industry overview - · pdf fileindustry overview: market evolution ... research & advisory...

TRANSCRIPT

Citi Investment Mgt. CAB | Armonk NY | March 11, 2010

Industry Overview:

Market Evolution – Where are We and What Will Happen Next?

Presented by

Larry Tabb

Founder & CEO

TABB Group

Agenda

Who is TABB Group?

The macro picture

The market

Professional management

Commissions & services

Regulation

House rules

SEC market structure review

Disjoint regulatory initiatives

Market Structure

Electronic trading

High frequency trading

Impact on market structure

Conclusions

Who is TABB Group?

Research & advisory firm focused on Financial Markets value chain Fiduciary, manager, broker, exchange, custodian, depository & their ecosystem

Over 100 pieces of financial markets research a year

25 employees located in New York, Boston, London & Chicago

Built on The Value of First Person Knowledge

We interview nearly 1,000 industry professionals a year

Major studies include US, European & Asian Institutional Equity Trading

Hedge Funds Analysis

Options & OTC Derivatives Analysis

US and European Market Structure

High Frequency Trading

OMS & EMS Platform Trends

Latest initiative TabbFORUM Where Capital Markets Speak

Free Industry Blog

Markets around the globe were challenged over the past 1 3/4 years – but coming back

Korea

FTSEHK

DAX

India0%

CAC

CA

S&P China

Japan

Over past 11mths we are in huge bull market – global mkts up a min of 45+%

0%

Korea

CACFTSE

HK

DAX

India

Japan

China

S&P

CA

However, all is not great in professional money management land

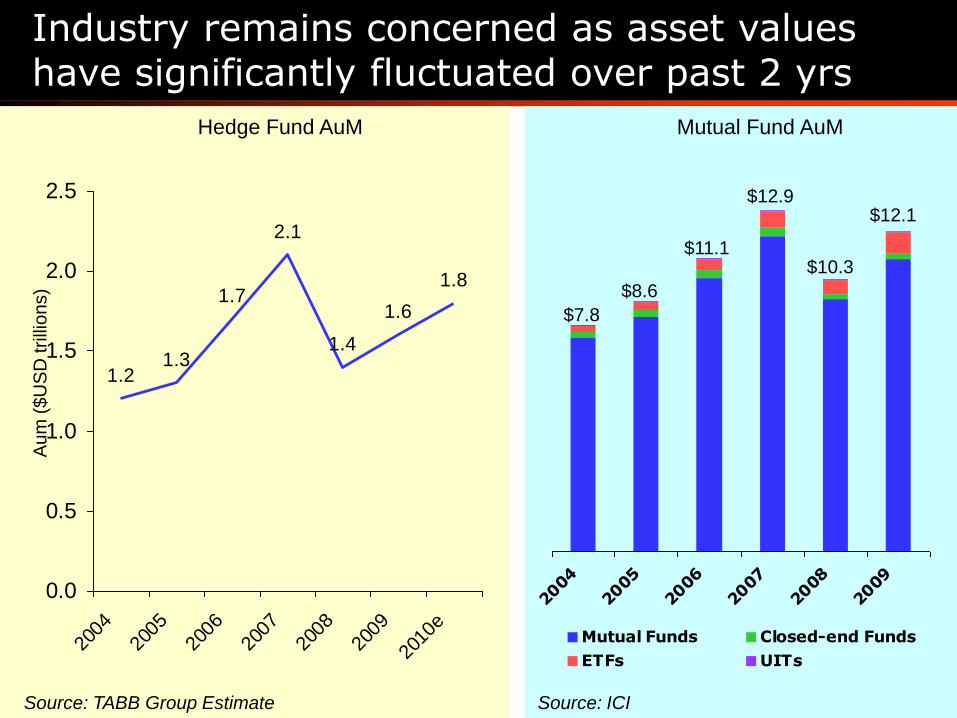

1.21.3

1.7

2.1

1.4

1.6

1.8

0.0

0.5

1.0

1.5

2.0

2.5

2004

2005

2006

2007

2008

2009

2010

e

Hedge Fund AuM

Industry remains concerned as asset values have significantly fluctuated over past 2 yrs

