implementing a new accounting...

TRANSCRIPT

Implementing a New Accounting StandardGASB Statement Nos. 49 and 51 & FASB Staff

Position (FSP) FAS 117-1

Chris BronsdonDirector of Financial Reporting

San Diego State University

Goals

• Think about what resources are available to you as the GAAPer on your campus.

• Understand what things to be looking for and what the “bottlenecks” might be.

• Collaborate as a group to think about issues, problems, and solutions (this means your participation is welcomed).

GASB Statement No. 49, Accounting and Financial Reporting for Pollution Remediation Obligations

• Approach to resources– KPMG training (even reviewing the slides is good)

• We had our Director of Environmental Health & Safety do the training

– Read the Standard• It’s only 27 paragraphs• Read it twice

– Chapter Z: Other Implementation Guidance of the GASB Staff Implementation Guide

– CSU GAAP Manual: new Section 4-12

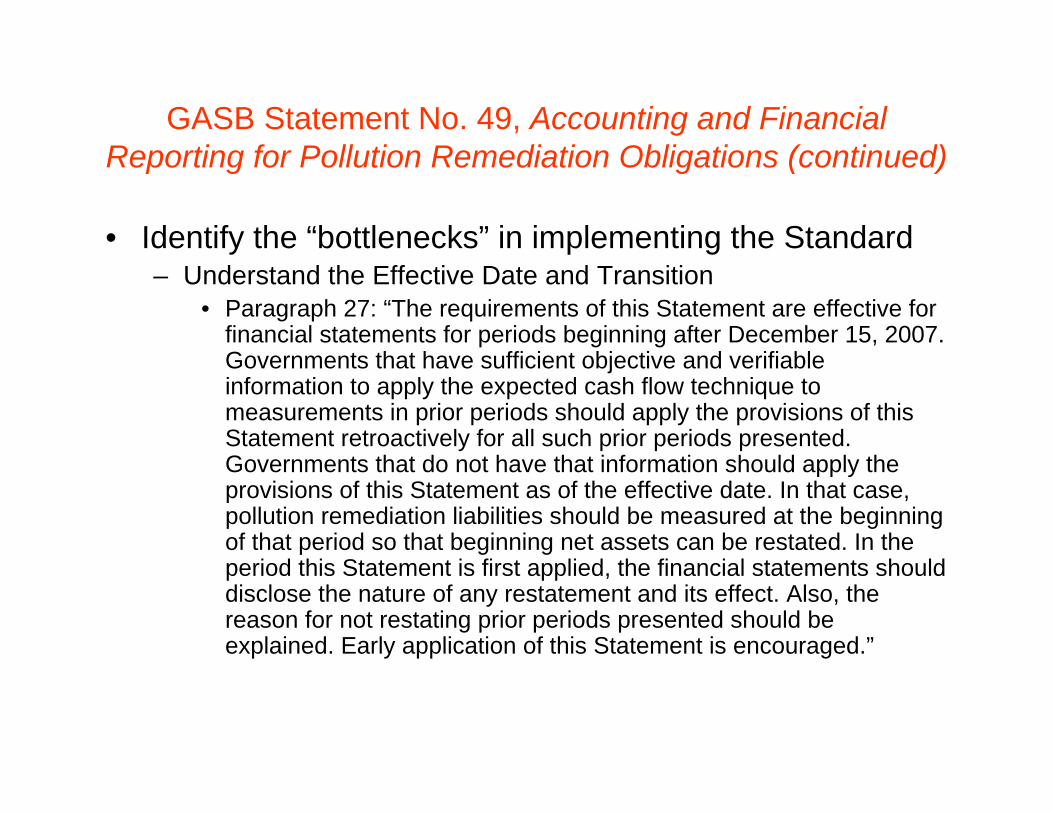

GASB Statement No. 49, Accounting and Financial Reporting for Pollution Remediation Obligations (continued)

• Identify the “bottlenecks” in implementing the Standard– Understand the Effective Date and Transition

• Paragraph 27: “The requirements of this Statement are effective for financial statements for periods beginning after December 15, 2007. Governments that have sufficient objective and verifiable information to apply the expected cash flow technique to measurements in prior periods should apply the provisions of this Statement retroactively for all such prior periods presented. Governments that do not have that information should apply the provisions of this Statement as of the effective date. In that case, pollution remediation liabilities should be measured at the beginning of that period so that beginning net assets can be restated. In the period this Statement is first applied, the financial statements should disclose the nature of any restatement and its effect. Also, thereason for not restating prior periods presented should be explained. Early application of this Statement is encouraged.”

