indian solar manufacturing : revitalization

TRANSCRIPT

6st Dec 2013

Under the Guidance of

Professor P. D. Jose

Submitted by

Dhiraj Kumar Pal (1211337)

Amrapali Bhowmik (1211246)

Clio Morfino (12E5302)

Vagish Sharma (12E5319)

Moser Baer: Reviving Domestic Manufacturing with eco-sensitive strategy

Table of Contents

Indian Energy Scenario .............................................................................................................................................................................. 2

Energy Security .......................................................................................................................................................................................... 2

Renewable energy sources in India ........................................................................................................................................................... 3

Solar Energy ............................................................................................................................................................................................... 3

National Solar Mission ........................................................................................................................................................................... 3

Domestic manufacturing ........................................................................................................................................................................... 4

Solar cell Technology: Future Outlook ....................................................................................................................................................... 4

Disaster in waiting ...................................................................................................................................................................................... 5

Manufacturing Hazards ......................................................................................................................................................................... 5

Crystalline Silica Cells ........................................................................................................................................................................ 5

Thin film Technology ......................................................................................................................................................................... 5

Usage Hazards ....................................................................................................................................................................................... 5

Hazards at disposal stage ...................................................................................................................................................................... 6

End-of-life hazards for Solar PV ............................................................................................................................................................. 6

Other Concerns .......................................................................................................................................................................................... 6

Land use pattern and utilization ............................................................................................................................................................ 6

Water balancing .................................................................................................................................................................................... 6

Interference with desert ecosystem ....................................................................................................................................................... 6

Existing regulations .................................................................................................................................................................................... 6

Regulation in other nations ....................................................................................................................................................................... 7

China Case ............................................................................................................................................................................................. 7

Californian case ..................................................................................................................................................................................... 7

European case ....................................................................................................................................................................................... 7

Risk Life Cycle Assessment ......................................................................................................................................................................... 8

Policy imperatives for India ....................................................................................................................................................................... 8

Domestic Manufacturing: Case for Sustainability ...................................................................................................................................... 9

Domestic Manufacturer: Moser Baer .................................................................................................................................................... 9

Issues & concerns ................................................................................................................................................................................ 10

Non- Market factor: Stakeholder Analysis ............................................................................................................................................... 11

Cost Benefit Analysis ................................................................................................................................................................................ 11

Conclusion ................................................................................................................................................................................................ 12

Recommendation..................................................................................................................................................................................... 12

a) Initiate discussions on waste management ................................................................................................................................ 12

b) Product insurance and take back clause ..................................................................................................................................... 13

c) R&D investments......................................................................................................................................................................... 13

d) Collaboration on common treatment plants .............................................................................................................................. 13

e) Switch to other renewable technologies ..................................................................................................................................... 13

f) Integrated Eco-industrial Park .................................................................................................................................................... 13

References ............................................................................................................................................................................................... 14

Endnotes .................................................................................................................................................................................................. 14

Indian Energy Scenario

Energy demand in India has been growing over the years and country is now placed fourth in terms of primary

energy consumption. On comparing this with world average of 1797 kilograms of oil equivalent (kgoe), India's

per capita consumption of 585 kilograms of oil equivalent (kgoe) is very low.

But, as per Planning Commission estimates consumption would rise to to 738.07 mtoe by 2016-171 and with

supply side bottlenecks there will be about 38 percent import reliance.

Country Primary Energy

Consumption

China 2210.3 mtoe

United States 2205.9 mtoe

Russian

Federation

644.4 mtoe

India 487.6 mtoe

Japan 474 mtoe

Country KGOE

United States 7034

Russian Federation 4559

Japan 3707

UK 3184

China 1698

Brazil 1240

India 585

World 1797

Table-1: Primary Energy Consumption of Top Five

Countries (2009)2

Table-2: Per Capita Energy Consumption (2009)3

Energy consumption in India is highly dependent on hydrocarbon fuels with only 10% made up by cleaner and

renewable sources.

