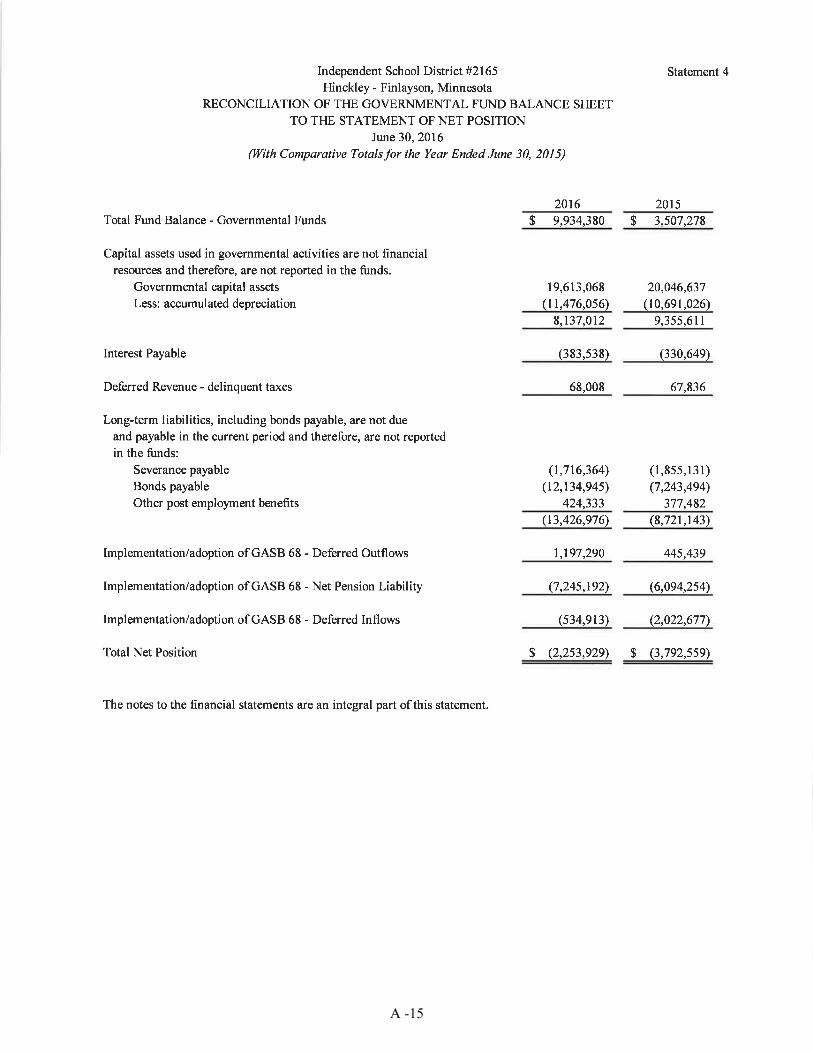

independent school district no. 2165 (hinckley … · franchise tax on corporations and financial...

TRANSCRIPT

Th

is P

relim

ina

ry O

ffic

ial S

tate

me

nt

an

d t

he

info

rma

tio

n c

on

tain

ed

he

rein

is d

ee

me

d b

y t

he

Is

su

er

to b

e f

ina

l a

s o

f th

e d

ate

he

reo

f fo

r p

urp

os

es

of

SE

C R

ule

15

c2

-12

(b)(

1),

ho

we

ve

r, t

he

pri

cin

g a

nd

un

de

rwri

tin

g in

form

ati

on

is s

ub

jec

t to

re

vis

ion

, co

mp

leti

on

or

am

en

dm

en

t. U

nd

er

no

cir

cu

ms

tan

ce

s s

ha

ll th

is P

relim

ina

ry O

ffic

ial S

tate

me

nt

co

ns

titu

te a

n o

ffe

r to

se

ll o

r th

e s

olic

ita

tio

n o

f a

n o

ffe

r to

bu

y t

he

se

se

cu

riti

es

, no

r s

ha

ll th

ere

be

an

y s

ale

of

the

se

se

cu

riti

es

in a

ny

juri

sd

icti

on

in w

hic

h s

uc

h o

ffe

r, s

olic

ita

tio

no

r s

ale

wo

uld

be

un

law

ful p

rio

r to

re

gis

tra

tio

n o

r q

ua

lific

ati

on

un

de

r th

e s

ec

uri

tie

s la

ws

of

an

y s

uc

h ju

ris

dic

tio

n.

In the opinion of Dorsey & Whitney LLP, Minneapolis, Minnesota, Bond Counsel, based on present federal and Minnesota laws, regulations, rulings and decisions, andassuming compliance with certain requirements of the Internal Revenue Code of 1986, as amended, (the "Code"), and certain covenants, interest to be paid on the Bondsis excluded from gross income for federal income tax purposes and from taxable net income of individuals, estates, and trusts for Minnesota income tax purposes, andis not an item of tax preference for federal or Minnesota alternative minimum tax purposes. Such interest is included in taxable income for purposes of the Minnesotafranchise tax on corporations and financial institutions and in adjusted current earnings of corporations for federal alternative minimum tax purposes. The Bonds willbe designated as "qualified tax-exempt obligations" for purposes of Section 265(b)(3) of the Code. See "TAX EXEMPTION" and "RELATED TAX CONSIDERATIONS".

New Issue Rating Application Made: Moody's Investors Service

(Minnesota School District Credit Enhancement Program)PRELIMINARY OFFICIAL STATEMENT DATED NOVEMBER 2, 2017

INDEPENDENT SCHOOL DISTRICT NO. 2165 (HINCKLEY-FINLAYSON), MINNESOTA(Pine, Kanabec, and Aitkin Counties)

$3,085,000* GENERAL OBLIGATION FACILITIES MAINTENANCE BONDS,SERIES 2017B

PROPOSAL OPENING: November 13, 2017, 10:00 A.M., C.T. CONSIDERATION: November 13, 2017, 6:30 P.M., C.T.

PURPOSE/AUTHORITY/SECURITY: The $3,085,000* General Obligation Facilities Maintenance Bonds, Series 2017B(the "Bonds") are being issued pursuant to Minnesota Statutes, Chapter 475 and Section 123B.595 (long-term facilitiesmaintenance revenue) by Independent School District No. 2165 (Hinckley-Finlayson), Minnesota (the "District") to providefunds for deferred maintenance projects included in the ten-year facility plan of the District and approved by theCommissioner of Education. The Bonds will be general obligations of the District for which its full faith, credit and taxingpowers are pledged. Delivery is subject to receipt of an approving legal opinion of Dorsey & Whitney LLP, Minneapolis,Minnesota.DATE OF BONDS: December 6, 2017MATURITY: February 1 as follows:

Year Amount* Year Amount* Year Amount*2019 $135,000 2024 $175,000 2029 $260,0002020 155,000 2025 180,000 2030 270,0002021 155,000 2026 185,000 2031 280,0002022 160,000 2027 190,000 2032 285,0002023 165,000 2028 195,000 2033 295,000

MATURITY ADJUSTMENTS:

* The District reserves the right to increase or decrease the principal amount of the Bonds onthe day of sale, in increments of $5,000 each. Increases or decreases may be made in anymaturity. If any principal amounts are adjusted, the purchase price proposed will be adjustedto maintain the same gross spread per $1,000.

TERM BONDS: See "Term Bond Option" herein.INTEREST: August 1, 2018 and semiannually thereafter.OPTIONAL REDEMPTION:

Bonds maturing February 1, 2028 and thereafter are subject to call for prior redemption onFebruary 1, 2027 and any date thereafter, at par.

MINIMUM PROPOSAL: $3,054,150.GOOD FAITH DEPOSIT: A cashier's check in the amount of $61,700 may be submitted contemporaneously with the

proposal or, alternatively, a good faith deposit shall be made by the winning bidder by wiretransfer of funds.

PAYING AGENT: Bond Trust Services Corporation, Roseville, Minnesota.BOOK-ENTRY-ONLY: See "Book-Entry-Only System" herein (unless otherwise specified by the purchaser).

REPRESENTATIONS

No dealer, broker, salesperson or other person has been authorized by the District to give any information or to make any representation otherthan those contained in this Official Statement and, if given or made, such other information or representations must not be relied upon ashaving been authorized by the District. This Official Statement does not constitute an offer to sell or a solicitation of an offer to buy anyof the Bonds in any jurisdiction to any person to whom it is unlawful to make such an offer or solicitation in such jurisdiction.

This Official Statement is not to be construed as a contract with the Syndicate Manager or Syndicate Members. Statements contained hereinwhich involve estimates or matters of opinion are intended solely as such and are not to be construed as representations of fact. Ehlers &Associates, Inc. prepared this Official Statement and any addenda thereto relying on information of the District and other sources for whichthere is reasonable basis for believing the information is accurate and complete. Bond Counsel has not participated in the preparation of thisOfficial Statement and is not expressing any opinion as to the completeness or accuracy of the information contained therein. Compensationof Ehlers & Associates, Inc., payable entirely by the District, is contingent upon the sale of the issue.

COMPLIANCE WITH S.E.C. RULE 15c2-12

Certain municipal obligations (issued in an aggregate amount over $1,000,000) are subject to Rule 15c2-12 promulgated by the Securities andExchange Commission pursuant to the Securities Exchange Act of 1934, as amended (the "Rule").

Official Statement: This Official Statement was prepared for the District for dissemination to potential investors. Its primary purpose isto disclose information regarding the Bonds to prospective underwriters in the interest of receiving competitive proposals in accordance withthe sale notice contained herein. Unless an addendum is posted prior to the sale, this Official Statement shall be deemed nearly final forpurposes of the Rule subject to completion, revision and amendment in a Final Official Statement as defined below.

Review Period: This Official Statement has been distributed to prospective bidders for review. Comments or requests for the correctionof omissions or inaccuracies must be submitted to Ehlers & Associates, Inc. at least two business days prior to the sale. Requests for additionalinformation or corrections in the Official Statement received on or before this date will not be considered a qualification of a proposal receivedfrom an underwriter. If there are any changes, corrections or additions to the Official Statement, interested bidders will be informed by anaddendum prior to the sale.

