13.2 §3.4 ANNUITY VALUES

ON ANY DATE . . . 2059

Information for Students in MATH 329 2005 01

A.14 Supplementary Notes for the Lec-ture of February 4th, 2005 . . 2063A.14.1 §3.4 ANNUITY VALUES

ON ANY DATE (contin-ued) . . . . . . . . . . 2063

A.14.2 §3.5 PERPETUITIES 2066A.15 Supplementary Notes for the Lec-

ture of February 7th, 2005 . . 2067A.15.1 §3.5 PERPETUITIES (con-

tinued) . . . . . . . . 2067A.15.2 §3.6 NONSTANDARD TERMS

AND INTEREST RATES 2068A.15.3 §3.7 UNKNOWN TIME 2068

A.16 Supplementary Notes for the Lec-ture of February 9th, 2005 . . 2070A.16.1 §3.7 UNKNOWN TIME

(continued) . . . . . . 2070A.16.2 §3.8 UNKNOWN RATE

OF INTEREST . . . . 2073A.16.3 §3.9 VARYING INTER-

EST . . . . . . . . . . 2081A.16.4 §3.10 ANNUITIES NOT

INVOLVING COMPOUNDINTEREST . . . . . . 2081

A.17 Supplementary Notes for the Lec-ture of February 11th, 2005 . 2082A.17.1 §4.1 INTRODUCTION 2082A.17.2 §4.2 ANNUITIES PAYABLE

AT A DIFFERENT FRE-QUENCY THAN INTER-EST IS CONVERTIBLE 2082

A.18 Supplementary Notes for the Lec-ture of February 14th, 2005 . 2086A.18.1 §4.3 FURTHER ANALY-

SIS OF ANNUITIES PAYABLELESS FREQUENTLY THANINTEREST IS CONVERT-IBLE . . . . . . . . . 2086

A.18.2 §4.4 FURTHER ANALY-SIS OF ANNUITIES PAYABLEMORE FREQUENTLYTHAN INTEREST IS CON-VERTIBLE . . . . . . 2090

A.19 Supplementary Notes for the Lec-ture of February 16th, 2005 . 2093A.19.1 §4.5 CONTINUOUS AN-

NUITIES . . . . . . . 2093A.19.2 §4.6 BASIC VARYING

ANNUITIES . . . . . 2093A.20 Supplementary Notes for the Lec-

ture of February 18th, 2005 . 2094A.20.1 §4.6 BASIC VARYING

ANNUITIES (continued) 2094A.20.2 §4.7 MORE GENERAL

VARYING ANNUITIES 2099A.21 Supplementary Notes for the Lec-

ture of February 28th, 2005 . 2100A.21.1 §4.6 BASIC VARYING

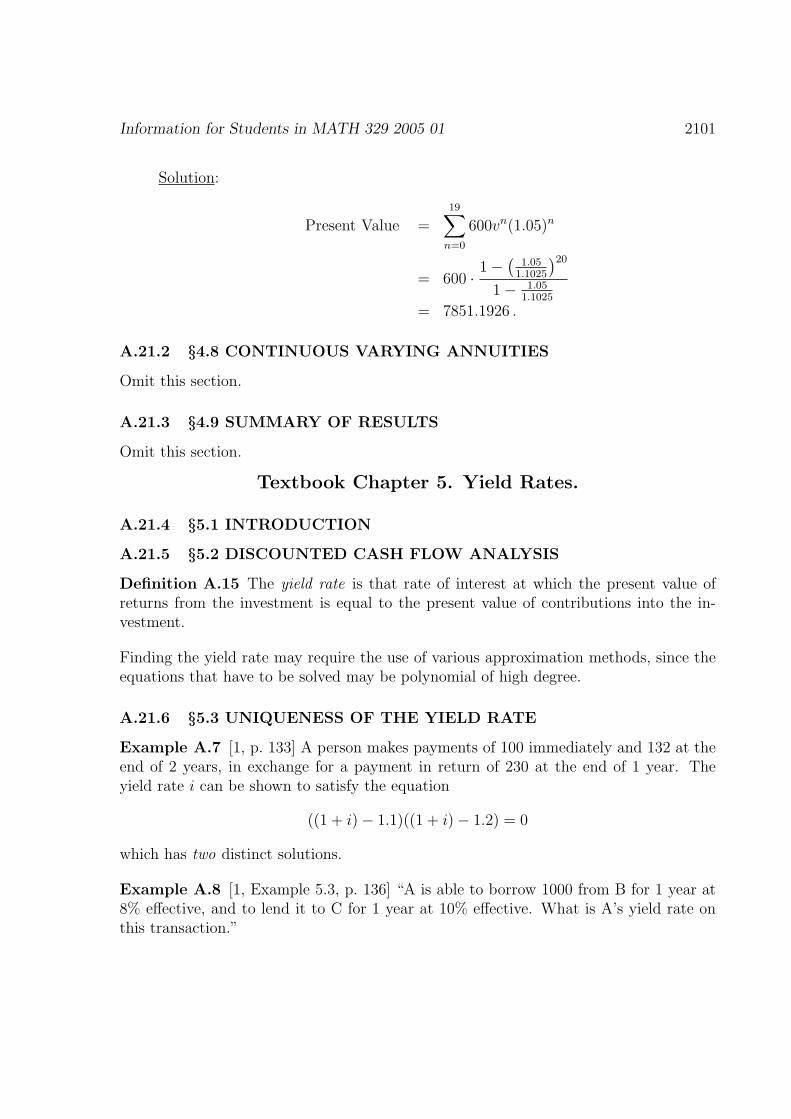

ANNUITIES (conclusion) 2100A.21.2 §4.8 CONTINUOUS VARY-

ING ANNUITIES . . 2101A.21.3 §4.9 SUMMARY OF RE-

SULTS . . . . . . . . 2101A.21.4 §5.1 INTRODUCTION 2101A.21.5 §5.2 DISCOUNTED CASH

FLOW ANALYSIS . . 2101A.21.6 §5.3 UNIQUENESS OF

THE YIELD RATE . 2101A.22 Supplementary Notes for the Lec-

ture of March 2nd, 2005 . . . 2103A.22.1 §5.4 REINVESTMENT

RATES . . . . . . . . 2103A.22.2 §5.5 INTEREST MEA-

SUREMENT OF A FUND 2106A.22.3 §5.6 TIME-WEIGHTED

RATES OF INTEREST 2106A.22.4 §5.7 PORTFOLIO METH-

ODS AND INVESTMENTYEAR METHODS . . 2106

Information for Students in MATH 329 2005 01

A.22.5 §5.8 CAPITAL BUDGET-ING . . . . . . . . . . 2106

A.22.6 §5.9 MORE GENERALBORROWING/LENDINGMODELS . . . . . . . 2106

A.23 Supplementary Notes for the Lec-ture of March 4th, 2005 . . . 2107A.23.1 §6.1 INTRODUCTION 2107A.23.2 §6.2 FINDING THE OUT-

STANDING LOAN BAL-ANCE . . . . . . . . . 2107

A.24 Supplementary Notes for the Lec-ture of March 7th, 2005 . . . 2112A.24.1 §6.3 AMORTIZATION SCHED-

ULES . . . . . . . . . 2112A.25 Supplementary Notes for the Lec-

ture of March 11th, 2005 . . . 2115A.25.1 §6.3 AMORTIZATION SCHED-

ULES (continued) . . 2115A.25.2 §6.4 SINKING FUNDS 2119

A.26 Supplementary Notes for the Lec-ture of March 14th, 2005 . . . 2123A.26.1 §6.4 SINKING FUNDS

(concluded) . . . . . . 2123A.26.2 §6.5 DIFFERING PAY-

MENT PERIODS ANDINTEREST CONVERSIONPERIODS . . . . . . . 2127

A.26.3 §6.6 VARYING SERIESOF PAYMENTS . . . 2127

A.26.4 §6.7 AMORTIZATION WITHCONTINUOUS PAYMENTS 2127

A.26.5 §6.8 STEP-RATE AMOUNTSOF PRINCIPAL . . . 2127

A.27 Supplementary Notes for the Lec-ture of March 16th, 2005 . . . 2128A.27.1 §7.1 INTRODUCTION 2128A.27.2 §7.2 TYPES OF SECU-

RITIES . . . . . . . . 2128A.28 Supplementary Notes for the Lec-

ture of March 21st, 2005 . . . 2130

A.28.1 §7.2 TYPES OF SECU-RITIES (conclusion) . 2130

A.28.2 §7.3 PRICE OF A BOND 2131A.29 Supplementary Notes for the Lec-

ture of March 21st, 2005 . . . 2138A.29.1 §7.2 TYPES OF SECU-

RITIES (conclusion) . 2138A.29.2 §7.3 PRICE OF A BOND 2140

A.30 Supplementary Notes for the Lec-ture of March 23rd, 2005 . . . 2144

A.31 Supplementary Notes for the Lec-ture of March 30th, 2005 . . . 2146A.31.1 §7.4 PREMIUM AND DIS-

COUNT . . . . . . . . 2146A.31.2 §7.7 CALLABLE BONDS 2149

A.32 Supplementary Notes for the Lec-ture of April 1st, 2005 . . . . 2153A.32.1 §7.6 DETERMINATION

OF YIELD RATES . 2157A.32.2 §7.5 VALUATION BE-

TWEEN COUPON PAY-MENT DATES . . . . 2157

A.32.3 §7.8 SERIAL BONDS 2159A.32.4 §7.9 SOME GENERAL-

IZATIONS . . . . . . 2159A.32.5 §7.10 OTHER SECURI-

TIES . . . . . . . . . . 2159A.32.6 §7.11 VALUATION OF

SECURITIES . . . . . 2159

B Problem Assignments, Tests, andExaminations from Previous Years 3001B.1 2002/2003 . . . . . . . . . . . 3001

B.1.1 First 2002/2003 ProblemAssignment, with Solu-tions . . . . . . . . . . 3001

B.1.2 Second 2002/2003 Prob-lem Assignment, with So-lutions . . . . . . . . . 3006

B.1.3 Third 2002/2003 Prob-lem Assignment, with So-lutions . . . . . . . . . 3011

Information for Students in MATH 329 2005 01

B.1.4 Fourth 2002/2003 Prob-lem Assignment, with So-lutions . . . . . . . . . 3018

B.1.5 Fifth 2002/2003 ProblemAssignment, with Solu-tions . . . . . . . . . . 3028

B.1.6 2002/2003 Class Tests, withSolutions . . . . . . . 3036

B.1.7 Final Examination, 2002/2003 3042B.2 2003/2004 . . . . . . . . . . . 3045

B.2.1 First 2003/2004 ProblemAssignment, with Solu-tions . . . . . . . . . . 3045

B.2.2 Second 2003/2004 Prob-lem Assignment, with So-lutions . . . . . . . . . 3048

B.2.3 Third 2003/2004 Prob-lem Assignment, with So-lutions . . . . . . . . . 3058

