indian ocean region seychelles

DESCRIPTION

Session ITRANSCRIPT

HOW THE GLOBAL FINANCIAL HOW THE GLOBAL FINANCIAL CRISIS HAS AFFECTED THE SMALL CRISIS HAS AFFECTED THE SMALL

STATES OF SEYCHELLES & STATES OF SEYCHELLES & MAURITIUSMAURITIUS

HOW THE GLOBAL FINANCIAL HOW THE GLOBAL FINANCIAL CRISIS HAS AFFECTED THE SMALL CRISIS HAS AFFECTED THE SMALL

STATES OF SEYCHELLES & STATES OF SEYCHELLES & MAURITIUSMAURITIUS

BY BY Dr. Gerard AdonisDr. Gerard Adonis

Seychelles

Background Information

• As a SIDS, Seychelles remains vulnerable to the vicissitude of the Global Economy

• This is illustrated by recent financial crisis which unfortunately has exacerbated the already dire economic situation of the country

• Being largely dependent on tourism (30% GDP) – make situation extremely difficult

• Tourism expected to decline in 2009 by almost 25%• Impact of the global recession became apparent

especially after defaulting on the sovereign bond repayment

• Government sought the IMF’s assistance. • An emergency stand-by agreement was accepted, s.t.

Government implementing some major structural economic reform

• This came into effect in October 2008, with the support of IMF

Economic Growth and FDI• Economic growth in 2008 has been predicted to fall

to nearly 0%, down from 5.5% in 2007. • GDP growth for 2009 has been projected to fall

further to -11%.• Main reasons;

Contraction in public and private consumption expenditure due to the reform programme Sharp drop in tourism revenue expected as a result of the global economic slow down.

• FDI is expected to drop to under US$ 200 mn compared to US$ 350 mn in 2008

Tourism Sector• This sector expected to perform badly in 2009 both in

terms of arrivals and FDI

• Tourism is Seychelles leading source of employment and foreign currency earnings

• Projected to fall by 25% in 2009)

Public Debt • This is an area where Seychelles has been severely

affected

• Despite being one of the richest country in Africa with GDP per capita of US $9,440.095 at real exchange Seychelles is a very indebted country.

• • In 2007 public debt stood at around 122.8% of GDP

• In Dec 2008 public debt stood at 175% of GDP

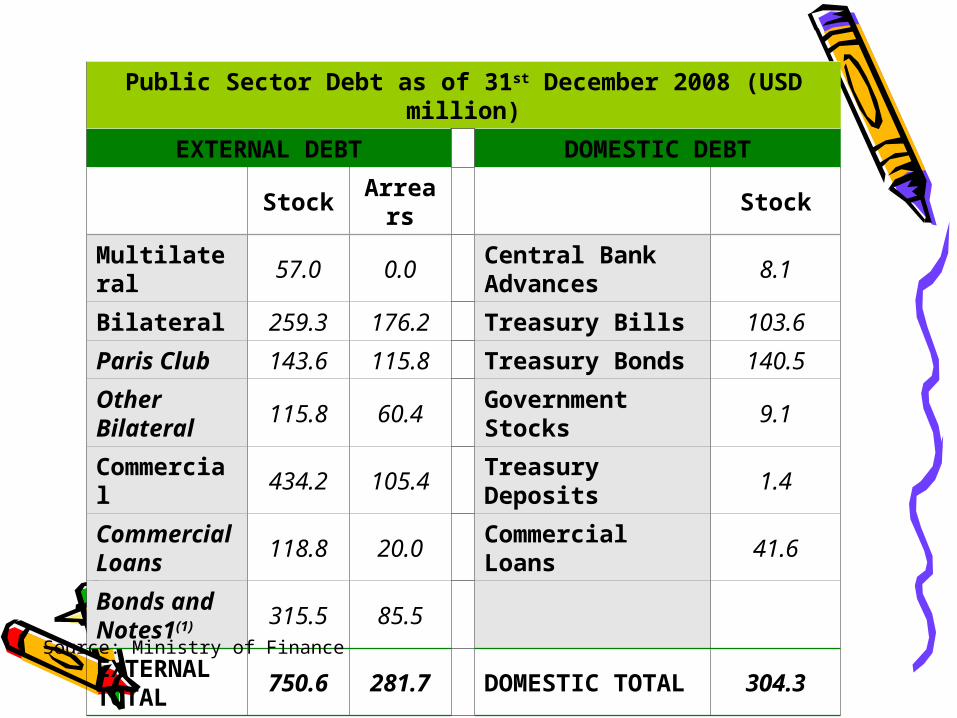

Public Sector Debt as of 31st December 2008 (USD million)

