important legal information, disclosures, and terms you ... · pdf filebusiness account...

TRANSCRIPT

The information in this disclosure may not be entirely accessible to screen readers. If you have any questions please contact your Wells Fargo banker or call our National Business Banking Center at 1-800-225-5935. Representatives are available to assist you 24 hours a day, 7 days a week.

Business Account Agreement

Important legal information, disclosures, and terms you need to

knowEffective April 24, 2017

IntroductionElectronic

banking services Rights and

responsibilitiesChecking and

savings accountsStatem

ents and error notifications

Resolving disputes through arbitration

i

Important legal

information

Introduction 1Words with specific meanings 1

Resolving disputes through arbitration 3Important legal information 6Statements and other information relating to your deposit account 7Rights and responsibilities 12Checking and savings accounts

Deposits to your account 16Funds availability policy 18Available balance, posting order, and overdrafts 20Setoff and security interest 24Bank fees and expenses; Earnings allowance 25Additional rules for checks and withdrawals 26Issuing stop payment orders and post-dated checks 27Interest earning accounts 29Time Accounts (CDs) 31

Electronic banking servicesDebit cards and ATM cards 32Phone Bank Services 41Termination of electronic banking privileges 42Funds transfer services 43

Table of contents

ii Business Account Agreement – Effective April 24, 2017

1

IntroductionElectronic

banking services Rights and

responsibilitiesChecking and

savings accountsStatem

ents and error notifications

Resolving disputes through arbitration

Important legal

information

Introduction

Welcome to Wells FargoYou have many choices when selecting a financial institution, and we are glad you chose Wells Fargo Bank, N A We value our relationship with you and hope we answered all your questions when you opened your account Please review this booklet for further details regarding your account and related services

What words do we use to refer to the customer, this booklet, and Wells Fargo?• Thecustomeristhe“accountowner,”“you,”“your,”“yours”and“authorized signer.”• WellsFargoBank,N.A.is“WellsFargo,”“we,”“us,”or“our.”• Thisbookletandthedisclosureslistedbelowconstitutethe“Agreement”:

-TheBusinessAccountFeeandInformationSchedule(“Schedule”),whichexplainsourfees and provides additional information about our accounts and services,

- Our Privacy Policy,- Our rate sheet for interest-earning accounts, and- Any additional disclosures we provide to you about your account and related services

Words with specific meaningsCertain words have specific meanings and are italicized throughout this booklet These words and their meanings are in this section

Authorized signerA person who has your actual or apparent authority to use your account even if they have not signed the signature card or other documents

Available balanceYour account’s available balance is our most current record of the amount of money available foryouruseorwithdrawal.Formoreinformation,pleaseseethesectionentitled“Howdowedetermine your account’s available balance?”intheAgreement.

Business dayEvery day is a business day except Saturday, Sunday, and federal holidays

Business deposit accountA business deposit account is any deposit account, other than one of Wells Fargo’s commercial deposit accounts, which is not held or maintained primarily for personal, family, or household purposes Examples of business deposit accounts include an account owned by an individual acting as a sole proprietor, a partnership, a limited partnership, a limited liability partnership, a limited liability company, a corporation, a joint venture, a non-profit corporation, an employee benefit plan, or a governmental unit including an Indian tribal entity

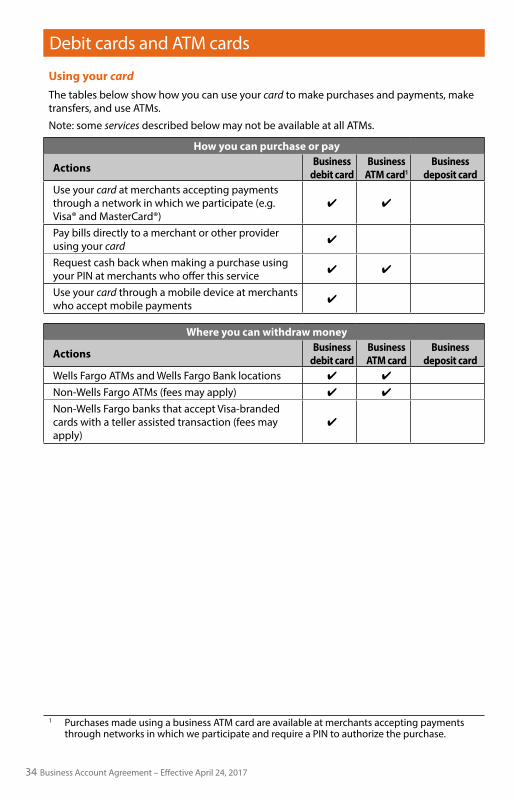

CardThis term includes every type of business debit card and business ATM card we may issue This term does not include any prepaid cards or the business deposit card unless otherwise noted

ItemAn item is an order, instruction, or authorization to withdraw or pay funds or money from an account Examples include a check, draft, and an electronic transaction (including AutomatedClearingHouse(ACH),anATMwithdrawal,andapurchaseusingacard to access an account) An item also includes a purported order, instruction, or authorization to withdraw or pay funds or money from an account, unless otherwise prohibited by law or regulation

2 Business Account Agreement – Effective April 24, 2017

Introduction

OverdraftAn overdraft is a negative balance in your account

ServiceA service is any service the Bank provides to you including without limitation any Treasury Management Service

What information does the Agreement contain?The Agreement• ExplainsthetermsofyourbankingrelationshipwithWellsFargo,• IstheentireAgreementbetweenWellsFargoandyouforyouraccountandanyservices,• Replacesallprioragreementsincludinganyoralorwrittenrepresentations,and• IncludeslegalinformationaboutyourbankingrelationshipwithWellsFargo.

You are responsible for ensuring that all authorized signers on your account(s) are familiar with this Agreement

We suggest you retain a copy of the Agreement — and any further information we provide you regarding changes to the Agreement — for as long as you maintain your Wells Fargo accounts

Are we allowed to change the Agreement?Yes, we can change the Agreement by adding new terms or conditions, or by modifying or deleting existing ones We refer to each addition, modification, or deletion to the Agreement asa“modification.”

Notice of a modification: If we are required to notify you of a modification to the Agreement, we will describe the modification and its effective date by a message within your account statement or any other appropriate means

Waiver of a term of the Agreement: We may agree in writing to waive a term of the Agreement, includingafee.Thisiscalleda“waiver.”Wemayrevokeanywaiveruponnoticetoyou.

How do you consent to a modification to the Agreement?You consent to a modification to the Agreement if you continue to use your account after a modification becomes effective or a waiver is revoked

What happens if a term of the Agreement is determined to be invalid?Any term of the Agreement that is inconsistent with the laws governing your account will be considered to be modified by us and applied in a manner consistent with such laws Any term of the Agreement that a court of competent jurisdiction determines to be invalid will be modified accordingly In either case, the modification will not affect the enforceability or validity of the remaining terms of the Agreement

Who will we communicate with about your account?We may provide you or an authorized signer with information about your account When we receive information from an authorized signer, we treat it as a communication from you You agree to notify us promptly in writing if an authorized signer no longer has authority on your account

3

Resolving disputes through arbitration

IntroductionElectronic

banking services Rights and

responsibilitiesChecking and

savings accountsStatem

ents and error notifications

Important legal

information

Resolvingdisputesthrougharbitration

Arbitration Agreement between you and Wells Fargo

If you have a dispute, we hope to resolve it as quickly and easily as possible First, discuss your dispute with a banker If your banker is unable to resolve your dispute, you agree that either Wells Fargo or you can initiate arbitration as described in this section

Definition: Arbitration means an impartial third party will hear the dispute between Wells Fargo and you and provide a decision Binding arbitration means the decision of the arbitratorisfinalandenforceable.A“dispute”isanyunresolveddisagreementbetweenWellsFargoandyou.A“dispute”mayalsoincludeadisagreementaboutthisArbitrationAgreement’s meaning, application, or enforcement

Exceptasstatedin“Nowaiverofself-helporprovisionalremedies”below,WellsFargoand you agree, at Wells Fargo’s or your request, to submit to binding arbitration all claims, disputes, and controversies between or among Wells Fargo and you (and their respective employees, officers, directors, attorneys, and other agents), whether in tort, contract or otherwise arising out of or relating in any way to your account(s) and/or service(s), and their negotiation, execution, administration, modification, substitution, formation, inducement, enforcement,default,ortermination(each,a“dispute”).

