industrials and materials delta air lines, inc

TRANSCRIPT

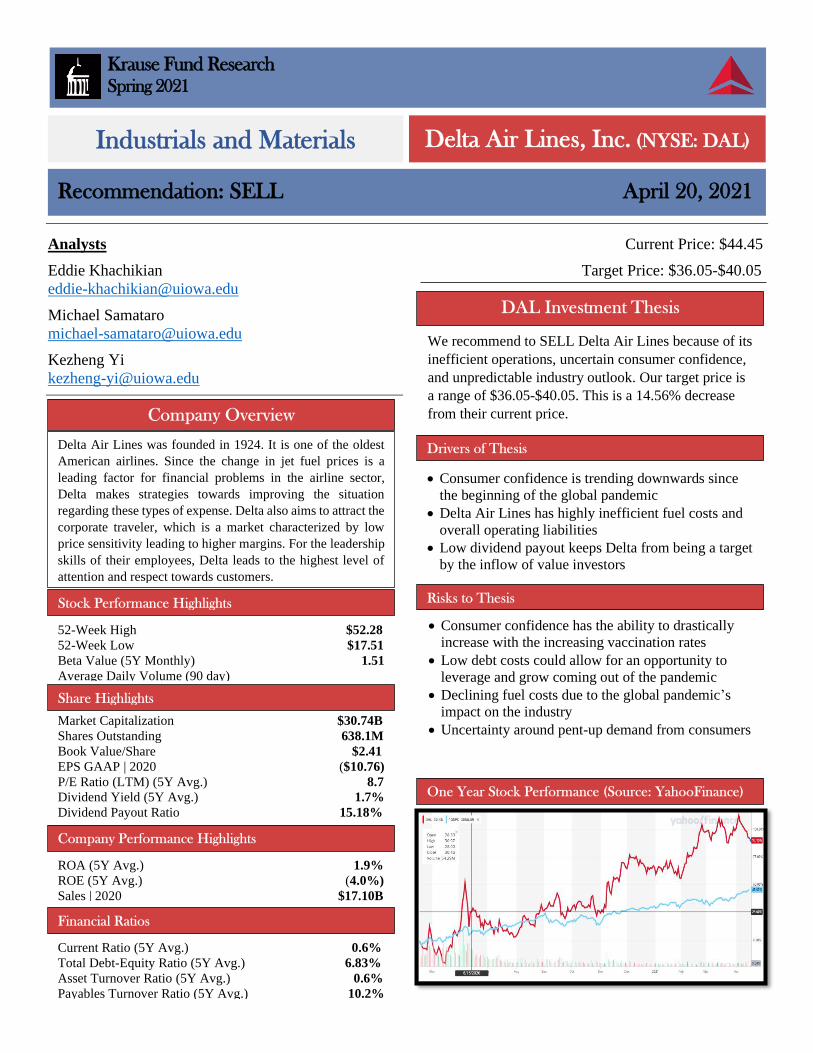

Analysts Current Price: $44.45

Eddie Khachikian Target Price: $36.05-$40.05

Michael Samataro

Kezheng Yi

Krause Fund Research Spring 2021

Industrials and Materials Delta Air Lines, Inc. (NYSE: DAL)

Recommendation: SELL April 20, 2021

We recommend to SELL Delta Air Lines because of its

inefficient operations, uncertain consumer confidence,

and unpredictable industry outlook. Our target price is

a range of $36.05-$40.05. This is a 14.56% decrease

from their current price.

52-Week High $52.28

52-Week Low $17.51

Beta Value (5Y Monthly) 1.51

Average Daily Volume (90 day)

13.6M

Market Capitalization $30.74B

Shares Outstanding 638.1M

Book Value/Share $2.41

EPS GAAP | 2020 ($10.76)

P/E Ratio (LTM) (5Y Avg.) 8.7

Dividend Yield (5Y Avg.) 1.7%

Dividend Payout Ratio 15.18%

Delta Air Lines was founded in 1924. It is one of the oldest

American airlines. Since the change in jet fuel prices is a

leading factor for financial problems in the airline sector,

Delta makes strategies towards improving the situation

regarding these types of expense. Delta also aims to attract the

corporate traveler, which is a market characterized by low

price sensitivity leading to higher margins. For the leadership

skills of their employees, Delta leads to the highest level of

attention and respect towards customers.

ROA (5Y Avg.) 1.9%

ROE (5Y Avg.) (4.0%)

Sales | 2020 $17.10B

Current Ratio (5Y Avg.) 0.6%

Total Debt-Equity Ratio (5Y Avg.) 6.83%

Asset Turnover Ratio (5Y Avg.) 0.6%

Payables Turnover Ratio (5Y Avg.) 10.2%

• Consumer confidence is trending downwards since

the beginning of the global pandemic

• Delta Air Lines has highly inefficient fuel costs and

overall operating liabilities

• Low dividend payout keeps Delta from being a target

by the inflow of value investors

• Consumer confidence has the ability to drastically

increase with the increasing vaccination rates

• Low debt costs could allow for an opportunity to

leverage and grow coming out of the pandemic

• Declining fuel costs due to the global pandemic’s

impact on the industry

• Uncertainty around pent-up demand from consumers

Company Analysis Notes:

-Connect Delta’s numbers to the industry analysis keys

2015 2016 2017 2018 2019 2020 2021E

Domestic 23,817.00 25,002.00 26,079.00 28,159.00 30,367.00 10,041.00 16,684.99

International 10,965.00 10,812.00 10,868.00 11,596.00 11,910.00 2,842.00 4,195.37

% of International 31.525% 30.189% 29.415% 29.169% 28.171% 22.060% 20.092%

In recent years, Delta Air Lines, Inc. (DAL) is showing

signs of expansion and involving themselves further into

foreign and international commercial travel. Due to the

fragmentation of the Airline Industry, the environment

is highly competitive overall across geographies and

product offerings. As the globalization keeps taking over

the airline industry, consolidation, increased corporate

partnerships and minority stake acquisitions will

continue in the long term. They tend to spend more in

capital expenditures than capital structure. However,

this spending is into more aircraft, airport slots, and

investments into other foreign airlines. We believe this

growth in spending will allow Delta Air Lines to take

advantage of the short-term growth. The airlines

industry will experience it as more people across the

globe are vaccinated.

In 2020, Delta lost a record $12.39 billion as the

pandemic drastically reduced customer travel demand.

Total revenue fell from $11.44 billion in the fourth

quarter of 2019 to $3.97 billion, down to about 35% of

what it was at the end of 2019. It is clear that Delta

Airlines’ total revenue is dramatically declined due to

the COVID-19 pandemic. It is a huge impact on the

airline company’s revenue. For example, people in US

are the main travelers to Europe. In particular, in 2019,

the flights generated about 15% of all passenger revenue

for Delta, or $6.4 billion. However, the European Union

is planning to bar most Americans to control the spread

of virus. The policy is the main reason to slash the Delta

Airline’s revenue in 2020. To control the spread of virus,

the ban flight policy is necessary. On the other hand, it

would slash the airline industry. The revenue would be

greatly impacted, and it needs time to recover. Adjusted

earnings per share had a loss of $2.53 versus an expected

loss of $2.50. Total revenue of $3.97 billion versus an

expected $3.59 billion in revenue and so they made

slightly more than forecasted. The flight ban policy

greatly impacted the airline industries economic. It

impacted the stock price of Delta Air Lines. On the other

hand, there is a slight increase from the expected

revenue. In this case, the wave of international students

returning to their home country is one of the main

reasons. For example, Chinese students are one of the

largest group of students in US university. During 2020,

many students feel that their studies are disrupted, fear

they will not be able to graduate and are struggling from

a lack of support and information by Chinese

universities and authorities over their return.

Frustrations have reached an all-time high, prompting

students to start several online courses for their quick

return to China. Not only them, but also their parents

urge them back to China. Thus, many Chinese student

returned to China to take online courses instead of

staying at the universities. The most important thing is

that they want to maintain safety. During this time, the

airline’s industry revenue returned a little back at the end

of the year, in particular the Delta Air Lines. All in all,

the total revenue was greatly slashed and is expected to

recover with the help of the vaccine within this next

year.

It is important to analyze the total operating expense in

2020 and the 4th quarter last year. According to the

analysis, the total operating expense is $4.3 billion in

2020, with a $10.8 billion decrease compared to 2019.

The adjusted operating expense decreased $16 billion

with a 40% decline over 2019. The total operating

expense is $930 million in the 4th quarter in 2020, with

a $5.2 billion decline compared to the 4th quarter in

2019. The adjusted operating expense in the 4th quarter

in 2020 decreased by $4.6 billion, which is 47% greater

than the 4th quarter in 2019”.15 Due to the pandemic,

Delta Air Lines tried to reduce its expenditures to

maintain its positive cash flow by reducing the number

of planes they had flying and reducing ticket costs. It is

important to maintain its normal operations and not fall

too behind due to the pandemic as they should settle

back to pre-pandemic levels within the next year or two.

Delta even attempted to hedge jet fuel costs in 2012 by

purchasing a refinery, being the first airline company to

own one. However, over time, they found that the

refinery barely made profit in some years and lost

money in others; overall it was not worth it. Last year in

2020, due to the pandemic and the decreased demand for

air travel, the refinery actually proved to be a liability

and is ultimately not seen as a successful venture.12

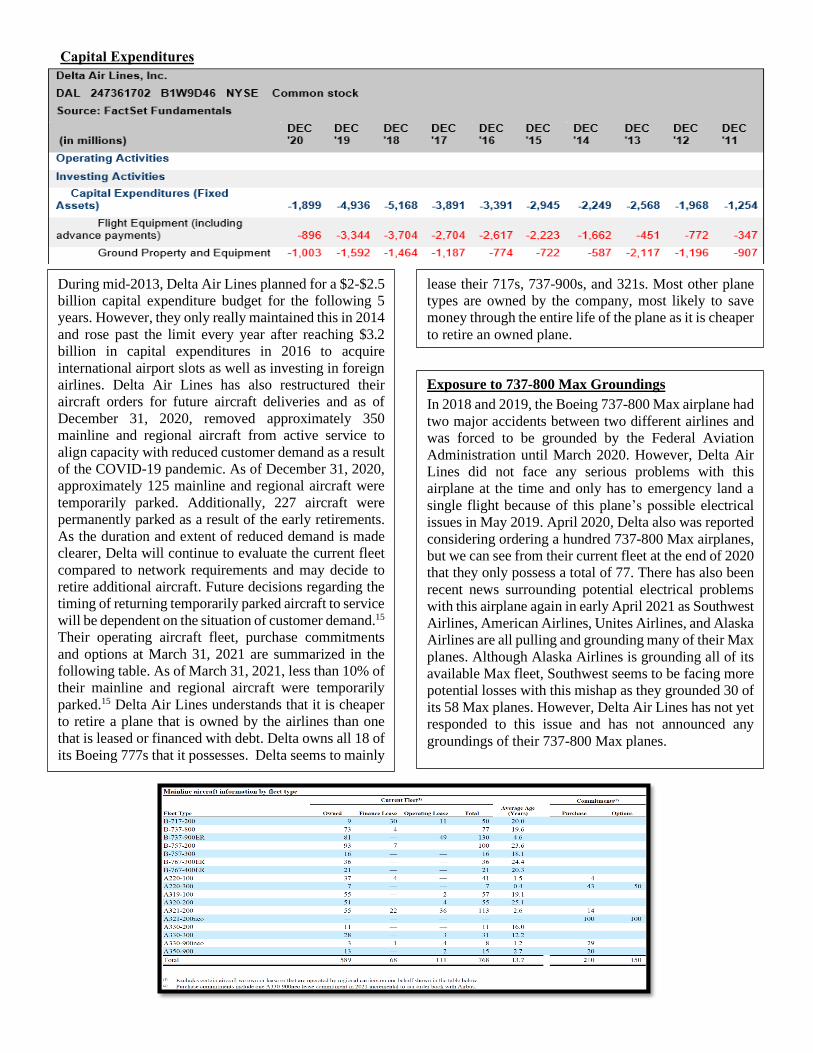

During mid-2013, Delta Air Lines planned for a $2-$2.5

billion capital expenditure budget for the following 5

years. However, they only really maintained this in 2014

and rose past the limit every year after reaching $3.2

billion in capital expenditures in 2016 to acquire

international airport slots as well as investing in foreign

airlines. Delta Air Lines has also restructured their

aircraft orders for future aircraft deliveries and as of

December 31, 2020, removed approximately 350

mainline and regional aircraft from active service to

align capacity with reduced customer demand as a result

of the COVID-19 pandemic. As of December 31, 2020,

approximately 125 mainline and regional aircraft were

temporarily parked. Additionally, 227 aircraft were

permanently parked as a result of the early retirements.

As the duration and extent of reduced demand is made

clearer, Delta will continue to evaluate the current fleet

compared to network requirements and may decide to

retire additional aircraft. Future decisions regarding the

timing of returning temporarily parked aircraft to service

will be dependent on the situation of customer demand.15

Their operating aircraft fleet, purchase commitments

and options at March 31, 2021 are summarized in the

following table. As of March 31, 2021, less than 10% of

their mainline and regional aircraft were temporarily

parked.15 Delta Air Lines understands that it is cheaper

to retire a plane that is owned by the airlines than one

that is leased or financed with debt. Delta owns all 18 of

its Boeing 777s that it possesses. Delta seems to mainly

lease their 717s, 737-900s, and 321s. Most other plane

types are owned by the company, most likely to save

money through the entire life of the plane as it is cheaper

to retire an owned plane.

Exposure to 737-800 Max Groundings

In 2018 and 2019, the Boeing 737-800 Max airplane had

two major accidents between two different airlines and

was forced to be grounded by the Federal Aviation

Administration until March 2020. However, Delta Air

Lines did not face any serious problems with this

airplane at the time and only has to emergency land a

single flight because of this plane’s possible electrical

issues in May 2019. April 2020, Delta also was reported

considering ordering a hundred 737-800 Max airplanes,

but we can see from their current fleet at the end of 2020

that they only possess a total of 77. There has also been

recent news surrounding potential electrical problems

with this airplane again in early April 2021 as Southwest

Airlines, American Airlines, Unites Airlines, and Alaska

Airlines are all pulling and grounding many of their Max

planes. Although Alaska Airlines is grounding all of its

available Max fleet, Southwest seems to be facing more

potential losses with this mishap as they grounded 30 of

its 58 Max planes. However, Delta Air Lines has not yet

responded to this issue and has not announced any

groundings of their 737-800 Max planes.

Fuel Costs

As shown in the quarter from 1 to 4 in 2020, the fuel cost

has declined dramatically. Normally, the average fuel

cost per quarter is above $1.2B. However, the situation

was different in 2020. The pandemic of COVID-19

started around March in 2020 in the US, which was close

to the end of the 1st quarter. The amount of fuel cost in

1st quarter reached above the normal level around

$1.6B. Afterwards, it slashed to below $400M. It

generally increased to 500 M in quarter 3 and to $700M

in quarter 4. According to the forecast, it still needs a

long time to reach the normal level. On the other hand,

Delta Air Lines did a good job to maintain its cash

streams and Revenue Passenger Mile (RPM) by

reducing its expenditures. Generally, it reached the top

level of RPM among its competitors during the

pandemic period. As shown in quarter 4 of 2020, real

GDP seems to have stabilized in the short-term for the

United States economy. We expect that in the short-

term, real GDP will see even higher increases when the

first half of 2021’s real GDP is reported. This is due to

the second round of stimulus checks flooding into the

economy as well as a positive increase in consumer

confidence due to the growing positive vaccination

results stemming from the federal government’s

research.

