il cop bangladesh survey of the jute and cotton textile...

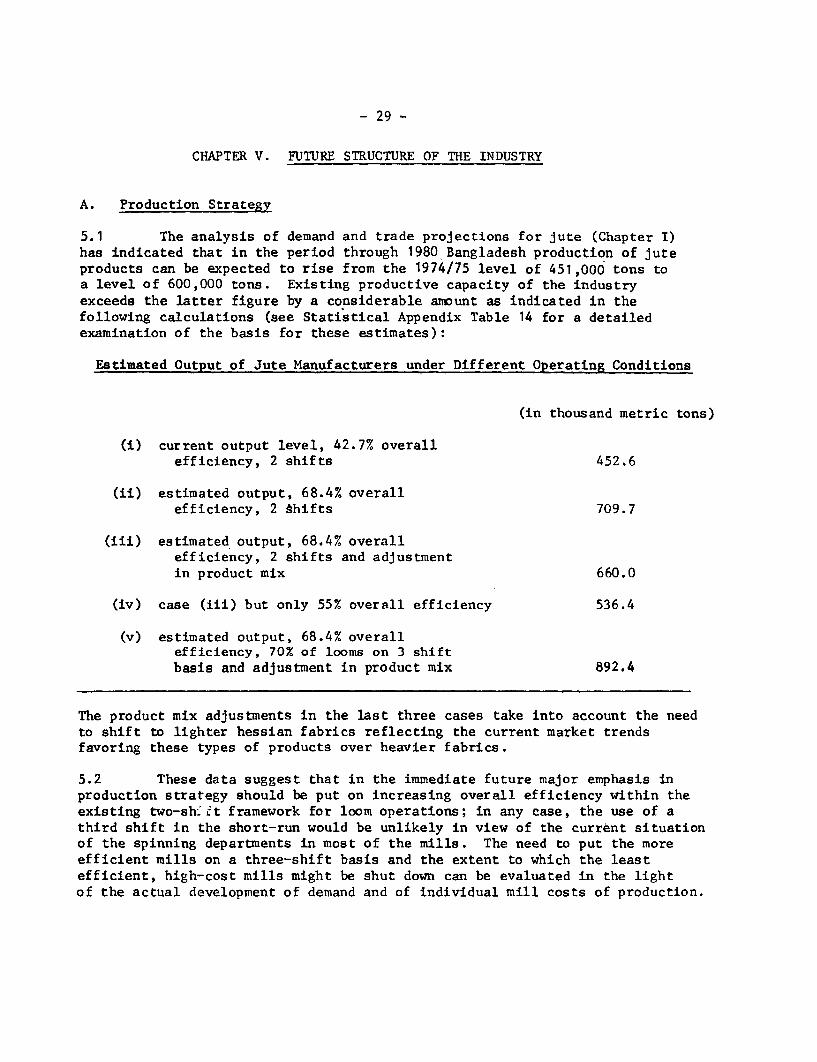

TRANSCRIPT

Report No. 883-BD "'IL COPBangladeshSurvey of the Jute and CottonTextile IndustriesStudies in connection with the appraisal of the Fourth Industrial Import Credit.

September 25, 1975

Industrial Projects Department

Not for Public Use

Document of the World Bank

This document has a restrfcted distribution and may be used by recipientsonly in the performance of their official duties. Its contents may nototherwise be disclosed without World Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

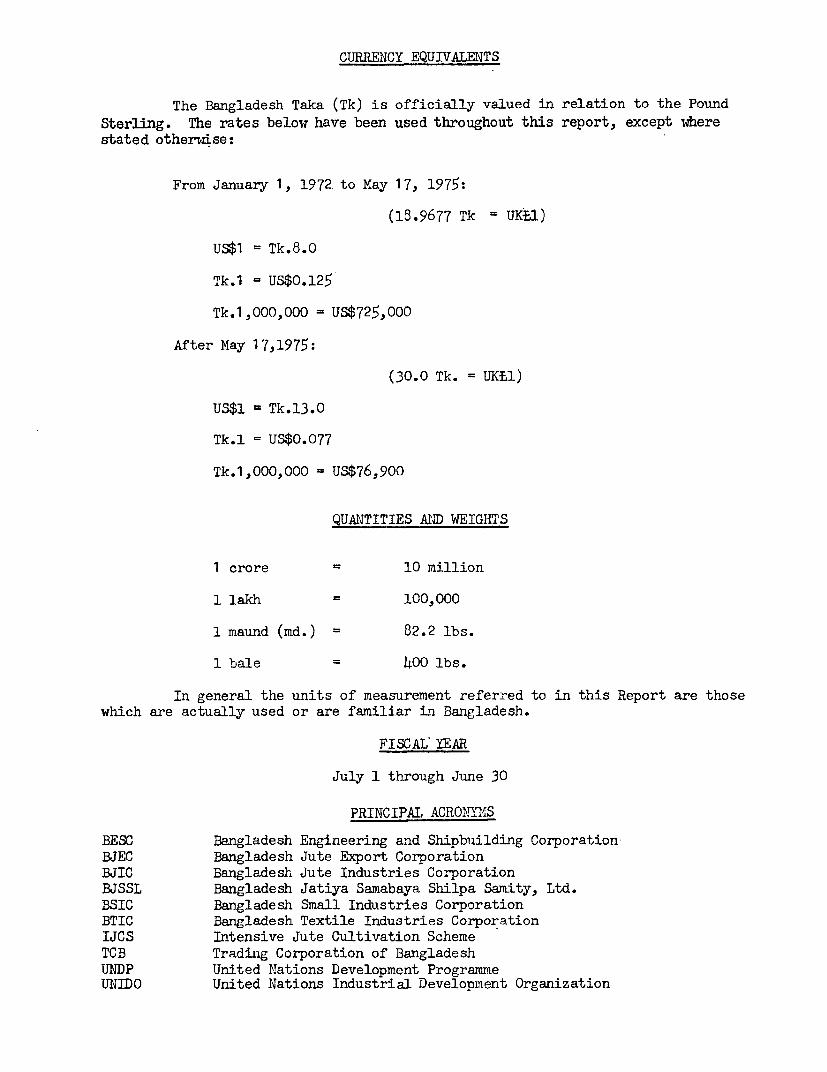

CURRENCY EQUIVALENTS

The Bangladesh Taka (Tk) is officially valued in relation to the PoundSterling. The rates below have been used throughout this report, except wherestated otherwise:

From January 1, 1972 to May 17, 1975:

(18.9677 Tk = UKA1A)

US$1 = Tk.8.0

Tk.1 = US$0.125

Tk.1,000,000 = US$725,000

After May 17,1975:

(30.0 Tk. = UKE1)

US$1 Tk.13.0

Tk.1 = US$0.077

Tk.1,000,000 = US$76,900

QUANTITIES AID WEIGHTS

1 crore 10 million

1 lakh 100,000

1 maund (md.) 82.2 lbs.

1 bale 4 OO lbs.

In general the units of measurement referred to in this Report are thosewhich are actually used or are familiar in Bangladesh.

FISCAL YEAR

July 1 through June 30

PRINCIPAL kCROhTlNS

BESC Bangladesh Engineering and Shipbuilding CorporationBJEC Bangladesh Jute Export CorporationBJIC Bangladesh Jute Industries CorporationBJSSL Bangladesh Jatiya Samabaya Shilpa Samity, Ltd.BSIC Bangladesh Small Industries CorporationBTIC Bangladesh Textile Industries CorporationIJCS Intensive Jute Cultivation SchemeTCB Trading Corporation of BangladeshUNDP United Nations Development ProgrammeUNDO United Nations Industrial Development Organization

This report was prepared by a mission consisting of Irwin Baskind (Chief),Samir Bhatia, Ronald Brigish, Benjamin Cu Kok and William Whitesell, anda consultant team conposed of Martin Stussi, Gino Oggero and Enrico Vitali.The mission visited Bangladesh Febraary-March l975.

BANGLADESH

Survey of the Jute and Cotton Textile Industries

Table of Contents

Page No.

FOREWORD .................................................

PART I - THE JUTE INDUSTRY.

SUMMARY OF CONCLUSIONS AND PRINCIPAL RECOMMENDATIONS.... ii - vii

I. INTRODUCTION

Historical Background . .......................The Demand Situation ............................ 3

II. THE JUTE INDUSTRY IN BANGLADESH

General Characteristics ..................... 8The Bantladesh Jute Industries Corporation ... 8

III. ASSESSMENT OF PRODUCTION CAPABILITIES

Analysis of Productivity .................... . 10Analysis of Structure of Costs .............. . 15Financial Condition of the Mills . .17

Raw Material Supplies ............................. 19BJIC Proposals for Rehabilitation and

Expansion .. ................................ 19

IV. MEASURES TO IMPROVE PERFORMANCE

Production Performance ....................... 20Financial Measures Required ................... 26Improving Marketing Information .............. 27External Assistance ..... ..... . . .. ........ 28

V. FUTURE STRUCTURE OF THE INDUSTRY

Production Strategy ..... . ................... .29Possible Changes in Manufacturing Costs ...... 30Price Strategy for Short and Medium-Term ..... 31Longer-Term Considerations ..... .............. 32

ANNEX I Review of Current Situation for JuteCultivation

Addendum IAddendum II

ANNEX II Evaluation of the MillsANNEX III Analysis and Review of Spare Parts RequirementsANNEX IV Organization Chart of the Ministry of Jute

STATISTICAL APPENDIX

Table I Production of Jute and Allied FibersTable II Consumption and Export of Jute and Jute

ManufacturersTable III Production, Consumption, Exports and

Stocks of Jute ManufacturersTable IV Production of Jute ManufacturesTable V Actual Export of Jute ManufacturesTable VI List of Mills with Installed Loom CapacityTable VII Inventories of Jute Manufactures by ProductsTable VIII Inventories by Sold/Unsold CategoriesTable IX Unaudited Balance SheetTable X Consolidated Income StatementTable XI Typical Cost Structure for Major Jute

Manufactures, 1973 through 1975Table XII Projects and the BMR ProgramTable XIII Ongoing Projects of BJICTable XIV Calculation of Production Levels Under Various

Assumptions of Technical Efficiency and Use.