Figure-1: Indian Energy Mix 4

Now, with huge growth in projected demands and impending import dependence, it seems reasonable that

emphasis needs to be given on sustainable abundant sources of energy.

Energy Security

Over the years challenges have emerged with lack in domestic coal production mainly attributed to

infrastructure constraints, also there are concerns of environmental in case of large hydro plants, thermal power

plant emissions and then heightened nuclear risk after Fukushima disaster. With existing supply-demand

imbalance in range of 12.7% peak deficits, situation is likely to worsen in near future. Add to it, 50% of

population has little or no access to commercial and majority others face erratic supplies.

To address all these requirements it is necessary to arrive at a prudent energy mix by harnessing renewable

sources which are resourceful domestically. However, high costs of energy generation associated with

renewable sources are a major restraint but supportive government policies will allow it to compete

economically with fossil fuels over time.

Integrated Energy Policy, 2006 was the first formal step by Indian govt. to rationalize domestic energy mix.

This was followed by institution of a full-fledged Ministry on New and Renewable Energy (MNRE) which is a

nodal agency to facilitate implementation of all programmes on renewable energy resources.

Renewable energy sources in India

Renewable energy can be derived from natural sources like water, sun, wind, geothermal, tidal, biofuels etc.

Being inexhaustible and replenish able source, they are clean and have no harmful effects on natural ecosystem.

As per govt. data, wind energy is the largest harnessed renewable source in India. But, supporting policies are

increasing contribution from Solar for past few years.

Figure-2: Contribution of various RES (on-grid) Source: www.mnre.gov.in (as on 30/9/2013)

Solar Energy

Annually about 5,000 trillion kWh5 of solar energy is incident on India with average insolation of about 4-7

kWh per sq. m per day over most of the land area. This makes it technologically feasible to convert this huge

reservoir of energy efficiently into heat and electricity by using solar PV and solar thermal systems. Also,

geographical location of India is such that major land mass receives the average insolation for 5 hours daily and

this presents a case for easy scalability.

National Solar Mission6

Given the context, government embarked on the ambitious goal by launching Jawaharlal Nehru National Solar

Mission. The objective was to develop solar energy as a competitive alternative for hydrocarbons based energy

sources. Additional advantage was that change in energy mix, will make development more inclusive as off-

grid systems will empower marginalized and deprived people.

The mission also earmarked goals for promoting R&D program in collaboration with leading researchers in the

field. Mission targets are:

68%

13%

4% 8%

7% 0.34%

Wind Small Hydro Biomass Bagasse Cogeneration Solar PV Other

Table-3: JNNSM Capacity Addition Target

7

Domestic manufacturing

India’s Solar PV industry is dependent on imported components, major one being the silicon wafers. And to

promote domestic manufacturing, the mission set a target of 4-5 GW equivalent manufacturing capacity by

2020. By March 2013, the total capacity has touched 2000 MW as per MNRE announcement.8

The break-up of different components are,

Table-4: Manufacturing Facility

9

However, India doesn’t have any poly-silicon production capacity and no capability in solar thermal projects;

but with new policies and sector will get boost to develop these alternate technologies.

Solar cell Technology: Future Outlook

Currently crystalline silicon is the most common technology, and its manufacturing processes are similar to that

of electronic circuitry industry. But, gradual advancements and better efficiencies are making the “thin-film”

cells as preferred choices.

c-Si : Crystalline Silicon

a-Si : Amorphous Silicon

CIS : Copper Indium Selenide

CIGS : Copper Indium Gallium Selenide

CdTe : Cadmium Telluride

Figure-4: Solar PV Module Technology10

However, the neglected piece of the growth story is the management of waste generated by solar PV technology

as no discussions is happening on the issue.

Disaster in waiting

Recent researches show that cell manufacturing uses raw materials that pose health hazards among living

organisms. In addition, the entire value chain is fraught with processes and systems that can be a threat to the

environment. Even the extraction process of silicon or constituent elements causes environmental damages

when trapped, underground toxic gases escape into atmosphere. Thus, a systematic analysis will help us in

determining other potential sources of hazards.

