in-depth affiliated service groups with case studies

TRANSCRIPT

In-Depth Affiliated Service Groups

with Case Studies

Kelsey N.H. Mayo, J.D.

Partner, Employee Benefits Group

Poyner Spruill LLP

1

Agenda

• Why affiliated service groups matter

• Types of affiliated service groups

• What interests count?

• Three types of attribution

2

Why Affiliated Service Groups Matter

Why Does It Matter?

• Compliance begins with knowing the CG-ASG

• Places it might matter include:

– Nondiscrimination testing

– Counting service

– Distribution timing

– Loans

Nondiscrimination Testing

• All employees in CG-ASG count in determining

compliance with certain requirements, including:

– Minimum coverage

– Benefits rights and features

5

Nondiscrimination Testing

• If two or more plans within CG-ASG, must coordinate

compliance, including:

– 402(g) contribution limits

– Top-heavy testing

– 415 contribution limits

– Safe-harbor compliance

6

Counting Service

• All service in the affiliated service group must be counted

for certain purposes:

– Eligibility service

– Vesting service

• Plan might credit service for other purposes as well

7

Eligibility Service

• If an employee transfers from another employer in the

affiliated service group, must give them credit for that

service for eligibility

• Example

– Corp A and Corp B are in an affiliated service group,

and each maintain a different plan

– Dennis works for Corp A for five years and then

transfers to Corp B

8

Audience Poll 1: Vesting Service

Facts: Corp A and Corp B are in a affiliated service group,

and each maintain a different plan. Corp B’s plan has a

three-year cliff vesting schedule. Dennis works for Corp A

for five years and then transfers to Corp B. Question: Can

Corp B require Dennis to work for an additional three years

before he is vested?

A. Yes

B. No

9

Distributions

• Employee is not eligible for distribution if he or she is

employed anywhere within CG-ASG

• Must terminate from all entities before distribution

10

Plan Loans

• Limits on loans are aggregated among all plans in the

CG-ASG

– If CG-ASG has two 401(k) plans,

employee cannot have a

$50,000 loan in each plan

11

Types of Affiliated Service Groups

Types of Affiliated Service Groups

• A-org group

• B-org group

• Management service group

• Combinations

ASG Basics

• A-organization group

– First Service Organization (FSO) and at least one “A

organization”

• B-organization group

– First Service Organization (FSO) and at least one “B

organization”

• Management service group

– Management organization and one other entity

14

ASG Basics

• A-organization group

– Must have two “service organizations,” one of which

also qualifies as a “first service organization”

• B-organization group

– Must have at least one “service organization,” one of

which also qualifies as a “first service organization”

• Management service group

– No “service organization” requirement

15

What Is a Service Organization?

• An organization that primarily performs services

• Automatic:

– Health

– Law

– Engineering

– Architecture

– Accounting

– Actuarial science

– Performing arts

– Consulting

– Insurance

16

What Is a Service Organization?

• Automatic categories:

– Don’t include companies merely engaged in the

manufacture or sale of equipment or supplies used in

the field

– Don’t include a business that simply has someone

who performs listed services in-house

17

What Is a Service Organization?

• Not automatic:

– Service organization if

– Capital is not a material income-producing factor

• Examples

– Banks: capital is material income-producing factor

– Substantial investment in inventory, equipment, plant, and machinery = capital is material income-producing factor

– Capital is NOT material income-producing factor if income is primarily from fees/commissions for personal services

18

What Is a First Service Organization?

• Generally, any service organization

• Special rule for A-org test

– A corporation is an FSO only if it is a professional

service corporation

– Professional service corporation

• A corporation organized under state law

• For the purpose of providing professional services

• At least one shareholder who is

licensed/authorized to provide the professional

services

19

Affiliated Service Group Overview

Is the entity a service organization?

Does entity regularly perform services for

the FSO?

Is entity regularly associated with FSO in performing services for

third parties?

Entity owns interest in FSO?

A-Org ASG

Significant portion of entity’s business is service to FSO or

A Org?

Services are historically performed by employees in

service field of FSO or A-Org?

10% of entity is owned by designated members

(officers, HCEs, common owners) of FSO or A-Org?