Final Official Statement: Upon award of sale of the Bonds, the Official Statement together with any previous addendum of corrections oradditions will be further supplemented by an addendum specifying the offering prices, interest rates, aggregate principal amount, principalamount per maturity, anticipated delivery date, and Syndicate Manager and Syndicate Members, together with any other information requiredby law, and, as supplemented, shall constitute a "Final Official Statement" of the District with respect to the Bonds, as defined in the Rule. Copies of the Final Official Statement will be delivered to the underwriter (Syndicate Manager) within seven business days following theproposal acceptance.

Continuing Disclosure: Subject to certain exemptions, issues in an aggregate amount over $1,000,000 may be required to comply withprovisions of the Rule which require that underwriters obtain from the issuers of municipal securities (or other obligated party) an agreementfor the benefit of the owners of the securities to provide continuing disclosure with respect to those securities. This Official Statement describesthe conditions under which the Bonds are required to comply with the Rule.

CLOSING CERTIFICATES

Upon delivery of the Bonds, the underwriter (Syndicate Manager) will be furnished with the following items: (1) a certificate of the appropriateofficials to the effect that at the time of the sale of the Bonds and all times subsequent thereto up to and including the time of the delivery ofthe Bonds, this Official Statement did not and does not contain any untrue statement of a material fact or omit to state a material fact necessaryto make the statements therein, in the light of the circumstances under which they were made, not misleading; (2) a receipt signed by theappropriate officer evidencing payment for the Bonds; (3) a certificate evidencing the due execution of the Bonds, including statements that(a) no litigation of any nature is pending, or to the knowledge of signers, threatened, restraining or enjoining the issuance and delivery of theBonds, (b) neither the corporate existence or boundaries of the District nor the title of the signers to their respective offices is being contested,and (c) no authority or proceedings for the issuance of the Bonds have been repealed, revoked or rescinded; and (4) a certificate setting forthfacts and expectations of the District which indicates that the District does not expect to use the proceeds of the Bonds in a manner that wouldcause them to be arbitrage bonds within the meaning of Section 148 of the Internal Revenue Code of 1986, as amended, or within the meaningof applicable Treasury Regulations.

ii

TABLE OF CONTENTSINTRODUCTORY STATEMENT . . . . . . . . . . . . . . . . . . . . 1

THE BONDS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1GENERAL . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1OPTIONAL REDEMPTION . . . . . . . . . . . . . . . . . . . . . 2AUTHORITY; PURPOSE . . . . . . . . . . . . . . . . . . . . . . . 2ESTIMATED SOURCES AND USES . . . . . . . . . . . . . 2SECURITY . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2RATING . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3STATE OF MINNESOTA CREDIT ENHANCEMENT PROGRAM FOR SCHOOL DISTRICTS . . . . . . . . . . . . . . . . . . . . . . . . . 3CONTINUING DISCLOSURE . . . . . . . . . . . . . . . . . . . 4LEGAL OPINION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5TAX EXEMPTION AND RELATED TAX CONSIDERATIONS . . . . . . . . . . . . . . . . . . . . . 6MUNICIPAL ADVISOR . . . . . . . . . . . . . . . . . . . . . . . . 8MUNICIPAL ADVISOR AFFILIATED COMPANIES 8INDEPENDENT AUDITORS . . . . . . . . . . . . . . . . . . . . 9RISK FACTORS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

VALUATIONS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11OVERVIEW . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11CURRENT PROPERTY VALUATIONS . . . . . . . . . . 122016/17 NET TAX CAPACITY BY CLASSIFICATION . . . . . . . . . . . . . . . . . . . . . . . . . . . 13LARGER TAXPAYERS . . . . . . . . . . . . . . . . . . . . . . . 14

DEBT . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15DIRECT DEBT . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15STATE AID FOR DEBT SERVICE . . . . . . . . . . . . . . 15SCHEDULE OF BONDED INDEBTEDNESS . . . . . . 16BONDED DEBT LIMIT . . . . . . . . . . . . . . . . . . . . . . . 17OVERLAPPING DEBT . . . . . . . . . . . . . . . . . . . . . . . . 17DEBT PAYMENT HISTORY . . . . . . . . . . . . . . . . . . . 17DEBT RATIOS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18FUTURE FINANCING . . . . . . . . . . . . . . . . . . . . . . . . 18LEVY LIMITS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

TAX RATES, LEVIES AND COLLECTIONS . . . . . . . . . . 19TAX LEVIES AND COLLECTIONS . . . . . . . . . . . . . 19TAX CAPACITY RATES . . . . . . . . . . . . . . . . . . . . . . 20

THE ISSUER . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21EMPLOYEES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21PENSIONS; UNIONS . . . . . . . . . . . . . . . . . . . . . . . . . 21POST EMPLOYMENT BENEFITS . . . . . . . . . . . . . . 21STUDENT BODY . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22SCHOOL BUILDINGS . . . . . . . . . . . . . . . . . . . . . . . . 22FUNDS ON HAND . . . . . . . . . . . . . . . . . . . . . . . . . . . 22LITIGATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23MUNICIPAL BANKRUPTCY . . . . . . . . . . . . . . . . . . 23

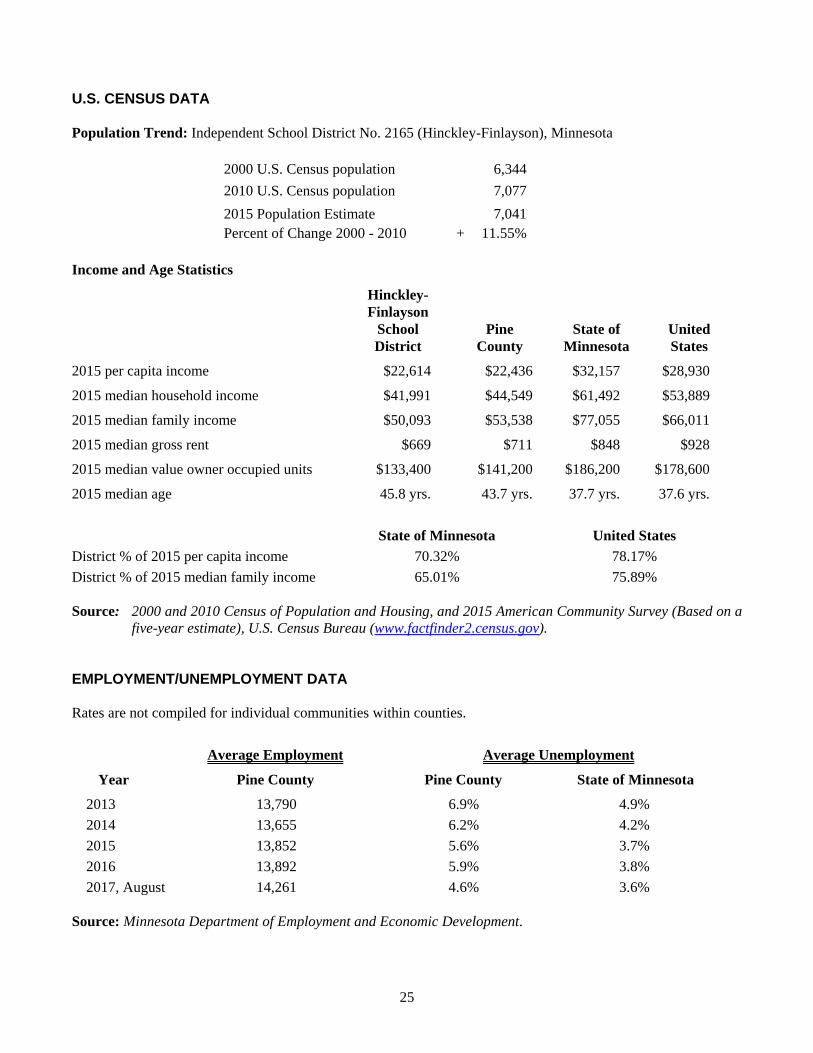

GENERAL INFORMATION . . . . . . . . . . . . . . . . . . . . . . . . 25LOCATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25LARGER EMPLOYERS . . . . . . . . . . . . . . . . . . . . . . . 25U.S. CENSUS DATA . . . . . . . . . . . . . . . . . . . . . . . . . . 26EMPLOYMENT/UNEMPLOYMENT DATA . . . . . . 26

FINANCIAL STATEMENTS . . . . . . . . . . . . . . . . . . . . . . . . . . . A-1

FORM OF LEGAL OPINION . . . . . . . . . . . . . . . . . . . . . . . . . . . B-1

BOOK-ENTRY-ONLY SYSTEM . . . . . . . . . . . . . . . . . . . . . . . . C-1

FORM OF CONTINUING DISCLOSURE COVENANTS (EXCERPTS FROM SALE RESOLUTION) . . . . . . . . . . . D-1

TERMS OF PROPOSAL . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . E-1

iii

BOARD OF EDUCATION

Term Expires

Mary Ellen VonRueden Chairperson January 2018

Bill Randall Vice Chairperson January 2018

Steve Grinsteinner Clerk January 2018

Leo Irlbeck Treasurer January 2020

Lisa Blowers Director January 2018

Kala Roberts Director January 2020

Angela Grochowski Director January 2020

ADMINISTRATION

Rob Prater, Superintendent of Schools

Joanne Bruns, Business Manager

PROFESSIONAL SERVICES

Dorsey & Whitney LLP, Bond Counsel, Minneapolis, Minnesota

Ehlers & Associates, Inc., Municipal Advisors, Roseville, Minnesota(Other offices located in Waukesha, Wisconsin, Chicago, Illinois and Denver, Colorado)

iv

INTRODUCTORY STATEMENT

This Preliminary Official Statement contains certain information regarding Independent School District No. 2165(Hinckley-Finlayson), Minnesota (the "District") and the issuance of its $3,085,000* General Obligation FacilitiesMaintenance Bonds, Series 2017B (the "Bonds") or the "Obligations". Any descriptions or summaries of the Bonds,statutes, or documents included herein are not intended to be complete and are qualified in their entirety by referenceto such statutes and documents and the form of the Bonds to be included in the resolution awarding the sale of theBonds (the "Award Resolution") to be adopted by the Board of Education on November 13, 2017.

Inquiries may be directed to Ehlers & Associates, Inc. ("Ehlers" or the "Municipal Advisor"), Roseville, Minnesota,(651) 697-8500, the District's Municipal Advisor. A copy of this Preliminary Official Statement may be downloadedfrom Ehlers’ web site at www.ehlers-inc.com by connecting to the Bond Sales link and following the directions atthe top of the site.