EXTERNAL DEBT DOMESTIC DEBT

Stock Arrears Stock

Multilateral 57.0 0.0Central Bank Advances

8.1

Bilateral 259.3 176.2 Treasury Bills 103.6

Paris Club 143.6 115.8 Treasury Bonds 140.5

Other Bilateral

115.8 60.4 Government Stocks 9.1

Commercial 434.2 105.4 Treasury Deposits 1.4

Commercial Loans

118.8 20.0 Commercial Loans 41.6

Bonds and Notes1(1)

315.5 85.5

EXTERNAL TOTAL

750.6 281.7DOMESTIC TOTAL

304.3

Source: Ministry of Finance

Evolution of Monetary and Exchange Rate after Implementation of Reform

• Immediate effect following the floatation of the exchange rate was a sharp depreciation of the local currency by more than 100%.

• As a result (depreciation): Inflation escalated by more than 60%Aggregate demand fell sharply Cost of production increased due to doubling in the price of

raw materials Some businesses faced with bankruptcies The Development Bank the heart of business development

in the Seychelles was faced with the risk of closure.

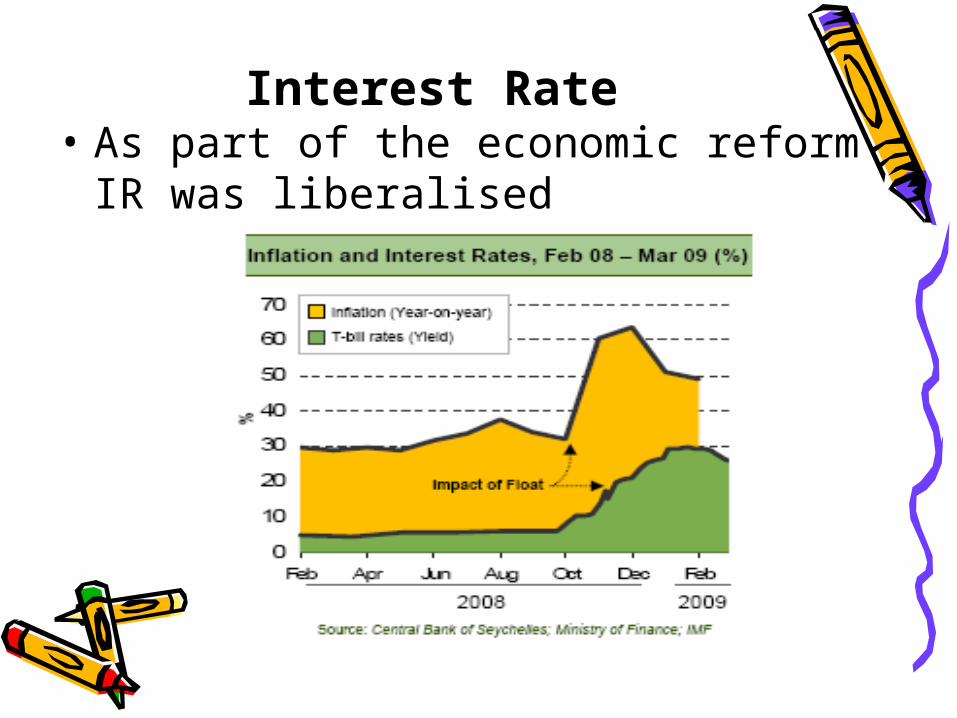

Interest Rate• As part of the economic reform IR was

liberalised

• As a result of higher return on Government bonds an unpleasant situation for private sector investment was created.

