important considerations for the do-it-yourself (diy) investor

DESCRIPTION

Important Considerations For The Do-It-Yourself (DIY) Investor. Presentation to AAII Baltimore 1/09/2010 By Robert Wasilewski, President RW Investment Strategies. DIY: Agenda. Background Emotional Roller Coaster DIY Investor Advantages Save investment management costs - PowerPoint PPT PresentationTRANSCRIPT

Presentation to AAII Baltimore1/09/2010

By Robert Wasilewski, PresidentRW Investment Strategies

Background Emotional Roller Coaster DIY Investor Advantages

◦ Save investment management costs◦ Understand philosophy and process

What the DIYer Needs to Do and to Know Suggested Approach Conclusions

Background

Pension fund Insurance Company Investment Manager

Bank Trust Departments Private Money Managers

Active Management Indexed

Emotions continued to play havoc with investor returns in 2008. DALBAR’s update of its Quantitative Analysis of Investor Behavior (QAIB) study found that, while the S&P 500 has returned 8.35% over a 20-year period ending in 2008, the average equity investor earned just 1.87%, which was less than the inflation rate of 2.89%. Bond investors fared no better. They earned returns of just 0.77% compared to 7.43% for the index.

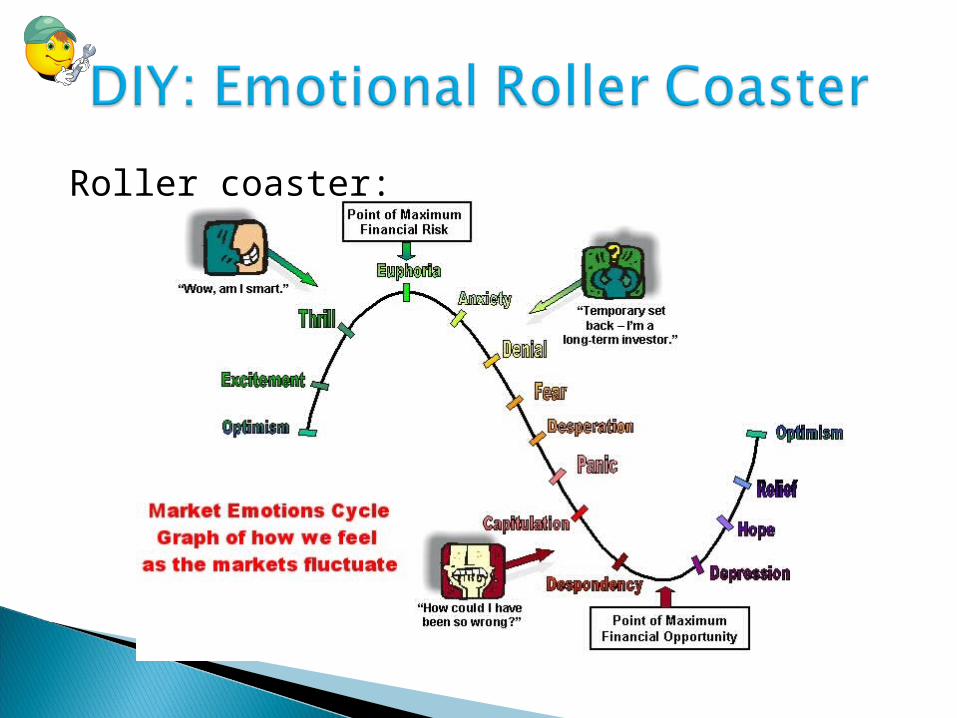

Roller coaster:

