indepth review and analysis gbenga badejo

TRANSCRIPT

Leading and Managing Strategic Change for Effective Service Delivery

November, 2020.

Gbenga Badejo

Leading Public financial management (PFM) Reforms in Nigeria: In-depth review and analysis

© Periscope Consulting Ltd. All rights reserved. Printed in Nigeria.

Outline

• Course Objectives

• PFM Reforms in Nigeria

• GIFMIS

• Transparency

• Treasury Single Account

• Conclusion

© Periscope Consulting Ltd. All rights reserved. Printed in Nigeria.

Objectives

§ What kinds of reforms have Nigeria pursued in the past decade?

§ Where have reform ideas come from?

§ What lessons can be learnt from past approaches?

§ What are the current challenges and how well do existing reform approaches addressing these?

© Periscope Consulting Ltd. All rights reserved. Printed in Nigeria.

PFMREFORMSINNIGERIA

© Periscope Consulting Ltd. All rights reserved. Printed in Nigeria.

Risk-based audit (Enhancing value for

money)

Adoption of Global Reporting

Standards (IPSAS)

Risk-based audit (Enhancing value for

money)

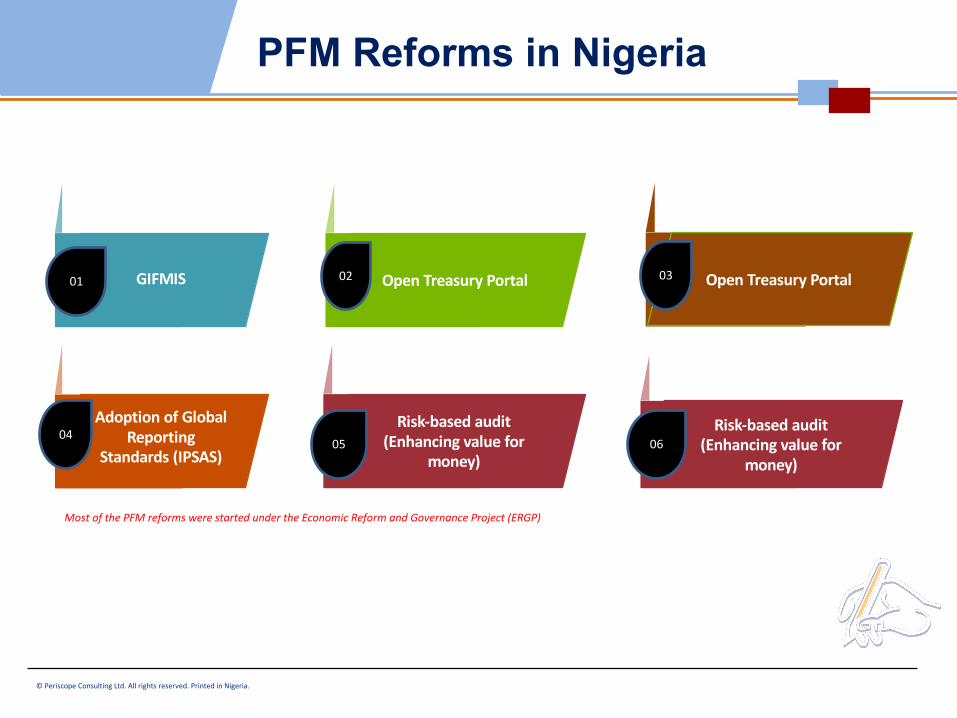

GIFMIS01

PFM Reforms in Nigeria

Open Treasury Portal 02

0405 06

Open Treasury Portal 03

Most of the PFM reforms were started under the Economic Reform and Governance Project (ERGP)

PFM Reforms in Nigeria

© Periscope Consulting Ltd. All rights reserved. Printed in Nigeria.

PFM Reforms in Nigeria

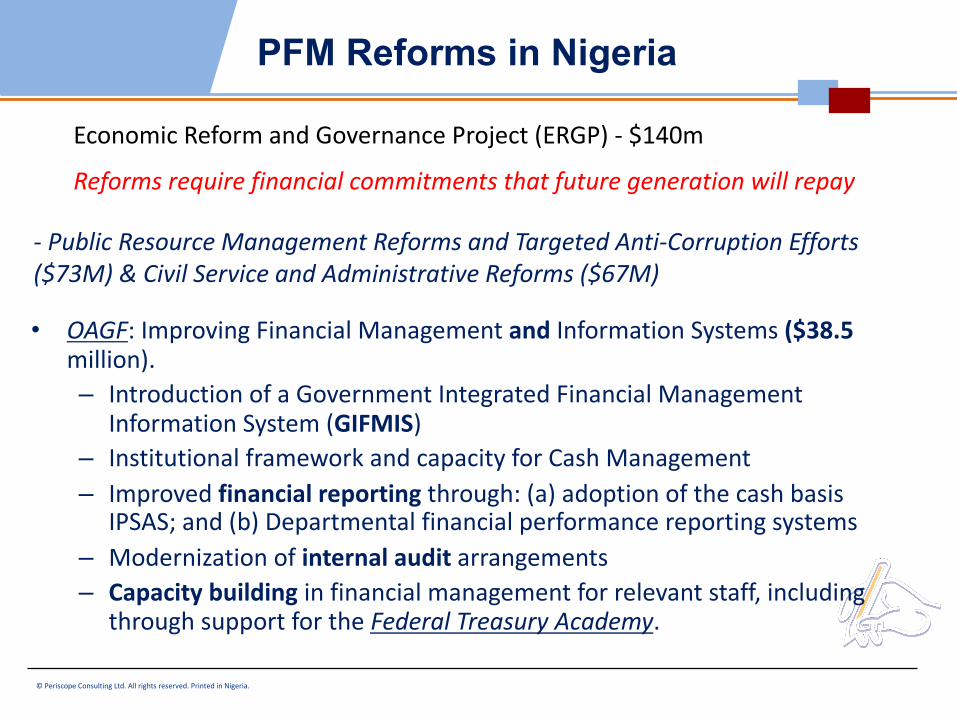

Reforms require financial commitments that future generation will repay

- Public Resource Management Reforms and Targeted Anti-Corruption Efforts ($73M) & Civil Service and Administrative Reforms ($67M)

• OAGF: Improving Financial Management and Information Systems ($38.5 million).– Introduction of a Government Integrated Financial Management

Information System (GIFMIS)– Institutional framework and capacity for Cash Management– Improved financial reporting through: (a) adoption of the cash basis

IPSAS; and (b) Departmental financial performance reporting systems– Modernization of internal audit arrangements – Capacity building in financial management for relevant staff, including

through support for the Federal Treasury Academy.

