improving development results through excellence in … · improving development results through...

TRANSCRIPT

48032 v5

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

IMPROVING DEVELOPMENT RESULTS THROUGH EXCELLENCE IN EVALUATION

Review of IDA Internal Controls An Evaluation of Management’s Assessment

and the IAD Review

Volume V

Report on the Completion of Part IA Process Mapping and Effectiveness of Control Design

This paper is available upon request from IEG-World Bank.

2009 The World Bank

Washington, D.C.

©2009 The Independent Evaluation Group, The World Bank Group 1818 H Street NW Washington DC 20433 Telephone: 202-473-1000 Internet: www.worldbank.org E-mail: [email protected] All rights reserved 1 2 3 4 5 10 09 08 07

This volume, except for the elements contributed by group and institutions outside the Independent Evaluation Group, is a product of the staff of the Independent Evaluation Group of the World Bank Group. The findings, interpretations, and conclusions expressed in this volume do not necessarily reflect the views of the Executive Directors of The World Bank or the governments they represent. This volume does not support any general inferences beyond the scope of this evaluation, including any references about the World Bank Group’s past, current, or prospective overall performance.

The World Bank Group does not guarantee the accuracy of the data included in this work. The boundaries, colors, denominations, and other information shown on any map in this work do not imply any judgment on the part of the World Bank Group concerning the legal status of any territory or the endorsement or acceptance of such boundaries.

Rights and Permissions

The material in this publication is copyrighted. Copying and/or transmitting portions or all of this work without permission may be a violation of applicable law. The Independent Evaluation Group encourages dissemination of its work and will normally grant permission to reproduce portions of the work promptly.

For permission to photocopy or reprint any part of this work, please send a request to the Independent Evaluation Group. ISBN: 978-60244-113-2 Independent Evaluation Group Knowledge Programs and Evaluation Capacity Development (IEGKE) E-mail: [email protected] Telephone: 202-458-4497 Facsimile: 202-522-3125 Printed on recycled paper

Acronyms and Abbreviations

AAA Analytical and Advisory Activities AC Audit Committee ACS Administrative and Client Support

Network AICPA American Institute of Certified

Public Accountants AROE Annual Review of Operations

Evaluation ARDE Annual Review of Development

Effectiveness ARPP Annual Review of Portfolio

Performance AS2 Audit Standard No. 2 BP Bank Procedure BPM Business Process Module CAS Country Assistance Strategy CDS Control Detail Sheet CODE Committee on Development

Effectiveness COSO Committee of Sponsoring

Organizations, of the Treadway Commission

CPIA Country Policy and Institutional Assessment

CTR Controller’s DEC Development Economics and Chief

Economist DPL Development Policy Loan ESW Economic and Sector Work GPN General Procurement Notice FM Financial Management FMA Fiduciary Monitoring Agent IAD Internal Audit Department ICR Implementation Completion Report IDA International Development

Association IEG Independent Evaluation Group

(formerly OED) IL Investment Lending

IRMF Integrated Risk Management Framework

ISR(R) Implementation Status (and Results) Report

IT Information Technology LOA Loan Department NGO Non-Governmental Organization OD Operational Directive OED Operations Evaluations Department OM Operational Memorandum OP Operational Policy OPCS Operations Policy and Country

Services PAS Procurement Accredited Specialist PCAOB Public Company Accounting

Oversight Board PCPI Post Conflict Performance

Indicators PMT Project Management Team PO Process Overview PPF Project Preparation Facility PS Procurement Specialist SME Subject Matter Experts QAG Quality Assurance Group QEA Quality at Entry Assessment QSA Quality of Supervision Assessment RMCVP Vice President, Resource

Mobilization and Co-financing RMFM Regional Manager, Financial

Management ROC Regional Operations Committee ROW Risk Opportunity Workshop SIL Specific Investment Loan SOX Sarbanes-Oxley Legislation TSS Transition Support Strategy TTL Task Team Leader RS Risk Scan VAA VPU Access Administrator VPU Vice Presidential Unit WBI World Bank Institute

i

Contents KEY TECHNICAL TERMS .........................................................................................III

PREFACE................................................................................................................... V

EVALUATION SUMMARY ....................................................................................... VII

1. BACKGROUND AND DESCRIPTION OF APPROACHES..........................1

Origins of the Study.................................................................................................1 The COSO Perspective ............................................................................................2 Integrating the COSO Framework into Bank Operations .....................................4 IEG’s Approach to its Evaluation ...........................................................................4 Summary of Approaches: Management Assessment and the IAD Review........7

2. MANAGEMENT’S ASSESSMENT .............................................................11

Background and Objective....................................................................................11 Management’s Method: From the IDA Charter to Policies to Business Processes ...............................................................................................................11 IEG’s Evaluation of Management’s Approach and Method................................17 Management’s Main Findings and Conclusions: IEG Comment and Evaluation.................................................................................................................................22

Management’s Broad Conclusions................................................................................. 22 Management’s Highlighted Deficiencies (paragraph 26 of its report)............................. 23 Management’s List of Additional Issues ......................................................................... 25

Findings from IEG’s own Analysis .......................................................................26 Issues Related to Controls ............................................................................................. 26 Issues Related to Management’s Descriptive Materials and Mapping........................... 27

3. THE IAD REVIEW AND REPORT ..............................................................31

Context for IEG’s Review of IAD’s Work..............................................................31 IAD’s Objective.......................................................................................................31 IAD’s Scope and Approach for Part IA.................................................................31 IAD’s General Observation and Key Issues ........................................................32

4. CONCLUSIONS AND RECOMMENDATIONS...........................................37

Overall IEG Evaluation...........................................................................................37

Evaluation Managers Vinod Thomas

Director-General, Evaluation

Ajay Chhibber Director, Independent Evaluation Group-World Bank

Nils Fostvedt Task Manager

Ian Hume Team Leader

ii

Boxes Box 4. Stages in the Study of IDA Internal Controls.................................................... 2 Box 5. Key Components in the Management Assessment, IAD Review, and IEG Evaluation (Part I) ....................................................................................................... 7 Box 6. Overall Timeline for Completion of IDA 14 Assessment .................................. 8 Box 7. Building Blocks in Management’s Approach ...................................................13 Box 8. Management’s List of 30 Business Process Modules .....................................14 Box 9. Business Process Modules Excluded from Compliance Assessment.............15 Box 10. Summary of Principal Issues Identified by Management, IAD, and IEG ..........39

Figures Figure 1. The COSO Framework: Components, Objectives, and Risk Factors........... 3 Figure 2. Overview Scope Map of Management’s Assessment .................................16

Annexes ANNEX A. THE COSO FRAMEWORK .....................................................................43 ANNEX B. STANDARDS AGREED BY MANAGEMENT, IAD AND IEG TO BE USED IN ASSESSING DEFICIENCIES, SIGNIFICANT DEFICIENCIES AND MATERIAL WEAKNESSES ......................................................................................47 ANNEX C. ILLUSTRATION OF POTENTIAL INTERNAL CONTROL DESIGN WEAKNESSES..........................................................................................................50 ANNEX D. A TYPICAL BPM: DESCRIPTIVE MATERIAL........................................57 ANNEX E. DOES THE CLUSTER OF BPMS REPRESENT THE UNIVERSE OF IDA CONTROLS?.............................................................................................................65 ANNEX F. METHOD AND RESULTS IN APPLYING THE BUSINESS PROCESS TEMPLATE................................................................................................................70 ANNEX G. STATISTICAL APPENDIX ......................................................................73

