income class – guarantee scenarios · the lwa base and the lwa 10 2) what ... contract for...

TRANSCRIPT

Income Class – Guarantee Scenarios

September 2010 – Page 1

Income Class – Guarantee Scenarios

September 2010 – Page 2

TABLEOFCONTENTSImportantnotes 4

Definitions 5

Scenarios

1) HowdepositsandwithdrawalsaffecttheLWABaseandtheLWA 10

2) Whathappensatyearend? 11

3) Takingmaximumadvantageofthe5%Bonuses 12

4) IncomeClassresets–accumulationphaseandearlyretirementyears 13

5) IncomeClassresets–withdrawal(retirement)phase 14

6) MakingwithdrawalsbeforeLWAbecomesavailable(EarlyWithdrawal) 15

7) ExceedingtheLWA(ExcessWithdrawal) 16

8) RRIFMinimumAnnualPaymentgreaterthantheLWAallowsclienttowithdrawMAPwithoutincurring

proportionalreduction(RRIFcontractholdingIncomeClassunitsonly) 17

9) RRIFcontractholdingInvestmentandIncomeClass(showsthedifferencebetweencontractlevelMAPandLWARRIFMAP) 18

10) RRIFminimumtakenfromInvestmentClasstomaximize5%BonusinIncomeClass(advantageoftheonecontractstructure) 19

11) RRIFminimumtakenfromInvestmentClasstomaximize5%BonusinIncomeClass

(advantageoftheonecontractstructure)–ExtendedVersion 20

12) HowLWABaseadditionsafterLWAcommencementdateimpacttheGLWBvalueswhenthere

isaGLWBresetandtheLWARateincreases(higherLWARateforLWABaseadditioninhigheragetier) 21

13) HowLWABaseadditionsafterLWAcommencementdateimpacttheGLWBvalueswhenthere

isnoGLWBresetandnoLWARateincrease(blendedLWARate) 22

Income Class – Guarantee Scenarios

September 2010 – Page 3

14) Two‐LifeIncomeStreamselected(incomedeferred) 23

15) Two‐LifeIncomeStreamSelected(EarlyWithdrawal) 24

16) SettingupaTwo‐LifeIncomeStream,non‐registeredaccount,negativereturns 25

17) SettingupaOne‐LifeIncomeStream,jointannuitant,non‐registeredaccount,negativereturns

(comparingagainsttheTwo‐LifeIncomeStream) 26

18) Two‐LifeIncomeStreamselected,RRIFcontractholdingInvestmentandIncomeClass 27

19) GuaranteedPaymentPhase(IncomeClassmarketvaluegoestozero) 28

20) LWADeferrals 29

21) LWAisgreaterthanLIFmaximumpayments

(showshowclientsmaybepreventedfromtakingthefullLWAamountduetoLIFregulationsincertainyears) 30

22) LWAisgreaterthanLIFmaximumpayments,unlock50%

(showshowclientscanreducetheimpactoftheLIFmaximumbyunlocking50%followingLIFguidelines) 31

23) Latedepositreductionoverage75(80%DeathBenefitforthreeyears,100%thereafter) 32

Income Class – Guarantee Scenarios

September 2010 – Page 4

ImportantNotesCalculationoftheGuaranteedLifetimeWithdrawalBenefitismadeusingcalculationsdefinedintheSunWiseEssentialSeriesinformationfolderandcontractforSunWiseEssentialSeriesIncomeClass.(Someguaranteevalueshavenotbeencalculatedincertainscenarios.)Inallexamples,marketvaluesandratesofreturnareforillustrationpurposesonly.Theyareshownnetoffeesandmaybeexaggeratedpositivelyornegativelytoillustratehowcertainproductfeaturesworkindifferentsituations.(Forsimplicity,calculatedvaluesareroundedtothenearestdollar.)AllscenariosandguaranteedamountsarehypotheticalandcannotbeusedtopredictfutureperformanceorGLWBvalues.(Individualresults,generatedbytheSunWiseEssentialSeriesIllustrationtool,willvarywithfundperformance,transactiontimingandamounts.)Redemptionsmadetopayanyfeesdonotaffectanyguaranteedamounts,includingtheLWABase,the5%BonusBase,theLWA,theDeathBenefitandContractMaturityBenefit.(Forsimplicity,theLWABaseFees,initialsalescharge,deferredsaleschargefeesandtaxeshavenotbeenfactoredintotheexamples.)LWAfiguresareshownatDecember31,referringtotherecalculatedLWAavailableforthefollowingcalendaryear.ContractMAP,LWARRIFMAP,LIFMAPandLIFMAXareshownatDecember31,referringtotheamountsapplicableforthefollowingcalendaryear.Inalltheexamples,theowneristheannuitantunlessotherwiseindicated.

Income Class – Guarantee Scenarios

September 2010 – Page 5

DefinitionsPleasebecomefamiliarwiththissectionbeforereviewingthescenarios

GLWBFeature Description/objective(Whatisit?)

Calculation(Howdoesitwork?)

OneLifeIncomeStream

EligibilitytoreceivetheLWAfromanydayafterJanuary1oftheyeartheAnnuitant(ordesignatedAnnuitantfornon‐registeredjointcontracts)turnsage65untilthedeathoftheAnnuitantorthecontractisterminated.

TwoLifeIncomeStream

EligibilitytoreceivetheLWAfromanydateafterJanuary1oftheyeartheyoungeroftheAnnuitantandtheSecondlifeturnsage65untilthedeathoftheAnnuitant,ortheSecondLife(whicheveroccurslater),orthedateonwhichthecontractisterminated.

SecondLife–ifthecontractisregistered,theOwner’sspouseorcommon‐lawpartner,mustbethesolebeneficiary;ifthecontractisnon‐registered,thespouseorcommon‐lawpartneroftheAnnuitant,mustbetheJointAnnuitant.

LWABase

TheamountusedtocalculatetheLWA.

AnamountequaltothefirstdepositallocatedtoIncomeClassunits.

Changesdollar‐for‐dollarforanyfuturedepositsorreclassificationofInvestmentorEstateClassunitstotheIncomeClass(LWABaseAdditions).

ImmediatelyadjustedbyGLWBresets,5%Bonus,EarlyandExcessWithdrawals.

EarlyandExcessWithdrawalsreducetheLWABaseproportionally.

LWACommencementDate

ThefirstdateonwhichclientsredeemIncomeClassunitsorreclassifyIncomeClassunitstoadifferentclassaftertheLWAEligibilityDate.

Income Class – Guarantee Scenarios

September 2010 – Page 6

GLWBFeature Description/objective

(Whatisit?)Calculation(Howdoesitwork?)

LifetimeWithdrawalAmountorLWA

TheamountguaranteedtobeavailableforwithdrawalfromIncomeClasseachcalendaryearforthelifeoftheAnnuitantforaOne‐LifeIncomeStream,orforboththeAnnuitantandtheSecondLifeinthecaseoftheTwo‐LifeIncomeStream.

LWAEligibilitydateisJanuary1oftheyeartheAnnuitantortheyoungeroftheAnnuitantandtheSecondLife,ifapplicable,turns65yearsold.

LWAiscalculatedasapercentageoftheLWABaseontheLWACommencementDateandissubjecttoimmediaterecalculation(seeLWABase).TheLWAissubjecttoquarterlyprorationwhentheinitialdepositismadeaftertheLWAEligibilityDate,whenapplicable.

LWARate

ThepercentageusedtocalculatetheLWA,whichmayincreaseduetoLWABaseAdditionsinahigheragetier,orGLWBResetsthatoccurinahigheragetier.

Atage65,theOne‐LifeIncomeStreamstartsat5%andtheTwo‐LifeIncomeStreamstartsat4.5%.

LWARatevariesbasedontheexpectedageoftheannuitantonDecember31ofthecalendaryearinwhichtheLWACommencementDateoccurs.

FortheTwo‐LifeIncomeStream,theLWARateisbasedontheexpectedageoftheyoungeroftheAnnuitantandtheSecondLifeatDecember31inthecalendaryearinwhichtheLWACommencementDateoccurs.

Agetiers LWARatefor

OneLifeIncomeStream

LWARateforTwo

LifeIncomeStream

65to69 5% 4.5%70to74 5.25% 4.75%75to79 5.5% 5%80orolder 6% 5.5%

TheLWARateapplicabletoaLWABaseAdditionwillbedeterminedbytheagetierthatappliestotheAnnuitant(or,wheretheTwo‐LifeIncomeStreamhasbeenselected,theyoungeroftheAnnuitantandtheSecondLife)onthedayoftheLWABaseAddition.IftheLWABaseAdditionismadewhentheagetieroftheAnnuitantorSecondLifediffersfromtheagetierthatappliedontheLWACommencementDate,oraftertheLWARatewaspreviouslyrecalculatedforanLWABaseAddition,thiswillresultinanewblendedLWARatebeingappliedtotheLWABase.

Income Class – Guarantee Scenarios

September 2010 – Page 7

GLWBFeature Description/objective

(Whatisit?)Calculation(Howdoesitwork?)

LWABaseAdditionDeadline

MaximumageofAnnuitanttoinvestinIncomeClassunits.

One‐LifeIncomeStream–December31ofthecalendaryearinwhichtheannuitantturns80yearsofage.Two‐LifeIncomeStream–December31ofthecalendaryearinwhichtheyoungeroftheAnnuitantandtheSecondLifeturns80yearsofage.

LWADeferral IfthefullamountoftheLWAisnotwithdrawnin

anygivenyear,theamountmaybewithdrawninasubsequentyear.

AnLWADeferralisnotconsideredtohaveoccurredina5%Bonusyear(LWADeferralsfromprioryearswillnotbeaffectedbyanintervening5%Bonusyear).LWADeferralsarenotpermittedaftertheContractMaturityDateorduringtheGuaranteedPaymentPhase.

LWAforayear,togetherwithallavailableLWADeferrals,cannotexceed15%oftheLWABase.

LWADeferralsareresettozerowheneverthereisaGLWBReset.

LWADeferralsterminateontheDeathBenefitDateandarenotaddedtotheDeathBenefit.

LWARRIFMAP LWARRIFMAPappliesiftheContractisaRRIF,LIF,LRIF,PRIForRLIF.ItistheportionofyourcontractlevelMinimum

AnnualPayment(MAP)thatappliestotheIncomeClassunitsonlybasedonthemarketvalueofIncomeClassunitsasaproportionofthetotalmarketvalueoftheContract.IftheLWARRIFMAPisgreaterthantheLWA,clientswillbeallowedtowithdrawuptotheLWARRIFMAPwithouttriggeringanExcessWithdrawal.

5%Bonus Arewardforinvestorswhodonottakewithdrawals

fromtheIncomeClass.Usefultomitigateagainstnegativereturnsduringtheaccumulationphaseleadingtoretirement.

Anamountequalto5%ofthe5%BonusBaseasofDecember31.ItisallottedonaproratedbasisforthefirstyearIncomeClassunitsarepurchased,plusthenext15fullcalendaryears,whentherearenowithdrawalsofIncomeClassunits.5%BonusesincreasetheLWABaseusedforcalculatingguaranteedincomebutdonotimpactcontractualmaturity/deathbenefits,orthemarketvalueoftheIncomeClassunits.

Income Class – Guarantee Scenarios

September 2010 – Page 8

GLWBFeature Description/objective

(Whatisit?)Calculation(Howdoesitwork?)

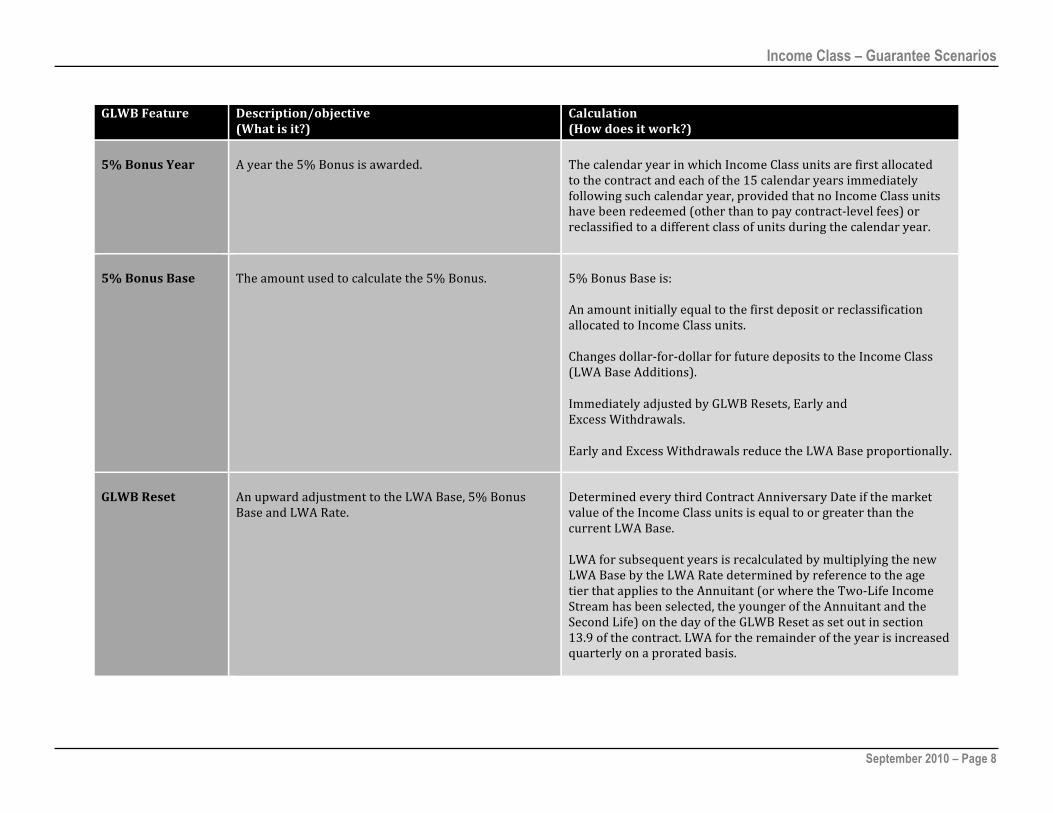

5%BonusYear

Ayearthe5%Bonusisawarded.