Economic Reform and Governance Project (ERGP) - $140m

© Periscope Consulting Ltd. All rights reserved. Printed in Nigeria. 7

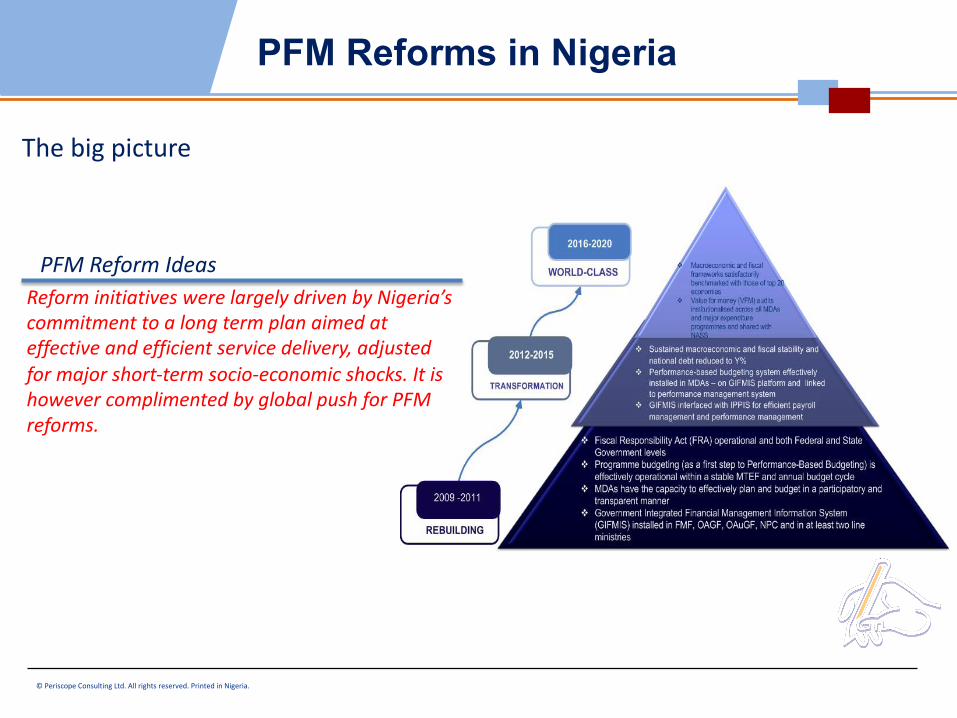

PFM Reform IdeasReform initiatives were largely driven by Nigeria’s commitment to a long term plan aimed at effective and efficient service delivery, adjusted for major short-term socio-economic shocks. It is however complimented by global push for PFM reforms.

The big picture

PFM Reforms in Nigeria

© Periscope Consulting Ltd. All rights reserved. Printed in Nigeria.

GIFMIS

© Periscope Consulting Ltd. All rights reserved. Printed in Nigeria. 9

Solution Channels and Integration Components

Budget Preparation

RDBMS Content ManagementApplication Server Integration Platform

NortalBusiness SolutionsPlatform

Master Data

Management

Reporting Services and

Analytics

SecurityAuthenticationAuthorisation

Workflowand

Business Rules

Budget Execution Accounting and Reporting Integration Adapters

Budget limits planning

Budget Draft Preparation

AppropriationsMacro - fiscal scenarios

Budget Projections

Investments Projects

Contracts

Commitments

Payments and Revenue

Cash Management Assets

Management

Inventory

Management

Other Systems

Revenue Administrators

IPPIS

Central Bank (CBN)General Ledger

GIFMISThe Promissory Note: Scope Vs. Quick-wins?

© Periscope Consulting Ltd. All rights reserved. Printed in Nigeria. 10

01 02 04

Strong governance structure and

institutional support engendered success

Incremental Approach –Subsystems (Modules)

implementation

03

Bureaucracy in implementing

Turnkey contract

System Security, Quality Assurance and handling over

GIFMIS

© Periscope Consulting Ltd. All rights reserved. Printed in Nigeria.

TransparencyPortal

© Periscope Consulting Ltd. All rights reserved. Printed in Nigeria.

