improving health outcomes through strategic sourcing of ... · this report assesses the global...

TRANSCRIPT

Improving Health Outcomes Through Strategic Sourcing of ARVs and Viral Load Technologies

January 2016

Geneva, Switzerland

Page 2

Contents

I. Executive Summary ................................................................................................................................. 4

II. Introduction ......................................................................................................................................... 5 01 The HIV/AIDS Context .................................................................................................................... 5 02 Introduction and Report Overview ................................................................................................. 6

III. ARVs ..................................................................................................................................................... 7 01 Market Overview .............................................................................................................................. 7 02 Market Challenges ........................................................................................................................... 8 03 Global Fund Market Interventions ................................................................................................. 8

IV. Viral Load Monitoring and Early Infant Diagnosis .......................................................................... 19 01 Market Overview and Recent Market Shifts .................................................................................. 19 02 Market Challenges .......................................................................................................................... 19 03 Global Fund Market Interventions ............................................................................................... 20

V. Next Steps ........................................................................................................................................... 24

VI. References .......................................................................................................................................... 25

3

Figures

Figure 1: Causal chain linking inputs and activities to outcomes and impact ................................................ 11 Figure 2: Causal chain of the Global Fund’s procurement strategy ................................................................ 11 Figure 3: Causal chain of manufacturer evaluation ......................................................................................... 12 Figure 4: Manufacturer OTIF rate .................................................................................................................... 13 Figure 5: Improvement in manufacturer OTIF rate over time ........................................................................ 13 Figure 6: Causal chain of longer-term contracting and target pricing ........................................................... 14 Figure 7: ARV price trajectory, 1 January – 22 October, 2015 ........................................................................ 15 Figure 8: 2015 cost savings ................................................................................................................................ 16 Figure 9: Causal chain of long-term framework agreement ............................................................................ 16 Figure 10: Causal chain of Vendor Managed Inventory .................................................................................. 17 Figure 11: Historic variability in viral load monitoring prices, 2012-2014 .................................................... 20 Figure 12: Snapshot of the viral load and early infant diagnostic tool ............................................................ 21 Figure 13: Causal chain of publication of the benchmark tool ....................................................................... 22 Figure 14: Current viral load monitoring prices in comparison with 2012-2014 historic variability .......... 23

4

I. Executive Summary

The world requires a reliable supply of greater volumes of HIV products in order achieve the

scale required to achieve global targets. The world is pursuing the 90–90–90 target: by 2020, 90

percent of all people living with HIV will know their HIV status, 90 percent of all people diagnosed with

HIV infection will receive sustained antiretroviral (ARV) therapy, and 90 percent of all people receiving

ARV therapy will have viral suppression. The targeted scale-up of ARV medicines and Viral Load

technologies will be pivotal to reach these targets. The Global Fund is one of the largest financiers of HIV

health products and has a key role to play to facilitate this scale-up and close the coverage gap.

The scale-up of ARV medicines and viral load technologies requires a healthy market. Product

scale up can be accelerated when healthy market conditions exist across six key dimensions - innovation,

availability, demand and adoption, quality, affordability and delivery.

The Global Fund has designed and implemented product strategies for ARV medicines and

viral load technologies. The Global Fund aimed to leverage its procurement capabilities and role in the

market to improve market conditions. Since the implementation of the Global Fund’s ARV strategy in July

2014, it has focused on improving availability, affordability, innovation, adoption and reliable on-time

delivery, while continuing to deliver quality-assured products. The ARV and viral load strategies involved

in collaboration and consultations with partner organizations and manufacturers, both of which are

supportive of the more comprehensive strategies.

The procurement strategies are already having positive impacts on the market. While implementation is still in the very early stages, initial successes have already be seen:

Improved affordability. The Global Fund has provided long-term demand commitments to manufacturers.

These commitments have enabled manufacturers to generate efficiencies. The Global Fund has also worked

with manufacturers to implement target price trajectories. Manufacturers are encouraged to transfer

efficiencies into lower product prices. Sustainable price declines have already been achieved, generating

over US$35 million in savings for the Global Fund in the first year alone. These savings could provide

treatment for 300,000 additional patients.

Improved delivery performance and fewer stock-outs. The strategy has placed emphasis on achievement of

on-time, in-full delivery (OTIF) and a reliable and uninterrupted medicine supply. As a result of the

procurement strategy, manufacturer OTIF has improved from 20 percent to 85 percent.1 The Global Fund

has also developed a mechanism to respond rapidly to shortages of ARVs, which has reduced the delivery

time for emergency orders to countries to three to seven weeks. Such improvements reduce risks of

treatment interruptions that can have severe medical consequences and contribute to drug resistance.

Improved treatment availability. The strategy has improved ARV availability in a number of ways. First, the

Global Fund has worked with manufacturers to diversify their supply base for active pharmaceutical

ingredients (API). This can help prevent API shortages that might trigger volatile pricing or unreliable

supply. Second, the Global Fund has bundled demand so that manufacturers receiving orders for high

volume ARV products must also supply the lower volume and less commercially attractive products. Finally,

the Global Fund continues to lead the Paediatric ARV Procurement Working Group (PAPWG) to improve

the availability of paediatric ARVs. All of these interventions have improved the availability of the right

treatment at the right time for patients worldwide.

Increased innovation. A number of manufacturers have joined the Global Fund in collaborative projects

aimed at driving product improvements to better meet patient.

The Global Fund’s viral load procurement strategy was implemented in June 2015 and initial

successes are starting to be seen. While efforts in this market are at an even earlier stage than ARV

interventions, some impacts can already be seen. The Global Fund created an online tool that provides

technical and commercial information, such as pricing benchmarks, to viral load buyers in a transparent

manner. As a result, manufacturers now offer a consistent price to all purchasers and average test price

declined by approximately 30 percent.

The Global Fund will be closely monitoring the impact of all interventions in the future. In addition, it will

continue to monitor key product markets for opportunities to support healthy market conditions, and to

deliver improved health outcomes through strategic procurement initiatives.

1 The improvement was from 20 percent in April 2013 to 85 percent at the end of September 2015.

5

II. Introduction

01 The HIV/AIDS Context AIDS is a leading cause of mortality worldwide. Since 2000, more than 38 million people have become infected with HIV, and 25 million people have died of AIDS-related illnesses.2 Only 15 years ago, close to 20 million people were living with HIV/AIDS in Sub-Saharan Africa, and only 11,000 were receiving treatment, due to inaccessibility and unaffordable prices.3,4

Since 2000, the global community has made significant progress in curbing the HIV/AIDS epidemic. Targeted prevention interventions and ARVs have been pivotal in slowing the pace of the epidemic. The scale up of prevention and treatment efforts over the last decade has resulted in a decline in new HIV infections from 3.5 million cases in 2000 to 1.1 million in 2014.5,6

The fight against HIV/AIDS is ongoing, and the world is now pursuing a new target. The new 90–90–90 treatment target set by WHO aims to ensure that by 2020, 90 percent of all people living with HIV are aware of their HIV status, 90 percent of all people diagnosed with HIV infection will receive sustained ARV therapy, and 90 percent of all people receiving ARV therapy will have achieved viral suppression.7 There is still a long way to go to reach this new target. Currently, only 48 percent of the people estimated to be living with HIV are diagnosed, only 37 percent receive ARV treatment and only 32 percent are virally suppressed.8,9 Pediatric treatment is lagging even further behind, with only 32 percent of children living with HIV receiving ARV treatment.10

The Global Fund has a key role to play in strengthening HIV product markets to contribute to reach these new targets. The Global Fund can leverage its position as one of the largest financiers of ARVs and other HIV products to help reach the 90-90-90 target. As part of its contribution, the Global Fund can use its strategic procurement capabilities to build healthier global markets for ARVs, viral load monitoring and early infant diagnostics, and negotiate prices to make products more affordable. This will allow the same funding envelope to stretch further, help to drive uptake and reduce the coverage gap.

