indiabulls real estate ltd.ideasfirst.in/admin/downloads/reports/2082604312_ibrel... ·...

TRANSCRIPT

A Qualitative Equity Research Company

Analyst: Lovelesh Manocha [email protected]

Vishal Chopda [email protected]

Indiabulls Real Estate Ltd (IBREL) is a real estate company engaged

in development of commercial properties, residential properties and

SEZs having a pan-India presence.

The company also has presence in power

subsidiary Indiabulls Power Ltd (IPL) in which it holds 58.6% of equity.

Further, the company has a 52.3% effective stake (45.3% equity + 7%

through fees) in Indiabulls Properties Investment Trust (IPIT) which is

listed in Singapore. IPIT develops commercial and residential

properties mainly in south central Mumbai.

The company recently bought around 11 acres of mill land in Worli for

a total consideration of Rs.19,790 mn.

September 22

Investment Rationale

Like manufacturing companies, for a real estate company

successful there are must have set of traits, viz.

raw material (land and capital), (2) liaisoning abilities with

government agencies, (3) strong & growing end user demand in

the region and (4) strong execution capabilities.

IBREL has assets in prime areas like Central Mumbai, upcoming Navi

Mumbai Airport & Gurgaon, strong project pipeline in both residential

commercial space and huge land bank which is in possession

paid for. Further, the company has successfully bid for land auctions in

the past and has received higher FSI under various schemes.

IBREL scores highly on parameters 1, 2 and

capabilities of the company are yet to be ascertained due to the young

age of the company. However, given the past track record of

promoters and group companies we feel the company has the

capability to execute the projects on time.

Further, the company has a stake in the power business

currently quoting at inexpensive valuations with the stock trading below

book value.

Valuation

With inexpensive valuations, huge land bank and a stake in the power

business, IBREL is an attractive opportunity with a potential to give

triple digit percentage return over medium-long term horizon.

Based on a SOTP valuation for its various assets, we estimate a NAV

of ` ` ` ` 287 per share for IBREL. At CMP of ` ` ` ` 179.20

at a discount of 38% to its NAV. We feel as the view of the market on

the real estate sector improves the stock will start trading near to its

NAV implying a good upside for the stock from its current levels.

The company scores a 4 (out of 5) on our star matrix and has been

assigned the low risk-medium return rating.

We recommend a Strong Buy on the stock

implying an upside of 60% from current levels.

al Chopda [email protected]

Risk Return Matrix

Real Estate Ltd (IBREL) is a real estate company engaged

in development of commercial properties, residential properties and

generation through its

IPL) in which it holds 58.6% of equity.

Further, the company has a 52.3% effective stake (45.3% equity + 7%

through fees) in Indiabulls Properties Investment Trust (IPIT) which is

listed in Singapore. IPIT develops commercial and residential

The company recently bought around 11 acres of mill land in Worli for

CMP (`̀̀̀)

179.20

-

20

40

60

80

100

120

140

Indiabulls Real Estate

Shareholding Pattern (%)

DII

3.4

Others

15.4

Relative Performance

Indiabulls Real Estate Ltd.September 22, 2010

Like manufacturing companies, for a real estate company to be

there are must have set of traits, viz. (1) easy access to

capital), (2) liaisoning abilities with

government agencies, (3) strong & growing end user demand in

the region and (4) strong execution capabilities.

assets in prime areas like Central Mumbai, upcoming Navi

ct pipeline in both residential &

commercial space and huge land bank which is in possession & fully

Further, the company has successfully bid for land auctions in

the past and has received higher FSI under various schemes.

and 3 while the execution

capabilities of the company are yet to be ascertained due to the young

age of the company. However, given the past track record of

promoters and group companies we feel the company has the

in the power business and is

nexpensive valuations with the stock trading below

With inexpensive valuations, huge land bank and a stake in the power

IBREL is an attractive opportunity with a potential to give

long term horizon.

Based on a SOTP valuation for its various assets, we estimate a NAV

179.20, the stock is trading

% to its NAV. We feel as the view of the market on

roves the stock will start trading near to its

NAV implying a good upside for the stock from its current levels.

The company scores a 4 (out of 5) on our star matrix and has been

stock with a target of ` ` ` ` 287

% from current levels.

BSE NSE

532832 IBREALEST

Face Value (`̀̀̀)

Book Value (`̀̀̀)

52 -week range (`̀̀̀)

M cap (`̀̀̀ Mn)

12-mnth Avg. Daily Vol.

Shares Outstanding Equity (Mn)

Free Float (%)

Market Data

1

Return Matrix

Target (`̀̀̀) Rating

287.00

Indiabulls Real Estate BSE Sensex

Shareholding Pattern (%)

Promoter

22.1

FII

59.2

Relative Performance

Indiabulls Real Estate Ltd.

Initiating Coverage

BLOOMBERG REUTERS

IBREALEST IBREL@IN INRL.BO

: 2

: 235

: 298/142

: 71,977

mnth Avg. Daily Vol. : 5,411,484

Shares Outstanding Equity (Mn) : 401.7

: 78.0

September 22, 2010

IBREL

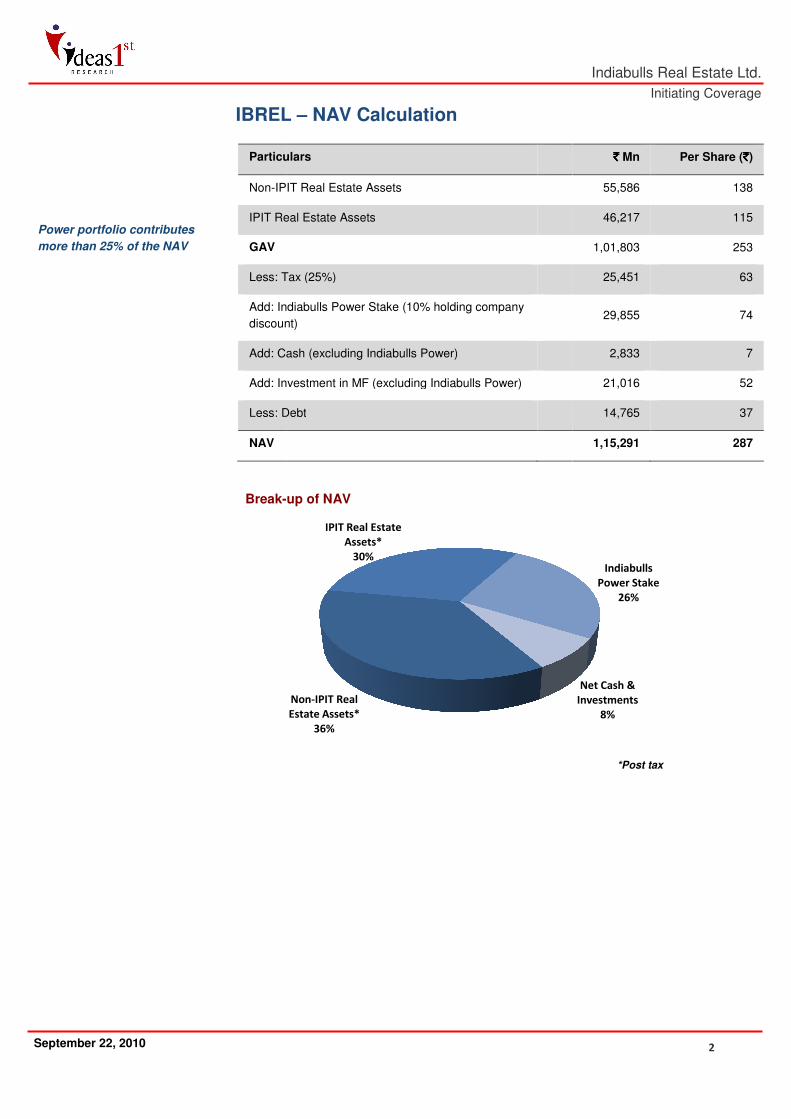

Particulars

Non-IPIT

IPIT Real Estate Assets

GAV

Less: Tax (25%)

Add: India

discount)

Add: Cash (excluding

Add: Investment in MF (excluding

Less: Debt

NAV

Break-

Power portfolio contributes

more than 25% of the NAV

IBREL – NAV Calculation

Particulars

IPIT Real Estate Assets

Real Estate Assets

Less: Tax (25%)

ndiabulls Power Stake (10% holding company

discount)

Add: Cash (excluding Indiabulls Power)

Add: Investment in MF (excluding Indiabulls Power)

Less: Debt

-up of NAV

Non-IPIT Real

Estate Assets*

36%

IPIT Real Estate

Assets*

30%

Indiabulls Real Estate Ltd.