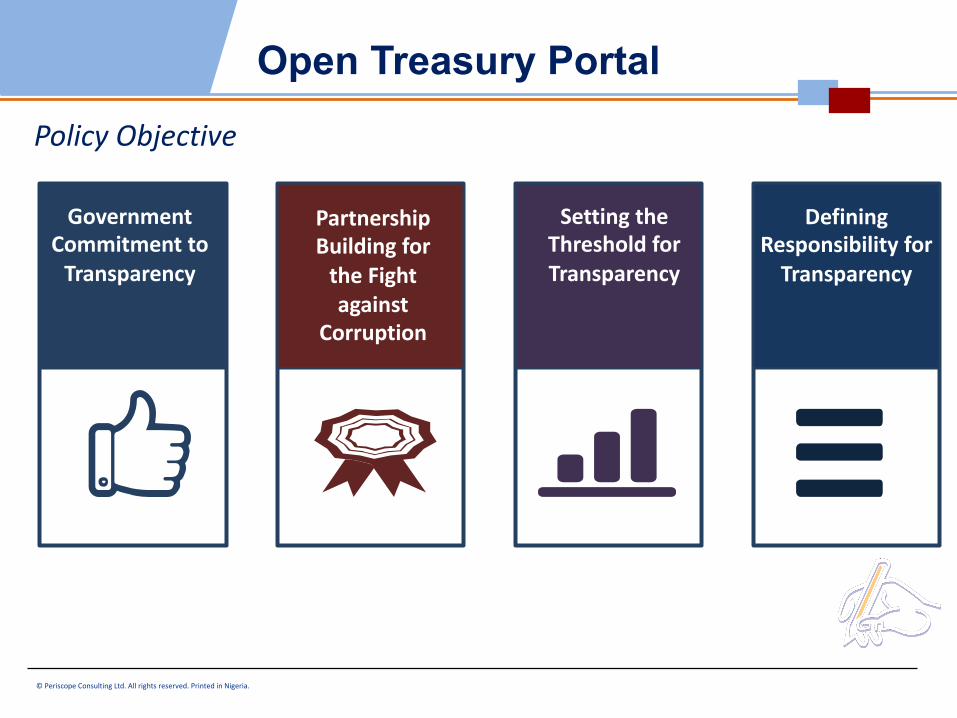

Policy Objective

Government Commitment to

Transparency

Partnership Building for the

Fight against Corruption

Setting the Threshold for Transparency

Defining Responsibility for

Transparency

Partnership Building for

the Fight against

Corruption

Open Treasury Portal

© Periscope Consulting Ltd. All rights reserved. Printed in Nigeria.

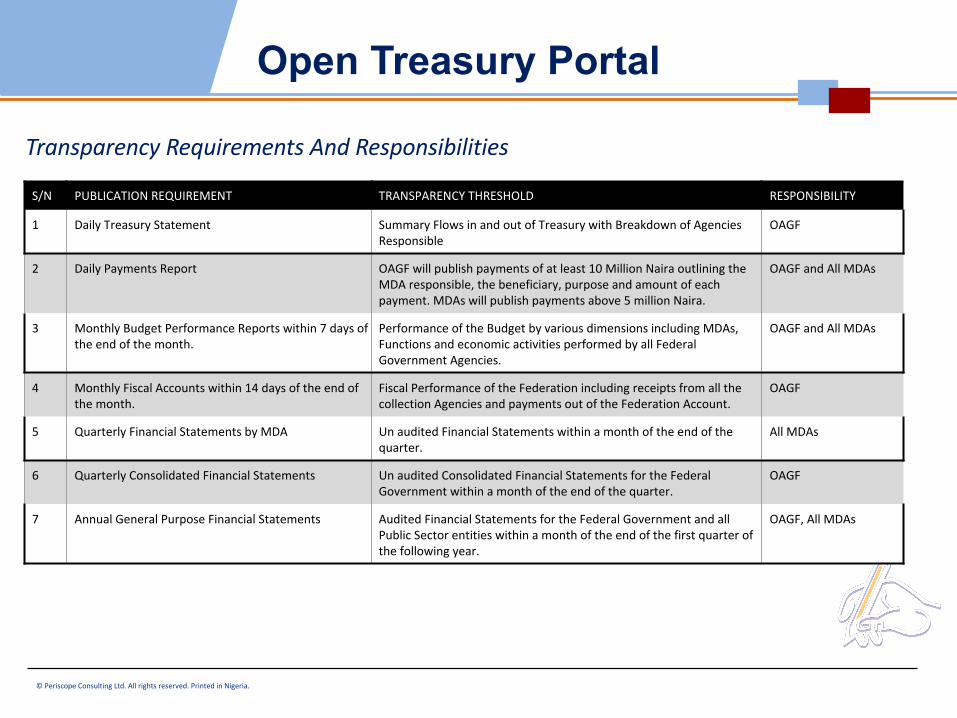

S/N PUBLICATION REQUIREMENT TRANSPARENCY THRESHOLD RESPONSIBILITY

1 Daily Treasury Statement Summary Flows in and out of Treasury with Breakdown of Agencies Responsible

OAGF

2 Daily Payments Report OAGF will publish payments of at least 10 Million Naira outlining the MDA responsible, the beneficiary, purpose and amount of each payment. MDAs will publish payments above 5 million Naira.

OAGF and All MDAs

3 Monthly Budget Performance Reports within 7 days of the end of the month.

Performance of the Budget by various dimensions including MDAs, Functions and economic activities performed by all Federal Government Agencies.

OAGF and All MDAs

4 Monthly Fiscal Accounts within 14 days of the end of the month.

Fiscal Performance of the Federation including receipts from all the collection Agencies and payments out of the Federation Account.

OAGF

5 Quarterly Financial Statements by MDA Un audited Financial Statements within a month of the end of the quarter.

All MDAs

6 Quarterly Consolidated Financial Statements Un audited Consolidated Financial Statements for the Federal Government within a month of the end of the quarter.

OAGF

7 Annual General Purpose Financial Statements Audited Financial Statements for the Federal Government and all Public Sector entities within a month of the end of the first quarter of the following year.

OAGF, All MDAs

Transparency Requirements And Responsibilities

Open Treasury Portal

© Periscope Consulting Ltd. All rights reserved. Printed in Nigeria.

