impact of economic recession induced problems on...

TRANSCRIPT

Journal of Emerging Issues in Economics, Finance and Banking (JEIEFB)

An Online International Research Journal (ISSN: 2306-367X)

2017 Vol: 6 Issue: 2

2334 www.globalbizresearch.org

Impact of Economic Recession –

Induced Problems on Nigerian Economic Growth

Georgina Obinne Ugwuanyi,

College of Management Sciences,

Michael Okpara University of Agriculture, Nigeria.

E-mail: [email protected]

Chinelo Jenevive Obiekwe,

College of Management Sciences,

Michael Okpara University of Agriculture, Nigeria.

E-mail: [email protected]

___________________________________________________________________________

Abstract

This study examines the Impact of Economic Recession –induced problems on the Nigerian

economic growth for the period 1985 to 2015. The major objective of this research is to

ascertain the impact of these problems on Nigerian economic growth. The study adopted ex-

post-facto research design. Data were obtained from secondary sources mainly from: Central

Bank of Nigeria published statistical Bulletin of 2015, Nigeria’s Bureau for Statistics quarterly

reports, and World Bank Development Indicator. As the unit root test on the time series data

revealed a combination of I(0) and I (1) variables, the Auto-regressive Distributed Lag (ARDL)

Model technique was employed for data estimation. The findings reveal that focusing on the

short run relationship, most of the explanatory variables and their lags are significant functions

of Nigerian economic growth at 5% level of significance. Conclusively, all the economic

recession induced outcomes under study responded significantly and negatively or positively

to economic growth contemporaneously or with a lapse of time (lag). For the independent

variables under study and their lags, only exchange rate with time lapses of three years

produced a negative impact of 8% reduction on the Nigerian economic growth while other

variables (public debt with four years lapses of time, unemployment rate with a year lapse of

time, and the lagged dependent variable (lagged GDP as a regressor) impacted positively on

the economic growth producing 4%, 6% and 84% increase on the GDP (at every1% change),

respectively. This broadly means that economic growth is the function of the recession induced

variables.

___________________________________________________________________________

Key Words: Economic recession, Recession –induced problems, Economic Growth,

Nigeria

JEL Classification: H 3

Journal of Emerging Issues in Economics, Finance and Banking (JEIEFB)

An Online International Research Journal (ISSN: 2306-367X)

2017 Vol: 6 Issue: 2

2335 www.globalbizresearch.org

1. Introduction

In a layman’s understanding, a recession is a period of general economic slowdown. But in

economics, a recession is a negative growth in GDP for two consecutive quarters.

According to Dictionary of Contemporary English, New edition for advanced learners, a

recession is a difficult time when there is less trade, business activity, etc in a country than

usual. A recession also means a slowdown in Gross Domestic Product or National outputs. The

business dictionary also defines recession as a period of general economic decline usually as a

contraction in the GDP for six months (two consecutive quarters). A recession will typically be

characterized by high unemployment, falling average incomes, increased inequality and higher

government borrowing, etc (Tejvan, 2012). Uzie (2016) also added that the greatest recession

of 2008 to 2012 has shown many of the negative impact of recession to workers and also has

resulted to: high inflation rate, increase in crime rate, and strained family relationship.

Equity (2017) noted that during any recession, every news in the headings of newspapers

are about unemployment figures in which the families encountering the recession keep

suffering, and silently too. The citizens make extra efforts to let ends meet hoping that economy

will soon turn around yet all to no avail. Although many families strive to keep afloat as if

nothing wrong happens, gradually the recession can impose profound effect on the day-to-day

activities of these citizens and on their ways of living their lives.

When a recession lasts for a long time it becomes depression, hence, a depression is a deep and

long lasting recession (Investopedia, 2017, L.L.C). An economic recession is not a permanent

situation but rather a temporal one; hence hopefully Nigerian economy will soon bounce back

in a short while.

If economic recession lingers on in a country, it induces some problems that are bound to

impact on the growth of the economy or sometimes directly on the basic physiological needs

of such country’s citizens hence the need for this research study which investigates into the

impact of economic recession-induced problems on Nigerian economic growth.

1.1 Objectives of the Research

The main objective of this research is to examine the impact of Economic Recession Induced

problems on the Nigerian economic growth.

The specific objective is to:

i) Ascertain the extent of impact of economic recession induced problems on Nigerian

economic growth.

1.2 Hypothesis

The researcher formulated the following hypothesis for the study:

Ho1: Economic recession-induced problems have no significant impact on Nigerian

economic growth.

Journal of Emerging Issues in Economics, Finance and Banking (JEIEFB)

An Online International Research Journal (ISSN: 2306-367X)

2017 Vol: 6 Issue: 2

2336 www.globalbizresearch.org

2. Literature Review

2.1 Conceptual Framework

A global recession is the recession that affects many countries around the world, that is, a

period of global economic-slow down or declining economic output (Wikipedia, 2017).

However, an economic recession is typically defined as a significant decline in economic

activity, real GDP, real income, employment industrial production and sales following a decline

in the aggregate demand for at least two consecutive quarters (myaccountrycourse.com, 2017).

On the other hand, the National Bureau of economic research (NBER) defined recession as a

“significant decline in economic activity. The National Bureau of Economic Research (NBER)

defined a recession as a “significant decline in economic activity spread across the economy,

lasting more than a few months, normally visible in a real gross domestic product (GDP), real

income, employment, industrial production and wholesale-retail sales” (Noko,

2016;NBER,2008).

The setup of economic recession gradually induced its effect in ripples: when the

government imposes higher interest rates, the cost of money rises, thus lowering consumer and

government borrowing. The consumer confidence also declines hence lowering the demand for

goods and services; if business operations are difficult to be financed by means of borrowing,

the firms start retrenching their staff thereby increasing unemployment. Eventually when

recession follows the downward phase of an economy (with stagnation or decline in the

investment, reduction of income, and increase of unemployment), the economy either enters a

recession or it resumes to the expansion phase (myaccountingcourse.com).

According to Tejvan (2011) therefore, there are several problems induced by economic

recession such as:

Falling Output: This means that less will be produced resulting to lower real GDP and

lower average incomes. Wages tend to rise much more slowly or not at all.

Unemployment: a rise in cyclical unemployment is the biggest problem of recession.

Higher Government Borrowing: As levels of government borrowing increases, it

leads to higher interest rates costs.

Devaluation in Exchange rate and others such as falling asset prices, falling share

prices, social problems associated with rising unemployment; increased inequality, etc.