ThecalendaryearinwhichIncomeClassunitsarefirstallocatedtothecontractandeachofthe15calendaryearsimmediatelyfollowingsuchcalendaryear,providedthatnoIncomeClassunitshavebeenredeemed(otherthantopaycontract‐levelfees)orreclassifiedtoadifferentclassofunitsduringthecalendaryear.

5%BonusBase

Theamountusedtocalculatethe5%Bonus.

5%BonusBaseis:AnamountinitiallyequaltothefirstdepositorreclassificationallocatedtoIncomeClassunits.

Changesdollar‐for‐dollarforfuturedepositstotheIncomeClass(LWABaseAdditions).

ImmediatelyadjustedbyGLWBResets,EarlyandExcessWithdrawals.

EarlyandExcessWithdrawalsreducetheLWABaseproportionally.

GLWBReset

AnupwardadjustmenttotheLWABase,5%BonusBaseandLWARate.

DeterminedeverythirdContractAnniversaryDateifthemarketvalueoftheIncomeClassunitsisequaltoorgreaterthanthecurrentLWABase.

LWAforsubsequentyearsisrecalculatedbymultiplyingthenewLWABasebytheLWARatedeterminedbyreferencetotheagetierthatappliestotheAnnuitant(orwheretheTwo‐LifeIncomeStreamhasbeenselected,theyoungeroftheAnnuitantandtheSecondLife)onthedayoftheGLWBResetassetoutinsection13.9ofthecontract.LWAfortheremainderoftheyearisincreasedquarterlyonaproratedbasis.

Income Class – Guarantee Scenarios

September 2010 – Page 9

GLWBFeature Description/objective

(Whatisit?)Calculation(Howdoesitwork?)

EarlyWithdrawal

AnyRedemptionofIncomeClassUnits(otherthantopayContract‐LevelFees)orreclassificationofIncomeClassUnitstoadifferentClassofUnits,ineachcasebeforetheLWAEligibilityDate.

Aproportionalreductionofthe5%BonusBaseandtheLWABase.

ExcessWithdrawal

TheamountredeemedduringtheyearaftertheLWACommencementDate(otherthantopaycontract‐levelfees),orreclassifiedduringsuchyearthatexceedsthesumoftheLWAthenineffect(ortheLWARRIFMAP,ifgreater)andanyLWADeferralsthenavailableforsuchyear.AnysubsequentwithdrawalofIncomeClassunitsfollowinganExcessWithdrawalmadeinthesameyearisalsotreatedasanExcessWithdrawal.

Aproportionalreductionofthe5%BonusBaseandtheLWABasethatexceedsthesumoftheLWAthenineffect(ortheLWARRIFMAP,ifgreater)andanyLWADeferralsthenavailableforsuchyear.

DoesnottriggerachangeoftheLWARate.

TimingofadjustmentstotheGLWB Deposits,withdrawals,reclassificationsandothertransactionsmayincreaseordecreasetheLWABaseandthe5%BonusBase,resultinginpotentialincreasesordecreasestotheLWAandtheGLWB.Thesechangestakeeffecteitherimmediatelyorattheendofthecalendaryear,asdescribedbelow:

Transaction/Event

ImpacttoLWA,LWABaseand5%BonusBase

InitialDeposit ImmediatelySubsequentDeposits ImmediatelyReclassification(fromInvestmentClassUnitsorEstateClassUnitstoIncomeClassUnits) ImmediatelyEarlyWithdrawal(doesnotapplytoLWA) ImmediatelyExcessWithdrawal ImmediatelyDepositsubsequenttoanExcessWithdrawal Immediately5%Bonus(additiontotheLWABase) December31st(noimpactto5%BonusBase)

GLWBReset(everythirdContractAnniversaryDate) Immediately

Income Class – Guarantee Scenarios

September 2010 – Page 10

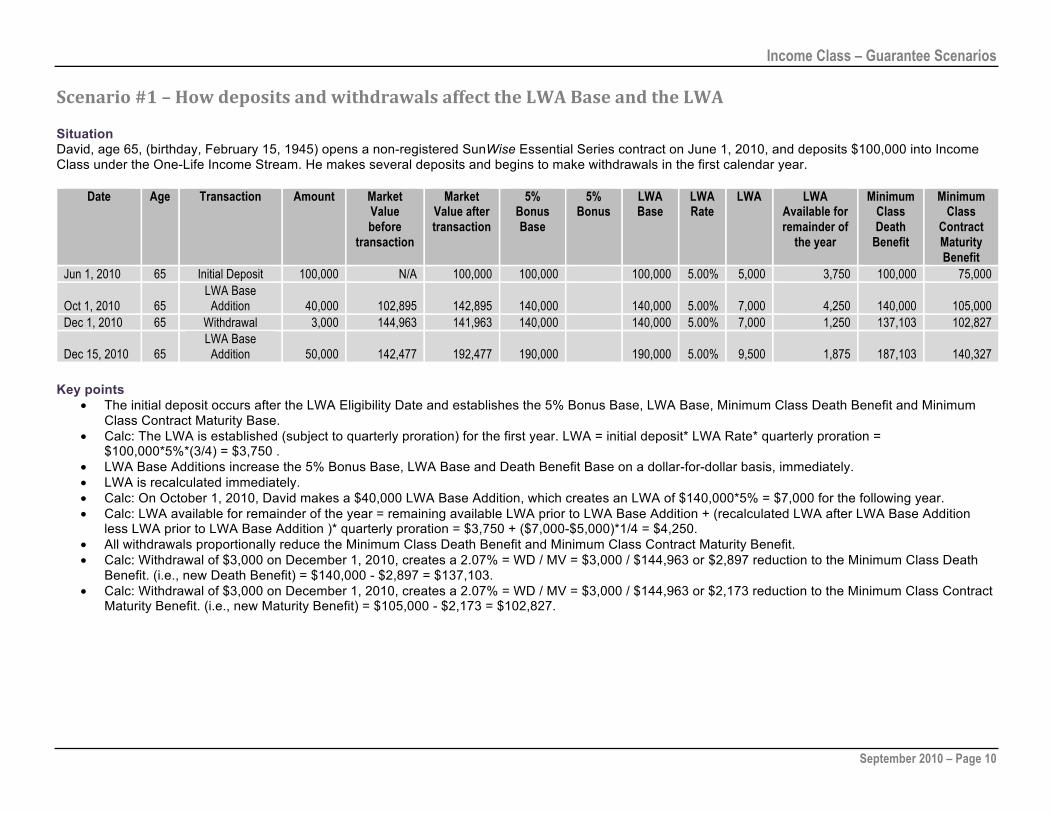

Scenario#1–HowdepositsandwithdrawalsaffecttheLWABaseandtheLWASituationDavid, age 65, (birthday, February 15, 1945) opens a non-registered SunWise Essential Series contract on June 1, 2010, and deposits $100,000 into Income Class under the One-Life Income Stream. He makes several deposits and begins to make withdrawals in the first calendar year.

Date Age Transaction Amount Market Value before

transaction

Market Value after transaction

5% Bonus Base

5% Bonus

LWA Base

LWA Rate

LWA LWA Available for remainder of

the year

Minimum Class Death

Benefit

Minimum Class

Contract Maturity Benefit

Jun 1, 2010 65 Initial Deposit 100,000 N/A 100,000 100,000 100,000 5.00% 5,000 3,750 100,000 75,000

Oct 1, 2010 65 LWA Base

Addition 40,000 102,895 142,895 140,000 140,000 5.00% 7,000 4,250 140,000 105,000 Dec 1, 2010 65 Withdrawal 3,000 144,963 141,963 140,000 140,000 5.00% 7,000 1,250 137,103 102,827

Dec 15, 2010 65 LWA Base

Addition 50,000 142,477 192,477 190,000 190,000 5.00% 9,500 1,875 187,103 140,327

Key points

• The initial deposit occurs after the LWA Eligibility Date and establishes the 5% Bonus Base, LWA Base, Minimum Class Death Benefit and Minimum Class Contract Maturity Base.

• Calc: The LWA is established (subject to quarterly proration) for the first year. LWA = initial deposit* LWA Rate* quarterly proration = $100,000*5%*(3/4) = $3,750 .

• LWA Base Additions increase the 5% Bonus Base, LWA Base and Death Benefit Base on a dollar-for-dollar basis, immediately. • LWA is recalculated immediately. • Calc: On October 1, 2010, David makes a $40,000 LWA Base Addition, which creates an LWA of $140,000*5% = $7,000 for the following year. • Calc: LWA available for remainder of the year = remaining available LWA prior to LWA Base Addition + (recalculated LWA after LWA Base Addition

less LWA prior to LWA Base Addition )* quarterly proration = $3,750 + ($7,000-$5,000)*1/4 = $4,250. • All withdrawals proportionally reduce the Minimum Class Death Benefit and Minimum Class Contract Maturity Benefit. • Calc: Withdrawal of $3,000 on December 1, 2010, creates a 2.07% = WD / MV = $3,000 / $144,963 or $2,897 reduction to the Minimum Class Death

Benefit. (i.e., new Death Benefit) = $140,000 - $2,897 = $137,103. • Calc: Withdrawal of $3,000 on December 1, 2010, creates a 2.07% = WD / MV = $3,000 / $144,963 or $2,173 reduction to the Minimum Class Contract

Maturity Benefit. (i.e., new Maturity Benefit) = $105,000 - $2,173 = $102,827.

Income Class – Guarantee Scenarios

September 2010 – Page 11

Scenario#2–Whathappensatyearend? SituationBuilding on Scenario #1, this shows what happens at year end.

Date Age Transaction Amount Market Value before

transaction

Market Value after transaction

5% Bonus Base

5% Bonus

LWA Base

LWA Rate

LWA LWA Available for

remainder of the year

LWA Deferral

Minimum Class Death

Benefit

Minimum Class

Contract Maturity Benefit

Jun 1, 2010 65 Initial Deposit 100,000 N/A 100,000 100,000 100,000 5.00% 5,000 3,750 100,000 75,000

Oct 1, 2010 65 LWA Base

Addition 40,000 102,895 142,895 140,000 140,000 5.00% 7,000 4,250 140,000 105,000 Dec 1, 2010 65 Withdrawal 3,000 144,963 141,963 140,000 140,000 5.00% 7,000 1,250 137,103 102,827

Dec 15, 2010 65 LWA Base

Addition 50,000 142,477 192,477 190,000 190,000 5.00% 9,500 1,875 187,103 140,327

Dec 31, 2010 65 Year End 193,174 193,174 190,000 No

Bonus 190,000 5.00% 9,500 1,875 187,103 140,327 Jan 1, 2011 65 193,174 193,174 190,000 190,000 5.00% 9,500 9,500 1,875 187,103 140,327 Dec 31, 2011 66 Bonus 193,786 193,786 190,000 9,500 199,500 5.00% 9,975 1,875 187,103 140,327

Key points

• A 5% Bonus is only applied during a 5% Bonus year (i.e., if no withdrawals have been made from Income Class during the calendar year). • Following the December 15, 2010 LWA Base Addition, for the remainder of the year, only $1,875 is available for withdrawal without causing a

proportional reduction in the LWA Base and 5% Bonus Base. • Since the client did not withdraw the full LWA available for the remainder of the year, there will be a deferral of $1,875. If the client had selected LWA

as the GLWB payment type, a $1,875 withdrawal would have been made automatically at year end. • Calc: On December 31, 2010, the LWA is calculated and available January 1, 2011, (the following calendar year), $190,000*5% = $9,500. • Calc: On December 31, 2011, there are no withdrawals and the 5% Bonus is calculated and added to the LWA Base, $190,000*5% = $9,500. LWA Base = $190,000 + $9,500 = $199,500.

Income Class – Guarantee Scenarios

September 2010 – Page 12

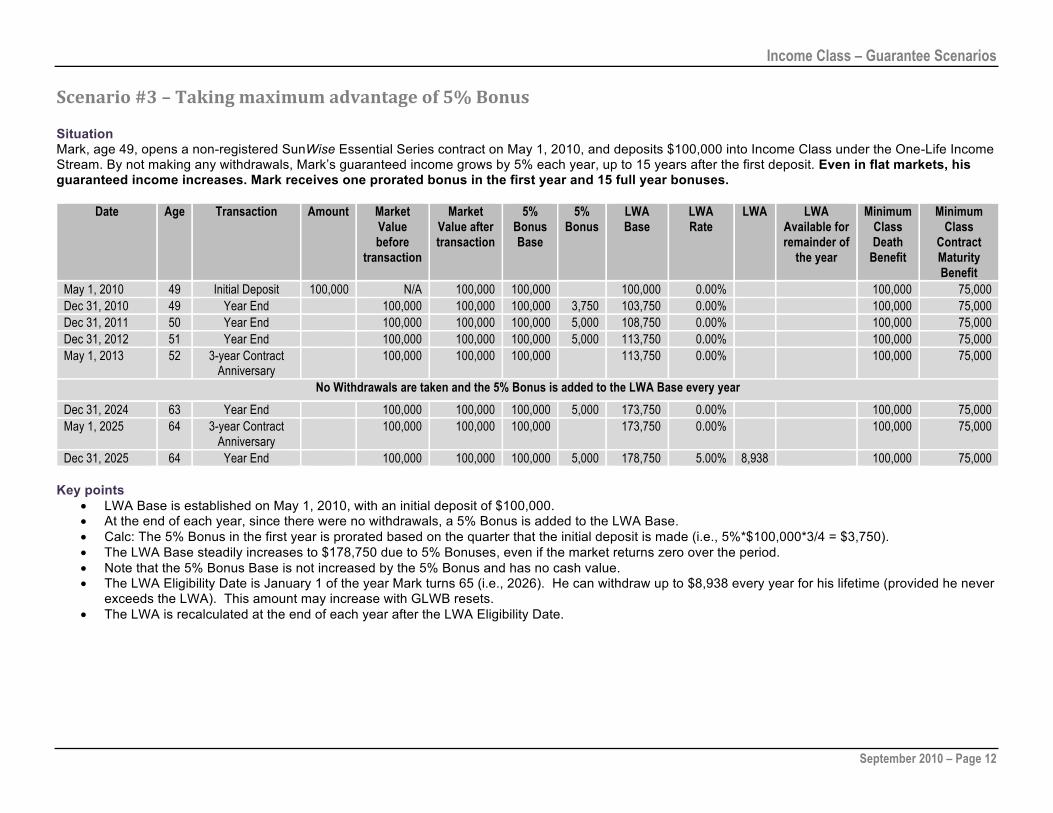

Scenario#3–Takingmaximumadvantageof5%BonusSituationMark, age 49, opens a non-registered SunWise Essential Series contract on May 1, 2010, and deposits $100,000 into Income Class under the One-Life Income Stream. By not making any withdrawals, Mark’s guaranteed income grows by 5% each year, up to 15 years after the first deposit. Even in flat markets, his guaranteed income increases. Mark receives one prorated bonus in the first year and 15 full year bonuses.