Global Airline Traffic Growth

Due to the pandemic of COVID-19, the global airline

traffic growth was slashed during the 2020. Comparing

to its main competitors, such as United, Southern

western, American Airlines, Delta gained its profit by

generating its positive brand. Many people tend to buy

Delta’s ticket, regardless of the pandemic. Therefore, it

gains its loyal customers and could generate its

profitability in the long run. This 5.7% year-over-year

growth decrease is due to the disruption from the global

pandemic. This sharp decline reveals that consumption

decreased as well as consumer confidence. For

industries to make up a high percentage of GDP, such

as financial services and airlines, the government needs

to make drastic changes to our economy to slow the

drop in GDP. Luckily, the federal government did just

that by increasing spending in the latter half of 2020 and

implementing stimulus checks. As shown below, this

increase in government spending created a quick and

positive impact on GDP.

Load Factor

In general, load factor is a key measure of the

company’s capacity utilization among industries. This

is a challenge for airline industry because people do not

tend to buy airline tickets for travelling during the

pandemic of COVID-19. Besides, there are some

airline-ban-policies in some countries, such as Spain,

UK, Italy, and so on. On the other hand, Delta did a

great job in this field among its competitors. Delta Air

Lines followed closely behind American Airlines

(Revenue Passenger Mile) RPM of 128.5 B with 121.7

B, as well as its RPM was closed by their industry-

leading load factor of 86.5%. In conclusion, Delta

generates a higher profitability than its competitors and

maintains the top level of its capacity utilization by its

highest load factor in the airline industry.

Consumer Confidence Index

In general, the Consumer Confidence Index (CCI) has

decreased due to the COVID-19 pandemic. The CCI

indicates the customers' confidence for their spending in

a specific industry. During the specific period, people

tend to stay in their safety at home instead of traveling

to other destinations. On the other hand, the CCI in Delta

Airlines is relatively higher than its competitors.

Because of COVID-19, people’s wages are slashed by

the economic recession. People do not have enough

money to spend in travel, such as personal and business

travel. Compared to its main competitors, such as United

and Southwestern Airlines, Delta Air Lines has a

relative lower price. Therefore, people might afford it

and it increases their CCI.

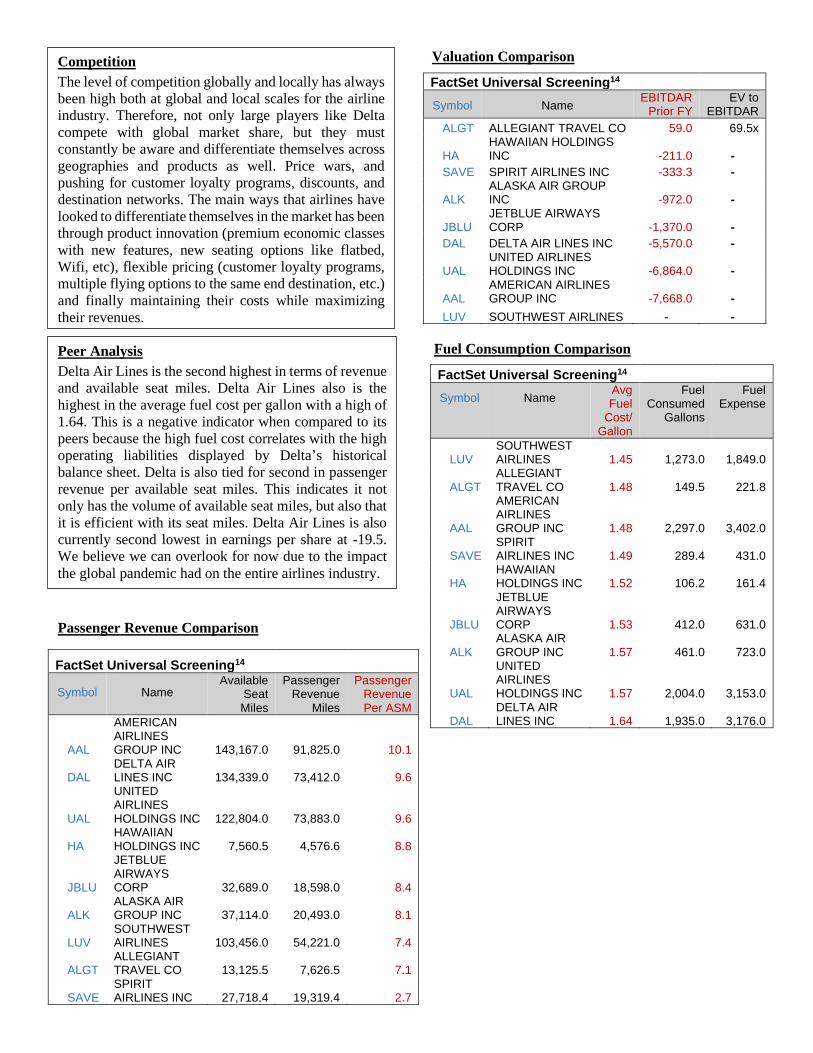

Valuation Comparison

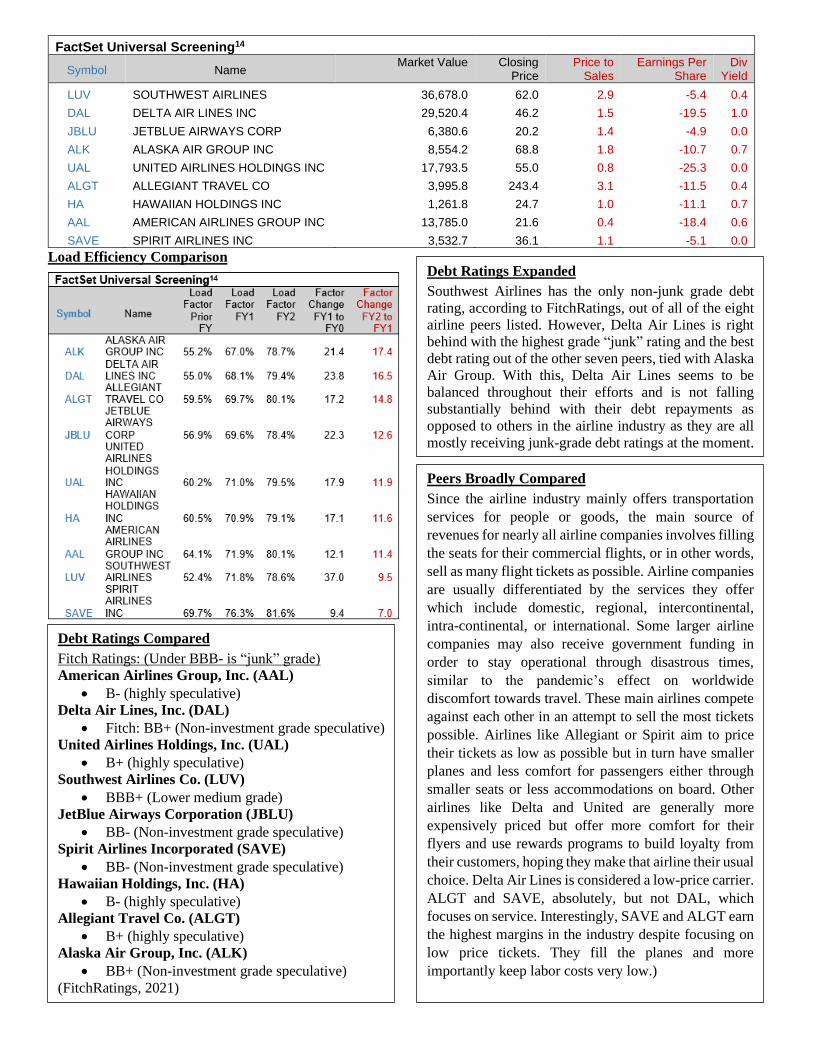

FactSet Universal Screening14

Symbol Name EBITDAR

Prior FY EV to

EBITDAR

ALGT ALLEGIANT TRAVEL CO 59.0 69.5x

HA HAWAIIAN HOLDINGS INC -211.0 -

SAVE SPIRIT AIRLINES INC -333.3 -

ALK ALASKA AIR GROUP INC -972.0 -

JBLU JETBLUE AIRWAYS CORP -1,370.0 -

DAL DELTA AIR LINES INC -5,570.0 -

UAL UNITED AIRLINES HOLDINGS INC -6,864.0 -

AAL AMERICAN AIRLINES GROUP INC -7,668.0 -

LUV SOUTHWEST AIRLINES - -

FactSet Universal Screening14

Symbol Name Avg Fuel

Cost/ Gallon

Fuel Consumed

Gallons

Fuel Expense

LUV SOUTHWEST AIRLINES 1.45 1,273.0 1,849.0

ALGT ALLEGIANT TRAVEL CO 1.48 149.5 221.8

AAL

AMERICAN AIRLINES GROUP INC 1.48 2,297.0 3,402.0

SAVE SPIRIT AIRLINES INC 1.49 289.4 431.0

HA HAWAIIAN HOLDINGS INC 1.52 106.2 161.4

JBLU

JETBLUE AIRWAYS CORP 1.53 412.0 631.0

ALK ALASKA AIR GROUP INC 1.57 461.0 723.0

UAL

UNITED AIRLINES HOLDINGS INC 1.57 2,004.0 3,153.0

DAL DELTA AIR LINES INC 1.64 1,935.0 3,176.0

FactSet Universal Screening14

Symbol Name Available

Seat Miles

Passenger Revenue

Miles

Passenger Revenue Per ASM

AAL

AMERICAN AIRLINES GROUP INC 143,167.0 91,825.0 10.1

DAL DELTA AIR LINES INC 134,339.0 73,412.0 9.6

UAL

UNITED AIRLINES HOLDINGS INC 122,804.0 73,883.0 9.6

HA HAWAIIAN HOLDINGS INC 7,560.5 4,576.6 8.8

JBLU

JETBLUE AIRWAYS CORP 32,689.0 18,598.0 8.4

ALK ALASKA AIR GROUP INC 37,114.0 20,493.0 8.1

LUV SOUTHWEST AIRLINES 103,456.0 54,221.0 7.4

ALGT ALLEGIANT TRAVEL CO 13,125.5 7,626.5 7.1

SAVE SPIRIT AIRLINES INC 27,718.4 19,319.4 2.7

Competition

The level of competition globally and locally has always

been high both at global and local scales for the airline

industry. Therefore, not only large players like Delta

compete with global market share, but they must

constantly be aware and differentiate themselves across

geographies and products as well. Price wars, and

pushing for customer loyalty programs, discounts, and

destination networks. The main ways that airlines have

looked to differentiate themselves in the market has been

through product innovation (premium economic classes

with new features, new seating options like flatbed,

Wifi, etc), flexible pricing (customer loyalty programs,

multiple flying options to the same end destination, etc.)

and finally maintaining their costs while maximizing

their revenues.

Fuel Consumption Comparison

Passenger Revenue Comparison

Peer Analysis

Delta Air Lines is the second highest in terms of revenue

and available seat miles. Delta Air Lines also is the

highest in the average fuel cost per gallon with a high of

1.64. This is a negative indicator when compared to its

peers because the high fuel cost correlates with the high

operating liabilities displayed by Delta’s historical

balance sheet. Delta is also tied for second in passenger

revenue per available seat miles. This indicates it not

only has the volume of available seat miles, but also that

it is efficient with its seat miles. Delta Air Lines is also

currently second lowest in earnings per share at -19.5.

We believe we can overlook for now due to the impact

the global pandemic had on the entire airlines industry.

Load Efficiency Comparison

FactSet Universal Screening14

Symbol Name Market Value Closing

Price Price to

Sales Earnings Per

Share Div

Yield

LUV SOUTHWEST AIRLINES 36,678.0 62.0 2.9 -5.4 0.4

DAL DELTA AIR LINES INC 29,520.4 46.2 1.5 -19.5 1.0

JBLU JETBLUE AIRWAYS CORP 6,380.6 20.2 1.4 -4.9 0.0

ALK ALASKA AIR GROUP INC 8,554.2 68.8 1.8 -10.7 0.7

UAL UNITED AIRLINES HOLDINGS INC 17,793.5 55.0 0.8 -25.3 0.0

ALGT ALLEGIANT TRAVEL CO 3,995.8 243.4 3.1 -11.5 0.4

HA HAWAIIAN HOLDINGS INC 1,261.8 24.7 1.0 -11.1 0.7

AAL AMERICAN AIRLINES GROUP INC 13,785.0 21.6 0.4 -18.4 0.6

SAVE SPIRIT AIRLINES INC 3,532.7 36.1 1.1 -5.1 0.0

Debt Ratings Compared

Fitch Ratings: (Under BBB- is “junk” grade)

American Airlines Group, Inc. (AAL)

• B- (highly speculative)

Delta Air Lines, Inc. (DAL)

• Fitch: BB+ (Non-investment grade speculative)

United Airlines Holdings, Inc. (UAL)

• B+ (highly speculative)

Southwest Airlines Co. (LUV)

• BBB+ (Lower medium grade)

JetBlue Airways Corporation (JBLU)

• BB- (Non-investment grade speculative)

Spirit Airlines Incorporated (SAVE)

• BB- (Non-investment grade speculative)

Hawaiian Holdings, Inc. (HA)

• B- (highly speculative)

Allegiant Travel Co. (ALGT)

• B+ (highly speculative)

Alaska Air Group, Inc. (ALK)

• BB+ (Non-investment grade speculative)

(FitchRatings, 2021)

Debt Ratings Expanded

Southwest Airlines has the only non-junk grade debt

rating, according to FitchRatings, out of all of the eight

airline peers listed. However, Delta Air Lines is right

behind with the highest grade “junk” rating and the best

debt rating out of the other seven peers, tied with Alaska

Air Group. With this, Delta Air Lines seems to be

balanced throughout their efforts and is not falling

substantially behind with their debt repayments as

opposed to others in the airline industry as they are all

mostly receiving junk-grade debt ratings at the moment.

Peers Broadly Compared

Since the airline industry mainly offers transportation

services for people or goods, the main source of

revenues for nearly all airline companies involves filling

the seats for their commercial flights, or in other words,

sell as many flight tickets as possible. Airline companies

are usually differentiated by the services they offer

which include domestic, regional, intercontinental,

intra-continental, or international. Some larger airline

companies may also receive government funding in

order to stay operational through disastrous times,

similar to the pandemic’s effect on worldwide

discomfort towards travel. These main airlines compete

against each other in an attempt to sell the most tickets

possible. Airlines like Allegiant or Spirit aim to price

their tickets as low as possible but in turn have smaller

planes and less comfort for passengers either through

smaller seats or less accommodations on board. Other

airlines like Delta and United are generally more

expensively priced but offer more comfort for their

flyers and use rewards programs to build loyalty from

their customers, hoping they make that airline their usual

choice. Delta Air Lines is considered a low-price carrier.

ALGT and SAVE, absolutely, but not DAL, which

focuses on service. Interestingly, SAVE and ALGT earn

the highest margins in the industry despite focusing on

low price tickets. They fill the planes and more

importantly keep labor costs very low.)