THE BONDS

GENERAL

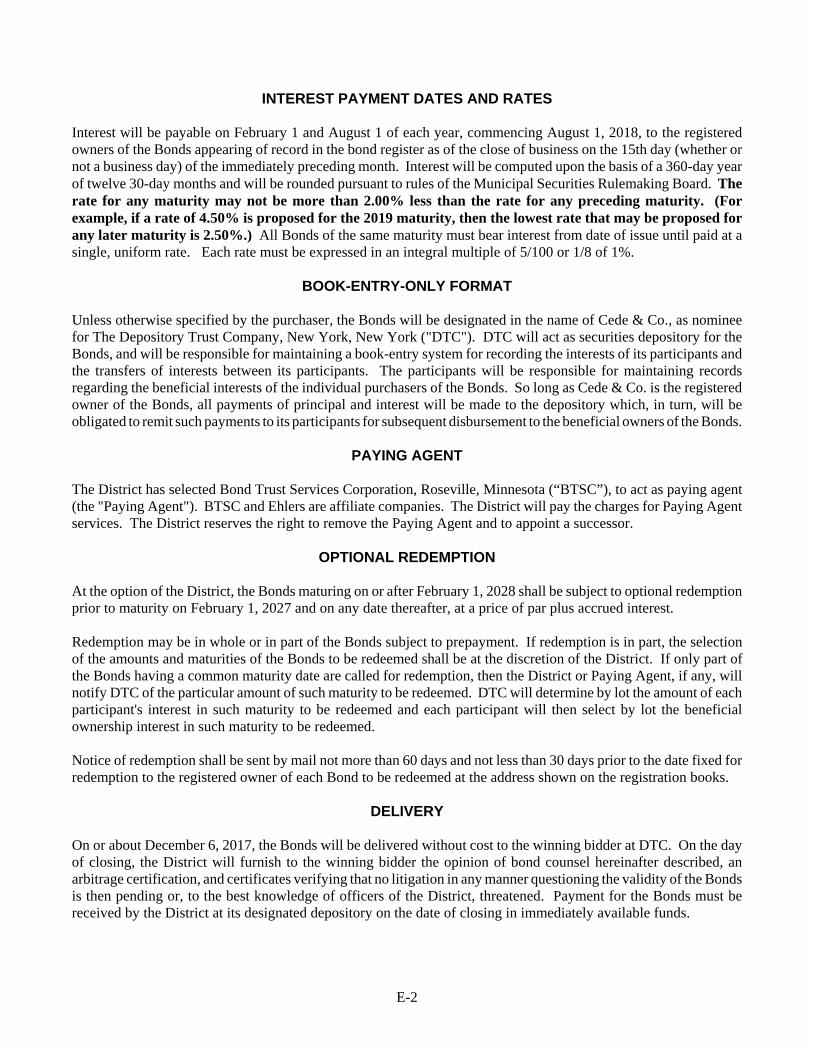

The Bonds will be issued in fully registered form as to both principal and interest in denominations of $5,000 eachor any integral multiple thereof, and will be dated, as originally issued, as of December 6, 2017. The Bonds willmature on February 1 in the years and amounts set forth on the cover of this Preliminary Official Statement. Interestwill be payable on February 1 and August 1 of each year, commencing August 1, 2018, to the registered owners ofthe Bonds appearing of record in the bond register as of the close of business on the 15th day (whether or not abusiness day) of the immediately preceding month. Interest will be computed upon the basis of a 360-day year oftwelve 30-day months and will be rounded pursuant to rules of the Municipal Securities Rulemaking Board("MSRB"). The rate for any maturity may not be more than 2.00% less than the rate for any precedingmaturity. (For example, if a rate of 4.50% is proposed for the 2019 maturity, then the lowest rate that may beproposed for any later maturity is 2.50%.) All Bonds of the same maturity must bear interest from the date of issueuntil paid at a single, uniform rate. Each rate must be expressed in an integral multiple of 5/100 or 1/8 of 1%.

Unless otherwise specified by the purchaser, the Bonds will be registered in the name of Cede & Co., as nominee forThe Depository Trust Company, New York, New York ("DTC"). (See "Book-Entry-Only System" herein.) As longas the Bonds are held under the book-entry system, beneficial ownership interests in the Bonds may be acquired inbook-entry form only, and all payments of principal of, premium, if any, and interest on the Bonds shall be madethrough the facilities of DTC and its participants. If the book-entry system is terminated, principal of, premium, ifany, and interest on the Bonds shall be payable as provided in the Award Resolution.

The District has selected Bond Trust Services Corporation, Roseville, Minnesota, to act as paying agent (the "PayingAgent"). Bond Trust Services Corporation and Ehlers are affiliate companies. The District will pay the charges forPaying Agent services. The District reserves the right to remove the Paying Agent and to appoint a successor.

*Preliminary, subject to change.

1

OPTIONAL REDEMPTION

At the option of the District, the Bonds maturing on or after February 1, 2028 shall be subject to optional redemptionprior to maturity on February 1, 2027 and on any date thereafter, at a price of par plus accrued interest.

Redemption may be in whole or in part of the Bonds subject to prepayment. If redemption is in part, the selectionof the amounts and maturities of the Bonds to be redeemed shall be at the discretion of the District. If only part ofthe Bonds having a common maturity date are called for redemption, then the District or Paying Agent, if any, willnotify DTC of the particular amount of such maturity to be redeemed. DTC will determine by lot the amount of eachparticipant's interest in such maturity to be redeemed and each participant will then select by lot the beneficialownership interest in such maturity to be redeemed.

Notice of redemption shall be sent by mail not more than 60 days and not less than 30 days prior to the date fixed forredemption to the registered owner of each Bond to be redeemed at the address shown on the registration books.

AUTHORITY; PURPOSE

The Bonds are being issued pursuant to Minnesota Statutes, Chapter 475 and Section 123B.595 (long-term facilitiesmaintenance revenue) by the District to provide funds for deferred maintenance projects included in the ten-yearfacility plan of the District and approved by the Commissioner of Education.

ESTIMATED SOURCES AND USES

Sources

Par Amount of Bonds $3,085,000

Estimated Premium 105,688

Total Sources $3,190,688

Uses

Project Costs $3,114,538

Estimated Discount 30,850

Finance Related Expenses 45,300

Total Uses $3,190,688

SECURITY

The Bonds are general obligations of the District to which its full faith, credit and taxing powers are pledged. Inaccordance with Minnesota Statutes, the District will levy each year an amount not less than 105% of the debt servicerequirements on the Bonds, less estimated collections of other revenues pledged for payments on the Bonds. In theevent funds on hand for payment of principal and interest are at any time insufficient, the District is required to levyadditional taxes upon all taxable properties within its boundaries without limit as to rate or amount to make up anydeficiency.

2

RATING

The District will be participating in the State of Minnesota Credit Enhancement Program ("MNCEP") for this issueand is requesting a rating from Moody’s Investors Service, Inc. (“Moody’s”). Moody’s has a policy which assignsa minimum rating of "Aa2" to issuers participating in the MNCEP. The "Aa2" rating is based on the State ofMinnesota’s current "Aa1" rating from Moody’s. See "STATE OF MINNESOTA CREDIT ENHANCEMENTPROGRAM FOR SCHOOL DISTRICTS" for further details.

The District currently has an "A2" underlying rating from Moody’s and will be requesting an underlying rating onthis issue. Such rating reflects only the views of such organization and explanations of the significance of such ratingmay be obtained from the rating agency furnishing the same. Generally, a rating agency bases its rating on theinformation and materials furnished to it and on investigations, studies and assumptions of its own. There is noassurance that such rating will continue for any given period of time or that it will not be revised downward orwithdrawn entirely by such rating agency, if in the judgement of such rating agency circumstances so warrant. Anysuch downward revision or withdrawal of such rating may have an adverse effect on the market price of the Bonds.

Such rating is not to be construed as a recommendation of the rating agency to buy, sell or hold the Bonds, and therating assigned by the rating agency should be evaluated independently. Except as may be required by the DisclosureUndertaking described under the heading "CONTINUING DISCLOSURE" neither the District nor the underwriterundertake responsibility to bring to the attention of the owner of the Bonds any proposed changes in or withdrawalof such rating or to oppose any such revision or withdrawal.

STATE OF MINNESOTA CREDIT ENHANCEMENT PROGRAM FOR SCHOOL DISTRICTS

By resolution adopted for this issue on September 11, 2017 (the "Resolution"), the District has covenanted andobligated itself to be bound by the provisions of Minnesota Statutes, Section 126C.55, which provides for paymentby the State of Minnesota in the event of a potential default of a school district obligation (herein referred to as the"State Payment Law" or the "Law"). The provisions of the State Payment Law shall be binding on the District as longas any obligations of the issue remain outstanding.

Under the State Payment Law, if the District believes it may be unable to make a principal or interest payment for thisissue on the due date, it must notify the Commissioner of Education as soon as possible, but not less than 15 workingdays prior to the due date (which notice is to specify certain information) that it intends to exercise the provisions ofthe Law to guarantee payment of the principal and interest when due. The District also covenants in the Resolutionto deposit with the Paying Agent for the issue three business days prior to the date on which a payment is due anamount sufficient to make that payment or to notify the Commissioner of Education that it will be unable to make allor a portion of the payment.

The Law also requires the Paying Agent for this issue to notify the Commissioner of Education if it becomes awareof a potential default in the payment of principal and interest on these obligations, or if, on the day two business daysprior to the payment date, there are insufficient funds to make the payment or deposit with the Paying Agent.

The Law also requires, after receipt of a notice which requests a payment pursuant to the Law, after consultation withthe Paying Agent and District, and after verifying the accuracy of the information provided, the Commissioner ofEducation shall notify the Commissioner of Management and Budget of the potential default. The State Payment Lawprovides that "upon receipt of this notice . . . the Commissioner of Management and Budget shall issue a warrant andauthorize the Commissioner of Education to pay to the Paying Agent for the debt obligation the specified amount onor before the date due. The amounts needed for purposes of subdivision are annually appropriated to the Departmentof Education from the state general fund."

3

The Law requires that all amounts paid by the State on behalf of any School District are required to be repaid by theDistrict to the State with interest, either via a reduction in State aid payable to the District, or through the levy of anad valorem tax which may be made with the approval of the Commissioner of Education.