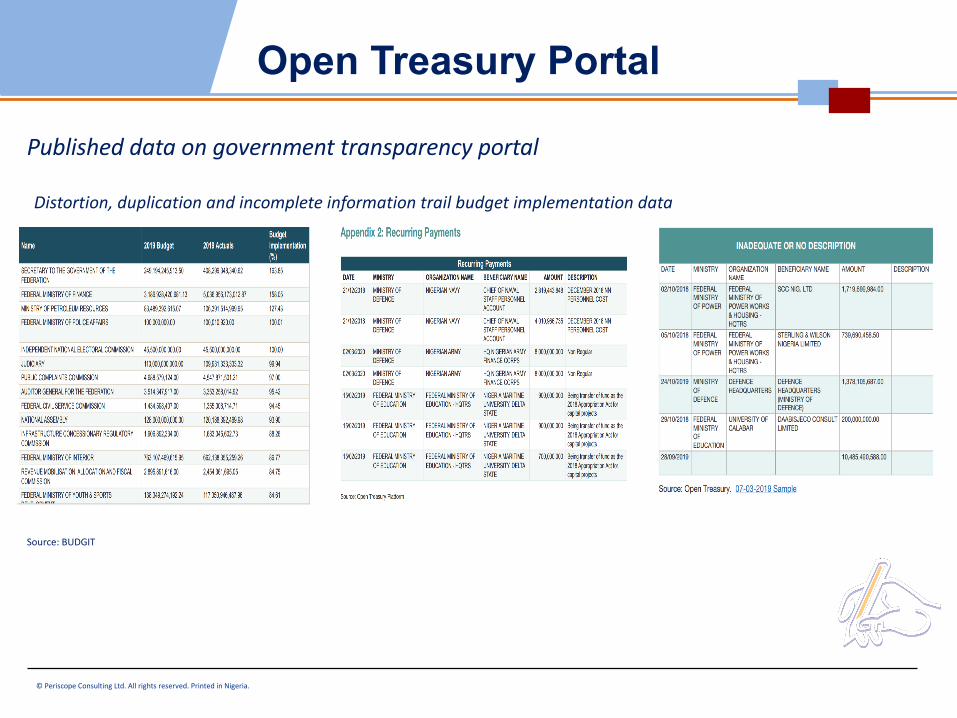

Source: BUDGIT

Distortion, duplication and incomplete information trail budget implementation data

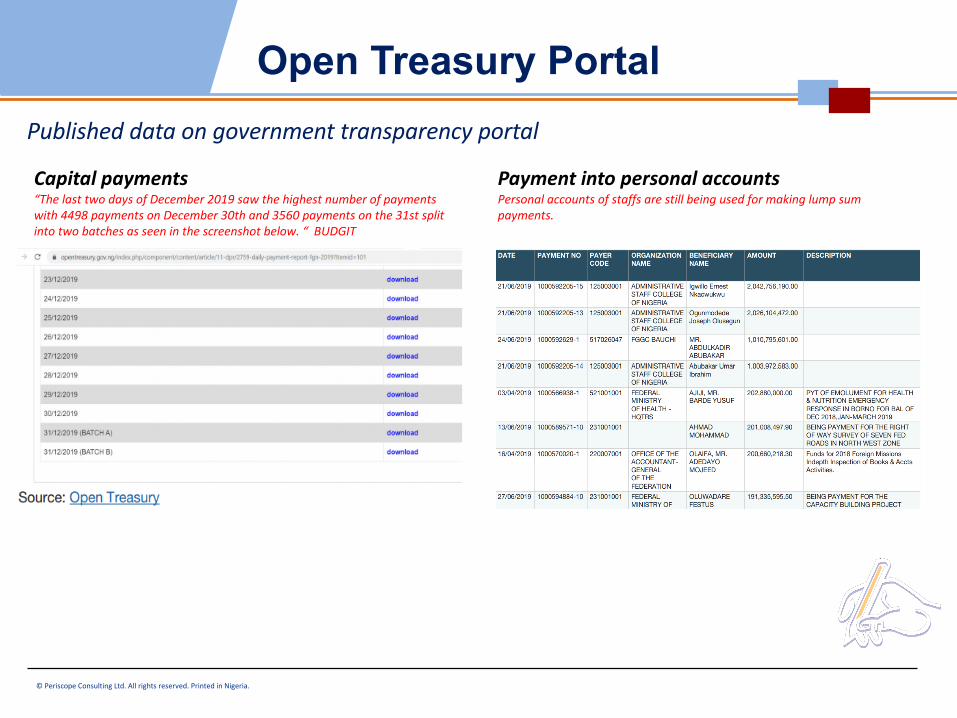

Published data on government transparency portal

Open Treasury Portal

© Periscope Consulting Ltd. All rights reserved. Printed in Nigeria.

Capital payments “The last two days of December 2019 saw the highest number of payments with 4498 payments on December 30th and 3560 payments on the 31st split into two batches as seen in the screenshot below. “ BUDGIT

Payment into personal accountsPersonal accounts of staffs are still being used for making lump sum payments.

Published data on government transparency portal

Open Treasury Portal

© Periscope Consulting Ltd. All rights reserved. Printed in Nigeria.

1. Why are the budget figures different from those in the Appropriation Act?2. What is the explanation for making several payments on the same day to the same beneficiary? 3. Why are large payments being made to personal accounts as opposed to company accounts?4. How can the public easily view all payments made to a particular beneficiary?5. Why are there capital payments at the end of the year when project implementation is then impossible?6. What are these payments amounts which do not indicate ministry name, organization and beneficiary name?

Suggested way forward:§ Improve user experience on the platform§ Increase the transparency of the data available on the platform§ Engage citizens and stakeholders beyond the platform§ Publish the report of the quality assurance and compliance committee

Open portal opens you to the world………………..encourage best practice

citizens are asking

Open Treasury Portal

© Periscope Consulting Ltd. All rights reserved. Printed in Nigeria.

TreasurySingleAccount

© Periscope Consulting Ltd. All rights reserved. Printed in Nigeria.

