income recognition, asset classification , provisioning ... · income recognition, asset...

TRANSCRIPT

ANDHRA PRAGATHI GRAMEENA BANK

HEAD OFFICE :::: KADAPA Cir.No 54-2008-BC-CST Dt:12-03-2008

INCOME RECOGNITION, ASSET CLASSIFICATION , PROVISIONING &

COMPILATION OF YEAR-END RETURNS AS ON 31.03.2008

-oOo-

The prudential norms applicable as on 31-03-2008 and necessary guidelines are furnished hereunder. Branches are required to conduct the exercise of asset classification, interest reversal and computation of provision requirement for all borrowal accounts accordingly and compile the Year End Returns pertaining to advances as on 31-03-2008 for the purpose of audit and annual closing of accounts. Branches are advised to strictly adhere to the norms and there shall not be any deviations. 1.00. ASSET CLASSIFICATION & INCOME RECOGNITION Branches shall classify all borrowal accounts into Performing (Standard) Assets and

Non Performing (Sub-standard, Doubtful & Loss ) assets as per delinquency norms. The norms and guidelines are furnished below. The availability of security or net worth of the borrower/guarantor should not be taken into account for the purpose of treating an advance as NPA or otherwise, as income recognition is to be based on record of recovery only.

1.01. A non-performing asset (NPA) is defined as a loan/advance where-

i) Interest and/or instalment of principal remains overdue for a period more than 90

days in respect of a term loan, ii) The account remains „out of order‟ for 90 days in respect of an Overdraft/Cash Credit

(OD/CC),

iii) The bill remains overdue for a period of more than 90 days in the case of bills purchased and discounted. iv) A loan granted for short duration crops will be treated as NPA, if the instalment of principal or interest thereon remains overdue for two crop seasons. v) A loan granted for long duration crops will be treated as NPA if the instalment of principal or interest thereon remains overdue for one crop season, vi) Any amount to be received remains overdue for a period of more than 90 days in respect of other accounts.

(..2)

Cir.No 54-2008-BC-CST Dt:12-03-2008

-2-

1.02. For the purpose of above norms, “long duration” Crops would be crops with crop

season longer than 1 year and crops which are not “long duration” crops would be treated as “Short duration” crops. The Crop season for each crop, which means the

period upto harvesting of the crops raised, would be as determined by the “State Level Bankers” Committee/District Level Technical Committee. Depending upon the duration of crops raised by an agriculturist, the above NPA norms would also be made applicable to agricultural term loans availed by him. In the light of the above, the crop loans disbursed for cultivation of Banana, Papaya, Sugarcane etc., and crop loans disbursed for maintenance of Horticultural/Plantation crops like Citrus, Mango etc., which are repayable not beyond one year shall also be treated as crop loans extended for short duration crops.

1.03.The norms 1.01 (iv & v) are applicable to all direct agricultural advances listed in

Annexure-1.

In respect of agricultural loans other than those specified in Annexure-1 i.e. loans

for allied activities viz. Dairy, Poultry, Sericulture, animal Husbandry etc, and term loans given to non-agriculturists, identification of NPAs shall be done on the same basis as non-agriculture advances i.e. 90 day delinquency norm.

1.04. „Out of order‟: An account should be treated as „out of order‟, if the outstanding

balance remains continuously in excess of the sanctioned limit/drawing power. In cases where the outstanding balance in the principal operating account is less than the sanctioned limit/drawing power, but there are no credits continuously for 90 days as on the date of Balance sheet (31st March) or credits are not enough to cover the interest debited during the same period, these accounts should be treated as „out of order‟ (from the beginning of 90 days and hence the account becomes NPA on 90th day).

1.05. „Overdue‟: Any amount due to the bank under any credit facility is „overdue‟ if it is

not paid on the due date fixed by the Bank 1.06. Other parameters to treat an Overdraft (OD)/Cash Credit (CC) accounts as NPAs: 1.06.1.Non submission of stock statement:

The outstanding in the cash credit /overdraft account based on drawing power calculated from stock statements older than three months would be deemed as irregular. A cash credit/ overdraft account will become NPA if such irregular drawings are permitted in the account for a continuous period of 90 days even though the unit may be working or the borrowers financial position is satisfactory

Ex: Drawals permitted during November against drawing power based on stock statement as on 31st July or before are irregular. Drawals permitted during December against drawing power based on stock statement as on 31st August or before are irregular. If such irregular drawals are permitted in an account continuously for 90 days, the account becomes NPA on 90th day. In the above case, if drawals are permitted during November based on stock statement as on 31st July or before, during December based on stock statement as on 31st August or before and during January based on stock statement as on 30th September or before, the account will slip to NPA on 29th January.

(..3)

Cir.No 54-2008-BC-CST Dt:12-03-2008

-3- 1.06.2.Non renewal/review of Credit limits:

Regular and adhoc credit limits need to be reviewed/regularised not later than three months from the due date/date of adhoc sanction. In case of constraints such as non-availability of financial statements and other data from the borrowers, the branch should furnish evidence to show that renewal/review of credit limit is already on and would be completed soon. In any case, delay beyond six months is not considered desirable as a general discipline. Hence an account, where the regular/adhoc credit limits have not been reviewed/renewed within 180 days (not 90 days) from the due date/date of adhoc sanction shall be treated as NPA.

Ex.1: If a regular OD limit, the validity of which has expired on 31st July, is not renewed or reviewed upto 26th January, it will slip to NPA on 26th January. Ex.2: If adhoc sanction given on 31st July is not renewed or reviewed upto 26th January, it will slip to NPA on 26th January.

1.07.Advances, which need not be classified as NPA: 1.07.1.Advances against Term Deposits, NSC, KVP/IVP etc::

Advances against Term Deposits, NSC, and KVP/IVP etc inclusive of accrued interest if any, NSCs eligible for surrender, Indira Vikas Patras, Kisan Vikas Patras and SV (Surrender Value) of life insurance policies shall not be treated as NPAs. Such securities are exempt from provision requirement to the extent so covered by such securities and hence they shall be classified as „Standard‟ assets only. Advances against gold ornaments, government securities and all other securities are not covered by this exemption. These are to be classified as per the normal procedure applicable to other loans.

1.08. Explanation with examples: 1.08.1. Loans repayable in installments:

a). A loan repayable in instalments becomes NPA when interest and /or instalments of principal remain overdue for a period of more than 90 days. Therefore 91st day from the due date of earliest unpaid interest or installment of principal is the date of NPA.

Illustrations:

i). If interest due for the month ended 30th September is not paid, it becomes NPA on 29th December. ii) If interest due for the month ended 31st October is not paid, it becomes NPA on 29h January . iii). If instalment towards principal due on 15th October is not paid, it becomes NPA on 13th January.

(..4)

Cir.No 54-2008-BC-CST Dt:12-03-2008

-4-

b). Branches shall recover monthly interest on the due dates i.e. last day of the month. However, for the purpose of asset classification, interest debited at the end of a month, other than quarter ending month, shall be deemed as overdue on the last day of the quarter only. In other words, if interest debited to an account at the end of January, February, April, May, July, August, October and November is not paid, the same shall be deemed as overdue from the end of the quarter, for the purpose of asset classification and the account shall be classified as NPA if the interest is not paid within 90 days from the end of the quarter. Illustration: If interest due on 31.10.2007 is not paid, it becomes NPA on 30.03.2008 (interest is deemed to be overdue on 31.12.2007 and becomes NPA after 90 days i.e. on 30.03.2008).

1.09. Special cases: 1.09.1. Equated monthly instalments: In the case of loans repayable in equated monthly

instalments where a part of the interest is included in the instalment, NPA status shall be determined on the basis of non payment of equated monthly instalments and not with reference to the date of debit of monthly interest.

1.09.2. Education Loans: As per the scheme guidelines prescribed by the Government of

India, the repayment is to be made in 5-7 years after the completion of course period + one year or six months after getting the job whichever is earlier. Interest is also payable along with the instalment. Hence the Education loans shall be treated as NPAs if the same is overdue for more than 90 days from the due date as explained above.

1.09.3. Staff Housing/Vehicle Loans: In the case of housing /vehicle loan or similar advances granted to staff members where interest is payable after recovery of principal, interest need not be considered as overdue from the first month onwards. Such loans/advances should be classified as NPA only when there is a default in repayment of installment of principal or payment of interest on the respective due dates.

1.09.4. Advance Payments : Where the borrower has made advance payment of instalments fixed towards the loan and as on 31.03.2008 the loan account is regular such loan account need not be treated as NPA even if technically interest is due for more than 90 days.