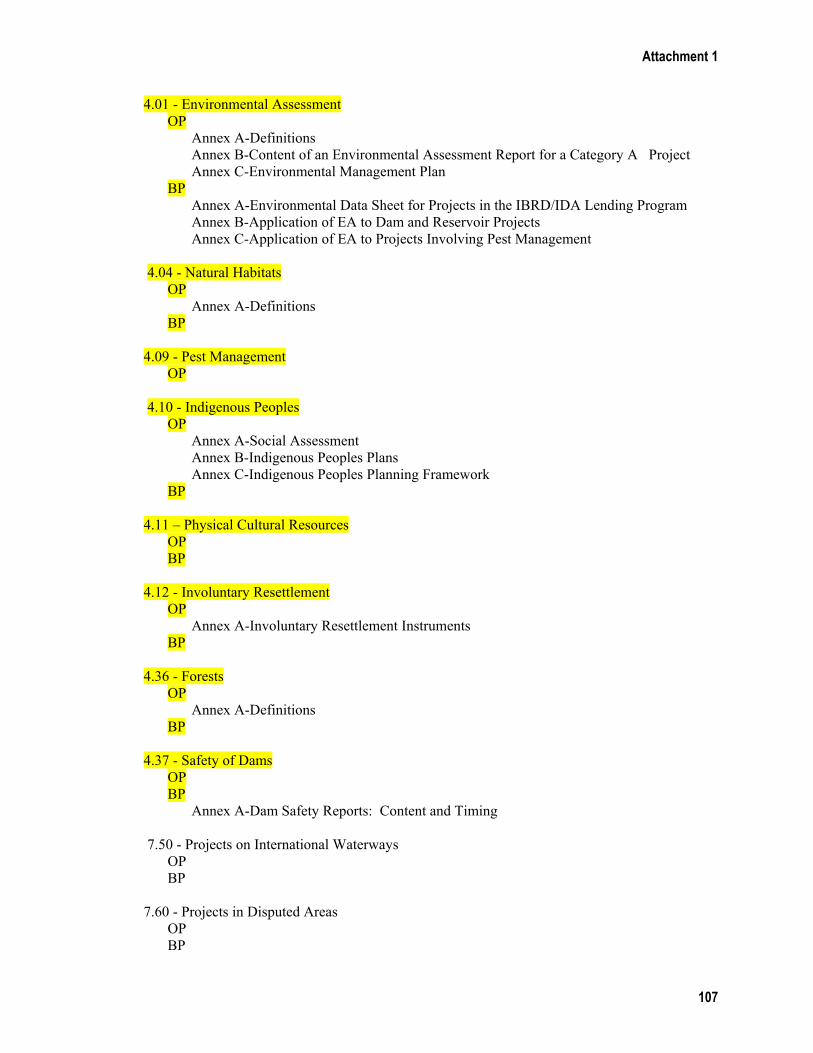

Source Reports ATTACHMENT 1: MANAGEMENT REPORT ON ITS REVIEW OF IDA CONTROLS...................................................................................................................................83 ATTACHMENT 2: IAD REVIEW OF MANAGEMENT’S ASSESSMENT................117

KEY TECHNICAL TERMS

iii

Key Technical Terms Internal Controls: Controls, individually or in collective fashion, are structured means within an organization to enable it to achieve its business objectives, while addressing risk. Control instruments in-clude the control framework (in IDA’s case, the COSO framework), organizational checks and balances, published policies and required procedures, among others.

COSO Integrated Framework: A framework of management princi-ples (“COSO components”) in an organization which, when collec-tively operating as intended, will ensure the attainment of three key organization goals (“COSO objectives”), namely: reliable financial re-porting; operational effectiveness and efficiency; and compliance with laws and regulations, (or in IDA’s case with its charter and internal policies and procedures). The COSO components are: Control Envi-ronment; Risk Assessment; Control Activities; Monitoring and Learn-ing; Information and Communications.

Risk Focal Points: In the way the Management of the Bank and IDA have adapted the COSO framework to their own needs, four key points of risk which face the mission of the Bank Group—and are es-pecially relevant to IDA—have been defined and added to the COSO framework, namely: Strategy Effectiveness; Operational Efficiency; Financial Soundness; and Stakeholder Support.

Audit Standards: Criteria established by recognized accounting and audit bodies, which, in the course of reviews of internal controls sys-tems, enable the definition of deficiencies, significant deficiencies, and material weaknesses that may be revealed in those systems.

Business Process Modules (BPMs): Management chose to conduct this review of internal controls by identifying the main business proc-esses in which IDA is engaged on a daily basis in the course of its op-erations. These processes, 30 in all, covering IDA allocation, the CAS process, the main lending products (SILs and DPLs), and the fiduci-ary, contractual, safeguards and quality assurance processes that sup-port lending, were each mapped and described as separate business process modules, each containing the key internal controls that are the subject of the review.

Process Map: The flow chart that graphically depicts all steps in a business process module.

KEY TECHNICAL TERMS

iv

Key Control: A gateway and decision point, involving key units and IDA staff, in a given business process module, through which a busi-ness transaction being processed must pass. It is the effectiveness in design of these controls and the subsequent testing of the effective-ness of their operation that is at the center of this review.

Business Process Template: A standardized questionnaire and rating system used by IEG to provide quality ratings of Management’s method and approach in identifying, describing and mapping the business processes, and its method in assessing control design effec-tiveness and effectiveness of control operation.

Evaluation Panels: In applying its Business Process Template, IEG as-sembled 3-4 person panels, including specialists in the particular dis-cipline covered by the given BPM. The panels arrived at consensus judgments on what should be the ratings applied to each section of the module, according to their evaluation of the materials presented by Management.

Entity Level Controls: This refers to the control framework that gov-erns an organization at its aggregate level, emanating from central management down to the operating or business process level. In IDA’s case, the reference is to the elements of the COSO framework. Doing a controls review that started with an examination of entity-level controls, could be described as a “top down” approach.

Bottom up Approach: The approach adopted by Management in its assessment did not begin with a “top-down” entity-level review, but focused first on business processes at the operating level. Hence, it has been described as a “bottom-up” approach.

Walkthrough: An inter-active interview and review of process docu-mentation conducted by Management with relevant teams of IDA staff knowledgeable in a particular business process and its associated controls, with a view to verifying that controls are designed in the way described, and operate in the way intended.

Deficiencies, Significant Deficiencies, Material Weaknesses: Design flaws, omissions, or non-compliant operation of controls, discovered in the course of a controls review, denoting ascending order of seri-ousness. The precise criteria by which the three categories of material-ity are distinguished are explained in Annex B.

v

Preface In the IDA 14 Replenishment Report Bank management committed to carry out an independent comprehensive assessment of IDA’s control framework including internal controls over IDA operations and com-pliance with its charter and policies. Each part of this review is to be done in a three-phase approach: the first phase would be a self as-sessment by Management, to be followed by an Internal Audit De-partment (IAD) review and report on management’s self assessment, and an IEG independent evaluation of management and IAD work. This report contains IEG’s evaluation of the work done by manage-ment, and reviewed by IAD, for Part IA of the overall review.

The basis for the work done by IEG in its evaluation included: the re-port prepared by Management reflecting its assessment (Attachment 1); access to all the underlying materials that Management generated in its process based descriptions, definitions of controls and its “walk-through” testing of control design effectiveness; and the report pre-sented by IAD (Attachment 2).

Under the task management of Nils Fostvedt, this report was pre-pared by Ian Hume, with the assistance of a core consultant team, in-cluding: Dexter Peach (Strategic Advisor, formerly Assistant Comp-troller General for Planning and Reporting, GAO), James Campbell and Rosemary Jellish (Consultants, both former Assistant Directors, GAO) and Barbara Yale. The core team was assisted, in selected top-ics, by: Jed Shilling, Tribhuwan Narain, David Goldberg, and Mo-hammed Farhandi.

vii

Review of IDA Internal Controls:

An Evaluation of Management’s Assessment and the IAD Review

This report has its origins in a commitment that IDA Management made as part of the IDA 14 Replenishment process, in which it undertook “to carry out an independent, comprehensive assessment of IDA’s internal control framework, including internal controls over IDA operations and compliance with its charter and policies.” Management proposed, and the Board agreed, that Management would make an assessment of the controls, to be followed by an IAD review of the assessment and an IEG independent evaluation of both Management and IAD reports.

Contacts Director-General, Evaluation Vinod Thomas, 202-473-6300 Director, IEGWB Ajay Chhibber, 202-458-4219 Evaluation Manager Nils Fostvedt, 202-458-0719 Evaluation Author Ian Hume

Press contact Melanie Zipperer, 202-458-2902

Web site www.worldbank.org/ieg

Management decided that it would conduct its assessment within the COSO integrated controls framework, but it would divide its study into two parts: Part I would deal with compliance issues, and be focused on controls at the level of 30 business proc-esses, identified as representing IDA alloca-tion, CAS and IDA lending products, sup-porting contractual, fiduciary and safeguard processes, and quality assurance; Part II would deal with issues of operational effi-ciency and effectiveness, and would include an examination of entity-level controls, within the full COSO framework.

Management subsequently divided Part I of the assessment into two stages: Part IA, recently completed and the subject of the present re-port, covers Management’s ap-proach and method in identifying and map-ping the business processes that represent IDA operations, and assesses the effective-ness of the design of controls within these processes; Part IB, to be completed early in 2007, will deal with the testing of how these controls actually operate, compared to their design. Part II is intended for completion by Management at the end of calendar 2007, with the full IEG evaluation expected in early 2008.

This IEG report contains the evalua-tion made by IEG of the work completed by both Management and IAD in their re-spective assessments and review of Part IA. IEG conducted its evaluation using a com-bination of approaches:

• Verifying the legal, methodological, and operational basis for the approach taken in the Management assessment;

• Reviewing Management’s findings and conclusions;

• Participating as observers in a selec-tion of Management’s “walkthroughs” (verification interviews with knowl-edgeable Bank staff, concerning the actual design and working of key con-trols in the business processes);

• Creating an evaluation tool (a stan-dardized template), which generated a quality data base, enabling IEG’s analysis and evaluation of Manage-ment’s method in identifying and building the process maps and de-scriptive materials, and in conducting its assessment of the effectiveness of control design;

• Within the context of COSO, making an evaluation of the scope limitations inherent in Management’s approach, and their impact on the quality of conclusions that can be drawn at this stage of the review.

