imagine - new york university

TRANSCRIPT

the possibilities

2001

Financial Report

and 10k

the possibilities

imagine

financials

Securities and Exchange CommissionWashington, D.C. 20549

FORM 10-K

ANNUAL REPORT EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2001 Commission file number 1-3507

ROHM AND HAAS COMPANY(Exact name of registrant as specified in its charter)

DELAWARE 23-1028370(State or other jurisdiction of (I.R.S. Employer Identification No.)

incorporation or organization)

100 INDEPENDENCE MALL WEST, PHILADELPHIA, PA 19106(Address of principal executive offices) (Zip Code)

Registrant's telephone number, including area code: 215-592-3000

Securities registered pursuant to Section 12(b) of the Act:

Name of Each Exchange onTitle of Each Class Which Registered

Common Stock of $2.50 par value New York Stock Exchange

Securities registered pursuant to Section 12(g) of the Act:

NONE

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of theSecurities Exchange Act of 1934 during the preceding 12 months, and (2) has been subject to such filing requirements forthe past 90 days.Yes X No .

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein,and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporatedby reference in Part III of this Form 10-K or any amendment to this Form 10-K.

Aggregate market value of voting stock held by nonaffiliates of the registrant as of February 28, 2002: $4,313,328,027

Common stock outstanding at February 28, 2002: 220,677,633 shares.

Documents incorporated by reference:

Part III- Definitive Proxy Statement to be filed with the Securities and Exchange Commission, except the Report onExecutive Compensation, Graph titled “Cumulative Total Return to Shareholders” and Audit Committee Report includedtherein.

3

Rohm and Haas Company -

Net Sales by Business (in millions)

Pro Forma2001(1) 2000( 1) 1999 (1,2)

Coatings $ 1,445 $ 1,494 $ 1,512Adhesives and Sealants 661 707 737Plastics Additives 398 441 490Monomers 357 382 305Surface Finishes 309 373 507Performance Polymers $ 3,170 $ 3,397 $ 3,551

Consumer and Industrial Specialties $ 388 $ 406 $ 374Inorganic and Specialty Solutions 203 236 248Ion Exchange Resins 214 224 211Chemical Specialties $ 805 $ 866 $ 833

Shipley Ronal $ 470 $ 699 $ 621Microelectronics 472 511 246Electronic Materials $ 942 $ 1,210 $ 867

Salt $ 749 $ 876 $ 930

Total Net Sales $ 5,666 $ 6,349 $ 6,181

(1) Restated to conform to current year presentation and exclude the discontinued oper-ations of the Agricultural Chemicals business.

(2) Pro forma results include Morton International, Inc. (Morton), a specialty chemicals pro-ducer (acquired in June 1999) and LeaRonal, Inc. (LeaRonal), an electronic materialsbusiness (acquired in January 1999) as if these acquisitions had occurred on January 1,1999. The results are restated to conform to the current year presentation and exclude thediscontinued operations of the Agricultural Chemicals business. Pro forma information isnot presented for other acquisitions and divestitures occurring in 2001, 2000 and 1999because they were not material to the Company's results of operations or consolidatedfinancial position.

PART I

Item 1. Business

Rohm and Haas

Company

Rohm and Haas Company (theCompany), is a global specialty mate-rials company that reported 2001 netsales of approximately $5.7 billion.The Company is a public corporationwhose shares are traded on the NewYork Stock Exchange under the‘‘ROH’’ symbol and was incorporatedin 1917 under the laws of the State ofDelaware. The Company’s head-quarters office is located at 100Independence Mall West,Philadelphia, Pennsylvania 19106-2399 (phone number (215) 592-3000; internet addresswww.rohmhaas.com).

In 2001, the Company operated fourglobal businesses:

Performance Polymers (56 percent of2001 sales): This segment includesthe sales and operating results forCoatings, Adhesives and Sealants,Plastics Additives, Monomers andSurface Finishes.

Chemical Specialties (14 percent of2001 sales): This segment includesthe sales and operating results forConsumer and Industrial Specialties,Inorganic and Specialty Solutionsand Ion Exchange Resins.

Electronic Materials (17 percent of2001 sales): This segment includesthe sales and operating results forShipley Ronal (including PrintedWiring Board and Electronic andIndustrial Finishes) and Micro-electronics (including Shipley Micro-electronics and Rodel).

Salt (13 percent of 2001 sales): This seg-ment includes the sales and operat-ing results for the most recognizedconsumer salt brands in NorthAmerica (Morton Salt and Windsor

Salt), along with sales derived fromother end-use markets, includingwater conditioning, highway ice con-trol, food processing, chemical/industrial and agriculture.

Rohm and Haas is a geographicallydiverse company, with approximately100 manufacturing and technicallocations in 25 countries. In 2001,53% of net sales were made outsideof the United States. The Company’stechnology can be found in a widerange of end-use markets, includingbuilding and construction, electron-ic and computing devices, food, foodprocessing and packaging, architec-tural and industrial coatings, watertreatment, pharmaceutical, homecleaning and personal care.

Strategy

Rohm and Haas brings technologyand innovation to the market thatenhances the performance of the

end-use consumer products made byits customers and by leveraging itsbroad technology base on a globalbasis within markets where it enjoysleading positions.

The Company is committed to:

• continually bring innovation to themarketplace; even through the2000-2001 economic downturn,the Company maintained its levelof investment in research anddevelopment.

• continually improve the efficiencyof its cost structure, and repositionthe Company geographically toenhance the ability of its customersto serve their market needs.

• achieve, enhance and defend lead-ing market positions; this meansholding the first or second posi-tion in each of the markets or mar-ket segments in which theCompany competes.

financials

4

Summary of Business Segments

Business 2001 Sales Markets Products/ End UsesTechnology

Performance $3,170 millionPolymers:

Coatings $1,445 million Bldg. and Construction A range of House paintsHome Improvement intermediate Traffic paints(do-it-yourself products and Metal coatingsand contractor additives for Coated paperssegments) paints and coatings, Printing inksPackaging textiles, non-woven Non-woven fibersGraphic Arts and leather applications Textile finishesApparel an array of versatile InsulationHome/Office Goods emulsion polymers and LeatherTransportation other technologies

Adhesives $ 661 million Packaging A full-range of Pressure-sensitiveand Sealants Bldg and Construction adhesives and tapes and labels

Transportation laminate materials Packaging tapesHome Improvement (acrylic, urethane, Car interiors

polyester/urethane Weather strippingemulsion polymers) Engine mounts

Flexible packagingGraphic artsCaulks, cementsRoof coatingsSealants

Plastics $ 398 million Bldg. and Construction A wide range of PVC pipeAdditives Home/Office Goods additives that impart Plastic packaging

Transportation desired properties Vinyl sidingRecreation into the end plastic, Wall systemsPackaging or help machinery Vinyl windows

run more efficiently Fencing and decks(acrylic-based Interior automotive modifiers, tin based partsstabilizers, lubricants Appliances andand additives) business machines

Monomers $ 357 million Bldg. and Construction Produces essential AdhesivesPersonal Care starting materials Paints and coatingsAutomotive for acrylic products Floor polishesPackaging and specialty Hair sprays

monomers Super-absorbentproducts

5

Business 2001 Sales Markets Products/ End UsesTechnology

Surface $ 309 millionFinishes

Automotive $ 98 million Transportation Water, solvent and Cars Coatings urethane-based Trucks

exterior and interiorcoatings for plasticparts

Powder $ 211 million Home/Office Goods Epoxy, polyester Cars, shelving, Coatings Recreation, Lawn and and acrylic powder tables and chairs,

Garden Coatings office furniture,Transportation Lamineer, a low cabinetry andBldg. and Construction temperature curing machineryElectronics and coating

Comms. Devices

Chemical $ 805 millionSpecialties:

Consumer and $ 388 million Household Products Antimicrobial, Laundry andIndustrial Personal Care dispersant, and dishwasher Specialties Industrial Processing a range of other detergents

Bldg. and Construction technologies Shampoos, lotionsconditioners andhair sprays

Inorganic $ 203 million Industrial Processing Sulfur-based Corrosionand Specialty Lubricants and Fuels intermediates inhibitorsSolutions and salt-forming Pharmaceutical

bases productsSodium borohydride Papers and and related recycled newsprinttechnologies

Ion $ 214 million Food and Food-related Anion and cation Soft drinks andExchange Electronics and ion exchange resins juicesResins Comms. Devices and adsorbents Ultrapure water

Pharmaceutical CatalysisHome/Office Goods PharmaceuticalsIndustrial Processing

financials

6

Business 2001 Sales Markets Products/ End UsesTechnology

Electronic $ 942 millionMaterials:

Shipley $ 470 million Electronics and Enabling technology Cellular phonesRonal Comms. Devices for all aspects of the PCs

Transportation manufacture of Mainframe Home/Office Goods printed wiring computersRecreation boards; processes Automotive parts

critical to electronic Office equipmentcomponents, advanced Electronic gamespackaging and industrial Steel and metalfinishing markets finishing

Micro- $ 472 million Electronics and Essential technology PCselectronics Comms. Devices for creating state- Cellular phone and

Home/Office Goods of-the-art integrated other comms. Transportation circuits: devicesRecreation photoresists, Home appliances

anti-reflective Office equipmentcoatings, Electronic gameschemical mechanical Cars, trucks, etc.planarization (CMP)

Salt $ 749 million Food and Food Salt in all forms Table saltrelated produced through Cooking saltTransportation vacuum pan Home waterIndustrial Processing production, conditioning saltHome/Office Goods solar evaporation, or Highway salt

mined rock salt Chemical processingsalt

Salt blocks for feed

7

In addition to the summary of busi-ness segments, additional informa-tion appears in Item 7,“Management’s Discussion andAnalysis of Financial Condition andResults of Operations,” and theinformation indicated below appearsin the 2001 “Notes to ConsolidatedFinancial Statements” and is incorpo-rated herein by reference:

Notes toConsolidated

Financial Statements

Industry segment Footnote 9information for years 1999-2001

Foreign operations Footnote 9for years 1999-2001

Raw Materials

The Company uses a variety of com-modity chemicals as raw materials inits operations. In most cases, theseraw materials are purchased frommultiple sources under long-termsupply contracts, created to provideaccess to key raw materials. For theCompany’s Performance Polymersand Chemical Specialties segments,many of these materials are hydro-carbon derivatives such as propylene,acetone and styrene.

