in the name of allah, the most merciful, the most ... plan e 6-3.pdf · the international...

TRANSCRIPT

1

In The Name of Allah, the Most Merciful, the Most Compassionate

2

Introduction:The General Auditing Bureau (GAB) of the Kingdom of Saudi Arabia, guided by its ambitious goals and core values enshrined in its charter issued by the Royal Decree No. m/9 dated 1970, is determined to pursue its mission and fulfill its broad mandate with full objectivity, impartiality, efficiency and professionalism. It also has a genuine desire to keep up with new developments in its profession’s field, through the utilization of modern technological tools in conducting various audit operations, in accordance with the best practices and government audit standards.

To achieve such ambitious objectives, and overcome any challenges, GAB adopted, for the first time back in 2004, the concept of strategic planning as an effective methodology to strengthen its performance and accomplish its strategic goals. Accordingly, GAB issued its First Strategic Plan (2005 - 2009) which consisted of a number of important goals and priorities and was able to attain most of them despite some serious challenges, including human, technical and material difficulties.

Therefore, GAB was eager, in the process of developing its second strategic plan (2010 - 2014), to evaluate its limited experience in this field, in order to draw lessons learned and identify elements of strengths and weaknesses .

Over the past decade, GAB actively sought to accomplish its strategic goals and objectives. It has succeeded in introducing and implementing a number of important initiatives for the benefit of the public sector as a whole, chief among them are:

3

1. GAB undertook to organize an annual seminar for senior government officials from all audittees, with the aim of promoting cooperation and strengthening communication, to overcome common obstacles, in order to enhance public sector performance.

2. GAB succeeded in obtaining the Council of Ministers Resolution No.: 235, dated 20/ 8/ 1425 making the establishment of internal audit units in all government agencies mandatory.

3. The Council, also, approved GAB’s initiative to adopt electronic techniques by all public sector departments for: book-keeping, preparing financial statements and closing accounts, in order to enable GAB to implement its (IT) audit systems.

4. GAB also developed a unified internal audit regulations for all public sector entities, and secured its endorsement by the Council of Ministers Resolution No.: 129, dated 20/ 8/ 1425. Furthermore, GAB prepared guidelines to enable internal auditors to conduct their audit activities in an efficient and professional manner.

5. The Council of Ministers also adopted, by Resolution No.: 363, dated 15/ 9/ 2013, GAB’s recommendation to update the government accounting system and entrusted a committee of experts, led by GAB, with this important task.

In order to maintain the momentum for improving its performance, GAB prepared its Third Strategic Plan (1436 / 1440) by adopting a scientific methodology based on the evaluation outcome of its first and second strategic plans. It has also benefited greatly from the experience gained through its active membership in the International Organization of Supreme Audit Institutions (INTOSAI), as well as the relevant regional organizations, and the INTOSAI Development Initiative (IDI) guide for strategic planning.

4

The following five Strategic Goals have been identified:

Goal1: Improving Audit Quality in accordance with Relevant Professional Standards and Best Practices.

Goal2: Continuing GAB’s Policy for Human Resource Development and Institutional Capacity Building.

Goal3: Adopting and Gradually Implementing the INTOSAI Standards of Supreme Audit Institutions (ISSAI) and its Guidelines.

Goal4: Expanding Performance Audit and Ensuring Effective Revenue Collection Process for the Realization of Comprehensive Audit Objectives.

Goal5: Strengthening Cooperation and Knowledge Sharing with Relevant Professional Institutions, internally and Externally.

The Third Strategic Plan will also focus on a number of important priorities, including:

• Ensuring GAB’s full independence according to the UN Resolution No.: A/66 /209 of December 22, 2011.

• Strengthening GAB’s institutional capacities.

• Gradually implementing ISSAI and its guidelines.

• Improving audit outcome reports.

GAB, also, sought to align its strategic goals with the Kingdom’s reform policies and economic diversification, in addition to ensuring the provision of basic services to all citizens and the community as a whole through

5

extensive performance audit to help government agencies accomplish their stated goals in the national development plans. The central aim of this strategy is to enable GAB to fulfill its obligation under article (20&21) of its charter, to present highly credible and objective reports to H.M. the King, the Council of Ministers and the Shoura Council (Parliament), highlighting the performance quality of all government agencies and the overall financial position of the Kingdom.