Findings Management decided the best way to

track the use of IDA resources, was to fo-cus its assessment at the transactions level on business processes. Doing so, it pro-vided a rigorous, transparent and concrete

viii

method for addressing internal controls, which was applied thoroughly and well documented. The assessment resulted in the production of 30 busi-ness process maps, accompanied by detailed de-scription for each module and its key controls. Overall, the assessment resulted in the amassing of over 700 pages of evidentiary documentation, and in identifying a significant number of potential deficiencies. This represents progress in develop-ing an understanding of IDA’s internal controls at the transactions level.

As evidence of this progress IEG would cite the following: • As a basis to test for compliance, Manage-

ment has made a credible linkage between the IDA Articles, the Bank’s policies and proce-dures, and the business processes identified to represent IDA operations;

• The mapped Business Process Modules have provided a concrete and transparent means of identifying, assessing and testing key controls;

• Management’s methods of mapping and as-sessing the BPMs were rated by IEG to be of a generally satisfactory quality, though with some notable qualifications relating to the treatment of risk, and the need to improve some of the descriptive materials;

• Management’s “walkthrough” method of veri-fying the accuracy of the selected business processes and testing the design effectiveness of their key controls was rigorous, compre-hensive, transparent, and documented to a sat-isfactory standard, with some qualifications. Management asserts that its approach gave a

representative picture of IDA transactions proc-esses, and that controls for the IDA allocation process as well as other controls over various as-pects of IDA lending are appropriately designed to suggest that IDA resources are allocated and used in accordance with the IDA articles, and in-ternal policies and procedures. It also documents that the approach succeeded in uncovering a sig-nificant number of specific controls-related issues. Of these, Management highlighted five it consid-ered to be most serious: • Difficulties with retention of and accessibility

to documentation needed to verify the opera-tion of key internal controls;

• Problems in keeping current the IDA OPs and BPs, which have not kept pace with the pace of change within the Bank Group;

• The policy framework for SILs being seen as too complex and cumbersome;

• Existing processes and documentary re-quirements for projects is seen by staff as on-erous and inefficient;

• A disparity in the frequency with which DPLs (always) and SILs (seldom) are sent for Cor-porate Review, instead of Decision Meeting processing. An evaluation of controls within the COSO

framework requires that all its components be ex-amined. Since this has not yet been done, is too early to make definitive conclusions on the state of the overall framework. However, from the de-ficiencies so far revealed, IEG considers that the issues highlighted by Management related to documentation retention, and the state of OPs/BPs are areas of potential material weakness. Management has initiated remedial programs in both these areas, and a firmer basis to draw con-clusions about their materiality will be in place once testing has been completed in Part IB. IEG has also had to take account of the trade-offs and implications of process-based, bottom-up method chosen by Management for its assessment, and the scope limitations this has implied. From this per-spective, notwithstanding the progress made, IEG found notable weaknesses in Management’s ap-proach: • Because conclusions on controls within

COSO cannot be made piecemeal, but only within the framework as a whole, staging and dividing the study has effectively postponed the ability to make definitive conclusions on the outcomes of each stage of the review un-til the overall (Part II) assessment has been completed.

• Even the staging of the study between Part IA and Part IB makes conclusions on control design (Part IA) difficult until Part IB has been completed, because final judgments on design effectiveness cannot be made until the operation of the control has also been tested.

• Separating compliance and efficiency and ef-fectiveness is really not possible in practice: many business processes and their associated controls are as much to do with compliance as with efficiency and effectiveness, and these are best treated together rather than in sequence. To illustrate, although management has fo-cused its efforts to date on assessing compli-

ix

ance, most of the potential issues it has identi-fied are related to efficiency and effectiveness.

• Other scope limitations flowing from the de-lineation of the study—in particular the deci-sion to deal with IT systems and field offices in Part II, have yet further limited the conclu-sions that can be drawn in Part I, especially given IDA’s increasing decentralization, and the growing importance of IT in maintaining the integrity of central controls.

• In taking 30 business process modules to rep-resent the totality of IDA operations, Man-agement has given a good representation of lending operations and the associated fiduci-ary processes; however, it has chosen to ex-clude AAA and other Knowledge Products, which IEG regards as a significant omission.

• In principle, it is possible that by completing the entity-level review during Part II, and ad-dressing the postponed parts of the frame-work, Management will be able to mitigate these deficiencies in approach by linking re-sults from the various parts together, to pro-vide an overall statement. However, this will depend on there being no changes in any ba-sic parameters: controls will be assessed at different points in time, and policies, proce-dures, systems, organization structures may change during this period. IEG therefore arrives at a mixed conclusion

on completion of this stage of the study: satisfac-tory progress has been made in defining, locating and assessing key internal controls at the transac-tions level, and the results have revealed a number of deficiencies and possible weaknesses in the un-derlying controls; on the other hand, the general approach and scope limitations applying to this stage of the assessment prevent any positive asser-tions being made now regarding the effective op-eration of the overall system of controls.

IAD was also positive in its findings of what Management had contributed to the Bank Group’s knowledge of its internal controls sys-tems, and the new information provided at the process level, stating that it provided a compelling baseline to streamline operations and improve ef-ficiency going forward. IAD identified eight key issues which it drew to Management’s attention: The exclusion of certain processes from the IDA processes selected; the fact that IT controls were not examined during Part I; the absence of fraud

and corruption controls in the scope for Part I; outdated OPs and BPs; the need to categorize and take remedies for deficiencies; the issue of docu-mentation retention and accessibility; the assess-ment of entity level controls; and issues relating to walkthroughs.

With the exception of the emphasis given to fraud and corruption and walkthroughs, all of these issues are also raised by IEG, with similar emphasis, and are covered in IEG’s overall evalua-tion. With regard to fraud and corruption, IEG believes that they (a) should be examined as part of the entity-level controls, and (b) were implicitly handled by Management in its process level ap-proach. IEG agrees with IAD that more explicit mention of fraud and corruption issues could have been made in Management’s process-level assess-ment. With regard to walkthroughs, Management and IAD have applied differing concepts of the term. In addition to these highlighted issues, IAD has also indicated that it has found a number of other deficiencies (55 in all). While these have been listed by broad type, IAD has not yet catego-rized these as to their materiality (i.e. seriousness of their possible impact on risk mitigation).

Recommendations Given the interim nature of the work so far

completed and the limited conclusions that can be drawn from it in relation to the overall system is-sues, IEG’s recommendations are focused on the issues to be dealt with in completing the remain-ing phases of the review, and on the broader con-trol framework issues that may emerge going for-ward. In this context, IEG makes six recommendations to Management (including one also to IAD), as follows: • Confirming the Validity of the BPM Cluster:

Management has argued, but has not conclu-sively demonstrated, that the core SIL proto-type module in the cluster of BPMs can be used as a proxy for all investment type lend-ing, because all ILs have the same controls as SILs. This proposition should be tested, and this could be done during Part IB. (para 2.18).

• Reform of the OPs/BPs: IEG considers this topic an area of potential material weakness, whose remedy Management should treat as a priority. IEG notes that Management has a stated strategy to address the problem, both

x

to streamline and to update the OPs/BPs. (para 2.37).

• Completing the Remaining Stages: IEG rec-ommends that preparation for the Part II stage should begin promptly upon comple-tion of Part I. It would seem useful to pre-cede this work with a work plan (which could be discussed with the Board), that could benefit from consultations between Manage-ment, IAD, and IEG, much as the Audit Standards were discussed under Part I. Part II should preferably be completed expeditiously, also because if it should be delayed, the con-trols parameters that were tested during Part I may have changed, and there may be diffi-culties in integrating the two parts of the as-sessment. (para 2.24).

• Resolving Specific Issues and Potential Defi-ciencies (Management and IAD): It is impor-tant that the several deficiencies uncovered by both Management’s assessment and IAD re-view, as listed and described in Annex C, be addressed during completion of Part IB. While some of these issues relate to lack of clarity in documentation, others to efficiency and effec-tiveness of controls, others are potential defi-ciencies in controls. It is the seriousness of the latter group—the materiality of their potential impact on risk mitigation—that must be ad-dressed before conclusions can be drawn on the state of the overall control framework. (paras 2.41,2.44 and 3.3, third bullet).