Manufacturing Hazards

Crystalline Silica Cells

Manufacturing process requires chemicals like Hydrogen Chloride and Chlorosilanes, which are toxic and

explosive in its reaction with water. Silicon Tetrachloride is also produced during the process which is a skin

irritant and can cause burns if exposed in high concentrations.

Figure-5: Crystalline Silicon Generation Process

11

In order to react the substances large temperatures are required that leads to energy waste. Sulfur hexafluoride

(SF6) is also a by-product in the process and is known for its more potent harmful greenhouse effect in

comparison to Carbon dioxide. Other constituents like ethyl vinyl acetate, nitrogen, hydrogen peroxide, titanium

dioxide etc too have been identified as hazardous.

Thin film Technology

The main element is cadmium which is known to have damaging effects on livers, lungs and kidneys. Also,

being new technology very limited information is available on the toxicity of cadmium telluride (CdTe).

Usage Hazards

Solar PV systems have complex electric circuitry and associated electrical systems like inverters, power

devices. There working is based on electromagnetic induction, which is known to have carcinogenic properties

on long term exposure.

Also, being an active circuit during solar insolation makes them very dangerous during fire as de-energizing is

very difficult. The elemental constituent, Ethyl Vinyl Acetate can easily form explosive mixtures with air under

such conditions.

Hazards at disposal stage

Components like Cadmium, Arsenic and Tellurium can interfere with the natural food chains because of their

toxicity and pose harmful long term consequences.

EU Classification/Labelling Dangerous Substances12

has identified Cadmium as extremely toxic and

carcinogenic.

End-of-life hazards for Solar PV

This is an important issue which has so far missed the industry notice. Much of the waste generated can be

categorized as e-waste and requires sophisticated mechanisms for disposal and recycling. Also, being a

hazardous waste only certified agencies have the capability to handle this. But, Indian scenario is not very

promising as only 5% of e-waste is handled by organized sector. Main reasons for this lackadaisical case are

ignorant society, tardy policy making and lack of recycling capacity.

With these concerns any rise in e-waste due to solar PV will surely aggravate the condition.

Other Concerns

Land use pattern and utilization

Solar plants require large tracts of land for electricity generation, as per technical estimates roughly 5 to 10

acres of land generates 1 MW13

. Following this with JNNSM’s ambitious target of 20 GW, land requirement

will rise to a whopping figure of 20 million sq. mt. 14

India is already land starved and growing urbanization is

straining arable area.

Moreover, land acquisition process is very archaic and calls for revolutionary changes to make it equitable with

the concerns of dislodged population.

When large areas are made available for solar plants, no major policy steps have been implemented to highlight

concerns on theissue of adequate compensation. Also, exploitation can’t be ruled out at hands of private parties

when acquisition is done in absence of any laid guidelines.

Water balancing

Solar thermal runs on similar energy cycles like coal based plants and thus will require large volumes of water

for cooling of systems. This restricts the choice of sites for putting up solar thermals and forces presence in

vicinity of water sources. The current thought process is narrow in sense that it considers only sun-rich areas of

Rajasthan or Gujarat,, but with scarce water availability, there’s seems to a mismatch in resource mapping .

Also, water is needed for cleaning & maintenance purposes and once large areas get covered with panels there

will be a proportional rise in demand. This concern is also neglected by the policy makers.

Interference with desert ecosystem

Desert topography and ecology is very sensitive, any external influences can greatly affect the local bio-

diversity. Cell surfaces are very shiny and often deceive aquatic insects as water source where they can lay their

eggs15

. This can be a major detriment to the life-cycle of the insects and lead to their extinction. With each

organism playing a role in local food-chain, this missing portion can interfere with the entire ecological balance.

However, current planning being a macro approach is indifferent to these aspects of ecosystem.

