in menat renewables - amazon simple storage services+wh… · who’s who in menat renewables will...

TRANSCRIPT

SPONSORED BY

IN MENAT RENEWABLES

ADVERTISING MEDIA PACK 2016/17

Everybody is aware of the massive potential for renewable energy in MENA & Turkey but it can be difficult for international companies to know who to talk to. Building on the success of the Desert Energy Leadership Summit, Dii is putting together an exclusive ‘who’s who’ list of the top 400 decision makers and thought leaders active in the region that will act as an authoritative guide to the sector and the region.

Who’s Who in MENAT Renewables will be distributed both digitally and in print and offers a unique opportunity to communicate directly with the industry’s top influencers and those who are looking for a route to market in the region.

Jack CeadelBusiness Development DirectorDii, Desert Energy Leadership SummitWho’s Who in MENAT Renewables

Who are the top 400 most influential people in the MENAT renewable energy sector?

CONTENT

Who’s Who in MENAT Renewables will provide invaluable insight into the ecosystem of the sector. Who are the rising stars in the big companies? Who is most active behind the scenes? Which markets are the CEO most excited about and why?

PROFILES WILL INCLUDE:

• Why you need to know this person• Career milestones and achievements• Personal market insights and thoughts for the future

WHO’S WHO WILL TELL YOU WHO IS THE MOST INFLUENTIAL IN THE FOLLOWING CATEGORIES:

• Government Ministers• Developers• Financiers• EPCs• Manufacturers• Suppliers• Tech Firms • Lawyers• Consultants

AUDIENCE & DISTRIBUTION

Who’s Who in MENAT Renewable will be distributed in print to all profiled executives, companies and agencies free of charge.

It will also be distributed at all major renewables events in MENAT and Europe.

A digital version will be available for download at our website in exchange for a marketing opt in.

Print: 2000 high quality printed books

Digital: online at our website

Events: Desert Energy Leadership Summit and other major industry events

IN MENAT RENEWABLES

WHY ADVERTISE?

Your brand, message or product will be in front of the most powerful and influential people in the renewables industry in MENAT and beyond. This book will be a fantastic resource that people will return to time and time again.

Who’s Who in MENAT Renewables will be on desks and board room tables where decisions are made for many months. It will be a conversation starter, a sign of achievement and it will be a definitive reference guide for the sector.

SPECIAL OFFERBook advertising this year and lock in the same rates for 2017.

Are you part of the Dii “Supporters of Desert Energy” network? Then you qualify for a 25% discount.

IN MENAT RENEWABLES

PROFILED ORGANIZATIONS

3M

5 Capitals

Aalborg

ABB

Abdul Latif Jameel

Abengoa Solar S.A.

Abu Dhabi Future Energy Company

Access Consultants Ltd.

Acciona Solar S.A

ACS Cobra

ACWA Power

Adenium Energy Capital

ADEREE

Advisian, WorleyParsons Group

ADWEA

Akuo Energy

Al Rajhi Banking and Investment Corp

Alcazar Energy

Alec Energy

Alfanar Construction Co.

ALSA Solar Systems

Alstom Grid

Altran Technologies S.A.

Amana Holdings

Ambata Capital Middle East

Apricum GmbH

Arab Renewable Energy Commission

Arbaah Capital

Archimede Solar Energy Srl

Archimede Solar S.L.R.

Arthur D. Little

Arup

Astrom Technical Advisors

Attijariwafa Bank

Authority for Electricity Regulation, Oman (AER)

Avancis GmbH & Co. Kg

AWS TRUEPOWER

Baker & MacKenzie

Bayern LB

Belectric Middle East

Bracewell & Giuliani

BrightSource Energy

Brookstone Partners

Building Energy

Canadian Solar

Capital Bank

Castalia Strategic Advisors

CESI

Cevital S.p.a.