Competition and

Seasonality

The Company experiences vigorouscompetition in each of its segmentsand its competitors include manylarge multinational chemical firmsbased in Europe, Asia and the UnitedStates. In some cases, the Companycompetes against firms which areproducers of commodity chemicalswhich the Company must purchaseas the raw materials to make its prod-ucts. The Company however, doesnot believe this places it at any signif-icant competitive disadvantage. TheCompany's products compete withproducts offered by other manufac-turers on the basis of product qualityand specifications, customer serviceand price. Most of the Company'sproducts are specialty chemicalswhich are sold to customers whodemand a high level of customerservice and technical expertise fromthe Company and its sales force. TheSalt segment is most affected byweather-driven sales of highway icecontrol salt in the Eastern UnitedStates and Eastern Canada. To amuch lesser extent, sales in theCoatings segment destined for thepaint market are affected by weatherin various regions.

Research and

Development

The Company maintains its principalresearch and development laborato-ries at Spring House, Pennsylvania.Research and development expensestotaled $230 million, $224 millionand $174 million in 2001, 2000 and1999, respectively. The Companybelieves that its many intellectualproperties are of substantial value inthe manufacturing, marketing andapplication of its various products.Though the Company is not depend-ent, to a material extent, upon anyone trademark, patent or license,certain of the Company’s businessesmay be so dependent.

Environmental

A discussion of environmental relat-ed factors is incorporated herein byreference to Footnote 25:“Contingent Liabilities, Guaranteesand Commitments” in the accompa-nying “Notes to ConsolidatedFinancial Statements.”

Item 2. Properties

The Company, its subsidiaries andaffiliates presently operate morethan 100 manufacturing facilities,mines and salt evaporation facilitiesin 25 countries. The facilities andthe segment for which they are pro-ductive are detailed below:

financials

8

Manufacturing Locations

Argentina: Zarate(1) United States:

Australia: Geelong(1) Arizona: Glendale(4), Phoenix(3)

Bahamas: Inagua(4) California: Hayward(1), La Mirada(1), LongBeach(4), Newark(4), Sunnyvale(3)

Brazil: Jacarei(1,2) Delaware: Newark(3)

Canada: Iles-De-La-Madeleine(4); Lindbergh(4); Ojibway(4); Pugwash(4); Regina/Belle Plaine(4); West Hill(1,2); Windsor(4) Florida: Cape Canaveral(4)

China: Beijing(1); Dongguan(3); Illinois: Chicago Heights(1),Hong Kong(3); Elk Grove(1), Kankakee(1),Shanghi(1); Songjiang(2) Lansing(1), Ringwood(1)

Colombia: Barranquilla(1,2) Indiana: Warsaw(1)

France: Chauny(2); Lauterbourg(1,2); Semoy(1); Villers-Saint-Paul(2) Kansas: Hutchinson(4)

Germany: Bremen(1); Marl(1); Strullendorf(1) Kentucky: Louisville(1)

Indonesia: Cilegon(1,2) Louisiana: Weeks Island(4)

Italy: Castronno(2,3); Garlasco(1); Mozzanica(1); Mozzate(1); Parona(1); Robecchetto(1); Massachusetts: Marlborough(3), Romano d’Ezzelino(1) North Andover(2,3)

Japan: Kodama(3); Kurosaki(3); Mie(3); Nagoya(1); Nara(3); Ogaki(3); Osaka(3); Sasagami(3); Soma(1); Tokyo(2) Michigan: Manistee(2,4)

Mexico: Apizaco(1,2); Toluca(1) Mississippi: Moss Point(3)

Netherlands: Amersfoort(1,2); Delfijl(2) New Jersey: Perth Amboy(4)

New Zealand: Auckland(1,2) New York: Freeport(2,3), Silver Springs(4)

Philippines: Las Pinas(1,2) North Carolina: Charlotte(1)

Singapore: Singapore(1,3) Ohio: Cincinnati(4), Painesville(4),Rittman(4), West Alexandria(1)

South Africa: New Germany(1) Pennsylvania: Bristol(1), Croydon(1), Philadelphia(2), Reading(1)

Spain: Tudela(1) South Carolina: Greenville(1), Spartanburg(3)

Sweden: Landskrona(1) Tennessee: Knoxville(1)

Switzerland: Buchs(2); Lucerne(3) Texas: Bayport(1), Deer Park(1,2), Grand Saline(4)

Taiwan: Chiayi Hsien(3); Ta Yuan(1,2); Taoyuan Hsien(3) Utah: Grantsville(4)

Thailand: Maptaphut(1,2) Virginia: Wytheville(1)

United Buxton(3); Coventry(3); Kingdom: Dewsbury(1,2); Grangemouth(1);

Jarrow(2); Warrington(2,3)

9

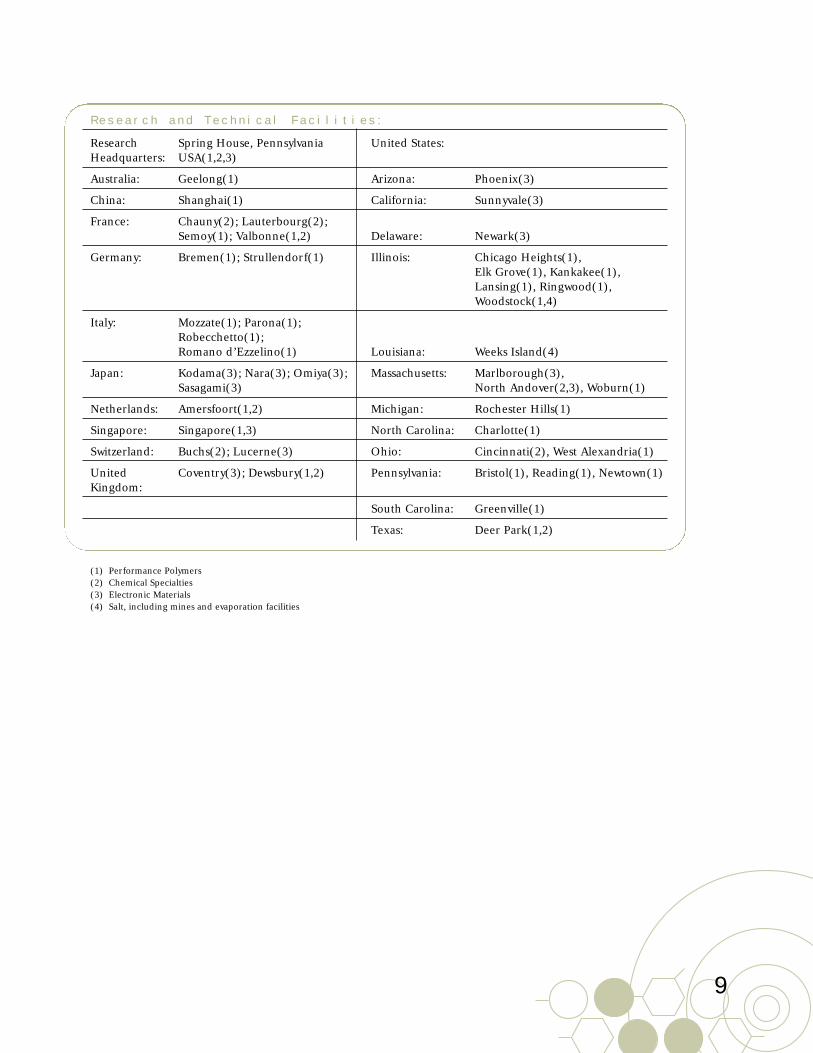

Research and Technical Facilities:

Research Spring House, Pennsylvania United States:Headquarters: USA(1,2,3)

Australia: Geelong(1) Arizona: Phoenix(3)

China: Shanghai(1) California: Sunnyvale(3)

France: Chauny(2); Lauterbourg(2); Semoy(1); Valbonne(1,2) Delaware: Newark(3)

Germany: Bremen(1); Strullendorf(1) Illinois: Chicago Heights(1), Elk Grove(1), Kankakee(1), Lansing(1), Ringwood(1),Woodstock(1,4)

Italy: Mozzate(1); Parona(1); Robecchetto(1);Romano d’Ezzelino(1) Louisiana: Weeks Island(4)

Japan: Kodama(3); Nara(3); Omiya(3); Massachusetts: Marlborough(3), Sasagami(3) North Andover(2,3), Woburn(1)

Netherlands: Amersfoort(1,2) Michigan: Rochester Hills(1)

Singapore: Singapore(1,3) North Carolina: Charlotte(1)

Switzerland: Buchs(2); Lucerne(3) Ohio: Cincinnati(2), West Alexandria(1)

United Coventry(3); Dewsbury(1,2) Pennsylvania: Bristol(1), Reading(1), Newtown(1)Kingdom:

South Carolina: Greenville(1)

Texas: Deer Park(1,2)

(1) Performance Polymers (2) Chemical Specialties (3) Electronic Materials (4) Salt, including mines and evaporation facilities

10

CashPeriod High Low Dividends

20011st Quarter $ 38.7000 $ 29.7700 $ 0.202nd Quarter $ 37.2300 $ 30.0900 $ 0.203rd Quarter $ 36.7800 $ 24.9000 $ 0.204th Quarter $ 37.3000 $ 30.8000 $ 0.20

20001st Quarter $ 47.6250 $ 33.0000 $ 0.192nd Quarter $ 49.4375 $ 32.8750 $ 0.193rd Quarter $ 37.5000 $ 25.6875 $ 0.204th Quarter $ 37.3125 $ 24.3750 $ 0.20

The Company’s manufacturing oper-ations ran well throughout 2001.The plants recorded good operatingefficiencies and cost control, espe-cially considering the decline indemand due to slower globaleconomies. Safety was a key focus, aswell, and significant improvementwas made during the year. The over-all corporate safety record improvedfrom a rate of 2.3 injuries for every200,000 hours worked in 2000, to 1.7injuries on a comparable basis for2001. Sixty-three sites operatedinjury-free throughout the year.

As part of the Company’s compre-hensive 2001 repositioning efforts,Rohm and Haas closed manufactur-ing facilities in Tustin and Orange,California; Moss Point, Mississippiand Paterson, New Jersey. TheCompany announced plans to makefurther reductions in manufacturingcapacity in several businesses in 2002.Continual improvements in design,operation, and process control havesignificantly improved the efficiencyof the Company’s remaining manu-facturing capacity. The Companybelieves it has the ability to generatesignificant additional productioncapacity using its existing manufac-turing operations.