2.2 History of Economic Recession

In the history of economic recession there was a recession called Wall Street Crash that took

place in 1929. The international Monetary Fund defines a global recession as “a decline in

annual per-capita real world GDP (purchasing power parity weighted), backed up by a decline

or worsening for one or more of the seven other global macro-economic indicators. Industrial

production, trade, capital flows, oil consumption, unemployment rate, per-capita investment,

Journal of Emerging Issues in Economics, Finance and Banking (JEIEFB)

An Online International Research Journal (ISSN: 2306-367X)

2017 Vol: 6 Issue: 2

2337 www.globalbizresearch.org

and per-capita consumption (Wall Street Journal, 2009; Economic Outlook, 2009). By this

definition since World War II only four global recessions existed (in 1975, 1982, 1991 and

2009). Each of them lasted for a year (but the 1991 recession would have lasted until 1993 if

the IMF had used normal exchange rate weighted per capita real world GDP rather than the

purchasing power parity weighted per capita real world GDP). (Wall Street Journal 2009;

World Economic Outlook 2009). The 2009 global recession called the Great Recession, was by

far the worst of the four war recessions, both in terms of the number of countries affected and

the decline in real world GDP per capita (Wall street Journal; 2009; World Economic Outlook,

2009).

Prior to April 2009, the IMF argued that a global annual real GDP growth rate of 3.0 percent

or less was “equivalent to a global recession (Economist.com; 2008; Lall, Subir, 2008) Based

on this measure, there have been six global recessions since 1970:

1974-75 (http://www.imf.org/external/pubs,2009

1980 – 83 (http://www.imf.org/external/pubs, 2004

1990 – 93 (Bloombere.com,2008)

1998 (Bloomberg.com,2008)

2001-02 (Bloomberg.com,2008)

2008-2009 (World Economic Outlook, 2013)

By distinction therefore a national recession is identified by two quarters of decline.

Furthermore, a developing country is expected to have a higher GDP growth than a Developed

country (IMF World Economic Outlook, 2008).

According to IMF, the real GDP growth of the emerging and developing countries is on an

uptrend and that of the advanced economies is on a downtrend since 1980s (Wikipedia, the free

encyclopedia)

Nigeria’s first full year recession began in the year 1987 with output contracted to 0.4

percent in the first quarter from a year earlier, and 0.7 percent point in the fourth quarter

(Bohlund, 2016). In 2006, there occurred a recession called the bursting of the real estate bubble

on the summer which originally led to the bankruptcy of a large number of floating rate

mortgages and then moved to the market of corporate subordinated bonds issued to finance

securitized mortgages. The outcome was a wave of collapse, mergers, and nationalizations after

September 2008.

The 2008 recession is said to be one of the major economic recessions called subprime

mortgage crisis. The consequence of the subprime crisis gave birth to instant movement to the

financial markets of other countries causing a surprise decline of 40 to 70% (my accounting

course, 2017).

Journal of Emerging Issues in Economics, Finance and Banking (JEIEFB)

An Online International Research Journal (ISSN: 2306-367X)

2017 Vol: 6 Issue: 2

2338 www.globalbizresearch.org

2.3 Recession Indicators

The technical indicator of a recession is two consecutive quarters of negative quarters of

economic growth as measured by a country’s Gross Domestic Product (GDP), although the

National Bureau of Economic Research (NBER) does not necessarily need to see this occur to

call it a recession (Investoperdia, 2017, LLC).

Besides the two consecutive quarters of GDP decline, economists have two categories of

recession indicators:

(i) Leading indicators that materialize prior to official declaration of recession. This

is the most common leading indicator being the contraction in the stock market.

Declines in bread stock indices such as Dow Jones Industrial Average (DJIA) and

standard of poor’s (S & P) 500 index, often appear several months prior to a

recession taking place. This exemplifies 2007 case where the market began

declining in August, four months ahead of the official recession in December 2007

(Investopedia, 2017, LLC).

(ii) Lagging Indicators: These of a recession include unemployment rate. Though the

Great Recession began in December 2007, the unemployment rate still indicated

full employment - a rate of 5% or lower – four months later. The unemployment

rate began declining in May 2008, and did not recover until several months after

the recession ended in June, 2009. (Investopedia, 2017 LLC).

Recession: Way Forward

A professor of History and former transitional chairman of the movement for the survival

of Ogoni People (MOSOP), Ben Naanen suggested that the Federal Government of Nigeria

should return to history in order to find out why various economic reforms have failed in the

past and that our leaders should head towards an economic rebirth. He further argued that the

government must have to spend its way out of the recession by creating jobs, revitalizing

businesses; to pull the country out of the recession, and also boost education and utilize the

abundant human capital the nation has (Naanen, 2016).

2.4 Theoretical Review

There exist some theories proposed by earlier researchers on the areas of economic recession

and the impact of the induced problems on economic growth and basic physiological needs.

These are:

2.5 Keynesian Economic Theory in recession

Keynes (1936), first presented his theories forming the basis of the Keynesian economics

during the Great Depression. These are the different theories of how in the short run, and

especially during recession economic output is strongly influenced by aggregate demand (total

spending in the economy). Keynes opined that in recession, that the way to break the cycle is

Journal of Emerging Issues in Economics, Finance and Banking (JEIEFB)

An Online International Research Journal (ISSN: 2306-367X)

2017 Vol: 6 Issue: 2

2339 www.globalbizresearch.org

for the government to push in spending heavily into the economy by building roads and bridges

and other public works. He argued that level of economic activity is dependent on aggregate

demand and that if demand comes low it results to recession and high unemployment.

2.6 Hangover Theory

Krugmen (1998) in this theory gives an idea that slumps are the price we pay for booms,

meaning that the suffering an economy experiences during a recession is a necessary

punishment for the excesses of the previous expansion. After a long argument on this theory by

comparing it with Keynesiansism and Austrian theorists for and against the above theory, this

theory was said to have turned out to be intellectually incoherent since nobody has managed to

explain why bad investments in the past require the unemployment of good workers in the

present. It was then concluded that often if not always that “it is ideas, not vested interests that

are dangerous for good or evil (www.pkarchive.org)

2.7 Empirical Review

Impact of Economic Recession on Economic Growth and Citizens

Massavrat and Sha (2015) carried out a research to assess the impact of recession on

Consumer’s behavior as an empirical study in Dubai. Their aim was to understand the impact

of global recession on consumer shopping behavior and how consumer consumption and saving

pattern changed across different product categories during and after recession. A total of 235

respondents were issued structured questionnaire. Paired sample t-test and ANOVA were

employed to analyse the data. The research finding revealed empirical evidence that the

priorities of the consumers significantly changed after recession.