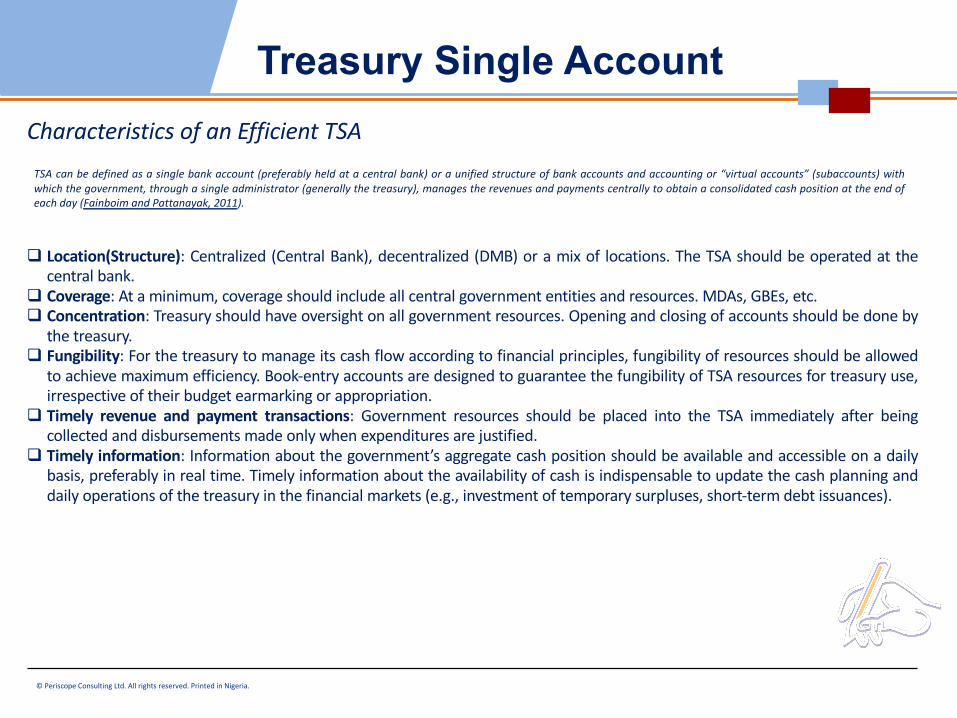

TSA can be defined as a single bank account (preferably held at a central bank) or a unified structure of bank accounts and accounting or “virtual accounts” (subaccounts) withwhich the government, through a single administrator (generally the treasury), manages the revenues and payments centrally to obtain a consolidated cash position at the end ofeach day (Fainboim and Pattanayak, 2011).

q Location(Structure): Centralized (Central Bank), decentralized (DMB) or a mix of locations. The TSA should be operated at thecentral bank.

q Coverage: At a minimum, coverage should include all central government entities and resources. MDAs, GBEs, etc.q Concentration: Treasury should have oversight on all government resources. Opening and closing of accounts should be done by

the treasury.q Fungibility: For the treasury to manage its cash flow according to financial principles, fungibility of resources should be allowed

to achieve maximum efficiency. Book-entry accounts are designed to guarantee the fungibility of TSA resources for treasury use,irrespective of their budget earmarking or appropriation.

q Timely revenue and payment transactions: Government resources should be placed into the TSA immediately after beingcollected and disbursements made only when expenditures are justified.

q Timely information: Information about the government’s aggregate cash position should be available and accessible on a dailybasis, preferably in real time. Timely information about the availability of cash is indispensable to update the cash planning anddaily operations of the treasury in the financial markets (e.g., investment of temporary surpluses, short-term debt issuances).

Characteristics of an Efficient TSA

Treasury Single Account

© Periscope Consulting Ltd. All rights reserved. Printed in Nigeria.

Centralised Decentralised§ Counterparty (credit) risk is minimal. § Risk of bank failure or liquidity crisis

§ No public commercial bank is placed in an

advantageous situation with respect to the rest of

the commercial banks.

§ Favouritism in selecting the commercial banks

§ Risk of the central bank failing to remunerate the

TSA cash balance or setting lower-than-market

interest rates (lower than those offered by

commercial banks)

§ Higher interest rate if cash is actively managed.

However, regulation may prevent placement of funds

by MDAs.

§ The effort and the costs of controlling liquidity in

this case become the responsibility of the treasury

or the Ministry of Finance.

§ The cost and the effort to control liquidity will fall to

the central bank forcing the central bank to undertake

significant open-market operations to control bank

liquidity

§ Facilitates coordination between fiscal and

monetary policy.

§ Excess liquidity created from government cashflow

may disrupt price stability

§ Tightens monetary policy § Frees up liquidity for the banks leading to speculative

activities rather than real sector development

Characteristics of an Efficient TSA

There is a strong call for relocating liquidity back to the Money Deposit banks

Treasury Single Account

© Periscope Consulting Ltd. All rights reserved. Printed in Nigeria.

