index to financial statements of prudential insurance

TRANSCRIPT

F-1

INDEX TO FINANCIAL STATEMENTS

OF PRUDENTIAL INSURANCE

Page

Report of Independent Accountants as of December 31, 2003 and 2002 and for the years ended December 31, 2003 and 2002 .....................................................................................................................................F-2

Audited Statutory Financial Statements as of December 31, 2003 and 2002 and for the years ended December 31, 2003 and 2002: Statutory Statements of Admitted Assets, Liabilities and Surplus...................................................................................F-4 Statutory Statements of Operations and Changes in Surplus............................................................................................F-5 Statutory Statements of Cash Flows ......................................................................................................................................F-6 Notes to Statutory Financial Statements ...............................................................................................................................F-7

F-2

Report of Independent Auditors

To the Board of Directors of The Prudential Insurance Company of America

We have audited the accompanying statutory statements of admitted assets, liabilities and capital and surplus of The Prudential Insurance Company of America (the "Company") as of December 31, 2003 and 2002, and the related statutory statements of operations and changes in capital and surplus, and cash flows for the years then ended. These financial statements are the responsibility of the Comp any's management. Our responsibility is to express an opinion on these financial statements based on our audits.

We conducted our audits in accordance with auditing standards generally accepted in the United States of America. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

As described in Note 2 to the financial statements, the Company prepared these financial statements using accounting practices prescribed or permitted by the New Jersey Department of Banking and Insurance (the "Department"), which practices differ from accounting principles generally accepted in the United States of America. The effects on the financial statements of the variances between the statutory basis of accounting and accounting principles generally accepted in the United States of America are material; they are described in Note 2.

In our opinion, because of the effects of the matter discussed in the preceding paragraph, the financial statements referred to above do not present fairly, in conformity with accounting principles generally accepted in the United States of America, the financial position of the Company as of December 31, 2003 and 2002, or the results of its operations or its cash flows for the years then ended.

In our opinion, the financial statements referred to above present fairly, in all material respects, the admitted assets, liabilities and capital and surplus of the Company as of December 31, 2003 and 2002, and the results of its operations and its cash flows for the years then ended, on the basis of accounting described in Note 2.

Our audit was conducted for the purpose of forming an opinion on the basic statutory basis financial statements taken as a whole. The accompanying Annual Statement Schedule 1 – Selected Financial Data, Supplemental Investment Risk Interrogatories and Summary Investment Schedule (collectively, the "Schedules") of the Company as of December 31, 2003 and for the year then ended are presented for purposes of additional analysis and are not a required part of the basic statutory basis financial statements. The effects on the Schedules of the variances between the statutory basis of accounting and accounting principles generally accepted in the United States of America are material; they are described in Note 2. As a consequence, the Schedules do not present fairly, in conformity with accounting principles generally accepted in the United States of America, such information of the Company as of December 31, 2003 and for the year then ended. The Schedules have been subjected to the auditing procedures applied in the audit of the basic statutory basis financial statements and, in our opinion, are fairly stated in all material respects in relation to the basic statutory basis financial statements taken as a whole.

/s/ PricewaterhouseCoopers LLP New York, New York April 16, 2004

F-3

THE PRUDENTIAL INSURANCE COMPANY OF AMERICA (Parent Only)

STATUTORY FINANCIAL STATEMENTS AND ADDITIONAL INFORMATION December 31, 2003 and 2002 and Report of Independent Auditors

THE PRUDENTIAL INSURANCE COMPANY OF AMERICA STATUTORY STATEMENTS OF ADMITTED ASSETS, LIABILITIES AND CAPITAL AND SURPLUS

See Notes to Statutory Financial Statements

F-4

December 31, 2003 2002 (In Millions) ASSETS

Bonds .............................................................................................................................. $ 83,825 $ 83,456 Preferred stocks............................................................................................................. 404 180 Common stocks............................................................................................................. 5,226 4,291 Mortgage loans on real estate..................................................................................... 13,740 13,702 Real estate ...................................................................................................................... 474 585 Policy loans and premium notes................................................................................. 6,359 7,216 Cash and short term investments................................................................................ 9,922 8,583 Other invested assets.................................................................................................... 5,109 5,944

Total cash and invested assets ..................................................................................... 125,059 123,957

Premiums due and deferred......................................................................................... 520 437 Accrued investment income ........................................................................................ 1,344 1,346 Federal income tax recoverable- ................................................................................ 1,166 719 Other assets .................................................................................................................... 567 1,040 Separate account assets ................................................................................................ 66,310 59,113

TOTAL ASSETS ............................................................................................................ $ 194,966 $ 186,612

LIABILITIES AND SURPLUS

Liabilities Policy liabilities and insurance reserves:

Future policy benefits and claims .......................................................................... $ 87,264 $ 86,577 Advanced premiums ................................................................................................. 28 69 Policy dividends........................................................................................................ 2,485 2,450 Policyholders' account balances ............................................................................. 10,175 8,945

Notes payable and other borrowings......................................................................... 684 230 Asset valuation reserve................................................................................................ 2,139 2,131 Federal income tax payable......................................................................................... 497 126 Interest maintenance reserve....................................................................................... 1,220 1,084 Transfers to separate accounts due or accrued......................................................... (143) (141) Cash collateral held for loaned securities ................................................................. 12,798 14,320 Other liabilities .............................................................................................................. 4,290 6,215 Separate account liabilities.......................................................................................... 66,058 58,907

Total liabilities ................................................................................................................. 187,495 180,913

Capital and Surplus

Common capital stock and gross paid in and contributed surplus....................... 4,307 4,276 Surplus notes.................................................................................................................. 691 990 Special surplus fund..................................................................................................... 916 853 Unassigned surplus....................................................................................................... 1,557 (420)

Total capital and surplus .............................................................................................. 7,471 5,699

TOTAL LIABILITIES, CAPITAL AND SURPLUS ........................................... $ 194,966 $ 186,612

THE PRUDENTIAL INSURANCE COMPANY OF AMERICA STATUTORY STATEMENTS OF OPERATIONS AND CHANGES IN SURPLUS

See Notes to Statutory Financial State ments

F-5

Years Ended December 31, 2003 2002 (In Millions) REVENUE Premiums and annuity considerations.................................................................................. $ 13,859 $ 16,218 Net investment income ........................................................................................................... 7,291 7,020 Other income ............................................................................................................................ 724 890 Total Revenue ......................................................................................................................... 21,874 24,128

BENEFITS AND EXPENSES

Death benefits........................................................................................................................... 4,424 4,165 Annuity benefits....................................................................................................................... 4,133 3,268 Disability benefits .................................................................................................................... 622 597 Other benefits ........................................................................................................................... 90 90 Surrenders, benefits and fund withdrawals ......................................................................... 7,906 8,699 Net (decrease) increase in reserves....................................................................................... (83) 3,351 Commissions............................................................................................................................ 253 228 Net transfer from separate accounts ..................................................................................... (1,532) (1,640) Other expenses ......................................................................................................................... 2,024 1,827 Total Benefits and Expenses ............................................................................................... 17,837 20,585

Operating income before dividends and income taxes ...................................................... 4,037 3,543 Dividends to policyholders..................................................................................................... 2,431 2,575

Operating income before income taxes ................................................................................ 1,606 968 Income tax provision............................................................................................................... 273 261

Income from Operation ....................................................................................................... 1,333 707 Net Realized Capital Losses ................................................................................................ (102) (1,197)

NET INCOME (LOSS) ........................................................................................................ $ 1,231 $ (490)