B-Org ASG

Principal business of entity is performing

management services for another

entity (or related group of entities)

Management Service Org

Not an ASG

A-Organization Group

• Requires FSO and A-org

• A-org

– Is a service organization

– Has ownership interest in FSO

– Regularly performs services for the FSO or is

regularly associated with the FSO in performing

services for third parties

21

A-Organization Group

• “Regularly”

– Facts and circumstances

– Factor: amount of income derived from services

performed for FSO or from services associated with

FSO

22

Audience Poll 2: A-Organization

Facts: Kelsey owns 100 percent of Corporation A.

Corporation A owns one percent of Poyner Spruill LLP.

Kelsey provides services to Poyner Spruill clients through

Corporation A, Kelsey has Poyner Spruill business cards,

etc. Question: Are Corporation A and Poyner Spruill an A-

org ASG?

A. Yes

B. No

23

A-Organization

Does one entity qualify as a First Service Organization?

Is the other entity a service organization?

Is the entity regulation associated with FSO in performing services

for third parties?

Does entity own interest in FSO?

A-Org ASG

Yes, Corporation A is professional

services corporation

Yes, Poyner Spruill is in legal field

Yes, regularly associated

Let’s try it with Corp A as the FSO:

Well… not directly.

Might attribution get us there…?

A-Organization

Does one entity qualify as a First Service Organization?

Is the other entity a service organization?

Is the entity regulation associated with FSO in performing services

for third parties?

Does entity own interest in FSO?

A-Org ASG

Yes, Poyner Spruill is a service org

(no need to look further because

LLP)

Yes, Corp A is in legal field

Yes, regularly associated

Let’s try it with Poyner Spruill as the FSO:

Yes, Corp A owns one percent of

Poyner Spruill

Affiliated Service Group Overview

Is the entity a service organization?

Does entity regularly perform services for

the FSO?

Is entity regularly associated with FSO in performing services for

third parties?

Entity owns interest in FSO?

A-Org ASG

Significant portion of entity’s business is service to FSO or

A Org?

Services are historically performed by employees in

service field of FSO or A-Org?

10% of entity is owned by designated members

(officers, HCEs, common owners) of FSO or A-Org?

B-Org ASG

Principal business of entity is performing

management services for another

entity (or related group of entities)

Management Service Org

Not an ASG

B-Organization Group

• Requires FSO and B-organization

– Not required to have two service organizations

• B-organization

– Significant portion of business is performance of

services for an FSO or for A-orgs associated with

FSO (or both)

– Services are type historically performed by

employees

– Ten-percent ownership requirement met

27

B-Org: Significant Portion

• Significant portion of business

– Facts and circumstances

– BUT “safe harbors”

• Less than five percent of service receipts = not

significant

• At least ten percent of total receipts = significant

• Look at greater of percent for year of determination

or three-year period ending in year of

determination

28

B-Org: Significant Portion

• Corp A has the following receipts for the last three years:

• Is a significant portion of Corp A’s business providing

services to the law firm?

29

All Clients Law Firm

2014 Service Receipts $100,000 $5,000

Total Receipts $200,000

2015 Service Receipts $300,000 $6,000

Total Receipts $600,000

2016 Service Receipts $400,000 $8,000

Total Receipts $600,000

B-Org: Significant Portion

• Corp A has the following receipts for the last three years:

30

All Clients Law Firm

2014 Service Receipts $100,000 $5,000

Total Receipts $200,000

2015 Service Receipts $300,000 $6,000

Total Receipts $600,000

2016 Service Receipts $400,000 $8,000

Total Receipts $600,000

Ratio One-year Three-year

Service

Receipts

$8k/$400k = 2% $19k/$800k =

2.375%

Total Receipts $8k/$600k = 1.5% $19k/$1400k =

1.36%

B-Org: Employee Performance

• Historically performed by employees

– For a particular service field, if it were not unusual for

the services to be performed by employees of

organizations in that service field

– In the U.S. on December 13, 1980

31

B-Org: Ten-Percent Ownership

• Ten-percent ownership test

– At least ten percent of B-org is owned by

– Officers, HCEs, or common owners

of FSO or A-orgs

• Common owner = someone who owns at least

three percent of FSO or A-org

32

Example: B-Organization

• Facts:

– Four law firms decide to create Corporation A to

provide legal assistant support

– HCEs of each firm owns 25 percent of Corporation A

– Each firm accounts for 25 percent of Corporation A’s

gross receipts

• Is there a B-org ASG here?