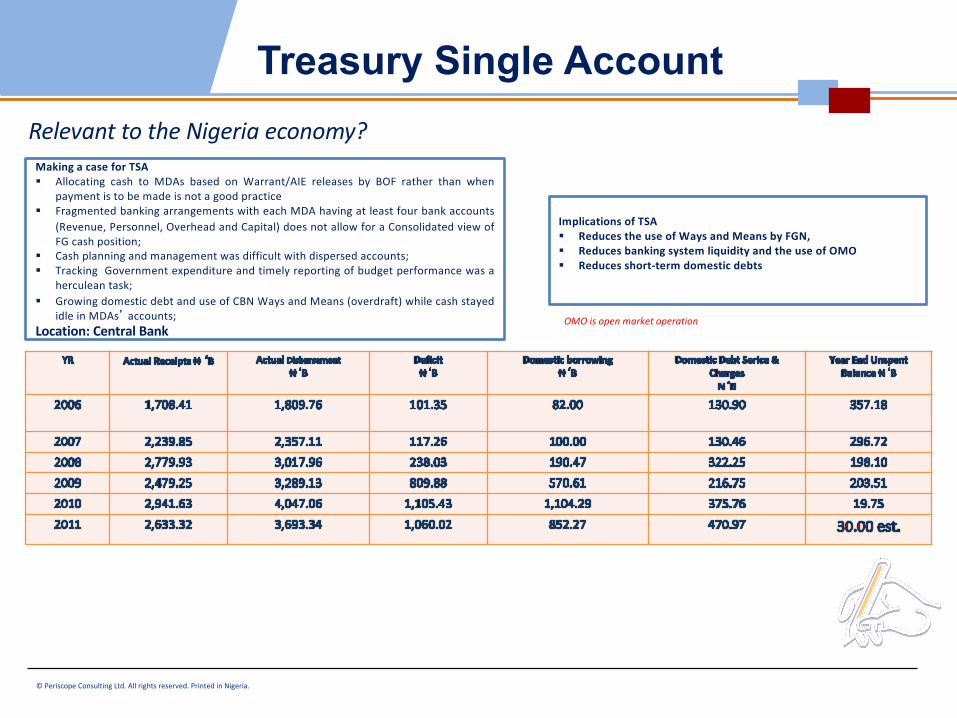

Making a case for TSA§ Allocating cash to MDAs based on Warrant/AIE releases by BOF rather than when

payment is to be made is not a good practice§ Fragmented banking arrangements with each MDA having at least four bank accounts

(Revenue, Personnel, Overhead and Capital) does not allow for a Consolidated view ofFG cash position;

§ Cash planning and management was difficult with dispersed accounts;§ Tracking Government expenditure and timely reporting of budget performance was a

herculean task;§ Growing domestic debt and use of CBN Ways and Means (overdraft) while cash stayed

idle in MDAs� accounts;Location: Central Bank

Implications of TSA § Reduces the use of Ways and Means by FGN,§ Reduces banking system liquidity and the use of OMO§ Reduces short-term domestic debts

OMO is open market operation

Relevant to the Nigeria economy?

Treasury Single Account

© Periscope Consulting Ltd. All rights reserved. Printed in Nigeria.

Delivering the promise?