In its Official Statement dated September 27, 2017, for General Obligation State Bonds, Series 2017A, 2017B, 2017C,2017D, and 2017E, the State of Minnesota disclosed the following information about the State Credit EnhancementProgram for School Districts.

"As the date of this Official Statement, the total amount of principal on certificates of indebtedness and capitalnotes issued for equipment, certificates of participation and bonds, plus the interest on these obligations, throughthe year 2046, is approximately $12.5 billion. Based upon these currently outstanding balances now enrolled inthe program, during the Current Biennium the total amount of principal and interest outstanding as of the dateof this Official Statement is $1.9 billion, with the maximum amount of principal and interest payable in any onemonth being $760 million. However, more certificates of indebtedness, capital notes, certificates of participationand bonds are expected to be enrolled in the program and these amounts are expected to increase.

The State has not had to make any debt service payments on behalf of school districts or intermediate schooldistricts under the program and does not expect to make any payments in the future. If such payments are madethe State expects to recover all or substantially all of the amounts so paid pursuant to contractual agreements withthe school districts and intermediate school districts."

CONTINUING DISCLOSURE

In order to assist the Underwriters in complying with SEC Rule 15c2-12 promulgated by the Securities and ExchangeCommission, pursuant to the Securities Exchange Act of 1934 (hereinafter the "Rule"), the District shall covenantto take certain actions pursuant to a Resolution adopted by the Board of Education by entering into a ContinuingDisclosure Undertaking (the "Disclosure Undertaking") for the benefit of holders, including beneficial holders. TheDisclosure Undertaking requires the District to provide electronically or in the manner otherwise prescribed certainfinancial information annually and to provide notices of the occurrence of certain events enumerated in the Rule. Thedetails and terms of the Disclosure Undertaking for this issue are set forth in Appendix D to be executed and deliveredby the District at the time of delivery of the Bonds. Such Disclosure Undertaking will be in substantially the formattached hereto.

In the previous five years, the District believes it has not failed to comply in all material respects with its priorundertakings under the Rule.

A failure by the District to comply with any Disclosure Undertaking will not constitute an event of default on thisissue or any issue outstanding. However, such a failure may adversely affect the transferability and liquidity of theBonds and their market price.

The District will file its continuing disclosure information using the Electronic Municipal Market Access ("EMMA")system or any system that may be prescribed in the future. Investors will be able to access continuing disclosureinformation filed with the MSRB at www.emma.msrb.org. Ehlers is currently engaged as disclosure disseminationagent for the District.

4

LEGAL OPINION

An opinion in substantially the form attached hereto as Appendix B will be furnished by Dorsey & Whitney LLP,Minneapolis, Minnesota, bond counsel to the District.

TAX EXEMPTION AND RELATED TAX CONSIDERATIONS

The following discussion is not intended to be an exhaustive discussion of collateral tax consequences arising fromownership or disposition of the Bonds or receipt of interest on the Bonds. Prospective purchasers should consult theirtax advisors with respect to collateral tax consequences, including, without limitation, the determination of gain orloss on the sale of a Bond, the calculation of alternative minimum tax liability, the inclusion of Social Security orother retirement payments in taxable income, the disallowance of deductions for certain expenses attributable to theBonds, and applicable state and local tax rules in states other than Minnesota. The form of the approving opinion ofDorsey & Whitney LLP, Bond Counsel, is attached as Appendix B hereto.

Tax Exemption

It is the opinion of Dorsey & Whitney LLP, Minneapolis, Minnesota, Bond Counsel, based on present federal andMinnesota laws, regulations, rulings and decisions, and on certifications to be furnished at closing, and assumingcompliance by the District with certain covenants (the "Tax Covenants"), that interest to be paid on the Bonds isexcluded from gross income for federal income tax purposes and from taxable net income of individuals, estates, andtrusts for Minnesota income tax purposes. Such interest is, however, included in taxable income for purposes of theMinnesota franchise tax on corporations and financial institutions.

Certain provisions of the Internal Revenue Code of 1986, as amended (the "Code"), however, impose continuingrequirements that must be met after the issuance of the Bonds in order that interest on the Bonds be and remainexcludable from federal gross income and from Minnesota taxable net income of individuals, estates, and trusts. These requirements include, but are not limited to, provisions regarding the use of Bond proceeds and the facilitiesfinanced or refinanced with such proceeds; restrictions on the investment of Bond proceeds and other amounts; andprovisions requiring that certain investment earnings be rebated periodically to the federal government. Noncompliance with such requirements of the Code may cause interest on the Bonds to be includable in federal grossincome or in Minnesota taxable net income retroactively to their date of issue. Compliance with the Tax Covenantswill satisfy the current requirements of the Code with respect to exclusion of interest on the Bonds from federal grossincome and from Minnesota taxable net income of individuals, estates, and trusts. No provision has been made forredemption of or for an increase in the interest rate on the Bonds in the event that interest on the same becomesincludable in federal gross income or in Minnesota taxable net income.

Qualified Tax-Exempt Obligations

The District will designate the Bonds as "qualified tax-exempt obligations" for purposes of Section 265(b)(3) of theCode relating to the ability of financial institutions to deduct from income for federal income tax purposes a portionof the interest expense that is allocable to carrying and acquiring tax-exempt obligations. Sections 265(a)(2) and 291of the Code impose additional limitations on the deductibility of such interest expense.

5

Original Issue Discount

Certain maturities of the Bonds may be issued at a discount from the principal amount payable on such Bonds atmaturity (collectively, the "Discount Bonds"). The difference between the price at which a substantial amount of theDiscount Bonds of a given maturity is first sold to the public (the "Issue Price") and the principal amount payable atmaturity constitutes "original issue discount" under the Code. The amount of original issue discount that accrues toa holder of a Discount Bond under section 1288 of the Code is excluded from federal gross income and fromMinnesota taxable net income of individuals, estates, and trusts to the same extent that stated interest on such DiscountBond would be so excluded. The amount of the original issue discount that accrues with respect to a Discount Bondunder section 1288 is added to the owner’s federal and Minnesota tax basis in determining gain or loss upondisposition of such Discount Bond (whether by sale, exchange, redemption or payment at maturity). Original issuediscount is taxable under the Minnesota franchise tax on corporations and financial institutions.

Interest in the form of original issue discount accrues under section 1288 pursuant to a constant yield method thatreflects semiannual compounding on dates that are determined by reference to the maturity date of the Discount Bond.The amount of original issue discount that accrues for any particular semiannual accrual period generally is equal tothe excess of (1) the product of (a) one-half of the yield on such Bonds (adjusted as necessary for an initial shortperiod) and (b) the adjusted issue price of such Bonds, over (2) the amount of stated interest actually payable. Forpurposes of the preceding sentence, the adjusted issue price is determined by adding to the Issue Price for such Bondsthe original issue discount that is treated as having accrued during all prior semiannual accrual periods. If a DiscountBond is sold or otherwise disposed of between semiannual compounding dates, then the original issue discount thatwould have accrued for that semiannual accrual period for federal income tax purposes is allocated ratably to the daysin such accrual period.

If a Discount Bond is purchased for a cost that exceeds the sum of the Issue Price plus accrued interest and accruedoriginal issue discount, the amount of original issue discount that is deemed to accrue thereafter to the purchaser isreduced by an amount that reflects amortization of such excess over the remaining term of such Bond. If such excess isgreater than the amount of remaining original issue discount, the basis reduction rules in the Code for amortizableBond premium might result in taxable gain upon sale, redemption or maturity of the Bonds, even if the Bonds are sold,redeemed or retired for an amount equal to or less than their cost.

Except for the Minnesota rules described above, no opinion is expressed as to state and local income tax treatmentof original issue discount. It is possible under certain state and local income tax laws that original issue discount ona Discount Bond may be taxable in the year of accrual, and may be deemed to accrue differently than under federallaw.

Holders of Discount Bonds should consult their tax advisors with respect to the computation and accrual of originalissue discount and with respect to the other federal, state and local tax consequences associated with the purchase,ownership, redemption, sale or other disposition of Discount Bonds.

Bond Premium

Certain maturities of the Bonds may be issued at a premium to the principal amount payable at maturity. Except inthe case of dealers, which are subject to special rules, Bondholders who acquire Bonds at a premium, even Bonds thatwere not initially offered at a premium, must, from time to time, reduce their federal and Minnesota tax bases for theBonds for purposes of determining gain or loss on the sale or payment of such Bonds. Premium generally isamortized for federal and Minnesota income and franchise tax purposes on the basis of a Bondholder’s constant yieldto maturity or to certain call dates with semiannual compounding. Accordingly, Bondholders who acquire Bonds ata premium might recognize taxable gain upon sale of the Bonds, even if such Bonds are sold for an amount equal toor less than their original cost. Amortized premium is not deductible for federal or Minnesota income tax purposes. Bondholders who acquire Bonds at a premium should consult their tax advisors concerning the calculation of Bondpremium and the timing and rate of premium amortization, as well as the state and local tax consequences of owningand selling Bonds acquired at a premium.

6

Related Tax Considerations

Interest on the Bonds is not an item of tax preference for federal or Minnesota alternative minimum tax purposes, butis included in adjusted current earnings of corporations for purposes of the federal alternative minimum tax. Section86 of the Code and corresponding provisions of Minnesota law require recipients of certain Social Security andrailroad retirement benefits to take interest on the Bonds into account in determining the taxability of such benefits. Passive investment income, including interest on the Bonds, may be subject to taxation under section 1375 of theCode, and corresponding provisions of Minnesota law, for an S corporation that has accumulated earnings and profitsat the close of the taxable year, if more than 25 percent of its gross receipts is passive investment income. Section265 of the Code denies a deduction for interest on indebtedness incurred or continued to purchase or carry the Bonds,and Minnesota law similarly denies a deduction for such interest in the case of individuals, estates, and trusts. Indebtedness may be allocated to the Bonds for this purpose even though not directly traceable to the purchase of theBonds. Federal and Minnesota laws also restrict the deductibility of other expenses allocable to the Bonds. [Becauseof the basis reduction rules in the Code for amortizable Bond premium, Bondholders who acquire Bonds at a premiummight recognize taxable gain upon sale of the Bonds even if the Bonds are sold for an amount equal to or less thantheir original cost.] In the case of an insurance company subject to the tax imposed by section 831 of the Code, theamount which otherwise would be taken into account as losses incurred under section 832(b)(5) of the Code must bereduced by an amount equal to 15 percent of the interest on the Bonds that is received or accrued during the taxableyear. Interest on the Bonds may be included in the income of a foreign corporation for purposes of the branch profitstax imposed by section 884 of the Code, and is included in net investment income of foreign insurance companiesunder section 842(b) of the Code.

