indian processed foods industry and the ready to eat market

TRANSCRIPT

Indian Processed Food Industry with reference to Ready to Eat Market 09020242007

1

DISSERTATION PROJECT REPORT

Course Name: Dissertation Code: 020242402

Project name: THE INDIAN PROCESSED FOOD INDUSTRY

WITH REFERENCE TO READY TO EAT

MARKET

Programme: MBA- AB Batch: 2009-11 [Fresh]

Season: April 2011.

Semester- IV

Name of the Student: Boddu Divya

PRN: 09020242007

Submitted to Final submission date:

Mr. Suresh Bhosale 12th Feb’11

SYMBIOSIS INSTITUTE OF INTERNATIONAL BUSINESS (SIIB) is a constituent of SYMBIOSIS INTERNATIONAL UNIVERSITY (SIU) (Estd. Under section 3 of the UGC act 1956,Vide notification no. F-9-12/2001-U-3 of the Govt of India) Accredited by NAAC with ‘A’ grade

2

ACKNOWLEDGEMENT

During the perseverance of this project, I was supported by different people, whose names if not

mentioned would be inconsiderate on my part.

I would like to extend my sincere gratitude and appreciation to my project guide

Mr. Suresh Bhosale, H.O.D Agri-Business, Symbiosis Institute of International Business-Pune;

for extending valuable guidance and encouragement from time to time, without which it would

not have been possible to undertake and complete this project.

I would also like to thank my family and friends; the respondents of the research; and experts

and students contacted for details, for their support and patience throughout the completion of

the project.

DIVYA BODDU

3

Index

CHAPTER 1- INTRODUCTION

1.1 BACKGROUND ................................................................................................................................... 7

1.2 INDIAN FOOD PROCESSING INDUSTRY ............................................................................................. 7

1.2.1 Dairy .......................................................................................................................................... 9

1.2.2 Fruits and Vegetables .............................................................................................................. 10

1.2.3 Grains ...................................................................................................................................... 11

1.2.4 Meat and Poultry Processing .................................................................................................. 12

1.2.5 Fisheries .................................................................................................................................. 13

1.2.6 Consumer Foods including Packaged foods, Beverages and Packaged Drinking Water /Ready

to Eat (RTE).............................................................................................................................................. 14

1.3 READY TO EAT MARKET .................................................................................................................. 16

1.3.1 Concept of RTE ............................................................................................................................... 16

1.3.2 RETORT & ITS PACKAGING ............................................................................................................. 17

1.3.3 Types Of Ready To Eat Food .......................................................................................................... 20

1.3.4 Players In Ready To Eat Food Market ............................................................................................ 20

CHAPTER 2: REVIEW OF LITERATURE

Tata Strategic Management Group ............................................................................................................ 24

Ratna Bhushan (The Hindu) ........................................................................................................................ 25

SUBHA J RAO (The Hindu) ........................................................................................................................... 26

Indrajit Basu ................................................................................................................................................ 27

4

CHAPTER 3: RESEARCH METHODOLOGY

3.1 EXPLORATORY RESEARCH ..................................................................................................................... 32

3.1.1 Secondary Research ....................................................................................................................... 32

3.2 DATA COLLECTION DESIGN ................................................................................................................... 32

3.2.1 Survey Type: ................................................................................................................................ 32

3.2.2 Type of questionnaire: ................................................................................................................ 33

3.2.3 Classificatory variable .................................................................................................................... 33

3.3 SAMPLE DESIGN .................................................................................................................................... 34

3.3.1 Sample Size: ................................................................................................................................... 34

3.3.2 Sample Type: .................................................................................................................................. 34

3.4 FIELD WORK DESIGN ............................................................................................................................. 35

3.4.1 Data collection period: 1 week in the month of January 2010....................................................... 35

3.4.2 No. of Investigators: 1 .................................................................................................................... 35

3.4.3 Area of Operation: Different retail outlets in Pune area (Aundh, FC etc) ..................................... 35

3.4.5 Time required for each Respondent: 10 minutes approximately .................................................. 35

3.5 LIMITATIONS ....................................................................................................................................... 35

3.5.1 Validity limitation: ........................................................................................................................ 35

3.5.2 Reliability limitation: ................................................................................................................... 35

CHAPTER 4: ANALYSIS AND DATA INTERPRETATION

4.1 INDIAN FOOD PROCESSING INDUSTRY ................................................................................................. 36

4.1.1 S.W.O.T ANALYSIS .......................................................................................................................... 36

4.2 THE READY TO EAT MARKET ................................................................................................................. 40

4.2.1 POTER’S 5 FORCE MODEL .............................................................................................................. 40

4.2.2 S.W.O.T ANALYSIS .......................................................................................................................... 45

4.3 ITC FOODS Vs MTR FOODS .................................................................................................................... 47

4.3.1 The Big Decision ............................................................................................................................. 48

4.3.2 Market Entrance ............................................................................................................................ 48

5

4.3.3 Distribution Network ..................................................................................................................... 49

4.3.4 Market differentiation ................................................................................................................... 49

4.3.5 Cost control strategy ...................................................................................................................... 49

4.3.6 Diversification of products: ............................................................................................................ 50

4.3.7 Extensive advertising ..................................................................................................................... 50

4.3.8 Maintenance of freshness and hygiene ......................................................................................... 51

4.3.9 Other factors .................................................................................................................................. 51

4.4 RTE AND CONSUMER BEHAVIOUR ........................................................................................................ 51

Chapter 5: Main Findings

Main findings……………………………………………………………………………………………………………………………………….57

CHAPTER 6: SCOPE FOR FURTHER RESEARCH

6.1 CHECK FOR GROUND REALITIES ........................................................................................................... 59

6.2 CONSUMER BEHAVIOR Vs DIVERSITY ................................................................................................... 59

6.3 GLOBAL SCENARIO Vs INDIAN SCENARIO IN RTE .................................................................................. 59

CHAPTER 7: CONCLUSION and RECOMMENDATIONS

7.1 RECOMMENDATIONS............................................................................................................................ 60

7.2 CONCLUSION ......................................................................................................................................... 61

BIBLIOGRAPHY

BOOKS ..................................................................................................................................................... 62

WEB-RESOURCES .................................................................................................................................... 62

APPENDICES

6

List of figures:

Figure 1: Food Processing ..................................................................................................................... 8

Figure 2: Dairy Products ........................................................................................................................ 9

Figure 3: Processed F Vs- Canned slices; Juices; Flavors ..................................................................... 10

Figure 4: Processed Grains-Bread; Flour ............................................................................................. 11

Figure 5: Meat n Poultry Processing- Meats; Egg liquid; Egg Albumin and Egg Yolk .......................... 12

Figure 6: Processed Fisheries- Fillets; Canned Tuna and Sardines ..................................................... 13

Figure 7: Packaged Food and Beverages ............................................................................................. 14

Figure 8: Retort Packaging Process Flowchart .................................................................................... 18

Figure 9: Retort Packaging machinery ................................................................................................ 18

Figure 10: Market share pie in RTE ..................................................................................................... 47

Figure 11: RTE KNOWLEDGE ............................................................................................................... 52

Figure 12: RTE KNOWLEDGE SOURCE ................................................................................................. 52

Figure 13: RTE PRODUCT PURCHASE PERCENTAGE ............................................................................ 53

Figure 14: NON-COOKING OPTIONS ................................................................................................... 53

Figure 15: RTE PURCHASE TIME .......................................................................................................... 54

Figure 16: WEEKLY CONSUMPTION ON AGE BASIS ............................................................................ 54

Figure 17: Reasons for buying RTE foods ............................................................................................ 55