Chadbourne & Parke

Chrysalix Energy Venture Capital

Citadel Capital

Citi

Clean Energy Business Council

CLS Energy Consultants

COMPANY

Conergy

Corys Environment

DEG

Desert Technologies

Deutsche Bank AG

DEWA

DNV GL AS

Dorsch Holding GmbH

Dubai Electricity and Water Authority

Dubai Electricity and Water Authority (DEWA)

Dubai Supreme Council of Energy

E.ON Climate & Renewables GmbH

E.ON Masdar Integrated Carbon LLC

EBRD - European Bank For Reconstruction And Development

EcoSolifer AG

EDF Energies Nouvelles

Effergy energia

EFG Hermes

El Sewedy Electric Group

Elecnor S.A

Electricity & Cogeneration Regulatory Authority (ECRA)

Elsewedy Electric Company

EMIRATES ENVIRONMENTAL GROUP

Empresarios Agrupados

Enara

ENEL Green Power

Energynest

enerray

Enerwhere

Engie

Enviromena Power Systems

ERG Renew spa

Ernst and Young

eSolar

EU GCC Clean Energy Network

European Jordanian Renewable Energy Projects

Eversheds

FEWA

First Gulf Bank

First Solar

FMO Entrepreneurial Development Bank

Fonds National pour la Maîtrise de l’Energie - FNME

Fotowatio Renewable Ventures

Fraunhofer ISE

Frenell

Fronius

FRV

FRV Services Middle East DMCC

Full Power Solution

Gamesa

GE Gulf

GE Middle East

GEK TERNA Group

GeoModel Solar

GeoModel Solar s.r.o.

Gestamp Wind

Ghorfa, Arab-German Chamber of Commerce and Industry

GlassPoint

GP Tech (Green Power Technologies)

Green Emirates

Green Gulf Holding

GreenGulf Inc.

Greenpeace

Gulf Cooperation Council Interconnection Authority

Gulf New Energy

Hassan Allam Construction

Heindl Energy GmbH

Helios Investment Partners

Heliovis

HSBC

Huiyin Group

IGEL Electric

ILF Beratende Ingenieure GmbH

Industrial and Commercial Bank of China

Infinity Solar

Infra Invest

Intec

International Energy Agency

International Finance Corporation

Intesa Sanpaolo S.p.A — Dubai Branch

Investec Bank Limited

IRENA

IRESEN

Italcementi Group

Italgen S.p.A.

JA Solar

Jinko Solar

JinkoSolar Holding Co., Ltd

Jordan Kuwait Bank

Jordanian Ministry of Energy and Mineral Resources (MEMR)

PROFILED ORGANIZATIONS

Jordanian National Electric Power Company (NEPCO)

Juwi

KACO New Energy

KAN Renewables

KAUST

Kawar Energy

KEMA Middle East Fze

Khaled Juffali Energy and Utilities

King Abdullah City for Atomic and Renewable Energy

KPMG

Kuwait Institute for Scientific Research (KISR)

Kuwait Oil Company

Lahmeyer International GmbH

League of Arab States

Lekela

Leoni

M+W Group

MAC GROUP FINANCIAL ADVISOR ENERGY

Macquarie Capital

Mainstream Renewable Power

Martifer Solar

Martifer Solar S.A.

MASDAR

MASEN

Max Planck Institute

Millennium Energy Industries (Catalyst Private Equity)

Ministry of Economy and Planning, Saudi Arabia

Ministry of Electricity and Energy

Ministry of Energy and Industry

Ministry of Energy and Mineral Resources (MEMR)

Monitor Deloitte

Moroccan Ministry of Energy

Moroccan Ministry of Environment

Munich RE

Nareva

Nareva Holding

National Bank of Abu Dhabi

National Electric Power Company (NEPCO)

Nedbank Capital Limited

New and Renewable Energy Authority (NREA)

NOMAC First National Operation & Maintenance Co. LTD

NOMADD Desert Solar

Norton Rose Fullbright

NRG Energy Inc

Nur Energie Limited

ONEE

Orascom Construction

Paradigm Change Capital Partners

Paradise Capital

Phoenix Solar

Poyry PLC

PPP Organizing Unit

PSA

Public Authority for Electricity and Water (PAEW)

PwC Middle East

Qatar Solar

Qmega

Qudra Energy

RCREE

RCREEE (Regional Center for Renewable Energy and Energy Efficiency)

REC Solar

Red Eléctrica Internacional S.A.

Red Med Group

RedMed

Rioglass Solar Intrernational

RnE Partner

Roland Berger

Royal Air Maroc

RSB for Electricity & Water

RWE

RWE New Energy Ltd.