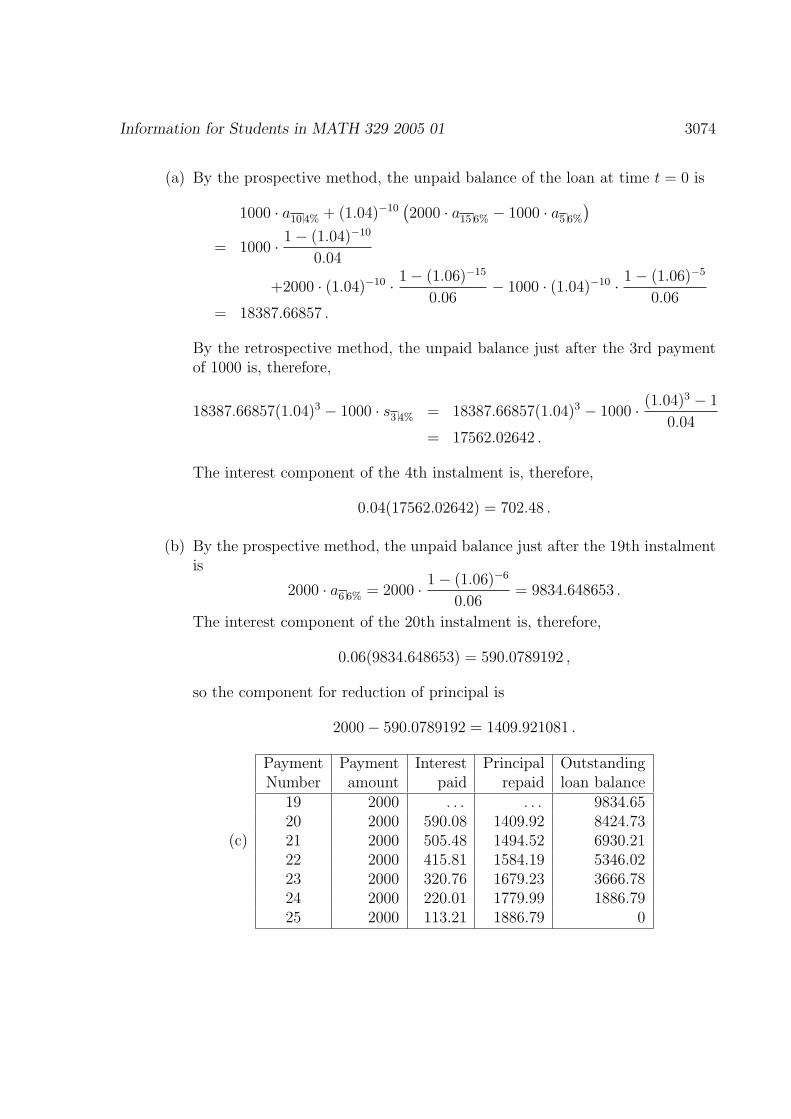

B.2.4 Fourth 2003/2004 Prob-lem Assignment, with So-lutions . . . . . . . . . 3068

B.2.5 Fifth 2003/2004 ProblemAssignment, with Solu-tions . . . . . . . . . . 3073

B.2.6 2003/2004 Class Test, Ver-sion 1 . . . . . . . . . 3079

B.2.7 2003/2004 Class Test, Ver-sion 2 . . . . . . . . . 3080

B.2.8 2003/2004 Class Test, Ver-sion 3 . . . . . . . . . 3082

B.2.9 2003/2004 Class Test, Ver-sion 4 . . . . . . . . . 3083

B.2.10 Solutions to Problems onthe 2003/2004 Class Tests 3085

B.2.11 Final Examination, 2003/2004 3094B.2.12 Supplemental/Deferred Ex-

amination, 2003/2004 3097

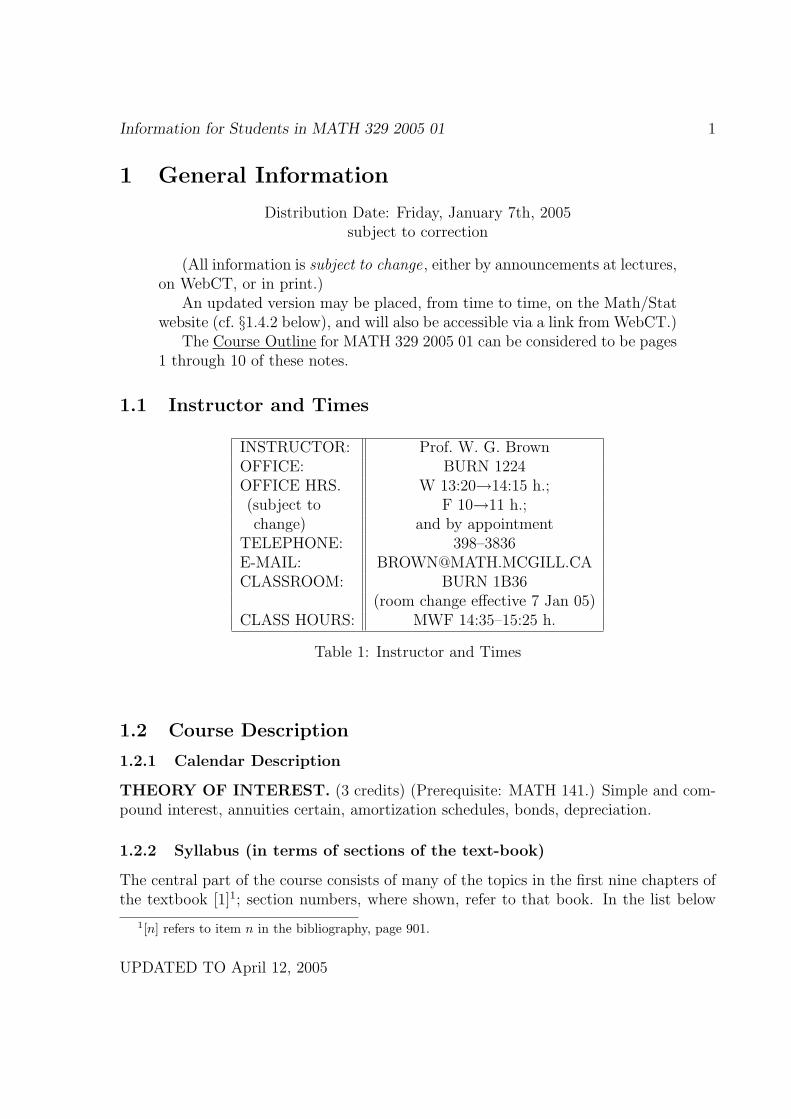

Information for Students in MATH 329 2005 01 1

1 General Information

Distribution Date: Friday, January 7th, 2005subject to correction

(All information is subject to change, either by announcements at lectures,on WebCT, or in print.)

An updated version may be placed, from time to time, on the Math/Statwebsite (cf. §1.4.2 below), and will also be accessible via a link from WebCT.)

The Course Outline for MATH 329 2005 01 can be considered to be pages1 through 10 of these notes.

1.1 Instructor and Times

INSTRUCTOR: Prof. W. G. BrownOFFICE: BURN 1224OFFICE HRS. W 13:20→14:15 h.;(subject to F 10→11 h.;change) and by appointment

TELEPHONE: 398–3836E-MAIL: [email protected]: BURN 1B36

(room change effective 7 Jan 05)CLASS HOURS: MWF 14:35–15:25 h.

Table 1: Instructor and Times

1.2 Course Description

1.2.1 Calendar Description

THEORY OF INTEREST. (3 credits) (Prerequisite: MATH 141.) Simple and com-pound interest, annuities certain, amortization schedules, bonds, depreciation.

1.2.2 Syllabus (in terms of sections of the text-book)

The central part of the course consists of many of the topics in the first nine chapters ofthe textbook [1]1; section numbers, where shown, refer to that book. In the list below

1[n] refers to item n in the bibliography, page 901.

UPDATED TO April 12, 2005

Information for Students in MATH 329 2005 01 2

we show the chapters and appendices of the textbook. Following each is a descriptionas of the date of this revision, of the sections to be excluded. This list will be updatedduring the semester, as becomes apparent that certain sections are not appropriate tothe level of the course or the lecture time available.

Chapter 1. The Measurement of Interest §§1.1-1.8. Portions of §1.9, will beomitted. For the present §1.10 will also be omitted.

Chapter 2. Solution of Problems in Interest In §2.6 You may omit the discussion[1, pp. 45-46] of the “method of equated time”.

Chapter 3. Elementary Annuities You may omit [1, §3.6 Nonstandard terms andinterest rates], [1, §3.10 Annuities not involving compound interest, pp. 82-88] and cor-responding exercises. We will also omit [1, §3.8 Unknown rate of interest] and [1, §3.9Varying interest] for the present (possibly to return).

Chapter 4. More General Annuities In the following section we shall consider theproblems strictly on an ad hoc basis: students are not expected to derive nor to applythe identities obtained: [1, §4.2 Annuities payable at a different frequency than interestis convertible; §4.3 Further analysis of annuities payable less frequently than interest isconvertible; §4.4 Further analysis of annuities payable more frequently than interest isconvertible]. Omit [1, §4.5 Continuous annuities] for the present. In [1, §4.6 Nonstandardterms and interest rates] we shall consider the derivation of formulæ for (Ia)n, (Is)n,(Da)n, (Ds)n, and their due and perpetual variants, also the question of annuities ingeometric progression. Omit [1, §4.7 More general varying annuities, §4.8 Continuousvarying annuities, §4.9 Summary of results] for the present, together with their exercises.

Chapter 5. Yield Rates Omit [1, §5.2 Discounted cash flow analysis], except for thedefinition [1, p. 131] of yield rate. Omit [1, §5.3 Uniqueness of the yield rate] except youshould read and understand the example [1, p. 133] of a problem where the yield rateis not unique. Omit [1, §5.5 — §5.9] and accompanying exercises; but we will study [1,§5.4 Reinvestment rates] in preparation for Chapter 6.

Chapter 6. Amortization Schedules and Sinking Funds In [1, §6.4] omit pages178-179, where the function an i&j is introduced. Omit [1, §6.5 — §6.8] and accompanyingexercises.

Information for Students in MATH 329 2005 01 3

Chapter 7. Bond and Other Securities Omit [1, §7.6 Determination of yield rates],[1, §7.8 Serial bonds], [1, §7.9 Some generalizations], [1, §7.10 Other securities], [1, §7.11Valuation of securities].

Chapter 8. Practical Applications Omit this chapter.

Chapter 9. More Advanced Financial Analysis Omit this chapter.

Chapter 10. A Stochastic Approach to Interest Omit this chapter.

Appendix I. Table of compound interest functions While most calculations willbe done using calculators, these tables may prove useful.

Appendix II. Table numbering the days of the year

Appendix III. Basic mathematical review Topics that are beyond the requiredprerequisites will be explained if, as, and when they are used.

Appendix IV. Statistical background Omit this section: no background in prob-ability is prerequisite to Math 329.

Appendix V. Iteration methods

Appendix VI. Further analysis of varying annuities Omit this Appendix, whichis concerned with the formula for “Summation by Parts”, analogous to integration byparts for functions of a continuous variable.

Appendix VII. Illustrative mortgage loan amortization schedule

Appendix VIII. Full immunization Omit this Appendix, which is related to [1,§9.9], which is not in the syllabus.

Appendix IX. Derivation of the variance of an annuity Omit this Appendix.

Appendix X. Derivation of the Black-Scholes formula Omit this Appendix.