Figure 18: SALES PATTERN OF READY TO EAT FOOD IN VARIOUS FORMATS ..................................... 55

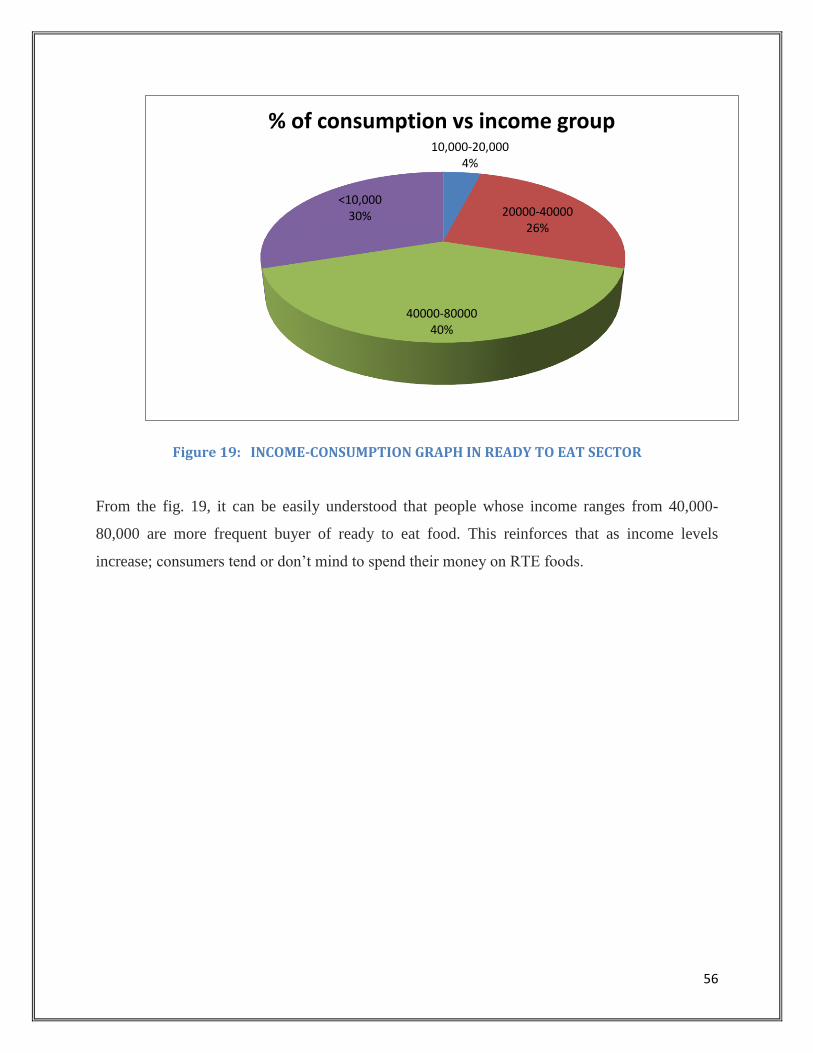

Figure 19: INCOME-CONSUMPTION GRAPH IN READY TO EAT SECTOR ........................................... 56

7

CHAPTER 1- INTRODUCTION

1.1 BACKGROUND

India has made lot of progress in agriculture & food sectors since independence in terms of

growth in output, yields and processing. It has gone through a green revolution, a white

revolution, a yellow revolution and a blue revolution. Today, India is the largest producer of

milk, fruits, cashew nuts, coconuts and tea in the world, the second largest producer of wheat,

vegetables, sugar and fish and the third largest producer of tobacco and rice.

India‘s Food Processing industry is one of the largest industries in the country - it is ranked fifth

in terms of production, consumption, export and expected growth. The industry employs 1.6

million workers directly. Now the time is to provide better food processing & marketing

infrastructure for Indian industries to serve good quality & safest processed food like

READY TO EAT (RTE) food, keeping in mind the changing tastes and lifestyle of the Indian

demography. In fact, it is opening a new window in world scenario as far as taste & acceptance is

concerned. For example, the Excise Duty is now ZERO % on RTE and 100 % tax deduction for

the first 10 years for new units.

1.2 INDIAN FOOD PROCESSING INDUSTRY

India‘s Food Processing industry is one of the largest industries in the country - it is ranked fifth

in terms of production, consumption, export and expected growth. The Indian food industry is

estimated to be worth over US$ 200 billion and is expected to grow to US$ 310 billion by 2015.

India is one of the world‘s major food producers but accounts for only 1.7 per cent (valued at

US$ 7.5 billion) of world trade in this sector – this share is slated to increase to 3 per cent (US$

20 billion) by 2015. The Indian food processing industry is estimated at US$ 70 billion. It

contributed 6.3 per cent to India‘s GDP in 2003 and had a share of 6 per cent in the total

industrial production. The industry employs 1.6 million workers directly.

8

Food processing is a large sector that covers activities such as agriculture, horticulture,

plantation, animal husbandry and fisheries. It also includes other industries that use agriculture

inputs for manufacturing of edible products. The Ministry of Food Processing, Government of

India has defined the following segments within the Food Processing industry:

• Dairy, fruits & vegetable processing

• Grain processing

• Meat & poultry processing

• Fisheries

• Consumer foods including packaged foods, beverages and packaged drinking water.

Figure 1: Food Processing

While the industry is large in terms of size, it is still at a nascent stage in terms of development.

Out of the country‘s total agriculture and food produce, only 2 per cent is processed. The highest

share of processed food is in the Dairy sector, where 37 per cent of the total produce is

processed, of which 15 per cent is processed by the organized sector. Primary food processing

(packaged fruit and vegetables, milk, milled flour and rice, tea, spices, etc.) constitutes around 60

per cent of processed foods. It has a highly fragmented structure that includes thousands of rice-

mills and hullers, flour mills, pulse mills and oil-seed mills, several thousands of bakeries,

traditional food units and fruits, vegetable and spice processing units in unorganized sector. In

comparison, the organized sector is relatively small, with around 516 flour mills, 568 fish

processing units, 5,293 fruit and vegetable processing units, 171 meat processing units and

numerous dairy processing units at state and district levels.

9

1.2.1 Dairy

Figure 2: Dairy Products

The dairy sector ranks first in terms of processed foods with 37 per cent of the produce being

processed. The organized sector processes an estimated 15 per cent of the total milk output in

India. There are 676 dairy plants registered with Government of India, which come under the

organized sector. Milk and milk products contribute to a significant 17 per cent of the country‘s

total expenditure on food. Traditional dairy products account for about 50 per cent of the total

milk produced. The market for dairy products is expected to grow at 15-20 per cent over the next

three years.

India stands first in the world in terms of milk production .The output is expected to be

about 108 million tonnes, growing at a compounded annual growth rate of 4 per cent.

The dairy whitener market comprises of sweetened milk powders, condensed milk and

creamers. Its market size is estimated at US$ 450 million.

Ghee is the most widely marketed and branded product with a nation-wide penetration of

24.1 per cent. It is estimated to be growing at a rate of 8 per cent per annum

The cheese market is estimated at US$ 2.49 million for (54000 tonnes in volume terms),

growing at a rate of nearly 10 per cent per annum. The organized cheese market is

dominated by processed cheese which accounts for 74 per cent market share

The ice-cream market in India is estimated at US$ 226 million, with the organized market

at US$ 158.2 billion. This is currently growing at 20 per cent

10

1.2.2 Fruits and Vegetables

Figure 3: Processed F Vs- Canned slices; Juices; Flavors

o India produces the widest range of fruits and vegetables in the world. It is the second

largest vegetable and third largest fruit producer accounting for 8.4 per cent of the

world‘s food and vegetable production.

o The share of organized sector in fruit processing is estimated to be nearly 48 per cent.

o Fruit production in India registered a growth of 3.9 per cent during the period whereas the

fruit processing sector grew several times faster at 20 per cent over the same period.

o However, less than 2 per cent of the total vegetables produced in the country are

commercially processed, as compared to nearly 70 percent in Brazil and 65 percent in

USA.

o India‘s installed capacity for fruits and vegetable processing nearly doubled during from

1.1 million tonnes in to 2.33 million tonnes.

o About 20 per cent of processed fruits and vegetables are exported. Major products

exported include fruit pulps, pickles, chutneys, canned foods, concentrated pulps and

juices and vegetables. Fruit exports have registered a growth of 16 per cent in volume and

25 per cent in value terms. Mango and mango based products alone constitute 50 per cent

of the exports.

