inflation targeting in emerging market economies

TRANSCRIPT

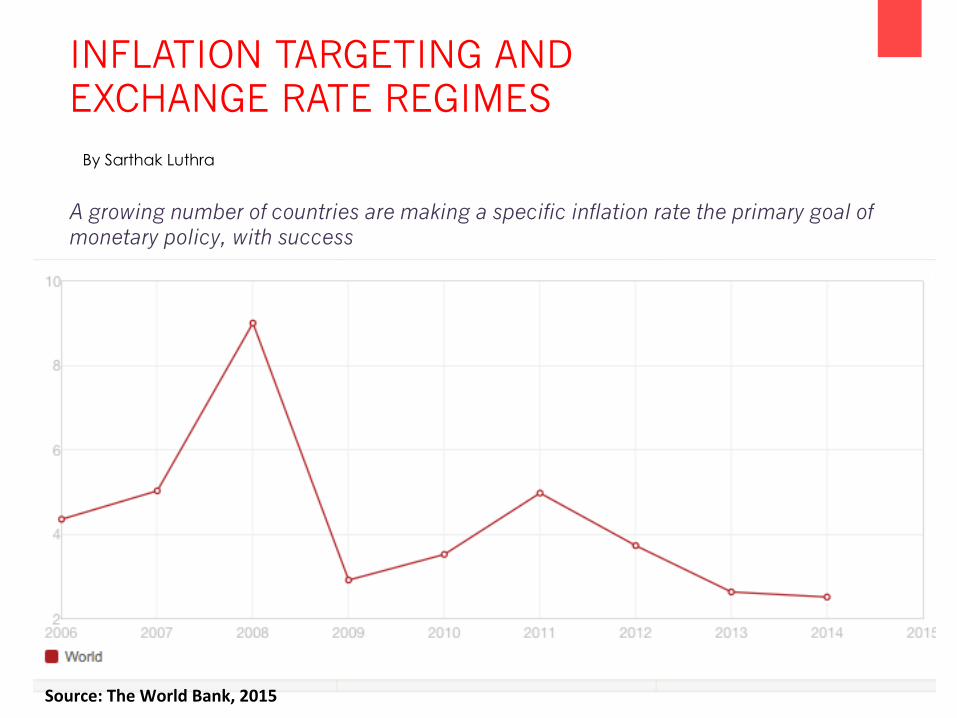

INFLATION TARGETING AND EXCHANGE RATE REGIMES

A growing number of countries are making a specific inflation rate the primary goal of monetary policy, with success

Source:TheWorldBank,2015

By Sarthak Luthra

Table of Contents

• WhatisInfla+onTarge+ng(IT)?• HistoryofIT• Infla+onandGrowth• IMFClassifica+on• NaturalClassifica+on• ExchangeRateArrangements• AsianPerspec+ve• Infla+on Targeters: Korea, Thailand, Philippines, andIndonesia

• DeJureversusDeFacto• Findings• KeyTakeaways

“A monetary policy opera0ng strategy with four elements; an ins&tu&onalizedcommitment to price stability as the primary goal of monetary policy,mechanisms rendering the central bank accountable for a8aining its monetarypolicy goals, the public announcement of targets for infla0on, and a policy ofcommunica&ngtothepublicandthemarketsthera&onaleforthedecisiontakenbythecentralbank”

Eichengreen,2001

“This involves the public announcement of medium-term numerical targets forinfla&on with an ins&tu&onal commitment by the monetary authority to achievethese targets. Addi0onal key features include increased communica&on with thepublic and themarkets about the plans and objec&ves ofmonetary policymakersandincreasedaccountabilityofthecentralbankforaDainingitsinfla0onobjec0ves.Monetarypolicydecisionsareguidedbythedevia0onofforecastsoffutureinfla0onfromtheannouncedtarget,withtheinfla0onforecastac0ng(implicitlyorexplicitly)astheintermediatetargetofmonetarypolicy”

IMF,2015

What is Inflation Targeting (IT)?

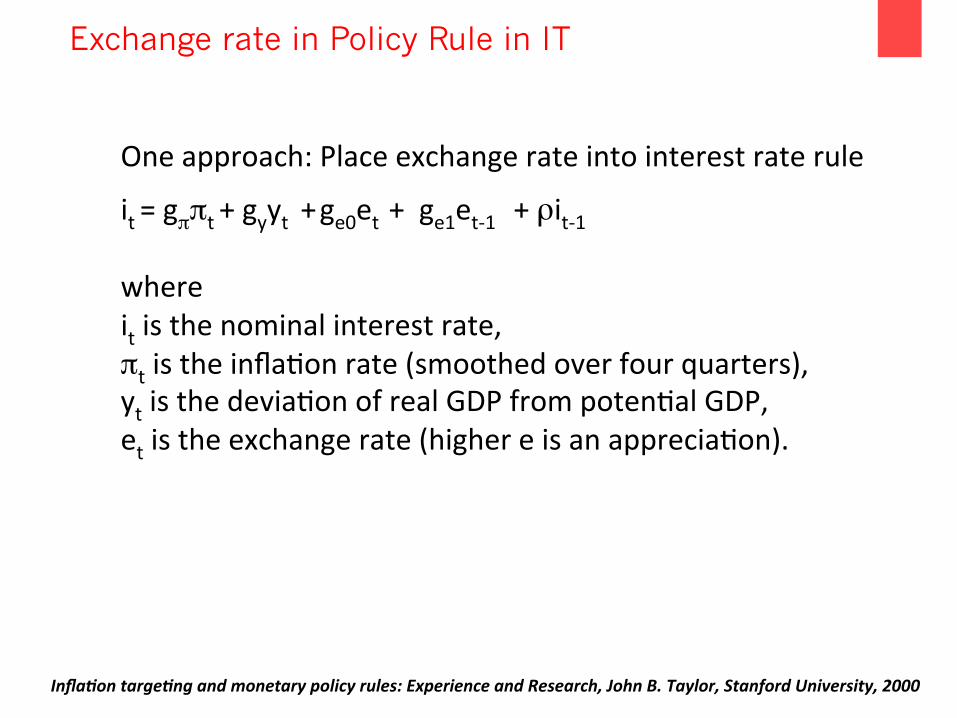

Oneapproach:Placeexchangerateintointerestraterule

it=gππt+gyyt+ge0et+ge1et-1+ρit-1 where

itisthenominalinterestrate,πtistheinfla+onrate(smoothedoverfourquarters),ytisthedevia+onofrealGDPfrompoten+alGDP,etistheexchangerate(highereisanapprecia+on).

