impact of gst law on mobile phone manufacturing in...

TRANSCRIPT

Research Report

Impact of GST Law on

Mobile Phone Manufacturing in India

Published by

Consumer Untiy & Trust Society

D-217, Bhaskar Marg, Bani Park, Jaipur 302016, India

Ph: +91.0141.2282821, Fax: +91.141.2282485

Email: [email protected], Website: www.cuts-international.org

© CUTS International, 2017

Author by

Rahul Singh, Assistant Policy Analyst, CUTS International,

#1710

1

Contents

Introduction 2

Mobile Phone Manufacturing in India: The Growth Story 5

Taxation Overview – Mobile Phone Manufacturing in India 9

Goods and Services Tax (GST) Implementation 10

Conclusion and Way Forward 12

Annexure I 14

Annexure II 16

2

Introduction

Since the formation of the new government in 2014, India has witnessed a different

form of governance and transformation that has helped in restoring faith in the

country’s corporate sector. India was ranked 142 in the 2014 Ease of Doing Business

(EoDB) Rankings by World Bank (WB), which the elected government took up as a

challenge and set an ambitious target of reaching the top 50 in the following few years.

A slew of business-friendly announcements and initiatives have been rolled out since

then, which has created a positive image of India and pushed the ranking to 130 in the

2017 EoDB Index.

On August 15, 2014, the Prime Minister Narendra Modi announced the ‘Make in India’

initiative, which was envisaged to improve India’s EoDB ranking by aligning 25 priority

sectors that will propel job creation and fuel the country’s growth. The Electronics

manufacturing sector was also chosen as the sector is import-intensive, with imports

accounted for as much as 58 percent of the total domestic consumption in 2014-15.1

Since the launch of the initiative, the sector has experienced significant growth and

generated remarkable interest amongst global original equipment manufacturers

(OEMs) to setup local manufacturing base in India. The Indian mobile phone segment, in

particular, has seen a lot of traction in this regard. The value of mobile phones

assembled in India has increased 373 percent in the last two years, from ₹19,000 crore

in 2014-15 to more than ₹90,000 crore in 2016-17.2

Mobile phone is identified as a big-ticket item under the ‘Electronic Manufacturing’

programme pillar of ‘Digital India’, which requires consistent policy support to boost

local manufacturing and achieve Net Zero Imports by 2020. All three Union Budgets

under the present government have announced various fiscal incentives and schemes

that have injected new lease of life in manufacturing activities for mobile phones. Table

1 compares the growth of India’s mobile phone manufacturing since 2014.

Table 1: Comparative Growth of India’s Mobile Phone

Financial Year Industry Value

(in ₹billion)

Manufactured Units

(in million)

2014-15 189 60

2015-2016 540 110

2016-2017

(Estimated)

940 220

Source: Teleanalysis

1 Make in India Strategy for Electronic Products - Niti Aayog Report - May 2016 2 Hindustan Times Article dated March 22, 2017

3

The current differential duty structure,3 announced in Union Budget 2014, provides

huge impetus to domestic manufacturing and local assembly of mobile phones, which is

steadily encouraging the ecosystem development.

The domestic mobile industry contributes 6.5 percent (US$140bn) to India’s Gross

Domestic Product (GDP) and employs over 4mn direct and indirect workforce. By 2020,

the industry is expected to contribute 8.2 percent to the GDP and generate 800,000

more jobs.

In terms of unique mobile phone subscribers, India is expected to cross the 1bn mark by

2020. India will see an increase in adoption of 4G services with number of 4G

connections estimated to grow to 280mn by 2020 from just 3mn in 2015. In 2015, India

overtook the United States to become the world’s second largest smart-phone

subscriber base with 275mn active connections and a total of 1.06bn telecom

connections.4 Discussions on 5G technology have already begun within the industry

stakeholders.

India holds a significant geographical advantage with 12 major ports currently active

along the 7,516.6 km coastline with immediate proximity to Middle East, Africa and

Central Europe in the West and the South East Asian countries, making a strong case as

an ideal mobile phone manufacturing destination and export hub for the world.