Initiating Coverage

2

`̀̀̀ Mn Per Share (`̀̀̀)

55,586 138

46,217 115

1,01,803 253

25,451 63

29,855 74

2,833 7

21,016 52

14,765 37

1,15,291 287

Indiabulls

Power Stake

26%

Net Cash &

Investments

8%

*Post tax

Indiabulls Real Estate Ltd.

Initiating Coverage

3 September 22, 2010

Table of Contents

Investment Rationale ............................................................................................................. 4

Overview ................................................................................................................................ 6

Real Estate Assets................................................................................................................... 7

Non – IPIT Real Estate Assets ........................................................................................... 7

IPIT Real Estate Assets ...................................................................................................... 9

Summary of Real Estate Assets ...................................................................................... 10

Indiabulls Power Ltd. ............................................................................................................ 11

Valuation .............................................................................................................................. 12

Methodology .................................................................................................................. 12

Assumptions for NAV Calculation ................................................................................... 12

Detailed NAV Calculation ................................................................................................ 14

Sensitivity Analysis .......................................................................................................... 16

Key Risks ............................................................................................................................... 17

Annexure I - Real Estate Project Status ................................................................................ 18

Annexure II - Power Project Status ...................................................................................... 21

Annexure III – Past Financials ............................................................................................... 22

Annexure IV – Industry View ................................................................................................ 23

Annexure V – About Indiabulls Group .................................................................................. 28

Indiabulls Real Estate Ltd.

Initiating Coverage

4 September 22, 2010

Investment Rationale

Assets in prime areas

IPIT has 3.3 msf of leasable commercial area, 3.3 msf of saleable residential area and 0.5 msf

of additional area in the prime locations (around Lower Parel) of Mumbai. Even though IPIT

forms a small proportion of the total area to be developed by IBREL, it constitutes a substantial

part of NAV due to the high sale & lease rates in those areas and as the projects are near

completion stage. The Lower Parel land (Jupiter & Elphistone mills) was acquired from NTC in

2005 through an auction process at a consideration of ` 7,200 mn. Land prices in this area

have appreciated substantially (more than 3x) since then. With the property prices near all times

highs, the company is set to make huge gains from these projects.

IBREL also has a project in Panvel which is quite close to the proposed Navi Mumbai airport.

Given the vantage location, the prices have already appreciated and the company stands to

gain even more if the airport comes up at the proposed site.

Continued stream of cash flows

Apart from the 7.1 msf of IPIT projects in Lower Parel which will start generating revenues from

FY12, IBREL has non-IPIT projects of 49.0 msf to be delivered over next 4-5 years. These

projects are located all across India with majority being in Panvel (20 msf). Currently, the

company has 14.46 msf of area under construction

At current market prices, the company expects to generate revenues of ` 217,720 mn from

these projects over the next 5 years and ` 10,250 mn during FY11 (excluding IPIT projects).

The Panvel project will be a major contributor to revenue in the coming years.

Huge land bank

Apart from IPIT projects and non-IPIT projects given above where work has started, IBREL has

residential land of 434 acres, commercial land of 56 acres and SEZ of 2500 acres. All of the

above land are fully paid for and is in the possession of the company.

The 434 acres of residential land includes 35 acres of prime land in South Delhi (Tehkand)

purchased in a DDA auction in 2006. The company recently received a favorable judgment from

the high court on this project. The project will aggregate to 1.2 msf of saleable residential area

and the company expects to receive necessary approvals soon. The remaining land area

includes 250 acres of the Savroli project (on Mumbai Pune highway) and 149 acres of the

Sonepat residential project.

The 2500 acres of SEZ land is located at Nashik, Maharashtra where the company plans to set-

up a multi-product SEZ. The proposed SEZ has good connectivity and is on the Shirdi-Nashik

highway while the nearest airport and railway station are 40-50 kms away.

Recently (July 2010-Aug 2010), the company bought Bharat mill land (8.37 acre) and Poddar

mill land (2.30 acre) for a consideration of Rs.15,040 mn and Rs.4,740 mn respectively.

7.1msf of area under development in Lower Parel, Mumbai (52.7% IBREL interest) IBREL’s share of revenue from the entire area under development at current market prices is ` ` ` ` 217,720 mn Land bank of 2,990 acres which is fully paid for and in possession of the company

Indiabulls Real Estate Ltd.

Initiating Coverage

5 September 22, 2010

Share in the power business

IBREL holds a 58.6% stake in Indiabulls Power Ltd (IPL) which was publicly listed in Oct 2009.

At IPL’s current market cap, IBREL’s stake in IPL is worth ` 34,416 mn.

Post the IPO, IPL has strong balance sheet which will help it to execute the projects it intends to

undertake. Work on the Nasik Phase I and Amravati Phase I have already started. Coal

linkages for both the projects were granted in November 2008.

Totally, IPL plans to have a capacity of 6615 MW (coal-fired) and 167 MW (hydro) in next 3-4

years. Coal linkages for Phase II of Nasik and Amravati project has also been granted in April

2010. Further, 1200MW has been tied up in long term Power Purchase Agreement with

Maharashtra State Electricity Distribution Company Limited at a tariff of ` 3.26/unit from the

Amravati Phase I project.

The share price of IPL has already seen a fall of 35% from its issue price and is currently

quoting at attractive valuations compared to its peers.

Inexpensive valuations

At CMP, IBREL is trading at P/BV of 0.76x based on June 2010 book value. The company has

already paid for the entire land it owns and its Mumbai land has been brought during 2005

where prices has increased considerably compared to the acquisition cost. Further, with many

of the projects in the execution phase the return on equity for the company is also bound to

improve.

58.6% stake in IPL which is

executing 5 coal-fired plants

aggregating 6615 MW and 4

hydro projects aggregating

167 MW

IBREL share price is

currently quoting at P/BV of

0.76x

Indiabulls Real Estate Ltd.

Initiating Coverage

6 September 22, 2010

Indiabulls Real Estate Ltd. (IBREL)

Non – IPIT Real Estate (100% ownership)

IPIT – Singapore Listed (45.3%

ownership + 7% fees)

Indiabulls Power (58.6% ownership)

Non-IPIT Real Estate (100% ownership)

Area Under Development

• 40.70 msf of residential area

• 8.30 msf of commercial area

Area owned by IBREL where work has not started

• Residential – 434 acres

• Commercial – 56 acres

• SEZ – 2500 acres

IPIT – Singapore Listed (45.3% ownership + 7% fees)

• 3.30 msf of commercial development

• 3.30 msf of residential development

• 0.50 msf of further development to be finalized

Indiabulls Power (58.6% ownership)

• Coal based power plants under development

• Phase I execution already in progress at Nashik and Amravati

• Phase II coal linkages received in April 2010

• Power Purchase Agreement (PPA) for 1200 MW from the Amravati

Phase I project tied up at a tariff of ` 3.26/unit for a term of 25 years

Overview

Market focusing only on IPIT and Power assets

Indiabulls Real Estate Ltd.

Initiating Coverage

7 September 22, 2010

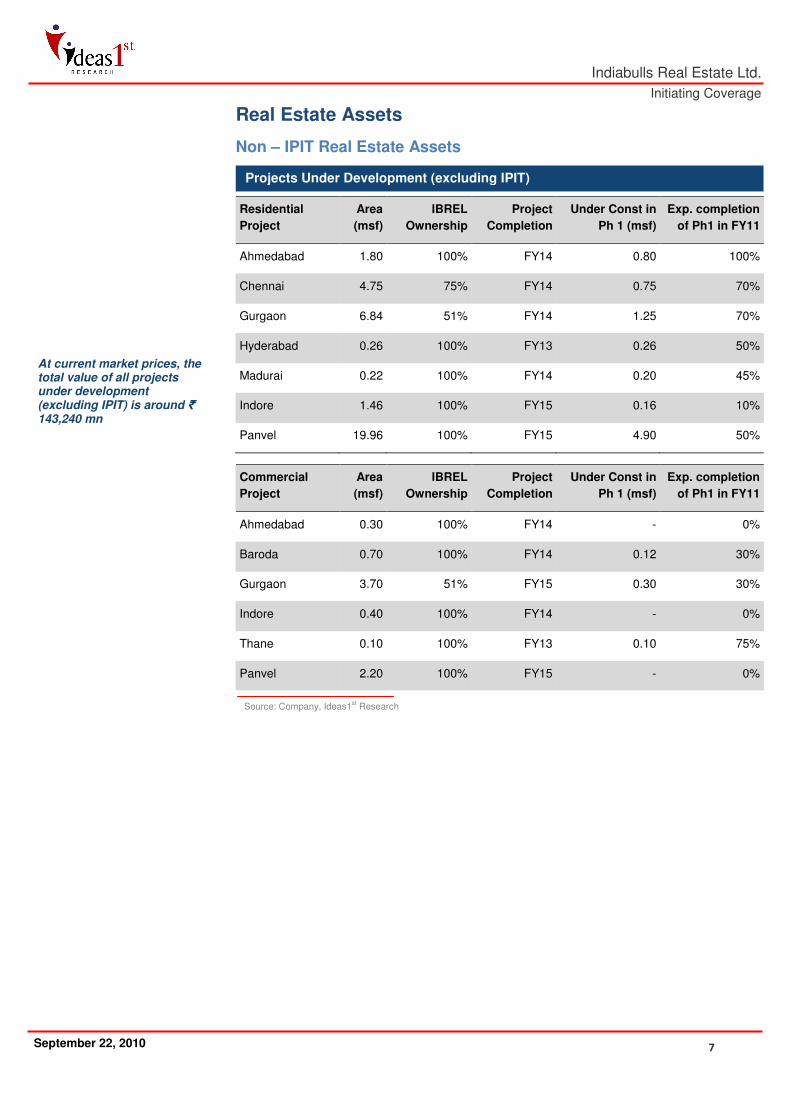

Real Estate Assets

Non – IPIT Real Estate Assets

Projects Under Development (excluding IPIT)