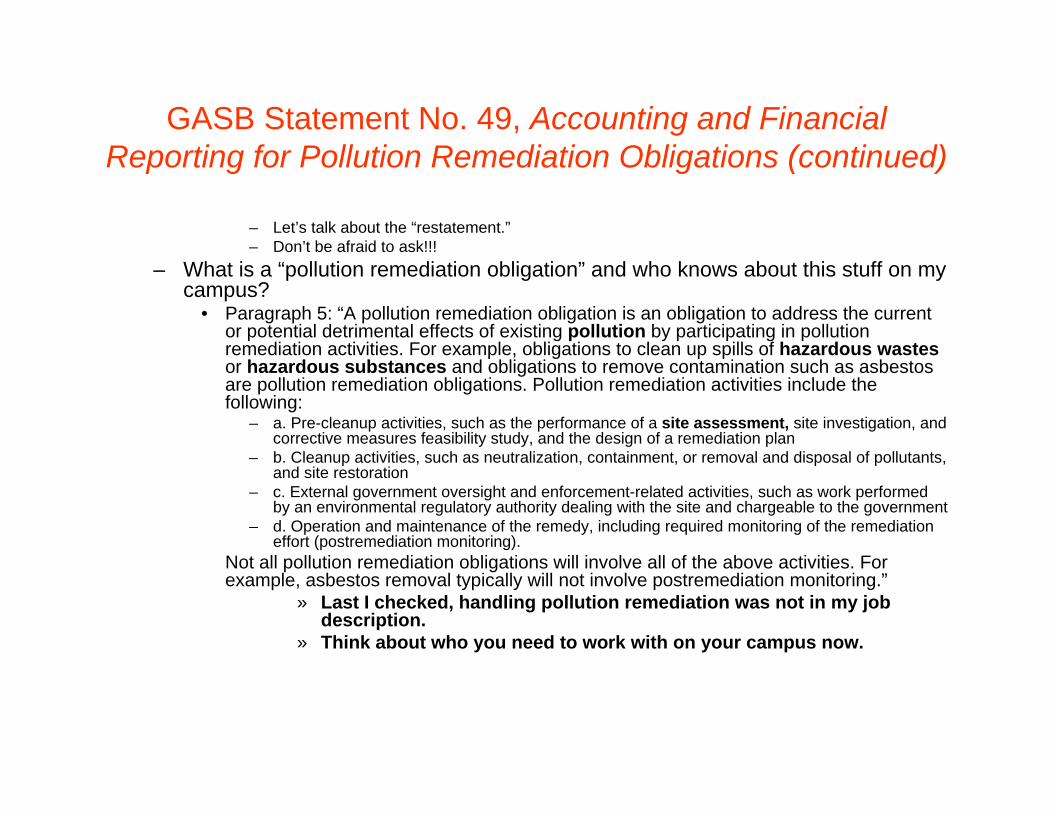

GASB Statement No. 49, Accounting and Financial Reporting for Pollution Remediation Obligations (continued)

– Let’s talk about the “restatement.”– Don’t be afraid to ask!!!

– What is a “pollution remediation obligation” and who knows about this stuff on my campus?

• Paragraph 5: “A pollution remediation obligation is an obligation to address the current or potential detrimental effects of existing pollution by participating in pollution remediation activities. For example, obligations to clean up spills of hazardous wastes or hazardous substances and obligations to remove contamination such as asbestos are pollution remediation obligations. Pollution remediation activities include the following:

– a. Pre-cleanup activities, such as the performance of a site assessment, site investigation, and corrective measures feasibility study, and the design of a remediation plan

– b. Cleanup activities, such as neutralization, containment, or removal and disposal of pollutants, and site restoration

– c. External government oversight and enforcement-related activities, such as work performed by an environmental regulatory authority dealing with the site and chargeable to the government

– d. Operation and maintenance of the remedy, including required monitoring of the remediation effort (postremediation monitoring).

Not all pollution remediation obligations will involve all of the above activities. For example, asbestos removal typically will not involve postremediation monitoring.”

» Last I checked, handling pollution remediation was not in my jobdescription.

» Think about who you need to work with on your campus now.

GASB Statement No. 49, Accounting and Financial Reporting for Pollution Remediation Obligations (continued)

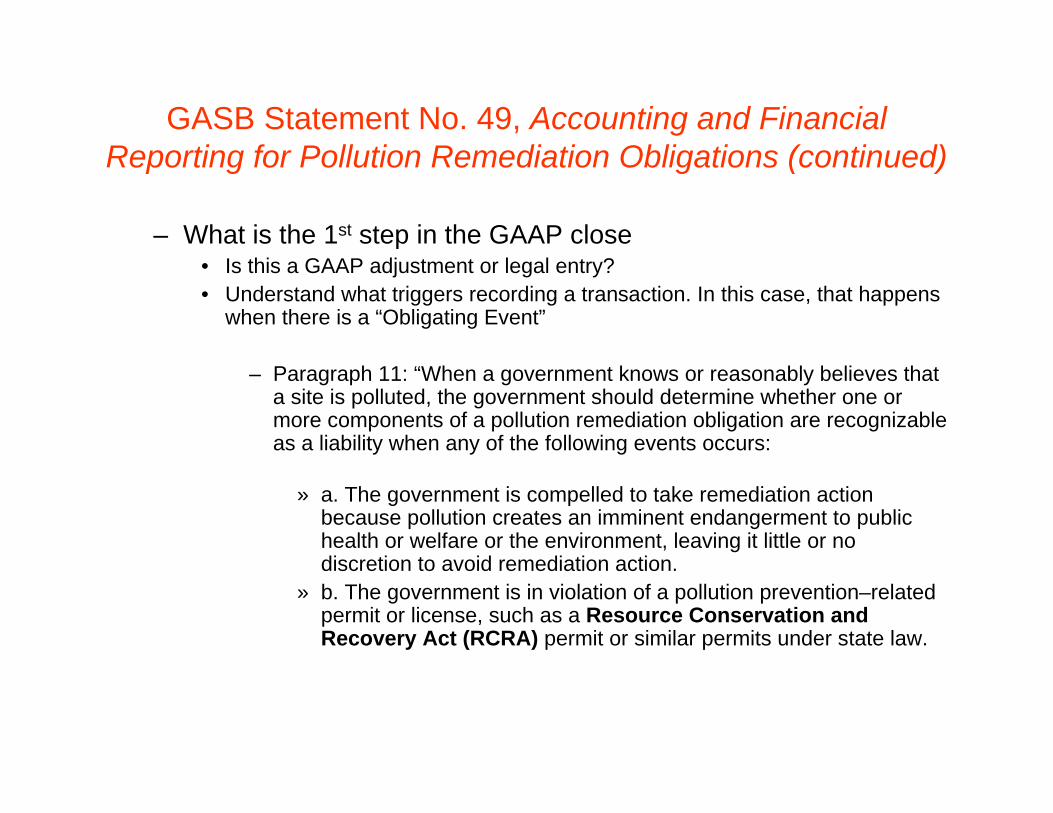

– What is the 1st step in the GAAP close• Is this a GAAP adjustment or legal entry?• Understand what triggers recording a transaction. In this case, that happens

when there is a “Obligating Event”

– Paragraph 11: “When a government knows or reasonably believes that a site is polluted, the government should determine whether one or more components of a pollution remediation obligation are recognizable as a liability when any of the following events occurs:

» a. The government is compelled to take remediation action because pollution creates an imminent endangerment to public health or welfare or the environment, leaving it little or no discretion to avoid remediation action.