PART II - THE COTTON TEXTILE INDUSTRY

SUMMARY OF CONCLUSIONS AND PRINCIPAL RECOMMENDATIONS... i - iv

I. INTRODUCTION

Status of the Cotton Textile Industry 1Handloom Weaving Industry . .Pre-Independence Pattern of Production and

Trade . .2

Difficulties in Restoring Production PostIndependence... .. 2

Man-Made Fibers . .4

Consumption of Textiles in Bangladesh Scope of this Study . .6

II. EVALUATION OF CURRENT PERFORMANCE OF THEINDUSTRY

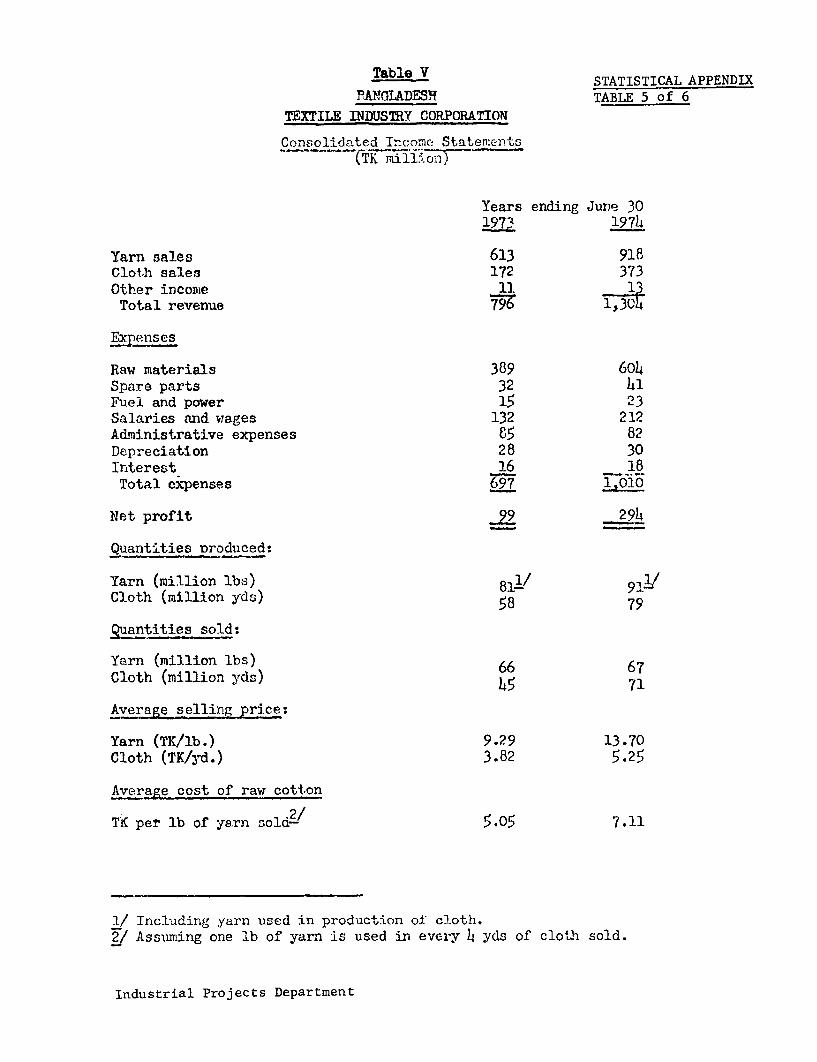

Overall Efficiencyc...... . . . .. . 6Marketing Aspects ........................... 9Cost Structure ........................... . . 11Financial Condition of BJIC ............... .. 13

III. MEDIUM-TERM DEVELOPMENT STRATEGY

Future Consumption and ProductionRequirements .. ............................ 14

Improving Production Performance . ........... 15Production Targets through 1977/78 .......... 16Longer-Term Objectives ...................... 18Marketing and Pricing Policies .............. 20External Assistance .. ....................... 22Relations with the Ministry of Industry ..... 22

ANNEX I Evaluation of MillsANNEX II Spare Part RequirementsANNEX III Weaving and FinishingANNEX IV Organization Chart of BJIC

STATISTICAL APPENDIX

Table I Production of Yarn by Counts during 1973/74Table II Installed and Working Capacity of Mills as

of January 1973Table III Size Distribution of Mills, January, 1973Table IV Consolidated Balance SheetTable V Consolidated Income StatementTable VI Basis of Estimating Yarn Output

FOREWORD

Since the independence of Bangladesh in late 1971, the InternationalDevelopment Association has provided three industrial import program credits,totalling $175 million, designed to assist the new government to overcome thedestruction resulting from hostilities and a series of natural disasterswhich befell the country almost simultaneously. In the face of an overwhelmingresource gap these funds were used to finance imports of critical raw mate-rials and spare parts for the highest priority economic activities, essentialfor the maintenance of minimal standards of living and for stimulating exportgrowth to permit expansion of import capacity.

In view of its concern that the proceeds of these credits be utilizedefficiently and that these credits support specific developmental objectives,the Association has decided to undertake a series of special studies of indi-vidual sub-sectors receiving these funds, examining the measures required inthe short and longer term for improving performance. For the fourth IndustrialImport Program Credit, it was decided to review the performance of jute andcotton textiles which are the two most important industries in the manufacturingsector, accounting for almost half of total value added. Moreover, manufacturedjute represents about 40% of total Bangladesh exports.

A Bank mission (to study the two industries) visited Bangladeshfrom February 17 through March 11, 1975; it visited 17 jute mills accountingfor 56% of the installed jute loomage, and 16 cotton mills representing 44%of the total cotton spindle capacity in the country. It also had discussionswith officials of the Bangladesh Jute Industries Corporation (BJIC), theBangladesh Textile Industries Corporation (BTIC), staff of the PlanningCommission, officials of the Bangladesh Engineering and Shipbuilding Corpora-tion (BESC) and of plants controlled by that Corporation which have capacityfor jute and cotton textile spare parts production, representatives of theprivate sector, and foreign experts assisting industries in the countryunder bilateral programs.

The findings of the mission and the principal recommendations havebeen discussed with the Government, and arrangements are being made forImplementation of the Action Programs presented in the summaries precedingPart I and Part II of this report. This is reflected in the documentationfor the proposed Fourth Industrial Import Program Credit.

PART ONE

THE JUTE INDUSTRY

SUMMARY OF CONCLUSIONS AND PRINCIPAL RECOMMENDATIONS

i. Short- and medium-term improvements in the balance of paymentsgap of Bangladesh rest heavily on measures taken by the Government to re-vitalize its trade in jute which in both raw and manufactured forms currentlyaccounts for more than 80% of its total exports. Recent measures have im-proved the competitive position of jute in comparison with synthetic fibers,but substantial measures are still needed to improve the performance of themanufacturing sector which has lost ground both in absolute and in relativeterms as compared to other jute and hard fiber exporting countries.

ii. The world-wide stagnation in jute demand during the last 15 yearsreflects the appearance of competitive synthetic fabrics and fibers whoseprices have been generally lower than those of jute products and the changesin transport and handling techniques which have reduced use of packagingmaterials. In spite of the increase in crude petroleum prices, the syntheticitems based on that commodity which are competitive with jute have increasedvery little in price. Extrapolation of present market trends, beset by someuncertainty due to the current recession, indicate only slight growth in totaldemand for jute products in the period through 1980. Nevertheless, Bankstudies have shown that consumption of hard fibers such as jute and syntheticsare price elastic, and that a well-organized jute price strategy could changethe previous trend (Chapters I and II).

iii. As a result of the exchange adjustment introduced in May 1975, sub-stantial reductions in external prices for most jute products are possiblewhile at the same time operating deficits of the mills can be eliminated.Nevertheless, in order to ensure the future viability of the industry and totake fullest advantage of the opportunities offered, measures must now betaken to improve performance, including a broad rehabilitation program de-signed to reduce costs, improve quality standards, and develop more effectivemarketing techniques.

iv. The rehabilitation program recommended (Chapter IV) would involvea series of simultaneous steps in the areas of marketing, production planningand management of mill operations. To implement the steps recommended itwould be necessary to reorganize the present Bangladesh Jute Industry Corpo-ration (BJIC), the public sector agency which controls all jute mills in thecountry (77 units as of June 1975). This would involve strengthening thepolicy and production planning functions of the Corporation; mill managerswould be given wider autonomy and would be held responsible for the dailyoperations of their enterprises.

- ii -

v. On the marketing side, it appears necessary to strengthen themarketing services of the Corporation to enable it to undertake certaincentral functions critical in the development of a more aggressive marketingstrategy. These would include market research, broader marketing informa-tion collection, overseas promotion and operating offices in a few selectedmajor importing centers (para. 4.23). As regards sales, the present approachis to provide a flexible structure to meet the requirements and preferencesof individual buyers; a number of larger mills, as well as groups of smallerones, have been given autonomy in sales while orders received directly bythe Corporation are being assignedt, after consultation with the buyers, toindividual mills. The mills have to equip themselves to improve customerservices, to respond more efficiently to buyer enquiries, requests forinformation such as shipping dates, etc. (para. 4.24). There is urgent needfor the Marketing Directorate to make a detailed study of the current orshort-term world market for the major jute products. This should be followedby studies of longer-term prospects. Since production planning requiresspecific product information, the timing of this work would be coordinatedwith the preparation of annual and longer-term production programs describedbelow.

vi. BJIC should establish a Production Planning Directorate (paras.4.15-4.18). At present there is considerable uncertainty over productioncontrol among the mills. Insufficient direction has been provided to millsto encourage production of specific jute goods for which demand prospectsappear favorable either in the long or short term or to discourage produc-tion of those items where market conditions are less favorable. To a greatextent mill managers have chosen to produce those items which raise fewestproblems in manufacture rather than produce in response to market demand ortrends. The net result is inventory accumulation of a number of goods withlimited sales potential and shortages of items in relatively good demand.The Corporation has not had the information base required to permit thedevelopment of a production strategy to meet actual and expected futuredemand, including control over inventory accumulation in the desired direc-tion. Thus the principal task of the Production Planning Directorate wouldbe to develop production programs for the sector, with specific targets byproduct lines for individual mills, established on the basis of productioncapabilities of the mills, demand forecasts and the financial resourcesavailable to the Corporation. While these targets would be prepared on anannual basis, they would be subject to systematic monthly reviews to permitmodifications -in the light of any new developments.

vii. In order to prepare this plan, it will be necessary to compile aninventory of the productive capacity of each mill for specific types ofproducts and to have an assessment by each mill manager of production capa-bility. This work could be started immediately and it is envisaged thatcomplete data could be available within about six months, by the end ofMarch 1976. At about the same time the Marketing Directorate would havecompleted its short-term detailed market analysis. The production planning

- iii -

group would then reconcile these two elements to provide a sector-wide pro-duction program with preliminary output targets for individual mills in accord-ance with their capabilities, and overall targets consistent with demand expec-tatic's and financial projections. One of the objectives of this excercisewould be to achieve specialization among the mills. TFe targets would bereviewed with the mill managers to assure understandlAg and agreement and,after any required revision, would be established as the annual productionprogram. It is envisaged that the 1976/77 plan would be formulated priorto July 1976 which is the beginning of the fiscal year.

viii. For fiscal 1975/76, only very broad production targets have beenset by BJIC with mills expected to react on an ad hoc basis depending on theflow of orders. In the absence of the detailed data required for setting upa comprehensive production plan, as outlined in the previous paragraph, theCorporation should nevertheless prepare by December 1975 a program for thesecond half of the fiscal year, in accordance with the information alreadyavailable to it, and should set targets for mills in accordance with currentexpectations of their capability and demand.

ix. The Production Planning Directorate should also prepare a longer-term development program for the industry which would reflect the longer-termdemand forecasts of the Marketing Directorate. This program would set outthe anticipated capacity requirements and analyze existing capacity in thelight of these needs. The analysis would then permit evaluation of thebalancing, modernization and rehabilitation (BMR) programs which have beenset up for 19 existing mills and the 8 new mills (or expansions) which havebeen under construction for a number of years but which have not yet beencompleted. In the light of the review of demand and current productioncapability contained in the longer-term production plan, conclusions shouldemerge regarding necessary changes in capacity.

x. The Finance Directorate should prepare before the end of calendaryear 1975 a financial projection for the fiscal year 1975/76. Full finan-cial statements and accounts for 1974/75 should be prepared by March 31,1976. The Directorate would participate in longer-term production planningthrough the preparation of appropriate financial projections (para. 4.21).The Corporation should accelerate the preparation of balance sheets re-flecting the true asset positions of the individual mills, for purposes ofproper financial control. A Cabinet Committee is currently reviewing thefinancial position of all public sector corporations with a view to theirfinancial restructuring. The Government should provide additional equity toBJIC to ensure an appropriate debt:equity ratio; this would permit reduc-tion of debt service charges which have in the past contributed to the highunit costs of manufactured jute products, and in turn to the large deficitsincurred by the Corporation which have required further bank borrowing andGovernment subsidies (para. 4.20).