11

1.2.3 Grains

Figure 4: Processed Grains-Bread; Flour

o India produced nearly 209.32 million tonnes of grains.

o India‘s production covers all major grains – rice, wheat, maize, barley and millets like

jowar, bajra and ragi.

o It ranks third in the production of grains in the world. With a share of 40 per cent, grain

processing is the biggest component of food sector.

o Primary processing constitutes 96 per cent with the remaining accounted for by the

secondary and tertiary sectors.

o Total rice milling capacity in the country is 186 million tonnes. There are about 516 large

flour mills in the country, as well as about 10,000 pulse mills.

12

1.2.4 Meat and Poultry Processing

Figure 5: Meat n Poultry Processing- Meats; Egg liquid; Egg Albumin and Egg Yolk

o India has the largest number of livestock population in the world accounting for 50 per

cent of buffaloes and 16 per cent of the goat population.

o Meat production grew at a CAGR of 34 per cent during the period 1999-2004 and stood

at US$ 12.44 million in 2005-06.

o Meat exports stood at US$ 0.104 million in 2005-06.

o Only 11 per cent of the buffalo population, 6 per cent of the cattle, 33 per cent of the

sheep and 38 per cent of the goat population is culled for meat.

o Consumption per head of both fresh and processed meat is very low at 1.5 kg compared

with world average of 35.5 kg.

o Indian poultry meat market was approximately US$ 2.03 billion in 2005. Indian broiler

industry has seen a rapid growth in the last few years - CAGR of more than 10 per cent a

year since 1998.

13

1.2.5 Fisheries

Figure 6: Processed Fisheries- Fillets; Canned Tuna and Sardines

o India is the third largest fish producer in the world and second in in-land fish production.

o The Fisheries sector in India has been classified into marine, inland and aquaculture.

o The fisheries sector contributes 1.1 per cent to the country‘s GDP.

o This segment also provides employment to 11 million people engaged fully, partially or

in subsidiary activities pertaining to the sector.

o India‘s fish production stood at a level of 6.4 million tons in 2004-05. Of this, about 60

per cent (3.9 million tons) came from marine resources.

o There are over 369 freezing units with a daily processing capacity of 10,266 tonnes and

499 frozen storage units with a capacity of 134,767 tonnes.

o Currently fish processing is mostly targeted for export markets. Processed fish product

exports include conventional block frozen products, individual quick frozen products and

minced fish products like fish sausage, cakes, cutlets, pastes etc. Export of marine fish

products touched of US$ 1.48 billion during 2004-05. Exports showed an increase of

11.97 per cent in volume and 11.1 per cent in value realisation. Frozen shrimp is the

largest item in terms of value contributing to 63.5 per cent of the total exports, and frozen

fish is the largest in terms of volume contributing to 34.62 per cent.

14

1.2.6 Consumer Foods including Packaged foods, Beverages and Packaged

Drinking Water /Ready to Eat (RTE)

Figure 7: Packaged Food and Beverages

o Packaged foods segment in India registered a growth of 8 per cent in 2005-06.

o Noodles/Vermicelli is the fastest growing category in this segment with a CAGR at 15

per cent. The market for branded noodles is estimated at 230 million servings per year.

o The Soups market is still small and nascent in India and is approximately US$ 14 million

in value.

o The market for culinary products is estimated at US$ 475,000 and estimated to grow at

18 to 20 per cent per annum.

o Products like Tomato Ketchup and Jams currently have low penetration levels, but are

growing rapidly. Ketchups, for example, have a penetration of just 3 per cent in India;

however this category is estimated to be growing at 20 per cent per annum.

15

Beverages

o The beverages market primarily consists of non-alcoholic beverages which can be

broadly classified into carbonated drinks, non-carbonated drinks and hot beverages.

o This segment is estimated at US$ 155 million out of which fruit juices and fruit-based

drinks account for US$ 60 million.

o The market size of organized carbonated drinks is estimated at US$ 119 million. In the

past decade the carbonated drinks market registered a healthy growth rate of 20 per cent,

driven by the positive changes in India‘s consumer profile.

o Hot beverages include health drinks such as white beverages (‗Horlicks‘ etc) and brown

beverages such as tea/coffee as well as branded drinks (Eg: ‗Boost‘). The total size of this

market is estimated at US$ 333 million by value and 85,000 tonnes by volume.

o White beverages account for 65 per cent of the market and brown beverages constitute

the remaining 35 per cent. India is the largest producer of tea in the world accounting for

28 per cent of the total global production, at 857 million kgs. Tea production in India has

been growing at 1.2 per cent per annum and India is the fourth largest exporter of tea in

the world with estimated exports of US$ 5 million in 2002-03. India is also the fifth

largest producer of coffee accounting for 4 per cent of the total production in the world.

Nearly 75 per cent of India‘s production is exported and coffee exports stood at US$ 5.2

million in 2005-06.

Staples – Bread, Wheat Flour, Salt and Sugar

o Bread is slowly coming to be a staple product consumed by people of all economic

classes in India. Total bread production in the country in 2004-05 was estimated at 2.7

million tons, growing at 7.5 per cent. About 55 per cent of bread production comes from

the organized sector.

o India is the second largest producer of wheat in the world with an output of more than 70

million tonnes. Branded ‗atta‘ (wheat flour) is an important item in this segment with an

estimated market of US$ 195 million.

16

1.3 READY TO EAT MARKET

Ready-to-eat food can be defined as food in a form that is edible without washing, cooking, or

additional preparation by the food establishment or the consumer. It is a category of convenience

food where the preparation time is extremely short and convenient, to where the product is

prepared in advance and can be eaten as sold depending upon the requirement of the users and

the weather conditions. These foods meet the specific needs of convenience, nutritional

adequacy, shelf stability, storage, distribution to the centers and have become very popular after

the year 2002. The pioneer introduction of retorting technology has made the sale of ‗Ready-to-

Eat‘ food products commercially viable with great taste.

1.3.1 Concept of RTE

Ready to Eat Meals like already cooked or prepared lunch & dinner are relatively new

products which came in market only a few years back and are now sold through retail

general stores in especially made sealed aluminum laminates.

The retorting or sterilization process ensures the stability of the Ready-to-Eat foods in

retort pouches, on the shelf and at room temperature. The application of sterilization

technology completely destroys all potentially harmful micro-organisms, thereby

making sure that the food product has a very long shelf life of over 12 months and

needed no refrigeration.

When customer needs to eat, the food item pouch is either put in microwave oven to

warm it or keep in heated water for a few minutes and then serve to eat.

Such ready to eat meals have been especially given to soldiers in army of many

countries who require carrying their rations while on war front or while located far

away from their main unit.

17

The advertisements like, "Hungry Kyaa" are adding zest to the market by

popularizing such food items which are pre-cooked and free from any preservative,

and yet have a long shelf life of over 12-months. These food items are normally sold

in pouches, well packed in cardboard printed boxes of small book size and carry

about 300 grams of cooked food at a price of about Rs. 40 to 200 in foreign market

depending upon the type of dish packed. One packet of vegetable dish is normally

sufficient for one meal for three persons and therefore falls in economic zone of

consumer‘s preferences.

1.3.2 RETORT & ITS PACKAGING

The water RETORT is an equipment or vessel or sterilization module through which steam (at

130 degree centigrade for 25 minutes) is applied on food products packed in retort pouches. The

retorts use water or steam/air combination as processing medium to heat the container/packages.