Gautan, et al (2014) carried out a research on global recession and its impact on

telecommunications industry as an empirical dissection. The study’s objective included

analyzing the flows of foreign Direct Investments in telecom sector in India and also examining

the reasons behind consistency in FDIs during global financial crisis period. Findings revealed

that even with recession, India has witnessed a steady growth in the economy with the FDI’s

inflows and the telecom sector and its various project were not hindered by global crisis.

Economic recession-induced problems do not only affect the economic growth but also

impose mental health disorders on some Nigerian citizens. For instance, recently, in Nigeria,

there have been increases in cases of documented suicides, violent crimes, depression, and

alcohol dependency among other vices that go with economic recession (Muanya, 2016). Even

the WHO statistics (2012) ranks Nigeria 102 among the list of nations in the incidence of

suicide among the population, with an annual figure of 6.5 for every 100,000 in the population

and a strong male preponderance. (Muanya, 2016)

Journal of Emerging Issues in Economics, Finance and Banking (JEIEFB)

An Online International Research Journal (ISSN: 2306-367X)

2017 Vol: 6 Issue: 2

2340 www.globalbizresearch.org

Opejobi (2017) also reported of a medical doctor by name Allwel Orji who jumped into

Lagos lagoon on March 21, reason being that government left doctors on half pay, irregular pay

or no pay at all because of recession –induced cash contraction in Nigerian economy.

Also, Olugbile (2017) who is a consultant psychiatrist and former chief Director of Lagos

State University Teaching Hospital (LASUTH) Ikeja, of past Nigeria also confirmed that there

is a positive relationship between economic recession and mental health disorders.

Rahman,Galvan and Martinez (2017) explored into the root causes, consequences and

recoveries of the economic recession for the sustainable economic growth in spain. They

employed a systematic examination of past researches on economic recession topics. The

findings reveal that one of the main reasons for the Spanish deep economic recession was the

burst of the housing bubble while one of the most prominent consequences is the increasing

unemployment and one of the most important recovery measures taken by the government was

the faster adjustment in the housing sector. The research concluded that Spain is facing its worst

crisis in the last fifty years and that the Spanish economic recovery depends specially on two

facts: that at the National level ,the reforms implemented over the past two years should be

pursued further while still initiating structural reforms in other areas; also that the process of

bank restructuring should be completed and the model of state organization should be

redesigned..ii) that at the European level , solutions should be promoted to eliminate the

fundamental problems of the Eurozone, the restrictions on the European Central Bank’s

intervention and the lack of fiscal integration (Paul,2010)

3. Methodology

3.1 Research Design

The study adopted ex-post-facto research design as the incidence bringing about the data

has occurred in the time past and hence, the researcher cannot manipulate them. Economic

growth is proxied by Real GDP as the dependent variable while the independent variables are

the indicators of the economic recession induced problems: public debt, unemployment rate

and the real exchange rate.

3.2 Research Questions

i) To what extent has economic recession induced problems impacted on the Nigerian

economic growth?

3.3 Data

Datasets were obtained from secondary sources mainly from Central Bank of Nigeria’s

published statistical Bulletin of 2015 and from Nigeria’s Bureau for statistics quarterly reports

of various issues, while the data for real effective exchange rate were sourced from World Bank

Development Indicators.

Journal of Emerging Issues in Economics, Finance and Banking (JEIEFB)

An Online International Research Journal (ISSN: 2306-367X)

2017 Vol: 6 Issue: 2

2341 www.globalbizresearch.org

The data so collected is annualized time series and covers the years 1985-2015. The choice

of the year 1985 is to have at least two years before the 1985 first full year recession in Nigeria.

Table 3.1: Datasets of Real Gross Domestic Product and the Variables Resulting

from Economic Recession Inducement:

YEAR RGDP PDEBT UNER REER

1985 14,953.91 40.48 6.10 489.6102

1986 15,237.99 45.25 5.30 267.468

1987 15,263.93 69.89 7.00 85.21023

1988 16,215.37 137.57 5.30 85.62721

1989 17,294.68 180.98 4.50 76.24926

1990 19,305.63 287.44 3.50 70.74783

1991 19,199.06 382.71 3.10 59.96909

1992 19,620.19 444.65 3.40 49.74446

1993 19,927.99 722.22 2.70 54.50262

1994 19,979.12 906.98 2.00 100.7952

1995 20,353.20 1056.39 1.80 160.1283

1996 21,177.92 1194.59 3.40 207.6351

1997 21,789.10 1037.29 3.20 235.9241

1998 22,332.87 1097.68 3.20 272.3435

1999 22,449.41 1193.84 3.00 70.14648

2000 23,688.28 3372.18 18.10 69.86898

2001 25,267.54 3995.63 13.70 77.83398

2002 28,957.71 4193.27 12.20 78.0773

2003 31,709.45 5098.89 14.80 73.19962

2004 35,020.55 6260.59 11.80 74.90703

2005 37,474.95 4220.97 11.90 85.54584

2006 39,995.50 2204.72 12.30 91.50221

2007 42,922.41 2608.52 12.70 89.64672

2008 46,012.52 2843.56 14.90 99.12479

2009 49,856.10 3818.46 19.70 92.13576

2010 54,612.26 5241.65 21.10 100

2011 57,511.04 6519.69 23.90 100.3086

2012 59,929.89 7564.44 25.40 111.3909

2013 63,218.72 8492.55 23.50 118.8171

2014 67,152.79 9535.54 24.30 127.1006

2015 69,023.93 10948.53 126.0723

Source: Central Bank of Nigeria Statistical Bulletin 2015; World Bank Development Indicators

The above table 3.1 represents the used datasets at level series. The datasets however, were

treated in order to standardize them before use.

3.4 Model Framework

This study follows the Autoregressive Distributed Lag Model as developed and popularized

by Pesaran, Shin and Smith (2001). The technique has several advantages over other methods

for which cause it is chosen for this work. Firstly, it is efficient in small samples and not

Journal of Emerging Issues in Economics, Finance and Banking (JEIEFB)

An Online International Research Journal (ISSN: 2306-367X)

2017 Vol: 6 Issue: 2

2342 www.globalbizresearch.org

restricted in terms of stationary properties of the variables under study. The approach can allow

for a combination of I(0) and I(1) variables.