• Both commercial banks and private individuals now preferring Government securities

• In consequence most funds were deviating into Government securities and none were available for investment purposes.

Business Confidence • Widespread belief that business confidence is at its

lowest.

• A combination of both local and international factors is responsible, notably; Recent global financial crisis Ongoing economic reform

• Unfortunately Economic Reform has stripped investors and businesses of their ability to undertake new investments

• Current climate characterised by; falling aggregate demand low confidencehigh interest rate undervalued currency hyper-inflation low investment rising unemployment increasing incidence of crime and social deprivation

KEY KEY ECONOMICECONOMIC INDICATORS AND INDICATORS AND

PROJECTIONPROJECTION

KEY KEY ECONOMICECONOMIC INDICATORS AND INDICATORS AND

PROJECTIONPROJECTION

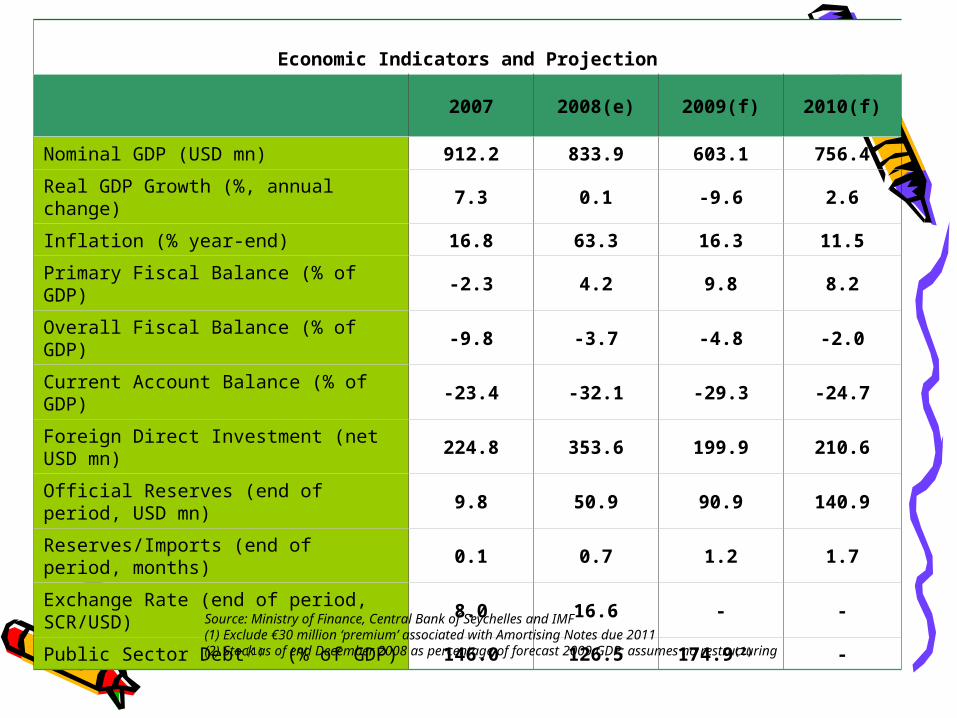

Table 2

Economic Indicators and Projection

2007 2008(e) 2009(f) 2010(f)

Nominal GDP (USD mn) 912.2 833.9 603.1 756.4

Real GDP Growth (%, annual change) 7.3 0.1 -9.6 2.6

Inflation (% year-end) 16.8 63.3 16.3 11.5

Primary Fiscal Balance (% of GDP) -2.3 4.2 9.8 8.2

Overall Fiscal Balance (% of GDP) -9.8 -3.7 -4.8 -2.0

Current Account Balance (% of GDP) -23.4 -32.1 -29.3 -24.7

Foreign Direct Investment (net USD mn) 224.8 353.6 199.9 210.6

Official Reserves (end of period, USD mn) 9.8 50.9 90.9 140.9

Reserves/Imports (end of period, months) 0.1 0.7 1.2 1.7

Exchange Rate (end of period, SCR/USD) 8.0 16.6 - -

Public Sector Debt(1) (% of GDP) 146.0 126.5 174.9(2) -

Source: Ministry of Finance, Central Bank of Seychelles and IMF(1) Exclude €30 million ‘premium’ associated with Amortising Notes due 2011(2) Stock as of end December 2008 as percentage of forecast 2009 GDP; assumes no restructuring