DISPUTES SUBMITTED TO ARBITRATION ARE NOT RESOLVED IN COURT BY A JUDGE OR JURY TO THE EXTENT ALLOWED BY APPLICABLE LAW, WELLS FARGO AND YOU EACH IRREVOCABLY AND VOLUNTARILY WAIVE THE RIGHT EACH MAY HAVE TO A TRIAL BY JURY FOR ANY DISPUTE ARBITRATED UNDER THIS AGREEMENT Asidefromself-helpremedies,thisArbitrationAgreementhasonlyoneexception:EitherWells Fargo or you may still take any dispute to small claims court

Arbitration is beneficial because it provides a legally binding decision in a more streamlined, cost-effective manner than a typical court case But, the benefit of arbitration is diminished if either Wells Fargo or you refuse to submit to arbitration following a lawful demand Thus, the party that does not agree to submit to arbitration after a lawful demand by the other party must pay all of the other party’s costs and expenses for compelling arbitration

Can either Wells Fargo or you participate in class or representative actions? No, Wells Fargo and you agree that the resolution of any dispute arising pursuant to the terms of this Agreement will be resolved by a separate arbitration proceeding and will not be consolidated with other disputes or treated as a class Neither Wells Fargo nor you will be entitled to join or consolidate disputes by or against others as a representative or member of a class, to act in any arbitration in the interests of the general public, or to act as a private attorney general If any provision related to a class action, class arbitration, private attorney general action, other representative action, joinder, or consolidation is found to be illegal or unenforceable, the entire Arbitration Agreement will be unenforceable

What rules apply to arbitration? WellsFargoandyoueachagreethatthearbitrationwill:• ProceedinalocationmutuallyagreeabletoWellsFargoandyou,orifthepartiescannot

agree, in a location selected by the American Arbitration Association (AAA) in the state whose laws govern your account

• BegovernedbytheFederalArbitrationAct(Title9oftheUnitedStatesCode),notwithstanding any conflicting choice of law provision in any of the documents between Wells Fargo and you

• BeconductedbytheAAA,orsuchotheradministratorasWellsFargoandyouwillmutually agree upon, in accordance with the AAA’s commercial dispute resolution procedures, unless the claim or counterclaim is at least $1,000,000 exclusive of claimed

4 Business Account Agreement – Effective April 24, 2017

Resolvingdisputesthrougharbitration

interest, arbitration fees and costs in which case the arbitration will be conducted in accordance with the AAA’s optional procedures for large, complex commercial disputes (the commercial dispute resolution procedures or the optional procedures for large, complexcommercialdisputestobereferredto,asapplicable,asthe“rules”).

If there is any inconsistency between the terms hereof and any such rules, the terms and procedures set forth herein will control Any party who fails or refuses to submit to arbitration following a lawful demand by any other party will bear all costs and expenses incurred by such other party in compelling arbitration of any dispute Nothing contained herein will be deemed to be a waiver by Wells Fargo of the protections afforded to it under 12U.S.C.Section91oranysimilarapplicablestatelaw.

No waiver of self-help or provisional remediesThisarbitrationrequirementdoesnotlimittherightofWellsFargooryouto:1 Exercise self-help remedies, including setoff or2 Obtain provisional or ancillary remedies such as injunctive relief or attachment, before,

during, or after the pendency of any arbitration proceeding

This exclusion does not constitute a waiver of the right or obligation of either party to submit any dispute to arbitration or reference hereunder, including those arising from the exercise of the actions detailed in (1) and (2) above

What are the Arbitrator qualifications and powers? Any dispute in which the amount in controversy is $5,000,000 or less will be decided by a single arbitrator selected according to the rules, and who will not render an award of greater than $5,000,000 Any dispute in which the amount in controversy exceeds $5,000,000 will be decided by majority vote of a panel of three arbitrators; provided however, that all three arbitrators must actively participate in all hearings and deliberations Each arbitrator will be a neutral attorney licensed in the state whose laws govern your account, or a neutral, retired judge in such state, in either case with a minimum of ten years experience in the substantive law applicable to the subject matter of the dispute to be arbitrated The arbitrator(s) will determine whether or not an issue is arbitratable and will give effect to the statutes of limitation in determining any claim In any arbitration proceeding the arbitrator(s) will decide (by documents only or with a hearing at the discretion of the arbitrator(s)) any pre-hearing motions which are similar to motions to dismiss for failure to state a claim or motions for summary adjudication The arbitrator(s) will resolve all disputes in accordance with the substantive law of the state whose laws govern your account and may grant any remedy or relief that a court of such state could order or grant within the scope hereof and such ancillary relief as is necessary to make effective any award The arbitrator(s) will also have the power to award recovery of all costs and fees, to impose sanctions, and to take such other action as deemed necessary to the same extent a judge could pursuant to the federal rules of civil procedure, the state rules of civil procedure for the state whose laws govern your account, or other applicable law Judgment upon the award rendered by the arbitrator(s) may be entered in any court having jurisdiction The institution and maintenance of an action for judicial relief or pursuit of a provisional or ancillary remedy will not constitute a waiver of the right of any party, including the plaintiff, to submit the controversy or claim to arbitration if any other party contests such action for judicial relief

5

Resolving disputes through arbitration

IntroductionElectronic

banking services Rights and

responsibilitiesChecking and

savings accountsStatem

ents and error notifications

Important legal

information

Resolvingdisputesthrougharbitration

Is discovery permitted in arbitration? Yes, in any arbitration proceeding, discovery will be permitted in accordance with the rules All discovery will be expressly limited to matters directly relevant to the dispute being arbitrated and must be completed no later than 20 days before the hearing date Any requests for an extension of the discovery periods, or any discovery disputes, will be subject to final determination by the arbitrator upon a showing that the request for discovery is essential for the party’s presentation and that no alternative means for obtaining information is available

Who pays the arbitration fees and expenses? The arbitrator will award all costs and expenses of the arbitration proceeding

Are there additional rules for an arbitration proceeding? Yes, to the maximum extent practicable, the AAA, the arbitrator(s), Wells Fargo and you will take all action required to conclude any arbitration proceeding within 180 days of the filing of the dispute with the AAA The arbitrator(s), Wells Fargo or you may not disclose the existence, content, or results thereof, except for disclosures of information by Wells Fargo or you required in the ordinary course of business, by applicable law or regulation, or to the extent necessary to exercise any judicial review rights set forth herein If more than one agreement for arbitration by or between Wells Fargo and you potentially applies to a dispute, the arbitration agreement most directly related to your account or the subject matter of the dispute will control This arbitration agreement will survive the closing of your account or termination of any service or the relationship between Wells Fargo and you

Do Wells Fargo and you retain the right to pursue in small claims court certain claims? Yes, notwithstanding anything to the contrary, Wells Fargo and you each retains the right to pursue in small claims court any dispute within that court’s jurisdiction Further, this arbitration agreement will apply only to disputes in which either party seeks to recover an amount of money (excluding attorneys’ fees and costs) that exceeds the jurisdictional limit of the small claims court

6 Business Account Agreement – Effective April 24, 2017

Important legal information

What laws govern your account?The laws governing your account include• Laws,rules,andregulationsoftheUnitedStates,and• Lawsofthestatewhereyouopenedyouraccount(withoutregardtoconflictoflaws

principles)

If a different state law applies, we will notify you; however, for certain account types (non-analyzed and savings accounts), your account statement will identify the state whose laws govern your account

Anyfundstransfer(includingawiretransfer)thatisa“remittancetransfer”asdefinedinRegulationE,SubpartB,willbegovernedbythelawsoftheUnitedStatesand,totheextentapplicable, the laws of the state of New York, including New York’s version of Article 4A of the UniformCommercialCode,withoutregardtoitsconflictoflawsprinciples.

