indonesia cement 14 january 2018 - indopremier.com for sumatera (5.2%) and ex-java/sumatera (6.4%)...

TRANSCRIPT

Refer to Important disclosures on the last of this report

Source: Bloomberg

2019 - Year of recouped price clout

� Domestic cement volume growth to stay modest (+4.9% yoy) in 2019.

� Mounting first-tier retail presence as second-tier operation lurches.

� Better supply control by first-tier players shall levitate their ASPs.

� We choose SMGR as our top pick but keep our SELL rating on SMBR.

Modest volume growth trend is to continue in 2019. We forecast cement sales

volume to grow 4.9% to 73mt in 2019 (2018: 4.6%) as populist fiscal policies during

election year may slow launch of new infrastructure projects. This, in fact, is reflected

on 2019 infra-budget of Rp421tn that paints a nuanced growth (+2.5% yoy).

Nevertheless, we also noted that populist policy could lever people’s purchasing power

in the form of higher disposable income that caters positive catalyst for cement bag

consumption are frequently used for renovation, especially in rural area and KPPIP

indicated 94 (out of 187) infrastructure project will keep rolling this year most of which

are decentralized outside Java. We thus forecast higher cement sales growth in 2019

for Sumatera (5.2%) and Ex-Java/Sumatera (6.4%) vs. 5% and 6%, respectively, in

2018, and flat Java volume growth of 4.1% (2018: 4%) to account for persistent

market saturation.

Industry should see less rivalry. We expect higher volume market share (84% vs.

2018: 81%) of first-tier players (Indocement, Semen Holcim, and Indonesia) in the

wake of both impaired retail presence of second-tier manufacturers, with their debt

burden problems (including Chinese players, such as Anhui Conch), and scale operating

in a well saturated market (most of them located in Java). This is evident from sales-

to-installed capacity metric of these second-tier manufacturers which had decreased to

33% in 2018 (vs. industry and first-tier at 60% and 74%, respectively) and we forecast

a lower second-tier utilization rate in the range of 30% going forward.

Industry consolidation spurs improved pricing power. We forecast national

installed capacity at 113mt in 2019 (+4.7% yoy) due to supply addition from Semen

Kupang (1.5mt) and Anhui Conch (3.6mt). These new mills will raise capacity share of

second-tier players (2018: 33% vs. 2015: 19%) though we are skeptical on their

capability to effectively run these new facilities, if not left dormant in operation. On the

other hand, We argue that national supply growth will be better managed by first-tier

players (with 67% of capacity share), especially SMGR that markedly holds 43% (up

from 31%) of capacity share post SMCB merger. Apropos of that, we expect better

pricing power for first-tier players, with SMGR leading in pricing power, as corollary of

both industry consolidation and less competition intensity. Moreover, we noted Eastern

Indonesia (Sulawesi, Maluku, and Papua) is actually on 5mt supply deficit and this

region holds 16% of market share and some region, like Borneo, C. Java, and

Sumatera, have benign overcapacity with considerable total market share of 41%.

Stock picks. Price recovery is the main theme for cement industry this year in which

our sensitivity analysis concludes the price to be the critical factor that drives

profitability. In particular, we like SMGR due to its capability of flexibly adjusting their

ASP on region-by-region basis due to extensive presence and the merger should further

empower company’s scale and scope. Moreover, SMGR current EV/ton of $154 implies

19% and 26% to average Indonesian and Global cement peers.

Stock Ticker Rating Price TP

19F P/E

20F P/E

19F P/B

20F P/B

19F ROA

19F ROE

(Rp) (Rp) (x) (x) (x) (x) (%) (%)

Semen Indonesia

SMGR Buy 11,575 14,000 22.0 16.4 0.8 0.8 3.6 9.1

Indocement INTP Hold 18,000 17,400 46.3 35.6 2.4 2.2 5.2 6.3

Semen Baturaja

SMBR Sell 1,715 400 175.1 187.9 4.6 4.6 2.0 2.7

Source: Bloomberg, IndoPremier Note: Share prices as of closing 14-January-2019

Indonesia Cement

14 January 2018

Sector Update

Sector Index Performance (JAKBIND)

3M 6M 12M

Absolute (%) 16.6 11.9 27.9

Relative to JCI (%) 6.5 5.3 28.4

52whigh/low (Rp) 886/681

Willy Goutama

PT Indo Premier Sekuritas

+62 21 5793 1168

70

80

90

100

110

120

130

140

150

12-Jan 12-Apr 12-Jul 12-Oct 12-Jan

JCI JAKBIND

Equity |

Indonesia

| C

em

ent

Cement Sector Update

2 Refer to Important disclosures on the last of this report

Fig. 1: Imbalance of Demand & Supply is to narrow... Fig. 2: … as second-tier ‘s utilization swoops

Source : ASI, CEIC, Indo Premier Source : ASI, CEIC, Indo Premier

Fig. 3: First-tier’s capacity share dominates nation-wide Fig. 4: First-tier domination contains overcapacity issue

Source : ASI, Companies, Indo Premier Source : ASI, CEIC, Indo Premier

Fig. 5: Plus, first-tier product presence should gradually up Fig. 6: Semen Indonesia looks attractive valuation-wise

Source : Companies, Indo Premier Source : Bloomberg, Indo Premier

-5%

10%

25%

40%

55%

70%

85%

100%

0

20

40

60

80

100

120

140

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018F2019F2020F2021F

Total Cement Demand (mt)

Total Industry Excess Capacity (mt)

Demand to Installed Capacity (%)- RHS

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

First-tier Players (mt) Second-Tier Players (mt)

First-tier Sales to Installed Capacity (%) - RHS Second-tier Sales to Installed Capacity S(%) - RHS

0%

20%

40%

60%

80%

100%

Sumatera

Sulawesi

BorneoW. Java

E. Java

Pre-merged SMGR INTP Post-merged SMGR First-tier Players

0%

10%

20%

30%

40%

50%

60%

(10,0)

-

10,0

20,0

30,0

40,0

50,0

60,0

70,0

80,0

90,0

W. Java C. Java E. Java Java Sumatera Borneo Eastern

Indonesia

Demand (mt) Excess Capacity (mt) Market Share (%)- RHS

44% 45%43%

41% 41%

44% 44%42% 43% 44%

40% 40% 41% 42%

32%30% 31% 32% 32%

30% 30%

27% 26% 25% 26% 26% 26% 26%

14% 14% 14%16% 16% 15% 15% 14%

12%15% 15% 15% 15% 15%

3% 3% 3% 3% 2% 2% 2% 2% 3% 3% 3% 3% 3% 3%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

SMGR INTP SMCB SMBR

-

100

200

300

400

500

600

700

Cement Sector Update

3 Refer to Important disclosures on the last of this report

Macroeconomics Overview

Solid pace in infrastructure and property should sustain cement volume growth

Indonesia economic profile continued to exhibit a steady increase (10-yr real GDP growth at 5.5%).

We also witnessed an ascending portion of investment to total GDP (fig. 7) from 25% in 2007 to

33% in 2017, supported by an upbeat in real investment (10-yr CAGR at 6.6%) that outpaces real

GDP growth (10-yr CAGR at 5.5%) which results to higher real investment-to-GDP ratio (2017: 33%

vs. 2007: 29%). This progress has been indispensable to current government main theme of

promoting an extensive infrastructure projects spanning from Western to Eastern Indonesia.

The infrastructure spending contains on state budget (fig. 9) had seen a gigantic growth (5-yr CAGR

FY12-17 at 22%) post Jokowi administration took place whose figure nearly tripled from Rp146tn in

2012 to Rp401tn in 2017 of which it has been recently allocated across ministries, rather than being

centralized in the Ministry of Public Work and Transportation (fig. 10).

The following chart (fig. 11) presents type of construction had been done in the past 10 years that

consists of building, civil, and specialized (dams. power generations, etc.) constructions. As a whole,

total gross construction output advanced reasonably well at 10-yr historical CAGR of 16% which was

well above the compounded growth of nominal GDP at 10% for the pertaining period (2010-2017).

The civil construction had been the main growth contributor for total gross construction output that

increased at 7-yr historical CAGR of 16.4%, followed by the building and specialized construction of

15.4% and 14%, respectively.