Au

m (

$U

SD

trilli

on

s)

2004

2005

2006

2007

2008

2009

Mutual Funds Closed-end Funds

ETFs UITs

$11.1

$12.9

$10.3

$12.1

$8.6

$7.8

Mutual Fund AuM

Source: TABB Group Estimate Source: ICI

54%

33%

27%

16%

13%

10%

8%

5%

Raising

Assets

Performance

Market

Volatility

Infrastructure

Regulatory

Liquidity

People

Broker

Relationships

Greatest Challenges Facing Your Firm?

Funds greatest concerns are raising assets while investors are worried about risk

41%

25%

20%

18%

7%

5%

2%

2%

2%

30%

Operational

Safety of

Strategy

Liquidity Risk

Market

Performance

Holdings

Managed

Accounts

Fund Size

Regulatory

Changes

Leverage

Pricing

Greatest Customer Concerns?

Source: TABB Group US Institutional Brokerage 2010

37%

26%

26%

19%

19%

16%

9%

Relative Performance

Absolute Performance

Return of Retail Investor

Confidence

Stock Selection

New & Alternative

Products

Return of Asset

Allocation

Acquisitions /

International Equities

What drives the growth of your firm in 2010?

Buy-side firms are fighting to recover from loss of equity assets, devastated performance records

Source: TABB Group US Institutional Brokerage 2010

23%

19%

11%

32%Liquidity,

Flow

Color,

Information,

Insight

Best

Execution

Research

39%

38%

36%

69%Research

Liquidity,

Flow

Algorithms

Sales

Trader

The number one business driver for brokers has flipped from liquidity to alpha-generating content

Commission Allocation Business Drivers

2009

Commission Allocation Business Drivers

2008

Source: TABB Group US Institutional Brokerage 2010

10%

40%

50%

12%

24%

64%

7%

29%

64%

Increased

Flat

Decreased

Quantitative Both Fundamental

Has Your Commission Wallet Increased or Decreased 2009 vs. 2008?

By Investment Style

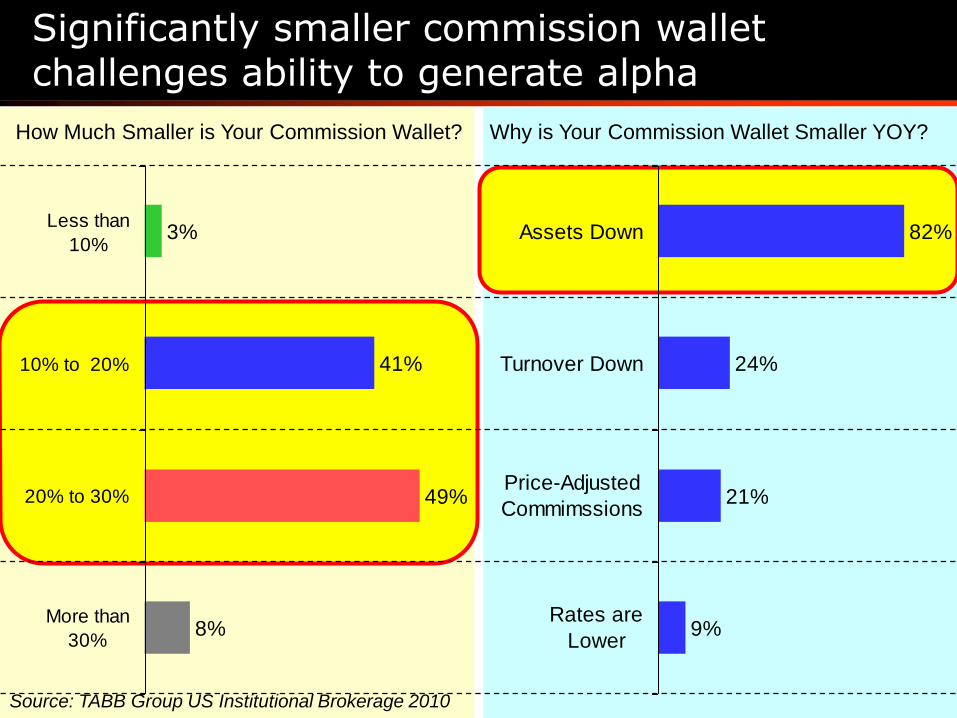

Assets & turnover are down, & ability to pay sell side for services is damaged at majority of firms

