implications for automotive, agriculture & energy · 2005 2010 2015 2020 2025 2030 potential...

TRANSCRIPT

Implications forAutomotive, Agriculture & Energy

Summary Marketing Presentation

Copyright © 2007 Global Insight, Inc. 2

The Biofuels Boom

Copyright © 2007 Global Insight, Inc. 3

Three Major Policy Drivers……ARE THEY COMPATIBLE?

EnvironmentEnvironment

Reduce criteria emissions at local, urban, metro, and national levelsReduce greenhouse gas emissions

AgricultureAgriculture

Create new markets for agricultural cropsReduce subsidies

EnergyEnergy

Energy securityReduce dependency on petroleum-based energy sourcesDiversify energy sources

Copyright © 2007 Global Insight, Inc. 4

Strategic Questions Addressed in The Biofuels Boom

• What are the global drivers of biofuels consumption?

• What role do the major economic powers play in biofuels growth?

• What is the range of long-term policy objectives?

How will they vary from country to country and at the regional and local levels?How will policy influence the creation of a commercially viable biofuels industry?

• Will these policies remainsynchronized in the future?

Copyright © 2007 Global Insight, Inc. 5

Strategic Questions Addressed in The Biofuels Boom

• How is the biofuels infrastructure evolving internationally?

• What is the current state of technology and how will it develop?

• What is the tipping point where biofuels will impact the energy, agriculture, and automotive markets?

• What are the expectations and limits to growth in the biofuels industry?

Copyright © 2007 Global Insight, Inc. 6

Two Global Scenarios are Evaluated

Alternative Future ScenariosAlternative Future ScenariosBased on Market’s Current Views

Market RemanagedMarket RemanagedReference Case

OPEC re-emerges as the market ‘governor’OPEC Price Management:

Attempts to manage price in the low $60/bbl range

OPEC re-emerges as the market ‘governor’OPEC Price Management:

Attempts to manage price in the low $60/bbl range

Supply ConstrainedSupply Constrained

New Oil Market Era: Supply/demand balance on demand, not supply.

Prices Spike:Unprecedented price levels of more that $100/bbl

The Industry Must Consider the AlternativesDramatically Different Implications, Paths, and Consequences

Global Climate Change regulations are taken as a predetermined condition in both scenarios

Copyright © 2007 Global Insight, Inc. 7

FUEL TYPES

Study Covers Multiple Feedstocks and Products

FEEDSTOCKSCORN SUGAR BEETS SWITCH GRASS &

WOOD CHIPS(NEXT GENERATION FUELS)

SUGAR CANE SOYBEANS CROP RESIDUES (NEXT GENERATION FUELS)

WHEAT & BARLEY RAPESEED, JATROPHA OIL, PALM OIL (BIO-DIESEL)

OTHER NON-CONVENTIONAL SOURCES (E.G.,ALGAE)

(Study does not include alternative fuels such as LPG, LNG, CNG, hydrogen, gas-to- liquids, or coal-to-liquids)

2ND GENERATION BIOFUELS

BIODIESELBIOETHANOL

Copyright © 2007 Global Insight, Inc. 8

Multiple Technologies Are Examined

Biomass Propagation, Growth, Harvesting, and CollectionBiomass PretreatmentBiomass Conversion Biochemical (Sugar) RouteBiomass Conversion Thermochemical Route

