impact of dividend announcement on … impact of dividend announcement on stock prices:a study in...

TRANSCRIPT

IMPACT OF DIVIDEND ANNOUNCEMENT ON STOCK PRICES:

A STUDY IN MALAYSIAN STOCK EXCHANGE CONTEXT

IBRAHIM SAMEER

A Master’s Project submitted in partial fulfillment of the requirements for the degree of

Master of Business Administration

Faculty of Business Management

Villa College

Open University Malaysia

2012

ii

DECLARATION

Ibrahim Sameer

S101061984

I hereby declare that this Master’s Project is the result of my own work, except for quotations

and summaries which have been duly acknowledged.

Signature: Date:

iii

IMPACT OF DIVIDEND ANNOUNCEMENT ON STOCK

PRICES:A STUDY IN MALAYSIAN STOCK

EXCHANGE CONTEXT

IBRAHIM SAMEER

June 2012

ABSTRACT

This study examined the stock market reaction on the announcement of dividend increase or

decrease in comparison with last year dividend. This study also assesses market efficiency

which exists in Malaysia Stock Exchange (Bursa Malaysia). The classical event study

methodology, ANOVA: Single Factor and Run Test are adopted to examine the price

reactions of 77 sampled listed companies sampled 2010 to 2012, from the Main Board of

Bursa Malaysia surrounding twenty one (+10, -10) days of the announcement dates. Results

of this study supports dividend signaling theory, especially for dividend increased firm,

because investors are able to earn abnormal return on the announcement of dividend

increased. But the firms which select to announce a relative decrease in their dividend firms,

investors expect that to happen therefore a clear picture was not able to draw. This result

shows that Bursa Malaysia Stock Exchange has not reached in its full efficiency in its semi –

strong form.

Keywords:

Abnormal return, ANOVA, Run Test, Event Study, dividend signaling theory

iv

ACKNOWLEDGEMENTS

Alhamdulillah!

In the name of Allah, most benevolent, ever merciful. All praise to be Allah, Lord of all the

worlds, giving me the forte, new ideas and forbearance from the commencement until the

completion of this project paper.

First and foremost, I owe my debt of gratitude especially to my supervisor, Mr. Muhammed

Tariq for his supportive censure, his erudite philosophies, reassurance and guidance to mould

and contour this project paper. Without his support and help, this paper cannot be completed

on time. Second, I owe my debt of gratitude especially to Villa College Rector Dr. Ahmed

Anwar for his support and encouragement throughout this project paper.

My indebtedness and thankfulness goes to my beloved wife and my offspring, Mausooma Ali

and Mariyam Azka Ibrahim respectively; who always heartens and show their endurance

through the accomplishment of this MBA project paper. Moreover, my distinct appreciations

also go to all my friends, directly and indirectly for the reason that of their association in

assisting, to gather all the imperative information related to this project Paper.

Thank you very much.

v

TABLE OF CONTENT

DECLARATION ....................................................................................................................... ii

ABSTRACT ............................................................................................................................. iii

ACKNOWLEDGEMENTS ...................................................................................................... iv

TABLE OF CONTENT ............................................................................................................. v

LIST OF TABLES ................................................................................................................. viii

LIST OF FIGURES .................................................................................................................. ix

DEFINITION OF TERMS ........................................................................................................ x

CHAPTER 1INTRODUCTION ................................................................................................ 1

1.1 Background of the Study ............................................................................................. 1

1.2 Problem Statement ...................................................................................................... 3

1.3 Objectives of the Study ............................................................................................... 4

1.4 Research Questions and Hypothesis ........................................................................... 4

1.4.1 Research Questions .............................................................................................. 4

1.4.2 Hypothesis............................................................................................................ 4

1.5 Significance of the Study ............................................................................................ 6

1.6 Scope of the Study....................................................................................................... 7

CHAPTER 2 REVIEW OF LITERATURE .............................................................................. 8

1.7 Theoretical Framework ............................................................................................... 8

1.8 Information Content Hypothesis ................................................................................. 9

vi

1.8.1 Middle East Market............................................................................................ 13

1.8.2 Asian Market ...................................................................................................... 14

1.8.3 European Market ................................................................................................ 16

1.8.4 America and African Market ............................................................................. 18

1.8.5 Malaysian Stock Exchange Market Specific ..................................................... 20

1.9 Agency Cost .............................................................................................................. 23

1.10 Efficient Market Hypothesis ..................................................................................... 24

1.11 Conclusion ................................................................................................................. 26

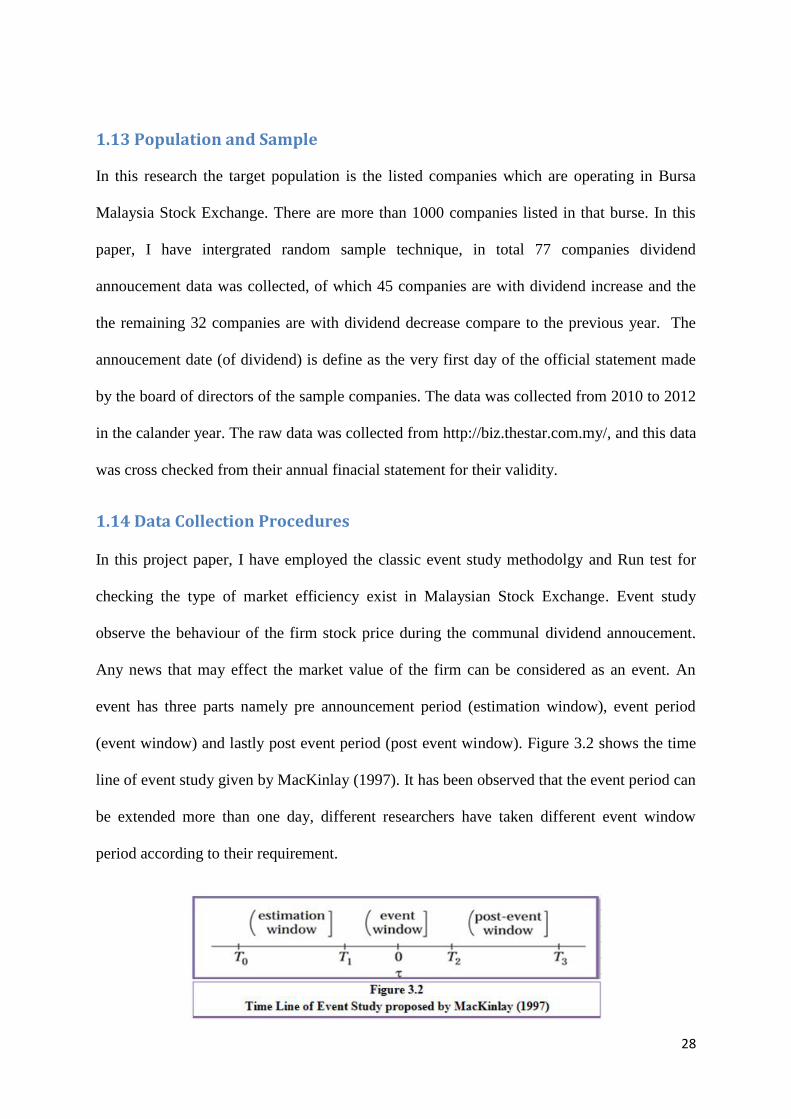

CHAPTER 3 METHODOLOGY ............................................................................................ 27

1.12 Research Design ........................................................................................................ 27

1.13 Population and Sample .............................................................................................. 28

1.14 Data Collection Procedures ....................................................................................... 28

1.14.1 Daily Return Measure ( ) ............................................................................ 30

1.14.2 Adjusted Mean Measures ..................................................................... 31

1.14.3 Abnormal Return .................................................................................. 31

1.14.4 Average Abnormal Return (AAR) ..................................................................... 32

1.14.5 Average Abnormal Return (CAAR) .................................................................. 32

1.14.6 Standard Deviation (σ) ....................................................................................... 32

1.14.7 Standard Error ................................................................................ 33

1.14.8 T-Test ( ) ............................................................................................ 33

1.14.9 Run Test ............................................................................................................. 33

vii

1.15 Framework for Data Analysis ................................................................................... 34

1.16 Methodological Issues ............................................................................................... 36