» b. The government is in violation of a pollution prevention–related permit or license, such as a Resource Conservation and Recovery Act (RCRA) permit or similar permits under state law.

GASB Statement No. 49, Accounting and Financial Reporting for Pollution Remediation Obligations (continued)

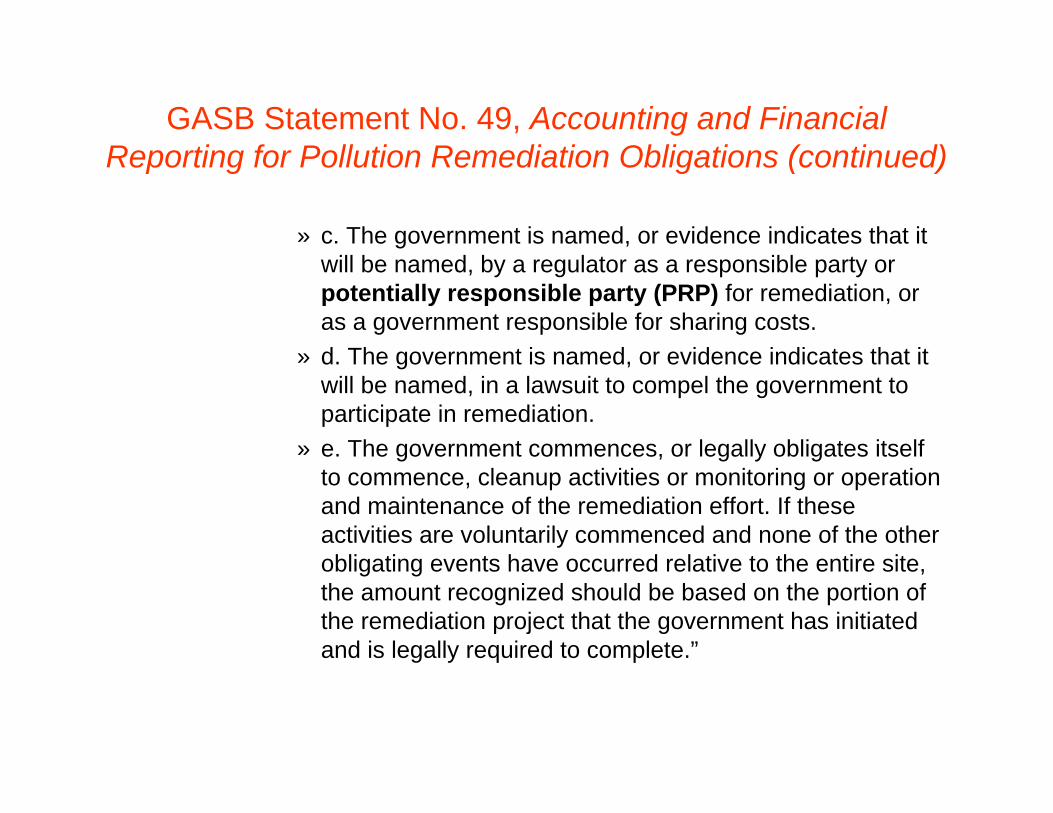

» c. The government is named, or evidence indicates that it will be named, by a regulator as a responsible party or potentially responsible party (PRP) for remediation, or as a government responsible for sharing costs.

» d. The government is named, or evidence indicates that it will be named, in a lawsuit to compel the government to participate in remediation.

» e. The government commences, or legally obligates itself to commence, cleanup activities or monitoring or operation and maintenance of the remediation effort. If these activities are voluntarily commenced and none of the other obligating events have occurred relative to the entire site, the amount recognized should be based on the portion of the remediation project that the government has initiated and is legally required to complete.”

GASB Statement No. 49, Accounting and Financial Reporting for Pollution Remediation Obligations (continued)