Residential

Project

Area

(msf)

IBREL

Ownership

Project

Completion

Under Const in

Ph 1 (msf)

Exp. completion

of Ph1 in FY11

Ahmedabad 1.80 100% FY14 0.80 100%

Chennai 4.75 75% FY14 0.75 70%

Gurgaon 6.84 51% FY14 1.25 70%

Hyderabad 0.26 100% FY13 0.26 50%

Madurai 0.22 100% FY14 0.20 45%

Indore 1.46 100% FY15 0.16 10%

Panvel 19.96 100% FY15 4.90 50%

Commercial

Project

Area

(msf)

IBREL

Ownership

Project

Completion

Under Const in

Ph 1 (msf)

Exp. completion

of Ph1 in FY11

Ahmedabad 0.30 100% FY14 - 0%

Baroda 0.70 100% FY14 0.12 30%

Gurgaon 3.70 51% FY15 0.30 30%

Indore 0.40 100% FY14 - 0%

Thane 0.10 100% FY13 0.10 75%

Panvel 2.20 100% FY15 - 0%

At current market prices, the total value of all projects under development (excluding IPIT) is around ` ` ` ` 143,240 mn

Source: Company, Ideas1st Research

Indiabulls Real Estate Ltd.

Initiating Coverage

8 September 22, 2010

Description of Key Projects (excluding IPIT)

Project Description

Central Park,

Ahmedabad

The project is located in the Saraspur Area and is 1 km from the railway

station. 1 BHK and 2 BHK apartments will be designed.

High Street,

Baroda

The project is located on Jaitalpur Road near railway station. High end

integrated development is planned.

Greens, Chennai

The project is located on OMR Road close to software companies like TCS,

Wipro, Infosys etc. Premium residential township of 900 units of 2 BHK and 3

BHK will be designed.

Central Park,

Gurgaon

The project is located on the new Gurgaon-Dwarka Expressway. The project

will entail both commercial and residential development.

Central Park,

Hyderabad

The project is located near Indra Park and Husain Sagar Lake in Central

Hyderbad. 2 BHK, 21/2 BHK, 3 BHK and 4 BHK apartments in harmony with

Vastu and modern architecture will be designed.

Central Park,

Madurai

The project is located off South Veli Street in close proximity to the Meenakshi

temple and 11 km from Madurai Airport. 2 BHK and 3 BHK apartments will be

designed.

Greens, Panvel

The project is located adjacent to NH4, 5 min drive from Panvel Station and

will also benefit from the upcoming Navi Mumbai Airport. Spread across 80

acres, 2 BHK, 3 BHK and 4 BHK will be designed along with commercial

development of 2.20 msf.

Source: Company, Ideas1st Research

Indiabulls Real Estate Ltd.

Initiating Coverage

9 September 22, 2010

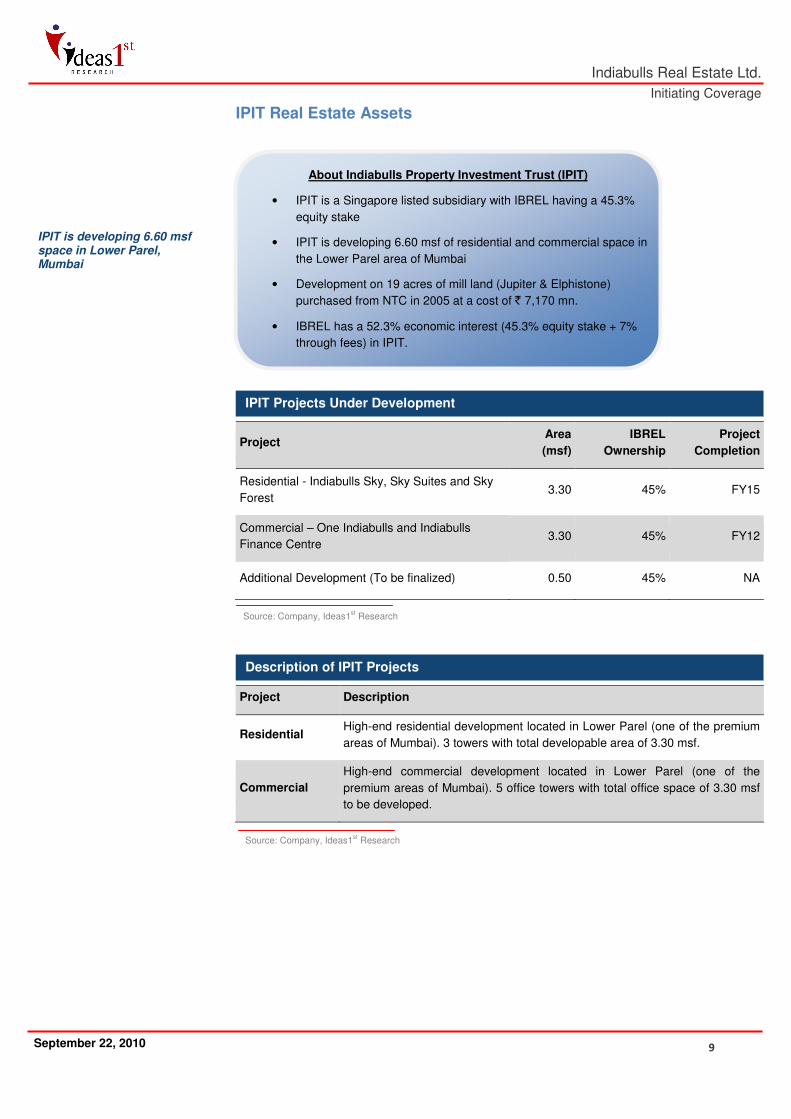

IPIT Real Estate Assets

IPIT is developing 6.60 msf space in Lower Parel, Mumbai

About Indiabulls Property Investment Trust (IPIT)

• IPIT is a Singapore listed subsidiary with IBREL having a 45.3%

equity stake

• IPIT is developing 6.60 msf of residential and commercial space in

the Lower Parel area of Mumbai

• Development on 19 acres of mill land (Jupiter & Elphistone)

purchased from NTC in 2005 at a cost of ` 7,170 mn.

• IBREL has a 52.3% economic interest (45.3% equity stake + 7%

through fees) in IPIT.

IPIT Projects Under Development

Project Area

(msf)

IBREL

Ownership

Project

Completion

Residential - Indiabulls Sky, Sky Suites and Sky

Forest 3.30 45% FY15

Commercial – One Indiabulls and Indiabulls

Finance Centre 3.30 45% FY12

Additional Development (To be finalized) 0.50 45% NA

Source: Company, Ideas1st Research

Description of IPIT Projects

Project Description

Residential High-end residential development located in Lower Parel (one of the premium

areas of Mumbai). 3 towers with total developable area of 3.30 msf.

Commercial

High-end commercial development located in Lower Parel (one of the

premium areas of Mumbai). 5 office towers with total office space of 3.30 msf

to be developed.

Source: Company, Ideas1st Research

Indiabulls Real Estate Ltd.

Initiating Coverage

10 September 22, 2010

Summary of Real Estate Assets

Total sales revenue from the entire area under development at current market prices is ` ` ` ` 310,860 mn

IBREL’s share of revenue from the entire area under development at current market prices is ` ` ` ` 217,720 mn

More than 90% of projects (by value) are in super metro cities –Mumbai Metro Region, NCR and Chennai.