UPDATED TO April 12, 2005

Information for Students in MATH 329 2005 01 4

1.2.3 “Verbal” arguments

An essential feature of investment and insurance mathematics is the need to be able tounderstand and to formulate “verbal” arguments; that is, explanations of the truth ofan identity presented verbally i.e., a proof in words, rather then an algebraic proof. Ina verbal argument we seek more than mathematically correctness: we wish to see anexplanation that could be presented to a layman who is not competent in the mathe-matical bases of this subject, but is still possessed of reason, and needs to be assuredthat he is not being exploited. This facet of the course will be seen, at first, to be quitedifficult. When the skill has been mastered it can be used to verify the correctness ofstatements proved mathematically. Verbal arguments require some care with the under-lying language; students who have difficulty with expression in English are reminded thatall students have the right to submit any written materials in either English or French.2

1.3 Evaluation of Your Progress

1.3.1 Term Mark

The Term Mark will be computed one-third from the assignment grades, and two-thirdsfrom the class test. The Term Mark will count for 30 of the 100 marks in the finalgrade, but only if it exceeds 30% of the final examination percentage; otherwise the finalexamination will be used exclusively in the computation of the final grade.

1.3.2 Assignments.

A total of about 6 assignments will be worth 10 of the 30 marks assigned to Term Work.

1.3.3 Class Test

A class test, will be held on Wednesday, March 09th, 2005, at the regular class time,counting for 20 of the 30 marks in the Term Mark. This date may be changed, afterdiscussion with the class at any scheduled lecture date. Students who don’t come toclass should ensure that they are aware of any changes in the date of the test. Therewill be no “make-up” test for persons who miss the test.

2For a lexicon of actuarial terms in English/French, see The Canadian Institute of Actuaries English-French lexicon [8], at

http://www.actuaries.ca/publications/lexicon/

UPDATED TO April 12, 2005

Information for Students in MATH 329 2005 01 5

1.3.4 Final Examination

Written examinations form an important part of the tradition of actuarial mathematics.The final examination in MATH 329 2004 01 will count for either 70% or 100% of thenumerical grade from which the submitted final letter grade will be computed. Wherea student’s Final Examination percentage is superior to her Term Mark percentage, theFinal Examination grade will replace the Term Mark grade in the calculations.

A 3-hour-long final examination will be scheduled during the regular examinationperiod for the winter term (April 14th, 2005 through April 29th, 2005). You are advisednot to make any travel arrangements that would prevent you from being present oncampus at any time during this period. Students who have religious or other constraintsthat could affect their ability to write examinations at particular times should watch forthe Preliminary Examination Timetable, as their rights to apply for special considerationat their faculty may have expired by the time the final examination timetable is published.

1.3.5 Supplemental Assessments

Supplemental Examination. For eligible students who obtain a Final Grade of For D in the course there will be a supplemental examination. (For information aboutSupplemental Examinations, see the McGill Calendar, [3].)

There is No Additional Work Option. “Will students with marks of D, F, or Jhave the option of doing additional work to upgrade their mark?” No. (“AdditionalWork” refers to an option available in certain Arts and Science courses, but not availablein this course.)

1.3.6 Machine Scoring

“Will the final examination be machine scored?” While there could be Multiple Choicequestions on quizzes, and/or the Final Examination, such questions will not be machinescored.

1.3.7 Plagiarism

While students are not discouraged from discussing assignment problems with their col-leagues, the work that you submit — whether through homework, the class test, or ontutorial quizzes or the final examination should be your own. The Handbook on StudentRights and Responsibilities states in ¶15(a)3 that

3http://ww2.mcgill.ca/students-handbook/chapter3secA.html

Information for Students in MATH 329 2005 01 6

“No student shall, with intent to deceive, represent the work of another personas his or her own in any academic writing, essay, thesis, research report,project or assignment submitted in a course or program of study or representas his or her own an entire essay or work of another, whether the material sorepresented constitutes a part or the entirety of the work submitted.”

You are also referred to the following URL:

http://www.mcgill.ca/integrity/studentguide/

1.4 Published Materials

1.4.1 Required Text-Book

The textbook for the course this semester is [1] Stephen G. Kellison, The Theory ofInterest, Second Edition. Irwin/McGraw-Hill, Boston, etc. (1991), ISBN 0-256-09150-1.

1.4.2 Website

These notes, and other materials distributed to students in this course, will be accessibleat the following URL:

http://www.math.mcgill.ca/brown/math329b.html

The notes will be in “pdf” (.pdf) form, and can be read using the Adobe Acrobat reader,which many users have on their computers. This free software may be downloaded fromthe following URL:

http://www.adobe.com/prodindex/acrobat/readstep.html 4

Where revisions are made to distributed printed materials — for example these informa-tion sheets — it is expected that the last version will be posted on the Web.

The notes will also be available via a link from the WebCT URL:

http://webct.mcgill.ca

but not all features of WebCT will be implemented.

1.4.3 Reference Books

The textbook used for 2001-2003 may be used as a reference: [5] Michael M. Parmen-tier, Theory of Interest and Life Contingencies, with Pension Applications: A Problem-Solving Approach, 3rd edition. ACTEX Publications, Winstead, Conn. (1999), ISBN0-56698-333-9.

4At the time of this writing the current version is 5.1.

Information for Students in MATH 329 2005 01 7

1.5 Other information

1.5.1 Prerequisites

It is your responsibility as a student to verify that you have the necessary calculusprerequisites. It would be foolish to attempt to take the course without them.

1.5.2 Calculators

The use of non-programmable, non-graphing calculators only will be permitted in home-work, tests, or the final examination in this course. Students may be required to convinceexaminers and invigilators that all memories have been cleared. The use of calculatorsthat are either graphing or programmable will not be permitted during test or examina-tions, in order to “level the playing field”.

1.5.3 Self-Supervision

This is not a high-school course, and McGill is not a high school. The monitoring ofyour progress before the final examination is largely your own responsibility. While theinstructor is available to help you, he cannot do so unless and until you identify theneed for help. While the significance of the homework assignments and class test in thecomputation of your grade is minimal, these are important learning experiences, andcan assist you in gauging your progress in the course. This is not a course that canbe crammed for: you must work steadily through the term if you wish to develop thefacilities needed for a strong performance on the final examination.

Working Problems on Your Own. You are advised to work large numbers of prob-lems from your textbook. The skills you acquire in solving textbook problems could havemuch more influence on your final grade than either the homework or the class test.

1.5.4 Escape Routes

At any time, even after the last date for dropping the course, students who are experi-encing medical or personal difficulties should not hesitate to consult their advisors or theStudent Affairs office of their faculty. Don’t allow yourself to be overwhelmed by suchproblems; the University has resource persons who may be able to help you.

1.5.5 Showing your work; good mathematical form; simplifying answers

When, in a quiz or examination problem, you are explicitly instructed to show all yourwork, failure to do so could result in a substantial loss of marks — possibly even allof the marks; this is the default . The guiding principle should be that you want to be

Information for Students in MATH 329 2005 01 8

able to communicate your precise reasoning to others and to yourself. You are alwaysexpected to “simplify” any algebraic or numerical expressions that arise in your solutionsor calculations. Verbal proofs are expected to be “convincing”: it will not be sufficientto simply describe mathematical expressions verbally.

Information for Students in MATH 329 2005 01 9

2 Timetable

Distribution Date: (original version) Tuesday, January 4th, 2005this revision as of April 12, 2005

(Subject to correction and change.)Section numbers refer to the text-book.5

MONDAY WEDNESDAY FRIDAY

JANUARY04 (TUESDAY!) §§1.1–

1.205 §§1.1–1.2 07 §§1.2–1.3

10 §§1.3–§§1.5 12 §1.6 14 §1.7, §1.8Course changes must be completed on MINERVA by Jan. 16, 2005

17 §§1.8, 1.9 (part) 19 §1.9, §§2.1, 2.2 21 §§2.2, 2.3, 2.4Deadline for withdrawal with fee refund = Jan. 23, 2005

24 §§2.5, 2.6 26 §§2.7, 2.8, §3.1 28 §§3.2, 3.3Verification Period: January 31–February 04, 2005

31 §3.3 1©FEBRUARY

02 §3.4 04 §§3.4, 3.5Deadline for withdrawal (with W) from course via MINERVA = Feb. 13, 2005

07 §3.7 09 §3.7 11 §§4.1, 4.214 §§4.3, 4.4 2© 16 §4.6 18 §4.6

Study Break: February 21–25, 2005No lectures, no regular office hours

21 NO LECTURE 23 NO LECTURE 25 NO LECTURE28 §5.3,§5.4

5

Notation: n© = Assignment #n due todayR© = Read OnlyX = reserved for eXpansion or review

Information for Students in MATH 329 2005 01 10

MONDAY WEDNESDAY FRIDAYMARCH

02 §5.4 04 §§6.1, 6.207 §6.3 3© 09 CLASS TEST 11 §§6.3, 6.414 §6.4 16 §7.1 18 §7.221 §7.3 23 §7.3, §7.4 25 NO LECTURE28 NO LECTURE 30

APRIL01

04 Discussion of oldexam

06 Discussion of oldexam

08 NO LECTURE

11 X 13 X

Information for Students in MATH 329 2005 01 11

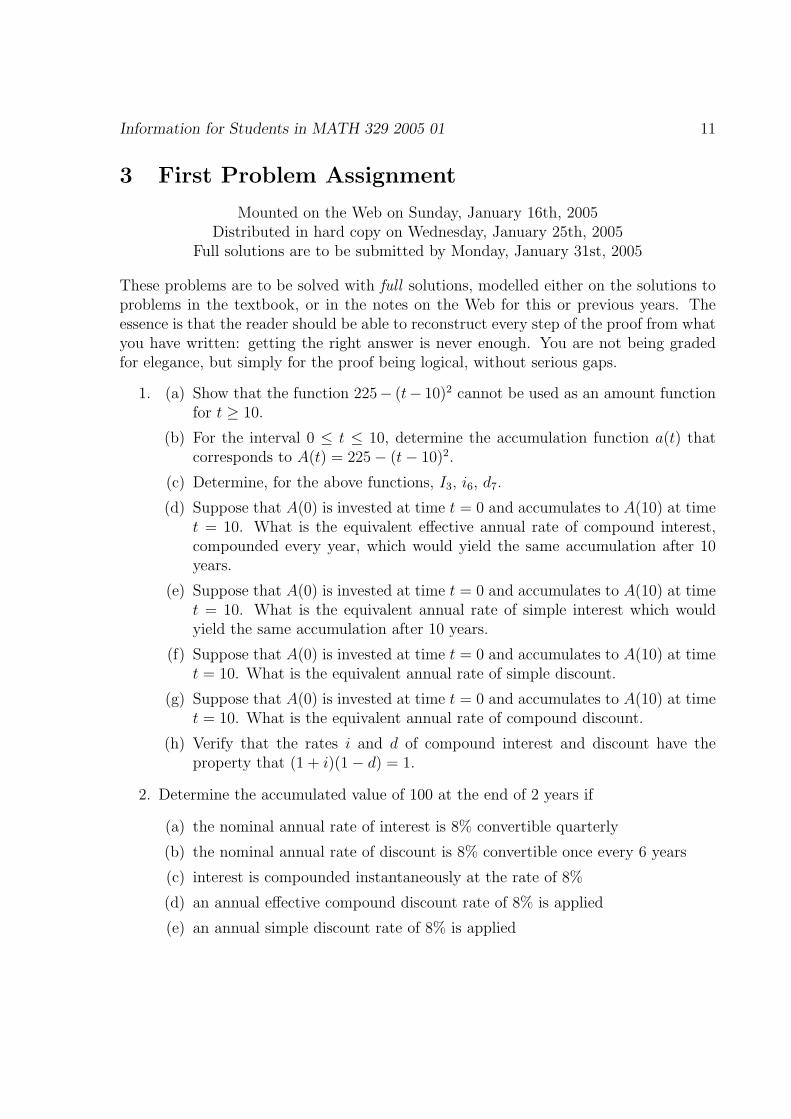

3 First Problem Assignment

Mounted on the Web on Sunday, January 16th, 2005Distributed in hard copy on Wednesday, January 25th, 2005

Full solutions are to be submitted by Monday, January 31st, 2005

These problems are to be solved with full solutions, modelled either on the solutions toproblems in the textbook, or in the notes on the Web for this or previous years. Theessence is that the reader should be able to reconstruct every step of the proof from whatyou have written: getting the right answer is never enough. You are not being gradedfor elegance, but simply for the proof being logical, without serious gaps.