• Gasification• Pyrolysis

Biodiesel and Renewable DieselBiobutanol

Copyright © 2007 Global Insight, Inc. 9

Commercial and Economic Feasibility of Technologies

Biomass Growth & Collection

Biomass Pre-

treatment

Biomass Biochemical Conversion

Biomass Gasification /Conversion

Biomass Pyrolysis Biodiesel Green Diesel Biobutanol

Breakthroughs Required

Politics & Regulatory Facing Challenges

Feedstock Supply

Inbound Logistics

Processing

Market Compatibility

Product Quality

Outbound Logistics

GHG/Environmental

Overall Economics

Commercial or likely to be

Success likely but development needed

Not known/depends on application

Pilot/or demo; success still to be determined

Major hurdle or cost to success

Copyright © 2007 Global Insight, Inc. 10

The Study also Looks at a Variety of Biofuels Crops

Feedstock Screening Criteria Corn Ag

Wastes Grasses PoplarPulp & Paper

Wastes

Vegetable Oils Jatropha Algae Oil MSW

Animal Fats &

Oils

Stage of Development

Likely Availability

Harvesting & Collection

Pretreatment

Quality

Cost

GHG/Environment

Food vs. Fuel

Commercial or likely to be

Success likely but development needed

Not known/depends on application

Pilot/or demo; success still to be determined

Major hurdle or cost to success

Copyright © 2007 Global Insight, Inc. 11

0

10

20

30

40

50

60

70

80

2005 2010 2015 2020 2025 2030 PotentialProduction

Bill

ions

of g

allo

ns

Market Remanaged

0

1

2

3

4

2005 2010 2015 2020 2025 2030 PotentialProduction

Bill

ions

of g

allo

ns

Market Remanaged

Supply/Demand Forecasts: BioethanolRegions Covered:

U.S. Bioethanol Supply/Demand EU Bioethanol Supply/Demand

• U.S. growth in bioethanol projected to reach 15 billion gallons by 2015 (about 1 mmb/d)

Supp

ly

Supp

ly

• EU growth to be limited by local supply and must rely on imports from Africa and South America

Demand Forecast Demand

Forecast

• European Union• Brazil

• China• India

• World• United States

• Africa

Copyright © 2007 Global Insight, Inc. 12

0

2

4

6

8

10

2005 2010 2015 2020 2025 2030 PotentialProduction

Bill

ions

of g

allo

ns

U.S. Biodiesel

0

2

4

6

8

2005 2010 2015 2020 2025 2030 PotentialProduction

Bill

ions

of g

allo

ns

EU Biodiesel

Supply/Demand Forecasts: Biodiesel

• Biodiesel demand and potential supply can be based on non-edible oils such as jatropha, algae, wood waste, and other non-food products

Demand Forecast

Demand Forecast

U.S. Biodiesel Supply Remanaged EU Biodiesel Supply Remanaged

• New technologies employing biomass conversion into liquids look promising such as NExBTL by Neste

Supp

ly

Supp

ly

Copyright © 2007 Global Insight, Inc. 13

Implications On-Road Petroleum Demand

• Biofuels (e.g., ethanol and diesel) will increase significantly possibly reaching 15% of motor fuel pool world-wide

• Under different scenarios, the United States could reach 35% of on-road petroleum demand — in same range as Brazil

• Biomass producers will be in advantageous position to produce renewable fuel feedstocks

• The move will affect oil and gas producers in the United States and Canada by shifting from petroleum-based fuels.