Finally, it is an honor for me to present this Third Strategic Plan of the General Auditing Bureau, sincerely hoping that it will enable GAB and its technical staff to enhance their professional skills and render their duties efficiently. The ultimate aim is for GAB to become a credible audit institution that can conduct its mission with full independence, objectivity integrity and professionalism, to live up to the expectations of the Kingdom’s respected people and leadership.

Osama J. Faquih

President, General Auditing BureauKingdom of Saudi Arabia

6

1. GAB:General Auditing Bureau of Saudi Arabia

2. Strategic Planning:Is a long-term planning which takes into account changing conditions of the organization whether local, regional or international. Time-frame is changeable to the circumstances of the organization and the process includes developing the strategic plan, implementation of operational plans and projects and evaluating the results.

3. Strategic Plan:Is a document drafted at the first phase.

As for GAB’s strategic plan, it includes needs assessment, priority issues, mission, vision, core values, goals, objectives, performance indicators, essential factors for the realization of goals and detailed operational plans.

Glossary of Terms

7

4. Needs Assessment:A process for determining and addressing needs, or gaps between current conditions and desired conditions, in light of the best international and regional practices, future-oriented vision and changing business environment.

5. Mission:A statement expressing the purpose of the organization. It is spelled out in the Act of Establishment or Statute.

6. Vision:A written description of the organization

,s future and what it would like to achieve or

accomplish. It should be clear, brief, possible and unique.

7. Core Values:Values that guide the organization

,s internal conduct as well as its relationship with the

external world.

8. Strategic Priority Issues:Matters that play a direct role in achieving the mission of the organization and determining

8

goals. It can be identified through needs assessment.

9. Goals:Objectives to be achieved within a long period of time (for example: five years).

10. General Policies:A framework formulated and enforced by the governing body of the organization, to direct and limit its actions in pursuit of its goals.

11. Expected Results:The positive future outcomes of an action or process.

12. Objectives:Secondary goals that should be accomplished to reach relevant primary goals.

13. Performance Indicators:Pre-determined quantitative tools, by which an objective can be judged to have been achieved or not achieved against expected results, and then reported through periodic and annual reports.

9

14. Implementation Matrix:It serves as a bridge connecting the objectives and goals to the annual plans. It is designed to identify all projects for each related goal and objective and develop a timeframe that prioritizes actions, resources, elements of success and potential risks.

15. Projects:A group of homogeneous activities that have a particular aim, especially one that is organized by any organization.

16. Success Indicators:They reflect the critical success factors of the project.

17. Probable Risk:The probability of something happening that, if it occurs, has a negative effect on the objective or the project.

18. Operational Plan:

10

Short term (e.g. one year) plans formulated to accomplish projects or objectives.

19. Results Evaluation:A comparison of results achieved and identify work accomplished and progress of the project.

20. Electronic Data Process Auditing:The use of automated methods in audits. It is built to reduce cost and time for accurate and risk-free results.

21. Quality Assurance:It provides assurance that quality control systems and audits are being implemented properly to achieve high quality operations.

22. Quality Control:Policies intended to ensure that audit operations adhere to a defined set of quality criteria.

23. Professional Standards:

11

Audit practice standards derived from international and local standards and legislations.

24. Building Institutional Capacities:Development of knowledge, management, skills that enables an organization to perform effectively. It can be divided into two types:

• Institutional or organizational capacities: through developing organizational structures and implementing relevant operations.

• Professional Development: through increasing capabilities of GAB staff to perform their duties effectively as required.

