ihs global economics & country risk conference · pdf fileihs global economics &...

TRANSCRIPT

© 2014 IHS

Presentation

ihs.com

IHS

Evolution in China’s economy, regions, and politics

IHS Global Economics & Country Risk Conference

Todd C. Lee, Senior Director, IHS, +1 781 301 9026, [email protected] Brian Jackson, Senior Economist, IHS, +86 10 6533 4567, [email protected] Chris Christopher, Director, IHS, +1 781 301 9113, [email protected] David Yang, Principal Analyst, IHS, +1 703 236 2403, [email protected]

11 November 2014

ECONOMICS & COUNTRY RISK

© 2014 IHS 2

Agenda Evolution in China’s Economy, Regions, and Politics / November 2014

Introduction Todd C. Lee, Senior Director, Global Economics

Economic evolution Brian Jackson, Senior Economist, Asia Economics

Regional development

Chris Christopher, Director, Global Consumer Service

Political outlook David Yang, Principal Analyst, Asia Country Risk

Q&A

© 2014 IHS © 2014 IHS 3

Introduction

Todd C. Lee

© 2014 IHS

0

2000

4000

6000

8000

10000

12000

14000

16000

0

2

4

6

8

10

12

14

16

1980 1990 2000 2010

Real per capita GDP growth (annual % ch, left) Real per capita GDP level (1990 PPP$, right)

China’s economic development since economic reform began

Source: Maddison (2013)

© 2014 IHS 5

China’s economic development during its march to modernity in 30-year spans

0

200

400

600

800

1000

-1.0-0.8-0.6-0.4-0.20.00.20.40.60.81.0

0 10 20 30

0

200

400

600

800

1000

-1.0-0.8-0.6-0.4-0.20.00.20.40.60.81.0

0 10 20 30

0

200

400

600

800

1000

-1.0-0.8-0.6-0.4-0.20.00.20.40.60.81.0

0 10 20 30

0

200

400

600

800

1000

1200

1400

1600

-20

-15

-10

-5

0

5

10

15

20

0 10 20 30

0

200

400

600

800

1000

1200

1400

1600

-20

-15

-10

-5

0

5

10

15

20

0 10 20 30

0

5000

10000

15000

20000

-20

-15

-10

-5

0

5

10

15

20

0 10 20 30

Real per capita GDP growth (% ch, left axis) Per capita GDP level (1990 PPP USD, right axis)

1830-1860 1860-1890 1890-1920

1920-1950 1950-1980 1980-2010

Opium War (Hong Kong ceded to Britain) Taiping Rebellion

1st Sino-Japanese War (Taiwan ceded to Japan)

Qing Dynasty ends

Warlord Era

Warlord Era

Nanjing Gov.

2nd Sino-Japanese War (WWII)

Birth of PRC

Great Leap

Forward

Culture Revolution

Market Reform

Source: Maddison (2013)

© 2014 IHS © 2014 IHS 6

Economic evolution

Brian Jackson

© 2014 IHS 7

Economic restructuring

© 2014 IHS 8

Over three decades China experienced radical changes in the composition of production and income

© 2014 IHS 9

Massive changes in China’s domestic economy mirrored by important shifts globally

© 2014 IHS 10

Ownership and efficiency

© 2014 IHS 11

Changing ownership and incentives in the economy played a key role in the economic boom

© 2014 IHS 12

…but the shift towards a private economy is not strictly one way

© 2014 IHS 13

SOEs remain major players in some sectors, despite clear inefficiencies

© 2014 IHS 14

Economic reform and growth

© 2014 IHS

Reform: The speed we’re used to

15

Reform Year

1978 Third Plenum

Opening for foreign investment projects Duel Track Currency Exchange Town-Village Enterprise

1978

Sino-Foreign Equity Joint Ventures Law 1979

Special Economic Zones: Shantou, Shenzhen, Xiamen, Zhuhai 1980

Household Responsibility Reform (rural farm reform) 1981

14 coastal cities and three provinces designated as open to foreign investment 1984