- iv -

xi, To improve production performance at the mill level, it will berecessary to undertake a series of assistance programs concentrating onthose areas which have adversely affected capacity utilization and increasedproduction costs. In the first phase, emphasis would be put on developingin individual mills appropriate maintenance programs, the lack of which hasbeen one of the major factors contributing to production difficulties (para.4.3). For this purpose the Technical Directorate of BJIC should organizein each of the four zones (excluding Adamjee) a maintenance task force com-prising one expatriate expert and two local counterparts; one of the latterwould be the zonal maintenance engineer, and the other would be drawn fromamong senior mill production staff who have demonstrated competence in thisarea. The task force would: (a) appraise the existing system in each millfor preventive maintenance programs and make recommendations for improvement;(b) assist in setting up the necessary equipment inventories; and (c) ifnecessary, assist in implementation of recommendations. It is envisagedthat within each zone at least four mills could be analyzed nine months afterthe services of the international experts had been obtained and by the endof 18 months the recommended improved systems would be in full operation. Theassessment should graduially be extended to other mills. The directorateshould organize its program so that in the first phase the 16 mills coveredshould account for at least 40% of loomage; this is a realistic target since50% of total existing looms (excluding Adamjee) are to be found in 15 mills.

xii. Another essential element in this urgent phase is the organizationwithin the Technical Directorate of a spare parts division which would assessthe capacity within the country to meet spare parts needs for jute manufac-turing and develop a program to meet those needs. This group should beestablished using necessary expatriate technical assistance in organizingits work as well as in the early stages of implementation of its program;it is anticipated that this can be achieved with a preliminary work programready within nine months. A number of mills, particularly the larger ones,have workshops which can supply all but the most sophisticated parts andthere are enterprises within the private sector and the Bangladesh Engineer-ing and Shipbuilding Corporation (BESC) which can produce parts as well ascomplete looms. The BJIC group would represent that agency in a committeeestablished in the Ministry of Industries to deal with this problem; thiscommittee would have to be revitalized (paras. 4.4 and 4.5).

xiii. More comprehensive assistance to improving productivity will beundertaken in a second phase which would involve the organization of produc-tivity advisory teams in each zone to review all aspects of production atthe level of individual mills (para. 4.6). Each team would be composed ofan expatriate jute production expert and two local counterparts, one ofwhich would be the Chief Production Engineer for the zone and the secondwould be drawn from senior production staff of the Corporation on a rotatingbasis. During these studies attention would be paid to labor use and costs,raw material preparation, problems in operation of equipment, etc. Theteams should provide detailed recommendations to mill management on specific

measures of assistance, including various training needs which could beprovided within the plant or which would be best provided in central locationsto serve several mills. BJIC should ensure that the 16 mills covered duringthe first period of this work should encompass at least 40% of total loomageof the industry (excluding Adamjee) (para. 4.6).

xiv. Aside from other elements mentioned earlier, operational autonomyof the individual mill managers should be increased in such matters as pur-chasing of raw jute, personnel management and local procurement. In general,the performance of mill managers needs to be underpinned by management assis-tance programs. It is also necessary to establish an appropriate system ofincentives for management (paras. 4.11 and 4.12).

xv. At the present time, in the case of hessian and sacking (narrowlooms), mills are expected, in principle, to follow the practice of 100%visual inspection at one of the final stages in manufacturing. However, dueto inadequate supervision, this is not being done in all the mills. Millmanagers must take steps to ensure proper performance of supervisory responsi-bilities in this regard. In the case of carpet backing (broad looms), 100%visual inspection is possible only if special facilities are provided; cur-rently these exist in only two carpet backing mills. They should be extendedto all mills producing carpet backing, in order that manual repair can bemade of all defects in excess of the limits acceptable to trade (para. 4.8).

xvi. An independent export inspection service should be set up outsidethe jurisdiction of BJIC which would be responsible for pre-shipping inspec-tion and certification of all export goods as a means to ensure conformitywith contract specifications (para. 4.8).

xvii. The current performance bonus system applied to piece workers inthe mills has not been effective and should be restructured. The presenthigh percentage of absenteeism of permanent workers, especially during harvest-ing and new planting seasons, interferes with achieving better machine per-formance and a more effective production bonus system may help to removethis bottleneck. It is essential that production standards used as thebasis for applying the system at the level of the individual mill reflectnot the average output for the industry but rather the technical character-istics of the particular types of machines determining their potential out-put. This will require more detailed surveys of the machines in use to fixthe standards according to types. Effective use of the bonus system alsorequires recognition on the part of the authorities concerned that, even ifthe average standard for the industry is reduced in the short term, resultingin some immediate increase in labor costs per unit of output, in the longerrun if absenteeism can be reduced increasing machine performance, substan-tial cost reduction can be obtained (para. 4.9).

xviii. The audit division within BJIC's Finance Directorate should expandits functions to include checking accuracy and completeness of data for themills and in general should promote effective cost control procedures (para.4.21).

- vi -

xix. The Ministry of Jute should keep under review the functioning ofthe four raw jute marketing corporations to ensure efficient distributionof raw jute, both for export and to the mills. Steps taken in recent monthshave :ubstantially reduced overlapping and wasteful procedures but furtherconsolidation of the purchasing agencies may be advisa'Ele. Moreover, consid-eration should be given to permit purchases directly from farmers, eitherindividually or in groups, as a means of reducing the gap between millgateand farmgate prices. The Government should keep the Association informed ofthe measures taken in these matters, including those measures relating tojute trading in the private sectqr. The Ministry should also improve thecollection of basic data on acreage under cultivation, yields and cultiva-tion costs (Annex I).

xx. To obtain the external assistance required to implement the program,the following steps are suggested (paras. 4.26 and 4.27). The first phasewould comprise the organization of maintenance task forces and of a sparparts division within the Technical Directorate of BJIC. The maintenancetask force would require 36 man-months of assistance while the spare partsprogram would require 1 expert for 12 months in this first phase, making atotal of 48 man-months of experts' time. The experts would be obtainedthrough an experienced engineering consulting firm; the foreign exchangecosts are estimated at about US$300,000. The Government should endeavor tohave the experts in the field prior to March 31, 1976; it could make use ofthe Association's Technical Assistance Project Credit (409-BD) to financethe foreign exchange costs.

xxi. The second phase comprises more comprehensive expatriate assistancefor improving productivity, assisting in organizing the work of the Produc-tion Planning Directorate and advising in the reorganization and strengtheningof the Marketing Directorate. The Government has been negotiating with UNDP/UNIDO for a project to assist the jute sector and it is envisaged that aprogram acceptable to the Association would be developed. The scope of theprogram would provide assistance in critical areas such as quality controladministration, cost accounting and financial planning, and would includetraining both locally and abroad in all of the fields which have been enum-erated. Moreover, funds made available under a UNDP project could financelaboratory equipment for quality control centers and training materials.

CHAPTER I. INTRODUCTION

A. Historical Background

1.1 Jute has been grown in the Ganges delta for centuries and Bangladesh

has some of the best jute growing lands in the world. While over thirtyvarieties exist, only two, Corchorus capsularis (white jute) and Corchorusolitorius (tossa jute) are widely grown. Both the cultivation and processing

of jute are labor intensive. Fiber is obtained from the plant by retting

(steeping) the stems in water and then separating the fiber from bark by hand.

1.2 The years following the end of World War II saw the first seriouslong-term difficulties developing for the jute trade world-wide, on accountof unreliability of supply and unstable prices. Demand was strong, but trans-port difficulties and coal shortages in India limited supplies. Consumptionwas restricted to about 80% of pre-War levels. These difficulties accelerated

the search for jute substitutes and gave impetus to efforts to improve tech-niques for bulk-handling of commodities.

1947-1971

1.3 The partition of. India in 1947 had a major impact on the world jutetrade. Pre-partition India accounted for over 96% of raw jute production andmost of the raw jute exports. It accounted for 57% of world jute loomage andexported 85% of her jute manufactures. After partition, all 108 mills were

located in India, while 71% of the jute growing areas, including the bestlands, were in East Pakistan. Most marketing and financial resources werealso in India. It was therefore a logical decision for India to expand itsraw jute production, to replace the raw jute supplies from Pakistan. In

1948-49, India launched a "grow more jute" campaign which consisted, amongother things, of distribution of seeds at subsidized rates, establishmentof seed farms, supply of fertilizers, and promotion of line-sowing, which

is more productive than traditional broadcast sowing.

1.4 On its part, Pakistan made the political decision to establish its

own jute manufacturing industry, and had to develop its manufacturing,marketing, and financial capabilities. It identified the jute industry asone which would receive full support in its Six-Year Development Program(1951-57), and extended to it a package of incentives which included, among

other things, preferential access to capital, tax concessions, and exportincentives. n 1951, the first jute mill was established in East Pakistan.Bawa Jute Mill, privately-owned, had 10 hessian and 125 sacking looms. The

next mill to begin producing was Adamjee. With 1,700 hessian and 1,300sacking looms, it was and still is the largest jute mill in the world. Theindustry expanded rapidly and, by 1958, 14 mills with a total of 7,849 loomswere operating. At the time, Pakistan processed one million bales of raw

jute annually, or less than 20% of its total raw jute output.

-2-

Effects of the Export Bonus Scheme

1.5 In 1959, Pakistan instituted its "export bonus scheme" to alleviateits foreign exchange difficulties. It was thought that by introducing amultiple exchange rate system, an outright devaluation might be avoided, andthat the economy could be steered in the specific directions desired byGovernment. Under the export bonus scheme some exports continued to receivethe rupee equivalent of export receipts at the official rate; however, forspecified items exporters were given, in addition, bonus vouchers equivalentto a certain percentage of export value. These vouchers could be used tofinance imports, or could be sold to others. While the price of vouchersfluctuated, the effective exchange rate for exports was substantially higherthan the official rate; exporters were in effect being subsidized by theconsumers of imports financed by the vouchers. The export bonus scheme wasused to discriminate against raw jute exports for a decade. Jute goodsexporters received bonus vouchers from 1959-60 on, while raw jute exportersreceived bonus vouchers only in 1970/71. Even then, raw jute exporters wereentitled to bonus vouchers worth 10% of their export earnings, while exportersof jute manufactures were entitled to 40%.