Item 3. Legal

Proceedings

A discussion of legal proceedings isincorporated herein by reference toFootnote 25: “Contingent Liabilities,Guarantees and Commitments” inthe accompanying “Notes toConsolidated Financial Statements.”

Item 4. Submission

of Matters to a

Vote of Security

Holders

There were no matters submitted toa vote of security holders during thefourth quarter of 2001.

PART II

Item 5. Market for

the Registrant's

Common Equity and

Related Stockholder

Matters

The Company's common stock of $2.50par value is traded on the New YorkStock Exchange (Symbol: ROH).There were 9,234 registered commonstockholders as of December 31, 2001.On February 28, 2002, the last sale priceof the Company’s common stock was$38.41. The following table sets forth,for the period indicated, the high andlow sales prices and cash dividends ofthe Company’s common stock.

financials

11

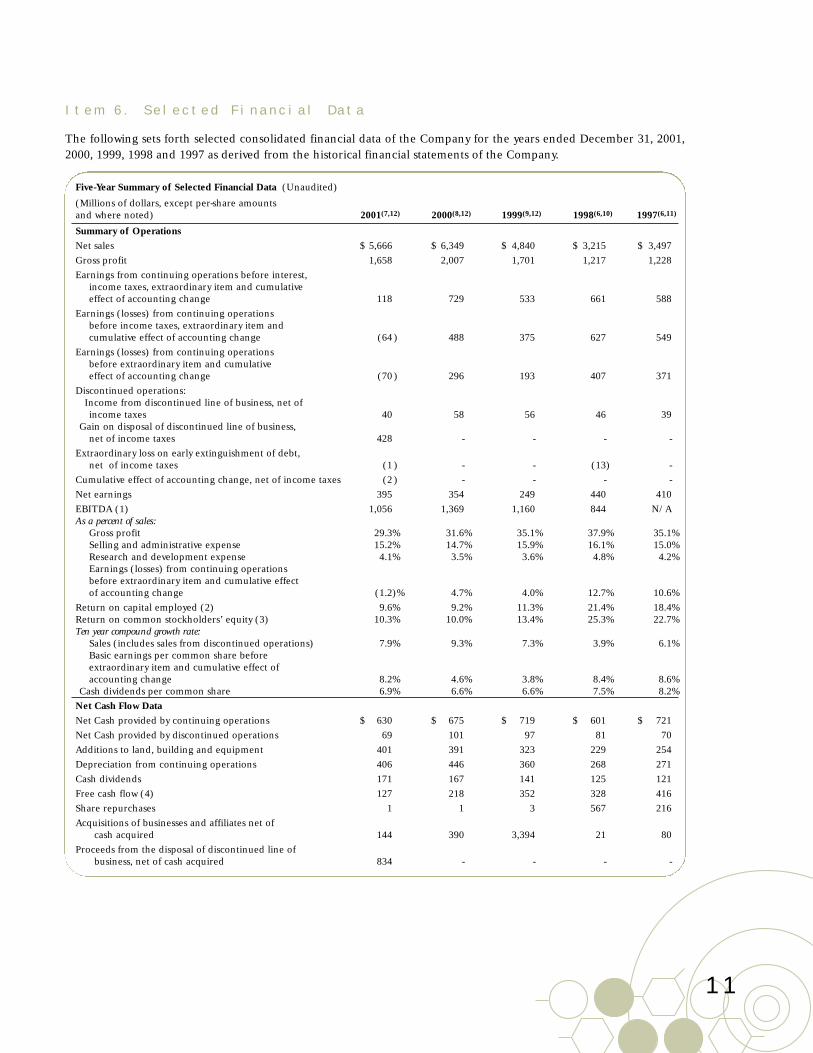

Item 6. Selected Financial Data

The following sets forth selected consolidated financial data of the Company for the years ended December 31, 2001,2000, 1999, 1998 and 1997 as derived from the historical financial statements of the Company.

Five-Year Summary of Selected Financial Data (Unaudited)

(Millions of dollars, except per-share amounts and where noted) 2001(7,12) 2000(8,12) 1999(9,12) 1998(6,10) 1997(6,11)

Summary of OperationsNet sales $ 5,666 $ 6,349 $ 4,840 $ 3,215 $ 3,497Gross profit 1,658 2,007 1,701 1,217 1,228Earnings from continuing operations before interest,

income taxes, extraordinary item and cumulative effect of accounting change 118 729 533 661 588

Earnings (losses) from continuing operations before income taxes, extraordinary item and cumulative effect of accounting change (64 ) 488 375 627 549

Earnings (losses) from continuing operations before extraordinary item and cumulative effect of accounting change (70 ) 296 193 407 371

Discontinued operations:Income from discontinued line of business, net of income taxes 40 58 56 46 39

Gain on disposal of discontinued line of business, net of income taxes 428 - - - -

Extraordinary loss on early extinguishment of debt, net of income taxes (1 ) - - (13) -

Cumulative effect of accounting change, net of income taxes (2 ) - - - -Net earnings 395 354 249 440 410EBITDA (1) 1,056 1,369 1,160 844 N/A As a percent of sales:

Gross profit 29.3% 31.6% 35.1% 37.9% 35.1%Selling and administrative expense 15.2% 14.7% 15.9% 16.1% 15.0%Research and development expense 4.1% 3.5% 3.6% 4.8% 4.2%Earnings (losses) from continuing operations before extraordinary item and cumulative effect of accounting change (1.2)% 4.7% 4.0% 12.7% 10.6%

Return on capital employed (2) 9.6% 9.2% 11.3% 21.4% 18.4%Return on common stockholders’ equity (3) 10.3% 10.0% 13.4% 25.3% 22.7%Ten year compound growth rate:

Sales (includes sales from discontinued operations) 7.9% 9.3% 7.3% 3.9% 6.1%Basic earnings per common share before extraordinary item and cumulative effect of accounting change 8.2% 4.6% 3.8% 8.4% 8.6%

Cash dividends per common share 6.9% 6.6% 6.6% 7.5% 8.2%Net Cash Flow DataNet Cash provided by continuing operations $ 630 $ 675 $ 719 $ 601 $ 721Net Cash provided by discontinued operations 69 101 97 81 70Additions to land, building and equipment 401 391 323 229 254Depreciation from continuing operations 406 446 360 268 271Cash dividends 171 167 141 125 121Free cash flow (4) 127 218 352 328 416Share repurchases 1 1 3 567 216Acquisitions of businesses and affiliates net of

cash acquired 144 390 3,394 21 80Proceeds from the disposal of discontinued line of

business, net of cash acquired 834 - - - -

financials

12

Five-Year Summary of Selected Financial Data (Unaudited) (continued)

(Millions of dollars, except per-share amounts and where noted) 2001(7,12) 2000(8,12) 1999(9,12) 1998(6,10) 1997(6,11)

Per Common Share Data and Other Share Information Earnings (losses) from continuing operations before

extraordinary items and cumulative effect of accounting changes:Basic $ (0.31) $ 1.34 $ .99 $ 2.29 $ 1.96Diluted $ (0.31) $ 1.34 $ .98 $ 2.26 $ 1.93

Cash dividends per common share $ .80 $ .78 $ .74 $ .70 $ .63Common stock price

High $ 38.7000 $ 49.4375 $ 49.2500 $ 38.8750 $ 33.7500Low $ 24.9000 $ 24.3750 $ 28.1250 $ 26.0000 $ 23.5625Year-end close $ 34.6300 $ 36.3125 $ 40.6875 $ 30.1250 $ 31.9375

Number of shares repurchased, in thousands 33 18 70 17,459 7,653Average number of shares outstanding –

basic, in thousands 220,249 219,535 192,586 175,591 185,808Average number of shares outstanding –

diluted, in thousands 220,249 220,500 195,700 179,700 192,400

At Year-EndGross fixed assets $ 6,618 $ 6,699 $ 6,349 $ 4,471 $ 4,492Total assets 10,350 11,252 11,256 3,648 3,900Total debt 2,898 3,774 4,053 581 606Stockholders’ equity 3,815 3,653 3,475 1,561 1,797Debt ratio (5) 42% 49% 52% 25% 22%Number of registered common stockholders 9,234 9,226 9,462 4,451 4,352Number of employees 18,210 20,248 21,512 11,265 11,592

(1) Earnings before interest, taxes, depreciation and amortization. EBITDA excludes non-recurring items and is presented to assist security ana-lysts and others in evaluating the Company’s performance and its ability to generate cash. EBITDA should not be considered an alternativeto cash flow from operating activities as a measure of liquidity or as an alternative to net income as an indicator of the Company’s operatingperformance in accordance with generally accepted accounting principles. The Company’s definition of EBITDA may not be consistent withthat used by other companies. The Company did not calculate this measure prior to 1998.

(2) Net earnings plus after-tax amortization and interest expense divided by average total assets less cash and average non-interest bearing lia-bilities. Years 2000 and 1999 exclude the purchased in-process research and development (IPR&D) charges. Years 2001 and 1998 excludeextraordinary loss on early extinguishment of debt and year 2001 excludes the cumulative effect of accounting change.

(3) Excluding ESOP adjustment and cumulative effect of accounting changes. Years 2000 and 1999 exclude IPR&D charges.(4) Cash provided by operating activities including discontinued operations less dividends and additions to land, building and equipment. (5) Total debt, net of cash (net debt), divided by the sum of net debt, minority interest, stockholders’ equity and ESOP shares.(6) Reclassified to conform to current year presentation, primarily as a result of discontinued operations.

Notes 7-11 reflect all amounts net of income taxes (see table on page 16 for additional information related to 2001, 2000 and 1999 non-recurringitems):

(7) Included in 2001 results are net non-recurring charges in continuing operations of $259 million, gain on disposal of line of business of $428million and income from discontinued operations of $40 million, an extraordinary loss on early extinguishment of debt of $1 million and a$2 million charge for the cumulative effect of accounting change.

(8) Included in 2000 results are net non-recurring charges in continuing operations of $28 million and income from discontinued operationsof $58 million.

(9) Included in 1999 results are net non-recurring charges in continuing operations of $161 million and income from discontinued operationsof $56 million. Also included in 1999 are results from Morton, a specialty chemicals producer acquired in June 1999 and LeaRonal, an elec-tronic materials business acquired in January 1999.

(10) Included in 1998 results is net non-recurring income of $45 million, consisting of a gain in continuing operations from the sale of the Company’sinterest in the AtoHaas and RohMax joint ventures, a loss from the early extinguishment of debt, the write-off of certain intangible assets inEurope and business realignment costs primarily in Asia. Also included is income from discontinued operations of $46 million.