General Principles of Civil Law: legal support for private market activity 1986

1993 Third Plenum

Exchange rate unification and reform Approved FDI permitted nationwide

1994

Fiscal reform 1995

Central bank reform 1995

Industrial state owned enterprise reform 1995

Price Law - price reform 1997

WTO entry 2001

© 2014 IHS

Reform: The speed we’re seeing today

16

Reform Year

2013 Third Plenum

Finance •Shanghai FTZ foreign deposit interest rate liberalization •Shanghai FTZ cross-border Chinese Yuan (CNY) payment services •Private banking trial •Deposit insurance •Interest rate liberalization

2014 2014 2014 2015(F) 2016-2017(F)

Monopolies and market competition •National and regional SOE reform plans issued •Simplified business registration and financial barriers to entrepreneurship •Red tape cutting – 500+ central approvals canceled or devolved •Increasing competition in service sectors (bank cards, express delivery, hospitals…)

2014 2014 2013-… 2014-…

Foreign investment •SH FTZ negative investment list revisions •12 new FTZ feasibility studies launched, 3 approved, more in pipeline •US-China Bilateral Investment Treaty negotiations begin •Provinces instructed to prepare negative investment lists

Annual review 2014-2015 2014 2014

Government, society and the environment Budget Law revision Environmental Law revision Hukou reform plan

2014 2014 2014

© 2014 IHS

Outlook and challenges

Indicator 1984 → 2013 2014 → 2043

GDP growth (average) 10.1% 5.4%

Services/GDP 25% → 46% → 60%

GDP per capita (USD) 300 → 6,700 → 65,000

Urban population (share) 23% → 53.7% → 75%

Exports (share of world) 1% → 12% → 14%

Imports (share of world) 1% → 10% → 14%

17

• Near-medium term challenges are numerous and substantial, but not insurmountable.

• Setbacks have occurred and will occur in some areas.

• Much implementation remains to be seen – but policy momentum is consistent with a rigorous decade-long reform agenda.

© 2014 IHS © 2014 IHS 18

Regional development

Chris Christopher

© 2014 IHS

China: Regional classification map

19

Northeast Central

Coast

West

© 2014 IHS

Coastal region consumer spending fuels global consumption

0

5

10

15

20

25

2000 2005 2010 2015 2020 2025 2030

Coast Central Northeast West NationalSource: NBS, IHS

20

Share of the China regional consumer spending in global consumption

© 2014 IHS

Sources of growth of global GDP and consumer spending - production and consumption balancing

(Percent of world GDP and consumption, US dollars)

GDP Consumer Spending

2004 2014 2024 2004 2014 2024

U.S. 28 22 19 33 27 23

India 2 3 6 2 3 6

China 4 14 22 3 8 15

Coast 3 8 12 2 5 8

Central 1 4 6 1 2 4

Northeast 1 2 3 0 1 2

West 0 1 2 0 1 2

Western Europe 31 23 18 30 24 19

21

© 2014 IHS

Coastal provinces’ growth slowing down, inner regions development picking up

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8

1980 1985 1990 1995 2000 2005 2010 2015 2020

Coast Central Northeast West

Real GDP per capita index (National average = 1.0)

Source: NBS, IHS

GDP per capita index (National average = 1.0)

Source: NBS, IHS

22

© 2014 IHS

China’s regions over the 1980-2013 period

0

4

8

12

16

20

0 5 10 15 20 25 30 35 40 45 50 55

Real

GDP

per

capi

ta g

row

th, C

AGR

(Per

cent

)

Real GDP Per capita (Thousand 2000 Yuan)

Source: NBS, IHS

Real GDP per capita growth vs Real GDP per capita

2000, 2000-09 1980, 1980-1989 2007, 2007-13 1990, 1990-1999

23

© 2014 IHS 24

China’s population by region

37.6%

35.2%

12.7%

14.6%

Coast Central Northeast West

Total population (1996)

Source: NBS, IHS

41.5%

32.1%

12.2%

14.2%

Coast Central Northeast West

Total population (2013)