What is the controlling language of our relationship?English is the controlling language of our relationship with you Items you write such as checks or withdrawal slips must be written in English For your convenience, we may translate some forms, disclosures, and advertisements into another language If there is a discrepancy between our English-language and translated materials, the English version prevails over the translation

What agreement applies when there is a separate agreement for a service?If a service we offer has a separate agreement, and there is a conflict between the terms of the Agreement and the separate agreement, the separate agreement will apply

What courts may be used to resolve a dispute?Wells Fargo and you each agree that any lawsuits, claims, or other proceedings arising from or relating to your account or the Agreement, including the enforcement of the Arbitration Agreement and the entry of judgment on any arbitration award, will be venued exclusively in the state or federal courts in the state whose laws govern your account, without regard to conflict of laws principles

How will we contact you about your account?In order for us to service your account or collect any amount you owe, you agree that we may contact you by phone, text, email, or mail We are permitted to use any address, telephone number or email address you provide You agree to provide accurate and current contact information and only give us phone numbers and email addresses that belong to you

When you give us a phone number, you are providing your express consent permitting us (and any party acting on behalf of Wells Fargo) to contact you at the phone number you provide We may call you and send you text messages When we call you, you agree that we may leave prerecorded or artificial voice messages You also agree that we may use automatic telephone dialing systems in connection with calls or text messages sent to any telephone number you give us, even if the telephone number is a mobile phone number or other communication service for which the called party is charged

7

IntroductionElectronic

banking services Rights and

responsibilitiesChecking and

savings accountsStatem

ents and error notifications

Resolving disputes through arbitration

Important legal

information

How do we share account statements and other notices with you?We will mail, send electronically, or otherwise make available to you an account statement reflecting your account activity for each statement period We’ll do the same with notices We will send all account statements and notices to the postal or electronic address associated with your account

Combined account statements: To reduce the number of separate account statements you receive each month, we may combine statements if you have more than one deposit account • If we provide a combined account statement for your accounts, we consider your first

account as your primary account You will receive your account statement at the address listed for your primary account Statements for accounts in a combined statement will be delivered according to the delivery preference of the primary account

• If you do not want us to automatically combine your accounts, you can opt-out by visiting a banking location or calling the number on your account statement

When is your account statement available?Mailed account statements: When we mail your account statement, we consider it received by you on the second business day after mailing it

Electronic delivery of account statements: Account statements will be made available through Wells Fargo Business Online® 24 – 48 hours after the end of the statement period You will be notified via email that the account statement is available for viewing We consider the account statement to be received by you on the notification date, even if the email notification is undelivered

What obligations do you have to review account statements and notices and notify us of errors?Youareobligatedto:• Examineyouraccountstatementpromptlyandcarefully.• Notifyuspromptlyofanyerrors.• Notifyuswithin30daysafterwehavemadeyouraccountstatementavailabletoyouof

anyunauthorizedtransactiononyouraccount.Note:Ifthesamepersonhasmadetwoor more unauthorized transactions and you fail to notify us of the first one within this 30 day period, we will not be responsible for unauthorized transactions made by the same wrongdoer

• Notifyuswithin6monthsafterwehavemadeyouraccountstatementavailabletoyouifyou identify any unauthorized, missing or altered endorsements on your items

Electronicfundtransfersaresubjecttodifferenttimeperiods,asdescribedinthe“Electronicfundtransferservices”partofthisbooklet.Commonexamplesofelectronicfundtransfersare ATM, debit card, and Online Bill Pay transactions

When is a transaction unauthorized?Atransactionisan“unauthorizedtransaction”whenitis• Missingarequiredsignatureorotherevidenceshowingyouhaveauthorizedit,or• Altered(forexample,theamountofacheckorthepayee’snameischanged).

Statements and other information relating to your deposit account

8 Business Account Agreement – Effective April 24, 2017

You can notify us of errors on your account statements by promptly• Callingthetelephonenumberlistedonyouraccountstatementorinanotice,or• Submittingawrittenreport(ifinstructedbyus)assoonaspossible,butinanyevent

within the specified time frames

What happens if you fail to notify us of an unauthorized transaction within the time frames specified above?If you fail to notify us of any unauthorized transaction, error, or claim for a credit or refund within the time frames specified above, your account statement will be considered correct We will not be responsible for any unauthorized transaction, error, or claim for transactions included in this statement

What happens when you report an unauthorized transaction?We investigate any reports of unauthorized activity on your account After you submit a claim,wemayrequireyouto:• Completetheclaimformweprovide,• Notifylawenforcement,• Completeandreturnanydocumentswerequest,and• Cooperatefullywithusinourinvestigation.

We can reverse any credit made to your account resulting from a claim of unauthorized transaction if you do not cooperate fully with us in our investigation or recovery efforts, or we determine the transaction was authorized

Protection against unauthorized itemsYou acknowledge that there is a growing risk of losses resulting from unauthorized items We offer services that provide effective means for controlling the risk from unauthorized items These servicesinclude:• Positivepay,positivepaywithpayeevalidation,orreversepositivepay• ACHfraudfilterand• PaymentAuthorizationservice

In addition, we may recommend you use certain fraud prevention practices to reduce your exposuretofraud.Eachofthesepracticesisanindustry“bestpractice.”Anexampleofabestpractice is dual custody, which requires a payment or user modification initiated by one user to be approved by a second user on a different computer or mobile device before it takes effect

If we have expressly recommended that you use one or more of these services or best practice (or any other service related to fraud prevention that we offer after the date of this Agreement) and you (a) either decide not to use the recommended service or best practice or (b) fail to use the service or best practice in accordance with the applicable service description or our other documentation applicable to the service or best practice, you will be treated as having assumed the risk of any losses that could have been prevented if you had used the recommended service or best practice in accordance with the applicable service description or applicable documentation

Statements and other information relating to your deposit account

9

IntroductionElectronic

banking services Rights and

responsibilitiesChecking and

savings accountsStatem

ents and error notifications

Resolving disputes through arbitration

Important legal

information

Are you responsible for taking reasonable steps to help prevent fraud and embezzlement on your account?Yes, you agree to take reasonable steps to ensure the integrity of your internal procedures with respect to your account and items drawn on your account or deposited to it To help preventembezzlementandprotectyourbusinessassets,werecommendthatyou:• Assignresponsibilitiesforyouraccounttomultipleindividuals.Thosewhoreconcile

statements for your account should be different from those who issue items drawn on your account

• Reconcilestatementsforyouraccountasyoureceivethemandnotifyusimmediatelyofany problem

• Contactuspromptlyifyoudonotreceivethestatementforyouraccountwhenyouwould normally expect to

• Watchforcheckscashedoutofsequenceormadeouttocash.Theseareclassicredflagsfor embezzlement

• Secureyoursupplyofchecksatalltimes.Stolenchecksitems are a common method of embezzlement

• Periodicallyreassignaccountingdutiessuchasreconcilingyouraccountormakingadeposit

• Reviewyourtransactionactivityforunexpectedfluctuations(e.g.comparethepercentage of cash deposits to total deposit size) Most businesses will maintain a constant average A large fluctuation might indicate embezzlement

• Destroyanycheckthatyoudonotintendtouse• Usetamperresistantcheckitems at all times• Notifyusimmediatelywhenanauthorized signer’s authority ends so that his/her name

can be removed from all signature cards and online banking access, and any cards we have issued to him/her can be cancelled

• Donotsignblankchecks• Obtaininsurancecoveragefortheserisks

What happens if your account statements or notices are returned or are undeliverable?Your account statements or notices will be considered unclaimed or undeliverable if• Twoormoreaccountstatementsornoticesarereturnedtousthroughthemailbecause

of an incorrect address; or• Wenotifyyouelectronicallythatyouraccountstatementisavailableforviewingat

Wells Fargo Business Online, and we receive email notifications that our message is undeliverable

In either event, we may• Discontinuesendingaccountstatementsandnotices,and• Destroyaccountstatementsandnoticesreturnedtousasundeliverable.