Source: TABB Group US Institutional Brokerage 2010

82%

24%

21%

9%

Assets Down

Turnover Down

Price-Adjusted

Commimssions

Rates are

Lower

3%

41%

49%

8%

Less than

10%

10% to 20%

20% to 30%

More than

30%

Why is Your Commission Wallet Smaller YOY? How Much Smaller is Your Commission Wallet?

How Much Smaller is Your Commission Wallet? Why is Your Commission Wallet Smaller YOY?

Significantly smaller commission wallet challenges ability to generate alpha

Source: TABB Group US Institutional Brokerage 2010

Average Commission Rates, 2006 – 2009

2.53

1.971.89

1.74

2006 2007 2008 2009

3 Year CAGR

-12% YOY ’08-’09

-8%

Brokers willing to cut rates – but they want consolidated flow

Source: TABB Group US Institutional Brokerage 2010

Increasingly CSAs are driving execution

48%

47%

28%

67%

65%

43%

80%

86%

50%

Large

Medium

Small

2007 2008 2009

29%

35%

34%

2 Year CAGR 2007 - 2009Percentage of Firms Using CSAs by Size

Source: TABB Group US Institutional Brokerage 2010

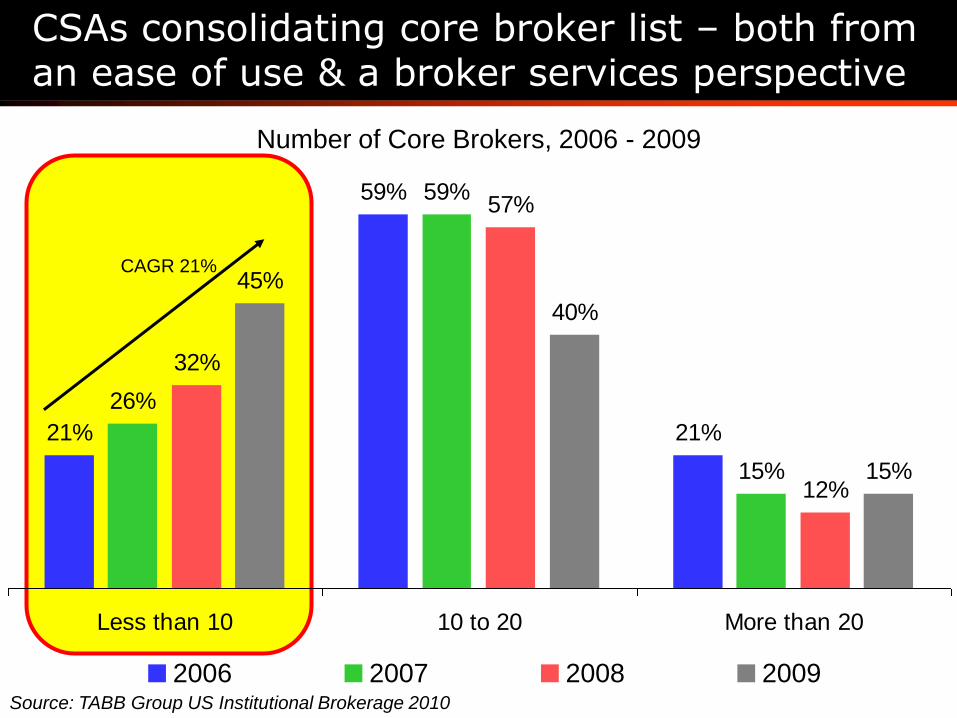

21%

59%

21%

26%

59%

15%

32%

57%

12%

45%

40%

15%

Less than 10 10 to 20 More than 20

2006 2007 2008 2009

CSAs consolidating core broker list – both from an ease of use & a broker services perspective