CAPITAL AND SURPLUS

Capital and Surplus, beginning of year ........................................................................... $ 5,699 $ 6,420 Capital paid in ...................................................................................................................... - 2 Surplus paid in ...................................................................................................................... 31 - Release of special surplus fund......................................................................................... - 538

Change in common capital stock and gross paid in and contributed surplus ...... 31 540 Change in surplus notes ....................................................................................................... (299) 1 Change in special surplus fund .......................................................................................... 64 (614) Net Income (Loss) ................................................................................................................... 1,231 (490) Change in net unrealized capital gains (losses).................................................................. 752 (24) Change in non-admitted assets .............................................................................................. 371 (829) Change in asset valuation reserve......................................................................................... (8) 216 Dividends to stockholders ...................................................................................................... - (228) Change in net deferred taxes .................................................................................................. 36 582 Change due to valuation method........................................................................................... (345) 26 Other changes, net ................................................................................................................... (61) 99 Change in unassigned surplus ............................................................................................ 1,976 (648) CAPITAL AND SURPLUS, END OF YEAR ................................................................ $ 7,471 $ 5,699

THE PRUDENTIAL INSURANCE COMPANY OF AMERICA STATUTORY STATEMENTS OF CASH FLOWS

See Notes to Statutory Financial Statements

F-6

Years Ended December 31, 2003 2002 (In Millions) CASH FLOWS FROM OPERATING ACTIVITIES Premiums and annuity considerations.................................................................................. $ 14,011 $ 16,551 Net investment income ........................................................................................................... 7,059 6,630 Other income received ............................................................................................................ 651 873 Separate account transfers...................................................................................................... 1,528 1,692 Benefits and claims paid ......................................................................................................... (17,510) (18,362) Policyholders' dividends paid ................................................................................................ (2,397) (2,645) Federal income taxes ............................................................................................................... 7 (162) Other operating expenses ....................................................................................................... (1,970) (2,059)

Net cash provided by operating activities ....................................................................... 1,379 2,518

CASH FLOWS FROM INVESTING ACTIVITIES

Proceeds from investments sold, matured, or repaid Bonds ..................................................................................................................................... 86,876 59,646 Stocks..................................................................................................................................... 791 2,102 Mortgage loans on real estate............................................................................................ 1,779 1,513 Real estate ............................................................................................................................. 146 32 Miscellaneous proceeds...................................................................................................... 3,620 1,347

Payments for investments acquired ...................................................................................... Bonds ..................................................................................................................................... (90,001) (67,417) Stocks..................................................................................................................................... (1,134) (2,537) Mortgage loans on real estate............................................................................................ (1,803) (2,034) Real estate ............................................................................................................................. (38) (44) Miscellaneous applications................................................................................................ (430) 5,692

Net cash used in investing activities .................................................................................. (194) (1,700)

CASH FLOWS FROM FINANCING ACTIVITIES

Payments on borrowed money .............................................................................................. 454 (701) Net proceeds from surplus paid in ........................................................................................ (300) 3 Dividends paid to stockholder............................................................................................... - (228)

Net cash provided by (used in) financing activities ...................................................... 154 (926)

Net increase (decrease) in cash and short-term investment ....................................... 1,339 (108) Cash and short-term investments, beginning of year......................................................... 8,583 8,691

CASH AND SHORT-TERM INVESTMENTS, END OF YEAR ............................ $ 9,922 $ 8,583

THE PRUDENTIAL INSURANCE COMPANY OF AMERICA

NOTES TO STATUTORY FINANCIAL STATEMENTS DECEMBER 31, 2003 and 2002

F-7

1. BUSINESS

The Prudential Insurance Company of America (the "Company" or "Prudential Insurance") is a wholly owned subsidiary of Prudential Holdings, LLC ("Prudential Holdings"), which is a wholly owned subsidiary of Prudential Financial, Inc. ("Prudential Financial"). The principal products and services of the Company include individual life insurance, annuities, group insurance and retirement services.

2. SIGNIFICANT ACCOUNTING POLICIES AND PRINCIPLES

The Company, domiciled in the state of New Jersey, prepares its statutory financial statements in accordance with accounting practices prescribed or permitted by the New Jersey Department of Banking and Insurance (the "Department"). Prescribed statutory accounting practices ("SAP") include publications of the National Association of Insurance Commissioners ("NAIC"), state laws, regulations and general administrative rules. Permitted statutory accounting practices encompass all accounting practices not so prescribed. NAIC SAP reporting differs from accounting principles generally accepted in the United States ("GAAP"). NAIC SAP is designed to address the concerns of regulators. GAAP is designed to meet the varying needs of the different users of financial statements. NAIC SAP is considered to be more conservative than GAAP in certain respects and attempts to determine at the financial statement date an insurer's ability to pay claims in the future. GAAP, on the other hand, stresses measurement of emerging earnings of a business from period to period, by matching revenue to expense.

A. Basis of presentation

The Company prepares its statutory financial statements in conformity with accounting practices prescribed or permitted by the State of New Jersey ("NJ SAP"). Effective January 1, 2001, the State of New Jersey required that insurance companies domiciled in the State of New Jersey prepare their statutory basis financial statements in accordance with the NAIC "Accounting Practices and Procedures Manual" ("NAIC SAP" or the "Manual"), subject to any deviations prescribed or permitted by the Department. The Company's statutory accounting policies differ from the Manual due to deviations prescribed and permitted by the Department.

These financial statements were prepared on an unconsolidated basis. NAIC SAP and NJ SAP differs from GAAP primarily as follows:

• the Commissioner's Reserve Valuation Method ("CRVM") is used for the majority of individual insurance reserves under SAP, whereas for individual insurance, policyholder liabilities are generally established using the net level premium method under GAAP. Policy assumptions used in the estimation of policyholder liabilities are generally prescribed under SAP, but are based upon actual company experience under GAAP;

• the Commissioner's Annuity Reserve Valuation Method ("CARVM") is used for the majority of individual deferred annuity reserves under SAP, whereas for individual deferred annuities, policyholder liabilities are generally equal to the full fund value under GAAP;

• policy acquisition costs are expensed when incurred under SAP rather than being deferred and charged against earnings over the periods covered by the related policies as under GAAP;

• surplus notes are recorded as a component of surplus under SAP rather than being recorded as a liability under GAAP;

• certain "non-admitted assets", such as fixed assets, prepaid pensions, and other prepaid assets, must be excluded under SAP through a charge against surplus;

THE PRUDENTIAL INSURANCE COMPANY OF AMERICA

NOTES TO STATUTORY FINANCIAL STATEMENTS DECEMBER 31, 2003 and 2002

F-8

• investments in the common stock of the Company's wholly owned subsidiaries are accounted for using the equity method under SAP rather than consolidated as under GAAP;

• bonds are carried at amortized cost under SAP, with the exception of certain below investment grade bonds which are carried at the lower of amortized cost or market value. Under GAAP, bonds are categorized as "held to maturity", "available for sale" or "trading". Bonds categorized as "held to maturity" are carried at amortized cost, and bonds categorized as "available for sale" or "trading" are carried at fair value;

• certain balances, in addition to those mentioned above, are classified differently in the financial statements under SAP and GAAP;

• reinsurance reserve credits taken by ceding entities as a result of reinsurance contracts are netted against the ceding entity's policy and claim reserves and unpaid claims. Under GAAP, reinsurance recoverables are reported as assets;

• the Asset Valuation Reserve ("AVR") and Interest Maintenance Reserve ("IMR") are required for life insurance companies under SAP.

