important notice - bihindustries.bih.nic.in/acts/ad-01-24-10-2007.pdf · sugar undertakings...

TRANSCRIPT

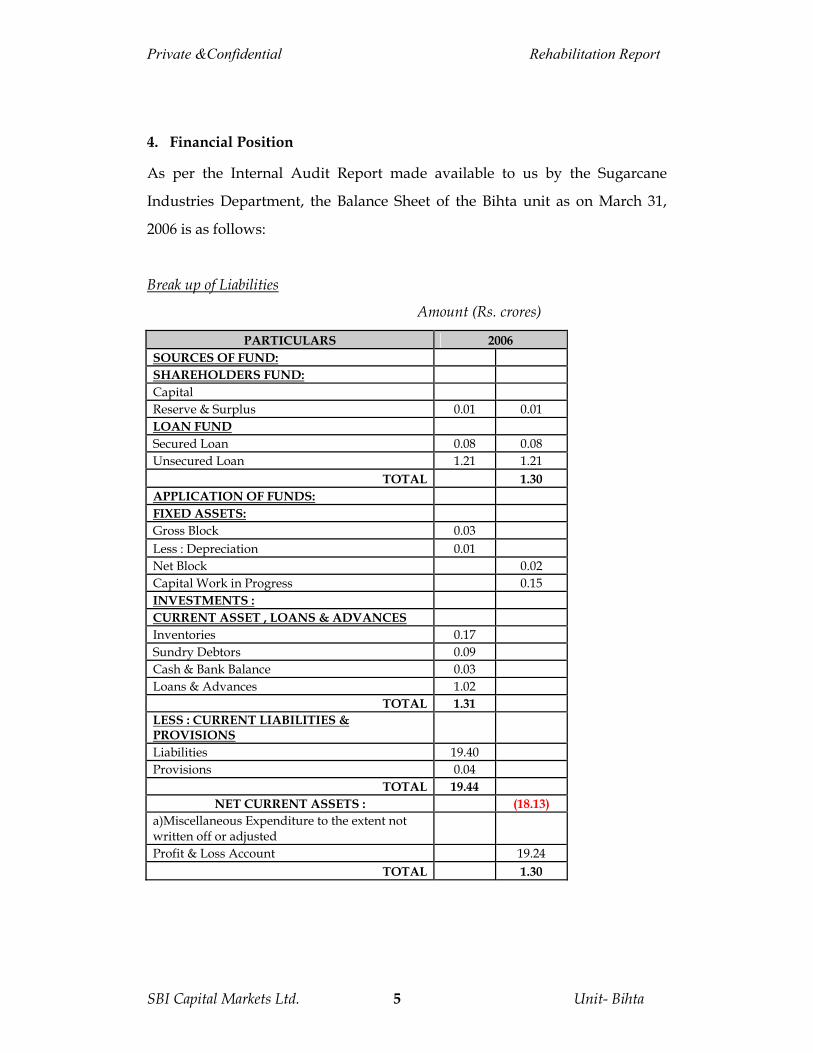

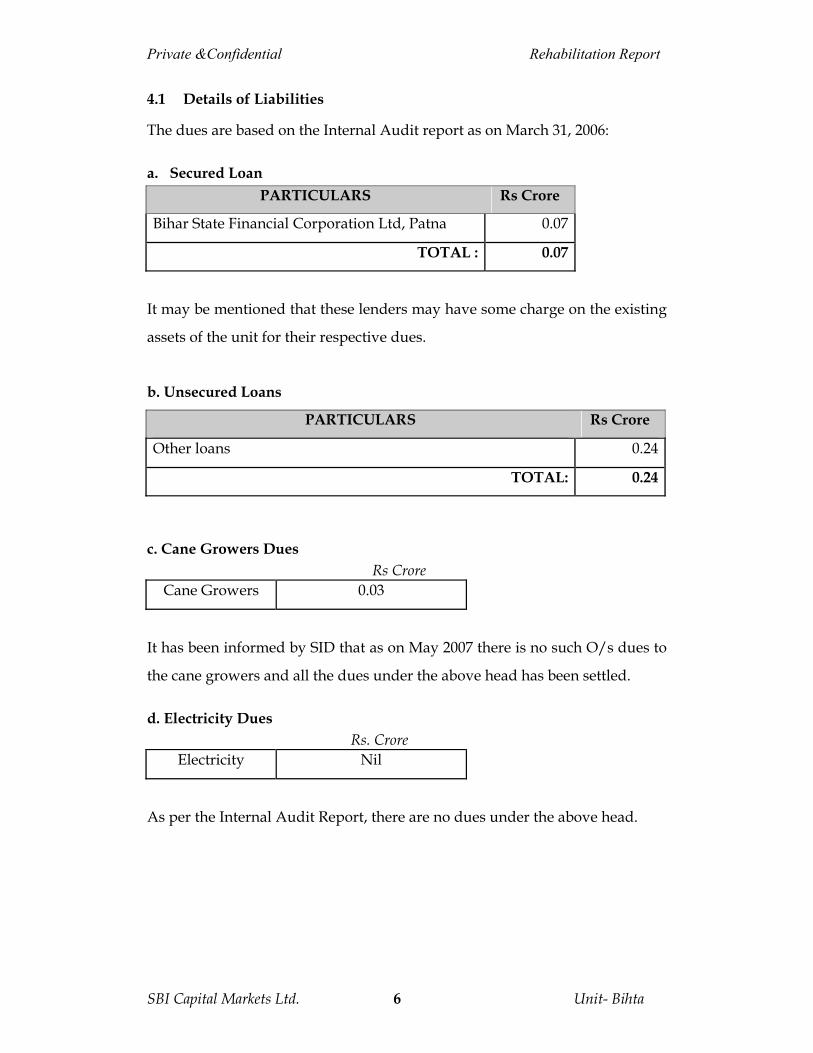

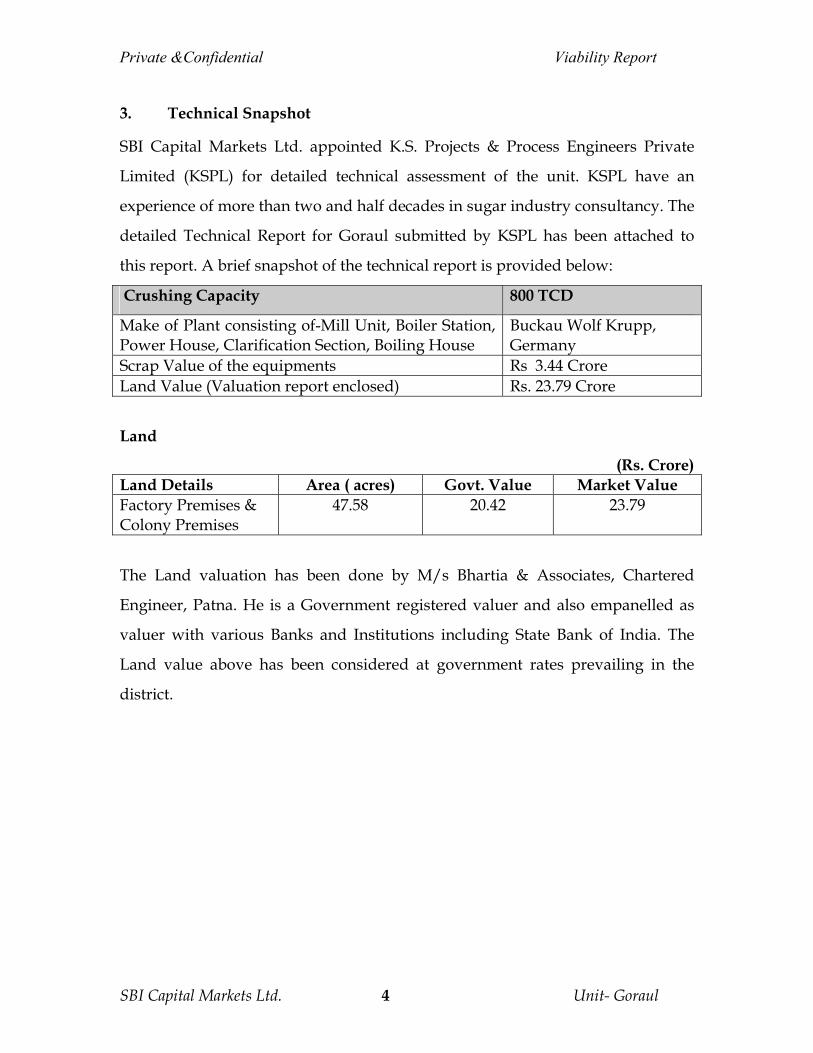

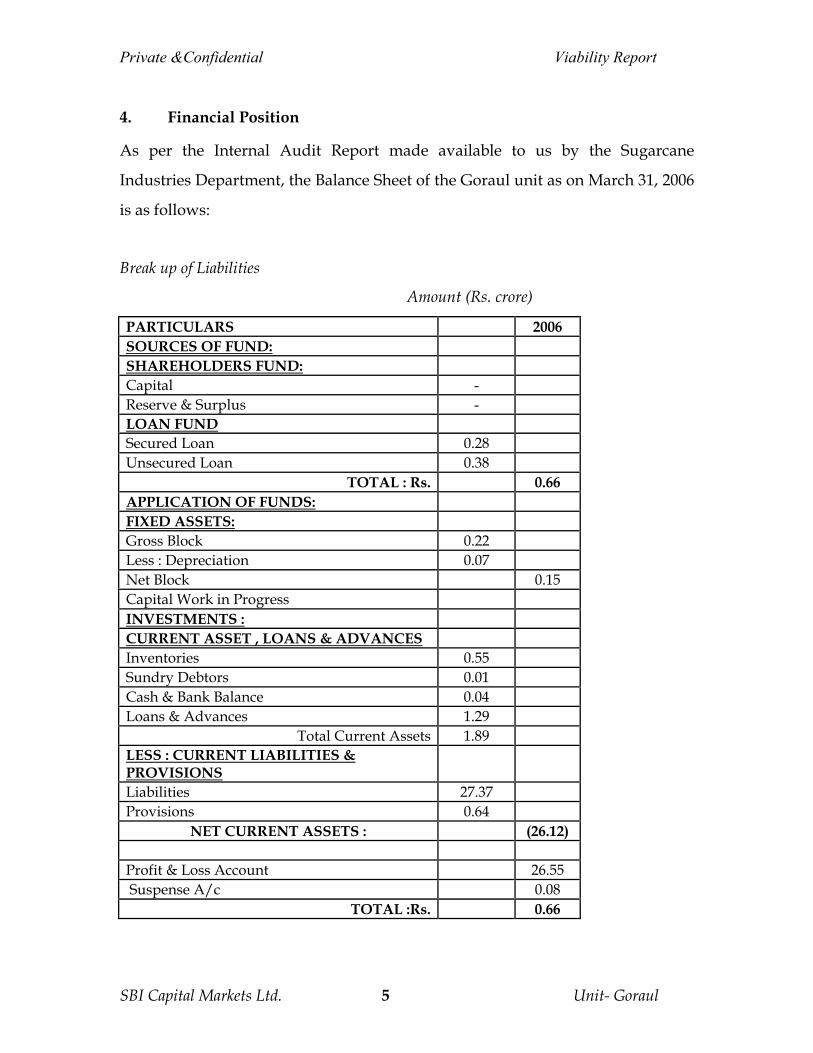

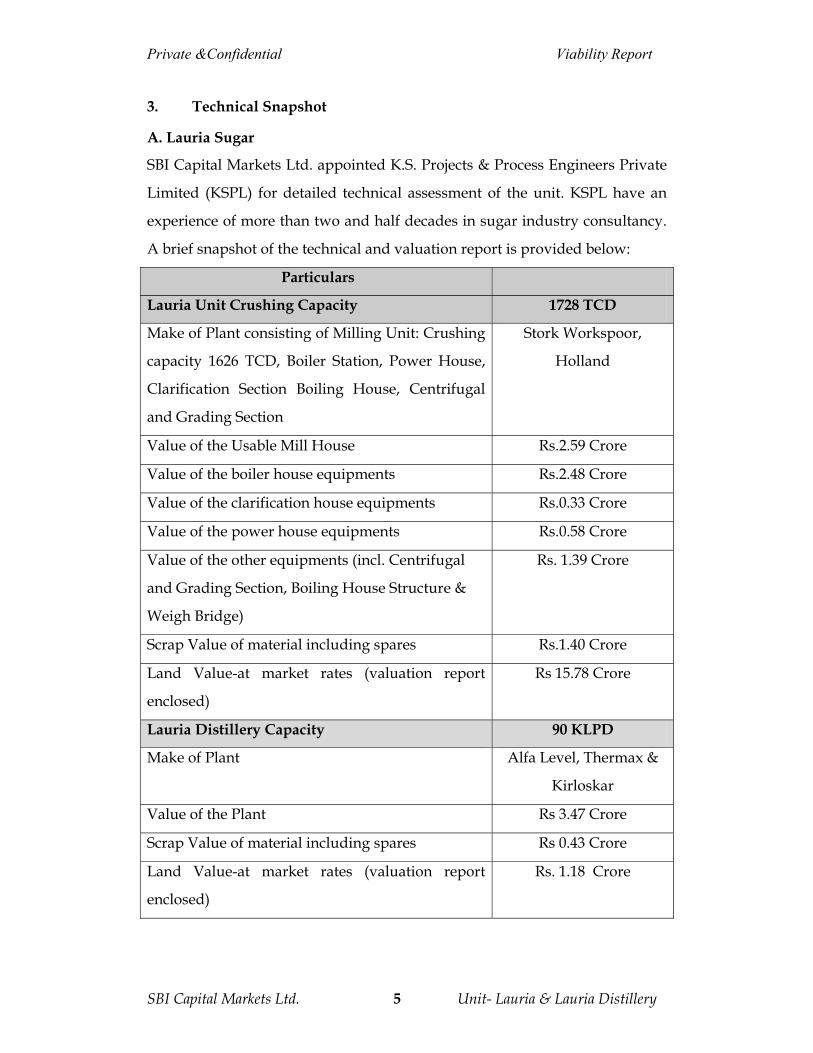

Private &Confidential Viability Report

Bihar State Sugar Corporation Ltd. 1

IMPORTANT NOTICE

This Report contains proprietary and confidential information regarding to Bihar State Sugar

Corporation Ltd (BSSC)’ or ‘the Corporation’).This has been prepared by SBI Capital Markets

Ltd. (‘SBICAP’) on the basis of information provided by the corporation, technical consultants,

valuers, legal advisor and publicly available sources, to be used for the purpose of providing

Advisory Services to the Corporation or Sugarcane Industries Department, Government of Bihar

for exploring the possibility of revival of the closed sugar units of the Corporation..

This report is based on information made available by BSSC. No assurance can be provided that

the assumptions or data upon which these recommendations have been based are accurate or

whether this business plan will actually materialize.

Neither SBICAP, nor State Bank of India or any of its associates, nor any of their respective

directors, employees or advisors make any expressed or implied representation or warranty and

no responsibility or liability is accepted by any of them with respect to the accuracy, completeness

or reasonableness of the facts, opinions, estimates, forecasts, projections, or other information set

forth in this Report or the underlying assumptions on which they are based .There is no

assurance on the success of the assignment and it is solely based on the judgment of the investors

and the current market conditions.

This Report is furnished strictly on confidential basis. Neither this Report, nor the information

contained herein, may be reproduced or passed to any person or used for any purpose other than

stated above. By accepting a copy of this Report, the recipient accepts the terms of this Notice,

which forms an integral part of this Report.