Number of Core Brokers, 2006 - 2009

CAGR 21%

Source: TABB Group US Institutional Brokerage 2010

13.4

11.4

12

12.3

13.6

10.6

13.7

12.8

18.6

13.3

14.8

15.5

Large

Medium

Small

Total

2009 2008 2007

-7%

-10%

-11%

-15%

Number of Core Brokers by Firm Size and Total 2 Year CAGR

…and average # of core brokers has declined to under 12.5 – declining 11% over last 2 years

Source: TABB Group US Institutional Brokerage 2010

While market is up, for the fund industry the business is still challenging

Business is difficult Investors are still scared – pulled out at wrong time

Assets are till mostly down

Alternatives are growing (ETFs)

Traditional distribution channels are being challenged (wirehouse branding)

Greater allocation to fixed income

Will assets come back? Boomers are starting to reach retirement age or are close

But where will boomers put assets?

Funds have cut costs to right-size

Opportunity is back But ability to capture opportunity is hampered

Commissions are down, but service demand is up Brokers want their more than fair share

And institutions have little alternative but to comply

CSAs are helping aggregate flow But hurting regionals, boutiques, and agency only brokers

And Regulation is around the corner

Regulation

House passes - Wall Street Reform and Consumer Protection Act of 2009

Creation of Consumer Financial Protection Agency (CFPA)

Financial Stability Council

Dissolution Authority and Ending “Too Big to Fail”

Executive Compensation

Investor Protections

Regulation of Derivatives

Mortgage Reform and Anti-Predatory Lending

Reform of Credit Rating Agencies

Hedge Fund, Private Equity & Private Pools of Capital Registration

Office of Insurance

Bill components

Consumer Financial Protection Agency (CFPA) Organization to vet financial products for consumers

Financial Stability Council Identify and regulate financial firms that are so large, interconnected, or risky

that their collapse would put the entire financial system at risk.

Dissolution Authority and Ending “Too Big to Fail” Gives government ability to take over and “resolve” large financial institutions

Executive Compensation A “say on pay,” oversight on executive comp & golden parachutes, enables

regulators to ban inappropriate or imprudently risky compensation practices,

& it requires disclosure of bonus plans

Investor Protections Strengthens SEC‟s powers so that it can better protect investors and regulate

the nation‟s securities markets

Bill components 2

Regulation of Derivatives Regulates OTC derivatives - standardized swaps have to be cleared &

traded on an exchange or electronic platform House amendment limits bank stakes in clearing houses to 20 percent

Mortgage Reform and Anti-Predatory Lending Mortgage reform and anti-predatory lending

Reform of Credit Rating Agencies Steps to reduce conflicts of interest, reduce market reliance on credit rating

agencies, & impose a liability standards on CRAs

Hedge Fund, Private Equity & Private Pools of Capital Registration Requires almost all private capital pool advisers to register with the SEC &

be subject to systemic risk regulation by the Financial Stability regulator

Unintended consequences

Will not be passed in tact Tremendous opposition and Senate has a different view

Much will be worked out in conference

Largest unintended consequences come from Derivatives bill Central clearing is not a panacea

How do you clear products that can‟t be valued? What happens to liquid products that become illiquid after a time?

Do we really want to incentivize the trading of OTC swaps?

Do we want to expand or contract these products

Who will provide liquidity? Traditional dealers will not provide liquidity with incentives

If we bring in more liquidity providers Will they have enough capital?

Who will guarantee them?

Depositories backed by banks limit counterparties to credit-worthy participants

Will banks join depositories with an unsound credit process?