CHAPTER 4 DATA ANALYSIS AND RESULTS ............................................................... 37

1.17 Dividend Increase 45 Firms ...................................................................................... 37

1.18 For dividend Decrease 32 Firms ............................................................................... 40

1.19 Combination of Dividend Increase / Decreased ........................................................ 43

1.20 ANOVA: Single Factor ............................................................................................. 45

1.21 Run Test .................................................................................................................... 45

CHAPTER 5 DISCUSSION AND CONCLUSION ............................................................... 47

1.22 Summary of Main Finding ........................................................................................ 47

1.23 Discussion ................................................................................................................. 49

1.23.1 Dividend Increase 45 Firms ............................................................................... 49

1.23.2 Dividend Decreased 32 Firms ............................................................................ 50

1.23.3 Combined CAAR ............................................................................................... 51

1.24 Implication ................................................................................................................ 53

1.25 Limitations of the Study ............................................................................................ 53

1.26 Directions for Future Research ................................................................................. 54

REFERENCES ........................................................................................................................ 56

APPENDICES ......................................................................................................................... 64

viii

LIST OF TABLES

Table 4.1: Stock Market Reaction to Average Abnormal Return (AAR), Cumulative Average

Abnormal Return (CAAR), T – Values for Dividend Increased Announcement of 45

Firms…………….………………………………………...………………………………….38

Table 4.2: Stock Market Reaction to Average Abnormal Return (AAR), Cumulative Average

Abnormal Return (CAAR), T – Values for Dividend Decreased Announcement of 45

Firms………………….……………………………………...……………………………… 41

Table 4.3: Test of Significance at different Event Window on Cumulative Average

Abnormal Return (CAAR) for dividend Increased (45) and Decreased (32)

Firms…………………………………………………………………………………….……44

Table 4.4: ANOVA: Single Factor Test Results ………………………..…………………..45

Table 4.5: Run Test Results for Dividend Increased / Decreased (77 Firms) (Observation

Period (+15, -15) …………..……………………………………………..……………….…46

ix

LIST OF FIGURES

Figure 2.1: Researchers who are in favor and against of Dividend Signaling

Hypothesis………………………………………………………………………………..……8

Figure2.2: The Capital Markets’ Reaction to (Unanticipated) Equity Cash Flow

Decisions…………………………………………………………………………………..... 12

Figure 2.3: Different Forms of Efficient Market Hypothesis Proposed by Fama, Fisher,

Jensen and Roll (1969)………………..…………………………………………………...... 26

Figure3.1: Research Framework………………....………….……..………………….…… 27

Figure3.2: Time Line of Event Study proposed by MacKinlay (1997) .………….…….…. 28

Figure3.3: Time Line for Event Window for this research………...……………………..... 30

Figure4.1: AAR Surrounding the Announcements of Dividend Increase / Initiation for 45

Observations in each Event Window (-10, +10)……….………………………....………….39

Figure4.2: CAAR Surrounding the Announcements of Dividend Increase / Initiation for 45

Observations in each Event Window (-10, +10)……….……………………...…….……….40

Figure4.3: AAR Surrounding the Announcements of Dividend Decrease / Initiation for 32

Observations in each Event Window (-10, +10)….………………………...……….……….42

Figure4.4: CAAR Surrounding the Announcements of Dividend Decrease / Initiation for 42

Observations in each Event Window (-10, +10)………………………………………….….43

Figure4.5: CAAR Surrounding the Announcements of Dividend Increased and Decreased for

77 Observations in each Event Window (-10, +10)………………………………...….…….44

x

DEFINITION OF TERMS

APT – Arbitrage Pricing Model

ANOVA – Analysis of Variance

AR – Abnormal Return

AAR – Average Abnormal Return

BM – Bursa Malaysia

CAAR – Cumulative Average Abnormal Return

CAPM – Capital Asset Pricing Model

CFPS – Cash Flow Per Share

EPS – Earning Per Share

EMH – Efficient Market Hypothesis

EW – Event Window

GDP – Gross Domestic Product

ROE – Return on Equity

NASDAQ– National Association of Securities Dealer Automated Quotations

NYSE– New York Stock Exchange

1

CHAPTER 1

INTRODUCTION

1.1 Background of the Study

Stockholders can earn return for the stock by means of two ways i.e. in the form of dividend

and capital gain. In the world of corporate finance, it is not a compulsion for the company to

pay dividend for the shareholders but was relatively noted that numerous organizations that

disburse dividend on customary basis. Now the question is why organizations pays dividend,

there has been lot of research done on this topic during the past five decades. In straight

forward terms dividend is an amount which pays to the stockholders in cash / stock by the

company from its earning every year or quarterly basis. As a result, when the firm pays

dividend it means that cash is going out from the firm, hence the capital structure of the firm

will get effected or changed depends upon the proportion of the payout ratio.

The pronouncement of dividend effect on the stock price will be based upon the dividend

policy of the firm. When the firms make proclamation of dividend in cash increase or

decrease the firm is making a dividend policy decision. When the firm makes the dividend

policy decision they need to make definite that they should be able to uphold the policy for a

quite elongated period. If they are not able to prolong the homogeny in their dividend payout

ratio, it might effect the stock market price of the company.

According to Ross, Westerfield, & Jaffe (2008) when the firm declared dividend increase

generally stock price increases and when the firm dividend decrease then the stock price

decrease according to the information content hypothesis.

2

The issue, whether the manager in the firm dupe the stockholder by declearing dividend

increase, the riposte to this question is yes, but it can be done for a diminutive epoch of time

and the stock market price may decrease much beneath than the intrinsic value of the stock

price. Another imperative fact that manager requisite to retain in mind when deciding the

payout policy, is there any project which can engender optimistic Net Present Value (NPV),

if so the managers need to contemplate about in investing those project rather than affirming

high dividend payout. If the firm desired to upturn their payout, then they perchance have to

forgo some of the positive NPV project, which may in the long run firm perhap shurt.

Agency cost is also one of the significant matter in the corporate finance world. Agency cost

ascend amongst the managers (management) and the shareholers due to the conflict of

interest. According to Ross, Westerfield, & Jaffe (2008) agency cost can be divided into two

namely direct and indirect. Indirect agency cost can be a lost opportunity. Direct agency cost

come in two forms. The first type is corporate expenditure of managers which benefits for

him/her (for instance costly car) but an expenditure for shareholders. The second type is

expenditure arise for monitoring managers action (for instance Auditors salary) but an

expenditure for shareholders.

Efficient Market Hypothesis (EMH) was propounded by Fama (1970) in his seminal paper

titled Efficient Capital Markets: A Review of Theory and Empirical Work. In an efficent

market all the security prices are fully reflected to all the available information and no one

will be able to earn excess profit using this information. According to him there are three type

of efficiency namley weak form, semi – strong, and strong form of market efficiency.

The main intention of this research is to examined the impact of dividend announcement on

stock price in the Malaysian stock exchange (Bursa Malaysia). The next aim of this research

is to find out which form of market efficiency exist in the Malaysian stock exchange namely

3

strong form, semi strong form or weak form of market efficiency. In this research I have used

event study methodology in order to measure the abnormal return of the company’s stock

prices that occurred during a fixed period, before and after the day of dividend increase or

decrease announcement.

1.2 Problem Statement

Malaysia is following a constitutional monarchy. The current king is Yang Di-Pertuan

Agong. He is the head of the states in a ceremonial role. The head of government is prime

minister. The incumbent prime minister is Najib Tun Razak. Malaysia is a developing

country. Prior to the 1997 crash, Malaysia is one of Asia’s “Tiger Economy” but it has

recovered. Currently, Malaysian economy ranks 30th

in the world in term of per capita GDP

[Szczepanski (2012)].

The stock exchange of Malaysia was established in 1964 but later it was renamed as Bursa

Malaysia Berhad on 14 April 2004. Bursa Malaysia is one of the prevalent stock exchanges in

Asia with more than 1000 companies trading through Bursa Malaysia Stock Exchanged

[BursaMalaysia (2012)].