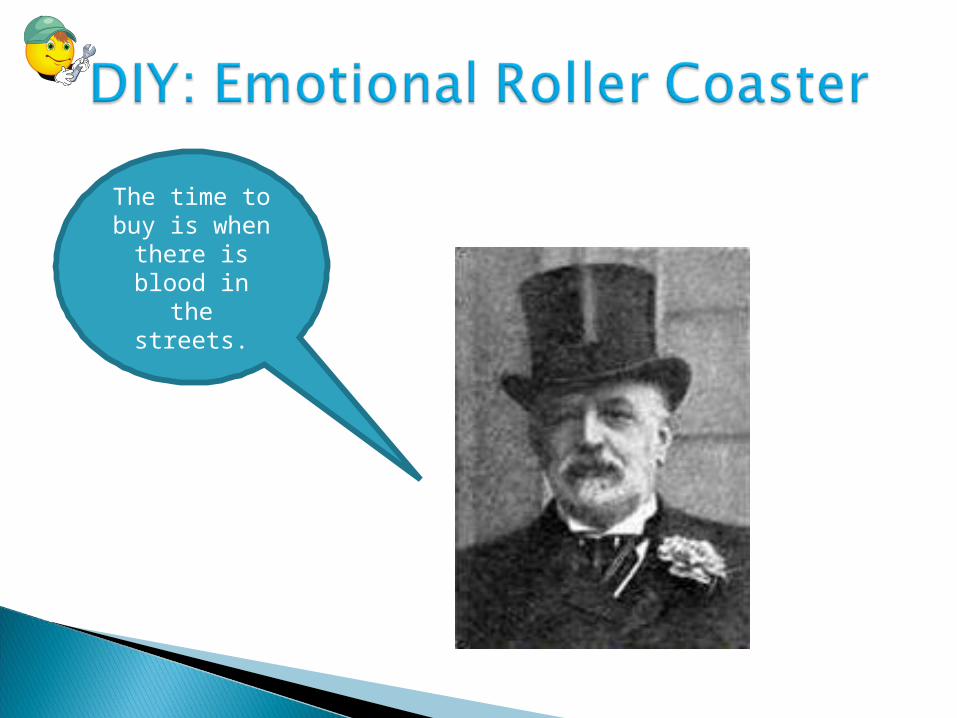

The time to buy is when

there is blood in the streets.

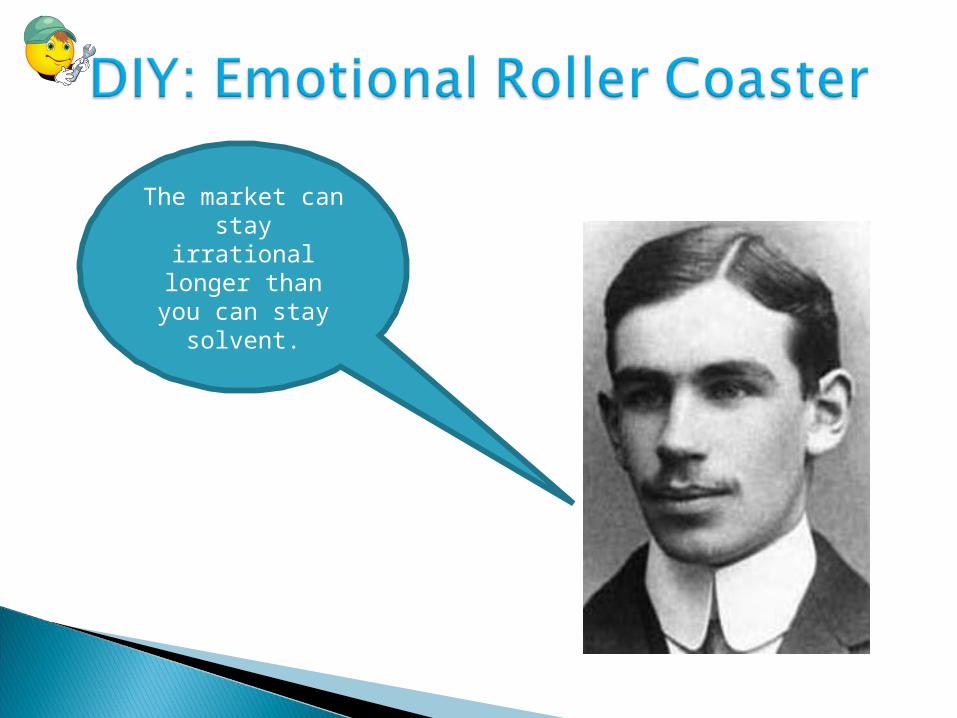

The market can stay irrational

longer than you can stay solvent.