(11) Included in 1997 results is a net non-recurring gain in continuing operations of $16 million, the net result of remediation settlements withinsurance carriers and discontinued operations income of $39 million.

(12) See 2001, 2000 and 1999 results in “Management’s Discussion and Analysis of Financial Condition and results of Operations” for additionalinformation.

13

Item 7.Management's

Discussion and

Analysis of

Financial Condition

and Results of

Operations

The following commentary shouldbe read in conjunction with the con-solidated financial statements andnotes to financial statements for theyears ended December 31, 2001,2000 and 1999.

“Same business basis” as it relates tothe comparison of sales betweenreporting periods includes onlythose businesses, segments or divi-sions that have been in place duringthe entire reportable period.

Earnings (losses) from continuingoperations before extraordinary itemand cumulative effect of accountingchange are abbreviated as “Earnings(losses) from continuing operations”within the “Management’s Discussionand Analysis of Financial Conditionand Results of Operations” and “Notesto Consolidated Financial Statements.”

Significant ItemsAffecting 2001, 2000and 1999 Results ofOperations

In January 1999, the Companyacquired LeaRonal, an electronicmaterials business and in June of1999, Morton. Details of these trans-actions are discussed under“Liquidity, Capital Resources andOther Financial Data” below. Theresults of these significant acquisi-tions have been included in the con-solidated financial statements sincethe dates of acquisition. Unauditedpro forma information is presentedin the table on page 19.

The LeaRonal and Morton acquisi-tions, accounted for using the pur-chase method, significantly impactedthe comparability of 2000 and 1999results. Accordingly, 1999 pro forma

sales and earnings excluding non-recurring items are provided in theresults of operations discussions tofacilitate comparisons. The proforma results include Morton andLeaRonal as if these significant acqui-sitions had occurred on January 1,1999. Pro forma adjustments weremade primarily to reflect increasedgoodwill and intangible amortizationand interest expense. Cost savingsfrom integration efforts were notreflected. Though useful for compar-ison, pro forma results are not intend-ed to reflect actual earnings had theacquisitions occurred on the datesindicated and are not a projection offuture results or trends. Pro formainformation is not presented for otheracquisition and divestiture activitiesoccurring in 2001, 2000 and 1999because these were not material to theCompany's results of operations orconsolidated financial position.

Non-recurring Items

Non-recurring items represent gains orlosses arising from events or transac-tions that are unusual in nature, occurinfrequently or satisfy the definition ofan extraordinary item in accordancewith Accounting Principles Board(APB) 30 “Reporting the Results ofOperations - Reporting the Effects ofDisposal of a Segment of a Businessand Extraordinary, Unusual andInfrequently Occurring Events andTransactions.” Unless otherwise indi-cated, the impact of non-recurringitems on operations within the contextof the Management’s Discussion andAnalysis is stated net of tax.

Sale of the

Agricultural Chemicals

Business

Following the sale of its AgriculturalChemicals business (Ag) in June2001, the Company reported theoperating results as discontinuedoperations in accordance with APB

30 “Reporting the Results ofOperations - Reporting the Effects ofDisposal of a Segment of a Businessand Extraordinary, Unusual andInfrequently Occurring Events andTransactions.” AgriculturalChemicals had been a separate majorline of business in the ChemicalSpecialties segment. The operatingresults of Ag have been reported sep-arately as discontinued operations inprior years.

Critical Accounting

Policies

In response to the Securities andExchange Commission’s (SEC)Release No. 33-8040, “CautionaryAdvice Regarding Disclosure AboutCritical Accounting Policies,” theCompany has identified the criticalaccounting policies that are mostimportant to the portrayal of theCompany’s financial condition andresults of operations. The policies setforth below require management’smost subjective or complex judg-ments, often as a result of the need tomake estimates about the effect ofmatters that are inherently uncertain.

• Litigation and EnvironmentalReservesThe Company is involved in liti-gation in the ordinary course ofbusiness, including personalinjury, property damage andenvironmental litigation. TheCompany also expends signifi-cant funds for environmentalremediation of both company-owned and third-party locations.In accordance with GenerallyAccepted Accounting Principles(GAAP), specifically Statement ofFinancial Accounting Standards(SFAS) No.5, “Accounting forContingencies” and Statement ofPosition 96-1, “EnvironmentalRemediation Liabilities”, theCompany records a loss andestablishes a reserve for litigation

financials

14

or remediation when it is proba-ble that an asset has beenimpaired or a liability exists andthe amount of the liability can bereasonably estimated. Reason-able estimates involve judgmentsmade by management after con-sidering a broad range of infor-mation including: notifications,demands, or settlements whichhave been received from a regu-latory authority or private party,estimates performed by inde-pendent engineering companiesand outside counsel, availablefacts, existing and proposed tech-nology, the identification ofother potentially responsible par-ties and their ability to contributeand prior experience. Thesejudgments are reviewed quarterlyas more information is receivedand the amounts reserved areupdated as necessary. However,the reserves may materially differfrom ultimate actual liabilities ifthe loss contingency is difficult toestimate or if management’sjudgments turn out to be inaccu-rate. If management believes nobest estimate exists, the mini-mum loss is accrued in accor-dance with GAAP.

• RestructuringIn June 2001, the Companyrecorded a $330 million restruc-turing and asset impairmentcharge in connection with its2001 repositioning efforts, ofwhich $82 million representedrestructuring charges. The repo-sitioning effort consisted of 112separate initiatives affecting allbusiness groups across theCompany, and will take approxi-mately twelve months to com-plete from date of commence-ment. The $82 million ofrestructuring included $71 mil-lion of severance terminationbenefits for 1,860 employeesaffected by plant closings or

capacity reductions, as well as var-ious personnel in corporate,administrative and shared servicefunctions. Severance termina-tion benefits were based on vari-ous factors including length ofservice, contract provisions andsalary levels. Management esti-mated the restructuring chargebased on these factors as well asprojected final service dates.

Given the complexity of esti-mates and broad reaching scopeof the 2001 repositioning effort,actual expenses could differ frommanagement’s estimates. If actu-al results are different from orig-inal estimates, the Company willrecord additional expense orreverse previously recordedexpense through the “Provisionfor Restructuring and AssetImpairment” line in theStatement of ConsolidatedEarnings. As of December 31,2001, the Company recognized afavorable change to the originalestimate of $4 million, due inpart to changes in estimates forseverance expense and the recog-nition of settlement gains.Management will continue tomake adjustments if necessary asactions under the plan are car-ried out.

• Valuation of Long-Lived AssetsThe Company's long-lived assetsinclude property, plant, equip-ment, long-term investments,goodwill and other intangibleassets. Long-lived assets, otherthan investments, goodwill andindefinite-lived intangible assets,are depreciated over their esti-mated useful lives, and arereviewed for impairment whenev-er changes in circumstances indi-cate the carrying value may not berecoverable. In conjunction withthe Company’s 2001 reposition-ing efforts, $245 million in assetswere deemed impaired and writ-

ten-off based on estimated fairvalue assumptions. Fair values areestimated based upon forecastedcash flows discounted to presentvalue. If actual cash flows or dis-count rate estimates change, theCompany may have to recordadditional impairment chargesnot previously recognized.

The fair value of the long-terminvestments is dependant on theperformance of the Company’sinvestees, as well as volatility inher-ent in their external markets. Inassessing potential impairment forthese investments the Companywill consider these factors as wellas the forecasted financial per-formance of its investees. If theseforecasts are not met, theCompany may have to recordadditional impairment chargesnot previously recognized.

• Pension and Other EmployeeBenefitsCertain assumptions are used inthe calculation of the actuarial val-uation of the Company-sponsoreddefined benefit pension plans andpost-retirement benefits. Theseassumptions include the weightedaverage discount rate, rates ofincrease in compensation levels,expected long-term rates ofreturn on assets and increases ortrends in health care costs. Ifactual results are less favorablethan those projected by manage-ment, lower levels of pensioncredit or other additional expensemay be required. See Notes 10and 11 in the accompanying“Notes to Consolidated FinancialStatements” for additional infor-mation regarding assumptionsused by the Company.

• Inventory ReservesThe Company adjusts the valueof its obsolete and unmarketableinventory to the estimated mar-ket value based upon assump-

15

tions of future demand and mar-ket conditions. If actual marketconditions are less favorable thanthose projected by management,additional inventory write-downsmay be required.

• Gain on Sale of the AgriculturalChemicals BusinessIn June 2001, the Company com-pleted the sale of its AgriculturalChemicals business to DowAgroSciences LLC (DAS), a whol-ly-owned subsidiary of the DowChemical Company for approxi-mately $1 billion, subject to aworking capital adjustment. Theworking capital adjustment hasnot been finalized as of December31, 2001. The Company hasrecorded a receivable from DASfor the amount of the workingcapital adjustment based uponmanagement's best estimate ofthe ultimate adjustment. TheCompany's calculation of theworking capital adjustmentrequired estimates related to thevaluation of certain assets, princi-pally accounts receivable, invento-ry, and rebate liabilities trans-ferred to DAS on June 1, 2001. Ifthe final working capital adjust-ment differs from management'sestimate as of December 31, 2001,the Company will be required torecord an adjustment to the gainon disposal of discontinued lineof business initially recorded inthe second quarter of 2001.

Consolidated Results

of Operations for the

Year Ended December

31, 2001, as Compared

to the Year Ended

December 31, 2000

Net SalesConsolidated net sales in 2001 were$5,666 million, 11% below 2000 net

sales of $6,349 million. The decreasefrom the prior-year was driven by per-sistently weak global demand acrossall businesses. 2001 net sales com-pared to the prior-year declined 22%for Electronic Materials, which hasbeen buffeted by a precipitous indus-try-wide decline since April 2001, 7%for Performance Polymers on lowervolumes and 7% for ChemicalSpecialties due to persistent sluggish-ness in the paper and industrial mar-kets served by the businesses in thisgroup. Salt sales, on a same businessbasis, remained flat as both periodsbenefited from strong demand forhighway ice control products in the2000 winter season. In the fourthquarter of 2000, the Company sold itsEuropean Salt business.