Area Under Development (including IPIT and Non-IPIT)

Area (msf)* Residential Commercial Total

Gross Developable Area 44.50 11.60 56.10

Less – Project Handover - 1.90 1.90

Net Developable Area 44.50 9.70 54.20

Area Under Construction 12.14 2.32 14.46

Source: Company, Ideas1st Research

*Does not include recent Mumbai Mill Land acquisition

Area Under Construction (including IPIT and Non-IPIT)

Area (msf) Residential Commercial Total

Super Metro* 10.70 2.20 12.90

Rest of India 1.44 0.12 1.56

Total 12.14 2.32 14.46

Source: Company, Ideas1st Research

*Super Metro includes Mumbai Region, NCR and Chennai

Land Bank Summary

Residential Commercial SEZ Total

Area (acres) 434 56 2,500 2,990

Source: Company, Ideas1st Research

The 434 acres of residential land includes 35 acres of prime land in South Delhi (Tehkand)

purchased in a DDA auction in 2006. The company recently received a favorable judgment from

the high court on this project. The project will aggregate to 1.2 msf of saleable residential area

and the company expects to receive necessary approvals soon. The remaining land area

includes 250 acres of the Savroli project (on Mumbai Pune highway) and 149 acres of the

Sonepat residential project.

The 2500 acres of SEZ land is located at Nashik, Maharashtra where the company plans to set-

up a multi-product SEZ. The proposed SEZ has good connectivity and is on the Shirdi-Nashik

highway while the nearest airport and railway station are 40-50 kms away.

Indiabulls Real Estate Ltd.

Initiating Coverage

11 September 22, 2010

Indiabulls Power Ltd.

At CMP, IPL has a market cap of ` 58,731 mn. The stock has already seen a fall of more than 35% since its listing in October 2009

IPL Thermal Projects Overview

Project Amravati

Phase I

Nashik

Phase I

Amravati

Phase II

Nashik Phase

II

Bhaiyathan,

Chattishgarh

Proposed

Capacity 1320 MW 1335 MW 1320 MW 1320 MW 1320 MW

Land Available Yes Yes No Yes No

Coal Linkage Yes Yes Yes Yes Yes

Off-take

Agreement

PPA for

1200 MW

signed

No No No PPA for 65% of

generated power

Expected

Commissioning June 2012

September

2011 March 2013 March 2013 December 2012

Expected Cost (`

mn) 68,880 60,480 55,866 57,338 67,960

Source: Company, Ideas1st Research

About Indiabulls Power Ltd. (IPL)

• IBREL has a 58.6% stake in IPL

• IPL was listed on NSE and BSE in October 2009

• IPL is developing 5 coal-fired plants aggregating 6615 MW and 4

hydro projects aggregating 167 MW.

Indiabulls Real Estate Ltd.

Initiating Coverage

12 September 22, 2010

Valuation

Methodology

Assumptions for NAV Calculation

Non-IPIT Residential Projects

Project

Selling

price

(`̀̀̀/sq ft)

Const.

cost (`̀̀̀/sq

ft)

Cash flow break-up

FY11 FY12 FY13 FY14 FY15

Central Park,

Ahmedabad 1,980 1,200 20% 30% 30% 20% -

Greens, Chennai 3,015 1,700 20% 30% 30% 20% -

Central Park, Gurgaon 2,655 1,700 20% 30% 30% 20% -

Central Park, Hyderabad 3,240 1,700 25% 45% 30% - -

Central Park, Madurai 2,250 1,600 20% 30% 30% 20% -

Central Park, Indore 1,980 1,500 - 20% 30% 30% 20%

Greens, Panvel 3,060 1,700 - 20% 30% 30% 20%

Non-IPIT Commercial Projects

Project

Selling

price

(`̀̀̀/sq ft)

Const.

cost (`̀̀̀/sq

ft)

Cash flow break-up

FY11 FY12 FY13 FY14 FY15

Central Park,

Ahmedabad 2,700 1,700 20% 30% 30% 20% -

High Street, Baroda 3,150 1,700 20% 30% 30% 20% -

Central Park, Gurgaon 4,500 1,700 20% 30% 30% 20% -

Central Park, Indore 1,980 1,700 20% 30% 30% 20% -

Mint, Thane 4,950 1,700 25% 45% 30% - -

Greens, Panvel 3,150 1,700 - 20% 30% 30% 20%

We have used Sum-of-the-Parts (SOTP) based valuation methodology to value IBREL. We

have calculated Gross Asset Value (GAV) by using DCF method to value the Non-IPIT & IPIT

properties under development and have assigned value to the land bank by assuming selling

price for the land bank. Finally, we have calculated Net Asset Value (NAV) by deducting taxes,

adding power business stake and net cash & investments (excluding power).

Indiabulls Real Estate Ltd.

Initiating Coverage

13 September 22, 2010

IPIT Residential Projects

Project

Selling

price

(`̀̀̀/sq ft)

Const.

cost (`̀̀̀/sq

ft)

Cash flow break-up

FY11 FY12 FY13 FY14 FY15

Indiabulls Sky, Sky

Suites and Sky Forest -

Mumbai

18,900 5,000 - 20% 30% 30% 20%

IPIT Commercial Projects

Project

Selling

price

(`̀̀̀/sq ft)

Const.

cost (`̀̀̀/sq

ft)

Cash flow break-up

FY11 FY12 FY13 FY14 FY15

One Indiabulls and

Indiabulls Finance Centre

- Mumbai

175 3,500 30% 70% - - -

WACC Calculation

Risk Free Rate 8%

Beta 1.54

Equity Risk Premium 8%

Cost of Equity 20%

Cost of Debt (pre tax) 13%

Tax rate 25%

Total Long Term Debt / Equity Ratio 1

WACC 15%

Other Assumptions

• Capitalization rate of 10%

• Residential project to be developed at 0.50 msf of IPIT land and cash flow

from the same to occur over FY15 - FY18

• 2,990 acres of land (including the Nashik SEZ land) has been valued at ` ` ` ` 150

/sq ft with a FSI of 1.0. This also includes the 35 acres of land in South Delhi.

• Recent land acquisitions in Mumbai and few other projects where details

not available are not considered for NAV calculation

• Tax rate of 25% since the GAV also includes land cost

Indiabulls Real Estate Ltd.

Initiating Coverage

14 September 22, 2010

Detailed NAV Calculation

Non-IPIT Residential Projects

Project `̀̀̀ Mn Per Share (`̀̀̀)

Central Park, Ahmedabad 1,150 3

Greens, Chennai 3,836 10

Central Park, Gurgaon 2,728 7

Central Park, Hyderabad 348 1

Central Park, Madurai 117 0.29

Central Park, Indore 499 1

Greens, Panvel 19,324 48

Total 28,001 70

Non-IPIT Commercial Projects

Project `̀̀̀ Mn Per Share (`̀̀̀)

Central Park, Ahmedabad 246 1

High Street, Baroda 831 2

Central Park, Gurgaon 4,327 11

Central Park, Indore 92 0.23

Mint, Thane 282 1

Greens, Panvel 2,271 6

Total 8,048 20

IPIT Projects

Project `̀̀̀ Mn Per Share (`̀̀̀)