Proposed Changes in Federal and State Law

From time to time, there are Presidential proposals, proposals of various federal committees and legislative proposalsin Congress and in the state that, if enacted, could alter or amend the federal and state tax matters referred to hereinor adversely affect the marketability or market value of the Bonds or otherwise prevent holders of the Bonds fromrealizing the full benefit of the tax exemption of interest on the Bonds. For example, in the recent past, legislationhas been proposed that effectively would have imposed a partial tax on otherwise tax exempt interest for certain higherincome taxpayers. In addition, regulatory and administrative actions may from time to time be announced that couldadversely affect the market value, marketability or tax status of the Bonds.

No prediction is made concerning future events. The opinions expressed by Bond Counsel in connection with theissuance of the Bonds are based upon existing law only. Purchasers of the Bonds should consult their own taxadvisors regarding any pending or proposed legislation, regulatory action, or litigation.

THE FOREGOING IS NOT INTENDED TO BE AN EXHAUSTIVE DISCUSSION OF COLLATERAL TAXCONSEQUENCES ARISING FROM OWNERSHIP OR DISPOSITION OF THE BONDS OR RECEIPT OFINTEREST ON THE BONDS. PROSPECTIVE PURCHASERS ARE ADVISED TO CONSULT THEIR OWNTAX ADVISORS AS TO THE TAX CONSEQUENCES OF, OR TAX CONSIDERATIONS FOR, PURCHASINGOR HOLDING THE BONDS.

MUNICIPAL ADVISOR

Ehlers has served as municipal advisor to the District in connection with the issuance of the Bonds. The MunicipalAdvisor cannot participate in the underwriting of the Bonds. The financial information included in this PreliminaryOfficial Statement has been compiled by the Municipal Advisor. Such information does not purport to be a review,audit or certified forecast of future events and may not conform with accounting principles applicable to compilationsof financial information. Ehlers is not a firm of certified public accountants. Ehlers is registered with the Securitiesand Exchange Commission and the MSRB as a Municipal Advisor.

7

MUNICIPAL ADVISOR AFFILIATED COMPANIES

Bond Trust Services Corporation ("BTSC") and Ehlers Investment Partners, LLC ("EIP") are affiliate companies ofEhlers. BTSC is chartered by the State of Minnesota and authorized in Minnesota, Wisconsin, and Illinois to transactthe business of a limited purpose trust company. BTSC provides paying agent services to debt issuers. EIP is aRegistered Investment Advisor with the Securities and Exchange Commission. EIP assists issuers with the investmentof bond proceeds or investing other issuer funds. This includes escrow bidding agent services. Issuers, such as theDistrict, have retained or may retain BTSC and/or EIP to provide these services. If hired, BTSC and/or EIP wouldbe retained by the District under an agreement separate from Ehlers.

INDEPENDENT AUDITORS

The basic financial statements of the District for the fiscal year ended June 30, 2016, have been audited by Althoffand Nordquist, LLC, Pine City, Minnesota, independent auditors (the "Auditor"). The report of the Auditor, togetherwith the basic financial statements, component units financial statements, and notes to the financial statements areattached hereto as "APPENDIX A – FINANCIAL STATEMENTS". The Auditor has not been engaged to performand has not performed, since the date of its report included herein, any procedures on the financial statementsaddressed in that report. The Auditor also has not performed any procedures relating to this Preliminary OfficialStatement.

RISK FACTORS

Following is a description of possible risks to holders of the Bonds without weighting as to probability. Thisdescription of risks is not intended to be all-inclusive, and there may be other risks not now perceived or listed here.

Taxes: The Bonds are general obligations of the District, the ultimate payment of which rests in the District's abilityto levy and collect sufficient taxes to pay debt service should other revenue (state aids) be insufficient. In the eventof delayed billing, collection or distribution of property taxes, sufficient funds may not be available to the District intime to pay debt service when due.

State Actions: Many elements of local government finance, including the issuance of debt and the levy of propertytaxes, are controlled by state government. Future actions of the state may affect the overall financial condition of theDistrict, the taxable value of property within the District, and the ability of the District to levy and collect propertytaxes.

Future Changes in Law: Various State and federal laws, regulations and constitutional provisions apply to the District and to the Bonds. The District can give no assurance that there will not be a change in or interpretation ofany such applicable laws, regulations and provisions which would have a material effect on the District or the taxingauthority of the District.

Ratings; Interest Rates: In the future, the District's credit rating may be reduced or withdrawn, or interest rates forthis type of obligation may rise generally, either possibility resulting in a reduction in the value of the Bonds for resaleprior to maturity.

8

Tax Exemption: If the federal government or the State of Minnesota taxes all or a portion of the interest onmunicipal obligations, directly or indirectly, or if there is a change in federal or state tax policy, the value of the Bondsmay fall for purposes of resale. Noncompliance following the issuance of the Bonds with certain requirements of theCode and covenants of the bond resolution may result in the inclusion of interest on the Bonds in gross income of therecipient for United States income tax purposes or in taxable net income of individuals, estates or trusts for State ofMinnesota income tax purposes. No provision has been made for redemption of the Bonds, or for an increase in theinterest rate on the Bonds, in the event that interest on the Bonds becomes subject to United States or State ofMinnesota income taxation, retroactive to the date of issuance.

Continuing Disclosure: A failure by the District to comply with the Disclosure Undertaking for continuingdisclosure (see "CONTINUING DISCLOSURE") will not constitute an event of default on the Bonds. Any suchfailure must be reported in accordance with the Rule and must be considered by any broker, dealer, or municipalsecurities dealer before recommending the purchase or sale of the Bonds in the secondary market. Such a failure mayadversely affect the transferability and liquidity of the Bonds and their market price.

State Economy; State Aids: State of Minnesota cash flow problems could affect local governments and possiblyincrease property taxes.

Book-Entry-Only System: The timely credit of payments for principal and interest on the Bonds to the accounts ofthe Beneficial Owners of the Bonds may be delayed due to the customary practices, standing instructions or for otherunknown reasons by DTC participants or indirect participants. Since the notice of redemption or other notices toholders of these obligations will be delivered by the District to DTC only, there may be a delay or failure by DTC,DTC participants or indirect participants to notify the Beneficial Owners of the Bonds.

Economy: A combination of economic, climatic, political or civil disruptions or terrorist actions outside of thecontrol of the District, including loss of major taxpayers or major employers, could affect the local economy and resultin reduced tax collections and/or increased demands upon local government. Real or perceived threats to the financialstability of the District may have an adverse effect on the value of the Bonds in the secondary market.

Secondary Market for the Bonds: No assurance can be given that a secondary market will develop for the purchaseand sale of the Bonds or, if a secondary market exists, that such Bonds can be sold for any particular price. Theunderwriters are not obligated to engage in secondary market trading or to repurchase any of the Bonds at the requestof the owners thereof. Prices of the Bonds as traded in the secondary market are subject to adjustment upward anddownward in response to changes in the credit markets and other prevailing circumstances. No guarantee exists asto the future market value of the Bonds. Such market value could be substantially different from the original purchaseprice.

Bankruptcy: The rights and remedies of the holders may be limited by and are subject to the provisions of federalbankruptcy laws, to other laws, or equitable principles that may affect the enforcement of creditors’ rights, to theexercise of judicial discretion in appropriate cases and to limitations on legal remedies against local governments. The opinion of Bond Counsel to be delivered with respect to the Bonds will be similarly qualified.

9

VALUATIONS

OVERVIEW

All non-exempt property is subject to taxation by local taxing districts. Exempt real property includes Indian lands, public property, andeducational, religious and charitable institutions. Most personal property is exempt from taxation (except investor-owned utility mains,generating plants, etc.).

The valuation of property in Minnesota consists of three elements. (1) The estimated market value is set by city or county assessors. Not lessthan 20% of all real properties are to be appraised by local assessors each year. (2) The taxable market value is the estimated market valueadjusted by all legislative exclusions. (3) The tax capacity (taxable) value of property is determined by class rates set by the State Legislature. The tax capacity rate varies according to the classification of the property. Tax capacity represents a percent of taxable market value.

The property tax rate for a local taxing jurisdiction is determined by dividing the total tax capacity or market value of property within thejurisdiction into the dollars to be raised from the levy. State law determines whether a levy is spread on tax capacity or market value. Majorclassifications and the percentages by which tax capacity is determined are:

Type of Property 2014/15 2015/16 2016/17

Residential homestead1 First $500,000 - 1.00%Over $500,000 - 1.25%

First $500,000 - 1.00%Over $500,000 - 1.25%

First $500,000 - 1.00%Over $500,000 - 1.25%

Agricultural homestead1 First $500,000 HGA - 1.00%Over $500,000 HGA - 1.25%First $1,900,000 - 0.50% 2

Over $1,900,000 - 1.00% 2

First $500,000 HGA - 1.00%Over $500,000 HGA - 1.25%First $2,140,000 - 0.50% 2

Over $2,140,000 - 1.00% 2

First $500,000 HGA - 1.00%Over $500,000 HGA - 1.25%First $2,050,000 - 0.50% 2

Over $2,050,000 - 1.00% 2

Agricultural non-homestead Land - 1.00% 2 Land - 1.00% 2 Land - 1.00% 2

Seasonal recreational residential First $500,000 - 1.00% 3

Over $500,000 - 1.25% 3First $500,000 - 1.00% 3

Over $500,000 - 1.25% 3First $500,000 - 1.00% 3

Over $500,000 - 1.25% 3

Residential non-homestead: 1 unit - 1st $500,000 - 1.00% Over $500,000 - 1.25%2-3 units - 1.25% 4 or more - 1.25%Small City 4 - 1.25%Affordable Rental: First $100,000 - .75% Over $100,000 - .25%

1 unit - 1st $500,000 - 1.00% Over $500,000 - 1.25%2-3 units - 1.25% 4 or more - 1.25%Small City 4 - 1.25%Affordable Rental: First $106,000 - .75% Over $106,000 - .25%

1 unit - 1st $500,000 - 1.00% Over $500,000 - 1.25%2-3 units - 1.25% 4 or more - 1.25%Small City 4 - 1.25%Affordable Rental: First $115,000 - .75% Over $115,000 - .25%

Industrial/Commercial/Utility5 First $150,000 - 1.50%Over $150,000 - 2.00%

First $150,000 - 1.50%Over $150,000 - 2.00%

First $150,000 - 1.50%Over $150,000 - 2.00%

1 A residential property qualifies as "homestead" if it is occupied by the owner or a relative of the owneron the assessment date.