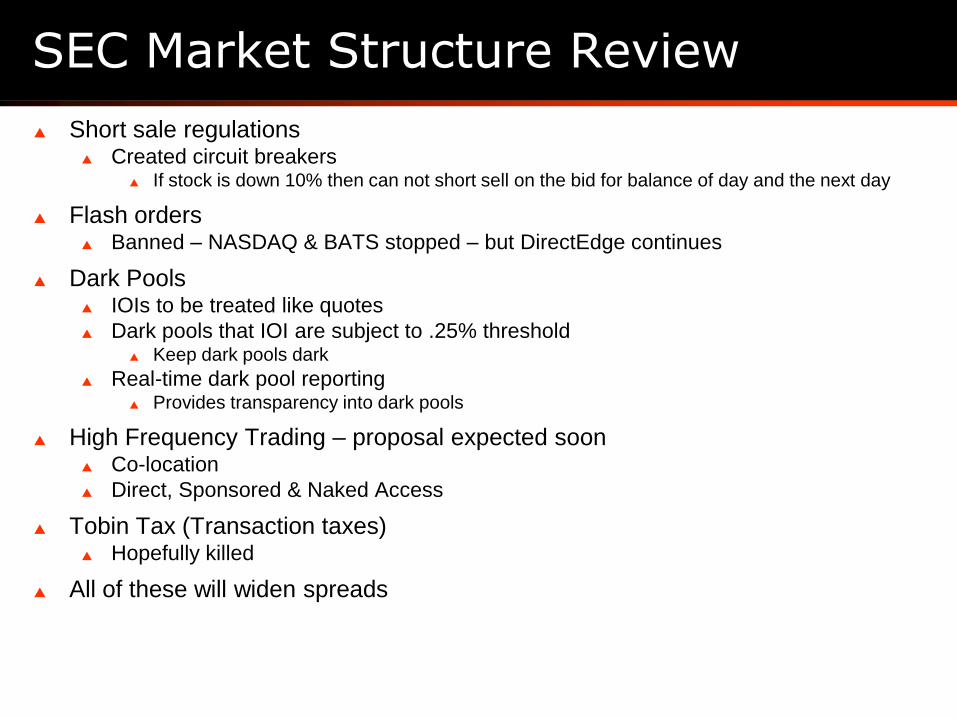

SEC Market Structure Review

Short sale regulations Created circuit breakers

If stock is down 10% then can not short sell on the bid for balance of day and the next day

Flash orders Banned – NASDAQ & BATS stopped – but DirectEdge continues

Dark Pools IOIs to be treated like quotes

Dark pools that IOI are subject to .25% threshold Keep dark pools dark

Real-time dark pool reporting Provides transparency into dark pools

High Frequency Trading – proposal expected soon Co-location

Direct, Sponsored & Naked Access

Tobin Tax (Transaction taxes) Hopefully killed

All of these will widen spreads

Other disjoint regulatory initiatives

The Volcker rule Eliminate banks proprietary trading desks - likelihood low

Bonus fever European bonus tax – done

US Windfall banking profits tax – likely

Transaction Tax Would be very detrimental to financial markets – hopefully not

Capital restrictions Increasing capital reserves for larger banks –likely

Speculator / CDS restrictions Restrictions on speculation most notably on “naked CDS” from the Greek debt crisis –

unclear

Lynch Amendment / Langen Initiative Restricting banks ownership in clearing houses to 20% collectively

Warner Langen of European Parliament initiative to ban bank ownership in European CCPs

European Private Equity restrictions Barring EU investments in non-EU private equity funds - unclear

Electronic Trading

Direct Feeds Black Boxes Algorithms DMAInternalization

& Crossing

Pre & Real

Time TCA

Electronic trading value chain has many components

Source: TABB Group

Market

Data

Analyzing data

from different

venues

Direct Feeds

Trade

Generation

What to buy

and sell - when

Black Boxes

HFT

Execution

Strategy

How to buy

and sell - where

Algorithms

Direct

Access /

Aggregation

Getting to the

right venue

DMA

Matching

Matching buyers &

sellers

Internalization

& Crossing

Transaction

Cost

Analysis

Did you made the

right decision?