Sabanci Holding

Saudi Aramco

Saudi Aramco Energy Ventures

Saudi Electricity Company

Saudi Electricity Company (SEC)

Saudi Electricity Company (SEC)

Saudi Minisitry of Water and Electricity

SAUDI MINISTRY OF WATER & ELECTRICITY

Saudi National Power Company

Saudi Oger

Scatec Solar

Schmid Group

SENER

SEWA

Shams Energy Solutions LLC

SIE (Energy Investment Organization)

Siemens

Siemens Technologies S.A.E.

Siemens Wind

SkyPower

SkyPower Global

SMA Middle East Ltd.

SMA Solar Technology

Société d’Investissements Energétiques (SIE)

Societe Nationale de l’Electricite et du Gaz (Sonelgaz)

Soitec Solar GmbH

Solar Reserve

Solar Shams

Solar Tower Systems GmbH

Solar Ventures

Solarcentury

SolarReserve

SolarWorld

Solida Energias Renovables S.L

Sowitec Group GmbH

Standard Chartered

Sun Infinite

SunCan Co Ltd

SUNTECH, DUBAI

Suntrace GmbH

Swicorp

Synergy Consulting Inc.

Tafoli

TAQA Arabia

TaylorHopkinson Associates

Terna

Terna Energy

Terra Nex

Terra Nex Financial Engineering

The Electricity &Co-Generation Regulatory Authority (ECRA)

The Future Energy Consulting Company Limited

The Oman Power and Water Procurement Company (OPWP)

TSK

TSK Flagsol

TSK Grupo

Tunisian Electricity and Gas Company (Société Tunisienne d’Electricite et du Gaz) - STEG

Tunisian Ministry of Energy

TÜV Süd

Vestas Mediterranean

WIP GmbH & Co KG . PV Solar Technologies

World Bank

Yingli Solar

RATES & OPTIONS

WHO’S WHO — PRINT

Full page spread*

Half page spread

Full page Half page Half page Third page Third page Quarter page

Orientation

Shape Vertical Horizontal Vertical Horizontal Island Vertical Horizontal Island

Bleed in mm (WxH)

425 x 302 385 x 135 215 x 302 195 x 135 130 x 195 70 x 255 195 x 85 130 x 120

Print area in mm (WxH)

420 x 297 380 x 130 210 x 297 190 x 130 125 x 190 65 x 250 190 x 80 115 x 125

Rate $4,000 $3,000 $2,400 $1,600 $1,600 $1,200 $1,200 $950

Dii Partner Rate

$3,000 $2,250 $1,800 $1,200 $1,200 $900 $900 $725

RENEWABLE ENERGY LIST — DIGITAL ADVERTISINGUp to 4 banner rotations allowed for each position visible on all pages

• Leaderboard: 728 x 90 pixels• Expanding banner: 728 x 270 pixels• Half page banner: 300 x 600 pixels• Medium rectangle banner: 300 x 250 pixels File types supported: SWF, GIF, PNG, JPG

Interested in digital advertising? We would love to discuss options with you. Please send me an email to [email protected]

ACCEPTED PRINT• PDF (preferred) press optimized

PDF/X-1a. Industry standard fonts must be embedded• EPS (CMYK) all fonts and graphics to be included in

the file• TIF/JPG (300dpi) dimensions must be consistent with

purchased ad size

ACCEPTED ONLINE & DIGITAL• JPEG, GIF, animated GIF or SWF. eNewsletters do not

accept animated files• Files should be no larger than 30KB• All files should be provided with URL to create weblink

DELIVERY• Email (for files under 15MB): Please email your artwork to

Jack Ceadel [email protected] • Post: physical material to be sent to:

Media Analytics Ltd, Suite C, Kingsmead House, Oxpens Road, Oxford OX1 1XX, UK

EXAMPLE PAGES

7

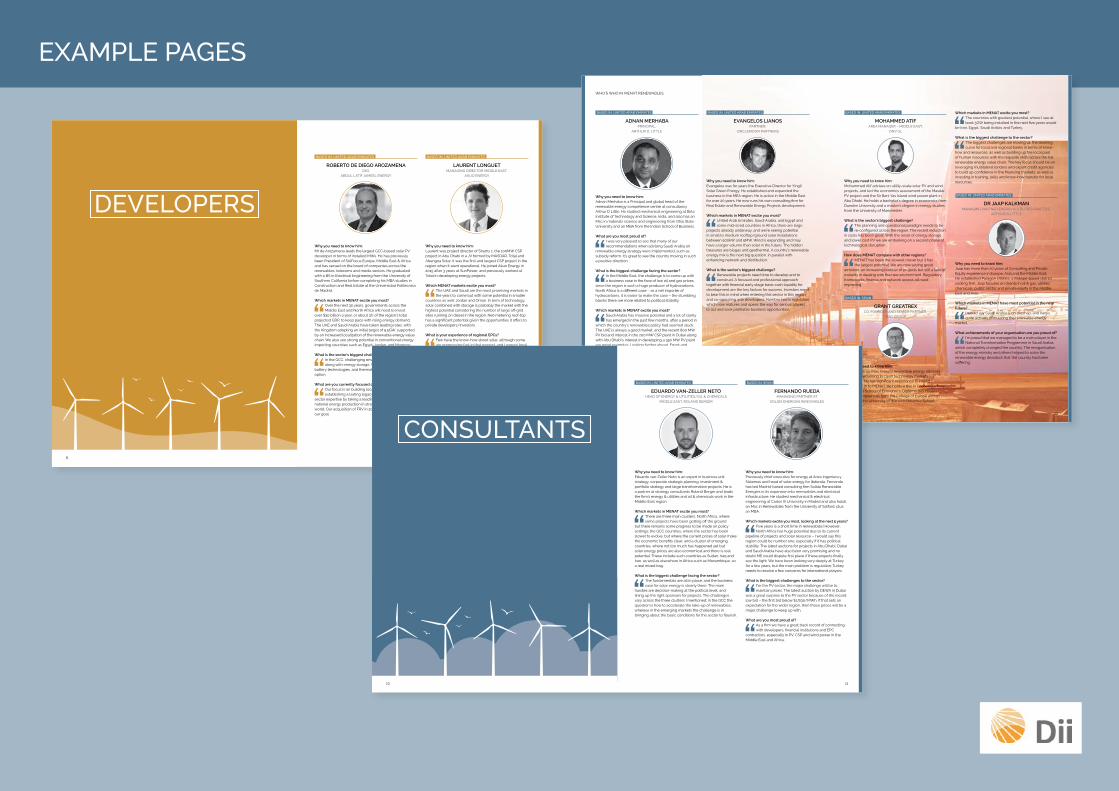

BASED IN: UNITED ARAB EMIRATES

ROBERTO DE DIEGO AROZAMENACEO,

ABDUL LATIF JAMEEL ENERGY

Why you need to know him: Mr de Arozamena leads the largest GCC-based solar PV developer in terms of installed MWs. He has previously been President of SolFocus Europe, Middle East & Africa and has served on the board of companies across the renewables, telecoms and media sectors. He graduated with a BS in Electrical Engineering from the University of Southern California before completing his MBA studies in Construction and Real Estate at the Universidad Politecnica de Madrid.

Which markets in MENAT excite you most?

“Over the next 30 years, governments across the Middle East and North Africa will need to invest

over $30 billion a year, or about 3% of the region’s total projected GDP, to keep pace with rising energy demand. The UAE and Saudi Arabia have taken leading roles, with the Kingdom adopting an initial target of 9.5GW, supported by an increased localization of the renewable energy value chain. We also see strong potential in conventional energy importing countries such as Egypt, Jordan, and Morocco.

What is the sector’s biggest challenge?

“In the GCC, challenging environmental conditions, along with energy storage. We are analysing all

battery technologies, and thermal storage is also a good option.

What are you currently focused on?

“Our focus is on building local capacity and establishing a lasting legacy of renewable energy

sector expertise by taking a leading role in diversifying national energy production in strategic markets across the world. Our acquisition of FRV in 2015 is tangible evidence of our goal.

BASED IN: UNITED ARAB EMIRATES

LAURENT LONGUETMANAGING DIRECTOR MIDDLE EAST,

AKUO ENERGY

Why you need to know him: Laurent was project director of Shams 1, the 100MW CSP project in Abu Dhabi in a JV formed by MASDAR, Total and Abengoa Solar. It was the first and largest CSP project in the region when it went operational. He joined Akuo Energy in 2015 after 3 years at SunPower, and previously worked at Total in developing energy projects.

Which MENAT markets excite you most?

“The UAE and Saudi are the most promising markets in the years to come but with some potential in smaller

countries as well: Jordan and Oman. In term of technology, solar combined with storage is probably the market with the highest potential considering the number of large off-grid sites running on diesel in the region. Net-metering roof-top has a significant potential given the opportunities it offers to private developers/investors.