1.10. Overdraft/Cash Credit:

1.10.1.An Overdraft/Cash Credit account shall be treated as NPA, if it remains „out of order‟

for 90 days. Balance in BG Paid account, if any, shall be added notionally to OD/CC/Current Account and the sum shall be compared with sanction limit/drawing power, whichever is less, to determine whether the balance outstanding was in excess of sanctioned limit/drawing power.

(..5)

Cir.No 54-2008-BC-CST Dt:12-03-2008

-5-

Eg .1. If liability under Overdraft/Cash Credit (after notionally adding devolved Liability

Under BG paid account) remains continuously in excess of sanctioned limit or drawing power, whichever is less, on all days during the period 1.11.07 to 29.01.08 , it becomes NPA on 29.01.08 (i.e. continuously overdrawn for 90 days).

Eg.2. If Current account (after notionally debiting devolved liability under BG paid Account) is continuously in debit balance on all days during the period 1.11.07 to 29.01.08, it becomes NPA on 29.01.08. (i.e. continuously overdrawn for 90 days).

1.10.2. in cases where the outstanding balance in the principal operating account i.e.

OD/CC account is less than the sanctioned limit or drawing power, whichever is less, but there are no credits continuously for 90 days as on the date of balance sheet or credits are not enough to cover the interest debited during the same period , these accounts should be treated as „out of order‟, from the beginning i.e. 1st Jan. In other words, the account shall be treated as out or order for 90 days as on 31st March and hence slips to NPA on the date of Balance Sheet i.e. 31st March. Eg.1. If an Overdraft/Cash Credit account is within limit and drawing power but there are no credits continuously (from 2nd January to 31st March in the case of leap years and 1st January to 31st March in case of other years), the account becomes NPA on 31st March (i.e. no credits continuously for 90 days). Eg.2. If an overdraft/cash credit account is within limit and drawing power but the credits received during the period (from 2nd January to 31st March in case of leap years and 1st January to 31st January to 31st March in the case of other years i.e. interest debited during the period is not covered by credits received during the period) the account becomes NPA on 31st March.

1.10.3. The outstanding in an account based on drawing power calculated from stock

statements older than 3 months would be deemed as irregular. An OD/CC account will become NPA if such irregular drawings permitted in the account for a continuous period of 90 days.

Eg. Drawals permitted during November against drawing power based on stock statement as on 31st July or before are irregular. Drawals permitted during December against drawing power based on stock statement as on 31st August or before are irregular. If such irregular drawals are permitted in an account continuously for 90 days, the account becomes NPA on 90 th day. In the above case, if drawals are permitted during November based on stock statement on 31st July or before, during December based on stock statement as on 31st August or before and during January based on stock statement as on 30th September or before and during January based on stock statement as on 30th September or before, the account will slip to NPA on 29th January.

1.10.4. An account where the regular/adhoc Credit limits have not been reviewed/renewed within 180 days (not 90 days) from the due date/date of adhoc

sanction shall be treated as NPA. (..6)

Cir.No 54-2008-BC-CST Dt:12-03-2008 -6-

Eg.1: If a regular OD limit, the validity of which has expired on 31.07.07, is not renewed or reviewed up to 26.01.08, it will slip to NPA on 26.01.08. Eg.2: If ad-hoc sanction given on 31.07.07 is not renewed/reviewed upto 26.01.08, it will slip to NPA on 26.01.08.

1.11. Bills Purchased/Discounted: A Bill purchased/discounted shall be treated as NPA, if it remains overdue for a period of more than 90 days. Eg: A cheque discounted (CDD) on 25.10.07 becomes due for payment on 31.10.07 (expected to be realized within 7 days). It becomes NPA on 29.01.08 (i.e. more than 90 days from the due date0) if it remains unpaid.

1.12. Agricultural loans-Pragathi Kisan Credit Card: PKCC facility being in the nature of advance for agricultural purposes, the prudential norms as applicable to Agricultural advances would apply to PKCC accounts.

1.13. Other accounts:

Any other credit facility shall be treated as NPA if any amount to be received remains overdue for a period more than 90 days. The type of accounts which fall under “ other accounts” are Bank Guarantee (BGF) Paid, Debit balance in SB account including debit balance occurred in SB/CA on account of debit of bills under credit card, JL where installment is not stipulated, etc. (JL where installment is fixed should be treated as loan and not as “other accounts”).

1.14. General Guidelines: 1.14.1. Accounts where there is erosion in the value of security/frauds committed by

Borrowers: i). In respect of account where there are potential threats for recovery on account

of erosion in the value of security or non-availability of security and existence of other factors such as frauds committed by borrowers, it will not be prudent that such accounts should go through various stages of asset classification, In cases of such serious credit impairment, the asset should be straightaway classified as doubtful or loss asset as appropriate.

ii). Branches shall classify accounts, where fraud has been identified, as loss asset and recommend provision accordingly.

iii). Erosion in the value of security can be reckoned as significant when the realizable value of the security is less than 50 percent of the value assessed by the

bank/approved valuers/NABARD at the time of last inspection, as the case may be. Such NPAs may be straightaway classified under doubtful category and

provisioning should be made as applicable to doubtful assets. (..7)

Cir.No 54-2008-BC-CST Dt:12-03-2008

-7- iv). If the realizable value of the security, as assessed by the bank/approved

valuers/NABARD at the time of last inspection, is less than 10 percent of the

outstanding in the borrowal accounts, the existence of security should be ignored and the asset should be straightaway classified as loss asset.

1.14.2.Asset classification to be borrower-wise and not facility-wise:

It is difficult envisage a situation when only one facility to a borrower/one investment in any of the securities issued by the borrower becomes a problem credit/investment and not others. Therefore, all the facilities granted by the Bank to a borrower and investment in all the securities issued by the borrower will have to be treated as NPA and not the particular facility/investment or part thereof which has become irregular. Eg: If one facility of a borrower/one investment in any of the securities issued by the borrower is „Standard asset‟, the second is a „Sub-standard‟ and the third is „Doubtful above 3 years‟, then all the facilities/investments shall be classified as „Doubtful above 3 years‟. However, if one account of a borrower is „Doubtful above three years‟ and the second account is a „loss asset‟, then both the accounts shall be classifieds as “ Doubtful above 3 years”.

1.14.3.Exceptions (where borrower-wise classification is not applicable):

i). Agricultural loans of „Farmers in Distress‟:

In case of agricultural loans rescheduled during 2004-05 under scheme for Relief to Farmers in Distress, Income Recognition and Asset Classification (IRAC) norms would be applicable from the 3rd year onwards‟, i.e. on expiry of the initial moratorium period of two years, while the fresh loans extended would be governed by the IRAC norms as applicable to agricultural loans. In other words, the restructured/rescheduled loan shall be treated as NPA, if the principal or interest thereon remains overdue for two crop seasons in case of loans granted for short duration crops and one crop season in case of long duration crops, after the expiry of two years. ii).Agricultural loans of „Farmers in Arrears‟:

In case of agricultural NPAs restructured/rescheduled during 2004-05 under the Scheme for relief to „Farmers in Arrears‟ the existing classification of the loan account restructured/rescheduled continued in the same asset category but fresh loans granted to them were treated as „Standard Asset‟. iii). Agricultural loans through FSCS: In respect of agricultural advances as well as advances for other purposes granted by bank to FSCS under the on-lending system, only that particular credit facility granted to FSCS which is in default, for a period of 2 crop seasons in case of short during crops and one crop season in case of long duration crops., as the case may be, after it has become due, shall be classified as NPA and not all the credit facilities granted to the FSCS.

(..8)

Cir.No 54-2008-BC-CST Dt:12-03-2008

-8- However, other direct loans and advances, if any, granted by the bank to the member borrower of FSCS outside the on-lending arrangement, will become NPA even if one of the credit facilities granted to the same borrower becomes NPA.

1.14.4.Borrower dealing with more than one branch: If a borrower is enjoying credit facilities in more than branch, the branch where the main accounts are maintained shall determine the asset classification, after collecting required information about the conduct of the account at other branches and communicate the asset classification and allocation of securities to the other branches. The other branches shall classify the account accordingly.

1.14.5. Asset Classification of Suit Filed/DICGC Claims Lodged accounts:

There cannot be any standard asset under Suit filed and DICGC claim lodged accounts. Hence the entire suit filed accounts and DICGC claim Lodged accounts shall be treated as NPA and shall be further classified into Sub- standard/ Doubtful/Loss assets. For determining the date of NPA, the conduct of the accounts prior to the date of filing of suit/claim shall be taken into account.