Date Age Transaction Amount Market Value before

transaction

Market Value after transaction

5% Bonus Base

5% Bonus

LWA Base

LWA Rate

LWA LWA Available for remainder of

the year

Minimum Class Death

Benefit

Minimum Class

Contract Maturity Benefit

May 1, 2010 49 Initial Deposit 100,000 N/A 100,000 100,000 100,000 0.00% 100,000 75,000 Dec 31, 2010 49 Year End 100,000 100,000 100,000 3,750 103,750 0.00% 100,000 75,000 Dec 31, 2011 50 Year End 100,000 100,000 100,000 5,000 108,750 0.00% 100,000 75,000 Dec 31, 2012 51 Year End 100,000 100,000 100,000 5,000 113,750 0.00% 100,000 75,000 May 1, 2013 52 3-year Contract

Anniversary 100,000 100,000 100,000 113,750 0.00% 100,000 75,000

No Withdrawals are taken and the 5% Bonus is added to the LWA Base every year Dec 31, 2024 63 Year End 100,000 100,000 100,000 5,000 173,750 0.00% 100,000 75,000 May 1, 2025 64 3-year Contract

Anniversary 100,000 100,000 100,000 173,750 0.00% 100,000 75,000

Dec 31, 2025 64 Year End 100,000 100,000 100,000 5,000 178,750 5.00% 8,938 100,000 75,000

Key points • LWA Base is established on May 1, 2010, with an initial deposit of $100,000. • At the end of each year, since there were no withdrawals, a 5% Bonus is added to the LWA Base. • Calc: The 5% Bonus in the first year is prorated based on the quarter that the initial deposit is made (i.e., 5%*$100,000*3/4 = $3,750). • The LWA Base steadily increases to $178,750 due to 5% Bonuses, even if the market returns zero over the period. • Note that the 5% Bonus Base is not increased by the 5% Bonus and has no cash value. • The LWA Eligibility Date is January 1 of the year Mark turns 65 (i.e., 2026). He can withdraw up to $8,938 every year for his lifetime (provided he never

exceeds the LWA). This amount may increase with GLWB resets. • The LWA is recalculated at the end of each year after the LWA Eligibility Date.

Income Class – Guarantee Scenarios

September 2010 – Page 13

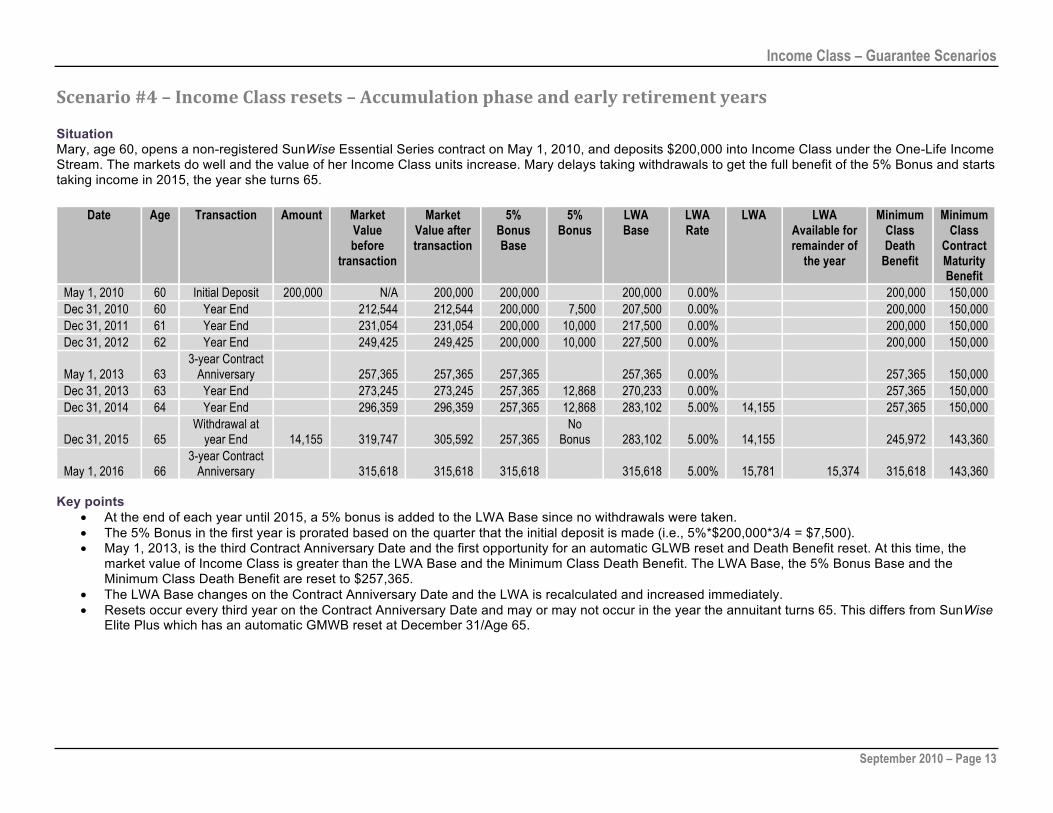

Scenario#4–IncomeClassresets–AccumulationphaseandearlyretirementyearsSituation Mary, age 60, opens a non-registered SunWise Essential Series contract on May 1, 2010, and deposits $200,000 into Income Class under the One-Life Income Stream. The markets do well and the value of her Income Class units increase. Mary delays taking withdrawals to get the full benefit of the 5% Bonus and starts taking income in 2015, the year she turns 65.

Date Age Transaction Amount Market Value before

transaction

Market Value after transaction

5% Bonus Base

5% Bonus

LWA Base

LWA Rate

LWA LWA Available for remainder of

the year

Minimum Class Death

Benefit

Minimum Class

Contract Maturity Benefit

May 1, 2010 60 Initial Deposit 200,000 N/A 200,000 200,000 200,000 0.00% 200,000 150,000 Dec 31, 2010 60 Year End 212,544 212,544 200,000 7,500 207,500 0.00% 200,000 150,000 Dec 31, 2011 61 Year End 231,054 231,054 200,000 10,000 217,500 0.00% 200,000 150,000 Dec 31, 2012 62 Year End 249,425 249,425 200,000 10,000 227,500 0.00% 200,000 150,000

May 1, 2013 63 3-year Contract

Anniversary 257,365 257,365 257,365 257,365 0.00% 257,365 150,000 Dec 31, 2013 63 Year End 273,245 273,245 257,365 12,868 270,233 0.00% 257,365 150,000 Dec 31, 2014 64 Year End 296,359 296,359 257,365 12,868 283,102 5.00% 14,155 257,365 150,000

Dec 31, 2015 65 Withdrawal at

year End 14,155 319,747 305,592 257,365 No

Bonus 283,102 5.00% 14,155 245,972 143,360

May 1, 2016 66 3-year Contract

Anniversary 315,618 315,618 315,618 315,618 5.00% 15,781 15,374 315,618 143,360

Key points • At the end of each year until 2015, a 5% bonus is added to the LWA Base since no withdrawals were taken. • The 5% Bonus in the first year is prorated based on the quarter that the initial deposit is made (i.e., 5%*$200,000*3/4 = $7,500). • May 1, 2013, is the third Contract Anniversary Date and the first opportunity for an automatic GLWB reset and Death Benefit reset. At this time, the

market value of Income Class is greater than the LWA Base and the Minimum Class Death Benefit. The LWA Base, the 5% Bonus Base and the Minimum Class Death Benefit are reset to $257,365.

• The LWA Base changes on the Contract Anniversary Date and the LWA is recalculated and increased immediately. • Resets occur every third year on the Contract Anniversary Date and may or may not occur in the year the annuitant turns 65. This differs from SunWise

Elite Plus which has an automatic GMWB reset at December 31/Age 65.

Income Class – Guarantee Scenarios

September 2010 – Page 14

Scenario#5–IncomeClassresets–Withdrawal(retirement)phaseSituationBuilding on Scenario #4, Mary has started to make withdrawals at age 65. The markets continue to do well and the value of her Income Class units increases.

Date Age Transaction Amount Market Value before

transaction

Market Value after transaction

5% Bonus Base

5% Bonus

LWA Base

LWA Rate

LWA LWA Available

for remainder of the year

Minimum Class Death

Benefit

Minimum Class

Contract Maturity Benefit

May 1, 2025 75 3-year Contract Anniversary

458,769 458,769 458,769 458,769 5.50% 25,232 24,341 458,769 93,799

Dec 31, 2025 75 Withdrawal at year End 24,341 471,098 446,756 458,769

No Bonus 458,769 5.50% 25,232 435,065 88,952

Dec 31, 2026 76 Withdrawal at year End 25,232 528,789 503,557 458,769

No Bonus 458,769 5.50% 25,232 414,305 84,708

Dec 31, 2027 77 Withdrawal at year End 25,232 560,674 535,442 458,769

No Bonus 458,769 5.50% 25,232 395,660 80,895

May 1, 2028 78 3-year Contract Anniversary

555,212 555,212 555,212 555,212 5.50% 30,537 29,211 555,212 80,895

Dec 31, 2028 78 Withdrawal at year End 29,211 594,753 565,542 555,212

No Bonus 555,212 5.50% 30,537 527,944 76,922

Dec 31, 2029 79 Withdrawal at year End 30,537 640,277 609,740 555,212

No Bonus 555,212 5.50% 30,537 502,763 73,253

May 1, 2030 80 80 year DB Reset check 620,502 620,502 555,212 555,212 5.50% 30,537 620,502 73,253 Dec 31, 2030 80 Withdrawal at year End

30,537 642,125 611,588 555,212 No

Bonus 555,212 5.50% 30,537 590,993 69,770 May 1, 2031 81 3-year Contract

Anniversary 627,846 627,846 627,846 627,846 6.00% 37,671 35,887 590,993 69,770

Dec 31, 2031 81 Withdrawal at year End 35,887 660,361 624,474 627,846

No Bonus 627,846 6.00% 37,671 558,876 65,978

Key points • Since withdrawals are taken every year, there is no 5% Bonus. • GLWB resets occur every three years on the Contract Anniversary Date, if the market value of the Income Class units is greater than or equal to the

LWA Base. • On May 1, 2025, there is an automatic GLWB reset. The 5% Bonus Base and the LWA Base increase and a new, higher LWA Rate is attained.

Because Mary is 75 and in a higher age tier, her LWA Rate is increased to 5.5% (see page 6 for LWA Rate table). • Calc: The LWA is recalculated immediately, 5.5%*$458,769 = $25,232 and a prorated LWA is available for remainder of the year = remaining available

LWA prior to GLWB Reset + (recalculated LWA after GLWB reset - LWA prior to LWA Base addition)* quarterly proration = $21,668 + ($25,232 - $21,668)*3/4 = $24,341.

• Death Benefit Resets occur every three years on the Contract Anniversary Date, if the market value is greater than the current Minimum Class Death Benefit. The last reset of the Minimum Class Death Benefit occurs on the Contract Anniversary Date in the year in which Mary turns age 80.

• On May 1, 2031, there is an automatic GLWB reset. Mary is 81 and in a higher age tier. This results in an increase to her LWA Rate to 6.0% and a recalculated LWA = $37,671. Her prorated LWA available for remainder of the year = $35,887.

Income Class – Guarantee Scenarios

September 2010 – Page 15

Scenario#6–MakingwithdrawalsbeforetheLWAbecomesavailable(EarlyWithdrawal) SituationBuilding on Scenario #4, this shows what happens if Mary needs to take income before the LWA is available.

Date Age Transaction Amount Market Value before

transaction

Market Value after transaction

5% Bonus Base

5% Bonus

LWA Base

LWA Rate

LWA LWA Available

for remainder of the year

Minimum Class Death

Benefit

Minimum Class

Contract Maturity Benefit

May 1, 2010 60 Initial Deposit 200,000 N/A 200,000 200,000 200,000 0.00% 200,000 150,000 Dec 31, 2010 60 Year End 212,544 212,544 200,000 7,500 207,500 0.00% 200,000 150,000 Dec 31, 2011 61 Year End 231,054 231,054 200,000 10,000 217,500 0.00% 200,000 150,000 Dec 31, 2012 62 Year End 249,425 249,425 200,000 10,000 227,500 0.00% 200,000 150,000

May 1, 2013 63 3-year Contract

Anniversary 257,365 257,365 257,365 257,365 0.00% 257,365 150,000

Dec 31, 2013 63 Early

Withdrawal 10,000 273,245 263,245 247,946 No

Bonus 247,946 0.00% 247,946 144,510 Dec 31, 2014 64 Year End 285,513 285,513 247,946 12,397 260,344 5.00% 13,017 247,946 144,510

Dec 31, 2015 65 Withdrawal at

year End 13,017 308,045 295,028 247,946 No

Bonus 260,344 5.00% 13,017 237,469 138,404

May 1, 2016 66 3-year Contract

Anniversary 304,707 304,707 304,707 304,707 5.00% 15,235 14,681 304,707 138,404 Key points

• Any withdrawal made before the LWA Eligibility Date will proportionally reduce the 5% Bonus Base and the LWA Base. (eg. $10,000 w/d / $273,245 (MV) creates a 3.7% reduction to the 5% Bonus Base and the LWA Base.)