Existing regulations

The Environment Impact Assessment (EIA) Notification, 2009 is a landmark legislation to safeguard

environment and mandates regulatory clearance before any industrial activity, but even it neglects solar PV

plants under its ambit. With respect to hazardous chemicals, various schedules under Hazardous Chemical

Rules have failed to include cadmium compounds, silane, argon, selenide gas. Unregulated emissions of these

can have harmful effects on the environment and when discharged to water bodies become more potent as it

then easily enter the food chain of living organisms.

Regulation in other nations

China Case

Society has started witnessing the ill-effects of irresponsible behaviour of Industry and subsequently discussions

have started to put more scrutiny and onus on the manufacturing industry. Even govt. has started to take of this

Figure-6: Silicon Tetrachloride dumping in Henan, China16

issue where in one case a plant of Zhejiang Jinko Solar company in Haining city had to stop production when

public protested about the huge untreated toxic waste resulting from factory compound.17

Californian case

As per the regulations, manufacturers are accountable through a pre-financed extended producer responsibility

scheme (EPR), which would promote eco-design and would fund the needed infrastructures for the PV module

recycling.18

Subsequently, domestic recycling treatment will come under the regulation as a check on

irresponsible practices of illegal dumping and mishandling.19

The situation now is more tensed because SVTC (Silicon Valley Toxic Coalition) issued a report stating on the

toxicity levels of the main composite (cadmium and tellurium), which classifies the PV compounds as

hazardous waste. Therefore, authorities are considering the proposal for enforcing hazardous waste control

laws, through permit issuing and fee impositions (pre-financed collection scheme).20

,21

While waiting for the regulation’s final approval, Californian solar firms have begun planning and creating

coalitions to recycle used PV panels before leaching stage through various recycling methods suggested by the

Norwegian Geotechnical Institute (NGI).22

European case

European authorities have launched the EWL (European Waste Law), whose WEEE directive (waste for

electrical and electronic equipment) states that manufacturers must finance a system for collecting, processing,

recycling and disposing them (Take-Back policy). Moreover, producers, importers and distributors should give

incentives to design electrical and electronic equipment in a more environmentally efficient way. 23

Finally, increasing targets are fixed at a European level, for which treatment standards have to be met, as the

below regulation:

“Four years after the entry into force of the present directive, member states must collect annually 45% of the

average weight of electrical and electronic equipment placed on their national markets. Three years later,

member states are to achieve a 65% collection rate.”24

Thus, societies are at trending at different stages in their sensitization of the impending hazard.

Risk Life Cycle Assessment

It is very evident that India discussions are still nascent but other countries are gradually moving up the

trajectory. And with information becoming more easily accessible in digital age, there will not be substantial lag

when issue becomes pertinent in domestic arena. Now, when Indian manufacturers are facing existential threats

it is quite obvious that they too have failed to incorporate this non-market strategy. However, industry in

developed nations has started to include these developments as part of strategy to thwart competition from

cheaper and non-standard Chinese imports.

Figure-7: Issue Development Life Cycle Process25

Policy imperatives for India

The growing debate at world level presents high point for India to start rationalizing its solar mission policy.

Basic calculation to identify the potential waste India is likely to face,

Solar cell dimension = 1642 x 979 x 38 (mm) 26

Volume of one panel = 61085.68 cm3

Weight = 19 Kg

Wattage = 250 W 27

Number of panel for 1 MW = 4000

1 ton = 907185 g

Waste from 1 MW = 83 ton

When India fulfills solar mission’s commitment of 20 GW

Potential e-waste = 16, 60,000 tons

Thus, when the debate sets in, there will be amendment to all existing legislations like CRZ notification,

Hazardous Waste Rules, Chemical rules, factory rules to prevent the likely impact on humans and environment.

And this presents an ideal case for domestic manufacturers to proactively shape their sustenance by being

ecologically sensitive.