1.6 The results of such discrimination were many. Farmer incomes werereduced while jute manufacturers were given a high level of protection. Asmost manufacturing was controlled by non-Bengalis, profits (estimated atabout 10-15% of sales value) were largely remitted to the West Wing. Profitlevels apparently remained high even in periods (e.g., 1968) when valueadded was negative. There were few incentives to manage mills efficiently.Production per loom declined from 31.7 tons in 1960/61 to 27.5 tons per yearin 1969/70, compared to a feasible output level in excess of 55 tons peryear. This was in an industry with no material shortage problems.

1.7 On the positive side, the establishment of the jute industry createdjobs in an area where employment opportunities are scarce. By the end of the1960's, the jute industry employed about 150,000 people and Pakistan's sharein manufactured jute exports had risen from negligible amounts to 44%.

1.8 The discriminatory pricing policy of the Pakistan government hadserious implications, however, on the international markets for raw jute andjute manufactures. While Pakistan was developing its jute manufacturingindustry, it still was exporting most of its jute crop as raw jute. Thedifferential exchange rates resulted in high implicit taxation of raw jute,which in turn led to reduced profitability in jute cultivation, smaller cropsand higher international prices. Although overall demand for jute was risingthrough the mid-1960's, users of raw jute, especially in Western Europe,increasingly switched to synthetic substitutes as price differentials betweenthe two began to grow. Had a smaller exchange rate differential been imposedbetween raw jute and jute manufactures, the end-use markets might have beenbetter preserved for the time when increased manufacturing capability inPakistan could supply them.

1.9 The differential exchange rate system also minimized the marketsignals that would have regulated expansion. By the late 1960's, valueadded in jute manufacturing generally was very low, and in a number of millsit was even negative, but profits remained high. The industry concentratedin the beginning on the large and well-developed mar'.ets for hessian andsacking, products which were relatively simple in technology and requiredrelatively low degrees of quality control. It was not until the 1960's thatPakistan started to produce carpet-backing in appreciable quantities. Withbetter market signals this growing market might have received earlier atten-tion.

Independence

1.10 The disturbed conditions that immediately preceded the birth ofBangladesh caused a complete stoppage in mill production. Non-Bengali millowners, managers, and supervisory personnel left the country. The basicstructure of the industry also changed when the Government nationalized 44of the 77 mills, including some of the largest and best run, as "abandonedproperty". Later, as part of the Government's program to nationalize allmedium and large-scale industry, the remaining 33 mills, owned by Bengalis,were also nationalized. A holding company, the Bangladesh Jute Mills Corpora-tion (renamed Bangladesh Jute Industries Corporation when the entire industrywas nationalized) was created to run the mills. The corporation was estab-lished under the Ministry of Industries; later, it was shifted to theMinistry of Jute.

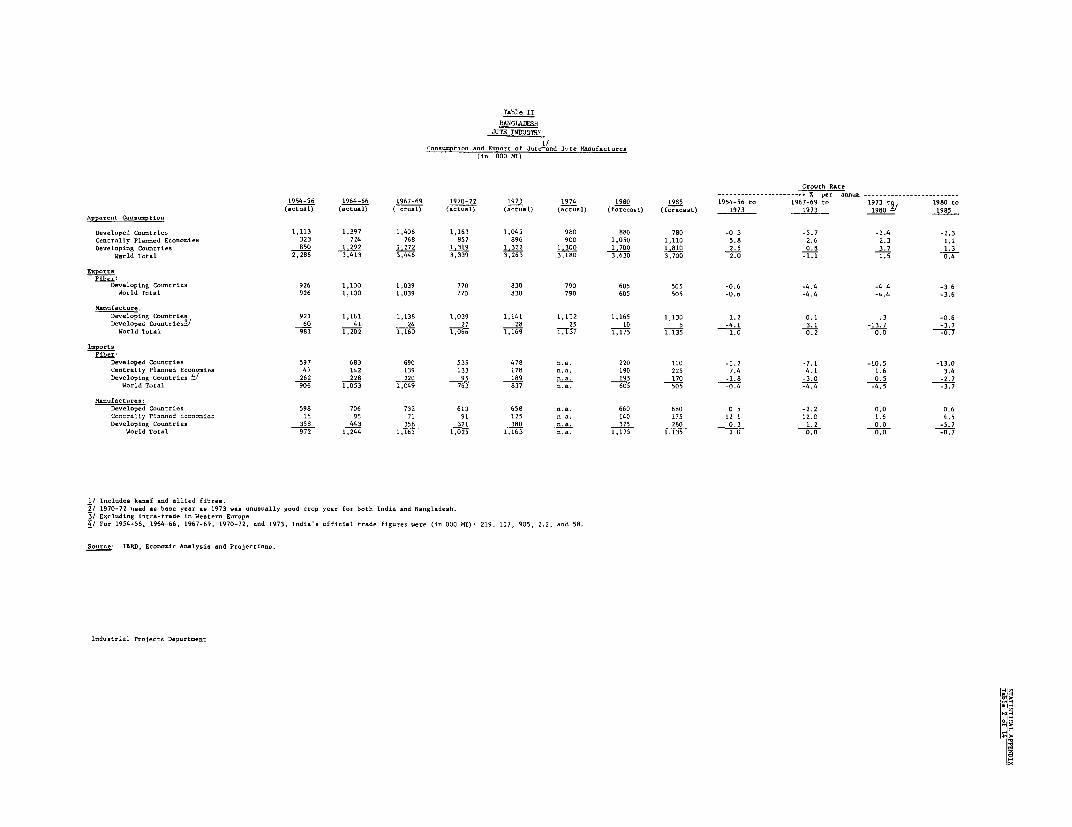

B. The Demand Situation 1/

1.11 World consumption of jute goods expanded at an average rate of4.1% per annum from the mid-fifties to the mid-sixties. This expansionarytrend halted in the latter half of the sixties, largely as a consequence ofthe stagnation in demand for jute in the developed countries. Changes inconsumer preferences - exemplified by the trend towards prepackaging offood - and technical innovations in transportation and handling of agricul-tural produce negatively affected the utilization of jute wrapping andsacking materials. At the same time, high and unstable prices for raw juteand jute goods, as well as uncertain supply and qualities, greatly stimulatedthe use of synthetic substitutes, which began to be marketed in increasingquantities in the late sixties. Textile polyolefins - polypropylene andpolyethylene - started to make significant inroads into all the major end-uses of jute - sacks, bags, industrial cloth, and carpet backing. Thisseverely constrained the demand growth of jute products in both WesternEurope and North America. The combined consumption of these marketsaccounted for a third of the world total. The existence of tariffs andquotas, only recently reduced, by the EEC countries on imports of jutegoods further reduced the demand in Europe.

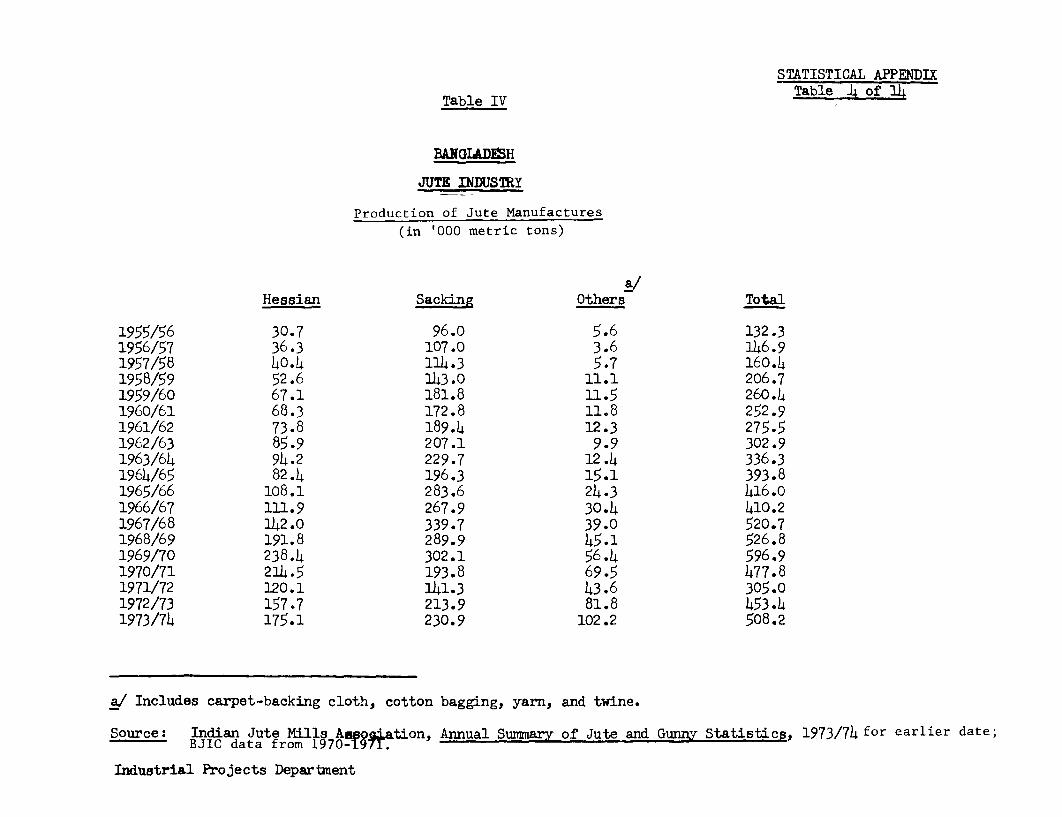

1/ For detailed data on production of jute, and consumption and trade injute and jute manufactures, see Statistical Appendix, Tables 1 and 2.

- 4 -

1.12 The shift to synthetics gained further momentum in the earlyseventies under the impact of supply disruptions and high prices caused bycivil disturbances in Bangladesh and the following war in the Asian sub-continent. Strikes in Calcutta, both in the jute mills and in the docks,and the labor unrest in Bangladesh further compounded the supply uncertainty.

1.13 Although the movement away from jute has been particularly strongin the developed countries, developing countries and centrally plannedeconomies - with the exception of the People's Republic of China - have alsobegun to shift to synthetics in the manufacture of bags and sacks. Consump-tion of jute goods has declined sharply in Western Europe - from 550,000metric tons in 1970 to 360,000 metric tons in 1973 - and ceased to grow inNorth America and other developed countries. In the centrally plannedeconomies and developing countries jute goods consumption has continued togrow, but much more slowly than in the past. On a world basis, jute goodsconsumption decreased from 3.40 million metric tons in 1970 to 3.30 millionmetric tons in 1973.

1.14 The "energy crisis" was thought by the major jute producing andexporting countries to be a welcome occasion to regain lost markets. Despitethe quadrupling of crude oil prices, which increased the prices of poly-propylene resin by about 70% in Western Europe and by about 40% in the UnitedStates, and of polypropyelene cloth by 15-20% in Western Europe and 5-10%in the United States, preliminary estimates indicate a further fall in theconsumption of jute manufactures of about 6%. Jute utilization increasedmarginally in the centrally planned countries and remained stationary in thedeveloping countries.