• Calc: For the withdrawal in 2013, the new 5% Bonus Base = prior 5% Bonus Base*(MV-WD)/MV = $257,365*($273,245 - $10,000)/$273,245 = $247,946 and the new LWA Base = prior LWA Base*(MV-WD)/MV = $257,365*($273,245 - $10,000)/$273,245 = $247,946.

• No 5% Bonus is applied on December 31, 2013, since a withdrawal was made during the 2013 calendar year. • On January 1, 2015, Mary’s LWA is $13,017; she can withdraw this amount for the rest of her life. (In Scenario #4, Mary’s LWA is $14,155).

Protect your income stream with the LWA Protection Service

• To assist in managing the GLWB, clients can use the LWA Protection Service. With this, any withdrawal that is requested prior to LWA Eligibility Date, or one that will exceed the LWA, is not processed until confirmation from the client or advisor (with underlying client consent) is received.

Income Class – Guarantee Scenarios

September 2010 – Page 16

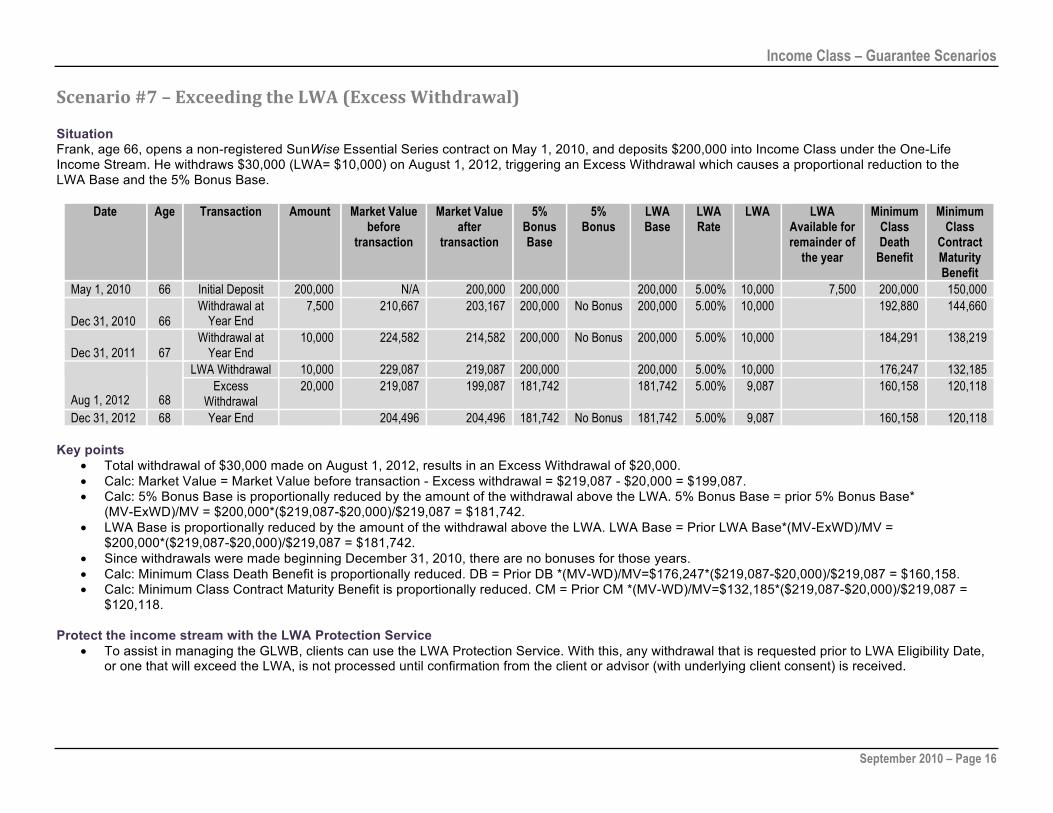

Scenario#7–ExceedingtheLWA(ExcessWithdrawal)Situation Frank, age 66, opens a non-registered SunWise Essential Series contract on May 1, 2010, and deposits $200,000 into Income Class under the One-Life Income Stream. He withdraws $30,000 (LWA= $10,000) on August 1, 2012, triggering an Excess Withdrawal which causes a proportional reduction to the LWA Base and the 5% Bonus Base.

Date Age Transaction Amount Market Value before

transaction

Market Value after

transaction

5% Bonus Base

5% Bonus

LWA Base

LWA Rate

LWA LWA Available for remainder of

the year

Minimum Class Death

Benefit

Minimum Class

Contract Maturity Benefit

May 1, 2010 66 Initial Deposit 200,000 N/A 200,000 200,000 200,000 5.00% 10,000 7,500 200,000 150,000

Dec 31, 2010 66 Withdrawal at

Year End 7,500 210,667 203,167 200,000 No Bonus 200,000 5.00% 10,000 192,880 144,660

Dec 31, 2011 67 Withdrawal at

Year End 10,000 224,582 214,582 200,000 No Bonus 200,000 5.00% 10,000 184,291 138,219

LWA Withdrawal 10,000 229,087 219,087 200,000 200,000 5.00% 10,000 176,247 132,185

Aug 1, 2012 68 Excess

Withdrawal 20,000 219,087 199,087 181,742 181,742 5.00% 9,087 160,158 120,118

Dec 31, 2012 68 Year End 204,496 204,496 181,742 No Bonus 181,742 5.00% 9,087 160,158 120,118 Key points

• Total withdrawal of $30,000 made on August 1, 2012, results in an Excess Withdrawal of $20,000. • Calc: Market Value = Market Value before transaction - Excess withdrawal = $219,087 - $20,000 = $199,087. • Calc: 5% Bonus Base is proportionally reduced by the amount of the withdrawal above the LWA. 5% Bonus Base = prior 5% Bonus Base*

(MV-ExWD)/MV = $200,000*($219,087-$20,000)/$219,087 = $181,742. • LWA Base is proportionally reduced by the amount of the withdrawal above the LWA. LWA Base = Prior LWA Base*(MV-ExWD)/MV =

$200,000*($219,087-$20,000)/$219,087 = $181,742. • Since withdrawals were made beginning December 31, 2010, there are no bonuses for those years. • Calc: Minimum Class Death Benefit is proportionally reduced. DB = Prior DB *(MV-WD)/MV=$176,247*($219,087-$20,000)/$219,087 = $160,158. • Calc: Minimum Class Contract Maturity Benefit is proportionally reduced. CM = Prior CM *(MV-WD)/MV=$132,185*($219,087-$20,000)/$219,087 =

$120,118. Protect the income stream with the LWA Protection Service

• To assist in managing the GLWB, clients can use the LWA Protection Service. With this, any withdrawal that is requested prior to LWA Eligibility Date, or one that will exceed the LWA, is not processed until confirmation from the client or advisor (with underlying client consent) is received.

Income Class – Guarantee Scenarios

September 2010 – Page 17

Scenario#8–RRIFMinimumAnnualPaymentgreaterthantheLWAallowsclienttowithdrawMAPwithoutincurringproportionalreduction(RRIFcontractholdingIncomeClassunitsonly) SituationDan, age 71, opens a SunWise Essential Series RRIF contract on May 1, 2010, and deposits $150,000 into Income Class under the One-Life Income Stream.

Date Age Transaction Amount Market Value before

transaction

Market Value after transaction

5% Bonus Base

5% Bonus

LWA Base

LWA Rate

LWA LWA Available for remainder of

the year

RRIF MAP

%

RRIF MAP for

following year

May 1, 2010 71 Initial Deposit 150,000 N/A 150,000 150,000 150,000 5.25% 7,875 5,906 Dec 31, 2010 71 Year End 151,835 151,835 150,000 5,625 155,625 5.25% 8,170 7.38% 11,205

Dec 31, 2011 72 Withdrawal at

Year End 11,205 157,682 146,477 150,000 No

Bonus 155,625 5.25% 8,170 7.48% 10,956

Dec 31, 2012 73 Withdrawal at

Year End 10,956 153,789 142,832 150,000 No

Bonus 155,625 5.25% 8,170 7.59% 10,841

May 1, 2013 74 3-year Contract

Anniversary 145,191 145,191 150,000 155,625 5.25% 8,170 8,170

Dec 31, 2013 74 Withdrawal at

Year End 10,841 149,908 139,067 150,000 No

Bonus 155,625 5.25% 8,170 7.71% 10,722 Key points

• Calc: At age 71, the LWA is established (subject to quarterly proration) for the first year. LWA = initial deposit* LWA Rate* quarterly proration = $150,000 * 5.25%*3/4 = $5,906.

• No withdrawal is required from the RRIF contract in the first calendar year. • Calc: Since no withdrawals were made in the first calendar year, a prorated 5% Bonus is applied ($150,000*5%*3/4 = $5,625). • At age 72, the LWA is $8,170, however, MAP is 7.38%*$151,835 = $11,205 (MAP amount is calculated on December 31 and must be withdrawn

the following year). Dan is allowed to withdraw MAP without incurring a proportional reduction in the LWA Base or the 5% Bonus Base.

Income Class – Guarantee Scenarios

September 2010 – Page 18

Scenario#9–RRIFcontractholdingInvestmentandIncomeClass(showsthedifferencebetweencontractlevelMAPandLWARRIFMAP)SituationJoe, age 71, opens a SunWise Essential Series RRIF contract on July 31, 2010, and deposits $50,000 into Investment Class and $150,000 into Income Class under the One-Life Income Stream.

Key points

• No withdrawal is required from the RRIF contract in the first calendar year. • Calc: At age 71, the LWA is established (subject to quarterly proration) for the first year. LWA = initial deposit* LWA Rate* quarterly

proration = $150,000 * 5.25%*2/4 = $3,938. • Calc: Since no withdrawals were made in the first calendar year, a prorated 5% Bonus is applied ($150,000*5%*2/4 = $3,750). • The first reset date for the entire contract and each class is July 31, 2013, regardless of when subsequent deposits are made and new classes opened. • Calc: In 2011, Joe must withdraw the contract MAP of 7.38%* ($54,000 + $160,000) = $15,793 (MAP amount is calculated on December 31 and must

be withdrawn the following year). Joe’s LWA is $8,071, however, his LWA RRIF MAP = MAP in effect for that calendar year * (total Income Class units on January 1 of that calendar year/ total units allocated to the contract on January 1 of that calendar year) = $15,793*($160,000/($54,000 + $160,000)) = $11,808. Joe is allowed to withdraw the LWA RRIF MAP amount without incurring a proportional reduction in LWA Base and the 5% Bonus Base.

• Joe withdraws $11,808 from Income Class and the remaining MAP, $3,985, from Investment Class. If Joe withdraws more than $11,808 from his Income Class units it would be considered an Excess Withdrawal resulting in a proportional reduction in future income payments.

Date Age Transaction Class Amount Market Value after transaction

5% Bonus Base

5% Bonus

LWA Base

LWA Rate

LWA Contract MAP %

Contract MAP for

following year

RRIF MAP

%

LWA RIF MAP for

following year

71 Initial Deposit Investment Class 50,000 Jul 31, 2010 Income Class 150,000 150,000 150,000 5.25% 7,875

71 Year end Investment Class 54,000 Dec 31, 2010 Income Class 160,000 150,000 3,750 153,750 5.25% 8,071 7.38% 15,793 7.38% 11,808

72 RRIF MAP Withdrawal Investment Class 3,985 50,015

Sept 1, 2011 RRIF MAP Withdrawal Income Class 11,808 148,192 150,000 153,750

72 Year end Investment Class 52,000

Dec 31, 2011 Income Class 149,000 150,000 No

Bonus 153,750 5.25% 8,071 7.48% 15,034 7.48% 11,145

Income Class – Guarantee Scenarios

September 2010 – Page 19

Scenario#10–RRIFminimumtakenfromtheInvestmentClasstomaximize5%BonusintheIncomeClass(advantageoftheonecontractstructure)SituationBuilding on Scenario #9, Joe decides to maximize his 5% Bonus and take his entire RRIF MAP from Investment Class.

Date Age Transaction Class Amount Market Value after

Transaction

5% Bonus Base

5% Bonus

LWA Base

LWA Rate

LWA Contract MAP %

Contract MAP for

following year

RRIF MAP

%

LWA RIF MAP for

following year

71 Initial Deposit Investment

Class 50,000

Jul 31, 2010 Income Class 150,000 150,000 150,000 5.25% 7,875

71 Year end Investment

Class 54,000 Dec 31, 2010 Income Class 160,000 150,000 3,750 153,750 5.25% 8,072 7.38% 15,793 7.38% 11,808

72 RRIF MAP Withdrawal

Investment Class 15,793 38,207

Sept 1, 2011 Income Class 160,000 150,000 153,750

72 Year end Investment

Class 39,723 Dec 31, 2011 Income Class 160,872 150,000 7,500 161,250 5.25% 8,466 7.48% 15,005 7.48% 12,033

Key points

• No withdrawal is required from the RRIF contract in the first calendar year. • Calc: Since no withdrawals were made in the first calendar year, a prorated 5% Bonus is applied ($150,000*5%*2/4 = $3,750). • In 2011, at age 72, Joe must withdraw the contract MAP of 7.38%*($54,000 + $160,000) = $15,793. He takes this amount from Investment Class to

preserve his 5% Bonus. • Joe’s LWA Base increases by $7,500 on December 31, 2011, due to the 5% Bonus. • This shows how he is able to withdraw the amount required from his RRIF without making withdrawals from Income Class. This allows him to preserve

his 5% Bonus, which will increase his LWA in the future.