– Both entities are service organizations, so you may

have to do the analysis more than once

33

B-Organization Example

Significant portion of entity’s business is service to FSO or

A-Org?

Services are historically performed by employees in

service field of FSO or A-Org?

10% of entity is owned by designated members (officers, HCEs, common

owners) of FSO or A-Org?

B-Org ASG

No, no evidence Corp A pays the

law firm for services

N/A

No; legal assistants don’t own

law firm

Let’s try it with Corp A as the FSO:

B-Organization Example

Significant portion of entity’s business is service to FSO or

A-Org?

Services are historically performed by employees in

service field of FSO or A-Org?

10% of entity is owned by designated members (officers, HCEs, common

owners) of FSO or A-Org?

B-Org ASG

Yes, greater than ten percent

of gross receipts

Yes, secretaries are

normally employees

Yes, Corp A owned 25 percent

by HCEs of FSO

Let’s try it with the law firm as the FSO:

Affiliated Service Group Overview

Is the entity a service organization?

Does entity regularly perform services for

the FSO?

Is entity regularly associated with FSO in performing services for

third parties?

Entity owns interest in FSO?

A-Org ASG

Significant portion of entity’s business is service to FSO or

A Org?

Services are historically performed by employees in service field of FSO or A-

Org?

10% of entity is owned by designated members

(officers, HCEs, common owners) of FSO or A-Org?

B-Org ASG

Principal business of entity is performing

management services for another

entity (or related group of entities)

Management Service Org

Not an ASG

Management Service Organization

• Two organizations

– One performs management functions

– Principal business of management organization is

• Performing management function

• On a regular and continuing basis

• To a recipient organization and/or organization

related to that recipient

– No need for overlapping ownership

37

Management Service Organization

• What is a “management function?”

– Very little guidance

– IRM says “only those management activities and

services historically performed by employees”

• Historically performed

– By employees in that business field on September 3,

1982

38

Management Service Organization

• What is a “management function?”

– Very little guidance

– IRM says “only those management activities and

services historically performed by employees”

• Historically Performed (per IRM)

– By employees in that business field on September 3,

1982

– OR “ever” by an employee of the particular

organization … for five years after they stop

performing the service in-house39

Management Service Organization

• Professional services…

– IRM says professional services related to

management activities count

– PLUS professional services that are the same as the

recipient performs for third parties

40

Management Service Organization

• Management functions, examples:

– Running daily business operations

• Production, sales, marketing, purchasing, advertising, etc.

– Personnel decisions

• Staffing, training, supervising, hiring, firing

– Setting compensation and benefits

– Goal setting and planning

• Product development, budgeting, financing, expanding operations, capital investment

– Organizational structure and ownership 41

Management Service Organization

• Principal business

– Facts and circumstances test

– Tests in withdrawn regulations

• Two-year rolling percentage

• Facts and circumstances

42

MSO: Principal Business

• Performance of management functions for recipient

organization is 50 percent of activities during two-year

period

– Current tax year

– And preceding tax year

43

MSO: Principal Business

• Once 50-percent test met, continued management group

until:

– Management functions for recipient organization is

less than 40 percent of activities during two-year

period

– Management organization meets 50-percent test for a

different recipient organization

– Services for recipient organization are less than five

percent of management organization’s receipts

44

MSO: Principal Business

• Determination of principal business based on:

Gross receipts from management activities

Gross receipts from all business activities

• Don’t average the percentages—use total receipts

• Commissioner can determine use of gross receipts is not

appropriate

45

Audience Poll 3

Facts: Kelsey owns Good Eats restaurant. Toni

incorporates Amazing Restaurants, Inc. Kelsey and Toni

are not related and there is no overlapping ownership

interests. Amazing Restaurants, Inc.’s sole business in

2016 is to run the day-to-day operations of Good Eats.

Question: Is this a management-service organization?

A. Yes

B. No

46

Audience Poll 4

Facts: Same facts. But in 2017 Amazing Restaurants, Inc.

gets a second restaurant customer, The Greasy Spoon.

Kelsey does not have any interest in The Greasy Spoon.

Question: Are Good Eats and Amazing Restaurants still in

a management-service organization?

A. Yes

B. No

C. It depends

47

Attribution!