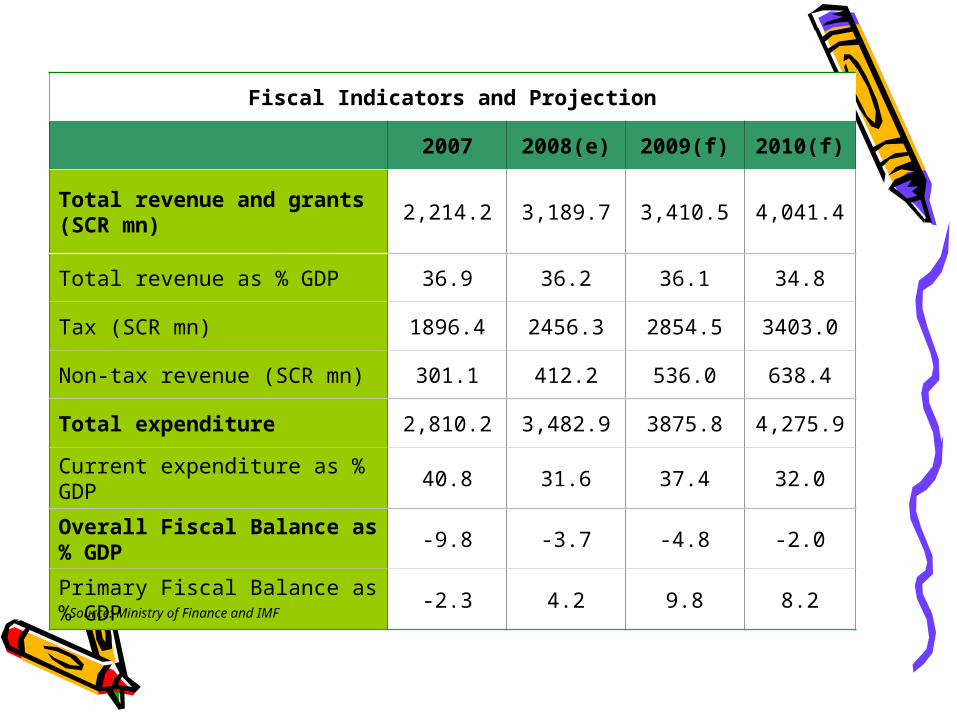

Fiscal Indicators and Projection

2007 2008(e) 2009(f) 2010(f)

Total revenue and grants (SCR mn)