In the past, the Global Fund has successfully shaped product markets through its Market Shaping Strategy. The Global Fund approved its first Market Shaping Strategy in 2007. This resulted in the creation of the Voluntary Pooled Procurement (VPP) and Price and Quality Reporting (PQR) mechanisms. In 2011, the Global Fund approved an updated Market Shaping Strategy. This strategy recognized challenges across the ARV market. In particular, the updated strategy identified the need to improve access and value for money across products, accelerate the introduction of new products, and secure the paediatric ARV market.11 The need to secure the ARV market resulted in the creation of the Paediatric ARV Procurement Working Group (PAPWG). The goal of this group is to bring together public actors to develop a coordinated approach to paediatric ARV market challenges.

In 2011, the Global Fund identified areas for improvement in the Market Shaping Strategy related to the VPP. Grants issued under the VPP were only around US$300 million in annual spend, limiting the Global Fund’s ability to leverage purchasing scale. Also, the VPP could only procure products following grant disbursements and specific country purchase orders. As a result, the Global Fund was prevented from offering stable, advanced demand visibility to manufacturers, and from effectively pooling volumes to reach economies of scale.

Building on the need for further progress, the Global Fund launched the Procurement for Impact (P4i) strategy. The P4i incorporated a number of initiatives aimed at establishing the Global Fund as the sector’s benchmark organization for sourcing and procurement. The P4i established a standard method to evaluate market conditions and to develop and implement a procurement strategy for each product category. It also included the transition from the VPP to the Pooled Procurement Mechanism

2 The Global Fund Website, accessed 17 November 2015. 3 Nolen, Stephanie. 28 Stories of AIDS in Africa, New York: Portobello Books, 2007. 4 WHO, Global health sector response to HIV, 2000-2015: focus on innovations in Africa, 2015. 5 United Nations, the Millennium Development Goal Report, 2015. 6 The Global Fund Website, accessed 3 December 2015 7 UNAIDS, 90-90-90 – An ambitious treatment target to help end the AIDS epidemic, 2014. 8 Dutta et al., “The HIV Treatment Gap: Estimates of the Financial Resources Needed versus Available for Scale-Up of Antiretroviral Therapy in 97 Countries from 2015 to 2020”, 2015 9 NAM, “Treatment cascades show 90-90-90 goal within reach for some – but Eastern Europe lags behind Africa”, 22 July 2015. 10 Dutta et al., “The HIV Treatment Gap: Estimates of the Financial Resources Needed versus Available for Scale-Up of Antiretroviral Therapy in 97 Countries from 2015 to 2020”, 2015 11 The Global Fund, “Report of the market dynamics and commodities ad-hoc committee”, 2011

6

(PPM). Under the PPM, the Global Fund is able to pool volumes and move away from spot tenders, and to negotiate agreements with manufacturers based on consolidated demand.

02 Introduction and Report Overview This report assesses the Global Fund’s use of strategic procurement practices to shape two health product markets i) ARVs, and ii) viral load monitoring and early infant diagnostic testing.12 . The report includes analyses up to the end quarter 3 2015. The report will first discuss ARV procurement, followed by viral load monitoring and early infant diagnosis test procurement. The Global Fund’s ARV product strategy was implemented first and serves as the main focus of this report. The report will provide a market overview and will highlight the shortcomings that led to the need for Global Fund intervention. The report will then outline the Global Fund’s objectives and strategic procurement actions, and evaluate the initial outcomes. Intervention in the viral load market is more recent and will be discussed using a similar structure, although in less detail. The current interventions are part of a set of product-specific procurement strategies. The Global Fund is currently analyzing the HIV rapid diagnostic test (RDT) market and is defining its market strategy. Strategic procurement is part of a wider market shaping tool kit. While strategic procurement is a critical lever, it is important to note that the Global Fund can, and does, bring other tools to bear to promote healthier markets, such as guidance to countries during the grant-making process and quality assurance policies.

12 Across the document, viral load refers to viral load monitoring and early infant diagnosis, unless specifically mentioned otherwise.

7

III. ARVs

01 Market Overview ARVs are segmented between first-line, second-line and third-line for adult and paediatric medicines. Adult first-line medicines account for the largest amount of the total market value (just over 80 percent in 2013), and demand is concentrated in a small sub-set of products.13,14

The market for ARVs consists of a high-value, low-volume market in high-income countries, and a high-volume, low-value market in the rest of the world. High-income countries (HICs) represent the majority of the overall market value. Seven HICs - US, Japan, France, Germany, Italy, Spain, and UK - had a combined ARV market value of almost US$12 billion in 2013. In comparison, the ARV market in Low-and middle-income countries (LMICs) was just US$1.4 billion in 2013. Despite its low value, the LMIC market comprises significantly larger volumes and 15 million people from LMICs worldwide are currently on ARV treatment; 8.1 million of these people are receiving treatment through Global Fund-supported programs.15

The market is expected to grow in the future, in part due to new treatment guidelines. The ARV market in LMICs is expected to continue to grow in value, at around 7 percent per year, over the next few years.16,17 In September 2015, the WHO recommended significant changes in ARV eligibility. The new guidelines recommend that anyone infected with HIV should be treated with ARVs immediately after diagnosis, and people at "substantial" risk of HIV should use preventive ARV treatment.18,19 As more countries adopt the test and treat guidelines, approximately 23 million people – 95 percent adults and 5 percent paediatric patients - are predicted to be on ARVs in LMICs by 2019.20

A small number of manufacturers supply the majority of the products. There are a relatively small number of manufacturers regularly producing the needed range of WHO-recommended ARVs. Of 30 manufacturers with products prequalified by WHO or approved by a Stringent Regulatory Authority, fewer than 8 have approvals and produce 10 or more for the 18 ARVs needed.21

The largest funders and buyers in the ARV market are the Global Fund, PEPFAR and the government of South Africa. The Global Fund finances approximately 40 percent of all ARVs for LMICs. It also plays a significant role in global markets for ARVs by negotiating procurement terms for the ARVs it finances through the PPM. ARVs financed through the PPM represent around half of the Global Fund volumes (20%). The remainder of Global Fund-financed ARVs represent approximately another 20 percent of the LMIC market, and are procured directly by recipient countries or their procurement agents.

13 CHAI, ARV market report, 2014. 14 The Global Fund PPM second-line market is around 50 percent bigger than the paediatrics market, Global Fund analysis. 15 UNAIDS, “UNAIDS announces that the goal of 15 million people on life-saving HIV treatment by 2015 has been met nine months ahead of schedule”, 14 July 2015. 16 The LMIC market is expected to grow with ~7 percent to US$2 billion by 2018, according to CHAI, ARV market report, 2014. In comparison the HIC market is expected to grow ~4 percent per year to US$17 billion by 2022. Source: UNAIDS, CHAI. 17 This assumes the funding envelope for ARVs will also increase over time 18 WHO, WHO Guideline on When to Start Antiretroviral Therapy and on Pre-exposure Prophylaxis for HIV, 2015 19 The early-release guideline will form part of the 2016 WHO consolidated guidelines on the use of ARV. 20 CHAI, ARV Market Report: The State of the Antiretroviral Drug Market in Low- and Middle-Income Countries, 2014-2019, November 2015. 21 Global Fund analysis.