Compressed air or additional steam is introduced during the processing cycle to provide the

overpressure (any pressure supplied to the retort in excess of that which can be normally

achieved under steam at any given retort temperature). Overpressure is important in preventing

package damage or loss of seal integrity (like bursting), during the heating process.

o Retort pouches is a flexible packaging material that basically consist of laminates

or bounded layers of different packaging films of Polyster-Nylon-Aluminium-

polypropylene that can withstand high process temperature & pressure.

o Their most important feature is that they are made of heat-resistant plastics unlike

the usual flexible pouches. This makes the retort pouches unique which are

suitable for the processing of food contents at temperatures around 120 degrees

Celsius. That is the kind of ambient temperature prevalent in the thermal

sterilization of foods.

18

Figure 8: Retort Packaging Process Flowchart

19

o Some of the major equipments used in packaging food materials are shown below

in Figure 9

Auto Can Feeder

Nozzle type vacuum and gas filler

Retort pouch filler

20

o ADVANTAGES OF RETORT PACKAGING:

Pouch laminates permits less chance to overcook during the retorting thus

products having better color, texture & less nutrients loss.

It requires less energy for sterilization.

It requires less disposal & storage space.

Low oxygen & moisture permeability.

Shelf stable for longer time & requires no refrigeration.

Sun light barrier, light weight, easy to open.

1.3.3 Types Of Ready To Eat Food

Veg Food Non Veg Food

Alloo Matar Chicken Curry

Palak paneer Butter Chicken

Sarso Ka Saag Karahi Chicken

Chana Masala Mughalai Chicken

Kadi Pakora Mutton Masala

Cheese Tomato Mutton Korma

Dal Makhani Karahi Mutton

Rajma Masala Mutton Biryani

Deserts

Gajar Ka Halwa / Sugi Ka Halwa / Milk Kheer

Snacks

Wafers/ Cream rolls/ Biscuits/ Soups

1.3.4 Players In Ready To Eat Food Market

Brands Descirption

Amul

Gujarat Cooperative Milk Marketing Federation (GCMMF) is India's largest food

products marketing organization. Apart from being known for its dairy products,

Amul has ventured into the ready-to-eat industry and includes Processed

Cheese, Pure Ghee, Shrikhand, Nutramul and Mithaee Gulab Jamuns among its

offerings.

Gits Gits produces the selected range of popular ready to cook and instant foods that

cover a range of ethnic Indian cuisine-and where the recipes have "Global pallete

acceptance".

21

Haldirams

The traditional Indian Sweet-Maker from a small set up has transformed into a full

fledged processing food industry and taking its wares beyond the domestic

frontiers to the Western World. Offers packaged Bhel puri chats such as Sev Puri,

Chana Masala, Samosa, Pakoras, Alu Tikki, Pao Bhaji, Gol Gappa, Dhokla

among others

Kitchens Of India,

ITC

ITC's Flagship brand 'Kitchens of India ' has begun to carry this exotic taste of

Indian cuisine beyond the shores of India . Connoisseurs of Indian food in the US,

UK, Switzerland, Bhutan, Bangladesh, Hongkong, Tanzania, Canada and

Australia now have the opportunity to taste these delicious recipes.

MTR

Amongst the top five processed food manufacturers in India, the company claims

to "market and export a wide range of packaged foods to global markets" that

include USA, UK, Australia, New Zealand, Malaysia, Singapore, UAE and Oman.

MTR foods currently comprises twenty-two delicious and completely authentic

Indian curries, gravies and rice.

Priyafoods

Priya has a range of popular traditional recipes starting from Dal Makhani,

Navaratan Kurma to Palak Paneer, Paneer Butter Masala, Punjabi Chhole and

Rajma Masala along with true southern delicacies like Andhra Veg Pulav, Mango

Dal, Gongura Dal. Priya's products are available in USA, Canada, West Indies,

UAE, Saudi Arabia, Kuwait, Bahrain, Qatar, Oman, Singapore, Malaysia,

Australia, U.K., New Zealand etc.

RainbowFoodsIndia

Exporters, manufacturers & suppliers of all types of Indian Frozen Vegetables,

Meals & Snacks to USA and UK. They procure Frozen Vegetables, Meals, Fruits,

Parathas, Punjabi Veg Curries, vegetables, fruits, pickles, pastes and

Snacks.Reputed professionals from 5-star hotels. Supply of Indian Frozen

Vegetables, Meals & Snacks food.

Satnam Overseas

Ltd

Kohinoor Heat & Eat Indian Curries are a range of ready - to - eat Indian

delicacies. Kohinoor claims that "Heat & Eat range of curries use the well-

established retort technology to offer extended shelf life to the products through

steam sterilization."

Tasty Bite

Tasty Bite has a range of entrées and Ready Meals. They have exceptional retort

pouches which was developed for the Apollo space program. Tested to withstand

extreme temperatures and heights from well below sea level to as high as the

moon, this retort packaging has made Tasty Bite a favorite with campers,

mountain climbers, sailing expeditions, desert safaris.

Veekay Impex.com

Exporters of Fresh Fruit Juice, ready to eat food products; kairameen

Moliee(Pearl-spot fish), Motha Fish curry, see Fish Curry,Chilly Chicken

(boneless).

Ashoka Ready to Eat

Ashoka is a Brand owned and managed by ADF Foods Limited (a BSE listed

Company) in India. Ashoka is our Flagship Brand and the leading Ethnic Indian

food brand made in India. It is among the widely distributed ethnic Indian brand.

Its range includes ready-to-eat curries (Heat & Eat), Frozen Foods (Indian Breads

& Snacks), pickles, condiment pastes, mango pulp/slices, chutneys, pappadums,

IQF ready-to-cook vegetables, and Microwaveable rice.

22

ITC Limited (BSE: 500875) public conglomerate company headquartered in Kolkata, India.

Its turnover is $6 billion and a market capitalization of over $30 Billion. The company has its

registered office in Kolkata. It started off as the Imperial Tobacco Company, and shares ancestry

with Imperial Tobacco of the United Kingdom, but it is now fully independent, and was

rechristened to Indian Tobacco Company in 1970 and then to I.T.C. Limited in 1974.

As one of India's most valuable and respected corporations, ITC is widely perceived to be

dedicatedly nation-oriented. ITC's diversified status originates from its corporate strategy aimed

at creating multiple drivers of growth anchored on its time-tested core competencies: unmatched

distribution reach, superior brand-building capabilities, effective supply chain management and

acknowledged service skills in hotels. Over time, the strategic forays into new businesses are

expected to garner a significant share of these emerging high-growth markets in India.

ITC's Agri-Business is one of India's largest exporters of agricultural products. ITC is one

of the country's biggest foreign exchange earners (US $ 3.2 billion in the last decade). The

Company's 'e-Choupal' initiative is enabling Indian agriculture significantly enhance its

competitiveness by empowering Indian farmers through the power of the Internet. This

transformational strategy, which has already become the subject matter of a case study at

Harvard Business School, is expected to progressively create for ITC a huge rural

distribution infrastructure, significantly enhancing the Company's marketing reach.

23

MTR Foods Private Limited is amongst the top five processed food manufacturers in India. We

manufacture, market and export a wide range of packaged foods to global markets that include

USA, UK, Australia, New Zealand, Malaysia, Singapore, UAE, Japan and Oman.

Starting with the legendary MTR restaurant in Bangalore, India‘s silicon valley, we now offer

''complete meal solutions'. Our wide range of products include ready-to-eat curries and rice,

ready-to-cook gravies, frozen foods, ice cream, instant snack and dessert mixes, spices and a

variety of accompaniments like pickles and papads.

MTR Foods was headed by Sadanand Maiya (son of the Yajnanarayana Maiya) until it was sold

toOrkla, a Norwegian company for $80 Million in March 2007. It produces packaged foods in

different ranges - spices, instant mixes, ready-to-eat foods, vermicelli, ready-to-cook gravies,

range of frozen products, papads, pickles, chips, snacks and ice creams. It bought the packaging

technology from the Defence Food Research Laboratory in Mysore and there are no

preservatives added to the food while packaging. MTR is also the first Indian processed foods

company to be certified with the Hazard Analysis Critical Control Point (HACCP) certification

which is a rigorous standard of food safety and hygiene.