Income Class – Guarantee Scenarios

September 2010 – Page 20

Scenario#11–RRIFminimumtakenfromInvestmentClasstomaximize5%BonusinIncomeClass(advantageoftheonecontractstructure)–ExtendedVersion SituationJim decides to maximize his 5% Bonus by investing $50,000 in Investment Class to take his RRIF MAP and $150,000 into Income Class.

Date Age Transaction Class Amount Market Value after

Transaction

5% Bonus Base

5% Bonus

LWA Base

LWA Rate

LWA Contract MAP %

Contract MAP for

following year

RRIF MAP

%

LWA RIF MAP for

following year

71 Transfer to RRIF

Investment Class 50,000

Mar 1, 2011 Income Class 150,000 150,000 150,000 5.25% 7,875 71 Year End Investment Class 53,000

Dec 31, 2011 Income Class 156,630 150,000 7,500 157,500 5.25% 8,269 7.38% 15,471

7.38% 11,559 72 RRIF MAP W/d Investment Class 15,471 40,709

Dec 31, 2012 Income Class 148,100 150,000 7,500 165,000 5.25% 8,663 7.48% 14,123

7.48% 11,078 73 RRIF MAP W/d Investment Class 14,123 29,029

Dec 31, 2013 Income Class 160,187 150,000 7,500 172,500 5.25% 9,056 7.59% 14,361

7.59% 12,158 74 RRIF MAP W/d Investment Class 14,361 16,409

Dec 31, 2014 Income Class 184,379 150,000 7,500 180,000 5.50% 9,900 7.71% 15,481

7.71% 14,216 75 RRIF MAP W/d Investment Class 15,481 1,913

Dec 31, 2015 Income Class 182,536 150,000 7,500 187,500 5.50% 10,313 7.85% 14,479

7.85% 14,329 76 RRIF MAP W/d Investment Class 2,028 0

Dec 31, 2016 Income Class 12,452 183,569 150,000 No Bonus 187,500 5.50% 10,313 7.99% 14,667

7.99% 14,667 77 RRIF MAP W/d Investment Class

Dec 31, 2017 Income Class 14,667 184,770 150,000 No Bonus 187,500 5.50% 10,313 8.15% 15,059 8.15% 15,059 78 RRIF MAP W/d Investment Class

Dec 31, 2018 Income Class 15,059 199,386 150,000 No Bonus 187,500 5.50% 10,313 8.33% 16,609 8.33% 16,609 Key points

• In 2012, at age 72, Jim must withdraw the contract MAP of 7.38%* ($53,000 + $156,630) = $15,471. He takes this amount from Investment Class to preserve his 5% Bonus on Income Class.

• Jim’s LWA Base increases by $7,500 on December 31, 2011, due to the 5% Bonus. • This shows how Jim is able to withdraw the amount required from his RRIF without making withdrawals from Income Class to preserve his 5% Bonus,

which will increase his LWA in the future. Jim makes four RRIF MAP withdrawals before exhausting his Investment Class investments and is able to increase his LWA Base to $187,500 through bonuses at the same time.

• No GLWB Resets occurred between 2011 and 2018, as a result of the LWA Base being greater than market value on every third contract anniversary.

Income Class – Guarantee Scenarios

September 2010 – Page 21

Scenario#12–HowLWABaseadditionsafterLWACommencementDateimpactGLWBvalueswhenthereisaresetandtheLWARateincreases(higherLWARateforLWABaseAdditioninhigheragetier) Situation Wayne, age 69, opens a non-registered SunWise Essential Series contract on May 1, 2010, and deposits $100,000 into Income Class under the One-Life Income Stream. On November 25, 2014, age 73, he makes a subsequent deposit (LWA Base Addition) of $75,000.

Date Age Transaction Amount Market Value Before

transaction

Market Value After transaction

5% Bonus Base

5% Bonus

LWA Base

LWA Rate

LWA LWA Available

for remainder of the year

Minimum Class Death

Benefit

Minimum Class

Contract Maturity Benefit

May 1, 2010 69 Initial Deposit 100,000 N/A 100,000 100,000 100,000 5.00% 5,000 3,750 100,000 75,000

Dec 31, 2010 69 Withdrawal at Year End 3,750 106,521 102,771 100,000 No Bonus 100,000 5.00% 5,000 96,480 72,360

Dec 31, 2011 70 Withdrawal at Year End 5,000 111,712 106,712 100,000 No Bonus 100,000 5.00% 5,000 92,161 69,121

Dec 31, 2012 71 Withdrawal at Year End 5,000 114,182 109,182 100,000 No Bonus 100,000 5.00% 5,000 88,126 66,094

May 1, 2013 72 3-year Contract

Anniversary 112,093 112,093 112,093 112,093 5.25% 5,885 5,664 112,093 66,094

Dec 31, 2013 72 Withdrawal at Year End 5,664 117,916 112,252 112,093 No Bonus 112,093 5.25% 5,885 106,709 62,920

Nov 25, 2014 73 Deposit 75,000 122,168 197,168 187,093 187,093 5.25% 9,822 6,869 181,709 119,170

Dec 31, 2014 73 Withdrawal at Year End 6,869 198,790 191,920 187,093 No Bonus 187,093 5.25% 9,822 175,430 115,052

Dec 31, 2015 74 Withdrawal at Year End 9,822 209,491 199,668 187,093 No Bonus 187,093 5.25% 9,822 167,205 109,657

Key points

• On May 1, 2013, there is an automatic GLWB reset. Wayne is age 72 and in a higher age tier, resulting in an increase to his LWA Rate to 5.25%. • He makes a subsequent deposit (LWA Base Addition) on November 25, 2014, of $75,000. This amount will also be at the higher age tier of 5.25%. • Calc: The LWA Base Addition increases the 5% Bonus Base = $112,093 + $75,000 = $187,093 and the LWA Base = $112,093 + $75,000 = $187,093. • The LWA Base Addition increases the LWA = $187,093*5.25% = $9,822. Since Wayne has not made any withdrawals year-to-date, the LWA Available

for remainder of the year = $5,885 + ($9,822 - $5,885)*1/4 = $6,869. • Calc: Minimum Class Death Benefit increases immediately by 100% of LWA Base Addition. Death Benefit = $106,709 + $75,000*100% = $181,709. • Calc: Minimum Class Contract Maturity Benefit increases immediately by 75% of the LWA Base Addition = $62,920 + $75,000*75% = $119,170.

Income Class – Guarantee Scenarios

September 2010 – Page 22

Scenario#13–HowLWABaseAdditionsafterLWACommencementDateimpacttheGLWBvalueswhenthereisnoGLWBresetandnoLWARateincrease(blendedLWARate) SituationBuilding on Scenario #12, this shows what happens when there are low returns and no GLWB resets. On November 25, 2014, at age 73, Wayne makes a subsequent deposit (LWA Base Addition) of $75,000.

Date Age Transaction Amount Market Value before transaction

Market Value after transaction

5% Bonus Base

5% Bonus

LWA Base

LWA Rate

LWA LWA Available for remainder of

the year

Minimum Class Death

Benefit

Minimum Class

Contract Maturity Benefit

May 1, 2010 69 Initial Deposit 100,000 N/A 100,000 100,000 100,000 5.00% 5,000 3,750 100,000 75,000

Dec 31, 2010 69 Withdrawal at

Year End 3,750 106,521 102,771 100,000 No

Bonus 100,000 5.00% 5,000 96,480 72,360

Dec 31, 2011 70 Withdrawal at

Year End 5,000 106,882 101,882 100,000 No

Bonus 100,000 5.00% 5,000 91,966 68,975

Dec 31, 2012 71 Withdrawal at

Year End 5,000 103,919 98,919 100,000 No

Bonus 100,000 5.00% 5,000 87,541 65,656

May 1, 2013 72 3-year Contract

Anniversary 97,271 97,271 100,000 100,000 5.00% 5,000 5,000 97,271 65,656

Dec 31, 2013 72 Withdrawal at

Year End 5,000 93,973 88,973 100,000 No

Bonus 100,000 5.00% 5,000 92,095 62,163 Nov 25, 2014 73 Deposit 75,000 91,420 166,420 175,000 175,000 5.11% 8,938 5,984 167,095 118,413

Dec 31, 2014 73 Withdrawal at

Year End 5,984 166,836 160,852 175,000 No

Bonus 175,000 5.11% 8,938 161,102 114,165

Dec 31, 2015 74 Withdrawal at

Year End 8,938 172,354 163,417 175,000 No

Bonus 175,000 5.11% 8,938 152,748 108,245 Key points

• Wayne does not receive a GLWB reset on May 1, 2013, and his LWA Rate remains at 5%. He receives a Death Benefit Reset to $97,271. • Wayne makes a subsequent deposit (LWA Base Addition) on November 25, 2014, of $75,000. This amount will be at the higher age tier of 5.25%. • Calc: The LWA Base Addition increases the 5% Bonus Base = $100,000 + $75,000 = $175,000 and the LWA Base = $100,000 + $75,000 = $175,000 • Calc: LWA Base Addition increases the LWA Rate to a blended rate:

(prior LWA Base)/(prior LWA Base + LWA Base Addition)*LWA% at prior year + (LWA Base Addition)/(prior LWA Base + LWA Base Addition)* LWA% at LWA addition age = $100,000/($100,000+$75,000)*5% + $75,000/($100,000+$75,000)*5.25%= 5.11%.

• The LWA Base Addition increases the LWA = $175,000*5.11% = $8,938. Since Wayne has not made any withdrawals year-to-date, the LWA Available for remainder of the year = $5,000 + ($8,938 - $5,000)*1/4 = $5,984.

• Calc: Minimum Class Death Benefit increases immediately by 100% of LWA Base Addition. Death Benefit = $92,095 +$75,000*100% = $167,095. • Calc: Minimum Class Contract Maturity Benefit increases immediately by 75% of the LWA Base Addition = $62,163 + $75,000*75% = $118,413.

Income Class – Guarantee Scenarios

September 2010 – Page 23

Scenario#14–TwoLifeIncomeStreamselected(incomedeferred) Situation Emma, age 60 and her spouse, Sam, age 65, open a non-registered, joint annuitant, SunWise Essential Series contract on May 1, 2010, and deposit $250,000 into Income Class under the Two-Life Income Stream. This scenario illustrates that there is no LWA before the year the younger of the two lives turns age 65. In this scenario Emma and Sam wait until the LWA becomes available to take income and take advantage of the 5% Bonus and GLWB resets. If they decide to take withdrawals before the LWA Eligibility Date, each Early Withdrawal would reduce the 5% Bonus Base and the LWA Base proportionally.

Date Emma Age

Sam Age

Transaction Amount Market Value before transaction

Market Value after transaction

5% Bonus Base

5% Bonus LWA Base

LWA Rate

LWA Minimum Class Death

Benefit May 1, 2010 60 65 Initial Deposit 250,000 N/A 250,000 250,000 250,000 0.00% 250,000 Dec 31, 2010 60 65 Year End 260,061 260,061 250,000 9,375 259,375 0.00% 250,000 Dec 31, 2011 61 66 Year End 273,070 273,070 250,000 12,500 271,875 0.00% 250,000 Dec 31, 2012 62 67 Year End 294,322 294,322 250,000 12,500 284,375 0.00% 250,000

May 1, 2013 63 68 3-year Contract

Anniversary 305,031 305,031 305,031 305,031 0.00% 305,031 Dec 31, 2013 63 68 Year End 326,449 326,449 305,031 15,252 320,283 0.00% 305,031 Dec 31, 2014 64 69 Year End 357,876 357,876 305,031 15,252 335,534 4.50% 15,099 305,031

Dec 31, 2015 65 70 Withdrawal at

Year End 15,099 378,425 363,326 305,031 No Bonus 335,534 4.50% 15,099 292,861 Key points

• Contract Anniversary Date is set at date of time of initial deposit, May 1, 2010. • Emma and Sam receive a GLWB reset on May 1, 2013. The 5% Bonus Base, LWA Base and Minimum Class Death Benefit are reset to $305,031. • The LWA is zero until the younger of the two lives (i.e., Emma) reaches the LWA Eligibility Date on January 1, 2015. • In 2015, the LWA Rate at the time of the first withdrawal is 4.5%. This is based on the younger of the two lives, (Emma, age 65) and the Two-Life

age tier. • Calc: On December 31, 2014, the LWA is calculated for the following year. LWA = 4.50% * $335,534 = $15,099 and available the January 1, 2015.