• Managing the Risk Framework and Extend-ing COSO: IEG believes the Integrated Risk Management Framework will need to be broadened to focus also on compliance and operations reporting, and in this context, the Bank may also consider adopting the recently extended version of COSO which provides for the addition of a new fourth objective (strategy—high level goals, aligning with sup-porting mission) and three new components to the existing five components of COSO: objective setting, event identification and risk response. (para 1.7 and Annex A paras 4-6)

• Mainstreaming Internal Controls Reviews: IDA should begin considering the value of adopting a policy requiring: (1) ongoing monitoring and reporting on internal controls in the course of operations for all three COSO objectives; and (2) separate evalua-tions and reporting as necessary. Attachments to the Executive Summary:

Given the relative complexity of this three-part review and the technical, detailed nature of the is-sues examined and the findings arrived at, IEG has provided tabular summaries of both the ap-proach and method of Management, IAD and IEG respectively (Box 1 and 2 below, extracted from Chapter 1), and of the main findings and po-sitions taken on the key issues (Box 3, extracted from Chapter 4, paragraph 4.6).

xi

Box 1. Key Components in the Management Assessment, IAD Review, and IEG Evaluation (Part I)

Management Assessment IAD Review IEG Evaluation Part IA

Define Approach and Method Business Process Based Fiduciary Focus Partial COSO Other Scope Limitations

Review Assumptions, Criteria, Methodology Criteria for Inclusion/ Exclusion Review process Test Methodology

Establish Framework/Tools The COSO Framework Business Process Template COSO Template Implications of Scope Limitations

Identify BPMs, Key Controls 4 Umbrella Areas 30 BPMs 114 Key Controls

Review Use of BPMs Criteria for Selection Definition of Key Controls Review of Process

Review Use of BPMs Criteria for Selection Definition of Key Controls Review of Process

Verify Mapping, Assessed Design of Key Controls Match Risks with Key Controls Conduct Walkthroughs Assessment of Design Effectiveness

Review of Management Assessment Attend Walkthroughs Review Assessment of Process and Design Effectiveness Apply Deficiency Tracker

Evaluate Individual BPMs Rank for Significance and Risk Provide Quality Ratings for Documentation and Mapping Assessment of Design Effectiveness Attend Selected Walkthroughs

Conclusions for Part IA Qualified Assurance

Conclusions for Part IA Opinion Postponed

Conclusions for Part IA Evaluate Quality of Management and IAD Conclusions Draw IEG Conclusions Implications for Part IB and Part II

Part IB Test Operation of Controls Conduct Audit of Controls Define Sampling Method Conduct Testing

Tabulate Findings Test Results Matrix

Review Testing of Controls Review test Methodology Review Process for Documenting Results Assess Process to Detect Fraud Review Deficiencies, Criteria

Evaluate Quality of Controls Tests Provide Quality Ratings for: Testing of Key Control Compliance Linkage to COSO Framework Conduct Independent Analysis of Management Exceptions data

Form Conclusions Statement of Assurance Make Recommendations

Unqualified Opinion or Modified Report

Overall Evaluation, Recommendations

Notes: BPMs—Business Process Modules

xii

Box 2. Overall Timeline for Completion of IDA 14 Assessment

Part IA Part IB Part II Management Report Aug 06* Dec 06 Sep 07 IAD Report Sept 06* Jan 07 Nov 07 IEG Report Oct 06 March 07 Jan 08 Source: Based on the Management paper to the Audit Committee and current esti-mates. * These reports were actually completed in early October 2006.

Box 3. Summary of Principal Issues Identified by Management, IAD, and IEG

Issues relating to approach and method

Management IAD IEG

A: Framework Issues 1. Bottom-up versus Top-down

Better start Top-down

Better start Top-down

2. Staging and Dividing the Assessment

Postpones Conclusions

Postpones Conclusions

3. Dealing only partially with COSO components

- Postpones Conclusions

4. Scope Limitations IT to be assessed in

Part IB

Optional; IT is part of Entity Level controls

B: Process Level Issues: 1. Definition of Objectives, Compliance

- Acceptable

2. From Articles to Key Policies and Procedures

- Acceptable

3. Linking OPs/BPs Explanations offered

- Only 50% linked to BPMs

4. Identifying BPMs - Acceptable 5. Quality of BPM mapping - Satisfactory,

some qualifications

5. The Cluster as Representing IDA Operations

Issue: Excluded Processes

a. Lending: Test ILs

b. Excluded AAA/KP

Issues relating to results: major controls issues

Highlighted Controls Issues By Management

1. Document Retention and Accessibility

Highlighted Deficiency

Highlighted Deficiency

Potential Material

Weakness Continued

xiii

Box 3 (continued) 2. Current Status of OPs/BPs: a. OPs/BPs outdated, often not current b. Complex, disjointed policy framework c. Onerous, inefficient processes

Highlighted Deficiency

Highlighted Deficiency

Potential Material

Weakness

3. Disparity in Corporate Review SILs and DPLs.

Highlighted -- Highlighted

By IAD (3) 1. Outdated OPs/BPs

Highlighted Highlighted

2. Definition of Walkthrough Disputed Management Consistent with AS2 concepts

3. Fraud and Corruption Controls

Should be assessed at

process level

Start with Entity level

controls; could have been

more explicitly treated

By IEG (4) (i) No control over “subject to” disbursement changes; (ii) no assurance all refunds received; (iii) No mechanism to assure country safeguard documents redone if necessary; (iv) No Bank-wide log for procurement complaints

Highlighted

Issues relating to Results:

Documentation and potential control Deficiencies.

Highlighted Additional

Issues

55

Identified; Materiality

not yet established

Materiality should be

established during Part IB

1

1. Background and Description of Approaches

Origins of the Study 1.1 In the IDA14 Replenishment Report1 Bank Management “has committed to carry out an independent comprehensive assessment of its control framework including internal controls over IDA operations and compliance with its charter and policies” (paragraph 39 of that document). Annex B Table 3 of the document stipulated that this as-sessment should be undertaken by the Independent Evaluation Group (IEG, formerly OED). That document has been approved by the Execu-tive Directors.

1.2 This Review of IDA’s controls was discussed briefly at a Board meeting in May 2005.2 At that time, Management reiterated that—consistent with the practice that is being followed under the Bank’s COSO-based3 control framework—there should first be a self-assessment of the controls system, with a role for IAD, leading up to the IEG evaluation. IEG confirmed that it was prepared to take on the requested evaluation if the Board should so wish. As this was not in the IEG work program, there would need to be a non-fungible addition to the IEG budget for this purpose.

1.3 Management has since confirmed that the Review will be con-ducted in two parts (I and II). Part I will deal with internal controls over IDA’s compliance with its charter and internal policies and pro-cedures; and Part II with internal controls over IDA’s operational ef-fectiveness and efficiency. Each part will have three phases: first a Management assessment of internal controls; second, an IAD review of Management’s assessment; and third, IEG’s independent evalua-tion of both the assessment and the review. Following certain delays that Management encountered in completing the first part (on com-pliance), it decided further to divide this part into two stages (Part IA and Part IB), as described in Box 4.

1.4 The present report covers only that portion of the study to be completed under Part IA. It therefore deals with the assessment of in-ternal controls over compliance, to the stage of examining the identifi-cation and mapping of business processes, and the assessment of the

Evaluation Essentials This report focuses on

compliance controls and the design effectiveness of controls within business processes

Previous evaluations have found that internal controls need improvement to support changing processes and new initiatives

IEG evaluates the assessment by Bank management and the review by Internal Audit Department within COSO and uses agreed audit standards

IDA 14 committed to a review of internal controls

CHAPTER 1 BACKGROUND AND DESCRIPTION OF APPROACHES

2

design effectiveness of key controls within these processes. It will be a prelude to the assessment of the operating effectiveness of these con-trols, which is to be completed during the next stage (Part IB). Part II will then follow.

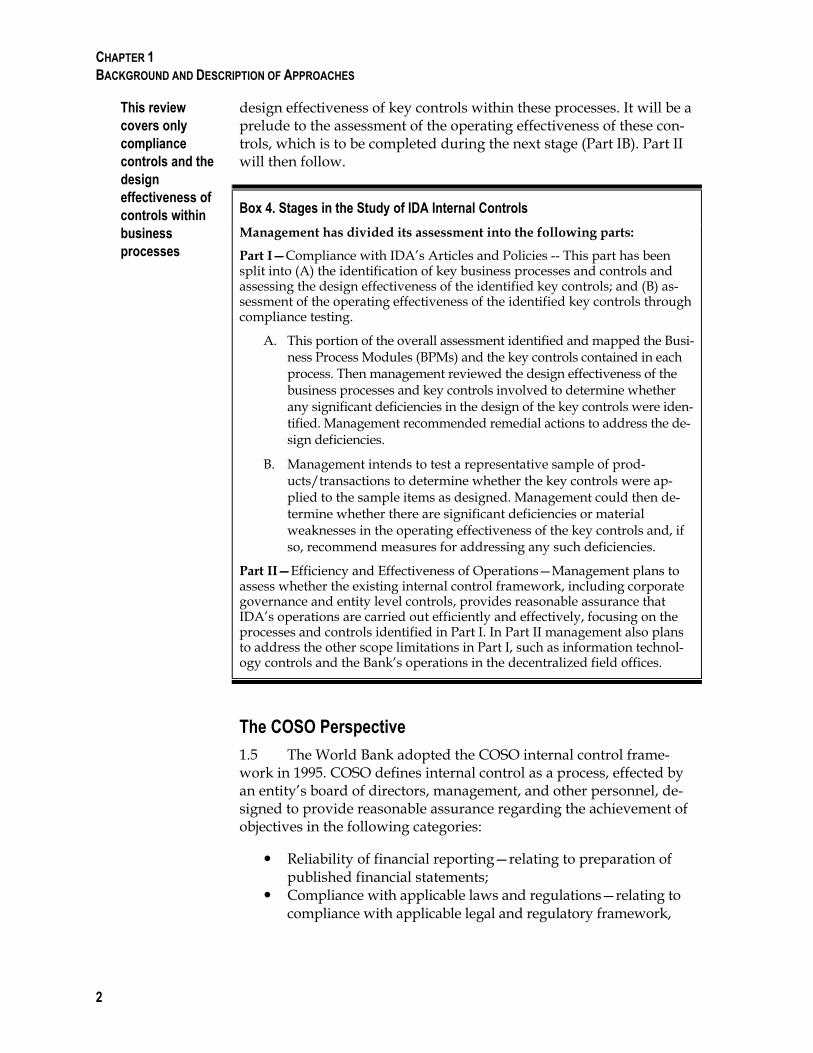

Box 4. Stages in the Study of IDA Internal Controls Management has divided its assessment into the following parts:

Part I—Compliance with IDA’s Articles and Policies -- This part has been split into (A) the identification of key business processes and controls and assessing the design effectiveness of the identified key controls; and (B) as-sessment of the operating effectiveness of the identified key controls through compliance testing.

A. This portion of the overall assessment identified and mapped the Busi-ness Process Modules (BPMs) and the key controls contained in each process. Then management reviewed the design effectiveness of the business processes and key controls involved to determine whether any significant deficiencies in the design of the key controls were iden-tified. Management recommended remedial actions to address the de-sign deficiencies.

B. Management intends to test a representative sample of prod-ucts/transactions to determine whether the key controls were ap-plied to the sample items as designed. Management could then de-termine whether there are significant deficiencies or material weaknesses in the operating effectiveness of the key controls and, if so, recommend measures for addressing any such deficiencies.

Part II—Efficiency and Effectiveness of Operations—Management plans to assess whether the existing internal control framework, including corporate governance and entity level controls, provides reasonable assurance that IDA’s operations are carried out efficiently and effectively, focusing on the processes and controls identified in Part I. In Part II management also plans to address the other scope limitations in Part I, such as information technol-ogy controls and the Bank’s operations in the decentralized field offices.

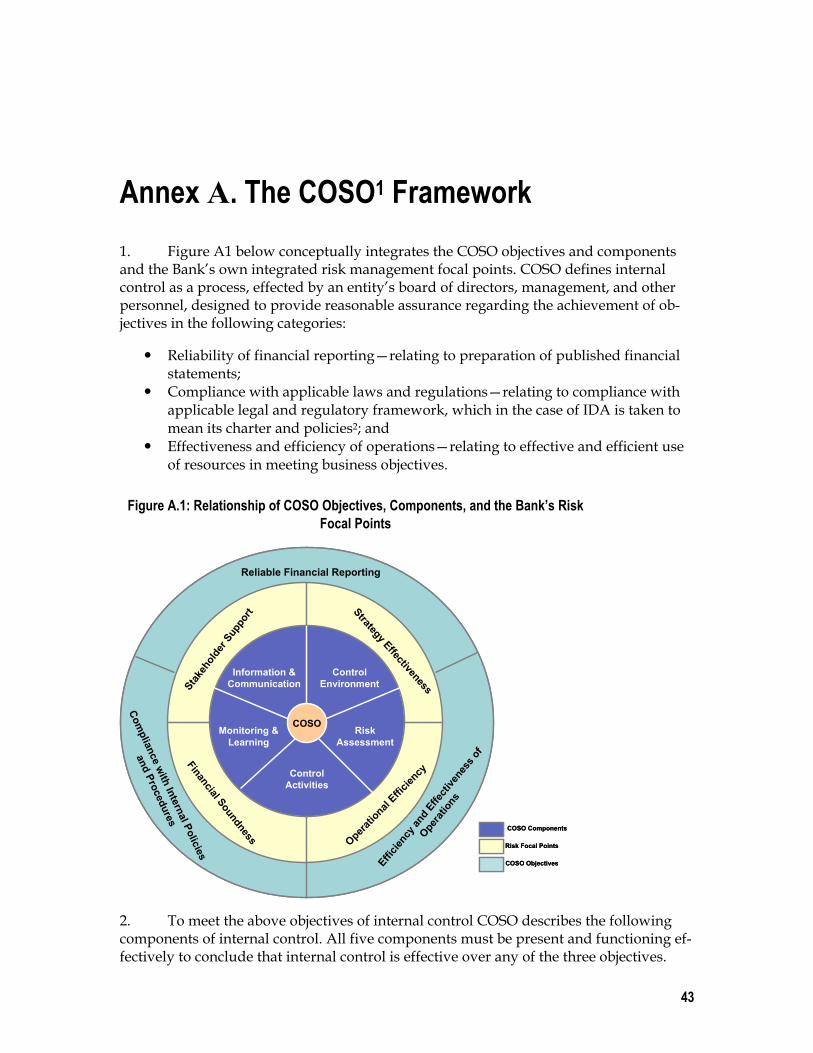

The COSO Perspective 1.5 The World Bank adopted the COSO internal control frame-work in 1995. COSO defines internal control as a process, effected by an entity’s board of directors, management, and other personnel, de-signed to provide reasonable assurance regarding the achievement of objectives in the following categories:

Reliability of financial reporting—relating to preparation of published financial statements;

Compliance with applicable laws and regulations—relating to compliance with applicable legal and regulatory framework,

This review covers only compliance controls and the design effectiveness of controls within business processes

CHAPTER 1 BACKGROUND AND DESCRIPTION OF APPROACHES

3

which in the case of IDA is taken to mean its charter and poli-cies; and

Effectiveness and efficiency of operations—relating to effective and efficient use of resources in meeting business objectives.

Figure 1. The COSO Framework: Components, Objectives, and Risk Factors4

Information & Communication

Monitoring & Learning

Control Activities

Risk Assessment

Control Environment

Fina

ncial

Rep

ortin

g

Opera

tions

Compli

ance

Strategy EffectivenessO

perational EfficiencyFinancial Soundness

Stakeholder SupportCOSO Components

Bank’s Risk Focal Points

COSO Objectives

Information & Communication

Monitoring & Learning

Control Activities

Risk Assessment

Control Environment

Fina

ncial

Rep

ortin

g

Opera

tions

Compli

ance

Strategy EffectivenessO

perational EfficiencyFinancial Soundness

Stakeholder SupportCOSO Components

Bank’s Risk Focal Points

COSO Objectives

1.6 To meet the three objectives, the COSO framework has five in-terrelated components that define the minimum level of quality accept-able for internal control and provide the basis against which internal control is to be evaluated. These internal control components, which apply to all aspects of an organization’s operations, include the control environment, risk assessment, control activities, monitoring and learn-ing, and information and communication. All five components must be present and effective in order for management to have reasonable as-surance that risks are managed to ensure the achievement of the or-ganization’s objectives. Management is responsible for developing the detailed policies, procedures, and practices to fit the organization’s op-erations and to ensure that they are built into and are an integral part of its operations, by conducting ongoing monitoring and, as needed, separate evaluations of internal controls.

1.7 A direct relationship exists between the three categories of ob-jectives—what the entity is striving to achieve—and components—the management dimensions the entity needs to achieve the objectives. These are depicted graphically in Figure 1, and are more fully de-scribed in Annex A. COSO is a dynamic framework which is being adapted continuously to changes in the global situation. Recent em-phasis in adapting COSO has been focused on better management of risk, and in 2004 COSO itself added a new strategic objective to the ex-

Internal controls focus on financial reporting, compliance with laws and regulations, and effectiveness and efficiency of operations

The COSO framework has recently emphasized risk management

CHAPTER 1 BACKGROUND AND DESCRIPTION OF APPROACHES

4

isting three objectives (financial reporting, operations and compli-ance) and three new components to the existing five shown in the fig-ure above: objective setting; event identification; and risk response. This expanded framework has not yet been adopted by the Bank.

1.8 Given that the Bank has, for a number of years, assessed the internal controls over its financial reporting, and has had the external auditor attest to the quality of the assessment, the present review5 does not deal with financial reporting, but focuses on the remaining two COSO objectives, namely compliance and operations.