8

02 Market Challenges

Products face different challenges based on their overall market potential and their stage in the product lifecycle. Given the large number of ARVs, there is a variety of products at different stages of the product lifecycle and in markets with varying degrees of attractiveness. As a result, each product faces a unique sub-set of challenges. A one-size-fits-all approach will not effectively drive uptake across all markets.

Affordability is the greatest concern for first-line products. Countries rely on first-line products to provide uninterrupted treatment to the majority of those people being treated for HIV / AIDS. These products must be affordable and continuously available.

Low and fragmented demand limits the affordability and availability of second-line and limited-use (WHO-recommended) products. Demand for second-line and limited-use ARVs is low and intermittent, which causes manufacturers to offer unpredictable lead times and potentially higher prices. Alternatively, they might be unwilling to supply at all. Limited-use paediatric products are especially affected as demand is highly fragmented and orders for some products can often be significantly smaller than a manufacturer’s minimum batch size.

Supply sustainability remains a challenge. Across all products, there is a risk of supply interruptions due to manufacturers’ dependency on a limited number of API sources.22 The narrow API supply base increases the risk that manufacturers will not be able to access API, and consequently will not be able to supply ARVs with the ensuing risk of treatment interruptions.

On-time delivery and response to risks of stock-outs has been a challenge. Across all products, manufacturer on-time delivery performance has been relatively poor with only 20% of products delivered “on-time and in-full” in April 2013. This is driven by limited ability of manufacturers to plan production due to lack of visibility due to, for example weak planning and late ordering.

03 Global Fund Market Interventions

3.1 Objectives In response to these challenges, the Global Fund designed and implemented a procurement strategy for ARVs procured through the PPM. The ARV procurement strategy focuses on six market dimensions - innovation, availability, demand and adoption, quality, affordability and delivery. The overall goal of the strategy is to reduce mortality and morbidity from HIV/AIDS and improve value for money. Over the course of the first year the Global Fund prioritized improving availability, affordability and delivery across ARV products, and improving the adoption of optimal regimens. The Global Fund is monitoring the impact of interventions to assess progress and to ensure there are no unintended consequences. The strategy aims to benefit other buyers beyond PPM. Grants participating in PPM will benefit from the strategy through the lower prices, shorter and more reliable lead-times and improved contractual terms negotiated by the Global Fund. Other ARV buyers will also benefit from this strategy through access to the PPM reference price information, new product innovations, and greater product availability.

22 API accounts for 60-80 percent of total ARV production cost.

9

Table 1: Objectives of the ARV strategic procurement strategy

Dimension23 Desired outcomes Interventions

Innovation Introduction of new products

(adult and paediatric)

Improved paediatric formulations

Products with longer shelf lives

Implementation of collaborative projects

Evaluation criteria that recognize

manufacturers that invest in product

development

Inclusion of new products in the procurement

strategy as they become available

Availability Improved availability of all

products (high and low volume,

and paediatric ARVs)

Production capacity of low volume

products maintained (new and

declining products)

Expanded registration footprint of

products

Faster responsiveness to risks of

stock-outs

Bundling of high and low volume products to

support the regular production of all the

needed products

Through multiagency coordinated

procurement, coordinate order placement and

provide better visibility to facilitate supply of

full batches of low volume products including

paediatric ARVs

Optimization of API sourcing and production

planning

Evaluation criteria that recognize

manufacturers planning to register products

in countries

Implementation of a Vendor Managed

Inventory mechanism

Demand and

adoption

Adoption of WHO recommended

regimens and products

Increased uptake of optimal

products and formulations

Promotion of the uptake of optimal

formulations

Pricing roadmaps to support uptake of

optimal and/or equivalent WHO-

recommended 1st and 2nd line products and

formulations for adults and children

Encouraging the update of treatment

guidelines to use optimal products including

for paediatric formulations (through the

PAPWG)

Quality Adherence to the Global Fund’s

quality assurance policies

Tender restricted to products meeting the

Global Fund’s quality assurance policy for

pharmaceutical products

Affordability Sustainable price reductions

(first-line and second-line

recommended products)

Stabilization of prices (for legacy,

low volume, specialized use

products)

Use of longer-term contracting

Implementation of pricing road maps, with

price targets based on an analysis of the cost

of goods (COGS)

Optimization of API sourcing

Delivery Increased number of products

delivered OTIF

Reduction in lead-time

Faster responsiveness to risks of

stock-outs

Use of an updated evaluation criteria that has

an emphasis on manufacturer OTIF

Use of longer-term framework agreements

Implementation of a Vendor Managed

Inventory mechanism for all products

23 The Global Fund’s Market Shaping Strategy, Committee Decision (SIIC) and Committee Information (FOPC), internal document, 2015.

10

3.2 Implementation The Global Fund issued a global tender with the goal of entering strategic long-term agreements with manufacturers and maintaining a broad supplier base. The Global Fund entered into two types of agreements with manufacturers. “Manufacturer Partnerships” have a duration of three years and “Supply Agreements” have a duration of two years. As part of the manufacturer partnerships, manufacturers commit to work with the Global Fund to achieve a set of agreed strategic objectives around ARV development, supply and pricing in a series of collaborative projects. The Global Fund provided a financial commitment that a fixed quantity of ARVs will be purchased at a pre-agreed price as part of both types of agreement. A two-step evaluation process was used to select manufacturers and allocate ARV demand. Manufacturer proposals were scored through a commercial and technical evaluation, and an evaluated collaborative workshop between the Global Fund and the manufacturer. Manufacturers were awarded partnerships or supply agreements depending on their score in the evaluation procedure.

3.3 Tender outcomes The Global Fund issued the tender in July 2014 and received proposals from 15 manufacturers. The tender process started with a Request for Proposals (RFP) in July, which closed in September. The tender was restricted to manufacturers producing WHO prequalified or Stringently Approved products. The Global Fund established Framework Agreements with a panel of eight manufacturers for PPM. Five manufacturers have been allocated manufacturer partnership agreements, and three have been allocated supply agreements. In year one of the strategy, 99.5 percent of all ARVs by volume and value were procured from these manufacturers, and remaining 0.5 percent of products, which were low volume or originator products, were purchased from six manufacturers outside the framework agreements. In 2014, the Global Fund purchased 99.8 percent of ARVs from eight manufacturers, and the remaining low volume products were purchased from another eight manufacturers. In summary, PPM procured from 14 manufacturers in 2015, down two from the 16 in 2014. Manufacturers under the framework agreements are supportive and complimentary of the strategy. When asked about their view on the strategy, most manufacturers were satisfied with the improvements it has brought to the market. Interviewed manufacturers praised the process and efficiency of the strategy. One manufacturer said “I think it is the first time a procurement agency has conducted such an extensive and professional process”.

