industry outlook presentation to annual asa/afra … · industry outlook presentation to annual...

TRANSCRIPT

Industry Outlook Presentation to annual ASA/AFRA Conference

Adam Pilarski,

Senior Vice President, AVITAS, Inc.

July 10th, 2017

Reston, VA

2 topics to be covered

World developments

The forthcoming burst of a bubble

Page 2

World Developments

Using economics to understand them

Implication on our life

Page 3

Page 4

To help us understand reality we can use 4

economic concepts

Trade offs

Game Theory

Principal/Agent dilemma

Analytical thinking

Page 5

Analytical Thinking

Page 6

“For every simple problem there is an answer that is murky, complex and

wrong.”

Paul Krugman

“For every complex problem there is an answer that is clear, simple and

wrong.”

H. L. Mencken (1880-1965)

Trade-offs Page 7

Brexit

Trade off

Benefit – economies of scale, lower costs (€)

Cost – bureaucrats far away tell you what to do

Page 8

Principal Agent Problem

Can we find better implementers?

Page 9

Movement from central authority

Business people?

Military?

Page 10

Page 11

“Trump is CEO of the country”

Nikki Haley

May 14th, 2017

Page 12

Judging by results (concentrate on efficiency)

Plethora of billionaires in cabinet

Use/acceptance of business principles to guide our life

Education – Charter Schools

Can military run better government (plethora of

generals in cabinet)

Page 13

Make America Great Again not the

same as America World Leader

Page 14

If not the U.S…………

Page 15

The New World Leader?

Page 16

Implications for business

Page 17

U.S. Share of World Traffic

67.6%

42.2%

31.8%

25.1% 21.4%

0%

10%

20%

30%

40%

50%

60%

70%

80%

1940 1950 1960 1970 1980 1990 2000 2010 2020

Page 18

Page 19

Page 20

2035 (Airbus/Boeing Forecasts)

World share of traffic

Asia (38-40%)

China 16.1% (B)

World share of GDP

Asia 40%

China 18.1% (B)

Page 21

Future role of dollar?

Demise has been predicted many times

Adam’s theory of tallest midget

Possible huge implication for our industry

Pricing of aircraft

Financing

Oil prices

Page 22

Possible bubble

Page 23

Concept of bubble

Irrational by definition

Both up and down

Impossible to predict

Burst usually caused by “wild developments”

Wars, policy mistakes……..

Page 24

0

1000

2000

3000

4000

5000

6000

7000

1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

Annual World Passenger Air Traffic 1970-2016E

Historical World Passenger Traffic

Preliminary Model Results

Billions of RPKs

Sources: ICAO historical data and AVITAS forecast.

Note: Model results are preliminary and may be subject to change.

9/11 and 2008 Financial

Crisis Ln RPK = -12.88 + 1.95*Ln GDP - ...