What is your experience of regional EPCs?

“Few have the know-how about solar, although some are progressing fast in that respect, and I expect local

companies to gradually displace foreign firms in the region over the next few years. What are you most proud of?

“Aside from Shams 1, in my new position, I’m extremely happy about the ambitious platform we set up

with Corys Environment for the development of roof-top opportunities in Dubai. After only 6 months, the first deals have been signed, construction is underway and the pipeline grows every day.

6

DEVELOPERS

WHO’S WHO IN MENAT RENEWABLES

BASED IN: UNITED ARAB EMIRATES

ADNAN MERHABAPRINCIPAL,

ARTHUR D. LITTLE

Why you need to know him: Adnan Merhaba is a Principal and global head of the renewable energy competence centre at consultancy Arthur D Little. He studied mechanical engineering at Birla Institute of Technology and Science, India, and also has an Msc in materials science and engineering from Ohio State University and an MBA from the Indian School of Business.

What are you most proud of?

“I was very pleased to see that many of our recommendations when advising Saudi Arabia on

renewable energy strategy were implemented, such as subsidy reform. It’s great to see the country moving in such a positive direction.

What is the biggest challenge facing the sector?

“In the Middle East, the challenge is to come up with a business case in the face of low oil and gas prices,

since the region is such a huge producer of hydrocarbons. North Africa is a different case – as a net importer of hydrocarbons, it is easier to make the case – the stumbling blocks there are more related to political stability.

Which markets in MENAT excite you most?

“Saudi Arabia has massive potential and a lot of clarity has emerged in the past few months, after a period in

which the country’s renewables policy had seemed stuck. The UAE is always a good market, and the recent 800 MW PV bid and interest in the 200 MW CSP plant in Dubai along with Abu Dhabi’s interest in developing a 350 MW PV plant are good examples. Looking further ahead, Egypt and perhaps Jordan could benefit a lot from renewables if the political landscape in Egypt improves.

12

BASED IN: UNITED ARAB EMIRATES

EVANGELOS LIANOSPARTNER,

CIRCLEMOON PARTNERS

Why you need to know him: Evangelos was for years the Executive Director for Yingli Solar Green Energy. He established and expanded the business in the MEA region. He is active in the Middle East for over 20 years. He now runs his own consulting firm for Real Estate and Renewable Energy Projects development.

Which markets in MENAT excite you most?

“United Arab Emirates, Saudi Arabia, and Egypt and some mid-sized countries in Africa, there are large

projects already underway, and we’re seeing potential in small to medium rooftop/ground solar installations between 500kW and 5MW. Wind is expanding and may have a larger volume than solar in the future. The hidden treasures are biogas and geothermal. A country’s renewable energy mix is the next big question, in parallel with enhancing network and distribution. What is the sector’s biggest challenge?

“Renewable projects need time to develop and to construct. A focused and professional approach

together with financial early stage basic cash liquidity for development are the key factors for success. Investors need to bear this in mind when entering this sector in this region and co-operating with developers. Number two is regulation which now matures and opens the way for serious players to act and seek profitable business opportunities.

Which markets in MENAT excite you most?

“The countries with greatest potential, where I see at least 5GW being installed in the next five years would

be Iran, Egypt, Saudi Arabia, and Turkey. What is the biggest challenge to the sector?

“The biggest challenges are moving up the learning curve for local and regional banks in terms of know-

how and resources, as well as building up the local pool of human resources with the requisite skills across the full renewable energy value chain. The key focus should be on leveraging multilateral lenders and export credit agencies to build up confidence in the financing markets, as well as investing in training, skills and know-how transfer for local resources.

BASED IN: UNITED ARAB EMIRATES

DR JAAP KALKMANMANAGING PARTNER ENERGY & UTILITIES PRACTICE,

ARTHUR D. LITTLE

Why you need to know him: Jaap has more than 20 years of Consulting and Private Equity experience in Europe, Asia and the Middle East. He established Paragon Utilities, a Bahrain-based district cooling firm. Jaap focuses on clients in oil & gas, utilities, chemicals, public sector and private equity in the Middle East and Asia.

Which markets in MENAT have most potential in the near future?

“I would say Saudi Arabia is on the map, and Iran is quite actively stimulating the renewable energy

market.

What achievements of your organisation are you proud of?