About 38 new mobile manufacturing units have been set up since September 2015,

which has ramped up the manufacturing of mobile phone units in 2015-16 by 90

percent to 110mn from 60mn in 2014-15 and generated 38,300 employment

opportunities.

The Department of Telecom (DoT) has constituted a Fast Track Task Force (FTTF) to

‘catalyse and re-establish’ massive growth in mobile handset and component

manufacturing ecosystem in India. The three-tier objective of the Department was to

promote large scale manufacturing/assembling activity and achieve target production

of 500mn mobile handsets by 2019, and establish a component industry worth US$8bn

and generate 1.5mn jobs.5

3 A special differential excise duty regime was introduced for mobile handsets in the Union Budget 2014 to provide protection against imports. Under this regime, an excise duty of 12.5% applies as CVD to imports but domestic producers can choose between the same 12.5% excise with VAT exemption on inputs used and a significantly lower excise duty and no VAT exemption. For a vertically integrated manufacturer, this regime can allow significant protection against imports. 4 Make in India 'Telecommunication Sector'- Achievement Report 5 Make in India 'Electronics & IT Sector'- Achievement Report

4

A quick glance on the student training and certification numbers prove that mobile

phone sector is attracting new talent, with 1,62,152 certified students under various

sector skill programmes relevant to the sector.6

Another key reform under consideration by this government is the Goods and Services

Tax (GST) that is expected to remove regional/local taxation barriers and transform

India into a single market with a single tax regime. Such a regime will add to the

euphoria of ‘Make in India’ and will push the Indian economy to new heights by

eradicating a number of EoDB issues currently plaguing the sector.

If one is expecting this positive coupler effect of job creation and GST implementation to

fuel the healthy growth of domestic manufacturing in mobile phone sector, it is

important to note that the current taxation incentives must be carried on once the GST

regime kicks from 2017.

There is no doubt that the fiscal incentives played a key role in building the current

momentum and further continuation will only ensure that the sector transforms into a

global supplier and further strengthens the economy. Mobile phone manufacturing

companies will be able to allocate better acquisition funds to attract local talent, provide

needful training and development and also encourage local R&D innovation activities.

As stated earlier, the ‘Make in India’ initiative was launched with the intention of

fuelling manufacturing activity, increase local value addition and job creation, which

will only be justified if the current schemes and incentives are continued for a longer

duration. CUTS International, through this report, would like to advocate the need for

fiscal incentives post the GST regime, so that mobile phone manufacturing ecosystem

matures to build strong domestic capabilities and support creation of skilled workforce

in India.

The report provides an overview of current growth and value chain of mobile phone

manufacturing activities in India, along with highlighting the employment status,

government schemes and taxation incentives currently applied to the sector. The report

also assesses the impact of GST regime on the sector, along with recommendations on a

financial incentive model for incentivising enhanced manufacturing in India.

6 Make in India 'Skill Development Sector'- Achievement Report

5

How do we carry forward the current momentum to ensure protection of domestic mobile phone manufacturers from importers?

How do we ensure that the sector creates more innovative products for the world markets?

How do we ensure that there is consistent creation of skilled workforce to meet the employment demand in the Indian economy?

How do we ensure that there is significant local value addition so that India as a nation reaps benefits from this sector?

6

Mobile Phone Manufacturing in India: The Growth Story

Mobile Phone manufacturing activities and investments kick-started in India from 2005

and have been rapidly growing that has cemented India’s position in the global supply

chain. Lenovo, LG, Nokia, Motorola, Samsung are the major global brands that have

regularly churned out feature phones and smartphones from these facilities. Major

contract manufacturers like Foxconn and Flextronics have also setup facilities to build

relevant ecosystem and provide services to meet the manufacturing demand of the

above-mentioned brands. Annexure I depicts the presence of various manufacturing

facilities across the country since the announcement of the ‘Make in India’ initiative.

Figure 1: State of Indian Mobile Phone Manufacturing

Source: TeleAnalysis, Business Standard

Value Chain Analysis

Mobile phone manufacturing is an inter-play between the design aspect, the

components and the actual device manufacturing. Most companies in India have formed

a large local manufacturing base and are manufacturing through a mix of local

production and assembly. While most of the manufacturing happens in Completely

Knock Down7 (CKD) and Semi Knock Down (SKD)8 forms with some level of localisation,

high-end products are imported in Completely Built Unit (CBU)9 form. Presently, most

of the localisation in India takes place in the last mile assembly stage.