1. (a) Show that the function 225− (t− 10)2 cannot be used as an amount functionfor t ≥ 10.

(b) For the interval 0 ≤ t ≤ 10, determine the accumulation function a(t) thatcorresponds to A(t) = 225− (t− 10)2.

(c) Determine, for the above functions, I3, i6, d7.

(d) Suppose that A(0) is invested at time t = 0 and accumulates to A(10) at timet = 10. What is the equivalent effective annual rate of compound interest,compounded every year, which would yield the same accumulation after 10years.

(e) Suppose that A(0) is invested at time t = 0 and accumulates to A(10) at timet = 10. What is the equivalent annual rate of simple interest which wouldyield the same accumulation after 10 years.

(f) Suppose that A(0) is invested at time t = 0 and accumulates to A(10) at timet = 10. What is the equivalent annual rate of simple discount.

(g) Suppose that A(0) is invested at time t = 0 and accumulates to A(10) at timet = 10. What is the equivalent annual rate of compound discount.

(h) Verify that the rates i and d of compound interest and discount have theproperty that (1 + i)(1− d) = 1.

2. Determine the accumulated value of 100 at the end of 2 years if

(a) the nominal annual rate of interest is 8% convertible quarterly

(b) the nominal annual rate of discount is 8% convertible once every 6 years

(c) interest is compounded instantaneously at the rate of 8%

(d) an annual effective compound discount rate of 8% is applied

(e) an annual simple discount rate of 8% is applied

Information for Students in MATH 329 2005 01 12

(f) interest is earned during the first year at a nominal annual rate of 8% con-vertible quarterly, and during the second year at a nominal annual rate ofdiscount of 8% convertible quarterly.

3. Today is New Year’s Day. In return for payments of 1500 at the end of January,February, and March, and of 3000 at the end of May, July, and September, aninvestor agrees to pay now the total value of the 6 payments, and to either makeor receive an additional payment at the end of December. Find the amount ofthat additional payment if it is known that the nominal annual interest rate is 6%,compounded monthly. (First set up an equation of value.)

4. Analogously to the “rule of 72”, you are asked to develop a rule of n to approximatehow long it takes for money to increase to 11

2times its initial value. (That is, to

determine a 2-digit integer N = 10n1 + n0 (where n0, n1 are decimal digits), forwhich (0.01)N

iis a good approximation to the number of years required.) Your

approximation should be best around 8%.

5. (a) Find the smallest nominal rate of interest convertible monthly at which theaccumulated value of 15,000 at the end of 3 years is at least 24,000.

(b) Find the smallest6 nominal rate of discount convertible semi-annually at whichthe accumulated value of 15,000 at the end of 3 years is at least 24,000.

6. Let x be a positive real number, 0 ≤ x < 1. Prove that

1

1− x≥ 1 + x

for all such x. Conclude that the accumulated value of 100 after 10 years at aninterest rate of x% is always less than or equal to the accumulated value of 100after 10 years at a discount rate of x%, with equality holding only when x = 0.

6Added 24 Jan 05: One student observed that the original wording of this problem, with largest , wasclearly not what was intended.

UPDATED TO April 12, 2005

Information for Students in MATH 329 2005 01 13

4 Second Problem Assignment

Mounted on the Web on Sunday, January 30th, 2005Distributed in hard copy on Wednesday, February 2nd, 2005

Full solutions are to be submitted by Monday, February 14th, 2005.(subject to correction)

These problems are to be solved with full solutions, modelled either on the solutions toproblems in the textbook, or in the notes on the Web for this or previous years. Theessence is that the reader should be able to reconstruct every step of the proof from whatyou have written: getting the right answer is never enough. You are not being gradedfor elegance, but simply for the proof being logical, without serious gaps.

1. (a) At a certain rate of compound interest an investment of 1000 will grow to1500 at the end of 12 years. Determine its value at the end of 5 years.

(b) At a certain rate of compound interest an investment of 1000 will grow to1500 at the end of 12 years. Determine precisely when its value is exactly1200.

(c) A debt of 7000 is due at the end of 5 years. If 2000 is paid at the end of1 year, what single payment should be made at the end of the 2nd year toliquidate the debt, assuming interest at the rate of 6.5% per year, compoundedquarterly.

(d) George agrees to buy his brother’s car for 7000. He makes a down payment of4000, and agrees to pay two equal payments, one at the end of 6 months, andthe other at the end of a year. If interest is being charged at 5% per annumeffective, how large should each of the equal payments be?

(e) A bill for 1500 is purchased for 1000 15 months before it is due. Determinethe nominal rate of discount, compounded monthly, which the purchaser ispaying.

(f) Bills for 1500 are regularly purchased for 1000 15 months before they are due.The purchaser knows that, among 10 such bills, he will be unable to collectanything on one of them, will have to pay his lawyers 500 each to effectcollection on 2 others, and will collect the others without any impediment.Lumping all of these together, what is the effective annual interest rate earnedby the purchaser on his investment, if it is assumed that the lawyers’ accountsare due at the same time as the bills?

2. A government offers savings bonds in multiples of $1000, which mature in 10 yearsat $2000, but pay no interest until they are redeemed.

Information for Students in MATH 329 2005 01 14

(a) Assuming interest compounded semi-annually, what nominal annual rate ofinterest does the bond holder earn?

(b) Suppose that the bonds earn interest at the nominal rate of i − 0.01 forthe first 5 years, compounded semi-annually; and that they earn interest atthe nominal rate of i + 0.01 compounded semi-annually for the last 5 years.Determine i.

(c) The government has contracted with a bank to market the bonds, at a costof $40 per $1000 bond. What interest rate, compounded semi-annually, is thegovernment paying for the net proceeds it receives for each $1000 bond?

3. The cash price of a new automobile is 18,000 plus 15.025% tax. The purchaseris prepared to finance the car and taxes at 18% convertible semi-monthly, and tomake payments of 230 at the end of every half-month for 3.5 years, with the firstpayment to be made one half-month after delivery. The dealer requires a downpayment upon delivery, both to make up the gap in the financing, and from whichto pay his immediate costs (commission to the salesperson, preparation costs, salestaxes).

(a) Determine the value of this down payment.

(b) Determine the value of the down payment if the purchaser decides, instead ofsemi-monthly payments, to make a payment of 460 at the end of every month,first payment a month after delivery, last payment to be made 3.5 years afterdelivery. The interest rate and compounding period do not change.

(c) Determine the value of the down payment if the original conditions are changedso that the first payment of 230 is made 1.5 months after delivery, but thesame number of payments of 230 are made as originally planned. The interestrate and compounding period do not change.

4. An employee aged exactly 40 decides to accumulate a fund for retirement at age 65by depositing 200 at the beginning of each month for 25 years. When she reachesage 65, she plans to withdraw a fixed amount at the beginning of each year for 15years. Assuming that all payments are made, determine the amount of the annualpayments that she will be able to withdraw:

(a) if the interest rate is always taken to be (a nominal annual rate of) 6% perannum, compounded monthly.

(b) if the interest rate is taken to be 6% per annum compounded monthly duringthe time when the fund is being built up, and 8% per annum effective whenshe reaches age 65.

Information for Students in MATH 329 2005 01 15

(c) if the interest rate is taken to be 4% per annum compounded monthly for thecoming 5 years, then 6% per annum compounded monthly for the next 20years while the fund is being built up, then 8% per annum effective when thefund is paying out annual payments.

5. In his will, a benefactor of McGill contributes a large sum of money to establisha fund, whose proceeds are to be used to provide annual bursaries of 5000 to6 actuarial students. The principal of the fund is to remain constant, and thebursaries are funded by the interest earned, forever.

(a) If the effective annual interest rate is assumed to be 6% forever, determine thelump sum that the benefactor’s estate needs to contribute to McGill a yearbefore the first payment of bursaries.

(b) If the effective annual interest rate is assumed to be 6% forever, determinethe lump sum that the benefactor’s estate needs to contribute to McGill ifthe first bursaries are to be issued immediately.

(c) Suppose that each student receives not a bursary of 5000, but an annualannuity-due of 1250 for 4 years. Under these changed conditions, determinethe lump sum payment needed now if the first bursaries are to be awardedimmediately or 1 year hence respectively. (The number of awards will remainthe same — each year 6 students are awarded a 4-year sequence of bursarypayments of 1250, the first payment to be made immediately.)

6. Let m and n be positive integers. Consider an annuity-immediate which pays 1 atthe end of every period for mn periods. Explain in words why each of the followingformulæ represents the value of this annuity m + 1 years before the first paymentis made. (If you have doubts about the truth of this claim, you may wish to verifyalgebraically that the claim is correct before you attempt to explain it in words.)

(a) vm · amn

(b) am(n+1)

− am

(c) vm · am(n+1)

− vm(n+2) · sm

Information for Students in MATH 329 2005 01 16

5 Solutions, First Problem Assignment

Mounted on the Web on Thursday, February 10th, 2005(Caveat lector! 7 There could be some undetected misprints or errors.)Full solutions were to be submitted by Monday, January 31st, 2005

Students were advised that “These problems are to be solved with full solutions, modelledeither on the solutions to problems in the textbook, or in the notes on the Web for thisor previous years. The essence is that the reader should be able to reconstruct everystep of the proof from what you have written: getting the right answer is never enough.You are not being graded for elegance, but simply for the proof being logical, withoutserious gaps.”

1. (a) Show that the function 225− (t− 10)2 cannot be used as an amount functionfor t ≥ 10.

(b) For the interval 0 ≤ t ≤ 10, determine the accumulation function a(t) thatcorresponds to A(t) = 225− (t− 10)2.

(c) Determine, for the above functions, I3, i6, d7.

(d) Suppose that A(0) is invested at time t = 0 and accumulates to A(10) at timet = 10. What is the equivalent effective annual rate of compound interest,compounded every year, which would yield the same accumulation after 10years.

(e) Suppose that A(0) is invested at time t = 0 and accumulates to A(10) at timet = 10. What is the equivalent annual rate of simple interest which wouldyield the same accumulation after 10 years.

(f) Suppose that A(0) is invested at time t = 0 and accumulates to A(10) at timet = 10. What is the equivalent annual rate of simple discount.

(g) Suppose that A(0) is invested at time t = 0 and accumulates to A(10) at timet = 10. What is the equivalent annual rate of compound discount.

(h) Verify that the rates i and d of compound interest and discount have theproperty that (1 + i)(1− d) = 1.

Solution:

(a) By condition [1, 2, p. 2], an accumulation function must be increasing (or atleast non-decreasing); the same property must hold for an amount function,

7Let the reader beware!

Information for Students in MATH 329 2005 01 17

since it is a positive multiple of its corresponding accumulation function. ButA(t) = 225− (t− 10)2 has the property that

d

dtA(t) = 2(10− t)

which is increasing only when 20− t ≥ 0, i.e., when t ≤ 10.