Exchange rate in Policy Rule in IT

Infla&ontarge&ngandmonetarypolicyrules:ExperienceandResearch,JohnB.Taylor,StanfordUniversity,2000

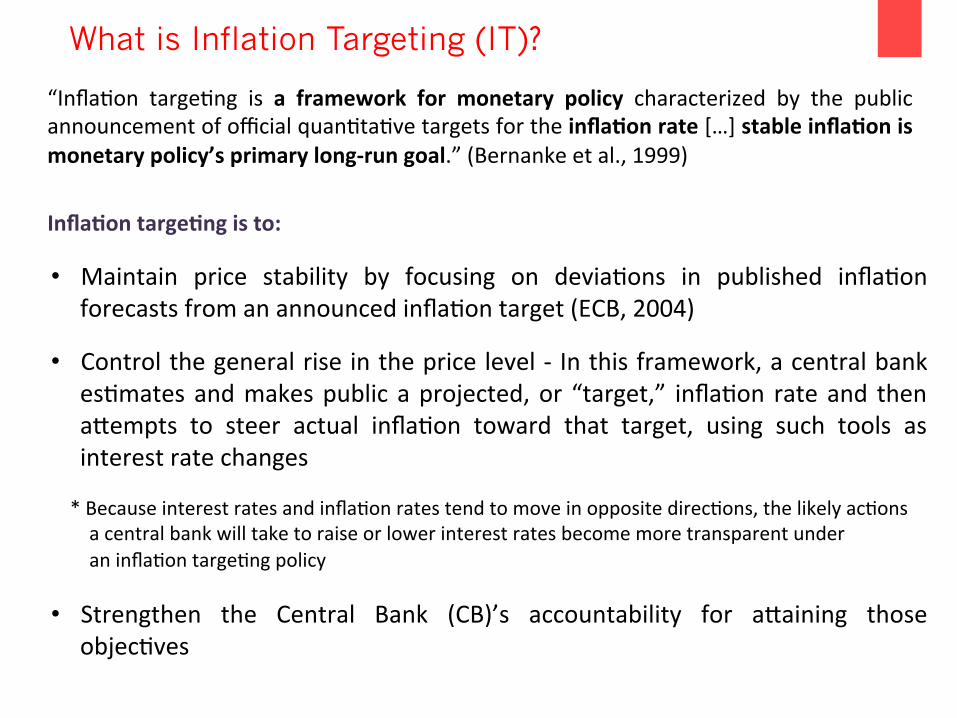

What is Inflation Targeting (IT)?

• Maintain price stability by focusing on devia+ons in published infla+onforecastsfromanannouncedinfla+ontarget(ECB,2004)

• Controlthegeneralriseinthepricelevel- Inthisframework,acentralbankes+matesandmakespublicaprojected,or “target,” infla+on rateand thena_empts to steer actual infla+on toward that target, using such tools asinterestratechanges

*Becauseinterestratesandinfla+onratestendtomoveinoppositedirec+ons,thelikelyac+onsacentralbankwilltaketoraiseorlowerinterestratesbecomemoretransparentunderaninfla+ontarge+ngpolicy

• Strengthen the Central Bank (CB)’s accountability for a_aining thoseobjec+ves

“Infla+on targe+ng is a framework for monetary policy characterized by the publicannouncementofofficialquan+ta+vetargetsfortheinfla@onrate[…]stableinfla@onismonetarypolicy’sprimarylong-rungoal.”(Bernankeetal.,1999)

Infla@ontarge@ngisto:

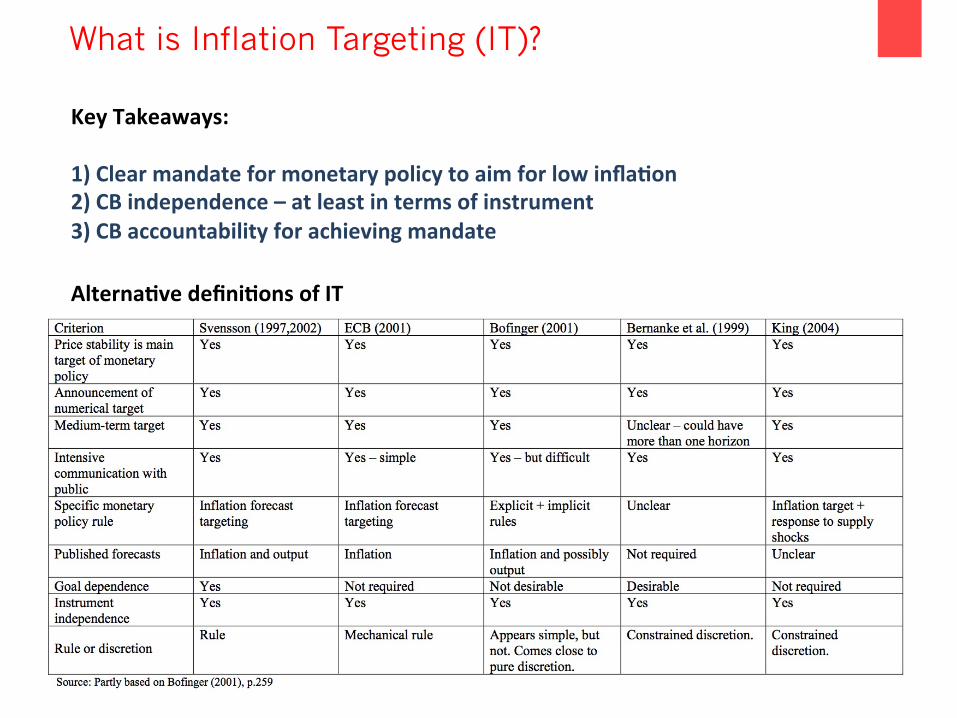

What is Inflation Targeting (IT)?

KeyTakeaways:1)Clearmandateformonetarypolicytoaimforlowinfla@on2)CBindependence–atleastintermsofinstrument3)CBaccountabilityforachievingmandate

Alterna@vedefini@onsofIT

Whyinfla@ontarge@ng:• Highinfla+ondistortsdecisionsoninvestment,

saving:mayleadtoslowereconomicgrowth;• Greaterins+tu+onalindependencetocentral

bankswithmonetarypolicycommitment;

• Preventdefla@onMonetarypolicyrestric0ve(expansionary)ifactualinfla0onissystema0callyabove(below)theinfla0ontarget.• Nominalanchortotheeconomy.Ex.Currencypeg

Concernwiththenominalanchor:Country’smonetarypolicyàDEPENDANTonthecountrytowhichitpeggedàLimi+ngthecentralbank’sabilitytorespondtoshocks(termsoftradeorchangesinrealinterestrateàManycountriesbegantoadoptflexibleexchangerates(NewAnchor)

History of IT – Why has it become popular?