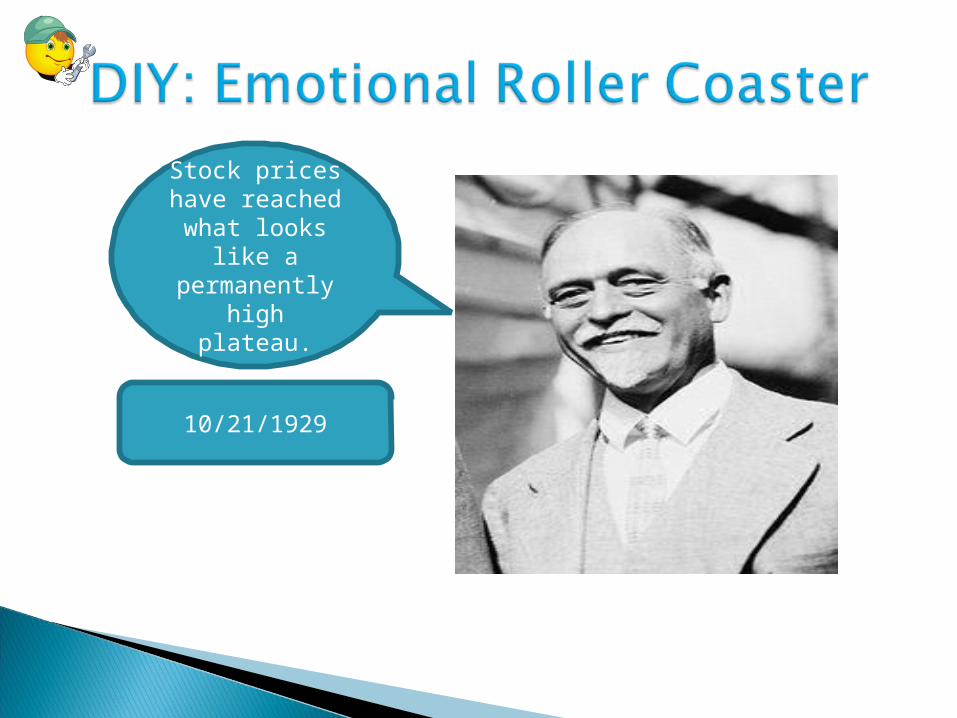

Stock prices have reached what looks like a permanently high plateau.