Private &Confidential Viability Report

Bihar State Sugar Corporation Ltd. 2

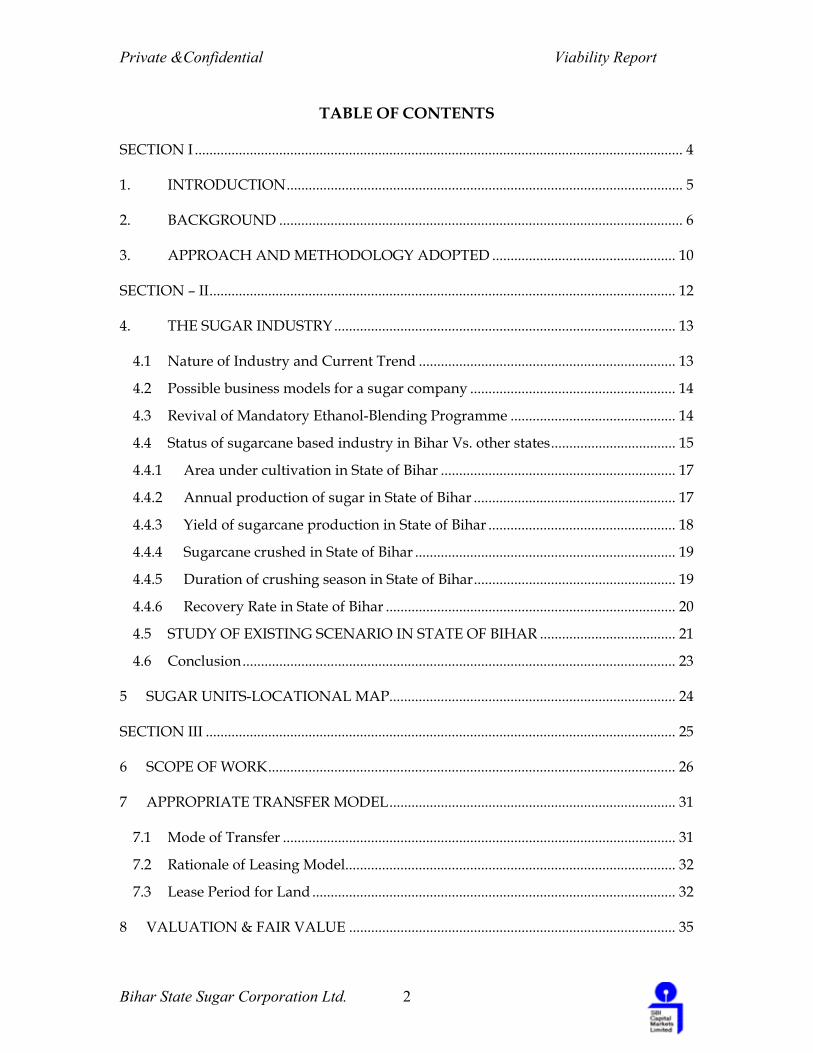

TABLE OF CONTENTS

SECTION I ..................................................................................................................................... 4

1. INTRODUCTION............................................................................................................ 5

2. BACKGROUND .............................................................................................................. 6

3. APPROACH AND METHODOLOGY ADOPTED .................................................. 10

SECTION – II............................................................................................................................... 12

4. THE SUGAR INDUSTRY............................................................................................. 13

4.1 Nature of Industry and Current Trend ...................................................................... 13

4.2 Possible business models for a sugar company ........................................................ 14

4.3 Revival of Mandatory Ethanol-Blending Programme ............................................. 14

4.4 Status of sugarcane based industry in Bihar Vs. other states.................................. 15

4.4.1 Area under cultivation in State of Bihar ................................................................ 17

4.4.2 Annual production of sugar in State of Bihar ....................................................... 17

4.4.3 Yield of sugarcane production in State of Bihar ................................................... 18

4.4.4 Sugarcane crushed in State of Bihar ....................................................................... 19

4.4.5 Duration of crushing season in State of Bihar....................................................... 19

4.4.6 Recovery Rate in State of Bihar ............................................................................... 20

4.5 STUDY OF EXISTING SCENARIO IN STATE OF BIHAR ..................................... 21

4.6 Conclusion...................................................................................................................... 23

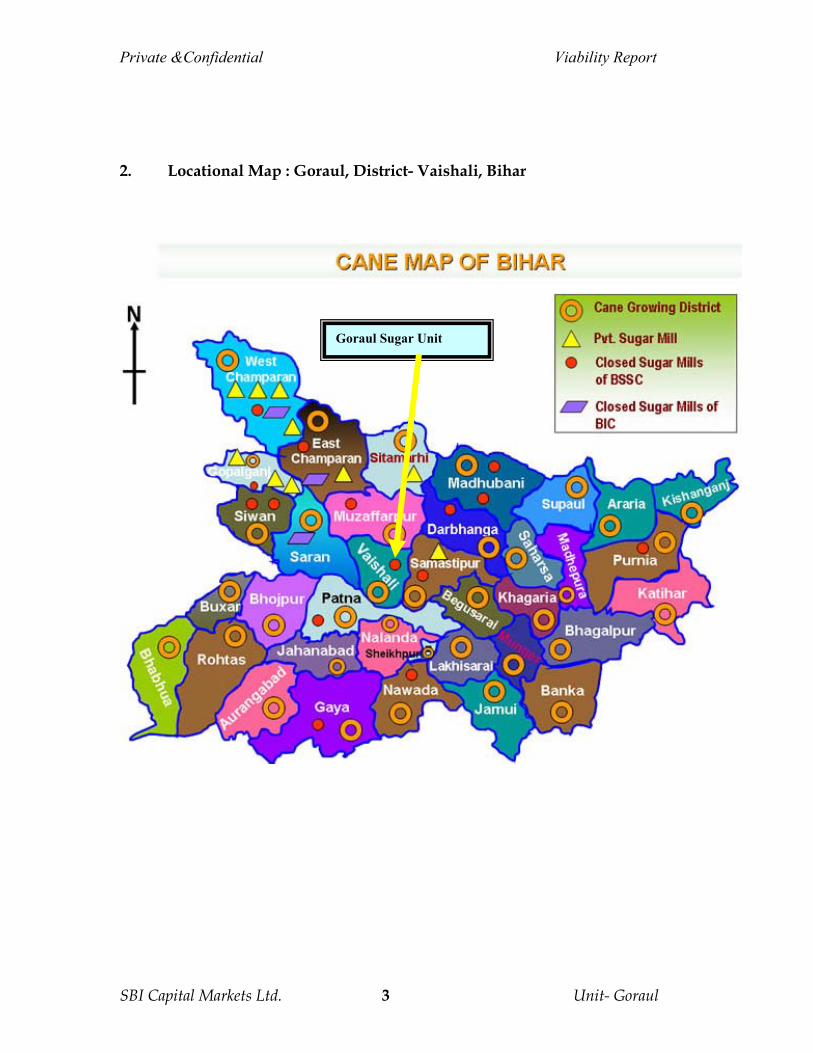

5 SUGAR UNITS-LOCATIONAL MAP.............................................................................. 24

SECTION III ................................................................................................................................ 25

6 SCOPE OF WORK............................................................................................................... 26

7 APPROPRIATE TRANSFER MODEL.............................................................................. 31

7.1 Mode of Transfer ........................................................................................................... 31

7.2 Rationale of Leasing Model.......................................................................................... 32

7.3 Lease Period for Land ................................................................................................... 32

8 VALUATION & FAIR VALUE ......................................................................................... 35

Private &Confidential Viability Report

Bihar State Sugar Corporation Ltd. 3

8.1 Valuation ........................................................................................................................ 35

8.2 Fair Value........................................................................................................................ 35

9 SETTLEMENT PROCESS, SACRIFICE & UTILISATION OF THE PROCEEDS ....... 37

9.1 Settlement process ......................................................................................................... 37

9.2 Sacrifices ......................................................................................................................... 37

9.3 Utilisation ....................................................................................................................... 40

10 LITIGATIONS AND SETTLEMENTS ........................................................................ 42

10.1 Litigations................................................................................................................... 42

11 SUGGESTED PLAN OF ACTION .............................................................................. 44

12 TENDERING/BIDDING PROCESS ........................................................................... 45

13 SELECTION CRITERIA................................................................................................ 46

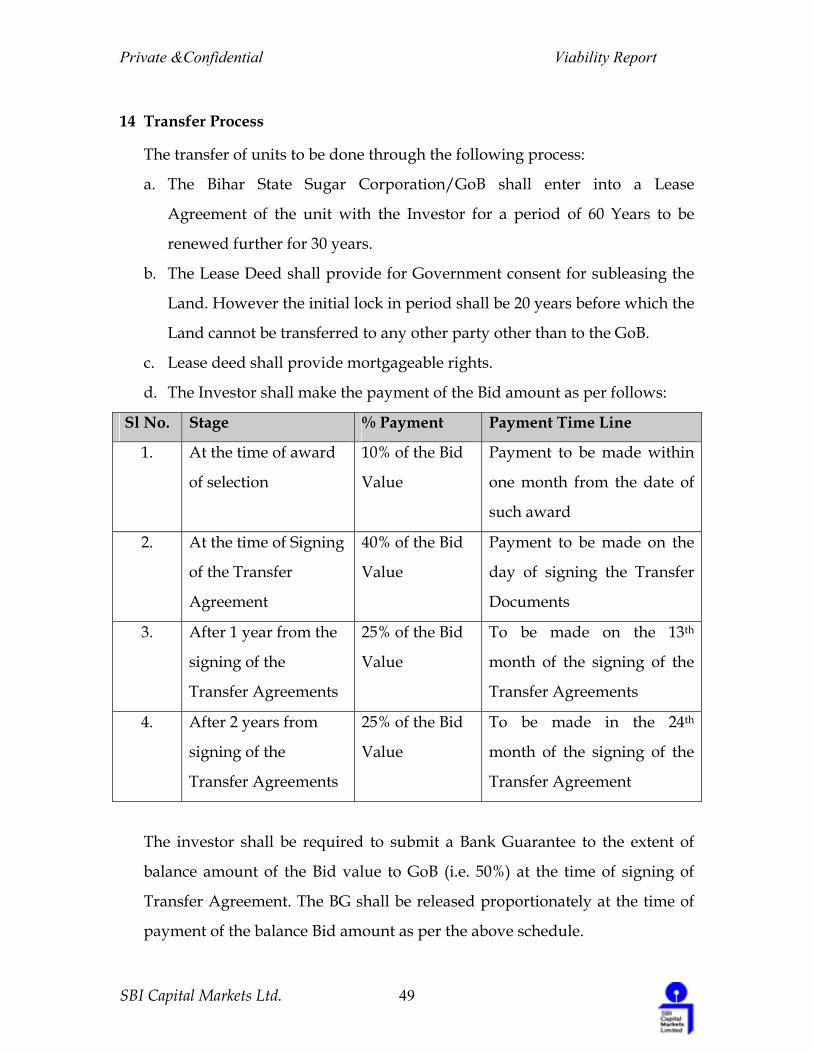

14 TRANSFER PROCESS .................................................................................................. 49

15 SUGGESTIONS FOR ADDITIONAL INCENTIVES FOR INCLUSION IN SUGAR

POLICY ........................................................................................................................................ 51

16 RECOMMENDATIONS ............................................................................................... 53

Private &Confidential Viability Report

Bihar State Sugar Corporation Ltd. 4

Section I

GGGeeennneeerrraaalll

Private &Confidential Viability Report

Bihar State Sugar Corporation Ltd. 5

1. Introduction

Bihar State Sugar Corporation Ltd. (a Government of Bihar Undertaking) was

incorporated in 1974 to manage, operate and control the loss making sugar and

distillery units under the control of State Government. The Government of Bihar

(GoB) under the Bihar Sugar Undertakings (Acquisition) Ordinance 1976 and

Sugar Undertakings (Acquisition) Act 1985 acquired 15 sick Sugar Mills and 2

distilleries from private companies/owners between 1977-1985. The said

takeover of the sick units was undertaken with an objective to revive them and

make them operational and viable.

Most of the units could not sustain the mounting pressure of declining prices and

increasing input costs and thereby the units started closing down one after

another. The units thereafter could not be revived and all the units were closed

by the crushing season 1996-97.

The machineries have not been refurbished since the closure. Due to the same,

the conditions of the units are presently not satisfactory.

The Government of Bihar, constituted a high level committee under the

chairmanship of Cane Development Commissioner in February 2006. The

Committee was of the opinion that a financial advisor shall be appointed for

valuation of the units and to suggest appropriate revival plan for the closed

sugar units of BSSC.

Private &Confidential Viability Report

Bihar State Sugar Corporation Ltd. 6

With a view to finalise the policy for making these units operational, GoB, finally

invited bids for Advisory Services to suggest the Methodology and Approach for

Revival/Restructuring/Sale/Lease of the closed sugar units of Bihar State Sugar

Corporation Limited.

Accordingly, SBI Capital Markets Limited was appointed to advise the

Government in adopting appropriate strategy subject to the approval of the State

Government. SBICAP will also assist the Government in preparing the Bid

Documents for inviting expression of interest, preparing Request for

Qualification and Request for participation etc as is necessary to attract investor

for revival/lease/sale of sugar units based on various parameters.

2. Background

Incorporated in 1974 under the companies Act 1956, the Bihar State Sugar

Corporation Limited (BSSC) was formed to acquire and manage sugar units of

Government of Bihar. The units were facing problems in satisfying their cane

growers dues, labour dues as also the statutory dues. Considering the same, the

Government of Bihar under the Bihar Sugar Undertakings (Acquisition)

Ordinance 1976 and Bihar Sugar Undertakings (Acquisition) Act 1985 acquired

various units under the aforesaid provisions. Since then the units were managed

under the BSSC.

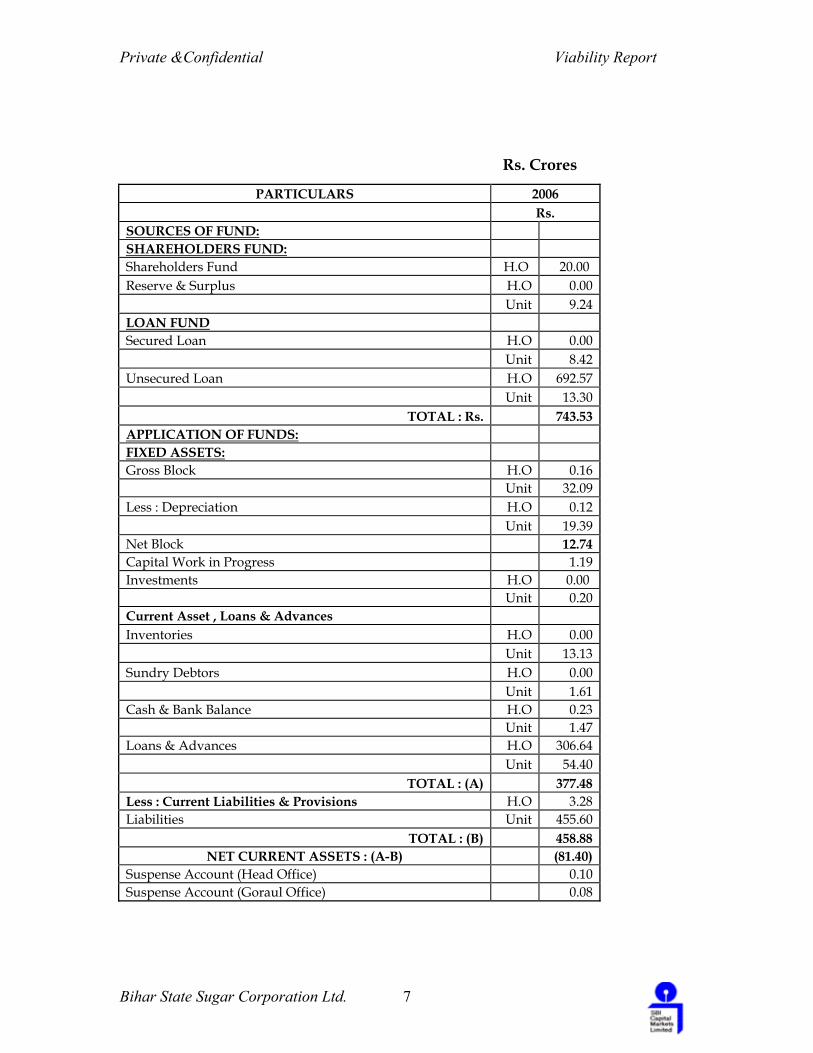

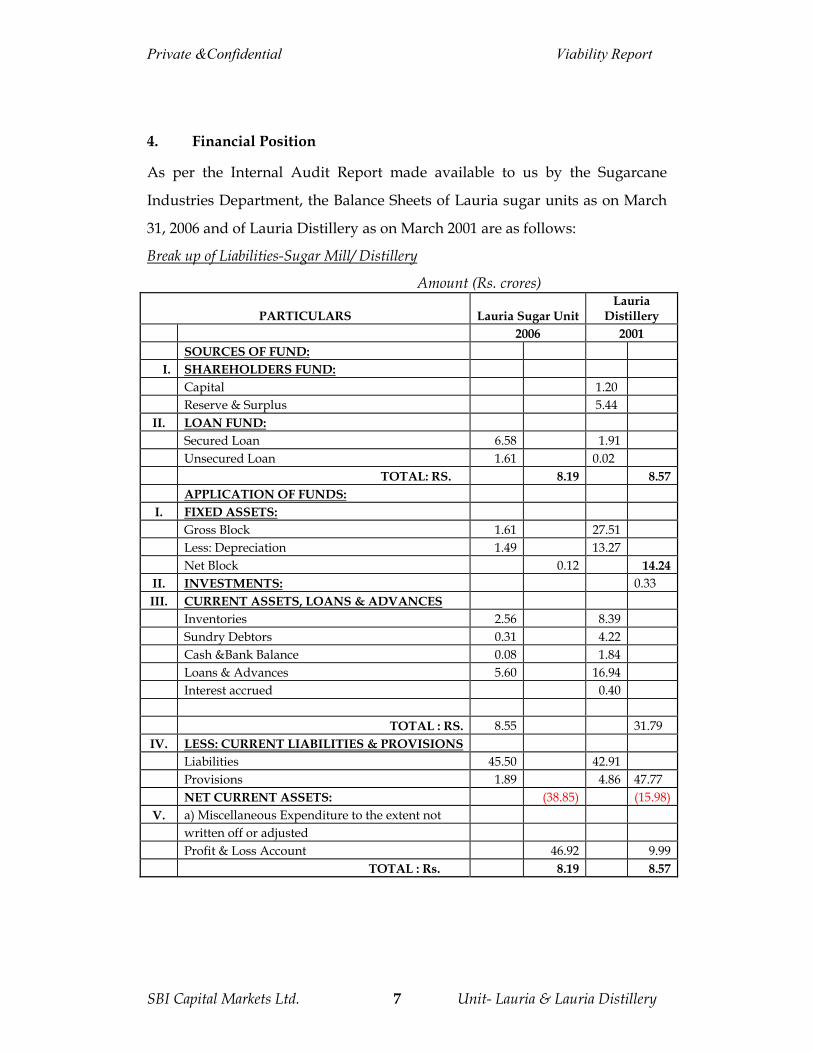

The financial statement of BSSC was internally audited in FY 2001-02. The

Balance Sheet as on March 31, 2002 is as under:

Private &Confidential Viability Report

Bihar State Sugar Corporation Ltd. 7

Rs. Crores

PARTICULARS 2006 Rs. SOURCES OF FUND: SHAREHOLDERS FUND: Shareholders Fund H.O 20.00 Reserve & Surplus H.O 0.00 Unit 9.24 LOAN FUND Secured Loan H.O 0.00 Unit 8.42 Unsecured Loan H.O 692.57 Unit 13.30

TOTAL : Rs. 743.53 APPLICATION OF FUNDS: FIXED ASSETS: Gross Block H.O 0.16 Unit 32.09 Less : Depreciation H.O 0.12 Unit 19.39 Net Block 12.74 Capital Work in Progress 1.19 Investments H.O 0.00 Unit 0.20 Current Asset , Loans & Advances Inventories H.O 0.00 Unit 13.13 Sundry Debtors H.O 0.00 Unit 1.61 Cash & Bank Balance H.O 0.23 Unit 1.47 Loans & Advances H.O 306.64 Unit 54.40

TOTAL : (A) 377.48 Less : Current Liabilities & Provisions H.O 3.28 Liabilities Unit 455.60

TOTAL : (B) 458.88 NET CURRENT ASSETS : (A-B) (81.40)

Suspense Account (Head Office) 0.10 Suspense Account (Goraul Office) 0.08

Private &Confidential Viability Report

Bihar State Sugar Corporation Ltd. 8

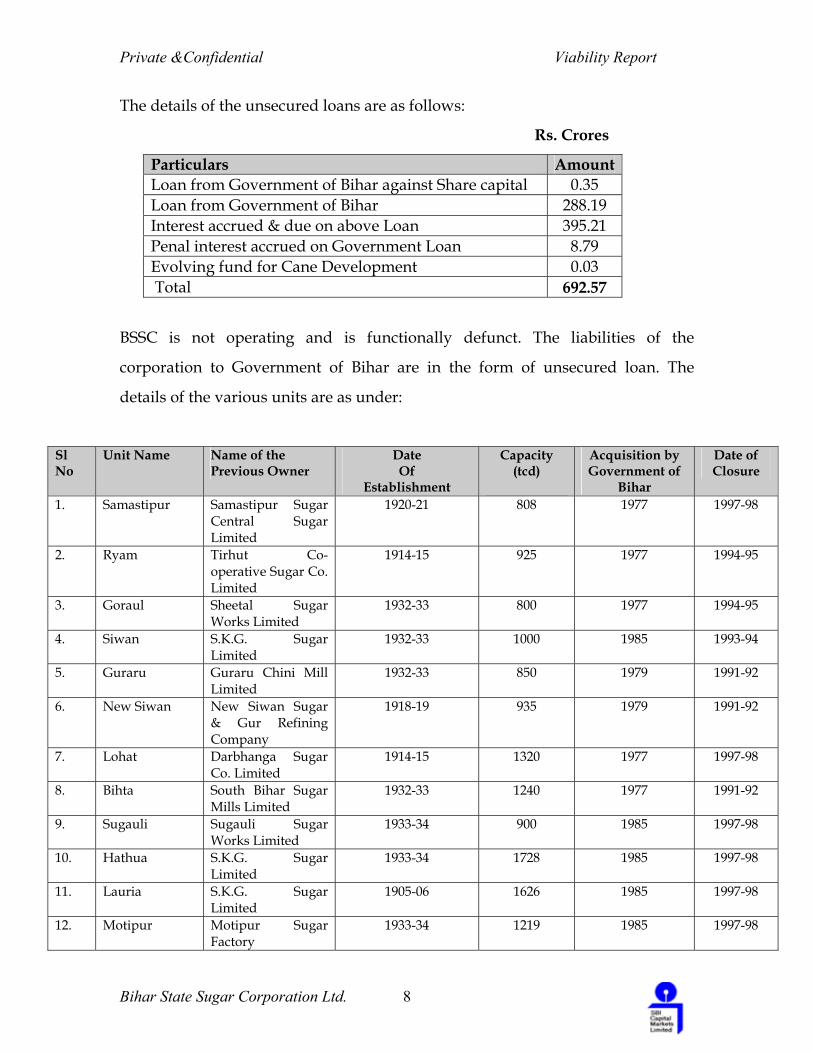

The details of the unsecured loans are as follows:

Rs. Crores

Particulars Amount Loan from Government of Bihar against Share capital 0.35 Loan from Government of Bihar 288.19 Interest accrued & due on above Loan 395.21 Penal interest accrued on Government Loan 8.79 Evolving fund for Cane Development 0.03 Total 692.57

BSSC is not operating and is functionally defunct. The liabilities of the

corporation to Government of Bihar are in the form of unsecured loan. The

details of the various units are as under:

Sl No

Unit Name Name of the Previous Owner

Date Of

Establishment

Capacity (tcd)

Acquisition by Government of

Bihar

Date of Closure

1. Samastipur Samastipur Sugar Central Sugar Limited

1920-21 808 1977 1997-98

2. Ryam Tirhut Co-operative Sugar Co. Limited

1914-15 925 1977 1994-95

3. Goraul Sheetal Sugar Works Limited

1932-33 800 1977 1994-95

4. Siwan S.K.G. Sugar Limited

1932-33 1000 1985 1993-94

5. Guraru Guraru Chini Mill Limited

1932-33 850 1979 1991-92

6. New Siwan New Siwan Sugar & Gur Refining Company

1918-19 935 1979 1991-92

7. Lohat Darbhanga Sugar Co. Limited

1914-15 1320 1977 1997-98

8. Bihta South Bihar Sugar Mills Limited

1932-33 1240 1977 1991-92

9. Sugauli Sugauli Sugar Works Limited

1933-34 900 1985 1997-98

10. Hathua S.K.G. Sugar Limited

1933-34 1728 1985 1997-98

11. Lauria S.K.G. Sugar Limited

1905-06 1626 1985 1997-98

12. Motipur Motipur Sugar Factory

1933-34 1219 1985 1997-98

Private &Confidential Viability Report

Bihar State Sugar Corporation Ltd. 9

13. Sakri Darbhanga Sugar Co. Ltd.

1933-34 782 1977 1997-98

14. Banmankhi Purnea Co-operative Sugar Factory Limited

1970-71 1000 1977 1997-98

15. Warisaliganj Warisaliganj Co-operative Sugar Mills

1933-34 700 1977 1993-94

16. Hathua-Distlillery

S.K.G. Sugar Limited

Not available 60 Klpd 2002 2002-03

17. Lauriya Distillery

S.K.G. Sugar Limited

Not available 90 Klpd 2002 2002-03

Private &Confidential Viability Report

Bihar State Sugar Corporation Ltd. 10

3. Approach and Methodology Adopted

The approach and methodology adopted for executing the assignment has been

detailed below:

Diagnostic Study

On obtention of the above information a Revival Strategy has been adopted. The

framework of the same is as follows:

Unit Visit

Collection of Preliminary information

Unit Valuation-Assets

Analysis of the existing liabilities

Litigation Status against BSSC/units

Land Title Deed

SBICAP Team along with Sugarcane Industries Department

To assess the status of the sugar units

Sugarcane Industries Department

To understand the details about the financial position of the respective sugar units.

To assess the current value & remaining life of the assets.

Through Chartered Engineers: K.S. Projects & Process Engineers Private Limited.

To suggest measures of settlement/waiver of liabilities.

Reports submitted by the SID.

Through Land valuer

To assess the value of land .

To understand the legal implications in case of reorganization of units amid existing pending cases.

Through Legal Consultant.

Private &Confidential Viability Report

Bihar State Sugar Corporation Ltd. 11

Unitwise Analysis

Viable Units Un-Viable Units

Suggestions for unitwise strategy

Proposal submitted to SID, GoB for

approval/suggestions

Approval from GoB along with

suggestions/alterations and appropriate

strategy

Invitation for Bids (RFP-RFQ)

Selection of Investor

Preparation of Transfer Documents

Handholding Support to SID for transfer of

units to Investors

Private &Confidential Viability Report

Bihar State Sugar Corporation Ltd. 12

Section – II

UUUnnniiittt LLLooocccaaatttiiiooonnnaaalll MMMaaappp

AAAnnnddd

SSSuuugggaaarrr IIInnnddduuussstttrrryyy PPPrrrooofffiiillleee

Private &Confidential Viability Report

SBI Capital Markets Ltd. 13

4. The Sugar Industry

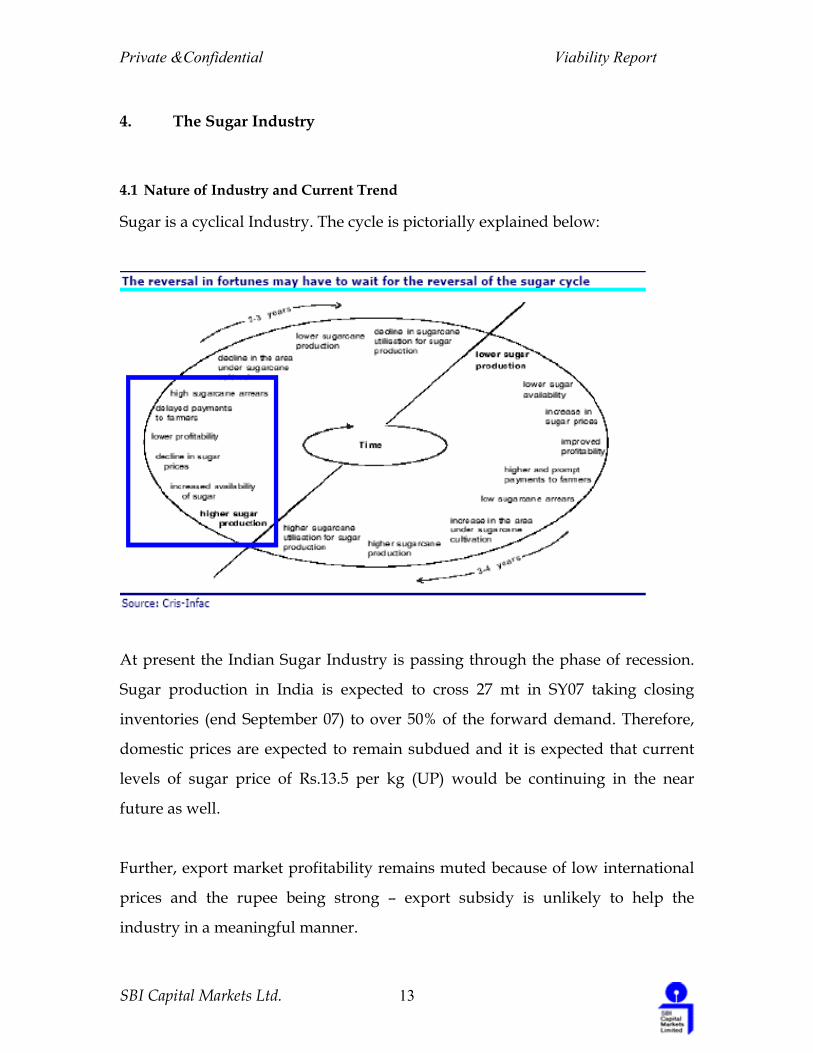

4.1 Nature of Industry and Current Trend

Sugar is a cyclical Industry. The cycle is pictorially explained below:

At present the Indian Sugar Industry is passing through the phase of recession.

Sugar production in India is expected to cross 27 mt in SY07 taking closing

inventories (end September 07) to over 50% of the forward demand. Therefore,

domestic prices are expected to remain subdued and it is expected that current

levels of sugar price of Rs.13.5 per kg (UP) would be continuing in the near

future as well.

Further, export market profitability remains muted because of low international

prices and the rupee being strong – export subsidy is unlikely to help the

industry in a meaningful manner.

Private &Confidential Viability Report

SBI Capital Markets Ltd. 14

This brings us to the view that standalone sugar mills would always be

vulnerable when the Industry go downward, as compared to integrated units.

4.2 Possible business models for a sugar company

1) Sugar – Mollases – Bagasse Model - Only sugar manufacturing & selling by-

products without any value addition

2) Sugar – Alcohol – Bagasse Model – Sugar manufacturing and molasses being

again converted into alcohol & further to ethanol and bagasse is sold without any

further value addition.

3) Sugar – Molasses – Power Model – Sugar manufacturing and bagasse based

co-generation, however, molasses is sold without any value addition.

4) Sugar – alcohol – power model – This is the integrated and most widely

preferred model wherein apart from the sugar manufacturing even the by-

products are further processed to manufacture alcohol/ ethanol and generate

power. An integrated model helps in protecting revenues and improving

profitability during periods of downturn in core sugar business. For e.g. sugar

prices fell sharply due to oversupply in the market but alcohol/ power sprices

were relatively stable and contributed heavily to the profitability.

4.3 Revival of Mandatory Ethanol-Blending Programme

The policy has again got revived and a national programme to blend 5% ethanol

with petrol has become effective from November 01, 2006. The programme has

Private &Confidential Viability Report

SBI Capital Markets Ltd. 15

been extended to the entire country except the states in North-east, J&K,

Lakshadweep and Andaman and Nicobar islands. However, the programme has

not been made mandatory and oil companies have been given freedom to protect

their commercial interests at arriving at a viable ethanol pricing. It is estimated

that by 2010-11, around 2500 mn ltr of alcohol/ ethanol will be required to meet

the demand for blending and for industrial, potable and other purposes. In the

event 10% blending becomes mandatory than around 3500 mn lts of alcohol/

ethanol will be required to satisfy the demand. In the event, even if the entire

molasses produced is processed into alcohol, the quantity of molasses required to

meet the projected demand will be 11.3 mn tones and 15.5 mn tones at 5% and

10% blending respectively .

4.4 Status of sugarcane based industry in Bihar Vs. other states

In 1930s, State of Bihar contributed around 30% of the total sugar production of

country which has now come down to 2% [Chart given below]. In 1930s 35 sugar

mills existed as against 28 in 1980s and 9 in 2006. Sugar mills are mostly

concentrated in two districts viz. West Champaran and Gopalganj.

S TATEM ENT S HOWI NG N ET B I H AR S UGAR P ROD UC TI ON % TO ALL I NDI A P ROD UC TI ON ( 5 YER S AVER AGE) FROM 19 3 1- 3 6 TO 2 0 0 1- 0 6

31.74

25.21

2.022.072.763.403.734.214.897.79

10.7714.13

16.3718.6718.41

0

5

10

15

20

25

30

35

1931-36

1936-41

1941-46

1946-51

1951-56

1956-61

1961-66

1966-71

1971-76

1976-81

1981-86

1986-91

1991-96

1996-01

2001-06

Private &Confidential Viability Report

SBI Capital Markets Ltd. 16

The downfall of the sugar industry in the state of Bihar was mainly due to non-

availability of sufficient quantity of sugarcane on account of lack of infra-

structure such as main and village link, lack of irrigation facilities, non-

availability of power, water logging in the absence of drainage etc. and non-

availability of good sugarcane varieties on a regular basis.

In Bihar the intensity of cane is not as high as compared to several sugarcane

producing regions in North India and the main reason for the same is that out of

the total cultivable area a sizeable portion is low-lying area which is not suitable

for cultivation of sugarcane in the absence of drainage facilities. The productivity

of sugarcane i.e. yield is 41.4 tonne per hectare in Bihar is much lower than the

national average of 59.4 tonne per hectare (Source- Co-operative Sugar, Nov.,06).

Among other major sugar producing states, sugar factories of Uttar Pradesh are

facing “Cane War” since new factories have been allowed to be established in

close proximity to existing sugar factories. In Tamil Nadu, the sugar factories

normally bring sugarcane from distance ranging from 50 to 60 kms and in some

cases even from distances upto 100 kms. In Maharashtra, the main cause for

sickness in the sugar sector is the establishment of sugar factories in the close

proximity of each other resulting in lack of availability of sufficient quantity of

sugarcane to each factory.

An effort has been made to map the status of sugarcane based industry in State

of Bihar vis-à-vis various others Indian states based on the various parameters to

understand the hidden and upside potential of sugarcane based industry in

Bihar. It may be mentioned that the data down below in the tables is upto 2004-

05 during which period it was draught in the state of Maharashtra and

Karnataka and a slight distortions and the decline in performance and

Private &Confidential Viability Report

SBI Capital Markets Ltd. 17

parameters has been seen in respect of these two states which may be considered

as temporary.

4.4.1 Area under cultivation in State of Bihar

The area under sugarcane cultivation in Bihar as compared to states which are

not much larger in size is very small and thus there is a great potential for

enlargement of the sugarcane growing area. This should be considered in the

perspective of the fact that Bihar has very fertile land and also has some

perennial rivers flowing through it there is very heavy rainfall in the state. All

this further underscores the potential of Bihar to emerge as a major sugarcane

growing state.