Infla@ontarge@nghasbeenadoptedintheearly1990sbyindustrialcountrieslikeNewZealand,Canada,theUnitedKingdomandSweden,Mexico,andCzechrepublic

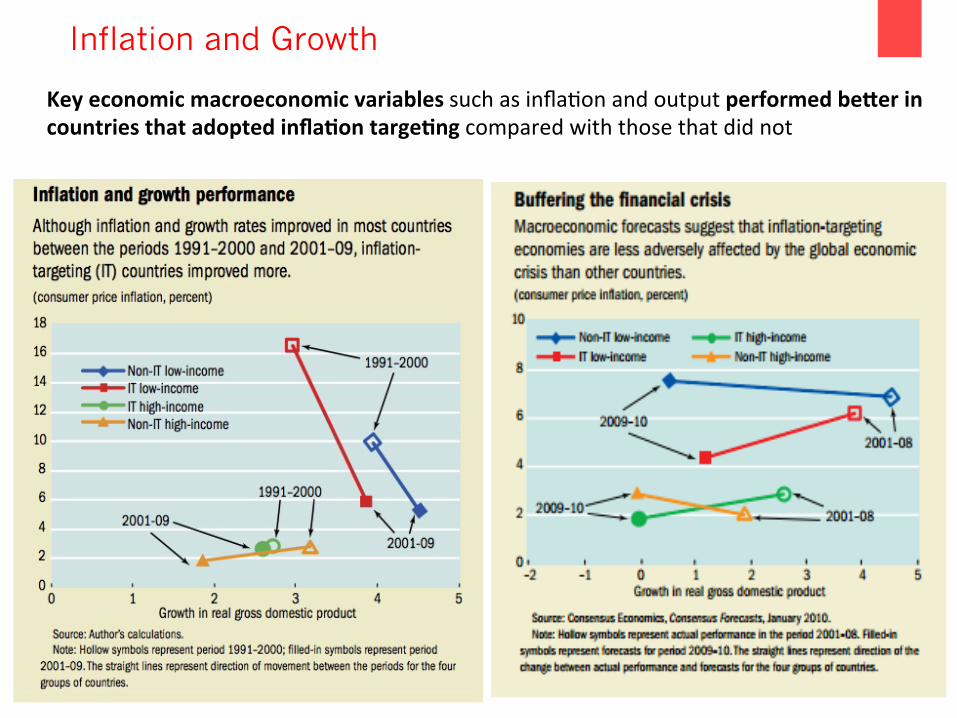

Inflation and Growth

Keyeconomicmacroeconomicvariablessuchasinfla+onandoutputperformedbeSerincountriesthatadoptedinfla@ontarge@ngcomparedwiththosethatdidnot

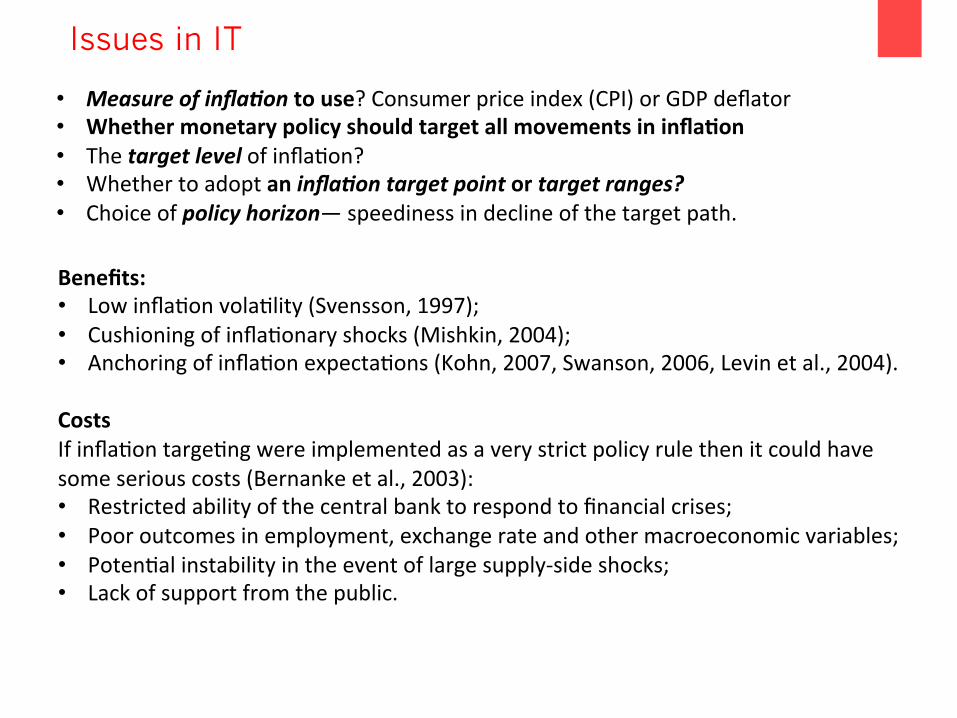

• Measureofinfla&ontouse?Consumerpriceindex(CPI)orGDPdeflator• Whethermonetarypolicyshouldtargetallmovementsininfla@on• Thetargetlevelofinfla+on?• Whethertoadoptaninfla&ontargetpointortargetranges?• Choiceofpolicyhorizon—speedinessindeclineofthetargetpath.

Issues in IT

Benefits:• Lowinfla+onvola+lity(Svensson,1997);• Cushioningofinfla+onaryshocks(Mishkin,2004);• Anchoringofinfla+onexpecta+ons(Kohn,2007,Swanson,2006,Levinetal.,2004).

CostsIfinfla+ontarge+ngwereimplementedasaverystrictpolicyrulethenitcouldhavesomeseriouscosts(Bernankeetal.,2003):• Restrictedabilityofthecentralbanktorespondtofinancialcrises;• Pooroutcomesinemployment,exchangerateandothermacroeconomicvariables;• Poten+alinstabilityintheeventoflargesupply-sideshocks;• Lackofsupportfromthepublic.

• Capital inflowsàcurrencyboardmonetaryauthoritybuysforexatfixedexchangerate,expandingmonetarybase.Theinterestrateare lowered and capital inflows arediscouraged.

• Case of automa+c adjustment mechanism.The interest rate à Capital inflows andouqlows are balanced. If capitalmobility ishigh, then the credible currency boardwillequate the domes+c interest ratewith theoneintheforeigncountrytowhichthepegismaintained(HongKong+USdollar).

• Underthecurrencyboard,thereisnoroomforindependentmonetarypolicy.