We will not attempt to deliver account statements and notices to you until you provide us with a valid postal or electronic address

Statements and other information relating to your deposit account

10 Business Account Agreement – Effective April 24, 2017

How can you or Wells Fargo change your address for your account?Address change requests you make: You can change your postal or email address by notifying us in writing or calling us at the number on your account statement at any time If you have a combined account statement, any owner of the first account (primary account) can change the address of all accounts included in the combined account statement We willactonyourrequestwithinareasonabletimeafterwereceiveit.Unlessyouinstructotherwise, we may change the postal or electronic address only for the account(s) you specify or for all or some of your other account(s) with us

Address changes we make: When necessary, we may update your listed address without a request from you if we receive• AnaddresschangenoticefromtheU.S.PostalServiceor• Informationfromanotherpartyinthebusinessofprovidingcorrectaddressdetailsthat

does not match your account’s listed address

When are notices you send to us effective?Any notice from you is effective once we receive it and have a reasonable opportunity to act on it

Are original paid checks returned with account statements?No We do not return original paid checks with your account statements Copies of your paid checks are available through Wells Fargo Business Online, banking locations, by calling Wells Fargo National Business Banking Center, or by enrolling in our check images with statements service Fees may apply for this service

When does my account become dormant?Generally, your account becomes dormant if you do not initiate an account-related activity for 12 months for a checking account, 34 months for a savings account, or 34 months after the first renewal for a Time Account (CD) An account-related activity is determined by the laws governing your account Examples of account-related activity are depositing or withdrawing funds at a banking location or ATM, or writing a check which is paid from the account Automatic transactions (including recurring and one-time), such as pre-authorized transfers/payments and electronic deposits, set up on the account may not prevent the account from becoming dormant

What happens to a dormant account?We put safeguards in place to protect a dormant account which may include restricting the following:

• TransfersbetweenyourWellsFargoaccountsusingyourATM/debitcard• Transfersbyphoneusingourautomatedbankingservice• Transfersorpaymentsthroughonline,mobile,andtextbanking(includingBillPay)• Wiretransfers(incomingandoutgoing)

Normal monthly service and other fees continue to apply (except where prohibited by law)

If you do not initiate an account-related activity on the account within the time period as specified by state law, your account funds may be transferred to the appropriate state This transferisknownas“escheat.”Youraccountwillbeclosed.Torecoveryouraccountfunds,you must file a claim with the state

Statements and other information relating to your deposit account

11

IntroductionElectronic

banking services Rights and

responsibilitiesChecking and

savings accountsStatem

ents and error notifications

Resolving disputes through arbitration

Important legal

information

What are checking subaccounts?For each checking account you maintain with us, we may establish on your behalf a master account and two subaccounts

All information that is made available to you about your account will be at the master account level The subaccounts are composed of a savings account and a checking account

On the first day of each month, we will allocate funds between the two subaccounts as appropriate Items received by us that are drawn against your master account will be presented for payment against the checking subaccount Funds will be transferred from the savings subaccount as may be needed to cover checks presented on the checking subaccount On the sixth transfer from the savings subaccount during a statement period, all of the funds on deposit in the savings subaccount will be transferred to the checking subaccount If your account earns interest, the use of subaccounts will not affect the interest you earn

Statements and other information relating to your deposit account

12 Business Account Agreement – Effective April 24, 2017

Rightsandresponsibilities

What responsibilities and liabilities do Wells Fargo and you have to each other?Weareresponsibleforexercising“ordinarycare”andcomplyingwiththeAgreement.Whenwe take an item forprocessingbyautomatedmeans,“ordinarycare”doesnotrequireustoexamine the item.Inallothercases,“ordinarycare”requiresonlythatwefollowstandardsthatdo not vary unreasonably from the general standards followed by similarly situated banks

Excepttotheextentwefailtoexercise“ordinarycare”ortocomplywiththeAgreement,you agree to indemnify and hold us harmless from all claims, demands, losses, liabilities, judgments, and expenses (including attorney’s fees and expenses) arising out of or in any way connected with our performance under the Agreement You agree this indemnification will survive termination of the Agreement

In no event will either Wells Fargo or you be liable to the other for any special, consequential, indirect or punitive damages The limitation does not apply where the laws governing your account prohibit it

We will not have any liability to you if your account has non-sufficient available funds to pay your items due to actions we have taken in accordance with the Agreement

Circumstances beyond your control or ours may arise and make it impossible for us to provide services to you or for you to perform your duties under the Agreement If this happens, neither Wells Fargo nor you will be in breach of the Agreement

If we waive a right with respect to your account on one or more occasions, it does not mean we are obligated to waive the same right on any other occasion

What are we allowed to do if there is an adverse claim against your account?An“adverseclaim”occurswhen• Anypersonorentitymakesaclaimagainstyouraccountfunds,• Webelieveaconflictexistsbetweenoramongyouraccount’sowners,or• Webelieveadisputeexistsoverwhohasaccountownershiporauthoritytowithdraw

funds from your account

Inthesesituations,wemaytakeanyofthefollowingactionswithoutanyresponsibilitytoyou:• Continuetorelyonthesignaturecard(s)foryouraccount.• Honortheclaimagainstyouraccountfundsifwearesatisfiedtheclaimisvalid.• Freezeallorapartofthefundsinyouraccountuntilwebelievethedisputeisresolvedto

our satisfaction • Closeyouraccountandsendacheckfortheavailable balance in your account payable to

you or to you and each person or entity who claimed the funds • Paythefundsintoanappropriatecourt.

We also may charge any account you maintain with us for our fees and expenses in taking these actions (including attorney’s fees and expenses)

If you carry special insurance for employee fraud/embezzlement, can we require you to file your claim with your insurance company before making any claim against us?Yes, as many businesses carry special insurance for employee fraud/embezzlement If you do, we reserve the right to require you to file your claim with your insurance company before making any claim against us In such event, we will consider your claim only after we have reviewed your insurance company’s decision, and our liability to you, if any, will be reduced by the amount your insurance company pays you

13

IntroductionElectronic

banking services Rights and

responsibilitiesChecking and

savings accountsStatem

ents and error notifications

Resolving disputes through arbitration

Important legal

information

Rightsandresponsibilities

Are we allowed to restrict access to your account?Yes, if we suspect any suspicious, unauthorized, or unlawful activities, we can restrict access to your account and other accounts with us that you maintain or control

How do we handle legal process?Legalprocessincludesanylevy,garnishmentorattachment,taxlevyorwithholdingorder,injunction, restraining order, subpoena, search warrant, government agency request for information, forfeiture or seizure, and other legal process relating to your account

We will accept and act on any legal process we believe to be valid, whether the process is served in person, by mail, by electronic notification, or at any banking location

If we incur any fees or expenses (including attorney’s fees and expenses) due to responding to legal process related to your account, we may charge these costs to any account you maintain with us

Are transactions subject to verification by the Bank? Yes All transactions are subject to the Bank’s verification This includes cash, items, or other funds offered for deposit for which we have provided a receipt We do not verify all transactions We reserve the right to reverse or otherwise adjust, at any time without prior notice to you, any debit or credit we believe we have erroneously made to your account

Who is responsible to make sure the declared amount of funds offered for deposit is accurate?It is your responsibility, and the Bank has no obligation, to make sure the declared amount of funds offered for deposit is accurate If we determine a discrepancy exists between the declared and the actual amount of the funds, we are permitted to adjust (debit or credit) your account We are also permitted to use the declared amount as the correct amount to be deposited and to not adjust a discrepancy if it is less than our standard adjustment amount We are permitted to vary our standard adjustment amount from time to time without notice to you and to use different amounts depending on account type

If you notify us of an error in the amount of a deposit shown on your account statement within 30 days of the date we mail or otherwise make the account statement available to you, we will review the deposit and make any adjustment we determine is appropriate, subject to any applicable fees

If you fail to notify us during this time frame, the deposit amount on your statement will be considered correct This means that if the actual amount is less than the amount on the statement, the difference will become your property If the actual amount is more than the amount shown on the statement, the difference will become the Bank’s property

Can you arrange to have us adjust all discrepancies identified during any verification without regard to our standard adjustment amount? Yes If your account is an analyzed business deposit account, you may arrange for the Bank to adjust all discrepancies identified during any verification without regard to our standard adjustment amount by contacting your local banker or calling the number on your statement

Are we allowed to convert your account without your request?Yes, we can convert your account to another type of deposit account (by giving you any required notice) if• Youuseitinappropriatelyorfailtomeetormaintaintheaccount’srequirements,or• Wedetermineanaccountisinappropriateforyoubasedonyouruse,or• Westopofferingthetypeofaccountyouhave.