The following is a summary of accounting practices permitted by the Department and reflected in the Company's statutory financial statements:

• On February 19, 1993, the Company received written approval from the Department to issue Fixed Rate Surplus Notes ("the Notes"). Interest and principal payments on the Notes are pre-approved by the Department. NAIC practices provide for Insurance Commissioner pre-approval of every interest payment, and principal, at the time the payment is made. The Notes matured in April of 2003; however, the Company made interest payments during the year.

• The Company sold synthetic guaranteed investment contracts ("GICs") containing minimum investment related guarantees on qualified pension plan assets. The assets are owned by the trustees of such plan, who invest the assets under the terms of investment guidelines agreed to with the Company. The investment related guarantees may include a minimum rate of return on the underlying assets and/or a guarantee of liquidity to meet plan cash flow requirements. The Company, with the approval of the Department, reports in Exhibit 7 of its Annual Statement the net reserve for these contracts. The net reserve is calculated as the excess, if any, of the present value of liability cash flows over the market value of the assets. NAIC guidance allows for an interest rate of up to 5% to be used for the calculation of the present value of liability cash flows. The practice permitted by the Department requires a 4.5% interest rate to be used.

• On November 20, 2001, the Company received approval from the Department to report as admitted assets on the Company's financial statements notes issued by the Company's ultimate parent, Prudential Financial. The request for a permitted practice was made as a result of the liability that was established on the books of the Company as a result of policyholder credits provided in connection with the demutualization. Pursuant to Statement of Statutory Accounting Principles ("SSAP") No. 25, Accounting for and Disclosures about Transactions with Affiliates and Other Related Parties, loans or advances made by a reporting entity from its parent or principal owner shall be admitted if approval for the transaction has been obtained from the domiciliary commissioner and the loan or advance is determined to be collectible based on the parent or principal owner's independent payment ability.

• On December 19, 2001, the Company received approval from the Department to report overnight loans from Prudential Financial as admitted assets of the Company. In order to facilitate this process, the intercompany cash management arrangement, called the Enterprise Liquidity Account ("ELA"), was

THE PRUDENTIAL INSURANCE COMPANY OF AMERICA

NOTES TO STATUTORY FINANCIAL STATEMENTS DECEMBER 31, 2003 and 2002

F-9

created to enable the Company, as well as other insurance and non-insurance entities that are affiliated with Prudential Financial, to advance and receive funds overnight to/from Prudential Financial. If an intercompany advance from Prudential Financial (an ELA Investment) is outstanding at quarter end or at year-end, the advance will be classified as an intercompany cash equivalent in "Cash and short-term investments". However, as of December 31, 2003 and 2002, there was no activity in this account for the Company.

• In conjunction with the Company's reinsurance of the Closed Block (See Note 2.H for further information regarding the Closed Block formation) in 2003, the Company received approval on January 29, 2004 from the Department to report the initial Modified Coinsurance ("MODCO") reserves ceded to the reinsurer as "Other income" in the revenue section of the Summary of Operations. Although not specifically outlined in statutory guidance, industry practice is to report this amount in "Premium and annuity considerations" in the Summary of Operations.

• The Company records leasehold improvements as admitted assets. NJ SAP allows insurance companies domiciled in New Jersey to admit leasehold improvements as admitted assets. Prescribed statutory accounting practices, per the Manual, require non-admittance of leasehold improvements.

A reconciliation of the Company's net income and capital and surplus at December 31, between NAIC SAP and NJ SAP is shown below:

2003 2002 (In Millions) Net Income, per the Manual ..................................................... $ 1,231 $ (490) State Prescribed Practices (Income)........................................... - - State Permitted Practices (Income)............................................ - -

Net (Loss) Income, NJ SAP ....................................................... $ 1,231 $ (490)

Statutory Surplus, per the Manual ......................................... $ 7,472 $ 5,297 State Prescribed Practices:

Admit leasehold improvements............................................... 81 102 State Permitted Practices:

Report notes in Surplus............................................................. - 300

Statutory Surplus, NJ SAP ....................................................... $ 7,391 $ 5,699

The effects of the difference on surplus and net income between accounting practices prescribed or permitted by the Department and GAAP are as follows:

• GAAP net income is decreased by $55 million and increased by $490 million, to $1,176 million and $0 million in 2003 and 2002, respectively.

• GAAP equity is increased by $10,495 million and $10,926 million, to $17,886 million and $16,625 million in 2003 and 2002, respectively.

B. Use of estimates

The preparation of financial statements in conformity with NJ SAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenue and expenses during the period. Actual results could differ from those estimates.

THE PRUDENTIAL INSURANCE COMPANY OF AMERICA

NOTES TO STATUTORY FINANCIAL STATEMENTS DECEMBER 31, 2003 and 2002

F-10

C. Investments

Bonds, which consist of long-term bonds, are stated primarily at amortized cost in accordance with the valuation prescribed by the Department and the NAIC. For other than temporary impairments, the cost basis of the bond is written down to fair market value as a new cost basis and the amount of the write down is accounted for as a realized loss.

Preferred stocks include unaffiliated preferred stocks and investments in subsidiaries. Unaffiliated preferred stocks rated by the NAIC are classified into six categories ranging from highest quality preferred stocks to those in or near default. Preferred stocks rated in the top three categories are generally valued at amortized cost while preferred stock rated in the lower three categories are valued at lower of amortized cost or market. Investments in subsidiaries are accounted for using an equity method as defined in SSAP No. 46, Investments in Subsidiary, Controlled and Affiliated Entities ("SSAP No. 46"). Investments in non-insurance subsidiaries that have no significant ongoing operations other than to hold assets that are primarily for the direct or indirect benefit or use of the reporting entity or its affiliates are recorded based on the underlying equity of the respective entity's financial statements adjusted to a statutory basis of accounting and the resultant proportionate share of the subsidiary's adjusted surplus, adjusted for unamortized goodwill as provided for in SSAP No. 68, Business Combinations and Goodwill ("SSAP No. 68").

Common Stocks includes unaffiliated common stocks and investments in subsidiaries. Unaffiliated common stocks are carried at fair value. Investments in subsidiaries are accounted for using an equity method as defined in SSAP No. 46. Investments in insurance subsidiaries are recorded based on the underlying statutory equity of the respective entity's financial statements, and adjusted for unamortized goodwill when required by SSAP No. 68. Investments in non-insurance subsidiaries that have no significant ongoing operations other than to hold assets that are primarily for the direct or indirect benefit or use of the Company or its affiliates are recorded based on the underlying equity of the respective entity adjusted to a statutory basis of accounting and the resultant proportionate share of the subsidiary's adjusted surplus, adjusted for unamortized goodwill as provided for in SSAP No. 68. Investments in non-insurance subsidiaries that have significant ongoing operations beyond the holding of assets that are primarily for the direct or indirect benefit or use of the Company or its affiliates are recorded based on the audited GAAP equity of the investee. The subsidiaries' change in net assets, excluding capital contributions and distributions, is included in "Change in net unrealized gains (losses)". Dividends are recognized in net investment income when declared. The subsidiaries are engaged principally in the business of life insurance and annuities.

Mortgage loans on real estate are stated primarily at unpaid principal balances, net of unamortized discounts and impairments. Impaired loans are identified by management as loans in which a probability exists that all amounts due according to the contractual terms of the loan agreement will not be collected.

Interest received on impaired loans, including loans that were previously modified in a troubled debt restructuring, is generally either applied against the principal or reported as revenue, according to management's judgment as to the collectibility of principal. Management discontinues accruing interest on impaired loans after the loans are 90 days delinquent as to principal or interest, or earlier when management has substantial doubts about collectibility. When this interest is deemed uncollectible, it is reversed against interest income on loans for the current period. Generally, a loan is restored to accrual status only after all delinquent interest and principal are brought current and, in the case of loans where interest has been interrupted for a substantial period, a regular payment performance has been established. Interest income on non-performing loans is generally recognized on a cash basis.