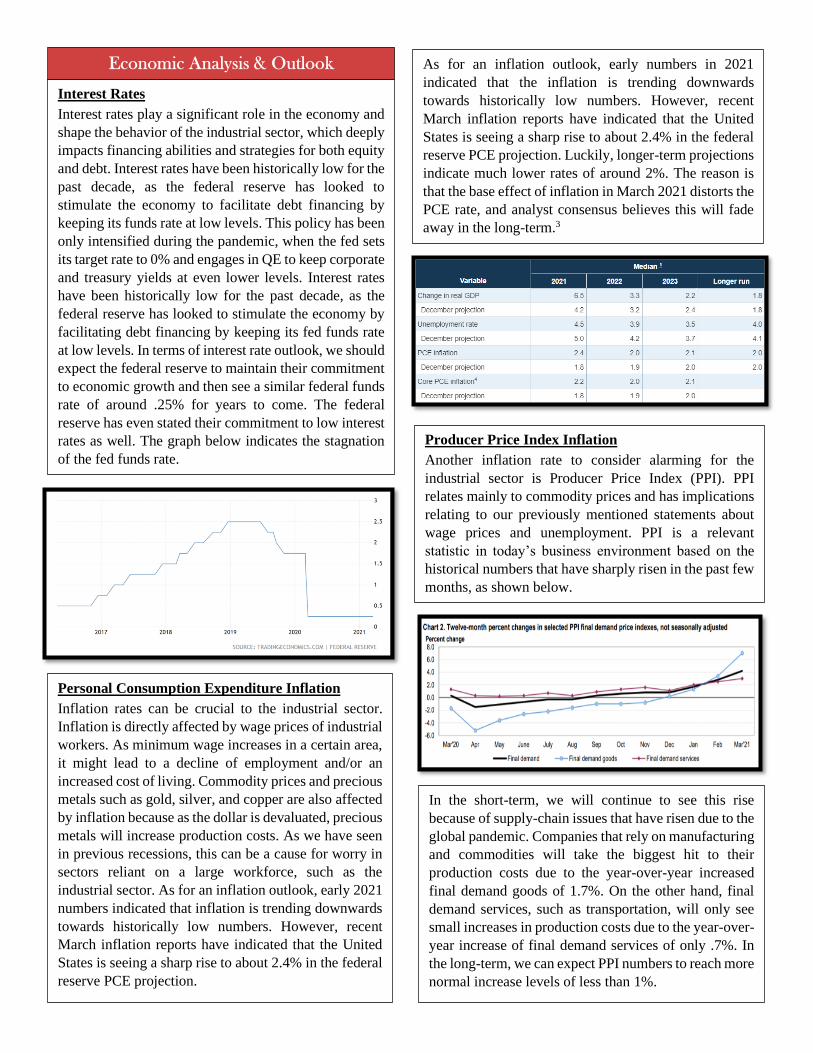

Interest Rates

Interest rates play a significant role in the economy and

shape the behavior of the industrial sector, which deeply

impacts financing abilities and strategies for both equity

and debt. Interest rates have been historically low for the

past decade, as the federal reserve has looked to

stimulate the economy to facilitate debt financing by

keeping its funds rate at low levels. This policy has been

only intensified during the pandemic, when the fed sets

its target rate to 0% and engages in QE to keep corporate

and treasury yields at even lower levels. Interest rates

have been historically low for the past decade, as the

federal reserve has looked to stimulate the economy by

facilitating debt financing by keeping its fed funds rate

at low levels. In terms of interest rate outlook, we should

expect the federal reserve to maintain their commitment

to economic growth and then see a similar federal funds

rate of around .25% for years to come. The federal

reserve has even stated their commitment to low interest

rates as well. The graph below indicates the stagnation

of the fed funds rate.

Personal Consumption Expenditure Inflation

Inflation rates can be crucial to the industrial sector.

Inflation is directly affected by wage prices of industrial

workers. As minimum wage increases in a certain area,

it might lead to a decline of employment and/or an

increased cost of living. Commodity prices and precious

metals such as gold, silver, and copper are also affected

by inflation because as the dollar is devaluated, precious

metals will increase production costs. As we have seen

in previous recessions, this can be a cause for worry in

sectors reliant on a large workforce, such as the

industrial sector. As for an inflation outlook, early 2021

numbers indicated that inflation is trending downwards

towards historically low numbers. However, recent

March inflation reports have indicated that the United

States is seeing a sharp rise to about 2.4% in the federal

reserve PCE projection.

As for an inflation outlook, early numbers in 2021

indicated that the inflation is trending downwards

towards historically low numbers. However, recent

March inflation reports have indicated that the United

States is seeing a sharp rise to about 2.4% in the federal

reserve PCE projection. Luckily, longer-term projections

indicate much lower rates of around 2%. The reason is

that the base effect of inflation in March 2021 distorts the

PCE rate, and analyst consensus believes this will fade

away in the long-term.3

Producer Price Index Inflation

Another inflation rate to consider alarming for the

industrial sector is Producer Price Index (PPI). PPI

relates mainly to commodity prices and has implications

relating to our previously mentioned statements about

wage prices and unemployment. PPI is a relevant

statistic in today’s business environment based on the

historical numbers that have sharply risen in the past few

months, as shown below.

In the short-term, we will continue to see this rise

because of supply-chain issues that have risen due to the

global pandemic. Companies that rely on manufacturing

and commodities will take the biggest hit to their

production costs due to the year-over-year increased

final demand goods of 1.7%. On the other hand, final

demand services, such as transportation, will only see

small increases in production costs due to the year-over-

year increase of final demand services of only .7%. In

the long-term, we can expect PPI numbers to reach more

normal increase levels of less than 1%.

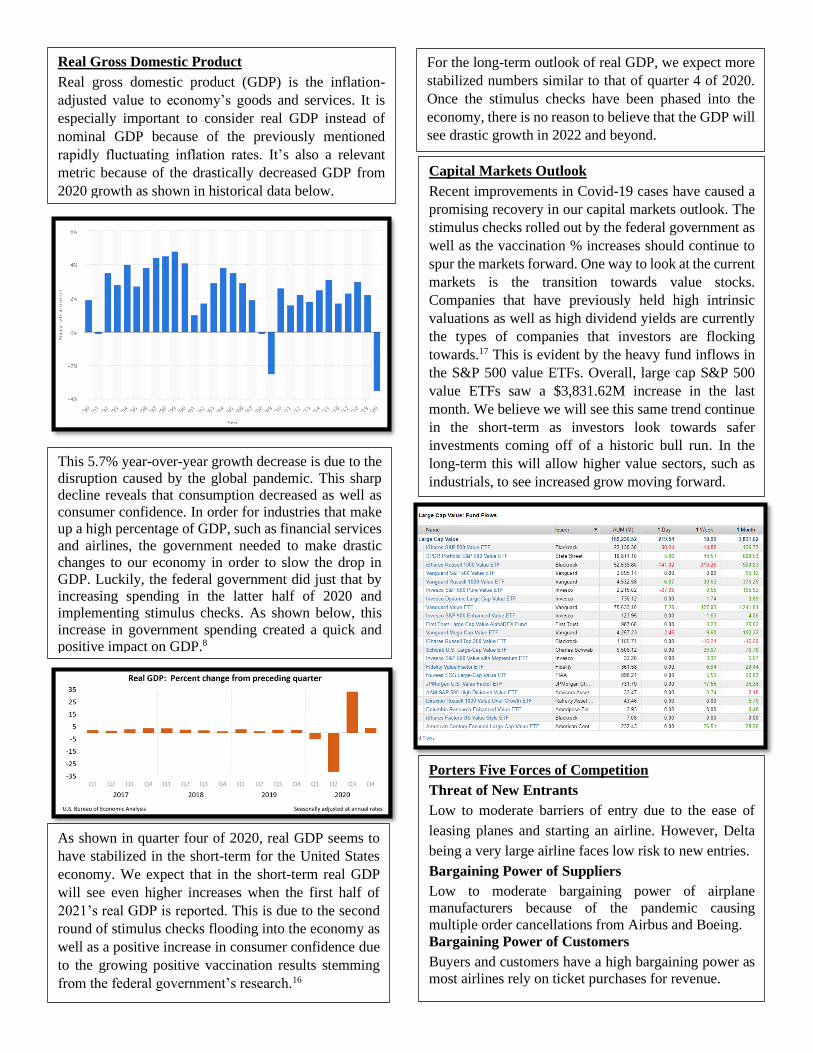

Real Gross Domestic Product

Real gross domestic product (GDP) is the inflation-

adjusted value to economy’s goods and services. It is

especially important to consider real GDP instead of

nominal GDP because of the previously mentioned

rapidly fluctuating inflation rates. It’s also a relevant

metric because of the drastically decreased GDP from

2020 growth as shown in historical data below.

This 5.7% year-over-year growth decrease is due to the

disruption caused by the global pandemic. This sharp

decline reveals that consumption decreased as well as

consumer confidence. In order for industries that make

up a high percentage of GDP, such as financial services

and airlines, the government needed to make drastic

changes to our economy in order to slow the drop in

GDP. Luckily, the federal government did just that by

increasing spending in the latter half of 2020 and

implementing stimulus checks. As shown below, this

increase in government spending created a quick and

positive impact on GDP.8

As shown in quarter four of 2020, real GDP seems to

have stabilized in the short-term for the United States

economy. We expect that in the short-term real GDP

will see even higher increases when the first half of

2021’s real GDP is reported. This is due to the second

round of stimulus checks flooding into the economy as

well as a positive increase in consumer confidence due

to the growing positive vaccination results stemming

from the federal government’s research.16

For the long-term outlook of real GDP, we expect more

stabilized numbers similar to that of quarter 4 of 2020.

Once the stimulus checks have been phased into the

economy, there is no reason to believe that the GDP will

see drastic growth in 2022 and beyond.

Capital Markets Outlook

Recent improvements in Covid-19 cases have caused a

promising recovery in our capital markets outlook. The

stimulus checks rolled out by the federal government as

well as the vaccination % increases should continue to

spur the markets forward. One way to look at the current

markets is the transition towards value stocks.

Companies that have previously held high intrinsic

valuations as well as high dividend yields are currently

the types of companies that investors are flocking

towards.17 This is evident by the heavy fund inflows in

the S&P 500 value ETFs. Overall, large cap S&P 500

value ETFs saw a $3,831.62M increase in the last

month. We believe we will see this same trend continue

in the short-term as investors look towards safer

investments coming off of a historic bull run. In the

long-term this will allow higher value sectors, such as

industrials, to see increased grow moving forward.

Porters Five Forces of Competition

Threat of New Entrants

Low to moderate barriers of entry due to the ease of

leasing planes and starting an airline. However, Delta

being a very large airline faces low risk to new entries.

Bargaining Power of Suppliers

Low to moderate bargaining power of airplane

manufacturers because of the pandemic causing

multiple order cancellations from Airbus and Boeing.

Bargaining Power of Customers

Buyers and customers have a high bargaining power as

most airlines rely on ticket purchases for revenue.

Valuation Reasoning

The final valuation range we arrived at was between

$36.05 and $40.05 per share. The way we arrived at this

range was mainly by using the DCF and EP models of

valuation and accounting for our sensitivity tables. The

DDM model of valuation was not a technique our group

put a lot of stock into due to its low skewed valuation.

The reason for the low-skewed valuation is because

Delta is not a company with a high payout ratio. To

account for the low-skewed valuation, we made sure to

show a range on the lower side when compared to the

DCF and EP valuation of $40.05 per share. This is

abnormal for many companies with as strong of cash

flows as Delta has seen over the past decade. These

strong cash flows are also what caused us to put more

stock into the DCF and EP models.

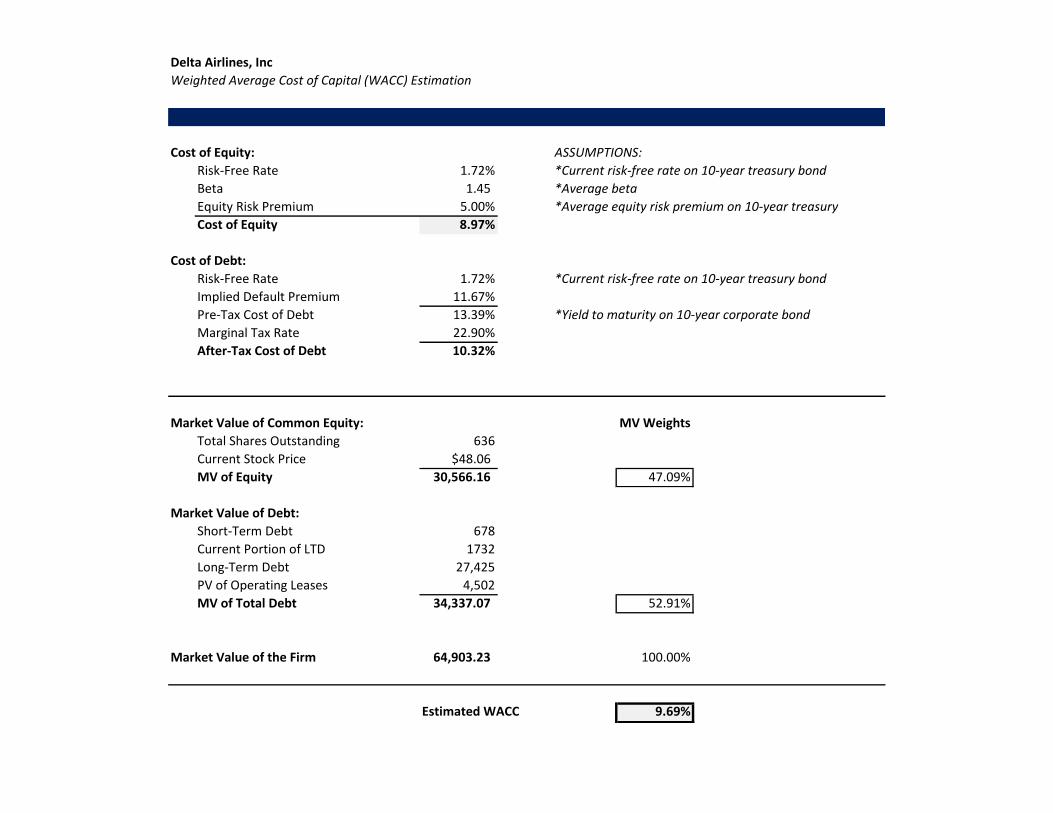

Weighted Average Cost of Capital

The WACC our group arrived at was 9.69%. We

arrived at this percentage by weighing out the cost of

equity as well as the cost of debt. By doing so we could

account for the changes in Delta’s capital structure.

using a risk-free rate of 1.72%, a beta of 1.45, and an

equity risk premium of 5%. This WACC valuation

seems to come out on the high side for the airlines

industry. This indicates to us that Delta does not have

an overwhelming amount of debt in their structure.

When compared to a company like American Airlines

who does have this type of structure, we can expect

Delta to see much less risk to their growth in the coming

years.

Critical Assumptions

A crucial operations assumption we made was to lower

the of growth made by “Cargo” and “Other” revenue.

These segments of revenue growth decreasing are

something we are comfortable with as Delta transitions

back towards its passenger revenue segments. Other

income statement assumptions were to not utilize the

2020 historical accounts. These accounts would drop the

revenue growth forecasts and not line up with

reasonable assumptions for industry metrics. We also

made sure to include a steady growth of foreign revenue.

As Delta intends to move more into this area, it logical

to assume they are almost guaranteed to grow in this

segment. The same critical assumption to not include

2020 balance sheet accounts in our forecasted averages

was also made. The reasoning for this was because the

2020 accounts were far too inconceivable to forecast in

the coming years. This would have completely thrown

off the forecasting of our model. Another balance sheet

assumption we made was to not include the first seven

years of taxes payable. This is because the taxes

Application of Valuation Model

We feel very confident in the implied share price range

we decided on. Going into the valuation we expected

the range to trend towards at a lower point than what

Delta is currently trading at. While Delta does have

good parts of their business, like its available seat miles,

low debt, and potential to operate in foreign countries,

we felt that in order for Delta to become a buy rating

our valuation would have to trend closer to the upper

trends of our sensitivity analysis. A number closer to the

upper trends on the “Current Dividend Yield” and

“Beta” table would reverse the sell rating. The way that

Delta Air Lines can do this is by paying out a higher

dividend yield. A higher dividend yield makes Delta a

more attractive company to the inflow of value

investors and increase its DCF and EP valuation. Based

on our sensitivity tables, they could focus on improving

their dividend payout ratio. One thing I do believe our

valuation understated is the underfunded pensions.

Another way Delta could reverse the sell rating is by

providing consistently lower operating liabilities. In the

post-pandemic world, this is still likely to continue

based on the fact that many people are cancelling

passenger flights and Delta still has to pay for their

highly inefficient fuel obligations. One thing that was

understated by our model was the underfunded

pensions. Delta steal has to deal with underfunded

pensions today compared to other airlines. This could

potentially change its DCF and EP valuation.

Degree of Rivalry or Competition

Since the airline industry is highly competitive, there is

a high degree of competition as they all use different

strategies to convince consumers to fly with them and

eventually stay loyal.

Threat of Substitutes

The threat of substitutes is moderate because at times,

consumers may only have the option to fly where they

need to get to, other times if the destination is closer, the

consumer may turn to another form of transportation.

payable account was not present in the final three years

of Delta’s financials. We also did this with other line

items that were in the same situation as the taxes

payable account. This will give us a more accurate

outlook of how Delta is moving forward with their

balance sheet items.