Integrating the COSO Framework into Bank Operations 1.9 The Bank’s Management has, since 1997, written internal, an-nual year-end reports on the status of the adaptation to COSO. IEG’s Annual Report on Operations Evaluation (AROE) 6 reports for 2000-2001 and 2002 addressed development effectiveness issues from the perspective of the COSO framework.7 The 2002 report noted the pro-found changes that had taken place in the Bank’s control environ-ment: new controls structures had been put in place and “a new cul-ture has taken root with respect to risk management,” but risk aversion appeared to have become a feature, and the report foresaw a need for what later became the Bank’s integrated risk management framework (IRMF). Under Control Activities, it saw the need for an accelerated conversion and updating of the Bank’s policies and pro-cedures, and under Monitoring it called for improved methods of evaluating Economic and Sector Work (ESW), grants and partner-ships. In the Information and Communication component it reported the major progress transforming the Bank as a Knowledge Bank, which had enabled rapid transfer of information on guidelines and best practice, and reported on the roles to be played by Development Economics Department and the World Bank Institute.

1.10 These themes are a relevant prelude to the present controls re-view. Being focused on development effectiveness, they preface the overall COSO-based approach that IEG is taking in the review, and the 2002 AROE stated the need for further developing the control en-vironment quite clearly: “… the drive to become a Knowledge Bank has engendered new initiatives and new processes, for which both the control environment and the evaluation framework have yet to be well defined.”8

IEG’s Approach to its Evaluation 1.11 IEG Objective: The objectives of the IEG evaluation for this Part IA Report must be viewed in light of the objectives of the overall review. IEG’s role in the overall review is to provide an independent

IEG previously has found a need for improved definition of the controls framework to keep pace with changing processes and new initiatives

CHAPTER 1 BACKGROUND AND DESCRIPTION OF APPROACHES

5

evaluation to determine whether Management and IAD have pro-vided a reasonable basis for judging whether internal controls over IDA compliance and operations are in place and working; whether any material weaknesses and other deficiencies have been identified; and, as necessary, whether internal control corrective action plans are being implemented. Within that context, and for the purposes of pro-ducing a report on the status of work completed during Part IA of the review, IEG has aimed to:

evaluate implications of scope limitations and management’s phased approach;

evaluate management’s method for and completion of the mapping of business processes;

evaluate Management’s assessment of control design; and evaluate IAD’s approach to its work and its conclusions.

1.12 IEG Scope: IEG’s overall evaluation of both the management assessment and the IAD review offers an independent conclusion to the Board as to the degree of assurance with which the assessment and opinion presented respectively in the final reports by Management and IAD can be taken to be fairly stated, in terms of their giving reasonable assurance (or other conclusion) that IDA’s controls over compliance with its charter and relevant policies and procedures are effective.

1.13 IEG took the COSO framework and the audit standards con-sistent with that framework as the starting point for its evaluation. It assumed that the judgments regarding the effectiveness of the inter-nal IDA controls over compliance and operations had to be made against criteria contained in the COSO framework as a whole. At the same time, IEG recognized that management took an approach in Part I that has certain scope limitations. These limitations will have a bear-ing on the quality of assertions that can be made at this stage to the management and Board of IDA.

1.14 IEG notes that the key scope limitations in Part I are: the post-ponement to Part II of issues relating to entity-level controls; consid-eration of only two out of the five COSO components;10 the treatment of compliance only, and not efficiency and effectiveness of operations; and the postponement to Part II of the treatment of decentralized lo-cations and IT systems. As described in Chapter 2 and summarized in Chapter 4, IEG has evaluated the implications of these postponements in making its judgments on the overall quality of the management as-sessment and on the conclusions that can be made at this stage of the exercise.

The scope of this review is based on COSO as a whole

CHAPTER 1 BACKGROUND AND DESCRIPTION OF APPROACHES

6

1.15 Audit Standards: Management had stated in its preparatory working papers that it intended to use audit standards similar to those used for its financial reporting (namely the general concepts of AS2 standard developed under the Sarbanes-Oxley legislation11), since these would provide due rigor and standardization. IEG be-lieved that this raised the question of whether it was indeed appro-priate to use the same standards for compliance and operations re-porting as for financial reporting, because the nature of the issues would be different. IEG therefore conducted significant research into this question. It was concluded that similar standards could be used, but that for compliance and operations reporting, assessing the mate-riality of deficiencies required more judgmental decision than for fi-nancial reporting. After consultations with both Management and IAD, agreement was reached both on the fact that all three parties would use the same standards, and on the precise definition for each. A description of the latter is given in Annex B.

1.16 IEG Evaluation Method: IEG has applied four principal meth-ods in making its evaluation:

It critically reviewed the available reports from management and IAD.

It conducted an independent analysis of the raw data gener-ated by Management’s assessment. This analysis addressed the quality and effectiveness of design of the underlying inter-nal controls.

IEG assembled evaluation panels for the purpose of rating each step in the assessment and review processes. The panels used an evaluation tool designed by IEG for this purpose, called a Business Process Template, which contained a series of standard questions on Management’s method of mapping and assessment of design of each business process module. This generated a data stream on the quality of Management’s method and approach to mapping and controls assessment.

IEG has reserved the option to conduct its own tests of the de-sign effectiveness of selected key controls, as a means of ob-taining verification independent from the results obtained by Management.12 This was found to be not necessary during Part IA. However, IEG did interview staff in selected units,13 in-cluding some that are involved in entity level controls, to gain a better understanding of the overall processes and controls that affect the business process modules included in Manage-ment’s assessment.

1.17 Advisory Panel: As is now normal for many of IEG’s major evaluations, a senior Advisory Panel will be invited to review and com-ment on the IEG evaluation report and will be requested to share its comments also with CODE and the Audit Committee (AC). The mem-

Management and IEG agreed on common audit standards

The IEG method used critical evaluation, independent analysis, and quality ratings developed by panels

CHAPTER 1 BACKGROUND AND DESCRIPTION OF APPROACHES

7

bers of the panel for this evaluation are former Auditors-General, from India, Norway, and Australia, respectively. However, the services of the Panel will be invoked only when IEG has completed its draft evaluation report on Part IB.

Summary of Approaches: Management Assessment and the IAD Review 1.18 A description of the approach taken by Management to its as-sessment, and the key findings arrived at, is contained in Chapter 2, and a copy of the Management report is in Attachment 1. A description is given in Chapter 3 for the method, approach and findings of the IAD review, and a copy of the IAD report is appended at Attachment 2. Box 5 and Box 6 summarize the three approaches and the current timetable.

Box 5. Key Components in the Management Assessment, IAD Review, and IEG Evaluation (Part I)

Management Assessment IAD Review IEG Evaluation Part IA

Define Approach and Method Business Process Based Fiduciary Focus Partial COSO Other Scope Limitations

Review Assumptions, Criteria, Methodology Criteria for Inclusion/ Exclusion Review process Test Methodology

Establish Framework/Tools The COSO Framework Business Process Template COSO Template Implications of Scope Limitations

Identify BPMs, Key Controls 4 Umbrella Areas 30 BPMs 114 Key Controls

Review Use of BPMs Criteria for Selection Definition of Key Controls Review of Process

Review Use of BPMs Criteria for Selection Definition of Key Controls Review of Process

Verify Mapping, Assessed Design of Key Controls Match Risks with Key Controls Conduct Walkthroughs Assessment of Design Effectiveness

Review of Management Assessment Attend Walkthroughs Review Assessment of Process and Design Effectiveness Apply Deficiency Tracker

Evaluate Individual BPMs Rank for Significance and Risk Provide Quality Ratings for Documentation and Mapping Assessment of Design Effectiveness Attend Selected Walkthroughs

Conclusions for Part IA Qualified Assurance

Conclusions for Part IA Opinion Postponed

Conclusions for Part IA Evaluate Quality of Management and IAD Conclusions Draw IEG Conclusions Implications for Part IB and Part II

Continued

CHAPTER 1 BACKGROUND AND DESCRIPTION OF APPROACHES

8

Box 5 (continued) Part IB

Test Operation of Controls Conduct Audit of Controls Define Sampling Method Conduct Testing

Tabulate Findings Test Results Matrix

Review Testing of Controls Review test Methodology Review Process for Documenting Results Assess Process to Detect Fraud Review Deficiencies, Criteria

Evaluate Quality of Controls Tests Provide Quality Ratings for: Testing of Key Control Compliance Linkage to COSO Framework Conduct Independent Analysis of Management Exceptions data

Form Conclusions Statement of Assurance Make Recommendations

Unqualified Opinion or Modified Report

Overall Evaluation, Recommendations

Notes: BPMs—Business Process Modules

Box 6. Overall Timeline for Completion of IDA 14 Assessment

Part IA Part IB Part II Management Report Aug 06* Dec 06 Sep 07 IAD Report Sept 06* Jan 07 Nov 07 IEG Report Oct 06 March 07 Jan 08 Source: Based on the Management paper to the Audit Committee and current esti-mates. * These reports were actually completed in early October 2006.

1. See “Report from the Executive Directors of the International Development Association to the Board of Governors, Additions to the IDA Resources: Fourteenth Replenishment, Working Together to Achieve the Millennium Development Goals” (approved by the Executive Directors of IDA on March 10, 2005).