(b) a(t) =A(t)

A(0)=

125 + 20t− t2

125=

(5 + t)(25− t)

125.

(c)

I3 = A(3)− A(2) = 15

i6 = a(6)− a(5) =A(6)− A(5)

A(5)=

9

200

d7 =I7

A(7)=

A(7)− A(6)

A(7)=

7

216

(d) Let i be the equivalent annual rate of compound interest. Since A(10) = 225,A(0) = 125,

125(1 + i)10 = 225 ⇒ 1 + i =

(225

125

) 110

⇒ i =10√

1.8− 1 = 6.0540482%.

(e) Let i be the equivalent annual rate of simple interest. Then

125(1 + 10i) = 225 ⇒ 1 + 10i =225

125⇒ i = 8%.

(f) Let d be the equivalent annual rate of simple discount. Then

125 = (1− 10d)225 ⇒ d =2

45= 4.4444%.

(g) Let d be the equivalent annual rate of simple discount. Then

125 = 225(1− d)10 ⇒ d = 1− 10

√5

9= 5.70845551%.

(h) (1 + 0.060540482)(1− 0.0570845551) = 1 .

Information for Students in MATH 329 2005 01 18

2. Determine the accumulated value of 100 at the end of 2 years if

(a) the nominal annual rate of interest is 8% convertible quarterly

(b) the nominal annual rate of discount is 8% convertible once every 6 years

(c) interest is compounded instantaneously at the rate of 8%

(d) an annual effective compound discount rate of 8% is applied

(e) an annual simple discount rate of 8% is applied

(f) interest is earned during the first year at a nominal annual rate of 8% con-vertible quarterly, and during the second year at a nominal annual rate ofdiscount of 8% convertible quarterly.

Solution:

(a) A nominal annual interest rate of 8% convertible quarterly is equivalent to a3-month rate of 8

4% = 2%. The accumulated value of 100 after 2

14

= 8 quarter

years is100(1.02)8 = 117.17 .

(b) We are given that

d( 16) = 8% .

The accumulated value of 100 after 26

= 13

6-year periods

100 (1− (6× 0.08))−26 = 124.36 .

(c) Interest compounded instantaneously at the rate of 8% yields an accumulationfactor of

limm→∞

(1 +

0.08

m

)m

= e0.08 .

After 2 years 100 accumulates to

100e2×0.08 = 117.35 .

(d) At an annual effective compound discount rate of 8%, 100 accumulates after2 years to

100(1− 0.08)−2 = 118.15 .

(e) At an annual simple discount rate of 8%, 100 accumulates after 2 years to

100

1− 2(0.08)= 119.05 .

Information for Students in MATH 329 2005 01 19

(f) The accumulated value of 100 after the first year will be 100(1.02)4. Duringthe second year this amount will accumulate to a final amount of

100(1.02)4

(1− 0.08

4

)−4

= 100

(1.02

0.98

)4

= 117.36 .

3. Today is New Year’s Day. In return for payments of 1500 at the end of January,February, and March, and of 3000 at the end of May, July, and September, aninvestor agrees to pay now the total value of the 6 payments, and to either makeor receive an additional payment at the end of December. Find the amount ofthat additional payment if it is known that the nominal annual interest rate is 6%,compounded monthly. (First set up an equation of value.)

Solution: Let us denote the final payment by the investor by X. The effectivemonthly interest rate is 6

12% = 1

2%. We will take as the comparison date the end

of December (although any date chosen would yield the same information). Thevalue on 31 December of the payments paid to the investor is

1500((1.005)11 + (1.005)10 + (1.005)9

)

+3000((1.005)7 + (1.005)5 + (1.005)3

)= 13, 957.74 .

The value on 31 December (just after she has paid the last payment) of the pay-ments paid out by the investor is

(3(1500) + 3(3000))(1.005)12 + X = 14332.65 + X .

Equating the two values yields X = −374.91. Thus the investor is entitled toreceive a final payment of 374.91 at the end of December. (The fact that the finalpayment would be received by the investor, rather than paid by her could havebeen reasoned without calculation; we didn’t need the mathematical calculation totell us that from the sign of the answer.)

4. Analogously to the “rule of 72”, you are asked to develop a rule of n to approximatehow long it takes for money to increase to 11

2times its initial value. (That is, to

determine a 2-digit integer N = 10n1 + n0 (where n0, n1 are decimal digits), forwhich (0.01) · N

iis a good approximation to the number of years required.) Your

approximation should be best around 8%.

Solution: We have to approximate a solution to the equation

(1 + i)n = 1.5,

which is equivalent to

n =ln 1.5

i· i

ln(1 + i).

We find that

Information for Students in MATH 329 2005 01 20

i (ln 1.5) · i

ln(1 + i)7.0% 0.4198.0% 0.4219.0% 0.423

so we take N = 42.

5. (a) Find the smallest nominal rate of interest convertible monthly at which theaccumulated value of 15,000 at the end of 3 years is at least 24,000.

(b) Find the smallest nominal rate of discount convertible semi-annually at whichthe accumulated value of 15,000 at the end of 3 years is at least 24,000.

Solution:

(a) Let i denote the nominal interest rate sought. Then

15000

(1 +

i

12

)36

≥ 24000

⇔(

1 +i

12

)36

≥ 1.6000

⇔ 1 +i

12≥ (1.6)

136 = 1.013141254

so i =≥ 15.7695048%. The smallest interest rate is 15.8%.

(b) This could be considered a trick question; but the fact is that the word largestwas not intended. I “solve” it both as written, and with the intended wording.Let d denote the nominal discount rate.

As written, “largest” Then

15000

(1− d

2

)−6

≥ 24000

⇔(

1− d

2

)6

≤ 5

8

⇔ 1− d

2≤ 6

√5

8= .9246555971

implying that d ≥ 15.068880%. Thus any discount rate d ≥ 15.1% hasthe desired property. There is no largest rate, since, as the rate d(2)

approaches 100% from below, the accumulated value approaches ∞. We

Information for Students in MATH 329 2005 01 21

haven’t attached a meaning to discount rates above 100%. (As for adiscount rate of 100% — that does make sense, but would not permit theaccumulation of funds: if we discount a sum X of money back from time1 to time 0 at an effective discount rate of 100%, we obtain a presentvalue of 0.)

Corrected to “smallest”

15000

(1− d

2

)−6

≤ 24000

⇔(

1− d

2

)6

≤ 5

8

⇔ 1− d

2≤ 6

√5

8= .9246555971

implying that d ≥ 15.068880%. Thus the smallest discount rate is 15.1%.

6. Let x be a positive real number, 0 ≤ x < 1. Prove that

1

1− x≥ 1 + x

for all such x. Conclude that the accumulated value of 100 after 10 years at aninterest rate of x% is always less than or equal to the accumulated value of 100after 10 years at a discount rate of x%, with equality holding only when x = 0.

Solution: Since x2 is a square, it cannot be negative, and can be 0 only when x = 0;hence 1− x2 ≤ 1, with equality holding precisely when x = 0. But this inequalityis equivalent to

1 ≥ (1− x)(1 + x)

or to1

1− x≥ 1 + x

since the inequality is preserved when we divide both sides by the positive number1− x; again, equality holds when x = 0.

The accumulated value of 100 at the interest rate of x% is 100(1 + x

100

)10. We

apply the preceding argument 10 times, after replacing x by x100

: this cannot exceed

100(1− x

100

)−10, which is the accumulated value of 100 at the discount rate of x%.

Equality holds when x100

= 0, i.e., when x = 0.

Information for Students in MATH 329 2005 01 22

6 Third Problem Assignment

Mounted on the Web on Sunday, February 13th, 2005Distributed in hard copy on Wednesday, February 16th, 2005

Full solutions were to be submitted by March 7th, 2005.

These problems are to be solved with full solutions, modelled either on the solutions toproblems in the textbook, or in the notes on the Web for this or previous years. Theessence is that the reader should be able to reconstruct every step of the proof from whatyou have written: getting the right answer is never enough. You are not being gradedfor elegance, but simply for the proof being logical, without serious gaps.

1. McGill plans to create a scholarship fund that will eternally pay 50 students amonthly stipend of $200 at the beginning of months September through April,plus an amount of $300 on the following May 1st.

(a) If interest is assumed to be at a nominal annual rate of 6% per annum, com-pounded monthly, determine the amount that is needed in this fund on Sep-tember 1st just before the fund begins making payments.

(b) Determine the amount that will be in the fund just after the December schol-arship payments in the first year, and on September 1st of the following year,just before the September payments.

(c) Suppose that at the beginning of September, 8 years after the fund is estab-lished, it is decided to increase the capital in the fund because the interestrate has changed to 4% per annum compounded monthly. Determine howmuch additional capital needs to be added to the fund.

(d) Suppose that 2 years after the interest rate is changed to 4%, it changes again,this time to 8%. This time it is decided to leave the capital unchanged, butto increase the payments to students by a lump sum of $M to each student,payable on December 1st, together with the regular December payment underthe scholarship. Determine the amount of that lump sum payment.

2. A loan of 10,000 is to be repaid by regular, half-yearly payments of 1,000, the firstto be made at the end of the 3rd year. The loan will be paid off by a final paymentwhich must be at least 1,000.

(a) If the interest rate is to be 8% per annum, compounded semi-annually, deter-mine the amount of the final payment, and when it is made.

(b) Suppose that the final payment is now not more than 1,000. and the inter-est rate remains 8% per annum compounded semi-annually. Determine theamount of the final payment, and when it is made.

Information for Students in MATH 329 2005 01 23

(c) Suppose that, after signing his original commitment, the borrower decidesthat he would like to make the first payment 6 months from the date ofborrowing, and that all the payments under this loan should be exactly equal.If the interest rate is 6% per annum, compounded semi-annually, determinethat payment level that would be closest to 1000 per half-year, and determineexactly when the loan will be paid off.

3. (An acknowledgement of source of this problem will be contained in the solutions,when published.) Katherine, 25 years old, deposits 10,000 at the beginning ofevery 4-year period into an RSSP account. The account pays compound interestannually, at the effective annual rate i. The accumulated amount in the account atthe end of 40 years is X, which is 6 times the accumulated amount in the accountat the end of 20 years. Determine X.

4. For each of the following sequences of payments as of the time stated,

• express the value using standard symbols, as simple as possible;

• give a formula for the value (in terms of i, v, d, etc.);

• evaluate using a calculator or computer — not with tables.

(a) a perpetuity-immediate paying 1 per year at effective annual interest rate4.25%, evaluated 1 year before the first payment;

(b) a perpetuity paying 1 per year at effective annual interest rate 4.25%, evalu-ated 2 years before the first payment;

(c) a perpetuity-due paying 1 per half-year at nominal interest rate 5%, com-pounded semi-annually, evaluated just before the first payment;

(d) a 20-year increasing annuity paying 1 the first year, 2 the second year, 3 the3rd year, etc., at an interest rate of 7% per year effective, evaluated just afterthe last payment;

(e) a 20-year increasing annuity paying 1 the first year, 2 the second year, 3 the3rd year, etc., at an interest rate of 7% per year effective, evaluated at thetime of the 2nd payment;

(f) a 10-year decreasing annuity paying 1 less each quarter-year, evaluated justafter the last payment, where the nominal interest rate is a 8% annual, com-pounded quarterly;

5. X and Y have sold their home for 400,000, and wish to purchase an annuity-immediate so that they can spread the proceeds over the next 10 years. The firstpayment will be one month from the date of purchase of the annuity.