Cost of Debt

We arrived at the cost of debt by using a risk-free rate

of 1.72%, an implied default premium of 11.67%, and a

marginal tax rate of 22.90%. The risk-free rate was

assumed by using the United States’ 10-year treasury

yield. The implied default premium was also found by

then subtracting the risk-free rate from the cost of debt.

The final piece, the marginal tax rate, we came to by

accounting for the domestic segments of Delta’s

business as well as their foreign segments.

Beta and Equity Risk Premium

This sensitivity table provided with a drastic range in

our company’s valuation. This is mainly because of the

fact that the beta is a key component in calculating

Delta’s WACC. The WACC is the number that can

skew the DCF and EP valuation the most. We took this

into consideration when analyzing this table, by

considering this to be a close range to our final valuation

range given the importance the beta has on the final

share price.

Cost of Equity

We arrived at the cost of equity by using a risk-free rate

of 1.72%, a beta of 1.45, and an equity risk premium of

5%. The risk-free was assumed the same way as our cost

of debt. The beta was taken from the average historical

beta for Delta Air Lines. The equity risk premium was

assumed by taking the difference between the average

market returns and the returns of Delta Air Lines stock

performance.

Risk Free Rate and CV Growth of NOPLAT

This sensitivity analysis had little effect on the final

valuation of our company. The overall NOPLAT

growth sees large increases up to .30% and only lightly

raises the valuation of the company. I believe this

comparison is a good benchmark showing that the

internal factors of the valuation were accurately

calculated.

Pre-tax Cost of Debt and WACC

The pre-tax cost of debt is especially important to

analyze because it is critical to the health of the airline

industry. However, Delta Air Lines has a WACC

indicates that it has a lower debt ratio meaning that the

Current Dividend Yield and Beta

This sensitivity analysis was an analysis that helped us

decide not to put much stock into the DDM model of

valuation. The dividend yield displayed here has an

extremely high amount of impact on the final stock

price and reaches either an unreasonably high price of

$51.64 or an unreasonably low price of $30.62. The

impact the dividend payout has on the final price

cannot be understated. These unreasonably low ranges

show that through the DDM model we will reach an

unreasonably low price due to Delta’s lacking dividend

payout.

WACC and Cost of Equity

In general, the WACC and Cost of Equity play an

important role in a company´s financial situation.

Because of the pandemic of COVID-19, WACC has

been slashed in Delta due to the fewer investors to invest

in airline industry. Because of the lower passenger, it

generates a relative lower revenue in this specific

sensitivity table. We consider this table to be of high

importance to the valuation because of the high amount

of equity in Delta’s capital structure.

The WACC considers of cost of debt and cost of equity.

It generally includes a company´s bonds and long-term

debt in the cost of debt and common and preferred stock

in the cost of equity. Comparing to Southwest Airlines

borrowing money from government bonds, Delta has

much less borrowing fonds from lenders. Furthermore,

due to the pandemic, the stock value does not have a

dramatically increase for Delta Airlines. Many people

tend to stay safety at home instead of travelling outside.

In general, the Airline industry cannot be able to attract

other investors to invest money. Therefore, the WACC

is gently slashed for Delta.

CV Growth of EPS and Pre-tax Cost of Debt

The EPS is critically important to the valuation. Delta

Air Lines EPS fell drastically in the final year of 2020

and revealed the large impact the pandemic had on the

company. As shown in the table the impact of the EPS

is shown by having extremely high and low valuation

with even the slightest changes. Pre-tax cost of debt did

not move the valuation much due to the low debt ratio

of Delta Air Lines. This kept the valuation consistent

across the table and strengthened our knowledge of the

effect of Delta’s EPS.

pre-tax cost of debt does not impact our valuation in a

large way. What this table does reveal is that the equity

going into our WACC is crucial to the valuation based

on the high changes in the valuation when we change

the WACC.

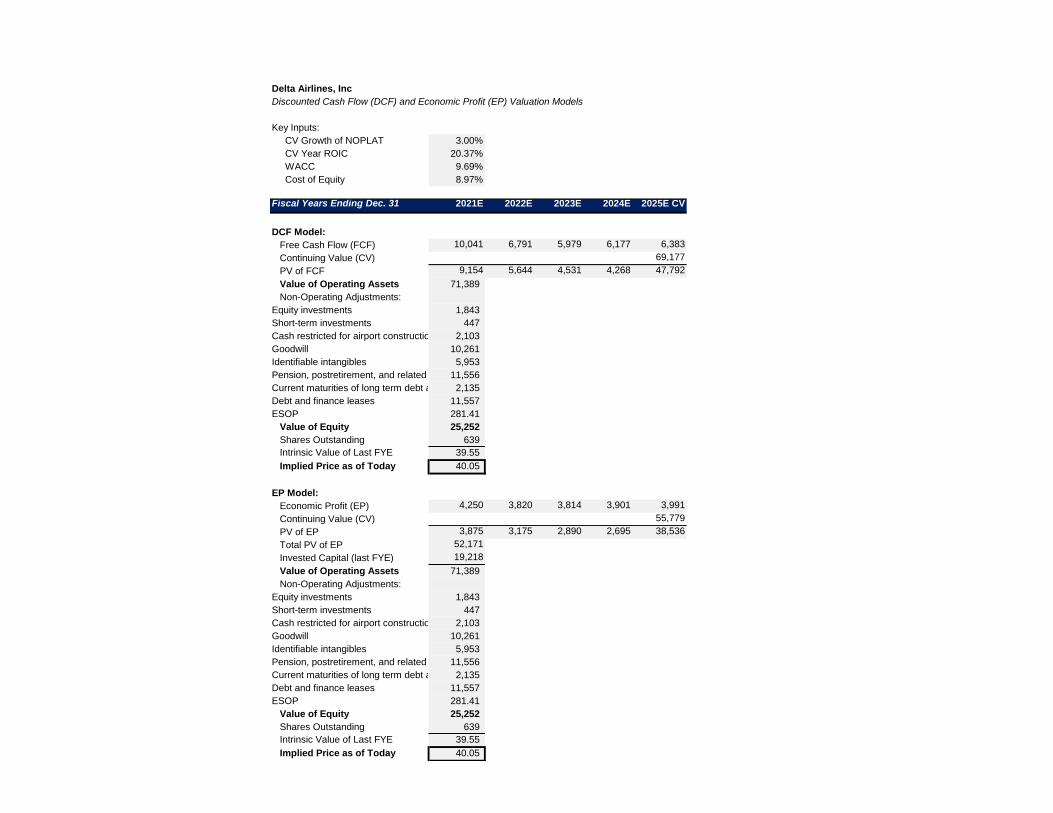

Delta Airlines, Inc

Discounted Cash Flow (DCF) and Economic Profit (EP) Valuation Models

Key Inputs:

CV Growth of NOPLAT 3.00%

CV Year ROIC 20.37%

WACC 9.69%

Cost of Equity 8.97%

Fiscal Years Ending Dec. 31 2021E 2022E 2023E 2024E 2025E CV

DCF Model:

Free Cash Flow (FCF) 10,041 6,791 5,979 6,177 6,383

Continuing Value (CV) 69,177

PV of FCF 9,154 5,644 4,531 4,268 47,792

Value of Operating Assets 71,389

Non-Operating Adjustments:

Equity investments 1,843

Short-term investments 447

Cash restricted for airport construction 2,103

Goodwill 10,261

Identifiable intangibles 5,953

Pension, postretirement, and related benefits11,556

Current maturities of long term debt and finance leases2,135

Debt and finance leases 11,557

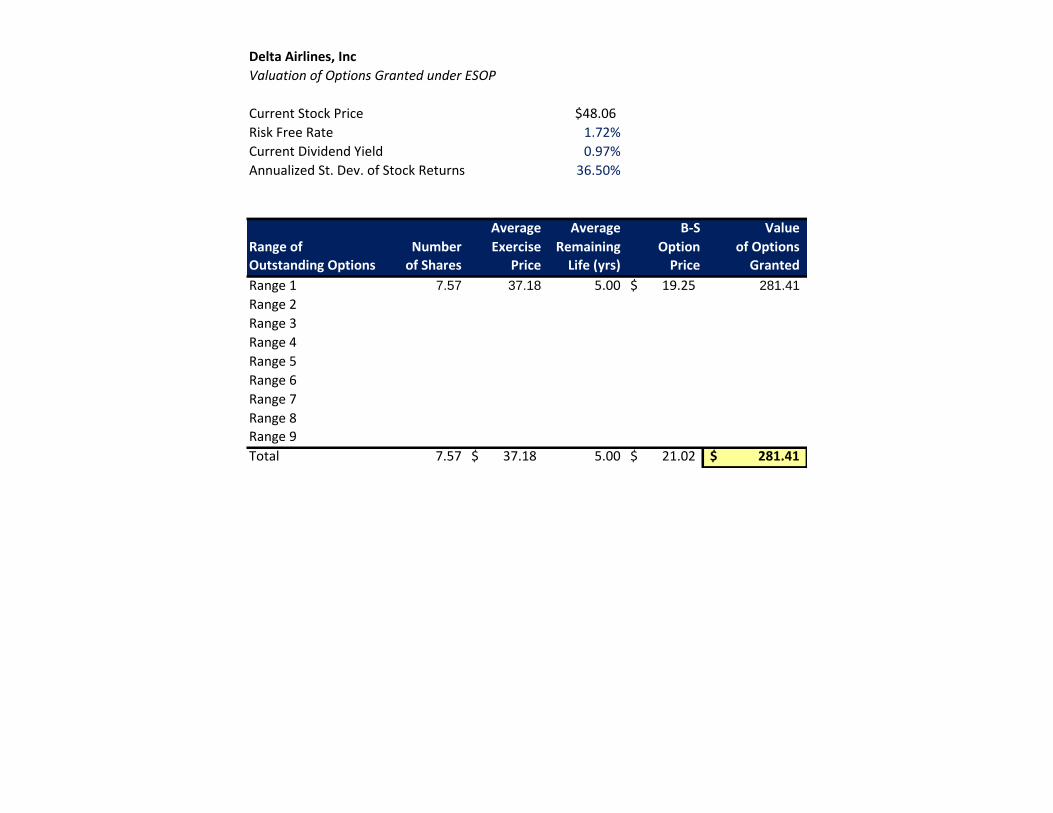

ESOP 281.41

Value of Equity 25,252

Shares Outstanding 639

Intrinsic Value of Last FYE 39.55

Implied Price as of Today 40.05

EP Model:

Economic Profit (EP) 4,250 3,820 3,814 3,901 3,991

Continuing Value (CV) 55,779

PV of EP 3,875 3,175 2,890 2,695 38,536

Total PV of EP 52,171

Invested Capital (last FYE) 19,218

Value of Operating Assets 71,389

Non-Operating Adjustments:

Equity investments 1,843

Short-term investments 447

Cash restricted for airport construction 2,103

Goodwill 10,261

Identifiable intangibles 5,953

Pension, postretirement, and related benefits11,556

Current maturities of long term debt and finance leases2,135

Debt and finance leases 11,557

ESOP 281.41

Value of Equity 25,252

Shares Outstanding 639

Intrinsic Value of Last FYE 39.55

Implied Price as of Today 40.05

Delta Airlines, Inc

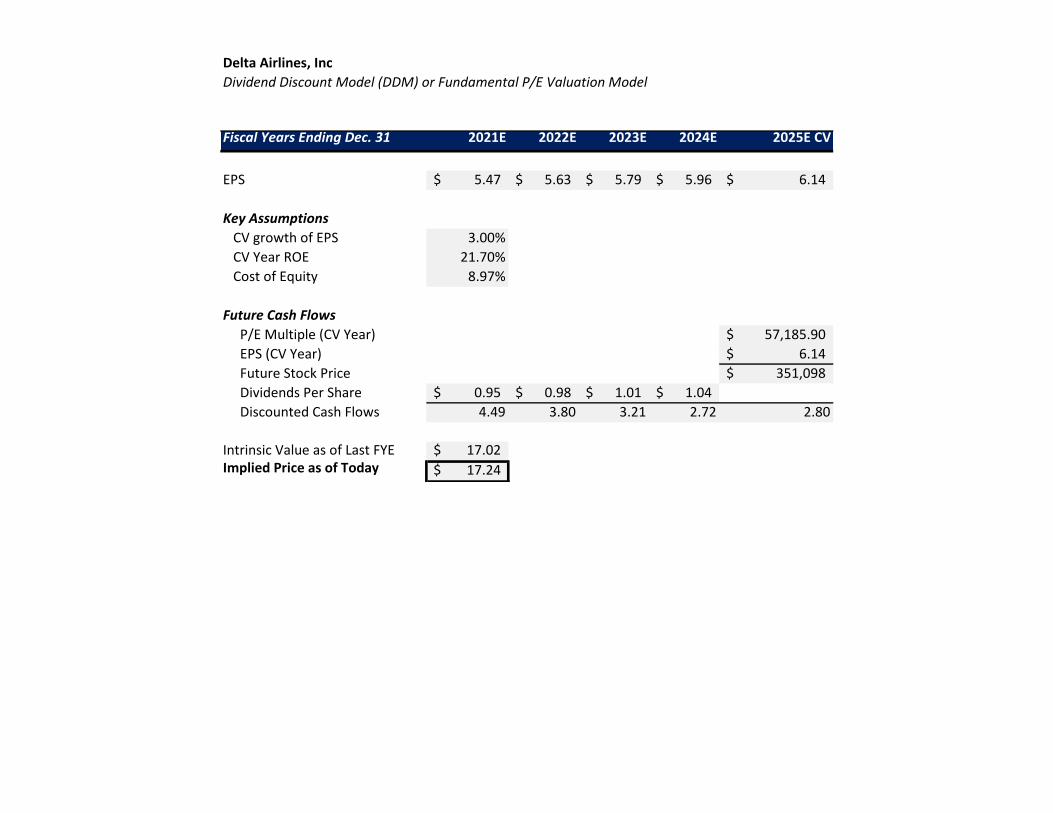

Dividend Discount Model (DDM) or Fundamental P/E Valuation Model

Fiscal Years Ending Dec. 31 2021E 2022E 2023E 2024E 2025E CV

EPS 5.47$ 5.63$ 5.79$ 5.96$ 6.14$

Key Assumptions

CV growth of EPS 3.00%

CV Year ROE 21.70%

Cost of Equity 8.97%

Future Cash Flows

P/E Multiple (CV Year) 57,185.90$

EPS (CV Year) 6.14$

Future Stock Price 351,098$

Dividends Per Share 0.95$ 0.98$ 1.01$ 1.04$

Discounted Cash Flows 4.49 3.80 3.21 2.72 2.80

Intrinsic Value as of Last FYE 17.02$ Implied Price as of Today 17.24$

Delta Airlines, Inc

Value Driver Estimation

Fiscal Years Ending Dec. 31 2018 2019 2020 2021E 2022E 2023E 2024E 2025E CV

NOPLAT:

Operating income 5,264 6,618 (12,469) 3,888 4,015 4,141 4,275 4,414

Operating lease interest 1,043 628 615 603 665 686 708 731 EBITA 6,307 7,246 (11,854) 4,491 4,680 4,827 4,983 5,145

Less: Adjusted Taxes:

Tax shield on interest expense (71) (69) (213) (175) (181) (186) (192) (199)

Tax shield on amortization of debt discount, net - - - (22) (23) (23) (24) (25)

Tax shield on loss on extinguishment of debt - - - (18) (18) (19) (19) (20)

Tax shield on impairments and equity losses (14) (14) (557) (3) (3) (3) (3) (3)

Tax shield on loss from investment - - (24) (3) (3) (3) (3) (3)

Tax on gains from investment 9 27 - - - - - -

Tax shield on miscellaneous, net 50 (40) 80 (20) (21) (22) (22) (23) Total Adjusted Taxes (127) (16) (825) (240) (248) (256) (264) (273)