Fig. 7: Steady Economic Growth with an Ascending Investment Fig. 8: Real Investment-to-GDP ticks up over time

Source : CEIC, Ministry of Finance, Indo Premier Source : CEIC, Ministry of Finance, Indo Premier

Fig. 9: Total Infrastructure Budget and Its Share as of GDP Fig. 10: Infrastructure Budget Allocation across Ministries

Source : CEIC, DJPBN, Ministry of Finance, Indo Premier Source : CEIC, Indo Premier

64% 61% 59% 56% 55% 56% 57% 57% 57% 58% 57%

8%8% 10%

9% 9% 9% 10% 9% 10% 10% 9%

25% 28% 31%33% 33%

35% 34% 35% 34%34%

33%

0%

1%

2%

3%

4%

5%

6%

7%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Private Consumption Government Spending Investment GDP Growth (%)- RHS

0%

5%

10%

15%

20%

25%

30%

35%

-

2.000

4.000

6.000

8.000

10.000

12.000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Real GDP (2010=100, Rptn) Real Investment (2010=100, Rptn)

Real Investment-to-GDP (RHS)

1,6%

1,4%1,3%

1,5%

1,7% 1,6%1,5%

2,2%

2,6%

3,0%2,8%

2,6%

0,0%

0,5%

1,0%

1,5%

2,0%

2,5%

3,0%

3,5%

-

50

100

150

200

250

300

350

400

450

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Total Infrastructure Budget (RHS, Rptn)

Infrastructure Budget (% of Total Nominal GDP)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Ministry of Public Work Budget Ministry of Transportation Budget

Other Ministries' Infrastructure Budget

Cement Sector Update

4 Refer to Important disclosures on the last of this report

As of 2017, the building, civil, and specialized construction output booked at Rp256tn, Rp478tn, and

Rp136tn which brought a total construction output of Rp871tn (+11% yoy), accounting for 6.41% of

total nominal GDP (2008: 2.06%). The distribution of gross construction output by region (fig. 12)

depicts the focus area of a realized infrastructure budget allocation. The figure shows a growing

trend in construction output proportion in Java from 49% in 2008 to 66% in 2017 which we think

could sustain the cement demand growth in an already saturated market. While, the Sumatera and

Ex- Java and Sumatera regions saw a decreasing trend in construction output proportion to both

17% (from 21% and 30% in 2008), consecutively.

Despite a decreasing construction output proportion in Sumatera and Ex-Java/Sumatera region, we

can see the proportion of construction output to each regional GDP (fig. 13) was actually increasing

for Sumatera, Borneo, and Sulawesi which means that the construction activities start to give more

contribution to their regional economy activities. Rapid and massive scale of infrastructure projects

had also rendered an increase in the construction input purchase which can be seen on the trend of

material spending as of total fiscal spending (fig. 14) that nearly tripled as well from 6% in 2008 to

15% in 2017 as the material spending (7-yr CAGR at 17%) outgrew the capital spending (7-yr

CAGR at 10%). It thus conveys an idea of increasing use of cement as one of the major material

input for constructions.

While the infrastructure expansion has taken a consequence of a heightened debt-to-GDP ratio (to

23% in 9M18 (from 15% in 2010), we think that this level is still relatively low compared to

countries with similar country risk (fig. 16) whose median debt-to-GDP ratio is 37.8% in 2017, but

raise the concern on the debt maturity management as the short-term portion is noticeably

increasing (fig. 15). Nevertheless, we believe this is a right step as the long-run effects of

infrastructure should outweigh the cost of short-run financial leverage.

Fig. 11: Gross Construction Output by Type (in Rptn) Fig. 12: Distribution of Gross Construction Output by Region

Source : CEIC, Indo Premier Source : CEIC, Indo Premier

Fig. 13 : Construction Output (% of regional GDP, 4-q MA) Fig. 14 : Capital and Material spending (% of fiscal spending)

Source : CEIC, Indo Premier Source : CEIC, Indo Premier

-

100

200

300

400

500

600

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Building Construction Civil Construction Specialized Construction

21% 19% 18% 19% 19% 19% 19% 17% 17% 17%

49% 53%64% 62% 63% 63% 63% 66% 66% 66%

30% 28%17% 19% 19% 18% 18% 17% 17% 17%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Sumatera Java Ex- Java and Sumatera

1,0%

1,5%

2,0%

2,5%

3,0%

3,5%

3M

11

6M

11

9M

11

20

11

3M

12

6M

12

9M

12

20

12

3M

13

6M

13

9M

13

20

13

3M

14

6M

14

9M

14

20

14

3M

15

6M

15

9M

15

20

15

3M

16

6M

16

9M

16

20

16

3M

17

6M

17

9M

17

20

17

3M

18

6M

18

9M

18

Sumatera W. Java C. Java E. Java Borneo Sulawesi

0%

2%

4%

6%

8%

10%

12%

14%

16%

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Material Spending Capital Spending

Cement Sector Update

5 Refer to Important disclosures on the last of this report

Going forward, we stay positive on the infrastructure outlook as Committee for Acceleration of

Priority Infrastructure Delivery (KPPIP) indicated that 66 projects will be completed in 2019 along

with the additional 187 infrastructure projects of which 93 projects and 1 special program (the

construction of 35GW electric generator) are under construction and have started the operation and

the other 94 projects and 1 airplane industry program are on its construction stage. Out of these

projects, KPPIP had selected 37 priority projects with the total investment value of $182bn with

most projects take place in Java and Sumatera that account for 24% of total priority project

investment value and 20% of total priority project number, consecutively. While, more than half of

total priority projects’ investment value (56%) are allocated to Ex-Java/Sumatera region on which

we can expect the positive growth catalysts for cement consumption in the middle and eastern part

of Indonesia on foreseeable future. Our infrastructure and property analyst, Joey Faustian, forecasts

the new contract and order book of our infrastructure coverage (ADHI, PTPP, WIKA, and WSKT) to

deliver a subdued growth at 3-yr CAGR 17-20F of 10% and 15%, consecutively (vs. 5-yr CAGR of

23% and 31%) as the effect of high base from the preceding period.

On the other hand, property sector which is the backbone of overall national cement growth had

painted a dynamic picture over the last 7 years as the nominal property output as of total regional

GDP (fig. 19) suggests Java region which comprises of West Java, Central Java, and East Java

flattens on its ratio of property output to regional GDP whose amounts are 1%, 2%, and 1%,

respectively. This flattening trend was driven by nominal construction GDP growth (7-yr CAGR at

15%) that outpaced real estate GDP growth (7-yr CAGR at 12%). The construction growth was also

slightly above Java nominal GDP (7-yr CAGR at 13%). Sulawesi region posted a slight decrease to

2.92% in 9M18 (from 3.03% in 2010). Conversely, Sumatera and Borneo had seen an increasing

trend over its property output to regional GDP recording at 2.67% and 1.52%, (2010: 2.33% and

1.32%), respectively. This trend was supported by both of construction and real estate growth that

outgrew its respective nominal GDP growth in both Sumatera (7-yr CAGR at 16%, 15%, and 13%,

consecutively) and Borneo (7-yr CAGR at 13%, 16%, and 11%, consecutively).

Fig. 15 : Indonesia Public Debt Profile Fig. 16 : Debt-to-GDP of BBB-rated (Fitch) Emerging Countries

Source : CEIC, Indo Premier Source : Bloomberg, Fitch Ratings, Indo Premier

Fig. 17: New Contract (in Rptn) Forecast of Our Coverage Fig. 18: Order Book (in Rptn) Forecast of Our Coverage

Source : Companies, Indo Premier Source : Companies, Indo Premier

0%

5%

10%

15%

20%

25%

30%

0%

20%

40%

60%

80%

100%

120%

Short-term Portion (%) Long-term Portion (%) Debt-to-GDP

0

10

20

30

40

50

60

70

80

Debt-to-GDP (%) Median (%)

43%

21%

10%

30%

26%

68%

-8%

18%

8% 6%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

70%

80%

0

50

100

150

200

250

2011 2012 2013 2014 2015 2016 2017 2018F 2019F 2020F

New Contract growth

50%

36%

18%25%

31%

58%

24%

17%15%

13%

0

0,1

0,2

0,3

0,4

0,5

0,6

0,7

0

100

200

300

400

500

600

2011 2012 2013 2014 2015 2016 2017 2018F 2019F 2020F

(Rp Tn) Orderbook growth

Cement Sector Update

6 Refer to Important disclosures on the last of this report

Another useful indicator for observing the trend in property sector development is to see the real

property indicator which is represented by the number of houses built by regional basis (fig. 20) that

showed a 7-yr historical CAGR of 7% from 10 thousand houses in 2010 to 17 thousand houses in

2017. On regional basis, this real measure portrays opposite picture to the gross property output

measure on respective regional GDP where the real measurement suggests that Java region

delivered strong 7-yr historical compounded growth of 9.6%, Sumatera region growth was half of

Java region growth at 4.8%, and Ex-Java/Sumatera region growth lagged behind at 2.1% compared

to national growth. This trend is confirmed by the regional distribution of houses built by region (fig.

21) where Java proportion skyrocketed to 61% in 2017 (2010: 52%), both Sumatera and Ex-

Java/Sumatera proportion was declining to 13% and 26% (2010: 18% and 30%), respectively.