Source: NBS, IHS

© 2014 IHS 25

China’s GDP by region

56.6% 24.5%

10.3%

8.6%

Coast Central Northeast West

Real GDP (1996)

Source: NBS, IHS

57.7% 24.1%

10.6%

7.6%

Coast Central Northeast West

Real GDP (2013)

Source: NBS, IHS

© 2014 IHS 26

China’s private consumption by region

50.7%

27.9%

10.7%

10.7%

Coast Central Northeast West

Real private consumption (1996)

Source: NBS, IHS

57.0% 24.6%

9.4%

9.0%

Coast Central Northeast West

Real private consumption (2013)

Source: NBS, IHS

© 2014 IHS 27

Coastal region no longer leads growth, the Western region has the most dynamic consumer markets

0

2

4

6

8

10

12

14

16

1995-99 2000-04 2005-09 2010-14 2015-20

Coast Central NortheastWest National

GDP per capita (Thousand yen)

Source: NBS, IHS

Real GDP per capita, compound annual growth rate Real GDP per capita, CAGR (percent)

Source: NBS, IHS

0

2

4

6

8

10

12

14

16

1995-99 2000-04 2005-09 2010-14 2015-20

Coast Central NortheastWest National

GDP per capita (Thousand yen)

Source: NBS, IHS

Real consumption per capita, compound annual GDP per capita (Thousand yen)

Source: NBS, IHS

Real GDP per capita, compound annual growth rate Real consumption per capita, CAGR

Source: NBS, IHS

© 2014 IHS 28

Urban population – central region growing faster

0

50

100

150

200

250

300

350

400

450

2005 2010 2015 2020 2025 2030

Coast CentralNortheast West

Urban population

Source: NBS, IHS

Urban population (millions)

Source: NBS, IHS

20

30

40

50

60

70

80

2005 2010 2015 2020 2025 2030

Coast CentralNortheast WestNational

Urbanization rate (percent)

Source: NBS, IHS

Urbanization rate (percent)

Source: NBS, IHS

© 2014 IHS

Over three decades, China experienced radical changes in the composition of income

29

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

1978 1983 1988 1993 1998 2003 2008 2013

Rural income Urban income

Rising per capita income and inequality

Source: NBS, Chen, Jiandong (2010), IHS

Nom

inal

USD

Rising per capita income and inequality

Source: NBS, IHS

© 2014 IHS

Consumer spending to GDP is picking up across all regions

20

25

30

35

40

45

50

55

60

1996 1999 2002 2005 2008 2011 2014 2017 2020 2023 2026 2029

Coast Central Northeast West National

Private consumption to GDP (percent)

Source: NBS, IHS

Private consumption to GDP (percent)

Source: NBS, IHS

30

© 2014 IHS

Coastal regions still on top in terms of consumption per capita levels

31

0

4

8

12

16

20

1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

Coast Central Northeast West National

Real Consumption per capita (Thousand 2000 Yuan)

Source: NBS, IHS

Real private consumption per capita (Thousand 2000 Yuan)

Source: NBS, IHS

© 2014 IHS © 2014 IHS 32

Political outlook

David Yang

© 2014 IHS

Overview: Domestic politics

• Pres. Xi Jinping has achieved high centralization of power

• Legal reforms emphasized at recent 4th Plenum • Administrative reforms to reduce local gov’t interference

• But local leaders have other levers to indirectly influence judges

• Anti-corruption campaign still ongoing • Instrument to remove obstacles to further economic reforms?

33

© 2014 IHS

Overview: External relations

• High-level dialogues with Japan resumed after 4-yr gap

• Military exchanges with Vietnam resumed after May standoff

• Current “One Belt, One Road” campaign - response to U.S. pivot?