Pre & Real

Time TCA

Market

Data

Trade

Generation

Execution

Strategy

Direct

Access /

AggregationMatching

Transaction

Cost

Analysis

Shares by Execution Venue (volume weighted)

1%

-5%

-22%

18%

-10%

37%

12%

14%

22%

15%

44%

11%

9%

24%

11%

38%

11%

9%

31%

12%

Sales Desk

Program

Desk

Direct To

Exchange

Algorithms

Crossing

Network

2007 2008 2009

2 Year CAGR

‟07-‟09

More than 50% of buy-side flow is direct & 40% is channeled through DMA or Algos

Source: TABB Group – Institutional Equity Trading in America ’09/’10

4.8%

9.1%

29.2%

Percentage of Share Volume Sent to Broker Algorithms

4 YR CAGR ‟05 – „09

+27%

90%

16.1%

Flow to algorithms continues to grow –significantly

5%

11%

21%22%

24%

31%

36%

2004 2005 2006 2007 2008 2009 2010E

Source: TABB Group – Institutional Equity Trading in America ’09/’10

US Equity Share Volume by Market Participant

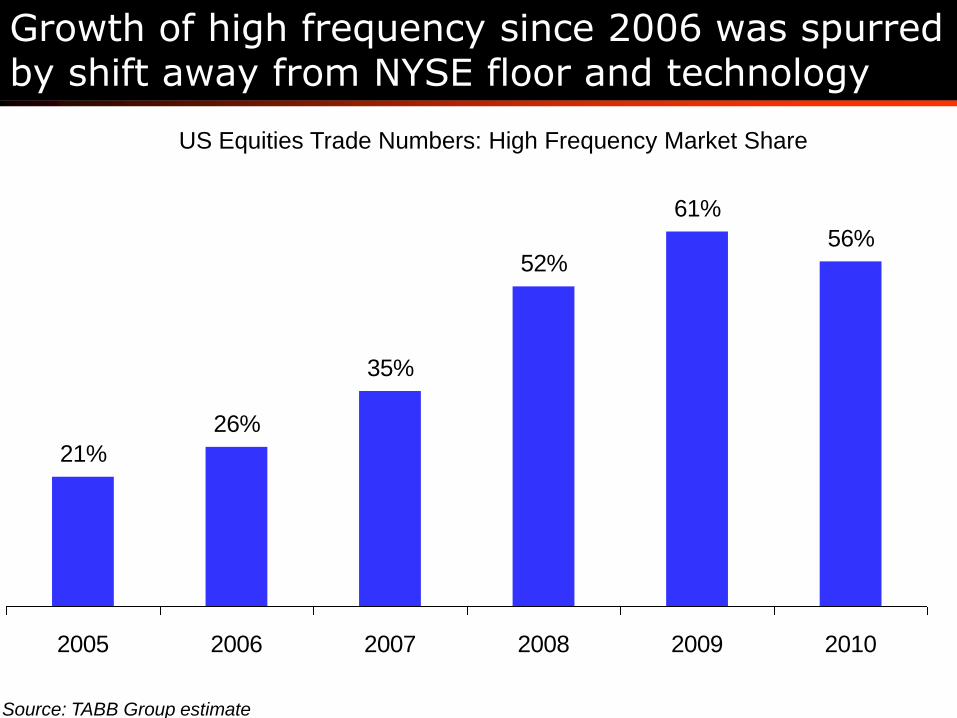

High Frequency Trading accounts for 61% of Share Volume

Source: TABB Group Estimate

3% 6.8% 13.0% 16.2%

3.9% 28.0% 29.4%

Investors

Liquidity Providers

Retail

Hedge Funds

Investment Bank Prop

Long Only

HFT Hedge Funds

HFT Broker/ Market Makers

Independent HFT

Investors Liquidity Providers

The majority of trading is done by professional traders / liquidity providers

56%

61%

52%

35%

26%

21%

201020092008200720062005

US Equities Trade Numbers: High Frequency Market Share

Growth of high frequency since 2006 was spurred by shift away from NYSE floor and technology