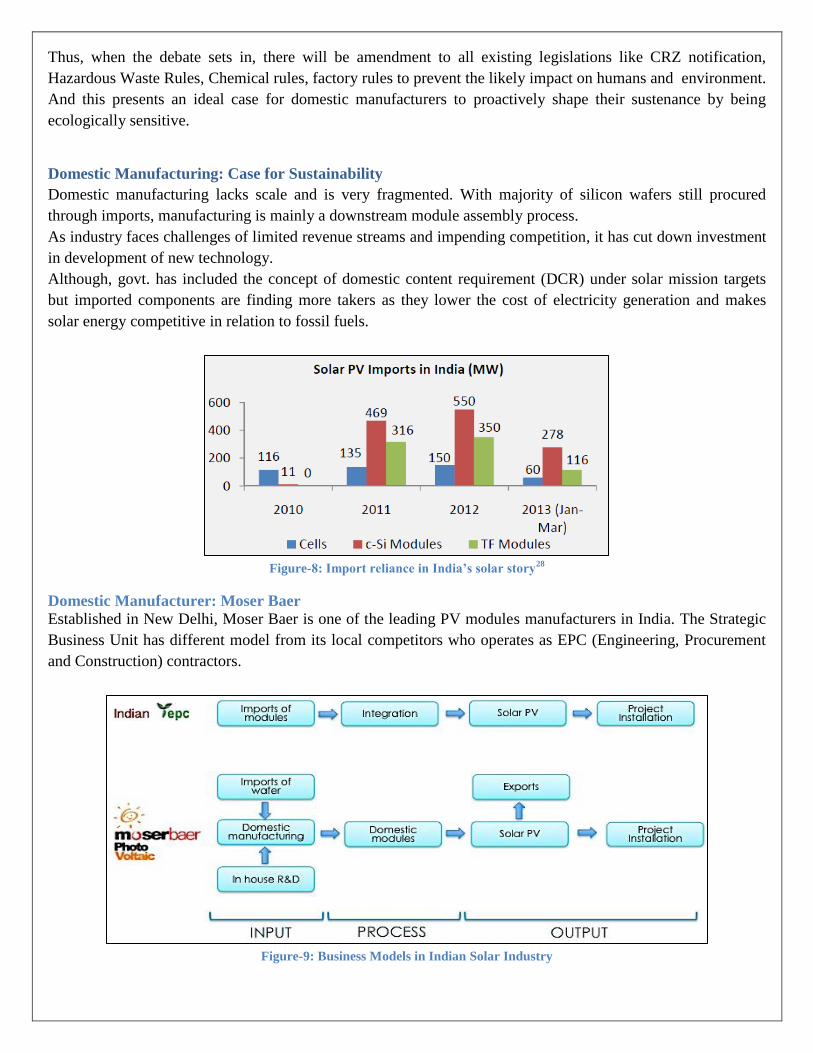

Domestic Manufacturing: Case for Sustainability Domestic manufacturing lacks scale and is very fragmented. With majority of silicon wafers still procured

through imports, manufacturing is mainly a downstream module assembly process.

As industry faces challenges of limited revenue streams and impending competition, it has cut down investment

in development of new technology.

Although, govt. has included the concept of domestic content requirement (DCR) under solar mission targets

but imported components are finding more takers as they lower the cost of electricity generation and makes

solar energy competitive in relation to fossil fuels.

Figure-8: Import reliance in India’s solar story

28

Domestic Manufacturer: Moser Baer

Established in New Delhi, Moser Baer is one of the leading PV modules manufacturers in India. The Strategic

Business Unit has different model from its local competitors who operates as EPC (Engineering, Procurement

and Construction) contractors.

Figure-9: Business Models in Indian Solar Industry

EPC contractor imports various parts and components, mostly from China, for their low cost advantage.

However, imported parts have concerns of quality, performance and longevity. The components are then

assembled and integrated and solar photovoltaic module is made ready for installation.