0% 5% 10% 15% 20% 25% 30% 35% 40%

World

United States

Europe

Asia-Pacific

Brazil

Other Latin America

Africa

Middle East

Rest of the World

Percent by Volume

Market Remanaged

Supply Constrained

Biofuel Shares of On-Road Petroleum Demand in 2030

Copyright © 2007 Global Insight, Inc. 14

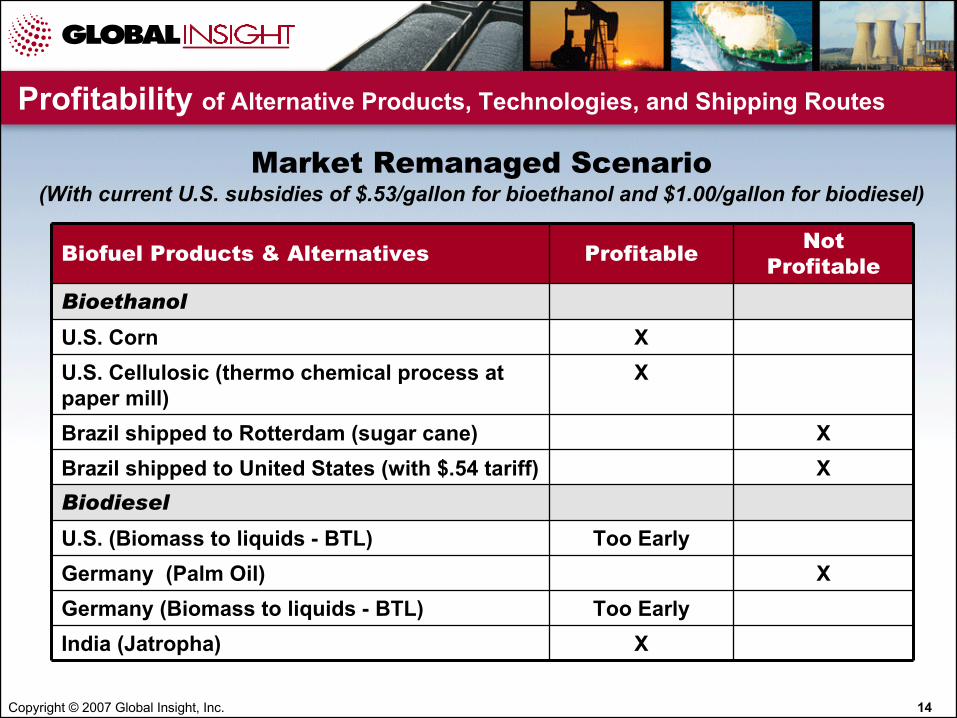

Profitability of Alternative Products, Technologies, and Shipping Routes

Biofuel Products & Alternatives Profitable Not Profitable

Bioethanol

U.S. Corn XU.S. Cellulosic (thermo chemical process at paper mill)

X

Brazil shipped to Rotterdam (sugar cane) XBrazil shipped to United States (with $.54 tariff) XBiodiesel

U.S. (Biomass to liquids - BTL) Too EarlyGermany (Palm Oil) XGermany (Biomass to liquids - BTL) Too EarlyIndia (Jatropha) X

Market Remanaged Scenario(With current U.S. subsidies of $.53/gallon for bioethanol and $1.00/gallon for biodiesel)

Copyright © 2007 Global Insight, Inc. 15

Implications for the Automotive Industry

• Based of survey of automotive manufacturers and analyses by Global Insight’s Automotive Group:

High volumes of biofuels in the United States will almost certainly require flex-fuel vehicles (FFVs) capable of running on blends up to 85% ethanol (E85)

In Europe, ethanol content is held for most countries to 10% (E10), which is technically compatible in current vehicles

Biodiesel levels of 5% (B5) are possible in virtually all vehicles, and new vehicles can be developed to accept blends up to 30% (B30)

Technical fixes to meet higher biofuels levels are known, but will add some costs to vehicles

Copyright © 2007 Global Insight, Inc. 16

Market RemanagedMarket Remanaged Supply ConstrainedSupply Constrained

Aggressive Increases in Vehicle Efficiency Standards in U.S.

• 2018: New vehicle fleet fuel economy reaches 32 mpg

(193 g/km CO2)

• 2030: New vehicle fleet fuel economy reaches 48 mpg

(128 g/km CO2)

• 2020: New vehicle fleet fuel economy reaches 45 mpg

(137 g/km CO2)Requires 60% hybridization in the United States

• 2030: New vehicle fleet fuel economy reaches 53 mpg

(117 g/km CO2)

Copyright © 2007 Global Insight, Inc. 17

Market RemanagedMarket Remanaged Supply ConstrainedSupply Constrained

EU also Needs to Tighten Fuel Efficiency Standards

• 2012: EU standard of 130 g/km CO2 emissions (without biofuels benefit) could be met

• 2018: EU new vehicle CO2emissions reach 120 g/km (without renewable fuel credit) and holds at this level to the end of the period

• 2012: EU standard of 130 g/km CO2 emissions (without biofuels benefit) could be met

• 2018: EU new vehicle CO2emissions reach 120 g/km

• 2025: EU new car efficiency is 90 g/km CO2

Copyright © 2007 Global Insight, Inc. 18

Implications for Hybrid Vehicles

• Hybrid vehicles are introduced across all major (high volume) model lines

• Hybrid diesels are introduced

• As cost of hybrid components decreases, the diesel-hybrid combination becomes attractive as a market differentiator

Hybrid vehicles will play a significant role in the United States to meet

stringent efficiency targets

Copyright © 2007 Global Insight, Inc. 19

Diesels will Continue to Play a Significant Role in EU

• 2008: Diesel cars trend at 50–60% of the new car fleet

• 2009: Diesel hybrids enter the market as mechanism for meeting fuel efficiency CO2 emissions targets

• 2015: Diesel vehicles are 65% of the new light duty vehicle fleet

• 2030: Diesels are 35% of light duty vehicle fleet and at least 25% of the on-road fleet

Copyright © 2007 Global Insight, Inc. 20

Who Should Participate?