2,214.2 3,189.7 3,410.5 4,041.4

Total revenue as % GDP 36.9 36.2 36.1 34.8

Tax (SCR mn) 1896.4 2456.3 2854.5 3403.0

Non-tax revenue (SCR mn) 301.1 412.2 536.0 638.4

Total expenditure 2,810.2 3,482.9 3875.8 4,275.9

Current expenditure as % GDP 40.8 31.6 37.4 32.0

Overall Fiscal Balance as % GDP -9.8 -3.7 -4.8 -2.0

Primary Fiscal Balance as % GDP -2.3 4.2 9.8 8.2

Source: Ministry of Finance and IMF

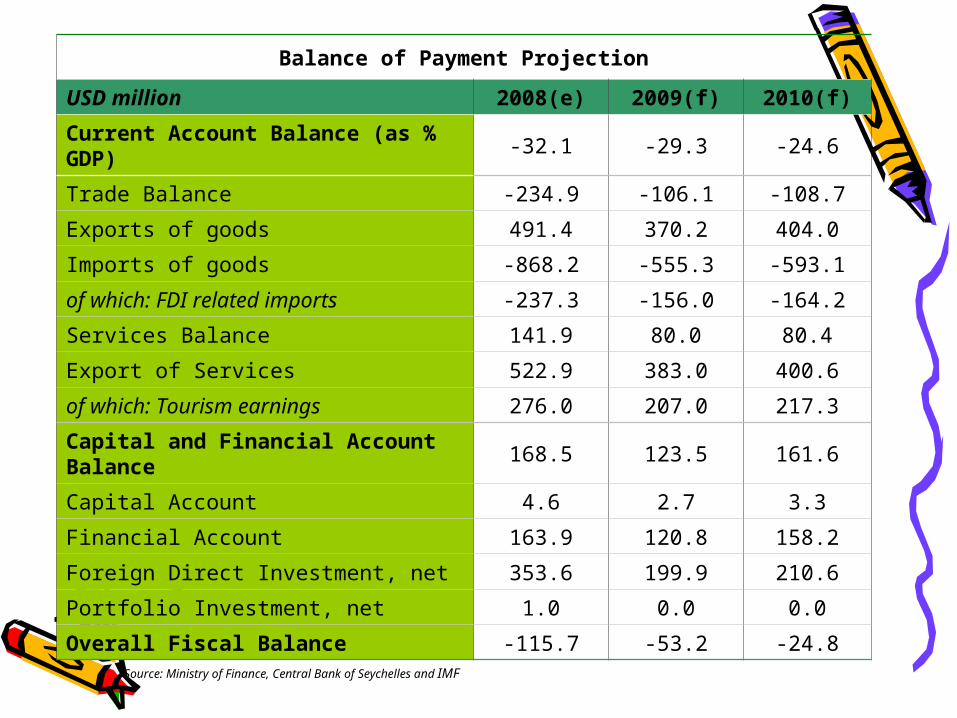

Balance of Payment Projection

USD million 2008(e) 2009(f) 2010(f)

Current Account Balance (as % GDP) -32.1 -29.3 -24.6

Trade Balance -234.9 -106.1 -108.7

Exports of goods 491.4 370.2 404.0

Imports of goods -868.2 -555.3 -593.1

of which: FDI related imports -237.3 -156.0 -164.2

Services Balance 141.9 80.0 80.4

Export of Services 522.9 383.0 400.6

of which: Tourism earnings 276.0 207.0 217.3

Capital and Financial Account Balance 168.5 123.5 161.6

Capital Account 4.6 2.7 3.3

Financial Account 163.9 120.8 158.2

Foreign Direct Investment, net 353.6 199.9 210.6

Portfolio Investment, net 1.0 0.0 0.0

Overall Fiscal Balance -115.7 -53.2 -24.8

Source: Ministry of Finance, Central Bank of Seychelles and IMF

MAURITIUS

Background Information • As for Mauritius the initial impact, was not as severe

as in the case of the Seychelles

• The well diversified aspect of the Mauritian economy and the stimulus package help

• However, since the beginning of the year Mauritius is feeling the heat of the global crisis

Impact of the Credit Crunch on the Economy

• Nearly all of the key sectors of the Mauritius economy have been hit by the global economic crisis.

• Signs include;decline in the tourism industry, closure of textile firms and slowing down of the construction industry (worse of all) the miscalculated decision by Air

Mauritius was fatal

• Mauritius is now in discussion with IMF, World Bank and AfDB for financial assistance to help deal with the impact of the global economic crisis

• Bailout of Air MauritiusStarted when the airline hedged 80% of its fuel

consumption at US$105/bblImmediately afterward global economy entered into

recession and oil price slumped to a record lowAir Mauritius found itself in deep financial problem

and was on the verge of collapse until the Government step in with a bailout

• Unemployment PressureStatistics indicate a drop in unemployment rate, from

8.5% in 2007 to 7.8% in 2008.With key sectors in recession it is expected that

figures for 2009 will be on the upside

• InflationInflation has gone down and MPC declared that they

expected inflation (both average and year-on-year) to converge to around 4% in 2009. (Now below 4%)

Economic Risk• Mauritius is already suffering from a drop in

domestic demand. • Real GDP is projected to grow between 2-2.5% in

2009-07-01• The fact that most of the major world economies

already entered into recession, is posing major risks to the important export industry in Mauritius

• With demand expected to drop by almost 15%, is a real blow to this sector

• Despite the large fiscal stimulus of US$ 310 mn Mauritius could not be rescued from the vicissitude of the global economy

Macroeconomic Imbalance• With tourism, textile, FDI and domestic demand all

declining, additional pressure was being put on the budget.