1.14.6.Jewel Loans: If interest is not serviced/recovered on any JL account before

90 days after the completion of one year of arranging the Jewel Loan, such account shall be classified as NPA.

1.15. Sub-classification of Non Performing Assets:

Non Performing Assets shall be classified as Sub-standard, Doubtful and Loss assets based on date of NPA/other parameters.

1.15.1.Sub-standard Assets:

The stay-in-period of sub-standard category was reduced to 12 months with effect from 31.03.2005. Further SSA shall be segregated in to „Secured Exposure‟ and „Unsecured Exposure‟ for the purpose of determining the rate of provision. „Unsecured exposure‟ is defined as an exposure where the realizable value of the security, as assessed by the bank/approved valuers/NABARD Inspecting officers, is not more than 10 per cent, ab initio, of the outstanding exposure. „Exposure” shall include all funded and non-funded exposures (including underwriting and similar commitments). Security means tangible security property charged to the Bank and will not include intangible securities like guarantees, comfort letters etc. Therefore all clean loans and loans with security less than 10% under sub-standard category may be treated as „Unsecured Exposure‟.

1.15.2. Doubtful Assets:

i). A Doubtful asset is one, which has remained NPA for a period exceeding 12 months. Doubtful Assets shall be classified into following categories.

(..9)

Cir.No 54-2008-BC-CST Dt:12-03-2008

-9- a). DA-1 : Doubtful Assets upto one year (NPAs exceeding 12 months but upto 2 years. b). DA-2 : Doubtful Assets above 1 year and upto 3 years (NPAs exceeding 2 years but upto 4 years) c). DA-3 : Doubtful Assets above 3 years (NPAs beyond 4 years). ii). Further each Doubtful asset shall be bifurcated into secured portion and unsecured portion for provisioning purpose.

1.15.3. Loss Assets:

A Loss Asset is one where the loss has been identified by the bank or external auditors or NABARD inspectors. Such an asset is considered uncollectible and of such little value that its continuance as a bankable asset is not warranted although there may be some salvage or recovery value. An asset may become uncollectible due to serious credit impairment, frauds, non-availability of security, erosion in value of security etc. For identification of Loss assets, following 3 conditions are to be satisfied. a). Account is classified as NPA ( age of the NPA is not the criteria) b). Realizable value of the security is NIL/Negligible. c). The account is identified as bad/irrecoverable by the branch/HO/Inspection officials/Auditors/NABARD inspectors. If the realizable value of the security, as assessed by the Bank/approved valuer is less than 10% of the out standings in the borrowal accounts, the existence of the security should be ignored and the asset should be straightaway classified as loss asset If any one of the three conditions (a,b,c) are not fulfilled the account should not be treated as loss asset. Note: An unsecured/clean loan, which has slipped to NPA, need not be classified as Loss asset merely because it is unsecured. Such accounts may be classified as Sub Standard asset with 20% provision for one year and doubtful asset with 100% provision after completion of one year as NPA.

1.15.4.Accounts where asset classification has been changed by Auditors/NABARD Inspectors/Head Office:

Where asset classification assigned by the branch was changed by Statutory Auditors/NABARD Inspectors/Head Office and the changed classification was communicated to branches, branches shall recommend the changed asset classification unless the account has been upgraded as Standard asset or the asset classification as per branch is lower than the changed asset classification communicated by Head Office.

(..10)

Cir.No 54-2008-BC-CST Dt:12-03-2008

-10-

Eg:1. Assume that

a). Branch had treated an account as Standard Asset as on 31.03.07. b). The asset classification is changed to Sub-standard Asset by the Statutory Auditors/NABARD inspectors/Head Office. c). The asset classification as per branch as on 31.03.08 is Standard Asset. In this case branch shall recommend classification as Doubtful-1 asset and recommend provision accordingly, unless the irregularity observed by the Auditors/NABARD Inspectors/HO is fully rectified and the account is regular in all respects.

Eg.2.Assume that a). branch had treated an account as Substandard as on 31.03.07 b). The asset classification is changed to DA-2 by the auditors/NABARD Inspectors/HO (may be due to deterioration/erosion in value of security) and provision made accordingly. c). The asset classification as per branch as on 31.03.08 is DA-1 . In this case branch shall recommend asset classification as DA-2 and recommend provision accordingly. However, if the asset classification as per branch as on 31.03.08 is DA-3 which is lower than the asset classification assigned by the Statutory Auditors/NABARD Inspectors, then branch shall recommend asset classification as DA-3 and recommend increased provision accordingly.

1.16. Valuation of land & building, plant & machinery, vehicles etc.

1.16.1.The collaterals such as immovable properties charged in favour of the Bank should be got valued once in 2 years by approved valueres.

i). The securities, primary or collateral, such as land and building, plant and machinery, Vehicles, etc., obtained as security for advances of Rs.2.00lakhs and above shall be got valued through the approved valuer once in 2 years. Branches should ensure that the valuation given by the approved valuer on land and building, plant & machinery etc. is realistic. However, this stipulation is exempted in case of Housing Loans, which are classified as Standard Assets. ii). In the case of advances against hypothecation of goods the value of the security should be updated by obtaining latest stock statements. Date of receipt shall be recorded by putting date stand on stock statement. In the case of Bill liability, realizable value of goods covered under documents of title to goods shall be ascertained and kept on record.

(..11)

Cir.No 54-2008-BC-CST Dt:12-03-2008

-11- 1.17. Verification of securities:

It is essential that securities charged to the bank are inspected at periodic intervals. Branches shall conduct the inspection of all securities charged to the bank such as stocks, vehicles, plant and machinery, equipment, land and buildings etc., and maintain record of inspection of securities.

1.18. Treatment of security for the purpose of provisioning:

i). Where a borrower enjoys more than one credit facility, the realizable value of the security shall be first reduced to the extent of outstanding liability under the credit facility to which it is taken as primary security and the surplus value of the security, if any, can be taken notionally as security for the unsecured portion of other credit facilities of the same borrower for calculation of provision. ii). Where the security is not taken as primary security to any of the credit facilities but treated as a common security to all the facilities, realizable value of such common security shall be apportioned on pro rata basis to cover the clean portion under each account. iii). In the case of pari passu charge, realizable value of security shall be taken on pro-rata basis. In the case of second/third charge, realizable value of security minus liability with first/second charge holder alone shall be taken into account.

2.00. Income Recognition: 2..01. Income from NPAs should not be recognized on accrual basis but shall be booked as

income only when it is actually received. Therefore, once an account is transferred from PA to NPA, interest shall not be debited to the account at monthly intervals or on due dates. Similarly fees, commission and similar income shall not be debited on accrual basis. As and when credits are received, fees/commission/interest/other income due in the account or actual amount received, whichever is less, shall be debited to the account and credited to Misc. income/interest on NPA.

2.02. Interest Reversal:

The unrecovered portion of fees/commission/interest/other income debited during the current year and corresponding previous year, in fresh NPA accounts shall be reversed at the end of the quarter in which the account is transferred from PA to NPA. The unrecovered portion of interest in Fresh NPAs, to be reversed, shall be ascertained by Minimum Balance Method explained and illustrated in Annexure-II.

2.03. Appropriation of Recovery in NPAs: Repayment received in NPAs shall be appropriated to Expenses, interest and Principal in that order. However, where One Time Settlement has been sanctioned, the repayment received shall be appropriated first towards Principal, then to Expenses and remaining to Interest.

(..12)

Cir.No 54-2008-BC-CST Dt:12-03-2008 -12-

3.00 PROVISION

3.01. Based on the Asset Classification of the borrowal accounts the provisioning requirements shall be computed for all the advances.

S.No.

Asset Classification % of Provision to be made

1. STANDARD ASSETS :

a). Direct advances to Agriculture &Small and Medium Enterprises (SME)

0.25*

b). Residential Housing Loans beyond Rs.20 lakh 1.00*

c). Personal Banking Loans 2.00*

d). All other advances not included in (a), (b) & (c) 0.40*

*(As the general provision will be made at Head Office level, branches need not calculate

provision amount in respect of Standard Asset at branch level)

2. Substandard Asset (On the balance outstanding without

making any allowance for security or DICGC guarantee cover available

a). Secured Exposure under SSA* 10%

B). Unsecured Exposure under SSA * 20%

* Unsecured/Secured Exposure is defined in Para No.2.15, 1

3. Doubtful Asset (on the book balance)

i) On secured liability

a) Doubtful upto 1 year 20 %

b) Doubtful for above 1 year but upto 3 year 30 %

c). Doubtful above 3 years 100%

ii. on secured / unsecured liability covered by DICGC Claims received

Nil

iii) On secured / unsecured liability not covered by DICGC claim received

100 %

4. Loss Asset: (on the Book Balance minus DICGC claim Received)

100 %

NOTE:

As per RBI guidelines advances against Term Deposits, NSC, IVP, KVP and SV of Life Insurance Policies are exempt from provisioning requirement provided the advances are fully covered by such securities. Further while computing provisioning requirements on doubtful assets guaranteed by DICGC, the realizable value of the security should be deducted first from the balance outstanding before DICGC Guarantee is offset.