48

Affiliated Service Group Attribution

• A-org and B-org tests each have an ownership

component

– A-org: must have some ownership in FSO

– B-org: ten percent of entity is owned by FSO (or its A-

org)

• May be satisfied by attributed/deemed ownership

49

Affiliated Service Group Attribution

• For affiliated service groups – use Code §318 attribution

rules

– Not the same as controlled group attribution

– Same rules used for HCE determination

• Written in terms of stock – look through to similar

ownership for other entities

– For trusts: look at beneficiaries

– For partnerships: look at partnership percentage

– For LLCs: look at membership interests

50

Affiliated Service Group Attribution

Four categories of attribution:

• Option attribution

• Attribution to owners

– Corporation to shareholder

– Partnership to partner

– Trusts and estates to beneficiaries

• Attribution from owners

– Shareholder to corporation

– Partner to partnership

– Beneficiaries to trusts/estates

• Family attribution

51

Option Attribution

52

If I have an option to

purchase stock, the

stock is attributed to me

I am deemed to own the

stock even though I

haven’t exercised the

option yet

Option Attribution

• An “option” is the right to buy stock from a corporation or

its shareholders

– May not be subject to any conditions, other than

• Lapse of time or

• Payment of the purchase price

– Don’t look at the name alone

• Agreement doesn’t have to be called an option

• Example: convertible preferred stock or bond

53

Option Attribution

• Example: I have a right to buy 100 shares of M Corp.

stock, but not until July 1, 2024. There are no other

restrictions.

– I have an option

– The only condition placed

on my right to buy is the lapse

of time

54

Option Attribution

• Example: I have a right to buy 100 shares of M Corp.

stock from Bill if Bill moves to another state

– I do not have an option

– The option is subject to conditions outside of my

control, and unrelated to the lapse of time or payment

of the purchase price

55

Option Attribution

• Example continued: Bill moves to another state!

56

I now have an option, and am deemed to own 100

shares of M Corp.

Audience Poll 5: Option Attribution

Facts: Ruth and Sandra are each 50 percent shareholders of RS

Corp. Shareholder agreement provides either may exercise a

right to purchase the other’s stock, but only after: (1) deadlocking

on an issue, (2) a 15-day cooling off period, and (3) the providing

Notice of Purchase. After receiving a Notice of Purchase, the

other shareholder can either accept or give notice of her intent to

purchase the other’s interest. Question: Is this an “option?”

A. Yes

B. No

57

Option Attribution

• No—there are conditions to right to purchase

• What about once there is a deadlock?

– Probably not

– Shareholder has an unconditional right to give notice

of intent to purchase

– BUT right to purchase is subject to the condition of

the other party choosing to sell rather than to buy

58

Audience Poll 6: Option Attribution

Facts: Continuing the example with Ruth and Sandra:

let’s say that Sandra gives notice of her intent to purchase.

Question: Who has an option?

A. Sandra

B. Ruth

59

Answer: Option Attribution

• Sandra does not have an option

– Her right to purchase is conditional on Ruth’s

choosing to sell her shares

• Ruth does have an option

– Once Sandra gave Notice of Purchase, Ruth had an

unconditional right to purchase Sandra’s shares

60

Option Attribution

• What if I have an option to purchase an option?

– An option to buy an option is treated as though it were

an option to buy the stock itself

61

Option Attribution

• Can I use an option to create an affiliated service group?

– Sure … if you don’t mind the person actually

exercising the option

• Can I use an option to split up an affiliated service

group?

– No. If actual ownership creates an affiliated service

group, the entities are in an affiliated service group.

62

Option Attribution

• Facts (Our B-org example):

– Four law firms decide to create Corporation A to

provide legal assistant support

– HCEs of each firm own 25 percent of Corporation A

– Each firm accounts for 25 percent of Corporation A’s

gross receipts

• If a firm gives another entity an option to purchase its

interest in Corporation A, does it stop being a B-org?

63

Option Attribution

• Example continued:

– No, even though the other firm is deemed to own

Corporation A stock for application of the attribution

rules, the firm still owns 25 percent for now

– The firm is in an affiliated service group until the

option is exercised

64

Affiliated Service Group Attribution

Four categories of attribution:

• Option attribution

• Attribution to owners

– Corporation to shareholder

– Partnership to partner

– Trusts and estates to beneficiaries

• Attribution from owners

– Shareholder to corporation

– Partner to partnership

– Beneficiaries to trusts/estates

• Family attribution

65

Attribution to Owners

• Partnership to partner

– Each partner is attributed proportionate share

– No threshold (like there is for controlled groups)

66

Attribution to Owners

• Partnership to partner

– Example: Cam, Mitch, and Pepper own interests in MF Partnership:

– MF Partnership owns 100 shares of Closets Co.