Their deep understanding of culinary expectations and needs has resulted in many new and

innovative products. Their investments in infrastructure and technology ensure that they can

scale rapidly and bring these to market. Today, consumers across the globe count on them to

bring them all-natural, wholesome and delicious food that is also convenient and no-fuss.

Ready to Eat dishes are an amazing combination of convenience, taste and variety. They're

100% natural and have absolutely no preservatives. The range currently comprises twenty-

two delicious and completely authentic Indian curries, gravies and rice. They have

successfully adapted technology from the Defense Food Research Laboratory, Mysore to

make sure each dish has that "just-cooked" freshness.

Indian Processed Food Industry with reference to Ready to Eat Market 09020242007

Ch

apte

r: R

evie

w O

f Li

tera

ture

24

CHAPTER 2: REVIEW OF LITERATURE

Tata Strategic Management Group

Ready-to-eat foods market in India October 18, 2007:

Ready-to-eat foods market in India to reach Rs 2900 Cr by 2015. Tata Strategic recommends

focusing on affordability, acceptability and availability of ready-to-eat foods.

Tata Strategic Management Group, today, released its analysis on the Ready-To-Eat (RTE) foods

market in India currently worth Rs. 128Cr. (2006), expecting it to further expand to Rs 2900 Cr.

by 2015. The factors contributing to this growth would be changes like cold chain development,

disintermediation, streamlining of taxation, economies of scale on the supply side, coupled with

increasing disposable incomes, diminishing culinary skills and the rising need for convenience

on the demand side.

The Tata Strategic report on the Ready-To-Eat (RTE) foods highlights that the RTE market in

India has remained under penetrated owing to factors like consumers‘ penchant for freshness,

low affordability and the Indian housewife‘s preference for home cooked food. The report also

draws attention to the ‗perceived‘ taste and nutrition gap and poor range availability for the

Indian consumers.

Significant RTE foods industry data highlighted in the Tata Strategic report:

Packaged foods in India have grown at approximately 7% per annum between 2000 and

2005, with Ready-to-eat foods (RTE) being the fastest growing category at CAGR 73%.

The Indian RTE foods market, canned/preserved segment is more popular, contributing

to approximately 90% of the market and growing at a CAGR of 63% between 2001 and

2006

The chilled and dried ready meal segments are non-existent.

According to the report, the packaged foods industry in India has not experienced significant

growth due to inadequate demand arising from low household incomes and consumer preference

for fresh and home-cooked food.

25

Speaking on the future outlook for the RTE market, Mr. Raju Bhinge, CEO, Tata Strategic

Management Group said, ―There is a huge untapped market opportunity arising due to rapid

demographic shifts in income, urbanization and proportion of urban working women in India.

The industry needs to concentrate on broadening the market and increasing penetration amongst

Indian consumers.‖

Tata Strategic analysis of the Indian RTE market also put forth that the industry players would

have to significantly improve their price competitiveness with respect to other options such as

domestic help, eating out and ordering in, available to the Indian consumer. Besides price

considerations, the product range offered by industry players will have to be strengthened. At the

moment the regional cuisine and non-vegetarian cuisine markets are relatively under serviced

with concentration on the vegetarian North Indian meals.

Mr. Pankaj Gupta, Practice Head- Consumer & Retail, Tata Strategic further added, ―According

to our analysis, India provides an attractive opportunity for both Indian and International players

with a mix of demand and supply side changes. If consumer demands of affordability,

availability and enhancing acceptability are met, the RTE foods market has the potential market

size of Rs 2900 Cr. by 2015 from its existing Rs. 128Cr.‖

Ratna Bhushan (The Hindu)

Ready-to-eat segment whets NRI appetite

MADE in India. Sold in Sainsbury, Selfridges, Walmart and Safeway.

It's fast becoming a reality. For, even as the Rs 25-crore ready-to-eat packaged foods market

faces challenges back home, the category is gathering momentum overseas. From ITC's

Kitchens of India and MTR Foods, to Tasty Bites Eatables and Satnam Overseas, everyone

seems to be wanting a slice of the NRI's food pie. ITC Foods has already had a test run of its

Kitchens of India range of ready-to-serve packaged foods in Selfridges, UK. Mr Ravi Naware,

Chief Executive, ITC Foods, said, "Retailing in the UK, other European countries and the US is

very much on the agenda. Next year, we plan to begin retailing in supermarkets in the UK." Or

take the Rs 130-crore MTR Foods. "We plan to begin selling our ready-to-eat food range in

26

Sainsbury, UK, within the next six months," said Mr Sadananda Maiya, Chairman & Managing

Director, MTR Foods. The company's presence on the global map - at roughly 8 per cent of its

sales - is currently marked by exports to the US, Canada, UK, Germany, France and Japan,

among other countries. MTR has projected exports to account for 20 per cent of its sales in five

years. The Pune-based Tasty Bite Eatables Ltd (TBEL) claims to be the largest-selling Indian

food brand in the `natural foods' category in the US. Mr Ravi Nigam, Executive Director and

President, TBEL, attributes the brand's performance in the US to "significant" investments on

the distribution front. "We have decided to focus on our largest revenue generator — the Ready-

To-Serve (RTS) or retort packaging category," Mr Nigam added. Tasty Bite's portfolio also

includes ready-to-cook (RTC) curry pastes — already popular in western markets.

SUBHA J RAO (The Hindu)

Cooking made convenient: Want to try out a new dish on your family? Just snip away at covers

to bring home the tastes of India

IT'S EIGHT in the evening, you're still in office, and some friends have invited themselves over

for dinner. What will you do? Rush home, don the apron and rustle up something delectable?

"Nah!" says Rohit, a self-confessed lover of cooking. The great stuff he churns out in the kitchen

has many of his bachelor friends lining up for home-made food. What Rohit does now in

moments of crisis is pick up ready-to-eat side dishes straight off the super market shelf and team

them up with pre-packed parathas and rotis. For dessert, he chooses from any of the readymade

ones on offer. His friends can't really make out the difference.

If you're a regular super market shopper, chances are you would've noticed the number of items

on offer in this segment growing by the day. Thanks to change in mindset on eating packed food

and the fact that no preservatives are used to extend the shelf life, more and more people,

especially working couples, are taking to ready-to-eat food in a big way.

And, the variety on offer is mindboggling. Five companies, MTR, ITC, Tasty Bite, Currie

Classic and Kohinoor, put together offer customers more than 25 options to choose from. The list

goes like this ... The modest Pongal (how does Madras lentil rice sound?), lemon rice and sambar

rice share shelf space with their North Indian and Pakistani cousins like Palace paneer, Daly

27

Machine, Narrating Korma, China Masala (all the way from Rawalpindi), Baghare Baigan

(Hyderabad), Methi Mutter Malai (from Agra, apparently concocted by Noor Jehan), Kashmiri

Rajmah, Avial, Peas and mushroom curry... Phew! And, this is just part of the list.

A staple offering of most companies is the ubiquitous Dal Makhni, a creamy mix of various

lentils, Indian spices and fragrant butter (Do I read like the menu card in a star restaurant?). And,

that is the fastest moving item in most stores.

These packs come in the range of Rs. 15 (for lemon rice and the like) to Rs. 40 (Palak Paneer et

al). The `Buy two get one free' scheme of ITC has caught on very well with customers, store

managers say.

M. Chellayan, Director, the Nilgiri Dairy Farm (Nilgiris), says that with more disposable income

on their hand, many middle and upper middle class people are going in for these dishes. S.

Prakash, Senior Manager of Alankar Supermarket, agrees. "We've had to replenish our stock

often," he says.

Though people are open to trying out new dishes, the fact that it is pre-cooked and packed

rankles some. But, one bite and they are hooked. "I opened a packet of MTR's Bisibela bhath

bravely, but wondered how it would taste. I refused to believe that something cooked a month

ago and packed, that too without any preservatives, would still be fresh. But, one spoon was

enough to make me a convert. I now buy packed subzis when I am in the mood to eat something

nice without going through the bother of cooking," says Leena, who works in the field of

medical transcription.