2 Applies to land and buildings. Exempt from referendum market value tax.

3 Exempt from referendum market value tax.

4 Cities of 5,000 population or less and located entirely outside the seven-county metropolitan area and theadjacent nine-county area and whose boundaries are 15 miles or more from the boundaries of a Minnesotacity with a population of over 5,000.

5 The estimated market value of utility property is determined by the Minnesota Department of Revenue.

10

CURRENT PROPERTY VALUATIONS

2016/17 Economic Market Value $758,717,1821

2016/17 Assessor’s Estimated Market Value

Pine County

AitkinCounty

KanabecCounty Total

Real Estate $620,938,300 $ 67,512,400 $ 50,953,000 $739,403,700

Personal Property 9,185,500 1,600 146,300 9,333,400

Total Valuation $630,123,800 $ 67,514,000 $ 51,099,300 $748,737,100

2016/17 Net Tax Capacity

Pine County

AitkinCounty

KanabecCounty Total

Real Estate $ 5,933,628 $ 619,278 $ 389,053 $ 6,941,959

Personal Property 180,422 32 732 181,186

Net Tax Capacity $ 6,114,050 $ 619,310 $ 389,785 $ 7,123,145

Less: Power Line Adjustment2 (4,596) 0 0 (4,596)

Taxable Net Tax Capacity $ 6,109,454 $ 619,310 $ 389,785 $ 7,118,549

1 According to the Minnesota Department of Revenue, the Assessor's Estimated Market Value (the"AEMV") for Independent School District No. 2165 (Hinckley-Finlayson) is about 94.82% of the actualselling prices of property most recently sold in the District. The sales ratio was calculated by comparingthe selling prices with the AEMV. Dividing the AEMV of real estate by the sales ratio and adding theAEMV of personal property and utility, railroads and minerals, if any, results in an Economic MarketValue ("EMV") for the District of $758,717,182.

2 Ten percent of the net tax capacity of certain high voltage transmission lines is removed when settinglocal tax rates. However, taxes are paid on the full value of these lines. The taxes attributable to 10% ofvalue of these lines are used to fund a power line credit. Certain property owners receive a credit whenthe high voltage transmission line runs over their property.

11

2016/17 NET TAX CAPACITY BY CLASSIFICATION

2016/17Net Tax Capacity

Percent of TotalNet Tax Capacity

Residential homestead $ 1,508,522 21.18%

Agricultural 2,045,978 28.72%

Commercial/industrial 1,228,858 17.25%

Public utility 37,498 0.53%

Railroad operating property 94,314 1.32%

Non-homestead residential 763,713 10.72%

Commercial & residential seasonal/rec. 1,263,076 17.73%

Personal property 181,186 2.54%

Total $ 7,123,145 100.00%

TREND OF VALUATIONS

LevyYear

Assessor'sEstimated

Market Value

Assessor'sTaxable

Market ValueNet Tax

Capacity1

TaxableNet Tax

Capacity2

Percent +/- inEstimated

Market Value

2012/13 $ 724,570,300 $ 655,353,450 $ 6,726,830 $ 6,515,966 - 10.13%

2013/14 696,774,100 633,285,400 6,534,235 6,323,516 - 3.84%

2014/15 700,356,500 638,678,500 6,571,329 6,566,878 + 0.51%

2015/16 717,045,600 655,551,750 6,763,653 6,759,228 + 2.38%

2016/17 748,737,100 688,577,285 7,123,145 7,118,549 + 4.42%

1 Net Tax Capacity includes power line values.

2 Taxable Net Tax Capacity does not power line values.

12

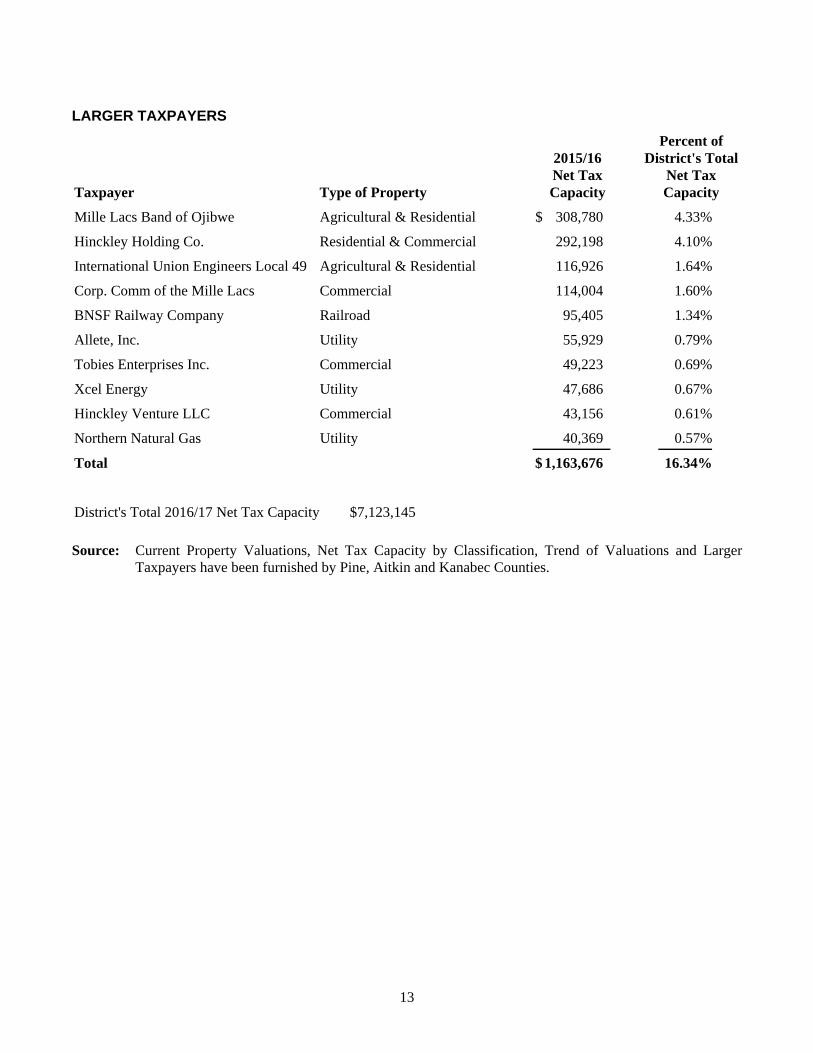

LARGER TAXPAYERS

Taxpayer Type of Property

2015/16Net TaxCapacity

Percent ofDistrict's Total

Net TaxCapacity

Mille Lacs Band of Ojibwe Agricultural & Residential $ 308,780 4.33%

Hinckley Holding Co. Residential & Commercial 292,198 4.10%

International Union Engineers Local 49 Agricultural & Residential 116,926 1.64%

Corp. Comm of the Mille Lacs Commercial 114,004 1.60%

BNSF Railway Company Railroad 95,405 1.34%

Allete, Inc. Utility 55,929 0.79%

Tobies Enterprises Inc. Commercial 49,223 0.69%

Xcel Energy Utility 47,686 0.67%

Hinckley Venture LLC Commercial 43,156 0.61%

Northern Natural Gas Utility 40,369 0.57%

Total $ 1,163,676 16.34%

District's Total 2016/17 Net Tax Capacity $7,123,145

Source: Current Property Valuations, Net Tax Capacity by Classification, Trend of Valuations and LargerTaxpayers have been furnished by Pine, Aitkin and Kanabec Counties.

13

DEBT

DIRECT DEBT1

General Obligation Debt (see schedule following)

Total g.o. debt being paid from taxes and state aids2 (includes the Bonds)* $ 10,930,000

*Preliminary, subject to change.

STATE AID FOR DEBT SERVICE

The Minnesota Debt Service Equalization program provides state aid to finance a portion of the principal and interestpayments on most school district bonds. Bonds not eligible for the program include all alternative facilities bonds,facilities maintenance bonds, capital facilities bonds and OPEB bonds, as well as building bonds with relatively shortmaturities.

Under the Debt Service Equalization Formula (the Formula) adopted by the 2001 Minnesota State Legislature, eachschool district is responsible for the amount of its qualifying annual debt service which is equal to 15.74% of itsAdjusted Net Tax Capacity (ANTC). The District does not currently qualify for debt service equalization aid.

In addition to debt service equalization aid, some school districts will qualify for state Long Term FacilitiesMaintenance Aid to finance a portion of the payments on Alternative Facilities Bonds and Facilities MaintenanceBonds, pursuant to the Long Term Facilities Maintenance Revenue (LTFMR) program approved by the State in 2015. If any aid is received, it is deposited into the District's debt service fund and must be used for payments on the bonds;any payment of state aid into the debt service fund causes a reduction in the tax levy for Alternative Facilities Bondsand Facilities Maintenance Bonds. The amount of aid received in the debt service fund will vary each year, dependingon a number of factors. Although the District expects to receive some Long Term Facilities Maintenance Aid in itsdebt service fund, Ehlers has not attempted to estimate the portion of debt service payments that would be financedby state aid.

1 Outstanding debt is as of the dated date of the Bonds.

2 Based upon the debt service equalization formula and current statistics, the District anticipates a portionof this debt will be paid by the State of Minnesota.

14

IND

EP

EN

DE

NT

SC

HO

OL

DIS

TR

ICT

NO

. 216

5 (H

INC

KL

EY

-FIN

LA

YS

ON

), M

INN

ES

OT

AS

ched

ule

of

Bo

nd

ed In

deb

ted

nes

sG

ener

al O

blig

atio

n D

ebt

Bei

ng

Pai

d F

rom

Tax

es(a

s o

f 12

/6/1

7)F

ISC

AL

YE

AR

BA

SIS

Dat

edA

mo

un

t

Mat

uri

ty

Fis

cal Y

ear

Est

imat

edT

ota

lT

ota

lT

ota

lP

rin

cip

alF

isca

l Yea

rE

nd

ing

Pri

nci

pal

Inte

rest

Pri

nci

pal

Inte

rest

Pri

nci

pal

Inte

rest

Pri

nci

pal

Inte

rest

Pri

nci

pal

Inte

rest

P &

IO

uts

tan

din

g%

Pai

dE

nd

ing

2018

565,

000

273,

423

010

9,30

021

5,00

044

,724

078

0,00

042

7,44

61,

207,

446

10,1

50,0

007.