7 Completely Knocked Down (CKD) – CKD unit is one which is imported or exported in parts and not as one assembled unit. Such units are first sent to an assembly plant in the target country where all these parts are assembled and one complete unit is made using the imported components. 8 Semi Knocked Down (SKD) – SKD unit is one that is shipped in the form of semi-finished products to target country, and full assembly is done in the target country. 9 Completely Built Unit (CBU) – CBU unit is imported from some other country as a complete unit fully assembled. These units do not require an assembly before they can be sold out to the buyers in the target country’s markets.

180

125

60

110

220

0

10

20

30

40

50

60

0

50

100

150

200

250

2012 2013 2014 2015 2016M

an

ufa

ctu

rin

g U

nit

s

Mil

lio

n U

nit

s

India Mobile Phone Industry Domestic Production vs Manufacturing Units

Domestic Production Manufacturing Units

7

Figure 3: Mobile Phone Manufacturing Value Chain in India10

10 Source: Vibrant Gujarat 2017 – Mobile Phones

R&D, IP

Ownership

Design

Services

Sourcing &

Fabrication

Mfg./System

Assembly

Configuration

& Testing

Distribution

& Repair

Marketing &

Sales

OEMs /

ODMs

ODMs Raw

Material

Suppliers

Plant

Equipment

Suppliers

Testing

Equipment

Suppliers

Distributors Distributors /

OEMs

IP reusability management

New IP / Architecture development

Form factor design

Device architecture

Specification assessment

Printed Circuit Board Fabrication

Component Sourcing

Final Product Assembly

Complex mechanical assembly

Final Product Configuration

Systems Integration

Testing

Software Loading

Packaging

Logistics

Fulfilment

After-sales Services

Product IP Marketing

Sales & Channel Management

Branding & Campaign Management

MANUFACTURING PROCESS

KEY STAKEHOLDERS

STAKEHOLDER ACTIVITIES

LOCAL VALUE ADDITION IN INDIA

Microsoft

Samsung

LG

Lenovo

Intex

Lava

Micromax

Karbonn

Spice

Inventec Salcomp

Sterlite

SoftTouch

Amphenol

Vishay Components

Dakshin Speakers

Lite-On Mobiles

Foxconn

Jabil

Flextronics

Sanmina SCI

Dixon

SFO Technologies

Elin India

Rangsons

Centum

Kaynes

Microsoft

Samsung

LG

Lenovo

Intex

Lava

Micromax

Karbonn

Spice

MAJOR PLAYERS PRESENT IN INDIA (Indicative List)

8

Government Schemes to Support Domestic Mobile Manufacturing11

1. Export Promotion Capital Goods (EPCG) Scheme: Under the EPCG scheme, imports

of capital goods for pre-production, production and post-production (including

CKD/SKD thereof as well as computer software systems) enter at zero custom duty.

As per the Foreign Trade Policy 2015-2020, the specific export obligation under the

EPCG scheme where capital goods are procured from indigenous manufacturers has

been reduced to 75 percent from 90 percent in order to promote domestic capital

goods manufacturing industry.

2. Modified Special Incentive Package Scheme (M-SIPS): The M-SIPS scheme,

developed by Ministry of Electronics & Information Technology (MeitY) to boost

manufacturing and attract investments in the electronic sector, was modified in

August 2015 by extending the scheme for five years more to 2020, and adding 15

new product categories like smart cards, liquid crystal modules, consumer

appliances, Internet of Things products, multi-functional electronic devices and

optical fibre etc. Moreover, 192 M-SIPs applications worth 1.1 lakh crore have been

received between April 2014-September 2016, from global OEMs/ODMs and

component manufacturers in various segments of electronics like Information

Technology (IT) and telecom, strategic, energy conservation, consumer, automotive,

industrial, medical, EMS etc. MeitY has approved 67 proposals worth ₹16,845 crore

from Tata Power Strategic Engineering Division (SED), Continental Automotive,

Samsung, Bosch, Nidec, Tejas Networks, Motherson Sumi Systems, Nippon

Audiotronix, Continental Automotive, GE BE Private Limited, Philips, Jabil,

Flextronics, Sterlite, Giesecke & Deverient, LG, Lava, Haier, Mitsubishi, Delphi,

Schneider Electric and WiproGE healthcare.