• Overall budget deficit has now been revised upward to 3.9% of GDP from earlier forecast of 3.3%.

• According to Reuters, the Mauritius Finance Minister had expressed views that the deficit could be even worse if necessary measures not taken.

• Dr. Sithanen hinted a deficit of 7% by the end of 2009

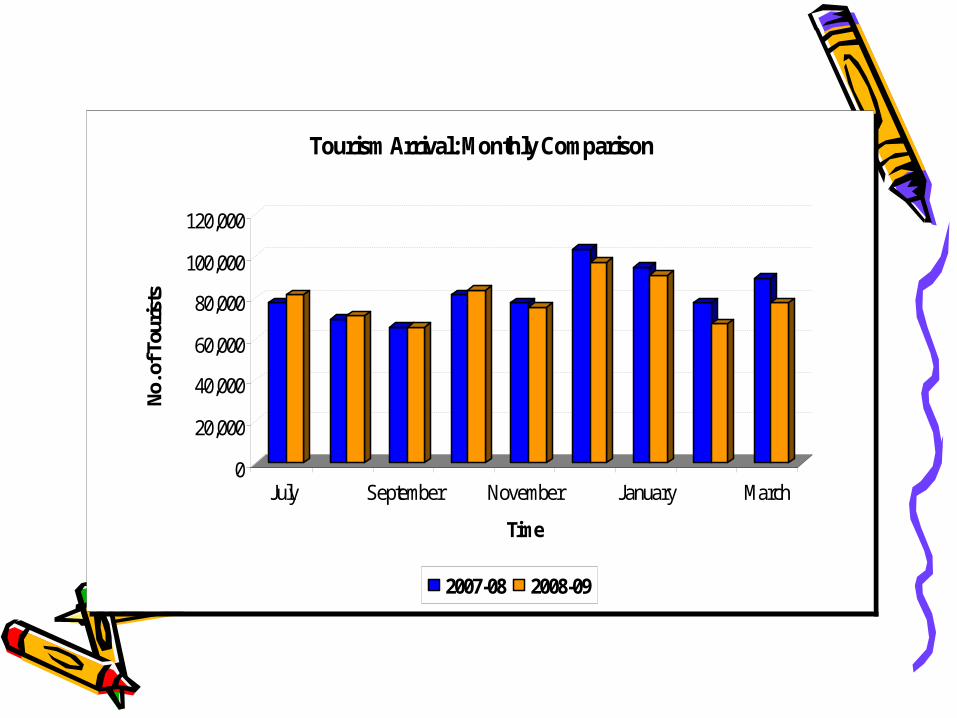

Tourism Sector

• Growth rate in tourism arrivals declined by 9.9% in 1st quarter of 2009

• Global economic recession in key European market, (accounts for 66% of total arrival) is the main reason

• Outlook for 2009 is expected to be worse, both in terms of arrivals and FDI

0

20,000

40,000

60,000

80,000

100,000

120,000

No.

of T

ouris

ts

July September November January March

Time

Tourism Arrival: Monthly Comparison

2007-08 2008-09

Business Confidence and FDI• FDI is expected to be on the decline in 2009

• FDI for 1st quarter 2009 shows an amount of only MUR 1.3 billion (compared to MUR 11.42 bn in 2008)

• According to MPC current environment is characterised by weak business sentiment

• Even the large fiscal stimulus was not enough to overturn the shattered business confidence

• In response to the falling international demand for Mauritian products, the Mauritius Exports Association is lobbying the Government to react swiftly by devaluing the local currency (MUR) by a further 30%

• Government is resisting pressure to do so as it fears this will compound on the already flimsy domestic demand, with many households finding it hard to manage