FixedExchangerateregime(undercurrencyboard)

FlexibleExchangerateregime

The exchange rate is ler to the marketforce , wh i le monetary po l i cy i sconcentrated on the domes+c pricestability. The central bank mandate is tokeep the domes+c price stability, andinterven+on into the foreign exchangemarketiskeptminimal,ifatall.*Three major economies—the US, theEuroland,andJapan—haveadoptedfreefloa@ng

Fixed and Floating Exchange Rate Regimes

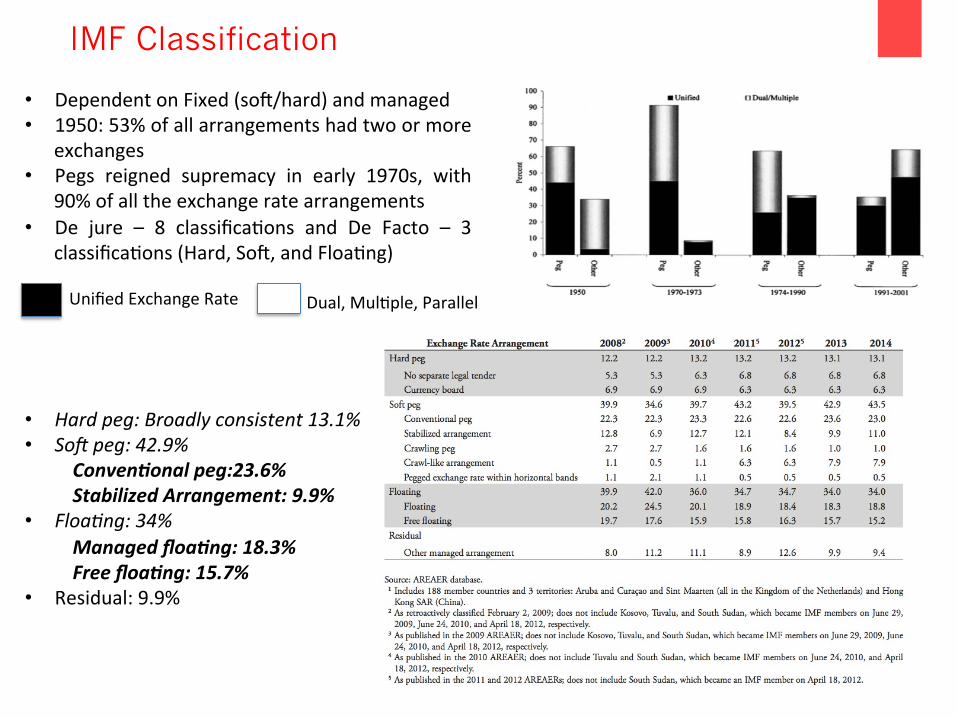

IMF Classification

• DependentonFixed(sor/hard)andmanaged• 1950:53%ofallarrangementshadtwoormore

exchanges• Pegs reigned supremacy in early 1970s, with

90%ofalltheexchangeratearrangements• De jure – 8 classifica+ons and De Facto – 3

classifica+ons(Hard,Sor,andFloa+ng)

UnifiedExchangeRate Dual,Mul+ple,Parallel

• Hardpeg:Broadlyconsistent13.1%• SoTpeg:42.9%

Conven&onalpeg:23.6%StabilizedArrangement:9.9%

• Floa0ng:34%Managedfloa&ng:18.3%Freefloa&ng:15.7%

• Residual:9.9%

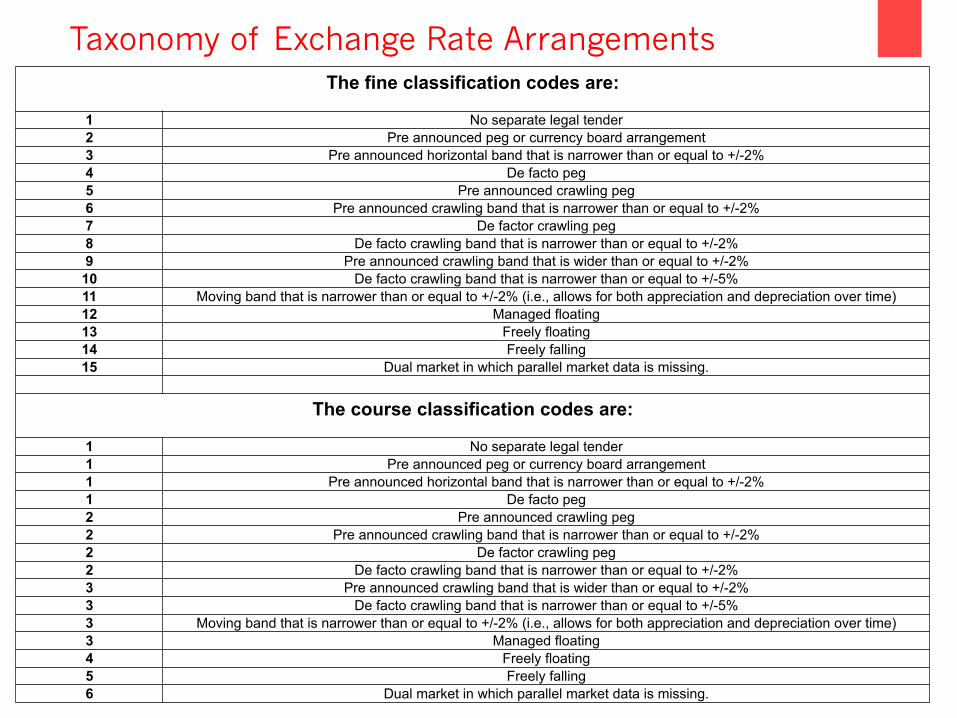

The fine classification codes are:

1 No separate legal tender 2 Pre announced peg or currency board arrangement 3 Pre announced horizontal band that is narrower than or equal to +/-2% 4 De facto peg 5 Pre announced crawling peg 6 Pre announced crawling band that is narrower than or equal to +/-2% 7 De factor crawling peg 8 De facto crawling band that is narrower than or equal to +/-2% 9 Pre announced crawling band that is wider than or equal to +/-2%

10 De facto crawling band that is narrower than or equal to +/-5% 11 Moving band that is narrower than or equal to +/-2% (i.e., allows for both appreciation and depreciation over time) 12 Managed floating 13 Freely floating 14 Freely falling 15 Dual market in which parallel market data is missing.

The course classification codes are:

1 No separate legal tender 1 Pre announced peg or currency board arrangement 1 Pre announced horizontal band that is narrower than or equal to +/-2% 1 De facto peg 2 Pre announced crawling peg 2 Pre announced crawling band that is narrower than or equal to +/-2% 2 De factor crawling peg 2 De facto crawling band that is narrower than or equal to +/-2% 3 Pre announced crawling band that is wider than or equal to +/-2% 3 De facto crawling band that is narrower than or equal to +/-5% 3 Moving band that is narrower than or equal to +/-2% (i.e., allows for both appreciation and depreciation over time) 3 Managed floating 4 Freely floating 5 Freely falling 6 Dual market in which parallel market data is missing.