3.4 Market outcomes The following section assesses the short-term outcomes of the strategy. In the long-term, the Global Fund’s ARV procurement strategy aims to reduce mortality and morbidity and improve value for money. However, it is too early to judge whether the strategy has had these impacts. Consequently, the report focuses on the short-term outcomes achieved across the first nine months of implementation. Figure 1 illustrates the difference between impact and outcomes, and how they relate to the inputs and activities.

11

Figure 1: Causal chain linking inputs and activities to outcomes and impact

The report will assess the outcomes achieved by each element of the strategy. The elements of the procurement strategy were designed to contribute to the outcomes outlined in Table 1. Each element of the strategy contributes to multiple outcomes. Therefore, the report considers each element of the strategy, and the outcomes it has contributed to, in turn. These outcomes are interlinked and will combine to impact mortality and morbidity, and improve value for money (Figure 2). The key elements will be evaluated in the following order: 1) evaluation criteria; 2) longer-term contracting, demand coordination and target pricing; 3) long-term framework agreements; 4) Vendor Managed Inventory; and 5) Multiagency coordinated procurement (PAPWG). The report will also assess the progress made through the collaborative projects between the Global Fund and manufacturers. Figure 2: Causal chain of the Global Fund’s procurement strategy

12

Evaluation criteria The strategy uses a broad set of criteria to evaluate manufacturers. The evaluation criteria focus on manufacturers’ ability to achieve on-time, in-full (OTIF) delivery and the diversity of their API supply base. The evaluation process also recognizes those manufacturers who are planning to invest in the research and development of new ARVs, and manufacturers who plan to widen their registration footprint. The process leads to selection of manufacturers that have a good track record of on-time delivery, a broad API supply base and a commitment to expand their registration footprint and develop new products. This supports the Global Fund’s objectives around delivery, availability and innovation as outlined in Figure 3. Figure 3: Causal chain of manufacturer evaluation

Selection and recognition for timely delivery has led to an improvement in OTIF. Manufacturer OTIF is defined as the number of orders that are produced in their full quantity and are ready for shipment within seven days of the promised date. By the third quarter of 2015 most manufacturers had improved their OTIF rate (Figure 4), and average monthly manufacturer OTIF across increased from 20 percent in April 2013, to 85 percent at the end of September, 2015 ( Figure 5). Improvements in manufacturer OTIF has led to more timely delivery of orders to countries. During the first eight months of 2015, almost 80 percent of shipments were delivered on-time and in-full to countries, compared to an average of 45 percent between 2013 and 2014. This is very close to the average OTIF rate of the private sector, which was estimated at 89 percent in 2013.24

24 Private all sectors, Europe, Asia, Americas PwC, Global Supply Chain Survey 2013

13

Figure 4: Manufacturer OTIF rate25

Figure 5: Improvement in manufacturer OTIF rate over time26

Selection of manufacturers with a broad supply base has de-risked the supply chain. Stakeholder interviews indicated that Global Fund manufacturers now have a broader API supply base. Two manufacturers reported that they had expanded their API supply base as a result of the Global Fund’s procurement strategy. A broader API base will help to avoid a situation where manufacturers cannot access API, or are dependent on a few API suppliers who might raise prices when stocks are low and demand is high. Avoiding these price fluctuations will enable manufacturers to reduce their cost of goods, and ultimately lower prices in the long-term. Additionally, manufacturers are looking to invest in product development and expand their registration footprint. It is too early to see any concrete innovation outcomes. However, one manufacturer reported they were investing in the development of pipeline ARV products as a result of the strategy. The Global Fund will continue to work with manufacturers to understand product development

25 Seven of the ARV manufacturers who entered the Global Fund framework agreement in 2015 have been included in the analysis. The eighth manufacturer did not supply any ARVs in 2015. Manufacturer OTIF rates have been weighted by the volume of ARVs each manufacturer supplied to the Global Fund in the respective period. 26 All ARV manufacturers included in the Global Fund tender process between 2013 and 2014, and only those manufacturers under the Global Fund framework agreements in 2015, were included in the analysis. Manufacturer OTIF rates have been weighted by the volume of ARVs supplied to the Global Fund by each manufacturer in the respective period.

3

OTIF rate increased significantly from ~30% to ~80% after implementation of the new ARV procurement strategy

Volume-weightedOTIF rate, %

The study assesses aggregated monthly OTIF performance of all ARV manufacturers who were included in tender process between 2013 and 2014, and those entered the Global Fund Framework Agreement in 2015.The OTIF rates have been weighted by volume of ARVs supplied to the Global Fund in the respective period.Source: The Global Fund, Dalberg analysis.

0

10

20

30

40

50

60

70

80

90

2015

Ap

r

2015

Ju

n

2015

Feb

2015

Jan

20

14

De

c

2015

Mar

2014

No

v

2015

May

2014

Oct

2014

Sep

2014

May

2014

Au

g

2014

Ju

l

2014

Ju

n

2015

Sep

2015

Au

g

2015

Ju

l

2013

Au

g

2013

Ju

l

2013

Oct

2013

Sep

2014

Ap

r

2013

No

v

2014

Feb

2014

Jan

2013

May

2013

Ap

r

2014

Mar

20

13

De

c

2013

Ju

n

Implementation of new ARV procurement

strategy

Announcement of the new Global Fund

tender process

Global Fund supplier engagement visits &

articulation of priorities

14

pipelines and to support product introduction when feasible and required. Two manufacturers have also indicated that they are looking to expand their registration footprint and expedite country registration processes.

Longer-term contracting, demand coordination and target pricing The strategy uses longer-term contracting, coordination of demand and target pricing to achieve sustainable reductions and stabilization of prices. These activities were specifically targeted at achieving the overall objective of improving affordability. The theory of change is outlined in Figure 6. Figure 6: Causal chain of longer-term contracting and target pricing

The bundling of demand helps to build the market for low demand products. The Global Fund provides manufacturers with demand forecasts. Demand forecasts give manufacturers improved visibility across the ARV market. The demand for low volume ARV products is bundled with the allocation of high-demand products. The aim is to ensure that producers remain interested and incentivized to enter and remain in the market for smaller and specialized products (such as paediatric ARVs). The long-term commitments offered by the Global Fund help manufacturers to plan production and lower their cost base. In the strategy, the Global Fund gives manufacturers a financial commitment for the purchase of a fixed quantity of ARVs at an agreed price. Provision of advanced notification of volumes allows manufacturers to optimize production planning, which will lower production and stock costs, and ultimately lower prices and improve affordability. The Global Fund has encouraged manufacturers to use the cost efficiencies generated through longer-term contracting to lower product prices in line with the price targets. The Global Fund set price targets based on the suppliers’ best estimate of cost of goods and market intelligence. Targets were planned to allow manufacturers to maintain competitive margins, and price targets will decline over the course of the first two years of the agreement. This gives manufacturers a chance to transfer the benefits conferred by the longer-term commitments into production efficiencies. The Global Fund set price targets for mid-2015 and 2016 for the following 3 groups of products:

Tenofovir based regimens, specifically: efavirenz-emtricitabine-tenofovir and efavirenz- lamivudine-tenofovir fixed dose combinations

Second line protease-inhibitor fixed dose combinations: lopinavir-ritonavir and atazanavir-ritonavir fixed dose combinations

Zidovudine based regimens, specifically: lamivudine-nevirapine-zidovudine fixed dose combination

The Global Fund believes that target pricing can also play a useful role in mitigating excessive price volatility. It is a normal business practice that manufacturers sometimes use price reductions to attempt to gain market share or eliminate excess inventory. However, pricing or tendering that is too aggressive in the short-term might cause negative long-term effects in the market, such as undesired manufacturer exits or an inability for manufacturers to make investments in product

“The new strategy has given a new life line to our ARV business.”