Table 1: State wise area under cultivation (in '000 hectares)

Year 97-98 98-99 99-00 00-01 01-02 02-03 03-04 04-05P

State

Maharashtra 460 530 590 595 578 573 443 324

Uttar Pradesh 1985 1975 2011 1938 2035 2149 2030 1955

Karnataka 310 339 373 417 407 383 243 178

Tamil Nadu 283 306 316 315 231 261 192 232

Bihar 108 107 97 94 113 107 104 104

4.4.2 Annual production of sugar in State of Bihar

The annual sugar production in the state is also very low when compared to

other states. This is mainly due to the very small area under sugarcane

cultivation but also due to less scientific way in which sugarcane is grown in

Bihar. This can be significantly improved by bringing in more area under

Private &Confidential Viability Report

SBI Capital Markets Ltd. 18

sugarcane cultivation and cultivating high yielding varieties of sugarcane in the

state.

Table 2: State wise annual production (in ‘000 tonnes)

Year 97-98 98-99 99-00 00-01 01-02 02-03 03-04 04-05P

State

Maharashtra 38174 47151 53143 49589 45140 42167 25668 20475

Uttar

Pradesh 129267 116483 115419 106068 117982 120948 112754 118715

Karnataka 28332 34771 37567 42924 33017 32485 16015 14276

Tamil Nadu 30183 33765 34285 33188 32620 24165 17656 23396

Bihar 4960 5101 4089 3988 5211 4521 4286 4112

4.4.3 Yield of sugarcane production in State of Bihar

The yield per hectare is much below that of other sugar producing states,

highlighting the fact that cultivation is not done in a very scientific manner and

that hybrid high yielding varieties that are currently in cultivation in other states

are most probably not grown in the state. However, this indicates that there is

scope for great improvement.

Table 3: State wise yield (tonnes per hectare)

Year 97-98 98-99 99-00 00-01 01-02 02-03 03-04 04-05P

State

Maharashtra 83 89 90.1 83.3 78.1 74.4 57.9 63.2

Uttar Pradesh 65.1 59 57.4 54.7 58 56.3 55.5 60.7

Karnataka 91.5 102.6 100.7 102.9 81.1 84.9 65.8 80.2

Tamil Nadu 106.7 110.3 108.4 105.3 101.6 92.4 91.9 100.8

Bihar 45.9 47.7 42 42.6 46 42.1 41.4 39.5

Private &Confidential Viability Report

SBI Capital Markets Ltd. 19

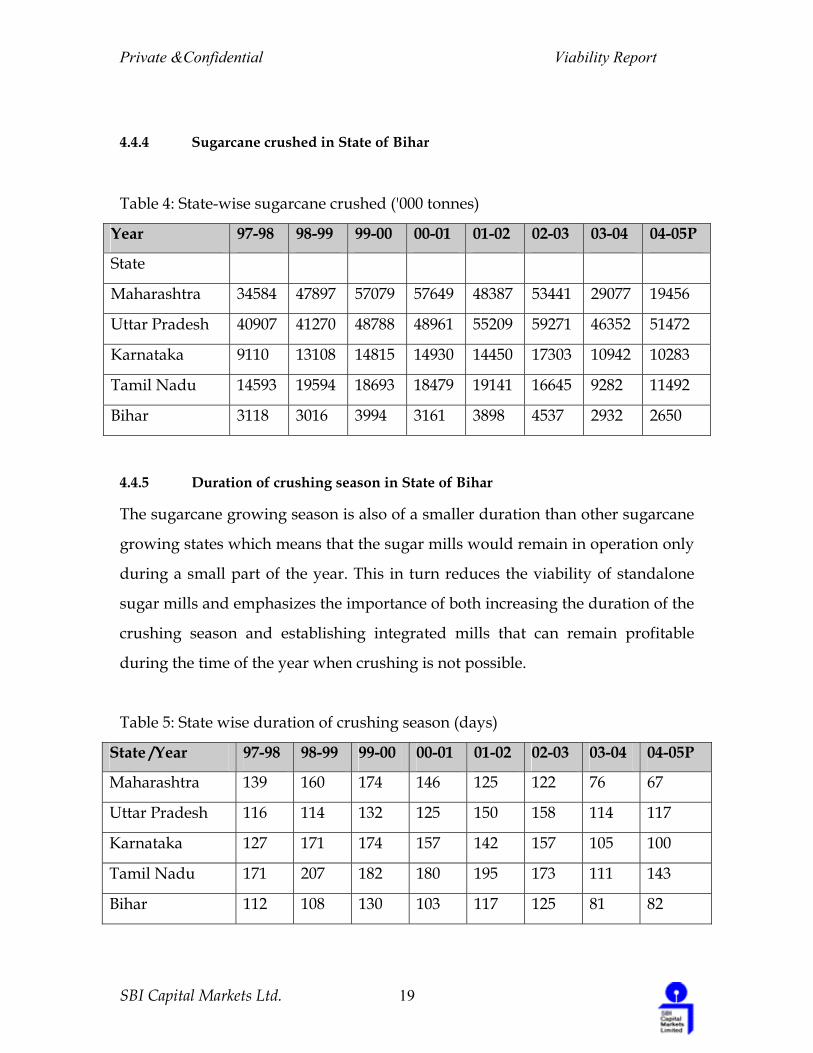

4.4.4 Sugarcane crushed in State of Bihar

Table 4: State-wise sugarcane crushed ('000 tonnes)

Year 97-98 98-99 99-00 00-01 01-02 02-03 03-04 04-05P

State

Maharashtra 34584 47897 57079 57649 48387 53441 29077 19456

Uttar Pradesh 40907 41270 48788 48961 55209 59271 46352 51472

Karnataka 9110 13108 14815 14930 14450 17303 10942 10283

Tamil Nadu 14593 19594 18693 18479 19141 16645 9282 11492

Bihar 3118 3016 3994 3161 3898 4537 2932 2650

4.4.5 Duration of crushing season in State of Bihar

The sugarcane growing season is also of a smaller duration than other sugarcane

growing states which means that the sugar mills would remain in operation only

during a small part of the year. This in turn reduces the viability of standalone

sugar mills and emphasizes the importance of both increasing the duration of the

crushing season and establishing integrated mills that can remain profitable

during the time of the year when crushing is not possible.

Table 5: State wise duration of crushing season (days)

State /Year 97-98 98-99 99-00 00-01 01-02 02-03 03-04 04-05P

Maharashtra 139 160 174 146 125 122 76 67

Uttar Pradesh 116 114 132 125 150 158 114 117

Karnataka 127 171 174 157 142 157 105 100

Tamil Nadu 171 207 182 180 195 173 111 143

Bihar 112 108 130 103 117 125 81 82

Private &Confidential Viability Report

SBI Capital Markets Ltd. 20

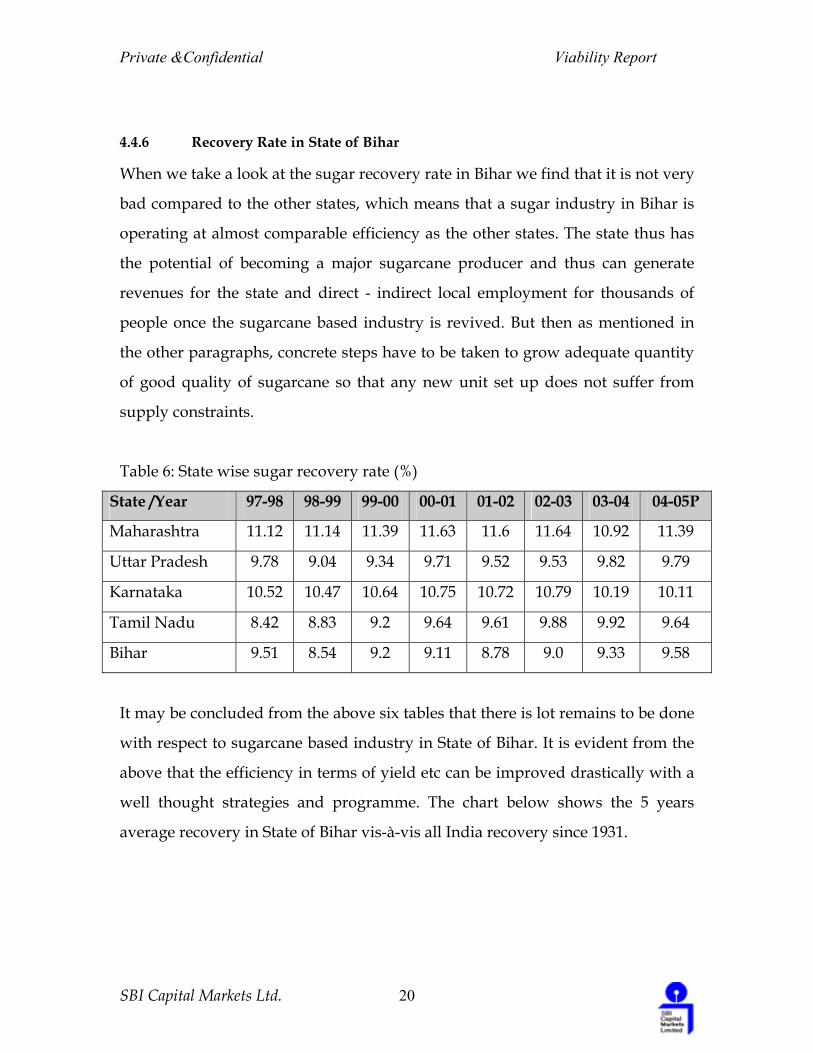

4.4.6 Recovery Rate in State of Bihar

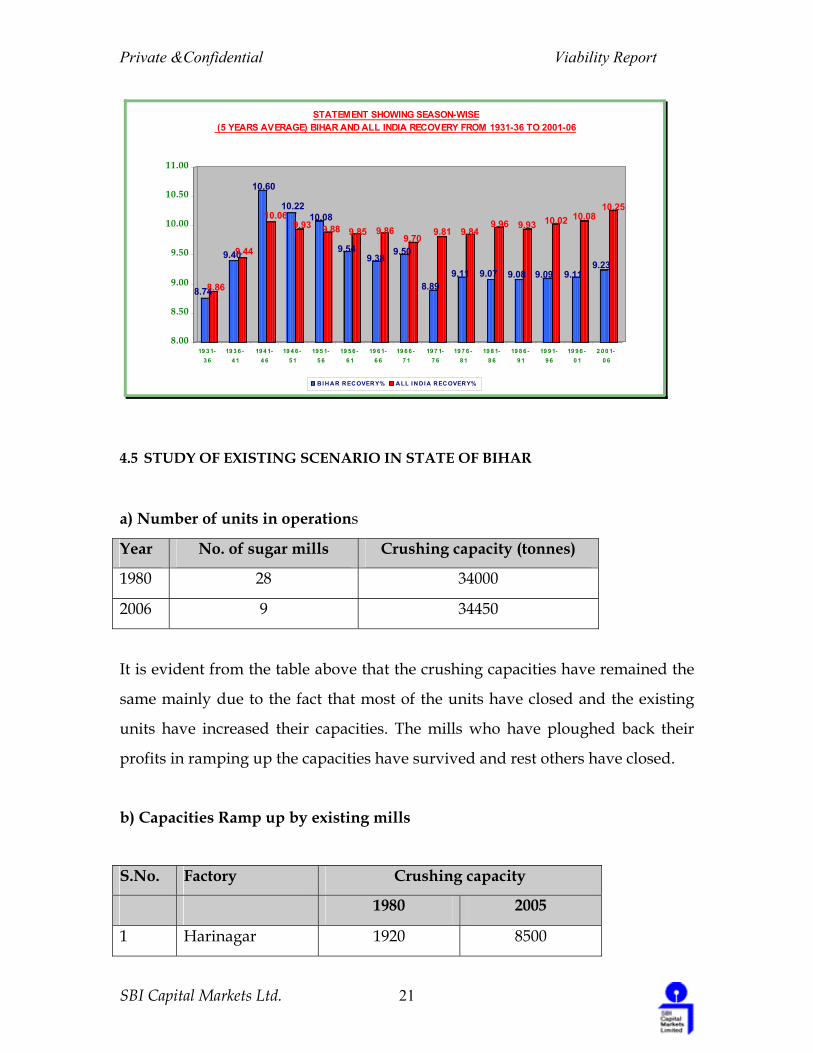

When we take a look at the sugar recovery rate in Bihar we find that it is not very

bad compared to the other states, which means that a sugar industry in Bihar is

operating at almost comparable efficiency as the other states. The state thus has

the potential of becoming a major sugarcane producer and thus can generate

revenues for the state and direct - indirect local employment for thousands of

people once the sugarcane based industry is revived. But then as mentioned in

the other paragraphs, concrete steps have to be taken to grow adequate quantity

of good quality of sugarcane so that any new unit set up does not suffer from

supply constraints.

Table 6: State wise sugar recovery rate (%)

State /Year 97-98 98-99 99-00 00-01 01-02 02-03 03-04 04-05P

Maharashtra 11.12 11.14 11.39 11.63 11.6 11.64 10.92 11.39

Uttar Pradesh 9.78 9.04 9.34 9.71 9.52 9.53 9.82 9.79

Karnataka 10.52 10.47 10.64 10.75 10.72 10.79 10.19 10.11

Tamil Nadu 8.42 8.83 9.2 9.64 9.61 9.88 9.92 9.64

Bihar 9.51 8.54 9.2 9.11 8.78 9.0 9.33 9.58

It may be concluded from the above six tables that there is lot remains to be done

with respect to sugarcane based industry in State of Bihar. It is evident from the

above that the efficiency in terms of yield etc can be improved drastically with a

well thought strategies and programme. The chart below shows the 5 years

average recovery in State of Bihar vis-à-vis all India recovery since 1931.

Private &Confidential Viability Report

SBI Capital Markets Ltd. 21

8.748.86

9.409.44

10.60

10.0610.22

9.9310.08

9.88

9.54

9.85

9.38

9.86

9.509.70

8.89

9.81

9.11

9.84

9.07

9.96

9.08

9.93

9.09

10.02

9.11

10.08

9.23

10.25

8.00

8.50

9.00

9.50

10.00

10.50

11.00

19 3 1-3 6

19 3 6 -4 1

19 4 1-4 6

19 4 6 -5 1

19 5 1-5 6

19 5 6 -6 1

19 6 1-6 6

19 6 6 -7 1

19 7 1-7 6

19 7 6 -8 1

19 8 1-8 6

19 8 6 -9 1

19 9 1-9 6

19 9 6 -0 1

2 0 0 1-0 6

STATEMENT SHOWING SEASON-WISE (5 YEARS AVERAGE) BIHAR AND ALL INDIA RECOVERY FROM 1931-36 TO 2001-06

BI H AR RECOVERY% A LL I N DI A REC OVERY%

4.5 STUDY OF EXISTING SCENARIO IN STATE OF BIHAR

a) Number of units in operations

Year No. of sugar mills Crushing capacity (tonnes)

1980 28 34000

2006 9 34450

It is evident from the table above that the crushing capacities have remained the

same mainly due to the fact that most of the units have closed and the existing

units have increased their capacities. The mills who have ploughed back their

profits in ramping up the capacities have survived and rest others have closed.

b) Capacities Ramp up by existing mills

S.No. Factory Crushing capacity

1980 2005

1 Harinagar 1920 8500

Private &Confidential Viability Report

SBI Capital Markets Ltd. 22

2 Bagaha 1100 2500

3 Narkatiaganj 1500 5000

4 Majhaulia 2000 3500

5 Riga 1300 3500

6 Hasanpur 1300 1750

7 Harkhua 1300 5000

8 Sidhwalia 1100 2500

9 Sasamusa 1100 2200

TOTAL 12620 34450

Going forward, ramping up of capacities backed by the adequate availability of

sugarcane for feeding mills and achieving economies of scale would be

important consideration in reviving the sick sugar mills.

c) Distance Criteria

The Central Government vide its recent notification has specified that no sugar

factory shall be set up within the range of 15 kms of an existing sugar factory or

another new sugar factory, provided that the State Government may with prior

approval of the Central Government, notify such minimum distance higher than

15 kms in their respective States.

The above distance criteria of 15 kms in the case of sugar factories in Bihar may

considered to be highly inadequate, in view of both low intensity of sugarcane

and low productivity of sugarcane due to reasons mentioned above. As a result

the sugar factories have historically faced the chronic problem of lack of

availability of adequate quantity of cane commensurate with their crushing

capacity resulting in large scale sickness in the industry due to which out of

Private &Confidential Viability Report

SBI Capital Markets Ltd. 23

twenty eight factories in 1980, nineteen factories have closed down and only nine

factories in the private sector are presently working.

In this connection it may be mentioned that Tuteja Committee (set up by the

Food Ministry under the Chairmanship of Shri S.K. Tuteja secretary, Department

of Food and Public Distribution in March, 2004 for suggesting measures for

revitalization of sugar industry) has also recommended a minimum radial

distance of 25 km between two sugar factories, based on the availability of

sugarcane for a 5000 TCD plant.

4.6 Conclusion

To attain the long term sustainability / viability of sugar mills, the focus should

be to create the large capacities integrated sugar complexes. Further it needs to

be ensured that the mills getting revived under this package could eventually

expand their capacities to 10000 tcpd each. It is therefore essential, in the larger

interest of these mills (getting revived), to identify the command area which

could eventually cater to above capacities of sugar mills.

Accordingly, GoB should adopt the policy of long term reservation of cane areas.