Then, these two nominal and real term measure that are consecutively represented by the gross

property output and number of houses built can be used to imply other interesting trends. Java and

ex-Java nominal property measurement (nominal real estate GDP) were recorded at 7-yr CAGR of

12% and 15%, respectively. Meanwhile, real measurement (number of houses built) were booked at

7-yr CAGR of 9.6% and 3.8%). Given these two measurements, we can conclude that Java property

price increase is slower than ex-Java region and this finding is confirmed by the residential property

price index for 18 major cities (fig. 22) where small cities category, mostly located in ex-Java

region, was gradually up relative to large and medium cities category for the last 27 quarters. Thus,

we could plausibly infer that the building material input (including cement) on ex-Java market is

systematically higher than Java market due to less cement product presence outside the Java region

(fig. 37).

Fig. 19: Gross Property Output (% of regional GDP, 4-q MA) Fig. 20: Number of Houses Built by Region (in thousand unit)

Source : CEIC, Indo Premier Source : CEIC, Indo Premier

Fig. 21: Distribution of Houses Built by Region (%) Fig. 22: Residential Property Price Indices for 18 Major Cities

Source : CEIC, Indo Premier Source : CEIC, Indo Premier

1,0%

1,5%

2,0%

2,5%

3,0%

3,5%

3M

11

6M

11

9M

11

20

11

3M

12

6M

12

9M

12

20

12

3M

13

6M

13

9M

13

20

13

3M

14

6M

14

9M

14

20

14

3M

15

6M

15

9M

15

20

15

3M

16

6M

16

9M

16

20

16

3M

17

6M

17

9M

17

20

17

3M

18

6M

18

9M

18

Sumatera W. Java C. Java E. Java Borneo Sulawesi

2 3 3 2 1 2 3

54

2

53 5

3

78

1010

1

2

33

4

4

5

22

-

2

4

6

8

10

12

14

16

18

2009 2010 2011 2012 2013 2014 2015 2016 2017

Sumatera Java Ex- Java and Sumatera

-

50

100

150

200

250

300

1Q

12

2Q

12

3Q

12

20

12

1Q

13

2Q

13

3Q

13

20

13

1Q

14

2Q

14

3Q

14

20

14

1Q

15

2Q

15

3Q

15

20

15

1Q

16

2Q

16

3Q

16

20

16

1Q

17

2Q

17

3Q

17

20

17

1Q

18

2Q

18

3Q

18

Small Cities Medium Cities Large Cities

Cement Sector Update

7 Refer to Important disclosures on the last of this report

Both infrastructure and property industry showed a solid pace as indicated by growing proportion of

gross construction and property value to the nominal GDP (fig. 23), though it recently slowed due to

the delayed infrastructure and property investment as populist policy usually ensues in political

years (2018 regional head elections and 2019 presidential election) as it can be seen on the

flattened growth on infrastructure budget in upcoming period as indicated by the earmarked state

infrastructure budget of Rp421bn in 2019 (+2.5% yoy). We, however, expect some recoveries going

forward for both infrastructure and property sector. On the other hand, we also see that nation-wide

construction growth (7-yr CAGR of 19%) had progressed in the faster pace than property (7-yr

CAGR of 16.3%) as suggested by the gross output measure. This dynamic has affected the cement

sales composition of bag and bulk for the last couple of years (fig. 24) as the volume growth of bulk

cement (7-yr CAGR of 14%) outstripped the bag cement (7-yr CAGR of 6%) that causes an increase

in bulk proportion to 27% in 9M18 (2010: 16%).

Despite of the growing proportion in bulk volume, we believe the bag volume growth will be

sustained at this rate, if not recovered upward. We also argue that bagged cement sales stems from

the residential houses built on rural areas, most of which are for house renovation. The statistics on

home purchasing plan (fig. 25) that was surveyed by Indonesia Statistical Bureau (BPS) confirms

our view in which most of houses are self-built across regions. Additionally, we think that self-built

home includes the home improvement and renovation. The self-built proportion is particularly high

for the region outside Java on which we can see that Borneo, Sumatera, and Sulawesi scored the

highest figure for self-built category. This also confirms our aforementioned finding on residential

property price (fig. 22) indices about the surging property price trend in small-cities that should

mostly include rural areas.

Fig. 25: Survey on the way home ownership is acquired (BPS, 2016)

Source : BPS, Indo Premier

Region Cities Rural Cities Rural Cities Rural Cities Rural

Sumatera 8.7% 0.6% 13.2% 5.1% 65.1% 81.3% 13.1% 13.0%

G. Jakarta 5.6% - 23.1% - 40.9% - 30.4% -

Java ex G. Jakarta 7.4% 0.3% 10.9% 2.5% 58.4% 75.9% 23.3% 21.4%

Bali, NTT, and NTB 5.3% 0.2% 3.6% 3.0% 72.0% 80.5% 19.2% 16.2%

Borneo 8.6% 0.5% 12.6% 3.2% 68.8% 86.1% 10.0% 10.2%

Sulawesi 8.0% 0.4% 6.8% 5.4% 74.1% 83.2% 11.1% 10.9%

Papua and Maluku 3.5% 0.1% 7.1% 1.9% 78.0% 80.5% 11.3% 17.5%

Indonesia 7.5% 0.4% 11.6% 3.6% 59.8% 78.2% 21.2% 17.8%

Developer Non-developer Self-built Other (Bequest, Grant, etc)

Fig. 23: Construction & Property (% GDP and % yoy, 4-q MA) Fig. 24: Cement Bag and Bulk Share and Its Growth (%)

Source : CEIC, Indo Premier Source : ASI, CEIC, Indo Premier

0%

5%

10%

15%

20%

25%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

3M

11

6M

11

9M

11

20

11

3M

12

6M

12

9M

12

20

12

3M

13

6M

13

9M

13

20

13

3M

14

6M

14

9M

14

20

14

3M

15

6M

15

9M

15

20

15

3M

16

6M

16

9M

16

20

16

3M

17

6M

17

9M

17

20

17

3M

18

6M

18

9M

18

Gross Construction Output Gross Real Estate Output

Construction Output Growth (% yoy) - RHS Real Estate Output Growth (% yoy) - RHS

17% 16% 16% 16% 19% 20% 21% 22% 24% 25% 25% 27%

-15%

-5%

5%

15%

25%

35%

45%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 9M18

Bag Bulk

Bag Sales Growth (% yoy) Bulk Sales Growth (% yoy)

Cement Sector Update

8 Refer to Important disclosures on the last of this report

Industrial Overview

The industry should see better profitability profile in the wake of improved pricing power and better supply control

We believe this year should be the tipping point for Indonesian cement industry toward recovery

spurred by the industry consolidation and less competition intensity. The industry consolidation

renders the first-tier players (Indocement, Semen Holcim, and Semen Indonesia) to exert significant

influence over the national supply growth with their considerable capacity share (67% of total

national installed capacity) equipped by better coordination as Semen Holcim and Indonesia are now

under one entity.

The price recovery will emanate from the blurry operational sustainability of second-tier players,

especially for Chinese players which are beleaguered with low utilization (below 40%), debt

burdens, and the end of tax holiday period which we think the second-tier will not conduct a price

predatory strategy going forward given their woeful financial performance. We believe the industry

should see better pricing environment going forward.

On the other hand, we see this year to be the inflection point for cement volume growth with

expected growth recoveries in 2020 onwards, though we expect this year with the same growth as

exhibited in 2018 due to political year that typically follows by flat cement growth as populist policy

and a delayed in both of infrastructure and property investment ensue on political year.