The value chain of Moser Baer (MB) is sensibly different and allows them to have a better control over

production costs, manufacturing processes, quality control and technological improvements. Moreover, their

manufactured items respect international quality standards and international certifications (ISO 9001:2000, SA

8000 and IEC certification). Also, thanks to its strategic alliances with American solar technology laboratories

and corporations, as Solfocus (high concentration photovoltaic tech.), Solaria (high efficiency solar tech.), Stion

Corporation (low cost high efficiency solar thin film panel) and HGS (High Gain Solar, producing durable and

easy to deploy solar systems), MB is able to complement the knowledge and capabilities. This allows the firm

to be at the forefront of technology and quality. However some compounds are still imported (from America

and Europe) because of the technological specificity and then assembled to be sold in domestic and

international market.29

30

MB implements as well recycling policies. As a member of PV Cycle, an international entity who promotes

voluntary waste management and recycling policies, Moser Baer is implementing a take-back policy which

applies nowadays just for the PV modules internationally sold. This initiative guarantees that every module at

the end of its life or warranty is recycled and its environmental impact minimized. This however, is not

practiced in India due to the lack of regulations. 31

Issues & concerns

Although, Moser Baer is a reckoning force in India, its plats are running below capacity. This is because of

higher module cost in comparison to Chinese imports, lower order book cascades into lesser plant utilization

and further higher cost. Another case is the dependency on imports of silicon wafers which exposes the firm to

exchange rate risks.

China meanwhile is going aggressive on capacity expansion and currently produces 3232

times more than what

local market demands. This additional capacity when operating under scale makes a threatening competitive

case for any countries domestic manufacturers as experienced in India.

Figure-10: Domestic manufacturing vis-à-vis global situation33

Non- Market factor: Stakeholder Analysis

Deriving learnings from stakeholder position in China and developed nations, gradual shift happens in the

positioning of various stakeholders. Under dormant case, courts and pollution regulators operate in the fringe

category and entire operating scope is managed by EPC, domestic manufacturers and government. But, when

India reaches Stage –III (fig.7), society activists will become stronger and shape the govt. policy through

collective voice and harsh steps will fall in place to regulate the sector.

Figure-9: Stakeholder Evolution34

Any such step will be life savior for domestic manufacturers as they have better technology and standard

products. But, analysis highlights that govt. role will mostly be reactive in nature and with no time certainty

many domestic manufacturers might fold by the time, succumbing to import competition. Thus, there is an

opportunity for Indian producers to take onus and initiate the discussion till now neglected from policy ambit.

Cost Benefit Analysis

A typical cost benefit analysis will more objectively validate this argument of how domestic manufacturers

should try and reclaim their share of market within the realms of sustainability. As per CERC benchmarkt,

installation costs have decreased over the years and driver is the 62% decrease in cost of PV module (import

phenomena). The guideline also misses any waste management cost.

S. No. Particulars (Crore/MW) 2010-11 2011-12 2012-13 2013-14

1 PV Modules 9.15 8.33 4.94 3.45

2 Land Cost 0.05 0.15 0.16 0.168

3 Civil & General Works 0.9 0.95 0.9 0.945

4 Mounting Structures 0.8 1.05 1 1.05

5 Power Conditioning Unit 1.8 1.6 0.98 0.6

6 Cables & Transformers 0.85 0.9 1 1.05

7 Preliminary & Pre-Operative Expenses 1.65 1.44 0.8 0.8

Total Capital Cost 15.2 14.42 9.78 8.058

Table-5: CERC benchmark capital cost for solar PV plants (as on 25/10/ 2012)35

Kerala Pollution Control Board has suggested that a capex of 10 crore is required for treating 1, 50,000 ton of

e-waste.36

Now, 1 MW generates = 83 ton of e-waste (proved earlier)

Therefore, capex cost per MW = Rs (10, 00, 00,000 ÷ 1, 50,000) x 83 = Rs 55,333

Also, we can find present value of investment that will be required at the end of life waste treatment for 1 MW

from waste management cost in U.K = Rs 12000 per ton (E-waste report in India)37

.

Using a discount rate of 9%, present value varies significantly with expected working life.

Expected Operating Life

Present Value of end-of-life

recycling cost (Lakh/MW)

5 yrs 10 yrs 15 yrs 20 yrs

6.49 4.22 2.74 1.78

Table-6: Present Value of end-of-life recycling cost

Conclusion

A careful observation presents this interesting point where treatment cost can vary for a player if his product

doesn’t function satisfactorily over stated lifetime. And, for any player per MW treatment plant installation cost

is less in comparison to per MW treatment cost.