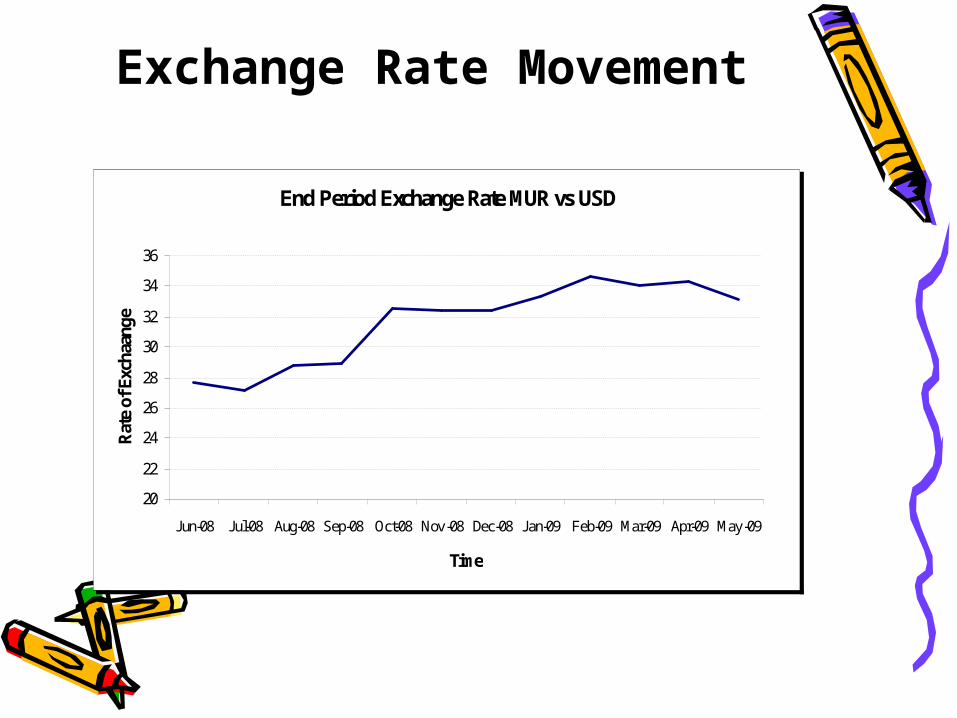

Exchange Rate Movement

End Period Exchange Rate MUR vs USD

20

22

24

26

28

30

32

34

36

Jun-08 Jul-08 Aug-08 Sep-08 Oct-08 Nov -08 Dec-08 Jan-09 Feb-09 Mar-09 Apr-09 May -09