1.15 The failure of jute to take any advantage of the oil crisis wascaused by various factors. In early 1974, a long strike in Calcutta jutemills curtailed production of jute goods and led to a 50% increase in hessianprices. Later the Calcutta dock strike in October 1974 and the forty-fourday jute mill strike in early 1975 introduced further supply disruptions.Bangladesh raw jute prices, which had remained stable during the 1972/73and 1973/74 seasons at E 115-120 per ton also sharply increased in mid-1974,peaking at E 200 per ton (Bangladesh D grade white f.o.b. Chittagong-Chalna)in November 1974. At that time, this price reflected speculation concerningthe anticipated shortfall in the 1974/75 crop in both India and Bangladesh;but the E 200 price was maintained by export agencies in spite of fallingdemand and a less severe crop situation than had been expected. Raw jutesales were as a consequence negligible in the first quarter of calendar 1975;and it was not until the devaluation of the Taka in May 1975 that priceswere reduced to b 160; in July the price was further lowered to b 155.

1.16 Secondly, the economic recession in Western Europe and North Americaled to declines in construction and auto manufacturing activities, curtailingdemand for carpets and carpet backing. In the US, the largest single marketfor jute carpet backing, the reduction in total demand for backing materialshappened at a time when polypropylene carpet backing manufacturing capacity

had just been expanded. The strong oversupply condition which prevailed allduring 1974 further sharpened the price competition between jute and poly-propylene over market shares. Polypropylene carpet manufactures fullyabsorued the cost increases created by higher resin prices and kept theirselling prices unchanged. Imported jute carpet backin; prices, on the otherhand, increased by about 16% relative to 1973. This resulted in anotherstaggering loss (about 7%) in the market share of jute in primary carpetbacking.

1.17 In 1974/75, Bangladesh jute goods exports reached only 377 thousandmetric tons, or 33% of the total world export market. This is in contrast toabout 506 thousand metric tons in 1969/70. At that time, Bangladesh (thenpart of Pakistan) had a 44.1% share in world total exports.

1.18 Bangladesh's share in export markets deteriorated relative tothat of India as well in the post-independence period. In sacking, Bangladeshaccounts for only 65.1% of the combined exports of India and Bangladesh,as opposed to 85% before independence. In hessian, Bangladesh now accountsfor 39.9% as opposed to 45% earlier. In carpet-backing, Bangladesh's shareincreased from a pre-independence share of 12% to 27.2% in 1972/73, butthen fell to 26% in 1973/74. The following table shows the world exportmarket and Bangladesh's sh4re.

Bangladesh Share in World Export Market for Jute Manufactures(in '000 metric tons)

Preliminary1969/70 1973/74 1974/75

World Exports 1,147 1,169 1,137Bangladesh Exports 506 443 377Bangladesh Share (%) 44.1 37.9 33.2

Future Demand Prospects

1.19 Extrapolations of present market demand trends, beset by someuncertainty due to the current recession, indicate only slight growth intotal world demand for jute products in the period through 1980. End-usedemand projections (prepared by Bank's Economic Analysis and ProjectionDepartment before the recent devaluation of the Taka) show that, even on thebasis of some improvement in price competitiveness of jute, consumption indeveloped countries is likely to stagnate through the current decade, andthere would be only a small increase in overall world trade. Neverthelessprevious studies by Bank staff have also shown that consumption of hardfibers such as jute and its synthetic competitors are price elastic; it isthis characteristic of recent trends which is the basis for advocating amore aggressive price policy for jute. The May 1975 devaluation representsa first measure in attempting to reverse past trends. Market sources currentlyindicate some adjustments in prices of jute manufactures exported by Bangladesh,

-6-

but the general weakness of demand at this time does not permit an evaluationof possible impact. For the purposes of this study, conservative projectionshave been made of future growth possibilities as follows:

Projected Bangladesh Share in Jute Manufactures Export Markets(in '000 metric tons)

1975/76 1980/81 1985/86

World Exports 1,135 1,175 1,135Bangladesh Exports 440 510 540Bangladesh Share (%) 38.8 43.4 47.6

1.20 Taking into account the expected increase in local consumption, theoverall production and export balance for Bangladesh may be summarised asfollows:

Bangladesh Production, Consumption and Exports of Jute Manufactures(in '000 metric tons)

Preliminary Forecast Projection1974/75 1975/76 1980/81

Production 451 480 600Exports 377 440 510Domestic Consumption

(including stockchanges and losses) 74 40 90

1.21 The possible future structure of the industry, taking into accountthe necessary measures to improve the performance of the existing industry,are presented in Chapter V. In the next section, attention is drawn to oneaspect of future demand, the development of new uses for jute, a topicwhich has been treated by successive Bank reports on this industry.

New Products, New Markets, and Long-Term Prospects

1.22 The long-term prospects of jute should be capable of substantialimprovement through development of new markets and new uses. To date,especially in the case of Bangladesh, there has been very little researchand development. Whereas producers of synthetic fibers have spent largesums in product development, market research and market development, themajor jute producers have been mostly passive in their marketing strategy.Very little has been done to develop new markets or new products.

1.23 Some promising developments have occurred in the cultivation andprocessing of jute. On the agricultural front, advances have been made

towards high yielding varieties, and towards better retting procedures andmethods. These improvements would imply higher yield of crops and lesswaste in jute utilization. But the benefits from these developments wouldbe marginal if no new commercially viable uses for jute are found anddeveloped. Some minor advances have been achieved to date, but none ofthese have become commercially significant.

1.24 In Bangladesh, the jute research institute has been poorly financedand poorly manned. While there have been good people working in the institute,many have left for better positions elsewhere. Morale has been low due tothe perceived low priority given to research, as reflected in funding. Somenew uses for jute being studied by the institute have been: jute substitutefor knitting wool, some cotton and jute blend materials for suiting, andjute carpets.

1.25 In the long-run, if jute cannot win back the markets lost tosynthetics, paper, and other materials, it should strive to complement theseand other materials. As a complement, jute may have better prospects than asa direct competitor. For example, synthetic lined jute bags for cement,fertilizer, etc. have been viable products. Other products using jute inblended form or as backing could be developed, provided jute is pricecompetitive for its qualities and functions.

1.26 A UNDP project for the industry wing of the Bangladesh Jute ResearchInstitute has' been contemplated for many years, but it is still not in opera-tion.

1.27 In January 1973, at the Sixth Session of the FAG IntergovernmentalGroup on Jute, Kenaf, and Allied Fibers held in Dacca, participating govern-ments and agencies proposed the establishment of "Jute International". Theobjectives of Jute International are "to maintain a strong and expandingdemand for jute and kenaf and their manufactures, and to maximize theirconsumption". Activities will include market development programs, agri-culture and utilization research, sales promotion, and public relations.The secretariat was proposed to be located in New Delhi and the researchinstitute in Dacca. Since January 1973, the Governments of India, Bangladesh,and Nepal have ratified the agreement on Jute International, and Thailandhas requested observer status. There is every indication that Jute Inter-national would do much to answer the very critical shortage of resources forresearch and marketing and would reduce the problems of duplication, over-administration, and lack of foreign exchange.

- 8 -

CHAPTER II. THE JUTE INDUSTRY IN BANGLADESH

A. General Characteristics

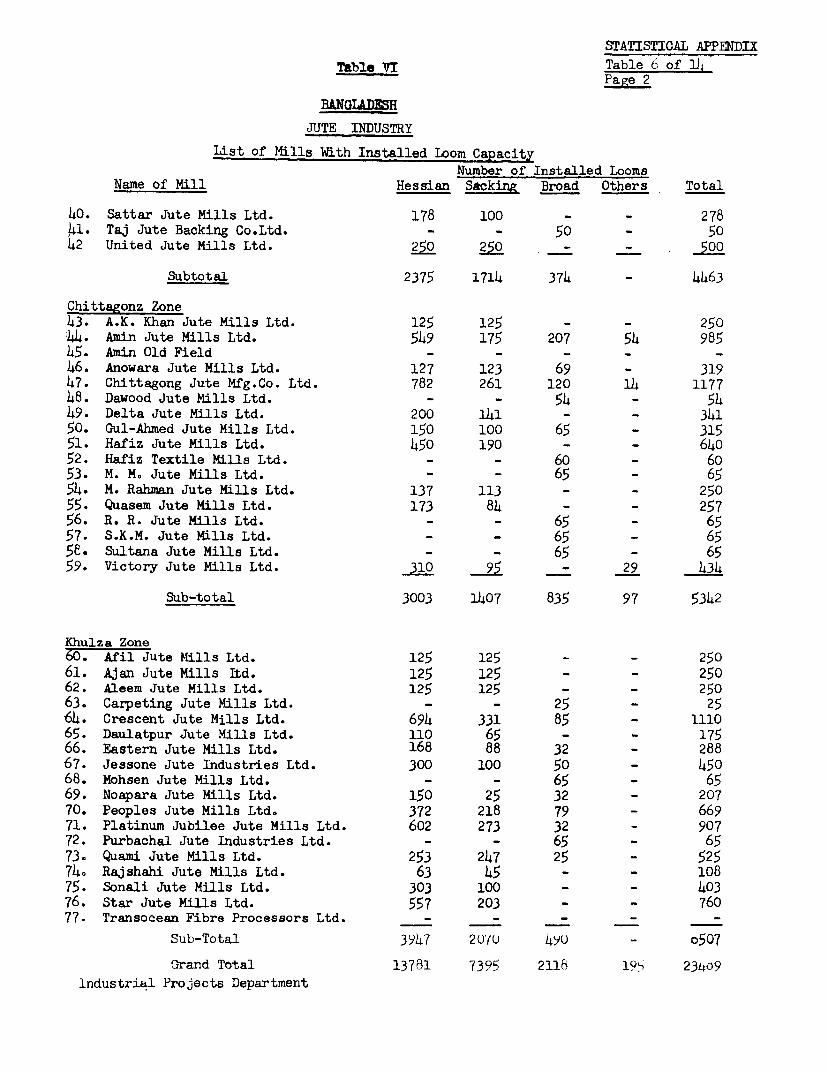

2.1 The jute goods industry now employs about 200,000 people in 77mills throughout Bangladesh and accounts for a little less than half of thetotal foreign exchange earnings of the country. All the mills are vestedin the Bangladesh Jute Industries Corporation (BJIC), under the jurisdictionof the Ministry of Jute. The biggest ten mills control 46.5% of the totalloomage; the biggest fifteen, 56.8%. As of 1974/75, official BJIC statisticsshow that there are a total of 23,289 looms in Bangladesh. Of the 77 mills,18 are integrated, 33 produce only hessian and/or sacking, 14 produce onlycarpet-backing cloth, and 2 produce other goods, such as cotton bagging,jute yarn, and plastic-backed jute bags. Six mills only spin yarn, andfour are not in operation.

2.2 A previous study 1/ had found that the larger integrated millsoperated at 5 to 10% lower cost than the smaller ones, as they could spreadoverhead costs over a larger output and purchase and utilize raw jute moreefficiently. Bangladesh mills have recorded wastes of 6 to 10% as opposedto 3 to 6% in mills of other producing countries.

2.3 Size, however, is only one determinant of efficiency. Otherfactors, such as managerial skills and supervision, affect productivitygreatly. With the mass exodus of non-Bengali jute mill managers and super-visory personnel, Bangladesh mills have suffered a great dearth of managerialand supervisory skills.