14%

2018

2019

635,

000

109,

300

50,0

0042

,515

135,

000

106,

690

820,

000

258,

505

1,07

8,50

59,

330,

000

14.6

4%20

1920

2064

5,00

096

,600

50,0

0041

,865

155,

000

88,5

0085

0,00

022

6,96

51,

076,

965

8,48

0,00

022

.42%

2020

2021

655,

000

83,7

0055

,000

41,2

1515

5,00

083

,850

865,

000

208,

765

1,07

3,76

57,

615,

000

30.3

3%20

2120

2267

0,00

070

,600

55,0

0040

,335

160,

000

79,2

0088

5,00

019

0,13

51,

075,

135

6,73

0,00

038

.43%

2022

2023

690,

000

57,2

0055

,000

39,4

5516

5,00

074

,400

910,

000

171,

055

1,08

1,05

55,

820,

000

46.7

5%20

2320

2471

0,00

043

,400

55,0

0038

,410

175,

000

69,4

5094

0,00

015

1,26

01,

091,

260

4,88

0,00

055

.35%

2024

2025

725,

000

29,2

0055

,000

37,3

6518

0,00

064

,200

960,

000

130,

765

1,09

0,76

53,

920,

000

64.1

4%20

2520

2673

5,00

014

,700

60,0

0036

,210

185,

000

58,8

0098

0,00

010

9,71

01,

089,

710

2,94

0,00

073

.10%

2026

2027

565,

000

34,9

5019

0,00

053

,250

755,

000

88,2

0084

3,20

02,

185,

000

80.0

1%20

2720

2860

0,00

018

,000

195,

000

47,5

5079

5,00

065

,550

860,

550

1,39

0,00

087

.28%

2028

2029

260,

000

41,7

0026

0,00

041

,700

301,

700

1,13

0,00

089

.66%

2029

2030

270,

000

33,9

0027

0,00

033

,900

303,

900

860,

000

92.1

3%20

3020

3128

0,00

025

,800

280,

000

25,8

0030

5,80

058

0,00

094

.69%

2031

2032

285,

000

17,4

0028

5,00

017

,400

302,

400

295,

000

97.3

0%20

3220

3329

5,00

08,

850

295,

000

8,85

030

3,85

00

100.

00%

2033

565,

000

273,

423

5,46

5,00

061

4,00

01,

815,

000

415,

044

3,08

5,00

085

3,54

010

,930

,000

2,02

8,35

611

,568

,356

*Pre

limin

ary,

sub

ject

to c

hang

e.

1)

Fac

iliti

es M

ain

ten

ance

Ser

ies

2017

B

12/6

/201

7$3

,085

,000

*

2/01

Alt

. Fac

iliti

es

$6,9

75,0

00

Ser

ies

2009

AR

efu

nd

ing

1)

Fac

iliti

es M

ain

ten

ance

Ser

ies

2017

AS

erie

s 20

16A

2/9/

2017

$1,8

15,0

005/

5/20

16$5

,465

,000

2/01

1/08

/09

2/01

2/01

Th

isis

sue

re

fun

de

d th

e 2

01

9 th

rou

gh

20

26

ma

turit

ies

of t

he

Dis

tric

t's $

6,9

75

,00

0 G

en

era

l Ob

liga

tion

Alte

rna

tive

Fa

cilit

ies

Bo

nd

s,S

erie

s 2

00

9A

, da

ted

Ja

nu

ary

8,

20

09

. T

he

se m

atu

ritie

s w

ill b

e c

alle

d f

or

prio

r re

de

mp

tion

on

Fe

bru

ary

1, 2

01

8, a

nd

ha

ve n

ot b

ee

n in

clu

de

d in

th

e c

alc

ula

tion

of

de

bt r

atio

s. T

he

Dis

tric

t is

re

spo

nsi

ble

for

pa

yin

g th

e d

eb

t se

rvic

e o

n th

e r

efu

nd

ed

ma

turit

ies

thro

ug

h F

eb

rua

ry 1

, 20

18

(th

e "

Ca

ll D

ate

").

Th

e e

scro

w a

cco

un

t is

resp

on

sib

le fo

r th

e p

aym

en

t of

de

bt s

erv

ice

on

the

re

fun

din

g b

on

ds

thro

ug

h th

e C

all

Da

te; t

he

rea

fter,

the

Dis

tric

t w

ill b

e r

esp

on

sib

le fo

r th

e p

aym

en

t of

de

bt s

erv

ice

. Th

e r

efu

nd

ed

ma

turit

ies

ha

ve n

ot b

ee

n in

clu

de

d in

th

e

calc

ula

tion

of d

eb

t ra

tios.

Pre

pare

d by

Ehl

ers

GO

Tax

es

15

BONDED DEBT LIMIT

Minnesota Statutes, Section 475.53, subdivision 4, presently limits the "net debt" of a school district to 15% of itsactual market value. The actual market value of property within a district, on which its debt limit is based, is (a) thevalue certified by the county auditors, or (b) this value divided by the ratio certified by the commissioner of revenue,whichever results in a higher value. The current debt limit of the District is computed as follows:

2016/17 Economic Market Value $758,717,182

Multiply by 15% 0.15

Statutory Debt Limit $113,807,577

Less: Long-Term Debt Outstanding Being Paid Solely from Taxes (includes the Bonds)* (10,930,000)

Unused Debt Limit* $102,877,577

*Preliminary, subject to change.

OVERLAPPING DEBT1

Taxing District

2016/17Taxable Net

Tax Capacity% In

District Total

G.O. Debt2

District'sProportionate

Share

Pine County $25,499,313 23.9593% $27,350,000 $ 6,552,869

Kanabec County 10,793,515 3.6113% 9,735,822 351,590

City of Hinckley 556,019 100.0000% 2,320,000 2,320,000

District's Share of Total Overlapping Debt $ 9,224,458

DEBT PAYMENT HISTORY

The District has no record of default in the payment of principal and interest on its debt.

1 Overlapping debt is as of the dated date of the Bonds. Only those taxing jurisdictions with generalobligation debt outstanding are included in this section. It does not include non-general obligation debt,self-supporting general obligation revenue debt, short-term general obligation debt, or general obligationtax/aid anticipation certificates of indebtedness.

2 Outstanding debt is based on information in official statements obtained on EMMA and the MunicipalAdvisor's records.

16

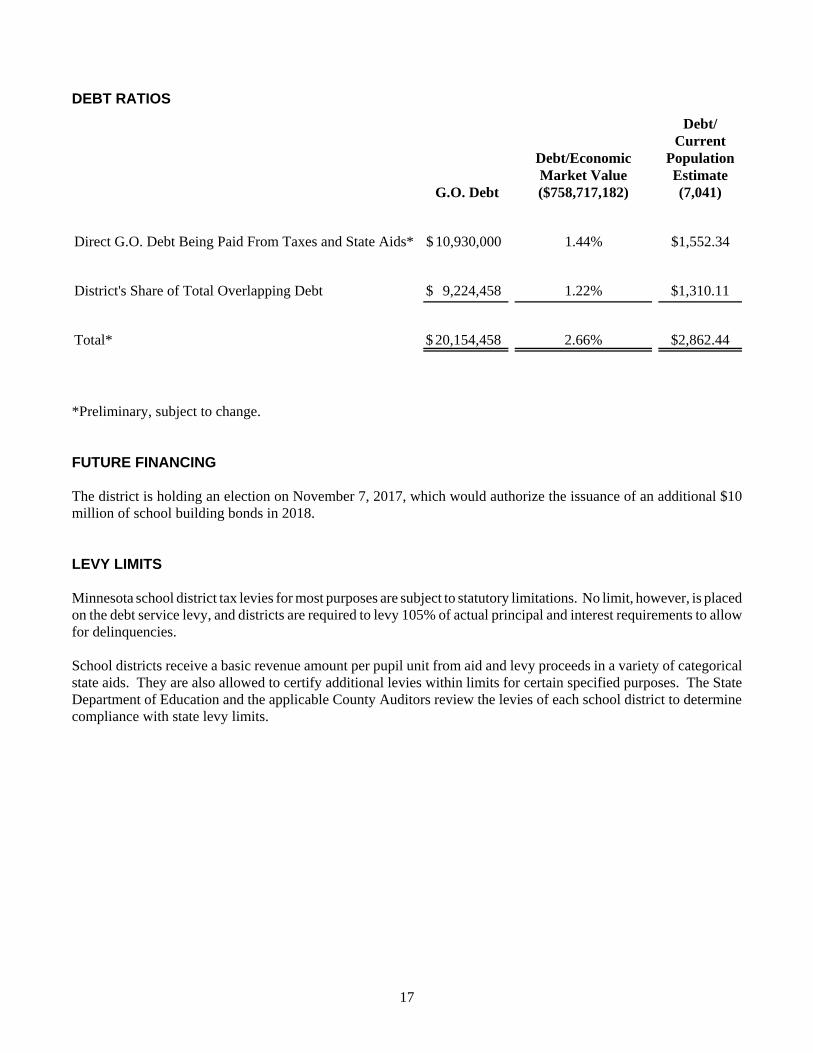

DEBT RATIOS

G.O. Debt

Debt/EconomicMarket Value($758,717,182)

Debt/Current

PopulationEstimate(7,041)

Direct G.O. Debt Being Paid From Taxes and State Aids* $ 10,930,000 1.44% $1,552.34

District's Share of Total Overlapping Debt $ 9,224,458 1.22% $1,310.11

Total* $ 20,154,458 2.66% $2,862.44

*Preliminary, subject to change.

FUTURE FINANCING

The district is holding an election on November 7, 2017, which would authorize the issuance of an additional $10million of school building bonds in 2018.

LEVY LIMITS

Minnesota school district tax levies for most purposes are subject to statutory limitations. No limit, however, is placedon the debt service levy, and districts are required to levy 105% of actual principal and interest requirements to allowfor delinquencies.

