indo rama synthetics (india) ltd. quarter 3 results : 2006-07 investor release 19 january, 2007

TRANSCRIPT

Indo Rama Synthetics (India) Ltd.

Quarter 3 Results : 2006-07

Investor Release

19 January, 2007

2

2

Agenda

1. Crude & Raw Material Outlook

2. Emerging Polyester Scenario

3. Update on Indo Rama Synthetics

Expansion Project

4. Indo Rama Synthetics - Financial

Performance Q3 07

3

3

Crude & Raw Material Outlook

4

4

500

600

700

800

900

1,000

1,100

1,200

25

30

35

40

45

50

55

60

65

70

75

PTA

Crude Oil

Behaviour of PTA & Crude Oil Prices

• 30% fall in PTA prices since September 06 : showing signs of better margins, augurs well for downstream in the petrochemical cycle

• Falling crude oil price pushes down Paraxylene prices resulting in softening PTA Prices

5

5

Improved PTA availability

World Asia

Supply Surging ahead of demand – likely softening of prices

6

6

0

200

400

600

800

1000

1200

1400

1600

1800

2002 2003 2004 2005 2006 2007 2008

$/T

on

ne c

fr A

sia

Inv Asia Spot Asia Contract

‘000 Tonnes

World MEG Inventory & Demand at maximum EO rates

Rising Projected Inventory likely to Soften MEG prices

7

7

Summary of Raw Material Outlook

Crude Oil : 36% decline from the peak of $78 in August 06

PTA : 30% decline in the price of PTA since September 06

Further softening of PTA prices expected with Supply increasing at faster pace than demand

MEG : prices likely to soften with increasing inventory

8

8

Emerging Polyester Scenario

9

9

Likely Duty Corrections in the Union Budget would be a Demand Booster for Polyester Industry

Current Excise duty Expected Excise duty after budget

Polyester 8% 4%

PTA 8% 4%

MEG 12% 4%

Cotton 4% 4%

10

10

World Polyester Demand & Supply

Globally Polyester Demand is forecast to go up steadily after the bottoming out in 2005/2006

11

11

Polyester tolling margins at historical low

All time low Polyester margins is leading to closure of plants in Korea, Taiwan and USA creating big opportunity for Indian Polyester Industry

12

12

Update on Indo Rama Synthetics Expansion

Project

13

13

Status of Polyester expansion project Commercial Production of POY plant started in

November 2006 PSF plant likely to be commissioned in February 2007. Rs. 747.10 Crore has been incurred on the polyester

expansion project till December 2006.

Status of Power Project of Indo Rama Petrochem Ltd. Consists of two units of 15 MW each Unit 1 was commissioned in the last week of

December 2006. Unit 2 is expected to be commissioned by mid of

March 2007. This will ensure an uninterrupted power supply to be

available to IRSL at competitive rate

14

14

Indo Rama Synthetics – Financial Performance Q3

07

15

15

ParticularsQ3 2006-07

Q3 2005-

06

Domestic Sales 506.42 376.52

Export Sales 69.04 13.79

Gross Turnover

575.45

446.18

Less : Excise Duty on Sales 38.54 47.73

Net Turnover

536.91

398.45

Other Income 37.09 19.66

Total Income 574.00 418.11

(Increase) / Decrease in Stock- in-Trade (25.22) (52.10)