Since the publication of the seminal work of Miller & Modigliani (1961) dividend irrelavance

theory, there has been number of row that have been proposed in the finance litarature for

instance Pettit (1972), Bhattacharya (1979), John & Williams (1985), Miller & Rock (1985),

Asquith & Mullins (1986), Ling, Mutalip, Shahrin, & Othman (2008), Jais, Karim, Funaoka

& Abidin (2009), Mohamed, et al., (2010), Hussin, Ahmed &Ying (2010), Isa & Lee (2011),

and Ismail & Rahman (2012), in order to rationalize why firm confer dividends to its

shareholders. By and large, the reasons why firm recompense dividend to their shareholders

that was documented in the above mention literature, first reason was firms pay dividend in

order to signal the information to the market, second reason was in order to return excess

4

cash if there is no positive NPV project for fairly to the shareholders and third reason may be

to attract clienteles. Upto today in the world of corporate finance there was no singal theory

which dominate, why firm pay dividends?

On the other hand researchers who are in favour of Miller & Modigliani (1961) theory

include such Abdullah, Rashid, & Ibrahim (2002), Ali & Chowdhury (2010), Akbar & Baig

(2010), Robbani & Bhuyan (2010) and Padmavathy & Ashok (2012).

1.3 Objectives of the Study

There are two motives behind in doing this research, at the outsetis to find out whether there

is an opportunity in the Bursa Malaysia for arbitrages and secondly examining which form of

market efficiency exist in the Bursa Malaysia Stock Exchange, because according to

Dr.Momani & Dr.Alsharari (2012) stock exchange is known as a mirror to the economic

situation of the Countries.

1.4 Research Questions and Hypothesis

1.4.1 Research Questions

1. What is the impact of dividend announcement on stock price, is there any opportunity

for arbitrage in Malaysian stock exchange (Bursa Malaysia)?

2. What kind of market efficiency exist in Malaysian stock exchange (Bursa Malaysia)

namely weak form, semi – strong form or strong form?

1.4.2 Hypothesis

In order to answer the above questions following hypothesis was developed:

5

1.4.2.1 Abnormal Return for dividend increase / initiationfirms

H₀: there is statistically zero significant abnormal return (positive or negative) due to

dividend increase / initiation. Therefore the Bursa Malaysia Stock Market is semi – strong

efficient with respect to the dividend increase / initiation.

H₁: there is statistically significant abnormal return (positive or negative) due to dividend

increase / initiation.

₁

1.4.2.2 Cumulative Average Abnormal Return for dividend increase / initiation firms

H₀: there is statistically zero significant cumulative average abnormal return (positive or

negative) due to dividend increase / initiation. Therefore the Bursa Malaysia Stock Market is

semi – strong efficient with respect to the dividend increase / initiation.

H₁: there is statistically significant cumulative average abnormal return (positive or negative)

due to dividend increase / initiation.

₁

1.4.2.3 Abnormal Return for dividend decrease / omission firms

H₀: there is statistically zero significant abnormal return (positive or negative) due to

dividend decrease / omission. Therefore the Bursa Malaysia Stock Market is semi – strong

efficient with respect to the dividend decrease / omission.

₁

H₁: there is statistically significant abnormal return (positive or negative) due to dividend

decrease / omission.

₁

6

1.4.2.4 Cumulative Average Abnormal Return for dividend decrease / omission firms

H₀: there is statistically zero significant cumulative average abnormal return (positive or

negative) due to dividend decrease / omission. Therefore the Bursa Malaysia Stock Market is

semi – strong efficient with respect to the dividend decrease / omission.

H₁: there is statistically significant cumulative average abnormal return (positive or negative)

due to dividend decrease / omission.

₁

1.4.2.5 ANOVA – Single Factor

H₀: Malaysian Stock Exchange all individual batch means are equal.

₁

H₁: Malaysian Stock Exchange all individual batch means are not equal.

₁ ₁

1.4.2.6 Run Test Hypothesis

H₀: Malaysian Stock Exchange stock data was produce in random manner.

H₁ Malaysian Stock xchange stock data was not produce in random manner.

₁

1.5 Significance of the Study

As highlighted in the problem statement, dividend is considered as a mechanism to signal

about the future prospect of the firm. Despite the fact that, there are countless studies done in

this on dividend in Malaysia, but a small number of studies have done on checking the form

of market efficiency and dividend announcement in collectively. As a result, I look forward

7

to that this research will shed supplementary illumination in the existing literature on this

topic in Malaysia.

I am optimism that this study perhaps be obliging for the government, impending investors,

researchers, managers and the current shareholders of the company in perceptive the dividend

policies of the firms in Malaysian economy.

1.6 Scope of the Study

In the world of corporate finance there are abundant causes which may affect the stock price

of firms, explicitly corporate dividend announcement, micro and macro environment of the

country investor’s buoyancy on the market etc.

Nevertheless, in this case study base paper I am going to test dividend signaling hypothesis in

Malaysia Stock Exchange, in other words I am going to study on the announcement of

dividend is there is any significant change in the Bursa Malaysia stock prices, and through

this I am going to test the form of market efficiency that exist in Bursa Malaysia., namely

weak form or semi – strong form or strong form. In this research paper data was collected

from 2010 to 2012 and total sample size is 77 firms, of which 45 have shown dividend

increased and 32 are dividend decreased firm. I also have incorporated firms who have

increased and decreased cash dividend and weigh against to their previous year

announcement. In this study I have not integrated any stock split, stock repurchase, stock

dividend, or merger and acquisitions.

8

CHAPTER 2

REVIEW OF LITERATURE

1.7 Theoretical Framework

The intention of this chapter is to review preceding work done by dissimilar academics on

this subject. In the world of corporate finance dividend payout policy is solitary dubious

topics among the researchers after publishing the seminal work of Miller & Modigliani

(1961) dividend irrelevance theory. The entire literature was alienated into two parts, some

are in support that dividend payout do convey information to the market participant and the

other group are support that dividend does not convey any information to the market

participants. Below figure 2.1 represent a snapshot of researchers who are in favor and not in

favor of dividend signaling hypothesis.

9

1.8 Information Content Hypothesis

Lintner (1956) was one of the pioneering scholar in the field of corporate finance. One of his

classic study was done on the topic of “Distribution of Incomes of Corporations Among

Dividends, Retained Earnings, and Taxes”. In this study he have used 600 observations from

28 listed companies. He states that “the belief on the part of many managements that most

stockholders prefer a reasonably stable rate and that the market puts a premium on stability

or gradual growth rate – were strong enough that most managements sought to avaoid

making changes in their dividend rates that might have to be reversed within a year or so.”

Therefore, Lintner argued that management of any organization desire to retain the firmness

of the dividend payout ratio rather than altering the payout ratio habitually. He affirm that

management of the organization consider about the future prospect of the company sooner

than deciding the dividend payout. If they sense organization going to carry outsound then

they conceivably declear high dividend and if they believe prospect is ambiguous then

management decleare low dividend. But on the other hand Lintner revealed that companies

are indisposed to lessen the dividend because it perhaps drive a negative signal.

Miller & Modigliani (1961) study was the most vital literature in the corparate finance world,

because Miller & Modigliani (1961) study documented that dividend payout does not add any

value to the firm, this phenomena was called ‘Dividend Irrelevence Theory’. It has to be

noted that the influential paper of Miller & Modigliani (1961) the Dividend Irrelevence

Theory exist in a market which is perfect, rational investors, no brokarage fee, tax free world,

no transetion cost. But now we are living bona fide world, postulation made by Miller &

Modigliani are now on reverse, namely there are diffierent types of taxes, market is not

perfect.

10

Nonetheless, there are numerous contemporary study which documented that dividend payout

do add value to the firm and information content hypothesis was true, which may include the

study of Pettit (1972), Bhattacharya (1979), John & Williams (1985), Miller & Rock (1985),

Asquith & Mullins (1986), DeAngelo, DeAngelo, & Skinner (2004), Ryan, Besley, & Lee

(2000)

Pettit (1972) have investigated the the validity of efficient market hypothesis and how the

dividend annoucment effect the market participant in the New York Stock Exchanged. He

have employ sample size of 625 observation for the period of January 1964 to June 1968. He

documented that there is no information leakage in the market. He also avow that dividend

annoucement do communicate valuable information to the market participant, dividend

increase annoucements good news and dividend decrease annoucemnt leads to bad news. He

states that “the market reacts very dramatically to these annoucements when dividends are

reduced or when a substantial increase takes place.”