Indiabulls Sky, Sky Suites and Sky

Forest - Mumbai 17,077 43

One Indiabulls and Indiabulls Finance

Centre - Mumbai 27,440 68

To be finalized (0.50 msf) – Mumbai 1,700 4

Total 46,217 115

September 22, 2010

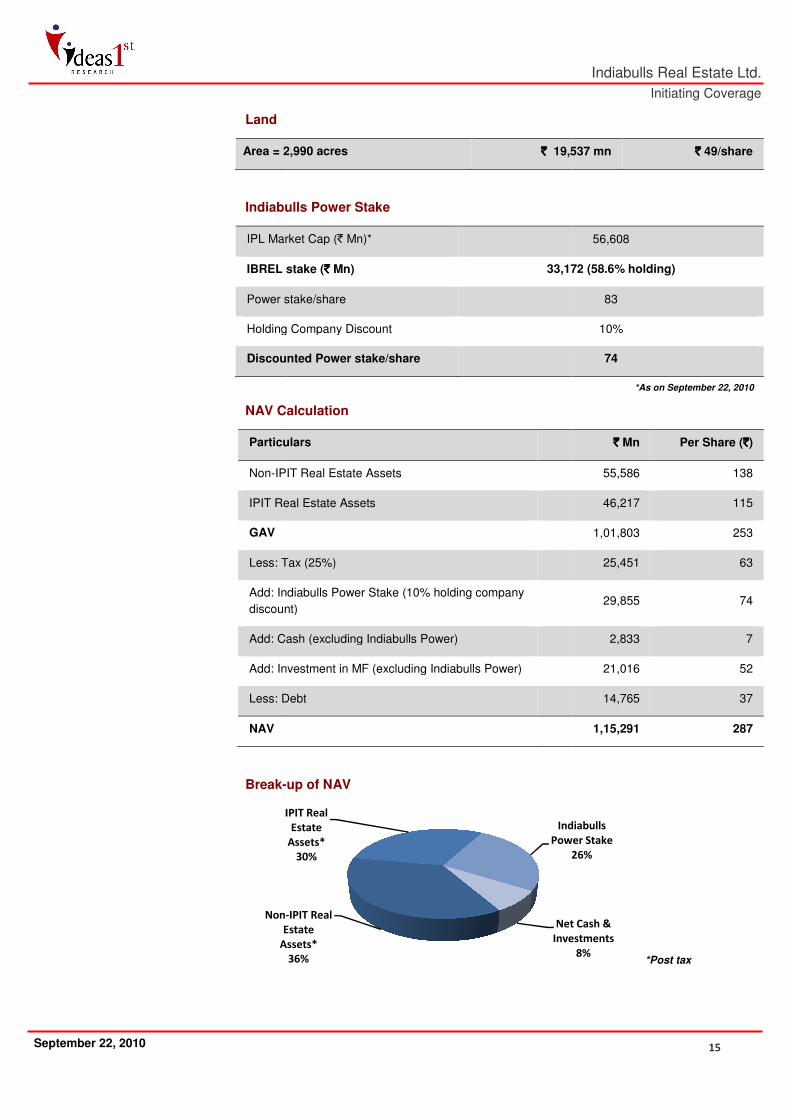

Land

Area = 2,990 acres

Indiabulls Power Stake

IPL Market Cap (

IBREL stake

Power stake/share

Holding Company

Discounted Power stake/share

NAV Calculation

Particulars

Non-IPIT

IPIT Real Estate Assets

GAV

Less: Tax (25%)

Add: India

discount)

Add: Cash (excluding

Add: Investment in MF (excluding

Less: Debt

NAV

Break-

Non-

Estate

Assets*

IPIT Real

2,990 acres `̀̀̀ 19,537

Indiabulls Power Stake

IPL Market Cap (` Mn)*

IBREL stake (`̀̀̀ Mn) 33,172

Power stake/share

Holding Company Discount

Discounted Power stake/share

NAV Calculation

Particulars

IPIT Real Estate Assets

Real Estate Assets

Less: Tax (25%)

ndiabulls Power Stake (10% holding company

discount)

Add: Cash (excluding Indiabulls Power)

Add: Investment in MF (excluding Indiabulls Power)

Less: Debt

-up of NAV

-IPIT Real

Estate

Assets*

36%

IPIT Real

Estate

Assets*

30%

Indiabulls

Power Stake

26%

Net Cash &

Investments

Indiabulls Real Estate Ltd.

Initiating Coverage

15

19,537 mn `̀̀̀ 49/share

56,608

3,172 (58.6% holding)

83

10%

74

*As on September 22, 2010

`̀̀̀ Mn Per Share (`̀̀̀)

55,586 138

46,217 115

1,01,803 253

25,451 63

29,855 74

2,833 7

21,016 52

14,765 37

1,15,291 287

Indiabulls

Power Stake

26%

Net Cash &

Investments

8%*Post tax

Indiabulls Real Estate Ltd.

Initiating Coverage

16 September 22, 2010

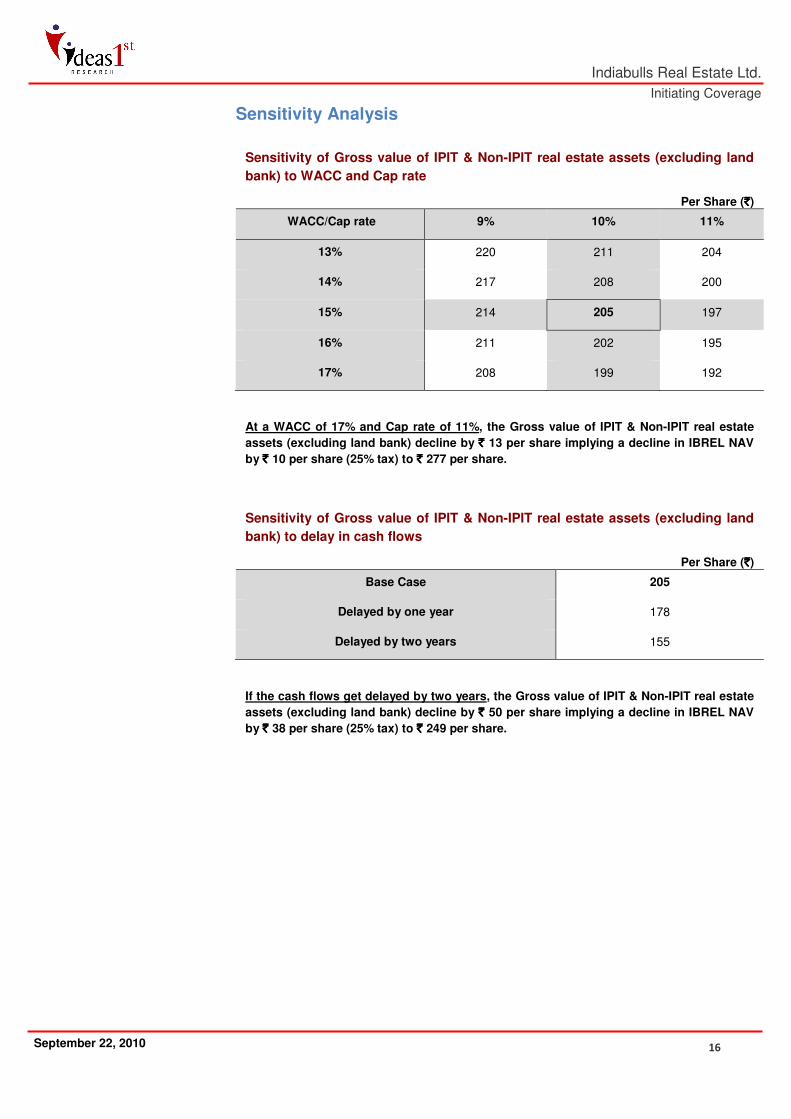

Sensitivity Analysis

Sensitivity of Gross value of IPIT & Non-IPIT real estate assets (excluding land

bank) to WACC and Cap rate

Per Share (`̀̀̀)

WACC/Cap rate 9% 10% 11%

13% 220 211 204

14% 217 208 200

15% 214 205 197

16% 211 202 195

17% 208 199 192

At a WACC of 17% and Cap rate of 11%, the Gross value of IPIT & Non-IPIT real estate

assets (excluding land bank) decline by ` ` ` ` 13 per share implying a decline in IBREL NAV

by ` ` ` ` 10 per share (25% tax) to ` ` ` ` 277 per share.

Sensitivity of Gross value of IPIT & Non-IPIT real estate assets (excluding land

bank) to delay in cash flows

Per Share (`̀̀̀)

Base Case 205

Delayed by one year 178

Delayed by two years 155

If the cash flows get delayed by two years, the Gross value of IPIT & Non-IPIT real estate

assets (excluding land bank) decline by ` ` ` ` 50 per share implying a decline in IBREL NAV

by ` ` ` ` 38 per share (25% tax) to ` ` ` ` 249 per share.

Indiabulls Real Estate Ltd.

Initiating Coverage

17 September 22, 2010

Key Risks

Oversupply in South Central Mumbai

With most of the real estate players, developing premium properties on the mill lands in South

Central Mumbai region there is a fear of oversupply in the area. This can slow down the

absorption of properties affecting the NAV of the company.

However, most of the players have a very healthy balance sheet and thus, have the capability to

hold on to inventory without reducing the prices.

Low promoter holding

Promoters of IBREL have only 22.1% stake (as on June 2010) in the company while most other

real estate companies have a promoter holding > 50%. The low promoter holding raises a risk

since IBREL has a lot of cash which is under the control of promoters & management. Further,

ROE delivered by the company has been historically very low. Hence, deployment of cash in

productive assets leading to improvement in ROE is required. However, over the past two

quarters the promoter stake has increased gradually from 16.7% to 22.1% indicating the

commitment and confidence of the promoters in the company.

Project execution risks

IBREL currently has 56.1 msf of area under development and 14.46 msf under construction.

Being a young company they have lesser experience and other bottlenecks like govt clearance,

availability of manpower and working capital requirement could hamper the execution of these

projects.

Further, the company is undertaking large scale power projects under its subsidiary IPL which is

also a new to the company.

Any delay in execution of these projects will significantly impact the valuation of the company.

Power business valuation

Since IBREL has a 58.6% stake in IPL, any deterioration in power business valuation will impact

IBREL valuation.

Economic slowdown

A slowdown in the economy due to any internal or external reasons could impact the demand

and pricing of real estate.

Delay in absorption will

reduce the NAV

Low promoter holding with

huge cash under control

Inexperience in executing

large real estate and power

projects could lead to delays

Indiabulls Real Estate Ltd.