34

© 2014 IHS

The anti-corruption campaign: Targeting both “Tigers” & “Flies”

• Current anti-corruption drive unprecedented in reach • Former Politburo Standing Committee member Zhou Yongkang

• Former Central Military Commission Deputy Chair Xu Caihou

35

0

5

10

15

20

25

30

0

10000

20000

30000

40000

50000

60000

2003 2005 2007 2009 2011 2013

Total Provincial/Ministerial level (RHS)

Figure 1: Number of officials formally investigated for corruption

Source: IHS

Notes: 2014 based on reports through August 2014.

• Number of senior officials censured in the first 20 months of Xi’s tenure more than the previous five years combined

© 2014 IHS

The anti-corruption campaign: Effect on businesses

• Some evidence that intensity of crackdown negatively correlated with GDP growth & FDI at provincial level

• Crackdown has slowed project approvals

• Reduced flow of funds has depressed real estate prices

36

2%

3%

4%

5%

6%

7%

8%

9%

10%

11%

12%

10 20 30 40 50 60

Figure 2: GDP growth vs. investigation rate by province

Source: IHS

Officials investigated per million

2014

Q1

GD

P gr

owth

rate

• IHS expects negative impact of the campaign to be only temporary

© 2014 IHS

The anti-corruption campaign: Outlook

• Current campaign will continue until at least 2017

• Intensity may slacken over the next 3 years

• We do not expect the current campaign to significantly reduce corruption risks beyond the next three years • Xi’s position will be unassailable after the next Party Congress

37

© 2014 IHS

The anti-monopoly campaign: Selective enforcement against MNCs?

• Multiple sectors affected since 2013

• Jan. 2013: Samsung and 5 other LCD makers fined $57M

• Aug. 2013: 5 foreign & 1 local baby formula makers fined $110M

• Nov. 2013: Qualcomm investigation began, w/ potential $1B fine

• May 2014: 5 foreign optometric makers fined $3.1M

• Jul. 2014: Microsoft offices raided in anti-trust probe

• Aug. 2014: Audi, Chrysler, Mercedes-Benz & Toyota investigated

38

© 2014 IHS

The anti-monopoly campaign: Selective enforcement against MNCs?

• Some domestic firms have been investigated

• Luxury distillers Maotai & Wuliangye

• Jewelry retailers such as Laofengxiang

• China Unicom & China Telecom (ongoing since 2011)

• Automaker FAW Group (ongoing since 2012)

• Major SOEs more likely to avoid fines through negotiation

• Similar enforcement bias in U.S. Sherman Act cases?

39

© 2014 IHS

The anti-monopoly campaign: Outlook

• Cases against foreign firms do not always benefit domestic producers who compete on price

• Sectoral struggles may be more important (e.g. insurers vs. auto-parts makers)

• Gov’t more sensitive to perceptions of selective enforcement

• MNCs that sell directly to consumers remain vulnerable LT

40

© 2014 IHS

The “Occupy Central” protests: Key issues

• Basic framework laid down by PRC National People’s Congress on 31 August:

• HKSAR Chief Executive to be elected by universal suffrage in 2017

• 2 – 3 candidates to be nominated by pro-Beijing nominating committee

• Opposition Pan-Democrats demand direct nominations

• But nominating committee is stipulated under Basic Law

• NPC framework must be adopted by HK Legislative Council

41

© 2014 IHS

The “Occupy Central” protests: Key players

The protests involve a range of groups, united in their dissatisfaction with the NPC framework, but unclear on specific demands:

• Student groups (e.g. Hong Kong Federation of Students, Scholarism) form the core

• Opposition parties have not played a leadership role

• Labor union participation is minimal

• A number of fringe groups are likely to be more militant

42

© 2014 IHS

The “Occupy Central” protests: Key players

• Student groups such as the Hong Kong Federation of Students & Scholarism form the core of the protests

• Opposition parties support the protests, but have not played a leadership role

• The participation of labour unions has been minimal

• A number of fringe groups are likely to be more militant

• Groups are united in their dissatisfaction with the NPC framework, but unclear on their specific demands

43

© 2014 IHS 44

The “Occupy Central” protests: Locations and numbers Protest sites in Hong Kong – November 2014