Net EarningsNet earnings as reported for the year2001 were $395 million, a 12%increase from 2000 net earnings of$354 million. Earnings per share on adiluted basis were $1.79 in 2001, com-pared with $1.61 per share in 2000.The Company reported a loss fromcontinuing operations for the year2001 of $70 million or $0.31 per com-mon share, compared to income fromcontinuing operations of $296 millionor $1.34 per common share in 2000.Net income excluding non-recurringitems for the year 2001 was $189 mil-lion, or 42% less than 2000 earningsof $324 million. The year-over-yeardecline can be attributed to theimpact of poor external economicconditions on all business segments,particularly Electronic Materials andPerformance Polymers whichaccounted for $134 million, or 99%,of the total decline from 2000. TheCompany actively managed throughthe economic downturn to mitigatesignificantly reduced demand byannouncing and implementingrestructuring initiatives to bringcapacity more in line with market

demand. Expenditures continued tobe made on research and develop-ment, enterprise resource planning(ERP) initiatives and small acquisi-tions in Adhesives and Sealants.

In June 2001, the Company complet-ed the sale of Ag to Dow AgroSciencesLLC (DAS), a wholly owned sub-sidiary of the Dow ChemicalCompany, for approximately $1 bil-lion, subject to a working capitaladjustment not yet finalized atDecember 31, 2001. The Companyrecorded a gain on the sale in theamount of $679 million pre-tax ($428million or $1.94 per share after-tax).Income from discontinued opera-tions, prior to the June 2001 sale, was$40 million or $0.18 per share after-tax as compared to income from dis-continued operations in 2000 of $58million or $0.27 per common shareafter-tax.

The impact of non-recurring items onearnings from continuing operationsin 2001 was a charge of $259 millionand consisted primarily of $226 mil-lion of restructuring and asset impair-ment charges; $18 million of costsassociated with the repositioningefforts including plant shutdown anddismantlement costs; $10 million ofasset valuation adjustments in theElectronic Materials segment; and $5million of remediation-relatedcharges, net of insurance settlements.The impact of non-recurring chargeson earnings from continuing opera-tions in 2000 was $28 million, andconsisted of $14 million of purchasedin-process research and development(IPR&D) and other one-time chargesrelated to the Rodel acquisition and$14 million of costs associated withrestructuring and integration efforts.Refer to the following table for a rec-onciliation of reported earnings toearnings excluding non-recurringitems for all years presented.

financials

16

Table of Non-Recurring Items

(in millions) 2001 2000 1999

Net Earnings as-reported $ 395 $ 354 $ 249

Non-recurring gains (losses):IPR&D and other one-time charges related to acquisitions - (14) (115)Joint venture dispositions - - (14)Remediation related charges, net of insurance settlements (5) - 17Provision for restructuring and asset impairments (226) (8) (23)Asset write-downs, integration and other restructuring costs (28) (6) (26)

Impact on continuing operations (259) (28) (161)

Income from discontinued line of business 40 58 56Gain on disposal of discontinued line of business 428 - -

Discontinued operations 468 58 56

Extraordinary loss on early extinguishment of debt (1) - -Cumulative effect of accounting change (2) - -

Total non-recurring gains (losses) 206 30 (105)

Earnings excluding non-recurring items $ 189 $ 324 $ 354

Gross Profit Gross profit for 2001 was $1,658 mil-lion, a 17% decline from $2,007 mil-lion in 2000 and the gross profit mar-gin was 29%, down from 32% in2000. The change in gross profitmargin is primarily the result oflower manufacturing efficiency driv-en by reduced demand. TheCompany continues to respond bymaintaining price increases andimproving internal efficiencies.

Selling, Administrative and Research(SAR) ExpensesSAR expenses were $1,091 millionfor 2001, a 6% decrease from $1,157million in 2000, reflecting savingsfrom the Company’s repositioningefforts as well as a decrease inemployee related expenses. Thesecost reductions were offset byincreased research and developmentcosts reflecting the Company’s con-tinued focus on developing cuttingedge technologies and ERP informa-tion system expenditures. SARexpenses were 19% of net sales for2001, compared to 18% in 2000.

Purchased In-Process Research andDevelopment (IPR&D)IPR&D in acquisitions accounted forby the purchase method, represents

the value assigned to research anddevelopment projects of an acquiredcompany where technological feasi-bility had not yet been established atthe date of the acquisition, andwhich, if unsuccessful, have no alter-native future use. Amounts assignedto IPR&D are charged to expense atthe date of acquisition. Accordingly,the Company charged $13 million toexpense in 2000 in connection withthe Rodel acquisition. (See Note 4:“Purchased In-process Research andDevelopment” in the accompanying“Notes to Consolidated FinancialStatements”).

Interest Expense Interest expense for 2001 was $182million, a 24% decline from $241million in 2000, primarily due tolower debt levels and interest rates ascompared to the prior-year period.

Amortization of Goodwill and OtherIntangiblesAmortization of goodwill and otherintangibles for 2001 was $156 mil-lion, a 2% decline from $159 millionin 2000.

Share of Affiliate Net Earnings Share of affiliate net earnings in 2001was $12 million, a 33% decline fromearnings of $18 million in 2000, pri-

marily due to the increased owner-ship in Rodel and the sale of affiliatesrelated to the disposition of Ag (SeeNote 2: “Acquisitions andDispositions of Assets” in the accom-panying “Notes to ConsolidatedFinancial Statements”). Prior toMarch 31, 2000 the investment inRodel was accounted for under theequity method with the Company'sshare of earnings reported as equityin affiliates. Since the second quar-ter of 2000, Rodel’s results of opera-tions have been fully consolidated.

Provision for RestructuringProvision for restructuring of $320million pre-tax or $226 million after-tax for the year ended December 31,2001 is comprised primarily of assetimpairment and restructuringcharges relating to the Company’srepositioning initiatives that com-menced in June 2001. The Companyrecognized a $330 million one-timerestructuring and asset impairmentcharge in the second quarter of 2001,to enable several of its businesses torespond to structural changes in theglobal marketplace. The largest com-ponent related to the partial closureof certain manufacturing andresearch facilities across all businessgroups and included exit costs related

17

to the Liquid Polysulfide Sealantsbusiness in Performance Polymersand part of the dyes business inChemical Specialties. Approximately75% of the assets impaired were in theNorth American region. The one-time charge included severance bene-fits; the employees receiving sever-ance benefits will include those affect-ed by plant closings or capacity reduc-tions, as well as various personnel incorporate, administrative and sharedservice functions. Approximately1,860 positions will be affected by therestructuring efforts. Offsetting theoriginal charge of $330 millionrecorded in June 2001, is a pre-taxgain of $4 million from the recogni-tion of settlement gains and changesin estimates to restructuring liabilitiesestablished for the 2001 initiatives, aswell as a pre-tax gain of $6 millionfrom changes in estimates to restruc-turing liabilities established in 1999. Itis the Company’s policy to recognizesettlement gains at the time anemployee’s pension liability is settled.

In the first half of 2000, a restructur-ing reserve of $13 million pre-tax wasrecorded in the Ion Exchange Resinsbusiness for the write-down of plantassets and severance costs for approx-imately 100 people. These chargeswere net of certain pension settle-ment and curtailment gains.

Other Income Other income for 2001 was $15 mil-lion, a 67% decline from $46 millionin 2000. The decline is primarily dueto lower foreign currency gains com-pared to the prior year. In addition,the Company incurred a $4 millioncasualty loss resulting from a fire at ajoint venture manufacturing facility.

Effective Tax RateThe loss from continuing operationsof $70 million contains $6 million ofincome taxes, which computes to a9% effective tax rate. This reflects theimpact of a 29% tax rate on the $320million loss provision for restructur-

ing and asset impairment, whichincluded non-deductible restructur-ing expenses. Excluding the impactof this provision, the effective tax rateon continuing operations was 39%,the same as 2000. The effective taxrate for 2000, excluding non-taxdeductible IPR&D charges was 38%.

Consolidated Results

of Operations for the

Year Ended December

31, 2000, as Compared

to the Year Ended

December 31, 1999

Net SalesNet sales in 2000 were $6,349 mil-lion, a 3% increase from 1999 proforma net sales of $6,181 million anda 31% increase from 1999 actual netsales of $4,840 million. The increasefrom pro forma 1999 net sales wasdriven largely by an acquisition-driv-en sales increase in the ElectronicMaterials segment and to a lesserextent the acquisition of 95% ofAcima A.G. (Acima) in the ChemicalSpecialties segment. The effect ofthese acquisitions was partially offsetby unfavorable currency impacts.

Net EarningsNet earnings on an as-reported basisfor 2000 were $354 million, a 42%increase from 1999 net earnings of$249 million. Diluted earnings percommon share were $1.61 in 2000compared to $1.27 in 1999. Earningsfrom continuing operations for theyear 2000 were $296 million or $1.34per diluted common share, comparedto $193 million or $0.98 per dilutedcommon share in 1999. Net earningsexcluding non-recurring items for theyear 2000 were $324 million, a 2%decline from pro forma 1999 and an8% decline from actual 1999 net earn-ings excluding non-recurring items.Earnings per share excluding non-recurring items on a diluted basis was$1.47 in 2000, compared with $1.81per share in actual 1999.

The impact of the non-recurringcharges on continuing operations in2000 was $28 million, and consistedof $14 million of IPR&D and otherone-time charges related to theRodel acquisition, and $14 million ofcosts associated with the restructur-ing and integration efforts. Non-recurring items impacting continu-ing operations for 1999 includecharges of $161 million, including acharge of $115 million for IPR&Dand other one-time charges from theMorton acquisition, a charge of $23million for restructuring costs result-ing both from the integration ofMorton and the Company's redesignof its selling and administrative infra-structure, $26 million related to assetwrite-downs, integration and otherrestructuring costs, a gain of $17 mil-lion from remediation related insur-ance recoveries, and a $14 millionloss on disposition of the AtoHaasjoint venture.

The operating results of Ag havebeen reported separately as discon-tinued operations in prior years.Income from discontinued opera-tions in 2000 was $58 million or $0.27per share as compared to incomefrom discontinued operations in1999 of $56 million or $0.29 per com-mon share.

Gross ProfitGross profit for the year 2000 was$2,007 million, an 18% increase from$1,701 million in 1999; however, thegross profit margin was 32% in 2000,down from 35% from 1999. Thechange in gross profit margin wasprimarily the result of increasedhydrocarbon-based raw materialprices in addition to higher energycosts in the form of higher naturalgas prices and increased freight costsdue to higher fuel prices. Theimpact of increased raw materialprices was primarily in thePerformance Polymers business seg-ment. Overall raw material price

financials

18

increases were not offset by overallselling price increases. To a lesserextent, higher depreciation resultingfrom fair values being assigned toacquired assets also contributed tothe change in gross profit margin.