Information for Students in MATH 329 2005 01 24

(a) Determine the level monthly payments they will receive if the effective annualinterest rate is 6%.

(b) X and Y live frugally, and don’t think they need as much income now asthey will as time passes. Accordingly they plan to receive monthly paymentswhich will gradually increase. If the first payment is 3,000, and the paymentsincrease each month by the same dollar amount K, determine K. The effectiveannual interest rate remains 6%. What is the final monthly payment?

(c) Suppose that the payments remain constant in any year. The first year’smonthly payments are all 3000, the next year’s 3000+L, the next years’ 3000+2L, 3000 + 3L, . . . , 3000 + 9L. Determine L if the nominal interest rate is6%, compounded monthly.

Information for Students in MATH 329 2005 01 25

7 Solutions, Second Problem Assignment

Mounted on the Web on March 3rd, 2005Full solutions were to be submitted by February 14th, 2005.

(Subject to Correction)

These problems were to be solved with full solutions, modelled either on the solutionsto problems in the textbook, or in the notes on the Web for this or previous years. Theessence is that the reader should be able to reconstruct every step of the proof from whatyou have written: getting the right answer is never enough. You are not being gradedfor elegance, but simply for the proof being logical, without serious gaps.

1. (a) At a certain rate of compound interest an investment of 1000 will grow to1500 at the end of 12 years. Determine its value at the end of 5 years.

(b) At a certain rate of compound interest an investment of 1000 will grow to1500 at the end of 12 years. Determine precisely when its value is exactly1200.

(c) A debt of 7000 is due at the end of 5 years. If 2000 is paid at the end of1 year, what single payment should be made at the end of the 2nd year toliquidate the debt, assuming interest at the rate of 6.5% per year, compoundedquarterly.

(d) George agrees to buy his brother’s car for 7000. He makes a down payment of4000, and agrees to pay two equal payments, one at the end of 6 months, andthe other at the end of a year. If interest is being charged at 5% per annumeffective, how large should each of the equal payments be?

(e) A bill for 1500 is purchased for 1000 15 months before it is due. Determinethe nominal rate of discount, compounded monthly, which the purchaser ispaying.

(f) Bills for 1500 are regularly purchased for 1000 15 months before they are due.The purchaser knows that, among 10 such bills, he will be unable to collectanything on one of them, will have to pay his lawyers 500 each to effectcollection on 2 others, and will collect the others without any impediment.Lumping all of these together, what is the effective annual interest rate earnedby the purchaser on his investment, if it is assumed that the lawyers’ accountsare due at the same time as the bills?

Solution:

(a) Let I be the effective annual rate of compound interest. Then

1000(1 + i)12 = 1500 (1)

Information for Students in MATH 329 2005 01 26

implies that

(1 + i)5 =

(1500

1000

) 512

= 1.184053587

so the investment is worth 1184.05 after 5 years.

(b) Let t be the time in years when the investment is worth exactly 1200. Then

1000(1 + i)t = 1200 ,

where i is the effective annual rate of compound interest. By equation (1),

ln(1 + i) =ln 1.5

12.

Hence

t =ln 1.2

ln(1 + i)=

12× ln 1.2

ln 1.5= 5.395923442 :

the investment has the desired value after 5.40 years.

(c) Let x denote the payment that must be made at the end of the 2nd year. Theequation of value at that time is

x + 2000

(1 +

0.065

4

)4

= 7000

(1 +

0.065

4

)−12

implying that

x = −2000

(1 +

0.065

4

)4

+ 7000

(1 +

0.065

4

)−12

= 3635.67

should be paid at the end of the second year to liquidate the debt.

(d) Let x denote the amount of each of the payments that should be made at theends of 6 months and 1 year. Then the equation of value at time 0 is

x((1.05)−

12 + (1.05)−1

)= 7000− 4000 = 3000 ,

implying that

x =3000

(1.05)−12 + (1.05)−1

= 1555.79 .

(e) Let d be the effective monthly rate of discount. Then

1000 = (1− d)151500 ,

Information for Students in MATH 329 2005 01 27

implying that

d = 1−(

1000

1500

) 115

= 2.66689392% .

This is the effective monthly rate. The nominal annual rate of discount,compounded monthly, is, therefore 12d = 32%.

(f) Of 10 bills which mature in 15 months, the total return that will enure to thepurchaser at that time is

7(1500) + 2(1500− 500) + 0(1500) = 12500 .

If we denote the effective annual interest rate by i, then the discounted valueof 12500 at time t = 0 will be 12500(1 + i)−

1512 . The equation of value at time

t = 0 is, therefore,

12500(1 + i)−1512 = 10(1000) = 10000 ,

implying that (1 + i)54 = 1.25, so i = 1.250.8 − 1 = 19.5440625%.

2. A government offers savings bonds in multiples of $1000, which mature in 10 yearsat $2000, but pay no interest until they are redeemed.

(a) Assuming interest compounded semi-annually, what nominal annual rate ofinterest does the bond holder earn?

(b) Suppose that the bonds earn interest at the nominal rate of i − 0.01 forthe first 5 years, compounded semi-annually; and that they earn interest atthe nominal rate of i + 0.01 compounded semi-annually for the last 5 years.Determine i.

(c) The government has contracted with a bank to market the bonds, at a costof $40 per $1000 bond. What interest rate, compounded semi-annually, is thegovernment paying for the net proceeds it receives for each $1000 bond?

Solution:

(a) Let i be the nominal interest rate, compounded semi-annually, earned by thepurchaser. The equation of value at time 10 is then

1000

(1 +

i

2

)20

= 2000

implying that

i = 2(2

120 − 1

)= 7.0529848%.

Information for Students in MATH 329 2005 01 28

(b) The equation of value is now

1000

(1 +

i− 1

2

)10 (1 +

i + 1

2

)10

= 2000

implying that(

1 +i− 0.01

2

)(1 +

i + 0.01

2

)= 2

110

⇒(

1 +i

2

)2

− (0.01)2

4= 2

110

⇒ 1 +i

2=

(2

110 +

(0.01)2

4

) 12

⇒ i = 2

(2

110 +

(0.01)2

4

) 12

− 2

= 7.0553996%

(c) Let i be the nominal interest rate, compounded semi-annually. From thegovernment’s point of view the equation of value at maturity is

960

(1 +

i

2

)20

= 2000

implying that

i = 2

((2000

960

) 120

− 1

)= 7.4760322%

3. The cash price of a new automobile is 18,000 plus 15.025% tax. The purchaseris prepared to finance the car and taxes at 18% convertible semi-monthly, and tomake payments of 230 at the end of every half-month for 3.5 years, with the firstpayment to be made one half-month after delivery. The dealer requires a downpayment upon delivery, both to make up the gap in the financing, and from whichto pay his immediate costs (commission to the salesperson, preparation costs, salestaxes).

(a) Determine the value of this down payment.

(b) Determine the value of the down payment if the purchaser decides, instead ofsemi-monthly payments, to make a payment of 460 at the end of every month,first payment a month after delivery, last payment to be made 3.5 years afterdelivery. The interest rate and compounding period do not change.

Information for Students in MATH 329 2005 01 29

(c) Determine the value of the down payment if the original conditions are changedso that the first payment of 230 is made 1.5 months after delivery, but thesame number of payments of 230 are made as originally planned. The interestrate and compounding period do not change.

Solution:

(a) The present value of the future payments is

230 · a(3.5)(24) 0.18

24= 230

(1− (1.0075)−84

0.0075

)

= 14295.41185

The excess of the purchase price and taxes over the present value of the futurepayments is, therefore,

(1.0015025)(18000)− 14295.41185 = 6409.08815 .

Thus the down payment will be 6,409.09.

(b) We can still interpret the payments as constituting an annuity-immediate.But the interval of payments has paid, while the compounding interval hasnot. So we need to determine the interest rate that corresponds to one month.This is

(1.0075)2 − 1 = 0.01505625 .

The present value of the future payments is

460a(3.5)(12) 0.01505625

= 460 · 1− (1.01505625)−42

0.01505625= 14242.00433

The excess of the purchase price and taxes over the present value of the futurepayments is, therefore,

(1.0015025)(18000)− 14242.00433 = 6462.49567 .

Thus the down payment will be 6,462.50.

(c) Since the repayment schedule is delayed by 2 payments, which are added atthe end, the present value of the future payments is

230a(3.5)(24)+2 0.18

24− 230a2 0.18

24= 230

(1− (1.0075)−86

0.0075− 1− (1.0075)−2

0.0075

)

= 230(63.20976257− 1.977722907)

= 14083.36912

Information for Students in MATH 329 2005 01 30

The excess of the purchase price and taxes over the present value of the futurepayments is now

(1.0015025)(18000)− 14083.36912 = 6621.13088 .

Thus the down payment will now be 6,621.13.

4. An employee aged exactly 40 decides to accumulate a fund for retirement at age 65by depositing 200 at the beginning of each month for 25 years. When she reachesage 65, she plans to withdraw a fixed amount at the beginning of each year for 15years. Assuming that all payments are made, determine the amount of the annualpayments that she will be able to withdraw:

(a) if the interest rate is always taken to be (a nominal annual rate of) 6% perannum, compounded monthly.

(b) if the interest rate is taken to be 6% per annum compounded monthly duringthe time when the fund is being built up, and 8% per annum effective whenshe reaches age 65.

(c) if the interest rate is taken to be 4% per annum compounded monthly for thecoming 5 years, then 6% per annum compounded monthly for the next 20years while the fund is being built up, then 8% per annum effective when thefund is paying out annual payments.

Solution:

(a) The effective interest rate per month is 6%12

= 12%. The number of contributions

will be 25× 12 = 300. The value of the fund at maturity, when the employeereaches age 65, will be

200s25×12 12% = 200

((1.005)300 − 1

(0.005)(

11.005

))

= 139291.7864

The withdrawals from the fund will be once a year. If we wish to interpretthem as payments under an annuity-due, we need to determine the rate ofinterest that corresponds to the period between the payments, i.e. to a 1-yearperiod; that is, we need to determine i, knowing i(12). This gives us an annualrate of (1.005)12 − 1 = 6.1677812%. If the annual withdrawal from the fund,at the beginning of each year, be denoted by X, then the equation of valuejust before the first withdrawal is