3. Electronics Development Fund (EDF): EDF was launched in February 2016, with

the objective of promoting companies in developing new technologies in the areas of

electronics, nano-electronics and IT. Besides, four venture funds worth ₹179 crore

have been approved and 12 venture funds approved for in-principle commitment of

₹510 crore.

11 Make in India 'Electronics & IT Sector'- Achievement Report

9

Taxation Overview – Mobile Phone Manufacturing in India

The country’s telecom sector is witnessing rapid growth and competition among key

players and is currently the world’s second largest market in terms of subscribers, with

more than 1.06bn connectivity [Telephone subscribers (wireless and wireline)], 616mn

unique subscribers, 166mn broadband subscribers, 430mn mobile broadband

connections, and more than 350mn internet users. This phenomenal growth of the

sector is driving the demand for telecom equipment including mobile phones, which is

around US$20bn currently and is estimated to exceed US$30bn by 2020.12

The volume and potential growth of the mobile market accompanied by favourable

policies makes India an important investment destination for domestic as well as

foreign investors. The present government recognises the sector’s potential and has

shown positive intent to support the ecosystem by providing various key reforms in the

taxation structure in order to boost the domestic manufacturing activities. Below-

mentioned are the key amendments announced in the Union Budget since 2014:

1. Concessional rate of Special Additional Duty (SAD) at 2 percent would be applicable

on populated Printed Circuit Boards (PPCB) for use in manufacture of mobile

phones, applicable up to June 30, 2017, after which SAD would be applicable at 4

percent.

2. Basic customs duty (BCD) and SAD have been withdrawn and importers of mobile

handset components, such as chargers, adaptors, batteries and wired headsets need

to pay only the countervailing duty (CVD) of 12.5 percent.

3. Duty advantage of 10.5 percent for local manufacturers of mobile speakers and

batteries and 8.5 percent duty advantage to local manufacturers of routers set top

boxes, CCTV cameras etc.

4. BCD and SAD have been exempted for assembly-test-mark-pack for semiconductor

wafer fabrication/LCD fabrication.

5. Correction of inverted duty structure in below mentioned products:

BCD of 7.5 percent imposed on e-Readers and BCD on raw materials or parts for

use in manufacture of e-Readers reduced to 5 percent

BCD exempted on inputs/raw materials, such as Capacitor grade polypropylene

granules or resins

BCD exempted on Magnetron of up to 1.5 KW used for the manufacture of

domestic microwave ovens

BCD exempted on specified raw materials and capital goods for use in

manufacture of subminiature fuses, micro fuses, resettable fuses and thermal

fuses

BCD exemption has been withdrawn on certain telecommunication equipment

(soft switches, VoIP equipment, optical transport equipment, carrier, Ethernet

Switch, Packet Transport Node (PTN) products, Multiprotocol Label Switching- 12 Make in India 'Telecommunication Sector'- Achievement Report

10

Transport Profile (MPLS-TP) products; Multiple Input/Multiple Output (MIMO)

and Long-Term Evolution (LTE) Products.

The duty differential structure was perhaps the most positive indirect tax reform

announced in the 2015 Union Budget that provided a benefit of almost 10 percent to

domestic mobile phone manufacturers and has created huge interest among all major

players. This reform has also helped fuel job creation and skill development in major

manufacturing locations situated in Uttarakhand, Uttar Pradesh, Delhi-NCR, Telengana

and Tamil Nadu.13 Major investments are also been considered in Maharashtra, Goa and

Andhra Pradesh. Annexure II shows a breakup of candidates trained and certified in

2015-2016 through the various sector skill council programmes formulated by the

Ministry of Skill Development under the Skill India Mission.