Income Class – Guarantee Scenarios

September 2010 – Page 24

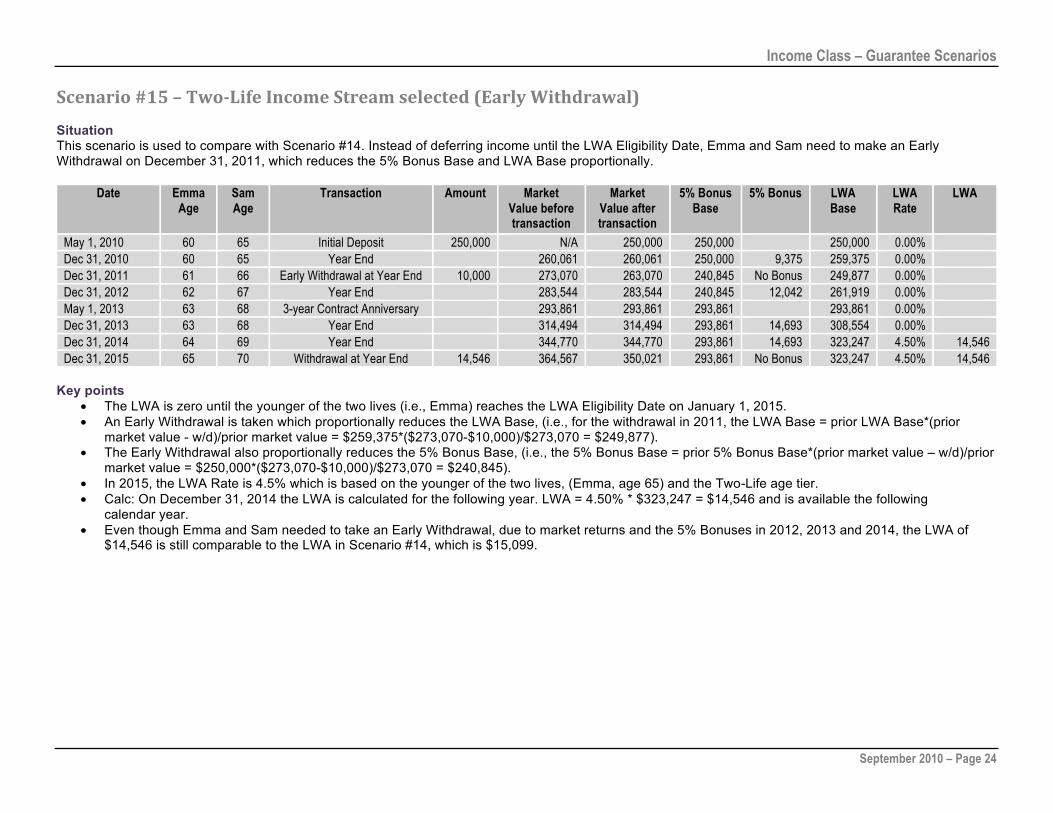

Scenario#15–TwoLifeIncomeStreamselected(EarlyWithdrawal) SituationThis scenario is used to compare with Scenario #14. Instead of deferring income until the LWA Eligibility Date, Emma and Sam need to make an Early Withdrawal on December 31, 2011, which reduces the 5% Bonus Base and LWA Base proportionally.

Date Emma Age

Sam Age

Transaction Amount Market Value before transaction

Market Value after transaction

5% Bonus Base

5% Bonus LWA Base

LWA Rate

LWA

May 1, 2010 60 65 Initial Deposit 250,000 N/A 250,000 250,000 250,000 0.00% Dec 31, 2010 60 65 Year End 260,061 260,061 250,000 9,375 259,375 0.00% Dec 31, 2011 61 66 Early Withdrawal at Year End 10,000 273,070 263,070 240,845 No Bonus 249,877 0.00% Dec 31, 2012 62 67 Year End 283,544 283,544 240,845 12,042 261,919 0.00% May 1, 2013 63 68 3-year Contract Anniversary 293,861 293,861 293,861 293,861 0.00% Dec 31, 2013 63 68 Year End 314,494 314,494 293,861 14,693 308,554 0.00% Dec 31, 2014 64 69 Year End 344,770 344,770 293,861 14,693 323,247 4.50% 14,546 Dec 31, 2015 65 70 Withdrawal at Year End 14,546 364,567 350,021 293,861 No Bonus 323,247 4.50% 14,546

Key points

• The LWA is zero until the younger of the two lives (i.e., Emma) reaches the LWA Eligibility Date on January 1, 2015. • An Early Withdrawal is taken which proportionally reduces the LWA Base, (i.e., for the withdrawal in 2011, the LWA Base = prior LWA Base*(prior

market value - w/d)/prior market value = $259,375*($273,070-$10,000)/$273,070 = $249,877). • The Early Withdrawal also proportionally reduces the 5% Bonus Base, (i.e., the 5% Bonus Base = prior 5% Bonus Base*(prior market value – w/d)/prior

market value = $250,000*($273,070-$10,000)/$273,070 = $240,845). • In 2015, the LWA Rate is 4.5% which is based on the younger of the two lives, (Emma, age 65) and the Two-Life age tier. • Calc: On December 31, 2014 the LWA is calculated for the following year. LWA = 4.50% * $323,247 = $14,546 and is available the following

calendar year. • Even though Emma and Sam needed to take an Early Withdrawal, due to market returns and the 5% Bonuses in 2012, 2013 and 2014, the LWA of

$14,546 is still comparable to the LWA in Scenario #14, which is $15,099.

Income Class – Guarantee Scenarios

September 2010 – Page 25

Scenario#16–SettingupaTwoLifeIncomeStream,nonregisteredaccount(negativereturns) SituationEmma, age 65 and her spouse Sam, age 70, deposit $250,000 into Income Class under the Two-Life Income Stream and begin taking their LWA of $11,250 immediately. The initial LWA rate is 4.5% based on Emma’s age and the Two-Life age tier. (The first year is a prorated LWA = $11,250* (3/4)) =$8,438.

Key points

• Due to negative market returns, no resets occur. • Annuitant (Emma) passes away on November 15, 2020. Since the Two-Life Income Stream was chosen, the LWA remains the same at $11,250.

Sam as Owner and Annuitant of the contract can continue to take withdrawals of the LWA for the remainder of his life. • The Minimum Class Death Benefit is not an option on Emma's death, as the contract continues until the death of the last survivor of the two lives

(i.e., Sam).

Date Emma Age

Sam Age

Transaction Amount Market Value before transaction

Market Value after transaction

5% Bonus Base

5% Bonus LWA Base

LWA Rate

LWA Minimum Class Death

Benefit May 1, 2010 65 70 Initial Deposit 250,000 N/A 250,000 250,000 250,000 4.50% 8,438 250,000 Dec 31, 2010 65 70 Withdrawal at Year End 8,438 246,682 238,244 250,000 No Bonus 250,000 4.50% 11,250 241,449 Dec 31, 2011 66 71 Withdrawal at Year End 11,250 233,593 222,343 250,000 No Bonus 250,000 4.50% 11,250 229,821

Withdrawals Continue Dec 31, 2017 72 77 Withdrawal at Year End 11,250 144,034 132,784 250,000 No Bonus 250,000 4.50% 11,250 154,911 Dec 31, 2018 73 78 Withdrawal at Year End 11,250 130,156 118,906 250,000 No Bonus 250,000 4.50% 11,250 141,521

May 1, 2019 74 79 3-year Contract

Anniversary 118,116 118,116 250,000 250,000 4.50% 11,250 141,521 Dec 31, 2019 74 79 Withdrawal at Year End 11,250 116,538 105,288 250,000 No Bonus 250,000 4.50% 11,250 127,860 Nov 15, 2020 75 80 Annuitant Dies (Emma) 103,895 103,895 250,000 250,000 4.50% 11,250 127,860 Dec 31, 2020 N/A 80 Withdrawal at Year End 11,250 103,224 91,974 250,000 No Bonus 250,000 4.50% 11,250 113,925

Income Class – Guarantee Scenarios

September 2010 – Page 26

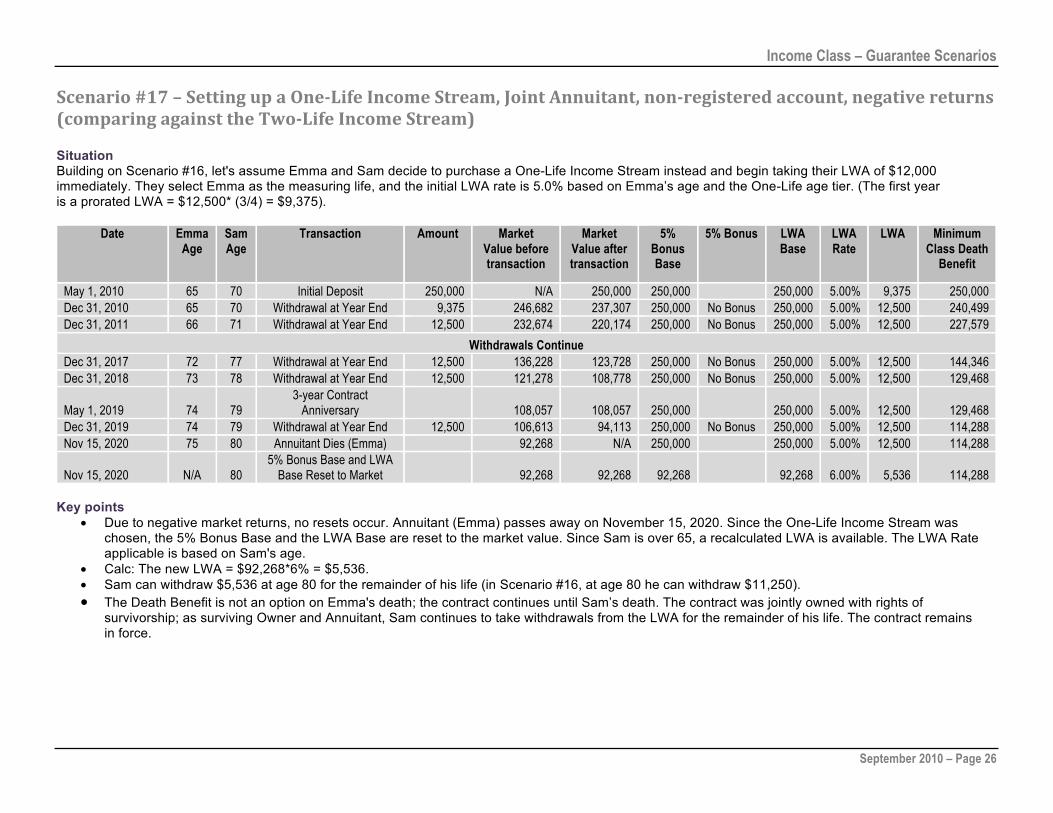

Scenario#17–SettingupaOneLifeIncomeStream,JointAnnuitant,nonregisteredaccount,negativereturns(comparingagainsttheTwoLifeIncomeStream)SituationBuilding on Scenario #16, let's assume Emma and Sam decide to purchase a One-Life Income Stream instead and begin taking their LWA of $12,000 immediately. They select Emma as the measuring life, and the initial LWA rate is 5.0% based on Emma’s age and the One-Life age tier. (The first year is a prorated LWA = $12,500* (3/4) = $9,375).

Date Emma Age

Sam Age

Transaction Amount Market Value before transaction

Market Value after transaction

5% Bonus Base

5% Bonus LWA Base

LWA Rate

LWA Minimum Class Death

Benefit

May 1, 2010 65 70 Initial Deposit 250,000 N/A 250,000 250,000 250,000 5.00% 9,375 250,000 Dec 31, 2010 65 70 Withdrawal at Year End 9,375 246,682 237,307 250,000 No Bonus 250,000 5.00% 12,500 240,499 Dec 31, 2011 66 71 Withdrawal at Year End 12,500 232,674 220,174 250,000 No Bonus 250,000 5.00% 12,500 227,579

Withdrawals Continue Dec 31, 2017 72 77 Withdrawal at Year End 12,500 136,228 123,728 250,000 No Bonus 250,000 5.00% 12,500 144,346 Dec 31, 2018 73 78 Withdrawal at Year End 12,500 121,278 108,778 250,000 No Bonus 250,000 5.00% 12,500 129,468

May 1, 2019 74 79 3-year Contract

Anniversary 108,057 108,057 250,000 250,000 5.00% 12,500 129,468 Dec 31, 2019 74 79 Withdrawal at Year End 12,500 106,613 94,113 250,000 No Bonus 250,000 5.00% 12,500 114,288 Nov 15, 2020 75 80 Annuitant Dies (Emma) 92,268 N/A 250,000 250,000 5.00% 12,500 114,288

Nov 15, 2020 N/A 80 5% Bonus Base and LWA

Base Reset to Market 92,268 92,268 92,268 92,268 6.00% 5,536 114,288 Key points

• Due to negative market returns, no resets occur. Annuitant (Emma) passes away on November 15, 2020. Since the One-Life Income Stream was chosen, the 5% Bonus Base and the LWA Base are reset to the market value. Since Sam is over 65, a recalculated LWA is available. The LWA Rate applicable is based on Sam's age.

• Calc: The new LWA = $92,268*6% = $5,536. • Sam can withdraw $5,536 at age 80 for the remainder of his life (in Scenario #16, at age 80 he can withdraw $11,250). • The Death Benefit is not an option on Emma's death; the contract continues until Sam’s death. The contract was jointly owned with rights of

survivorship; as surviving Owner and Annuitant, Sam continues to take withdrawals from the LWA for the remainder of his life. The contract remains in force.