• Cam is deemed to own 64 shares of Closets Co.

• Mitch is deemed to own 33 shares of Closets Co.

• Pepper is deemed to own three shares of Closets Co.

67

Attribution to Owners

• Partnership to partner

– What if the partnership divides profits and capital

differently?

– For controlled groups, we must use the greater of:

• Her interest in partnership profits, or

• Her interest in partnership capital

– For affiliated service groups, we don’t have guidance

• Controlled group may be reasonable

• So might other approaches

68

Attribution to Owners

• Corporation to shareholder

– Shareholders may be deemed to own their

proportionate share of stock held by the corporation

• Based on the value of the stock, not voting power

69

X

Attribution to Owners

• Corporation to shareholder

– C Corp: attributed ONLY IF shareholder is deemed to

own at least 50 percent of corporation’s stock

– S Corp: treated as a partnership; always attributed

(no ownership threshold)

70

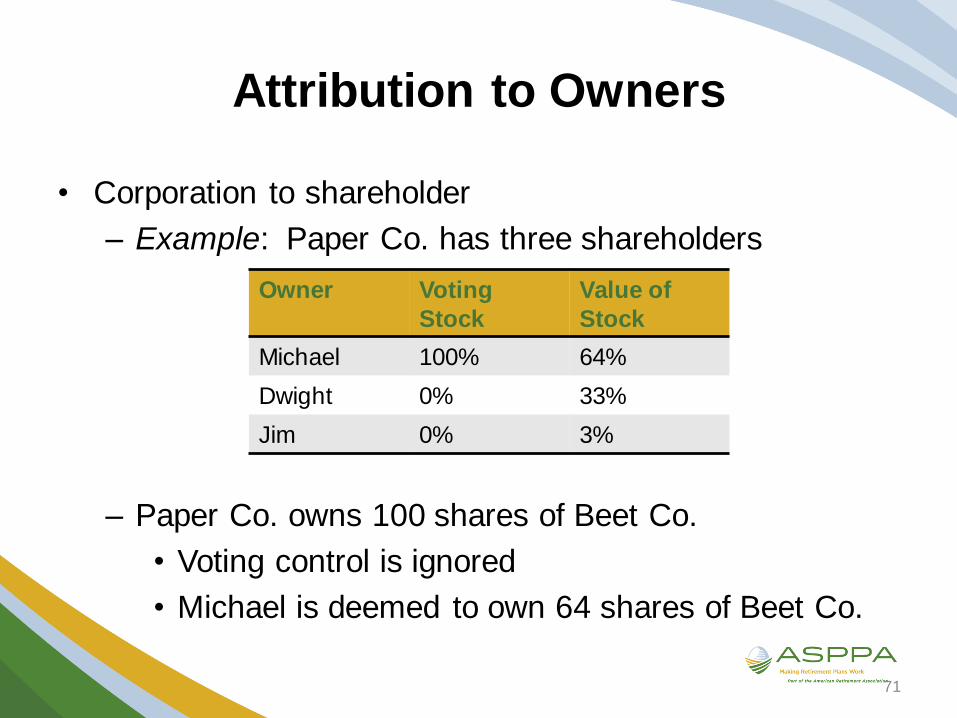

Attribution to Owners

• Corporation to shareholder

– Example: Paper Co. has three shareholders

– Paper Co. owns 100 shares of Beet Co.

• Voting control is ignored

• Michael is deemed to own 64 shares of Beet Co.

71

Owner Voting

Stock

Value of

Stock

Michael 100% 64%

Dwight 0% 33%

Jim 0% 3%

Attribution to Owners

• Corporation to shareholder

– Example continued: What about Dwight and Jim?

– If Paper Co. is a C-Corp, no attribution because they each own less than 50 percent of the value of the corporation

– If Paper Co. is an S-Corp:

• Dwight is deemed to own 33 shares

• Jim is deemed to own three shares

72

Owner Voting

Stock

Value of

Stock

Michael 100% 64%

Dwight 0% 33%

Jim 0% 3%

Attribution to Owners

• How do LLCs fit in here?