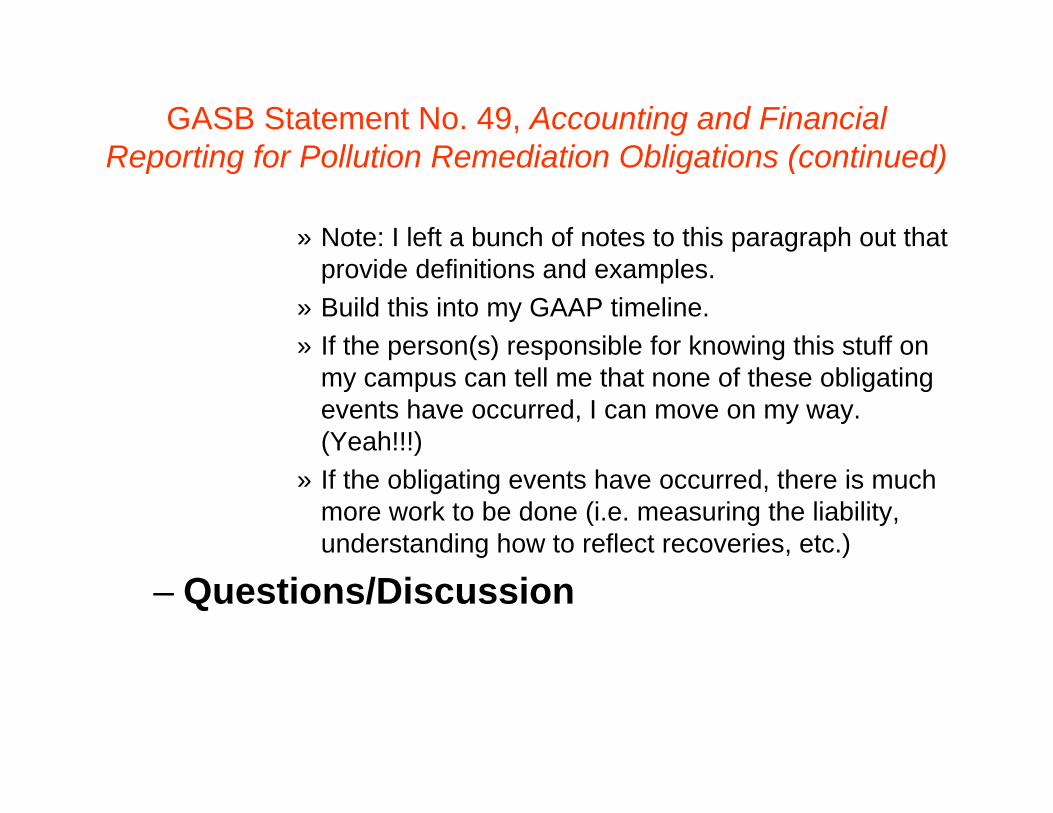

» Note: I left a bunch of notes to this paragraph out that provide definitions and examples.

» Build this into my GAAP timeline.» If the person(s) responsible for knowing this stuff on

my campus can tell me that none of these obligating events have occurred, I can move on my way. (Yeah!!!)

» If the obligating events have occurred, there is much more work to be done (i.e. measuring the liability, understanding how to reflect recoveries, etc.)

– Questions/Discussion

GASB Statement No. 51, Accounting and Financial Reporting for Intangible Assets

• Approach to resources– KPMG training (even reviewing the slides is

good)• It was lighter than the Statement No. 49 training.

– Read the Standard– Chapter Z: Other Implementation Guidance of

the GASB Staff Implementation Guide!!!– CSU GAAP Manual: updated Chapter 13

GASB Statement No. 51, Accounting and Financial Reporting for Intangible Assets (continued)

• Identify the “bottlenecks” in implementing the Standard– Understand the Effective Date and Transition

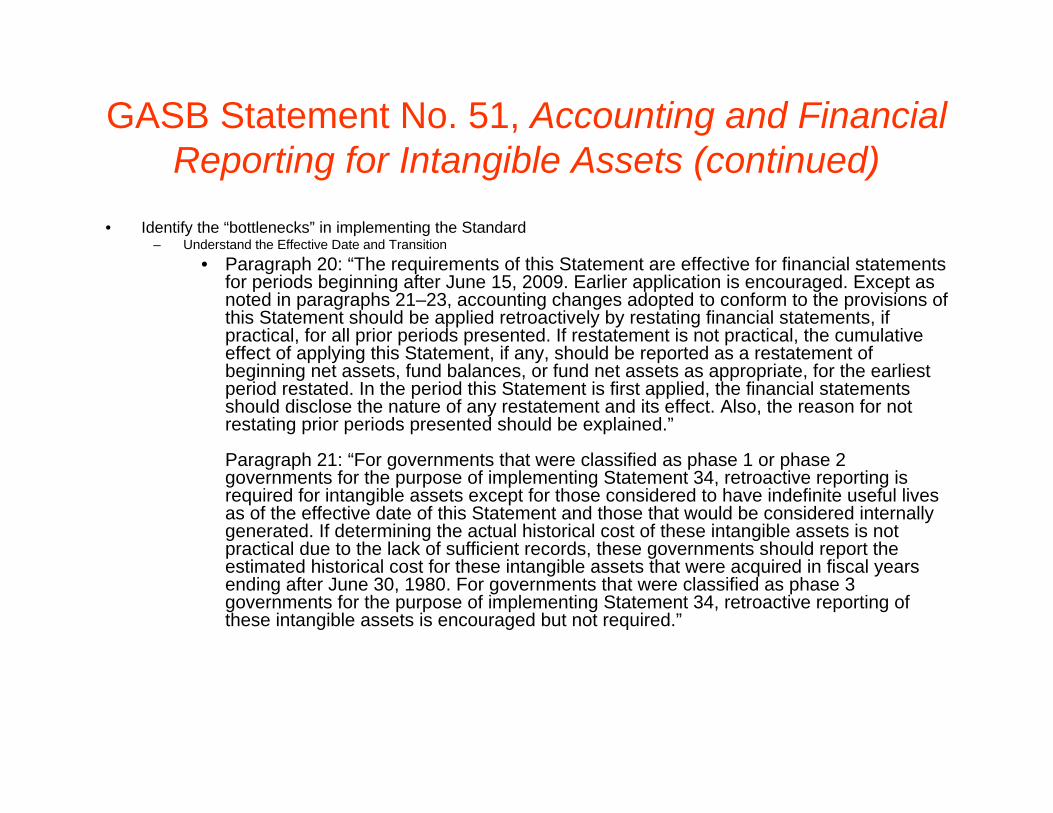

• Paragraph 20: “The requirements of this Statement are effective for financial statements for periods beginning after June 15, 2009. Earlier application is encouraged. Except as noted in paragraphs 21–23, accounting changes adopted to conform to the provisions of this Statement should be applied retroactively by restating financial statements, if practical, for all prior periods presented. If restatement is not practical, the cumulative effect of applying this Statement, if any, should be reported as a restatement of beginning net assets, fund balances, or fund net assets as appropriate, for the earliest period restated. In the period this Statement is first applied, the financial statements should disclose the nature of any restatement and its effect. Also, the reason for not restating prior periods presented should be explained.”

Paragraph 21: “For governments that were classified as phase 1 or phase 2 governments for the purpose of implementing Statement 34, retroactive reporting is required for intangible assets except for those considered to have indefinite useful lives as of the effective date of this Statement and those that would be considered internally generated. If determining the actual historical cost of these intangible assets is not practical due to the lack of sufficient records, these governments should report the estimated historical cost for these intangible assets that were acquired in fiscal years ending after June 30, 1980. For governments that were classified as phase 3 governments for the purpose of implementing Statement 34, retroactive reporting of these intangible assets is encouraged but not required.”