Indrajit Basu

Here's $20m, just don't make me cook

It took a while to catch on, but as the country's 15-year-old globalization process brings about

rapid changes in the lifestyles of urban Indians, ready-to-eat food is fast becoming a compelling

proposition. Over the past two years, the ready-to-eat packed food market has grown from an

almost insignificant number to become a US$20-million-revenue industry in 2004. Industry

28

players say that, considering the current 35% growth rate, revenues in this sector can easily touch

$50 million in the next three years.

Take the instance of Mumbai-based Ruma Banerjee, a 40-year-old market research professional,

who gets her ready-to-eat curry pastes or cooked packed meals from a grocery shop at the mall

next to her office. "It's not that I do not like to cook, but with a 70-hour work week, an equally

busy husband and a 10-year-old child at home, we have little time for regular cooking," she says.

For Shruti Rajam, 23, an insurance-industry professional living alone in Chennai on her first job,

time is not really a problem. Cooking is. Shruti never had to enter the kitchen in her life when

she was with her parents. But now that she is on her own, stuffing her kitchen cabinet with

ready-made food seems to be the obvious option. "It's cool," she says, "I have become an expert

at this. Even my friends think I am a great cook."

Ruma and Shruti are part of a rapidly growing tribe of urban Indians who are increasingly

shunning the painstaking job of chopping, slicing, dicing and mixing the right ingredients, to

simply picking up a pair of scissors and snipping open a pack of a two-minute everyday Indian

meal. Indeed, ready-made India curries that were unheard of even a few years back occupy the

pride of place in Indian kitchens now. Brands such asITC Aashirwad, Kitchens of India, MTR

Food, Tasty Bites and Currie Classic are not only gaining acceptance in double-income nuclear

families all over India, but are also spreading rapidly globally.

"Indian lifestyle is undergoing a massive socio-economic change, which is also being reflected in

food habits," says Ravi Naware, divisional chief executive of ITC Foods, a wing of ITC Ltd, one

of India's largest fast-moving consumer-goods company. "In urban India, where time is more

important than money, it's tough to return from office and put the hours into cooking that a

typical Indian meal demands.‖

J Suresh, chief executive officer (CEO) and executive director of MTR Foods that claims to be

the largest player in the segment with over 65% market share, adds that ready-made food is not

considered extravagant expense anymore. "Many Indian households with little time and

inclination to spend in the kitchen are adopting this as a necessity. Moreover, with disposable

income going up as families become more double-income and salaries going up, people don't

mind spending on something that will save them the sweat in kitchen," he says.

29

The quick-fix food concept is not really new in India, it has only picked up of late. It was

launched over a decade ago in different forms but failed to take off primarily because of a

general preference for freshly cooked food. And also, as Naware says, "because retail outlets in

India lacked the adequate refrigeration facilities". With the availability of a new technology

called Retort - that packs cooked food in a four-layer package, which is then heated to 120

degrees Celsius to kill all living organisms, thereby ensuring freshness through its much longer

shelf-life - the ready-to-eat food concept has become far more acceptable." Besides, says Suresh

of MTR Foods, all ready-made food makers have adopted Hazard Analysis Control Point

Certification from the British Standard Laboratory, which signifies that factories making such

products follow strict food and safety norms.

Nevertheless, all ready-made food makers say the primary driving force behind the growth of

this sector is the changing Indian mindset toward food. Convenience is the new buzzword.

"There was a time when eating out was a luxury," says Amit Jatia, managing director of

McDonalds India. "Not any more. Likewise, an urban Indian no longer hesitates to pick up a

phone and order meal from a neighborhood restaurant or pick up a ready-to-eat meal from the

next-door store." According to AC Neilsen ORG MARG, a top market research outfit, it is not

just ready-to-eat food that is growing at a scorching pace, but "eating habits are changing rapidly

and fast-food consumption is now a part of everyday life...Almost a third of urban Indians now

claim to opt for fast food, even for breakfast. Dinner, however, remains the most-preferred

occasion for eating fast food," says Sarang Panchal, executive director of AC Neilsen.

According to the findings of the latest online survey from AC Nielsen, urban Indians are among

the top 10 most-frequent consumers of fast food across the globe. The survey finds that a huge

71% of urban Indians consume food from take-away restaurants once a month. Some 37% of the

adult Indian population does so at least once a week. This makes India one of the top 10

countries among the 28 surveyed in terms of frequency of fast-food consumption.

30

"The incidence of fast food consumption in urban India is accelerating much faster than most

people anticipated," says Panchal. "Contrary to the belief that a reliance on traditional and home-

made preparation may hinder the growth of fast food, changing lifestyle has altered the view

toward out-of-home meals. A willingness to spend and, most importantly, the urban Indian

acquiring a more global palate has catalyzed consumption."

Among the international fast food chains and local operators, McDonald's is the most popular of

all take-away options. Nonetheless, selling fast food and ready-made food is not exactly easy,

say the players, especially for foreign players, as Domino's Pizza India CEO Arvind Nair

discovered. Which is why, he says, "Imported fast food chains were quick to adapt to Indian

tastes and even the regional variations. There are extensive vegetarian menus, for example, and

emphasis on the kind of meats that Indians have no objection to," says Nair.

Indians' discerning taste buds is a big reason why industry experts like Naware and Suresh feel

that foreign players would find little opportunity in this new fad "unless it is ready to tie up with

a local player". However, for foreign players, India could be a good sourcing point for the

overseas markets. "The growth of ready-made food and curry pastes has also been scorching in

overseas markets," says Naware. "The potential for exports are very good. We are experiencing

explosive demand for ready-made Indian food from overseas markets like the US, the UK,

Canada and Europe. This demand is not only generated by the non-resident Indian community

but also by the local populations that are increasingly getting exposed to Indian cuisine through

Indians living there, and also through their travels. I came across a projection recently that says

by 2020, no American will cook starting from basic ingredients all the way. They will either use

ready-to-cook or ready-to-eat food". India exported about $7 million worth ready-made Indian

food in 2004, which is growing at around 20% a year.

According to industry insiders, the opportunity for foreign players in the country's fast food

segment is huge. Nair of Domino's Pizza says although Indians' penchant for spicy food has

resulted in an Indian-Chinese cuisine that is quite unknown in Sichuan province or Guanzhou,

the snowballing retail revolution aimed at India's 300-million-strong middle class has created a

natural habitat for imported fast food. "Down the road, I can see not only pizzas and burgers and

31

fizzy drink but also branded sushi, Vietnamese soup, Lebanese kebabs and Thai food-in-bowls to

join our Mughlai and dosa," says Nair.

And according to Naware, yet another untapped segment that could be utilized by foreign players

through their marketing prowess are the smaller towns and suburbs of India. Despite its

scorching growth, the concept of ready-to-eat and fast food are still restricted to the six larger

Indian cities and a few smaller ones while a huge section of the country's billion-plus population

is still not exposed to it. "That has happened because marketing ready-made and fast foods in the

rest of India requires huge wherewithal that Indian companies do not have. This is where foreign

players can excel," says Naware.

Indian Processed Food Industry with reference to Ready to Eat Market 09020242007

Ch

apte

r: R

esea

rch

Met

ho

do

logy

32

CHAPTER 3: RESEARCH METHODOLOGY

3.1 EXPLORATORY RESEARCH

3.1.1 Secondary Research For the successful completion of the proposed objectives, a secondary research was undertaken.

This included thorough knowledge search from various resources like

Research Journals

Text Books related to Food Processing and Ready to Eat Foods

The FOOD Magazines

Internet resources including that of the Ready to Eat player‘s websites

Newspaper Articles on the trends and latest happenings in the RTE market.