Taxonomy of Exchange Rate Arrangements

Natural Classification- Carmen Reinhart Database

• BasedonMarketDeterminedrates• Be_erbarometersofunderlyingmonetarypolicy• Marketdeterminedexchangeratesconsistentlyan+cipatesdevalua+onofofficial

rate(posi+vecoefficient)• Be_er correla+on of market exchange rate with infla@on (be_er pulse of

monetarypolicy)• Presence of Dual (mul+ple) rates and parallel markets – in 1950 45% of the

countrieshaddualormul@pleexchangerates• InOfficialClassifica+onasmanagedfloa+ng–53%haddefactopegs,crawls,or

narrowbandsinnaturalclassifica@on• PopularregimesinEmergingAsiaandWesternHemisphere–Crawlingpeg(more

than36%and42%oftheobserva+ons),1990-2001• NewCategory–Freelyfalling(13%oftheobserva+onwithfreelyfallingcategory

in1990),whichis3+mesfreelyfloa+ngcategory(Whereinthe12monthinfla+onrateisabove40%)ExChilein1956

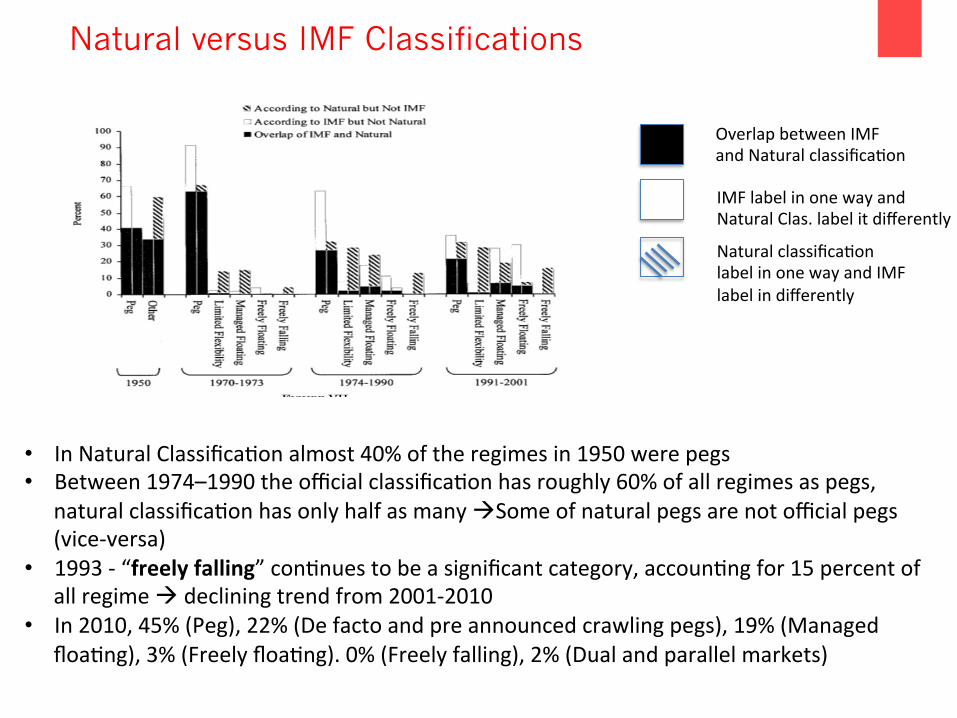

Natural versus IMF Classifications

• InNaturalClassifica+onalmost40%oftheregimesin1950werepegs• Between1974–1990theofficialclassifica+onhasroughly60%ofallregimesaspegs,

naturalclassifica+onhasonlyhalfasmanyàSomeofnaturalpegsarenotofficialpegs(vice-versa)

• 1993-“freelyfalling”con+nuestobeasignificantcategory,accoun+ngfor15percentofallregimeàdecliningtrendfrom2001-2010

• In2010,45%(Peg),22%(Defactoandpreannouncedcrawlingpegs),19%(Managedfloa+ng),3%(Freelyfloa+ng).0%(Freelyfalling),2%(Dualandparallelmarkets)

OverlapbetweenIMFandNaturalclassifica+on

IMFlabelinonewayandNaturalClas.labelitdifferently

Naturalclassifica+onlabelinonewayandIMFlabelindifferently

Natural versus IMF Classifications

• Naturalclassifica+onelevateslimitedflexibilityasanimportantregime(unlikeofficialarrangement)

• Naturalclassifica+on(lessthan10%between1991-2001)haslessfreelyfloa+ngregimesvis-à-visofficialclassifica+on(morethan30%)àFearofFloa+ng(CalvoandReinhart,2002)

IMF Classification Probability in Natural Classification Natural Classification

Peg 44% Flexible arrangment

Float 31% Peg / limited flexibility

Managed float 53% Peg / limited flexibility

• Correla+onbetweenNaturalandOfficialClassifica+on:0.42• GreateroverlapforEuropeancountries• Leastoverlapindevelopingcountries

Transi@on-%ofcountrieswithdifferentexchangerateregimes(1941–2010)

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

1940

1942

1944

1946

1948

1950

1952

1954

1956

1958

1960

1962

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

ONE

TWO

THREE

FOUR

FIVE

SIX

WORLDWIDE EXCHANGE RATE REGIMES

IMFDataonExchangeRateArrangements,CourseClassifica&on,1940-2010

• Recentdevelopment-Depolici@seexchangeratemovementssincesoapegsaresuscep@bletospecula@veaSacksàIncreasedpressurefordevelopingcountriestoadoptcornersolu+onstoexchangeratesarrangements;

• Theexchangerateisanimportantvariableforpolicydecisions;• Priorto1990,Asianeconomiesmaintainedfixedexchangerateàexchangerate

stabilityisessen+alforpromo+ngtradeandinvestment;• Fixedexchangerateregimebecamedifficulttomaintainwhenthecapitalaccounts

wereliberalized;• Someemergingmarketeconomies,includingMexicoandThailand,firstreceived

largecapitalinflowsfollowedbylargeouqlows;• Whenthecentralbank,facedwithmassiveouqlows,triedtomaintainthefixed

exchangerateandexhaustedtheforeignexchangeàCURRENCYCRISIS• Fearofapprecia+on–duetoasymmetricexchangerateinterven+on—i.e.,a

willingnesstoallowdeprecia+onsbutreluctancetoallowapprecia+ons Impossibilityofhavingcapitalmobility,thefixedexchangerate,andindependentmonetarypolicy,isoaencalled“impossibletrinity

Asian Economies – A Perspective

• Asiancrisis,the“two-cornersolu+on”wasadvocatedbytheIMFandtheUnitedStates.Itsaysthatthestableexchangerateregimeiseitherthehardpeg(currencyboardordollariza+on)orfreefloat.