B. The Bangladesh Jute Industries Corporation

Organizational Structure

2.4 The Bangladesh Jute Industries Corporation was established afterindependence as a holding company to operate the nationalized Bangladeshjute industry. It has achieved a certain measure of decentralization incontrol of operations by allowing substantial autonomy to the Adamjeecomplex, and by subdividing the remaining mills into four zones as follows:20 in Dacca Zone I, 20 in Dacca Zone II, 17 in Chittagong Zone, and 18 inKhulna Zone. Each zonal office is headed by a zonal manager and staff formarketing, quality control, and technical functions. The corporation issimultaneousl) one of two divisions under the Ministry of Jute. As. theJute Industries Division, it deals with jute manufactures, while the other,the Jute Division, handles matters pertaining to raw jute. The Chairman

1/ IBRD, The World Jute Economy, July 12, 1973. (114a-BD)

- 9 -

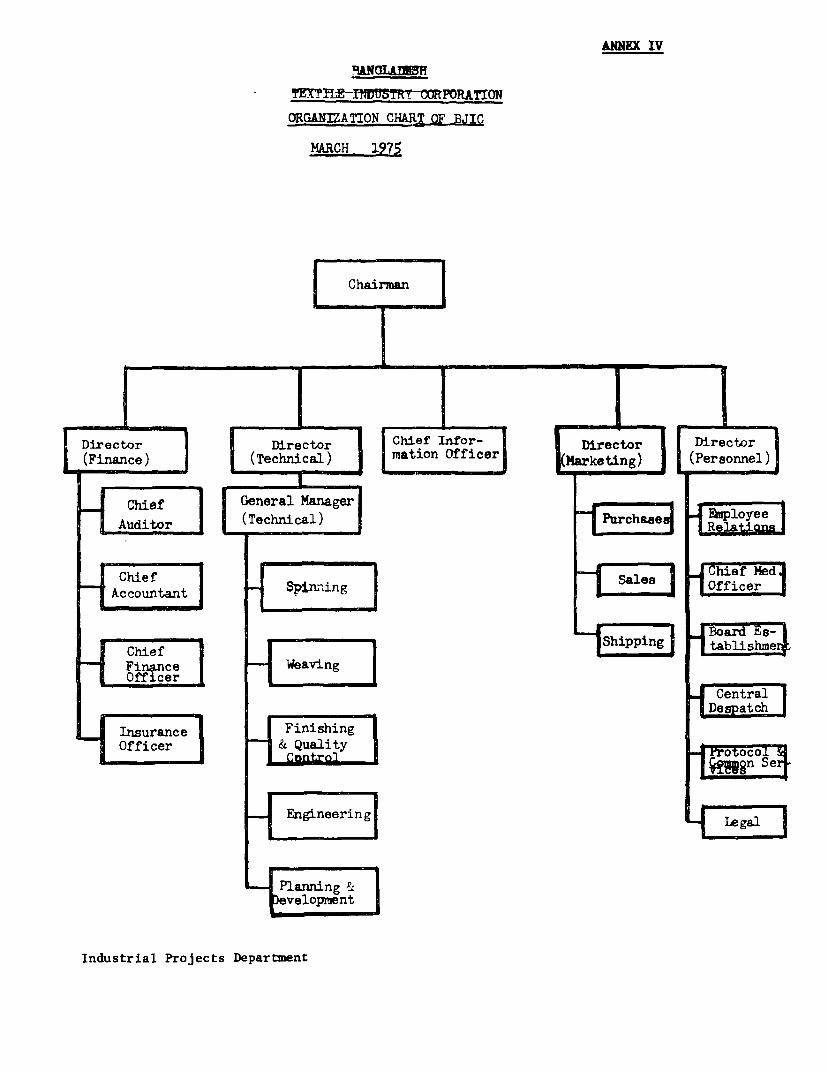

of the Corporation is concurrently Secretary of the Jute Industries Divisionand reports to the Minister of Jute. Under the Chairman are three keydirectors, Marketing, Technical, and Finance, and the newly created officeof Director of Quality Control. Annex IV gives the organization chart forthe Ministry of Jute. In the past, BJIC has acted au.onomously regarding theproduction and marketing of jute goods. However, BJIC must conform to Govern-ment policies regarding staffing, recruitment, and officer-level salaries.

Marketing and Production

2.5 Marketing has been centralized in the Corporation. Lack of adequatecommunication between Corporation headquarters and mills on one hand andbetween headquarters and end-users on the other have resulted in many problemsfor the jute goods industry; the mills have not been able to meet end-users'demand for specific products satisfactorily.

2.6 Prior to 1971 individual mills, through long-term relationshipswith their customers, took care of marketing their own production. Therewere incentives then for producing to meet market needs. Immediately follow-ing independence with the creation of the Bangladesh Jute Industries Corpora-tion, the links between individual mills and their respective customers weresevered. More recently, however, the Corporation has modified its marketingarrangements, adopting flexible procedures which are designed to attempt tomeet the requirements and preferences of individual buyers. A number ofthe large mills and groups of smaller ones have autonomy in sales. Ordersreceived directly by the Corporation are assigned, after consultation withthe buyers, to individual mills. Where buying is done through internationaltendering, as in the case of large contracts for sacking from governmentalagricultural marketing boards, the Corporation is responsible for submit-ting the bids. If it receives the contract, it assigns the order to one ormore mills depending upon the size. Nevertheless, the communication betweenthe Corporation and its constituent mills does continue to pose problems.Some of the mills are located in remote areas, accessible only with greatdifficulty, although efforts are being made to connect the Corporation withits mills by means of radio or telephone. But even if the Corporation hadperfect communications with its mills, it still would have to deal with theproblem of communication with its major customers in North America and thecountries of Western Europe. At this time, the Corporation is not adequatelyequipped to gather market information. The customers, more often than not,take the initiative in contacting the Corporation when they need Bangladeshjute goods. The Bangladesh jute industry thus stands at a disadvantagevis-a-vis the other jute manufacturers, who have their customer relationshipsand their representatives in major markets. For some importers, Bangladeshis the supplier of last resort, as when Calcutta mills were on strike in theearly part of the past two years.

- 10 -

Quality Control

2.7 A number of major importers in North America and Western Europe 1/have found that, despite the higher quality of its raw jute as compared tothat available in India, Bangladesh has not fully controlled the quality ofits exports. Commonly heard complaints are that weights do not conform tospecifications (either too light or too heavy, usually the latter), dimensionsdo not follow specifications (usually too narrow widths), and there are toomony weaving defects. Other complaints pertain to yard strength and evenness,and excessive oil content in the finished goods.

2.8 From the sample of mills visited, it became apparent that the lackof quality reliability can be attributed primarily to the lack of a properlyorganized quality control system. At present, each mill has personnel respon-sible for quality control, but their reporting relationships undermine theireffectiveness. The quality control officer reports directly to the produc-tion manager. This often creates occasions of conflict, and the qualitycontrol figures that are reported to the Bangladesh Jute Industries Corpora-tion often do not reflect the whole picture. While there are data in theforms submitted to the Corporation's Director for Quality Control that canbe cross-checked to provide accurate information, BJIC headquarters staffappear to suffer from limitations in their ability to use the qualitycontrol data submitted by the mills effectively. There are zonal qualitycontrol officers who make the rounds of mills to "spot-check" information.Too often, however, they are unable to achieve any significant results dueto the genuine reasons for poor quality: lack of trained personnel in bothproduction and quality control functions at the mills, inadequacies of produc-tion machinery and lack of equipment for testing quality.

CHAPTER III. ASSESSMENT OF PRODUCTION CAPABILITIES

A. Analysis of Productivity

Utilization of Capacity

3.1 As shown in the previous chapter, following the sharp decline inoutput at the time of independence, production of jute manufactures rosesteadily to reach a level of 500,000 tons in 1973/74; the rate of outputin mid-1974 was one of_the highest ever achieved, surpassed only by the1969/70 peak figure (Statistical Appendix Table 3). Nevertheless, this re-presents only slightly more than one-half of the actual installed capacity(Statistical Appendix Table 14).

1/ Interview data collected by the Bank mission in February-March, 1975.

- 11 -

3.2 With the accumulation of stocks by the end of 1974 as a result ofdecreased external demand, some cutback in output was undertaken. Most ofthe capacity for carpet backing was closed down, and there was some reduc-tion in the production of hessian; there was, however, an expansion in sackingoutput, and some mills shifted hessian looms to sacking manufacture.

3.3 For the purposes of determining the actual conditions of production,and the factors determining the utilization of capacity, visits were made toa sample of 17 mills of various sizes and characteristics, accounting forslightly more than half of installed capacity. For this sample, mill managersreported 80% of installed looms in operating condition; however, a large pro-portion of. these looms were in fact only intermittently used, due to break-downs and lack of timely repair: moreover, all of the weaving sections wereoperating two shifts, and less than half of the spinning facilities wereworking three shifts. These results are summarized as follows:

Production Performance of Jute Mills, July-December 1974

Percentage of Technical Overall Percentage ofInstalled Machinery Efficiency Efficiency Mills Running

Operation Utilized % % 3rd Shift

Spinning 81.0 59 48 43Weaving (overall) 80.3 53.5 43 None- Hessian 83.6 48.8 40.8- Sacking 85.9 56.9 48.8- C.B.C. 40.6 62.6 25.4

Overall efficiency is measured by relating actual output to total maximumpossible production, calculated by assuming use of installed capacity for thefull number of hours which have been planned for operation. Technicalefficiency measures only the utilization of equipment which is reported asoperating. The sample overall efficiency percentage, if applied to the totalinstalled capacity in all the mills, yields an output level slightly belowthat actually recorded, indicating that the level of utilization in the samplewas lower than that for the entire jute industry, but the difference is smallenough to not require modification of the mission's findings on factorsaffecting performance.

Factors Affecting Performance

3.4 The Bangladesh jute industry is relatively young. Most of theequipment was new at the time of installation, there being few instances ofsecond-hand machinery having been installed. Only a small part of the equip-ment park can be considered technologically obsolete. The major problem inthis regard is in the spinning process where some machinery currently in usehas become obsolete; moreover, the equipment manufacturer is no longer inproduction, cutting off the supply of spare parts and further encouraginggradual reduction in use.

- 12 -

3.5 Practically all the jute mills were constructed for balanced produc-tion i.e. equal number of shifts in all departments. Nevertheless, from areview of the machine park in a number of mills it appeared that there areinstances in which spinning capacity was inadequate for balanced production.The problem is made more difficult by the obsolescence of some spinningmachinery (noted above) and the difficulties experienced by a large numberof mills in maintaining their preparation and spinning equipment. Thecustomary practice at present, therefore, is to operate weaving sections on atwo shift basis but some spinning departments have to work for three shifts,in order to maintain an adequate flow of yarn to the looms. Only 18 of the77 mills have an integrated product-mix, including hessian, sacking and carpetbacking, while 14 mills produce only carpet backing. Integrated productionpermits more efficient use of raw jute through allocation of the better qualitygrades to carpet backing and the poorer to sacking.