10/21/1929

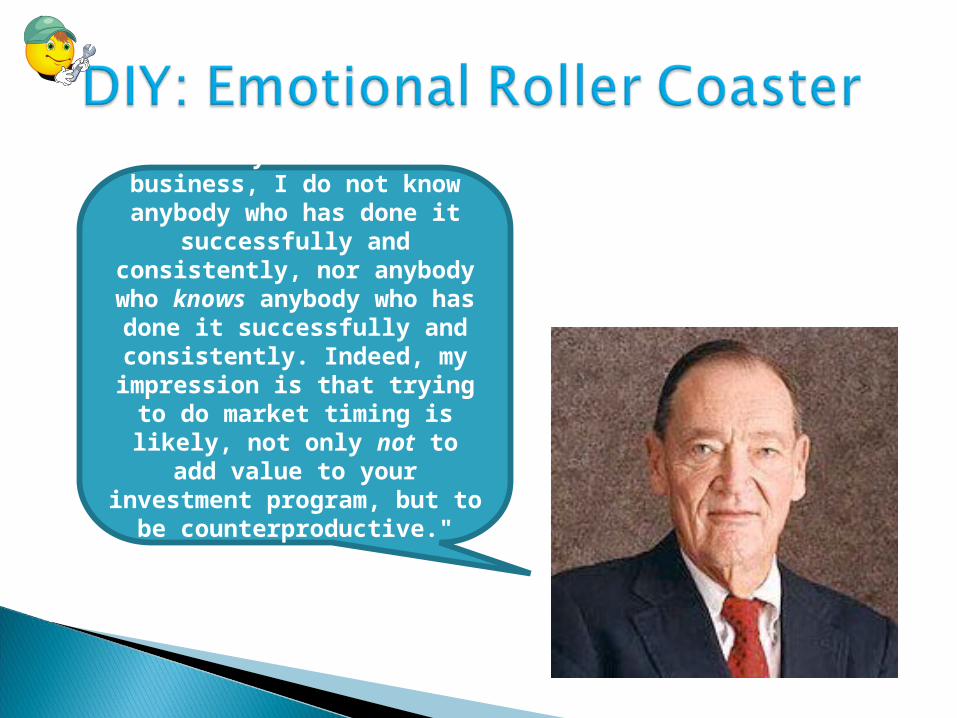

"In 30 years in this business, I do not know

anybody who has done it successfully and

consistently, nor anybody who knows anybody who has done it successfully

and consistently. Indeed, my impression is that

trying to do market timing is likely, not only not to add

value to your investment program, but to be counterproductive."

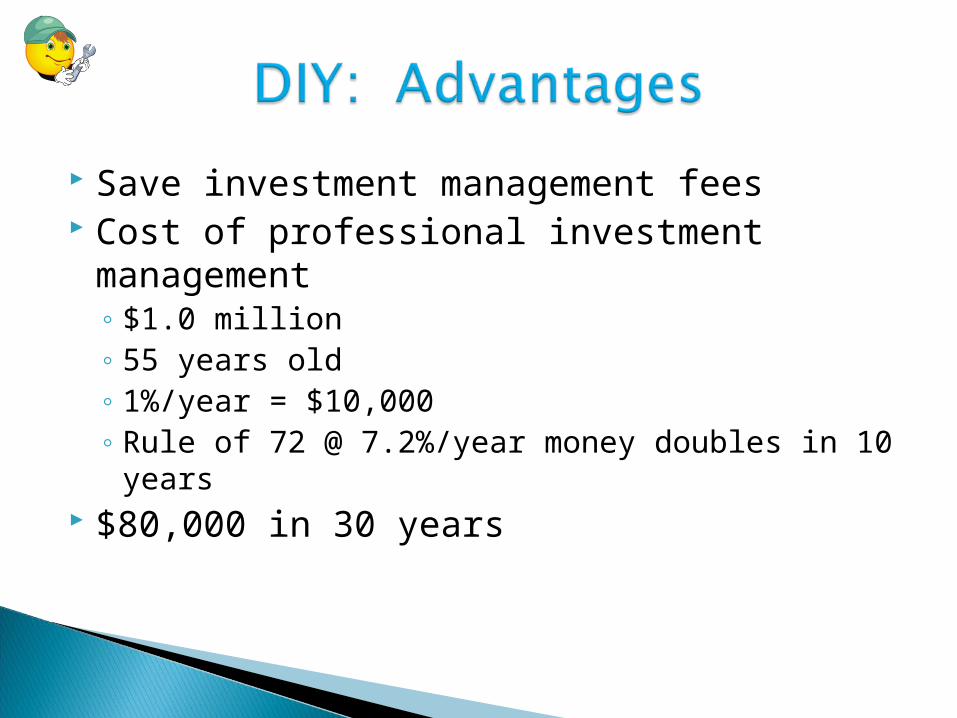

Save investment management fees Cost of professional investment

management◦ $1.0 million◦ 55 years old◦ 1%/year = $10,000◦ Rule of 72 @ 7.2%/year money doubles in 10