The secondary research helped establish knowledge base and give better insights for

interpretation, analysis and suggestions relating to the project.

3.2 DATA COLLECTION DESIGN

For the purpose of understanding the consumer behavior and other implications in the growth of

RTE market, a primary research is required. It will also reinforce the findings of secondary

research.

3.2.1 Survey Type: Mall interview (at the retail outlets)

a) Flexibility: The research requires that a direct and open communication is established

between the interviewer and the respondent, especially for the open ended questions. This

eliminated other methods of survey namely telephonic, mail or electronic survey methods and we

remain with personnel interviews, ie, farm, home or mall survey method. Personnel interviews

allow the investigator to explain and clarify difficult questions and entail probing and prompting

during the survey to enhance validity, diversity and exhaustiveness.

33

b) Quantity of information: Since the questionnaire was semi-structured, open questionnaire

and contained large amount of data to be collected, farm, home or mall interview was the

obvious choice for the survey method. Farm or home interview helps in easy recording of open

ended questions with more responses mall interview, the former was a better choice for survey

method. Further, it was found that the questionnaire requires a minimum of 15-20 minutes for

completing it. Since this much time is not there with the respondent in mall interview, farm or

home interview would have been the best option for the survey.

But due to the time and budget constraints it was decided to conduct mall survey for the research.

3.2.2 Type of questionnaire: Semi-Structured

The type of questionnaire is kept semi structured because, for some questions the respondent

may want to answer something that is not there in the options given. For example ―What do you

see before buying a RTE food product?‖

3.2.3 Classificatory variable

The secondary research suggests that the preference to RTE majorly depends upon the income

level of the consumer. Hence, the classificatory variable taken here is also the same.

a. less than 10,000

b. 10,000 – 25,000

c. 25,000 – 50,000

d. More than 50,000

34

3.3 SAMPLE DESIGN

3.3.1 Sample Size:

Since we have 4 classificatory variables, a minimum of 30 * 4 = 120 respondents should be

approached. For better results and keeping into mind the time and budget constraints, a sample

size of 200 is ideal.

3.3.2 Sample Type:

Non probabilistic sampling technique is adopted. Probability sampling is avoided as the

sampling has to be done among the respondents who visit the retail outlets and it is not possible

to pre-specify every potential sample of a given sample that could be drawn with their

probability of being selected. Further probability sampling required precise definition of the

target population which was lacking here. Thus due to inadequacy of sampling frame and not to

make the research complicated, non- probabilistic sampling technique is adopted. But efforts

were made to avoid selection biases while selecting the respondents for better representation. So

among non probabilistic sampling techniques, Quota sampling is done where the sample

elements selected fit the control characteristic of being a prospective RTE buyer. Quota ensures

that the composition of the sample is same as the composition of the population with respect to

the characteristic of interest. The sampling was also disproportionate as the criteria was to

achieve the target of 200 with each classificatory variable having a sample size of minimum 30

samples , thus flexibility of a range of 25-30 per variable and the decision on the number of

sample was not dependent on the secondary data analysis but based on judgment. Therefore even

though the sampling is non-probabilistic sampling, all care is taken to ensure the reliability of

sampling.

35

3.4 FIELD WORK DESIGN

3.4.1 Data collection period: 1 week in the month of January 2010

3.4.2 No. of Investigators: 1

3.4.3 Area of Operation: Different retail outlets in Pune area (Aundh, FC etc)

3.4.5 Time required for each Respondent: 10 minutes approximately

3.5 LIMITATIONS

There are some limitations of the research caused by time and budget constraints and are listed

as:

3.5.1 Validity limitation:

During the response there may be high interference from friends and relatives of the respondent.

This to some extent may cause the response to their opinion instead of the respondent‘s opinion.

Thus there is a compromise in the validity of the response. Even though this error is non

quantifiable still this will have somewhat effect on the overall validity of the research.

3.5.2 Reliability limitation:

Since the sampling technique used is non-probability technique an evaluation of the precision of

the sample results are not permitted and the estimates cannot be statistically projected to the

population.

Indian Processed Food Industry with reference to Ready to Eat Market 09020242007

Ch

apte

r: A

nal

ysis

an

d D

ata

Inte

rpre

tati

on

36

CHAPTER 4: ANALYSIS AND DATA INTERPRETATION

For the purpose of better understanding and flow of the report, this chapter is divided into 4

sections, each catering to the 4 objectives of the research.

4.1 INDIAN FOOD PROCESSING INDUSTRY

4.1.1 S.W.O.T ANALYSIS

STRENGTHS

o India has access to several natural resources that provides it a competitive

advantage in the food processing sector. Due to its diverse agro-climatic

conditions, it has a wide-ranging and large raw material base suitable for food

processing industries.

o India is world‘s largest producer of milk, tea and pulses and fruits and vegetables.

o India has large marine product and processing potential with varied fish resources

along the 8,041 km coastline, 28,000 km of rivers and millions of hectares of

reservoirs and brackish water.

o India possesses the largest livestock population in the world with 50 per cent of

world‘s buffaloes and 20 per cent of cattle.

37

o India‘s comparatively cheaper workforce can be effectively utilized to set up large

low cost production bases for domestic and export markets. Cost of production in

India is lower by about 40 per cent over a comparable location in EU and 10-15

per cent over a location in UK.

o Traditionally, different players across the value chain played the different roles

and worked more or less independently. Recently, the trend has been towards

increasing integration and collaboration across players in the value chain, to

garner mutual benefits. Thus taking advantage of forward and backward linkages

to the maximum.

o India has a large number of research institutions like Central Food Technological

Research Institute, Central Institute of Fisheries Technology, National Dairy

Research Institute, National Research and Development Centre etc. to support the

technology and development in the food processing sector in India.

WEAKNESSES

o Domestic penetration of processed fruits and vegetables overall is at 10 %.

o The relative share of branded milk products especially ghee is still low at 2 %.

o Domestic penetration of culinary products is still 13.3 % and is largely tilted

towards metros.

o Consumption of packaged biscuits for Indian consumers is still low at 0.48 %

while that for Americans is 4 %.

o Most of the processing in India is currently manual. There is limited use of

technology like pre-cooling facilities for vegetables, controlled atmospheric

storage and irradiation facilities. This technology is important for extended

storage of fruits and vegetables in making them conducive for further processing

38

o In the case of meat processing, despite the presence of over 3600 licensed

slaughter-houses in India, the level of technology used in most of them is limited,

resulting in low exploitation of animal population.

o Nearly 90 per cent of the food processing units are small in scale and hence are

unable to exploit the advantages of economies of scale.

OPPORTUNITIES

o The demographics at large are changing rapidly. Increased income, search for

convenience, increased work force per family etc happens to provide the required

boost to this sector.

o Food processing is being encouraged through contract farming and land leasing

arrangements to allow accelerated technology transfer, capital inflow and assured

market for crop production.

o The government of India is taking initiatives for enormous investments in this

sector.

o The national policy aims to increase the level of food processing from 2 per cent

to 10 per cent in 2010 and to 25 per cent in 2025.

• The level of institutional credit to be provided by banks and FIs has been

increased from US$ 17.41 billion during 2003-04 to about US$ 23.76 billion in

2005-06

• Allowing full repatriation of profits and capital.

• Automatic approvals for foreign investment up to 100 per cent, except in few

cases, and also technology transfer.

39

• Zero duty import of capital goods and raw material for 100 per cent export-

oriented units. Customs duty on packaging machines reduced. Central excise

duty on meat, poultry and fish reduced to 8 per cent

• Income tax rebate allowed (100 per cent of profits for 5 years and 25 per cent of

profits for the next 5 years) for new industries in fruits and vegetables besides

institutional and credit support.

• Allowing sales up to 50 per cent in domestic tariff area for agro-based, 100 per

cent export oriented units

• Government grants given for setting up common facilities in Agro Food Park.