Goods and Services Tax (GST) Implementation

The Goods & Services Tax Bill will be the most revolutionary reforms in the history of

Independent India, where the entire taxation and financial structure will undergo a

positive transformation and propel the nation towards becoming a single market with a

single tax, improving the economy, trade and business environment and giving thrust to

the present government’s mission to reach within top 50 of WB’s EoDB ranking.

Several local and state taxes will be subsumed within the GST regime removing the

cascading effect of multiple taxes. The domestic manufacturing companies, including the

mobile phone sector, will be able to abolish various taxation anomalies and standardise

their operations, which will lead to increased efficiency in business function and reduce

the mobility time of goods and services across the nation.

Improved business functions would mean efficient resource and fund utilisation that

may help this labour-intensive sector to focus on creating a conducive environment for

job creation, skill development, R&D and innovation.

However, it remains unclear whether the current benefits and taxation structure

enjoyed by the domestic mobile phone manufacturing sector, as explained earlier, will

be continued as the very base of GST regime is to subsume all taxes. This is a matter of

concern for the sector as the duty differential structure has helped in building a vibrant

environment where both domestic and international investments have led to the

growth of manufacturing activities across the nation, ecosystem development and

creating jobs for the skilled labour.

If it is assumed that the duty differential regime will be discontinued post the GST

implementation, then the sector will go through the déjà vu experience as both imports

13 Annexure I

11

and domestic manufacturing will be at par and it will become easier to import and sell.

This situation goes directly against the Net Zero Imports by 2020 envisaged under the

‘Digital India Mission’.

The GST Council Meeting held on May 19, 2017 has pegged the GST rate for mobile

phone at 12 percent.

Let us analyse two scenarios to understand the impact of GST on mobile phone business

in India. As the GST Rate on components for Mobile Phones is not yet decided, we have

assumed a 5 percent rate for such components for this analysis.

Scenario 1: A company is importing components to manufacture a mobile phone in

India.

Scenario 2: A company is importing a finished mobile phone to sell in India.