(..13)

Cir.No 54-2008-BC-CST Dt:12-03-2008

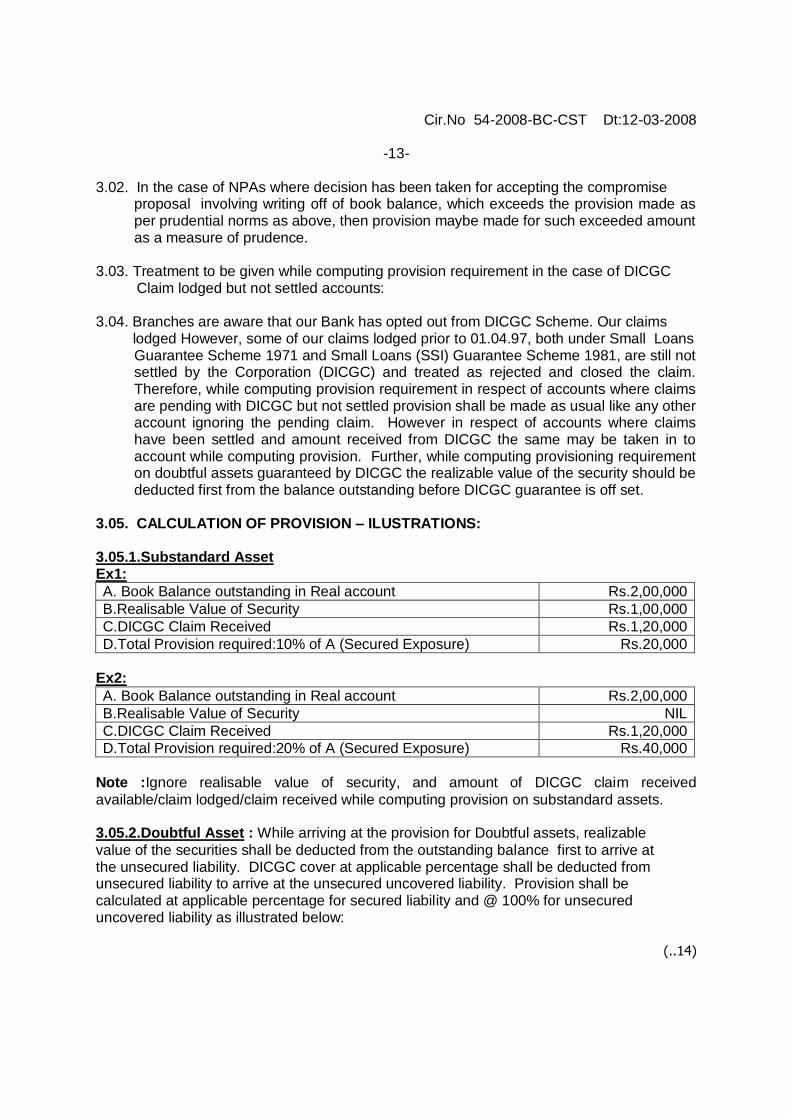

-13- 3.02. In the case of NPAs where decision has been taken for accepting the compromise

proposal involving writing off of book balance, which exceeds the provision made as per prudential norms as above, then provision maybe made for such exceeded amount as a measure of prudence.

3.03. Treatment to be given while computing provision requirement in the case of DICGC Claim lodged but not settled accounts: 3.04. Branches are aware that our Bank has opted out from DICGC Scheme. Our claims lodged However, some of our claims lodged prior to 01.04.97, both under Small Loans

Guarantee Scheme 1971 and Small Loans (SSI) Guarantee Scheme 1981, are still not settled by the Corporation (DICGC) and treated as rejected and closed the claim. Therefore, while computing provision requirement in respect of accounts where claims are pending with DICGC but not settled provision shall be made as usual like any other account ignoring the pending claim. However in respect of accounts where claims have been settled and amount received from DICGC the same may be taken in to account while computing provision. Further, while computing provisioning requirement on doubtful assets guaranteed by DICGC the realizable value of the security should be deducted first from the balance outstanding before DICGC guarantee is off set.

3.05. CALCULATION OF PROVISION – ILUSTRATIONS: 3.05.1.Substandard Asset Ex1:

A. Book Balance outstanding in Real account Rs.2,00,000

B.Realisable Value of Security Rs.1,00,000

C.DICGC Claim Received Rs.1,20,000

D.Total Provision required:10% of A (Secured Exposure) Rs.20,000

Ex2:

A. Book Balance outstanding in Real account Rs.2,00,000

B.Realisable Value of Security NIL

C.DICGC Claim Received Rs.1,20,000

D.Total Provision required:20% of A (Secured Exposure) Rs.40,000

Note :Ignore realisable value of security, and amount of DICGC claim received

available/claim lodged/claim received while computing provision on substandard assets. 3.05.2.Doubtful Asset : While arriving at the provision for Doubtful assets, realizable

value of the securities shall be deducted from the outstanding balance first to arrive at the unsecured liability. DICGC cover at applicable percentage shall be deducted from unsecured liability to arrive at the unsecured uncovered liability. Provision shall be calculated at applicable percentage for secured liability and @ 100% for unsecured uncovered liability as illustrated below:

(..14)

Cir.No 54-2008-BC-CST Dt:12-03-2008

-14-

Case 1 Case 2

A. Book Balance outstanding in the Real A/c as on 31.03.2007 after making interest reversal, if any

2,00,000 2,00,000

B. Realisable Value of security 3,00,000 60,000

C. Net Balance ( A-B ) Nil 1,40,000

D. Applicable percentage of DICGC Cover available on „C‟ above (say 75%) in case of

DICGC claim already received

Nil 1,05,000

Note: If DICGC claim already received is more than “D” above the claim amount shall be restricted to the amount equivalent to “D” only. If for any account DICGC Claim is lodged but the same is not yet settled, the same should be ignored and cover available be treated as NIL.

E. Unsecured liability (C-D) Nil 35,000

Provision Required for DA-1:

ii) On secured portion a) Secured Liability B or A whichever is less

2,00,000

60,000

b) Provision : 20 % 40,000 12,000

ii) On unsecured portion : 100 % of E Nil 35,000

Total Provision required 40,000 47,000 Provision Required for DA-2:

iii) On secured portion a) Secured Liability B or A whichever is less

2,00,000

60,000

b) Provision : 30 % 60,000 18,000

ii) On unsecured portion : 100 % of E Nil 35,000

Total Provision required 60,000 53,000

Provision for Doubtful Assets above 3 years

iv) On secured portion a) Secured Liability B or A whichever is less

2,00,000

60,000

b) Provision : 100 % For NPAs on DA-3 2,00,000 60,000

ii) On unsecured portion : 100 % of E Nil 35,000 Total Provision required 2,00,000 95,000

Loss Asset: 100% provision shall be made after deducting DICGC Claim

received from

the balance outstanding. A. Book Balance outstanding in the account as on 31.03.2007 after

making interest reversal, if any. 3,00,000

Amount of DICGC claim received, cover available / claim lodged claim received / or claim received and adjusted say 50% of a

1,50,000

B. Net Balance (A-B) 1,50,000

C. Total Provision required 100% of C 1,50,000

(..15)

Cir.No 54-2008-BC-CST Dt:12-03-2008

-15- 3.05.4.Existing provision:

The provision held for NPAs as on 31.03.2007( after audit corrections) should be taken as existing provision in Ret.1 and Ret.3 as on 31.03.2008.

3.05.5. Net Advances/Net NPAs

Net Advances and Net NPAs shall be arrived at as follows. Net Advances = Gross Advances minus DICGC claim Received minus provision made for NPAs Net NPAs = Book Balance outstanding in NPA ACCOUNT– (Credit balance in DICGC Claim Received account +Provision). 3.05. 6 Provision for Personal Banking Loans:

The loans which are being sanctioned for Demand Loan (Contingencies) i.e. Children‟s education, medical expenses, marriages etc., where creation of asset does not take place, such loans shall be treated as “Clean Advances” and necessary provision shall be made as applicable to unsecured advances, unless these loans are secured by collateral security, if any.