Bhattacharya (1979) was the first person who developed dividend signalling model for the

corporate finance world, though dividend are tax higher rate than the capital gain. He

acknowledged that increase in dividend signal the future prospect of the firm. He states that

“dividends function as a signal”. Another momentous conclusion he drew was manager

know more private information about the company than outside shareholders, therefore the

only way to commune with investors is through the payout policy of the firm. As an investors

we may suspect that financial statement presented by the management perhaps be backed by

the ghostwrting of well paid public relation firm or speicialist.

John & Williams (1985) advocate that there is positive correlation between dividend and

stock price. In their study, they put forward that when the organization amend its payout

policy to signal the future prospect of the firm, because managers in the organization know

11

more about the firm than the outsider (shareholders). John & Williams states that “corporate

insiders with more valuable private information optimally distribute larger dividends and

receive higher prices for their stock.” This has been proven by many researchers during the

past four decades in the corporate finance world.

Miller & Rock (1985) have probe the dividend policy of the firm when there is asymmetry of

information between the stockholders and the mangers. They established that dividend

annoucement merely provide the missing pieace of information to the investors. They also

documented that only large firm whose earning is more can make larger dividend

annoucements, another imperative thing they found was they are in favour of dividend

signaling hypothesis. They states that “dividends make sense as signals for the good news,

not the bad news firm.”

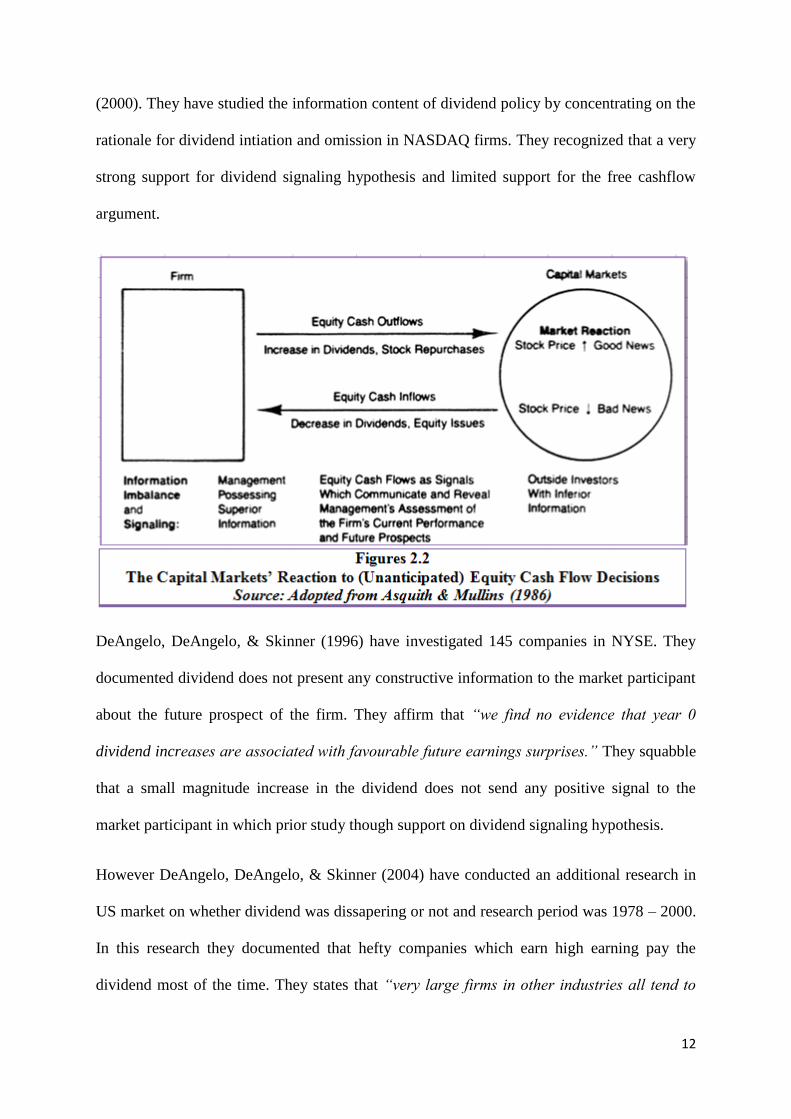

Asquith & Mullins (1986) have examined the NYSE market reaction to dividend

annocement, employe a sample size of 168 firm during a period of 1964 to 1980. In this study

they have incorporated the firm who pay dividend in their corporate history or recommence

paying dividend after a hiatus of atleast ten years. They documented that if the firm deaclared

a dividend yield of 0.67% then the stock price was not effected, but if dividend declared is

more than 0.67% investors pleasatly surprised, resulting postive return in the bourse. They

states that “on the annoucement day, the firm must fulfill investors’ expectations or suffer a

reduction in stock price.” The below figure 2.2 demonstrate that when there is an

unanticipated equity cash outflow (increased in dividend and stock repurchase) the stock

price move positivley and that is taken as good news by the market participants. On the other

hand if the organization requires cash inflow through captial market by issuing equity

(decrease in dividend and equity issue), the result is negative, the stock price move

downwards and the investors take it as a bad news. This result is consistent with their

previous research research Asquith & Mullins (1983) and more recently Ryan, Besley, & Lee

12

(2000). They have studied the information content of dividend policy by concentrating on the

rationale for dividend intiation and omission in NASDAQ firms. They recognized that a very

strong support for dividend signaling hypothesis and limited support for the free cashflow

argument.

DeAngelo, DeAngelo, & Skinner (1996) have investigated 145 companies in NYSE. They

documented dividend does not present any constructive information to the market participant

about the future prospect of the firm. They affirm that “we find no evidence that year 0

dividend increases are associated with favourable future earnings surprises.” They squabble

that a small magnitude increase in the dividend does not send any positive signal to the

market participant in which prior study though support on dividend signaling hypothesis.

However DeAngelo, DeAngelo, & Skinner (2004) have conducted an additional research in

US market on whether dividend was dissapering or not and research period was 1978 – 2000.

In this research they documented that hefty companies which earn high earning pay the

dividend most of the time. They states that “very large firms in other industries all tend to

13

pay dividend”. A research conducted by Fama & French (2001) found that firm paying cash

dividend fall from 66.5% in 1978 and in 1999 upto 29.8%, they have used aggregate dividend

from 1978 to 1999. This result is inconsistent with DeAngelo, DeAngelo, & Skinner (2004)

they have found that increase dividend over the past two decades. The result is inconsistent

due to fact that Fama & French (2001) have used cumulative dividend, which may be

misleading when declearing dividend because large firm probably dominate the collective

result of such dividends. Another vital issue documented by DeAngelo, DeAngelo, & Skinner

(2004) was that high tax bracket earner like to invest in a firm which don’t give dividend

because dividend are tax more than the capital gain. They states that “high tax bracket

investors desire to invest substantial amount of wealth.”

From here ownwards I am going to look into previous studies done on thistopic on the basis

of continental wise, so that it will be easy to relate theories and findings of this study based

on the region or the continents.

1.8.1 Middle East Market

By looking into Middle East Market Alzahrani & Skerratt (2009) have examined Saudi Stock

Market on the subject of dividend signaling hypothesis. They found that investors underreact

to positive news and overreact to negative news. An extra vital things they documented was

prior to the announcement dividend, their was an information leakage, which is also

establishedby Chander, Sharma, & Mehta (2007), Liargovas & Repousis (2011), Taneem &

Yüce (2011), Yilmaz & Selcuk (2010).

On the other hand, Alisinaei & Habibi (2012) have looked into the causes that are relevent to

payout ratio in Tehran stock exchange. In their delve, they have tested six hypothesis. In the

first hypothesis, they tested that CEO compansation was negatively related to payout ratio.

They originate that a siginificant relationship between them. In the second hypothesis they

14

studied the rapport between the market to book value ratio and dividend payout ratio. They

established that there is a significant rapport between them. In the third hypothesis they have

tested the relationship between cost of capital and dividend payout ratio, the reuslts found

that there is a significant relatioship between them. In the fourh hypothesis they have tested

the relationship between systematic risk and dividend payout ratio, the results found that no

relationship (no significant) found. The fifth hypothesis they have tested is the relatioship

between income and payout ratio, the results they found is there is no significant relatioship.