“The new strategy enables the company to invest in drug development.”

15

development or other improvements while remaining competitive. The Global Fund believes that target pricing can function as a valuable tool to stimulate and preserve the positive effects of competitive pricing, while mitigating some of the potential long-term negative effects. Manufacturers have reported that better demand visibility and long-term commitments have generated cost savings. In interviews, manufacturers stated that they have been able to realize cost-savings as a result of greater predictability and better production planning.

Manufacturers have used cost savings to meet the Global Fund’s price targets, and substantial price declines have already been achieved (Figure 7). The price of TEE has been reduced to that of TLE, and the price of both regimens are beginning to converge on the price of sub-optimal zidovudine-based regimens thus expediting the uptake of optimal tenofovir-based regimens. Figure 7: ARV price trajectory, 1 January – 22 October, 2015

As a result of these price reductions, initial estimates suggest that the Global Fund will achieve cost savings of at least US$35.1 million across the top 10 volume products in 2015. This saving will account for 10 percent of the value of the ARVs purchased (Figure 8). This equates to 96 percent of the Global Fund’s target savings, and could provide treatment for an additional ~300,000 patients.27. Forecasts suggest that the procurement strategy could save the Global Fund an additional US$63 million in 2016. If forecasted savings are achieved, the Global Fund will save a total of US$98 million over the first two years of the strategy. The Global Fund is therefore on track to meet the two year savings target set at the outset of the strategy.

27 These forecasted cost savings calculated at the beginning of Q4 2015 have been calculated using the difference in price between the baseline price (weighted average price between July 2013 and June 2014) and the actual price, multiplied by the purchased or forecasted volume. The 2015 savings estimate includes actual savings on all orders placed in Q1 to Q3 2015 and orders placed in Q4 but not yet delivered, and forecasted savings from purchases expected to be made by 31 December 2015. 2016 forecasted savings are based on Q4 reference prices and 2015 volumes. The 2016 price for TLE and TEE is based on a conservative estimate of price point. The number of patients treated was calculated by dividing the savings by a conservative average cost of treatment (US$120).

“The improved API supply has generated cost reductions for some ARVs. These cost reductions have been passed on to the Global Fund.”

“With the long-term forecast we are able to efficiently manage API across the production cycle. This

improved efficiency has generated savings.”

16

Figure 8: 2015 cost savings

Manufacturers agreed that the strategy is helping to improve the market situation. All manufacturers agreed that the visibility, predictability and stability of the long-term commitments have allowed for improvements in production planning and inventory management. In particular, ARV manufacturers indicated that the improved predictability and stability of orders have helped to improve ARV availability and delivery rates.

Long-term framework agreements The Global Fund has used long-term framework agreements to streamline the supply chain to improve availability, affordability and delivery. As Figure 9 shows, long-term framework agreements avoid the administrative time and enable manufacturers to better plan production and distribution. Figure 9: Causal chain of long-term framework agreement

“The procurement strategy is really improving market dynamics – it enables more people to be put on treatment with the same amount of funding.”

17

Supply chain improvements have reduced processing time and increased the time available for cost-effective shipment of goods. Improvements in the supply chain have freed up approximately 30 days which provides an opportunity to increase the use of shipment by sea. Shipment by sea requires more time compared to shipment by air, but is far more cost-effective. Individual countries are beginning to benefit from these improvements.

Shipment cost savings, Tanzania28 Tanzania increased the proportion of shipments it receives by sea Tanzania received over 50 percent of its shipments by sea in 2015, compared to only a quarter in 2014. This has resulted in large cost savings as air is substantively more expensive than sea freight. Preliminary estimates suggest that this saved Tanzania US$2 million in 2015. These savings could have treated approximately an additional 17,00o patients.29

The Global Fund aims to play a greater role in the strategic management of the supply chain in the future. Towards the end of 2016, the Global Fund aims to make further improvements to the supply chain by consolidating shipments and by negotiating improved rates with freight forwarders.

Vendor Managed Inventory The Global Fund established a new tool – the Vendor Managed Inventory – to rapidly respond to risks of shortages and stock-outs across the whole grant portfolio especially for non-PPM grants. Stock-outs can lead to treatment interruption and the development of drug resistance, increased mortality and morbidity, and erode patient faith in the health care system. Before the strategy, the Global Fund did not have an effective tool to respond to these urgent requirements other than to work to try to accelerate regular production. Figure 10: Causal chain of Vendor Managed Inventory

The Vendor Managed Inventory has reduced the delivery time of urgently required products

to three to seven weeks from the manufacturer to the country. Manufacturers commit to holding

a proportion of their annual commitment in readily accessible stocks under the Vendor Managed Inventory.

Manufacturers are also reporting on their overall stock levels for all products so the Global Fund has

visibility on available products. This allows the Global Fund to be far more responsive to supply shortfalls

and stock-outs, and deliver emergency products in just three to seven weeks. The Global Fund ensures that

the Vendor Managed Inventory does not encourage poor forecasting and planning by conducting an

analysis on the cause of each emergency request.

Country-level improvements in response to stock-outs have been achieved. In 2015, the Vendor

Managed Inventory was accessed by five countries facing ARV stock-outs or supply interruptions. In

Uganda, deliveries were made to the central medical store within six to eight weeks after a stock-out

occurred in June. Similarly, when a stock shortage was reported in Niger in August, an emergency shipment

occurred within just four weeks, and subsequent deliveries were completed within 6.5 weeks.

28 Global Fund analysis. Cost saving was estimated by calculating the difference between the actual spend on shipments in 2015 and the hypothetical spend on shipments if the ratio between air and sea shipments was the same as in 2013 and 2014. The number of patients treated was calculated by dividing the savings by a conservative average cost of treatment (US$120). 29 UNAIDS database, accessed on 3 December

18

Paediatric ARV Procurement Working Group

The Global Fund, along with partner organizations, established the PAPWG in 2011 to

improve market outcomes in the paediatric ARV market. The UNITAID / CHAI Paediatric Project,

which entailed a single procurement mechanism for paediatric ARVs in 40 countries, was phased out in

2011. This raised concerns that an already fragile market would revert to a more fragmented state. The

PAPWG was established to bring together the major financiers and procurers of paediatric ARVs and

technical bodies and experts to continue a coordinated approach to paediatric ARV procurement. The goal

of the PAPWG is to secure the market to ensure timely and consistent access to paediatric ARVs in order to

sustain and scale-up paediatric HIV treatment.

The Procurement Consortium of the PAPWG improves paediatric markets by aligning and

coordinating operational procurement activities. The Procurement Consortium is a sub-group

made up of PAPWG members who engage directly in paediatric ARV procurement. Among other activities,

the Procurement Consortium works to provide demand visibility to manufacturers and consolidate demand

towards the optimal formulations identified by technical partners.30 The Procurement Consortium also

coordinates orders across participating countries. This reduces fragmentation and allows manufacturers to

better plan production and produce full batches. Since 2011, the PAPWG has achieved tremendous progress

towards securing a steady supply of paediatric ARVs in more than 70 countries and has worked effectively

to promote the procurement of optimal paediatric ARVs. The supply of most optimal products is now

mainstreamed with few challenges and the group now focuses on the more challenging limited-use

products.