Initiating Coverage

18 September 22, 2010

Annexure I - Real Estate Project Status

Nashik SEZ

Gurgaon Centrum

Panvel - Greens

Chennai - Greens

Source: Company, Ideas1st Research

Indiabulls Real Estate Ltd.

Initiating Coverage

19 September 22, 2010

Real Estate Project Status

Ahmedabad – Central Park

Hyderabad – Central Park

Baroda – High Street

Madurai – Central Park

Source: Company, Ideas1st Research

Indiabulls Real Estate Ltd.

Initiating Coverage

20 September 22, 2010

Real Estate Project Status

Indiabulls Finance Centre – Tower 1

Indiabulls Finance Centre – Tower 2

Indiabulls Finance Centre – Tower 3

Source: Company, Ideas1

st Research

Indiabulls Real Estate Ltd.

Initiating Coverage

21 September 22, 2010

Annexure II - Power Project Status

Amravati Phase I

PCC & Reinforcement Work

Contractor’s Office

Site Office

Nashik Phase I

Boiler Unit Excavation

Contractor’s Offices

Batching Plant being erected

Source: Company, Ideas1st Research

Indiabulls Real Estate Ltd.

Initiating Coverage

22 September 22, 2010

Annexure III – Past Financials

Profit & Loss Statement

`̀̀̀ Mn

Year FY09 FY08 FY07

Net Sales 2,086 1,407 139

Total Income 10,646 16,942 2,447

Operating Profit 1,743 6,220 311

Interest 244 522 53

Depreciation 108 33 8

Net Profit 692 4,067 131

Minority Interest (after tax) 398 65 -9

Net Profit after Minority Interest & P/L of Assoc. Co. 295 4,002 140

Extraordinary Items 50 2,684 -

Adjusted Net Profit 245 1,319 140

EPS before Minority Interest 2.06 13.77 -

EPS after Minority Interest 0.52 13.50 0.03

Balance Sheet

`̀̀̀ Mn

Year FY09 FY08 FY07

Share Capital 1,890 1,857 3,322

Total Shareholders’ Funds 55,283 42,359 14,502

Minority Interest 14,457 14,248 3,418

Total Debt 11,956 3,783 1,420

Total Liabilities 81,696 60,390 19,339

Net Block 1,540 1,493 246

Capital Work in Progress 2,644 753 2

Investments 12,347 675 5,944

Inventories 17,566 11,441 1,993

Sundry Debtors 878 1,165 59

Cash and Bank 15,897 16,218 12,129

Loans and Advances 32,535 49,651 3,758

Total Current Assets 66,876 78,475 17,939

Total Current Liabilities 1,702 20,998 4,785

Net Current Assets 65,174 57,477 13,153

Total Assets 81,696 60,390 19,339

Indiabulls Real Estate Ltd.

Initiating Coverage

23 September 22, 2010

Annexure IV – Industry View

1. Current scenario

The real estate sector has witnessed a strong bull run over the last few years starting 2004, before plunging in second half of 2008. With

the rapid economic growth in the country, the income and surpluses in the hands of the people suddenly increased. Real estate being one

of the only two perennial & traditionally preferred asset class and with the inborn desire of Indians to own a house, the sector became a

natural choice for these excesses to be invested. This sudden spurt in demand caught the fancy of investors globally.

Real estate sector was one of the key beneficiaries of the foreign fund inflows or hot money. However with the global crisis in 2008, this

very fact went against the sector. Also, the crisis had its genesis in real estate sector and as a result the real estate stocks took a steep

plunge across all the countries, including India, even though India’s real estate market was safe and didn’t face proportional impact. The

sudden disappearance of the liquidity and the fear in investor’s minds resulted in steep fall in demand. Real estate companies in India

which had taken huge leveraged positions for expansion in anticipation of booming demand saw their market cap erode quickly and had to

hold projects due to negative cash flows. The share prices of these companies have fallen to unjustified levels even though the long term

fundamentals of the Indian real estate sector haven’t changed.

While economic growth returned and the markets improved beginning the first quarter of 2009, rationality has not come back to the real

estate stocks. Though other sector indices have appreciated many folds over the past one year, the BSE realty index continues to

underperform the broader market by a wide margin. This despite the fact that property prices are almost nearing and in fact even crossed

their 2008 peaks in most places. Further demand has returned to the sector now and projects are being sold out within days of their

launch. It is encouraging to know that even the demand for premium housing is growing fast. Most importantly the debt position and

balance sheet of real estate companies have improved significantly over the past two years. This disconnect in high property prices and

low realty stock prices can be attributed to the unwarranted fear of fall in housing demand due to the anticipated interest rates hike and the

fragile economic milieu in the western countries and their weak real estate stocks. As we discuss later, based on India’s and the sectors

long term fundamentals we believe the Indian real estate sector is in a secular bull run and currently smartly recovering out of the cyclical

bear run.

2. Demand

Even though post crisis the real estate sector has taken a major hit, fundamentally things have only improved. Based on our top down

approach and our strong macro view of the Indian economy we believe the Indian real estate sector is in a multiyear, stable growth

phase. Following are a few of the key points that make us confident on the sector.

a) Domestic consumption story

We believe that the growth matrix in India has never been better. With a focused, pro reform and a stable government at the

center, there is no stopping for India. Even though the global economy is going through an unusually uncertain phase, we believe

that over medium to long term the fundamentals would prevail and see a limited impact of the global developments on the real

sector in case of a negative fallout. . Unlike most other sectors, real estate is a pure domestic theme which is produced,

consumed & sold domestically; global developments in US, Europe, China; et al have only an indirect impact on demand through

confidence and capital channel. It’s surprising to see that while all experts & financial gurus are stressing to invest in Indian

domestic demand driven sectors, real estate has been given a total miss.

We expect the real estate sector to grow step-in-step with the fast growing GDP. A large part of the savings is expected to flow

into real-estate for the twin purpose of having own abode and making a stable investment.

b) Demographics

i. Working age population

In contrast to the aging population and rising dependency ratios in many countries, India is blessed with a young and

growing population. India has amongst the best demographic ratio globally and this would continue to improve over next

three to four decades. This comes at a time when western economies have deteriorating demographic ratio. Even China

is at fag end of its favorable demographic ratio which is expected to peak between 2012 & 2015 and decline sharply

thereafter for next few decades. While demographic dividend is a double edge sword, if handled in a right way it can be

hugely positive for a country. The rising proportion of persons of working age will stimulate savings as pressure on

household and public budgets for the needs of dependent children & elderly comes down. Young workers are

Indiabulls Real Estate Ltd.

Initiating Coverage

24 September 22, 2010

comparatively more mobile who are willing to take chances and ready to migrate where opportunity is available. The

rapidly growing work force implies growing savings leading to higher demand for housing.

ii. Exploding Middle Class

McKinsey Global Institute (MGI) predicts that the India’s middle class will reach 583 million from the current 50 million by

2025. Further it states that the average household income in India will triple over the next two decades and it will become

the world’s 5th-largest consumer economy by 2025, up from 12th now. Another study shows that according to Indian

standards, the middle class population in India is already more than the total population of the United States. With this

exploding middle class the demand for real estate is bound to go up unidirectionally.

iii. Changing trend towards nuclear families

The traditional ‘joint-family’ system in India is rapidly breaking up. With increasing expenses and with more people

migrating to cities for work, people are increasingly opting for nuclear and small families. This undoubtedly means more

demand for residential segments.

c) Huge Surpluses

i. High savings

India is among the very few economies globally that has a high savings rate. A savings rate of approximately 34% of

GDP implies savings of USD 400 million annually. Historically Indian’s have preferred two asset classes over others –

gold and real estate and an increase in savings would directly lead to an increase in demand for these asset classes.

People in urban areas are increasingly investing in second homes too.

ii. Parallel economy

The parallel economy or the ‘black money’ as more commonly known in India is estimated to be anywhere between 40 to

100 percent of the stated GDP. Property is the easiest and most attractive place to park this huge amount of

unaccounted funds. ‘Cash’ component in real estate deals has been a very common practice in India. Other than acting

as an invisible hand supporting the real estate market, the black or unaccounted component also provides a cushion to

banks financing the sector.

d) Growing Income

i. Increasing Employment

Barring the span of 12 to 18 months of the economic slowdown, the employment the employment for both blue and

white collared workers has been increasing in India. With the strong economic recovery in India, companies have

started hiring again. This entails increase in demand for commercial space. Further this increase in work force migration

also means more housing requirement by these corporate.

ii. Inclusive growth

There has been a notable shift in the ‘growth’ in India towards a more ‘inclusive growth’. As a result of the broader based

growth and the redistributive measures by the government, the surplus in the hands of the common man is fast

increasing. The National Rural Employment Guarantee Act (NREGA), the Sixth Pay Commission and the government’s

increased focus on infrastructure would further boost the growth at the ground level. Moreover with manufacturing and

service sector gaining traction in the rural economy, the reliance on farm-based income has decreased substantially over

the years reducing the income volatility.

e) Urbanisation

Approximately only 30% of the total population or 340 million people reside in cities. McKinsey Global Institute (MGI) predicts this

number will go up to 590 million, in next 20 years. This addition of 250 million to urban areas will be at a very rapid pace requiring

only half the time compared to the 40 years (1971-2008) needed to add the last 230 million to the urban population. Such rapid

urbanization would need to be supported by rapid development in real estate may it be residential, commercial or hospitality.