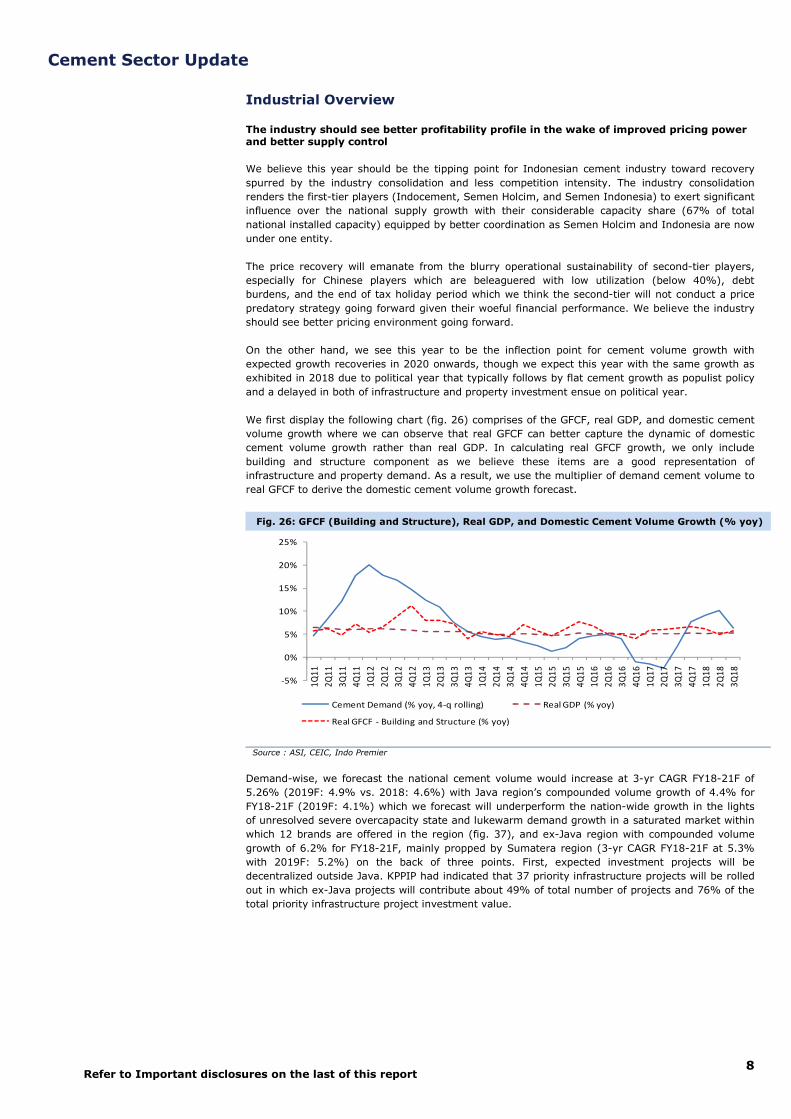

We first display the following chart (fig. 26) comprises of the GFCF, real GDP, and domestic cement

volume growth where we can observe that real GFCF can better capture the dynamic of domestic

cement volume growth rather than real GDP. In calculating real GFCF growth, we only include

building and structure component as we believe these items are a good representation of

infrastructure and property demand. As a result, we use the multiplier of demand cement volume to

real GFCF to derive the domestic cement volume growth forecast.

Fig. 26: GFCF (Building and Structure), Real GDP, and Domestic Cement Volume Growth (% yoy)

Source : ASI, CEIC, Indo Premier

Demand-wise, we forecast the national cement volume would increase at 3-yr CAGR FY18-21F of

5.26% (2019F: 4.9% vs. 2018: 4.6%) with Java region’s compounded volume growth of 4.4% for

FY18-21F (2019F: 4.1%) which we forecast will underperform the nation-wide growth in the lights

of unresolved severe overcapacity state and lukewarm demand growth in a saturated market within

which 12 brands are offered in the region (fig. 37), and ex-Java region with compounded volume

growth of 6.2% for FY18-21F, mainly propped by Sumatera region (3-yr CAGR FY18-21F at 5.3%

with 2019F: 5.2%) on the back of three points. First, expected investment projects will be

decentralized outside Java. KPPIP had indicated that 37 priority infrastructure projects will be rolled

out in which ex-Java projects will contribute about 49% of total number of projects and 76% of the

total priority infrastructure project investment value.

-5%

0%

5%

10%

15%

20%

25%

1Q

11

2Q

11

3Q

11

4Q

11

1Q

12

2Q

12

3Q

12

4Q

12

1Q

13

2Q

13

3Q

13

4Q

13

1Q

14

2Q

14

3Q

14

4Q

14

1Q

15

2Q

15

3Q

15

4Q

15

1Q

16

2Q

16

3Q

16

4Q

16

1Q

17

2Q

17

3Q

17

4Q

17

1Q

18

2Q

18

3Q

18

Cement Demand (% yoy, 4-q rolling) Real GDP (% yoy)

Real GFCF - Building and Structure (% yoy)

Cement Sector Update

9 Refer to Important disclosures on the last of this report

Second, we view Sumatera region as a potential growth engine as it demonstrates a relatively solid

growth indicated by a less growth volatility compared to other regions (fig. 28) and historically holds

more than a fifth of domestic market share which is nearly equivalent to the combined market share

of Ex-Java/Sumatera region (fig. 30). Third, solid property growth is expected following the populist

policy in 2019 as it increases the purchasing power through higher disposable income which could

then serve as a positive catalyst for cement bag consumption as it is mostly used for house

renovation or self-built houses in many rural areas, and expected property investment recoveries in

2020 onwards.

Supply-wise, we come with the growth forecast (fig. 31) of 2.7% CAGR FY18-21F as this will come

from the realized capacity expansion done by several second-tier players though we are skeptical on

their capability to effectively utilize their new capacity due to lack of scale to explore other markets.

We thus account this by narrowing down the industry excess capacity to 35mt in 2021F (2018:

37.7mt) and an improved sales-to-installed capacity ratio (fig. 32) to 74% (2018: 71%) as triggered

by recoveries in first-tier sales volume compounded growth of 6% in FY18-21F and flattish second-

tier sales volume compounded growth of 0.7% in FY18-21F.

In sum, the prospect of reduced demand and supply imbalances should help driving price recovery

going ahead. We believe the first-tier players are in the better position to capitalize this momentum

due to their extensive product, mills presence, and better costs structure compared to second-tier

players. We believe industry profitability profile should improve going ahead.

Fig. 27: Domestic Cement Volume-to-Real GFCF Multiplier (x) Fig. 28: Historical and Forecasted Cement Volume Growth

Source : ASI, CEIC, Indo Premier Source : ASI, CEIC, Indo Premier

Fig. 29: Quarterly Cement Demand Growth (% yoy, 4-q rolling) Fig. 30: Historical and Forecasted Volume Distribution

Source : ASI, CEIC, Indo Premier Source : ASI, CEIC, Indo Premier

(0,7)

(0,2)

0,3

0,8

1,3

1,8

2,3

2,8

2011 2012 2013 2014 2015 2016 2017 2018F 2019F 2020F 2021F

Java Sumatera Ex- Java and Sumatera

-5%

0%

5%

10%

15%

20%

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018F 2019F 2020F 2021F

Java Sumatera Ex- Java and Sumatera

-10%

-5%

0%

5%

10%

15%

20%

25%

Java Sumatera Ex- Java and Sumatera

56% 55% 54% 55% 55% 56% 56% 56% 54% 56% 56% 56% 55% 55%

23% 23% 24% 23% 22% 21% 21% 21% 22% 21% 21% 22% 22% 22%

21% 22% 22% 22% 23% 23% 23% 23% 24% 22% 22% 23% 23% 24%

0%

20%

40%

60%

80%

100%

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018F 2019F 2020F 2021F

Java Sumatera Ex- Java and Sumatera

Cement Sector Update

10 Refer to Important disclosures on the last of this report

Regional Analysis

Java region: a saturated market whose growth is haunted by both malignant overcapacity and tepid demand

Java market has long been the closely watched region to see the overall picture of how cement

industry in Indonesia fares as this region exerts significant influence in driving the overall demand

and supply growth of Indonesian cement industry. As suggested by the total Java sales volume (in

fig. 33), we can see that Java market share consistently tops 54% though attached with volatility in

its movement. This makes the region to be a home market for some well-established first-tier

cement players (Indocement, Semen Holcim, and Semen Indonesia) as well as the market

destination for new entrants which were recently dominated by Chinese-based companies. Many of

these companies are situated in West Java region because this sub-region holds considerable market

share in Java at 47% in 2017 though its share had declined from 51% in 2009.

The reason of declining West Java market share cannot be separated with the issue of excess

capacity (fig. 35) that still persists. As of 2017, West Java alone registered a 31mt in excess

capacity that accounts for 69% of total domestic excess capacity of 45.3mt. This sub-region is

beleaguered with two main issues brought by second-tier Chinese players (Juishin, Sun Fook,

Haohan, and Anhui cement). First, an over aggressive expansion by second-tier Chinese players (3-

yr CAGR FY15-18 of 41% vs. industry at 10%) spread across from Merak to Sukabumi. Though,

Indocement owns substantial capacity share of 55% as of total West Java installed capacity. The

second-tier Chinese players also grab 31% of capacity share which makes their products to have a

relatively equal presence.

Fig. 31: Indonesian Cement Supply Growth Outlook Fig. 32: Excess Capacity and Sales-to-Installed Capacity (%)

Source : ASI, CEIC, Indo Premier Source : ASI, CEIC, Indo Premier

Fig. 33: Java Volume (mt) and Its Market Share (%) Fig. 34: Java Demand Composition (%)

Source : ASI, CEIC, Indo Premier Source : ASI, CEIC, Indo Premier

-10%

0%

10%

20%

30%

40%

50%

-

20

40

60

80

100

120

140

Total Installed Capacity Growth (% yoy)

-5%

10%

25%

40%

55%

70%

85%

100%

0

20

40

60

80

100

120

140

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018F 2019F 2020F 2021FTotal Sales Volume (mt)

Total Industry Excess Capacity (mt)

Sales to Installed Capacity (%)- RHS

53.5%

54.0%

54.5%

55.0%

55.5%

56.0%

56.5%

57.0%

-

5

10

15

20

25

30

35

40

45

50

Java Sales Volume (mt) Market Share (%) - RHS

51% 52% 55% 54% 53% 53% 52% 49% 47%

24% 23% 23% 23% 24% 23% 24%26% 27%

25% 25% 23% 23% 23% 24% 24% 25% 25%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2009 2010 2011 2012 2013 2014 2015 2016 2017

W. Java C. Java E. Java

Cement Sector Update

11 Refer to Important disclosures on the last of this report

Second, second-tier Chinese players implemented a predatory pricing strategy to seize market

share. In fact, Indocement launched its fighting brand (Rajawali) in October 2016 to combat with

pricing issue. These two issues obviously bring disruption into the industry as it is depicted on

quarterly volume performance (fig. 36) in which West Java exhibits the most volatile volume growth

over time.