Plus: Change in deferred taxes - 1,456 (1,456) 188 6 6 6 7 NOPLAT 6,434 8,717 (12,485) 4,919 4,934 5,089 5,254 5,424

Invested Capital (IC):

Operating Current Assets:

Normal cash 1,565 1,655 602 1,708 1,763 1,819 1,878 1,939

Accounts receivable 2,314 2,854 1,396 2,963 3,057 3,155 3,257 3,363

Fuel Inventory 592 730 377 803 829 855 883 912

Prepaid expenses 1,203 1,262 1,180 1,232 1,272 1,312 1,355 1,399

Expendable parts and supplies inventories 463 521 355 473 488 504 520 537

Total Operating Current Assets 6,137 7,022 3,910 7,179 7,408 7,646 7,893 8,149

Non Interest-Bearing Current Liabilities

Accounts payable 2,976 3,266 2,840 2,689 2,791 2,896 3,006 3,120

Air traffic liability 4,661 5,116 4,044 4,270 4,438 4,613 4,794 4,982

Accrued expenses 3,287 3,701 2,086 2,474 2,569 2,668 2,770 2,876

Deferred revenue 2,989 3,219 1,777 2,436 2,513 2,594 2,678 2,765

Income taxes payable - - - - - - - -

Fuel card obligation 1,075 736 1,100 456 471 486 502 518

Current maturities of operating leases 955 801 678 632 652 673 695 717

Noncurrent operating leases 5,801 5,294 5,713 1,948 2,042 2,140 2,241 2,347

Other accrued liabilities 1,117 1,078 1,670 1,618 1,670 1,723 1,779 1,837

Total Current Liabilities 22,861 23,211 19,908 16,523 17,146 17,793 18,464 19,161

Plus: Net PPE 28,335 31,310 26,529 29,248 30,182 31,151 32,157 33,201

Plus: Net Other Operating Assets

Capitalized PV of operating leases 4,687 4,589 4,502 4,964 5,122 5,286 5,457 5,634

Operating lease right-of-use assets 5,994 5,627 5,733 5,174 5,371 5,575 5,788 6,008

Other noncurrent assets 3,608 1,078 1,357 2,005 2,069 2,136 2,205 2,276

Net Other Operating Assets 14,289 11,294 11,592 12,142 12,562 12,997 13,449 13,919

Less: Other Operating Liabilities

Deferred revenue 3,652 3,509 5,405 2,707 2,809 2,916 3,026 3,141

Noncurrent air traffic liability - - 500 - - - - -

Other noncurrent liabilities 1,132 1,386 4,862 1,393 1,460 2,230 1,602 1,676

Net Other Operating Liabilites 3,652 3,509 5,905 2,707 2,809 2,916 3,026 3,141

Total Invested Capital (IC) 22,248 22,907 19,218 24,340 26,196 27,086 28,009 28,967

Free Cash Flow (FCF):

NOPLAT 6,434 8,717 (12,485) 4,919 4,934 5,089 5,254 5,424

Change in IC (3,444) 659 (3,689) 5,122 1,857 889 923 958

FCF 2,990 9,376 (16,174) 10,041 6,791 5,979 6,177 6,383

Return on Invested Capital (ROIC):

NOPLAT 6,434 8,717 (12,485) 4,919 4,934 5,089 5,254 5,424

Beginning IC 25,691 22,248 22,907 19,218 24,340 26,196 27,086 28,009

ROIC 25.04% 39.18% -54.50% 26.60% 21.27% 20.43% 20.40% 20.37%

Economic Profit (EP):

Beginning IC 25,691 22,248 22,907 19,218 24,340 26,196 27,086 28,009

x (ROIC - WACC) 15.36% 29.50% -64.19% 16.91% 11.58% 10.74% 10.71% 10.68%

EP 3,945 6,562 (14,704) 4,250 3,820 3,814 3,901 3,991

Delta Airlines, Inc

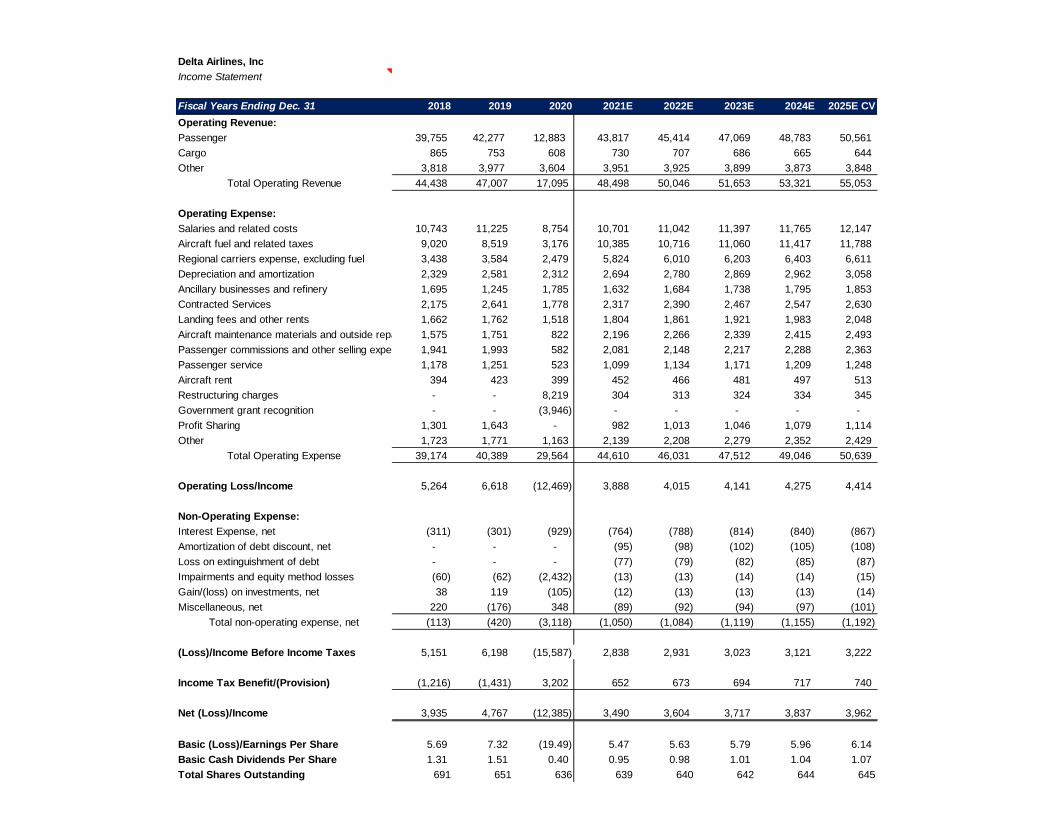

Income Statement

Fiscal Years Ending Dec. 31 2018 2019 2020 2021E 2022E 2023E 2024E 2025E CV

Operating Revenue:

Passenger 39,755 42,277 12,883 43,817 45,414 47,069 48,783 50,561

Cargo 865 753 608 730 707 686 665 644

Other 3,818 3,977 3,604 3,951 3,925 3,899 3,873 3,848

Total Operating Revenue 44,438 47,007 17,095 48,498 50,046 51,653 53,321 55,053

Operating Expense:

Salaries and related costs 10,743 11,225 8,754 10,701 11,042 11,397 11,765 12,147

Aircraft fuel and related taxes 9,020 8,519 3,176 10,385 10,716 11,060 11,417 11,788

Regional carriers expense, excluding fuel 3,438 3,584 2,479 5,824 6,010 6,203 6,403 6,611

Depreciation and amortization 2,329 2,581 2,312 2,694 2,780 2,869 2,962 3,058

Ancillary businesses and refinery 1,695 1,245 1,785 1,632 1,684 1,738 1,795 1,853

Contracted Services 2,175 2,641 1,778 2,317 2,390 2,467 2,547 2,630

Landing fees and other rents 1,662 1,762 1,518 1,804 1,861 1,921 1,983 2,048

Aircraft maintenance materials and outside repairs 1,575 1,751 822 2,196 2,266 2,339 2,415 2,493

Passenger commissions and other selling expenses 1,941 1,993 582 2,081 2,148 2,217 2,288 2,363

Passenger service 1,178 1,251 523 1,099 1,134 1,171 1,209 1,248

Aircraft rent 394 423 399 452 466 481 497 513

Restructuring charges - - 8,219 304 313 324 334 345

Government grant recognition - - (3,946) - - - - -

Profit Sharing 1,301 1,643 - 982 1,013 1,046 1,079 1,114

Other 1,723 1,771 1,163 2,139 2,208 2,279 2,352 2,429

Total Operating Expense 39,174 40,389 29,564 44,610 46,031 47,512 49,046 50,639

Operating Loss/Income 5,264 6,618 (12,469) 3,888 4,015 4,141 4,275 4,414

Non-Operating Expense:

Interest Expense, net (311) (301) (929) (764) (788) (814) (840) (867)

Amortization of debt discount, net - - - (95) (98) (102) (105) (108)

Loss on extinguishment of debt - - - (77) (79) (82) (85) (87)

Impairments and equity method losses (60) (62) (2,432) (13) (13) (14) (14) (15)

Gain/(loss) on investments, net 38 119 (105) (12) (13) (13) (13) (14)

Miscellaneous, net 220 (176) 348 (89) (92) (94) (97) (101)

Total non-operating expense, net (113) (420) (3,118) (1,050) (1,084) (1,119) (1,155) (1,192)

(Loss)/Income Before Income Taxes 5,151 6,198 (15,587) 2,838 2,931 3,023 3,121 3,222

Income Tax Benefit/(Provision) (1,216) (1,431) 3,202 652 673 694 717 740

Net (Loss)/Income 3,935 4,767 (12,385) 3,490 3,604 3,717 3,837 3,962

Basic (Loss)/Earnings Per Share 5.69 7.32 (19.49) 5.47 5.63 5.79 5.96 6.14

Basic Cash Dividends Per Share 1.31 1.51 0.40 0.95 0.98 1.01 1.04 1.07

Total Shares Outstanding 691 651 636 639 640 642 644 645

Delta Airlines, Inc

Balance Sheet

Fiscal Years Ending Dec. 31 2018 2019 2020 2021E 2022E 2023E 2024E 2025E CV

Assets

Current Assets:

Cash and cash equivalents 1,565 2,882 8,307 2,509 2,589 2,672 2,758 2,848

Short-term investments 203 - 5,789 447 461 476 491 507

Restricted cash - - - - - - - -

Accounts receivable 2,314 2,854 1,396 2,963 3,057 3,155 3,257 3,363

Fuel Inventory 592 730 377 803 829 855 883 912

Expendable parts and supplies inventories 463 521 355 473 488 504 520 537

Prepaid expenses and other 1,203 1,262 1,180 1,232 1,272 1,312 1,355 1,399

Hedge Derivative Asset - - - - - - - -

Hedge Margin Receivable - - - - - - - -

Total current assets 6,340 8,249 17,404 8,427 8,696 8,975 9,265 9,566

Noncurrent Assets

Property, plant, and equipment 28,335 31,310 26,529 29,248 30,182 31,151 32,157 33,201

Operating lease right-of-use assets 5,994 5,627 5,733 5,174 5,371 5,575 5,788 6,008

Goodwill 9,781 9,781 9,753 10,261 11,104 11,461 11,831 12,215

Identifiable intangibles 4,830 5,163 6,011 5,453 6,143 6,340 6,545 6,758

Cash restricted for airport construction 1,136 636 1,556 2,103 2,171 2,240 2,313 2,388

Equity investments - 2,568 1,665 1,843 1,902 1,963 2,027 2,092

Deferred income taxes, net 242 120 1,988 2,676 2,762 2,850 2,942 3,038

Other noncurrent assets 3,608 1,078 1,357 2,005 2,069 2,136 2,205 2,276

Total noncurrent assets 53,926 56,283 54,592 58,764 61,703 63,717 65,807 67,976

Total Assets 60,266 64,532 71,996 69,190 71,399 73,692 76,072 78,542

Liabilities and Stockholders' Equity

Current Liabilities:

Current maturities of long term debt and finance leases 1,518 2,287 1,732 1,937 1,999 2,063 2,130 2,199

Current maturities of operating leases 955 801 678 632 652 673 695 717

Air traffic liability 4,661 5,116 4,044 4,270 4,438 4,613 4,794 4,982

Accounts payable 2,976 3,266 2,840 2,689 2,791 2,896 3,006 3,120

Accrued Salaries and related benefits 3,287 3,701 2,086 2,474 2,569 2,668 2,770 2,876

Loyalty program deferred revenue 2,989 3,219 1,777 2,436 2,513 2,594 2,678 2,765

Taxes Payable - - - - - - - -

Fuel card obligation 1,075 736 1,100 456 471 486 502 518

Hedge Derivative Liability - - - - - - - -

Other accrued liabilities 1,117 1,078 1,670 1,618 1,670 1,723 1,779 1,837

Total current liabilities 18,578 20,204 15,927 16,512 17,103 17,716 18,353 19,014

Noncurrent Liabilities: -

Debt and finance leases 8,253 8,873 27,425 9,605 9,943 10,295 10,659 11,038

Noncurrent air traffic liability - - 500 - - - - -

Pension, postretirement, and related benefits 9,163 8,452 10,630 11,556 12,053 12,568 13,104 13,659

Loyalty program deferred revenue 3,652 3,509 5,405 2,707 2,809 2,916 3,026 3,141

Noncurrent operating leases 5,801 5,294 5,713 1,948 2,042 2,140 2,241 2,347

Deferred Income taxes, net - 1,456 - 188 194 200 206 213

Other noncurrent liabilities 1,132 1,386 4,862 1,393 1,460 2,230 1,602 1,676

Total noncurrent liabilities 28,001 28,970 54,535 27,398 28,502 30,348 30,839 32,074

Commitments and Contingencies

Stockholders' Equity:

Common stock at par value - - - - - - - -

Additional paid-in-capital 11,671 11,129 11,259 14,628 15,095 15,580 16,083 16,605

Retained earnings (deficit) 10,039 12,454 (428) 10,287 10,616 10,956 11,310 11,678

Accumulated comprehensive loss (7,825) (7,989) (9,038) (8,528) (8,800) (9,083) (9,376) (9,680)

Treasury stock (198) (236) (259) (306) (316) (326) (337) (348)

Total stockholders' equity 13,687 15,358 1,534 16,081 16,594 17,127 17,680 18,254

Total liabilities and stockholders' equity 60,266 64,532 71,996 69,190 71,399 73,692 76,072 78,542

Delta Airlines, Inc

Forecasted Cash Flow Statement

Source: FactSetFiscal Years Ending Dec. 31 2021E 2022E 2023E 2024E 2025E CV

Net Income 3,490 3,604 3,717 3,837 3,962

Adjustments to reconcile net income to cash from operating activities:

Depreciation and amortization 2,694 2,780 2,869 2,962 3,058

Changes in working capital accounts:

Restricted cash - - - - -

Accounts receivable (1,567) (95) (98) (102) (106)

Fuel inventory (426) (26) (27) (28) (29)

Expendable parts and supplies inventory (118) (15) (16) (16) (17)

Prepaid expenses and other (52) (39) (41) (42) (44)

Pension, postretirement, and related benefits (926) (497) (515) (535) (555)

Air traffic liability 226 168 175 181 188

Accounts payable (151) 102 106 110 114

Accrued Salaries and related benefits 388 95 99 102 106

Loyalty program deferred revenue 659 78 81 84 87

Taxes Payable - - - - -

Fuel card obligation (644) 15 15 16 16

Non current air traffic liability (500) - - - -

Deferred taxes (188) (6) (6) (6) (7)

Noncurrent operating leases 3,765 (94) (98) (101) (105)

Current maturities of operating leases (46) 20 21 22 23

Other accrued liabilities (52) 52 54 56 58

Net cash from operating activities 6,551 6,142 6,335 6,538 6,749

Change in cash from investing activities:

Change in short-term investments 5,342 (14) (15) (15) (16)

Capital expenditures (change in gross ppe) (25) 1,846 1,900 1,956 2,014

Capitalization of intangible assets 558 (690) (197) (205) (213)