Income Class – Guarantee Scenarios

September 2010 – Page 27

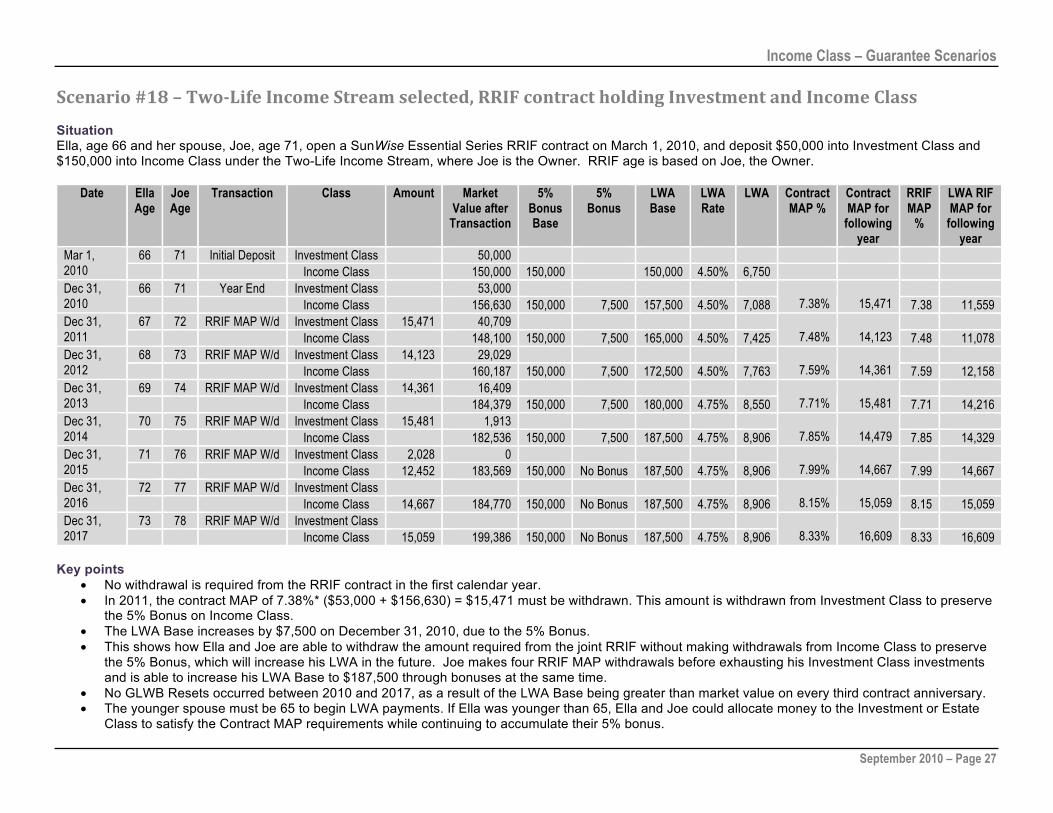

Scenario#18–TwoLifeIncomeStreamselected,RRIFcontractholdingInvestmentandIncomeClass SituationElla, age 66 and her spouse, Joe, age 71, open a SunWise Essential Series RRIF contract on March 1, 2010, and deposit $50,000 into Investment Class and $150,000 into Income Class under the Two-Life Income Stream, where Joe is the Owner. RRIF age is based on Joe, the Owner.

Date Ella Age

Joe Age

Transaction Class Amount Market Value after

Transaction

5% Bonus Base

5% Bonus

LWA Base

LWA Rate

LWA Contract MAP %

Contract MAP for

following year

RRIF MAP

%

LWA RIF MAP for

following year

66 71 Initial Deposit Investment Class 50,000 Mar 1, 2010 Income Class 150,000 150,000 150,000 4.50% 6,750

66 71 Year End Investment Class 53,000 Dec 31, 2010 Income Class 156,630 150,000 7,500 157,500 4.50% 7,088 7.38% 15,471 7.38 11,559

67 72 RRIF MAP W/d Investment Class 15,471 40,709 Dec 31, 2011 Income Class 148,100 150,000 7,500 165,000 4.50% 7,425 7.48% 14,123 7.48 11,078

68 73 RRIF MAP W/d Investment Class 14,123 29,029 Dec 31, 2012 Income Class 160,187 150,000 7,500 172,500 4.50% 7,763 7.59% 14,361 7.59 12,158

69 74 RRIF MAP W/d Investment Class 14,361 16,409 Dec 31, 2013 Income Class 184,379 150,000 7,500 180,000 4.75% 8,550 7.71% 15,481 7.71 14,216

70 75 RRIF MAP W/d Investment Class 15,481 1,913 Dec 31, 2014 Income Class 182,536 150,000 7,500 187,500 4.75% 8,906 7.85% 14,479 7.85 14,329

71 76 RRIF MAP W/d Investment Class 2,028 0 Dec 31, 2015 Income Class 12,452 183,569 150,000 No Bonus 187,500 4.75% 8,906 7.99% 14,667 7.99 14,667

72 77 RRIF MAP W/d Investment Class Dec 31, 2016 Income Class 14,667 184,770 150,000 No Bonus 187,500 4.75% 8,906 8.15% 15,059 8.15 15,059

73 78 RRIF MAP W/d Investment Class Dec 31, 2017 Income Class 15,059 199,386 150,000 No Bonus 187,500 4.75% 8,906 8.33% 16,609 8.33 16,609

Key points

• No withdrawal is required from the RRIF contract in the first calendar year. • In 2011, the contract MAP of 7.38%* ($53,000 + $156,630) = $15,471 must be withdrawn. This amount is withdrawn from Investment Class to preserve

the 5% Bonus on Income Class. • The LWA Base increases by $7,500 on December 31, 2010, due to the 5% Bonus. • This shows how Ella and Joe are able to withdraw the amount required from the joint RRIF without making withdrawals from Income Class to preserve

the 5% Bonus, which will increase his LWA in the future. Joe makes four RRIF MAP withdrawals before exhausting his Investment Class investments and is able to increase his LWA Base to $187,500 through bonuses at the same time.

• No GLWB Resets occurred between 2010 and 2017, as a result of the LWA Base being greater than market value on every third contract anniversary. • The younger spouse must be 65 to begin LWA payments. If Ella was younger than 65, Ella and Joe could allocate money to the Investment or Estate

Class to satisfy the Contract MAP requirements while continuing to accumulate their 5% bonus.

Income Class – Guarantee Scenarios

September 2010 – Page 28

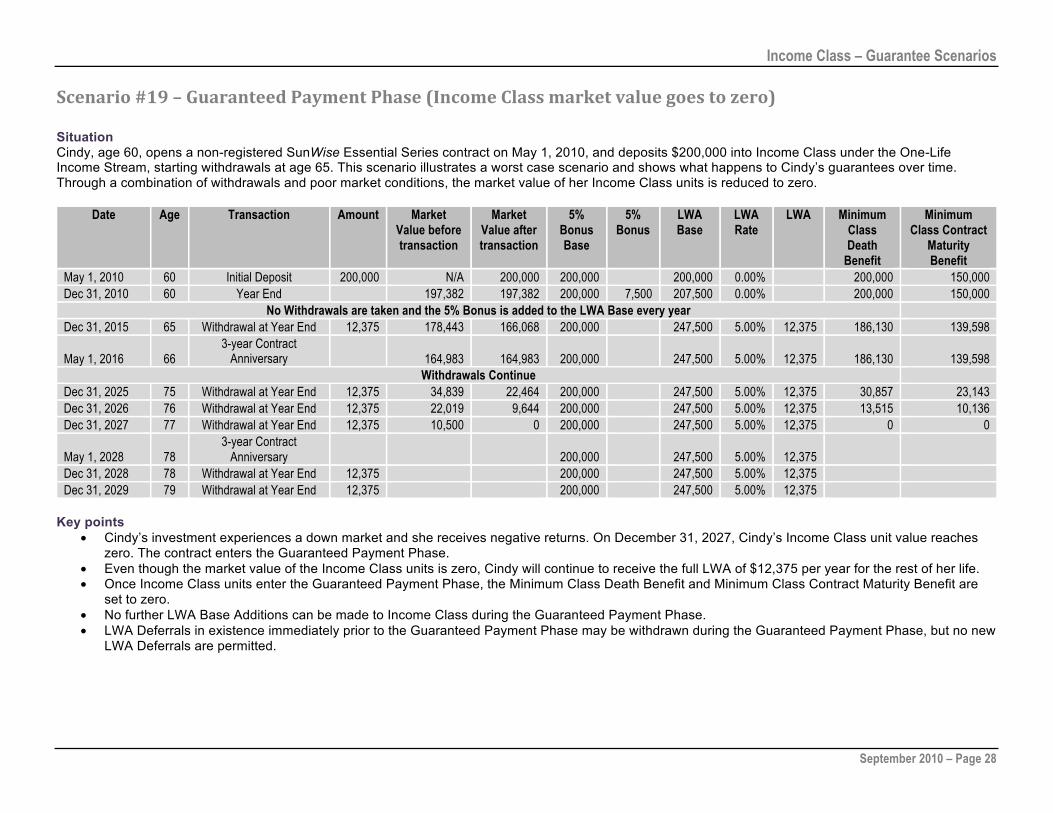

Scenario#19–GuaranteedPaymentPhase(IncomeClassmarketvaluegoestozero)

SituationCindy, age 60, opens a non-registered SunWise Essential Series contract on May 1, 2010, and deposits $200,000 into Income Class under the One-Life Income Stream, starting withdrawals at age 65. This scenario illustrates a worst case scenario and shows what happens to Cindy’s guarantees over time. Through a combination of withdrawals and poor market conditions, the market value of her Income Class units is reduced to zero.

Date Age Transaction Amount Market Value before transaction

Market Value after transaction

5% Bonus Base

5% Bonus

LWA Base

LWA Rate

LWA Minimum Class Death

Benefit

Minimum Class Contract

Maturity Benefit

May 1, 2010 60 Initial Deposit 200,000 N/A 200,000 200,000 200,000 0.00% 200,000 150,000 Dec 31, 2010 60 Year End 197,382 197,382 200,000 7,500 207,500 0.00% 200,000 150,000

No Withdrawals are taken and the 5% Bonus is added to the LWA Base every year Dec 31, 2015 65 Withdrawal at Year End 12,375 178,443 166,068 200,000 247,500 5.00% 12,375 186,130 139,598

May 1, 2016 66 3-year Contract

Anniversary 164,983 164,983 200,000 247,500 5.00% 12,375 186,130 139,598 Withdrawals Continue

Dec 31, 2025 75 Withdrawal at Year End 12,375 34,839 22,464 200,000 247,500 5.00% 12,375 30,857 23,143 Dec 31, 2026 76 Withdrawal at Year End 12,375 22,019 9,644 200,000 247,500 5.00% 12,375 13,515 10,136 Dec 31, 2027 77 Withdrawal at Year End 12,375 10,500 0 200,000 247,500 5.00% 12,375 0 0

May 1, 2028 78 3-year Contract

Anniversary 200,000 247,500 5.00% 12,375

Dec 31, 2028 78 Withdrawal at Year End 12,375 200,000 247,500 5.00% 12,375 Dec 31, 2029 79 Withdrawal at Year End 12,375 200,000 247,500 5.00% 12,375

Key points

• Cindy’s investment experiences a down market and she receives negative returns. On December 31, 2027, Cindy’s Income Class unit value reaches zero. The contract enters the Guaranteed Payment Phase.

• Even though the market value of the Income Class units is zero, Cindy will continue to receive the full LWA of $12,375 per year for the rest of her life. • Once Income Class units enter the Guaranteed Payment Phase, the Minimum Class Death Benefit and Minimum Class Contract Maturity Benefit are

set to zero. • No further LWA Base Additions can be made to Income Class during the Guaranteed Payment Phase. • LWA Deferrals in existence immediately prior to the Guaranteed Payment Phase may be withdrawn during the Guaranteed Payment Phase, but no new

LWA Deferrals are permitted.

Income Class – Guarantee Scenarios

September 2010 – Page 29

Scenario#20–LWADeferrals

Situation Bill, age 60, opens a non-registered SunWise Essential Series contract on May 1, 2010, and deposits $200,000 into Income Class under the One-Life Income Stream.

Date Age Transaction Amount Market

Value Before transaction

Market Value After transaction

5% Bonus Base

5% Bonus

LWA Base

LWA Rate

LWA LWA Available for remainder of

the year

LWA Deferral

Minimum Class Death

Benefit May 1, 2010 60 Initial Deposit 200,000 N/A 200,000 200,000 200,000 0.00% 200,000 Dec 31, 2010 60 Year End 212,814 212,814 200,000 7,500 207,500 0.00% 200,000

No Withdrawals Taken Dec 31, 2021 71 Year End 307,935 307,935 200,000 10,000 317,500 5.25% 16,669 259,840

May 1, 2022 72 3-year Contract

Anniversary 267,903 267,903 200,000 317,500 5.25% 16,669 16,669

267,903

Jul 31, 2022 72 Month

End/Withdrawal 10,000

284,583 274,583 200,000 317,500 5.25% 16,669 6,669

258,489 Dec 31, 2022 72 Year End 267,903 267,903 200,000 317,500 5.25% 16,669 6,669 258,489 Jan 1, 2023 72 267,903 267,903 200,000 317,500 5.25% 16,669 16,669 6,669 258,489

Key points

• Bill defers income in an up market until 2022, age 72. The LWA Rate is 5.25% since this is his first withdrawal and he is in the 70-74 age tier. LWA is calculated on December 31, 2021, = 5.25%*$317,500 = $16,669.

• During the years when no withdrawals were taken, Death Benefit Reset occurred, but no GLWB Resets occurred as a result of the LWA Base being greater than market value. The Minimum Class Death Benefit increased from $200,000 to $259,840 and again on May 1, 2022, increasing to $267,903.

• Bill’s first withdrawal is $10,000 on July 31, 2022. • Calc: Since Bill did not withdraw the full LWA entitlement in 2022, he receives a deferral of $6,669. On January 1, 2023, Bill is allowed to withdraw

$23,338 (LWA + LWA Deferral = $16,669 + $6,669 = $23,338).

Deferral rules: – deferrals cannot occur in a 5% Bonus Year – prior year deferrals to a 5% Bonus Year will continue – current LWA plus LWA Deferrals cannot exceed 15% of the LWA Base– deferrals are reset to zero whenever there is a GLWB Reset– existing Deferrals can be withdrawn during the Guaranteed Payment Phase but no new Deferrals are permitted.

Income Class – Guarantee Scenarios

September 2010 – Page 30

Scenario#21–LWAisgreaterthanLIFmaximumpayments(ThisshowshowclientsmaybepreventedfromtakingthefullLWAamountduetoLIFregulationsincertainyears.)

SituationMelanie, age 71, opens a SunWise Essential Series LIF contract on March 1, 2010 and deposits $250,000 into Income Class under the One-Life Income Stream. Her MAP amount on December 31, 2010, is 7.38% of the market value. Melanie’s pension is governed by Ontario pension legislation. There is no withdrawal in the first year and Melanie is allotted a 5% Bonus of $12,500, to her LWA Base.