Real estate includes properties occupied by the Company, properties held for production of income and properties held for sale. Properties occupied by the Company and properties held for the production of

THE PRUDENTIAL INSURANCE COMPANY OF AMERICA

NOTES TO STATUTORY FINANCIAL STATEMENTS DECEMBER 31, 2003 and 2002

F-11

income are carried at cost less accumulated straight-line depreciation, encumbrances and permanent impairments in value. Properties held for sale are valued at lower of depreciated cost or fair value less encumbrances and disposition costs.

Policy loans and premium notes are stated at unpaid principal balances.

Cash includes cash on deposit and cash equivalents. Cash equivalents are short-term, highly liquid investments, with original maturities of three months or less, that are both readily convertible to known amounts of cash and so near their maturity that they represent insignificant risk of changes in value because of changes in interest rates.

Short-term investments include money market funds and highly liquid debt instruments purchased with a remaining maturity of twelve months or less, excluding those investments classified as cash equivalents. They are stated at amortized cost, which approximates fair value.

Other invested assets include primarily the Company's investment in joint ventures, limited liability companies and other forms of partnerships. These investments, except for limited partnerships with a minor ownership interest, are accounted for using an equity method as defined in SSAP No. 46. Limited partnerships in which the entity has a minor ownership interest are valued based on the underlying audited GAAP equity of the investee. The cost method is used for all other assets.

Derivatives used by the Company include swaps, futures, forwards and option contracts and may be exchange-traded or contracted in the over-the-counter market. Derivatives are recognized on the Statements of Admitted Assets, Liabilities and Capital and Surplus at their estimated fair value in "Other invested assets" or "Other liabilities". Effective January 1, 2003 the company adapted SSAP 86, "Accounting for Derivative Instruments and Hedging Activities", and applied it to all derivative instruments held as of that date. The Company typically uses "to be announced" ("TBA") securities in reverse dollar repurchase agreements. In 2003, these securities were accounted for as derivatives and reported in "Other invested assets" with the change in value reported as "Change in net unrealized capital gains (losses)". Net realized capital gains (losses) are recorded upon termination of the agreements. In 2002, these securities were carried at amortized cost and included in "Bonds".

Securities lending is a program whereby the Company loans securities to third parties, primarily major brokerage firms. Company and NAIC policies require a minimum of 102% and 105% of the fair value of the domestic and foreign loaned securities, respectively, to be separately maintained as collateral for the loans. Cash collateral received of $4,824 million is not restricted and is invested in "Bonds", "Short-term investments" and "Cash"; the offsetting collateral liability of $4,824 million is included in "Cash collateral held for loaned securities". Non-cash collateral of $366 million is not reflected in the Statements of Assets, Liabilities and Capital and Surplus.

Reverse repurchase agreements are agreements between a seller and a buyer, whereby the seller of securities sells and simultaneously agrees to repurchase the same or substantially the same securities from the buyer at an agreed upon price and, usually, at a stated date. These securities are carried at amortized cost and included in "Bonds". Reverse dollar repurchase agreements involve debt instruments that are pay-through securities collateralized with GNMA, FNMA and FHLMC and similar securities.

Loan-backed and structured securities holdings are recalculated utilizing a retrospective method with the exception of interest only bonds. Each acquisition lot is reviewed to recalculate the effective yield. The recalculated effective yield is used to derive a book value as if the new yield is applied at the time of acquisition. Outstanding principal factors from the time of acquisition to adjustment date were used to calculate the prepayment history for all applicable securities. Conditional prepayment rates, computed with life to date factor histories and weighted average maturities, are used to affect the calculation of projected

THE PRUDENTIAL INSURANCE COMPANY OF AMERICA

NOTES TO STATUTORY FINANCIAL STATEMENTS DECEMBER 31, 2003 and 2002

F-12

payments for pass through, interest only and principal only security types. Interest only bond adjustments are developed on a prospective basis with adjustments made for permanent impairments, if needed.

Net realized capital gains/(losses) are computed using the specific identification method. Costs of investments are adjusted for impairments considered other than temporary. Interest rate related gains and losses are transferred to the IMR and amortized into net investment income over the expected remaining life of the investments sold.

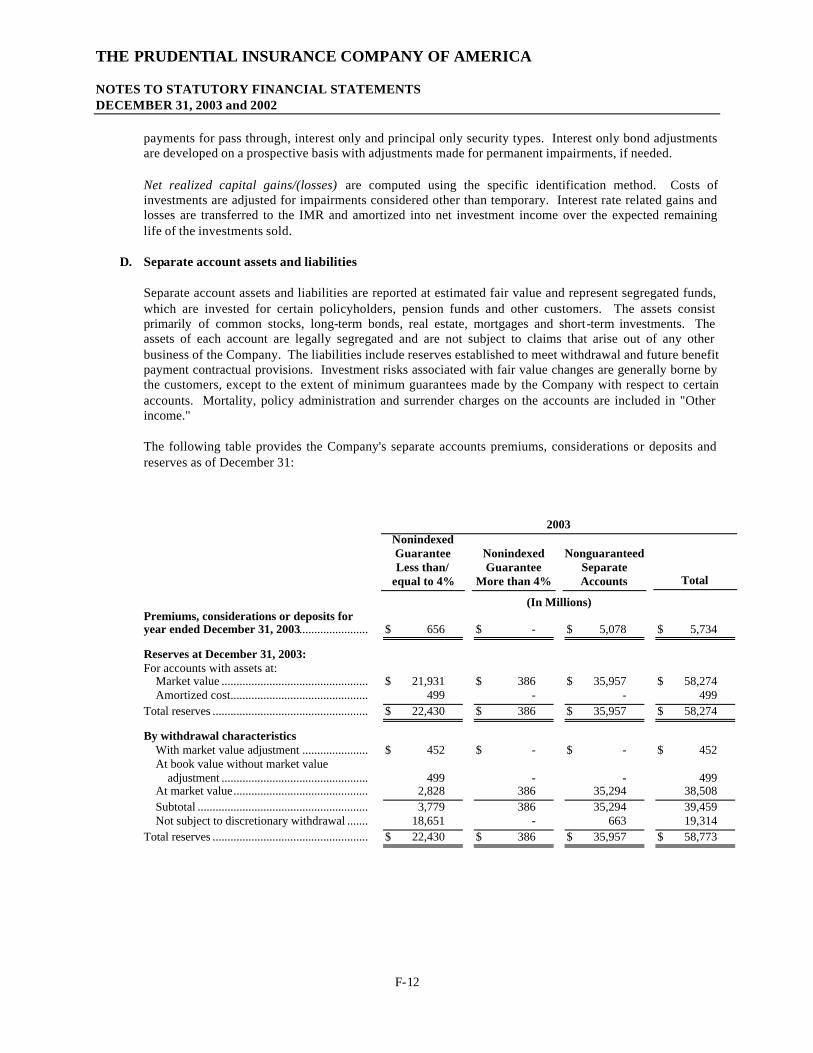

D. Separate account assets and liabilities

Separate account assets and liabilities are reported at estimated fair value and represent segregated funds, which are invested for certain policyholders, pension funds and other customers. The assets consist primarily of common stocks, long-term bonds, real estate, mortgages and short-term investments. The assets of each account are legally segregated and are not subject to claims that arise out of any other business of the Company. The liabilities include reserves established to meet withdrawal and future benefit payment contractual provisions. Investment risks associated with fair value changes are generally borne by the customers, except to the extent of minimum guarantees made by the Company with respect to certain accounts. Mortality, policy administration and surrender charges on the accounts are included in "Other income."