14 Business Account Agreement – Effective April 24, 2017

Rightsandresponsibilities

When can you close your account?If you request to close your account, we may allow you to keep funds in your account to cover outstanding items to be paid • Ifwedoallowyoutokeepfundsinyouraccount:

- For interest-earning accounts, it stops earning interest from the date you request to close your account

- Overdraft Protection and/or Debit Card Overdraft will be removed on the date you request to close your account

- The Agreement continues to apply - All outstanding items need to post and the account’s balance needs to be brought to zero

within 30 days from the date of your request to close After 30 days, unless your account has a negative balance, your account will be closed

• Wewillnotbeliableforanylossordamagethatmayresultfromnothonoringitems that are presented or received after your account is closed

You can close your account at any time if the account is in good standing (e g , does not have a negative balance or any restrictions such as legal order holds or court blocks on the account)

When can we close your account? We reserve the right to close your account at any time If we close your account, we may send the remaining balance on deposit in your account by traditional mail or credit it to another account you maintain with us

Are we allowed to terminate or suspend a service related to your account? Yes, we can terminate or suspend specific services (e g , wire transfers) related to your account without closing your account and without prior notice to you You can discontinue using a service at any time

Are we allowed to obtain credit reports or other reports about you?Yes, we can obtain a credit or other report about you and your co-owners to help us determine whether to open or maintain an account Other reports we can obtain include information fromthefollowing:1)motorvehicledepartments,2)otherstateagencies,or3)publicrecords.

When do we share information about your account with others?Generally, if we do not have your consent, we will not share information about your account However,wemayshareinformationaboutyouraccountinaccordancewithourPrivacyPolicy separately given to you

Are we allowed to monitor and record communications?Yes, we can monitor, record, and retain your communications with us at any time without further notice to anyone, unless the laws governing your account require further notice

Monitoredandrecordedcommunicationsinclude:• Telephoneconversations,• Electronicmessages,• Electronicrecords,or• Otherdatatransmissions.

15

IntroductionElectronic

banking services Rights and

responsibilitiesChecking and

savings accountsStatem

ents and error notifications

Resolving disputes through arbitration

Important legal

information

Rightsandresponsibilities

Can Wells Fargo benefit from having the use of funds in customers’ non-interest earning accounts?Yes We may benefit from having the use of funds in customers’ non-interest earning accounts We may use these funds to reduce our borrowing from other sources such as theFedFundsmarketorinvesttheminshort-terminvestmentssuchasitsFederalReserveAccount.Thisbenefitmaybereferredtoas“spread.”Itisnotpossibletoquantifythebenefitto us that may be attributable to a particular customer’s funds because funds from all customers’ non-interest earning accounts are aggregated both for purposes of reducing our borrowing costs and for investment and because our use of funds may vary depending on a number of factors including interest rates, Federal Funds rates, credit risks and our anticipated funding needs Our use of funds as described in this paragraph has no effect or impact on your use of and access to funds in your account

Can you transfer ownership of your account?No assignment will be valid or binding on us, and we will not be considered to have “knowledge”ofit,untilweconsentandtheassignmentisnotedinourrecords.However,bynoting the assignment, we do not have any responsibility to assure that the assignment is valid Any permitted assignment of your account is subject to our setoff rights

The Agreement is binding on your personal representatives, executors, administrators, and successors, as well as our successors and assigns

Is your wireless operator authorized to provide information to assist in verifying your identity?Yes, and as a part of your account relationship, we may rely on this information to assist in verifying your identity

Youauthorizeyourwirelessoperator(AT&T,Sprint,T-Mobile,USCellular,Verizon,oranyotherbranded wireless operator) to use your mobile number, name, address, email, network status, customer type, customer role, billing type, mobile device identifiers (IMSI and IMEI) and other subscriber status details, if available, solely to allow verification of your identity and to compare information you have provided to Wells Fargo with your wireless operator account profile information for the duration of the business relationship

You may opt out of this information sharing by contacting your wireless operator directly

16 Business Account Agreement – Effective April 24, 2017

Deposits to your account

Are there any restrictions on our accepting deposits to your account?We may accept a deposit to your account at any time and from any person When we cannot verify an endorsement, we can refuse to pay, cash, accept for deposit, or collect the item Also, we may require all endorsers be present We may require you to deposit an item instead of permitting you to cash it Checks drawn on credit account or made out to payees not on the account may not be accepted or may be sent for collection We reserve the right to refuse for deposit or to require to be sent for collection an item drawn on a credit account or to a payee not on the account For a deposit made to your account, we may require an acceptable form of primary identification in order to make such deposit

What happens if we send an item for collection?We may, upon notice to you, send an item for collection instead of treating it as a deposit This means that we send the item to the issuer’s bank for payment Your account will not be credited for the item until we receive payment for it

What are the requirements for a correct endorsement?An“endorsement”isasignature,stamp,orothermarkonthebackofacheck.Ifyouhavenot endorsed a check that you deposited to your account, we may endorse it for you Your endorsement (and any other endorsement before the check is deposited) must be in the 1-1/2–inch area that starts on the top of the back of the check (see sample below) Do not sign or write anywhere else on the back of the check

Are we bound by restrictions or notations on checks?No,wearenotboundbyrestrictionsornotations,suchas“Voidaftersixmonths,”“Voidover$50,”and“Paymentinfull.”

When you cash or deposit a check with a notation or restriction, you are responsible for any loss or expense we incur relating to the notation or restriction

What is a “substitute check?”A substitute check is created from an original check; under federal law, it is legally equivalent to that original check A substitute check contains an accurate copy of the front and back of theoriginalcheckandbearsthelegend:“Thisisalegalcopyofyourcheck.Youcanuseitthesamewayyouwouldusetheoriginalcheck.”Asnotedinthelegend,asubstitutecheckisthesame as the original check for all purposes, including proving that you made a payment Any check you issue or deposit that is returned to you may be returned in the form of a substitute check You agree that you will not transfer a substitute check to us, by deposit or otherwise, if we would be the first financial institution to take the substitute check, unless we have expressly agreed in writing to take it

17

IntroductionElectronic

banking services Rights and

responsibilitiesChecking and

savings accountsStatem

ents and error notifications

Resolving disputes through arbitration

Important legal

information

Deposits to your account

What happens if you breach a warranty associated with an item?If you breach any warranty you make to us under the laws governing your account with respect to any item, you will not be released or discharged from any liability for the breach so long as we notify you of the breach within 120 days after we learn of the breach If we fail to notify you within this 120 day period, you will be released from liability and discharged only to the extent our failure to notify you within this time period caused a loss to you

How do we handle non-U S items?A“non-U.S.item”isanitem1)payableinacurrencyotherthanU.S.dollarsor2)drawnonafinancialinstitutionthatisnotorganizedunderU.S.law.Wearenotrequiredtoacceptanon-U.S.itemfordeposittoyouraccountorforcollection.Wemayacceptnon-U.S.items on a collection basis without your specific instruction to do so We can reverse any amount we have credited to your account and send the item on a collection basis even if we have taken physical possession of the item

Ifweacceptanon-U.S.item,theU.S.dollaramountyoureceiveforitwillbedeterminedbyour exchange rate that is in effect at the time of deposit or our receipt of final payment (less any associated fees) of the collection item.Ifthenon-U.S.depositeditem is returned unpaid for any reason, we will charge the amount against your account (or any other account you maintain with us) at the applicable exchange rate in effect at the time of the return