years $80,000 in 30 years

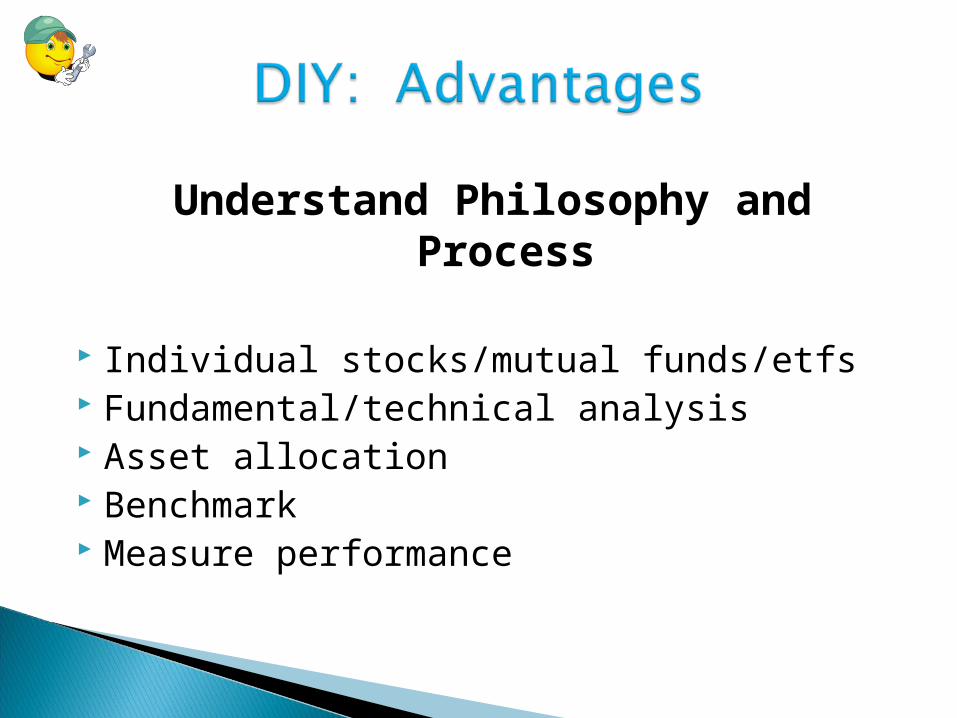

Understand Philosophy and Process

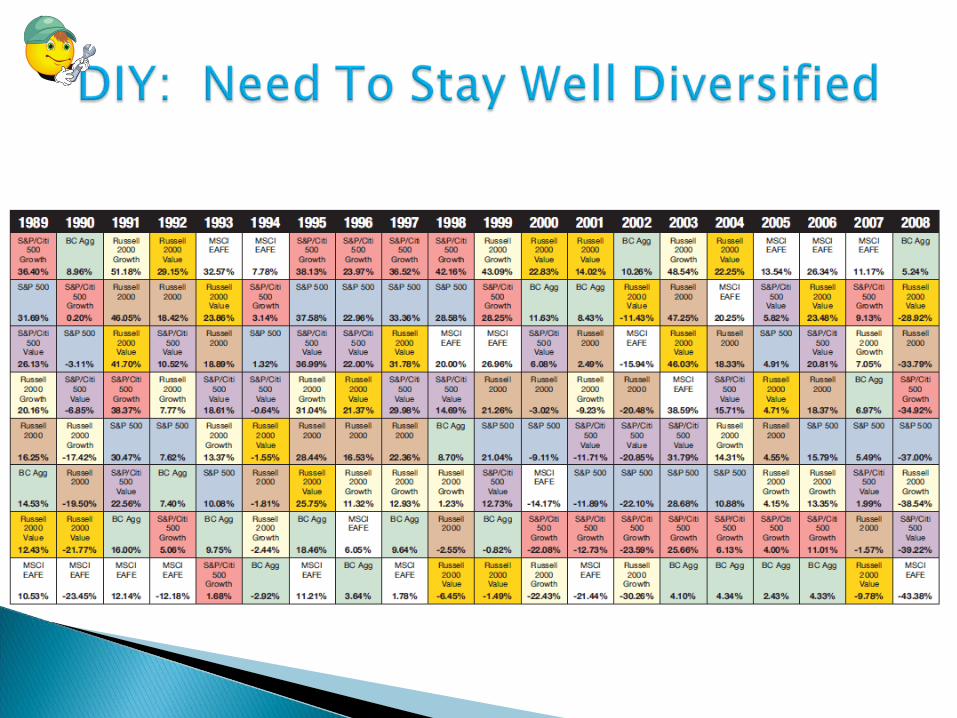

Individual stocks/mutual funds/etfs Fundamental/technical analysis Asset allocation Benchmark Measure performance

Individual security risk and industry riskMarket risk

◦Portfolio allocation

OBJECTIVE: SIMPLIFY

◦ By Broker

◦ By Account Type (Rollover 401 (k)s to IRAs)

***NUA

◦ Avoid “reverse $ cost averaging” when drawing down your “nest egg”

◦ Try not to draw down more than 5% (adjusted for inflation) of your “nest egg”

◦ Put interest-bearing investments in qualified accounts and earn qualified dividends and long- term cap gains in taxable accounts

◦ Draw down taxable accounts first◦ Be careful reaching for yield◦ Establish fund for withdrawals to weather