The following table provides the Company's separate accounts premiums, considerations or deposits and reserves as of December 31:

2003 Nonindexed

Guarantee Less than/

equal to 4%

Nonindexed Guarantee

More than 4%

Nonguaranteed Separate Accounts Total

(In Millions) Premiums, considerations or deposits for year ended December 31, 2003....................... $ 656 $ - $ 5,078 $ 5,734

Reserves at December 31, 2003: For accounts with assets at:

Market value ................................................. $ 21,931 $ 386 $ 35,957 $ 58,274 Amortized cost.............................................. 499 - - 499

Total reserves .................................................... $ 22,430 $ 386 $ 35,957 $ 58,274

By withdrawal characteristics With market value adjustment ...................... $ 452 $ - $ - $ 452 At book value without market value

adjustment ................................................. 499 - - 499 At market value............................................. 2,828 386 35,294 38,508 Subtotal ......................................................... 3,779 386 35,294 39,459 Not subject to discretionary withdrawal ....... 18,651 - 663 19,314

Total reserves .................................................... $ 22,430 $ 386 $ 35,957 $ 58,773

THE PRUDENTIAL INSURANCE COMPANY OF AMERICA

NOTES TO STATUTORY FINANCIAL STATEMENTS DECEMBER 31, 2003 and 2002

F-13

2002 Nonindexed

Guarantee Less than/

equal to 4%

Nonindexed Guarantee

More than 4%

Nonguaranteed Separate Accounts Total

(In Millions) Premiums, considerations or deposits for year ended December 31, 2002....................... $ 533 $ - $ 6,728 $ 7,261

Reserves at December 31, 2002: For accounts with assets at:

Market value ................................................. $ 20,800 $ 375 $ 31,620 $ 52,795 Amortized cost.............................................. 501 - - 501

Total reserves .................................................... $ 21,301 $ 375 $ 31,620 $ 53,296

By withdrawal characteristics With market value adjustment ...................... $ 451 $ - $ - $ 451 At book value without market value

adjustment ................................................. 501 - - 501 At market value............................................. 1,185 375 31,021 32,581 Subtotal ......................................................... 2,137 375 31,021 33,533 Not subject to discretionary withdrawal ....... 19,164 - 599 19,763

Total reserves .................................................... $ 21,301 $ 375 $ 31,620 $ 53,296

2002 Nonindexed

Guarantee Less than/

equal to 4%

Nonindexed Guarantee

More than 4%

Nonguaranteed Separate Accounts Total

(In Millions)

Transfers to separate accounts.......................... $ 533 $ - $ 6,652 $ 7,185 Transfers from separate accounts...................... 495 4 8,326 8,825 Net transfers to (from) separate accounts ......... $ 38 $ (4) $ (1,674) $ (1,640)

E. Policyholders' dividends

The amount of dividends to be paid to policyholders is determined annually by the Company's Board of Directors. The aggregate amount of policyholders ' dividends is based on statutory results and past experience of the Company, including investment income, net realized investment gains or losses over a number of years, mortality experience and other factors. Dividends declared by the Board of Directors, which have not been paid, are included in "Policy dividends" in the Statutory Statements of Admitted Assets, Liabilities, and Capital and Surplus.

F. Insurance revenue and expense recognition

Life premiums are recognized as income over the premium paying period of the related policies. Annuity considerations are recognized as revenue when received. Health premiums are earned ratably over the terms of the related insurance and reinsurance contracts or policies. Expenses incurred in connection with

THE PRUDENTIAL INSURANCE COMPANY OF AMERICA

NOTES TO STATUTORY FINANCIAL STATEMENTS DECEMBER 31, 2003 and 2002

F-14

acquiring new insurance business, including acquisition costs such as sales commissions, are charged to operations as incurred.

G. Income taxes

The Company and its domestic subsidiaries file a consolidated federal income tax return with Prudential Financial Inc. The Internal Revenue Code (the "Code") taxes the Company on operating income after dividends to policyholders.

Deferred income taxes are recognized in accordance with SSAP No. 10, based upon enacted rates, when assets and liabilities have different values for financial statement and tax reporting purposes. Income from sources outside the United States is taxed under applicable foreign statutes.

Pursuant to a tax allocation arrangement, total federal income tax expense is determined on a separate company basis . Members with losses record current tax benefits to the extent such losses are recognized in the consolidated federal and state and local provision.

H. Closed Block

On December 18, 2001 (the "date of demutualization") the Company converted from a mutual life insurance company to a stock life insurance company and became a direct, wholly owned subsidiary of Prudential Holdings, which became a direct wholly owned subsidiary of Prudential Financial. The demutualization was completed in accordance with the Company's Plan of Reorganization, which was approved by the Commissioner of Banking and Insurance of the State of New Jersey in October 2001.

On the date of demutualization, the Company established a closed block for certain individual life insurance policies and annuities issued by the Company in the United States and a separate closed block for participating individual life insurance policies issued by the Company's Canadian branch (collectively the "closed block"). The policies included in the closed block are specified individual life insurance policies and individual annuity contracts that were in force on the effective date of the Plan of Reorganization and on which the Company is currently paying or expects to pay experience-based policy dividends. Assets have been allocated to the closed block in an amount that has been determined to produce cash flows which, together with revenues from policies included in the closed block, are reasonably expected to be sufficient to support obligations and liabilities relating to these policies, including provision for payment of benefits, certain expenses, and taxes and to provide for continuation of the policyholder dividend scales in effect in 2000, if experience underlying such scale continues and for appropriate adjustments in such scales if the experience changes. The closed block assets, the cash flows generated by the closed block assets and the anticipated revenues form the policies in the closed block will benefit only the policyholders in the closed block. To the extent that, over time, cash flows from the assets allocated to the closed block and claims and other experience related to the closed block are, in the aggregate, more or less favorable than what was assumed when the closed block was established, total dividends paid to closed block policyholders in the future may be greater than or less than the total dividends that would have been paid to these policyholders if the policyholder dividend scales in effect in 2000 had been continued. Any cash flows in excess of amounts assumed will be available for distribution over time to closed block policyholders and will not be available to stockholders. If the closed block has insufficient funds to make guaranteed policy benefit payments, such payments will be made from assets outside of the closed block. The closed block will continue in effect as long as any policy in the closed block remains in-force.

I. Reclassification

Certain amounts in the prior year have been reclassified to conform to the current year presentation.

THE PRUDENTIAL INSURANCE COMPANY OF AMERICA

NOTES TO STATUTORY FINANCIAL STATEMENTS DECEMBER 31, 2003 and 2002

F-15

3. INVESTED ASSETS

A. Bonds and stocks

The Company invests in both investment grade and non-investment grade public and private bonds. The Securities Valuation Office of the NAIC rates the bonds held by insurers for regulatory purposes and classifies investments into six categories ranging from highest quality bonds to those in or near default. The lowest three NAIC categories represent primarily high-yield securities and are defined by the NAIC as including any security with a public agency rating equivalent to B+ or B1 or less. Securities in these lowest three categories approximated 4.4% and 4.5% of the Company's bonds at December 31, 2003 and 2002, respectively.