Ourfundsavailabilitypolicydoesnotapplytoanon-U.S.item

What is our responsibility for collecting a deposited item?We are responsible for exercising ordinary care when collecting a deposited item We will not be responsible for the lack of care of any bank involved in the collection or return of a deposited item, or for an item lost in collection or return

What happens when a deposited or cashed item is returned unpaid?We can deduct the amount of the deposited or cashed item from your account (or any other account you maintain with us) We can do this when we are notified that the item will be returned We do not need to receive the actual item (and usually do not receive it) We can do this even if you have withdrawn the funds and the balance in your account is not sufficient to cover the amount we hold or deduct and your account becomes overdrawn In addition, we will charge you all applicable fees and reverse all interest accrued on the item

We may place a hold on or charge your account for any check or other item deposited into your account if a claim is made or we otherwise have reason to believe the check or other item was altered, forged, unauthorized, has a missing signature, a missing or forged endorsement, or should not have been paid, or may not be paid, or for any other reason When the claim is finally resolved, we will either release the hold or deduct the amount of the item from your account We are not legally responsible if we take or fail to take any action to recover payment of a returned deposited item

What happens when an electronic payment is reversed?We may deduct the amount of an electronic payment credited to your account (e g , direct deposit) that is reversed We can deduct the amount from any account you have with us at any time without notifying you You agree to immediately repay any overdrafts resulting from the reversed payment

Are you responsible for assisting us in reconstructing a lost or destroyed deposited item?If a deposited item is lost or destroyed during processing or collection, you agree to provide all reasonable assistance to help us reconstruct the item

18 Business Account Agreement – Effective April 24, 2017

Funds availability policy

Your ability to withdraw fundsOur policy is to make funds from your check deposits to your checking or savings account (inthispolicy,eachan“account”)availabletoyouonthefirstbusiness day after the day we receive your deposits Incoming wire transfers, electronic direct deposits, cash deposited at a teller window and at a Wells Fargo ATM, and the first $400 of a day’s check deposits at a teller window and at a Wells Fargo ATM will be available on the day we receive the deposits Certain electronic credit transfers, such as those through card networks or funds transfer systems, will be available on the first business day after the day we receive the transfer Once they are available, you can withdraw the funds in cash and we will use the funds to pay checks and other items presented for payment and applicable fees that you have incurred

The first $400 of a business day’s check deposits to an analyzed account are not available to you on the day we receive the deposits Check deposits to an analyzed account are available on the first business day after we receive your deposits

Determining the day of receiptFor determining the availability of your deposits, every day is a business day, except Saturdays, Sundays, and federal holidays If you make a deposit before our established cutoff time on a business day that we are open, we will consider that day to be the day of yourdeposit.However,ifyoumakeadepositafterourcutofftimeoronadaywearenotopen, we will consider the day the deposit was made to be the next business day we are open

Our established cutoff time is when a branch closes for business and may vary by location The cutofftimeforchecksdepositedataWellsFargoATMis9:00p.m.localtime(8:00p.m.inAlaska).

Longer delays may applyIn some cases, we will not make the first $400 of a business day’s check deposits available to you on the day we receive the deposits Further, in some cases, we will not make all the funds that you deposit by check available to you on the first business day after the day of your deposit Depending on the type of check that you deposit, funds may not be available until the second business day after the day of your deposit The first $200 of your deposit, however, may be available on the first business day

Except as otherwise explained in this paragraph, if we are not going to make all funds from your deposit available on the business day of deposit or the first business day after the day of deposit, we will notify you at the time you make your deposit We will also tell you when the funds will be available If your deposit is not made directly to a Wells Fargo employee, or if we decide to take this action after you have left the premises, we will mail you the notice by the first business day after we receive your deposit

If you need the funds from a deposit right away, you may ask us when the funds will be available

In addition, funds you deposit by check may be delayed for a longer period under the followingcircumstances:

•Webelieveacheckyoudepositwillnotbepaid

•Youdepositcheckstotalingmorethan$5,000onanyoneday

•Youredepositacheckthathasbeenreturnedunpaid

•Youhaveoverdrawnyouraccountrepeatedlyinthelast6months

•Thereisanemergency,suchasfailureofcomputerorcommunicationsequipment

19

IntroductionElectronic

banking services Rights and

responsibilitiesChecking and

savings accountsStatem

ents and error notifications

Resolving disputes through arbitration

Important legal

information

We will notify you if we delay your ability to withdraw funds for any of these reasons, and we will tell you when the funds will be available The funds will generally be available no later than the seventh business day after the day of your deposit

Special rules for new accountsIf you are a new customer, the following special rules will apply during the first 30 days your account is open Incoming wire transfers, electronic direct deposits, and cash deposited at a teller window and at a Wells Fargo ATM will be available on the day we receive the deposit Funds from your check deposits will be available on the business day after the day we receive the deposits; no funds from a business day’s check deposits are available on the day we receive the deposits

Ifwedelaytheavailabilityofyourdepositthefollowingspecialrulesmayapply:• Thefirst$5,000ofaday’stotaldepositsofcashier’s,certified,teller’s,traveler’s,and

federal,state,andlocalgovernmentchecksandU.S.PostalServicemoneyordersmadepayable to you will be available on the first business day after the day of your deposit

• Theexcessover$5,000andfundsfromallothercheckdepositswillbeavailableontheseventh business day after the day of your deposit The first $200 of a day’s total deposit of funds from all other check deposits, however may be available on the first business day after the day of your deposit

We will notify you if we delay your ability to withdraw funds and we will tell you when the funds will be available

Holds on other funds (check cashing)If we cash a check for you that is drawn on another bank, we may withhold the availability of a corresponding amount of funds that are already in your account Those funds will be available at the time funds from the check we cash would have been available if you had deposited it

Holds on other funds (other account)If we accept a check for deposit that is drawn on another bank, we may make funds from the deposit available for withdrawal immediately but delay your ability to withdraw a corresponding amount of funds that you have on deposit in another account with us

The funds in the other account would then not be available until the time periods that are described in this Policy

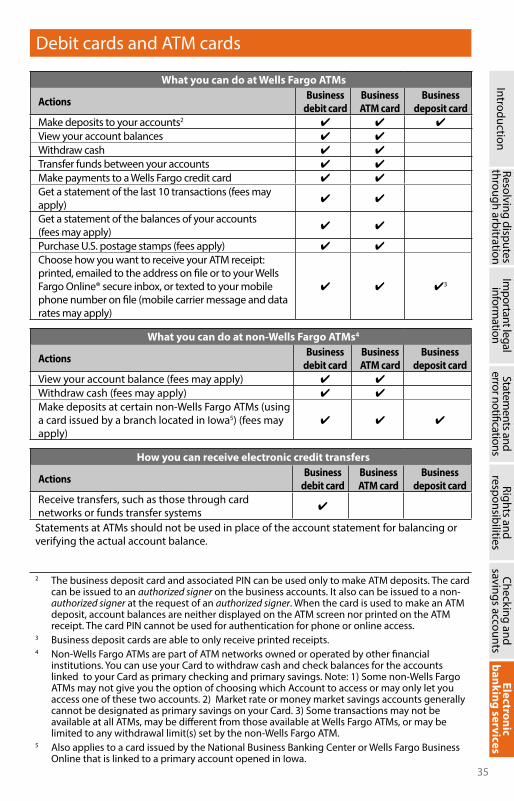

Delays on other fundsFunds from any deposit (cash or checks) made at eligible non-Wells Fargo ATMs using a card issued by a Wells Fargo branch located in Iowa1 will not be available until the third business day after the day of your deposit This rule does not apply at ATMs that we own or operate All ATMsthatweownoroperateareidentifiedonourmachinesas“WellsFargo.”