Business acquisitions (change in goodwill) (508) (843) (357) (370) (384)

Long-term loyalty program deferred revenue (2,698) 102 106 110 115

Other noncurrent assets (648) (64) (66) (69) (72)

Other noncurrent liabilities (3,469) 67 769 (628) 75

Net cash from investing activities (1,448) 404 2,141 779 1,519

Cash from financing activities:

Hedge derivative asset - - - - -

Hedge margin receivable - - - - -

Common stock at par value - - - - -

Additional paid-in-capital (3,369) (467) (485) (503) (522)

Retained earnings (deficit) 10,715 328 341 354 367

Accumulated comprehensive loss 510 (272) (283) (293) (304)

Treasury stock (47) (10) (10) (11) (11)

Hedge Derivative Liability - - - - -

Equity investments (178) (59) (61) (63) (66)

Current maturities of long term debt and finance leases 205 62 64 67 69

Net cash from financing activities 7,836 (418) (433) (450) (467)

Increase/decrease in cash/cash equivalents 12,939 6,128 8,042 6,867 7,801

Cash/cash equivalents beginning of the year 8,307 2,509 2,589 2,672 2,758

End of the year cash balance 21,246 8,637 10,631 9,539 10,559

Delta Airlines, Inc

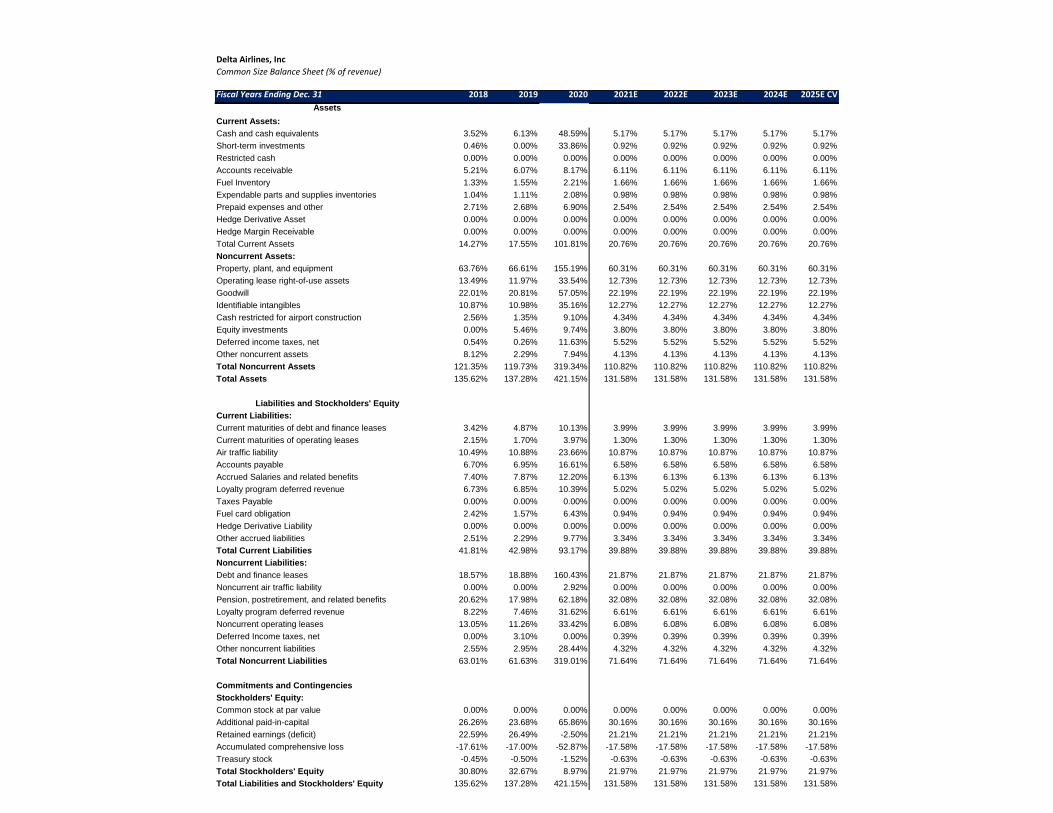

Common Size Balance Sheet (% of revenue)

Fiscal Years Ending Dec. 31 2018 2019 2020 2021E 2022E 2023E 2024E 2025E CV

Assets

Current Assets:

Cash and cash equivalents 3.52% 6.13% 48.59% 5.17% 5.17% 5.17% 5.17% 5.17%

Short-term investments 0.46% 0.00% 33.86% 0.92% 0.92% 0.92% 0.92% 0.92%

Restricted cash 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00%

Accounts receivable 5.21% 6.07% 8.17% 6.11% 6.11% 6.11% 6.11% 6.11%

Fuel Inventory 1.33% 1.55% 2.21% 1.66% 1.66% 1.66% 1.66% 1.66%

Expendable parts and supplies inventories 1.04% 1.11% 2.08% 0.98% 0.98% 0.98% 0.98% 0.98%

Prepaid expenses and other 2.71% 2.68% 6.90% 2.54% 2.54% 2.54% 2.54% 2.54%

Hedge Derivative Asset 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00%

Hedge Margin Receivable 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00%

Total Current Assets 14.27% 17.55% 101.81% 20.76% 20.76% 20.76% 20.76% 20.76%

Noncurrent Assets:

Property, plant, and equipment 63.76% 66.61% 155.19% 60.31% 60.31% 60.31% 60.31% 60.31%

Operating lease right-of-use assets 13.49% 11.97% 33.54% 12.73% 12.73% 12.73% 12.73% 12.73%

Goodwill 22.01% 20.81% 57.05% 22.19% 22.19% 22.19% 22.19% 22.19%

Identifiable intangibles 10.87% 10.98% 35.16% 12.27% 12.27% 12.27% 12.27% 12.27%

Cash restricted for airport construction 2.56% 1.35% 9.10% 4.34% 4.34% 4.34% 4.34% 4.34%

Equity investments 0.00% 5.46% 9.74% 3.80% 3.80% 3.80% 3.80% 3.80%

Deferred income taxes, net 0.54% 0.26% 11.63% 5.52% 5.52% 5.52% 5.52% 5.52%

Other noncurrent assets 8.12% 2.29% 7.94% 4.13% 4.13% 4.13% 4.13% 4.13%

Total Noncurrent Assets 121.35% 119.73% 319.34% 110.82% 110.82% 110.82% 110.82% 110.82%

Total Assets 135.62% 137.28% 421.15% 131.58% 131.58% 131.58% 131.58% 131.58%

Liabilities and Stockholders' Equity

Current Liabilities:

Current maturities of debt and finance leases 3.42% 4.87% 10.13% 3.99% 3.99% 3.99% 3.99% 3.99%

Current maturities of operating leases 2.15% 1.70% 3.97% 1.30% 1.30% 1.30% 1.30% 1.30%

Air traffic liability 10.49% 10.88% 23.66% 10.87% 10.87% 10.87% 10.87% 10.87%

Accounts payable 6.70% 6.95% 16.61% 6.58% 6.58% 6.58% 6.58% 6.58%

Accrued Salaries and related benefits 7.40% 7.87% 12.20% 6.13% 6.13% 6.13% 6.13% 6.13%

Loyalty program deferred revenue 6.73% 6.85% 10.39% 5.02% 5.02% 5.02% 5.02% 5.02%

Taxes Payable 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00%

Fuel card obligation 2.42% 1.57% 6.43% 0.94% 0.94% 0.94% 0.94% 0.94%

Hedge Derivative Liability 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00%

Other accrued liabilities 2.51% 2.29% 9.77% 3.34% 3.34% 3.34% 3.34% 3.34%

Total Current Liabilities 41.81% 42.98% 93.17% 39.88% 39.88% 39.88% 39.88% 39.88%

Noncurrent Liabilities:

Debt and finance leases 18.57% 18.88% 160.43% 21.87% 21.87% 21.87% 21.87% 21.87%

Noncurrent air traffic liability 0.00% 0.00% 2.92% 0.00% 0.00% 0.00% 0.00% 0.00%

Pension, postretirement, and related benefits 20.62% 17.98% 62.18% 32.08% 32.08% 32.08% 32.08% 32.08%

Loyalty program deferred revenue 8.22% 7.46% 31.62% 6.61% 6.61% 6.61% 6.61% 6.61%

Noncurrent operating leases 13.05% 11.26% 33.42% 6.08% 6.08% 6.08% 6.08% 6.08%

Deferred Income taxes, net 0.00% 3.10% 0.00% 0.39% 0.39% 0.39% 0.39% 0.39%

Other noncurrent liabilities 2.55% 2.95% 28.44% 4.32% 4.32% 4.32% 4.32% 4.32%

Total Noncurrent Liabilities 63.01% 61.63% 319.01% 71.64% 71.64% 71.64% 71.64% 71.64%

Commitments and Contingencies

Stockholders' Equity:

Common stock at par value 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00%

Additional paid-in-capital 26.26% 23.68% 65.86% 30.16% 30.16% 30.16% 30.16% 30.16%

Retained earnings (deficit) 22.59% 26.49% -2.50% 21.21% 21.21% 21.21% 21.21% 21.21%

Accumulated comprehensive loss -17.61% -17.00% -52.87% -17.58% -17.58% -17.58% -17.58% -17.58%

Treasury stock -0.45% -0.50% -1.52% -0.63% -0.63% -0.63% -0.63% -0.63%

Total Stockholders' Equity 30.80% 32.67% 8.97% 21.97% 21.97% 21.97% 21.97% 21.97%

Total Liabilities and Stockholders' Equity 135.62% 137.28% 421.15% 131.58% 131.58% 131.58% 131.58% 131.58%

Delta Airlines, Inc

Common Size Income Statement

Fiscal Years Ending Dec. 31 2018 2019 2020 2021E 2022E 2023E 2024E 2025E CV

Operating Revenue:

Passenger 89.46% 89.94% 75.36% 90.35% 90.74% 91.12% 91.49% 91.84%

Cargo 1.95% 1.60% 3.56% 1.50% 1.41% 1.33% 1.25% 1.17%

Other 8.59% 8.46% 21.08% 8.15% 7.84% 7.55% 7.26% 6.99%

Total Operating Revenue 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00%

Operating Expense:

Salaries and related costs 24.18% 23.88% 51.21% 21.26% 21.26% 21.26% 21.26% 0.00%

Aircraft fuel and related taxes 20.30% 18.12% 18.58% 21.41% 21.41% 21.41% 21.41% 21.41%

Regional carriers expense, excluding fuel 7.74% 7.62% 14.50% 12.01% 12.01% 12.01% 12.01% 12.01%

Depreciation and amortization 5.24% 5.49% 13.52% 5.55% 5.55% 5.55% 5.55% 5.55%

Ancillary businesses and refinery 3.81% 2.65% 10.44% 3.37% 3.37% 3.37% 3.37% 3.37%

Contracted Services 4.89% 5.62% 10.40% 4.78% 4.78% 4.78% 4.78% 4.78%

Landing fees and other rents 3.74% 3.75% 8.88% 3.72% 3.72% 3.72% 3.72% 3.72%

Aircraft maintenance materials and outside repairs 3.54% 3.72% 4.81% 4.53% 4.53% 4.53% 4.53% 4.53%

Passenger commissions and other selling expenses 4.37% 4.24% 3.40% 4.29% 4.29% 4.29% 4.29% 4.29%

Passenger service 2.65% 2.66% 3.06% 2.27% 2.27% 2.27% 2.27% 2.27%

Aircraft rent 0.89% 0.90% 2.33% 0.93% 0.93% 0.93% 0.93% 0.93%

Restructuring charges 0.00% 0.00% 48.08% 0.63% 0.63% 0.63% 0.63% 0.63%

Government grant recognition 0.00% 0.00% -23.08% 0.00% 0.00% 0.00% 0.00% 0.00%

Profit Sharing 2.93% 3.50% 0.00% 2.02% 2.02% 2.02% 2.02% 2.02%

Other 3.88% 3.77% 6.80% 4.41% 4.41% 4.41% 4.41% 4.41%

Total Operating Expense 88.15% 85.92% 172.94% 89.01% 89.01% 89.01% 89.01% 89.01%

Operating Loss/Income 11.85% 14.08% -72.94% 11.01% 11.01% 11.01% 11.01% 11.01%

Non-Operating Expense: 0.00% 0.00% 0.00%

Interest Expense, net -0.70% -0.64% -5.43% -1.58% -1.58% -1.58% -1.58% -1.58%

Amortization of debt discount, net 0.00% 0.00% 0.00% -0.20% -0.20% -0.20% -0.20% -0.20%

Loss on extinguishment of debt 0.00% 0.00% 0.00% -0.16% -0.16% -0.16% -0.16% -0.16%

Impairments and equity method losses -0.14% -0.13% -14.23% -0.03% -0.03% -0.03% -0.03% -0.03%

Gain/(loss) on investments, net 0.09% 0.25% -0.61% -0.03% -0.03% -0.03% -0.03% -0.03%

Miscellaneous, net 0.50% -0.37% 2.04% -0.18% -0.18% -0.18% -0.18% -0.18%

Total non-operating expense, net -0.25% -0.89% -18.24% -3.56% -3.56% -3.56% -3.56% -3.56%

(Loss)/Income Before Income Taxes 11.59% 13.19% -91.18% 8.87% 8.87% 8.87% 8.87% 8.87%

Income Tax Benefit/(Provision) -2.74% -3.04% 18.73% 1.34% 1.34% 1.34% 1.34% 1.34%

Net (Loss)/Income 8.86% 10.14% -72.45% 8.55% 8.55% 8.55% 8.55% 8.55%

Delta Airlines, Inc

Weighted Average Cost of Capital (WACC) Estimation

Cost of Equity: ASSUMPTIONS:

Risk-Free Rate 1.72% *Current risk-free rate on 10-year treasury bond

Beta 1.45 *Average beta

Equity Risk Premium 5.00% *Average equity risk premium on 10-year treasury

Cost of Equity 8.97%

Cost of Debt:

Risk-Free Rate 1.72% *Current risk-free rate on 10-year treasury bond

Implied Default Premium 11.67%

Pre-Tax Cost of Debt 13.39% *Yield to maturity on 10-year corporate bond

Marginal Tax Rate 22.90%

After-Tax Cost of Debt 10.32%

Market Value of Common Equity: MV Weights

Total Shares Outstanding 636

Current Stock Price $48.06

MV of Equity 30,566.16 47.09%

Market Value of Debt:

Short-Term Debt 678

Current Portion of LTD 1732

Long-Term Debt 27,425

PV of Operating Leases 4,502

MV of Total Debt 34,337.07 52.91%

Market Value of the Firm 64,903.23 100.00%

Estimated WACC 9.69%

Delta Airlines, Inc

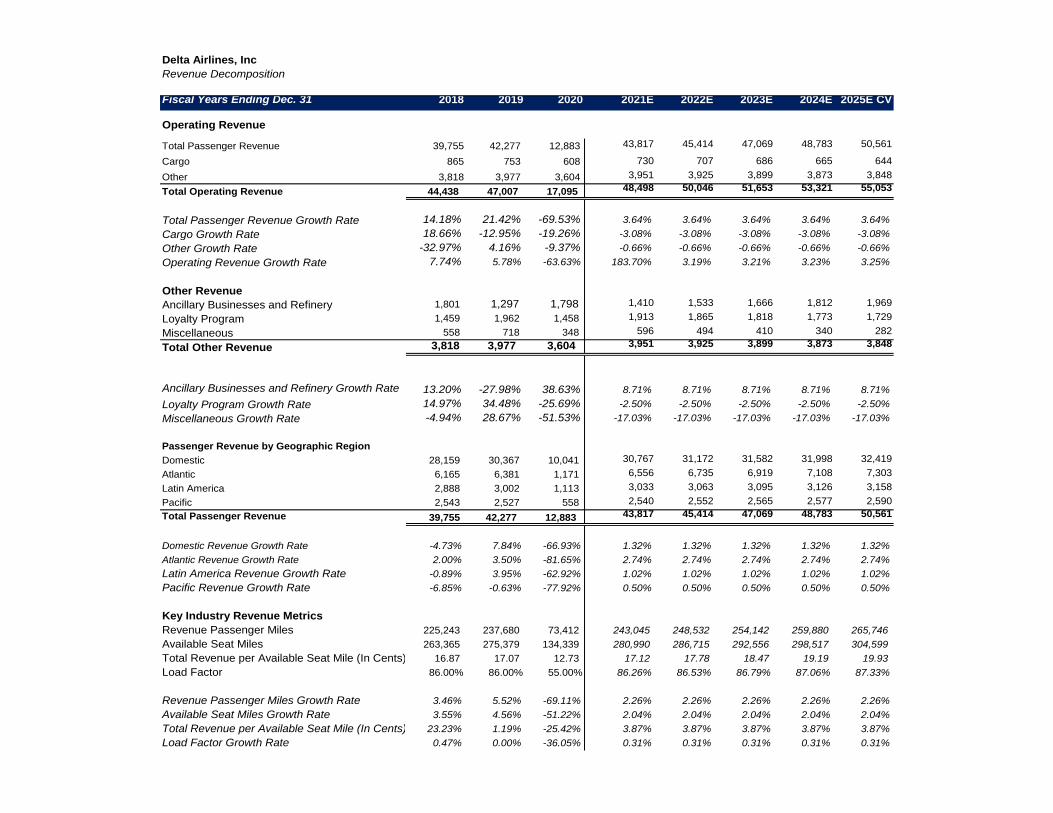

Revenue Decomposition

Fiscal Years Ending Dec. 31 2018 2019 2020 2021E 2022E 2023E 2024E 2025E CV

Operating Revenue

Total Passenger Revenue 39,755 42,277 12,883 43,817 45,414 47,069 48,783 50,561

Cargo 865 753 608 730 707 686 665 644

Other 3,818 3,977 3,604 3,951 3,925 3,899 3,873 3,848

Total Operating Revenue 44,438 47,007 17,095 48,498 50,046 51,653 53,321 55,053

Total Passenger Revenue Growth Rate 14.18% 21.42% -69.53% 3.64% 3.64% 3.64% 3.64% 3.64%

Cargo Growth Rate 18.66% -12.95% -19.26% -3.08% -3.08% -3.08% -3.08% -3.08%

Other Growth Rate -32.97% 4.16% -9.37% -0.66% -0.66% -0.66% -0.66% -0.66%

Operating Revenue Growth Rate 7.74% 5.78% -63.63% 183.70% 3.19% 3.21% 3.23% 3.25%

Other Revenue

Ancillary Businesses and Refinery 1,801 1,297 1,798 1,410 1,533 1,666 1,812 1,969

Loyalty Program 1,459 1,962 1,458 1,913 1,865 1,818 1,773 1,729

Miscellaneous 558 718 348 596 494 410 340 282

Total Other Revenue 3,818 3,977 3,604 3,951 3,925 3,899 3,873 3,848

Ancillary Businesses and Refinery Growth Rate 13.20% -27.98% 38.63% 8.71% 8.71% 8.71% 8.71% 8.71%

Loyalty Program Growth Rate 14.97% 34.48% -25.69% -2.50% -2.50% -2.50% -2.50% -2.50%

Miscellaneous Growth Rate -4.94% 28.67% -51.53% -17.03% -17.03% -17.03% -17.03% -17.03%

Passenger Revenue by Geographic Region

Domestic 28,159 30,367 10,041 30,767 31,172 31,582 31,998 32,419

Atlantic 6,165 6,381 1,171 6,556 6,735 6,919 7,108 7,303

Latin America 2,888 3,002 1,113 3,033 3,063 3,095 3,126 3,158

Pacific 2,543 2,527 558 2,540 2,552 2,565 2,577 2,590

Total Passenger Revenue 39,755 42,277 12,883 43,817 45,414 47,069 48,783 50,561

Domestic Revenue Growth Rate -4.73% 7.84% -66.93% 1.32% 1.32% 1.32% 1.32% 1.32%

Atlantic Revenue Growth Rate 2.00% 3.50% -81.65% 2.74% 2.74% 2.74% 2.74% 2.74%

Latin America Revenue Growth Rate -0.89% 3.95% -62.92% 1.02% 1.02% 1.02% 1.02% 1.02%

Pacific Revenue Growth Rate -6.85% -0.63% -77.92% 0.50% 0.50% 0.50% 0.50% 0.50%

Key Industry Revenue Metrics

Revenue Passenger Miles 225,243 237,680 73,412 243,045 248,532 254,142 259,880 265,746

Available Seat Miles 263,365 275,379 134,339 280,990 286,715 292,556 298,517 304,599

Total Revenue per Available Seat Mile (In Cents) 16.87 17.07 12.73 17.12 17.78 18.47 19.19 19.93

Load Factor 86.00% 86.00% 55.00% 86.26% 86.53% 86.79% 87.06% 87.33%

Revenue Passenger Miles Growth Rate 3.46% 5.52% -69.11% 2.26% 2.26% 2.26% 2.26% 2.26%

Available Seat Miles Growth Rate 3.55% 4.56% -51.22% 2.04% 2.04% 2.04% 2.04% 2.04%

Total Revenue per Available Seat Mile (In Cents) Growth Rate23.23% 1.19% -25.42% 3.87% 3.87% 3.87% 3.87% 3.87%

Load Factor Growth Rate 0.47% 0.00% -36.05% 0.31% 0.31% 0.31% 0.31% 0.31%

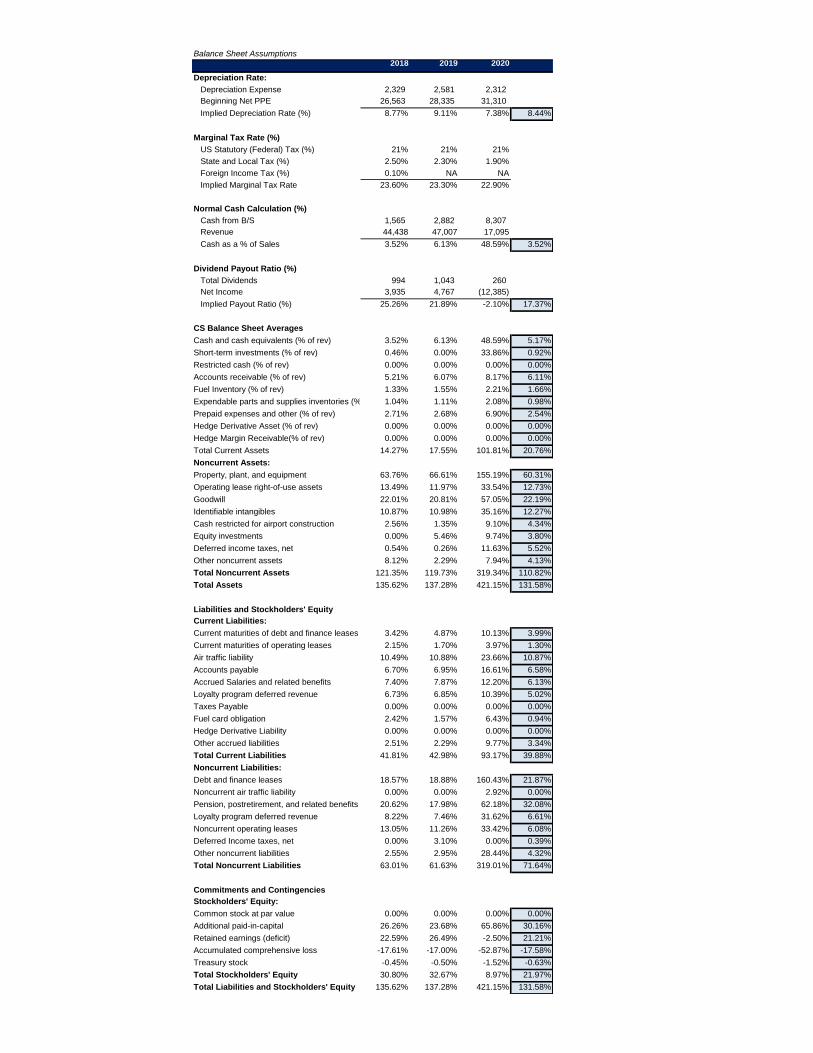

Balance Sheet Assumptions2018 2019 2020

Depreciation Rate:

Depreciation Expense 2,329 2,581 2,312

Beginning Net PPE 26,563 28,335 31,310

Implied Depreciation Rate (%) 8.77% 9.11% 7.38% 8.44%

Marginal Tax Rate (%)

US Statutory (Federal) Tax (%) 21% 21% 21%

State and Local Tax (%) 2.50% 2.30% 1.90%

Foreign Income Tax (%) 0.10% NA NA

Implied Marginal Tax Rate 23.60% 23.30% 22.90%

Normal Cash Calculation (%)

Cash from B/S 1,565 2,882 8,307

Revenue 44,438 47,007 17,095

Cash as a % of Sales 3.52% 6.13% 48.59% 3.52%

Dividend Payout Ratio (%)

Total Dividends 994 1,043 260

Net Income 3,935 4,767 (12,385)

Implied Payout Ratio (%) 25.26% 21.89% -2.10% 17.37%

CS Balance Sheet Averages

3.52% 6.13% 48.59% 5.17%

Short-term investments (% of rev) 0.46% 0.00% 33.86% 0.92%

Restricted cash (% of rev) 0.00% 0.00% 0.00% 0.00%

Accounts receivable (% of rev) 5.21% 6.07% 8.17% 6.11%

Fuel Inventory (% of rev) 1.33% 1.55% 2.21% 1.66%

Expendable parts and supplies inventories (% of rev)1.04% 1.11% 2.08% 0.98%

Prepaid expenses and other (% of rev) 2.71% 2.68% 6.90% 2.54%

Hedge Derivative Asset (% of rev) 0.00% 0.00% 0.00% 0.00%

Hedge Margin Receivable(% of rev) 0.00% 0.00% 0.00% 0.00%

Total Current Assets 14.27% 17.55% 101.81% 20.76%

Noncurrent Assets:

Property, plant, and equipment 63.76% 66.61% 155.19% 60.31%

Operating lease right-of-use assets 13.49% 11.97% 33.54% 12.73%

Goodwill 22.01% 20.81% 57.05% 22.19%

Identifiable intangibles 10.87% 10.98% 35.16% 12.27%

Cash restricted for airport construction 2.56% 1.35% 9.10% 4.34%

Equity investments 0.00% 5.46% 9.74% 3.80%

Deferred income taxes, net 0.54% 0.26% 11.63% 5.52%

Other noncurrent assets 8.12% 2.29% 7.94% 4.13%

Total Noncurrent Assets 121.35% 119.73% 319.34% 110.82%

Total Assets 135.62% 137.28% 421.15% 131.58%

Liabilities and Stockholders' Equity

Current Liabilities:

Current maturities of debt and finance leases 3.42% 4.87% 10.13% 3.99%

Current maturities of operating leases 2.15% 1.70% 3.97% 1.30%

Air traffic liability 10.49% 10.88% 23.66% 10.87%

Accounts payable 6.70% 6.95% 16.61% 6.58%

Accrued Salaries and related benefits 7.40% 7.87% 12.20% 6.13%

Loyalty program deferred revenue 6.73% 6.85% 10.39% 5.02%

Taxes Payable 0.00% 0.00% 0.00% 0.00%

Fuel card obligation 2.42% 1.57% 6.43% 0.94%

Hedge Derivative Liability 0.00% 0.00% 0.00% 0.00%

Other accrued liabilities 2.51% 2.29% 9.77% 3.34%

Total Current Liabilities 41.81% 42.98% 93.17% 39.88%

Noncurrent Liabilities:

Debt and finance leases 18.57% 18.88% 160.43% 21.87%

Noncurrent air traffic liability 0.00% 0.00% 2.92% 0.00%

Pension, postretirement, and related benefits 20.62% 17.98% 62.18% 32.08%

Loyalty program deferred revenue 8.22% 7.46% 31.62% 6.61%

Noncurrent operating leases 13.05% 11.26% 33.42% 6.08%

Deferred Income taxes, net 0.00% 3.10% 0.00% 0.39%

Other noncurrent liabilities 2.55% 2.95% 28.44% 4.32%

Total Noncurrent Liabilities 63.01% 61.63% 319.01% 71.64%

Commitments and Contingencies

Stockholders' Equity:

Common stock at par value 0.00% 0.00% 0.00% 0.00%

Additional paid-in-capital 26.26% 23.68% 65.86% 30.16%

Retained earnings (deficit) 22.59% 26.49% -2.50% 21.21%

Accumulated comprehensive loss -17.61% -17.00% -52.87% -17.58%

Treasury stock -0.45% -0.50% -1.52% -0.63%

Total Stockholders' Equity 30.80% 32.67% 8.97% 21.97%

Total Liabilities and Stockholders' Equity 135.62% 137.28% 421.15% 131.58%

Cash and cash equivalents (% of rev)

Delta Airlines, Inc

Valuation of Options Granted under ESOP

Current Stock Price $48.06

Risk Free Rate 1.72%

Current Dividend Yield 0.97%

Annualized St. Dev. of Stock Returns 36.50%

Average Average B-S Value

Range of Number Exercise Remaining Option of Options

Outstanding Options of Shares Price Life (yrs) Price Granted

Range 1 7.57 37.18 5.00 19.25$ 281.41

Range 2

Range 3

Range 4

Range 5

Range 6

Range 7

Range 8Range 9

Total 7.57 37.18$ 5.00 21.02$ 281.41$

Delta Airlines, Inc

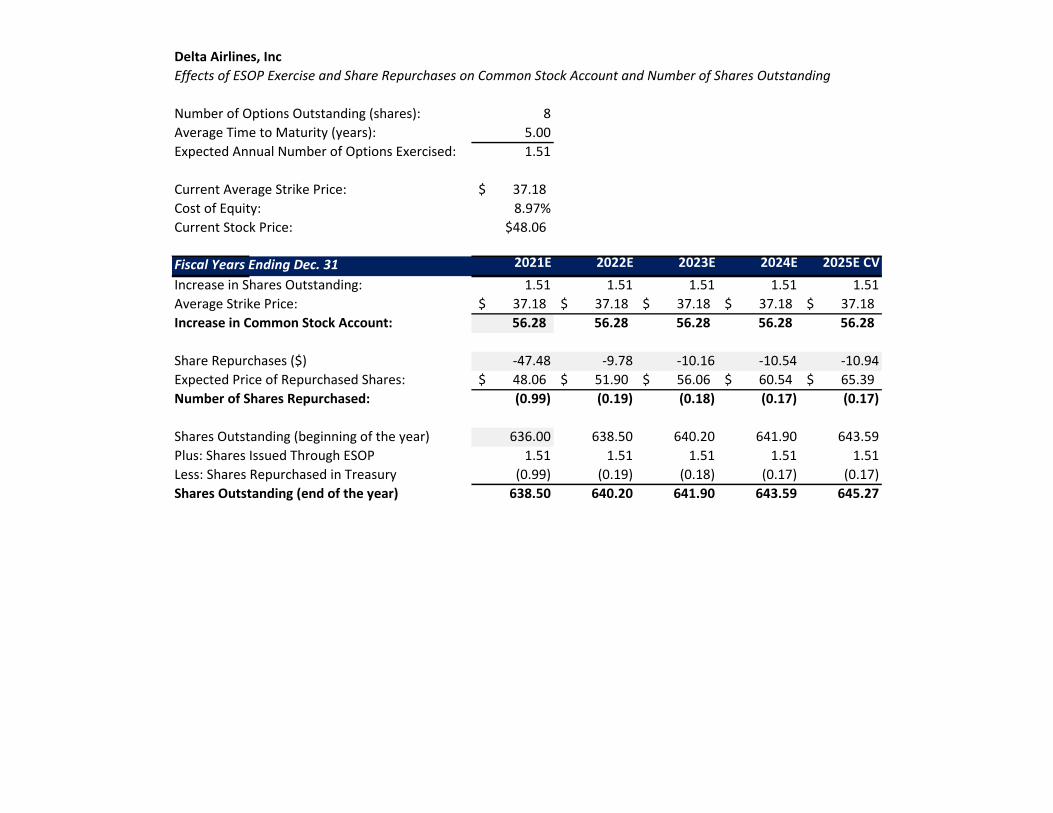

Effects of ESOP Exercise and Share Repurchases on Common Stock Account and Number of Shares Outstanding