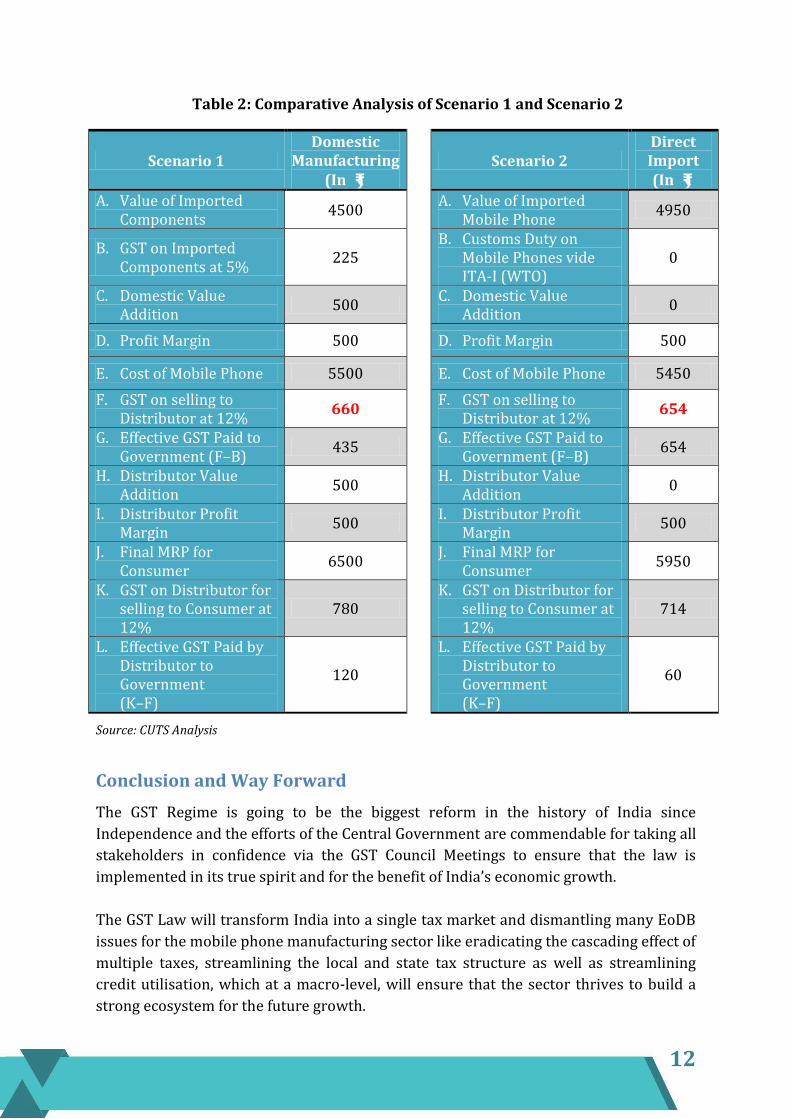

From both scenarios, the following inferences may be derived:

1. The domestic manufacturer ends up paying GST at the full rate of 12 percent of his

selling price to the distributor (₹990/) even though the components he used for

manufacturing the phone were initially taxed at a lower rate of 5 percent.

2. There is virtually no difference in the GST paid by manufacturer (₹990/) and the

importer (₹981/), thus providing no incentive to domestic manufacturer for making

mobile phones in India.

Thus, the proposed GST regime will create a level-playing field14 for both manufacturers

and traders, which will be detrimental for the mobile phone manufacturing sector that

has shown considerable positive commitments under the ‘Make in India’ initiative.

14 Economic Times Article dated April 13, 2017

12

Table 2: Comparative Analysis of Scenario 1 and Scenario 2

Scenario 1 Domestic

Manufacturing (In ₹)

Scenario 2 Direct Import (In ₹)

A. Value of Imported Components

4500 A. Value of Imported

Mobile Phone 4950

B. GST on Imported Components at 5%

225 B. Customs Duty on

Mobile Phones vide ITA-I (WTO)

0

C. Domestic Value Addition

500 C. Domestic Value

Addition 0

D. Profit Margin 500 D. Profit Margin 500

E. Cost of Mobile Phone 5500 E. Cost of Mobile Phone 5450

F. GST on selling to Distributor at 12%

660 F. GST on selling to

Distributor at 12% 654

G. Effective GST Paid to Government (F–B)

435 G. Effective GST Paid to

Government (F–B) 654

H. Distributor Value Addition

500 H. Distributor Value

Addition 0

I. Distributor Profit Margin

500 I. Distributor Profit

Margin 500

J. Final MRP for Consumer

6500 J. Final MRP for

Consumer 5950

K. GST on Distributor for selling to Consumer at 12%

780 K. GST on Distributor for

selling to Consumer at 12%

714

L. Effective GST Paid by Distributor to Government (K–F)

120

L. Effective GST Paid by Distributor to Government (K–F)

60

Source: CUTS Analysis

Conclusion and Way Forward

The GST Regime is going to be the biggest reform in the history of India since

Independence and the efforts of the Central Government are commendable for taking all

stakeholders in confidence via the GST Council Meetings to ensure that the law is

implemented in its true spirit and for the benefit of India’s economic growth.

The GST Law will transform India into a single tax market and dismantling many EoDB

issues for the mobile phone manufacturing sector like eradicating the cascading effect of

multiple taxes, streamlining the local and state tax structure as well as streamlining

credit utilisation, which at a macro-level, will ensure that the sector thrives to build a

strong ecosystem for the future growth.

13

However, if the current taxation incentives are discontinued post the GST regime, the

industry will once again witness rise of import activities, which will severely affect

balance of payments and contradict the current government’s ‘Make in India’ and

‘Digital India’ Missions.

With no clear incentives to manufacture, current domestic activities might slow down

threatening the job creation agenda of the Government and would stifle the future

skilling abilities of the sector, gravely impacting the sector’s potential to generate

millions of direct and indirect jobs.