Selling, Administrative and Research(SAR) ExpensesSAR expenses for 2000 decreased to18% of net sales from 19% in 1999.In 1999, the Company began imple-menting a redesign of its selling andadministrative infrastructure andinstituted other cost saving measuresassociated with the integration of theMorton and LeaRonal acquisitions.The stated goal of these efforts was toreduce annual procurement, SARand other expenses by $300 million.By year-end 2000, the run rate goalwas achieved through cost reductionsin support services, procurementand manufacturing.

Purchased In-Process Research andDevelopment (IPR&D)IPR&D in acquisitions accounted forby the purchase method, representsthe value assigned to research anddevelopment projects of an acquiredcompany where technological feasi-bility had not yet been established atthe date of the acquisition, andwhich, if unsuccessful, have no alter-native future use. Amounts assignedto IPR&D were charged to expense at

the date of acquisition. Accordingly,the Company charged $13 millionand $105 million to expense in 2000and 1999, respectively, related to theRodel and Morton acquisitions (SeeNote 4: “Purchased In-processResearch and Development” in theaccompanying “Notes to Consoli-dated Financial Statements”).

Interest ExpenseInterest expense in 2000 was $241million, a 53% increase from $158million in 1999, due to higher debtlevels resulting from acquisitions. Inyear 2000 a full year of interest at thehigher debt levels is reflected versussix months in 1999.

Amortization of Goodwill and OtherIntangiblesAmortization in 2000 was $159 mil-lion, a 92% increase from $83 mil-lion in 1999. The increase was attrib-utable to significant 1999 acquisi-tions and year 2000 reflects amortiza-tion for a full year versus six monthsin 1999 related to these acquisitions.

Share of Affiliate Net EarningsEarnings of $18 million in 2000increased from earnings of $6 millionin 1999. The 2000 earnings resultedfrom a full year of affiliates acquiredin mid-1999 and from earnings of cer-tain affiliated businesses of Rodel.Since the second quarter of 2000,

Rodel’s results of operations havebeen fully consolidated. The 1999earnings resulted largely from Rodel,which was an affiliate during that year.

Other IncomeOther income for 2000 was $46 mil-lion, a $32 million increase from $14million in 1999. The increase islargely from foreign currency gainsresulting from risk managementactivities. The 1999 period includesMorton integration costs offset by again related to a favorable settlementwith insurance carriers over certainenvironmental remediation matters.

Effective Tax RateThe effective tax rate for 2000 and1999 was 39% and 49%, respectively.The effective tax rate for 1999 was49%, largely as a result of the non-deductible write-off of IPR&D.Excluding the non-tax deductibleIPR&D charges, the effective tax ratewas 38% for both years. Rates alsoreflect the effect of certain non-taxdeductible amortization chargesresulting from the Company's acqui-sition activities.

Summary by Business SegmentThe Company's operations areorganized by worldwide business seg-ments. Descriptions of theCompany’s business segments arelocated in Item 1. Business includedin the beginning of this report.

19

Net Sales from Continuing Operations by Business Segment and Region

Performance Chemical ElectronicPolymers Specialties Materials Salt Total

(Millions of dollars)

North America2001 $ 1,915 $ 340 $ 488 $ 749 $ 3,4922000 2,083 399 584 750 3,8161999 1,847 320 352 326 2,845

Europe2001 $ 865 $ 268 $ 167 $ - $ 1,3002000 923 266 213 126 1,5281999 780 211 168 113 1,272

Asia-Pacific2001 $ 235 $ 146 $ 287 $ - $ 6682000 242 145 413 - 8001999 197 122 235 - 554

Latin America2001 $ 155 $ 51 $ - $ - $ 2062000 149 56 - - 2051999 115 54 - - 169

Total2001 $ 3,170 $ 805 $ 942 $ 749 $ 5,6662000 3,397 866 1,210 876 6,3491999 2,939 707 755 439 4,840

Summary of 1999-2001 Results by Business Segment

ProActual Forma(2)

(Millions of dollars) 2001 2000(1) 1999(1) 1999(1)

Net SalesPerformance Polymers $ 3,170 $ 3,397 $ 2,939 $ 3,551Chemical Specialties 805 866 707 833Electronic Materials 942 1,210 755 867Salt 749 876 439 930

Total $ 5,666 $ 6,349 $ 4,840 $ 6,181

Earnings (Loss) from Continuing Operations Before Extraordinary Item and Cumulative Effect of Accounting Change

Performance Polymers $ 85 $ 282 $ 350 $ 388Chemical Specialties 7 55 59 86Electronic Materials 1 110 57 64Salt 13 24 10 35Corporate(3) (176) (175) (283) (241 )

Total $ (70) $ 296 $ 193 $ 332

(1) Reclassified to conform to current year presentation.(2) Pro forma results include Morton and LeaRonal as if these 1999 acquisitions had occurred on January 1, 1999. Pro forma net earnings

exclude non-recurring items.(3) Corporate includes non-operating items such as interest income and expense, corporate governance costs, and corporate exploratory

research. In 2000 and 1999, it included charges for purchased in-process research and development costs associated with the Rodel andMorton acquisitions. (See “Management’s Discussion and Analysis”)

financials

20

Performance Polymers

2001 versus 2000Performance Polymers sales for 2001were $3,170 million, a 7% declinefrom $3,397 million in 2000. Salesand earnings decreases were felt inall businesses primarily due to poorexternal economic conditions and asa result of the continued slow downin the building and constructionindustry which are served largely bythe Coatings, Adhesives and Sealantsand Plastic Additives businesses.Automotive and Powder Coatingssales decreased primarily due to weakdemand in the automotive andindustrial markets, as compared tothe prior-year. Earnings from contin-uing operations for 2001 were $85million, a 70% decline from $282million in 2000. Excluding non-recurring items, earnings were $229million, an 18% decline from 2000earnings of $278 million.

2000 versus 1999Performance Polymers sales for 2000were $3,397 million, a decrease of 4%from $3,551 million pro forma 1999sales and a 16% increase from actualsales of $2,939 million in 1999.Earnings from continuing operationsfor 2000 were $282 million, a 19%decline from $350 million in 1999.Excluding non-recurring items, earn-ings were $278 million in 2000, a 28%decrease from 1999 pro forma earn-ings of $388 million and a 21%decrease from $352 million in 1999.Sales and earnings in the year wereimpacted by an economic slowing inthe U.S. building and constructionmarkets in the second half of 2000.These markets are served largely bythe Coatings, Adhesives and Sealantsand Plastics Additives businesses.Similar slowing in the automotive mar-kets served by Surface Finishes wasalso a factor. Sales were also affectedby weaker European currencies. The21% decrease in earnings, excludingnon-recurring items, was a result of

these demand factors and by sharplyhigher hydrocarbon base raw materialcosts and energy costs, particularly nat-ural gas (see Gross Profit discussionunder “Summary of ConsolidatedResults” below). The Monomer busi-ness continued to report stronggrowth in the year as a result of theacquired Stockhausen merchantmonomer business in Europe. Amongthe Surface Finishes businesses, salesof Powder Coatings on a pro formabasis continued to improve, but wereoffset by weaker sales in AutomotiveCoatings driven by slowing in the U.S.automotive markets.

Chemical Specialties

2001 versus 2000Chemical Specialties reported salesof $805 million, a 7% decline from$866 million in 2000. Inorganic andSpecialty Solutions sales decreased by$33 million, representing 54% of thetotal year-over-year decline, as thebusiness continues to suffer frompersistently low demand for sodiumborohydride related applications inthe newsprint, pharmaceutical andelectronic markets. Consumer andIndustrial Specialties sales declined$18 million from 2000, representing30% of the total decline as a result ofdecreased demand in industrial mar-kets. Ion Exchange Resins salesdeclined due to a weakness in indus-trial water treatment and catalystmarkets. Earnings from continuingoperations for 2001 were $7 million,an 87% decline from $55 million in2000. Earnings for 2001, excludingnon-recurring items were $63 mil-lion, a 10% decline from $70 millionin 2000 as lower demand producedhigher manufacturing variances,which negatively impacted earnings.

2000 versus 1999Chemical Specialties sales for 2000were $866 million, a 4% increasefrom pro forma 1999 sales of $833million and a 22% increase from

actual sales of $707 million in 1999.Sales increases were driven byConsumer and Industrial Specialties,helped by the acquired Acima bio-cides business, with a contributionfrom Ion Exchange Resins. Earningsfrom continuing operations for 2000were $55 million, a 7% decline from$59 million in 1999. Net earnings,excluding non-recurring items, were$70 million in 2000, a 19% declinefrom pro forma 1999 earnings of $86million and a 3% decline from actualearnings of $72 million in 1999.

Electronic Materials

2001 versus 2000Electronic Materials sales were $942million, a 22% decline from $1,210million in 2000. The sales decline wasdriven by a significant decrease indemand across all businesses, with theexception of sophisticated technolo-gies including deep UV photoresists,chemical mechanical planarizationproducts and anti-reflective coatings.Earnings from continuing operationsfor 2001 were $1 million compared to$110 million in 2000, reflecting costsassociated with the Company’s reposi-tioning efforts. Excluding non-recur-ring items, earnings were $27 million,a 76% decline from $112 million in2000, because of significantlydecreased demand impacting manu-facturing efficiencies.

2000 versus 1999Electronic Materials sales for 2000were $1,210 million, a 40% increasefrom pro forma 1999 sales of $867million and a 60% increase fromactual sales of $755 million in 1999.Earnings from continuing operationsfor 2000 were $110 million, a 72%increase from pro forma 1999 of $64million and a 93% increase from $57million in 1999. Excluding non-recurring items, earnings were $112million in 2000, a 62% increase from$69 million in 1999. Increases insales and earnings were evident in all

21

regions and markets within theElectronic Materials segment due tocontinued demand for new tech-nologies and contributions fromRodel, which was consolidated in2000, and from Shipley Ronal, partof which was acquired in 1999.Results of operations for Rodel wereconsolidated during the secondquarter of 2000, as a result of increas-ing the Company's ownership toapproximately 90% from 48%.