The following tables provide additional information relating to bonds and unaffiliated preferred stocks as of December 31:

2003

Carrying Amount

Gross Unrealized

Gains

Gross Unrealized

Losses

Estimated Fair

Value (In Millions) Bonds U.S. government ................................................................... $ 7,139 $ 461 $ 17 $ 7,583 All other governments........................................................... 1,139 167 1 1,305 States, territories and possessions ........................................ 616 110 - 720 Political subdivisions of states, territories and

possessions........................................................................ 16 1 - 17 Special revenue and special assessment obligations and

all non guaranteed obligations of agencies ....................... 3,430 252 10 3,672 Public utilities ....................................................................... 6,284 629 23 6,889 Industrial and miscellaneous (unaffiliated)........................... 63,241 4,426 351 67,317 Credit tenant loans (unaffiliated) .......................................... 34 7 - 41 Parent, subsidiaries and affiliates .......................................... 1,926 81 1 2,006 Total bonds............................................................................ $ 83,825 $ 6,134 $ 403 $ 89,556

Unaffiliated Preferred Stocks Redeemable ........................................................................... 74 5 - 79 Non-redeemable .................................................................... 8 1 - 9 Total unaffiliated preferred stocks........................................ $ 82 $ 6 $ - $ 88

THE PRUDENTIAL INSURANCE COMPANY OF AMERICA

NOTES TO STATUTORY FINANCIAL STATEMENTS DECEMBER 31, 2003 and 2002

F-16

2002

Carrying Amount

Gross Unrealized

Gains

Gross Unrealized

Losses

Estimated Fair

Value (In Millions) Bonds U.S. government .................................................................... $ 8,620 $ 739 $ 0 $ 9,359 All other governments............................................................ 902 120 25 997 States, territories and possessions ......................................... 716 134 8 842 Political subdivisions of states, territories and

possessions......................................................................... 24 0 2 22 Special revenue and special assessment obligations and

all non guaranteed obligations of agencies ........................ 6,535 327 3 6,859 Public utilities ........................................................................ 6,076 521 34 6,563 Industrial and miscellaneous (unaffiliated)............................ 59,857 3,951 655 63,153 Credit tenant loans (unaffiliated) ........................................... 37 7 0 44 Parent, subsidiaries and affiliates ........................................... 689 52 1 740 Total bonds............................................................................. $ 83,456 $ 5,851 $ 728 $ 88,579

Unaffiliated Preferred Stocks Redeemable ............................................................................ 130 4 1 133 Non-redeemable ..................................................................... 50 10 0 60 Total unaffiliated preferred stocks......................................... $ 180 $ 14 $ 1 $ 193

The carrying value and estimated fair value of bonds at December 31, 2003, categorized by contractual maturity, are shown below. Actual maturities may differ from contractual maturities because borrowers may prepay obligations with or without call or prepayment penalties.

Carrying Amount

Estimated Fair Value

(In Millions) Due in one year or less................................................... $ 5,429 $ 5,485 Due after one year through five years ......................... 23,840 25,078 Due after five years through ten years......................... 24,203 26,126 Due after ten years .......................................................... $ 28,038 $ 30,452

$ 81,510 $ 87,141

Mortgage-backed securities .......................................... 2,315 2,415

Total .................................................................................. $ 83,825 $ 89,556

Proceeds from the sale and maturity of bonds during 2003 and 2002 were $99,200 million and $65,125 million, respectively. Gross gains of $759 million and $630 million and gross losses of $285 million and $863 million were realized on such sales during 2003 and 2002, respectively.

Write-downs for impairments, which were deemed to be other than temporary, for bonds were $298 million and $569 million, for preferred stocks were $4 million and $47 million, and for unaffiliated common stocks were $62 million and $179 million for the years 2003 and 2002, respectively.

Additional information relating to the amortized cost and fair value of bond, unaffiliated preferred stock, and common stock lots held for which the estimated fair value had temporarily declined and remained below cost as of December 31, 2003 are shown below. The following table reflects the difference of cost and fair value for such lots and differs from gross unrealized losses reported in the previous table, which reflects the unrealized losses of aggregate lots of the identical bonds, unaffiliated preferred stocks, and common stocks, due to the varying costs associated with each lot purchased:

THE PRUDENTIAL INSURANCE COMPANY OF AMERICA

NOTES TO STATUTORY FINANCIAL STATEMENTS DECEMBER 31, 2003 and 2002

F-17

Declines For Less Than Twelve Months Declines For Greater Than Twelve Months Cost Fair Value Difference Cost Fair Value Difference

Bonds ...................................... $ 7,823 $ 7,608 $ (215) $ 1,416 $ 1,348 $ (68) Unaffiliated Preferred and Common Stocks ...................... 143 128 (15) 50 41 (9)

Total ........................................ $ 7,966 $ 7,736 $ (230) $ 1,466 $ 1,389 $ (77)

B. Mortgage Loans

The maximum and minimum lending rates for mortgage loans during 2003 were: Agricultural loans 18.0% and 3.8%; Commercial loans 7.2% and 3.2%. There were no purchase money mortgages loaned during the year. During 2002 the maximum and minimum lending rates were: Agricultural loans 7.9% and 4.5%; Commercial loans 8.5% and 2.8%

During 2003, the Company did not reduce interest rates of outstanding mortgage loans.

The maximum percentage of any one loan to the value of security at the time of the loan, exclusive of insured or guaranteed or purchase money mortgages was: 80% except loans made pursuant to title 17B, Chapter 20, Section 1h, Revised Statutes of New Jersey. The mortgage loans are geographically dispersed or distributed throughout the United States and Canada with the largest concentration in California (26.9%) and New York (9.1%).

Mortgages with interest more than 180 days past due totaled $28 million and interest past due on these mortgages totaled $2 million. Taxes, assessments, and other amounts advanced by the Company on account of mortgage loans outstanding are included in the mortgage loan total.

Impaired mortgage loans and the related allowance for losses at December 31 are as follows:

2003 2002 (In Millions)

Current year impaired loans with a related allowance for credit losses ........ $ 91 $ 110

Related allowance for credit losses...................................................................... $ 15 $ 14

Impaired mortgage loans without an allowance for credit losses................... $ 85 $ 140

Average recorded investment in impaired loans............................................. $ 213 $ 317

Interest income recognized during the period the loans were impaired ...... $ 13 $ 22 Amount of interest income recognized on a cash basis during the period

the loans were impaired ................................................................................... $ 13 $ 22 Activity in the allowance for credit losses for all mortgage loans is summa rized as follows:

2003 2002 (In Millions)

Balance, January 1 .................................................................................................. $ 14 $ 62 Additions charged / (Reductions credited) to operations................................. 1 (48)

Balance, December 31 ........................................................................................... $ 15 $ 14

C. Debt restructuring

There were no restructured mortgage loans at December 31, 2003 or December 31, 2002.

THE PRUDENTIAL INSURANCE COMPANY OF AMERICA

NOTES TO STATUTORY FINANCIAL STATEMENTS DECEMBER 31, 2003 and 2002

F-18

D. Loan-backed securities

The Company has elected to use the book value as of January 1, 1994 as the cost for applying the retrospective adjustment method to securities purchased prior to that date. Prepayment assumptions for single class and multi-class mortgage-backed/asset-backed securities were obtained from broker dealer survey values or internal estimates.