3.6 Immediately after independence the purchase of jute for use by themills had to be cleared through BJIC, a procedure which delayed transactions;subsequently the situation was eased somewhat by giving this authority tozonal offices. Currently mills are provided with purchasing autonomy. Ahigh proportion of the raw jute was obtained through the four marketing cor-porations, partly because the Corporation would finance these purchases andmany mills experienced working capital shortage. In these instances millsreceived their shipment from central terminals and were unable to controlthe quality, having to accept whatever was delivered to them. Some of theseshipments were of inferior quality or actually damaged. Recent efforts bythe Government to improve the functioning of the jute marketing corporationshave had beneficial results; not only has there been some reduction in theexcessive spread between farmgate and millgate prices but there has been amarked improvement in quality. (See Annex I.)

3.7 The tight financial position faced by practically all the-millsforced them to reduce their inventories of raw jute to minimum levels; butsome mills have reduced inventories below prudent levels. Raw jute requiresmaturing in batching oil for a period of about 10 days. In a number ofmills raw jute was found to be entering preparation for spinning withouthaving matured for the required time, and the explanation given was thatsufficient finance to permit necessary raw jute inventories had not beenavailable.

3.8 Spare Parts. The problem of spare parts supply is one of the mostcomplex faced b the industry, and perhaps the most critical productionbottleneck, requiring urgent attention. While most mill managers attributeto the shortage of spare parts the principal blame for continued low levelsof production and quality defects in output, there is actually great varietyin the manner in which the problem manifests itself in the different mills.One of the major factors underlying high spare parts needs is the almost totallack of planned repair and maintenance programs in the individual mills.Based on visual observation in the sample mills, perhaps as much as 40% ofcurrent estimated spare parts requirements are wasted in the absence ofadequate preventive maintenance programs which inter alia involve systematicreplacement of parts subject to wear (so-called "consumables").

- 13 -

3.9 A number of mills have extensive workshop facilities and can anddo produce a substantial portion of their spare parts needs. For example,the Adamjee complex, which accounts for almost 15% of the total installedloomage in the country, has equipment for casting, forging and machining;it produces a number of consumables for its own use which are normallypurchased from engineering enterprises manufacturing these items in largelots. On the other hand many mills have rather ' mited facilities andhave to rely on neighboring workshops for emergency repairs when major break-downs occur.

3.10 BJIC has attempted to centralize imports and distribution ofcertain spare parts (including.some locally made) which are commonly usedand most often replaced through the regional offices. This arrangement hasnot worked efficiently, mainly due to the lack of technical expertise of thestaff involved and the lack of established criteria and specification guidesfor purchasing. For example, among locally produced items the Corporationhas chosen to buy certain rubber and leather belting at slightly lower pricesthan competing products, even though the latter are considerably superior.in quality, last longer and operate more efficiently. Recently, mills havebeen given mDre autonomy in their spare parts purchasing; they are also beingpermitted to import needed spare parts through the foreign wage earners'scheme. 1/

3.11 In May 1974, a special working group within the M-finistry of Indus-tries met to examine the-possibility of expanding the production of spareparts for key industries such as jute, textile and sugar. Participating wererepresentatives of these branches as well as of the Bangladesh Engineeringand Shipbuilding Corporation which controls a number of enterprises whichare producing or have the capabilitv to produce both spare parts and certainspecific pieces of equipment used in those different activities. The groupalso made a survey of existing facilities in the private sector. It identi-fied a number of spare parts now imported which could be produced domestically;it recommended that steps be taken to expand. facilities for such manufacturebut did not suggest any specific action. No follow-up to this report hasyet been undertaken.

3.12 W4hile there are obviously great variations in the overall conditionsof plant and equipment in the mills, the general situation in the preparingand spinning sections is extremely poor, with much equipment standing idle.As noted previously these sections often are working three shifts in order toprovide sufficient yarn for the weaving sections to operate two shifts.Under certain conditions, this could be an efficient arrangement to producea given amount of yarn while minimizing spare part expenditures. But inmost of the mills visited, this was not the case. Deficiencies in thecarding, drawing and spinning operations resulted in poor quality of

l/ Under this system, Bengali citizens working abroad are permitted toremit their earnings in the form of specified goods.

- 14 -

yarn, which in turn led to weaving defects and slowed down weaving operations.More detailed comments on plant and equipment operating conditions areprovided in Annex II.

3.13 It was pointed out earlier in the chapter on Bangladesh exportperformance that quality problems have been affecting its sales. One meansto reduce defects in goods to be shipped is 100% visual inspection and manualrepair of damage. Among the carpet backing mills, this requires specialarrangements. Two of the mills visited have established this system; itappears that no other carpet backing mills follow the practice. For hessianand sacking, this is, in principle, done during one of the final stages ofprocessing; in a number of mills visited insufficient importance was attachedto this aspect by supervisors.

3.14 Labor Supply. Prior to independence a large proportion of thehighest skilled labor and the supervisory staff known as Sardars were non-Bengali, and many of them left during and immediately after the hostilities.At the mill level, attempts have been made to identify from among the remain-ing Bengali staff those with potential for higher responsibilities; littleformal training was provided for this purpose and the staff have had to learnon the job. A training center at Kaptai, operated with Swedish technicalassistance, has recently provided some technical training but the numbers ofstaff involved is small relative to needs.

3.15 As regards the supply of semi-skilled or unskilled labor, Bangladeshuses the traditional system found in the sub-continent of permanent workerssupplemented by occasional laborers (or badlis) who take up posts only whenthe former are absent. Base salaries are set by the Government within theoverall wage policy for the economy. About 60% of the working force areon a piecework basis and a system of performance incentives has been estab-lished; however, under present operating conditions the minimum output levelrequired before the bonuses are paid has rarely been exceeded and the systemhas been ineffective. Mill managers have expressed major concern with theproblem of absenteeism particularly during planting and harvesting seasonswhen many permanent workers as well as badlis leave to work on farms wherethey are able to earn as much as twice what the mills can pay. At suchtimes, some mills have had to reduce the nmtmber of looms in operation. Inspite of this, even a casual inspection of individual mills gives the observerthe impression of a surplus of labor on the site. Data from the mills visitedindicate an average of 3.7 workers per operating loom for two shifts ascompared to the generally accepted norm of three workers.

3.16 While labor unrest was a source of considerable disruption in produc-tion in the first years after independence, these difficulties have been easedconsiderably since early 1974.

3.17 Management. At the time of independence, 44 of the 77 mills currentlyunder public ownership were owned by non-Bengalis; these included practicallyall the larger establishments. Most of the top-level management, administ-rative and technical staffs of these mills were also non-Bengali and left

- 15 -

the country. In addition, when the remaining mills under Bengali ownershipwere nationalized many management personnel in those enterprises gave uptheir posts. Thus one of the major problems facing the Government was toidentify and put into place senior staff to operate the mills. On the otherhand, it would appear that a number of qualified personnel were not permittedto remain in their posts or were ignored as a result of political considera-tions. Moreover, inadequate salaries and lack of financial incentives formanagement discouraged some competent executives and technicians from con-tinuing in or taking responsible posts in the industry. Many of the currentmanagement-level staff had rather extensive experience in production butlimited experience in other aspects related to plant management. Thesedifficulties were compounded by the excessive degree of centralizationadopted by BJIC which hindered day-to-day operations of the mills. In recog-nition of this, some attempt at decentralization was introduced with theestablishment of four zonal offices in 1973. More recently the Adamjee millcomplex was given functional autonomy, and some autonomy in selected opera-tional areas was given to other mills as well.

3.18 There is, however, one aspect of this'problem whichi is particularlyimportant in analyzing production performance, which has to do with productionplanning. In principle the mill managers are directly responsible to BJICthrough the regional offices and receive policy guidelines through thischannel. In attempting to determine how production schedules are established,no clear picture emerges from the interviews undertaken at both the mill andcorporation level. WIhile many mills claim to produce only on order from theCorporation, it is evident that they had rejected requests to produce certainnon-standard items for which BJIC was receiving orders and continued insteadto produce other items for which orders had fallen off. In the case of carpetbacking, the growing stock during the second half of 1974 led the Corporationto order shut down of more than half the looms involved in its production.Failure at the mill level to adjust production to market developments is alsoevident in the continued growth of stocks of heavier types of hessian cloth.

3.19 It would appear that under the present system, the performance ofmill managers is being judged on the basis of volume of output, expressedin tonnage rather than yardage; hence the incentive to produce heavier items.With cost-price relationships distorted on account of an artificially main-tained exchange rate (up to May last), it was not possible to use anyconcept of "profitability" or production surplus as a guide to productionplanning decisions; and the only constraint to maintaining output appearedto be the availability of credit to finance production. In view of thechanged circumstances following devaluation of the Taka in May 1975, itshould be possible for BJIC to develop a more rational system of measuringperformance, and directing the production schedules of mills to maximizeprofit.

B. Analysis of Structure of Costs

3.20 Data on costs of production are limited, making it difficult todetermine the impact of the various elements on the competitive position of

- 16 -

individual mills. BJIC, with technical assistance from the UK, is attemptingto improve the accounting systems of the individual mills and develop necessarvinformation for cost control. (For a detailed discussion of financial organi-zation and problems, see paras. 3.25-3.28). Standardized procedures are beingdeveloped for apportioning costs among the major product groupings in arational manner.

3.21 Statistical Appendix Table 11 contains data on product costs for alarge integrated mill for three monthly periods, late-1973, mid-1974 andearly 1975. This table demonstrates the impact of high raw jute prices atthe end of 1974 and early 1975 when there was considerable uncertainty overits supply. Moreover, the high cost of production for carpet-backing for1975 reflects the verv low utilization of capacity of equipment for producingthis item at that time when all the carpet-backing mills had been ordered tocut-back or stop this production.

3.22 Analysis of these details must be undertaken with some caution,particularly for any international comparisons, in view of the arbitraryallocation of many items among different products. In March 1975, theBangladesh non-jute (conversion) costs for hessian were estimated at 3500 to3700 Takas per ton, slightly higher for carpet-backing and 2000 to 2200Taka/ton for sacking. The principal items were distributed as follows:

Principal Components of Jute Manufacturing Costs(March 1975)

Hessian Sacking Carpet-Backing----- (in percentages)---------------

Salaries and Wages 48 48 39Spare Parts 16 17 10Power 8 8 5Interest 10 10 19Depreciation 7 3 14All other Conversion Costs 11 14 14

Information available from a major competitor indicates that its conversioncosts for hessian were 30 to 35% below those in Bangladesh but only 10 to 15%in the cases of both sacking and carpet backing (at the prevailing exchangerates). In absolute terms, all of the major cost categories other than laborcosts were hi' :er in Bangladesh than in competing countries, reflecting essen-tially the low level of utilization of equipment in the former. In addition,Bangladesh has higher spare parts consumption for the reasons indicatedearlier, and considerably higher interest charges, reflecting the need toservice the loans which finance the accumulated deficits of the last fewyears.

- 17 -

3.23 Labor costs for the three products were roughly the same in monetarvterms in the two countries; for the competitor, however, they represent amuch higher proportion of conversion costs. While outnut per worker isnoticeably lower in Bangladesh, wage levels appear .lso to be considerablylower.