School districts receive a basic revenue amount per pupil unit from aid and levy proceeds in a variety of categoricalstate aids. They are also allowed to certify additional levies within limits for certain specified purposes. The StateDepartment of Education and the applicable County Auditors review the levies of each school district to determinecompliance with state levy limits.

17

TAX RATES, LEVIES AND COLLECTIONS

TAX LEVIES AND COLLECTIONS

Tax YearNet Tax

Levy1Total CollectedFollowing Year

Collectedto Date2 % Collected

2012/13 $ 1,505,057 $ 1,422,281 $ 1,495,662 99.38%

2013/14 1,463,976 1,380,959 1,451,860 99.17%

2014/15 1,603,252 1,526,391 1,580,691 98.59%

2015/16 1,780,007 1,728,385 1,758,253 98.78%

2016/17 1,997,004 In process of collection

Property taxes are collected in two installments in Minnesota--the first by May 15 and the second by October 15.3 Mobile home taxes are collectible in full by August 31. Minnesota Statutes require that levies (taxes and specialassessments) for debt service be at least 105% of the actual debt service requirements to allow for delinquencies.

1 This reflects the Final Levy Certification of the District after all adjustments have been made.

2 Collections are through May 31, 2017 for Pine County, September 12, 2017 for Aitkin County, and May20, 2017 for Kanabec County.

3 Second half tax payments on agricultural property are due on November 15th of each year.

18

TAX CAPACITY RATES1

2012/13 2013/14 2014/15 2015/16 2016/17

I.S.D. No. 2165 (Hinckley-Finlayson) 17.910% 19.829% 17.543% 19.011% 20.825%

Pine County 60.426% 63.275% 64.579% 66.457% 66.586%

Aitkin County 41.242% 42.908% 44.534% 46.147% 46.849%

Kanabec County 103.078% 111.355% 104.869% 100.155% 100.815%

City of Hinckley 41.141% 41.892% 43.421% 43.587% 20.143%

City of Finlayson 70.391% 64.795% 61.678% 61.828% 19.699%

City of Brook Park 33.658% 34.467% 34.465% 35.719% 29.100%

Town of Sandstone2 12.521% 12.842% 15.455% 15.293% 14.396%

North Pine Hospital District 3.127% 3.205% 3.061% 2.867% 2.681%

Regional Development 0.169% 0.179% 0.180% 0.179% 0.176%

Referendum Market Value Rates:

I.S.D. No. 2165 (Hinckley-Finlayson) 0.09678% 0.06521% 0.13261% 0.13988% 0.13588%

Kanabec County 0.02373% 0.02573% 0.02424% 0.02273% 0.02236%

Source: Tax Levies and Collections and Tax Capacity Rates have been furnished by Pine, Aitkin and KanabecCounties.

1 After reduction for state aids. Does not include the statewide general property tax againstcommercial/industrial, non-homestead resorts and seasonal recreational residential property.

2 Representative town rate.

19

THE ISSUER

EMPLOYEES

The District is governed by an elected school board and employs a staff of 170, including 83 non-licensed employeesand 87 licensed employees (80 of whom are teachers). The District provides education for 975 students in gradeskindergarten through twelve.

PENSIONS; UNIONS

Teachers’ Retirement Association (TRA)

All teachers employed by the District are covered by defined benefit pension plans administered by the State ofMinnesota Teachers Retirement Association (TRA). TRA members belong to either the Coordinated Plan or the BasicPlan. Coordinated members are covered by Social Security and Basic members are not. All new members mustparticipate in the Coordinated Plan. These plans are established and administered in accordance with MinnesotaStatutes, Chapter 354 and 356.

Public Employees’ Retirement Association (PERA)

All full-time and certain part-time employees of the District (other than those covered by TRA) are covered by adefined benefit plan administered by the Public Employees’ Retirement Association of Minnesota (PERA). PERAadministers the General Employees Retirement Fund (GERF) which is a cost-sharing, multiple-employer retirementplan. This plan is established and administered in accordance with Minnesota Statutes, Chapters 353 and 356.

Recognized and Certified Bargaining Units

Bargaining UnitExpiration Date of Current Contract

Hinckley-Finlayson Education Association June 30, 2017

Status of Contracts

The contract which expired on June 30, 2017 is currently in negotiations.

POST EMPLOYMENT BENEFITS

The District has obligations for some post-employment benefits for its employees. Accounting for these obligationsis dictated by Governmental Accounting Standards Board Statement No. 45 (GASB 45). The District's most recentactuarial study of its OPEB obligations shows an actuarial accrued liability of $1,905,155 as of July 1, 2016. TheDistrict has been funding these obligations on a pay-as-you-go basis, but will fund future benefit payments/employercontributions from an irrevocable trust. The trust value is $589,466 as of July 1, 2016.

20

STUDENT BODY

The number of students enrolled for the past four years and for the current year have been as follows:

Year Kindergarten Grades 1-6 Grades 7-12 Total

2012/13 82 459 419 960

2013/14 68 473 422 963

2014/15 73 466 416 955

2015/16 75 474 428 977

2016/17 65 493 417 975

Enrollments for the next three years are projected to be as follows:

Year Kindergarten Grades 1-6 Grades 7-12 Total

2017/18 67 491 423 981

2018/19 70 488 428 986

2019/20 67 487 426 980

SCHOOL BUILDINGS

School BuildingYear

ConstructedYears of Additions/

Remodelings

Finlayson Elementary 1980 1997

Hinckley Elementary 1956 1965, 1985, 1990, 1990

Hinckley-Finlayson High School 1941 1970, 1978, 1990, 1997

FUNDS ON HAND (as of June 30, 2017)

FundTotal Cash

and Investments

General $ 3,705,556

Community Service 1,252

Debt Service 700,713

Escrow Account 5,577,623

Building/Construction 1,633,640

Trust & Agency 801,657

OPEB Trust 589,465

Total Funds on Hand $13,009,906

21

LITIGATION

There is no litigation threatened or pending questioning the organization or boundaries of the District or the right ofany of its officers to their respective offices or in any manner questioning their rights and power to execute and deliverthe Bonds or otherwise questioning the validity of the Bonds.

MUNICIPAL BANKRUPTCY

Municipalities are prohibited from filing for bankruptcy under Chapter 11 (reorganization) or Chapter 7 (liquidation)of the U.S. Bankruptcy Code (11 U.S.C. §§ 101-1532) (the "Bankruptcy Code"). Instead, the Bankruptcy Codepermits municipalities to file a petition under Chapter 9 of the Bankruptcy Code, but only if certain requirements aremet. These requirements include that the municipality must be "specifically authorized" under State law to file forrelief under Chapter 9. For these purposes, "State law" may include, without limitation, statutes of generalapplicability enacted by the State legislature, special legislation applicable to a particular municipality, and/orexecutive orders issued by an appropriate officer of the State’s executive branch.

Currently there is no statutory authority for Minnesota school districts to file for bankruptcy relief under Chapter 9of the Bankruptcy Code.

Nevertheless, there can be no assurance (a) that State law will not change in the future while the Bonds areoutstanding; or (b) even absent such a change in State law, that an executive order or other executive action could noteffectively authorize the District to file for relief under Chapter 9; or (c) whether it would still be eligible for voluntaryor involuntary relief under Chapters of the Bankruptcy Code other than Chapter 9 or under similar federal or state lawor equitable proceeding regarding insolvency or providing for protection from creditors. Such action could impactthe rights of holders of the Bonds. Such modifications could be adverse to holders of the Bonds and there couldultimately be no assurance that holders of the Bonds would be paid in full or in part on the Bonds.

22

SUMMARY GENERAL FUND INFORMATION

Following are summaries of the revenues and expenditures and fund balances for the District's General Fund. These summariesare not purported to be the complete audited financial statements of the District, and potential purchasers should read the includedfinancial statements in their entirety for more complete information concerning the District. Copies of the complete statementsare available upon request. Appendix A includes the District’s 2016 audited financial statements.

FISCAL YEAR ENDING JUNE 30

COMBINED STATEMENT2014

Audited2015

Audited2016

Audited2017

Unaudited1

2017-18AdoptedBudget2

RevenuesLocal property taxes $ 652,168 $ 654,789 $ 1,072,654 $ 935,265 $ 990,119Other local and county revenues 275,388 281,780 728,789 19,000 183,500Revenues from state sources 8,542,199 8,711,875 9,293,705 9,755,446 9,775,458Revenues from federal sources 489,613 477,506 490,473 492,710 489,157

Insurance recovery and other 0 0 17,545 0 0Sales and other conversion of assets 53,728 23,983 20,119 815,010 30,000

Total Revenues $ 10,013,096 $ 10,149,933 $ 11,623,285 $ 12,017,431 $ 11,468,234

ExpendituresAdministration $ 599,972 $ 602,709 $ 614,938 $ 622,285 $ 690,903District support services 216,154 171,186 208,417 209,514 607,170Elementary & secondary regular instruction 4,904,164 4,969,479 5,422,069 5,499,463 5,128,105Vocational education instruction 268,117 261,579 261,094 245,454 189,140Special education instruction 1,899,165 2,012,363 2,100,490 2,383,300 2,163,597Instructional support services 495,266 384,742 301,617 348,563 439,004Pupil support services 798,491 958,515 1,077,780 892,664 995,654Sites and buildings 1,039,574 963,287 1,024,228 1,237,114 1,167,111Fiscal and other fixed cost programs 44,908 48,831 47,121 0 0

Total Expenditures $ 10,265,811 $ 10,372,691 $ 11,057,754 $ 11,438,357 $ 11,380,684

Excess of revenues over (under) expenditures $ (252,715) $ (222,758) $ 565,531 $ 579,074 $ 87,550

Other Financing Sources (Uses)Loan Proceeds $ 194,377 $ 0 $ 196,100Operating transfers out (104,878) (58,795) (56,420)

Total Other Financing Sources (Uses) $ 89,499 $ (58,795) $ 139,680

Net Change in Fund Balances $ (163,216) $ (281,553) $ 705,211

General Fund Balance July 1 3,127,680 2,964,464 2,682,911Prior Period Adjustment 0 0 0Residual Equity Transfer in (out) 0 0 0

General Fund Balance June 30 $ 2,964,464 $ 2,682,911 $ 3,388,122