Following this method, the model below chosen as the optimal model following the Akaike

Information criterion is estimated. The optimal lag is (1,4,4,3) and the model is shown below:

LRGDP = BO + B1 LRGDPt-1 + B2 LREERt + B3LREERt-1 + B4LREERt-2 + B5LREERt-3 +

B6LREERt-4 + B7LPDEBT+ B8 LPDEBTt-1 + B9LPDEBTt-2+ B10LPDEBTt-3+ B11LPDEBTt-4+

B12LUNER+ B13LUNERt-1 + B14LUNERt-2+ B15LUNERt-3+ ᶓt -------------------------------------------… Eq. 1

RGDP= Real gross Domestic Product

REER= Real Effective Exchange Rate

PDEBT=Public Debt

REER t-1 t-4 = Lag of Real Effective Exchange Rate

PDEBT t-1 t-4 =lag of public Debt

UNER t-1 t-3=lag of Unemployment rate

0 = intercept

1 ----- 15 = Coefficients of variables

ᶓt ------------------ error term

4. Results and Discussion

Standard and Basic descriptive statistics were applied on the datasets to confirm their basic

characteristics as follows:

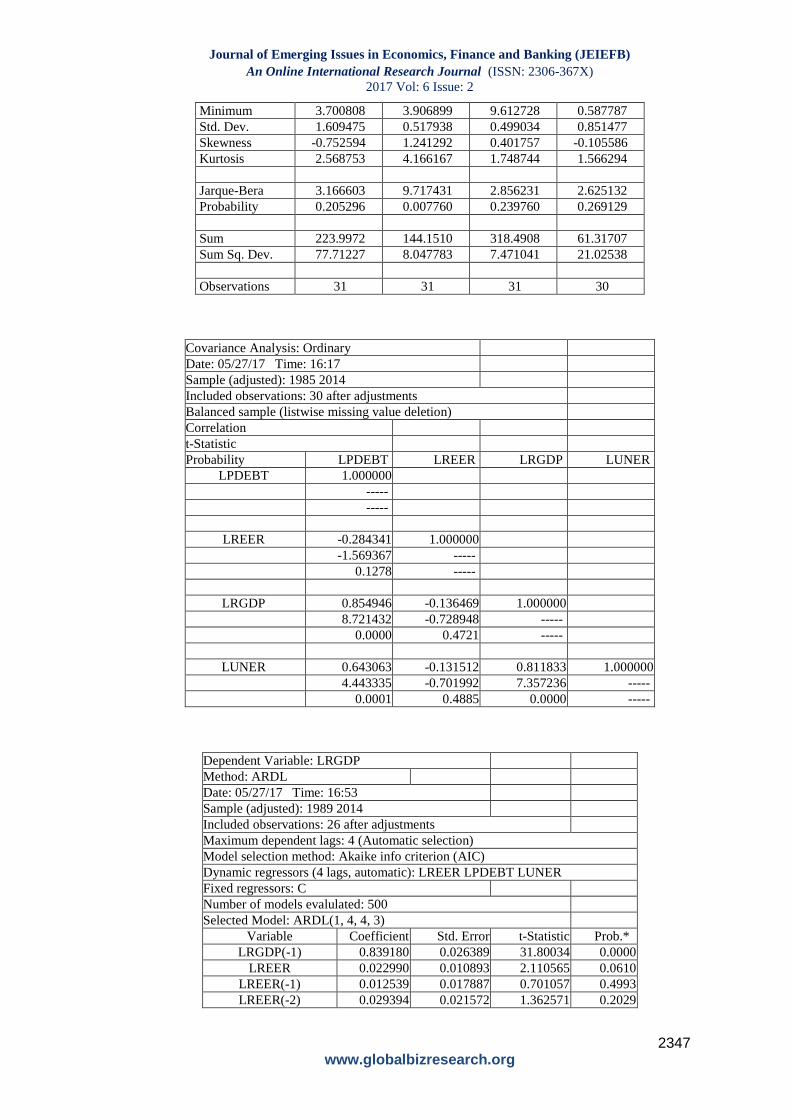

Table 2: Summary of Descriptive Statistics

Variables Mean Median Maximum Minimum Std

Deviation

Skewness Kurtosis Number of

observations

LPDEBT 7.23 7.69 9.30 3.70 1.61 -0.75 2.57 31

LREER 4.65 4.52 6.19 3.91 0.52 1.24 4.17 31

LRGDP 10.27 10.07 11.14 9.61 0.50 0.40 1.75 31

LUNER 2.04 2.21 3.23 0.59 0.85 -0.11 1.57 30

Table 2 above shows aggregative averages like the mean, median as well as measures of

spread and variation like standard deviation. It also shows skewness which is a measure of the

degree of symmetry and kurtosis which is a show of the degree of peakedness of the

observation. The results on skewness and kurtosis suggest a departure from normality. This is

not a point that is strong enough to discredit the goodness of the dataset for the analyses in

view.

Table 3: Summary of Unit Root Test Results

S/No Variables ADF Stat Critical Values Probability

Value

Inference

1% 5% 10%

1. LRGDP -3.10 -3.67 -2.97** -2.628* 0.038 I(1)

2. LREER -3.70 -3.67*** -2.96** -2.62* 0.009 I(0)

3. LUNER -6.00 -4.32*** -3.58** -3.23* 0.000 I(1)

4. LPDEBT -4.24 -4.30 -3.57** -3.22* 0.011 I(1)

The Unit root test results in Table 3 above show that the variables are integrated of different

orders which justifies the use of the Autoregressive distributed Lag Model (ARDL). While

Journal of Emerging Issues in Economics, Finance and Banking (JEIEFB)

An Online International Research Journal (ISSN: 2306-367X)

2017 Vol: 6 Issue: 2

2343 www.globalbizresearch.org

LRGDP, LUNER and LPDEBT are of order one variables following the ADF test, LREER is

order zero. This combination essentially validates the choice of ARDL.