• An LLC can elect to be taxed and treated as either a

partnership or a corporation

• This election will govern their treatment in a number of

areas, including under the attribution rules

73

Attribution to Owners

• Trust to beneficiaries

– Beneficiaries are generally attributed their

proportionate share of stock held by the estate or trust

• Share is determined by estate tax tables

• Based on actuarial interest

– Exceptions:

• No attribution from qualified plan to beneficiaries

• Owner of a grantor trust deemed to own all

interests, regardless of beneficial interest

74

Affiliated Service Group Attribution

Four categories of attribution:

• Option attribution

• Attribution to owners

– Corporation to shareholder

– Partnership to partner

– Trusts and estates to beneficiaries

• Attribution from owners

– Shareholder to corporation

– Partner to partnership

– Beneficiaries to trusts/estates

• Family attribution

75

Attribution from Owners

• Generally the same rules apply in reverse

• If owner would be attributed interest held by entity, then

entity is attributed interest held by owner

• Exceptions:

– Trust is not deemed to own interest held by

beneficiary if value of actuarial interest is five percent

or less AND the interest is not vested

– “Remote” and “contingent”

76

Affiliated Service Group Attribution

Four categories of attribution:

• Option attribution

• Attribution to owners

– Corporation to shareholder

– Partnership to partner

– Trusts and estates to beneficiaries

• Attribution from owners

– Shareholder to corporation

– Partner to partnership

– Beneficiaries to trusts/estates

• Family attribution

77

Family Attribution

• Spouse:

– Interest is attributed to other spouse

– No exception for non-involved spouse

78

Audience Poll 7: Family Attribution

Facts (Our B-org example): Kelsey and Dennis are married.

Kelsey owns Mayo Law. Mayo Law is one of the four law firms

that creates Corporation A to provide legal assistant support.

Kelsey does not have any interest in Corporation A. Dennis owns

25 percent of Corporation A. Mayo Law accounts for 25 percent

of Corporation A’s gross receipts. Question: Are Mayo Law and

Corp A an affiliated service group?

A. Yes

B. No

79

Audience Poll 7: Answer

Significant portion of entity’s business is service to FSO or

A-Org?

Services are historically performed by employees in

service field of FSO or A-Org?

10% of entity is owned by designated members (officers, HCEs, common

owners) of FSO or A-Org?

B-Org ASG

Yes, Mayo Law accounts for greater than

ten percent of Corp A’s gross receipts

Yes, secretaries are normally employees

Yes, Kelsey, the owner of the FSO (Mayo

Law), is deemed to own the 25 percent

interest held by her husband

Family Attribution

• Children and parents

– Parent deemed to own child’s interest

– Child deemed to own parent’s interest

• No age 21 nor 50 percent ownership requirement

81

Family Attribution

• Ownership of Corp A

– Kelsey owns one-third of Corp A

– Nicole, Kelsey’s 19 year-old child, owns one-third

– Will, Kelsey’s 25 year-old child, owns one-third

How much of Corp A is Kelsey deemed to own?

82

Family Attribution

• Ownership of Corp A

– Kelsey owns one-third directly

– Nicole, Kelsey’s 19 year-old child, owns one-third

– Will, Kelsey’s 25 year-old child, owns one-third

• Kelsey is deemed to own 100 percent

– Kelsey is automatically attributed both Nicole’s and

Will’s interest

– It doesn’t matter that Will is over 21

83

Family Attribution

• Grandparents and grandchildren

– Attributed to grandparent

– NOT attributed to grandchild

• Siblings

– No attribution

84

Audience Poll 8: Family Attribution

Facts: Ownership of Corp A: Kelsey owns one-third of

Corp A. Nicole, Kelsey’s 19-year-old child, owns one-third.

Will, Kelsey’s 25-year-old child, owns one-third. Question:

How much of Corp A is Nicole deemed to own?