Historically all developed countries have seen a boom in real estate specifically during their fastest growing years characterized

by rapid urbanization. A more recent parallel would be China, one of the few countries to experience such high rates of

urbanization. The real estate growth there over the last decade gives a fair idea about the growth potential of the real estate

sector in India.

Indiabulls Real Estate Ltd.

Initiating Coverage

25 September 22, 2010

f) Perennial investment destination

People in India have a natural tendency to save and are relatively more conservative when it comes to investments. Even today

majority of financially literate people park their surpluses in the traditionally safe haven, real estate. Further the desire to own a

home is relatively very high amongst Indians, house being the first major asset purchased by a majority of them.

g) Low Mortgage to GDP ratio

The real estate industry in India is not driven by bank / non bank finance with bulk of the purchases financed entirely from

savings. The mortgage to GDP ratio in India continues to remain one of the lowest globally with a very low penetration of housing

loans. It is surprising to know that only about 30% of the total realty deals in the country are financed by financial institutions. This

phenomenon can partially be attributable to high savings, huge parallel economy, lack of financial knowledge amongst the public

and limited availability of credit facilities.

Interestingly high value properties are rarely financed by financial institutions, with the portion being financed usually limited to

1/3rd

of the total value. Rather it is the low cost housing sector that forms bulk of the demand for finance.

However this situation is fast changing and the leverage ratio is improving more favorably. The opportunity lies in the problem

itself, offering a great upside to the real estate demand and prices as the mortgage’s market grows.

3. Why the real estate stocks have been beaten down by the investors?

While multiple reasons have been attributed to justify the disconnect between the high real estate prices and low realty stock prices, we

believe that it’s fear, fear and fear that is keeping investors away from the sector. Listed below are the most common fears that we believe

investors have in their minds. Needless to say, that these fears are unwarranted and do not hold in the Indian scenario.

a) Increase in Interest rates

The anticipated interest rate hike by RBI is one of the basic reasons driving the investors out of the real estate sector. With the

increase in cost of financing, investors believe that the demand for real estate would dry up. However we believe that unlike in

other countries, the rise in interest rate will not have a significant impact on the demand of real estate.

The real estate industry in India is not driven by bank / non bank finance with bulk of the purchases being financed entirely from

the savings. This can be easily deduced from its relatively low mortgage to GDP ratio and the fact that only about 30% of the total

realty deals in the country are financed by financial institutions. Additionally, bulk of the demand is coming from the end user and

not just investors, which further mitigates the impact on demand.

b) Global crisis fears

The fragile recovery in the United States, the instability in the Euro zone and the fears of a property bubble in China are

depressing the realty market. However based on India’s strong macroeconomic fundamentals and its limited exposure to the

international market we expect only a mild, if any, impact on India’s growth.

c) Many IPO’s scheduled for launch

The IPO’s scheduled by realty companies over the next few months are believed to be depressing the current investment in the

sector. We believe that given the low market value of the free float stocks in the sector the scheduled IPOs will have minimal, if

any impact on the demand over medium to long term or once sentiments turn around.

4. The transient irrationality

Many property stocks in India are currently trading at over 50% discount to their NAV and approximately 33% of their pre crisis peak price.

However we feel this is mainly because of the global meltdown in property prices and slowdown in China. Given the sector’s domestic

nature it won’t be long before the investors realize its true potential. Following are a few more points that highlight the disconnect between

the fundamentals and the stock prices

a) Real Estate prices nearing 2008 peak prices:

Indiabulls Real Estate Ltd.

Initiating Coverage

26 September 22, 2010

The real estate prices have moved up sharply after plummeting during the recent global economic meltdown. Property prices are

already nearing their 2008 peak prices and have even breached the peak in some regions. However the stock prices of these real

estate developers are yet to be adjusted upwards.

b) Stronger balance sheets:

Pre crisis, most developers had taken huge leveraged positions in anticipation of the growing demand over the coming years.

However with the melt down in second half of 2008, their cash flows deteriorated and balance sheets started bleeding. Debt

levels had grown to unsustainable levels. However these companies have put their house back in order by slowing down their

aggressive expansion plans, adopting a cautious and conservative strategy, and even selling their land. Their debt position and

cash flows are much more comfortable now. Consolidated debt position of the sector as a whole is much lower now. Despite

stronger financials their stock prices continue to get the beating.

c) Business reviving smartly:

The sector has seen smart recovery in the business. Projects are being sold within days of their launch and signs of demand

revival are clearly visible. Despite this optimism fear persists in the stock markets and investors continue to discount the stock

prices for these companies.

With an eye on the above three factors we see every reason for the realty sector to provide exceptional returns from their current

levels and believe the downside to be limited.

Proof

The signs of the revival of the sector are eminent. Projects are getting booked within days of their launch. Further the aggression and

optimism in the sector is clearly visible in the media. Whether it is land purchase at multiple times of reserve price or the size and volume

of their advertisement in most renowned publications, you yourself can judge. These are indirect yet significant indications of the boom

ahead.

5. Why is the Indian real estate sector different from the rest of the world?

The real estate sector in India is very peculiar owed majorly to its economic structure. These structural differences make it vacuous to

compare it with the real estate markets in other countries.

a) Perennial investment destination

People in India have an inborn tendency to save and are relatively more conservative when it comes to investments. Even today

majority of the people park their surpluses in gold and real estate, which are traditionally considered as safe havens for

investment. Further as compared to people across the globe, the desire to own a home is relatively very high amongst Indians,

house being the first major asset purchased by a majority of them. This habit of Indians provides strong support to the demand.

b) Parallel economy

The parallel economy or the ‘black money’ as more commonly known in India is estimated to be anywhere between 40 to 100

percent of the stated GDP. This huge surplus has limited avenues other than property markets to be invested in and ‘cash’

component in real estate deals is a very common practice in India. It also reduces the financing requirement. Other than acting as

an invisible hand supporting the real estate market, the black or unaccounted component also provides a cushion to banks

financing the sector.

This invisible force which gets even more active during slow periods is very peculiar to the Indian economy and a major factor

why the country’s real estate sector cannot be paralleled against any other country.

c) Low Mortgage to GDP ratio

The real estate industry in India is not driven by bank / non bank finance with bulk of the purchases being entirely financed from

savings. The mortgage to GDP ratio in India continues to remain one of the lowest globally with a very low penetration. It is

surprising to know that only about 30% of the total realty deals in the country are financed by financial institutions. This

phenomenon can partially be attributable to higher savings, huge parallel economy, limited availability of credit facilities and to

some extent lack of knowledge.

Interestingly high value properties are rarely financed by financial institutions, with the portion being financed limited to 1/3rd

of the

total value. Rather it is the low cost housing sector that forms bulk of the demand for finance.

Indiabulls Real Estate Ltd.

Initiating Coverage

27 September 22, 2010

The low dependence on the financial sector again differentiates the Indian realty sector form the sector across the world.

d) Difficulty in getting clear title land

This is probably the most important differentiator for the sector. It is very difficult to get a clear title land in India. Further legal

complications involving real estate deals take years to be resolved. Therefore clean properties typically demand a premium up to

50-100% of the property value. This again differentiates the sector from the realty markets world over.

e) High utilization of land in India

Owing to high population density, availability of natural water resources and presence of habitable & fertile land almost

everywhere in country, there is negligible percentage of the total land which has not been put to some use or for revenue

generation. This is in stark contrast to the western countries with low population density. Companies find it difficult to acquire large

track of land to set up their factories along with vendor’s production facilities and residential complexes.