Source: TABB Group estimate

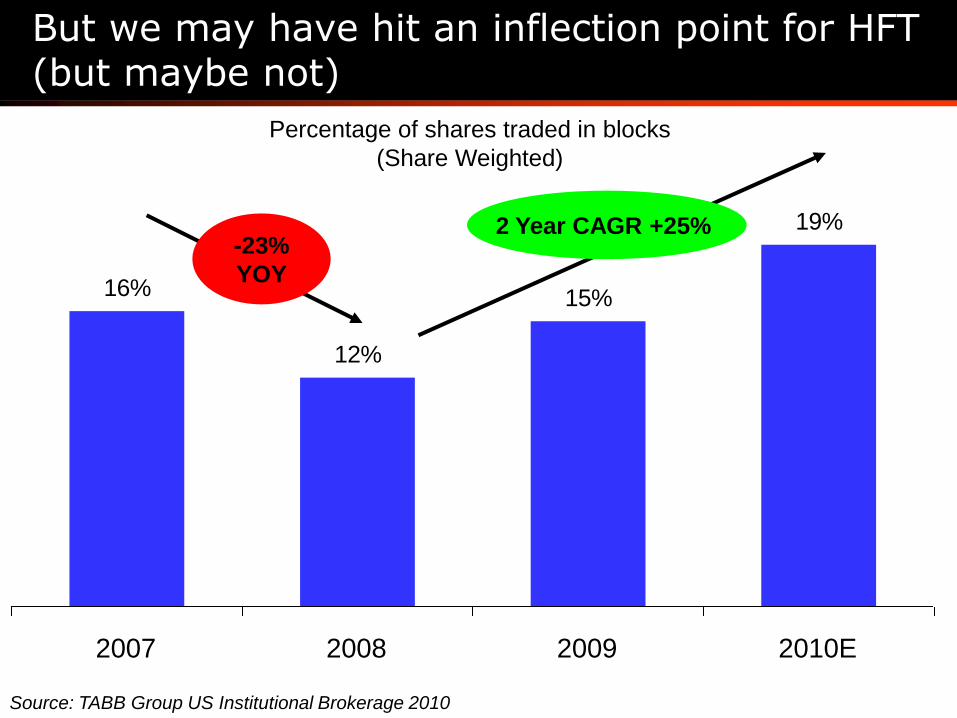

But we may have hit an inflection point for HFT (but maybe not)

19%

15%

12%

16%

2010E200920082007

2 Year CAGR +25%

Percentage of shares traded in blocks

(Share Weighted)

-23%

YOY

Source: TABB Group US Institutional Brokerage 2010

When it comes down to it – trading is now the battle of the trading bots Battlebots

Broker technologies protect the investor while fulfilling investors timeframe

Liquidity provider technologies determine supply and demand by bridging liquidity gaps The more liquidity providers, the greater the competition the more efficient the market

Liquidity provision is a zero sum game. Only one buyer and one seller match.

The three major constituents are well armed with technology Retail order flow usually goes to wholesales who compete heavily for this business

These providers fall under best execution guidelines

Institutional investors employ buy-side traders who focus on execution Buy-side traders are armed with algos, dark pools, and other liquidity finding technologies

Also fall under best execution guidelines

Firms average more than 20 brokers and switch on/off depending upon execution quality

Employ transaction cost analytics to measure execution cost This is a significant discussion point with their clients & investment consultants

Liquidity providers employ technology to find opportunities Co-location, high speed order routing and analysis engines, high speed market data, risk

management, and trading technology

The goal of investor-based order flow management is to balance investor protection vs. immediate execution

In last 3 years, exchanges have lost 32% market share to dark pools, ECNs, & regionals