The last hypothesis they tested is the relationship between debt to equity and dividend payout

ratio, the results found that there was a siginificant relationship between.

1.8.2 Asian Market

While reviewing Asian market, I found varied result. A research conducted by Mandal & Rao

(2010) found that Indian stock market is efficient in its semi strong form with reverence to

both events: dividend initiation and dividend omission. They have conducted their research

from 1990 to 2009 employing 40 securities in dividend initiation and 44 securities dividend

omission. In their research they have found enough evidence for the support of both

announcements dividend initiation and dividend omission carry new value relevant

information to the market participants. For the sample of dividend initiation they have used

cross sectional t-test at 5% significance and reveal that AAR values (1.197 & 1.434)

significantly are different from zero only for two days that is (t=-1 and t = 0), but in case of

dividend omission only the announcement day (t = 0) AAR values (-1.985) is significance at

1% and the rest of the event period AAR is not significance. Therefore they found that

investors react more on dividend omission compare to dividend initiation, in case of dividend

initiation though the market is little sluggish but for dividend omission it is more reactive.

However Ali & Chowdhury (2010) have investigated Dhaka Stock Exchange (DSE) in

Bangladesh the effect of dividend announcement on the stock price. They found that dividend

15

announcement does not carry information to the market participants, due to the fact that

insider information.Sharma (2011) also support the view of Ali & Chowdhury (2010).

Sharma (2011) documented that dividend annoucement does not result any random behaviour

in the stock burse, and he states that information content of dividend annoucement was fully

reflected in shares therefore in Bombay Stock Exchange in India, no stockholders are able to

earn abnormal return during the event period.

Another research conducted by Akbar & Baig (2010) in Karachi stock exchange, in Pakistan

found a mix result. They have cash dividend annoucement effects on stock price, they

concluded that annocement of cash dividend is statistically insignificants meaning their

results are inconsistent with dividend signaling theory hypothesis.

Taneem & Yüce (2011) have conducted research in Indian stock exchange. They have used

82 companies’ data in Bombay stock exchange which announce dividend during the year

2004 to 2007. Their research has shown that when the firm dividend increased then the

investors react to that information favorably and when the dividends decrease it’s vice versa.

They concluded their research, dividend announcement do have information content in the

Indian stock exchanged and it do influence the share price. Another research conducted by

Thanatawee (2011) found the same results, they support the free cash flow and life cycle

hypothesis.

Looking into a recent study, Mollah (2011) have conducted research in order to investigate

the behaviour of pay out policy in the Dhaka stock exchange in Bangladesh. He concluded

stating “dividends do convey information to the market; therefore, more uncertainty is

supposed to lead to fewer dividend payments and vice versa. These results indicate that

managers do convey right information to the market. The DSE listed firms follow stable

dividend pay out policy; so, they have a little scope of dividend adjustment; therefore,

16

dividend contains information but less significant and consequently dividend becomes less

informative to signal the profitablity. These results narrowly support information content

hypothesis of Miller and Modigliani (1961)”. But on the other hand, his result has produced a

clear cut evidence that agency cost transection do have influcene on the dividend pay out

policy.

Khan, Aamir, Qayyum, Nasir & Khan (2011) have conducted research in Pakisthan stock

exchange employ a sample size of 55 from a period of 2001 - 2010. They have found that

stockholders do expect or wants dividend because it provides signal about the future prospect

of the organization. In the concluding remarks they stated that “dividend policy is important

as it provides signal about the success of the company.” Therefore their result is consistent

with Arnott & Asness (2003) states that “anecdotal tales about managers signaling their

earnings expectation through dividend.”

Looking into most recent literature Padmavathy & Ashok (2012) documented that on the

annoucement of merger does not hold any significant share price movement (meaning no

investors were able to gain abnormal return during the event period) in the Indian stock

exchange. Hence in the concluding remarks they stated on the annoceuemnt of merger does

not hold any signficant information for the investors in the indian stock exchnaged.

1.8.3 European Market

When I look into European market regarding on this topic I found mixed result. A research

conducted by Capstaff, Kteboe, & Marshall (2004) documented that in Oslo stock exchnage

they found strong evidence of dividend signaling hypothesis. Skinner & Soltes (2009)

concluded that the idea of dividend provide information about the quality of reported

earnings, and also found that the relation between present earning and future earnings was

stronger for firms that pay dividends than for those that do not. Another research conducted

17

by Bouwman (2010) documented that dividend changes do generate abnormal price

reactions, and yet too little information do provide about the future earnings of the firm.

Yilmaz & Selcuk (2010) have examined the market reaction to dividend changed

annoucement in the Istabul Stock Exchange. They have used a sample of 184 annoucement

made be 46 companies during a period of 2005 to 2008. They found that market react

positively for dividend increase and market react nagetively for dividend decreased and no

abnormal return earned by no change in dividend. Therefore their results are consistent with

dividend signaling hypothesis theory. It has also been revealed that before the annocement of

dividend decrease, there was information leakage.

Liargovas & Repousis (2011) have examined the Althene stock exchanged in Greek on the

annoucement of merger and acquisition. They documented that investor was able to gain

significant cumulative average abnormal return (CAAR) ten day prior to the announcement

of merger and acquisition, it indicate the leakage of information and they reject that Althene

stock exchanged follow semi strong form of market efficiency.

Looking into some recent studies Scheufele, Haas, & Brosius (2011) try to investigate how

the media influence on stock price in Germany. They found that media report is one of the

important source which influence the stock price especially for small investors. While

concluding their research report they states that “we found strong correlations between media

coverage about listed German companies and the development of stock prices and trading

volumes”. Charitou, Lambertides, & Theodoulou (2011) found that the dividend initiation or

raise are linked with lessen in the default risk afar other systematic risk. Another research

conducted by Schanz & Haesner (2011) concluded that Germany stock market response to

positive dividend surprises was more pronounced under the full imputation system, where

18

dividends are normally more favourable to the shareholders from a tax outlook, than under

the half income system.

Apolinario, Santana, Sales, & Caro (2011) have conducted a research on day of the week

effect on european stock markets from july 1997 to march 2004. In their observation they

have taken data from major european stock market namely germany, Austria, Belgium,

Denmark, Spain, France, Netherland, Italy, Portuagal, United Kingdom, Czech Republic,

Sweden and Switzerland. The have concluded their research stating that most of the european

markets do not follow a day of the week effect because the result of each single day does not

differ significantly fro the other days of the week. Another research conducted by Oduncu

(2012) found that day of the week effect was not present in the Turkish Derivatives

Exchange.

1.8.4 America and African Market

While reviewing American and African market, I found varied result. Nikkinen, Sahlström,

Takko, & Äijö, (2009) documented in the US market anomalies do occur due to the

annocuement or release of news during around turn of the month. Another research by

Okpara (2010) studied the relationship between asymmetric information and dividend policy

in Nigeria. He doucmented that there is significant correlation between dividend policy and

asymmetric information, and his finding was consistent with dividend signaling hypothesis.

Robbani & Bhuyan (2010) have studied the Canadian Stock Exchange. In the conclusion they

stated that “financial market reacts negatively to any restatement of earnings. This is evident

from the fact that irrespective of the reasons for restatement, all restatements show a

negative effect on the stock price. The impact of the restatement announcements is significant

for all the prediction intervals.”

19

Aduda & Kimathi (2011) in their research paper have examined the applicability of constant

dividend model which are in Nairobi Stock Exchange. The sample size of the research is 18,

and they have conducted their research in 2002 to 2008. Their empirical researched revealed

that constant growth model was not applicable to Nairobi Stock Exchanged. In the

concluding remarks they states that “firms that increase dividends had a significant decrease

in systematic risk while firms which reduced dividends incurred a significant increase in

risk”.

Agyei & Yiadom (2011) have investigated the correlation between bank performance and

dividend payout policy in Ghana. They docuemented three things, first they found wasaround

24.65% bank do pay dividend, second banks who pay dividend perform better compare to

bank who don’t pay dividend and finally bank pay dividend in order to reduce the agency

cost problem.