The other sub regions, Central and Eastern Java, share the same excess capacity issue as in West

Java, albeit with a benign excess. These two sub regions also comprises of domestic first-tier and

second-tier players (fig. 37) on which we think domestic second-tier players have a different pricing

strategy vis-à-vis the second-tier Chinese players. Domestic second-tier players tend to be a price

taker and their pricing mostly dictates the first-tier players. Even though, the price competition does

happen between first-tier and second-tier, it is contained in a specific location and does not intend

to initiate a price war which inflicts the profitability.

As a result, the volume growth volatility in Central and Eastern Java are slightly better than West

Java. We can also observe that Central Java delivered best volume growth with less volatility post

2015 as it carries the least excess capacity figure in Java region (W. Java: 31mt, C.Java: 6.4mt, and

E.Java:10.6mt) with less second-tier player presence as indicated by their capacity share at 26% as

of total Central Java installed capacity. While, second-tier players in Eastern Java possesses 36% of

capacity share.

Fig. 37: Map of Major Indonesia Cement Manufacturers

Source : Companies, Indo Premier

Fig. 35: Demand, Excess Capacity, and Market Share of Java Fig. 36: Quarterly Java Volume Growth (% yoy, 4-q rolling)

Source : ASI, CEIC, Indo Premier Source : ASI, CEIC, Indo Premier

13.7%

13.8%

13.9%

14.0%

14.1%

14.2%

14.3%

14.4%

14.5%

14.6%

0

5

10

15

20

25

30

35

40

45

W. Java C. Java E. Java

Demand (mt) Excess Capacity (mt) Market Share (%)- RHS

-11%

-6%

-1%

4%

9%

14%

19%

24%

29%

W. Java C. Java E. Java

Cement Sector Update

12 Refer to Important disclosures on the last of this report

Going forward, we forecast Java cement volume to grow at a compounded rate of 4.4% in FY18-21F

(2019F: 4.1%) to 44mt in FY21F (from 39mt in FY18) on the back of a postponed infrastructure and

property project in FY19F as it is an usual case for the period that precedes the political years as

suggested in the quarterly Java volume data (fig. 36) in which the year of previous presidential

election took place in 2015 was followed with a decline in cement volume trend. Nevertheless, we

expect growth normalization in FY20F-FY21F in the lights of resuming infrastructure projects. KPPIP

had indicated that 93 infrastructure projects plus 2 special programs will be laid out. Moreover,

under infrastructure project priority lists, Java was awarded by 19 priority projects which account for

51% of the total projects or 24% of total priority project investment value.

Ex-java region: markets with less player presence and benign demand and supply imbalances

Ex-Java region consists of Sumatera, Borneo, Bali, NT, Maluku, and Papua which we will henceforth

categorize as two main sub regions, Sumatera and Ex-Java/Sumatera (consists of Borneo, Sulawesi,

NT, Maluku, and Papua). The characteristic of growth in these two regions are distinctive as

suggested by their growth over the last 16 quarters (fig. 38). In our view, Sumatera shares the

same market traits with Java region as suggested by their economic growth characteristic which

represented by Java and Sumatera nominal GDP measurement that expanded at 7-yr historical

CAGR of 13% and 12.9%, consecutively. Sumatera has also provided a less volatile volume growth

relative to Java region in the light of less cement players’ presence (fig. 37) and some players have

established their market with strong foothold, for instance Semen Baturaja and Padang that

exclusively focus their operation in South Sumatera and Central Sumatera, respectively. Therefore,

the possibility of severe price war is less likely to happen.

On the other hand, Ex-Java/Sumatera region has a characteristic of a significant volatility in its

volume growth that tends to amplify the national cement volume growth (fig. 39). One of the

reasons for this growth characteristic is that this region includes Borneo (with 28% volume share of

total Ex-Java/Sumatera volume) that is a base for some coal mining players. Moreover, Eastern and

Southern Borneo are known to be the largest coal production contributor to the nation. Ex-

Java/Sumatera volume growth are thus fairly exposed to the movement of coal prices. We

superimpose 12-month moving average coal price with 4-q rolling Ex-Java/Sumatera (the moving

average and rolling treatment are to reduce the seasonality effect) on which we can observe that

the movement of cement volume can be partially explained by the Indonesian coal benchmark

movement in recent three quarters.

This region also has a benign demand and supply imbalances with Sumatera region recorded 7.9mt

over capacity (only 17% of total national excess capacity) and the eastern Indonesia (Maluku, Bali,

NT, and Papua) actually experiences a deficit in supply of 5mt (fig. 40). In particular, Sumatera

overcapacity case is similar to Central Java region where it consists of second-tier domestic players,

like Semen Baturaja (SOE) and Semen Bosowa.

These players do not have a tendency to initiate a price war among players. Specifically for

Sumatera region, we argue that market operation is clustered as for Semen Baturaja settles in

South Sumatera, Lafarge Holcim Indonesia in North Sumatera, and both of Semen Padang and

Bosowa place their operation in Central Sumatera.

Fig. 38: Quarterly Cement Demand Growth (% yoy, 4-q rolling) Fig. 39: Ex-Java & Sumatera Growth vs. Indo. Coal Benchmark

Source : ASI, CEIC, Indo Premier Source : ASI, CEIC, Indo Premier

-5%

0%

5%

10%

15%

20%

25%

Java Sumatera

Ex- Java and Sumatera Total Indonesia

-

20

40

60

80

100

120

140

-10%

-5%

0%

5%

10%

15%

20%

25%

Ex- Java and Sumatera Volume (% yoy, 4-q rolling)

Indonesian Coal Benchmark (US$/t, 12m-MA)

Cement Sector Update

13 Refer to Important disclosures on the last of this report

On the other hand, both Sumatera and Ex-Java/Sumatera have 44% volume share as of total

nation-wide volume (fig. 41). Going forward, we forecast Sumatera (fig. 42) and Ex-Java/Sumatera

(fig. 43) region will set a compounded growth of 5.36% (2019F: 5.2%) and 7.05% (2019F: 6.4%)

consecutively. This brings a total ex-Java volume of 36.6mt in 2021 (3-yr CAGR 18-21F of 6.2%) as

government also indicates that this region will be apportioned with 18 government infrastructure

priority project with the total investment value of $139bn (76% of total infrastructure priority

budget) and a populist policy will improve bag consumption as well through government’s social

subsidy programs. Then, this region is capable of fueling the domestic cement growth engine going

forward as we expect the room of capacity deficit will be filled by Semen Indonesia that has

extensive logistical network altogether with enough economics of scale to run such a vast market

operation.

Supply outlook: expected overcapacity alleviation should be the major impetus for an improved pricing power

We believe the recent industry consolidation led by the merger of Semen Indonesia and Lafarge

Holcim Indonesia should cater a positive catalyst to industry in the form of a better supply control

by first-tier players (Indocement, Semen Holcim, and Semen Indonesia) which have 67% of

capacity share as of 2017 (fig. 45). Moreover, we view that second-tier players lurch forward to

maintain their operations as the lack of economics of scale and scope despite their growing capacity

share (fig. 45) of 33% in 2017 (2010: 9%) on which we believe this should lever up the pricing

power of first-tier company as reasoned the following argument. Second-tier players have been

struggling to keep up with industry’s proper utilization rate as these players have a lack of

economics of scale and scope to run their business. The nature of our country geographic profile

that consists of many islands and thousands of islets poses a logistical challenge for delivering

products to their desired market target that makes the positioning of cement and clinker mills a

critical issue for Indonesian cement players.