Once the units are confident that the given area would remain with them on a

permanent basis, they can undertake intensive cane development work which

would help in improving the productivity of sugarcane, which will ultimately

benefit the sugarcane farmers and the mills.

Private &Confidential Viability Report

SBI Capital Markets Ltd. 24

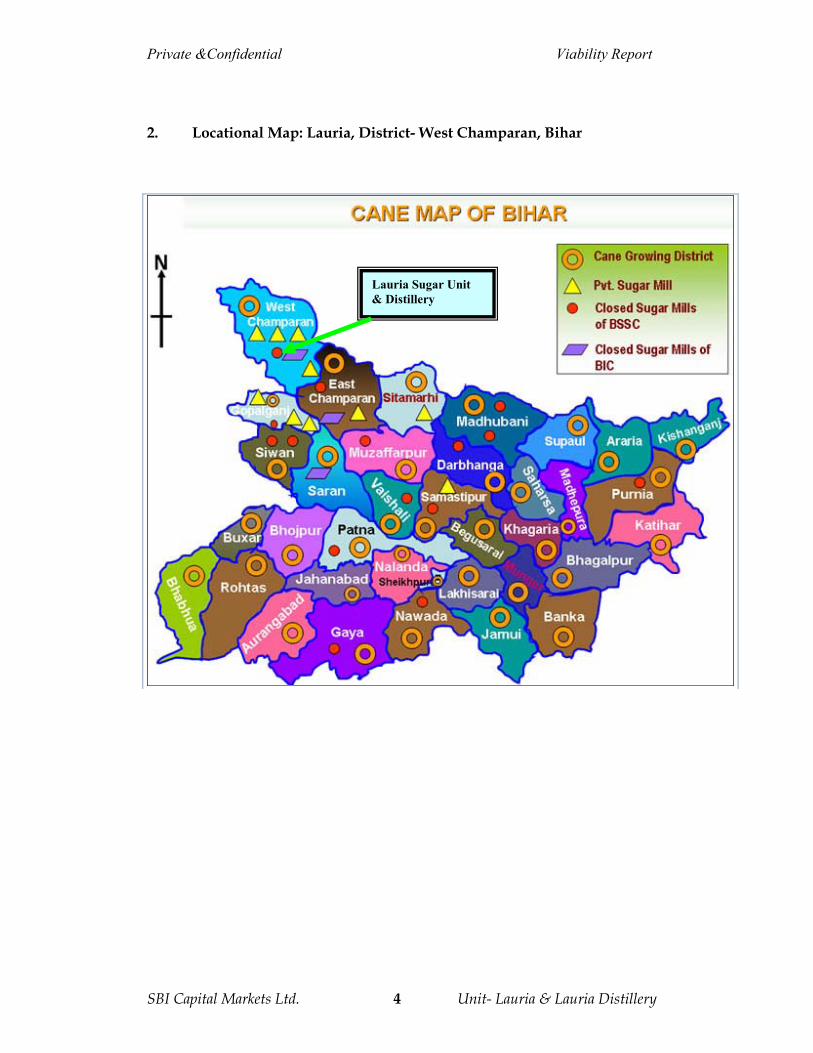

5 Sugar Units-Locational Map

Private &Confidential Viability Report

SBI Capital Markets Ltd. 25

Section III

RRREEEVVVIIIVVVAAALLL PPPLLLAAANNN

Private &Confidential Viability Report

SBI Capital Markets Ltd. 26

6 Scope of Work

As per the work order awarded by Government of Bihar (GoB), a diagnostic

study on as is where is basis, which inter alia included valuation of assets,

analysis for future viability based on operational and financial parameters, and

suggestions for revival plans. Accordingly, technical consultants & valuers were

appointed to value the assets and analyse the units’ health on as is where is basis.

Further, financial analysis of the units has been done by SBICAP based on the

internal audit report of the units provided. The viability and unviability of the

operations have been discussed in detail in the unitwise report, however,

summary of the same is given below:

Unitwise Summary Plan

S. No. Unit Name Remarks 1 Banmankhi Can be expanded to 2500 TCPD + 60 KLPD distillery +

12 MW Co-Gen plant with an additional investment of Rs. 164 crore approximately. However, it is felt that since there is no sugar mill in the close vicinity, therefore cane growing area suitably be allocated to take care of the future expansions. The unit also has a farm land area of 55 acres which may also be given alongwith the transfer of unit. The colony land may be allowed to be converted into factory land for immediate or future expansions. The adjacent farm land, if any, may be allowed to be used as factory land. There is no sugar unit in the vicinity and therefore it is proposed that GoB shall allocated a can growing area based on the proposed investment plans of the potential investor which may even be sufficient to cater to the integrated sugar complex with a capacity of 10000 TCPD.

2 Bihta The unit is located about 35 kms from Patna. The plant was installed in 1938 and condition of the plant is dilapidated. No substantial expansion is possible since

Private &Confidential Viability Report

SBI Capital Markets Ltd. 27

land area including colony is only 24 acres only, which is located in the town area. The unit may be used for other industrial/ commercial purposes. A Greenfield plant may be considered in the farm land (located at Jinneswargarh) based on the availability of sugarcane in the area.

3 Goraul A juice based distillery of 90 klpd can be planned taking into account the milling capacity of the existing plant for which a boiler, TG and a distillery will have to be installed. The estimated cost of the project would be around Rs. 140 crore. The unit also has a farm land area of around 6.83 acres which may also be given alongwith the transfer of unit. The colony land may be allowed to be converted into factory land for immediate or future expansions. The adjacent farm land, if any, may be allowed to be used as factory land.

4 Guraru The plant is very old and of small capacity. It is also in poor condition and cannot be expanded in a small area and can be explored for alternative commercial / industrial uses.

5 Hathua & Hathua Distillery

Located in Gopalganj district, where three private sugar mills are operating with a total capacity of 9700 TCPD. The unit may be expanded to 2500 TCPD alongwith 12 MW Co-gen plant. Hathua distillery of 60 KLPD may be used for production of alcohol/ ethanol out of the juice produced from Hathua unit. The estimated cost of the unit would be Rs. 164 crore approximately. The attachment of Hathua distillery with Hathua sugar unit will improve the viability and thereby investors’ interest. The unit also has a farm land area of around 10 acres which may also be given alongwith the transfer of unit. The colony land may be allowed to be converted into factory land for immediate or future expansions. The adjacent farm land, if any, may be allowed to be used as factory land. As indicated above, GoB can allocate the maximum

Private &Confidential Viability Report

SBI Capital Markets Ltd. 28

possible cane growing area to this unit taking into account the requirement of existing units and their expansion plans, if any.

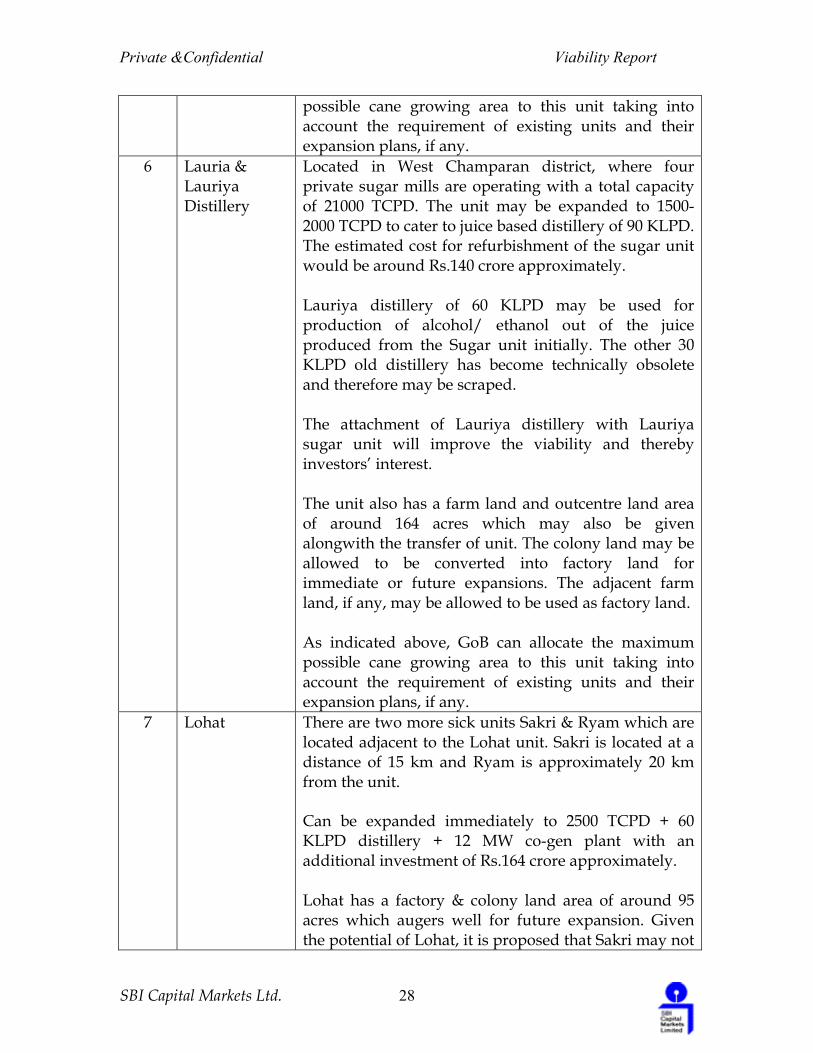

6 Lauria & Lauriya Distillery

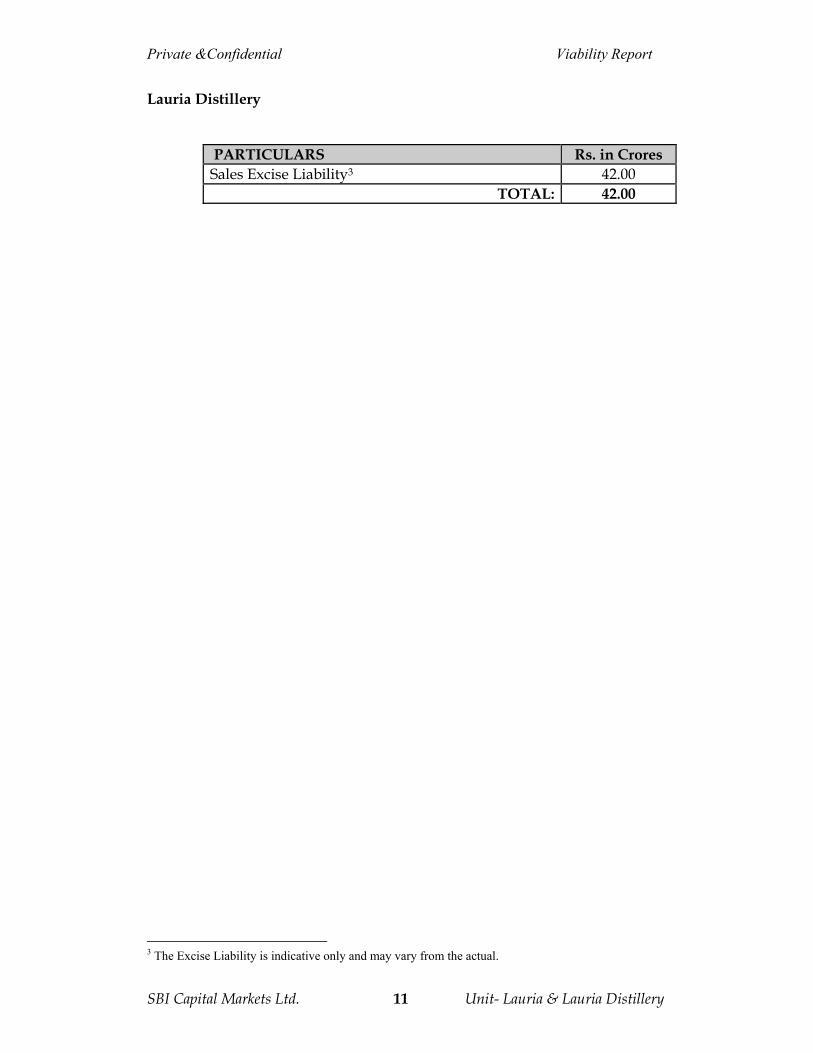

Located in West Champaran district, where four private sugar mills are operating with a total capacity of 21000 TCPD. The unit may be expanded to 1500- 2000 TCPD to cater to juice based distillery of 90 KLPD. The estimated cost for refurbishment of the sugar unit would be around Rs.140 crore approximately. Lauriya distillery of 60 KLPD may be used for production of alcohol/ ethanol out of the juice produced from the Sugar unit initially. The other 30 KLPD old distillery has become technically obsolete and therefore may be scraped. The attachment of Lauriya distillery with Lauriya sugar unit will improve the viability and thereby investors’ interest. The unit also has a farm land and outcentre land area of around 164 acres which may also be given alongwith the transfer of unit. The colony land may be allowed to be converted into factory land for immediate or future expansions. The adjacent farm land, if any, may be allowed to be used as factory land. As indicated above, GoB can allocate the maximum possible cane growing area to this unit taking into account the requirement of existing units and their expansion plans, if any.

7 Lohat There are two more sick units Sakri & Ryam which are located adjacent to the Lohat unit. Sakri is located at a distance of 15 km and Ryam is approximately 20 km from the unit. Can be expanded immediately to 2500 TCPD + 60 KLPD distillery + 12 MW co-gen plant with an additional investment of Rs.164 crore approximately. Lohat has a factory & colony land area of around 95 acres which augers well for future expansion. Given the potential of Lohat, it is proposed that Sakri may not

Private &Confidential Viability Report

SBI Capital Markets Ltd. 29

be revived for sugarcane based industry, which is aunit in the vicinity. Therefore cane growing area be suitably allocated to take care of the future expansions of capacity of the mill. The unit also has a farm land area of 115 acres which may also be given alongwith the transfer of unit. The colony land may be allowed to be converted into factory land for immediate or future expansions. The adjacent farm land, if any, may be allowed to be used as factory land.

8 Motipur Can be expanded immediately to 2500 TCPD + 60 KLPD distillery + 12 MW co-generation plant with an additional investment of Rs. 164 crore approximately. Motipur has a factory & colony land area of around 66 acres which augers well for future expansion and accordingly cane growing area be suitably allocated. The unit also has a farm land area of 1297 acres out of which 300 acres may be given along with the transfer of unit. The colony land may be allowed to be converted into factory land for immediate or future expansions. The adjacent farm land, if any, may be allowed to be used as factory land.

9 New Siwan The unit is inside the town of New Siwan. Transport of cane through the township is difficult. The unit can be used for other commercial / industrial purposes.

10 Ryam Ryam has a land area of around 26 acre which is very small and possibility of reviving may be difficult since Lohat unit, having better potential for revival is in close proximity. The unit can be used for other commercial / industrial purposes. However if there is no potential bidder for Lohat, Ryam may be looked for revival.

11 Sakri The unit is inside the town of Sakri and is near to Lohat (which has a bigger potential of revival). Thus while Lohat may be revived, Sakri may not be used as Sugar unit. The unit can be used for other commercial /

Private &Confidential Viability Report

SBI Capital Markets Ltd. 30

industrial purposes.

12 Samastipur The unit is inside the town of Samastipur. Transport of cane through the township is difficult. The unit can be used for other commercial / industrial purposes.

13 Siwan The unit is inside the town of Siwan. Transport of cane through the township is difficult. The unit can be used for other commercial / industrial purposes.

14 Suguali Located in East Champaran district with a land area of 82 acres and farm land area of around 319 acres. Can be expanded immediately to 1500 TCPD + 90 KLPD distillery + 7 MW co-generation plant with an additional investment of Rs. 140 crore approximately. Suitable cane growing area be allocated to take care of the units requirement. The farm land of 200 acres out of 319 acres may also be given alongwith the transfer of unit. The colony land may be allowed to be converted into factory land for immediate or future expansions. The adjacent farm land, if any, may be allowed to be used as factory land.

15 Warisaliganj Can be expanded immediately to 1500 TCPD + 90 KLPD distillery + 7 MW co-generation plant with an additional investment of Rs. 140 crore approximately. The unit also has a farm land area of 36 acres which may also be given alongwith the transfer of unit. The colony land may be allowed to be converted into factory land for immediate or future expansions. The adjacent farm land, if any, may be allowed to be used as factory land.

Note : 1) The above estimated cost has been worked out considering the usable plant & machinery of the respective unit. The actual investment may differ from the suggested investment based on the capacities ad configuration of machinery, as per the plan of the new investor. Thus the costs are only indicative in nature. 2) It is proposed that Farm Land which is not given to the Investor along with the unit may be used by the Government for some other industrial or agricultural purpose. Alternatively the GoB may decide to allocate the entire farm Land and outcentre Land to the investor along with the units which have been proposed viable for sugarcane based industry.