• Intermediateregimesàmanagedfloat/fixedexchangerateregimewithoutacurrencyboardarrangement,wereregardedasinherentlyunstable.Fischer(2001)

• Since1998,theIMFhasrecommendedtoemergingmarketeconomiesinaddi+ontoadvancedcountriesacombina+onoffreefloatandinfla@ontarge@nginordertolessentheprobabilityofacurrencycrisiswithstabilityofdomes+cprices.

• Thefreefloatregime,seemedtohavegainedmorepopularity,andsohasinfla+ontarge+ng.InEastAsia,Korea,Thailand,thePhilippines,andIndonesiaadoptedinfla+ontarge+ngsince1998

• ManyEMcountriesadoptedafully-fledgedITregimeormanyelementsofitinthelate1990sasatransi+onarrangement,mostlyinresponsetodifficul+esinkeepingpeggedcurrenciesstableinthewakeoftheEastAsiancrisis.During2003–2011,themovefromfixedexchangeratearrangementstoinfla+ontarge+ngormixedpolicyregimescon+nuedamongEMcountries

Post Asian Crisis

Exchange Rate Regimes

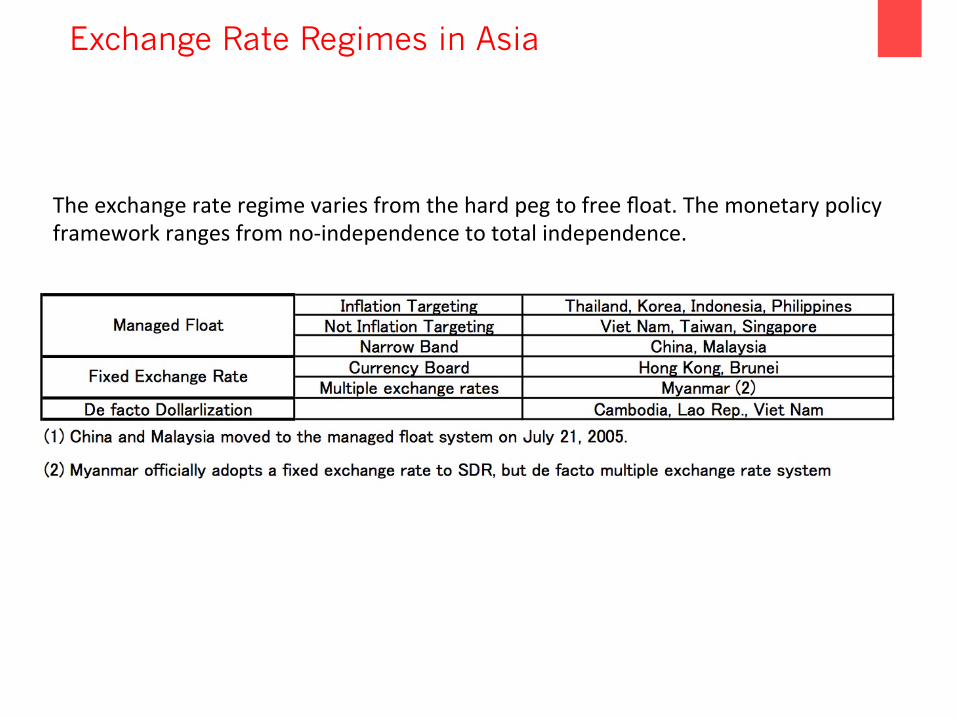

Theexchangerateregimevariesfromthehardpegtofreefloat.Themonetarypolicyframeworkrangesfromno-independencetototalindependence.

Exchange Rate Regimes in Asia

InEastAsia,Korea,Thailand,thePhilippines,andIndonesiaadoptedinfla@ontarge@ngsince1998

Inflation Targeting Economies – East Asia

0

200

400

600

800

1000

1200

0

2000

4000

6000

8000

10000

12000

14000

1961

1964

1967

1970

1973

1976

1979

1982

1985

1988

1991

1994

1997

2000

2003

2006

2009

2012

Indonesia

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

40.00

45.00

50.00

-5.00

0.00

5.00

10.00

15.00

20.00

25.00

30.00

1961

1964

1967

1970

1973

1976

1979

1982

1985

1988

1991

1994

1997

2000

2003

2006

2009

2012

Thailand

0.00

10.00

20.00

30.00

40.00

50.00

60.00

0.00

10.00

20.00

30.00

40.00

50.00

60.00

1961

1964

1967

1970

1973

1976

1979

1982

1985

1988

1991

1994

1997

2000

2003

2006

2009

2012

Philippines Korea

0.00

200.00

400.00

600.00

800.00

1000.00

1200.00

1400.00

1600.00

0

5

10

15

20

25

30

35

1961

1964

1967

1970

1973

1976

1979

1982

1985

1988

1991

1994

1997

2000

2003

2006

2009

2012

Inflation and Exchange Rate Movements

Infla@on(BlueandLeaAxis)Exchangerate(RedandRightAxis)