4.RESTRUCTURING/RESCHEDULING OF ADVANCES & ASSET CLASSIFICATION. 4.01Restructuring/Rescheduling of Advances:

4.01.1. Loans and advances extended by the Bank may become irregular due to genuine difficulties viz. Delay in implementation of the project, delay in commencement of commercial production, bottlenecks in production and/or distribution, natural calamities and other factors which are beyond the control of the borrowers. In such genuine cases, the borrowers may be assisted to overcome the difficulties by restructuring the credit facilities or rescheduling/rephrasing terms of repayment with or without interest concession. 4.01.2. Restructuring of credit facilities normally involve conversion of short-term loans into term loans, conversion of working capital finance into term loans, waiver/funding of overdue interest etc. Rescheduling/rephrasing normally involve increase in moratorium period, increase in repayment period, postponement of instalments, revision of amount of instalments etc. 4.01.3. Restructuring/rescheduling/rephrasing in all cases should be based on viability, rehabilitation potential and cash flows of the borrower. Branches shall not resort to restructuring/rescheduling/rephasing for the purpose of avoiding slippage to NPA.

(..16)

Cir.No 54-2008-BC-CST Dt:12-03-2008

-16-

4.02.Asset classification of restructured/rescheduled/rephrased advances:

RBI has stipulated different norms for asset classification of restructured / rephrased / rescheduled agricultural and other loans and advances. Branches shall strictly adhere to these norms, furnished below, for asset classification of restructured/rescheduled/Rephased loans and advances. 4.03. General Guidelines: i). Asset Classification of Sub-standard asset after specified period:

The substandard asset, which has been subjected to restructuring/rescheduling, would be eligible to be upgraded to standard asset after the specified period, subject to restructuring/rescheduling, would be eligible to be upgraded to standard asset after the specified period, subject to satisfactory performance during the period. If satisfactory performance is not evidenced during the period, the asset classification of the restructured sub-standard asset would be governed as per the applicable prudential norms with reference to the pre-restructuring payment schedule.

ii) Restructuring of credit facilities extended to traders:

As trading involved only buying and selling of commodities, and the problems associated with the manufacturing units such as bottleneck in commercial production, time and cost escalation etc., are not applicable to them, the rescheduling/rephasement shall be discouraged.

iii). Relevant date of asset classification after restructuring:

Branches shall not restructure/reschedule borrowal accounts with retrospective effect. The asset classification, status as on the date of approval of the restructured package by the competent authority would be relevant to decide the asset classification status of the account after restructuring/rescheduling/renegotiation. iv). Repeated Restructuring: Branches shall not restructure/reschedule accounts repeatedly unless there are very strong and valid reasons that warrant such repeated restructuring/rescheduling. v). Request for Restructuring:

Normally restructuring cannot take place unless alteration/changes in the original loan agreement are made with the formal consent/application of the borrower. However, the process of restructuring can be initiated by the branch in deserving cases subject to customer agreeing to the terms and conditions.

(..17)

Cir.No 54-2008-BC-CST Dt:12-03-2008

-17- vi). Security: While assessing the extent of security cover available to the restructured/rescheduled credit facilities, collateral securities would also be reckoned, provided such collateral is a tangible security properly charged to the bank and is not in intangible form like guarantee etc., of the promoter/others. vii). Funded Interest

Income Recognition in respect of the NPAs, regardless of whether these are or are not subjected to rescheduling/restructuring, should be done strictly on cash basis, only on realization and not if the amount of overdue interest has been funded. If, however, the amount of funded interest is recognized as income, a provision for an equal amount should also be made simultaneously. In other words, any funding of interest in respect of NPAs, if recognized, as income, should be fully provided for. viii). Reversal of Provision:

Provision made for NPAs shall be reversed when the account becomes a standard asset. However, the provision made towards interest sacrifice, can be reversed only on satisfactory completion of all repayment obligations and the outstanding in the account is fully repaid. Branches shall not re-compute the extent of sacrifice each year and make adjustments in the provisions made towards interest sacrifice. 4.04. Restructured/Rescheduled Agricultural Advances: 4.04.1Scheme for relief to farmers affected by Natural Calamities:

Where natural calamities impair the repaying capacity of agricultural borrowers, banks may extend, on their own, following relief measures. a). Conversion of short-term production loan due in the year of occurrence of natural calamity into a term loan or reschedulement of the repayment period suitably.

b). Reschedule/postpone installments of existing term loans keeping in view the repaying capacity and nature of natural calamity. c). Provide fresh crop loans and term loans for development purpose. Where relief in the form of conversion/reschedulement of loans is extended to farmers, term loan as well as fresh short term loan may be treated as current dues and need not be classified as NPA. The asset classification of these loans would thereafter be governed by revised terms and conditions.

(..18)

Cir.No 54-2008-BC-CST Dt:12-03-2008

-18-

4.04.2.Package of Relief measures for debt stressed farmers: a) Package of relief measures is extended for the debt stressed farmers in 25 districts of Andhra Pradesh. All the 5 districts in the area of operation of our Bank are identified for extending the relief measures. Under the package, entire interest on overdue loans as on 01.07.2006 was waived, the overdue loans are rescheduled over a period of 3-5 years with one year moratorium and fresh finance may be ensured to them. b). Where relief is extended to farmers under the above package, the term loan as well as fresh short term loan may be treated as current dues and need not be classified as NPAs.

4.05 Restructured Rescheduled Advances other than Industrial and Agricultural Advances:

4.05.1. Branches may consider accounts, other than industrial and agriculture advances i.e. housing, personal loans, loans to traders/business enterprises/professionals etc., for restructuring/rescheduling/rephasing provided such accounts qualify the basic test of viability, rehabilitation, potential and cash flows of the borrower.

4.05.2. However, these accounts would not qualify for the special asset classification status

available to restructured/rescheduled/rephased industrial or agricultural advances, but would continue to age and migrate to the next asset classification status in the normal course. In other words, the asset classification of these accounts shall be based on the original terms of repayment.

4.05.3. If concession in rate of interest is permitted as per the rephased terms, branches

shall compute and recommend provision for the amount of sacrifice in interest, measured in present value terms.

4.05.4. These restructured/rescheduled accounts would be eligible to be upgraded to

standard category after a period or one year after that date when „first payment of interest or of principal, whichever is earlier, falls due under the revised terms subject to satisfactory performance during that period. The amount of provision made for NPA, net of the amount provided, for the sacrifice in interest in present value terms as aforesaid, could be reversed after the one-year period.

Eg: 1). A PBS loan, which was Substandard as on 31st December (date of NPA-15th

December) is rescheduled/rephrased during January. EMIs are due from 1st February as per the rephased terms. The account will be continued to be Sub-standard upto 14th December next year and will slip to Doubtful-1 on 15th December next year. Account can be upgraded as Standard asset on 1st Feb next year, provided all instalments and interest as per rephased terms are paid by the borrower.

(..19)

Cir.No 54-2008-BC-CST Dt:12-03-2008

-19-

Eg.2: Housing loan, which will become NPA on 30th November (overdue from 1st September) is rescheduled/rephased on 15th November i.e. before the account has slipped to NPA. EMIs are due from 1st January as per rephased terms. The account shall be classified as sub-standard from 30th November to 29th November next year and Doubtful-1 from 30th November next year. It may be upgraded to Standard in January next year subject to payment all EMIs as per rephased terms.

5.00. UPGRADATION OF LOAN ACCOUNTS CLASSIFIEDS AS NPA 5.01. Upgradation:

If arrears of interest and principal are paid by the borrower in the case of loan accounts classified as” NPAs”, the account should no longer be treated as non-performing and may be classified as „standard‟. In other words, an account, which became NPA due to non-payment of interest and/or instalments of principal, upon payment of arrears of interest and/or instalments of principal in full, stands upgraded as Standard Asset on the day of clearing the arrears in full.

5.02.Accounts classified as NPA get upgraded to Performing Asset any day during the year by recovery or otherwise.

Eg: i). Entire arrears of interest and instalments of loan account are paid and account is

fully regularized. ii). Overdrawal allowed in OD/CC account has been regularized or the party has started operating the account within limit/drawing power. iii).In case of account classified as NPA on account of other account/s of borrower

being NPA, and such other account/s are upgraded/closed. iv). In case of a NPA, so classified for non-submission of stock statement, non-renewal

of limits etc., account is regularised by submission of stock statements or limit is renewed or reviewed.