GASB Statement No. 51, Accounting and Financial Reporting for Intangible Assets (continued)

Paragraph 22: “Retroactive reporting of intangible assets considered to have indefinite useful lives as of the effective date of this Statement is not required but is permitted. Retroactive reporting of internally generated intangible assets (including ones that are in development as of the effective date of this Statement) also is not required but is permitted to the extent that the approach in paragraph 8 can be effectively applied to determine the appropriate historical cost of an internally generated intangible asset as of the effective date of the Statement.”

Paragraph 23: “The provisions related to intangible assets with indefinite useful lives should be applied retroactively only for intangible assets previously subjected to amortization that have indefinite useful lives as of the effective date of this Statement. Accumulated amortization related to these assets reported prior to the implementation of this Statement should be restated to reflect the fact that these assets are not to be amortized.”

– O.K. This is confusing.– This sounds like I am going to need to go back and record

transactions from prior periods. How am I going to do so?– This may be something that we should do consistently as all

campuses of the CSU because there are options.

GASB Statement No. 51, Accounting and Financial Reporting for Intangible Assets (continued)

• What is an intangible asset other than what we have been recording all along?

– Chapter Z: Other Implementation Guidance of the GASB Staff Implementation Guide is a good resource. See examples:

• Z.51.2. Q—Should a government’s website be considered computer software for purposes of applying the provisions of Statement 51? (Q&A2008-Z.51.2)A—Yes. Websites should be considered computer software. If the website meets the description of internally generated computer software, the outlays associated with its development should be accounted for based on the guidance in paragraphs 10–15 of Statement 51. (See questions Z.51.12–Z.51.18 about internally generated computer software; see questions Z.51.21–Z.51.23 about the measurement of commercially available

computer software that is not considered internally generated.)– O.K. I don’t think we ever capitalized our website as intangible asset. We

need to confirm that issue. Also, we need to understand if the website was internally or externally generated. That may impact if we need to record it depending on what selections were make above.

GASB Statement No. 51, Accounting and Financial Reporting for Intangible Assets (continued)

• Z.51.6. Q—Should the provisions of Statement 51 be applied to an intangible asset that upon acquisition or development is expected to be used both in operations and for the purpose of directly obtaining income or profit, for example, a trademark that will be used by a government in various venues as its emblem and to generate revenue through merchandise licensing agreements?

A—The applicability of the provisions of Statement 51 in this case depends on the primary purpose of the government in acquiring or creating the intangible asset. If the primary purpose of the intangible asset is to be used in operations, then the asset should be considered within the scope of Statement 51. If the primary purpose of the intangible asset is to directly obtain income or profit, then the asset would meet the scope exclusion in paragraph 3a of Statement 51 and, therefore, would not be subject to the provisions of the Statement. To assist in determining the primary purpose of the intangible asset, a government in exercising professional judgment may consider the amount of revenue that the intangible asset is expected to generate in comparison to the expected level of service capacity to be provided through its use in operations. (See question Z.51.19 about the reporting of intangible assets excluded from the scope of Statement 51 under paragraph 3a.)

– O.K. I need to capitalize trademarks.– Again, were these internally or externally generated?– Does the University own these trademarks or does an auxiliary organization?– What does this primary purpose stuff mean?

GASB Statement No. 51, Accounting and Financial Reporting for Intangible Assets (continued)

• Z.51.21. Q—A government acquires commercially available computer software through a five-year licensing agreement. Under the terms of the agreement, the government is required to make annual installmentpayments to the software vendor for the right to use the software over the life of the agreement. How should this transaction be reported?

A—As discussed in question Z.51.1, in such circumstances, the government should report the licensed software as an intangible asset. A long-term liability representing the government’s obligation to make the annual payments over the life of the contract also should be reported. The provisions of NCGA Statement No. 5, Accounting and Financial Reporting Principles for Lease Agreements of State and Local Governments , which incorporates by reference the provisions of FASB Statement 13 , should not be applied to determine the financial reporting for such a licensing agreement, even if the agreement is referred to as a lease, because the provisions of FASB Statement 13 do not apply to licensing agreements.

– O.K. We need to make sure our Procurement Dept. starts to look for these transactions as a part of the capital lease review process.

– You want to be recording these transactions during FY 08/09 and not looking for them at year-end.

GASB Statement No. 51, Accounting and Financial Reporting for Intangible Assets (continued)

– Z.51.9. Q—At what level of detail should (1) the specific objective of a project to develop an intangible asset and (2) the nature of the service capacity that is expected to be provided by the intangible asset upon completion of the project be determined to meet item (a) of the recognition criteria for internally generated intangible assets in paragraph 8 of Statement 51?A—Determination of the specific objective of the project to develop an intangible asset should be at a level that details the purpose or the function of the expected asset. For example, the specific objective of a research project at a medical university may be the development of a patent related to the creation of a new material for stitches formed from a combination of specific microfibers. Determination of the nature of service capacity expected to be provided by the intangible asset should, at a minimum, be at a broad qualitative level. For example, in the case of the project to develop a new stitch material discussed above, the nature of the service capacity could be the improvement of services provided to patients of the university’s hospital. The nature of the service capacity does not have to be quantifiable, for example, in a number of service units.

• O.K. They want us to capital R&D to patents? We need to contact our auxiliary organization. This impacts them. Who owns the patents?

• Discussion/Questions on GASB Statement No. 51.

FAS 117-1: Endowments of Not-for-Profit Organizations - Net Asset Classification of Funds Subject to an Enacted Version of the Uniform Prudent

Management of Institutional Funds Act, and Enhanced Disclosures for All Endowment Funds

• Just look at the title – you know it’s going to be complicated!!!