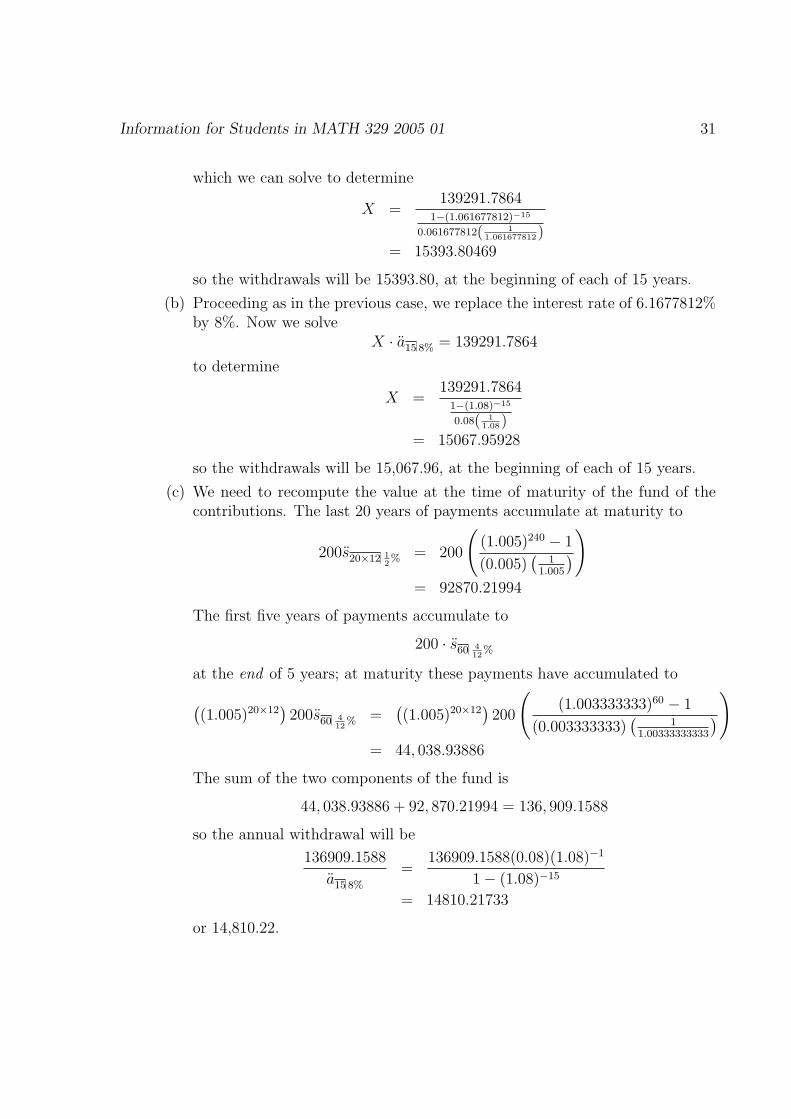

X · a15 6.1677812% = 139291.7864

Information for Students in MATH 329 2005 01 31

which we can solve to determine

X =139291.7864

1−(1.061677812)−15

0.061677812( 11.061677812)

= 15393.80469

so the withdrawals will be 15393.80, at the beginning of each of 15 years.

(b) Proceeding as in the previous case, we replace the interest rate of 6.1677812%by 8%. Now we solve

X · a15 8% = 139291.7864

to determine

X =139291.7864

1−(1.08)−15

0.08( 11.08)

= 15067.95928

so the withdrawals will be 15,067.96, at the beginning of each of 15 years.

(c) We need to recompute the value at the time of maturity of the fund of thecontributions. The last 20 years of payments accumulate at maturity to

200s20×12 12% = 200

((1.005)240 − 1

(0.005)(

11.005

))

= 92870.21994

The first five years of payments accumulate to

200 · s60 412

%

at the end of 5 years; at maturity these payments have accumulated to

((1.005)20×12

)200s60 4

12% =

((1.005)20×12

)200

((1.003333333)60 − 1

(0.003333333)(

11.00333333333

))

= 44, 038.93886

The sum of the two components of the fund is

44, 038.93886 + 92, 870.21994 = 136, 909.1588

so the annual withdrawal will be

136909.1588

a15 8%

=136909.1588(0.08)(1.08)−1

1− (1.08)−15

= 14810.21733

or 14,810.22.

Information for Students in MATH 329 2005 01 32

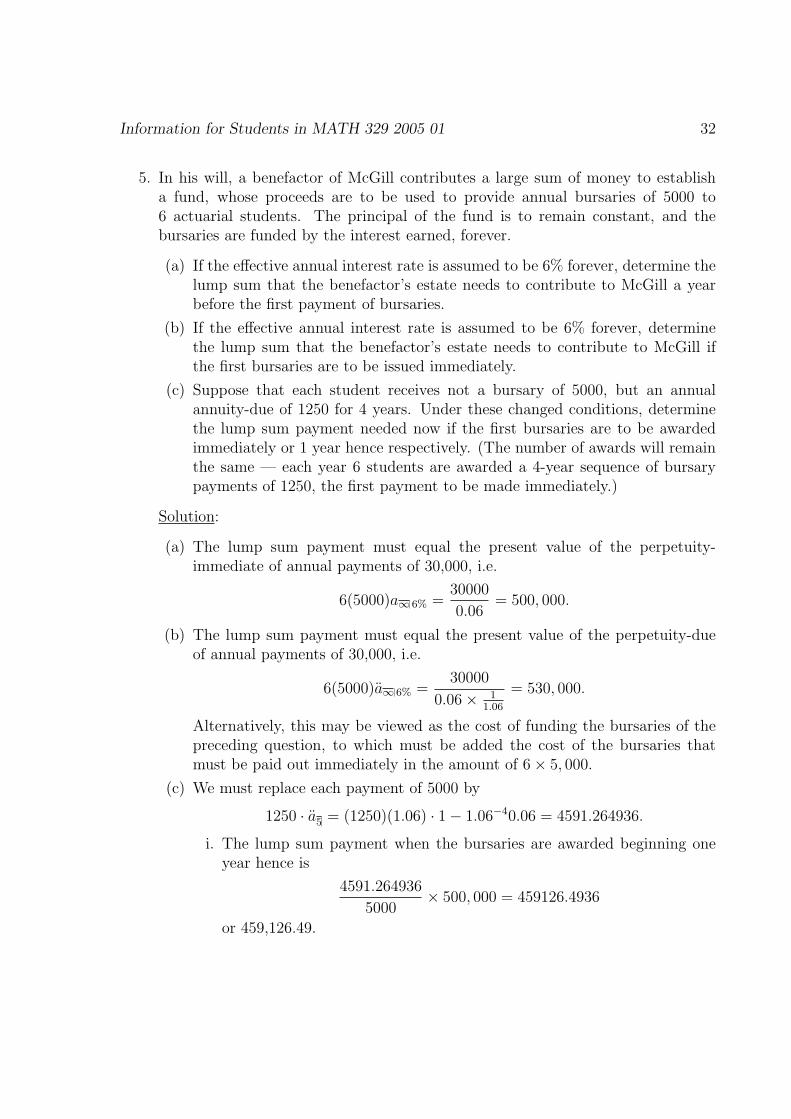

5. In his will, a benefactor of McGill contributes a large sum of money to establisha fund, whose proceeds are to be used to provide annual bursaries of 5000 to6 actuarial students. The principal of the fund is to remain constant, and thebursaries are funded by the interest earned, forever.

(a) If the effective annual interest rate is assumed to be 6% forever, determine thelump sum that the benefactor’s estate needs to contribute to McGill a yearbefore the first payment of bursaries.

(b) If the effective annual interest rate is assumed to be 6% forever, determinethe lump sum that the benefactor’s estate needs to contribute to McGill ifthe first bursaries are to be issued immediately.

(c) Suppose that each student receives not a bursary of 5000, but an annualannuity-due of 1250 for 4 years. Under these changed conditions, determinethe lump sum payment needed now if the first bursaries are to be awardedimmediately or 1 year hence respectively. (The number of awards will remainthe same — each year 6 students are awarded a 4-year sequence of bursarypayments of 1250, the first payment to be made immediately.)

Solution:

(a) The lump sum payment must equal the present value of the perpetuity-immediate of annual payments of 30,000, i.e.

6(5000)a∞ 6% =30000

0.06= 500, 000.

(b) The lump sum payment must equal the present value of the perpetuity-dueof annual payments of 30,000, i.e.

6(5000)a∞ 6% =30000

0.06× 11.06

= 530, 000.

Alternatively, this may be viewed as the cost of funding the bursaries of thepreceding question, to which must be added the cost of the bursaries thatmust be paid out immediately in the amount of 6× 5, 000.

(c) We must replace each payment of 5000 by

1250 · a5 = (1250)(1.06) · 1− 1.06−40.06 = 4591.264936.

i. The lump sum payment when the bursaries are awarded beginning oneyear hence is

4591.264936

5000× 500, 000 = 459126.4936

or 459,126.49.

Information for Students in MATH 329 2005 01 33

ii. The lump sum payment when the bursaries are awarded beginning im-mediately is

4591.264936

5000× 530, 000 = 486674.0832

or 486,674.08.

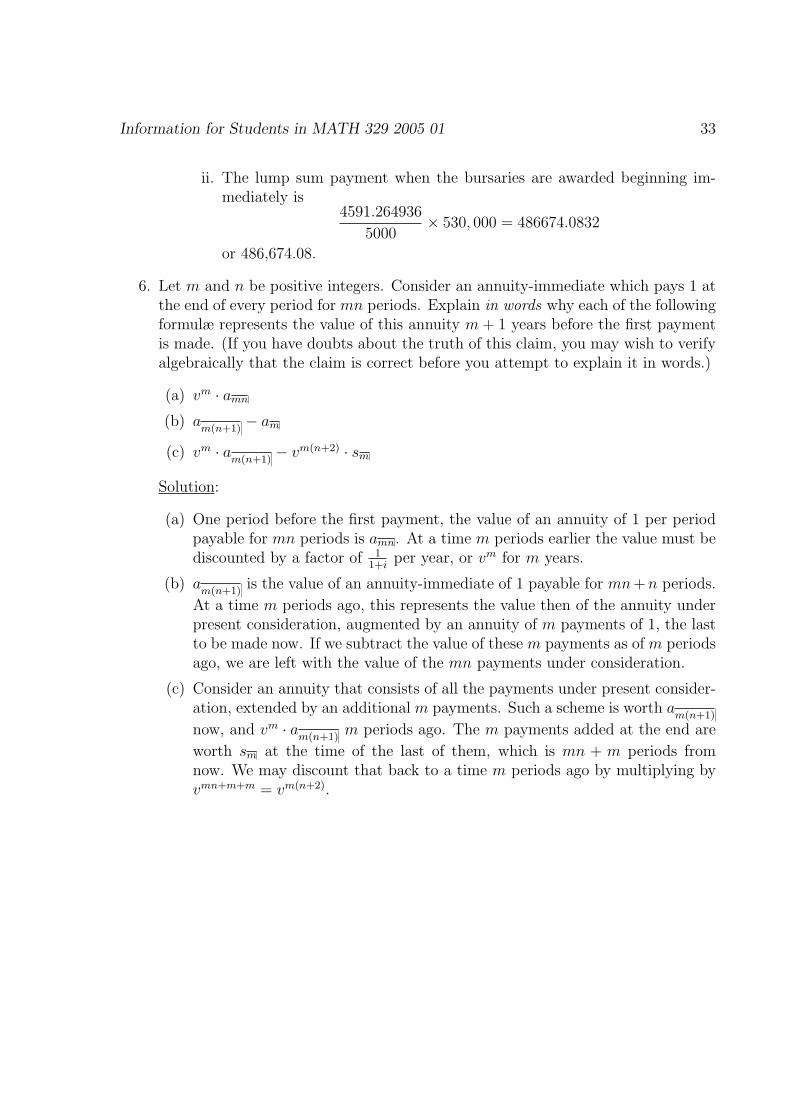

6. Let m and n be positive integers. Consider an annuity-immediate which pays 1 atthe end of every period for mn periods. Explain in words why each of the followingformulæ represents the value of this annuity m + 1 years before the first paymentis made. (If you have doubts about the truth of this claim, you may wish to verifyalgebraically that the claim is correct before you attempt to explain it in words.)

(a) vm · amn

(b) am(n+1)

− am

(c) vm · am(n+1)

− vm(n+2) · sm

Solution:

(a) One period before the first payment, the value of an annuity of 1 per periodpayable for mn periods is amn. At a time m periods earlier the value must bediscounted by a factor of 1

1+iper year, or vm for m years.

(b) am(n+1)

is the value of an annuity-immediate of 1 payable for mn+n periods.