2. The May 12 2005 discussion of IEG-WB’s FY06-08 work program and FY06 budget.

3. Committee of Sponsoring Organizations of the Treadway Commission, which published a report in 1992: Internal Control—Integrated Framework.

4. This representation of the COSO framework is what is currently in use in the Bank and IDA, showing also the Risk Focal Points, which have been added to the framework, following adoption by the Bank of the Integrated Risk Management Framework (IRMF) in 2002. For a fuller explanation, see Annex A.

5. IEG has verified that in recent years (2002-2005) the Bank published the management assessment report and the auditor’s attestation report in the An-nual Report, Volume 2, Financial Statements. This includes a transmittal letter, management’s discussion and analysis (covering just IBRD), IBRD financial

NOTES

CHAPTER 1 BACKGROUND AND DESCRIPTION OF APPROACHES

9

statements and internal control reports, and IDA financial statements and in-ternal control reports.

6. Annual Report on Operations Evaluation (formerly OED, now IEG).

7. The AROEs for 2003 and 2004 also covered specific individual topics within the framework, namely monitoring and evaluation.

8. AROE 2002, page 31.

9. In management’s approach the focus was mainly on Risk Assessment (at the unit level) and Control Activities, and there was no direct focus on the other three components (Control Environment, Monitoring and Learning, and Information and Communications), which are postponed until Part II.

10. Auditing Standard No. 2 (AS2) An Audit of Internal Control over Finan-cial Reporting Performed in Conjunction with An Audit of Financial State-ments, was issued by the U.S. Public Company Accounting Oversight Board (PCAOB) to respond to the provisions of Section 404 of the Sarbanes-Oxley legislation as much as possible.

11. As set down in the Approach Paper, IEG might consider commissioning its own testing, if and when: (i) A general random selected testing of controls seems warranted; (ii) Certain controls were found not to have been tested; and (iii) Testing that was done may be deemed inadequate, for example be-cause of sampling deficiencies or other flaws in approach.

12. To discuss entity-level control issues, the IEG team had separate meetings with Bank units dealing with: IDA allocation (FRM); the Integrated Risk Management Framework (SFRSI); issues of fraud and corruption detection (INT); quality assurance (QAG); and safeguards (QACU).

11

2. Management’s Assessment 2.1 This chapter divides into two parts: the first part (paras 2.2-2.11) gives a descriptive synopsis of Management’s approach and method; the second part (from para 2.12) contains IEG’s evaluation of the assessment. Management’s report is in Attachment 1.

Background and Objective 2.2 Management intended to conduct the review of IDA internal controls within the context of the COSO framework, but would focus in this phase of the study only on the assessment of internal controls over compliance. The report states that the COSO framework includes both “top-down” and “bottom-up” analysis. Management determined that Part I of the study would be “more valuable if carried out follow-ing a bottom-up approach,” in order to best track directly the use of IDA resources. Accordingly, the report describes how Management has identified, described and mapped a collection of the key business processes that it used to represent the principal operations activities of IDA, which will be used both to assess compliance in Part I, and to lay a “solid foundation” for the examination of institutional efficiency and effectiveness to be undertaken in Part II. 1

2.3 Management’s objective was to provide an assessment of whether the internal control framework over IDA’s operations pro-vides reasonable assurance to Senior Management and the Board that such operations are carried out in a manner that complies with the provisions of the IDA charter and internal policies governing IDA’s operations, including the mechanisms in place to ensure that funds are disbursed for the intended purposes.

Management’s Method: From the IDA Charter to Policies to Business Processes 2.4 Defining “Compliance” for IDA: Management chose to re-define the meaning of “compliance” in IDA’s case.2 Under COSO, compliance generally implies compliance with local laws and regula-tions. In IDA’s case, as “an international organization established by international treaty with privileges and immunities” Management suggested instead that compliance should be measured against the

Evaluation Essentials The Management

assessment subdivides the compliance controls using business processes

The model requires that controls both be well designed and operate as designed to be effective

IEG finds the method logical, transparent, and convincing and the quality of its results satisfactory

However, it does not capture non-lending activities and may rely on dated OPs and BPs,

The Management assessment identifies several important deficiencies

The bottom-up approach complicates the assessment; affirmative conclusions have to be postponed

The Management assessment aimed to determine whether internal controls, under COSO, provide reasonable assurance that business processes comply with IDA’s charter and policies

CHAPTER 2 MANAGEMENT’S ASSESSMENT

12

relevant provisions of the charter (IDA Articles) and against IDA’s in-ternal policies and procedures.

2.5 Accordingly, Management states in its report that “any com-pliance assessment of internal controls over IDA’s operations must therefore go through a four-step process:

1. identifying key provisions of the IDA Articles that govern IDA’s operations;

2. identifying main policies that were adopted by IDA to ensure that IDA’s operations are carried out consistently with these provisions;

3. identifying the manner in which these policies are intended to be carried out by cataloguing the business processes and key controls put in place to ensure compliance with the identified policies and assessing the “design effectiveness” of these proc-esses and key controls; and

4. assessing compliance with the business process and key con-trols by testing a sample of transactions.” (The subject of Part IB).

2.6 Key Policies and Instruments: Based on this concept of com-pliance, Management sought to establish clear links between the IDA Articles, related policies and procedures, and the actual business processes whose internal controls would be the subject of assessment and testing. The specific hierarchy of these steps is given in summary form in Box 7. It shows how the provisions of the Articles link to spe-cific policies and procedures and the related operational instruments. It shows that the approach stemmed from eight specific provisions of Article V of the IDA Articles, covering allocation and use of IDA re-sources. From over 100 published policies and procedures, Manage-ment made a selection of those that related to the allocation of IDA re-sources and the three key instruments governing IDA operations—country assistance strategies, and the two main forms of lending—Specific Investment Loans (SILs) and Development Policy Loans (DPLs)—citing the four “umbrella” statements in these “flagship” policies and procedures. Having identified these primary operational instruments, Management then also addressed the need to take ac-count of the fiduciary, contractual and safeguards aspects of IDA lending, adding the relevant policy provisions in each of these areas.

Compliance was redefined

IDA Articles were linked to specific policies, procedures, and operational instruments

CHAPTER 2 MANAGEMENT’S ASSESSMENT

13

Box 7. Building Blocks in Management’s Approach

IDA Articles Article V—Operations

• Concessional Resources to Less Developed Areas

• Financing High Priority Devel-opment

• Specific Projects and Special Cir-cumstances Lending

• Lender of Last Resort

• Use of Funds for Purposes In-tended

• Due Regard for Economy and Efficiency

• Non-political interference • Linking Disbursements to Ex-

penditures incurred

Policies and Procedures From >100 OPs and BPs Management Focused on

Three Primary Instruments: Country Assistance Strategy(CAS)

Investment Lending Operations (IL) Development Policy Lending (DPL)

“Flagship” OPs and BPs The Flagships Contain four “Umbrella Statements,” namely:

• Umbrella Statement governing financial terms of and eligibility for IDA financ-ing

• Umbrella Statement governing Country Assistance Strategies • Umbrella Statements governing Investment Lending • Umbrella Statement governing Development Policy Lending

Specific Policies for Fiduciary, Contractual and Safeguards Aspects All lending instruments are accompanied by supporting policies and proce-

dures covering:

• Financial management of projects • Disbursement aspects • Procurement aspects • Contractual/Legal and Loan Administration aspects • Safeguard aspects • Quality Assurance

30 Business Process Modules Source: Management Report

2.7 The Business Process Modules (BPMs): Based on this hierar-chy of policies and procedures, Management identified 30 Business Process Modules (BPMs)3 which it saw as representing “the relevant business processes currently in place which staff are expected to use as guidance and best practice when working on IDA operations.” The modules covered the “umbrella” business functions, (allocation, CAS and lending instruments) plus the supporting fiduciary and other as-pects and quality assurance. The material for each BPM included de-scriptions, process flow maps, and specifically defined and located

Thirty Business Process Modules, and their key controls, were identified as representing IDA operations

CHAPTER 2 MANAGEMENT’S ASSESSMENT

14

key controls. It is these controls whose design and operating effec-tiveness are the central subject matter of the review. A listing of the BPMs, broadly organized by business function, is given in Box 8.

Box 8. Management’s List of 30 Business Process Modules (Listed by Business Function*)

“UMBRELLA” PROCESSES (8 Modules)

FRM IDA Allocation (IDA Allocation Model) (Post-Conflict Allocation) Debt Sustainability Analysis CAS Products SIL Project Cycle DPL Project Cycle Corporate Review (ROC/OC)

QUALITY ASSURANCE (1 Module)

QAG Processes QEA QSA

FIDUCIARY PROCESSES (21 Modules)

LEGAL SIL Legal Regime DPL Legal Regime Project Changes Contractual Remedies

FINANCIAL MANAGEMENT SIL DPL

PROCUREMENT SIL Procurement Regime Procurement Complaints Procurement Non-Compliance

LOAN ADMINISTRATION Loan Administration SIL Loan Administration DPL Loan Application Review Special Commitment Amendment or Extension Refund Process Loan Cancellation Process Loan Suspension Process Loan Closing (Standard) Loan Closing (Special Procedure)

SAFEGUARDS Safeguards SIL Safeguards Corporate Risk (QACU)

Source: Management listing, organized across business function by IEG.