• Resources– KPMG/Chancellor’s Office training (even reviewing the slides is good)– Read the Standard (nothing beats this step)– CSU GAAP Manual: will be updated to reflect the treatment of

underwater endowments for FASB and GASB entities– New Ideas

• NACUBO Underwater Endowment Webcast– Available for infinite playback– Covers operational issues

» Example: Call your bond counsel.– Excellent Q&A’s

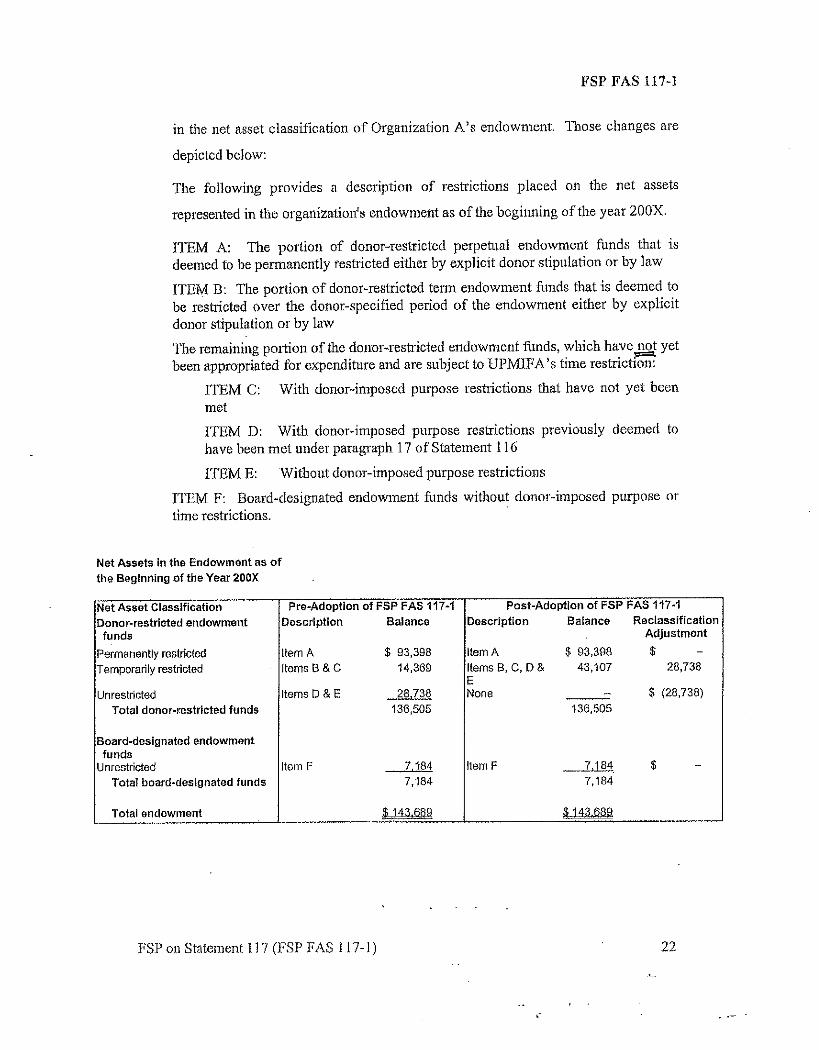

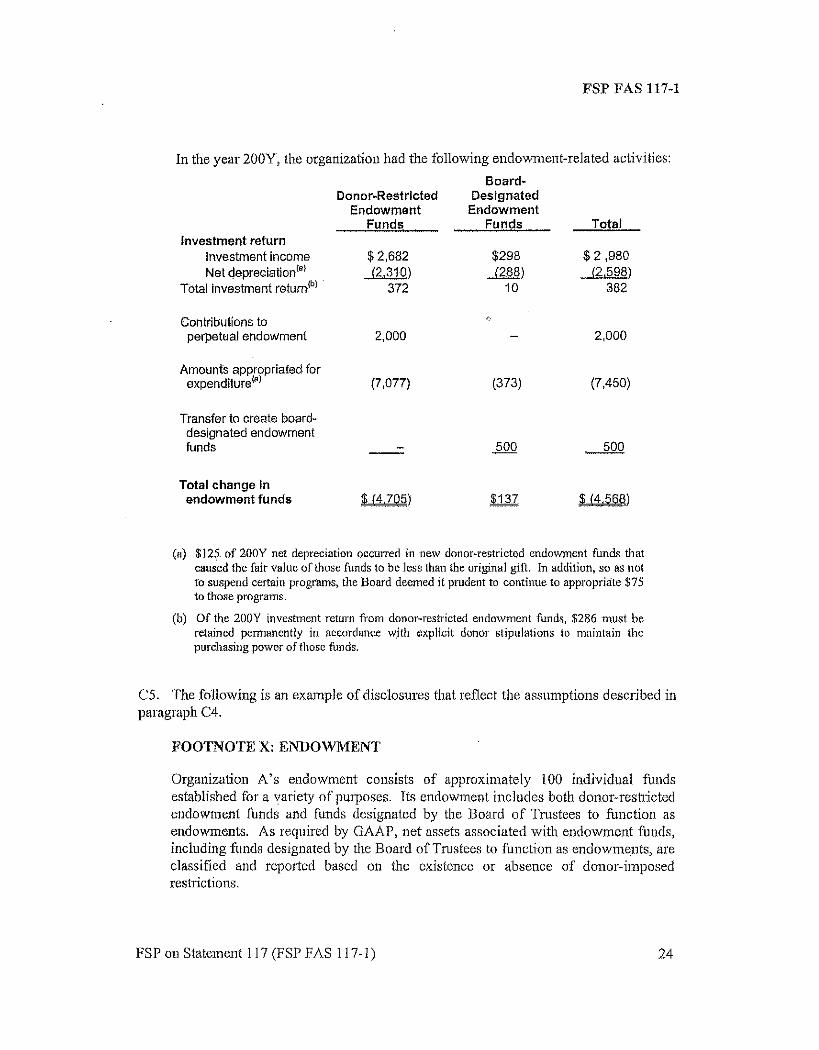

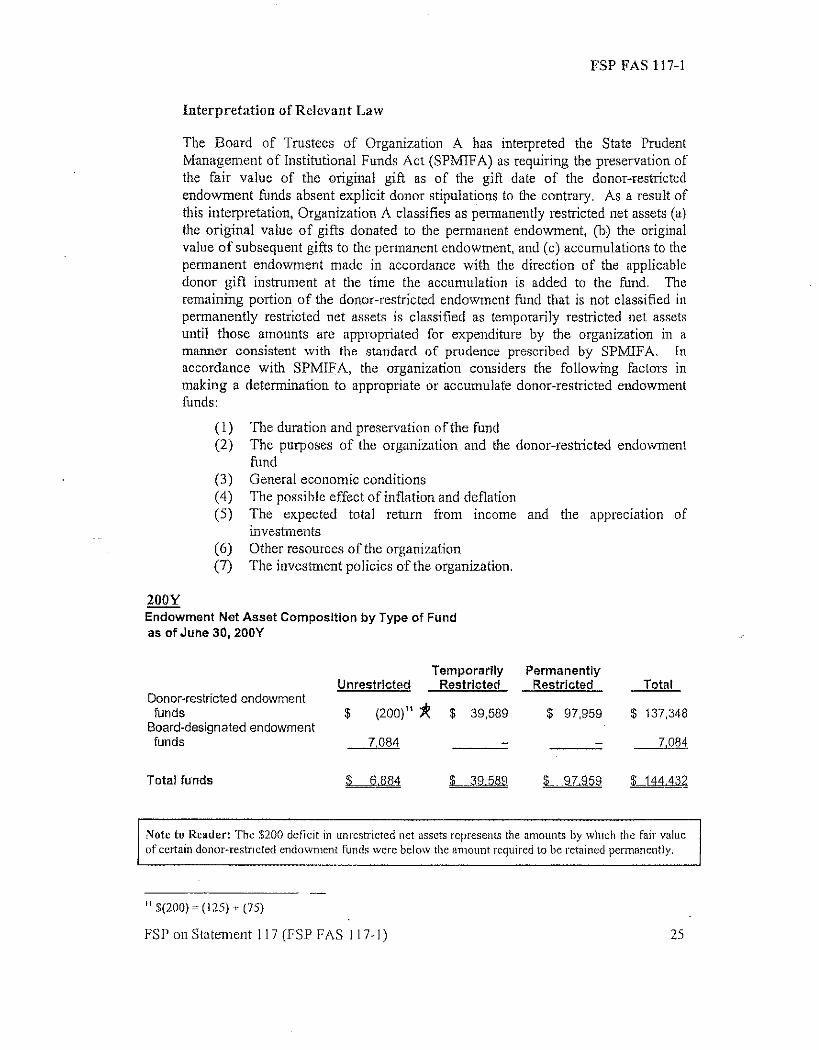

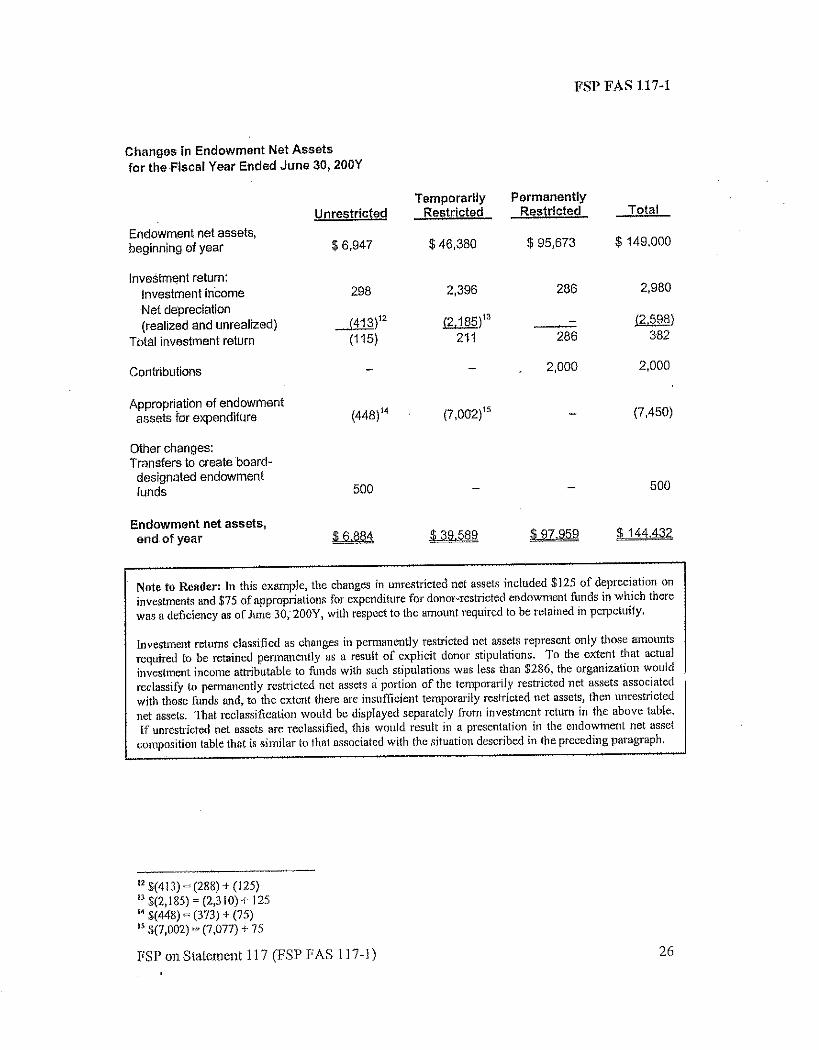

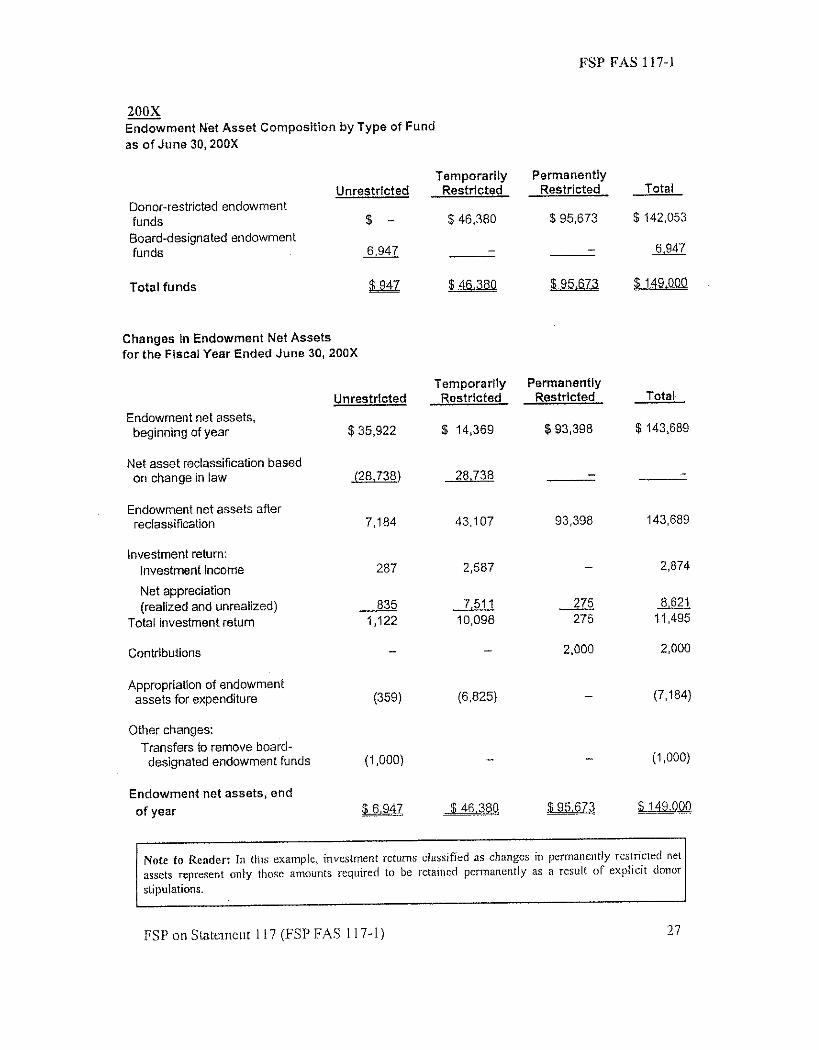

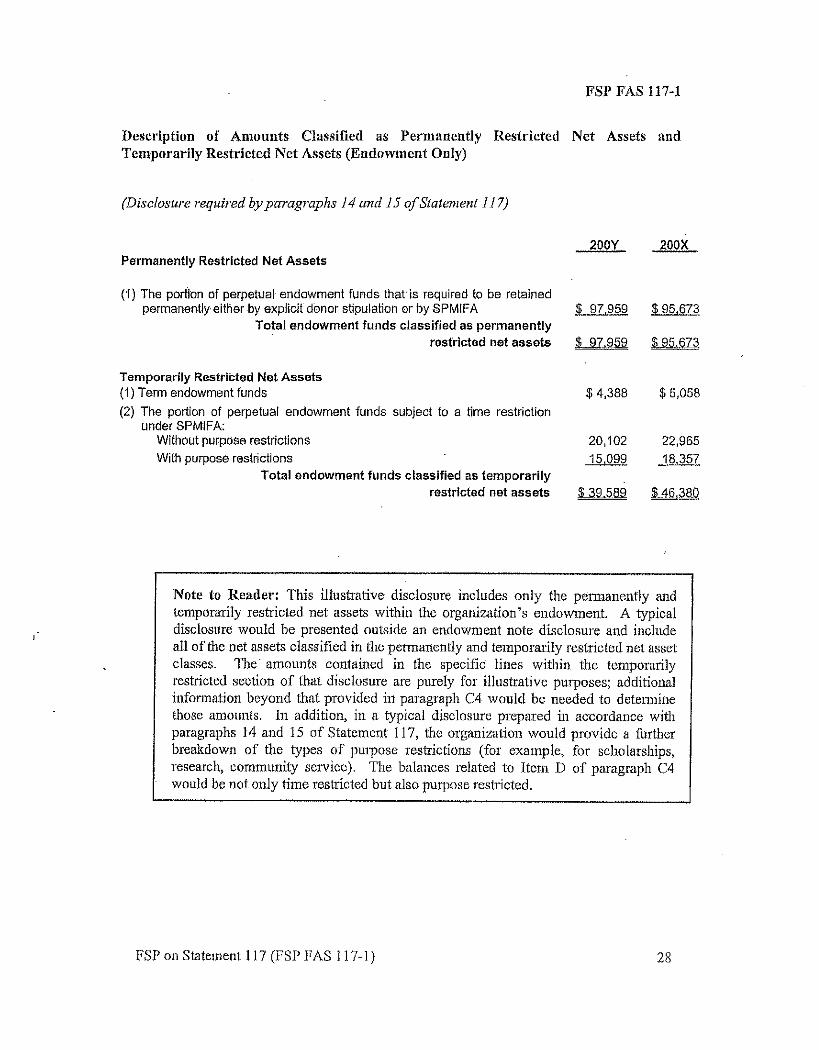

• See Appendix C – It gives an example of the new required disclosure

FAS 117-1: Endowments of Not-for-Profit Organizations - Net Asset Classification of Funds Subject to an Enacted Version of the Uniform Prudent Management of Institutional

Funds Act, and Enhanced Disclosures for All Endowment Funds (continued)

• Appendix C– Auxiliary Organization: Do your current records support these

required disclosures? You probably want to figure this out now and not in August/September.0

– Other Bottlenecks:Take a look at the paragraph on the governing board’s interpretation of UPMIFA.