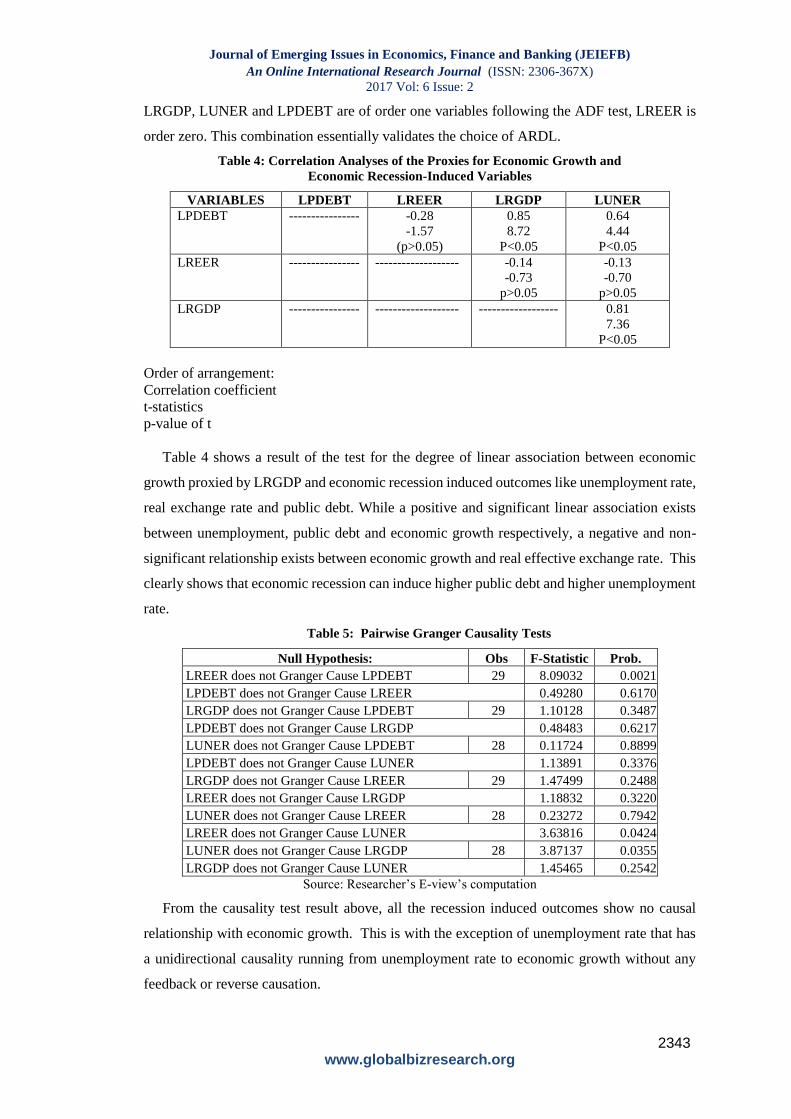

Table 4: Correlation Analyses of the Proxies for Economic Growth and

Economic Recession-Induced Variables

VARIABLES LPDEBT LREER LRGDP LUNER

LPDEBT ---------------- -0.28

-1.57

(p>0.05)

0.85

8.72

P<0.05

0.64

4.44

P<0.05

LREER ---------------- ------------------- -0.14

-0.73

p>0.05

-0.13

-0.70

p>0.05

LRGDP ---------------- ------------------- ------------------ 0.81

7.36

P<0.05

Order of arrangement:

Correlation coefficient

t-statistics

p-value of t

Table 4 shows a result of the test for the degree of linear association between economic

growth proxied by LRGDP and economic recession induced outcomes like unemployment rate,

real exchange rate and public debt. While a positive and significant linear association exists

between unemployment, public debt and economic growth respectively, a negative and non-

significant relationship exists between economic growth and real effective exchange rate. This

clearly shows that economic recession can induce higher public debt and higher unemployment

rate.

Table 5: Pairwise Granger Causality Tests

Null Hypothesis: Obs F-Statistic Prob.

LREER does not Granger Cause LPDEBT 29 8.09032 0.0021

LPDEBT does not Granger Cause LREER 0.49280 0.6170

LRGDP does not Granger Cause LPDEBT 29 1.10128 0.3487

LPDEBT does not Granger Cause LRGDP 0.48483 0.6217

LUNER does not Granger Cause LPDEBT 28 0.11724 0.8899

LPDEBT does not Granger Cause LUNER 1.13891 0.3376

LRGDP does not Granger Cause LREER 29 1.47499 0.2488

LREER does not Granger Cause LRGDP 1.18832 0.3220

LUNER does not Granger Cause LREER 28 0.23272 0.7942

LREER does not Granger Cause LUNER 3.63816 0.0424

LUNER does not Granger Cause LRGDP 28 3.87137 0.0355

LRGDP does not Granger Cause LUNER 1.45465 0.2542

Source: Researcher’s E-view’s computation

From the causality test result above, all the recession induced outcomes show no causal

relationship with economic growth. This is with the exception of unemployment rate that has

a unidirectional causality running from unemployment rate to economic growth without any

feedback or reverse causation.

Journal of Emerging Issues in Economics, Finance and Banking (JEIEFB)

An Online International Research Journal (ISSN: 2306-367X)