0

1

2

3

4

5

6

1940

1943

1946

1949

1952

1955

1958

1961

1964

1967

1970

1973

1976

1979

1982

1985

1988

1991

1994

1997

2000

2003

2006

2009

INDONESIA

0

1

2

3

4

5

6

1940

1943

1946

1949

1952

1955

1958

1961

1964

1967

1970

1973

1976

1979

1982

1985

1988

1991

1994

1997

2000

2003

KOREA

0

1

2

3

4

5

6

1940

1943

1946

1949

1952

1955

1958

1961

1964

1967

1970

1973

1976

1979

1982

1985

1988

1991

1994

1997

2000

2003

2006

2009

PHILIPPINES

0

1

2

3

4

5

6

7

1940

1943

1946

1949

1952

1955

1958

1961

1964

1967

1970

1973

1976

1979

1982

1985

1988

1991

1994

1997

2000

2003

2006

2009

THAILAND

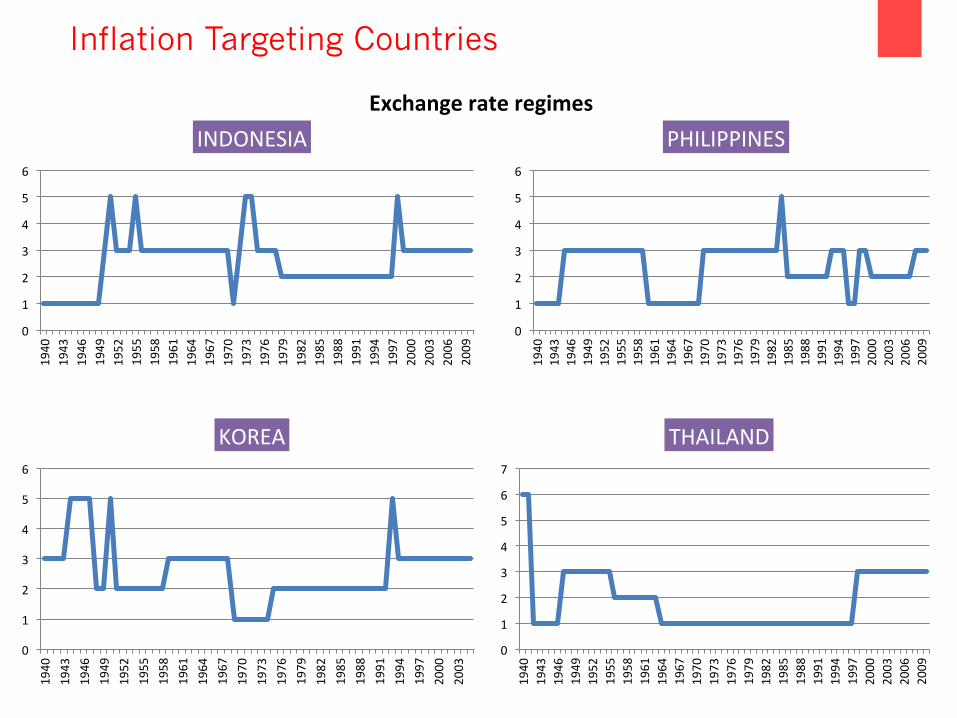

Inflation Targeting Countries

Exchangerateregimes

Un+l1998àeasytoobtaindejureexchangerateclassifica+onsàdatawascompiledfromna+onalsourcesbytheIMFàbasedonself-repor+ngofna+onalpoliciesbyvariousgovernmentsConcern:Divergencesbetweendefactoanddejurepolicies—IMF’sexchangerateclassifica+onmethodologyshiredtocompilingunofficialpoliciesofcountriesasdeterminedbytheFund.• IMFreplaceditscompila+onofdejureexchangerateregimeswiththebehavioral

classifica+onofexchangerates.• NewIMFcodingisbasedonvarioussources,includinginforma+onfromIMFstaff,

pressreports,otherrelevantpapers,aswellasthebehaviorofbilateralnominalexchangeratesandreserves.

De Jure versus De Facto Classification

Country De Jure Exchange Rate Regimes in Asia'

Bangladesh The exchange rates set by the dealer banks themselves, based on Demand and-supply interaction. Bangladesh Bank is not present in the market on a day-to-day basis and undertakes purchase/sale transactions with dealer banks (if need be)

PRC 2005 - managed floating exchange rate regime based on market supply and demand (link to basket of currencies). The new exchange rate system has operated stably The exchange rate of the RMB against US dollar has been moving both upward and downward with greater flexibility

Hong Kong, SAR

1983 - Hong Kong dollar linked to US dollar Maintained under strict and robust Currency Board system (requiring) both the stock and the flow of the Monetary Base to be fully backed by foreign reserves

India Monitoring and management of exchange rates with flexibility, without a fixed target or a pre-announced target or a band

Indonesia

2005- Bank Indonesia launched new monetary policy known as the Inflation targeting framework: (1) use of the BI rate as a reference rate in monetary control in replacement of the base money operational target (2) forward looking monetary policymaking process (3) more transparent communications strategy (4) strengthening of policy coordination with the Government The rupiah exchange rate is determined wholly by market supply and demand

Korea

Inflation targeting - Central bank announces an explicit inflation target and achieves its target directly. Inflation targeting places great emphasis on inducing inflation expectations to converge on the central bank’s inflation target level by the prior public announcement and successful attainment of that target level The exchange rate is, in principle, decided by the interplay of supply and demand in the foreign exchange markets

Malaysia 2005 - Shifted from a fixed exchange rate regime to a managed float against a basket of currencies Exchange rate determined demand and supply in the foreign exchange market. Economic fundamentals and market conditions are the primary determinants of the level of the ringgit exchange rate

Pakistana Floating inter-bank exchange rate since 2001 Monetary-cum-exchange rate policies are judgment- and discretion-based rather than model- or rule-based

Philippines 2002 - Inflation targeting framework for monetary policy in January 2002 The Monetary Board determines the exchange rate policy of the country, determines the spot rates

Singapore

1981 - monetary policy has been centered on the management of the exchange rate. (1) Managed against a basket of currencies of its major trading partners and competitors. (2) Monetary Authority of Singapore operates a managed float regime withtrade-weighted exchange rate (3) Use of exchange rate as the intermediate target --> MAS gives up control over domestic interest rates (and money supply).

Sri Lanka Independently floating exchange rate regime within a framework of targeting monetary aggregates Reserve money (i.e., high powered money) as the operating target broad money (M2b) as the intermediate target.

Thailand 1997 - Managed-float exchange rate regime Value of baht is determined by market forces (both on-shore and off-shore foreign exchange market Bank of Thailand implements monetary policy by influencing short-term money market rates

Viet Nam Crawling peg with the US dollar for its exchange rate Set official exchange rate daily and dealing rate within a trading band of plus or minus 0.25%percent. Currencey if depreciated against US dollar by keeping the exchange rate on an upward trend.