Fig. 40: Demand, Excess Capacity, and Market Share of Ex-Java Fig. 41: Regional Demand, Excess Capacity, and Market Share

Source : ASI, CEIC, Indo Premier Source : ASI, CEIC, Indo Premier

Fig. 42: Sumatera Volume(mt) and Its Market Share Fig. 43: Ex- Java and Sumatera Volume (mt) and Market Share

Source : ASI, CEIC, Indo Premier Source : ASI, CEIC, Indo Premier

0%

5%

10%

15%

20%

25%

(5)

-

5

10

15

20

25

Sumatera Borneo Eastern Indonesia

Demand (mt) Excess Capacity (mt) Market Share (%)- RHS

0%

10%

20%

30%

40%

50%

60%

(5.0)

5.0

15.0

25.0

35.0

45.0

55.0

65.0

75.0

85.0

Java Sumatera Ex- Java and Sumatera

Demand (mt) Excess Capacity (mt) Market Share (%)- RHS

20.5%

21.0%

21.5%

22.0%

22.5%

23.0%

23.5%

24.0%

-

2

4

6

8

10

12

14

16

18

20

Sumatera Sales Volume (mt) Market Share (%) - RHS

20.5%

21.0%

21.5%

22.0%

22.5%

23.0%

23.5%

24.0%

-

5

10

15

20

25

Ex- Java and Sumatera Volume (mt) Market Share (%) - RHS

Cement Sector Update

14 Refer to Important disclosures on the last of this report

Furthermore, this problem is compounded with the product nature that is unable to last long that

raises the need of special inventory facility (storage silos in desired market targets). So, extensive

logistical (sea ports, logistical ships, etc.) and packaging facility are essential to maintain operational

efficiencies. The absence of these critical aspects makes it hard for second-tier (both Chinese- and

domestic-based) players to sustain their operational efficiency, let alone achieving profitability. It is

reflected on consistently a lower sales-to-installed capacity of second-tier players that decouples in

trend with first-tier players (fig. 46) compared to first-tier players (Indocement, Semen Holcim, and

Semen Indonesia). On average, the sales-to-installed capacity of second-tier players (at 64%) has

been 19% lower than first-tier players (at 83%) for the last seven years. This ratio

underperformance is particularly pronounced for second-tier Chinese players (fig. 47) whose

capacity is always below 60% as we think the strategy of invading West Java market is

inappropriate for players without proper scope and scale.

The harsh competition environment in Java had caused several second-tier cement players lurches

forward to maintain their operation, if not ceased their activity and went bankrupt. For instance,

Anhui Conch operations are on the brink of the ending of tax holiday period which adds pressure to

maintain their operations and profitability. Semen Bosowa and Gombong’s loan performances had

recently been declared non-performing at several banks at which they are now seeking a strategic

investor to help them sustaining the operation.

This development together with recently announced merger of Semen Indonesia and Lafarge Holcim

Indonesia are positive for the industry supply outlook as post-merged Semen Indonesia’s capacity

share (fig. 48) improves in Sumatera, West Java, Central Java, and East Java to 63%, 14%, 81%,

and 42%, respectively; compared to pre-merged capacity share of 56%, 0%, 64%, and 42%. Post-

merger Semen Indonesia’s aggregate capacity share also increases to 43% (from 31%).

Indocement, on the other hand, has an aggregate capacity share of 23% which comprises of West

Java and Borneo’s capacity share of 55% and 34%.

Fig. 44: Snapshot on Excess Capacity by Regions Fig. 45: First-tier and Second-tier Capacity Share (%)

Source : ASI, CEIC, Indo Premier Source : ASI, CEIC, Indo Premier

Fig. 46: Capacity Share with Sales-to-Installed Cap. (%) Fig. 47: Chinese Player Utilization Rate (Conch and Jui Shin)

Source : ASI, CEIC, Indo Premier Source : ASI, CEIC, Indo Premier

0%

10%

20%

30%

40%

50%

60%

(10.0)

-

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

W. Java C. Java E. Java Java Sumatera Borneo Eastern

Indonesia

Demand (mt) Excess Capacity (mt) Market Share (%)- RHS

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

F

20

19

F

20

20

F

20

21

F

Share of First-tier Players (% total Installed Cap.) Share of Second-tier Players

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

First-tier Players (mt) Second-Tier Players (mt)

First-tier Sales to Installed Capacity (%) - RHS Second-tier Sales to Installed Capacity S(%) - RHS

-10%

0%

10%

20%

30%

40%

50%

60%

70%

-

0,5

1,0

1,5

2,0

2,5

3,0

3,5

4,0

4,5

Sales Volume (mt, 4-q rolling) Sales to Installed Capacity (%)

Cement Sector Update

15 Refer to Important disclosures on the last of this report

Fig. 48: Capacity Share of First-tier Players in Overcapacity Regions

Source : ASI, CEIC, Indo Premier

Fig. 49: Capacity Share of Second-tier Players in Overcapacity Regions

Source : ASI, CEIC, Indo Premier

First-tier capacity share for West Java, East Java and Sumatera (account for 89% of nation-wide

overcapacity) are then gauged at 69%, 81%, and 63%, respectively, post industry consolidation. In

addition, The first-tier players are now consisting of only two players (Indocement and Semen

Indonesia) that enable better coordination to control regional supply growth, if not on nation-wide

scale, as we also see that second-tier capacity share is only strong on several regions (fig. 49). We

believe an increased pricing power will be the by-product of both better supply control by first-tier

players and reduced second-tier players’ retail product presence as their operation topple over with

specific intra-company problems as main consequence of initiating a price wars with lack of scale

and scope.

0%

20%

40%

60%

80%

100%

Sumatera

Sulawesi

BorneoW. Java

E. Java

Pre-merged SMGR INTP Post-merged SMGR First-tier Players

0%

10%

20%

30%

40%

50%

60%

70%Sumatera

Sulawesi

Borneo

W. Java

E. Java

C. Java

Second-tier Players

Fig. 50: First-tier Sales-to-Installed Capacity Fig. 51: Second-tier Sales-to-Installed Capacity (%)

Source : ASI, CEIC, Indo Premier Source : ASI, CEIC, Indo Premier

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

-

10

20

30

40

50

60

70

Sales Volume (mt) Excess Capacity (mt)

Sales-to-Installed Capacity (%) - RHS

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

(3)

2

7

12

17

22

27

32

37

42

Sales Volume (mt) Excess Capacity (mt)

Sales-to-Installed Capacity (%) - RHS

Cement Sector Update

16 Refer to Important disclosures on the last of this report

Thus, we forecast a flat supply growth at 3-yr CAGR FY18-21F of 2.7% (2019: 113mt; +4.7% yoy)

to 116mt in 2021F (2017: 107mt) to account the industry development, with additional capacity of

1.5mt from Semen Kupang third facility and Anhui Conch additional Sepinang and Merak cement

mills of 3.6mt and 0.8mt, in FY19F and FY21F. Though, we question their capability to assume the

operation of these additional cement mills. We assumed no additional capacity for first-tier players

for the forecasted periods and also narrow down industry excess capacity to 38mt in 2021F (2017:

41mt) with the expected improvement for first-tier players and deterioration for second-tier players

in their excess capacity of 8mt (2017: 18mt) and 30mt (2017: 23mt), respectively.

Industry competition landscape: first-tier players are the winner from industry consolidation

We view Indonesian cement industry has an oligopoly-alike market structure because the industry

has the number of sellers that are originally few (prior to the incoming of Chinese players),

homogeneous product offered, high barrier entries, and some firms hold pricing power attribute.

This oligopoly market structure puts competitive advantage as an important aspect to consider. The

need of mapping the competition is increasing after second-tier Chinese players settled their

presence in the region with aggressive expansion and predatory pricing strategy.

We first exhibit the sales performance of first-tier (fig. 52) and second-tier players (fig. 53) where

we can see that first-tier players generally outperformed their 10-yr compounded growth and the

otherwise for second-tier players prior to 2014. The trend suddenly changed for the period of 2015-

2017 where second-tier players was able to score above 30% growth in 2015 and 2016 while first-

tier players’ sales growth plummeted well below their compounded growth in pertaining period.

This change in trend can be explained by both of a commencement of second-tier Chinese players

(Juishin and Anhui) and some of foreign-JV second tier player (Siam Cement and Semen

MerahPutih) in 2015 with combined additional capacity of 6.9mt (c.10% of total capacity of 70mt in

2014) and government price intervention in curtailing the cement retail price as much as Rp3,000

per sack for SOE cement companies.

These led significant industry disruptions that were aggravated by predatory pricing strategy by the

newcomers (especially second-tier Chinese players). This pricing strategy proved to be effective to

establish some market position which can be seen on the bag (fig. 54) and bulk (fig. 55) volume

proportion of first-tier and second-tier players where Chinese players gained a share on national bag

and bulk sales with the larger proportion in bag format as they apply the pricing strategy at retail

level to gain brand recognitions. This effectively spurred a growth creation, albeit proven to be

short-lived, unsustainable growth.