InvestorsInvestors

Agri-BusinessAgri-Business

AutomotiveAutomotive

EnergyEnergy

Policy & GovernmentPolicy & Government

Biofuels IndustryBiofuels Industry

TransportationTransportation

Equipment ManufacturerEquipment Manufacturer

Copyright © 2007 Global Insight, Inc. 21

Final Report: Abridged Table of Contents

• EXECUTIVE SUMMARY• OIL PRICES & SCENARIOS

• Possible Future Oil Price Paths• Scenario Assumptions

• GOVERNMENT POLICY: MAJOR BIOFUELS DRIVER• Policy Goals Are Evolving• Review of Existing Biofuels Policies• Assumptions about Future Policy Development

• AGRICULTURE SECTOR RESPONSE• First-Generation Ethanol Boosted by Gains in Yields• Food vs. Fuel: Some Limitations, Especially for Biodiesels• Agriculture Industry's Future Role in Biofuels

• BIOFUELS TECHNOLOGY SCREENING & STATUS• Feedstock Screening Summary• Technology Screening Summary• Biomass Propagation, Growth, Harvesting, and Collection• Biomass Pretreatment• Biomass Conversion: Biochemical (Sugar) Route,

Thermochemical Route – Gasification and Thermochemical Route - Pyolysis

• Biodiesel and Renewable Diesel• Biobutanol

• LIFE-CYCLE GREENHOUSE GAS EMISSIONS: AN EMERGING DRIVING FORCE FOR BIOFUELS

• BIOFUELS ECONOMICS• Biofuels Prices Relative to Petroleum• Cost Analysis/Cost Escalators• Experience Curves• Biofuels Costs: Results• Biofuels Margins: Profitability Comparisons• Feedstock Prices and Break-Even Values

• BIOFUELS PRODUCTION BY TYPE & REGION• Supply Evolution• Projected Production Potential: Summary• Implications for Industry Structure: Agriculture or Refining?

• BIOFUELS DEMAND: OVERVIEW & ANALYSIS• Biofuels Requirements Are Increased Around World• Total Motor Fuel Demand Growth Will Be Limited• Deviations in Supply Constrained Scenario

• REGIONAL DEMAND & SUPPLY OUTLOOK• Regional Ethanol Demand and Potential Production• Regional Bio-based Diesel Demand and Potential Production

• REFINING IMPLICATIONS• Refining Industry Impacts: Ethanol Blending and Biobutanol• Refiners: Some Synergies

• AUTOMOTIVE INDUSTRY RESPONSE• Flex-Fuel Vehicles• Ethanol Blends• Bio-based Diesel Blends• OEMs: Biofuel Conclusions• Fuel Efficiency Improvements

Copyright © 2007 Global Insight, Inc. 22

Project Team

Kevin LindemerRefining Sector Agricultural Economics

Phil GottAutomotive Technology

Stewart RamseyAgricultural Economics

Juliette KerrLatin American Biofuels Industry Policy & Analysis

Joseph AudetteAutomotive Sector

Sarah KingsburyAutomotive Sector

Dennis BanasiakTechnology Development Economics

Mary NovakEnergy Policy & Modeling

Margaret RhodesEnergy Policy & Modeling

Copyright 2007 Global Insight, Inc. 22

Copyright © 2007 Global Insight, Inc. 23

Previous Studies in Biofuels by Global Insight

• Study of the Global Biofuels Market to Identify Business Opportunities – 2006

• U.S. Federal Highway Administration: Forecasting Revenues from Highway Trust Fund

• Global: Biofuels – The Next Step Towards Environmentally Neutral Transportation?

• National Railroad – Prospects for U.S. Ethanol Production• White Paper: The Potential for Increased Market Share for

Alternative Fuels• Study: Winners and Losers of Ethanol Mandates• Identification and Assessment of Alternative Fuels Market

Drivers

For Additional InformationDavid CallananGlobal Insight Energy+33(0)[email protected]

WWW.GLOBALINSIGHT.COM/ENERGY

Mack BrothersGlobal Insight [email protected]