Private &Confidential Viability Report

SBI Capital Markets Ltd. 31

7 Appropriate Transfer Model

7.1 Mode of Transfer

The Government had acquired the units to protect the labor and cane growers

from hardship, which they were facing due to units not doing well during those

times. The acquisition was primarily oriented at ensuring continued production

of sugar and other goods, safeguard the interest of the sugarcane farmers and

laborers engaged therein. Therefore, any transfer model shall primarily ensure

the well being of cane growers as also the labours. The various transfer models

has been discussed hereunder:

The units can be transferred to the successful bidder in three possible ways.

i. Outright Sale of the Unit

The first option of outright Sale of the unit may invite litigation as the purpose of

the Government at the time of acquisition was revival of the units and thereby

outright sale of the units to private owners may lead to difficulty in transfer.

ii. Public Private Partnership (PPP)

While Public private partnership has been successful in infrastructure sector, in

manufacturing sector, the investors generally like to run the unit free from any

possible external interferences. Secondly, accepting the shareholding by carving

out a unit under PPP model would also tantamount to sale (equity holding of

BSSC in JV Company being consideration for land, building and Plant &

machinery) and may lead to legal hurdles. In addition to the above, conversion

for the value assets into equity may not bring direct cash flow which would be

required for settlement of some of the liabilities.

Private &Confidential Viability Report

SBI Capital Markets Ltd. 32

iii. Long Term Lease of the Unit

In case of opting for long term lease the ultimate ownership of the Land

remains with the BSSC/Government. Again the investors may also benefit for

having access to land with adequate infrastructure for sugar mill/ industrial

production. The Government has right and option to renew the Lease after

the Lease period.

In view of the above, it is proposed to adopt the Lease Model for successfully

transferring the assets for smooth revival of the units.

7.2 Rationale of Leasing Model

a) GoB will be the actual owner of the land, and its only the right of use is

being transferred to the investor on lease basis.

b) In an event when the Investors have not been able to implement the

project in specified time then the GoB would reserve the right to take back the

unit after providing adequate time and paying adequate compensation.

c) The lease model would avoid the possible litigations as indicated above.

d) The Lease model shall be adopted for sugarcane based industries in case of

revival or else the Land would be leased out for commercial or industrial

activity.

7.3 Lease Period for Land

A lease period of 60 years (further renewable for 30 years) is being proposed

for the consideration of GoB. The above lease period is being proposed

because of the following reasons:

a) It has become generally accepted norm of offering lease of land on Long

Term basis to provide continuity.

Private &Confidential Viability Report

SBI Capital Markets Ltd. 33

b) Long term lease provides a comfort to the lenders’ community for purpose

of creating mortgages.

c) Investment in manufacturing sector is generally made with a long term

horizon. Once substantial investment has been made, the investors’ needs

longer period to get adequate return on the investment. If the lease period is

short, long term investment may not be viable for the investor. Thus a long

term lease may be more attractive to the investor for considering substantial

investment in the unit.

d) Discussions were carried out with the prospective investors who had

earlier shown interest in investing in sugar sector in the state, and they were

comfortable only on outright sale basis, and thus it is felt that any lesser

period of Lease may not attract potential bidders for Long Term investment

in the state.

It may be mentioned that farm land attached to the unit have not been offered in the

bid process management. In order to enhance the attractiveness of the bid process, it

may be recommended to allot a portion of farm land preferably as suggested in the

table below to the potential investors in sugarcane based industry only the prices for

which has not been considered in the fair value. The farm land would be allotted on

lease basis for the similar period of 60 years and would be utilized only for the sugar

industry. The balance farm land may be utilized by Government of Bihar for other

agricultural/ industrial/ commercial purpose.

Private &Confidential Viability Report

SBI Capital Markets Ltd. 34

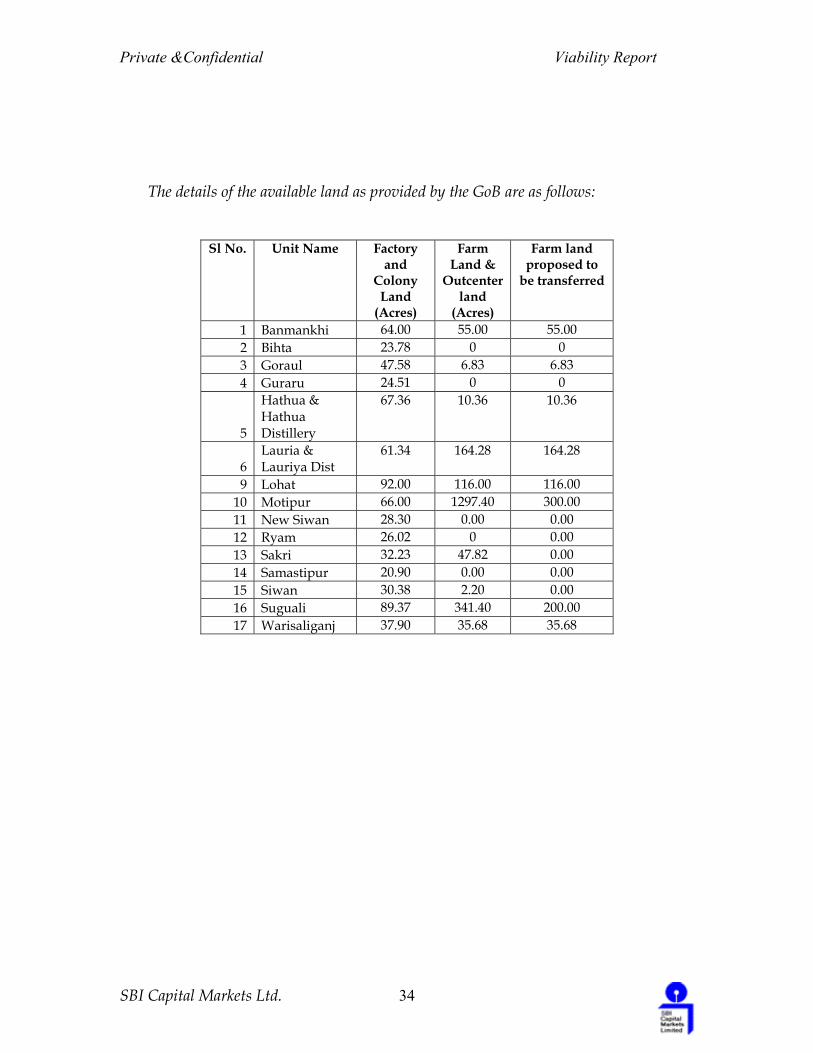

The details of the available land as provided by the GoB are as follows:

Sl No. Unit Name Factory and

Colony Land

(Acres)

Farm Land &

Outcenter land

(Acres)

Farm land proposed to

be transferred

1 Banmankhi 64.00 55.00 55.00 2 Bihta 23.78 0 0 3 Goraul 47.58 6.83 6.83 4 Guraru 24.51 0 0

5

Hathua & Hathua Distillery

67.36 10.36 10.36

6 Lauria & Lauriya Dist

61.34 164.28 164.28

9 Lohat 92.00 116.00 116.00 10 Motipur 66.00 1297.40 300.00 11 New Siwan 28.30 0.00 0.00 12 Ryam 26.02 0 0.00 13 Sakri 32.23 47.82 0.00 14 Samastipur 20.90 0.00 0.00 15 Siwan 30.38 2.20 0.00 16 Suguali 89.37 341.40 200.00 17 Warisaliganj 37.90 35.68 35.68

Private &Confidential Viability Report

SBI Capital Markets Ltd. 35

8 Valuation & Fair Value

8.1 Valuation

The valuation of a unit is normally done on running concern basis or fair value of

the assets. All the units of BSSC are inoperative and therefore the basis of

valuation have broadly been fair value of the assets. Valuation of both land and

plant & machinery have been done by the independent valuers and the land

valuation has been done based on both market and government rates while the

valuation of plant & machinery have been done based on the usable and scrap

value of equipment.

a) Land : Land have been valued at both market rates as also based on the

government rates. Generally, it has been observed that value as per market rate

have been more than that as per government rate and that the aggregate market

value for all the 17 units is more than the aggregate government value.

b) Plant & Machinery: An effort has been made to segregate plant & machinery

into usable and scrap items and accordingly have been valued by the

independent Chartered Engineer. The valuation report has been provided in the

unitwise reports.

8.2 Fair Value

Sugar industry in India is facing a downturn cycle due to steep fall in prices of

sugar. Further in Bihar, the cane growers have shifted to alternate crops and

although are keen to see the revival of these units to cash on this cash crop viz.

sugarcane, but at the same time are jittery as the units have remained closed for

long. From the point of view of investors, they would need to create the complete

Private &Confidential Viability Report

SBI Capital Markets Ltd. 36

infrastructure for running the sugar mill successfully, which would include right

from starting of development of sugarcane cultivation to ensure the availability

of sugarcane required for the mill.

In light of the above backdrop, it is felt that attracting the investor in the current

industry scenario would be difficult unless some attractive pricing structure is

framed for luring the investments in the State so that the deal becomes attractive

for the prospective investors.

The basis of arriving at Fair Value that may be considered during Bid

evaluation process has been separately discussed and suggested.

Private &Confidential Viability Report

SBI Capital Markets Ltd. 37

9 Settlement Process, Sacrifice & Utilisation of the Proceeds

9.1 Settlement process

The settlement process is based on the fact that the new investors would be

interested only if the units are handed over to him free from all encumbrances

and liabilities settled before the units are actually handed over. The annual

reports of the units (internal audit) have been analysed and it has been observed

that all possible liabilities as prevalent in any closed unit are there. However, for

the purpose of settlement of liabilities of these units, we have considered labour

and secured liabilities (bank dues) as the basic liabilities which are expected to be

settled out of the bid proceeds. Apart from the labour and secured liabilities

(bank dues) all other liabilities would either be waived or settled by GoB.

Further, government would indemnify the potential investor of all such liabilities

which may accrue in future as a result of takeover.

It may be mentioned that while the Land has been proposed to be offered on Long term

Lease, the ownership for Plant and Machinery including scrap is to transferred to the

Investors who would have right to sale or use the same as per their convenience.

9.2 Sacrifices

As indicated above, not all the liabilities can be met out of proceeds and therefore

certain liabilities have to be waived or met by GoB. The liabilities which have

been identified and is expected to come up in course of revival is given in the

table below. Besides certain other unidentified liabilities may also arise because

of certain court decrees or other reasons, which would also need to be settled by

GoB.

Private &Confidential Viability Report

SBI Capital Markets Ltd. 38

The liabilities which are to be settled and the mode of settlement /sacrifice are as

follows:

SL.

No.

Nature of

Liability

Settlement

Process

Reasons/Remarks Possible

Problems

1. Labour Dues

To be settled out

of the bid

realization

proceeds

The claims of labour

including settlement

claims need to be

satisfied before

transferring the units

to the investors for

smooth transition of

the revival package.

In case shortfall

from the

proceeds, the full

settlement may

not take place

and thereafter,

GoB has to settle

the liabilities.

2. Payment

arising due to

Court Order

May be settled

out of the

remaining

surplus

(Proceeds-1)

The amount is

contingent upon award

of any compensation to

any aggrieved party by

Court of Law and

therefore the amount

cannot be estimated

currently.

In case the

amount cannot

be paid out of

the surplus, the

same has to be

settled by GoB.

3. Secured

Loans

To be settled out

of the remaining

(Proceeds -1-2)

The secured loans are

generally from

Banks/SDF/Co-

Operative Banks who

have charge on the

assets of the unit.

In case of

shortfall, the

Government has

to settle the

liability.

4. Cane

Growers

Settled/in the

process of

As per the information

provided to us, the

No difficulty

envisaged

Private &Confidential Viability Report

SBI Capital Markets Ltd. 39

Dues settlement by

GoB

same has been settled

by GoB.

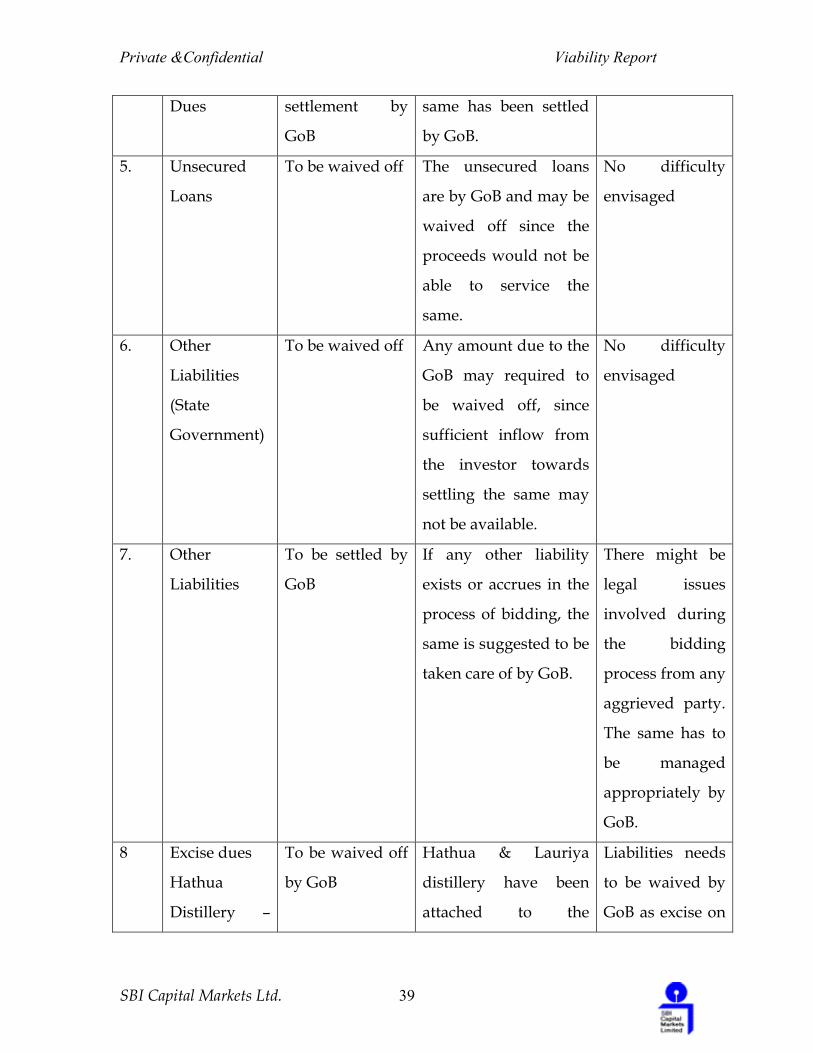

5. Unsecured

Loans

To be waived off The unsecured loans

are by GoB and may be

waived off since the

proceeds would not be

able to service the

same.

No difficulty

envisaged

6. Other

Liabilities

(State

Government)

To be waived off Any amount due to the

GoB may required to

be waived off, since

sufficient inflow from

the investor towards

settling the same may

not be available.

No difficulty

envisaged

7. Other

Liabilities

To be settled by

GoB

If any other liability

exists or accrues in the

process of bidding, the

same is suggested to be

taken care of by GoB.

There might be

legal issues

involved during

the bidding

process from any

aggrieved party.

The same has to

be managed

appropriately by

GoB.

8 Excise dues

Hathua

Distillery –

To be waived off

by GoB

Hathua & Lauriya

distillery have been

attached to the

Liabilities needs

to be waived by

GoB as excise on

Private &Confidential Viability Report

SBI Capital Markets Ltd. 40

Rs.64.72 crore

and Lauriya

Dstillery – Rs.

42 crore

respective units in the

bidding process and

therefore settlement of

excise liabilities is

important without

which Hathua and

Lauriya units could not

be put on bidding

process.

distillary is a

state subject.

9.3 Utilisation

Once the bid price is decided (of the possible alternatives provided separately)

by the appropriate authority, the same may be considered as the Reserve Price

for the unit in the Bid documents.

However the proceeds from the above may not be able to satisfy the entire

liabilities of the units and it is proposed that the proceeds may be utilized for the

following priority payments:

a. Settlement of Labor Liabilities including compulsory retirement.

b. Settlement of Bank/SDF dues to the extent of principal amount

only.

c. Settlement of dues for any claim for which Court may/has ordered

for payment of any specific amount or guided any method of

calculation for payment of such amount.

Private &Confidential Viability Report

SBI Capital Markets Ltd. 41

However, in an event where the proceeds from the bidding is lower than the

above claims, the Government has to make necessary arrangement for settlement

of the above dues. The liabilities shall not be transferred to the asset transferee.

Private &Confidential Viability Report

SBI Capital Markets Ltd. 42

10 Litigations and Settlements

10.1 Litigations

An effort was made by the Legal Counsel to identify the legal cases pending

against Bihar State Sugar Corporation/ GoB with respect of the above units,

which have been mentioned in the reports of individual units. Apart from those

there are certain other major legal cases, which has the propensity to adversely

affect the entire revival process. The legal opinion on these cases is detailed as

under:

i. Settlement of Labour Issues

As per section 11(2) of Bihar Sugar Undertakings Acquisition Act, 1985 all

persons who were workmen within the meaning of Industrial Disputes Act, 1947

engaged under the scheduled undertakings on or before 29.10.1978 became

employee of the State Sugar Corporation and there services legally deemed to be

continued without any break.

It may be worthwhile to mention that any investor would be interested to invest

only if the units are offered to him free from all encumbrances, litigations as also

the liabilities (including labour liabilities).