The government, on its part, is also contemplating on identifying alternate routes to

continue duty differential to ensure that mobile phone manufacturing in India remains

an attractive proposition even under the GST regime. In April 2017, Joint Secretaries

from the Prime Minister’s Office, Ministry of Electronics and Information Technology

(MeitY), Department of Revenue, Department of Commerce and Department of

Industrial Policy and Promotion (DIPP), among others held a meeting with

representatives of government-backed Fast Track Task Force (FTTF) to explore a long-

term plan with predictable policy regime and associated incentives for the mobile

phone manufacturing sector.15

One strongly feels that in order to sustain the sector and make India a true global

manufacturing destination of mobile phones, it is important that policymakers devise a

mechanism to incentivise the sector under the GST regime, so that the momentum is not

lost.

As part of our recommendation, we propose that OEMs that adhere to local value

addition norms be offered tax refunds proportionate to achieved local value

addition target.

These above mentioned recommendations will lead to the following advantages:

As tax refund will be linked to proportionate local value addition, manufacturers

will be encouraged to increase local value addition by building supply chain for

components as well as skilling local talent to design innovative mobile phones.

With increased local value addition efforts and GST regime removing cascading

effect on manufacturing, prices of mobile phones will come down and benefit

consumers across the world and

Ensure the success of ‘Make in India’ and ‘Digital India’ initiatives by reducing

imports and promoting indigenous manufacturing for India and the world

15 Economic Times Article dated April 8, 2017

14

Annexure I

List of the Mobile Manufacturing Units Established in India since September 2015

Brand/ Company/ EMS

Company

No. of

Units

Location of Units Manufacturing Capacity

(Mn Units/Month)

Employment

(In No.)

Foxconn (Rising Star

Mobiles India Pvt. Ltd.)

5 1. Sri City 2.5 8000

2. Sri City

3. Sri City

4. Sri City

5. Maharashtra

Micromax (Bhagwati

Products Ltd.)

1 Hyderabad, Telangana

0.3 600

MCM (Million Club

Manufacturing)

1 Noida, UP 1 1500

Lava International

2 1. Noida, UP 2 5000

2. Noida, UP

Intex Technologies

4 1. Noida, UP 3 5000

2. Noida, UP

3. Jammu

4. Baddi, HP

Celkon Mobiles 1 Medchal, Telangana 0.5 1200

Dixon Technologies

(India) Private Limited

1 Noida, UP 1 900

GDN 1 Greater Noida, UP 1 1200

Vivo Mobile 1 Greater Noida, UP 0.3 500

Videocon 2 Aurangabad, Maharashtra

1 2000

Kasipur, Uttarakhand

Flextronics 1 Sriperumbudur, TN 1.3 2500

SEPL 1 Haridwar, Uttarakhand

0.5 1000

TMB Electronics

1 Kundli, Haryana 0.4 800

Innovative Industries

1 Delhi 0.4 700

15

Labanyo Electronics

1 Noida, UP 0.2 500

KMC Electronics

1 Kotdwar, UP 0.7 1000

Champion Computers

1 Delhi 0.3 500

BGM Electronics

1 Shahibabad, UP 0.4 500

SST Electronics 1 Kundli, Haryana 0.4 500

Hyve Mobiles 1 Delhi 0.3 300

Bingo Mobiles Tech.

1 Noida, UP 0.2 300

Delhi Phone Battery

1 Haridwar, Uttarakhand

0.5 800

ADCOM 1 Delhi (Kirti Nagar) 0.1 300

VSUN 1 Bawal, Haryana 1.7 1800

Hi-tech 1 Kolkata, WB 0.2 600

Higher Industries

(India) Pvt. Ltd.

1 Mundka, Delhi 0.5 300

Runsheng Technologies

Pvt. Ltd.

1 Faridabad, UP

Compal (Manufacturing

for LeEco)

1 Greater Noida, UP

Penguine Electronics

1 Daman

Total 38 20.7 38300

16

Annexure II

Details of Candidates Trained and Certified under Sector Skill Council during

2015-2016

Sector Skill Council No. of Candidates

Enrolled

No. of Candidates

Trained

No. of Candidates

Passed

No. of Candidates

Certified

Electronics Sector

Skill Council

176258 176108 138032 122843

Telecom Sector Skills Council

53788 53723 34016 28567

IT-ITeS Sector Skills Council (NASSCOM)

40650 40627 14537 10742

Grand Total 270696 270458 186585 162152

17