Time

Rat

e of

Exc

haan

ge

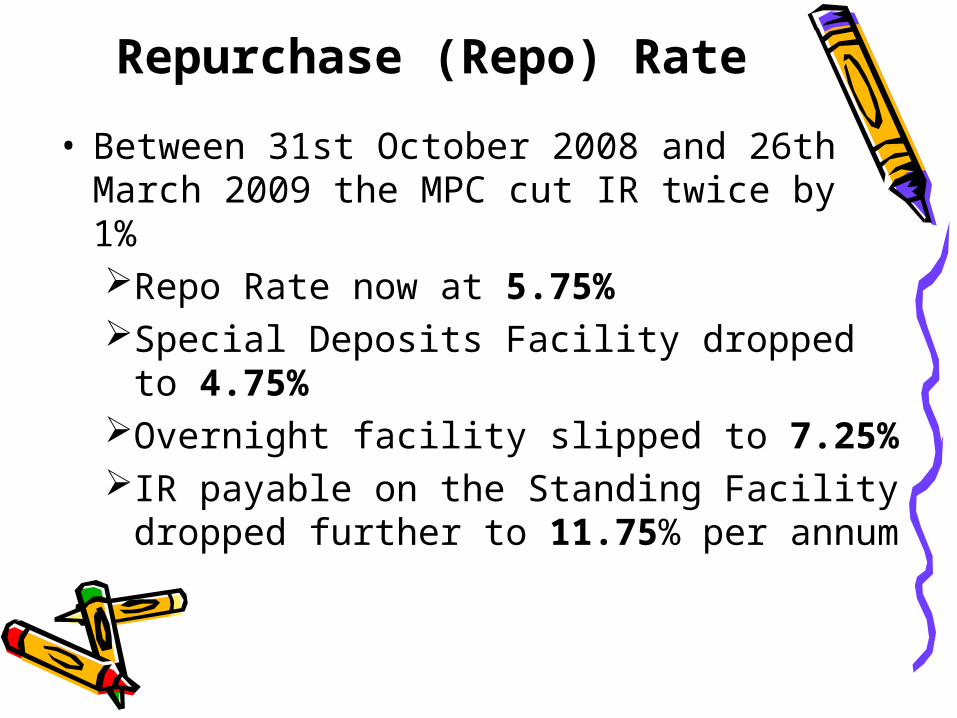

Repurchase (Repo) Rate

• Between 31st October 2008 and 26th March 2009 the MPC cut IR twice by 1%Repo Rate now at 5.75% Special Deposits Facility dropped to 4.75%Overnight facility slipped to 7.25% IR payable on the Standing Facility dropped

further to 11.75% per annum

BALANCE OF PAYMENT DEVELOPMENT

• Overall BoP for 1st quarter of 2009 recorded a surplus of US$ 5 million

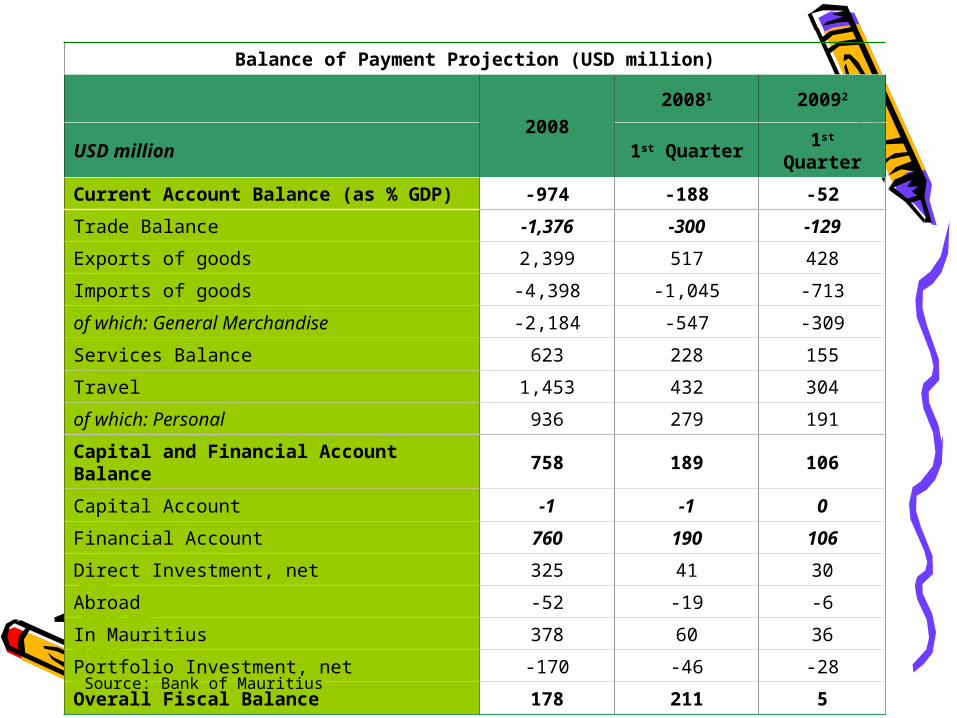

Balance of Payment Projection (USD million)

200820081 20092

USD million 1st Quarter 1st Quarter

Current Account Balance (as % GDP) -974 -188 -52

Trade Balance -1,376 -300 -129

Exports of goods 2,399 517 428

Imports of goods -4,398 -1,045 -713

of which: General Merchandise -2,184 -547 -309

Services Balance 623 228 155

Travel 1,453 432 304

of which: Personal 936 279 191

Capital and Financial Account Balance 758 189 106

Capital Account -1 -1 0

Financial Account 760 190 106

Direct Investment, net 325 41 30

Abroad -52 -19 -6

In Mauritius 378 60 36

Portfolio Investment, net -170 -46 -28

Overall Fiscal Balance 178 211 5

Source: Bank of Mauritius