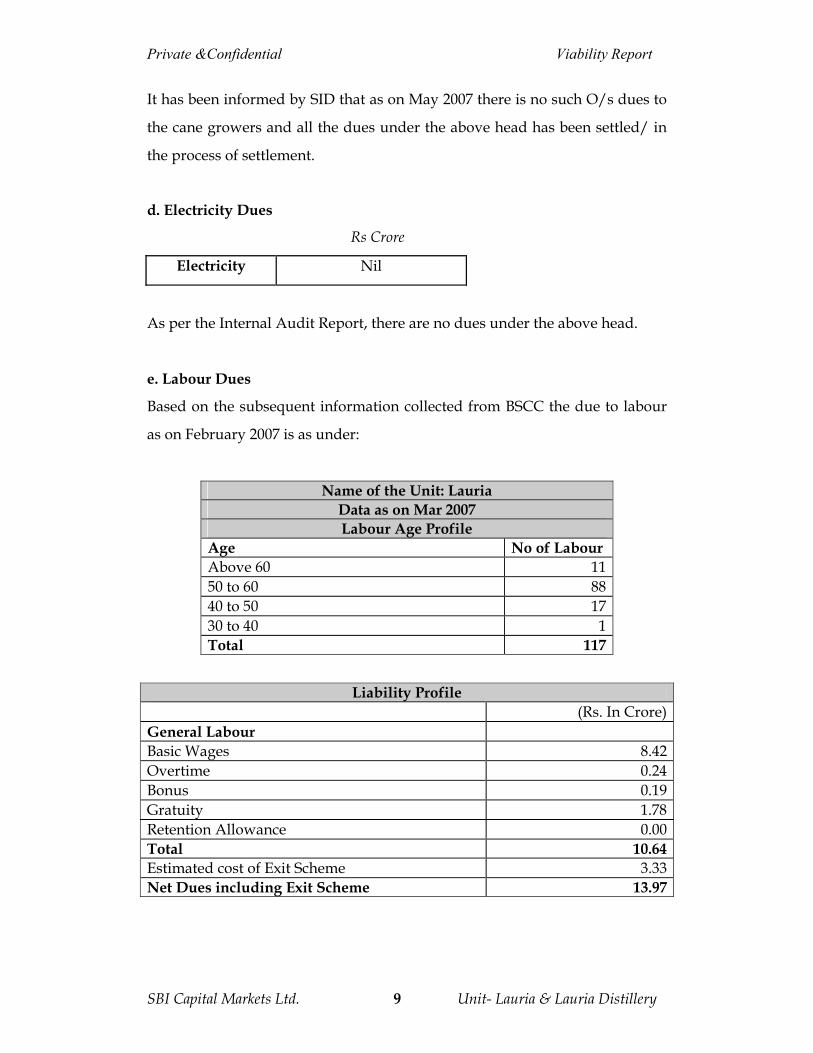

The units of BSSC (excluding the two distilleries) employs 1574 labours/ staffs/

officers as on February 2007. The unitwise labour liabilities both in terms of

arrears as also the settlement (based on 15 days for each completed year of

service and 45 days for the remaining service period) has been provided by the

officials of the respective units. It may be mentioned that the settlement terms

Private &Confidential Viability Report

SBI Capital Markets Ltd. 43

was based as per the provisions of Section 25F of the Industrial Disputes Act,

1947.

ii. Settlement of Pending Suits

It has been observed that majority of the pending legal cases are from aggrieved

labors for payment of their dues. The same would be settled once the proceeds

from the bids are allocated towards settling their dues. As per the legal opinion

the above type of issues would not be affecting the transfer process. The unit

wise litigation cases has been separately discussed in the unitwise reports and

more specifically provided in the report submitted by the Legal Counsel and

provided hereto. Besides certain erstwhile owners have also filed suit against the

GoB.

iii) Excise Matter

Excise on distillery is a state subject payable to the department of excise, GoB and

therefore the GoB can very well fix a moratorium, waive or otherwise deal with

these dues.

Private &Confidential Viability Report

SBI Capital Markets Ltd. 44

11 Suggested Plan of Action

a) The model suggested in this report is required to be approved by

appropriate authority of GoB, with/without suggestions/ modifications.

Thereafter, permission from the High Court is required to be taken since

Liquidation petition is pending before the Honorable Court.

b) Legal opinion regarding Winding up Petition Already Filed:

“Since no winding up order is yet been passed and no Official Liquidator is

appointed, it is within the powers of the corporation to file application for

closure and / or negotiate the matter with the concerned parties. But once

winding up order is passed and Official Liquidator is appointed then nothing

can be done unless consented and permitted by the Company Judge.

However as the Hon’be Company Judge is in the seisin of the matter, the

Court should be apprised about all the steps including unit wise bidding and

order be obtained so that the winding up petition remain pending in the

court”

Private &Confidential Viability Report

SBI Capital Markets Ltd. 45

12 Tendering/Bidding Process

Once the plan is approved by Honorable High Court, bids shall be invited from

various parties for Long Term Lease of the units. The investors shall have the

right to utilise/sell the existing plant and machineries to their satisfaction. The

investor would not have right to sell the land. The investor would however be

allowed to mortgage the land and other assets to its lenders for arranging debt

for the unit.

The Tendering Process shall be as follows:

a. An advertisement will be issued by GoB in major dailies with regard to

the proposed Revival package and asking the potential bidders for about

the package and units being offered.

b. The Bid documents shall also be uploaded on Government of Bihar

website.

c. The bidders shall be given a time period of 30 days for submission of the

Bid.

d. The Bid selection criteria shall be described in the Bid documents.

e. The successful Bidder has to submit a Bank Guarantee for the balance bid

proceeds at the time of execution of transfer agreements.

Private &Confidential Viability Report

SBI Capital Markets Ltd. 46

13 Selection Criteria

The Bidding shall be carried out in two separate parameters

i. Technical Bid

ii. Financial Bid

The eligibility of the technical part shall be the first stage of selection. The basis

of selection of Technical Bid has been enumerated in the table below.

SL No. Criteria Legend Weightage (%)

1. Group turnover <25 Crore-0

Rs. 25-100 Crore-5

>Rs.100 Crores-10

20%

2. PBT of the Group <1 Crore-0

Rs. 1-10 Crore-5

>Rs. 10 Crores-10

15%

3. Net worth of the

Group

<50 Crore-0

Rs.50-100 Crore-5

>Rs.100 Crores-10

20%

4. Proposed Total

Investment #

<Rs25 Crores-0

Rs.25-50 Crores-2.5

Rs. 50-100 Crores-5

Rs.100-150 Crores-7.5

>Rs. 150 Crores-10

20%

5. Management

Capability

Experience in Sugar

Manufacturing=> 3 Years-10

Experience in other

Manufacturing Sector=>5

years-10

Business experience in Other

15%

Private &Confidential Viability Report

SBI Capital Markets Ltd. 47

than manufacturing Sector

>10 Years -10

None-0

6. Proposal for

setting up sugar

unit in Bihar

already approved

by GoB

Yes – 10

No – 0

10%

# Performance guarantee of 5% of the investment amount as indicated in the bid documents to be furnished at the time of execution of transfer agreements. The guarantee will be released once the 80% of the investment proposed is made and the unit becomes operational.

The Minimum selection Criteria value shall be 3.75 based on the selection criteria

above. However in case the same is not met by sufficient number of bidders, the

minimum selection base may be further relaxed after analyzing the quality of the

bids received.

Once the Bidder is selected on the above criteria, the H1 Bidder shall be selected

based on the Highest Bid Value. The names of H2 and H3 Bidders shall also be

announced and in case of non-performance of the obligations of H1 bidder for

payment of fees, the units would be offered to the next highest bidder. However,

in case there is a tie in the financial bids then bidder with highest score in

technical evaluation will be declared as the winner.

The Bidders shall also have to submit Earnest Money Deposit of Rs.10 lakh with

their bids. The EMD of the unsuccessful Bidders shall be released after the

announcement of the H1, H2 and H3 Bidders. The EMD of H2 and H3 would be

released after part payment by H1 in a specified time. In case H1 has failed the

payment of the Bid value, the unit would be automatically allotted to H2 at a

Private &Confidential Viability Report

SBI Capital Markets Ltd. 48

price of H1 and EMD of H1 shall be forfeited. Similarly H3 will be considered in

case H2 fails under the bid process management.

The successful bidder would have to arrange for Bank guarantee for the unpaid

bid amount, before the documentation of the handing over of units. The signing

of lease/transfer documents would complete the process.

However in case of failure on payment by all the three Bidders above, GoB may

take appropriate decision.

Private &Confidential Viability Report

SBI Capital Markets Ltd. 49

14 Transfer Process

The transfer of units to be done through the following process:

a. The Bihar State Sugar Corporation/GoB shall enter into a Lease

Agreement of the unit with the Investor for a period of 60 Years to be

renewed further for 30 years.

b. The Lease Deed shall provide for Government consent for subleasing the

Land. However the initial lock in period shall be 20 years before which the

Land cannot be transferred to any other party other than to the GoB.

c. Lease deed shall provide mortgageable rights.

d. The Investor shall make the payment of the Bid amount as per follows:

Sl No. Stage % Payment Payment Time Line

1. At the time of award

of selection

10% of the Bid

Value

Payment to be made within

one month from the date of

such award

2. At the time of Signing

of the Transfer

Agreement

40% of the Bid

Value

Payment to be made on the

day of signing the Transfer

Documents

3. After 1 year from the

signing of the

Transfer Agreements

25% of the Bid

Value

To be made on the 13th

month of the signing of the

Transfer Agreements

4. After 2 years from

signing of the

Transfer Agreements

25% of the Bid

Value

To be made in the 24th

month of the signing of the

Transfer Agreement

The investor shall be required to submit a Bank Guarantee to the extent of

balance amount of the Bid value to GoB (i.e. 50%) at the time of signing of

Transfer Agreement. The BG shall be released proportionately at the time of

payment of the balance Bid amount as per the above schedule.

Private &Confidential Viability Report

SBI Capital Markets Ltd. 50

e. The Labour liabilities for each unit shall be settled by the proceeds from

the Bid amount. The payment may be structured in a phased manner

based on the receipt of the proceeds. However an agreement to this effect

has to be entered with the Labour Unions by the GoB whereby the

Government has to undertake the payment as per a specified schedule.

f. Depending on the success of Bids, the units for which investors are not

interested may be suitably used for some other commercial / industrial

purposes.

g. GoB may decide on identifying a nodal agency for assisting the units,

collection of lease premium and appropriating the same towards payment

of the liabilities.

h. The Government may consider to dispose of the assets of the units for

which no interest is being received from investors and may Lease the

Land for alternate commercial/ industrial / any other purposes.

i. GoB shall indemnify the potential investor for losses incurred in the event

of transfer process not being successful even after the investor meeting his

obligations in entirety. Further, GoB shall indemnify any unidentified

liabilities / events which may tend to disrupt the implementation/

operations of the unit.

j. GoB shall transfer the unit free from all encumberances to the successful

bidder within 3 months from the date of award of the unit and the initial

payment received by GoB, failing which GoB will have to pay an interest

of 15% p.a. for next 3 months on the amounts received from the investor.

If GoB fails to handover the unit in the above six months then either with

mutual agreement the time frame for handing over the land can be

extended or GoB shall refund the amount alongwith interest to the

investor.

Private &Confidential Viability Report

SBI Capital Markets Ltd. 51

15 Suggestions for additional incentives for inclusion in Sugar Policy

Sugar industry has been a politically sensitive industry and governmental

intervention is frequent to control on the supply as well as the prices of sugar. It

is evident that sugar industry in Bihar is lagging both in sugarcane cultivation as

also the yield because of which there has not been any substantial investment in

the recent past. Further, governmental support to promote the sugar industry in

the state was also not very visible so far. As a result, canegrowers have shifted to

alternate crop making the things more difficult for the government. It is therefore

advised to formulate a comprehensive sugarcane policy to exploit the sugarcane

growing potential of the state as also to promote the industrial development in

the state. The revival of closed sugar mills is a step in the right direction.

However, these units are closed for more than a decade and a substantial

support /concessions would need to be granted to these units to see the effective

revival of the units. It is therefore suggested that the following measures may be

considered by GoB for an overall inclusive growth and attract Investors in the

state on the continuous basis :

i. Decontrol of Molasses: Considering a downturn in Sugar Industry, the

investors shall be considering economically viable alternatives for

sustainable growth. The control on sale of molasses might act as a

hinderance to the independent sugar producing units. The

Government may approve decontrol of molasses produced by sugar

mills. Further free sale of molasses produced in the state to any other

state should be allowed. The Alcohol manufactured in the state should

also be permitted to be exported outside the state.

ii. Decontrol of Bagasse Disposal: The Baggase Disposal Policy may be

suitably framed to allow the companies to sale the Bagasse

Private &Confidential Viability Report

SBI Capital Markets Ltd. 52

interstate/intrastate without any control. Again the same should also

be free from any trade tax.

iii. Capital Subsidy: Presently the Government is providing 10% subsidy

on plant and Machinery subject to a maximum of Rs. 10.00 crores. To

attract bigger investment the maximum ceiling should be removed and

the subsidy may be 10% of the Plant and Machinery.

iv. For captive power plant/cogen, the current capital incentive is to the

extent of 10% which may be increased to 50% as per the present

industrial policy.

v. The State Electricity Board has to enter into a firm PPA with Co-

generation owners for excess sale. The payment mechanism may be

guaranteed by the Government of Bihar for generating interest and

better security mechanism i.e. By way of revolving Letter of Credits

which is generally followed by most of the states.

vi. Permission should be granted to sugar mills to manufacture

alcohol/ethanol from cane juice directly at the choice of manufacturer.

vii. The government may formulate proper policy for enhancing irrigation

support to the farmers by providing subsidies and equipment.

viii. It is highly recommended that the Government should provide

commitment to the investors by allocating an area of minimum 30 km

of radius directly to the new sugar unit and restriction on setting of

any other new unit in the designated area. The same is required to be

announced in the Bid document and at the time of tender process to

elicit interest from the investors.

Private &Confidential Viability Report

SBI Capital Markets Ltd. 53

16 Recommendations

Based on the analysis indicated above, it is proposed that GoB may approve the

following:

1. Revival plan for units and suggested course of action.

2. GoB shall approve the reserve price and Bid criteria as also the Bid Process

Management.

3. GoB shall approve the estimated cost of revival scheme and means of finance

and shall agree to fund the deficit, if any from its own sources.

4. GoB shall agree to indemnify the investor against all the present and future

liabilities which may arise out of these units in course of revival process.

5. GoB shall agree to transfer the land within 3 months failing which it would

pay interest for next 3 months @ 15% p.a. and further extension would be only

with mutual consent.

6. GoB shall waive all the unsecured loans owed by the unit and shall also agree

to settle / waive excise liabilities, sales tax, any other tax liabilities and other

liabilities.

7. GoB shall settle all the labour issues and litigations related to labour as also

other issues. Any further liability arising out of these settlements shall also be

borne by GoB directly.

8. GoB shall allow conversion of residential and colony Land for industrial

purpose and in case farm land is attached, the farm Land to be used for factory

purpose.

8. GoB shall assure the investors that they would be given single window

clearance as is being done presently by few other State Governments including

Central government in case of Ultra Mega Power Project.

9. GoB shall ensure infrastructural support to the units viz. flood control, roads,

power, irrigation and other related issues as present or support for any other

Private &Confidential Viability Report

SBI Capital Markets Ltd. 54

such issues which may hinder the implementation process as also the operations

of the unit.

10. GoB shall agree to lease the land for a period of 60 years (further renewable

for 30 years) and attach the farm land to the concerned unit as suggested above,

the price of which does not form part of the bid price. Incidentally, the farm land

so attached would also be on lease basis, the usage of which would be restricted

to sugarcane based industry including setting of the Greenfield unit (sugarcane

based).

11. GoB may consider providing exemptions/ incentives etc as indicated above

in the note and such exemptions shall be continued on continuous basis.

12. It is proposed to provide suitable approving powers to Industrial

Development Commissioner or any other appropriate authority for approving

various documents relating to the Bid process Management such as Tendering,

Request for Qualification, Lease Agreement and other Transfer Agreements

including modifications in the Bid process criteria and any other Act which may

be necessary for smooth revival of the units.