© 2014 IHS

Source: AFP

Hong Kong & Vicinity

Number of Occupy protesters as of late October

• Admiralty/Central: ~4,000; ~2,000 tents

• Mongkok: ~2,800; 100 tents

• Causeway Bay: 200; 37 tents

© 2014 IHS

The “Occupy Central” protests: Prospects for resolution

• Direct Chinese intervention is unlikely

• No compromise is likely on Beijing’s basic framework

• Economic impact of the protests will be relatively minor – the HK gov’t can afford to be patient

• No clear consensus among protesters, a resolution will likely have to be brokered by opposition party leaders

• Some police coercion may be needed to remove hold-outs

45

© 2014 IHS © 2014 IHS 46

Appendix Additional slides on China regional development

© 2014 IHS

The long-term trend in world trade is expected to flatten

World imports as a percent of GDP

10

15

20

25

30

35

40

1980 1984 1988 1992 1996 2000 2004 2008 2012 2016 2020 2024

Perc

ent

© 2014 IHS

Sources of growth of global GDP and consumer spending - production and consumption balancing

(Percent of world GDP and consumption, US dollars)

GDP Consumer Spending

2004 2014 2024 2004 2014 2024 North America 33 26 23 37 32 27

U.S. 28 22 19 33 27 23

Asia-Pacific 24 31 39 22 26 35

Japan 11 6 4 11 7 5

China 4 14 22 3 8 15

India 2 3 6 2 3 6

Western Europe 31 23 18 30 24 19

Emerging Europe 5 7 8 5 7 7

Latin America 3 6 6 3 7 7

ME & Africa 4 7 8 3 4 5

48

© 2014 IHS

Lower wages give Vietnam a cost advantage

Average annual manufacturing wages, USD

© 2014 IHS

Source: General Statistics Office, Vietnam, China’s NBS Note: China data refers to urban manufacturing wages, VNM data is manufacturing wages in state sector

0

2,000

4,000

6,000

8,000

10,000

12,000

© 2014 IHS

Region Province

2013 Real GDP/pop

2008-2013 CAGR

Real GDP per capita Population

(2000 Yuan, 1000s) (millions) Beijing 55.6 21.2 8.8% Tianjin 66.9 14.8 15.3% Shanghai 72.1 24.2 8.3% Jiangsu 49.7 79.7 11.1% Zhejiang 45.0 55.2 9.2%

Coast Guangdong 43.0 106.9 9.7% Liaoning 45.6 44.1 11.5% Hebei 27.0 73.6 10.3% Shandong 40.0 97.7 10.9% Fujian 43.7 37.9 12.1% Hainan 22.9 9.0 11.7% Chongqing 26.7 29.8 14.8% Jiangxi 19.4 45.4 12.1% Hunan 23.3 67.2 12.4%

Central Hubei 31.8 58.2 12.6% Sichuan 21.8 81.4 13.4% Anhui 21.8 60.5 12.7% Henan 22.8 94.5 10.7%

Province mapping classification – coast & central

50

© 2014 IHS

Province mapping classification – northeast & west

51

Region Province 2013 Real GDP/pop

2008-2013 CAGR

Real GDP per capita Population (2000 Yuan, 1000s) (millions)

Heilongjiang 32.7 38.5 10.8%

Jilin 30.1 27.6 12.2%

Northeast Inner Mongolia 38.2 25.1 13.3%

Shanxi 18.8 36.4 10.2%

Shaanxi 21.1 37.8 13.2%

Ningxia 16.9 6.6 11.7%

Tibet 17.0 3.1 12.3%

Qinghai 20.4 5.8 12.4%

West Xinjiang 22.3 22.7 10.7%

Gansu 15.0 25.9 11.5%

Yunnan 16.2 47.1 12.6%

Guizhou 8.1 34.7 13.0%

Guangxi 19.1 47.4 12.4%

© 2014 IHS

Chinese government subsidized inner-land provinces’ economic growth

0

5

10

15

20

25

1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013

Coast Central Northeast West National

Government spending to GDP (percent)