Abdalla (2012) found that day of the week effect was not present in the Khartoum Stock

Exchange (KSE) in Sudan.

Looking into the most recent study, Farooq, Saoud and Agnaou (2012) have conducted

research in Casablanka Stock Exchange, in Morocco regarding the dividend policy as a

signaling mechanism under different market condition. They have concluded that stating “we

find a significantly negative relatioship between dividend payout ratio and stock price

volatility during the stable growth period. We also show a significantly positive relationship

between dividend payout ratio and stock returns during the same period. However, this

relationship turns insignificant during the high growth period. One of the reasons for our

results may be that investors pay lesser attention to the signaling value of dividends during

the periods when they are earning higher returns on their investments.” This result is

consistent with Salminen (2008) where he concluded his thesis stating that “the abnormal

20

returns of dividend increases were clearly positively larger during the recession than the

boom. This is in line with the view that investors respect dividend increase more during

recession than a boom.” Therefore it means that stockholder do expect a dividend during bad

economic condition (recession) and they don’t expect dividend when the economy in good

condition (boom), during boom investors wantmore captial gain.

Another research by Ramadan (2012) studied that the validity of Arbitrage Pricing Theory

(APT) in in Amman Stock Exchange (ASE),they found that enough evidence to support the

validity of APT in ASE.

1.8.5 Malaysian Stock Exchange Market Specific

While reviewing Malaysian context, I found mixed result, some are in support of dividend

signaling hypothesis and some oppose. The academics who are in support include such as

Ling, Mutalip, Shahrin, & Othman (2008), Jais, Karim, Funaoka & Abidin (2009), Mohamed,

et al., (2010), Hussin, Ahmed & Ying (2010), Isa & Lee (2011), and Ismail & Rahman

(2012).

Ling, Mutalip, Shahrin, & Othman (2008) have examined the dividend policy of 100

Malaysian public listed companies in the bourse. They found that there are more dividend

paying firm than non dividend paying firm over the period of 2002 to 2005, unswerving with

Fama & French (2001). They conclude their research stating that “we find that dividend

payment has a positive correlation with the past earnings, little or no correlation with

current earnings, and is negatively correlated with future eanings. The finding suggest that

dividend policy for Malaysian public listed companies is influenced by their past

performance more than their current and future performances. The dividend policy for

Malaysian public listed companies is rigid and sticky as managers are reluctant to cut or

avoid omit dividend even when the performance of the companies are deteriorating.”

21

Jais, Karim, Funaoka & Abidin (2009) have examined the Malaysian stock exchange

dividend announcements reaction. They have used a sample size of 853 dividend increase

announcements and 376 dividend decrease announcements from 2001 to 2005. They have

found that dividend increase announcements signal as good news and dividend decrease

announcements greeted as bad news. They also found that stockholder do not react more

when there is small change or increase in the dividend compare to the previous year.

However the post announcement return shows that stockholders treat increase dividend

announcement as good news and they positively react to those announcements. Looking into

the other side, dividend decrease announcement they found that across all the investors in the

immediate event window surrounding the announcement was negative. But the result is not

statistically significant. Therefore no investors are able to gain abnormal return in the 3 day

event period. One possible reason for that is due to investors expect that happen because in

Malaysia all the company need to publish their accounts in quarterly hence investors analyze

those data on regular basis.

Mohamed, et al., (2010) have conducted an empirical study in Malaysian Stock Exchange,

regarding the determinants of dividend payment: profitability and liqudity. In their study they

have employ 200 companies in the Bursa Malaysia with highest market capitalization. They

found that Malaysian organization paid out on average 40 percent of their earnings as

dividends. It means that on average, about a quarter of their operating cash flow was used to

payout dividend for their shareholdres. They also revealed that Earnig Per Share (EPS),

Return on Equity (ROE) and Cash Flow Per Share (CFPS) are significants of dividend

determinant of Malaysian companies. In their concluding remarks they states that “this study

confirms the fact that profitability and liquidity are two important determinants of

dividends.”

22

Hussin, Ahmed & Ying (2010), in their study they have used sample size of 120 companies

listed the Bursa Malaysia for a period from 1 January to 30 November 2006. They found that

the capital market reaction to dividend announcement strongly support the information

content dividend hypothesis. In their result it is revealed that the higher dividend

announcements, on an average, earned positive abnormal return; lower dividend

announcement resulted in negative abnormal return. They concluded that “Malaysian stock

exchange has not yet reached its full efficiency level in semi strong form, as the time required

for the market to absorb the information conveyed by the dividend and earnings

announcements is extensively long. The cumulative abnormal returns still exhibit clear

upward or downward trends within two weeks (10 trading days) after the announcements

day, indicating a long delayed response to newly released public information.”

Muhammed & Rahman (2010) have conducted a research on day of the week effect in

Malaysian stock exchange from January 1999 to December 2006. They found that in

Malaysian stock exchange the day of the week effect was present. Another research by Isa &

Lee (2011) have observed the impact of acquisition annoucement to the acquirer’s form in the

Bursa Malaysia. They establish that acquiring firm do acquire significant abnormal return

during the annoucement period (-1 to +1).

A very recent study done by Ismail & Rahman (2012), have used 76 listed companies in the

Malaysian stock exchange. In their study they examine by publishing the quarterly financial

report does it have any effect on the share price? They employed event study methodology in

their research and they have developed three hypothesis. In the first hypothesis they found

that the announcements of quarterly report have no significant positive relationship with the

share price in the Malaysian stock exchange. In the second hypothesis they examine the

relationship between the level disclosure of quarterly financial report and firm share price and

found that no significant relationship. In the third hypothesis they examine the relationship

23

between the changes in quarterly earnings and firm share price and reveal that the changes in

quarterly earnings have significant positive relationship with share price. Therefore it is clear

that always the investors look into the earning capacity of the firm.

However the results of Abdullah, Rashid, & Ibrahim (2002) conducted emprical research on

the effect of dividend annoucements on the stock returns for the companies in the malaysian

stock exchange. They have included 120 observation from the year 1996 to 1999. They found

that decreasing dividend annoucment leads to positive abnormal return trend. The

annoucement period day t-60 to t+60, t-30 to t+30, t-0 to t+1 and t+1 to t+60 the CAAR

values are 15.79%, 8.49%, 1.42% and 9.59% respectively. These result indicate that by

decreasing dividend annoucements are associated with positive abnormal return and all the t-

values are statistically significant. Hence, dividend annoucement does not send bad news to

the bourse. Therefore these results are inconsistent with dividend signalling theory

(information content hypothesis) proposed by Bhattacharya (1979/1980), John and Williams

(1985), and Miller and Rock (1985).

1.9 Agency Cost

In the world of corporate finance agency cost is one of the important area which the

researchers have highlighted, how can agency cost can be reduced. According to Peavler

(2012) agency cost mean shareholders and corporate excutive (managers) are not necessarily

in agreement on the measure best suited to the business operation and that there is a cost

involved in such agreement. This is know as the agency problem.

Easterbrook (1984) is one of the pioneering scholar who first talk about the agency problem.

According to him when the firm decelare dividend help to reduce the agency cost problem

because declaring dividend leads to reduction in the free cash flow with the managers.

Therefore if the managers want to raise more fund then they have to go the capital market. He

24

argue that if there are more free cash flows with the manager he may invest a project which

may not be in the interest of the shareholders or he may not invest in the most profitable

project. Easterbrook states that sometime the risk – averse manager may opt a project that are

safe but perhaps the lesser expected return than a riskier venture, but the shareholders

(owners) may have contrarypenchant.

Al-Jafari & Altaee (2011) have conducted a research on whether the prices in Egypt

emerging equity market follow a random walk hypothesis. They have used a sample size of

3189 observation from January 1998 to December 2010. In their empirical researched they

have employs unit root test, run test and variance root test. In their conclusion they stated that

“the Egyptian stock market did not follow a random walk and informational inefficient at the

weak form level. Therefore, prudent investors will realize abnormal returns by using

historical sequences of stock prices, data related to trading volumes and other market

generated information.”