• Full duty exemption on all imports for units in export processing zones.

o The Government of India is looking to promote terminal markets, as a means of

integrating domestic produce with retail chains. There are plans to set up such

markets in eight cities across five states, at a cost of US$ 131 million. The cities

being considered are Mumbai, Nashik, Nagpur, Chandigarh, Rai,Patna, Bhopal

and Kolkata.

THREATS

o Increased processing of food means increased spending of resources such as

water, electricity, raw materials for appropriate machinery etc.

o Since any kind of processing will generate lot of waste effluents of chemical and

non-degradable nature which may affect the environment in the long run.

o Also, processed foods require special packaging which again will involve lot of

paper and plastics, thus harming the environment even further.

40

4.2 THE READY TO EAT MARKET

4.2.1 POTER’S 5 FORCE MODEL

Packaged food industry has been lately drawing criticism from Industry pundits and experts, for

it has shelved its status of being a recession proof Industry. It was only a few months back when

the same pundits were going gung-ho about the opportunities lying galore ahead of players in

this Industry. It almost seemed packaged food had evolved over the years from its status from a

bare psychological need in Maslow‘s hierarchy to aesthetic needs of health and well being. The

only chant heard around was about the forces of consumerism, globalization and rising income

levels in third world countries, which would be upholding the future of this Industry high.

However, it didn‘t take long for this recent recession to shed those claims and reject those

profound theories.

The matter of fact is that packaged food Industry, particularly its consumption is as susceptible to

cyclical trends of economy as any other Industry today. It doesn‘t take much for any consumer to

trim his food budget in wake of credit crunch and move to alternate cheaper avenues like fresh

foods. Hence, it becomes imperative for both, Incumbent players and New Entrants to estimate

the very forces that will be deciding the fate of this industry over a period of next 2-3 years.

41

Competition and Rivalry

Characteristic Comments Conclusion

Product Differentiation There has been convergence in the

attributes of food labels with most

desirable being Natural, Nutrients, High

Quality and Convenience. Traditional

differentiation models based on brand

and product formulation are losing

relevance.

Unfavorable

Low Switching Cost The customer is not loosing on

anything by switching from one brand

to the other, hence leading to frequent

churning and fierce advertisement

rivalry to attract and retain customers

Unfavorable

Price and Process War Rigorous price and process wars are

waging the entire spectrum of value

chain from raw material procurement to

customer delivery. The recent

supermarket was between Tesco and

Walmart‘s Asda serves as a testimony.

Unfavorable

Consolidation &

Concentration

Due to spate of acquisitions and

expansions, the industry is getting

concentrated and consolidated.

Currently Nestle has highest market

share, approx 3.3%. But this

consolidation trend may lead to an

oligopoly where some are price setters

and others price takers.

Unfavorable

Storage Costs & Time to

Market

As this industry deals with highly

perishable products there storage costs

are significant and time to market forms

a critical part. This occasionally leads

to unloading of similar products at the

same time by different players and

further intensifies the game.

Unfavorable

Growth Worldwide packaged food industry has

been witnessing more than 7% growth

over the last 3 years, much better than

4-5% growth rate of the entire

economy.

Favorable

Economies of Scale Economies of scale are becoming more

and more important in attaining cost

efficiencies. Each player is trying to

exploit the global sourcing model to

rationalize its cost and pass on the

benefits to its customers

Favorable

42

Buyer Power

Buyers for packaged food industry players can be categorized into retailers and

consumers, hence different set of forces are applicable to each of them.

Characteristic Comments Conclusion

Buyer Awareness Consumer is becoming more aware and

capable to compare each product on all

the 3 fronts of health ingredients, safety

and alternate price discounts making it

more challenging for players to enjoy

consumer focus and loyalty.

Unfavorable

Price Sensitivity In the wake of recent recession,

consumers have trimmed their

expenditures drastically and have

further led to closing of several retail

chains. The only mantra that‘s working

for marketer is price discounts.

Unfavorable

Incentives and Rebate Retailers are expecting the big players

of this industry to share their

expenditure and losses, helping them

sustain their operations in the cut throat

price wars. And are vouching for

products with which companies that are

sharing their burden.

Unfavorable

Product innovation Customer is loaded with plethora of

new and attractive product options to

initiate their buying momentum, ever

increasing his expectations and further

rewarding him with significant buying

power to exercise.

Unfavorable

Availability of Substitutes The option of moving to alternate foods

like fig bars for cookies and soy

proteins instead of meat reduces the

bargaining power that the food

manufacturer would have enjoyed

otherwise.

Unfavorable

Low threat of backward

Integration

Retailers do not pose credible

backward integration threat. This is not

feasible for their cost efficiencies and

also because the producers subsidize a

large part of their marketing budgets

Favorable

Buyer Concentration The buyers for this industry are highly

fragmented and only likes of Walmart,

Carrefour are able to exert any

influence, retaining the threat of

retaliation.

Favorable

43

Supplier’s Power

Characteristic Comments Conclusion

Raw Material Availability There has been a marked shortage in

the raw materials due to usage of

agrarian lands for energy crops. This

has been further worsened by the

commodity trading leading to highly

volatile prices of grain and animal feed.

Unfavorable

Low Concentration Majority of suppliers of these food

companies are cooperatives or

individual farmers who supply

commodities to the producers. This

takes away the leverage they could

have utilized if they were providing

large volume of suppliers individually.

Unfavorable

Low input differentiation The raw materials procured by food

companies are commodity products or

livestock that cannot be differentiated

on any factor other than quality. This

gives the companies alternate sources

of raw materials, rather than depending

on a sole supplier for its highly

specialized unit.

Favorable

Switching Costs The switching cost for the suppliers are

huge as the procurement for raw

materials are done through contracts

and tender processes and are long term

in nature.

Favorable

Threat of substitutes

Substitutes are specific to product categories in this industry and they may or may not

pose the relevant threat. They can be a significant threat if the price performance value

offered by substitute is better than products being offered, hence to be considered on a

case by case basis.

44

Barriers to entry

Characteristic Comments Conclusion

Access to Distribution With opening of array of retail chains in

every nook and corner, and as a

consequence of rapid globalization, the

unique access to distribution channels

earlier enjoyed by only a few is

available to all

Unfavorable

Customer Loyalty The buyers of packaged food are

exhibiting easy brand switching for

promotions and discounts. This makes it

easy for a new player to enter and

attract customers

Unfavorable

Capital requirements Capital required for setting up plants,

machinery and regional sales offices is

no more difficult with easy access to

equity, loans and seed funding.

Unfavorable

Compliance regulations With new laws emerging like COOL

and MTC, it becomes difficult for a new

player to manage the legal and quality

requirements by these laws.

Favorable

Asset Specification The plant and machinery and processes

for food companies are highly

specialized and cannot be used in other

industries. This makes it difficult for

players to exit the industry because of

low re-usability of assets.

Favorable

Expected retaliation With neck to neck price wars in the

industry, any effort by a player to

outsmart rivals by cutting prices or

offering new product formats is

matched by rivals. This fear of

retaliation also deters new players from

entering using low cost advantages or a

new product.

Favorable

45

4.2.2 S.W.O.T ANALYSIS

STRENGTHS

o Ready to eat packaged food industry is over Rs. 4000 crore or 1 billion US $.

o These foods meet the specific needs of convenience, nutritional adequacy, shelf

stability, storage, distribution to the centers and have become very popular after

the year 2002.

o These food items are normally selling in pouches, well packed in cardboard

printed boxes of small book size and carry about 300 grams of cooked food at a

price of about Rs. 40 to 200 in foreign market depending upon the type of dish

packed. One packet of vegetable dish is normally sufficient for one meal for three

persons and therefore falls in economic zone of consumer‘s preferences

o Euro monitor International, a market research company says that amount of

money Indian spend on ready to eat snacks & food is 5 billion US $ in a year

while on abroad Indian or Indian subcontinents spend 30 billion US $ in a year.

WEAKNESSES

o Low level of technology usage n the country brings down the efficiency that is

required for this sector to flourish.