12

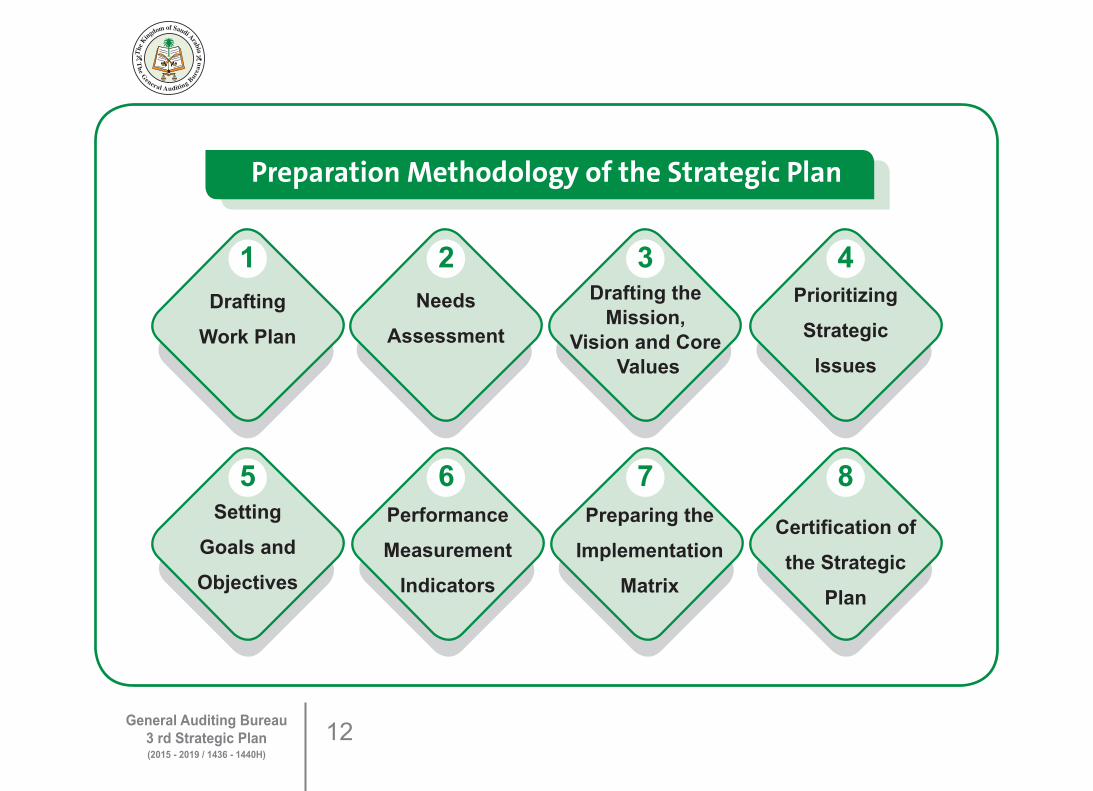

Prioritizing

Strategic

lssues

Certification of

the Strategic

Plan

Preparing the

Implementation

Matrix

Performance

Measurement

Indicators

Setting

Goals and

Objectives

Drafting theMission,

Vision and Core Values

Needs

AssessmentDrafting

Work Plan

4

8

3

7

2

6

1

5

Preparation Methodology of the Strategic Plan

13

Needs Assessment

Areas Gaps/GAB's Current Needs

GAB's Independence

and Legal Framework

- The need to Achieve complete financial and administrative independence.- Enhancing efforts aimed at transparency and accountability.

HumanResources

- Difficulty in attracting and maintaining competent employees due to lack of incentives and benefits in contrary to other government agencies and private sectors. - Stepping up training to meet GAB

,s actual needs.

- Lack of material, human and technical capabilities with high professional qualifications.- High turnover of auditors due to rigorous competition and availability of other external opportunities.- Absence of employees loyalty.

Auditing Standards and its

Methodology

- Limited application of auditing standards and manuals by auditors - Emphasizing the need for applying best practices in audit missions.- Gap between the authorized and applied procedures.

14

Governance- The need to apply quality assurance system on audit missions.- Incomplete operationalization of techniques and information systems.- The need for applying GAB’s Performance Measurement Framework.

InstitutionalSupport

- Expediting the use of safe means of communication and exchanging data electronically among GAB’s different departments and branches to create a paperless environment.- The need for enhancing GAB’s work environment.

Continuous Improvement

- The need for a wide application of modern audit techniques, like electronic audit and use of new programs in auditing. - Poor participation of GAB’s staff in auditing studies an research and in related disciplines. - The need to expand revenues audits.- Continuation of expanding the scope of performance and comprehensive audits.

GAB's Relations with Other

Related Agencies

- Continuation of strengthening cooperation with national organizations to improve professional performance. - Strengthening cooperation with international organizations.- Expanding the scope of cooperation with peer organizations.