1.10 Efficient Market Hypothesis

In an efficient market it is impractical to beat the market and gain abnormal return, for the

reason that in efficient market it is always assumed that stocks are traded at its fair value. The

pioneering study done on Efficient Market Hypothesis (EMH) was Fama, Fisher, Jensen, &

Roll 1969, have examined (NYSE, January 1927 – December 1959) the stock price

adjustment towards the annoucement of stock split. They have documented that stock price

adjust very rapidly to the annoucement of stock split, and it indicate that NYSE is efficient in

its semi strong form. In their concluding remarks they state that “the stock market is

‘efficient’ in the sense that stock prices adjust very rapidly to the new information.” Another

significant fact found in their seminal study was split cannot be used to increase expected

abnormal profit perhaps seems to be bit anomalous.

25

Efficient Market Hypothesis (EMH) was propounded by Fama (1970) in his seminal paper

titled Efficient Capital Markets: A Review of Theory and Empirical Work. In an efficent

market all the security prices are fully reflected to all the available information and no one

will be able to earn excess profit using this information. Fama (1970) states that “a market in

which prices at any time ‘fully reflect’ available information is called ‘efficient’.” In his

paper he categorize EMH into three form efficiency namely Weak form, Semi – Strong form

and Strong form. Figure 2.3 depict those three form of efficiencies. In the weak form of

market efficiency if the current price is fully reflected by past or historical data, therefore no

investors should be able to earn abnormal return using company historical data. In his paper

he states that “weak form tests, in which the information set is just historical prices, are

discussed.” In semi – strong form the stock price should be reflected by all publically

available information, consequently no investors should be able to gain abnormal return using

public inforamtion (annoucement of dividend, merger, stock split or bonus). In his paper he

states that “semi – strong form tests, in which the concern is whether prices efficently adjust

to other information that is obviously publicaly available are considered.” Finally last form

of market efficiency was strong form, which is tremendously sporadic case. In strong form it

is asssumed that all stock price are fully reflected to all the information public as well as

insider information.

Sewell (2011) in his critic article on EMH, he have reviewed more than 163 article and found

that 50% reviewed are in support of EMH. In the conclusion he documenented that EMH is

false, but in spirit it is overwhelmingly true. He advocate that no real market in the factual

world will ever be efficient, signifying that EMH is virtually unquestionably made-up.

26

1.11 Conclusion

I would like to conclude this literature chapter a quote from Black (1976) “the harder we

look at the dividend picture, the more it seems like a puzzle, with pieces that don’t fit

together.” Hence, I believe there is always room or gap in this filed i.e, dividend signaling

hypothesis to be researched on.

27

CHAPTER 3

METHODOLOGY

1.12 Research Design

In figure 3.1 show the research framwork of this project paper. In the first phase through

literature review I have highlighted the main theories that was developed by previous

researchers on this topic. The famous theories that was developed include dividend signaling

hypothesis (relevent or irrelevent), information content hypothesis, agency cost, information

assymmetry, Efficient Market Hypothsis (EMH) and finally days of the week effect. In the

second phase hypothesis was developed based on theories in order to test market efficiency

and dividend signalling, after that data was collected and it was analysed and finally the

results was checked whether it support the exisiting theories or not.

28

1.13 Population and Sample

In this research the target population is the listed companies which are operating in Bursa

Malaysia Stock Exchange. There are more than 1000 companies listed in that burse. In this

paper, I have intergrated random sample technique, in total 77 companies dividend

annoucement data was collected, of which 45 companies are with dividend increase and the

the remaining 32 companies are with dividend decrease compare to the previous year. The

annoucement date (of dividend) is define as the very first day of the official statement made

by the board of directors of the sample companies. The data was collected from 2010 to 2012

in the calander year. The raw data was collected from http://biz.thestar.com.my/, and this data

was cross checked from their annual finacial statement for their validity.

1.14 Data Collection Procedures

In this project paper, I have employed the classic event study methodolgy and Run test for

checking the type of market efficiency exist in Malaysian Stock Exchange. Event study

observe the behaviour of the firm stock price during the communal dividend annoucement.

Any news that may effect the market value of the firm can be considered as an event. An

event has three parts namely pre announcement period (estimation window), event period

(event window) and lastly post event period (post event window). Figure 3.2 shows the time

line of event study given by MacKinlay (1997). It has been observed that the event period can

be extended more than one day, different researchers have taken different event window

period according to their requirement.

29

The corerationale of an event study methodolgy review the extent to which stock price

performance around the time of an event is abnormal or not, therefore the extent in which

stock returns are dissimilar from those known by the model determining equilibrium return.

Event studies has been used in various field of researches namley for earning annoucement,

debt or equity issues, merger and acquisitions, lawsuits, investment decision, impact of the

value of the firm when there is change in the regulatory environment (MacKinlay, 1997).

In this research I am going to use 21 day event windowincluding the annoucement day that is

(-10 to +10), in order to capture whether there is abnormal return or not. Previous researcher

who have used 21 day event window namley include Capstaff, Kteboe, & Marshall (2004),

Mandal & Rao (2010), and Hussin, Ahmed, & Ying (2010). On the other hand for the

calculation of adjusted mean, I have taken 100 days as the estimation period (-130 to -30). In

general in the finance literature 100 days to 250 days has been taken as estimation period. But

Michaely, Thaler, & Womack (1995) have used -254, +1 and -1, +758 days, conversely I

don’t distinguish any use of taking such an elongated event period for this study, and I

presume that within 21 days period if there is any abnormal return then it can be captured. By

means of event window, I can test the hypothesis draw conclusion in the anon in this chapter.

Event study methodogy is a statistical method, in order to review the effect of the security

market on annoucement of an event. Therefore in order to review the event study I have to

measure the abnormal return for each day.

In this research I have used mean adjusted model to estimated abnormal returns of the

securities, the main reason behind the use of this model in my project, due to its simplicities

and easiness of calculation. Brown & Warner (1985) found that mean adjusted model is more

sophisticated model than the other model. Chander, Sharma, & Mehta (2007) acknowledged

that Average Abnormal Return (AAR) under the mean adjusted model seemed to be cogently

more unswerving around the dividend announcement.

30

For each company, calendar time of the announcement is converted to event time by defining

the date of announcement as t=0. For announcement on stock exchange holiday in Malaysia

includes Friday and Saturday, I have used the next available trading as the event day, t=0. In

the mean adjusted model, where it assumes the expected returns are equal across all stocks at

a point of time t, but not necessarily constant for a stock at different times. In this study I

have used 130 days prior to the announcement, of which -130 to -30 (total 100 days) was

used to calculate the adjusted mean for the event window. Timeline I have used is shown in

figure 3.3. The speculative period -29 to 0 days data was not used in calculating the adjusted

mean in order to minimize the error. The actual return on each security on a particular day is

calculated using mean adjusted model.

1.14.1 Daily Return Measure ( )

There are abundant ways in calculating the the return for the security including the log return.

But here in this project report for the purpose of ease I have used an extremely trouble-free

arithametic ratio. The raw return at day t for firm i can be methametically symbolized as

follows:

31

(

)

Where indicate the return for firm i security on a t day, denotes the daily closing

security i on day t and symbolize the return for firm i security on a t day, denotes the

daily closing security i on previous day.

1.14.2 Adjusted Mean Measures

Adjusted mean is calculatd by averaging the raw return of stock i in given period of time

here in this study it was -130 to -30 days. The adusted mean of a firm can be methametically

symbolized as follows:

∑

Where denote adjusted mean for the data and = +1 equals the number of time

periods used to calculate the average return. For the use of this project paper = 100 days

where ( +1 is used.

1.14.3 Abnormal Return

After the calculation of daily return ( ) and Adjusted mean [ ] then I have to

calcualte abnormal return under the event study methodology. Abnormal return is the

excess return over the expected return on a security. The Abnormal return at day t for

firm i can be methametically symbolized as follows:

Where is the abnormal return on security i on day t, ( ) is the daily return on on

security i on day t and is the expected return on security i on the day t.

32

1.14.4 Average Abnormal Return (AAR)

After calculating, daily abnormal return then averaged across the firms in the choosen

samples using the following formula. for the definite cluster of companies are

examined in order to determine if the event produeces any return that perhaps cannot be

expained by the Capital Asset Pricing Model (CAPM).