The Global Fund continues to lead the PAPWG as part of its ARV strategy.

The Global Fund pursues its strategic objectives for paediatric ARVs through the PAPWG. For example, a

key objective of the procurement strategy was to ensure rapid adoption of WHO recommended regimens.

The advocacy and country support provided by the PAPWG has contributed to 87 percent of paediatric ARV

spend going to IATT optimal or limited use products in 2014. Of paediatric ARVs purchased through the

PPM, almost 95 percent of spend was on optimal products by August 2015, compared to only 50 percent in

2011. Going forward, the Global Fund, in partnership with UNITAID will leverage the PAPWG platform to

pursue similar interventions for other small, fragmented markets supporting the supply of existing

introduction of new optimal WHO-recommended products.

Collaborative projects The Global Fund is working with manufacturers to improve other aspects of the ARV market

through collaborative projects. In addition to the joint initiatives around target pricing, API

optimization and the Vendor Managed Inventory, the Global Fund is working with manufacturers to

achieve other objectives such as stimulating development of the African pharmaceutical sector. As part of

this collaborate project, a number of suppliers have expanded their production and packaging activities in

Sub-Saharan Africa. Others have completed feasibility studies. Additionally, the Global Fund has procured

ARVs from Cipla Quality Chemical Industries in Uganda for the first time. The Global Fund also has

collaborative projects around product development. Through these projects the Global Fund monitors

product development, and has regular reviews with manufacturers to ensure the Global Fund is poised to

support the introduction of new products.

30 The list of optimal formulations is developed by the Inter-Agency Task Team on the Prevention and Treatment of HIV Infection in Pregnant Women, Mothers and Children.

19

IV. Viral Load Monitoring and Early Infant Diagnosis

01 Market Overview and Recent Market Shifts Viral load monitoring is a critical pillar for the effective diagnosis of HIV/AIDS. WHO guidelines recommend quantitative viral load monitoring as the tool for diagnosing and confirming the failure of antiretroviral therapy. Viral load testing is also the recommended technology for identifying HIV positive infants (Early Infant Diagnosis). The viral load monitoring market is forecasted to continue to grow due to increasing demand and the arrival of new point-of-care (POC) technologies.31 The volume of the global viral load market is expected to reach between 20-40 million tests per year by the end of this decade, with total market value potentially exceeding US$200 million.32,33,34,35,36 New POC products are expected to enter the market in the next years. Demand forecasts for early infant diagnostic tests vary by source, and range from one million to three million tests in 2018. 37

The Global Fund expects to be an increasingly important financier of viral load monitoring and early infant diagnosis. The Global Fund has an annual viral load spend of US$20-30 million across all Principal Recipients (PRs), and purchased tests from three different manufacturers in 2014.38 The Global Fund spend could grow by 50-100 percent per annum over the few next years, depending on the rate of technological innovation, the funding envelope approved for HIV products, and the extent to which viral load is prioritized.39

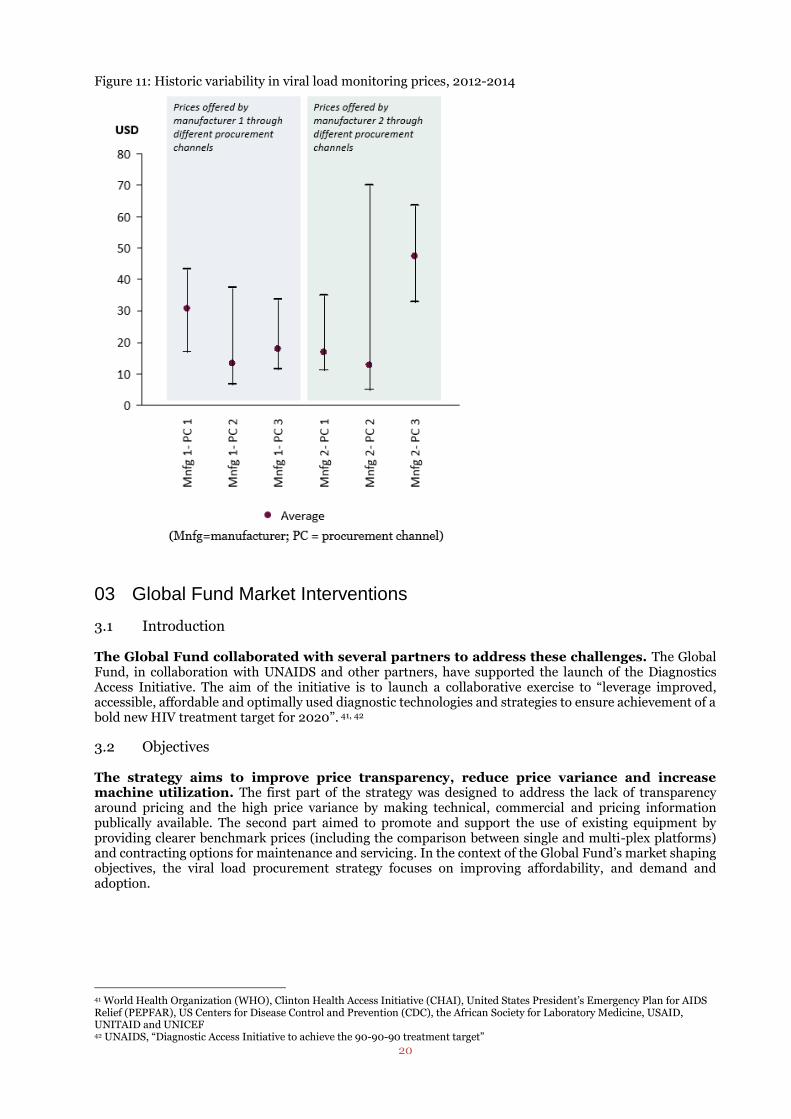

02 Market Challenges There are significant market challenges in the viral load and early infant diagnostic markets, predominantly around affordability. Viral load monitoring tests are relatively expensive that is aggravated by a lack of price transparency. In the past, manufacturers have offered very different prices to programmes and procurement channels. The price variance is illustrated in Figure 11. It shows that the price of viral load monitoring (including reagents and the other components) is highly variable, even for a given manufacturer, with prices ranging between US$10–85 per test.40 There are additional challenges around low utilization and limited operational capacity. Timely delivery of reagents and installation of equipment, ensuring repair and maintenance services, especially at lower levels in health systems, has been challenging. This leads to downtime, lack of machine utilization and low availability of tests. Additionally, programmes often have challenges in adoption, training and integration of diagnostic tests into clinical workflows.

31 CHAI, HIV Viral Load Testing Market Analysis, 2012. 32 This assumes that the size of the funding envelope also increases 33 CHAI estimates that ~8 million tests will be done in small rural clinics and ~9 million tests in larger peri-urban clinics (2020). 34 WHO, HIV diagnostic tests in low- and middle-income countries: forecasts of global demand for 2014-2018, 2015. 35 CHAI, HIV Viral Load Testing Market Analysis, 2012 36 Total volume of 20-40 million tests is based on a range of estimates; market size of US$200 million is a CHAI forecast for 2020. 37 WHO, HIV diagnostic tests in low- and middle-income countries: forecasts of global demand for 2014-2018, 2015. 38 The Global Fund, Request For Proposal (RFP) Tgf-14-063, 22 December 2014. 39 Ibid. 40 This price includes only the reagents and (most of) the consumables.