5.03.In case of a borrower having multiple accounts, the accounts can be upgraded as standard asset only if all accounts of the borrower are regular on the day of upgradation. 5.04.Regularisation of account for upgradation:

Accounts shall be regularized by genuine credits for upgrading the account from NPAs to standard assets. Regularisation of accounts by allowing temporary OD/adhoc limit, rephasement of instalments, conversion of loan, discounting/purchasing of accommodation cheques, transfer of funds from accounts of sister concern, other than on genuine trade/business related transaction, etc shall not allow the account to be upgraded as standard asset.

(..20)

Cir.No 54-2008-BC-CST Dt:12-03-2008

-20- 6.00. ACCOUNTING PROCEDURE-NON PERFORMING ASSETS 6.01. Income Recognition:

Income from Non-performing assets is not recognized on accrual basis but is booked as income only when it is actually received. Therefore interest on NPAs shall be charged to the account only when it is actually received. As and when recovery is made in NPAs, expenses incurred but not charged to the accounts shall be debited to the account and credited to Miscellaneous. Income first. Balance of recovery made or interest upto the end of previous month not charged to the account whichever is less shall be debited to the account and credited to interest on NPA. After debiting the expenses and interest to the NPA (Real account), balance in Real account shall not exceed the balance in shadow account since balance in shadow account is the total dues of the borrower.

6.02.Interest Reversal: 6.02.1.In the case of accounts which are already classified as NPA as on 31.03.2007

and continue to be NPA as on 31.03.2008, the question of interest reversal as on 31.3.2008 does not arise as interest is being collected in such cases as and when the recovery is received and the same is appropriated towards the interest.. As per the guidelines when a borrowal account is classified as NPA for the first time as at the end of an accounting year, the unrecovered portion of interest debited to the borrowal account and credited to the income account in the previous accounting year as well as in the current accounting year should be reversed.

Therefore, in the case of all loans and advances, non-operative overdraft accounts and other accounts which were classified as performing /standard assets last year as on 31.3.2007 but which are now classified as non-performing assets (NPA) as on 31.03.2008, branches shall first debit interest on accrual basis for the month ending 31.03.2008. Thereafter, the unrecovered portion of the interest debited during the year 2006-2007as well as during 2007-2008 (i.e. entire interest arrears in the account) shall be reversed by passing the following entries separately for 2006-2007 and 2007-2008.

DEBIT: Interest on Advances ( or IOL) CREDIT: Loan/Non operative O.D/other accounts of the borrower.

(..21)

Cir.No 54-2008-BC-CST Dt:12-03-2008 -21-

6.02.2.Operative NPOD accounts classified as existing NPAs:

Branches are advised to debit the interest reversal made as on 31.03.07 to all operative accounts on 02.04.2008 and to continue to debit monthly interest on accrual basis during the current year. This procedure is laid down to ensure that credits received in the operative NPOD accounts, during the current year are appropriated towards interest first. The un recovered portion of interest, if any, in those accounts as on 31.03.2007 shall be reversed by passing following entries: Debit : Interest income on NPAs. Credit : Operative NP Overdraft account of the borrower. The unrecovered portion of interest in operative NPOD account shall be ascertained as under.

a). Total interest debited to NPOD a/c during the year 2007-08 (Including the interest debited to operative OD account on 02.04.2007 pertaining to interest reversal made for 2006-07 :Rs. b). Less: Total credits received during 2007-08 :Rs. c). Unrecovered portion of interest (a-b) :Rs.

6.02.3.Operative NPOD accounts slipped during current year (New NPAs):

In the case of operative overdraft accounts classified as NPAs for the first time as at the end of the current year, branches shall first debit interest on accrual basis upto the end of March2008. Thereafter, the unrecovered portion of interest debited during 2006-07 and 2007-08 shall be reversed by passing the following entries Debit : Interest income on Performing Assets (or IOL) Credit : Operative Overdraft account of the borrower.

6.02.4.Bills:

In the case of cheques, drafts, bills discounted which are classified as NPA, the question of reversal of interest as at the end of year does not arise as interest on overdue bills is not debited and not taken into income account unless collected in Cash. However Branches shall calculate interest receivable (compounded monthly) on all overdue bills outstanding as at the end of the current year and pass the following contra entries.

Debit : Interest Receivables on Overdue Bills A/c Credit: Unrealized interest on overdue Bills A/c The contra entries already passed at the end of the previous year shall be reversed.

6.02.05 Transfer of PAs to NPAs:

i). Outstanding balance, after interest reversal in accounts which have slipped to NPA on 31.03.08 shall be transferred to NPL/NPOD/NPB etc., on 31.03.08 by passing the following entries.

(..22)

Cir.No 54-2008-BC-CST Dt:12-03-2008 -22-

Debit : NPL/NPOD/NPB account Credit: Respective Loan/OD/Bill account ii). NPAs upgraded as standard assets during the current year, shall be transferred to respective loan account by passing following entries. Debit : Respective Loan/OD/Bill account Credit: NPL/NPOD/NPB account 6.02.6.Unrealised Interest in NPA and Shadow account: i). Branches shall maintain shadow accounts for all NPAs, which shall depict the total dues of the borrower including uncharged interest and unrecovered expenses. Hence shadow accounts shall be opened as at the end of the year for all accounts slipped to NPA during the year. The amount transferred from Standard accounts to NPAs as at the end of the year shall be the opening balance in the shadow account. The unrecovered portion of interest reversed as at the end of the year shall be added in the shadow account. The following contra entries shall be passed for the unrecovered portion of interest.

Debit : Interest Receivable on NPAs Credit: Unrealised Interest on NPAs ii). Branches shall calculate interest for all NPAs at stipulated rates, add them in respective shadow accounts and account for the same by passing the following contra entries. Debit : Interest Receivable on NPAs Credit: Unrealised Interest on NPAs 6.02.7. Out of the total recovery in NPA, amount recovered towards interest shall be ascertained and transferred to Interest on NPA by passing following entries. Debit : NPA account Credit: Interest income on NPA Following contra entries shall be passed for the recovery towards interest. Debit : Unrealised Interest on NPAs Credit: : Interest Receivable on NPAs.

Note: The difference between shadow balance and real balance is the unrecovered interest in case of non-suit filed NPAs and unrecovered expenses and interest in case of suit filed accounts. 6.02.8.Maintenance of Real & Shadow Accounts: Branches are advised to follow the accounting procedure and maintenance of Real and Shadow Register. Branches are already aware of this since erstwhile RRBs have informed about the same . 7.00SUBMISSION OF RETURNS

While preparing the NPA annual returns pertaining to advances, as on 31.3.2008 the following guidelines be observed/noted/kept in view without fail and comply with the same.

(..23)

Cir.No 54-2008-BC-CST Dt:12-03-2008 -23-

7.01. RETURN-I: It is for reporting Borrower- wise and Asset wise classification of NPAs as at 31.03.2008

in Return-1, use separate sheet in accordance with classification, by ticking the box ” / “wherever applicable. The amount shall be furnished In Rupees.

7.02.RETURN-II: It is for reporting purpose wise and Asset Wise classification of advances (Standard Assets

and NPAs) In the said statement it is to be noted that the DICGC Claim Received Amount shown in Return II shall be equal to the DICGC Claim Received amount shown in Trial Balance under DICGC Claim received Head. In the return, the amount shall be corrected to nearest „thousand‟. Decimals shall not be used.

7.03.RETURN-III: It is for reporting Summary of NPAs and provisioning requirements as at 31.03.2008. The amount shall be furnished in Rupees

7.04.RETURN-IV: It is for reporting Asset wise NPAs under Government sponsors Schemes as at 31.03.2008 (Amount shall be furnished in thousands

7.05.Preparation of Returns: The Return-I (green colored sheets) is to be prepared in duplicate and submit the original to Regional Office retaining the copy for branch records. (Return-I need not be submitted to HO) The returns II, III & IV are to be prepared in Triplicate and submit the original to Regional

Office, retaining two copies at the branch (one in NPA Returns file and the other in Audited statements file). Return II & III are incorporated in one sheet and Return IV is devised in a separate sheet. Return –I format is printed on both sides of the sheet. Branches are advised to use separate sheet (one side or both sides depending upon the need) for each category of asset under suit filed and non-suit filed A/cs for both Existing and NEW NPAs separately by marking a Tick “ “ in relevant box provided on the top of the return. While reporting the NPAs in RET-I, all outstanding NPAs under Crop, DL, MT Loan etc (General Category) are to be written first and thereafter the NPAs outstanding under various Government sponsored loans may be written scheme-wise separately. This is to facilitate the branch to report the details of Govt. Sponsored loans in RET-IV correctly and easily.