Activation of Performance

Results

- Weak follow-up mechanism to track GAB’s recommendations. - Untimely communication of audit results. - Improving quality of audit reports.

15

Royal Directives and Council of Ministers’ Decrees.

The 9th Development Plan of the Kingdom.

Needs Assessment Report of GAB.

Shoura Council’s Debates and Recommendations Related to GAB and Other Government Agencies Annual Reports.

The Evaluation Results of the Implementation of the Second Strategic Plan.

Feedback from GAB's Departments and Branches.

1

2

3

4

5

6

Bases of Current Needs Assessment

16

To firmly implement audit of all state revenues and expenditures, audit of all fixed and current assets of the state, as well as auditing the performance of government agencies, including monitor of the proper use of public resources, efficiency, economy and effectiveness in order to reach the defined goals and objectives successfully.

A developed, professionally progressing, independent and credible auditing institution that contributes to enhancing the efficiency of audittees, strengthening the principles of transparency, governance and accountability.

Independence and Impartiality, Objectivity and Professionalism, Integrity and Credibility, Transparency and Accountability.

Mission

Vision

Core Values

17

Strategic Issues

No Strategy Relevant Strategic Goal

1 Adopting best practices in audit missions.

Goal 1Improving Audit Quality in Accordance with

Relevant Professional Standards and Best Practices

2 Reducing gap between authorized procedures and actions applied.

3 Application of quality assurance on audit missions.

4 Promoting the effective use of information systems and techniques

5Activating the spread use of communication means and exchanging data electronically among GAB’s different departments and branches to create a paperless environment.

6 Expanding the use of modern audit techniques, particularly electronic tools and EDP audit software.

7 Proposing more effective mechanism to follow-up GAB’s recommendations.

8 Accelerating communication of audit findings.

9 Present professional, objective, reliable reports.

18

No Strategy Relevant Strategic Goal10 Achieving full administrative and financial independence.

Goal 2Continuing GAB’s Policy for Human

Resource Development and Institutional Capacity Building

11 Enhancing Efforts aimed at Transparency and Accountability.

12 Attracting and maintaining competent employees.

13 Adopting training programs that meet GAB’s actual needs.

14 Qualifying and training auditors professionally.

15 Enhancing the sense of occupational loyalty in GAB’s employees.

16 Implementing a performance measurement framework for GAB

17 Improving GAB’s work environment.

18Encouraging GAB’s employees to engage in auditing studies and researches related to GAB’s functions.

19 Applying professional standards and audit manuals during the implementation of audit missions.

Goal 3 Adopting and Gradually Implementing

the INTOSAI Standards of Supreme Audit Institutions (ISSAI) and its Guidelines

Auditing Standards and Manuals.

20 Expanding the execution of revenues audit missions. Goal 4Expanding Performance Audit and Ensuring

Effective Revenue Collection Process for the Realization of Comprehensive Audit

Objectives21 Continuing the expansion of performance audit and comprehensive audit missions.

22 Cooperating with a specialized national entities to improve the professional performance. Goal 5Strengthening Cooperation and Knowledge

Sharing With Relevant Professional Institutions, Internally and Externally

23 Strengthening cooperation between GAB and related international organizations.

24 Strengthening communication with peer SAIs.

19

Priorities of the Third Strategic Plan

The current Statute of GAB needs to be updated to comply with the new developments in the administrative and financial aspects, in addition to the new developments in accounting, auditing and performance auditing in Saudi Arabia. In realizing the Royal Decree No.: 7593/M, dated 11/ 10/ 1992 stating that all current systems should be amended according to The Basic Law of GAB has re-visited its Statute that was issued by Royal Decree No.: 9, dated 07/ 04/ 1971. As a result, a new Statute was proposed to meet the new developments in GAB’s field of specialty. It has been put into consideration, while preparing the GAB’s Statute, issues of independence, identification of tasks and the methods of performing these tasks, in addition to the means of providing the basic financial, personnel, and technical requirements. GAB’s Statute was submitted to H.M the Custodian of the two Holy Mosques by letter No.: 22/S/W, dated March 29, 1998. Furthermore, GAB submitted to H.M for information the UN General Assembly Resolution number A/66/ 209: «Promoting the efficiency, accountability, effectiveness and transparency of public administration by strengthening Supreme Audit Institutions.», where the first paragraph of this resolution recognizes that: (Supreme Audit Institutions can accomplish their tasks objectively and effectively only if they are independent of the audited entities and are protected against outside influence). GAB in its turn, requested the Royal Court that this resolution is to be submitted to the Bureau of Experts at the Council of Ministers to be considered while preparing the study of promoting the control systems and Internal Control Units to enable these control systems to accomplish its duties effectively.