∑

Where N is the total number of observation, here in this research N is 45 & 32 for dividend

increase& decrease firm respectively.

1.14.5 Average Abnormal Return (CAAR)

The usual way to study performance over longer interval is by means of Cumulative Average

Abnormal Return (CAAR), where the Average Abnormal Returns (AAR) are aggregated

from the start of the event period, t₁, up to time t . The CAAR at day t for firm i stock can be

methametically symbolized as follows:

∑

₁

1.14.6 Standard Deviation (σ)

Standard deviation give an idea about the dispersion that subsist from the average mean of

the data, a low standard deviation specify that the data points are close to the mean where as

high standard deviation signify data are spread over a hefty range of values. The σ at day t for

firm i security can be methametically symbolized as follows:

√

∑

33

1.14.7 Standard Error

The standard error compute the precision whether the sample represents the population. The

standard error at day t for firm i security can be methametically symbolized as follows:

σ

√

Where N is the total number of observation, here in this research N is 45 & 32 for dividend

increase & decrease firm respectively.

1.14.8 T-Test ( )

In order to find out the statistical significance of the AAR I have employ a parametric test

which is t-test. The t-test make use of the cross sectional standard deviation of abnormal

returns. T-Values are calculated by means of the following formula.

σ

Where t - statistics values for checking the significant level. is the Average

Abnormal Return on security i on the day t. σ on security i on the day t.

1.14.9 Run Test

Another name for the run test is Geary test, it is a non parametric test in which we try to

calculate the number of positive and negative hits and compare against its sampling

distribution under the random walk hypothesis. A run is defined as repeated occurance of the

same value. In this research the first run is marked as ‘0’ and the second run is marketd as

‘1’. A stock price runs can be positive, negative or no changes. The expected return and

standard deviation in the run test is calcuated using the following formula:

34

1.14.9.1 Expected Return

1.14.9.2 Standard Deviation

√

Where is the number of observation is number of first run cycle and is number of

second run cycle.

1.14.9.3 Z – test

Where R is the number of run in the market. & are expected return and standard

deviation respectively.

1.15 Framework for Data Analysis

Objectives 1. Find out whether there is an opportunity

in the Bursa Malaysia for arbitrages

2. Which form of market efficiency exist in

the Bursa Malaysia Stock Exchange

Research Question 1. What kind of market efficiency exist in

Malaysian stock exchange (Bursa

Malaysia) namely weak form, semi –

strong form or strong form?

2. What is the impact of dividend

35

announcement on stock price, is there any

opportunity for arbitrage in Malaysian

stock exchange (Bursa Malaysia)?

Hypothesis For dividend increase / initiation Firms

Abnormal Return

₁

Cumulative Average Abnormal Return

₁

For dividend decrease / omission

Abnormal Return

₁

Cumulative Average Abnormal Return

₁

ANOVA Single Factor

₁

₁ ₁

Run Test

₁

36

Source of Data

http://thestar.com.my/ and Annual Financial

Statement of Listed Companies.

Type of Data Secondary Data

Technique of Analysis 1. Event study methodology

2. Quantitative Analysis.

3. Descriptive statistics

1.16 Methodological Issues

Though there are advantages of using event study methodology and its wide spread usage in

the world stock market trade it do have some shortcoming. Since I have used mean adjusted

model in this research it has been very difficult in ascertaining the estimation period. Another

vital point to be documented is during the estimation period of means there perhaps interim

dividend announcements or other event which may impact on stock price, which may impact

on the results of this research by McWilliams & Siegel (1997) highlighted some of the issues

in event study in particulary the field of management research included that unaticipated

event, confounding effects, samples size, non parametric test to identify outliers, length of

event window and explanation of abnormal return are issues to be address in order to get

competent event studies.

37

CHAPTER 4

DATA ANALYSIS AND RESULTS

Stock market reactions on the announcement of event dividend (increase / decrease) are

captured by its Average Abnormal Return (AAR) values and Cumulative Average Abnormal

Return (CAAR) surrounding the event announcement day. The main intention of doing this

research is to find the answer the research questions which were developed in chapter 1, in

order to do that I have developed some hypothesis in chapter 1.

1.17 Dividend Increase 45 Firms

H₀: there is statistically zero significant abnormal return (positive or negative) due to

dividend increase / initiation. Therefore the Bursa Malaysia Stock Market is semi – strong

efficient with respect to the dividend increase / initiation.

H₁: there is statistically significant abnormal return (positive or negative) due to dividend

increase / initiation.

₁

Table 4.1 depict 45 dividend increased firm AAR, CAAR and T – Values (AAR), on each

event window (-10, +10) correspondingly. From table 4.1 it is found that 62% of the firms

have positive AAR and 38% have negative AAR during post event and pre-event period. The

firm who have increased their dividend compare to previous year found that on the day of

announcement of dividend, day 0 AAR is negative i.e., -0.19%, but in the following day, but

on the immediate event day+1 AAR is positive i.e., +1.25 (t – value +3.6048) and it is

significant at 1%. Figure 4.1 shows pre – announcement period negative curve, but after the

38

announcement of dividend day +1 it instantly increased and market has been adjusted after

day +3. This market rejoinder implied that increase in dividends release positive information

about the organization or the firm. In overall this results indicate significant market reaction

on the announcement data to positive dividend change. This result is consistent with dividend

signaling hypothesis theory. Therefore I do accept the null hypothesis .

Table 4.1

Stock Market Reaction to Average Abnormal Return (AAR), Cumulative Average

Abnormal Return (CAAR), T – Values for Dividend Increase Announcement of 45

Firms.

Event Window AAR CAAR T – Values (AAR)

-10 +0.07% +0.07% +0.1951

-9 +0.04% +0.11% +0.1003

-8 +0.23% +0.34% +0.9133

-7 +0.02% +0.36% +0.0463

-6 -0.57% -0.21% -1.5421*

-5 -0.16% -0.37% -0.4914

-4 +0.06% -0.31% +0.2006

-3 +0.07% -0.24% +0.1569

-2 -0.15% -0.39% -0.6655

-1 -0.04% -0.43% -0.1899

0 -0.19% -0.62% -0.6793

+1 +1.25% +0.63% +3.6048***

+2 +0.08% +0.71% +0.3008

+3 +0.86% +1.57% +2.2106**

+4 +0.04% +1.61% +0.1455

+5 +0.23% +1.84% +0.7299

+6 -0.39% +1.45% -1.4334*

+7 +0.35% +1.80% +1.1799

+8 -0.01% +1.79% -0.0471

+9 -0.15% +1.64% -0.5272

+10 +0.08% +1.72% +0.1874

* Significant at 10%, ** Significant at 5% and *** Significant at 1%

39

As we know that the exact occurrence of information content involves uncertainties, therefore

it is very much indispensable to test the cumulative effects of AAR. Hence under here am

going to test the significance of CAAR.

Cumulative Average Abnormal Return

H₀: there is statistically zero significant cumulative average abnormal return (positive or

negative) due to dividend increase / initiation. Therefore the Bursa Malaysia Stock Market is

semi – strong efficient with respect to the dividend increase / initiation.

H₁: there is statistically significant cumulative average abnormal return (positive or negative)

due to dividend increase / initiation.

₁

Figure 4.2 represents Cumulative Average Abnormal Return (CAAR), it reveals that 67% of

the firms have positive CAAR and 33% have negative CAAR during post event and pre-

event period. Figure 4.2 demonstrate CAAR for the firm who have increased their dividend

compare to previous year, found that in the day of announcement of dividend, day 0 CAAR is

negative i.e., -0.62%, but in the following day, day +1 CAAR is positive i.e., +0.63. The

40

announcement effect was spread to, day 2 as well as day 3, CAAR values are +0.71% and

+1.57% respectively, but after that market has been adjusted. In overall this results indicate

significant market reaction on the announcement data to positive dividend change. Therefore

I do accept the null hypothesis .

1.18 For dividend Decrease 32 Firms

Abnormal Return

H₁: there is statistically zero significant abnormal return (positive or negative) due to

dividend decrease / omission. Therefore the Bursa Malaysia Stock Market is semi – strong

efficient with respect to the dividend decrease / omission.

₁