downturns

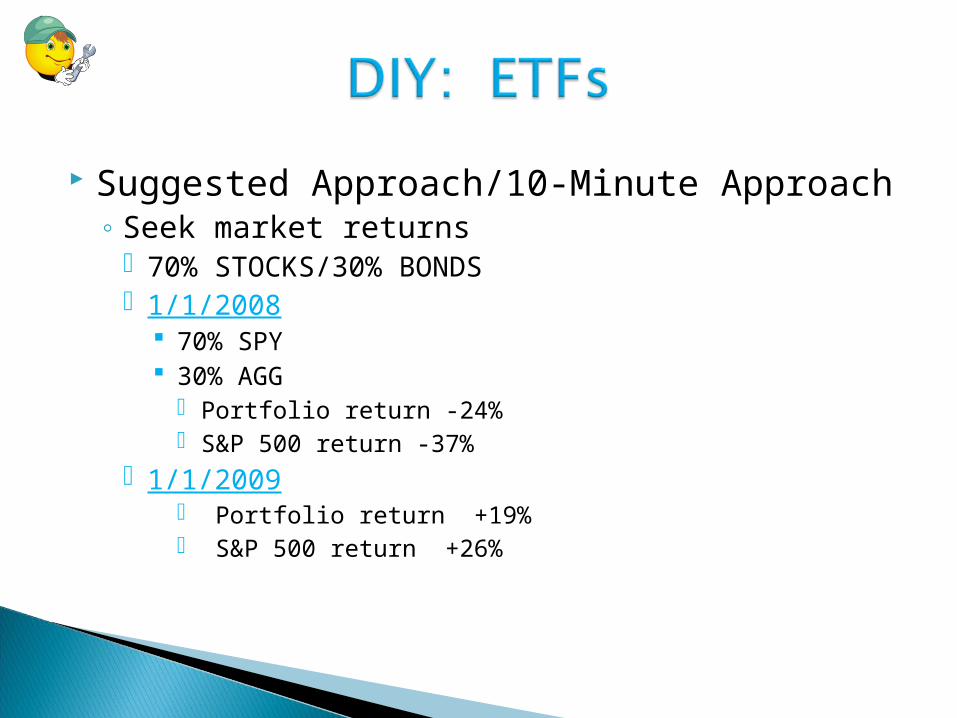

Suggested Approach/10-Minute Approach◦ Seek market returns

70% STOCKS/30% BONDS 1/1/2008

70% SPY 30% AGG

Portfolio return -24% S&P 500 return -37%

1/1/2009 Portfolio return +19% S&P 500 return +26%

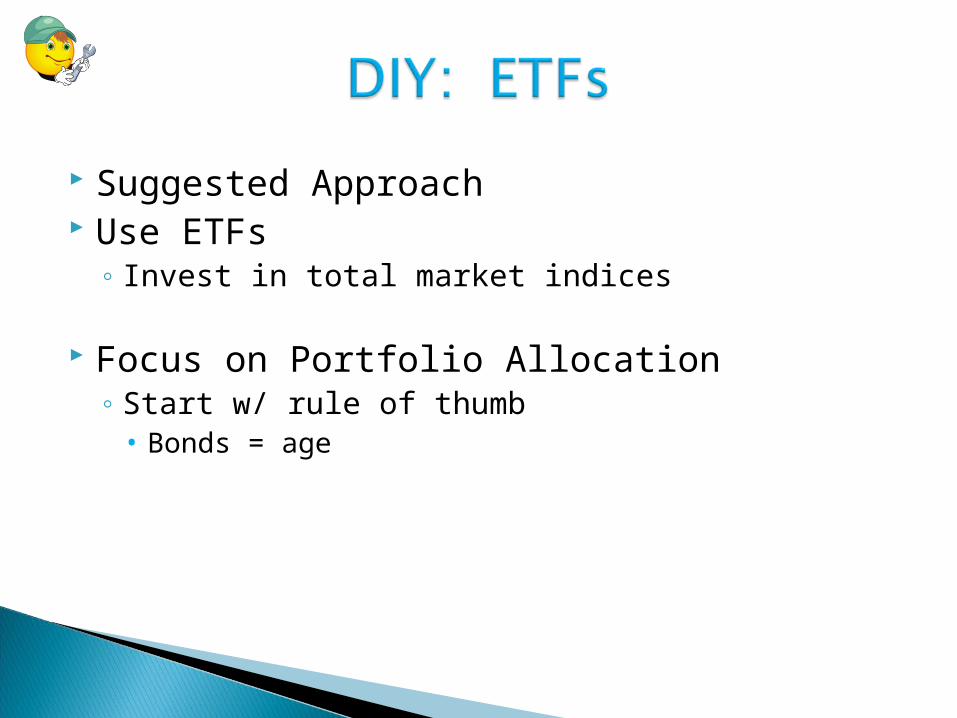

Suggested Approach Use ETFs

◦ Invest in total market indices