GAB,s efforts to achieve full administrative, financial, and organizational independence:

20

In conjunction with the support received from H.M,GAB will continue to follow-up the issuance of its new Statute to achieve the required financial and administrative independence. This step will enable GAB to perform its responsibilities in protecting the public fund with greater efficiency and higher professionalism and assures that all resources and public utilities are economically utilized. Furthermore, the new Statute will be providing auditors with the required incentives and immunity according to Lima and Mexico Declarations, and the UN Resolution number A/66/ 209, dated September 22, 2011.

The two previous GAB’s Strategic Plans (2004 - 2010) and (2011 - 2014) were focused on the capacity building of GAB and due care was used to develop and prepare human resources scientifically, practically and professionally in the fields of audit, accounting, performance audit, and financial analysis. Moreover, efforts have been made to enhance work methods and to apply the professional standards and quality systems that aim to increase productivity and enhance the quality of performance. The previous Strategic Plans, also, devoted care to create a good work environment to help its staff to perform their duties according to the best professional methods and practices. In this regard, GAB has signed contracts of building new offices for its head quarter and all branches in the kingdom. In the area of capacity building, GAB has enrolled many of its staff in training institution and specialize organizations inside and outside the Kingdom. Furthermore, GAB has set up programs of scholarship to its staff to study for the master and high diploma in accounting, auditing and information technology.

GAB is more than determined to continue its quest for building its capacity by continuing to perform a specialized training programs to raise the professional level of auditors and at the same time applying a Performance Measurement Framework (PMF). Furthermore, GAB is seeking to have in hand GAB’s new headquarter and branches buildings earlier so that it can be equipped with latest technical solutions to provide its employees with a good working environment.

2- Maintaining and developing capacity building of GAB:

21

GAB is devoted to enable its staff to perform audits according to the best professional practices. Therefore, GAB started issuing audit manuals since 1978. The title of the first audit manual issued was: «Auditors Manual of instructions in General Auditing Bureau of Saudi Arabia». Since then 17 audit manuals have been issued. Additionally, GAB is now moving forward updating these manuals by a group of experts according to new developments in the audit field. GAB designated the 10th Annual Seminar to identify the importance of the audit standards titled: «Role of the Government Audit Standards in Promoting efficient Audit Work».

Adopting the 3rd Strategic Plan will enable GAB to expand the application of professional standards and audit manuals and will allow updating these manuals. The plan will, also, contain programs for raising the awareness of the importance of these manuals to GAB’s employees.

GAB realizes the importance of clarifying the concepts of transparency, disclosure, accountability, and is trying to activate the positive audit concept. GAB, also, attaches great importance to its partnership with all audittees. This will promote the general interest of the country and will contribute in conducting economic, financial, and administrative reforms and protecting integrity and fighting corruption, along with providing all possible effective means of protecting the public fund. All these measures taken will have good impact on the national economy. GAB aims at benefiting positively from the rapid change in audit field and performance measurement. GAB successfully uses these tools and new developed techniques

3- Applying professional standards Criteria and Audit Manuals:

4- Quality Improvement of Audits and its Outputs:

22

35

Strategic GoalObjectives Responsibility Performance Measurement Indicators

(Achieving the Objective)Goal objective

4 - 1

− Increasing the scope of performance audit to include plans and programs of audittees.

− Assistant Vice-President for Performance Audit.

− Auditing the development programs for public education, judicial system, scholarships, housing and export diversification.

4 - 2− Focusing on civil services departments related to the welfare of citizens.

− Assistant Vice-President for Performance Audit.