Number of Options Outstanding (shares): 8

Average Time to Maturity (years): 5.00

Expected Annual Number of Options Exercised: 1.51

Current Average Strike Price: 37.18$

Cost of Equity: 8.97%

Current Stock Price: $48.06

Fiscal Years Ending Dec. 31 2021E 2022E 2023E 2024E 2025E CV

Increase in Shares Outstanding: 1.51 1.51 1.51 1.51 1.51

Average Strike Price: 37.18$ 37.18$ 37.18$ 37.18$ 37.18$

Increase in Common Stock Account: 56.28 56.28 56.28 56.28 56.28

Share Repurchases ($) -47.48 -9.78 -10.16 -10.54 -10.94

Expected Price of Repurchased Shares: 48.06$ 51.90$ 56.06$ 60.54$ 65.39$

Number of Shares Repurchased: (0.99) (0.19) (0.18) (0.17) (0.17)

Shares Outstanding (beginning of the year) 636.00 638.50 640.20 641.90 643.59

Plus: Shares Issued Through ESOP 1.51 1.51 1.51 1.51 1.51

Less: Shares Repurchased in Treasury (0.99) (0.19) (0.18) (0.17) (0.17)

Shares Outstanding (end of the year) 638.50 640.20 641.90 643.59 645.27

Delta Airlines, Inc

Key Management Ratios

Fiscal Years Ending Dec. 31 2018 2019 2020 2021E 2022E 2023E 2024E 2025E

Liquidity Ratios:

Current ratio=current assets/current liabilities 0.34 0.41 1.09 0.51 0.51 0.51 0.50 0.50

Quick ratio=(Cash & equivalents + Marketable securities + Account receivable)/Current liabilities0.21 0.28 0.61 0.33 0.33 0.33 0.33 0.33

Operating cash flow ratio=Non operating expenses/Current liabilities(0.01) (0.02) (0.20) (0.06) (0.06) (0.06) (0.06) (0.06)

Asset-Management Ratios:

AR turnover ratio=Sales/Account receivable net 16.93 14.15 21.18 15.06 15.06 15.06 15.06 15.06

Inventory turnover ratio=Sales/Avg. Inventory 66.17 55.33 78.42 55.55 55.54 55.55 55.54 55.54

Fixed assets turnover ratio=Net sales/Avg. Fixed assets 0.73 0.72 0.54 0.76 0.75 0.75 0.75 0.74

Financial Leverage Ratios:

Debt-Equity ratio=total liabillity/total shareholder's equity 3.40 3.20 45.93 2.73 2.75 2.81 2.78 2.80

Equity multipler=Total assets/total liabilities 1.29 1.31 1.02 1.58 1.57 1.53 1.55 1.54

Total debt to capitalization=Short-term debt + long-term debt/short-term debt + long-term debt + total shareholder's equity0.44 0.44 0.95 0.43 0.43 0.43 0.43 0.43

Profitability Ratios:

Return on Equity (NI/Beg TSE) 0.28 0.35 (0.81) 2.27 0.22 0.22 0.22 0.22

ROE=NI/Shareholder's equity 28.75% 31.04% -807.37% 21.70% 21.72% 21.70% 21.70% 21.70%

EBITDA Margin=(Earnings before interest and tax + depreciation + amortization)/total revenue4,840.05 5,897.05 (16,515.86) 2,073.91 2,143.06 2,209.02 2,280.83 2,354.57

Net profit margin=NI/Total revenue 8.86% 10.14% -72.45% 7.20% 7.20% 7.20% 7.20% 7.20%

Payout Policy Ratios:

Dividend Payout Ratio (Dividend/EPS) 23.02% 20.63% -2.05% 17.37% 17.37% 17.37% 17.37% 17.37%

Total Payout Ratio ((Divs. + Repurchases)/NI) 0.03% 0.03% 0.00% 94.92% 97.80% 100.60% 103.59% 106.66%

Divident Payout Ratio=Dividend/NI 0.03% 0.03% 0.00% 0.03% 0.03% 0.03% 0.03% 0.03%

Delta Airlines, Inc

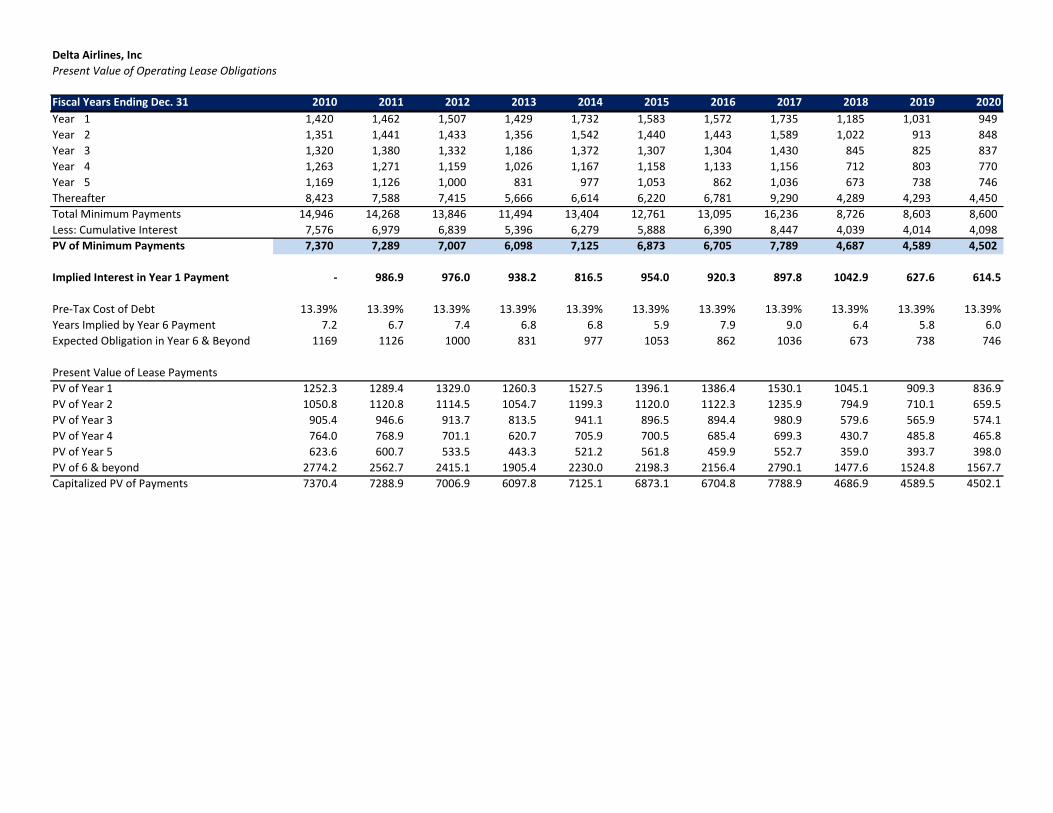

Present Value of Operating Lease Obligations

Fiscal Years Ending Dec. 31 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Year 1 1,420 1,462 1,507 1,429 1,732 1,583 1,572 1,735 1,185 1,031 949

Year 2 1,351 1,441 1,433 1,356 1,542 1,440 1,443 1,589 1,022 913 848

Year 3 1,320 1,380 1,332 1,186 1,372 1,307 1,304 1,430 845 825 837

Year 4 1,263 1,271 1,159 1,026 1,167 1,158 1,133 1,156 712 803 770

Year 5 1,169 1,126 1,000 831 977 1,053 862 1,036 673 738 746

Thereafter 8,423 7,588 7,415 5,666 6,614 6,220 6,781 9,290 4,289 4,293 4,450

Total Minimum Payments 14,946 14,268 13,846 11,494 13,404 12,761 13,095 16,236 8,726 8,603 8,600

Less: Cumulative Interest 7,576 6,979 6,839 5,396 6,279 5,888 6,390 8,447 4,039 4,014 4,098

PV of Minimum Payments 7,370 7,289 7,007 6,098 7,125 6,873 6,705 7,789 4,687 4,589 4,502

Implied Interest in Year 1 Payment - 986.9 976.0 938.2 816.5 954.0 920.3 897.8 1042.9 627.6 614.5

Pre-Tax Cost of Debt 13.39% 13.39% 13.39% 13.39% 13.39% 13.39% 13.39% 13.39% 13.39% 13.39% 13.39%

Years Implied by Year 6 Payment 7.2 6.7 7.4 6.8 6.8 5.9 7.9 9.0 6.4 5.8 6.0

Expected Obligation in Year 6 & Beyond 1169 1126 1000 831 977 1053 862 1036 673 738 746

Present Value of Lease Payments

PV of Year 1 1252.3 1289.4 1329.0 1260.3 1527.5 1396.1 1386.4 1530.1 1045.1 909.3 836.9

PV of Year 2 1050.8 1120.8 1114.5 1054.7 1199.3 1120.0 1122.3 1235.9 794.9 710.1 659.5

PV of Year 3 905.4 946.6 913.7 813.5 941.1 896.5 894.4 980.9 579.6 565.9 574.1

PV of Year 4 764.0 768.9 701.1 620.7 705.9 700.5 685.4 699.3 430.7 485.8 465.8

PV of Year 5 623.6 600.7 533.5 443.3 521.2 561.8 459.9 552.7 359.0 393.7 398.0

PV of 6 & beyond 2774.2 2562.7 2415.1 1905.4 2230.0 2198.3 2156.4 2790.1 1477.6 1524.8 1567.7

Capitalized PV of Payments 7370.4 7288.9 7006.9 6097.8 7125.1 6873.1 6704.8 7788.9 4686.9 4589.5 4502.1

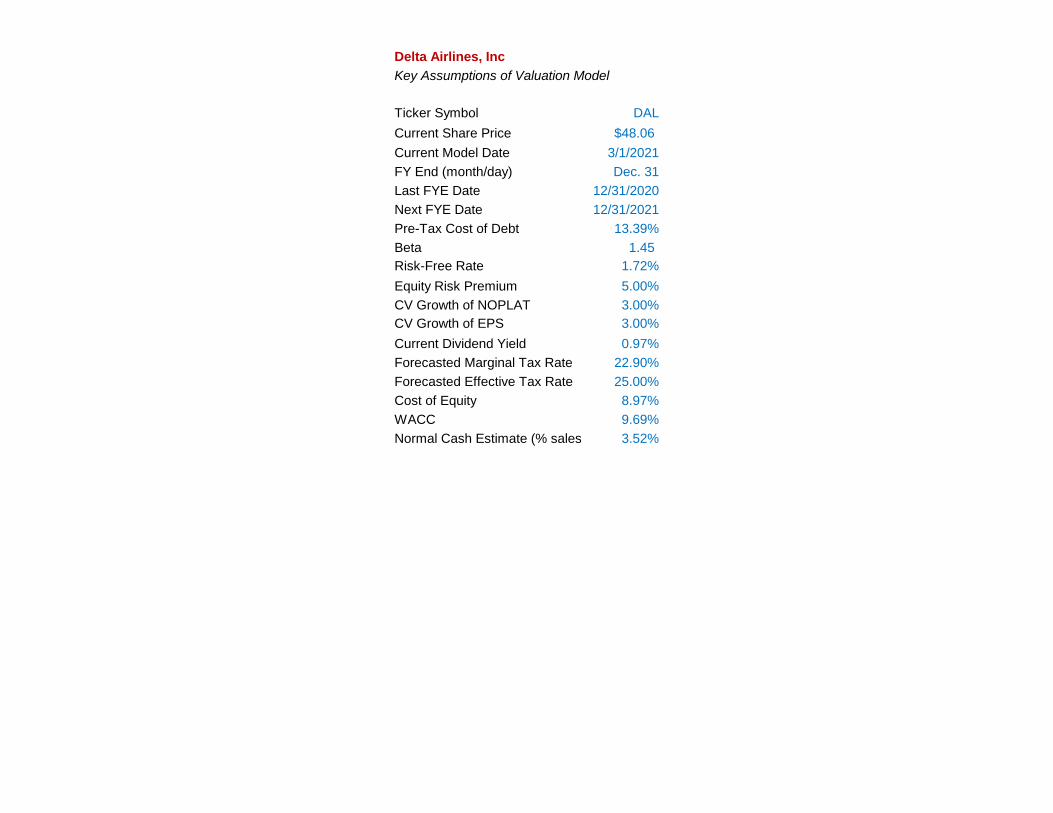

Delta Airlines, Inc

Key Assumptions of Valuation Model

Ticker Symbol DAL

Current Share Price $48.06

Current Model Date 3/1/2021

FY End (month/day) Dec. 31

Last FYE Date 12/31/2020

Next FYE Date 12/31/2021

Pre-Tax Cost of Debt 13.39%

Beta 1.45

Risk-Free Rate 1.72%

Equity Risk Premium 5.00%

CV Growth of NOPLAT 3.00%

CV Growth of EPS 3.00%

Current Dividend Yield 0.97%

Forecasted Marginal Tax Rate 22.90%

Forecasted Effective Tax Rate 25.00%

Cost of Equity 8.97%

WACC 9.69%

Normal Cash Estimate (% sales) 3.52%

Delta Airlines, Inc

Sensitivity Tables

40.05 1.15 1.25 1.35 1.45 1.55 1.65 1.75 40.05 0.67% 0.77% 0.87% 0.97% 1.07% 1.17% 1.27%

4.40% 57.91 53.83 50.02 46.46 43.12 39.98 37.03 1.15 51.66 51.65 51.64 51.64 51.63 51.62 51.61

4.60% 55.74 51.64 47.81 44.24 40.89 37.75 34.80 1.25 47.51 47.50 47.50 47.49 47.48 47.47 47.47

4.80% 53.65 49.52 45.68 42.10 38.75 35.61 32.66 1.35 43.66 43.65 43.65 43.64 43.63 43.63 43.62

5.00% 51.64 47.49 43.64 40.05 36.70 33.57 30.62 1.45 40.07 40.06 40.06 40.05 40.05 40.04 40.03

5.20% 49.69 45.53 41.67 38.08 34.73 31.60 28.67 1.55 36.72 36.71 36.71 36.70 36.70 36.69 36.69

5.40% 47.81 43.64 39.78 36.19 32.84 29.72 26.80 1.65 33.58 33.58 33.57 33.57 33.56 33.56 33.55

5.60% 45.99 41.81 37.95 34.36 31.02 27.91 25.00 1.75 30.64 30.63 30.63 30.62 30.62 30.61 30.61

40.05 1.42% 1.52% 1.62% 1.72% 1.82% 1.92% 2.02% 40.05 7.47% 7.97% 8.47% 8.97% 9.47% 9.97% 10.47%

2.70% 40.05 39.37 38.71 38.05 37.40 36.76 36.13 3.98% 607.91 608.38 608.85 609.31 609.77 610.24 610.69

2.80% 40.74 40.05 39.37 38.70 38.04 37.38 36.74 4.48% 383.57 383.87 384.16 384.45 384.75 385.04 385.33

2.90% 41.44 40.74 40.05 39.36 38.69 38.02 37.37 4.98% 272.46 272.67 272.88 273.09 273.29 273.50 273.71

3.00% 42.17 41.46 40.75 40.05 39.36 38.68 38.01 5.48% 206.09 206.25 206.41 206.56 206.72 206.88 207.03

3.10% 42.93 42.19 41.47 40.76 40.06 39.36 38.68 5.98% 161.95 162.07 162.19 162.32 162.44 162.56 162.69

3.20% 43.70 42.95 42.22 41.49 40.77 40.07 39.37 6.48% 130.45 130.55 130.65 130.75 130.85 130.94 131.04