Focus on Portfolio Allocation◦ Start w/ rule of thumb• Bonds = age

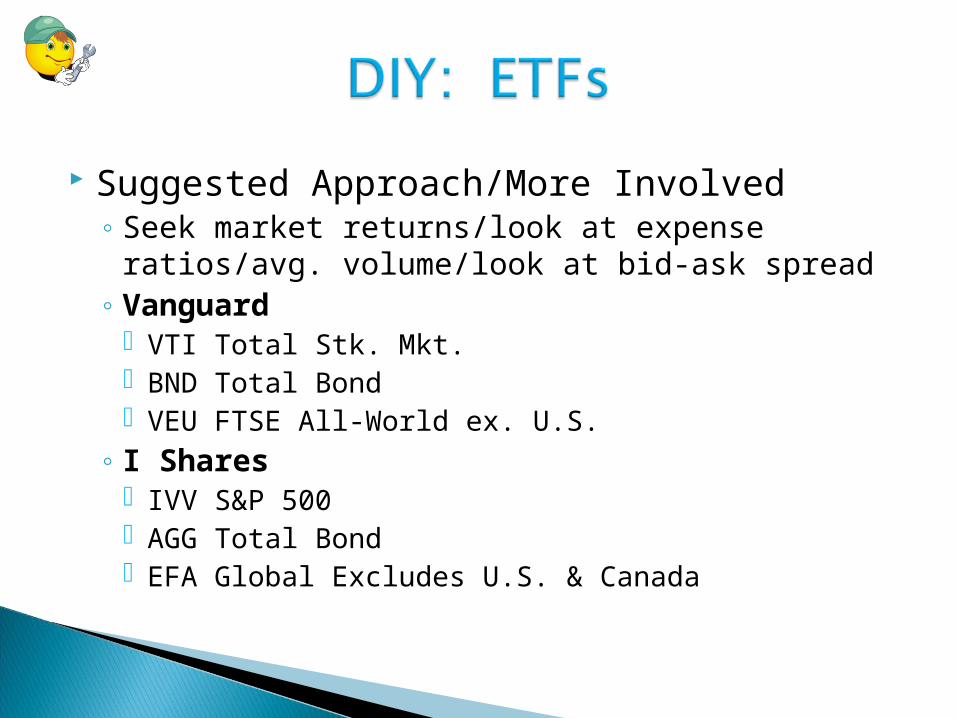

Suggested Approach/More Involved◦ Seek market returns/look at expense ratios/avg.

volume/look at bid-ask spread◦ Vanguard

VTI Total Stk. Mkt. BND Total Bond VEU FTSE All-World ex. U.S.

◦ I Shares IVV S&P 500 AGG Total Bond EFA Global Excludes U.S. & Canada