20

Figure 11: Historic variability in viral load monitoring prices, 2012-2014

03 Global Fund Market Interventions

3.1 Introduction The Global Fund collaborated with several partners to address these challenges. The Global Fund, in collaboration with UNAIDS and other partners, have supported the launch of the Diagnostics Access Initiative. The aim of the initiative is to launch a collaborative exercise to “leverage improved, accessible, affordable and optimally used diagnostic technologies and strategies to ensure achievement of a bold new HIV treatment target for 2020”. 41, 42

3.2 Objectives

The strategy aims to improve price transparency, reduce price variance and increase machine utilization. The first part of the strategy was designed to address the lack of transparency around pricing and the high price variance by making technical, commercial and pricing information publically available. The second part aimed to promote and support the use of existing equipment by providing clearer benchmark prices (including the comparison between single and multi-plex platforms) and contracting options for maintenance and servicing. In the context of the Global Fund’s market shaping objectives, the viral load procurement strategy focuses on improving affordability, and demand and adoption.

41 World Health Organization (WHO), Clinton Health Access Initiative (CHAI), United States President’s Emergency Plan for AIDS Relief (PEPFAR), US Centers for Disease Control and Prevention (CDC), the African Society for Laboratory Medicine, USAID, UNITAID and UNICEF 42 UNAIDS, “Diagnostic Access Initiative to achieve the 90-90-90 treatment target”

21

3.3 Implementation In the strategy, the Global Fund enters into framework agreements with selected manufacturers. These framework agreements define the contractual and pricing frameworks for the procurement of viral load monitoring and early infant diagnosis for the next three to seven years. As part of the framework agreements, agreed terms, conditions and pricing will be used for the Global Fund PRs and other public buyers.43 The framework agreements do not include any volume commitments, per se, however efforts to coordinate demand and contracting can be put in place if it is advantageous to do so. The Global Fund has used the outcomes from its tender to create an online tool which provides technical and commercial information for buyers. The Global Fund has combined information from the framework agreements with market intelligence to create a publicly available online selection and procurement tool (Figure 12).44 The tool provides guidance on programmatic considerations, technology and platform selection, contracting options and benchmark prices. Figure 12: Snapshot of the viral load and early infant diagnostic tool45

43 (i) Global Fund Grant PRs and sub-recipients; (ii) Governments of host countries; (iii) United Nations-related organizations, non-governmental organizations and not-for-profit organizations; and (iv) development and/or public health financing mechanisms 44 The Global Fund, Viral load and early infant diagnosis selection and procurement information tool, 2015 45 Left Graph: Viral Load and Early Infant Diagnosis Selection and Procurement Information Tool- Navigation diagram. Right Graph: Total Cost of Ownership – Viral Load at 100k pa price break. Graph provides indicative TCO price make-up for each supplier assuming 100k global tests undertaken per annum (i.e. 300k over three years). Indicative TCO as individual suppliers will have slightly different models; for example, logistics costs will vary between countries.

22

3.4 Tender outcomes The Global Fund issued an RFP to manufacturers supplying quality approved products, and selected manufacturers through a two-step process. First, the Global Fund evaluated manufacturer responses on commercial and technical factors. Second, the Global Fund held face-to-face meetings to get further commercial and technical clarity and obtain best and final offers. The Global Fund selected a panel of seven viral load manufacturers. This included four new manufacturers. Manufacturers have provided contractually binding technical and commercial information on their available offerings, including an all-inclusive price, or TCO, for each offering. Manufacturers have been very supportive of the strategy. Manufacturers were very positive and supportive of the interventions, and praised the collaborative approach the Global Fund has taken in particular.

3.5 Market outcomes Publication of the selection and procurement tool is expected to lead to more informed and cost-effective buying decisions. Increased knowledge of the technical, contractual and commercial options available will allow buyers to make more informed buying decision. Informed decisions will include agreeing commercial arrangements that benefit both buyers and manufacturers, for example with more market certainty. As buyers change their purchasing behavior, manufacturers may reactively or proactively adjust their pricing. The long-term impact is greater value-for-money for Global Fund PRs, achieved through more cost-effective allocation of resources and more affordable pricing (Figure 13). Furthermore, this tool is publicly available and may also be used by countries or other buyers purchasing with their own funds. As the tool increases transparency in the market place, this reduces barriers to other manufacturers and may also help to further diversify the supply base. In addition, increased reagent rental options and more informed decision-making should lead to reduced downtime, ensure adequate service and maintenance, a higher availability of viral load testing and a reduction in long-term mortality and morbidity. Figure 13: Causal chain of publication of the benchmark tool

Reductions in price variance and average price are already being observed. The positive trend in achieving lower test pricing has already been seen for a number of programmes. Additionally, some manufacturers have adjusted their offering in response to the publishing of the online tool, and have removed the difference in price offered between purchasers(Figure 14). The price of the test has declined by 33 percent on average.

23

Figure 14: Current viral load monitoring prices in comparison with 2012-2014 historic variability

The Global Fund has realized cost savings and better contractual terms through the strategy. The decreased test price has resulted in cost savings of around 33 percent. This will save the Global Fund at least US$30 million over three years in direct costs alone, with the potential of significantly larger savings in the future if volumes increase. Other buyers and implementers will also benefit from the strategy through use of the price-comparison tool and by accessing the improved pricing and contractual terms. There are already advanced discussions taking place with PEPFAR and UNITAID on leveraging the tender outcomes.

The strategy has also increased the range of reagent rental options available, which will help to drive increased utilization in the long-term.46 The new tool provides more detail on the expanded range of technical and commercial operations available, and provides benchmark prices and contracting options for maintenance and servicing. Previously, only a couple of manufacturers had offered rental options to PRs, whereas now nearly all manufacturers offer such options. As well as providing benefits for the Global Fund and buyers, manufacturers have also benefited from the new tool. New and existing manufacturers agreed that the new tool is helping to improve transparency. Manufacturers also mentioned that the tool is improving their dialogues with countries and distributers.

46 Reagent rental contracts are an agreement between the diagnostic company and buyer in which the diagnostic company provides an all-inclusive price including the analyser, support, service and maintenance (at no upfront cost) and the buyer agrees to purchase reagents from the company over a defined period of time. The company is thus incentivised to ensure the analyser is fully operational.

Transparency is the biggest advantage of the process. People know what is available. That matters a lot.”

“I think I can speak for all suppliers when I say we were all initially slightly uncomfortable with the idea of pricing data being published so broadly, but in reality it has made conversations with buyers

much easier”

“The online tool is an example of a very good business practice: it is a very educational tool for the buyers; it gives buyers a very good sense of the complexity of viral load products, and where to buy

them; and it also lays out the cost structure...we will continue to use this tool.”

24

V. Next Steps The new ARV and viral load procurement strategies have already shown early signs of positive impacts on the market. These impacts will continue to emerge. Meanwhile, the Global Fund is continuously assessing the achievement of its market shaping objectives and pursuing additional opportunities. The Global Fund recognizes that additional actions might be required to further enhance the impact of the ARV strategy. The main points of feedback from manufacturers and partners were for the Global Fund to closely monitor the risk of market exits or unsustainable pricing offered by manufacturers that received reduced volumes as result of the tender, and to monitor the long-term impact on the ARV market structure. A set of potential next steps based on this feedback, and an assessment of progress-to-date, is outlined below.