2017 Vol: 6 Issue: 2

2344 www.globalbizresearch.org

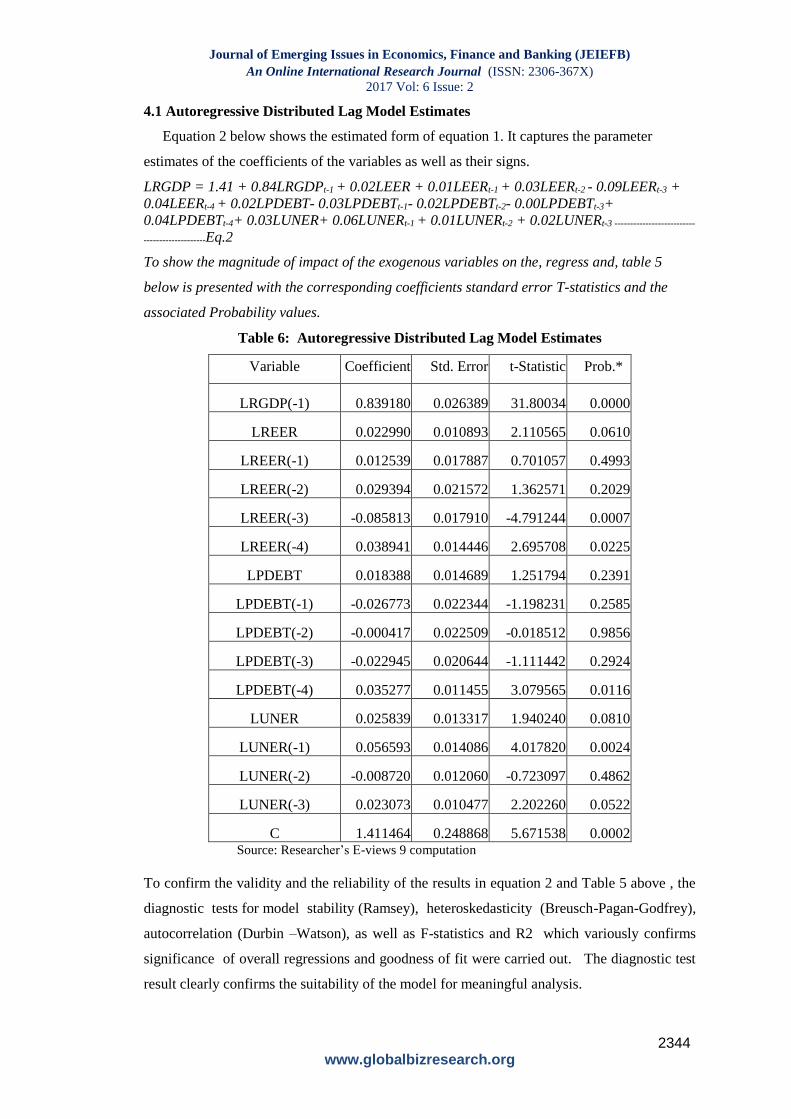

4.1 Autoregressive Distributed Lag Model Estimates

Equation 2 below shows the estimated form of equation 1. It captures the parameter

estimates of the coefficients of the variables as well as their signs.

LRGDP = 1.41 + 0.84LRGDPt-1 + 0.02LEER + 0.01LEERt-1 + 0.03LEERt-2 - 0.09LEERt-3 +

0.04LEERt-4 + 0.02LPDEBT- 0.03LPDEBTt-1- 0.02LPDEBTt-2- 0.00LPDEBTt-3+

0.04LPDEBTt-4+ 0.03LUNER+ 0.06LUNERt-1 + 0.01LUNERt-2 + 0.02LUNERt-3 --------------------------

--------------------Eq.2

To show the magnitude of impact of the exogenous variables on the, regress and, table 5

below is presented with the corresponding coefficients standard error T-statistics and the

associated Probability values.

Table 6: Autoregressive Distributed Lag Model Estimates

Variable Coefficient Std. Error t-Statistic Prob.*

LRGDP(-1) 0.839180 0.026389 31.80034 0.0000

LREER 0.022990 0.010893 2.110565 0.0610

LREER(-1) 0.012539 0.017887 0.701057 0.4993

LREER(-2) 0.029394 0.021572 1.362571 0.2029

LREER(-3) -0.085813 0.017910 -4.791244 0.0007

LREER(-4) 0.038941 0.014446 2.695708 0.0225

LPDEBT 0.018388 0.014689 1.251794 0.2391

LPDEBT(-1) -0.026773 0.022344 -1.198231 0.2585

LPDEBT(-2) -0.000417 0.022509 -0.018512 0.9856

LPDEBT(-3) -0.022945 0.020644 -1.111442 0.2924

LPDEBT(-4) 0.035277 0.011455 3.079565 0.0116

LUNER 0.025839 0.013317 1.940240 0.0810

LUNER(-1) 0.056593 0.014086 4.017820 0.0024

LUNER(-2) -0.008720 0.012060 -0.723097 0.4862

LUNER(-3) 0.023073 0.010477 2.202260 0.0522

C 1.411464 0.248868 5.671538 0.0002 Source: Researcher’s E-views 9 computation

To confirm the validity and the reliability of the results in equation 2 and Table 5 above , the

diagnostic tests for model stability (Ramsey), heteroskedasticity (Breusch-Pagan-Godfrey),

autocorrelation (Durbin –Watson), as well as F-statistics and R2 which variously confirms

significance of overall regressions and goodness of fit were carried out. The diagnostic test

result clearly confirms the suitability of the model for meaningful analysis.

Journal of Emerging Issues in Economics, Finance and Banking (JEIEFB)

An Online International Research Journal (ISSN: 2306-367X)

2017 Vol: 6 Issue: 2

2345 www.globalbizresearch.org

4.2 Diagnosis and Discussion of Test Results

R2 = 99%, DW Stat= 2.1; Ramsey (RESET) F-stat = 0.14(0.70)

BP for H F-Stat = 0.44(0.93)

In the ARDL result, for the appropriate or optimal lag, the selected model having the least

information criterion is ARDL (1, 4, 4, and 3) for real gross domestic product, exchange rate,

public debt and unemployment, respectively. It is therefore confirmed that economic recession

influences exchange rate, public debt, and unemployment which in turn impact on gross

domestic product. In the result, 1% change in the previous value of GDP induces 84% change

in succeeding years. For the real exchange rate, every 1% with the lapse of three years brings

about a negative effect of 8% reduction in the Nigerian gross domestic product. For the public

debt, each 1% change within the lapse of four years, results to 4% change. In the same manner

for the unemployment rate: 1% change in the previous value of unemployment results to 6%

change in the succeeding years. These results agree with the empirical work carried out by

Tejvan (2012)

which stated that a recession will typically be characterized by high employment rate,

higher government borrowing ,etc The result also agree with the research of Coile and Levine

(2011) who noted that the most prominent social effect of economic crises is job loss.

Looking at the results also, one can infer that these variables impact on the economic growth

at different degrees. Hence, this inference concurs with one of the findings of Rahman et al

(2017) which states that the severity of impacts would be determined by various factors, such

as Government policies, sources of revenue, categories of debt; and for individuals- educational

background which all together dictates who to be affected and the level of the impact.

Focusing on the short run relationship as shown in Table 6, we found most of the explanatory

variables and their lags as significant functions of Economic Growth at 5% level of significance.

Those with p-values less than 0.05 are significant as opposed to those above 0.05.

All the economic recession induced outcomes, including their own lags responded

negatively or positively to economic growth either contemporaneously or with a lapse of time

(lag). This broadly means that economic growth is a function of recession induced variables.

5. Conclusion

For the independent variables under study and their lags, only exchange rate with time lapses

of three years produced a negative impact of 8% reduction on the Nigerian economic growth

while other variables (public debt with four years lapses of time, unemployment rate with a

year lapse of time, and the lagged dependent variable (lagged GDP as a regressor) impacted

positively on the economic growth producing 4%, 6% and 84% increase on the GDP (at

every1% change), respectively.