Lack of self imposed fiscal discipline may invalidate reform efforts

Treasury Single Account

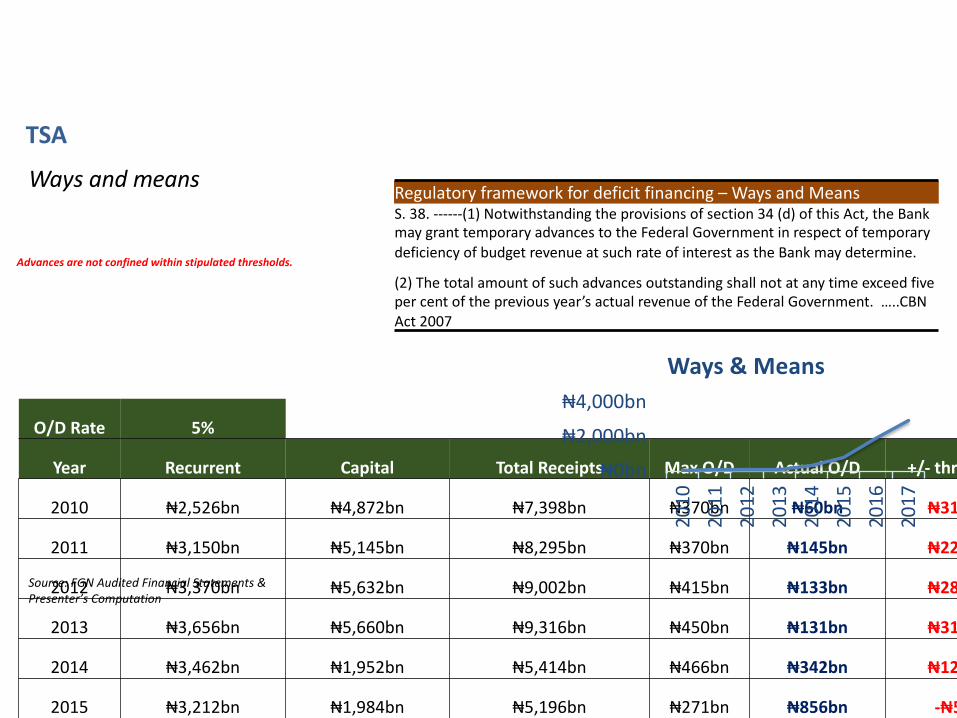

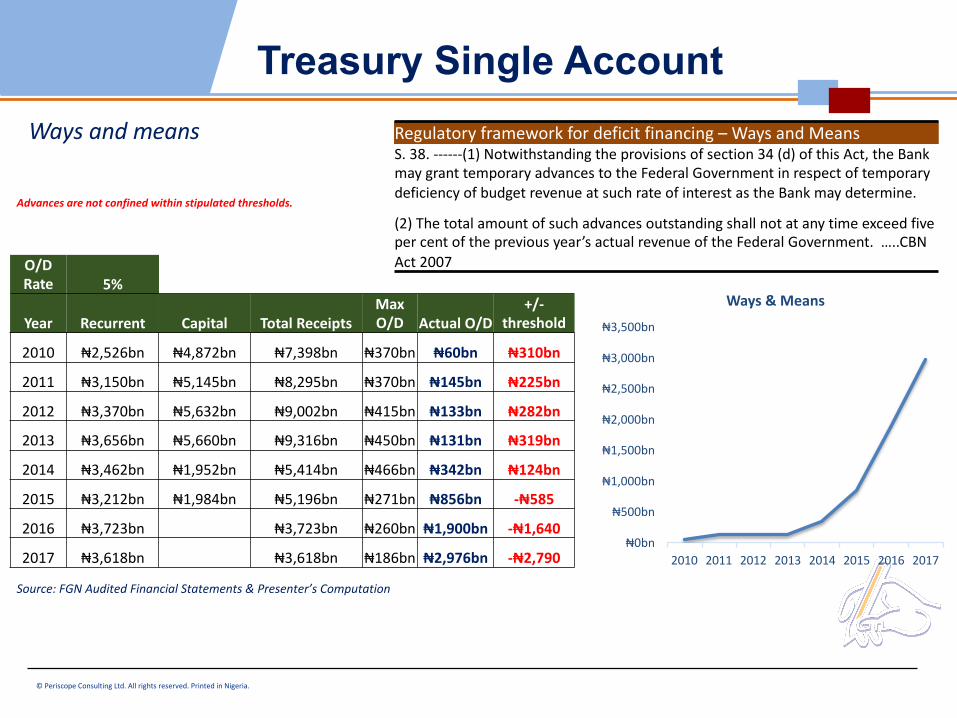

O/D Rate 5%

Year Recurrent Capital Total Receipts Max O/D Actual O/D +/- threshold

2010 ₦2,526bn ₦4,872bn ₦7,398bn ₦370bn ₦60bn ₦310bn

2011 ₦3,150bn ₦5,145bn ₦8,295bn ₦370bn ₦145bn ₦225bn

2012 ₦3,370bn ₦5,632bn ₦9,002bn ₦415bn ₦133bn ₦282bn

2013 ₦3,656bn ₦5,660bn ₦9,316bn ₦450bn ₦131bn ₦319bn

2014 ₦3,462bn ₦1,952bn ₦5,414bn ₦466bn ₦342bn ₦124bn

2015 ₦3,212bn ₦1,984bn ₦5,196bn ₦271bn ₦856bn -₦585

Source: FGN Audited Financial Statements & Presenter’s Computation

₦0bn₦2,000bn₦4,000bn

2010

2011

2012

2013

2014

2015

2016

2017

Ways & Means

Ways and means

TSA

Regulatory framework for deficit financing – Ways and Means S. 38. ------(1) Notwithstanding the provisions of section 34 (d) of this Act, the Bank may grant temporary advances to the Federal Government in respect of temporary deficiency of budget revenue at such rate of interest as the Bank may determine.

(2) The total amount of such advances outstanding shall not at any time exceed five per cent of the previous year’s actual revenue of the Federal Government. …..CBN Act 2007

Advances are not confined within stipulated thresholds.

© Periscope Consulting Ltd. All rights reserved. Printed in Nigeria.

O/D

Rate 5%

Year Recurrent Capital Total Receipts

Max

O/D Actual O/D

+/-

threshold

2010 ₦2,526bn ₦4,872bn ₦7,398bn ₦370bn ₦60bn ₦310bn

2011 ₦3,150bn ₦5,145bn ₦8,295bn ₦370bn ₦145bn ₦225bn

2012 ₦3,370bn ₦5,632bn ₦9,002bn ₦415bn ₦133bn ₦282bn

2013 ₦3,656bn ₦5,660bn ₦9,316bn ₦450bn ₦131bn ₦319bn

2014 ₦3,462bn ₦1,952bn ₦5,414bn ₦466bn ₦342bn ₦124bn

2015 ₦3,212bn ₦1,984bn ₦5,196bn ₦271bn ₦856bn -₦585

2016 ₦3,723bn ₦3,723bn ₦260bn ₦1,900bn -₦1,640

2017 ₦3,618bn ₦3,618bn ₦186bn ₦2,976bn -₦2,790

Source: FGN Audited Financial Statements & Presenter’s Computation

₦0bn

₦500bn

₦1,000bn

₦1,500bn

₦2,000bn

₦2,500bn

₦3,000bn

₦3,500bn

2010 2011 2012 2013 2014 2015 2016 2017

Ways & Means

Ways and means Regulatory framework for deficit financing – Ways and Means S. 38. ------(1) Notwithstanding the provisions of section 34 (d) of this Act, the Bank may grant temporary advances to the Federal Government in respect of temporary deficiency of budget revenue at such rate of interest as the Bank may determine.

(2) The total amount of such advances outstanding shall not at any time exceed five per cent of the previous year’s actual revenue of the Federal Government. …..CBN Act 2007

Advances are not confined within stipulated thresholds.

Treasury Single Account

© Periscope Consulting Ltd. All rights reserved. Printed in Nigeria.