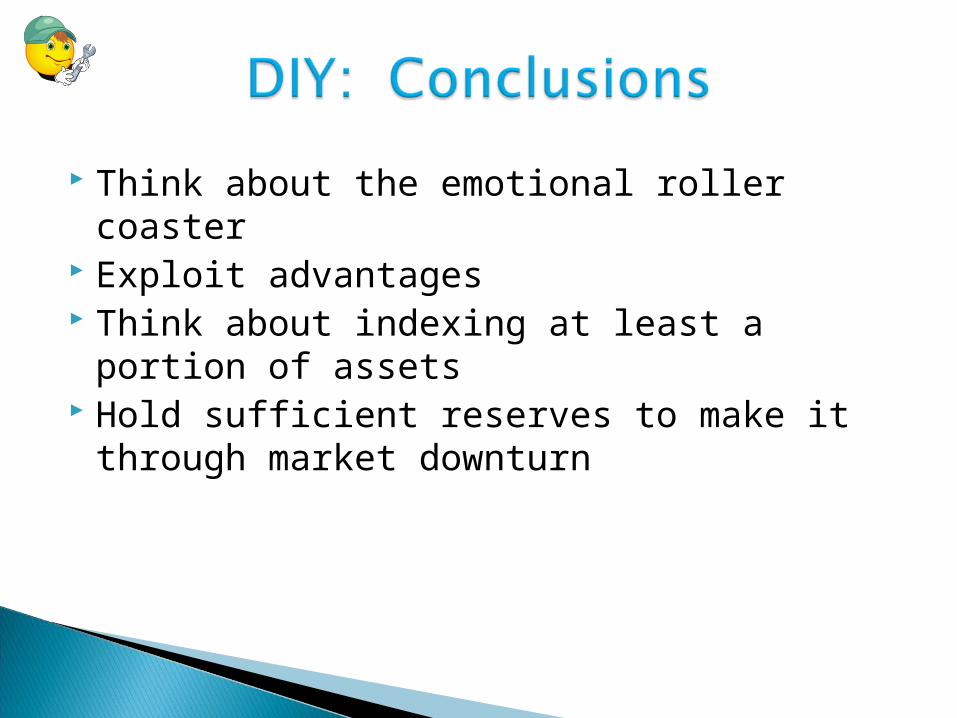

Think about the emotional roller coaster Exploit advantages Think about indexing at least a portion of

assets Hold sufficient reserves to make it through

market downturn

Hourly consulting◦ “Do-it-yourself” investor◦ Second opinions◦ Company presentations

Investment Management◦ Low fee indexed approach