BANMANKHI

TABLE OF CONTENTS

1. BRIEF BACKGROUND .................................................................................................. 2

2. LOCATIONAL MAP : BANMANKHI, DISTRICT- PURNIA, BIHAR ................... 3

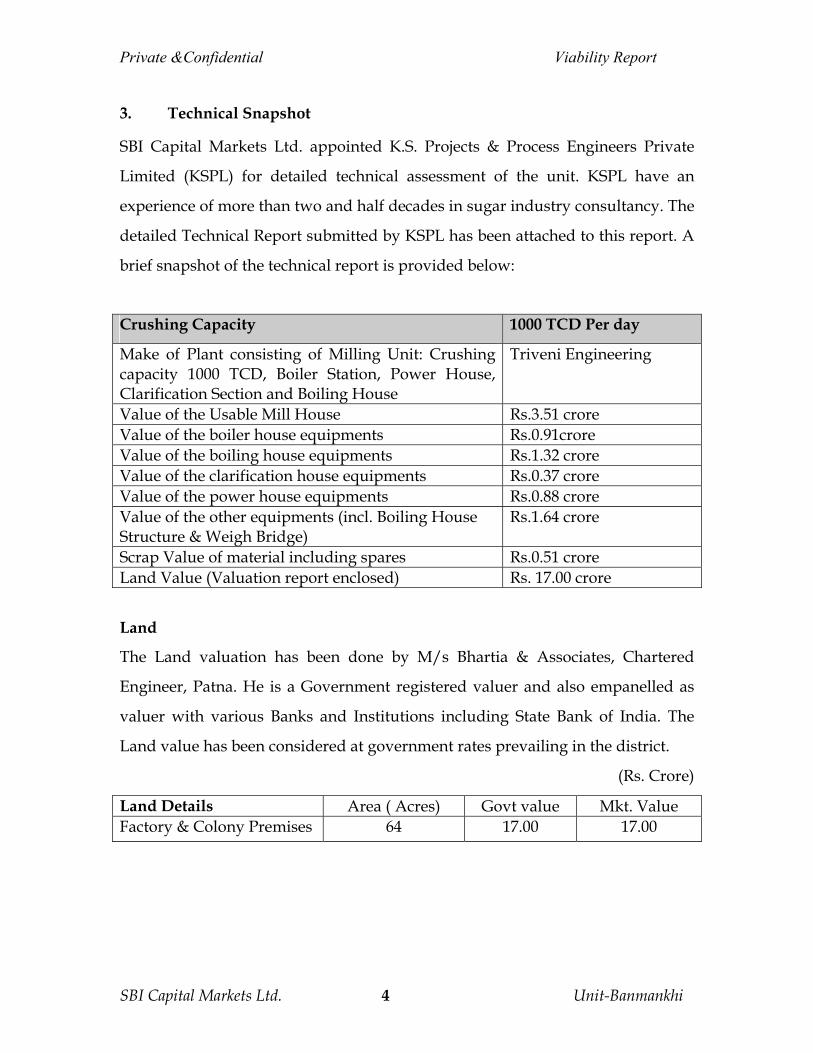

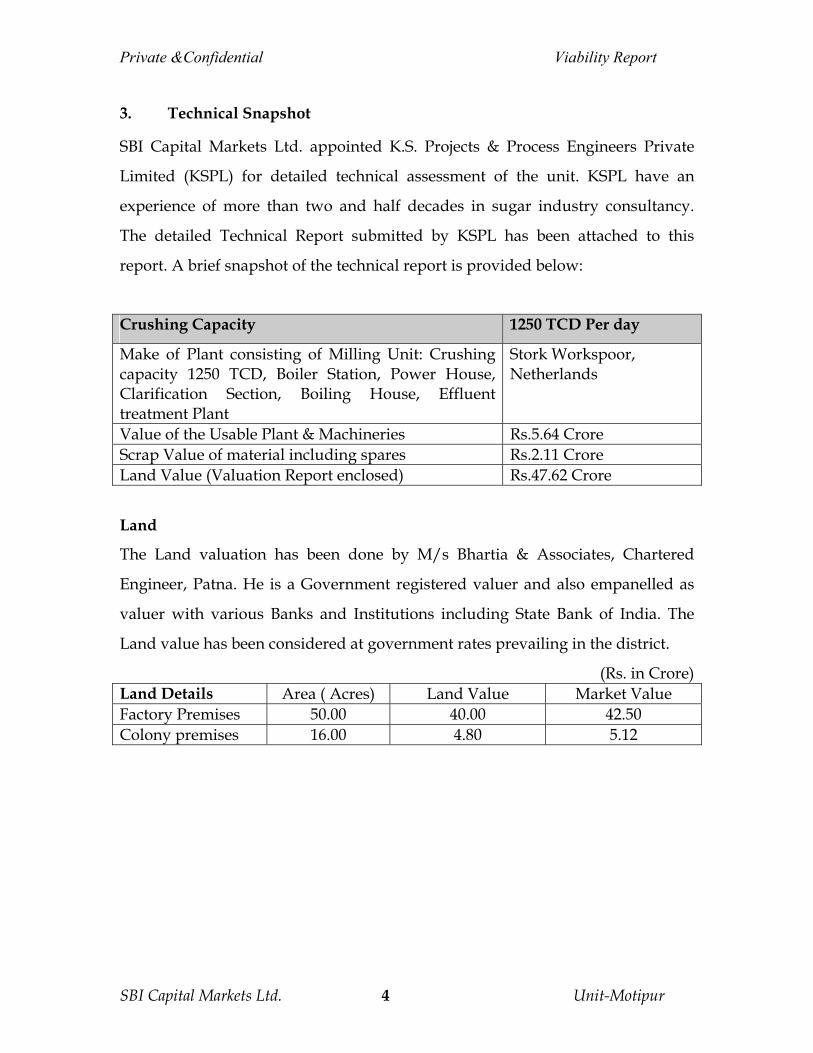

3. TECHNICAL SNAPSHOT............................................................................................. 4

4. FINANCIAL POSITION................................................................................................. 5

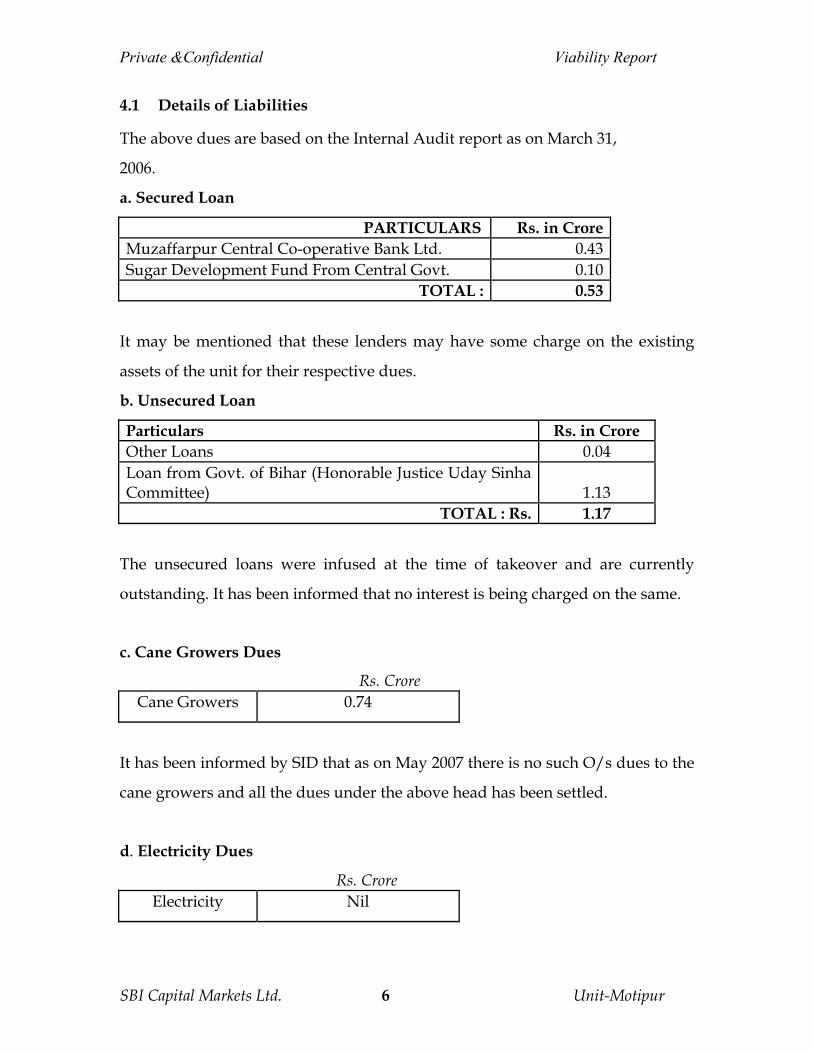

4.1 Details of Liabilities......................................................................................................... 6

5. PROPOSED REVIVAL PLAN........................................................................................ 9

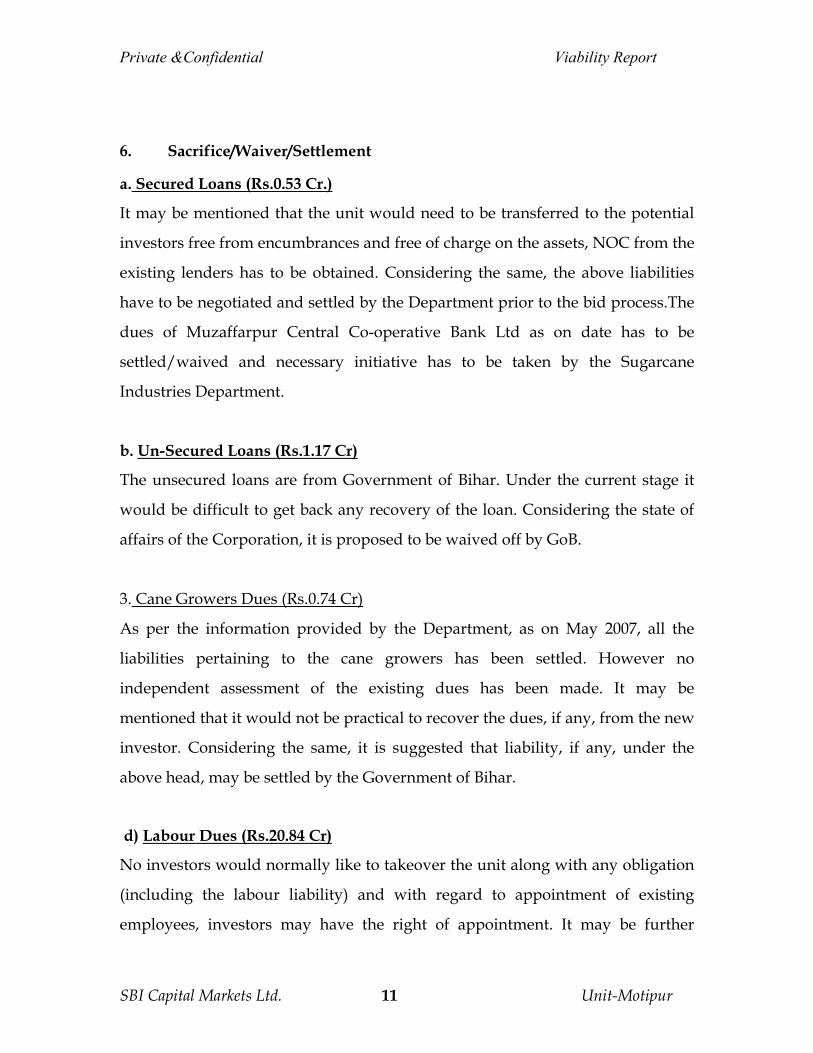

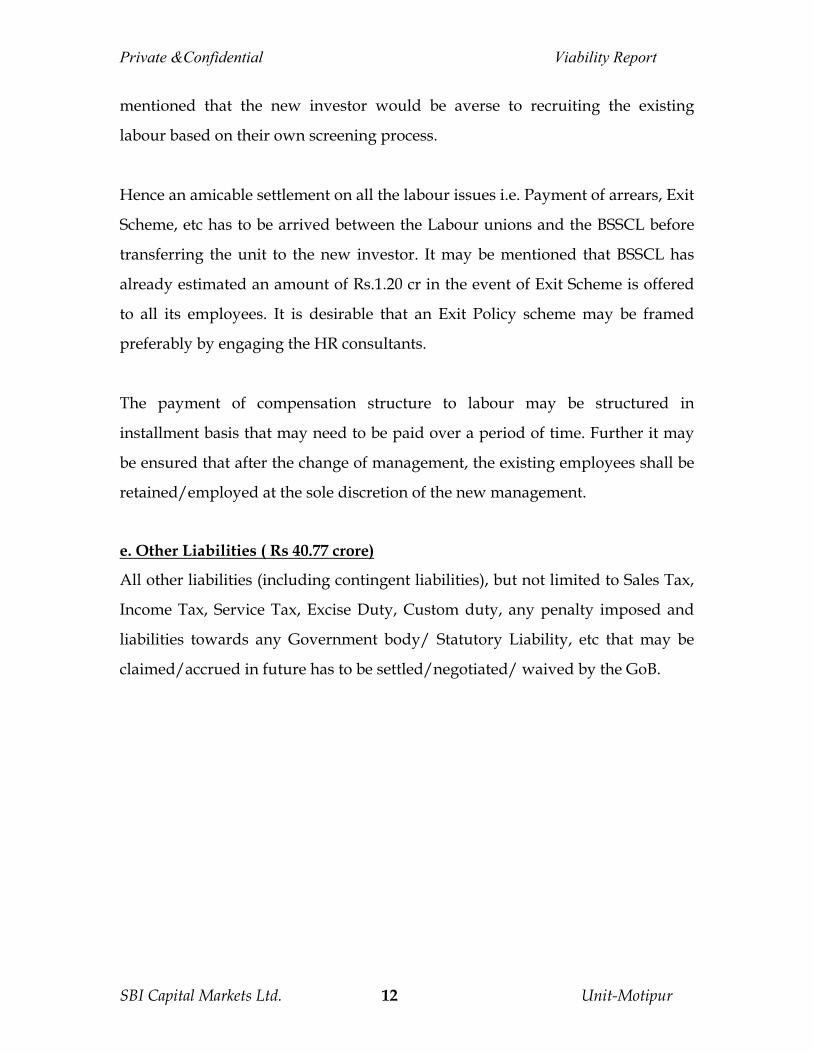

6. SACRIFICE/WAIVER/SETTLEMENT...................................................................... 11

7. UTILISATION OF PROCEEDS IN THE SETTLEMENT PROCESS....................... 13

8. LITIGATION CASES .................................................................................................... 14

9. CONCLUSIONS AND RECOMMENDATIONS...................................................... 16

Private &Confidential Viability Report

SBI Capital Markets Ltd. 2 Unit-Banmankhi

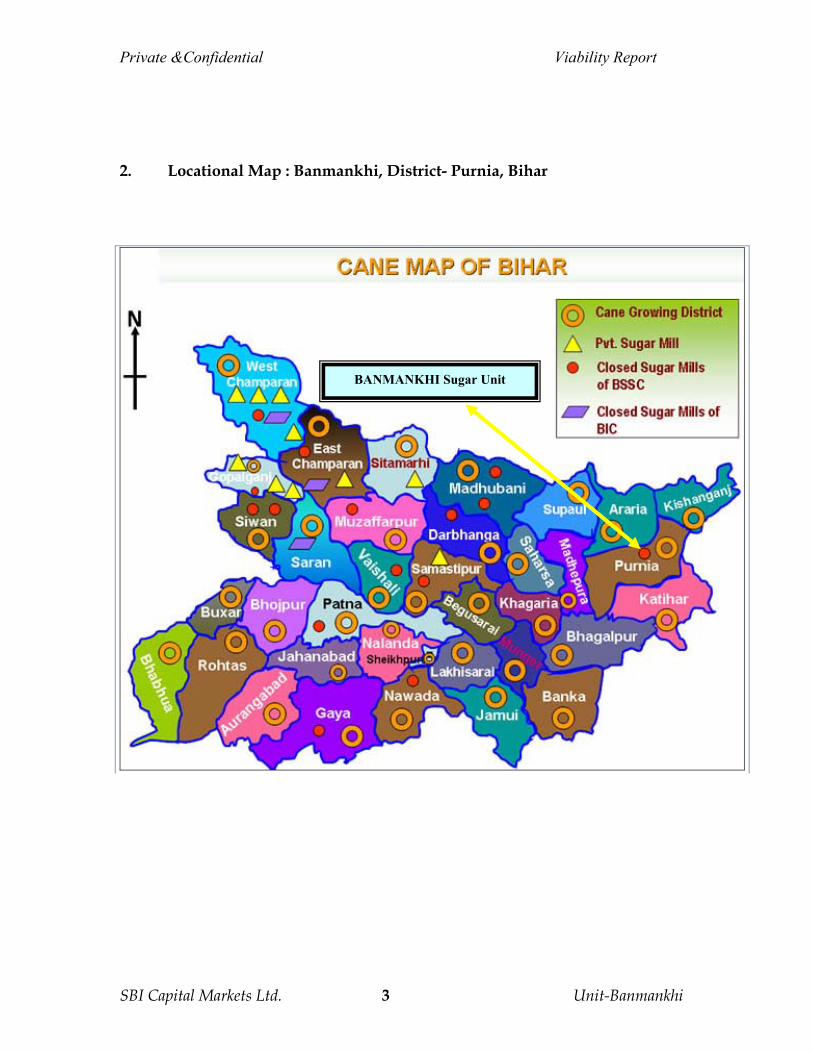

1. Brief Background The Banmankhi Sugar Unit is located 500 mtrs away from nearest Banmankhi

Railway Station of Purnia District and 38 Km away from District Town of Purnia.

The factory is situated at a distance of 2 Km from approach road of Purnia-

Saharsa Road. No other Sugar Unit is located in the radius of 15 km from this

unit.

The Banmankhi Sugar Unit with 1000 TCD capacity, was incorporated in 1970 by

Purnia Co-operative Sugar Factory Limited. In 1977 it was taken over by Bihar

State Sugar Corporation (BSSC) under Bihar Sugar Undertakings (Acquisition)

Acts. 1977.

The unit has land of 64 acres which is being used as Factory Premises-cum-

Colony Premises. It has also 55 acres of land as Farm Land.

After the take over of the unit by BSSC, the maximum cane of 10.68 lakh quintal

was crushed in the year 1982-83 (Assuming the no. of crushing days as 180 days,

capacity utilization during that year was 59%). The unit was operational till 1996-

97 but the management of BSSC took the decision of closure of the mill due to

continuous losses.

Private &Confidential Viability Report