Journal of Emerging Issues in Economics, Finance and Banking (JEIEFB)

An Online International Research Journal (ISSN: 2306-367X)

2017 Vol: 6 Issue: 2

2346 www.globalbizresearch.org

References

Bloomberg.com (2008): Global Recession Risk Grows as U.S Damage Spreads Jan. 28 Bohlund, Mark

(2016). Analysis: Why Nigerian Economy Is Facing its First-full year Recession since 1987. Bloomberg

Intelligence Economist, June 9 Nairametrics.com

Coile, C. and Levine, P. (2011) The Market Crash and Mass Layoffs: How the Current Economic Crisis

may Affect Retirement. The B.E.Journal of Economic Analysis and Policy 11(1)

Economist.Com (2008). The World Economy Bad or Worse 9th

Guatam, Omviri; Singh V.K. and Sharma, R (2015). Global recession and its Impact on

Telecommunication Industry: An Empirical Dissection. International Journal of Management and

Business 5(2) 107-116.

IMF World Economic Outlook Update (2008) Rapidly Weakening Prospects call for New Policy

Stimulus imf.org, 6th November.

Krugman, Paul (1998). Are Recessions the Inevitable Payback for good Times? Mises Review. 5 No

(spring, 1999) Dec. 3.

Lall, Subir (2008). “IMF predicts slower World Growth amid Serious Market Crisis”. International

Monetary Fund, 9th April.

Masarrat, Ghazal and Jha Suchita (2015) Assessing the Impact of Recession on Consumer’s Behaviour:

An Empirical Study in Dubai Researchers World, July www.questa.com.

Muanya, Chukwu (2017). Tackling Economic Recession-induced mental Health Disorder Guardian

Newspaper of 16 August.

My accounting course.com (2017) what is an economic Recession .Paul, D. (2010). Crisis in the

Eurozone and How to Deal with It. The Centre for Economic Policy Studies Policy Brief, 204, 1-6.

Naanen, Ben (2016). Recession: Nigeria Neglected History-Historic Society Business Day, 31st Oct.

National Bureau of Economic Recession (2008). Recession Dating Procedure;

http://www.nber.org/cycles/jan08bcdc_memo.html

OLugbile, Femi (2016) cited in Muanya (2017) Tackling Economic Recession-induced Mental Health

Disorders. Guardian Newspapers, 16 August.

Opejobi, Seun (2017). Why Dr Orji jumped into Lagos Lagoon- Colleague Reveals. Daily Post Daily

post.ng/2017/03/21 Reported by Essien Attah at 3rd Mainland Bridge in Lagos.

Pesaran, M.H: Shin, Y and Smith, R.J (2001) an Autoregressive Distributed Lag Modelling Approach to

Co-integration Analysis.

Rahman ,Md,Habibur;Galvan, Ramar Sanguino and Martinez, Ascension Barroso (2017), Economic

Recession in Spain :Exploring the Root causes , consequences and Recoveries For the Sustainable

Economic Growth. International Journal Of Economics and Financial Management 5(2),60-68 DOI

10.1269/ijefin-5-2-5 www.myaccountingcourse.com/accountingdictionary economic recession

Tejvan, Pettinger (2011). Problems of Recessions Economics Help.org. Oct 11 economics. The Wall

street Journal (2009). What is a Global Recession? 22nd April.

Wikipedia, the free Encyclopedia (2017) Global Recession Retrieved on 24/05/17.

World Economic Outlook (2009). Crisis and Recovery (PDF) Box 1.1 pp11-14 IMF April 24.

World Economic Outlook (2013). Statistical Appendix-Table – A summary of World Output (PDF) IMF.

Appendices

Descriptive Statistics

LPDEBT LREER LRGDP LUNER

Mean 7.225717 4.650033 10.27390 2.043902

Median 7.698356 4.516363 10.07274 2.207005

Maximum 9.300960 6.193609 11.14221 3.234749

Journal of Emerging Issues in Economics, Finance and Banking (JEIEFB)

An Online International Research Journal (ISSN: 2306-367X)

2017 Vol: 6 Issue: 2

2347 www.globalbizresearch.org

Minimum 3.700808 3.906899 9.612728 0.587787

Std. Dev. 1.609475 0.517938 0.499034 0.851477

Skewness -0.752594 1.241292 0.401757 -0.105586

Kurtosis 2.568753 4.166167 1.748744 1.566294

Jarque-Bera 3.166603 9.717431 2.856231 2.625132

Probability 0.205296 0.007760 0.239760 0.269129

Sum 223.9972 144.1510 318.4908 61.31707

Sum Sq. Dev. 77.71227 8.047783 7.471041 21.02538

Observations 31 31 31 30

Covariance Analysis: Ordinary

Date: 05/27/17 Time: 16:17

Sample (adjusted): 1985 2014

Included observations: 30 after adjustments

Balanced sample (listwise missing value deletion)

Correlation

t-Statistic

Probability LPDEBT LREER LRGDP LUNER

LPDEBT 1.000000

-----

-----

LREER -0.284341 1.000000

-1.569367 -----

0.1278 -----

LRGDP 0.854946 -0.136469 1.000000

8.721432 -0.728948 -----

0.0000 0.4721 -----

LUNER 0.643063 -0.131512 0.811833 1.000000

4.443335 -0.701992 7.357236 -----

0.0001 0.4885 0.0000 -----

Dependent Variable: LRGDP

Method: ARDL

Date: 05/27/17 Time: 16:53

Sample (adjusted): 1989 2014

Included observations: 26 after adjustments

Maximum dependent lags: 4 (Automatic selection)

Model selection method: Akaike info criterion (AIC)

Dynamic regressors (4 lags, automatic): LREER LPDEBT LUNER

Fixed regressors: C

Number of models evalulated: 500

Selected Model: ARDL(1, 4, 4, 3)

Variable Coefficient Std. Error t-Statistic Prob.*

LRGDP(-1) 0.839180 0.026389 31.80034 0.0000

LREER 0.022990 0.010893 2.110565 0.0610

LREER(-1) 0.012539 0.017887 0.701057 0.4993

LREER(-2) 0.029394 0.021572 1.362571 0.2029

Journal of Emerging Issues in Economics, Finance and Banking (JEIEFB)

An Online International Research Journal (ISSN: 2306-367X)