“I’m proud that we managed to be a main player in the National Transformation Programme in Saudi Arabia,

which completely changed the country. The reorganisation of the energy ministry and others helped to solve the renewable energy deadlock that the country had been suffering.

BASED IN: UNITED ARAB EMIRATES

MOHAMMED ATIFAREA MANAGER – MIDDLE EAST,

DNV GL

Why you need to know him: Mohammed Atif advises on utility-scale solar PV and wind projects, and led the economics assessment of the Masdar PV project and the Sir Bani Yas Island wind power plant in Abu Dhabi. He holds a bachelor’s degree in economics from Dundee University and a master’s degree in energy studies from the University of Manchester.

What is the sector’s biggest challenge?

“The planning and operational paradigm needs to be re-configured across the region. The recent reduction

in costs has been great. With the onset of energy storage and lower cost PV we are embarking on a second phase of technological disruption.

How does MENAT compare with other regions?

“MENAT has been the slowest mover but it has the largest potential. We are now seeing great

ambition, an increasing number of projects but still a lack of maturity in dealing with the new environment. Regulatory frameworks, finance and network access all need improving.

BASED IN: SPAIN

GRANT GREATREXCO-FOUNDER AND SENIOR PARTNER,

MAC GROUP

Why you need to know him: Grant heads up MaC Group’s renewable energy advisory division, specialising in clean technology markets worldwide. He has significant experience in inward investment in to MENAT. He holds a Bsc in Economics from the London School of Economics, Diplôme des Hautes Études Européennes from the College of Europe and an MBA from the University of Warwick Business School.

13

11

BASED IN: UNITED ARAB EMIRATES

EDUARDO VAN-ZELLER NETOHEAD OF ENERGY & UTILITIES/OIL & CHEMICALS

MIDDLE EAST, ROLAND BERGER

Why you need to know him: Eduardo van-Zeller Neto is an expert in business unit strategy, corporate strategic planning, investment & portfolio strategy and large transformation projects. He is a partner at strategy consultants Roland Berger and leads the firm’s energy & utilities and oil & chemicals work in the Middle East region.

Which markets in MENAT excite you most?

“There are three main clusters. North Africa, where some projects have been getting off the ground

but there remains some progress to be made on policy settings; the GCC countries, where the sector has been slower to evolve, but where the current prices of solar make the economic benefits clear; and a cluster of emerging countries, where not too much has happened yet but solar energy prices are also economical and there is real potential. These include such countries as Sudan, Iraq and Iran, as well as elsewhere in Africa such as Mozambique, so a real mixed bag.

What is the biggest challenge facing the sector?

“The fundamentals are all in place, and the business case for solar energy is clearly there. The main

hurdles are decision-making at the political level, and lining up the right sponsors for projects. The challenges vary across the three clusters I mentioned; in the GCC the question is how to accelerate the take-up of renewables, whereas in the emerging markets the challenge is in bringing about the basic conditions for the sector to flourish.

BASED IN: SPAIN

FERNANDO RUEDAMANAGING PARTNER AT

SOLIDA ENERGIAS RENOVABLES

Why you need to know him: Previously chief executive for energy at Aries Ingeniera y Sistemas and head of solar energy for Ibderola, Fernando has led Madrid-based consulting firm Solida Renewable Energies in its expansion into renewables and electrical infrastructure. He studied mechanical & electrical engineering at Carlos III University in Madrid and also holds an Msc in Renewables from the University of Salford, plus an MBA.

Which markets excite you most, looking at the next 5 years?

“Five years is a short time in renewables! However, North Africa has huge potential due to its current

pipeline of projects and solar resource – I would say this region could be number one, especially if it has political stability. The latest auctions for projects in Abu Dhabi, Dubai and Saudi Arabia have also been very promising and no doubt ME could dispute first place if these projects finally see the light. We have been looking very deeply at Turkey for a few years, but the main problem is regulation; Turkey needs to resolve a few concerns for international players.

What is the biggest challenges to the sector?

“For the PV sector, the major challenge will be to maintain prices. The latest auction by DEWA in Dubai

was a great surprise to the PV sector because of the record low bid – the first bid below $US30/MWh. If that sets an expectation for the wider region, then those prices will be a major challenge to keep up with.

What are you most proud of?

“As a firm we have a great track record of connecting with developers, financial institutions and EPC

contractors, especially in PV, CSP and wind power in the Middle East and Africa.

CONSULTANTS

10