At a time m periods ago, this represents the value then of the annuity underpresent consideration, augmented by an annuity of m payments of 1, the lastto be made now. If we subtract the value of these m payments as of m periodsago, we are left with the value of the mn payments under consideration.

(c) Consider an annuity that consists of all the payments under present consider-ation, extended by an additional m payments. Such a scheme is worth a

m(n+1)

now, and vm · am(n+1)

m periods ago. The m payments added at the end are

worth sm at the time of the last of them, which is mn + m periods fromnow. We may discount that back to a time m periods ago by multiplying byvmn+m+m = vm(n+2).

Information for Students in MATH 329 2005 01 34

8 Class Tests

8.1 Class Test, Version 1

McGILL UNIVERSITY, FACULTY OF SCIENCECLASS TEST in MATH 329, THEORY OF INTEREST

EXAMINER: Professor W. G. Brown DATE: Wednesday, 9 March, 2005.ASSOCIATE EXAMINER: Professor N. Sancho TIME: 45 minutes, 14:35→15:20

FAMILY NAME:

GIVEN NAMES:

STUDENT NUMBER:

Instructions

• The time available for writing this test is about 45 minutes.

• This test booklet consists of this cover, Pages 35 through 38 containing questions togetherworth 66 marks; and Page 39, which is blank.

• Show all your work. All solutions are to be written in the space provided on the page wherethe question is printed. When that space is exhausted, you may write on the facing page, onthe blank page, or on the back cover of the booklet, but you must indicate any continuationclearly on the page where the question is printed! (Please inform the instructor if you findthat your booklet is defective.)

• All your writing — even rough work — must be handed in.

• Calculators. While you are permitted to use a calculator to perform arithmetic and/or ex-ponential calculations, you must not use the calculator to calculate such actuarial functionsas ani, sni, etc. without first stating a formula for the value of the function in terms ofexponentials and/or polynomials involving n and the interest rate. You must not use yourcalculator in any programmed calculations. If your calculator has memories, you are expectedto have cleared them before the test.

• In your solutions to problems on this test you are expected to show all your work. You areexpected to simplify algebraic and numerical answers as much as you can.

• Your neighbours may be writing a version of this test which is different from yours.

PLEASE DO NOT WRITE INSIDE THIS BOX

1(a) 1(b) 1(c) 2(a) 2(b) 2(c) 3(a) 3(b) 4 Total

/4 /4 /4 /6 /6 /6 /6 /12 /18 /66

Information for Students in MATH 329 2005 01 35

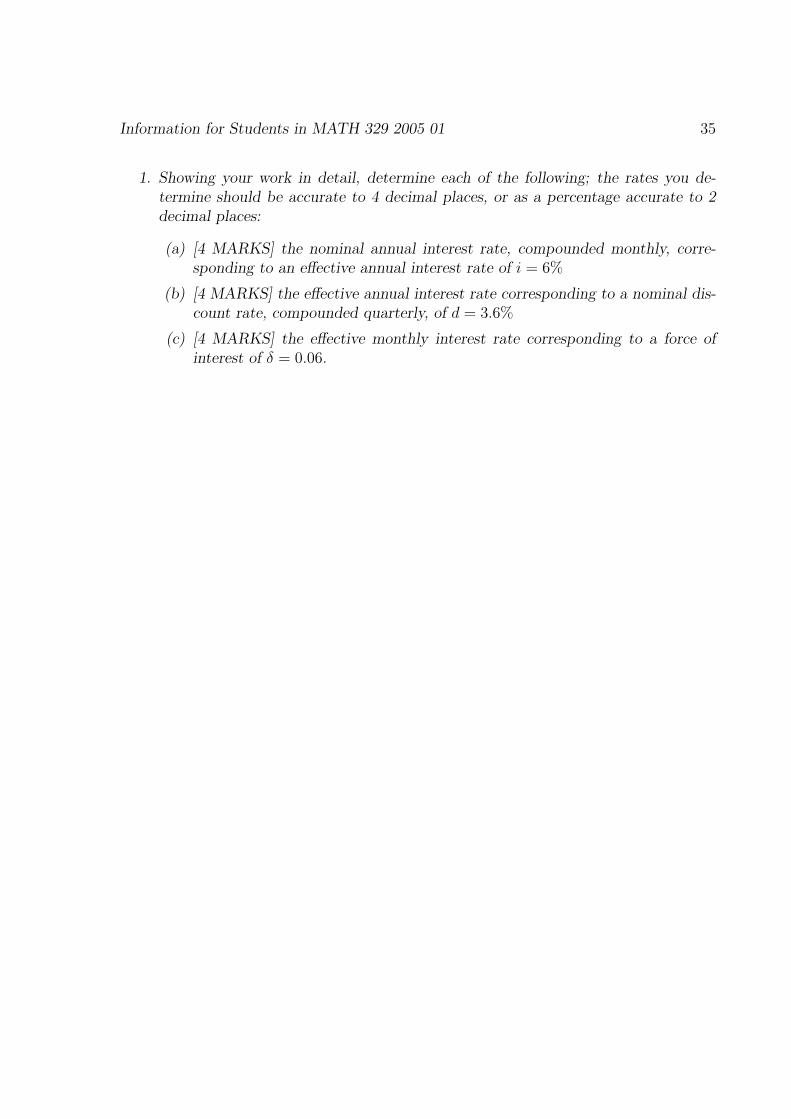

1. Showing your work in detail, determine each of the following; the rates you de-termine should be accurate to 4 decimal places, or as a percentage accurate to 2decimal places:

(a) [4 MARKS] the nominal annual interest rate, compounded monthly, corre-sponding to an effective annual interest rate of i = 6%

(b) [4 MARKS] the effective annual interest rate corresponding to a nominal dis-count rate, compounded quarterly, of d = 3.6%

(c) [4 MARKS] the effective monthly interest rate corresponding to a force ofinterest of δ = 0.06.

Information for Students in MATH 329 2005 01 36

2. For each of the following sequences of payments, determine, as of the given time,and for the given interest or discount rate, the value, showing all of your work.Before determining the numeric value you are expected to express the value usingstandard symbols.

(a) [6 MARKS] the value now of 20 payments of 1 at the end of every year startingone year from now, at an interest rate of 4%

(b) [6 MARKS] the value one year ago of 10 payments of 1 at the end of everyhalf-year, the first to be paid 5 years from now, at a nominal interest rate of8% compounded semi-annually

(c) [6 MARKS] 300 payments of 1 at the end of every month, as of the dateof the 100th payment, which has just been made; the interest rate is 12%compounded monthly

Information for Students in MATH 329 2005 01 37

3. (a) [6 MARKS] An annuity at interest rate i consists of payments of 10 now, 12at the end of one year, 14 at the end of two years, increasing by a constantamount until the last payment in the amount of 40, is to be evaluated as of 1year ago. Express its value in terms of symbols (Ia)n, (Is)n, an, sn, i, v, butdo not evaluate.

(b) [12 MARKS] The accumulated value just after the last payment under a 15-year annuity of 1000 per year, paying interest at the rate of 8% per annumeffective, is to be used to purchase a perpetuity, first payment to be made2 years after the last payment under the annuity. Showing all your work,determine the size of the payments under the perpetuity, assuming that theinterest rate from the time of the last payment under the 15-year annuity is5%.

Information for Students in MATH 329 2005 01 38

4. [18 MARKS] A loan of 6000 is to be repaid by annual payments of 350 to commenceat the end of the 1st year, and to continue thereafter for as long as necessary. Findthe time and amount of the final payment if the final payment is to be larger thanthe regular payments. Assume i = 4%.

Information for Students in MATH 329 2005 01 39

continuation page for problem number

You must refer to this continuation page on the page where the problem is printed!

Information for Students in MATH 329 2005 01 40

8.2 Class Test, Version 2

McGILL UNIVERSITY, FACULTY OF SCIENCECLASS TEST in MATH 329, THEORY OF INTEREST

EXAMINER: Professor W. G. Brown DATE: Wednesday, 9 March, 2004.ASSOCIATE EXAMINER: Professor N. Sancho TIME: 45 minutes, 14:35→15:20

FAMILY NAME:

GIVEN NAMES:

STUDENT NUMBER:

Instructions

• The time available for writing this test is about 45 minutes.

• This test booklet consists of this cover, Pages 41 through 44 containing questions togetherworth 66 marks; and Page 45, which is blank.

• Show all your work. All solutions are to be written in the space provided on the page wherethe question is printed. When that space is exhausted, you may write on the facing page, onthe blank page, or on the back cover of the booklet, but you must indicate any continuationclearly on the page where the question is printed! (Please inform the instructor if you findthat your booklet is defective.)

• All your writing — even rough work — must be handed in.

• Calculators. While you are permitted to use a calculator to perform arithmetic and/or ex-ponential calculations, you must not use the calculator to calculate such actuarial functionsas ani, sni, etc. without first stating a formula for the value of the function in terms ofexponentials and/or polynomials involving n and the interest rate. You must not use yourcalculator in any programmed calculations. If your calculator has memories, you are expectedto have cleared them before the test.

• In your solutions to problems on this test you are expected to show all your work. You areexpected to simplify algebraic and numerical answers as much as you can.

• Your neighbours may be writing a version of this test which is different from yours.

PLEASE DO NOT WRITE INSIDE THIS BOX

1 2(a) 2(b) 2(c) 3(a) 3(b) 3(c) 4(a) 4(b) Total

/18 /4 /4 /4 /6 /6 /6 /6 /12 /66

Information for Students in MATH 329 2005 01 41

1. [18 MARKS] A loan of 7000 is to be repaid by annual payments of 450 to commenceimmediately, and to continue at the beginning of each year for as long as necessary.Find the time and amount of the final payment if the final payment is to be nolarger than the regular payments. Assume i = 6%.

Information for Students in MATH 329 2005 01 42

2. Showing your work in detail, determine each of the following; the rates you de-termine should be accurate to 4 decimal places, or as a percentage accurate to 2decimal places:

(a) [4 MARKS] the effective annual discount rate corresponding to a nominalinterest rate, compounded quarterly, of i = 2.4%

(b) [4 MARKS] the nominal annual interest rate, compounded quarterly, equiva-lent to an effective semi-annual discount rate of d = 4%

(c) [4 MARKS] the effective semi-annual interest rate corresponding to a force ofinterest of δ = 0.04.

Information for Students in MATH 329 2005 01 43

3. For each of the following sequences of payments, determine, as of the given time,and for the given interest or discount rate, the value, showing all of your work.Before determining the numeric value you are expected to express the value usingstandard symbols.

(a) [6 MARKS] the value of 25 payments of 1 at the end of every year, the lastone having just been made, at an interest rate of 6%

(b) [6 MARKS] the value 4 months from now of 30 payments of 1 at the end ofevery 4 months, the first to be paid 2 years from now, at a nominal interestrate of 9% compounded 3 times a year

(c) [6 MARKS] 120 payments of 1 at the end of every 2 months, as of the dateof the 90th payment, which has just been made; the interest rate is 6% com-pounded every 2 months.

Information for Students in MATH 329 2005 01 44

4. (a) [6 MARKS] An annuity at interest rate i consists of payments of 100 now, 95at the end of 1 year, 90 at the end of 2 years, decreases by a constant amountuntil the last payment in the amount of 25, is to be evaluated as of the timeof the payment of 95. Express its value then in terms of symbols (Ia)n, (Is)n,an, sn, i, v, but do not evaluate.