6. The emerging trend

a) Growing interests amongst NRIs

There is a renewed interest amongst Non-Resident Indians specially amongst the older generation who are purchasing properties

and houses in Indian Tier I & Tier II cities for investment, as second homes and also increasingly with a view to spend their

retirement years in India. Encouraged by this trend a number of developers are tapping their pockets and have conducted road-

shows for the premium projects specifically targeted towards this affluent group.

b) Demand for premium housing

Over the last few months, especially in the Tier I & Tier II cities, demand for premium housing and larger properties have been

growing. There have been a slew of launches of premium and luxury residential projects. Further demand for larger residential

properties is also increasing.

c) Macroeconomic policies

The macroeconomic policies will play a very important role in shaping the future of the industry. With 100% FDI being allowed in

single brand retail stores and under ‘cash-n-carry’ formats, a lot of demand for retail space in the Tier I & Tier II cities has been

generated. As and when the FDI norms are relaxed the sector is expected to benefit from a demand spike.

d) Improving connectivity & mass transport

The improving connectivity and public transport is helping the cities to spread and also rationalizing the realty prices by reducing

concentration. It would an increasingly important role in the growth of the sector.

e) Strong emergence of new categories for demand of land

Shopping malls, warehouses, airports, resorts, multiplex theatres, entertainment centres like fun parks, sports facilities,

educational institutes, parking facilities & venues for public gathering for purpose of conferences, workshops, celebrations et al

are all contributing to a positive upswing to this new phase of land sale in India.

Indiabulls Real Estate Ltd.

Initiating Coverage

28 September 22, 2010

Annexure V – About Indiabulls Group

Indiabulls Group has business interest in real estate, infrastructure, financial services, retail, multiplex and power sectors. Currently the

Group operates its real estate business through Indiabulls Real Estate Limited (IBREL), financial services business through Indiabulls

Financial Services Limited (IBFSL) and capital market business through Indiabulls Securities Limited (IBSL).

Indiabulls Group of Companies

• Indiabulls Financial Services Limited (IBFSL)

IBFSL is one of the market leaders in the Indian non banking financial services sector. The company offers a wide range of services

such as consumer finance, housing finance, commercial loans, life insurance, asset management and advisory services. IBFSL along

with MMTC Limited, the largest commodity trading company in India, has set up India’s 4th

Multi- Commodity Exchange.

• Indiabulls Real Estate Limited (IBREL)

IBREL was originally a wholly owned subsidiary of IBFSL. However, effective from 1 May 2006, the company demerged from IBFSL

through a scheme of arrangement under Companies Act. The company focuses on construction and development of properties,

project management, investment advisory and construction services. Also its operations cover all aspects of real estate development

from identification of land, to the planning, execution, construction, marketing of its projects and so on. IBREL partnered with Farallon

Capital Management LLC of USA was the first to bring in Foreign Direct Investment (FDI) into real estate sector.

• Indiabulls Securities Limited (IBSL)

Pan India presence and an extensive client base has made IBSL country’s leading capital market company. The main business of the

company is providing securities and commodities broking and advisory services and related activities like buying, selling, dealing,

transferring and hypothecating shares and debentures. The company acts as a financial consultant or portfolio manager and also

managing the funds of investors.

• Indiabulls Power Limited (IPL)

Indiabulls group made its foray in the power sector through Indiabulls Power Limited. IBREL has a 58.6% stake in IPL and the

company got listed on BSE & NSE during October 2009. IPL is developing 5 coal-fired plants aggregating 6615 MW and 4 hydro

projects aggregating 167 MW.

Indiabulls Real Estate Ltd.

Initiating Coverage

29 September 22, 2010

I deas1s t

Research i s a reg i s tered t rademark o f I deas1s t

I n fo rmat ion Serv ices Pr i va te L im i ted.

Ideas1s t

I n f ormat ion Serv ices Pr iva te L im i ted i s ne i t her autho r i zed no r regu la ted by the F inanc ia l Serv ices Author i t y .

Th is document i s not fo r pub l i c d is t r ibu t ion and has been f urn ished to you so le l y fo r you r in f ormat ion and mus t not b e

rep roduced o r red is t r ibu t ed to any o ther pe rson. Pe rsons in to whose possess ion th is document may come are requ i red to

observe these res t r i c t ions .

Th is mater ia l i s fo r the pe rsona l in f ormat ion o f t he autho r ized rec ip ient , and we a re not so l i c i t ing any ac t ion based upon

i t . Th is repo r t i s not to be cons t rued as an o f fe r to s e l l o r the so l i c i ta t i on o f an o f fer to buy any secu r i t y in any ju r i sd ic t ion

where such an o f fe r o r so l i c i ta t ion would be i l l ega l . I t i s fo r the genera l in f ormat ion o f c l ien ts o f Ideas 1s t

I n f ormat ion

Serv ices Pvt . L td . I t does not cons t i tu te a pe rsona l recommendat ion o r t ake in t o account the par t i c u la r i nves tment

ob jec t i ves , f inanc ia l s i tua t i ons , or needs o f ind i v i dua l c l ien ts .

W e have rev i ewed the repor t , and in s o far as i t i nc ludes cur rent o r h is to r i ca l in fo rmat ion, i t i s be l i eved to be re l iab le

though i t s accu racy or comple teness cannot be guaranteed. Ne i ther I deas 1s t

I n format ion Serv ices P v t . L td . , no r any

person connec ted wi th i t , accepts any l i ab i l i t y a r i s ing f rom the use o f th is document . The rec ip i ents o f th is mater ia l shou ld

re l y on the i r own i nves t iga t ions and tak e the i r own p ro fess iona l adv ic e . Pr ice and va lue o f the inves tments re fer red to in

th is mater ia l may go up o r down. Pas t per fo rmance i s not a gu ide fo r fu tu re pe r formance. Cer t a in t ransac t ions - inc l ud ing

those invo lv i ng f u tures , op t ions and o t he r de r i va t i ves as wel l as non- inves tment grade sec ur i t i es - i nvo lve subs tant ia l r i sk

and a re not su i tab le fo r a l l i nves tors . Repor ts based on techn ica l ana lys is cen ters on s tudy ing cha r ts o f a s tock 's pr i ce

movement and t rad ing vo lume, as opposed to foc us ing on a company 's fundamenta ls and as such, may not match wi th a

repor t on a company 's fundamenta ls .

Op in i ons exp ressed a re ou r cur rent op in i ons as o f the date appear ing on th is mater i a l on ly . W hi le we endeavor to update

on a reasonable bas is the in format ion d iscussed in t h is mater ia l , the re may be regu la to ry , compl iance, o r o the r reasons

that p revent us f rom do ing so. Prospec t i ve inves to rs and o the rs a re caut ioned that any f orward - look ing s ta t ements are no t

pred ic t ions and may be sub jec t to change wi thout not i ce . Our propr ie ta ry t rad ing and inves tment bus inesses may make

inves tment dec is ions that are i ncons is tent w i th the recommendat ions expressed he re in .

W e and our a f f i l i a tes , o f f i cers , d i rec tors , and employees wor l d wide may: (a ) f rom t ime to t ime, have long or shor t

pos i t ions i n , and buy or s e l l the sec ur i t i es the reof , o f company ( ies ) ment i oned here in or (b ) be engaged in any o t he r

t ransac t ion i nvo lv ing such secur i t ies and ea rn b roke rage or o ther c ompensat ion or ac t as a market maker in the f inanc ia l

ins t ruments o f the company ( i es ) d iscussed here in o r ac t as adv is or o r lende r / bor rower to such company ( i es ) or have

o the r pot ent ia l conf l i c t o f i n teres t wi th respec t to any recommendat ion and re l a ted in f ormat ion and op in ions .

The ana lys t fo r th is repo r t cer t i f i es that a l l o f t he v i ews exp ressed in t h is repor t accu ra te ly re f l ec t h is or he r persona l

v iews about the sub jec t company o r companies and i t s or the i r secur i t ies , and no pa r t o f h is o r he r compensat ion was , i s

or w i l l be , d i rec t l y or ind i rec t l y re la ted to spec i f i c recommendat ions o r v iews exp ressed in th is repor t . No par t o f th i s

mater ia l may be dup l i ca ted in any fo rm and/or red is t r ibu ted wi t hout Ideas 1s t

I n format ion Serv ic es ’ p r io r wr i t ten consent .

Th is document i s not fo r pub l i c d is t r ibu t ion and has been f urn ished to you so le l y fo r you r in f ormat ion and mus t not b e

rep roduced o r red is t r ibu t ed to any o ther pe rson. Pe rsons in to whose possess ion th is document may come are requ i red to

observe these res t r i c t ions .

Ideas 1st Information Services Pvt. Ltd.

Corporate Off:

Gr. Floor, 11, Raheja Centre,

Free Press Marg, Nariman Point,

Mumbai – 400 021. India.

Tel: +91 22 6148 5700

Fax: +91 22 6148 5750

Regd. & Adm. Off:

3rd

Floor, 28 Rajabahadur Mansion,

Mumbai Samachar Marg, Fort,

Mumbai – 400 001. India.

Tel: +91 22 6521 4836

Fax: +91 22 2265 6905

E-mail:

Website:

www.ideasfirst.in

Ideas1st

Research is also available on Bloomberg <IFIS> GO

Disclaimer

Contact Details