E. Repurchase agreements

The Company’s policies require a minimum of 100% of the fair value of securities purchased under repurchase agreements to be maintained as collateral. Securities subject to reverse repurchase agreements and dollar reverse repurchase agreements as of December 31:

2003

Book Value Fair Value Maturities

Weighted Average Interest Rate

(In Millions) Reverse repurchase agreements..........................$ 7,451 $ 7,846 28 Years 3.76% Dollar reverse repurchase agreements................................12 12 26 Years 5.53%

2002

Book Value Fair Value Maturities

Weighted Average Interest Rate

(In Millions) Reverse repurchase agreements..........................$ 7,763 $ 8,405 14 Years 4.85% Dollar reverse repurchase agreements................................2,003 2,010 27 Years 6.04%

F. Real estate

Impairment losses of $12 million and $14 million at December 31, 2003 and 2002 respectively, were recognized on real estate and are included in "Net realized capital losses". The impairments were the result of unfavorable market conditions and fair value was determined via internal appraisals.

G. Restricted assets and special deposits

Assets in the amount of $328 million and $334 million at December 31, 2003 and 2002, respectively, were on deposit with government authorities or trustees as required by law. Assets valued at $71 million and $119 million at December 31, 2003 and 2002, respectively, were maintained as compensating balances or pledged as collateral for bank loans and other financing agreements. Restricted stocks amounted to $8 million in 2003 and $14 million in 2002.

Restricted stocks by asset class at December 31 are as follows:

2003 2002 (In Millions) Common Stocks ................................................................$ 3 $ 7 Preferred Stocks ................................................................ 5 7

Total ................................................................................................$ 8 $ 14

THE PRUDENTIAL INSURANCE COMPANY OF AMERICA

NOTES TO STATUTORY FINANCIAL STATEMENTS DECEMBER 31, 2003 and 2002

F-19

H. Accrued investment income

Due and accrued income was excluded from investment income on the following bases:

Mortgage loans - Interest overdue is accrued up to a maximum of three months. If this interest subsequently becomes greater than 180 days overdue it is non-admitted and therefore excluded from investment income. The total amount of non-admitted interest on mortgage loans at December 31, 2003 and 2002, was $1.7 million and $0.8 million, respectively.

Real estate - Rent that is in arrears for more than three months or the collection of rent that is uncertain is non-admitted and excluded from investment income. Non-admitted due and accrued rental income on real estate at December 31, 2003 and 2002, was $0.02 million and $0.01 million, respectively.

Bonds - Income is not accrued on bonds in or near default and is excluded from net investment income. Income not accrued on bonds at December 31, 2003 and 2002, were $80 million and $50 million, respectively.

I. Wash sales

In the course of the Company’s asset management, securities are sold and reacquired within 30 days of the sale date. The details by NAIC designation 3 or below of securities sold during 2003 and 2002, respectively, and reacquired within 30 days of the sale date are:

2003

Number of

Transactions

Book Value of

Securities Sold

Cost of Securities

Repurchased (In Millions) Gain/(Loss)

(In Millions) Bonds NAIC 3................................................................ 26 $ 6 $ 6 $ - NAIC 4................................................................ 8 4 4 - Total bonds................................................................ 34 $ 10 $ 10 $ -

2002

Number of

Transactions

Book Value of

Securities Sold

Cost of Securities

Repurchased (In Millions) Gain/(Loss)

(In Millions) Bonds NAIC 3................................................................ 53 $ 17 $ 17 $ - NAIC 4................................................................ 33 8 8 - Total bonds................................................................ 86 $ 25 $ 25 $ -

There were no wash sales for preferred stocks in 2003 and 2002.

THE PRUDENTIAL INSURANCE COMPANY OF AMERICA

NOTES TO STATUTORY FINANCIAL STATEMENTS DECEMBER 31, 2003 and 2002

F-20

4. RESERVES FOR LIFE CONTRACTS AND DEPOSIT-TYPE CONTRACTS

A. Life and annuity contracts’ reserves

Claims reserves for life insurance and annuities include estimates of benefits on reported claims and those that are incurred but not reported.

Individual life insurance future policy benefit reserves are calculated using various methods, interest rates and mortality tables, which are prescribed by the Department and produce reserves that in the aggregate meet the requirements of state laws and regulations. Approximately 46% and 48% at December 31, 2003 and 2002, respectively, of individual life insurance reserves are determined using the net level premium method, or by using the greater of the net level premium method reserve or the policy cash value. About 54% and 52% of individual life insurance reserves are calculated according to the Commissioner’s Reserve Valuation Method (“CRVM”), or methods, which compare CRVM to policy cash values at December 31, 2003 and 2002, respectively.

For group life insurance, about 50% and 31% of the reserves at December 31, 2003 and 2002, respectively, are associated with extended death benefits. These reserves are primarily calculated using modified 1970 Group Life Disability Valuation Table at various interest rates. The remainder are unearned premium reserves (calculated using the 1960 Commissioner’s Standard Group Table), reserves for group life fund accumulations and other miscellaneous reserves.

Reserves for other supplementary benefits relative to the Company’s life insurance contracts are calculated using methods, interest rates, and tables appropriate for the benefit provided.

Reserves for individual deferred annuity contracts are determined based on the Commissioner’s Annuity Reserve Valuation Method. These account for 61% and 66% of the individual annuity reserves at December 31, 2003 and 2002, respectively. The remaining reserves are equal to the present value of future payments using prescribed annuity mortality tables and interest rates.

Reserves for annuities purchased under group contracts are equal to the present value of future payments, using prescribed mortality tables and interest rates. Reserves for other deposit funds reflect the contract deposit account or experience accumulation for the contract.

The reserve for guaranteed interest contracts, deposit funds and other liabilities without life contingencies equal either the present value of future payments discounted at the appropriate interest rate or the fund value, if greater.

The reserve for waiver of the deduction of deferred fractional premiums upon death of the insured, and for return of a portion of final premium for periods beyond the date of death is at least as great as that computed using the minimum standards of mortality, interest and valuation method, taking into account the aforementioned treatment of premiums. The Company does not promise surrender values in excess of the legally computed reserves.

Reserves on policies issued at or subsequently subject to a premium for extra mortality or otherwise issued on lives classed as substandard for the plan of contract issued or on special class lives, including paid-up insurance, are reported in “Future policy benefits and claims” in the Statutory Statements of Assets, Liabilities and Capital and Surplus according to mortality and interest bases applicable to the respective years of issue. In addition, an extra mortality reserve is held for ordinary life insurance policies classed as group conversions, contractual conversions from Ordinary term insurance, or otherwise substandard, equal to the excess, if any, over a basic reserve, of a substandard reserve based on mortality rates appropriately increased over the standard class mortality rates. For all other such policies, the extra mortality reserve is

THE PRUDENTIAL INSURANCE COMPANY OF AMERICA

NOTES TO STATUTORY FINANCIAL STATEMENTS DECEMBER 31, 2003 and 2002

F-21

one-half the appropriate net additional premium. Weekly premium policies issued at ages higher than true ages are valued according to the higher ages as are Ordinary second-to-die policies.

The reserve items above have been determined using accepted actuarial methods applied on a basis consistent with the appropriate Standards of Practice as promulgated by the Actuarial Standards Board and with accounting practices prescribed or permitted by the Department. These actuarial methods have been applied on a basis consistent with the prior year’s methods except for changes in bases of valuation as of December 31, 2003, resulting in a net $345 million increase in reserves. These changes in bases of valuation were approved by the Department. Additionally, as a result of these basis changes, premium deficiency reserves decreased by approximately $258 million, and additional reserves due to asset adequacy testing decreased by approximately $206 million, as of December 31, 2003.

As of December 31, 2003 and 2002, the Company had $22.4 billion and $18.7 billion, respectively, of insurance in force for which gross premiums for the life insurance benefits are less than the net premiums according to the standard of valuation required by the Department.