2.8 Management also explicitly excluded a number of business process modules (10 in total) either because they were deemed not to have direct bearing on lending, or for other reasons, as shown in Box 9. More details on these exclusions are given in Annex E.

Some processes were excluded

CHAPTER 2 MANAGEMENT’S ASSESSMENT

15

Box 9. Business Process Modules Excluded from Compliance Assessment Exclusion By Management’s Reso-lution That the Process Does Not Have Critical Bearing on Current Assessment Objective

Exclusion Based on Determination of No Input to IDA Operations

• Country Policy and Institutional Assessment (CPIA)

• Procurement DPL(Procurement is minor in DPLs)

• Post-Conflict Performance Indi-cators (PCPI)

• IEG Process

• Project Preparation Facility (PPF) • IAD Process

• Loan Management—PPF Refi-nancing

• AAA Products

• Annual Report on Portfolio Per-formance (ARPP)

• Inspection Panel Source: Management Methodology Note (working level paper)

2.9 Management has provided a graphic depiction of the full scope of its assessment, show in Figure 2. It depicts the project cycle for SILs and DPLs as the central element, which is linked to the CAS process, to IDA allocation, and to the associated fiduciary, legal, safe-guards and quality assurance processes. These are the essential proc-esses which Management has captured in the 30 BPMs described above, and which Management has taken to represent the totality of IDA operations.

2.10 The Concept of “Design Effectiveness”: While Management has identified the business processes as the vehicles which deliver the various IDA business objectives, it also makes clear that the key con-trols within them (114 in all) are critical to the review of internal con-trols and the forthcoming testing for compliance. As stated in the standards, Management has distinguished between control design and a control operation. To be fully effective, a control must not only be well designed, it must also operate as designed, i.e staff must respect its provisions in the execution of transactions. In Part IA Management has assessed the design effectiveness of these 114 controls under the following definition:

“whether the system of such internal controls is both comprehensive as well as suitably designed to prevent or detect on a timely basis, mate-rial issues of non-compliance or significant control deficiencies.” 4

The model requires that controls both be well designed and operate as designed to be effective

Figu

re 2.

Ove

rview

Sco

pe M

ap o

f Man

agem

ent’s

Ass

essm

ent

Sour

ce: M

anag

emen

t wor

king

mat

eria

ls

CHAPTER 2 MANAGEMENT’S ASSESSMENT

17

2.11 Management explained in its report that its working teams conducted their assessment of the design effectiveness of these con-trols through a combination of observation, examination of documen-tary evidence and verification of control design. The output from this process was a series of fully mapped BPMs and accompanying de-scriptive documentation, namely: for each business process module, a Process Overview (PO); and for each key control, a Control Detail Sheet (CDS). An example of a process flow chart—i.e. the graphic mapping of the flow of a transaction through the management sys-tem—together with descriptive materials showing the content of a sample Process Overview and a typical Control Detail Sheet, are also shown in Annex D.

IEG’s Evaluation of Management’s Approach and Method 2.12 The foregoing comprises IEG’s synopsis of Management’s ap-proach. The remainder of Chapter 2 contains IEG’s evaluation of Management’s approach (paragraphs 2.14 -2.26) and of Manage-ment’s main findings (paragraphs 2.27-2.45).

2.13 Management made a number of key choices related to its ap-proach and method, the most important of which are summarized be-low and accompanied by IEG’s findings and conclusions. In particu-lar, choices on basic approach and other scope limitations significantly limit conclusions about the adequacy of internal controls that can be drawn at this stage of management’s work.

2.14 Objectives of the Compliance Assessment: IEG finds the objec-tive of the assessment as stated in para 2.3 above to be reasonably stated, appropriate, clear and complete.

2.15 The Definition of Compliance: IEG agrees that an adaptation of the definition of compliance was necessary in IDA’s case, and finds reasonable Management’s rationale and decision to use compliance with the IDA charter, internal policies and procedures. IEG examined the legal theory underlying this issue and found that very generalized reference to “laws and regulations” does not in the case of a special institution such as IDA provide any guidance as to which laws and regulations are determinate and may give rise to ambiguity as to the role of local law. In the circumstances, it was preferable to refer spe-cifically to the Articles, the lending (or financial) agreements includ-ing the General Conditions, and IDA Policies and Procedures, as con-stituting the governing “laws and regulations” for IDA transactions.1

2.16 From the IDA Articles to Policies to BPMs: Management also correctly located the benchmark for the compliance elements as being the appropriate provisions of the IDA Articles, and the relevant Bank Operational Policies and Bank Procedures (OPs and BPs). Both spe-

The objectives are reasonable, appropriate, clear, and complete

The redefinition of compliance was justified

CHAPTER 2 MANAGEMENT’S ASSESSMENT

18

cific Article provisions and the published OPs/BPs were used as the basis to decide which operational instruments and business processes would best represent the panoply of IDA operations. IEG does find the method of developing the 30 business process modules to be logi-cal, transparent, and generally convincing. However, IEG does have comments regarding the possible lack of completeness of the universe of BPMs, as discussed in paragraph 2.18 below.

2.17 Are the Bank’s OPs and BPs an Apt Expression of the Bank’s Policies and Procedures? IEG finds that in each business process module, each control has been linked to one or more specific OPs/BPs, and/or risk statement from the IRMF. However, there are two issues that have been identified regarding OPs/BPs:

The fact that the reform of OP/BP has seriously lagged the pace of change in the Bank Group is acknowledged by Man-agement, and is widely known already;

What was uncovered by IEG during its evaluation, is that there appear to be a significant number of OPs/BPs—some 50%—which were not directly linked by Management to any key controls or business processes. Management has given a satisfactory explanation for those OPs/BPs not linked to spe-cific BPMs, to the effect that: (1) they relate to trust funds and grants, not financed by IDA resources; (2) they apply to other lending products, not SILs; (3) they govern guarantees, which are a very small portion of the IDA portfolio; (4) they govern topics that feed into the processes that were mapped (e.g. eco-nomic evaluation of investment operations; co-financing); or (5) they relate to contractual or other issues that are addressed in the processes that were mapped.

2.18 Does the Cluster of BPMs Adequately Represent the Universe of IDA Operations?2 IEG conducted an analysis of the cluster against some key criteria: What portion of IDA’s operating budget did the clus-ter account for? What product lines? Where processes were excluded from the cluster, did this create gaps in measuring compliance? The content of this analysis is shown in Annex E. IEG concludes that the cluster is broadly representative of IDA’s lending operations (which covers 78% of IDA’s overall operational expenditure). However, by us-ing only SILs to represent all investment lending, Management needs to verify its claim that all other investment loan products have the same controls as SILs (see Annex E paragraph 6). Also, the cluster is essen-tially lending and fiduciary in focus, suggesting that IDA operations are simply IDA lending operations. The cluster omits all Knowledge Products, specifically Analytical and Advisory Activities (AAA), all of which have direct relevance to compliance. As argued in Annex E, AAA has a direct bearing on the quality of IDA lending, as well as ac-counting for about 22% of the IDA budget (almost the same as lending

The method used to develop the business process modules was logical, transparent, and convincing

OPs and BPs may not accurately reflect Bank policies and procedures

The business process modules broadly represent IDA’s lending operations, but not its non-lending activities, and it is not clear that all investment lending uses the same controls as SILs

CHAPTER 2 MANAGEMENT’S ASSESSMENT

19

preparation—24%). This is therefore a significant gap in coverage. Management will not be in a position to report on whether internal controls are achieving the business objectives involved until these addi-tional IDA functions and activities are assessed.

2.19 The Quality of Management’s methods in BPM Mapping and Assessing design Effectiveness: IEG conducted a systematic quality evaluation of the methods used in Management’s mapping of the BPMs and assessment of control design. This involved assembling evaluation panels, consisting of 3-4 specialist consultants, who used an evaluation tool created by IEG (the Business Process Template) to give quality ratings to the process of mapping and assessing each of the business process modules. The questions in the Template tested (i) Management’s method for completeness and accuracy of BPM map-ping, and (ii) clarity in Management’s assessment of the effectiveness of their controls design. Details of the content of the Template and rat-ing system are provided in Annex F. Ratings ranged from Highly Sat-isfactory (1), to Satisfactory (2), Satisfactory with Qualification (3) and Less than Satisfactory (4). The evidence on which the ratings were based came from Management’s process maps, the accompanying de-scriptive materials, other working materials Management made avail-able, and the “walkthroughs” i.e. verification interviews between Management and operations staff, many of which IEG panel members attended as observers.