(..24)

Cir.No 54-2008-BC-CST Dt:12-03-2008

-24- 7.06.Submission of Returns: All branches are advised to submit- i). NPA Flash Report to Regional Office by 02.04.2008 ii).Annual return I, II, III & IV so as to reach Regional Office concerned by 05.04.2008.

Regional Offices are advised to – i). Communicate the consolidated NPA Flash Report to HO on 02.04.2008

ii). Ensure that the returns are verified and consolidated immediately. The consolidated returns of II, III, Iv shall reach Head Office by 08.04.2008 unfailingly. 7.07.SUPLY OF PRINTED ANNUAL RETURNS:

Sufficient numbers of printed NPA annual returns forms are being supplied to Regional Offices for onward supply to branches. Buffer stock are being supplied to Regional Offices to meet the additional requirement of branches, in case of need. All columns of the NPA returns are self-explanatory. Branches shall note that the divergence in classification of assets, non-compliance of RBI/NABARD guidelines, if any noticed, would be viewed seriously. We would like to reiterate that deterrent action including monitory penalty will be imposed against the official/s responsible for such wrong classification/concealment. Branches are once again advised to thoroughly go through all the guidelines and ensure classification of assets properly and calculate the provisions accurately and submit the returns in time. Clarifications, if any required, may be obtained from Head Office, Chairman‟s Secretariat (Recovery Cell). (M.JAIPRAKASH) CHAIRMAN

(..25)

Cir.No 54-2008-BC-CST Dt:12-03-2008

-25-

ANNEXURE - 1

Details of agricultural activities for which the NPA status shall be determined if interest or installment of principal remains overdue for period of 2 crop seasons in case of short duration crops and one crop season in case of long duration crops.

DIRECT FINANCE

1. Finance to individual farmers (including Self Help Groups (SHGs) or Joint Liability Groups (JLGs) i.e. groups of individual farmers, provided banks maintain disaggregated data on such finance for Agriculture.

2. Short term loans for raising crops i.e., for crop loans. This will include traditional/non-

traditional plantations and horticulture. 3. Advances upto Rs. 10 Lakh to farmers against pledge/hypothecation of agricultural

produce (including warehouse receipts) for a period not exceeding 12 months, irrespective of whether the farmers were given crop loans for raising the produce or not.

4. Loans to small and marginal farmers for purchase of land for agricultural purposes. 5. Loans to distressed farmers indebted to non-institutional lenders, against appropriate

collateral or group security. 6. .Medium and Long Term loans (Provided directly to farmers for financing production and

development needs). (i). Purchase of agricultural implements and machinery

(a).Purchase of agricultural implements – Iron ploughs, harrows, hose, land-levellers,

bund formers, hand tools, sprayers, dusters, hay-press, sugarcane, crushers, thresher machines, etc.,

(b). Purchase of farm machinery-Tractors, trailers, power tillers, tractor accessories viz., disc ploughs, etc.,

(c). Purchase of trucks, mini-trucks, jeeps, pick-up vans, bullock carts and other transport equipment, etc., to assist the transport of agricultural inputs and farm products.

(d). Transport of agricultural inputs and farm products. (e). Purchase of plough animals. (ii). Development of irrigation potential through-

(a). Construction of shallow and deep tube wells, tanks, etc., and purchase of drilling units.

(b). Constructing, deepening clearing of surface wells, boring of wells, electrification of wells, purchase of oil engines and installation of electric motor and pumps.

(c). Purchase and installation of turbine pumps, construction of f ield channels (open as well as underground) etc.,

(d). Construction of lift irrigation Project. ( e). Installation of sprinkler irrigation system. (f). Purchase of generator sets for energisation of pump sets used for agricultural

purposes (..26)

Cir.No 54-2008-BC-CST Dt:12-03-2008

-26- (iii).Reclamation and Land Development Schemes

Bunding of farm lands, leveling of land, terracing, conversion of dry paddy lands into wet irrigable paddy lands, wasteland development, development of farm drainage, reclamation of soil lands and prevention of salinisation, reclamation of revine lands, purchase of bulldozers, etc.,

(iv). Construction of farm buildings and structures, etc.,

Bullocks Sheds, implement sheds, tractor and truck sheds, farm stores etc. (v)Construction and running of storage facilities.

Construction and running of warehouses, go downs, silos and loans granted to farmer for establishing cold storages used for storing own produce,

(vi). Production and processing of hybrid seeds for crops. (vii). Payment of irrigation charges, etc.

Charges for hired water from wells and tube wells, canal water charges, maintenance and upkeep off oil engines and electric motors, payment of labour charges, electricity charges, marketing charges, service charges to Customs Service Units, payment of development cess, etc.,

(viii). Other types of direct finance to farmers.

a). Short Term Loans 1.To traditional/non-traditional plantations and horticulture. b). Medium and Long Term loans. 1.Development loans to all plantations, horticulture, forestry and wasteland. 2.Financing of small and marginal farmers for purchase of land for agricultural

purpose. However, Agricultural Allied Activities like Dairy, Poultry, Animal Husbandry, Fisheries, Sericulture, Social forestry, Farm Forestry etc., are not included in the above cited list. Hence for these activities, the definition given for determination of NPA status as per 90 days norm shall be made applicable.

(..27)

Cir.No 54-2008-BC-CST Dt:12-03-2008 -27-

ANNEXURE-II

MINIMUM BALANCE METHOD FOR INTEREST REVERSAL AND ASSET CLASSIFICATION

For the limited purpose of identifying NPA status and unrecovered portion of interest in the case of loans, any credit received is to be first adjusted towards expenses and interest in the chronological order of date of debit and any advance payment received is to be notionally set off towards interest debited subsequent to the date of receipt of advance payment. Hence, in the case of loan (except partly released loans), the minimum balance outstanding on a particular date indicates that all the interest and expenses debited to the loan prior to that date stands fully recovered. This implies that – I).The difference between the original advance and minimum balance indicates that the repayment received towards principal. Repayment towards principal = Original advance – Minimum balance. II).The difference between the present balance and minimum balance indicates the arrears of interest and charges i.e. interest and charges debited to the loan but not paid by the borrower. Interest arrears = Present balance – Minimum balance – Advance pay ment if any. From the above two data, the asset classification and unrecovered portion of interest in the case of loans can be determined. This is illustrated below. ILLUSTRATION 1:

Term Loan classified as New NPA as on 31-03-2008. Date of Agreement : 04-06-2007 Original Advance : RS.50,000/- Repayment : RS.1000/- per month commencing from 04-07-2007.

Date Dr Cr Balance

04-06-2007 To amount advanced 50000 50000

30-06-2007 To int upto 30-06-07 480 50480

04-07-2007 By cash 1500 48980

31-07-2007 To int upto 31-07-07 579 49559

10-08-2007 By cash 1500 48059

31-08-2007 To int upto 31-08-07 534 48593

22-09-2007 By cash 1200 47393

30-09-2007 To int upto 30-09-07 515 47908

31-10-2007 To int upto 31-10-07 528 48436

17-11-2007 By cash 1500 46936

30-11-2007 To int upto 30-11-07 524 47460

01-12-2007 By cash 1500 45960

31-12-2007 To int upto 31-12-07 489 46449

31-01-2008 To int upto 31-01-08 510 46959

03-02-2008 By cash 400 46559

28-02-2008 To int upto 28-02-08 493 47052

31-03-2008 To int upto 31-03-08 509 47561

Note: The account was not NPA as on 31-12-2007. (..28)

Cir.No 54-2008-BC-CST Dt:12-03-2008

-28- Step 1 :Determination of Asset Classification & Date of NPA:

Repayment towards principal = Original advance – minimum balance = 50000 – 45960 = 4040

No. of instalments paid = Repayment towards principal/Amount of installment = 4040/1000 = 4.040 The borrower has paid four instalments i.e. instalments upto 04-10-07. The installment due on 4-11-07 is not fully paid. Hence the account became NPA 0n 02-02-08 (i.e. 90 days After 04-11-07). Step-2: Asset classification on the basis of non-payment of interest:

Interest arrears = Present balance – Minimum balance – Advance payment = 47561 – 45960 – 0 = 1601. Add debit entries backwards till the total just crosses the figure of RS. 1601/- to find out the earliest date of unpaid interest as under:

31-03-2008 509 509

28-02-2008 493 1002

31-01-2008 510 1512

31-12-2007 489 2001

Arrears of interest of RS.1601/- is greater than Rs.1512/- but less than Rs.2001. This means that interest of Rs.489/- pertaining to month ended 31-12-2007 is not fully paid. Hence the account became NPA on 31-03-2008(i.e. 90 days after 31-12-2007). As per Step-1, the date of NPA with reference to non-payment of installment is 02-02-2008 and as per step-2, the date of NPA with reference to non-payment of interest is 31-03-2008. Earliest of these two dates i.e. 02-02-2008 is the date of NPA. Calculation of unrecovered portion of interest:

As the account is classified as New NPA as on 31-03-2008, the unrecovered portion of interest debited during 2006-07 and 2007-08 is required to be reversed. As per Step-2 above, the unrecovered portion of interest (i.e. entire interest arrears) is Rs.1601/-. This shall be split up as under: i) Unrecovered portion of interest relating to 2007-08 : Rs.1601 ii) Unrecovered portion of interest relating to 2006-07 : Nil iii) Total interest arrears as on 31-12-2007 Rs. 1601

(..29)

Cir.No 54-2008-BC-CST Dt:12-03-2008

-29-

ILLUSTRATION 2 :

Term Loan classified as New NPA as on 31-03-2008. Date of Agreemen : 06-05-2007 Original advanace :Rs.50,000 Repayment : Equated monthly instalments of RS.1300/- per month commencing from 06-06-2006.

Date Dr Cr Balance

06-05-2007 To amount advanced 50000 50000

31-05-2007 To int. upto 31-05-2007 392 50392

06-06-2007 By cash 1300 49092

30-06-2007 To int upto 30-06-2007 634 49726

11-07-2007 By cash 1300 48426

31-07-2007 To int upto 31-07-2007 522 48948

22-08-2007 By cash 1300 47648

31-08-2007 To int upto 31-08-2007 536 48184

25-09-2007 By cash 1300 46884

30-09-2007 To int upto 30-09-2007 512 47396

14-10-2007 By cash 1300 46096

31-10-2007 To int upto 31-10-2007 515 46611

30-11-2007 To int upto 30-11-2007 516 47127

31-12-2007 To int upto 31-12-2007 504 47631

12-01-2008 By cash 500 47131

31-01-2008 To int upto 31-01-2008 522 47653

03-02-2008 By cash 300 47353

28-02-2008 To int upto 28-02-2008 538 47891

31-03-2008 To int upto 31-03-2008 527 48418

Note: The account was not NPA as on 31-12-2007 Determination of, Asset Classification & Date of NPA:

Step-1 : Asset Classification on the basis of non-payment of installment: Total repayment received in the account =Rs.7300 No.of equated monthly instalments received = Repayment received/EMI = 7300 / 1300 = 5.61 The borrower has paid five equated monthly instalments i.e. upto 06-10-2007. The installment due on 06-11-2007 is not fully paid. Hence the account became NPA on 04-02-2008( i.e. 90 days after 06-11-2007).

(..30)

Cir.No 54-2008-BC-CST Dt:12-03-2008

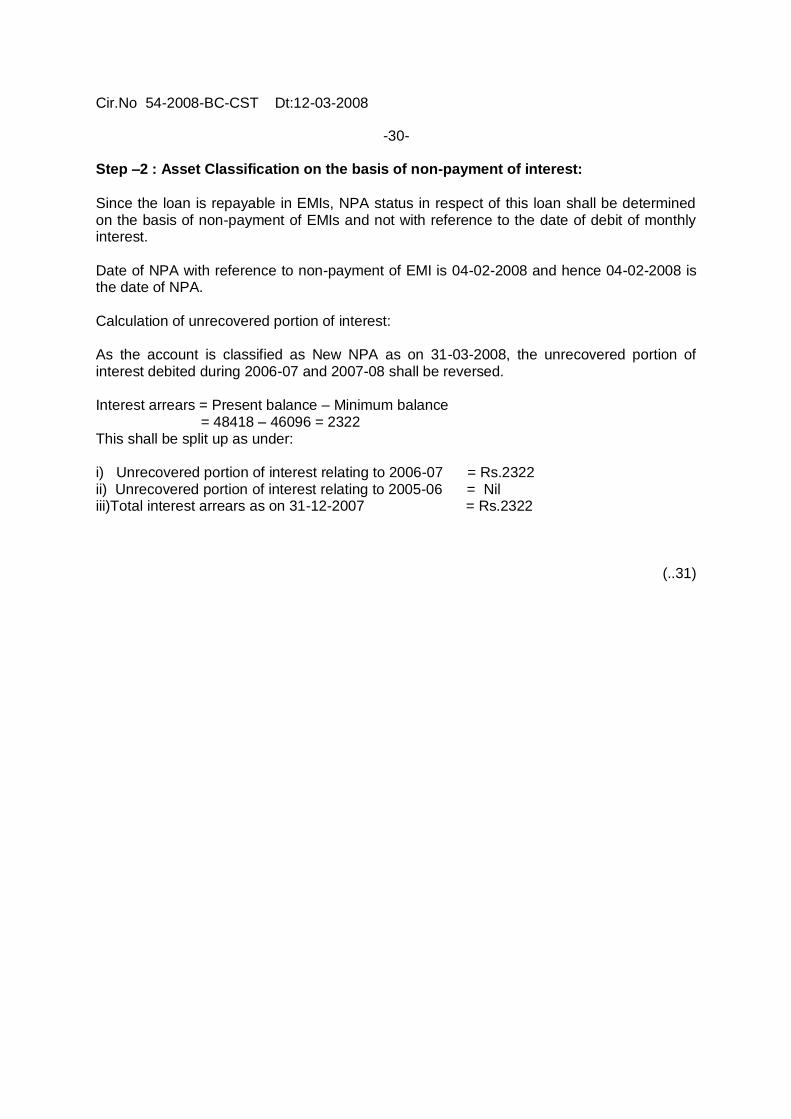

-30- Step –2 : Asset Classification on the basis of non-payment of interest:

Since the loan is repayable in EMIs, NPA status in respect of this loan shall be determined on the basis of non-payment of EMIs and not with reference to the date of debit of monthly interest. Date of NPA with reference to non-payment of EMI is 04-02-2008 and hence 04-02-2008 is the date of NPA. Calculation of unrecovered portion of interest: As the account is classified as New NPA as on 31-03-2008, the unrecovered portion of interest debited during 2006-07 and 2007-08 shall be reversed. Interest arrears = Present balance – Minimum balance = 48418 – 46096 = 2322 This shall be split up as under: i) Unrecovered portion of interest relating to 2006-07 = Rs.2322 ii) Unrecovered portion of interest relating to 2005-06 = Nil iii)Total interest arrears as on 31-12-2007 = Rs.2322

(..31)

Cir.No 54-2008-BC-CST Dt:12-03-2008

-31-

ANNEXURE-III

NPA FLASH REPORT

Branches are required to submit the NPA Flash Report as on 31.03.08 to respective Regional Office along with annual NPA Returns. Amount shall be furnished in THOUSANDS eliminating decimals as per the example

shown hereunder

Code Details Amount

A NPAs as on 31.03.2007 2050

B Add:Increase in existing NPA due to operations during the year 20

C Add:Fresh NPAs added during the year 370

D Add:Increase in NPAs due to transfer from other branches 80

E Less:Reduction in NPA due to transfer to other branches 20

F Less:Reduction in NPA due to upgradation from NPA to PA 100

G Less:Reduction in NPA due to General Write-off 40

H Less:Reduction in NPA due to Write off in OTS 10

I Less:Reduction in NPA due to operations during the year 20

J Less:Reduction in NPA due to recovery towards principal 180

K NPAs at the end of the year (A+B+C+D-E-F-G-H-I-J) 2150

L Total Provision required for outstanding NPAs on 31.03.2008 1020

MANAGER ---------------------------------------------------------------------------------------------------------------------

TABLE –I

CHART FOR DETEMINING ASSET CLASSIFICATION AS ON 31.03.2008 For Non Performing Assets as per 90 days norm

(Both Existing & New NPAs)

Date of NPA as per 90 days norm

Asset classification as on 31.03.2008 As per 90 days norm

Between 01.04.2007 and 31.03.2008 Sub-Standard Asset (SSA)

Between 01.04.2006 and 31.03.2007 Doubtful Asset upto 1 year ( DA-1)

Between 01.04.2004 and 31.03.2006 Doubtful Asset 1 to 3 years (DA-2)

Any date prior to 31.03.2004 Doubtful Assets above 3 years