Salt

2001 versus 2000Salt sales were $749 million for 2001,a 14% decline from $876 million in2000. Sales, on a same business basis,remained unchanged from the priorperiod. Earnings from continuingoperations for 2001 were $13 million,a 46% decline from $24 million in2000. The Company sold itsEuropean salt business in the fourthquarter of 2000 (see Note 2:“Acquisitions and Dispositions ofAssets” in the accompanying “Notesto Consolidated FinancialStatements”). Excluding non-recur-ring items, earnings remained con-stant at $24 million in 2001 and 2000.

2000 versus 1999Salt sales in 2000 were $876 million,a 6% decline from pro forma 1999sales of $930 million. Sales werecomparatively lower in 2000 in partdue to the absence of fourth quarterEuropean Salt sales following thedivestiture of that business. Earningsfrom continuing operations for 2000

were $24 million, a 31% decline frompro forma 1999 of $35 million and a$14 million increase from $10 mil-lion in 1999. Despite strong weatherrelated results in the fourth quarterof 2000, the change in sales and earn-ings was largely attributable to theimpact of a mild winter at the begin-ning of 2000 on sales of ice controlsalt in contrast with a more severewinter in early 1999. Excluding non-recurring items, earnings were $24million in 2000, a $15 millionincrease from $9 million in 1999.

Corporate

2001 versus 2000Corporate loss from continuing oper-ations in 2001 totaled $176 millioncompared to $175 million in 2000.The current period benefited frominterest cost savings as a result oflower debt levels and interest ratescompared to the prior-year.Offsetting the interest savings areadditional provisions for environmen-tal remediation (net of insurancerecoveries) and increased employeerelated expenses. Excluding non-recurring items, corporate lossesdecreased 4% to $154 million com-pared to $160 million in 2000.

2000 versus 1999Corporate loss from continuing oper-ations in 2000 totaled $175 million, a

38% decline from $283 million in1999. The years 2000 and 1999included charges of $13 million forRodel and $105 million for Morton,respectively, for IPR&D related tothese acquisitions. Excluding non-recurring items, corporate lossesincreased 8% to $160 million com-pared to $148 million in 1999.

Liquidity, Capital

Resources and Other

Financial Data

Cash and cash equivalents remainedunchanged at $92 million atDecember 31, 2001. Net cash in-flowsduring 2000 and 1999 resulted in netincreases in cash and cash equivalentsof $35 million and $41 million,respectively. Each of these yearsincluded acquisition, divestiture andfinancing activities having a signifi-cant effect on the Company's cashflows. (See Note 2: “Acquisitions andDispositions of Assets” in the accom-panying “Notes to ConsolidatedFinancial Statements”).

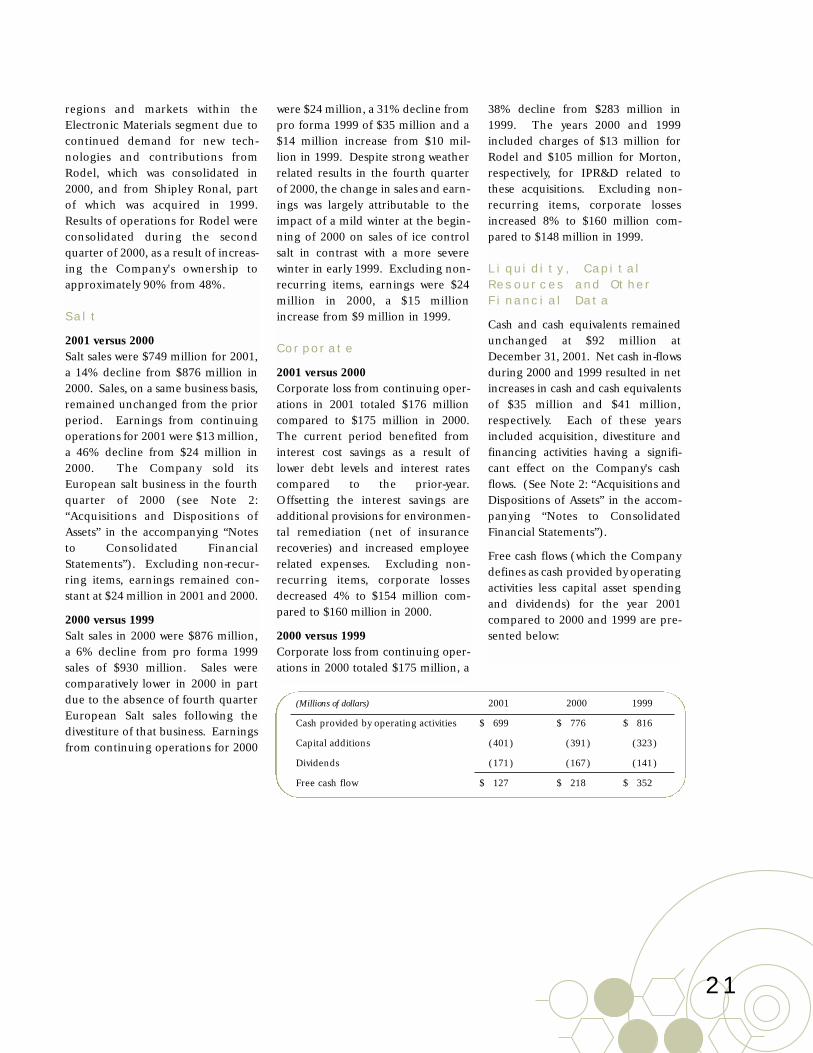

Free cash flows (which the Companydefines as cash provided by operatingactivities less capital asset spendingand dividends) for the year 2001compared to 2000 and 1999 are pre-sented below:

(Millions of dollars) 2001 2000 1999

Cash provided by operating activities $ 699 $ 776 $ 816

Capital additions (401) (391) (323)

Dividends (171) (167) (141)

Free cash flow $ 127 $ 218 $ 352

financials

22

The Company’s short-term, primarysource of liquidity will be cash flowfrom operations, supplemented asnecessary with commercial paperand or bank borrowings. At year end2001, the Company maintains anunused credit facility with a syndicat-ed group of banks of $900 million;$500 million of which is committeduntil 2004. The commitment of thisfacility is not contingent on theCompany’s credit rating. TheCompany does not believe there is amaterial risk to short-term liquidity.As of December 31, 2001, theCompany had no letters of credit ormaterial guarantees outstanding.

Financing Total borrowings at year-end 2001were $2,898 million, only 7% ofwhich is due prior to 2004. Total bor-rowings were $3,774 million at yearend 2000. At the end of 2001, thedebt ratio was 42% compared with49% at the end of 2000.

In 2000, the Company issued 400 mil-lion Euros (or $376 million) of 6.0%notes due 2007.

On February 27, 2002, the Companyissued 20 billion yen (or $149 mil-lion) of 3.5% notes, interest payablesemiannually on March 29th and

September 29th, beginning in March2002. The maturity date is March 29,2032, callable annually after March2012. Proceeds from the issuance ofthe note will be used for general cor-porate purposes.

The Company contemplates someearly retirement of debt via calls andrepurchases as opportunities arise inorder to gain the long-term benefitsof reduced interest expense. As aresult, some non-recurring losses willbe recorded during 2002.

Contractual Obligations

The following table provides the Company’s contractual obligations and commitments for future payments:

(Millions of dollars) Payments due by period

Less thanContractual obligations Total 1 year 1-3 years 4-5 years Over 5 years

Total borrowings/ capital lease obligations $ 2,898 $ 178 $ 516 $ 375 $ 1,829Operating leases 228 50 90 57 31

Total contractual cash obligations $ 3,126 $ 228 $ 606 $ 432 $ 1,860

Trading ActivitiesThe Company does not have anytrading activity that involves non-exchange traded contracts account-ed for at fair value.

Unconsolidated EntitiesThe Company has no controlling own-ership in significant entities which arenot consolidated. There are no signif-icant contractual requirements tofund losses of unconsolidated entities.Material contingent liabilities, guaran-tees and commitments not included inthe consolidated balance sheet are dis-closed in the accompanying “Notes toConsolidated Financial Statements”under Note 25: “Contingent Liabilities,Guarantees and Commitments.”

Environmental There is a risk of environmentalimpact in chemical manufacturingoperations. The Company's environ-mental policies and practices are

designed to ensure compliance withexisting laws and regulations and tominimize the possibility of significantenvironmental impact.

The laws and regulations underwhich the Company operates requiresignificant expenditures for capitalimprovements, the operation of envi-ronmental protection equipmentand remediation. Future develop-ments and even more stringent envi-ronmental regulations may requirethe Company to make additionalunforeseen environmental expendi-tures. The Company's major com-petitors are confronted by substan-tially similar environmental risks andregulations.

The Company is a party in variousgovernment enforcement and privateactions associated with former wastedisposal sites, many of which are on

the U.S. Environmental ProtectionAgency's (EPA) National Priority Listand has been named a potentiallyresponsible party at approximately140 inactive waste sites where remedi-ation costs have been or may beincurred under the Federal Com-prehensive Environmental Response,Compensation and Liability Act andsimilar state statutes. In some of thesecases the Company may also be heldresponsible for alleged property dam-age. The Company has provided forfuture costs at certain of these sites.The Company is also involved in cor-rective actions at some of its manufac-turing facilities.

23

The Company considers a broad rangeof information when determining theamount of its remediation accruals,including available facts about thewaste site, existing and proposed reme-diation technology and the range ofcosts of applying those technologies,prior experience, government propos-als for this or similar sites, the liabilityof other parties, the ability of otherprincipally responsible parties to paycosts apportioned to them and currentlaws and regulations. These accrualsare assessed quarterly and updated asadditional technical and legal informa-tion becomes available. However, atcertain sites, the Company is unable,due to a variety of factors, to assess andquantify the ultimate extent of itsresponsibility for study and remedia-tion costs. Major sites for whichreserves have been provided are thenon-company-owned Lipari, Wood-land and Kramer sites in New Jersey,Whitmoyer in Pennsylvania and com-pany-owned sites in Bristol andPhiladelphia, Pennsylvania andHouston, Texas. The Morton acquisi-tion introduced two major sites: MossPoint, Mississippi and Wood-Ridge,New Jersey.