Thus, a domestic manufacturer can pursue this idea of plant installation rather than accounting for treatment

cost. With current lack in capacity for e-waste treatment any plant can have alternate feeders for capacity

utilization. On the other hand, the imported product quality is unproven and concerns exist regarding

operational life. With no objective estimation, factoring for treatment cost is fraught with heavy risks and once

some parameter are developed, incorporation of ROI will push the prices for these imported components.

Indian products on the other hand have international certifications and reliable working life, which makes any

such waste treatment accounting a precise activity. According to industry sources any cost in excess of 50 Lakh

for a plant (avg. plant size in India is 15 MW) can bring domestic manufacturing at par competition with

cheaper imports.

Thus, Indian solar case can be a classic example where interplay of environment concern and sustainability is

markedly evident. Here, survival necessitates integration of non-market strategy and proactive engagement to

change industry course.

Recommendation

Following are some suggestion on how manner of strategy implementation based on time-lines and their

reasonability in achieving the intended objectives.

a) Initiate discussions on waste management

This strategy could be initiated on a short-term perspective. Replicating the Californian model, the company

would introduce the issue to the governmental authorities. With the debate, society will be also aware and more

involved in it. As a consequence, more efficient and durable products will be developed and will make domestic

manufacturers more competitive, thanks to their superiority in quality, performance and durability. Therefore,

this action will revitalize the Indian PV modules manufacturing sector and will promote the development of

new technologies for the recycling process.

The involved stakeholders will be:

- domestic manufacturers: new product developments and R&D expenditures;

- government : policy creation and implementation;

- pollution regulators: participation in the regulation discussion and set up of new standards.

b) Product insurance and take back clause

Moser Baer will provide a longer guarantee certifying the quality and the longevity (20 years) of its products.

This will redefine the industry standards and self-selection dynamics will force poor quality products (the

imported ones) to wind up. This will revitalize the domestic industry and strengthen the case of better quality

domestic components.

The stakeholders involved would be: domestic manufacturers, government, and consumers.

c) R&D investments

On a short/medium term, the company should invest more in R&D in order to improve the quality, longevity

and sustainability of the components, which will have more acceptability in the market. This will also help the

industry to gain learning curve advantage when more advanced technologies emerge.

d) Collaboration on common treatment plants

On a medium term perspective, the various Indian manufacturers should join their forces and invest collectively

in recycling and treatment facilities (as it is currently done in California, US). Moreover, they could lease their

recycling services to the EPCs or other e-waste generators at higher price. This will be an alternative income

stream, which could then be reinvested in the infrastructure improvement.

e) Switch to other renewable technologies

On a long run perspective, it would be necessary to convert the solar energy technologies into other ways as: 4th

generation nuclear plants, bio-fuels, small hydro, wind-offshore, geo-thermal which have tremendous potential.

However, such a shift is likely to take quite a long time to realize but will be beneficial in terms of waste

management and minimization.

f) Integrated Eco-industrial Park

By following the Kalundborg Eco-Industrial Park example, the waste derived from PV modules becomes the

raw material for another industry or re-enters in the value chain. The glass, for example, could be used in other

factories while the toxic compound could be chemically treated and recycled properly. Of course this could be

done on a more long-term perspective, but this model could have great potential for minimizing the

environmental impact and increasing the productivity of diversified industries.38

References

1. http://www.atkearney.com/utilities/ideas-insights/article/-/asset_publisher/LCcgOeS4t85g/content/solar-

power-in-india-preparing-to-win/10192#sthash.1SFEOYMH.dpuf

2. http://bridgetoindia.com/blog/?p=1791

3. http://www.semi.org/en/press/ctr_029193

4. India’s Energy Scenario in 2013 – Challenges & Prospects (Hydrocarbon Asia, Jan-Mar 2013)

5. http://www.thingsworsethannuclearpower.com/2012/09/the-real-waste-problem-solar-edition.html