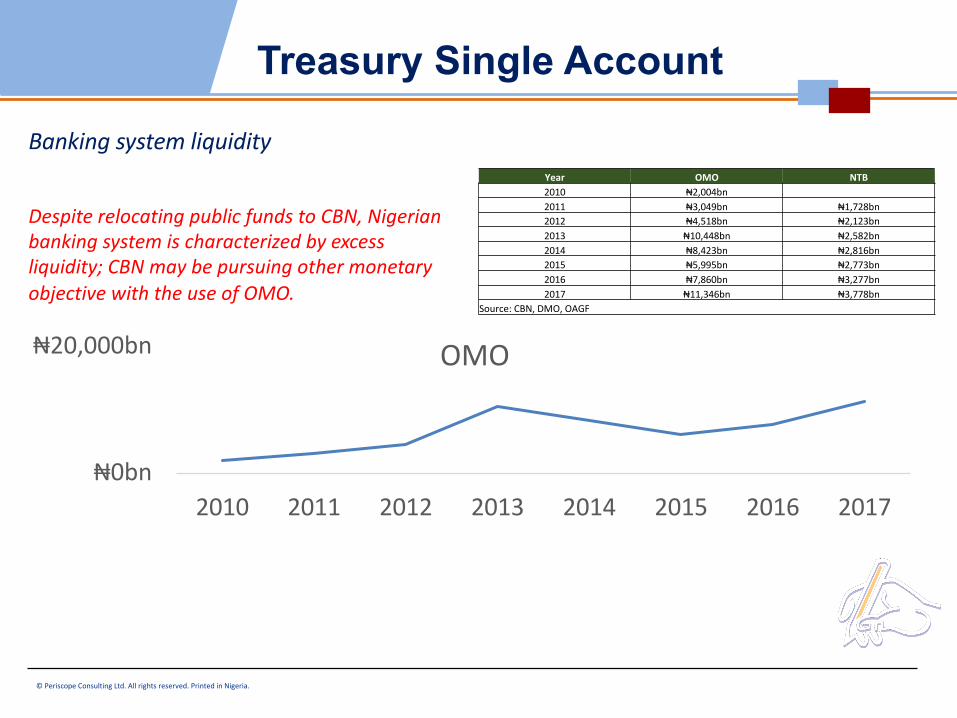

TSA – Nigeria : Delivering the promise? Year OMO NTB2010 ₦2,004bn2011 ₦3,049bn ₦1,728bn2012 ₦4,518bn ₦2,123bn2013 ₦10,448bn ₦2,582bn2014 ₦8,423bn ₦2,816bn2015 ₦5,995bn ₦2,773bn2016 ₦7,860bn ₦3,277bn2017 ₦11,346bn ₦3,778bn

Source: CBN, DMO, OAGF

₦0bn

₦20,000bn

2010 2011 2012 2013 2014 2015 2016 2017

OMO

Banking system liquidity

Despite relocating public funds to CBN, Nigerian banking system is characterized by excess liquidity; CBN may be pursuing other monetary objective with the use of OMO.

Treasury Single Account

© Periscope Consulting Ltd. All rights reserved. Printed in Nigeria.

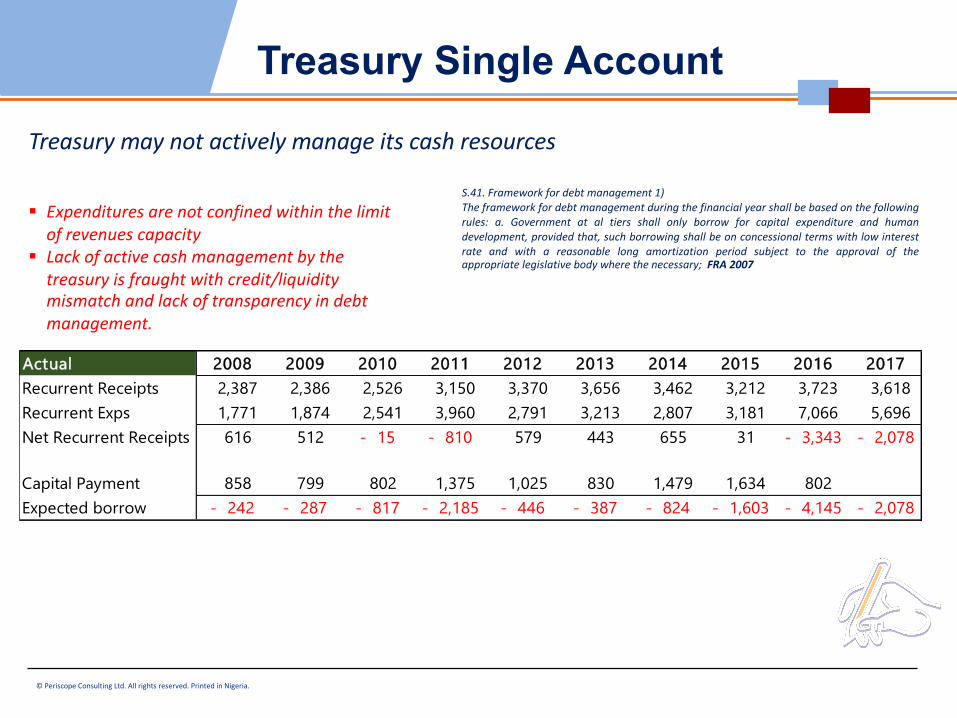

TSA – Nigeria : Delivering the promise? Treasury may not actively manage its cash resources

S.41. Framework for debt management 1)The framework for debt management during the financial year shall be based on the followingrules: a. Government at al tiers shall only borrow for capital expenditure and humandevelopment, provided that, such borrowing shall be on concessional terms with low interestrate and with a reasonable long amortization period subject to the approval of theappropriate legislative body where the necessary; FRA 2007

§ Expenditures are not confined within the limit of revenues capacity

§ Lack of active cash management by the treasury is fraught with credit/liquidity mismatch and lack of transparency in debt management.

Actual 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017Recurrent Receipts 2,387 2,386 2,526 3,150 3,370 3,656 3,462 3,212 3,723 3,618Recurrent Exps 1,771 1,874 2,541 3,960 2,791 3,213 2,807 3,181 7,066 5,696Net Recurrent Receipts 616 512 - 15 - 810 579 443 655 31 - 3,343 - 2,078

Capital Payment 858 799 802 1,375 1,025 830 1,479 1,634 802Expected borrow - 242 - 287 - 817 - 2,185 - 446 - 387 - 824 - 1,603 - 4,145 - 2,078

Treasury Single Account

© Periscope Consulting Ltd. All rights reserved. Printed in Nigeria.

• It takes time for PFM reforms to yield tangible result• Strengthening PFM system requires open and transparency information management • Active cash management by the treasury will align spending, revenue and borrowing • Provision of timely, accurate and transparent information may enhance fiscal discipline • In the meantime, OAGF may need to review all the Power of Attorney it has granted • Lastly, political buy-in is required

Conclusion

© Periscope Consulting Ltd. All rights reserved. Printed in Nigeria. 27

Thank You