− Carrying out annual audits in the field of education, health, municipalities, transportation, water, electricity and environment

4 - 3

− Continuing to supply the performance audit department with qualified auditors.

− Assistant Vice-President for Performance Audit.− Administrative and Financial Affairs Department.

Annually, increasing performance auditing staff by 10% annually.

4 - 4 − Adopting new methods in the field of revenue audit.

− Assistant Vice-President for Financial Audit.

− Adopting modern methods in revenue auditing.

4 - 5

− Organizing a specialized training courses in the field of income audit specially those related to taxation.

− Assistant Vice-President for Financial Audit. − Administrative Development Department.

− Introducing specialized courses for Zakat and income tax, custom and facilities auditing.− Annually, provide training to 20% of revenue auditing staff.

Goal 4: Expanding Perform

ance Audit and Ensuring Effective Revenue Collection Process for the Realization of Com

prehensive Audit Objectives.

36

Strategic GoalObjectives Responsibility Performance Measurement Indicators

(Achieving the Objective)Goal objective

4 - 6− Increasing regularly the number of revenue audit missions annually.

− Assistant Vice-President for Financial Audit.

− Annually, Increasing the number of revenue audits to 10%.

4 - 7− Continuing to supply the income audit department with qualified auditors.

− Assistant Vice-President for Financial Audit.− Administrative and Financial Affairs Department.

− Annually, increasing revenue auditing staff to 10%.

37

Strategic GoalObjectives Responsibility Performance Measurement Indicators

(Achieving the Objective)Goal objective

5 - 1

− Continuing to promote cooperation and exchange of expertise with other qualified audit entities and universities.

− President,s Office.

− Administrative Development Dept.

− Holding a biennial meeting with audit and professional agencies as well as universities.

5 - 2

− Sharing knowledge and exchange expertise with peer SAIs and related international and regional organizations.

- President,s Office.

− Administrative Development Dept.

− The effective participation in seminars and workshops.The participation in executing audit missions with peer agencies.

5 - 3

− Participating actively in the membership of professional and quality committees of the international and regional organizations.

− President,s Office.

− Administrative Development Dept.

− The participation of GAB representatives in professional and quality committees.

5 - 4

− Promoting the importance and value of GAB

,s role

and its effect on the national economy and community.

− President,s Office.

− Public Relations Dept. (Audit publication)

− Activating all means of social communication.

5 - 5

− Promoting cooperation and communication with audittees by holding the annual seminar and workshops to contribute in the improvement of its performance.

− President,s Office

− Administrative Development Dept.

− The continuance of holding the annual symposium for enhancing ways of cooperation between GAB and relevant agencies.

Goal 5: Strengthening Cooperation and Know

ledge Sharing with

Relevant Professional Institutions, Internally and Externally.

38

The most important Prerequisites of Success in implementing the Strategic Goals defined in the strategic plan are as follows:

• GAB leadership providing support to the process of attaining the strategic plan goals in order to realize GAB’s message and future-oriented vision.

• Providing the financial support during the period covered by the plan in order to cover the costs of implementing its projects.

• Formulating a team to measure and evaluate the annual and final results of implementing the strategic plan goals.

• Activation of efforts in the annual follow-up on the accomplishments of the operational plan through specifying the team or agency specialized in tracking the implementation of the plan, complying with principals of disclosure, transparency and data credibility, as well as considerations of flexibility in facing the variables and developments.

• The commitment of department, committees and work forces (all within their respective responsibilities) in implementing the operational plan according to the approved matrix of implementation.

Prerequisites of Success in Achieving the Strategic Plan Goals

39

• The appropriate selection of work force members, with observance of the integral distribution of roles between individuals participating in implementing the plan and enabling them to perform their duties.

• Overcoming obstacles on a periodic basis, avoiding unexpected variables that could affect the success of the plan and achieving the desired outcomes.

40

NO. Topic Page

1 Introduction 2

2 Glossary 6

3 Methodology 12

4 Needs Assessment 13

5 Sources Used in Assessment of Current Needs 15

6 Mission, Vision and Core Values 16

7 Priority Issues 17

8 Key Goals and Policies 23

9 Objectives 25

10 Performance Measurement Indicators 31

11 Prerequisites of Success in Achieving the Strategic Plan Goals 38

Content