3.24 Raw jute costs in Bangladesh were substantially higher than incompeting countries. A major factor has been the gap between farmgate andmillgate prices in Bangladesh, reflecting the inefficient marketing system.In addition, the mills in Bangladesh have higher raw jute consumption per tonof finished product, of the order of 6 to 10% depending upon product, ascompared to 3 to 6% in other countries manufacturing jute.

C. Financial Condition of -the MIills

3.25 The jute mills and BJIC have experienced serious financial diffi-culties since independence. During the period of strife prior to independence,a large proportion of the liquid assets of these enterprises were transferredto banks outside East Pakistan; moreover some of the owners took loans againsttheir fixed assets and transferred these funds to other areas. Since thattime, the liquidity position of the mills has been exacerbated by an almostunbroken chain of operating deficits the full extent of which is difficultto estimate because of inadequate data. For the two fiscal years, 1972/73and 1973/74, for which preliminary consolidated profit and loss statementsare available, the aggregate loss was estimated at over 650 million Takas,equivalent to more than 20% of total sales value of 3,200 million Takas(Statistical Appendix Table 10). The cash flow deficit for the two years isprovisionally estimated at 500 million Takas. For 1974/75, the preliminaryestimate of the deficit is 570 million Takas, with a cash flow deficit ofthe order of 500 million Takas. For 1973/74, the Government extended a sub-sidy of 75 million Takas part of wlhich was actually paid in the 1974/75fiscal year; in the second half of 1974/75, three subsidy payments (inFebruary, April and June) were made to the Corporation totalling some 500million Takas. The uncovered deficits continue to be financed throughcommercial bank credit. Earlier, in an attempt to ease the financial strainon the industry, the Government in June 1973 required commercial banks toconvert a portion of their loans to the jute industry into 20 year debentureswith five years grace. The debentures bear interest at a rate of 4.5% perannum. At the time, the amount of the debentures was designed to be equivalentto the excess of short-term bank borrowings over current assets of the industry.Also in June 1973 the Government declared a moratorium on repayments by thejute industry on long-term loans outstanding to the two official developmentbanks in Bangladesh.

3.26 Prior to the May 1975 devaluation, the accumulated deficit and thefinancial implications of the growing inventories of unsold goods as a conse-quence of the fall in export demand were leading to a chaotic situation.A large number of mills had exceeded the credit limits fixed for them bythe banks, which were limited to 80% of the value of finished goods inventories

- 18 -

or 10 million Takas per 250 looms, whichever was less. BJIC was negotiatingto raise the limits. In the meantime a number of mills had had to limit rawjute purchases, and to delay lifting even essential imported spare parts fromcustoms. Their huge accumulated debts were contributing to the already highcosts of production, creating a vicious circle of increasing operationaldeficit. As noted in the analysis of costs of production, interest ratecharges were accounting for 10 to as much as 20% of manufacturing costs(excluding raw material costs) as compared to 3 to 5% expected under normalconditions; the situation had further deteriorated when commercial short-terminterest rates were raised from 9 to 12% as of July 1, 1974.

3.27 At present, virtually all the mills prepare for BJIC data on theiroperating results on a monthly basis, separately for hessian, sacking andcarpet backing. Each quarter, and annually, the Corporation prepares anaggregated profit and loss statement. The aggregated statements for 1972/73and 1973/74 for mills accounting for 97% of output are shown in StatisticalAppendix Table 10. Although the mills normally prepare annual operatingbudgets, few mills apparently maintain periodic reviews of the actual de-velopment of financial elements. As a consequence, they are unable to re-act with sufficient anticipation to many events which could be foreseen ifproper financial planning were undertaken.

3.28 A full evaluation of the financial position of the industry ishampered by the lack of proper accounting data, primarily a result of insuffi-cient trained personnel capable of keeping accounts. In addition, becauseof the disruption at the time of independence, there are serious gaps in thedata on asset evaluation. Not all of the mills have yet been able to prepareproper balance sheets; by March 1975 BJIC had received only 57 balance sheetsfor the year ended June 30, 1974. Since mills have not yet taken completeinventories of the assets they show on their books, asset values are likelyto be overstated because of damage and other losses suffered during theindependence struggle. BJIC is providing direction in undertaking the taskof proper asset evaluation and corrected statements are expected shortly.

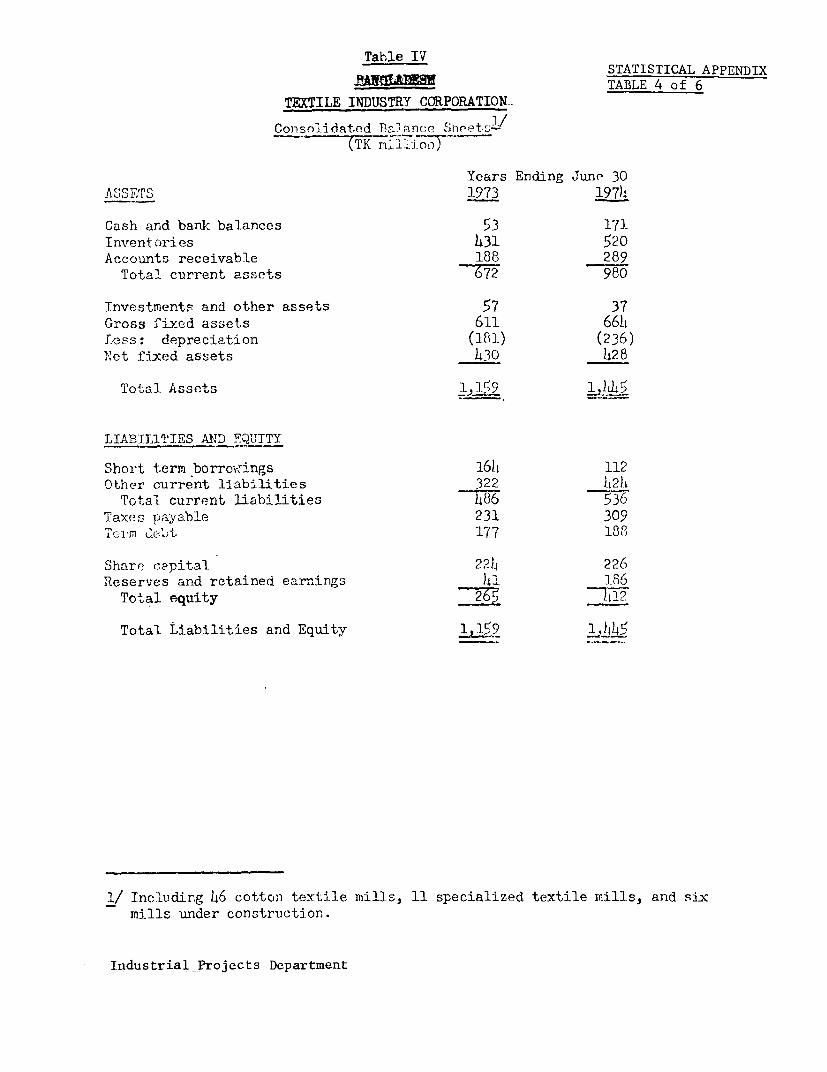

3.29 The consolidated balance sheets for 1973/74, based on existingdata for 57 mills representing 77% of production, is shown in StatisticalAppendix Table 9. The following summary provides an indication of thecurrent situation:

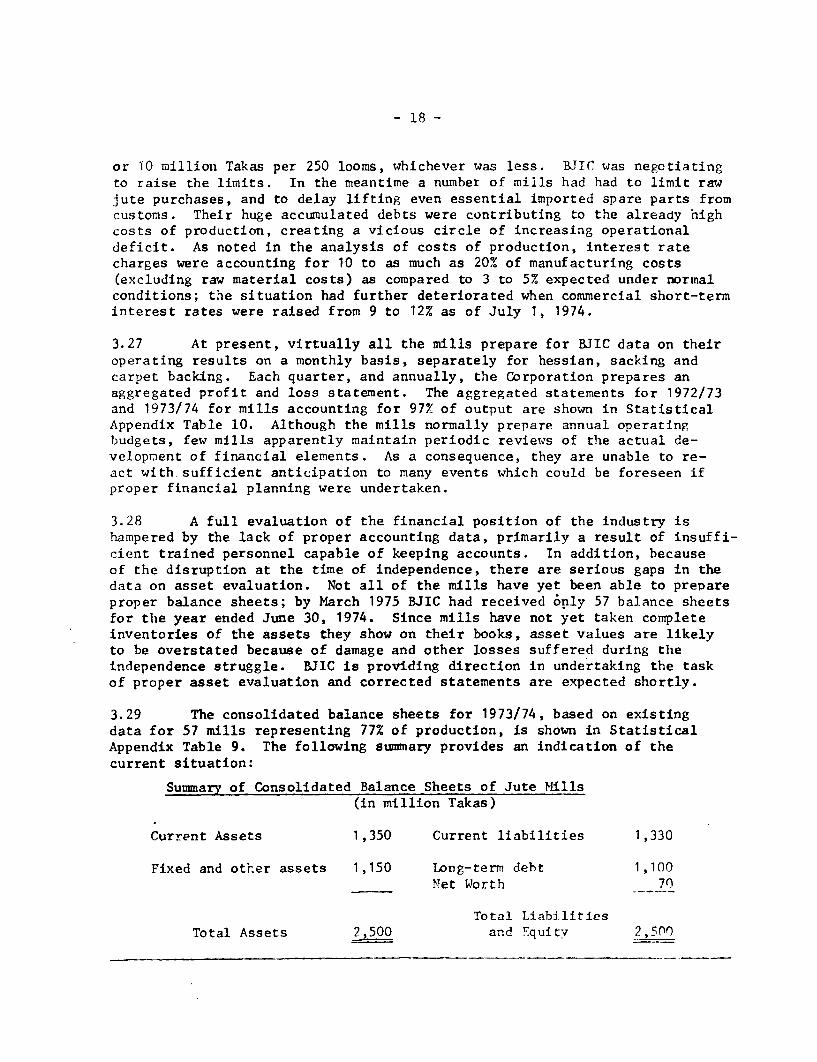

Summary of Consolidated Balance Sheets of Jute Mills(in million Takas)

Current Assets 1,350 Current liabilities 1,330

Fixed and other assets 1,150 Long-term debt 1,100Net Worth 70

Total LiabilitiesTotal Assets 2,500 and Equitv 2,500

- 19 -

D. Raw Material Supplies

3.30 As the principal source of the world's supply of raw jute, Bangladeshhas had few problems in providing sufficient raw material for development ofits own manufacturing industry. In fact, as mentioned in Chapter I, thestrategy of the previous (East Pakistan) as well as the current Governmenthas been to raise the percentage of locally processed jute. Even at peakmanufacturing activity (in 1969/70) the local mills consumed less than halfthe recorded crop for that year. Nevertheless the policies adopted towardjute cultivation and the minimum prices for raw jute established by govern-ment authorities have played a major role in determining the prices whichmills have had to pay for their requirements. These in turn are closelylinked to other elements of basic economic policy, principally the policyfor rice prices. The jute-rice relationship, current jute cultivation policiesand the role of government institutions dealing with these matters are reviewedin detail in Annex I.