Movement in Excise Duty on Stocks 3.86 8.04

Raw - materials 468.10 347.58

Staff Cost 9.72 8.47

Other Expenditure 71.97 68.38

Total Expenditure 528.43 380.37

Financial Highlights – IRSLRs. Crores

16

16

Financial Highlights – IRSLRs. Crores

Particulars Q3 2006-07

Q3 2005-

06

EBDITA

45.57

37.74

Interest 12.67 5.01

EBDT

32.90

32.73

Depreciation 28.01 25.00

Profit Before Tax (PBT) 4.89

7.73

Provision for Taxation

-MAT 0 0

-FBT 0.20 0.20

-Deferred Tax 1.65 2.90

Profit after Tax (PAT) 3.04 4.63

17

17

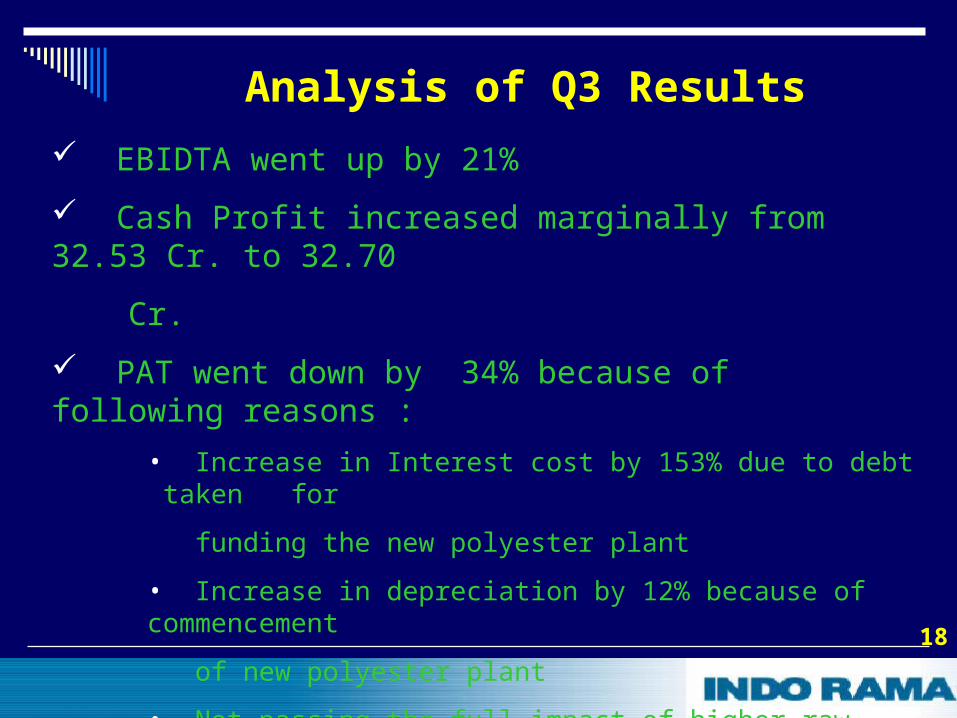

Analysis of Q3 Results

Significant achievement of placing the enhanced capacity by penetrating new markets

35% increase in net turnover

47% increase in net sales after adjusting for the

merchant sales of 55.87 cr in Q3 of 2005-06

37% increase in sales volume

34% increase in domestic sales

401% surge in exports

48% increase in production volume

18

18

Analysis of Q3 Results

EBIDTA went up by 21%

Cash Profit increased marginally from 32.53 Cr. to 32.70

Cr.

PAT went down by 34% because of following reasons :

• Increase in Interest cost by 153% due to debt taken for

funding the new polyester plant

• Increase in depreciation by 12% because of commencement

of new polyester plant

• Not passing the full impact of higher raw material prices at their

peak to significantly increase the market share

19

19

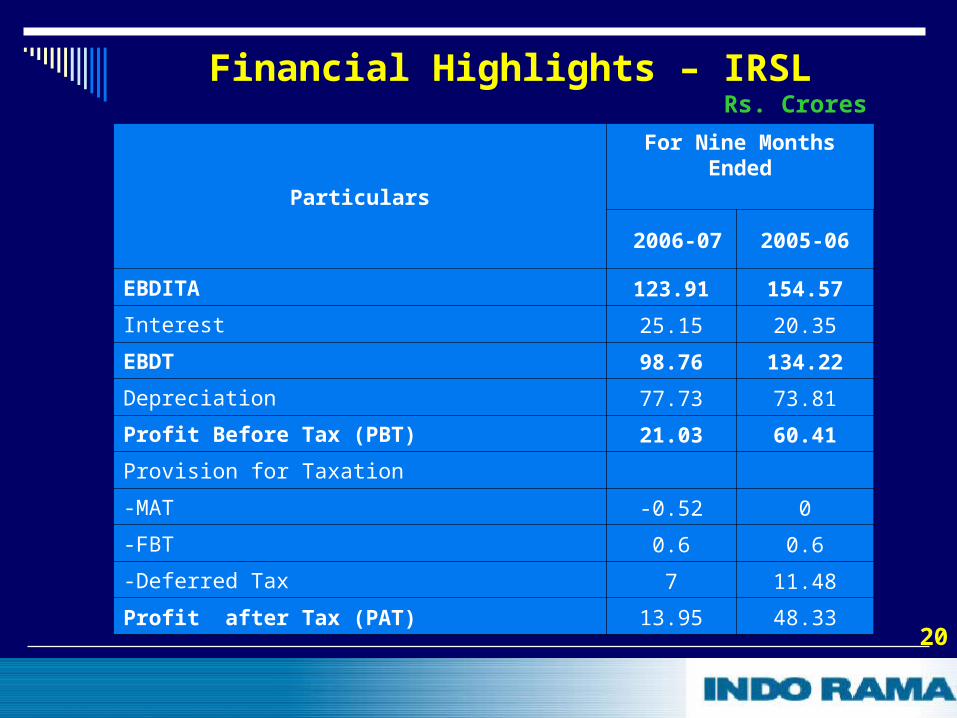

Financial Highlights – IRSLRs. Crores

Particulars

For Nine Months Ended

2006-07 2005-06

Domestic Sales 1385.05 1401.34

Export Sales 89.09 28.60

Gross Turnover 1,502.47 1,538.21

Less : Excise Duty on Sales 104.15 183.89

Net Turnover 1,398.32 1,354.32

Other Income 38.41 53.98

Total Income 1436.73 1408.30

(Increase) / Decrease in Stock- in-Trade

(124.72) 119.75

Movement in Excise Duty on Stocks 12.12 (23.16)

Raw - materials 1,193.91 955.77

Staff Cost 28.76 24.51

Other Expenditure 202.75 176.86

Total Expenditure 1,312.82 1,253.73

20

20

Financial Highlights – IRSLRs. Crores

Particulars

For Nine Months Ended

2006-07 2005-06

EBDITA 123.91 154.57

Interest 25.15 20.35

EBDT 98.76 134.22

Depreciation 77.73 73.81

Profit Before Tax (PBT) 21.03 60.41

Provision for Taxation

-MAT -0.52 0

-FBT 0.6 0.6

-Deferred Tax 7 11.48

Profit after Tax (PAT) 13.95 48.33

21

21

Analysis of YTD Results

3% increase in net turnover

Exports surged by 211%

EBDITA decreased by 20%

Interest cost gone up by 24%

Depreciation marginally up by 5%

PBT declined by 65%

PAT fell by 71%

22

22

House Open for Questions