The Tabular Interest has been determined by formula as prescribed by the NAIC except for individual unmatured annuities, group universal life insurance and group annuity fund accumulation reserves, for which tabular interest has been determined from the basic data. The Tabular Less Actual Reserve Released has been determined by formula as prescribed by the NAIC. The Tabular Cost has been determined by formula as described in the instructions prescribed by the NAIC except for certain variable and universal life insurance policies for which tabular cost has been determined from the basic data for the calculation of policy reserves.

The following table is an analysis of annuity actuarial reserves and deposit liabilities by withdrawal characteristics as of December 31:

2003 2002

Amount Percentage

of Total Amount Percentage

of Total (In Millions) (In Millions) Subject to discretionary withdrawal-with adjustment

With market value adjustment......................................................$ 10,988 $ 10,418 At book value less surrender charges of 5% or more........................ 1,429 13% 1,419 13% At market value ......................................................................... 19,743 2% 16,481 2% Total with adjustment or at market value................................ 32,160 23% 28,317 20% At book value without adjustment (minimal or no charge or

adjustment)........................................................................... 16,284 19% 15,316 19% Not subject to discretionary withdrawal provision ................................ 37,415 43% 37,303 46% Total gross annuity reserves ................................................................ 85,859 100% 80,936 100%

Reinsurance Ceded............................................................................. - - Total net annuity reserves................................................................$ 85,859 $ 80,936

Reconciliation of total annuity actuarial reserves and deposit liabilities

Life and Accident & Health Annual Statement $ 41,712 $ 39,676 Separate Accounts Annual Statement............................................ 44,147 41,259

Total annuity actuarial reserves and deposit liabilities..............................$ 85,859 $ 80,936

B. Accident and health

Accident and health reserves represent the estimated value of the future payments, adjusted for contingencies and interest. The remaining reserves for active life reserves and unearned premiums are

THE PRUDENTIAL INSURANCE COMPANY OF AMERICA

NOTES TO STATUTORY FINANCIAL STATEMENTS DECEMBER 31, 2003 and 2002

F-22

valued using the preliminary term method, gross premium valuation method, or a pro rata portion of gross premiums. Reserves are also held for amounts not yet due on hospital benefits and other coverages.

The Company anticipates investment income as a factor in the premium deficiency calculation, in accordance with SSAP No. 54, Individual and Group Accident and Health Contracts.

Claim reserves for Group Long Term Disability are discounted at interest rates ranging from 3.5% to 6.75%, depending on the year in which the disability occurred. Group Long Term Disability reserves are discounted using the 2000 Company modification of the 1987 GLTD Table.

Reserves for Single Premium policies are discounted using 1958 CSO at an interest rate of 4.5% and 1971 IAM at an interest rate of 5.5%.

Active Life reserves for Long Term Care policies are discounted at interest rates ranging from 4.5% to 5.5% depending on the effective date of coverage of each participant.

Claim reserves for Long Term Care policies are discounted using 1983 GAM mortality at interest rates ranging from 4.5% to 5.5%, depending on the year of benefit incurral.

Claim reserves for Individual Disability are discounted using the 1964 Commissioner Disability Table at interest rates ranging from 3.5% to 6%, depending on year of coverage.

Claim reserves for other Individual Guaranteed Renewable Accident and Health policies are discounted at interest rates ranging from 3.5% to 6% from the assumed date of payment to the year incurred. The applicable interest rate depends on the year of coverage, except for Major Medical Expense and Extended Medical Expense, which use 3.5%.

Claim reserves for Individual Cancelable Accident and Health policies are discounted at 3.5% from the assumed date of payment to the year incurred.

The following table provides a reconciliation of the activity in the liability for unpaid claims and claim adjustment expenses for accident and health business (included in “Future policy benefits and claims”) at December 31:

2003 2002 (In Millions) Balance at January 1......................................................... $ 50 $ 161

Less reinsurance recoverables ................................................................11 119 Net balance at January 1 ................................................................ 39 42 Incurred related to:

Current year ................................................................................................465 468 Prior years ................................................................................................4 (5)

Total incurred ................................................................................................469 463 Paid related to:

Current year ................................................................................................143 150 Prior years ................................................................................................333 316

Total paid................................................................................................ 476 466 Net balance at December 31 ................................................................ 32 39

Plus reinsurance recoverables................................................................3 11

Balance at December 31................................................................$ 35 $ 50

THE PRUDENTIAL INSURANCE COMPANY OF AMERICA

NOTES TO STATUTORY FINANCIAL STATEMENTS DECEMBER 31, 2003 and 2002

F-23

The reinsurance recoverable balances include amounts attributable to the Company’s healthcare business sold to Aetna of $1 million and $9 million at December 31, 2003 and 2002, respectively.

The provision for claims and claim adjustment expenses decreased by $2 million in 2003 and 2002, primarily due to changes in claim costs trends in health care and a declining inforce.

5. REINSURANCE

The Company participates in reinsurance in order to provide greater diversification of business, provide additional capacity for future growth, limit the maximum net loss potential arising from large risks, and generally manage certain risks associated with its products. Life reinsurance is accomplished through various plans of reinsurance, primarily yearly renewable term and coinsurance.

Most of the Company’s ceded reinsurance is undertaken as indemnity reinsurance, which does not discharge the Company as the primary insurer. Ceded balances would represent a liability to the Company in the event the reinsurers were unable to meet their obligations to the Company under the terms of the reinsurance agreements. The Company periodically reviews the financial condition of its reinsurers and amounts recoverable there from, recording an allowance when necessary for uncollectible reinsurance.

There are no non-affiliated reinsurers that were owned in excess of 10% or controlled, either directly or indirectly, by the Company or by any representative, officer, trustee, or director of the Company.

6. NOTES PAYABLE AND OTHER BORROWINGS

Notes payable and other borrowings consisted of the following as of December 31:

2003

Debt Name Date Issued Kind of

Borrowing Original

Face Amount Carrying

Value Rate of Interest

(In Millions) Structured Principal Unit Redeemable Securities................................07/30/98 Debenture $ 393 $ 172 6.375% Prudential Funding, LLC (a wholly owned subsidiary)................................07/21/03 - 12/31/03 Cash $ 504 $ 504 0.94% -1.02% 2002

Debt Name Date Issued Kind of

Borrowing Original

Face Amount Carrying

Value Rate of Interest

(In Millions) Structured Principal Unit Redeemable Securities................................07/30/98 Debenture $ 393 $ 222 6.375%

Accrued interest expense of $8 million in 2003 and $7 million in 2002 is included in “Notes payable and other borrowings” in the Statutory Statements of Admitted Assets, Liabilities and Capital and Surplus. Interest paid for notes payable and other borrowings was $45 million and $74 million for the year ended December 31, 2003 and 2002, respectively.

Scheduled principal repayments on debt as of December 31, 2003 are as follows: $558 million in 2004, $57 million in 2005, $61 million in 2006, $0 in 2007 and 2008.

THE PRUDENTIAL INSURANCE COMPANY OF AMERICA

NOTES TO STATUTORY FINANCIAL STATEMENTS DECEMBER 31, 2003 and 2002

F-24

7. EMPLOYEE BENEFIT PLANS

A. Pension plans and other postretirement benefits

The Company has funded non-contributory defined benefit pension plans which cover substantially all of its employees. The Company also has several non-funded non-contributory defined benefit plans covering certain executives. For some employees, benefits are based on final average earnings and length of service, while other employees are based on a notional account balance that takes into consideration age, service and salary during their careers. The Company’s funding policy is to contribute annually an amount necessary to satisfy the Code contribution guidelines applicable to such plans. During 2003 and 2002, benefit payments under non-funded non-contributory defined benefit plans totaled $30 million and $11 million, respectively.