Pursue relevant opportunities to reduce costs sustainably for buyers and manufacturers;

Improve visibility of ARV demand, particularly predicting the timing of shifts in demand due to product or regimen changes;

Continue to stimulate the usage of the most cost-effective products and treatment regimens

Influence the relative pricing of WHO recommended “alternative” or “interchangeable” products to generate a balanced range of products that are not solely price-driven.

Continue to ensure the sustainable supply of low-volume, limited use or specialized products for adults and children; and

Continue to work with countries to standardize packaging and labelling and expand country registration, with the aim to maximize production efficiency and flexibility;

The viral load strategy could also be refined through additional action to increase the overall impact of the strategy. The main points of feedback emphasized the difficult balance that the Global Fund is trying to strike between simplicity and comprehensiveness. Interviewees mentioned the need and desire to maintain a simple and easily understandable tool, but also one that takes all nuances into account to enable users to make greater apples-to-apples comparisons. To enhance the impact of the viral load procurement strategy further, and to improve the tool going forward, the Global Fund will take the following actions:

Continue to develop and improve the tool in collaboration with partners;

Incentivize the provision of acquisition models, where manufacturers provide staggered deliveries to take into account the short shelf-life of diagnostics and the requirement for refrigerating test kits, should an annual order be desired.47

47 WHO, Technical and operational considerations for implementing HIV viral load testing, July 2014

25

VI. References

i. The Global Fund Website, 17 November 2015, http://www.theglobalfund.org/en/hivaids/ ii. Stephanie Nolen, 28 Stories of AIDS in Africa. New York: Portobello Books, 2007.

iii. WHO, Global health sector response to HIV, 2000-2015: focus on innovations in Africa, Progress Report, 2015, available at http://apps.who.int/iris/bitstream/10665/198065/1/9789241509824_eng.pdf?ua=1

iv. United Nations, the Millennium Development Goal Report, 2015, http://www.un.org/millenniumgoals/2015_MDG_Report/pdf/MDG%202015%20rev%20(July%201).pdf

v. The Global Fund Website, “Global Fund Embraces Fast-Track Approach on AIDS”, 1 December 2015, http://www.theglobalfund.org/en/news/2015-11-30_Double_the_Number_of_People_on_HIV_Treatment_by_2020/

vi. UNAIDS, 90-90-90 – An ambitious treatment target to help end the AIDS epidemic, 2014, http://www.unaids.org/en/resources/documents/2014/90-90-90

vii. Dutta et al., “The HIV Treatment Gap: Estimates of the Financial Resources Needed versus Available for Scale-Up of Antiretroviral Therapy in 97 Countries from 2015 to 2020”, 24 November 2015

viii. NAM, “Treatment cascades show 90-90-90 goal within reach for some – but Eastern Europe lags behind Africa”, 22 July 2015, http://www.aidsmap.com/Treatment-cascades-show-90-90-90-goal-within-reach-for-some-but-Eastern-Europe-lags-behind-Africa/page/2986802/

ix. The Global Fund, “Report of the market dynamics and commodities ad-hoc committee”, 11-12 May 2011, http://www.theglobalfund.org/documents/board/23/BM23_09MDC_Report_en/

x. Datamonitor, the HIV Market outlook to 2016, 2011, http://store.datamonitorhealthcare.com/Product/the_hiv_market_outlook_to_2016?productid=960DEEF7-F3E9-413F-AED9-F71F89E0C508

xi. CHAI, ARV market report, 2014, http://45.55.138.94/content/uploads/2015/05/ARV-Market-Report_Dec-2014_TO-PUBLISH-2.pdf

xii. UNAIDS, “UNAIDS announces that the goal of 15 million people on life-saving HIV treatment by 2015 has been met nine months ahead of schedule”, 14 July 2015, http://www.unaids.org/en/resources/presscentre/pressreleaseandstatementarchive/2015/july/20150714_PR_MDG6report

xiii. WHO, Antiretroviral medicines in low- and middle-income countries: forecasts of global and regional demand for 2014-2018, 2015, http://www.who.int/entity/hiv/pub/amds/arv-forecast2014-2018/en/index.html

xiv. WHO, WHO Guideline on When to Start Antiretroviral Therapy and on Pre-exposure Prophylaxis for HIV, 2013, http://apps.who.int/iris/bitstream/10665/186275/1/9789241509565_eng.pdf?ua=1

xv. CHAI, ARV Market Report: The State of the Antiretroviral Drug Market in Low- and Middle-Income Countries, 2014-2019, November 2015, http://www.clintonhealthaccess.org/content/uploads/2015/11/CHAI-ARV-Market-Report-2015_FINAL.pdf

xvi. UNITAID, HIV Medicines Technology and Market Landscape, 2014, http://www.unitaid.eu/images/marketdynamics/publications/HIV-Meds-Landscape-March2014.pdf

xvii. The Global Fund, 2015 Results Report, 2015, http://www.theglobalfund.org/documents/publications/annual_reports/Corporate_2015ResultsReport_Report_en

xviii. The Global Fund, The Global Fund’s Market Shaping Strategy, Committee Decision (SIIC) and Committee Information (FOPC) internal document, 2015.

xix. PwC, Global Supply Chain Survey 2013, https://www.pwc.com/gx/en/consulting-services/supply-chain/global-supply-chain-survey/assets/global-supply-chain-survey-2013.pdf

xx. UNAIDS database, accessed 19 November 2015, available at http://aidsinfo.unaids.org/ xxi. The Global Fund, The Global Fund Register of Unfunded Quality Demand, accessed 19 November 2015,

available at http://www.theglobalfund.org/en/uqd/ xxii. CHAI, HIV Viral Load Testing Market Analysis, 2012,

http://mat1.gtimg.com/gongyi/2012/enzhenduandahui/6ZachKatz.pdf xxiii. WHO, HIV diagnostic tests in low- and middle-income countries: forecasts of global demand for 2014-2018,

2015, http://apps.who.int/iris/bitstream/10665/179864/1/9789241509169_eng.pdf?ua=1 xxiv. CHAI, HIV Viral Load Testing Market Analysis, 2012,

http://mat1.gtimg.com/gongyi/2012/enzhenduandahui/6ZachKatz.pdf xxv. The Global Fund, Request for Proposal (Rfp) Tgf-14-063, 22 December 2014, accessed 17 November 2015,

http://www.theglobalfund.org/documents/psm/TGF-14-063/Solicitation_TGF-14-063_RFP_en/ xxvi. UNAIDS, “Diagnostic Access Initiative to achieve the 90-90-90 treatment target” The Global Fund,

http://www.unaids.org/sites/default/files/media_asset/20150422_diagnostics_access_initiative.pdf xxvii. Viral load and early infant diagnosis selection and procurement information tool, 2015, accessed 17

November 2015, http://www.theglobalfund.org/documents/psm/PSM_ViralLoadEarlyInfantDiagnosis_Content_en/

xxviii. WHO, Technical and operational considerations for implementing HIV viral load testing, July 2014, http://www.who.int/hiv/pub/arv/viral-load-testing-technical-update/en/