89%

87%88

%

86%85

%85

%

82%83

%

73%76

%77

%76

%77

%

73%74

%

72%72

%71

%70

%

67%69

%69

%69

%

67%66

%66

%

62%

59%58

%57

%

53%53

%55%57

%58

%57

%

4% 5%3%

5% 6% 7% 8% 9%

15%14

%14

%14

%13

%14

%13

%15%15

%16

%18%19

%19

%19

%18

%21%22

%22

%24%25

%27%27

%30%29

%

26%25

%

22%22

%

5% 6% 6% 6% 6% 6% 7% 6%8% 8% 7% 8% 7% 8% 8% 9% 9% 9% 8%

10%

8% 7%9% 9%

11%10

%10

%10

%10

%10

%11

%11

%11

%10

%12%13

%

0%

20%

40%

60%

80%

100%

Jan-0

7

Mar

-07

May

-07

Jul-0

7

Sep

-07

Nov

-07

Jan-0

8

Mar

-08

May

-08

Jul-0

8

Sep

-08

Nov

-08

Jan-0

9

Mar

-09

May

-09

Jul-0

9

Sep

-09

Nov

-09

NYSE,

NASDAQ, &

Arca

BATS /

DirectEdge

Crossing /

Dark Pools

Regional

Exchanges

Source: TABB Group LiquidityMatrixTM

Matched US Equity Flow as a Percentage of Total US Equity Matched Flow

Market share of liquidity pools are beginning to converge

US Equity Market Share (includes Internalized)

Consolidated NYSE/NASDAQ Listed Equities

Jul 2008 – Jan 2010

4% 4% 4% 4%3% 3% 3% 3%

3%

5% 5% 5% 5%6%

7%8% 8%

7%

30%29% 29%

30% 30%

27% 27%

26%

23%

21%20% 20% 20%

19%19%

21% 21%20% 20%

16%

14% 14%15%

16%15% 15% 15%

14% 14% 14% 13% 13%

14% 14% 14% 14%

18.10%18.00%

19.90%20.10%19.90%

18.00%17.90%18.30%17.20%

16.40%16.00%15.10%14.60%14.00%

13.00%13.00%13.10%13.20%13.20%

10% 10% 11%11%

10%11%

11% 11%10%

10% 11% 11%10%

9% 9% 9% 9%10%

5%6% 5% 5%

6%6% 7% 7%

9%10%

10% 10%

12%13%

12%10% 10% 10%

8%7%

9%

7% 7%

9% 8%9% 9% 9% 9% 9% 8%

10% 9% 9% 10% 9% 9% 9%10%9% 9%

8%9%

11% 11%12%

14%

16%17%

17%

15%

16% 16%15% 15%

16%

18%

8%

14%15%

10%

-5.00%

5.00%

15.00%

25.00%

35.00%

Jul-08

Aug-0

8

Sep-0

8

Oct

-08

Nov-

08

Dec

-08

Jan-0

9

Feb-0

9

Mar-

09

Apr-

09

May-

09

Jun-0

9

Jul-09

Aug-0

9

Sep-0

9

Oct

-09

Nov-

09

Dec

-09

Jan-1

0

Regionals Nasdaq NYSE Arca BATS DirectEdge Dark Pools Internalized

Source: TABB Group LiquidityMatrixTM, Exchanges

Why is trading done by machines?

Liquidity has fragmented More than 50 places to electronically trade equities

No way to check each venue by hand

Order size had declined significantly Message traffic has increased significantly

Buy-side wants to execute this way Hide larger orders

Doesn‟t want to pay higher commissions

Brokers don‟t want staff

Measuring tools have allowed buy-side to better measure trading cost

Algorithms have improved to take complexity away from execution

Reg NMS preferences fast liquidity pools over slow

Conclusions

While market is up – money management has challenges Capital raising is more challenging

Investment strategies are more global Expanded operations – expanded complexity

Distribution channels compromised FoF & wirehouses brands tarnished

Rise of the independents

Shifting demographics

Declining commission dollars reduces buying power Research becoming more critical as managers cutting back expenses

Brokers will cut commissions but want more flow

Agency brokers have a more difficult time competing

Regulation will pass – it will be extensive – but not sure what will pass Will not be as extensive as the House version but will be significant

New trading technologies changes complexion of the market Market makers on the decline – high frequency traders on the increase

Need to be more careful with trading strategies / gaming

Changing the dynamics of the exchange fabric This is a globally phenomena

Citi Investment Mgt. CAB | Armonk NY | March 11, 2010

Industry Overview:

Market Evolution – Where are We and What Will Happen Next?

Presented by

Larry Tabb

Founder & CEO

TABB Group