2017 Vol: 6 Issue: 2

2348 www.globalbizresearch.org

LREER(-3) -0.085813 0.017910 -4.791244 0.0007

LREER(-4) 0.038941 0.014446 2.695708 0.0225

LPDEBT 0.018388 0.014689 1.251794 0.2391

LPDEBT(-1) -0.026773 0.022344 -1.198231 0.2585

LPDEBT(-2) -0.000417 0.022509 -0.018512 0.9856

LPDEBT(-3) -0.022945 0.020644 -1.111442 0.2924

LPDEBT(-4) 0.035277 0.011455 3.079565 0.0116

LUNER 0.025839 0.013317 1.940240 0.0810

LUNER(-1) 0.056593 0.014086 4.017820 0.0024

LUNER(-2) -0.008720 0.012060 -0.723097 0.4862

LUNER(-3) 0.023073 0.010477 2.202260 0.0522

C 1.411464 0.248868 5.671538 0.0002

R-squared 0.999686 Mean dependent var 10.33759

Adjusted R-squared 0.999216 S.D. dependent var 0.447875

S.E. of regression 0.012543 Akaike info criterion -5.644022

Sum squared resid 0.001573 Schwarz criterion -4.869809

Log likelihood 89.37229 Hannan-Quinn criter. -5.421077

F-statistic 2124.275 Durbin-Watson stat 2.123246

Prob(F-statistic) 0.000000

*Note: p-values and any subsequent tests do not account for model

selection.

Heteroskedasticity Test: Breusch-Pagan-Godfrey

F-statistic 0.442235 Prob. F(15,10) 0.9255

Obs*R-squared 10.36891 Prob. Chi-Square(15) 0.7959

Scaled explained SS 4.478827 Prob. Chi-Square(15) 0.9957

Test Equation:

Dependent Variable: RESID^2

Method: Least Squares

Date: 05/27/17 Time: 17:00

Sample: 1989 2014

Included observations: 26

Variable Coefficient Std. Error t-Statistic Prob.

C -0.003710 0.003627 -1.022781 0.3305

LRGDP(-1) 0.000472 0.000385 1.228309 0.2475

LREER -2.32E-05 0.000159 -0.146339 0.8866

LREER(-1) -8.98E-05 0.000261 -0.344301 0.7378

LREER(-2) 0.000242 0.000314 0.768902 0.4597

LREER(-3) -0.000219 0.000261 -0.837655 0.4218

LREER(-4) 3.79E-05 0.000211 0.180189 0.8606

LPDEBT -0.000100 0.000214 -0.467729 0.6500

LPDEBT(-1) 0.000230 0.000326 0.707604 0.4954

LPDEBT(-2) -0.000277 0.000328 -0.844066 0.4184

LPDEBT(-3) 0.000212 0.000301 0.704360 0.4973

LPDEBT(-4) -0.000175 0.000167 -1.046152 0.3201

LUNER 2.75E-05 0.000194 0.141631 0.8902

LUNER(-1) 7.11E-05 0.000205 0.346146 0.7364

LUNER(-2) -3.27E-05 0.000176 -0.186056 0.8561

LUNER(-3) -0.000116 0.000153 -0.759908 0.4648

R-squared 0.398804 Mean dependent var 6.05E-05

Adjusted R-squared -0.502989 S.D. dependent var 0.000149

S.E. of regression 0.000183 Akaike info criterion -14.10081

Sum squared resid 3.34E-07 Schwarz criterion -13.32659

Log likelihood 199.3105 Hannan-Quinn criter. -13.87786

Journal of Emerging Issues in Economics, Finance and Banking (JEIEFB)

An Online International Research Journal (ISSN: 2306-367X)

2017 Vol: 6 Issue: 2

2349 www.globalbizresearch.org

F-statistic 0.442235 Durbin-Watson stat 2.799480

Prob(F-statistic) 0.925452

Ramsey RESET Test

Equation: UNTITLED

Specification: LRGDP LRGDP(-1) LREER LREER(-1) LREER(-2) LREER(

-3) LREER(-4) LPDEBT LPDEBT(-1) LPDEBT(-2) LPDEBT(-3)

LPDEBT(-4) LUNER LUNER(-1) LUNER(-2) LUNER(-3) C

Omitted Variables: Squares of fitted values

Value Df Probability

t-statistic 0.392511 9 0.7038

F-statistic 0.154065 (1, 9) 0.7038

F-test summary:

Sum of Sq. Df Mean Squares

Test SSR 2.65E-05 1 2.65E-05

Restricted SSR 0.001573 10 0.000157

Unrestricted SSR 0.001547 9 0.000172

Unrestricted Test Equation:

Dependent Variable: LRGDP

Method: ARDL

Date: 05/27/17 Time: 17:04

Sample: 1989 2014

Included observations: 26

Maximum dependent lags: 4 (Automatic selection)

Model selection method: Akaike info criterion (AIC)

Dynamic regressors (4 lags, automatic):

Fixed regressors: C

Variable Coefficient Std. Error t-Statistic Prob.*

LRGDP(-1) 1.299411 1.172857 1.107903 0.2966

LREER 0.037076 0.037648 0.984805 0.3505

LREER(-1) 0.017774 0.022964 0.773996 0.4588

LREER(-2) 0.043952 0.043405 1.012592 0.3377

LREER(-3) -0.127796 0.108586 -1.176914 0.2694

LREER(-4) 0.061138 0.058532 1.044530 0.3235

LPDEBT 0.029164 0.031456 0.927135 0.3780

LPDEBT(-1) -0.041007 0.043132 -0.950719 0.3666

LPDEBT(-2) -1.96E-05 0.023548 -0.000832 0.9994

LPDEBT(-3) -0.035509 0.038602 -0.919858 0.3816

LPDEBT(-4) 0.050415 0.040385 1.248372 0.2434

LUNER 0.036644 0.030847 1.187929 0.2653

LUNER(-1) 0.083388 0.069834 1.194091 0.2630

LUNER(-2) -0.013857 0.018169 -0.762647 0.4652

LUNER(-3) 0.035834 0.034304 1.044580 0.3235

C -0.771049 5.566470 -0.138517 0.8929

FITTED^2 -0.025223 0.064262 -0.392511 0.7038

R-squared 0.999692 Mean dependent var 10.33759

Adjusted R-squared 0.999143 S.D. dependent var 0.447875

S.E. of regression 0.013110 Akaike info criterion -5.584072

Sum squared resid 0.001547 Schwarz criterion -4.761471

Log likelihood 89.59294 Hannan-Quinn criter. -5.347193

F-statistic 1823.048 Durbin-Watson stat 2.133603

Prob(F-statistic) 0.000000

*Note: p-values and any subsequent tests do not account for model

selection.