Page 25

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

16%

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%

6%

7%

8%

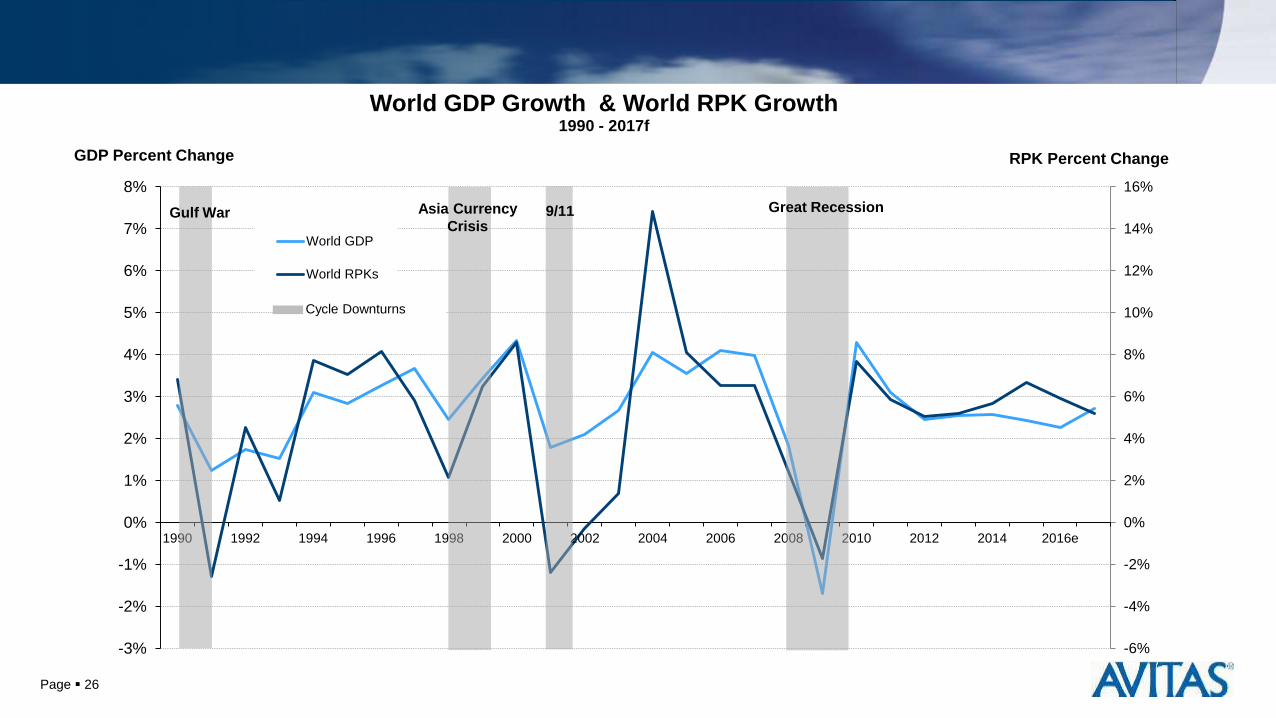

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016e

RPK Percent Change GDP Percent Change

World GDP Growth & World RPK Growth 1990 - 2017f

World GDP

World RPKs

Gulf War Great Recession 9/11 Asia Currency

Crisis

Cycle Downturns

Page 26

-

500

1,000

1,500

2,000

2,500

3,000

3,500

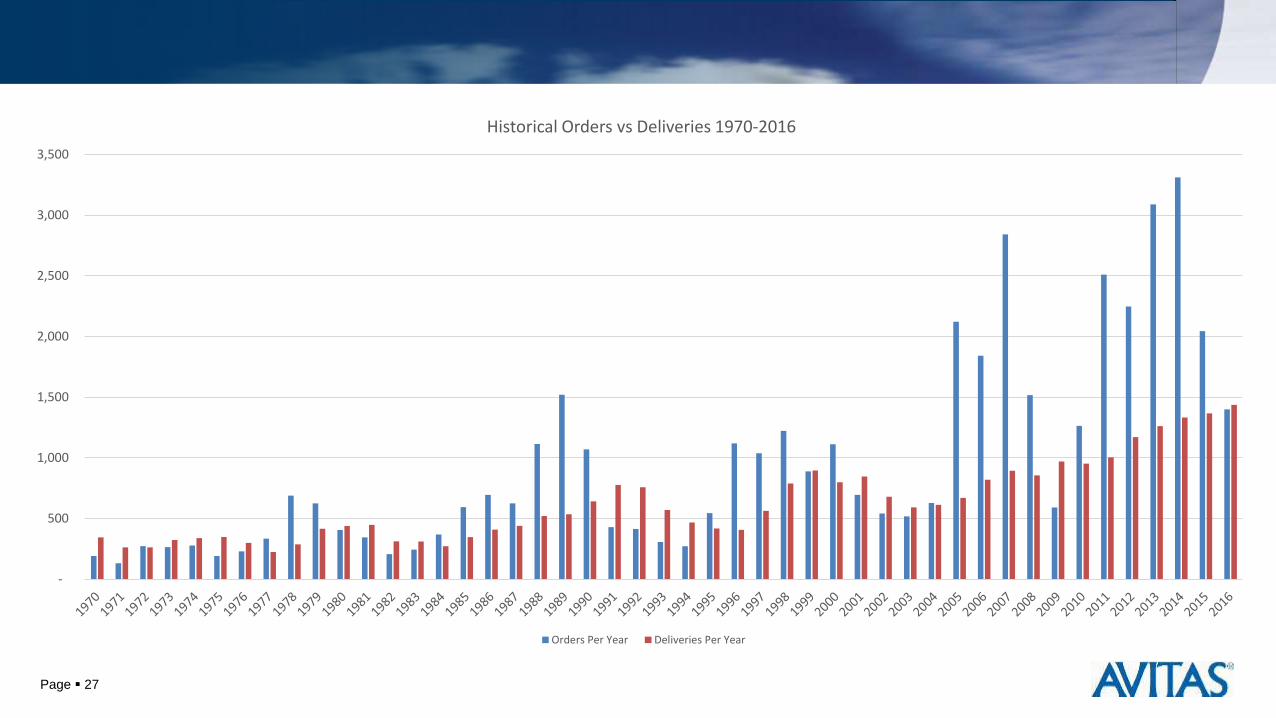

Historical Orders vs Deliveries 1970-2016

Orders Per Year Deliveries Per Year

Page 27

-

200

400

600

800

1,000

1,200

1,400

1,600

1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994

Historical Orders vs Deliveries 1984-1994

Orders Per Year Deliveries Per Year

Page 28

-

500

1,000

1,500

2,000

2,500

3,000

3,500

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Historical Orders vs Deliveries 2004-2016

Orders Per Year Deliveries Per Year

Page 29

Why large orders

Double counting

Low interest rates

High oil prices

Proliferation of new narrow body models

Page 30

This time possible bubble pricks can be

identified

Stage One : Middle East

Stage Two : Leasing companies, especially in China

Page 31

Summary

“May you live in interesting times” is becoming reality

Heightened uncertainties may produce new opportunities

Coming to peak of cycle, though still positives likely

What to do?

Page 33

危 机 Crisis

Danger Opportunity

喂 鸡 Wei Ji

Hello Chicken

Washington 14520 Avion Parkway #300 Chantilly, VA 20151 USA

Phone: +1 703 476 2300 Fax: +1 703 860 5855

London PO Box 38

Betchworth Surrey RH3 7YZ UK

Phone/Fax: +44 1737 843 756 New York 857 Post Road #253 Fairfield, CT 06824 USA Phone: +1 703 480 0568

www.AVITAS.com @AVITASInc