Fig. 52: First-tier Sales Performance Fig. 53: Second-tier Sales Performance

Source : ASI, CEIC, Indo Premier Source : ASI, CEIC, Indo Premier

-6%

-1%

4%

9%

14%

19%

0

10

20

30

40

50

60

70

80

First-tier Player (mt) Growth (%, 10-yr CAGR) Growth (% yoy)

-10%

0%

10%

20%

30%

40%

50%

60%

0

2

4

6

8

10

12

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018F2019F2020F2021F

Second-Tier Player (mt) Growth (%, 10-yr CAGR) Growth (% yoy)

Cement Sector Update

17 Refer to Important disclosures on the last of this report

This unsustainable growth quality of second-tier players is attributable to several facts. We view

newcomers’ predatory pricing strategy is inappropriate for oligopoly market structure that rely on

economics of scope and scale to gain both market share and price power over the market. These

aspects are not owned by most of second-tier players. The scope relates to how well the business

can distribute the cost over the quantity produced that operates as a function of their mills (both

clinker and cement) capacity and location, logistical network and capability, as well as bargaining

power to suppliers. The mills location is particularly important as it defines their home market and

confines their market exploration. This aspect dictates the players’ product presence which is one of

the key success to maintain market share as we believe the customers is not only price-sensitive

but they also value the consistency in product presence at retail level as most people are still

purchasing cement in proximity to their residential area and it is confirmed by the survey by

Indonesian Statistical Bureau.

In conjunction with the way of home ownership is acquired (fig. 25), Indonesian Statistical Bureau

(BPS) also conducts another survey on the payment plan for the purchased home (fig. 58) where we

see that people build their home themselves and opted the cash payment across region, especially

in rural area. In our view, this implies that people are still purchasing the home material input

nearby their locality as this case is particularly relevant for rural area which we believe cement

players that has extensive presence across regions will be directly benefited.

Fig. 54: Bag Volume Share of First-tier and Second-tier Fig. 55: Bulk Volume Share of First-tier and Second-tier

Source : ASI, CEIC, Indo Premier Source : ASI, CEIC, Indo Premier

Fig. 56: First-tier Sales Proportion by Bag and Bulk Fig. 57: Second-tier Sales Proportion by Bag and Bulk

Source : ASI, CEIC, Indo Premier Source : ASI, CEIC, Indo Premier

94% 93% 92% 91% 91% 91% 92% 92% 89%83% 81% 80%

6% 7% 8% 9% 9% 9% 8% 8% 10% 13% 14% 13%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 9M18

First-tier Second-tier Chinese Second-tier Ex-Chinese

94% 95% 94% 94% 94% 93% 92% 92%85%

80% 79% 81%

6% 5% 6% 6% 6% 7% 8% 8% 11%16% 15% 13%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 9M18

First-tier Second-tier Chinese Second-tier Ex-Chinese

83% 84% 84% 83% 81% 80% 79% 78% 77% 76% 76% 73%

17% 16% 16% 17% 19% 20% 21% 22% 23% 24% 24% 27%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 9M18

Bag Bulk

82%89% 87% 89% 86% 84%

79% 79%71% 72% 73% 74%

18%11% 13% 11% 14% 16%

21% 21%29% 28% 27% 26%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 9M18

Bag Bulk

Cement Sector Update

18 Refer to Important disclosures on the last of this report

Fig. 58: Survey on Home Purchasing Plan (BPS, 2016)

Source : BPS, Indo Premier

We observed that most of second-tier players base their mills in Java region where their direct

competitors are the first-tier players that have an advantage of well-established brand recognition,

distribution channel, and have printed strong retail presence for a long time. To understand this, we

present the seaport and packing plant location of first-tier player to give a picture of how well their

distribution capabilities are (fig. 59).

Fig. 59 : Packing Plants and Sea Ports Facilities of First-tier Players

Source : Companies, Indo Premier

Second-tier players found a hardship to establish an extensive retail presence given their lack of

scale and scope together with weak distribution channel. We believe first-tier players are in the

great position to capture the advantage of post industry consolidation that further enhances their

product retail presence given the resulted synergy of Semen Indonesia and Lafarge Holcim

Indonesia’s extensive distribution networks.

Second-tier players also found it hard to pass through some of the costs to their product. This is

specifically a main challenge of second-tier Chinese players that see more pressures on profitability

as the result of their pricing strategy (even Holcim Indonesia only managed to book a break-even on

operating-level as of 9M18). We present the several cost ratio as of sales for cement listed

companies (most of them are first-tier players with Semen Baturaja as the only second-tier player)

to give a glance on their costs structure.

Region Cities Rural Cities Rural Cities Rural Cities Rural

Sumatera 57% 71% 29% 5% 11% 20% 3% 4%

Java ex G. Jakarta 62% 90% 32% 4% 5% 4% 1% 2%

Bali, NTT, and NTB 37% 63% 53% 11% 9% 24% 1% 2%

Borneo 55% 77% 30% 2% 12% 19% 3% 2%

Sulawesi 51% 82% 44% 1% 3% 13% 1% 3%

Papua and Maluku 72% 77% 15% 0% 9% 9% 3% 14%

Indonesia 59% 82% 34% 4% 6% 11% 2% 3%

Cash Mortgage Non-mortgage Installment Others

Cement Sector Update

19 Refer to Important disclosures on the last of this report

The two costs that serve as critical factor in shaping profitability are energy usage and logistical

costs as these costs altogether occupy about 30-40% of the sales, with the exception of Semen

Baturaja of 15% of sales as these company frequently engages in clinker purchase from other

parties (related or third-parties). As we can see on the energy costs trend (fig. 60), Indocement,

who has reasonably achieved proper scale and scope, carries highest energy costs proportion as of

sales over time compared to Semen Indonesia and Baturaja that are SOEs which have better

bargaining power to suppliers as the nation’s major energy input producers (coal, electricity, fuels,

and gas) is also SOEs.

Logistical cost is another important thing to watch (fig. 61) as we can see Indocement again has the

largest logistical costs as of its sales. This is partly due to the location of its mills (fig. 37) and

seaport location (fig. 59) that are heavily concentrated in Java region, but markets its product

across islands. While, Semen Baturaja is able to keep their logistical low despite having a

concentrated mills location (fig. 37), because Semen Baturaja places a focused operational location

exclusively in South Sumatera which does not entail transporting the products inter-islands.

We thus view second-tier players to encounter difficulties to stay afloat in business with such a low

mills utilizations (below 40% in 2017, depicted in fig. 46). Moreover, we deem second-tier Chinese

players to be under more pressure as we noted that Anhui Conch started its investment in 2011

granted with tax holiday for 7 years. It means Anhui will have to start paying taxes for running its

operation in this year. We believe the end of tax holiday period will soon come for the other Chinese

players. The combination of low utilization, leverage on the books, and the end of tax holiday period

should hamper the second-tier players to aggressively implement aggressive pricing and capacity

expansion. Thus, we expect some price recoveries and subdued supply growth for Indonesian

cement industry in foreseeable future in which we believe first-tier players will lead the price and

supply control post industry consolidation and readily monetize this momentum to improve their

profitability.

Company Positioning

Semen Indonesia will be our top pick this year and Semen Baturaja is our least preferred pick for those seeking an exposure in sector

The industry consolidation should enable selective recovery for Indonesia cement players. We think

this should give more benefit for the players who have the attributes of extensive production and

logistical facilities. We opt for Semen Indonesia as our top pick as we consider this company has the

aforementioned attributes. In the event of the merger with Semen Holcim, we should expect further

rising on scale and scope of Semen Indonesia. Semen Holcim, in turn, should also expect some

synergies with Semen Indonesia.

We also noted that the Holcim brand usage will be ceased in 2020 though we believe that

Indonesian customers are price sensitive rather than brand sensitive. As a result, the company who

can offer the product with lower price relative to the competitors and consistent in the retail

presence should win over the market which we think Semen Indonesia is able to do those things and

better prepared to capitalize on this industry consolidation momentum.

Fig. 60: Energy Costs as of Sales (%) Fig. 61: Logistical Costs as of Sales (%)

Source : Companies, Indo Premier Source : Companies, Indo Premier

0%

5%

10%

15%

20%

25%

30%

35%

SMGR INTP SMBR

0%

2%

4%

6%

8%

10%

12%

14%

16%

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018F 2019F 2020F 2021F

SMGR SMCB INTP SMBR

Cement Sector Update

20 Refer to Important disclosures on the last of this report

We take into account the industry consolidation by placing higher volume share for Semen Indonesia

and flat volume share for Indocement, Semen Baturaja, and Semen Holcim. We reason that the

synergy created from the merger of Semen Holcim and Semen Indonesia will enable Semen

Indonesia to strengthen their product presence through joining the extensive logistical hub of both

companies. Specifically, Holcim owns a sea port facility in outermost of West Java (fig. 59) enables

both Semen Indonesia to cater its product (cement or clinker) to South Sumatera and a cement

mills facility in Naragong (fig. 37), West Java that should be used to further solidify Semen

Indonesia presence in Java, with the cautions on persistent and pervasive competition. We account

this by lowering Semen Indonesia’s volume share to approximate Indocement’s share as we assume

price recovery in the region that entails with a slight reduction in volume share.

We should expect an improvement in both Sumatera (fig. 64) and Ex-Java/Sumatera volume share

of Semen Indonesia (fig. 65). Semen Indonesia will be able to extend its presence in Northern

Sumatera by utilizing Holcim’s facility in Andalas for both domestic sales and foreign sales.