A. One-third

B. Two-thirds

C. Three thirds

85

Audience Poll 8: Answer

• Ownership of Corp A

– Kelsey owns one-third directly

– Nicole, Kelsey’s 19-year-old child, owns one-third

– Will, Kelsey’s 25-year-old child, owns one-third

• Nicole is deemed to own two-thirds

– Nicole is automatically attributed Kelsey’s one-third

interest (because Kelsey is her parent)

– Although Will’s interest is attributed to Kelsey, it is not

“attributed again” to Nicole (no double family

attribution)

86

Affiliated Service Group Attribution

• Can the same ownership interests be attributed more

than once?

– In general, yes

– Exceptions:

• Attribute only once under family attribution rules

• Stock attributed to a company is not attributed

back to its owners

– Option attribution should be considered first

87

Audience Poll 9: Family Attribution

Facts: Ownership of Corp A: Kelsey owns one-third of

Corp A. Nicole, Kelsey’s 19-year-old child, owns one-third.

Will, Kelsey’s 25-year-old child, owns one-third. Kelsey

has an option to purchase Will’s interests. Question: How

much of Corp A is Nicole deemed to own?

A. One-third

B. Two-thirds

C. Three-thirds

88

Audience Poll 9: Answer

• Ownership of Corp A

– Kelsey owns one-third directly

– Nicole, Kelsey’s 19-year-old child, owns one-third

– Will, Kelsey’s 25-year-old child, owns one-third

– Kelsey has an option to purchase Will’s interest

• Nicole is deemed to own 100 percent

– Kelsey is attributed Will’s interest because of the

option—giving her a two-thirds interest

– Nicole is attributed Kelsey’s two-thirds interest

(because Kelsey is her parent)

– Double attribution of Will’s interest not prohibited

because family attribution is used only once

89

90

What If Members in an

Affiliated Service Group Change?

91

Changes in Affiliated Service Groups

• Plans may be covered by what the Code calls the

coverage transition rule

• This provides a grace period of sorts for more than one

year, during which the plan passes minimum

participation and coverage requirements

• BUT:

Changes in Affiliated Service Groups

• To take advantage of the transition rule:

– Plan’s sponsor must be involved in the group

membership change

– Plan must exist before the change

– Plan must have met minimum participation and

minimum coverage requirements before the change

and

– Benefits and coverage must not change significantly

during the transition rule’s grace period (unless

directly related to the change)

92

Changes in Affiliated Service Groups

• Example:

– JJ Co. becomes an A-org Group with Waffles Co.

on April 1, 2018

– JJ Co.’s 401(k) plan passed participation and

coverage tests immediately before the change

– JJ Co. amends the plan effective December 1, 2018,

to increase employer contributions from three to

seven percent of pay

– Effect?

93

Changes in Affiliated Service Groups

• Example continued:

– This is a material change in benefits during the

coverage transition grace period

– The grace period ends immediately (as of December

1)

94

Changes in Affiliated Service Groups

• So, if there’s another change during the grace period,

can I “tack” together grace periods to avoid complying

with the coverage and participation rules forever?

95

Changes in Affiliated Service Groups

• No

• In looking to see whether a plan satisfied minimum

requirements before the change, the plan must satisfy

the requirements before any transition grace period

96

Changes in Affiliated Service Groups

• Example:

– Waffles Co. becomes an ASG with JJ Co. on April 1, 2018

• It relies on the transition grace period to meet minimum

requirements

– On September 1, 2018, Sweet Co. buys all the stock of

Waffles Co. from JJ Co., and Waffles Co. joins the new

controlled group

– Waffles Co. can continue to rely on old grace period until it

expires. However, if it wants a new grace period based on

transaction with Sweet Co., it must show that it actually met

minimum requirements on: ________.

97

Changes in Affiliated Service Groups

• Example continued:

– Waffles Co. must show that it actually met minimum

requirements on September 1, 2018, (immediately

before the Sweet Co. transaction)

– Waffles Co. cannot rely on the transition grace period

to show that it met requirements on September 1,

2018

98

Changes in Affiliated Service Groups

• These rules are somewhat complex, with varying

requirements for considerations such as:

– Separate lines of business

– Effect of rule on elective deferrals and matching

contributions

– Effect on plans that have a nondiscrimination safe

harbor

– Etc.

99

Questions?

Miss the 2018 Spring Virtual Conference?

Go to: https://ecommerce.asppa-net.org/Webcasts-Conferences/Meeting-

Details/productId/8935914

Order the On-Demand Recording!

Member price: $299

Nonmember price: $349

Worth 7.5 CE Credits!