Date Age Transaction Amount Market

Value before transaction

Market Value after transaction

5% Bonus Base

5% Bonus

LWA Base

LWA Rate

LWA Contract MAP %

Contract MAP for

following year

LIF MAX %

LIF MAX for

following year

Mar 1, 2010 71 Initial Deposit 250,000 N/A 250,000 250,000 250,000 5.25% 13,125 Dec 31, 2010 71 Year End 245,932 245,932 250,000 12,500 262,500 5.25% 13,781 7.38% 18,150 8.45% 20,793

Dec 31, 2011 72 Withdrawal at

Year End 18,150 240,509 222,359 250,000 262,500 5.25% 13,781 7.48% 16,632 8.71% 19,367

Withdrawals Continue

Dec 31, 2017 78 Withdrawal at

Year End 13,781 128,265 114,483 250,000 262,500 5.25% 13,781 8.33% 9,536 11.25% 12,882

Dec 31, 2018 79 Withdrawal at

Year End 12,882 112,240 99,357 250,000 262,500 5.25% 13,781 8.53% 8,475 11.96% 11,885

Dec 31, 2019 80 Withdrawal at

Year End 11,885 96,417 84,532 250,000 262,500 5.25% 13,781 8.75% 7,397 12.82% 10,835

Dec 31, 2020 81 Withdrawal at

Year End 10,835 83,039 72,204 250,000 262,500 5.25% 13,781 8.99% 6,491 13.87% 10,015

Key points • LIF Max % based on requirements as of January 1, 2010, for the province of Ontario. • At age 72, the LWA is $13, 781. The MAP is $18,150 and Melanie withdraws her MAP amount without any penalties. • At age 78, the LWA is $13, 781. The LIF max is $13,874 = 10.66% * MV on January 1, 2017 = 10.66% * $130,150.

Melanie can take her full LWA, $13,781. • At age 79, the LWA is $13, 781. The LIF max is $12,882. Melanie is only allowed to take $12,882 according to LIF regulations. • At age 80, the LWA is $13, 781. The LIF max is $11,885. Melanie is only allowed to take $11,885 according to LIF regulations. • At age 81, the LWA is $13, 781. The LIF max is $10,835. Melanie is only allowed to take $10,835 according to LIF regulations.

Income Class – Guarantee Scenarios

September 2010 – Page 31

Scenario#22–LWAisgreaterthanLIFmaximumpayments,unlock50%(ThisshowshowaclientcanreducetheimpactoftheLIFMaximumbyunlocking50%followingLIFguidelines.) Situation Building on Scenario #21, let’s assume Melanie decides to unlock 50% of her LIF and transfer it to a RRIF. There is no withdrawal in the first year and Melanie is allotted a 5% Bonus, $6,250, to her LWA Base for both her LIF and RRIF accounts.

Key points

• LIF Max % based on requirements as of January 1, 2010, for the provinces of Ontario. • At age 72, Melanie can withdraw $13,782 ($6,891 locked in LWA + $6,891 unlocked LWA). The contract MAP = ($122,966 + $122,966) * 7.38% =

$18,150 and Melanie withdraws her MAP amount without any penalties. • At age 78, Melanie can withdraw $13,782. LIF MAX = $6,935 = 10.66% * MV of LIF on January 1, 2017 = 10.66% * $65,060 ($6,891 LIF account +

$6,891 RRIF account) vs. previous example of $13,781. • At age 79, Melanie can withdraw $13,332. ($6,441 LIF account + $6,891 RRIF account) vs. previous example of $12,882. • At age 80, Melanie can withdraw $12,833. ($5,942 LIF Max + $6,891 RRIF account) vs. previous example of $11,855. • At age 81, Melanie can withdraw $12,309. ($5,418 LIF Max + $6,891 RRIF account) vs. previous example of $10,835.

Date Age Transaction Class Amount Market Value before Transaction

Market Value after

Transaction

LWA Base

LWA Rate

LWA MAP % MAP for following

year

LIF MAX %

LIF MAX for following

year 71 Initial Deposit LIF N/A 125,000 125,000 5.25% 6,563

Mar 1, 2010 RRIF N/A 125,000 125,000 5.25% 6,563 71 Year-End LIF 122,966 122,966 131,250 5.25% 6,891 7.38% 9,075 8.45% 10,391

Dec 31, 2010 Year-End RRIF 122,966 122,966 131,250 5.25% 6,891 7.38% 9,075 72 Withdrawal at Year-End LIF 9,075 120,254 111,180 131,250 5.25% 6,891 7.48% 8,316 8.71% 9,684

Dec 31, 2011 Withdrawal at Year-End RRIF 9,075 120,254 111,180 131,250 5.25% 6,891 7.48% 8,316 Withdrawals Continue

78 Withdrawal at Year-End LIF 6,891 64,132 57,242 131,250 5.25% 6,891 8.33% 4,768 11.25% 6,441 Dec 31, 2017 Withdrawal at Year-End RRIF 6,891 64,132 57,242 131,250 5.25% 6,891 8.33% 4,768

79 Withdrawal at Year-End LIF 6,441 56,120 49,679 131,250 5.25% 6,891 8.53% 4,238 11.96% 5,942 Dec 31, 2018 Withdrawal at Year-End RRIF 6,891 56,120 49,229 131,250 5.25% 6,891 8.53% 4,199

80 Withdrawal at Year-End LIF 5,942 48,208 42,266 131,250 5.25% 6,891 8.75% 3,698 12.82% 5,418 Dec 31, 2019 Withdrawal at Year-End RRIF 6,891 47,772 40,882 131,250 5.25% 6,891 8.75% 3,577

81 Withdrawal at Year-End LIF 5,418 41,519 36,102 131,250 5.25% 6,891 8.99% 3,246 13.87% 5,007 Dec 31, 2020 Withdrawal at Year-End RRIF 6,891 40,159 33,269 131,250 5.25% 6,891 8.99% 2,990

Income Class – Guarantee Scenarios

September 2010 – Page 32

Scenario#23–Latedepositreductionoverage75(80%DeathBenefitforthreeyears,100%thereafter) SituationJared, age 72, opens a non-registered SunWise Essential Series contract on March 1, 2010, and deposits $200,000 into Income Class under the One-Life Income Stream. Jared delays taking withdrawals to get the full benefit of the 5% Bonus and starts taking income in 2018, the year he turns 80. Jared makes a subsequent deposit into Income Class on February 15, 2014, at age 76.

Date Age Transaction Amount Market Value before

Transaction

Market Value after

Transaction

5% Bonus Base

5% Bonus

LWA Base

LWA Rate

LWA LWA Available

for remainder of the year

Minimum Class Death Benefit (Prior to Late Deposit

Reduction)

Minimum Class Death

Benefit (includes Late Deposit Reduction)

Mar 1, 2010 72 Initial Deposit 200,000 N/A 200,000 200,000 200,000 5.25% 10,500 10,500 200,000 Dec 31, 2010 72 Year-End 212,006 212,006 200,000 10,000 210,000 5.25% 11,025 200,000 Dec 31, 2011 73 Year-End 220,493 220,493 200,000 10,000 220,000 5.25% 11,550 200,000 Dec 31, 2012 74 Year-End 229,043 229,043 200,000 10,000 230,000 5.25% 12,075 200,000

Mar 1, 2013 75 3-year Contract

Anniversary 235,292 235,292 235,292 235,292 5.50% 12,941 12,941 235,292 Dec 31, 2013 75 Year-End 238,181 238,181 235,292 11,765 247,056 5.50% 13,588 235,292

Feb 15, 2014 76 Subsequent

Deposit 100,000 240,629 340,629 335,292 347,056 5.50% 19,088 19,088 335,292 315,292 Dec 31, 2014 76 Year-End 348,389 348,389 335,292 16,765 363,821 5.50% 20,010 335,292 315,292 Dec 31, 2015 77 Year-End 358,938 358,938 335,292 16,765 380,585 5.50% 20,932 335,292 315,292

Mar 1, 2016 78 3-year Contract

Anniversary 361,757 361,757 335,292 380,585 5.50% 20,932 20,932 361,757 340,516 Dec 31, 2016 78 Year-End 370,345 370,345 335,292 16,765 397,350 5.50% 21,854 361,757 340,516

Feb 15, 2017 79 Late Deposit

Reduction Expires 381,615 381,615 335,292 397,350 5.50% 21,854 21,854 361,757 361,757 Dec 31, 2017 79 Year-End 386,385 386,385 335,292 16,765 414,115 6.00% 24,847 361,757 361,757

Mar 1, 2018 80 Age 80 DB Reset

check 390,467 390,467 335,292 414,115 6.00% 24,847 24,847 390,467 390,467

Dec 31, 2018 80 Withdrawal at

Year-End 24,847 397,998 373,151 335,292 No

Bonus 414,115 6.00% 24,847 366,090 366,090

Income Class – Guarantee Scenarios

September 2010 – Page 33

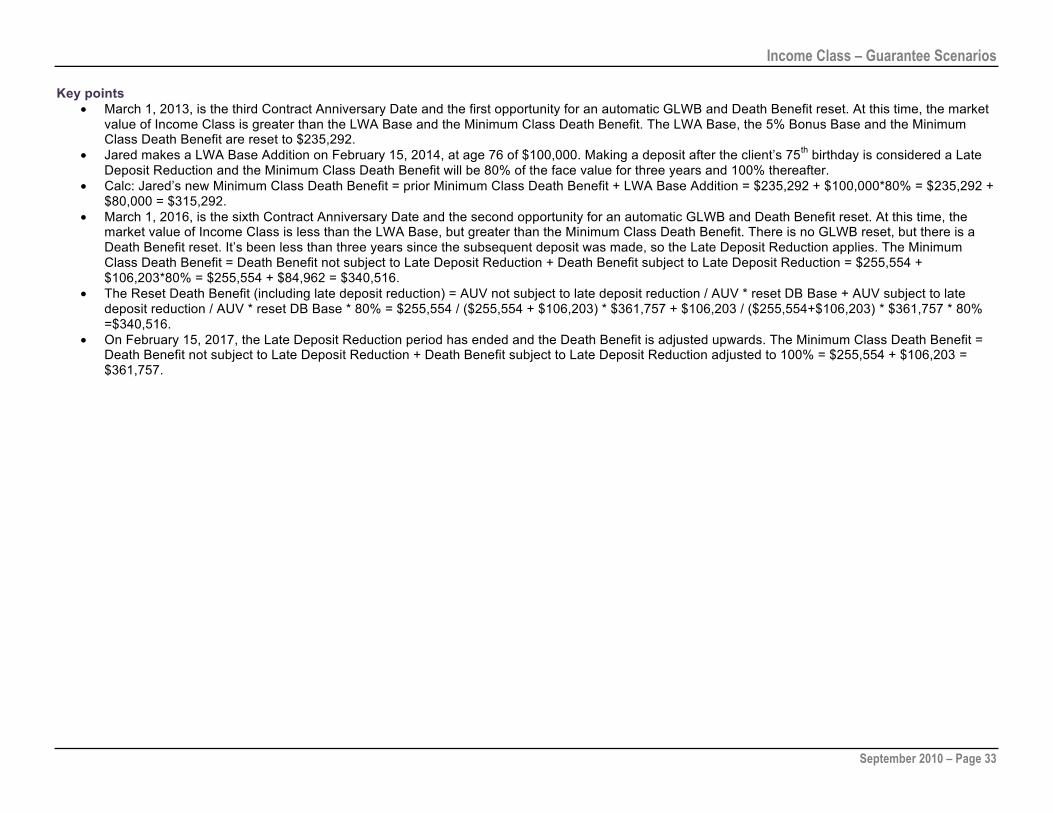

Key points • March 1, 2013, is the third Contract Anniversary Date and the first opportunity for an automatic GLWB and Death Benefit reset. At this time, the market

value of Income Class is greater than the LWA Base and the Minimum Class Death Benefit. The LWA Base, the 5% Bonus Base and the Minimum Class Death Benefit are reset to $235,292.

• Jared makes a LWA Base Addition on February 15, 2014, at age 76 of $100,000. Making a deposit after the client’s 75th birthday is considered a Late Deposit Reduction and the Minimum Class Death Benefit will be 80% of the face value for three years and 100% thereafter.

• Calc: Jared’s new Minimum Class Death Benefit = prior Minimum Class Death Benefit + LWA Base Addition = $235,292 + $100,000*80% = $235,292 + $80,000 = $315,292.

• March 1, 2016, is the sixth Contract Anniversary Date and the second opportunity for an automatic GLWB and Death Benefit reset. At this time, the market value of Income Class is less than the LWA Base, but greater than the Minimum Class Death Benefit. There is no GLWB reset, but there is a Death Benefit reset. It’s been less than three years since the subsequent deposit was made, so the Late Deposit Reduction applies. The Minimum Class Death Benefit = Death Benefit not subject to Late Deposit Reduction + Death Benefit subject to Late Deposit Reduction = $255,554 + $106,203*80% = $255,554 + $84,962 = $340,516.

• The Reset Death Benefit (including late deposit reduction) = AUV not subject to late deposit reduction / AUV * reset DB Base + AUV subject to late deposit reduction / AUV * reset DB Base * 80% = $255,554 / ($255,554 + $106,203) * $361,757 + $106,203 / ($255,554+$106,203) * $361,757 * 80% =$340,516.

• On February 15, 2017, the Late Deposit Reduction period has ended and the Death Benefit is adjusted upwards. The Minimum Class Death Benefit = Death Benefit not subject to Late Deposit Reduction + Death Benefit subject to Late Deposit Reduction adjusted to 100% = $255,554 + $106,203 = $361,757.

Income Class – Guarantee Scenarios

September 2010 – Page 34