Endnotes

1 IEC 2013 Securing tomorrow’s energy today: Policy & Regulations, Long Term Energy Security (Deloitte) 2 BP Statistical Review 2012 3 IEA Key World Statistics 2011 4 BP Statistical Review 2012 5 http://www.mnre.gov.in/schemes/grid-connected/solar/ 6 Jawaharlal Nehru National Solar Mission : Towards Building SOLAR INDIA 7 Jawaharlal Nehru National Solar Mission : Towards Building SOLAR INDIA 8 http://www.intersolar.in/en/news-india/industry-news/status-of-pv-manufacturing-in-india.html 9 Future of Solar Energy in India : K. N. Subramaniam (CEO, Moser Baer Solar Ltd); Sept 23,2013 10 NPD Solarbuzz PV Equipment Quarterly 11Toward a Just and Sustainable Solar Energy Industry : A Silicon Valley Toxics Coalition White Paper,2009 12 http://www.oehc.uchc.edu/news/EU%20and%20Labeling-%20Deeds.pdf 13 http://infochangeindia.org/environment/features/the-hidden-impacts-of-solar-india.html 14

Jawaharlal Nehru National Solar Mission : Towards Building SOLAR INDIA 15 http://news.discovery.com/animals/solar-panels-insects.htm 16 http://articles.washingtonpost.com/2008-03-09/business/36778308_1_polysilicon-plants-solar-energy-chinese-companies 17 http://www.bbc.co.uk/news/world-asia-pacific-14963354 18 (California Department of Toxic Substances Control, 2013) 19 (PV recycling, Llc, 2010) 20 (California Department of Toxic Substances Control, 2010) http://dtsc.ca.gov/IDManifest/Fees.cfm 21 (California Department of Toxic Substances Control, 2010) http://dtsc.ca.gov/PollutionPrevention/p2gbp.cfm 22 (Norwegian Geotechnical Institute, 2010) http://www.dtsc.ca.gov/LawsRegsPolicies/upload/Norwegian-Geotechnical-Institute-Study.pdf 23 (Norwegian Geotechnical Institute, 2010) http://www.dtsc.ca.gov/LawsRegsPolicies/upload/Norwegian-Geotechnical-Institute-Study.pdf,

(European Commission, 2013) http://ec.europa.eu/environment/sme/legislation/waste_en.htm#3 24 (European Commission, 2013)http://ec.europa.eu/environment/sme/legislation/waste_en.htm#3 25 Lecture Slides: CSE Term V, PGP 2012-14 (Prof. P D Jose, IIM Bangalore) 26 http://www.solaronline.com.au/250w-k-solar-solar-panel.html 27 http://www.solaronline.com.au/250w-k-solar-solar-panel.html 28 Future of Solar Energy in India: K.N. Subramaniam (CEO, Moser Baer Solar Ltd) 29 (MoserBaer Solar, 2010)and (MoserBaer Solar, 2010) and (MoserBaer Solar, 2010) 30 (MoserBaer Solar, 2010) 31 (MoserBaer Solar, 2010) and (MoserBaer Solar, 2011) 32 Future of Solar Energy in India: K.N. Subramaniam (CEO, Moser Baer Solar Ltd) 33 Future of Solar Energy in India: K.N. Subramaniam (CEO, Moser Baer Solar Ltd) 34 Lecture Slides: CSE Term V, PGP 2012-14 (Prof. P D Jose, IIM Bangalore) 35 http://www.re-solve.in/perspectives-and-insights/cerc-revises-capital-cost-of-solar-pv-projects-to-rs-8-croresmw-for-fy-2013-14/ 36

http://articles.timesofindia.indiatimes.com/2013-03-18/kochi/37813526_1_e-waste-plastic-waste-brahmapuram 37 Research Unit (Larrdis) Rajya Sabha Secretariat New Delhi, June 2011 38 (Wikipedia, 2013) http://en.wikipedia.org/wiki/Kalundborg_Eco-industrial_Park