1 Also applies to a card issued by the National Business Banking Center or Wells Fargo Business Online that is linked to a primary account opened in Iowa

Funds availability policy

20 Business Account Agreement – Effective April 24, 2017

Available balance, posting order, and overdrafts

How do we determine your account’s available balance?Your account’s available balance is our most current record of the amount of money available for your use or withdrawal We use the available balance to authorize your transactions during the day (e g , debit card purchases and ATM withdrawals) We also use the available balance to pay your transactions in our nightly processing We calculate your available balanceasfollows:• Westartwiththeendingdailyaccountbalancefromourpriorbusiness day nightly

processing that includes all transactions deposited to or paid from your account • Wesubtractfromthisamountanyholdsplacedonadeposittoyouraccountandany

holds placed due to legal process • Weadd“pending”depositsthatareimmediatelyavailableforyouruse(includingcash

deposits, electronic direct deposits, and the portion of a paper check deposit we make available;see“Fundsavailabilitypolicy”sectionfordetails).

• Wesubtract“pending”withdrawalsthatwehaveeitherauthorized(suchasdebitcard purchases and ATM withdrawals) or are known to us (such as your checks and preauthorizedautomaticACHwithdrawalsthatwereceiveforpaymentfromyouraccount) but have not yet processed

Important note: The available balance does not reflect every transaction you have initiated or previously authorized For example, your available balance may not includethefollowing:• Outstandingchecksandauthorizedautomaticwithdrawals(suchasrecurringdebitcard

transactions,transfers,andACHtransactionsthatwehavenot received for payment or received too close to our nightly processing to include in your available balance)

• Thefinalamountofadebitcardpurchase.Forexample,wemayauthorizeapurchaseamount prior to a tip that you add

• Debitcardtransactionsthathavebeenpreviouslyauthorizedbutnotsenttousforfinalpayment We must release the transaction authorization hold after 3 business days (or up to 30 business days for certain types of debit or ATM card transactions, including car rental, cash, and international transactions) even though the transaction may be sent for payment from your account, which we must honor, at a later date

How do we process (post) transactions to your account?We process transactions each business day (Monday through Friday except federal holidays) duringalatenightprocess.Onceweprocessyourtransaction,theresultsare“posted”toyouraccount There are three key steps to this process The most common types of transactions are processed as described below

First, we determine the available balance in your account (as described above) that can be used to pay your transactions NOTE:Certain“pending”transactionscanimpactyouravailable balance:• CashdepositsortransfersfromanotherWellsFargoaccountthataremadeAFTERthe

displayed cutoff time (where the deposit was made) will be added to your available balance if they are made before we start our nightly process

• Youravailable balancewillbereducedby“pending”withdrawals,suchasdebitcardtransactions we have authorized and must pay when they are sent to us for payment These pending withdrawals may be sent to us for payment at a later date In some circumstances, these transactions may be paid into overdraft if other posted transactions or fees have reduced your balance before the pending transactions are presented for payment

21

IntroductionElectronic

banking services Rights and

responsibilitiesChecking and

savings accountsStatem

ents and error notifications

Resolving disputes through arbitration

Important legal

information

Available balance, posting order, and overdrafts

Then, we sort your transactions into categories before we process them • First,wecredityouraccountfordeposits,includingcashandcheckdepositsand

incoming transfers, received before the cutoff time at the location the deposit or transfer was made

• Then,weprocesswithdrawals/paymentswehavepreviouslyauthorizedandcannotreturn unpaid, such as debit card purchases, ATM withdrawals, account transfers, Business Bill Pay transactions, and teller-cashed checks If we receive more than one of these transactions for payment from your account, we will generally sort and pay them based on the date and time you conducted the transactions For a debit card transaction, if a merchant does not seek authorization from the Bank at the time of the transaction, we will use the date the transaction is received for payment from your account For some transactions, such as Business Bill Pay transactions or teller-cashed checks, the time may be assigned by our systems and may vary from the time it was conducted Multiple transactions that have the same time will be sorted and paid from lowest to highest dollar amount

• Finally,weuseyourremainingfundstopayyourchecksandpreauthorizedautomaticACHpayments(suchasbillsyoupaybyauthorizingathirdpartytowithdrawfundsdirectly from your account) If there is more than one of these types of transactions, they will be sorted by the date and time that they are received by us Multiple transactions that have the same time will be sorted and paid from lowest to highest dollar amount

Finally, if the available balance in your account is not enough to pay all of your transactions, we will take the following steps:• First use Overdraft Protection (if applicable): We will transfer/advance available funds

from a savings and/or credit account you have linked to your checking account for Overdraft Protection (described on p 22)

• Then, decide whether to pay your transaction into overdraft or return it unpaid: At our discretion, we may pay a check or automatic payment into overdraft, rather than returning it unpaid This is our standard overdraft coverage If we pay the transaction into overdraft, it may help you avoid additional fees that may be assessed by the merchant Debit card transactions presented to us for payment (whether previously approved by us or not) will be paid into overdraft and will not be returned unpaid, even if you do not have sufficient funds in your account

IMPORTANT INFORMATION ABOUT FEES:Fees may be assessed with each item paid into overdraft or returned unpaid subject to thefollowing:

- A single Overdraft Protection Transfer or Advance Fee will be assessed when we need to transfer/advance funds from your linked account(s) into your checking account, but only if the transfer/advance helped you avoid at least one overdraft or returned item

- If both the ending daily account balance and available balance are overdrawn by $5 or less and there are no items returned for non-sufficient funds — after we have processed all of your transactions — we will not assess an overdraft fee on the item(s).

- We limit the number of overdraft and/or returned item (non-sufficient funds/NSF) fees to no more than 8 for business accounts per business day

- Any overdraft or returned item fees assessed are deducted from your account during the morning of the next business day following our nightly process

22 Business Account Agreement – Effective April 24, 2017

What is Overdraft Protection?When you enroll in Overdraft Protection, we transfer/advance available funds in your linked account(s) to your checking account when needed to cover your transaction(s) You can link up to two accounts (one savings, one credit) but we will charge you only one fee, even if we need to move money from more than one account Also, we will not charge a fee unless the transfer/advance helped you avoid at least one overdraft or returned item If you link two accounts, you may tell us which account to use first to transfer/advance funds If you do not specify an order, we will first transfer funds from the linked savings account • Transfers from linked savings account We will transfer the amount needed (including

funds to cover the transactions and the transfer fee) from the available money in your linked savings account or a minimum of $25 The Overdraft Protection Transfer Fee (if any) will be charged to your checking account

• Advances from linked credit card or line of credit We will advance the exact amount needed from the available credit in a linked credit card or a minimum of $25 The Overdraft Protection Advance Fee (if any) will be charged to your credit card account Advances from an eligible linked Wells Fargo line of credit are made in increments of $100 or $300 (specific details will be provided when you link accounts) and the Overdraft Protection Advance Fee will be charged to the checking account

What is Debit Card Overdraft Service?Your eligible checking account is automatically enrolled in this optional service The service allows Wells Fargo to approve (at our discretion) your ATM and everyday (one-time) debit card transaction if you do not have enough money to cover your transaction in your checking account or in accounts linked for Overdraft Protection With this service, we may approve these transactions into overdraft and allow you to continue with your ATM withdrawaloreverydaydebitcardtransaction.However,ifyoudonotmakeacoveringdeposit or transfer before the posted cutoff time (where the deposit or transfer is made), overdraft fees will be assessed

If you remove this service and you do not have enough money in your checking account (or in accounts linked for Overdraft Protection), your ATM or everyday debit card transaction will not be approved In addition, no overdraft fees will be assessed on ATM or everyday debit card transactions that are paid from your account, even if you no longer have sufficient funds to cover previously approved transactions

What is Wells Fargo’s standard overdraft coverage? Our standard overdraft coverage is when, at our discretion, we pay checks or automatic payments(suchasACHpayment)intooverdraftratherthanreturningthemunpaid.Youcan request to remove our standard overdraft coverage from your account by speaking to a banker

Important: If you ask us to remove our standard overdraft coverage from your account, the following will apply if you do not have enough money in your account or accounts linked for OverdraftProtectiontocoveratransaction:• Wewillreturnyourchecksandautomaticpayments(suchasACHpayments)andassessa

non-sufficient funds (NSF) returned item fee and you could be assessed additional fees by merchants

• WewillnotauthorizetransactionssuchasATMwithdrawalsoreverydaydebitcardpurchases into overdraft