Meanwhile, other companies should see a gradual increase in the region over time. For the Ex-

Java/Sumatera region, the industry consolidation will result to a more efficient means to cater the

product outside Java to Borneo region through the joint used of both Semen Holcim and Indonesia

seaport and packing plant facilities (fig. 59).

We thus expect significant improvement in Ex-Java/Sumatera volume share for Semen Indonesia

and gradual increase for both Indocement and Semen Holcim in forecasted period. In sum, we view

the holistic-oriented marketeering players (Semen Holcim and Semen Indonesia) should be able to

hike its national volume share while clustered-oriented marketeering players (Indocement and

Semen Baturaja) should see a flat trend over its national volume share (fig. 66).

Fig. 62: Volume Share of Our Coverage Fig. 63: Java Volume Share of Our Coverage

Source : Companies, Indo Premier Source : ASI, Companies, Indo Premier

Fig. 64: Sumatera Volume Share of Our Coverage Fig. 65: Ex-Java & Sumatera Volume Share of Our Coverage

Source : ASI, Companies, Indo Premier Source :ASI, Companies, Indo Premier

44% 45%43%

41% 41%

44% 44%42% 43% 44%

40% 40% 41% 42%

32%30% 31% 32% 32%

30% 30%

27% 26% 25% 26% 26% 26% 26%

14% 14% 14%16% 16% 15% 15% 14%

12%15% 15% 15% 15% 15%

3% 3% 3% 3% 2% 2% 2% 2% 3% 3% 3% 3% 3% 3%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

SMGR INTP SMCB SMBR

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018F 2019F 2020F 2021F

SMGR INTP SMCB SMBR

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018F 2019F 2020F 2021F

SMGR INTP SMCB SMBR

0%

10%

20%

30%

40%

50%

60%

70%

80%

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018F 2019F 2020F 2021F

SMGR INTP SMCB SMBR

Cement Sector Update

Refer to Important disclosures on the last of this report

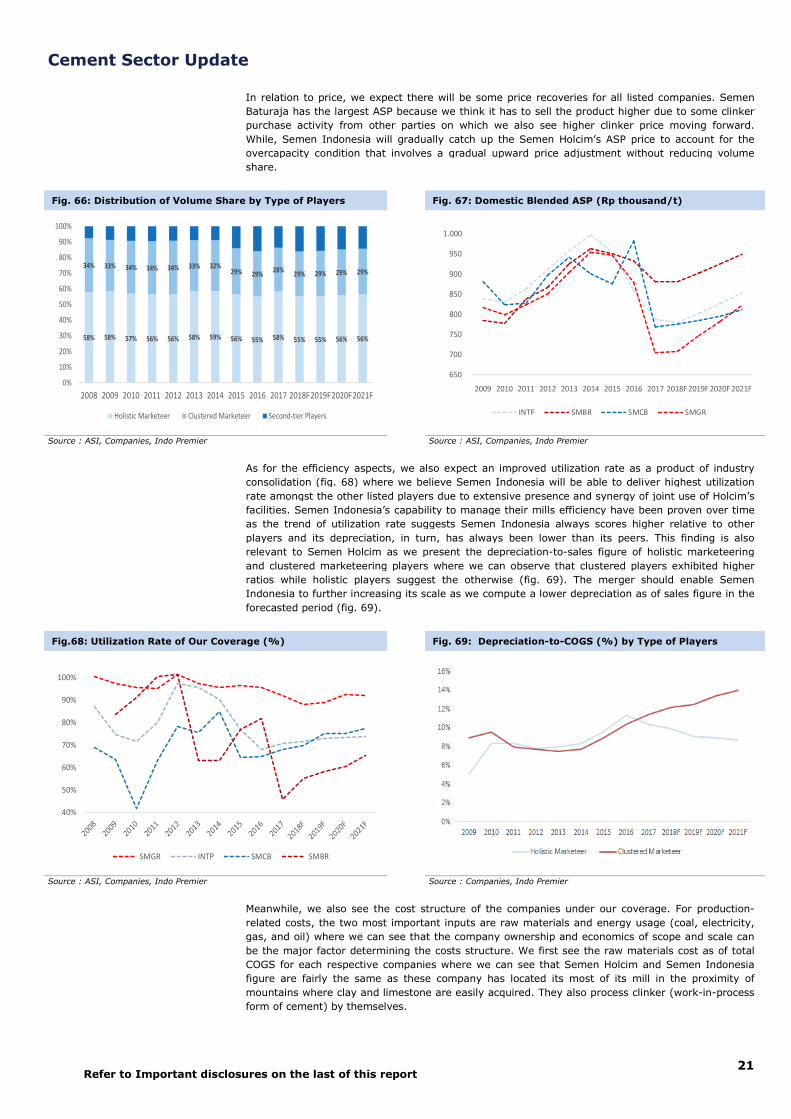

In relation to price, we expect there will be some price recoveries for all listed companies. Semen

Baturaja has the largest ASP because we think it has to sell the product higher due to some clinker

purchase activity from other parties on which we also se

While, Semen Indonesia will gradually catch up the Semen Holcim’s ASP price

overcapacity condition that involves a gradual upward price adjustment without reducing volume

share.

As for the efficiency aspects, we

consolidation (fig. 68

rate amongst the other listed players due to extensive presence and synergy of joint use of Holcim’s

facilities. Semen Indone

as the trend of utilization rate suggests Semen Indonesia always scores higher relative to other

players and its depreciation, in turn, has always been lower than its peers.

relevant to Semen Holcim as we present the depreciation

and clustered marketeering players where we can observe that clustered players exhibited higher

ratios while holistic player

Indonesia to further increasing its scale as we compute a lower depreciation as of sales figure in the

forecasted period

Meanwhile, we also see t

related costs, the two most important inputs are raw materials and energy usage (coal, electricity,

gas, and oil) where we can see that the company ownership and economics of scope and s

be the major factor determining the costs structure. We first see the raw materials cost as of total

COGS for each respective companies where we can see that Semen Holcim and Semen Indonesia

figure are fairly the same as these company has located

mountains where clay and limestone are easily acquired. They also process clinker (work

form of cement) by themselves.

Fig. 66: Distribution of Volume Share by Type of

Source : ASI, Companies, Indo Premier

Fig.68: Utilization Rate of Our Coverage (%)

Source : ASI, Companies, Indo Premier

58% 58% 57% 56% 56% 58% 59% 56% 55% 58%

34% 33% 34% 34% 34% 33% 32%29% 29%

28%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Holistic Marketeer Clustered Marketeer Second-tier Players

40%

50%

60%

70%

80%

90%

100%

SMGR INTP SMCB

disclosures on the last of this report

In relation to price, we expect there will be some price recoveries for all listed companies. Semen

Baturaja has the largest ASP because we think it has to sell the product higher due to some clinker

purchase activity from other parties on which we also see higher clinker price moving forward.

While, Semen Indonesia will gradually catch up the Semen Holcim’s ASP price

overcapacity condition that involves a gradual upward price adjustment without reducing volume

As for the efficiency aspects, we also expect an improved utilization

nsolidation (fig. 68) where we believe Semen Indonesia will be able to deliver highest utilization

rate amongst the other listed players due to extensive presence and synergy of joint use of Holcim’s

facilities. Semen Indonesia’s capability to manage their mills efficiency have been proven over time

as the trend of utilization rate suggests Semen Indonesia always scores higher relative to other

players and its depreciation, in turn, has always been lower than its peers.

relevant to Semen Holcim as we present the depreciation-to-sales figure of holistic marketeering

and clustered marketeering players where we can observe that clustered players exhibited higher

ratios while holistic players suggest the otherwise (fig. 69).

Indonesia to further increasing its scale as we compute a lower depreciation as of sales figure in the

forecasted period (fig. 69).

Meanwhile, we also see the cost structure of the companies under our coverage. For production

related costs, the two most important inputs are raw materials and energy usage (coal, electricity,

gas, and oil) where we can see that the company ownership and economics of scope and s

be the major factor determining the costs structure. We first see the raw materials cost as of total

COGS for each respective companies where we can see that Semen Holcim and Semen Indonesia

figure are fairly the same as these company has located its most of its mill in the proximity of

mountains where clay and limestone are easily acquired. They also process clinker (work

form of cement) by themselves.

ype of Players Fig. 67: Domestic Blended ASP (Rp thousand/t)

Source : ASI, Companies, Indo Premier

Fig. 69: Depreciation-to-COGS

Source : Companies, Indo Premier

55% 55% 56% 56%

29% 29% 29% 29%

2017 2018F2019F2020F2021F

Second-tier Players

650

700

750

800

850

900

950

1.000

2009 2010 2011 2012 2013

INTP SMBR

SMBR

21

In relation to price, we expect there will be some price recoveries for all listed companies. Semen