De Jure Exchange Rate Classification- Asia

Theevolu&onandimpactofAsianExchangerateregimes,RamkishenS.Rajanno.208,July2010

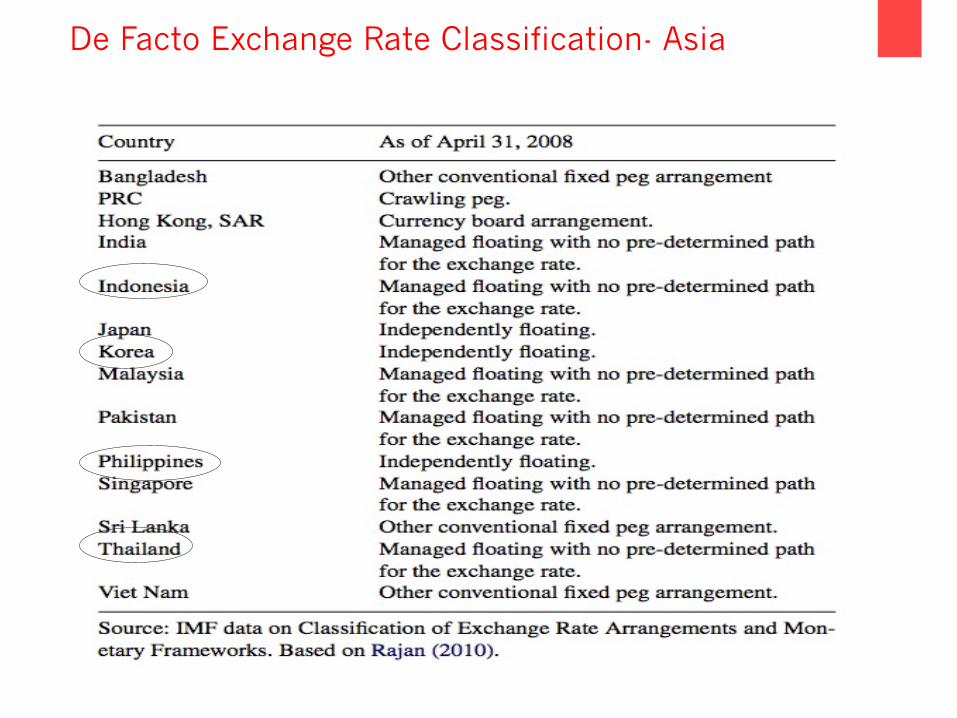

De Facto Exchange Rate Classification- Asia

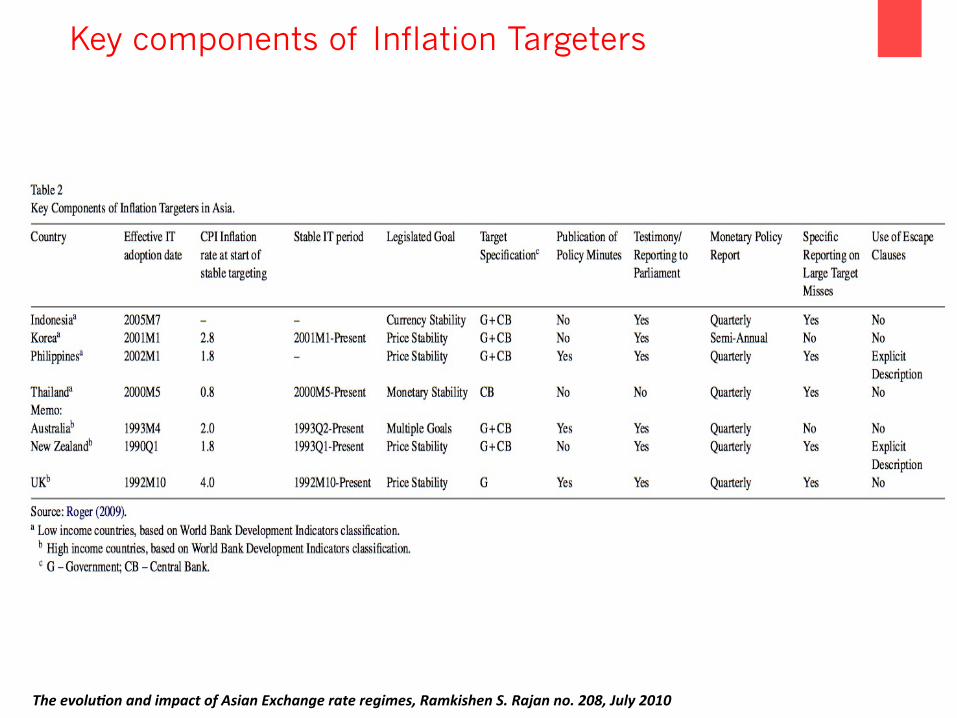

Key components of Inflation Targeters

Theevolu&onandimpactofAsianExchangerateregimes,RamkishenS.Rajanno.208,July2010

• ThereisnodiscrepancybetweenthedejureanddefactoregimesofHongKong,China,whichoperatesanexchangeratefixedtotheUSdollar

• India,Malaysia,Pakistan,Singapore,andThailandarecategorizedasmanagedfloaters,broadlyconsistentwiththeirofficialpronouncements

• KoreaandthePhilippinesarecharacterizedasindependentfloaters,consistentwiththeirofficialasser+onsbutsomewhatoddinviewofthefactthatbothcountrieshavebeenrapidlybuildingupreserves.

• VietNamisclassifiedashavingaconven+onalfixedpegregimecomparedtoitsofficialpronouncementofmaintainingacrawlingpegandbandaroundtheUSdollar.

• Bangladesh,Indonesia,andSriLankahavealsobeencharacterizedasmanagedfloaters(withnopredeterminedexchangeratepath),despitetheirofficialdeclara+onsofbeingindependentfloaters

Findings

• Centralbanksshouldprac@cebothinfla@ontarge@ngandsubstan@alinterven@on

• Thecorrela@onbetweentheinfla@onrateandtheexchangeratemovementisreviewedforAsianinfla@ontarge@ngcountries

• Monetarypolicyac@onsinordertokeeptheinfla@onratestablecaninternalizetheimpactontheexchangeratefromtheinfla@onshock

• Anexchangerateshockmaybecounteredbymonetarypolicythatwillkeepboththeexchangerateandtheinfla@onratestable

Key Takeaways

• ExchangeratearrangementsforEastAsiapost-crisis:examiningthecaseforopeneconomyinfla+ontarge+ng,TonyCavoliandRamkishenRajan,April2003

• IMFpolicypaper,condi+onalityinevolvingmonetarypolicyregimes,March2014• Theroleofexchangerateininfla+ontarge+ng,TakatoshiIto,UniversityofTokyo,post-conferenceversionfinal,

May2007• Thecountrychronologiesandbackgroundmaterialtoexchangeratearrangementsintothe21stcentury:Will

theanchorcurrencyhold?Ethanilzetzki,LondonSchoolofEconomics,CarmenM.Reinhart,UniversityofMarylandandNBER,KennethS.Rogoff,HarvarduniversityandNBER,March2011

• Annualreportonexchangearrangementsandexchangerestric+ons,IMF,2014• Infla+ontarge+ngturns20,ScoDRoger,March2010• Theevolu+onandimpactofAsianExchangerateregimes,RamkishenS.Rajanno.208,July2010• Characterizingexchangerateregimesinpost-crisiseastasia,TaimurBaig,IMF,AsiaandPacificdepartment,

October2001• Dejureversusdefactoexchangerateregimesinsub-saharanafrica,SlaviSlavov,imf,August2011• Exchangeratearrangementsenteringthe21stcentury:whichanchorwillhold?,EthanIlzetzki,CarmenM.

ReinhartandKennethS.Rogoff• Themodernhistoryofexchangeratearrangements:areinterpreta+on*,Carmenm.ReinhartandKennethS.

Rogoff,quarterlyjournalofeconomics,February2004• Macroeconomicpolicy,thedefini+onofinfla+ontarge+ng,JenniferSmith-UniversityofWarwick

Bibliography