In Wood-Ridge, New Jersey, Mortonand Velsicol Chemical Corporation("Velsicol") have been held jointlyand severally liable for the cost ofremediation necessary to correctmercury-related environmentalproblems associated with a mercuryprocessing plant on the site prior toits acquisition by Morton. At the dateof acquisition, Morton had disclosedand accrued for certain ongoingstudies, which are expected to becompleted during 2002, with regula-tory decisions expected by the end of2002. In its allocation of the pur-chase price of Morton, the Companyaccrued for additional study costs atDecember 31, 1999 and additionalremediation costs in 2000 based onthe progress of the technical studies.A separate study of probable contam-

ination in Berry's Creek, which runsnear the plant site, and of the sur-rounding wetlands is on a timetableyet to be determined. Therefore, theestimated costs of this separate studyand any resulting remediationrequirements have not been consid-ered in the allocation of the Mortonpurchase price. There is muchuncertainty as to what will berequired to address Berry’s Creek butcleanup costs could be very high andthe Company’s share of these costscould be material. The Company'sexposure will also depend upon thecontinued ability of Velsicol and itsindemnitor, Fruit of the Loom, Inc.,which has filed for protection underthe bankruptcy laws, to contribute tothe cost of remediation. In 2001,these parties have stopped payingtheir share of expenses. Ultimately,the Company’s exposure will alsodepend on the results of attempts toobtain contributions from othersbelieved to share responsibility. Acost recovery action against theseresponsible parties is pending in fed-eral court. This action has beenstayed pending future regulatorydevelopments and the appeal of asummary judgment ruling in favor ofone of the defendants. Settlementshave been reached with some defen-dants for claims considered de min-imis associated with the Wood-Ridgeplant site.

During 1996, the EPA notifiedMorton of possible irregularities inwater discharge monitoring reportsfiled by its Moss Point, Mississippiplant in early 1995. Morton investi-gated and identified other environ-mental issues at the plant. Though atthe date of acquisition Morton hadaccrued for some remediation andlegal costs, the Company revisedthese accruals as part of the alloca-tion of the purchase price of Mortonbased on its discussions with theauthorities and on the informationavailable as of June 30, 2000. In

2000, the Company reached agree-ment with the EPA, the Departmentof Justice and the State of Mississippi,resolving these historical environ-mental issues. The agreementreceived court approval in early2001. The final settlement includespayment of $20 million in civil penal-ties, which were paid in the first quar-ter of 2001, $2 million in criminalpenalties, which were paid in thefourth quarter of 2000 and $16 mil-lion in various SupplementalEnvironmental Projects. The accru-als established for this matter weresufficient to cover these and otherrelated costs of the settlement. InDecember 2001, the Company closedthe chemicals portion of the MossPoint facility.

The amount charged to earningsbefore-tax for environmental remedi-ation was $28 million and $4 millionfor the years ended December 31,2001 and 1999, respectively, and theamount charged in 2000 was immate-rial. The reserves for remediationwere $156 million and $185 million atDecember 31, 2001 and 2000, respec-tively, and are recorded as “other lia-bilities” (current and long-term). TheCompany is pursuing lawsuits overinsurance coverage for environmentalliabilities. It is the Company's practiceto reflect environmental insurancerecoveries in results of operations forthe quarter in which the litigation isresolved through settlement or otherappropriate legal processes.Resolutions typically resolve coveragefor both past and future environmen-tal spending. The Company settledwith several of its insurance carriersand recorded income before-tax ofapproximately $13 million, $1 millionand $17 million for the years endedDecember 31, 2001, 2000 and 1999,respectively.

In addition to accrued environmentalliabilities, the Company had reason-ably possible loss contingencies relat-

financials

24

ed to environmental matters ofapproximately $73 million and $73million at December 31, 2001 and2000, respectively. Further, theCompany has identified other sites,including its larger manufacturingfacilities, where additional future envi-ronmental remediation may berequired, but these loss contingenciescannot reasonably be estimated at thistime. These matters involve signifi-cant unresolved issues, including thenumber of parties found liable at eachsite and their ability to pay, the out-come of negotiations with regulatoryauthorities, the alternative methods ofremediation and the range of costsassociated with those alternatives.The Company believes that these mat-ters, when ultimately resolved, whichmay be over an extended period oftime, will not have a material adverseeffect on the consolidated financialposition or consolidated cash flows ofthe Company, but could have a mate-rial adverse effect on consolidatedresults of operations or cash flows inany given period.

Capital spending for new environ-mental protection equipment was$26 million in 2001 versus $27 mil-lion in 2000 and $30 million in 1999.Spending for 2002 and 2003 isexpected to be $26 million and $21million, respectively. Capital expen-ditures in this category include proj-ects whose primary purposes are pol-lution control and safety, as well asenvironmental aspects of projects inother categories that are intendedprimarily to improve operations orincrease plant efficiency. TheCompany expects future capitalspending for environmental protec-tion equipment to be consistent withprior-year spending patterns. Capitalspending does not include the cost ofenvironmental remediation of wastedisposal sites.

Cash expenditures for waste disposalsite remediation were $51 million in2001, $33 million in 2000 and $27million in 1999. The expenditures

for remediation are charged againstaccrued remediation reserves. Thecost of operating and maintainingenvironmental facilities was $129 mil-lion, $114 million and $107 millionin 2001, 2000 and 1999 respectively,and was charged against current-yearearnings.

Other LitigationThere has been increased publicityabout asbestos liabilities faced by man-ufacturing companies. As a result ofthe bankruptcy of most major asbestosproducers, plaintiffs’ attorneys areincreasing their focus on peripheraldefendants. The Company believes ithas adequate reserves and insuranceand does not believe its asbestos expo-sure is material.

There are pending lawsuits filedagainst Morton related to employeeexposure to asbestos at a manufactur-ing facility in Weeks Island, Louisianawith additional lawsuits expected. TheCompany expects that most of thesecases will be dismissed because theyare barred under worker’s compensa-tion laws; however, cases involvingasbestos-caused malignancies may notbe barred under Louisiana law.Subsequent to the Morton acquisition,the Company commissioned medicalstudies to estimate possible futureclaims and recorded accruals based onthe results. Morton has also been suedin connection with the former FrictionDivision of the former ThiokolCorporation which merged withMorton in 1982. Settlements to datetotal $350 thousand and many caseshave closed with no payment. Thesecases are fully insured. In addition,like most manufacturing companies,Rohm and Haas has been sued, gener-ally as one of many defendants, bynon-employees who allege exposureto asbestos on the Company premises.

The Company and its subsidiaries arealso parties to litigation arising out ofthe ordinary conduct of its business.Recognizing the amounts reservedfor such items and the uncertainty of

the ultimate outcomes, it is theCompany’s opinion that the resolu-tion of all these pending lawsuits,investigations and claims will nothave a material adverse effect, indi-vidually or in the aggregate, uponthe results of operations, cash flowsor the consolidated financial posi-tion of the Company.

Dividends Total common stock dividends paid in2001 were $.80 per share, compared to$.78 per share in 2000. TheCompany's common stock dividendpayout is targeted at approximately35% of trend-line earnings. Commonstock dividends have been paid eachyear since 1927, and the payout hasincreased annually since 1977.

Additions to Land, Building andEquipment Capital additions were $401 millionin 2001 compared to $391 million in2000. Fixed asset additions during2001 included spending on theCompany’s upgrade and consolida-tion of its ERP infrastructure; spend-ing on a human resource/payrollproject; completion of the Rodelexpansion and the de-bottleneckingof the USA Methyl Methacrylate(MMA) facility in Houston. Capitaladditions during 2000 includedacrylics expansion in Texas; spendingon emulsions plants in the UnitedKingdom and Argentina; facilityexpansion in Electronic Materials,particularly at the Rodel facilities andspending on the Company’s ERPproject.

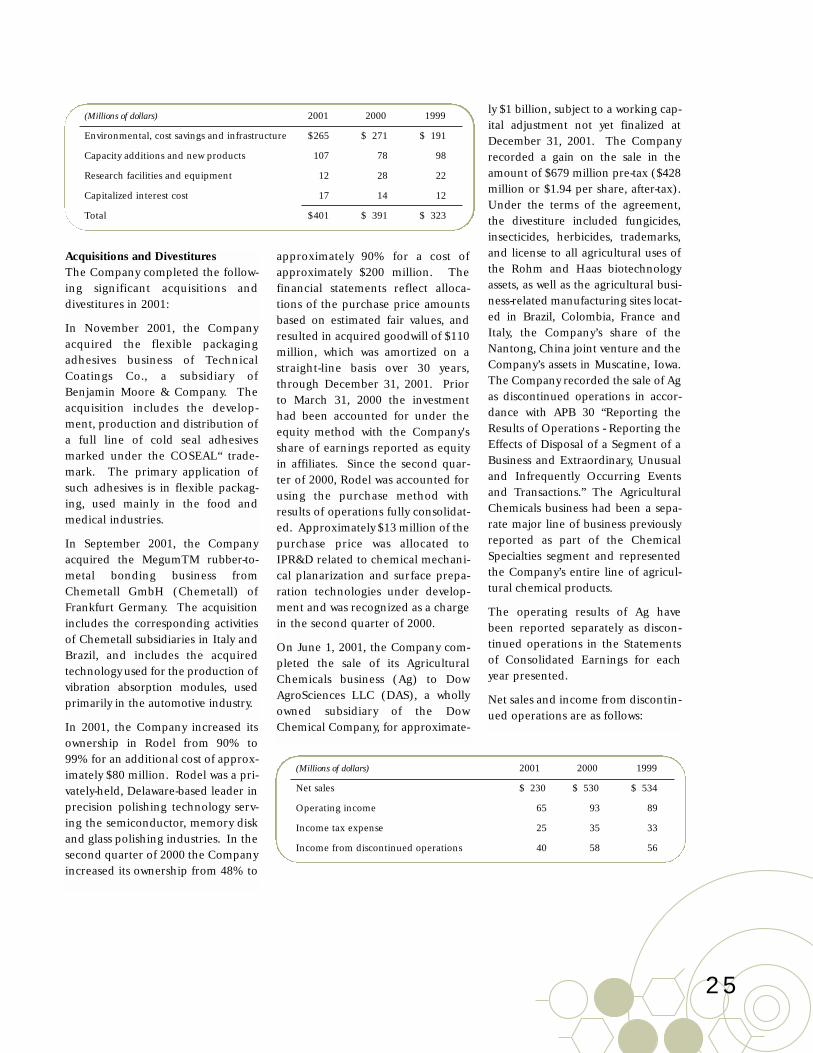

Capital expenditures in 2002 are notexpected to exceed depreciationexpense. Spending for environmen-tal protection equipment, which isincluded in several of the categoriesin the table shown below, was $26million in 2001, $27 million in 2000and $30 million in 1999.

Expenditures for the past threeyears, categorized by primary pur-pose of project, are presented below:

25