Available balance, posting order, and overdrafts

23

IntroductionElectronic

banking services Rights and

responsibilitiesChecking and

savings accountsStatem

ents and error notifications

Resolving disputes through arbitration

Important legal

information

Available balance, posting order, and overdrafts

• Wewillnotauthorizecertaintransactions(suchascashedchecks,recurringdebitcardtransactions,orBillPaytransactions)intooverdraft.However,ifthesetransactionsareauthorized when your account has enough money but are later presented for payment when your account does not have enough money, we will pay the transaction into overdraft and charge an overdraft fee

What is your responsibility if your account has an overdraft?If you have an overdraft on your account (including transactions we have paid on your behalf into overdraft, plus any fees), you must make a deposit or transfer promptly to return your account to a positive balance

If you fail to bring your checking account to a positive balance, we will close your account Also we may report you to consumer reporting agencies and initiate collection efforts You agree to reimburse us for the costs and expenses (including attorney’s fees and expenses) we incur

24 Business Account Agreement – Effective April 24, 2017

Are we allowed to use the funds in your accounts to cover debts you owe us?Yes, we have the right to apply funds in your accounts to any debt you owe us This is known as“setoff.”Whenwesetoffadebtyouoweus,wereducethefundsinyouraccountsbytheamount of the debt We are not required to give you any prior notice to exercise our right of setoff

A“debt”includesanyamountyouoweindividuallyortogetherwithsomeoneelsebothnowor in the future It includes any overdrafts and our fees We may setoff for any debt you owe us that is due or past due as allowed by the laws governing your account If your account is a joint account, we may setoff funds in it to pay the debt of any joint owner

If your account is an unmatured time account (or CD), then we may deduct any early withdrawal fee or penalty This may be due as a result of our having exercised our right of setoff

Do you grant us a security interest in your accounts with us?Yes, to ensure you pay us all amounts you owe us under the Agreement (e g , overdrafts and fees), you grant us a lien on and security interest in each account you maintain with us By opening and maintaining each account with us, you consent to our asserting our security interest should the laws governing the Agreement require your consent Our rights under this security interest are in addition to and apart from any other rights under any other security interest you may have granted to us

Can you grant anyone else a security interest in your accounts with us?No, you may not grant a security interest in, transfer, or assign your accounts to anyone other than us without our written agreement

Setoff and security interest

25

IntroductionElectronic

banking services Rights and

responsibilitiesChecking and

savings accountsStatem

ents and error notifications

Resolving disputes through arbitration

Important legal

information

Bank fees and expenses; Earnings allowance

Are you obligated to pay our fees? Yes, you agree to pay us in accordance with our Business Account Fee and Information Schedule You also agree to pay an amount equal to any applicable taxes, however designated, exclusive of taxes based on our net income

How do you pay our fees and expenses?We are permitted to either directly debit your account or invoice you for our fees and expenses and taxes incurred in connection with your account and any service If there are non-sufficient funds in your account to cover the debit, we may create an overdraft on your account

You agree to promptly pay any invoiced amount We may assess finance charges on any invoiced amounts that are not paid within 45 days of the date of invoice Finance charges are assessed at a rate of 1 5% per month (18% per annum) or the highest amount permitted by the laws governing your account, whichever is less Charges for accrued and unpaid interest and previously assessed finance charges will not be included when calculating finance charges Payments and other reductions of amounts owed will be applied first to that portion of outstanding fees attributable to charges for accrued and unpaid interest and previously assessed finance charges, then to other fees and charges

If an earnings allowance accrues on your account, do we apply it to our fees and expenses?Yes, if an earnings allowance accrues on your account, we will periodically apply your accrued earnings allowance to eligible fees and expenses (unless we otherwise indicate in writing) If both an earnings allowance and interest accrue on your account, the interest will be shown as an offset to the earnings allowance on the client analysis statement for your account If your earnings allowance exceeds your total maintenance and activity fees for the statement cycle for your account, the excess credit is not paid to you, nor is it carried forward to the following statement cycle We may debit your account (or any other account you maintain with us) or invoice you for any amount by which the fees and expenses exceed the accrued earnings allowance on your account The earnings allowance applied as a creditagainstfeesandexpenseswillbereportedasincometotheIRS,state,andlocaltaxauthorities if required by applicable law and you are responsible for any federal, state or local taxes due on the credited earnings allowance

26 Business Account Agreement – Effective April 24, 2017

Additional rules for checks and withdrawals

What identification do we request to cash checks presented over-the-counter by a non-customer?For these transactions, we require acceptable identification, which can include a fingerprint from the person presenting your check We may not honor the check if the person refuses to provide us with requested identification

Are there special rules if you want to make a large cash withdrawal or deposit?We may place reasonable restrictions on a large cash withdrawal These restrictions include requiring you to provide reasonable advance notice to ensure we have sufficient cash on hand We do not have any obligation to provide security if you make a large cash withdrawal If you want to deposit cash for a very large amount, we have the right to require you to provide adequate security or exercise other options to mitigate possible risks

Are we responsible for reviewing checks for multiple signatures?No, we are not responsible for reviewing the number of signatures required on your account If you have indicated that more than one signature is required, we will not be liable if a check does not meet this requirement

Are we required to honor dates and special instructions written on checks?No, we may, without inquiry or liability, pay a check even if it• Hasspecialwritteninstructionsindicatingweshouldrefusepayment(e.g.,“Voidafter30

days”or“Voidover$100”);• Isstale-dated(i.e.,thecheck’sdateismorethan6monthsinthepast),evenifweare

aware of the check’s date;• Ispost-dated(i.e.,thecheck’sdateisinthefuture);or• Isnotdated.

WemayalsopaytheamountencodedonyourcheckinU.S.dollars,evenifyouwrotethecheck in a foreign currency or made a notation on the check’s face to pay it in a foreign currency The encoded amount is in the line along the bottom edge of the front of the check where the account number is printed

Can you use a facsimile or mechanical signature?Yes, if you use a facsimile or mechanical signature (including a stamp), any check appearing to use your facsimile or mechanical signature will be treated as if you had actually signed it

Are you liable if you pay a consumer ACH debit entry on my account?No,undertheACHoperatingrules,certaintypesofACHdebitentriesmayonlybepresentedonaconsumeraccount(each,a“consumerACHdebitentry”).Wewillhavenoobligationtopay,andnoliabilityforpaying,anyconsumerACHdebitentryonyouraccount.

What is the acceptable form for your checks?Your checks must meet our standards, including paper stock, dimensions, and other industry standards Your checks must include our name and address, as provided by us Certain check features, such as security features, may impair the quality of a check image that we or a third party create

We reserve the right to refuse checks that do not meet these standards or cannot be processed or imaged using our equipment We are not responsible for losses that result from your failure to follow our check standards

27

IntroductionElectronic

banking services Rights and

responsibilitiesChecking and

savings accountsStatem

ents and error notifications

Resolving disputes through arbitration

Important legal

information

Issuing stop payment orders and post-dated checks

How do you stop payment on a check?You may request a stop payment on your check in a time and manner allowing us a reasonable opportunity to act on it before we pay, cash, or otherwise become obligated to pay your check

Each stop payment order is subject to our verification that we have not already paid or otherwise become obligated to pay the check from your account This verification may occur after we accept your stop payment order

Inordertoissueastoppaymentorderonacheck,werequestthefollowinginformation:• Yourbankaccountnumber,• Thechecknumberorrangeofnumbers,• Thecheckamountoramounts,• Thepayee(s)name(s),and• Thedateonthecheck.

We are not responsible for stopping payment on a check if you provide incorrect or incomplete information about the check

What is the effective period for a stop payment order?A stop payment order on a check is valid for 6 months We may pay a check once a stop payment order expires You must place a new stop payment order if you do not want it to expire We treat each renewal as a new stop payment order We will charge you for each stop payment order you place (as well as each renewal)

How do you cancel a stop payment order?To cancel a stop payment order, we must receive your request in a time and manner allowing us a reasonable opportunity to act on it

Are you still responsible if we accept a stop payment on a check?Yes, even if we return a check unpaid due to a stop payment order, you may still be liable to the holder (e g , a check cashing business) of the check