Source: NBS, IHS

Government spending to GDP (percent)

Source: NBS, IHS

52

© 2014 IHS

Foreign investment drove coastal regions’ economic growth

0

2

4

6

8

10

12

1990 1995 2000 2005 2010 2015 2020 2025 2030

Coast Central

Foreign direct investment to GDP (percent)

Source: NBS, IHS

Foreign direct investment to GDP share (percent)

Source: NBS, IHS

53

© 2014 IHS

Region Province Symbol Region Province Symbol Beijing Heilongjiang Tianjin Jilin Shanghai Northeast Inner Mongolia Jiangsu Shanxi Zhejiang Shaanxi

Coast Guangdong Liaoning Hebei Shandong Fujian Hainan Chongqing Ningxia

Jiangxi Tibet Hunan Qinghai Hubei West Xinjiang

Central Sichuan Gansu Anhui Yunnan Henan Guizhou Guangxi

Regions’ GDP growth and GDP per capita - Legend

54

© 2014 IHS

China’s regions over the 1980-2013 period

0

4

8

12

16

20

0 5 10 15 20 25 30 35 40 45 50 55Real

GDP

per

capi

ta g

row

th, C

AGR

(Per

cent

)

Real GDP Per capita (Thousand 2000 Yuan)

Source: NBS, IHS

Real GDP per capita growth vs Real GDP per capita

2000, 2000-09 1980, 1980-1989 2007, 2007-13 1990, 1990-1999

55

© 2014 IHS

China’s regions over the 1980-89 period

0

4

8

12

16

20

0 5 10 15 20 25 30 35 40 45 50 55

Real

GDP

per

capi

ta g

row

th, C

AGR

1980

-89

(Per

cent

)

1980 Real GDP Per capita (Thousand 2000 Yuan)

Source: NBS, IHS

Real GDP per capita growth vs Real GDP per capita

Northeast Central Coast West

56

© 2014 IHS

China’s regions over the 1990-99 period

0

4

8

12

16

20

0 5 10 15 20 25 30 35 40 45 50 55

Real

GDP

per

capi

ta g

row

th, C

AGR

1990

-99

(Per

cent

)

1990 Real GDP Per capita (Thousand 2000 Yuan)

Source: NBS, IHS

Real GDP per capita growth vs Real GDP per capita

Northeast Central Coast West

57

© 2014 IHS

China’s regions over the 2000-09 period

0

4

8

12

16

20

0 5 10 15 20 25 30 35 40 45 50 55

Real

GDP

per

capi

ta g

row

th, C

AGR

2000

-09

(Per

cent

)

2000 Real GDP Per capita (Thousand 2000 Yuan)

Source: NBS, IHS

Real GDP per capita growth vs Real GDP per capita

Northeast Central Coast West

58

© 2014 IHS

China’s regions over the 2007-13 period

0

4

8

12

16

20

0 5 10 15 20 25 30 35 40 45 50 55

Real

GDP

per

capi

ta g

row

th, C

AGR

2007

-13

(Per

cent

)

2007 Real GDP Per capita (Thousand 2000 Yuan)

Source: NBS, IHS

Real GDP per capita growth vs Real GDP per capita

Northeast Central Coast West

59

© 2014 IHS

China’s regions over the 1980-2013 period

0

4

8

12

16

20

0 5 10 15 20 25 30 35 40 45 50 55Real

GDP

gro

wth

, CAG

R 19

80-8

9 (P

erce

nt)

1980 Real GDP Per capita (Thousand 2000 Yuan)

Source: NBS, IHS

Real GDP growth vs Real GDP per capita

60

1980, 1980-1989 1990, 1990-1999 2000, 2000-09 2007, 2007-13

© 2014 IHS

China’s regions over the 1980-89 period

0

4

8

12

16

20

0 5 10 15 20 25 30 35 40 45 50 55Real

GDP

gro

wth

, CAG

R 19

80-8

9 (P

erce

nt)

1980 Real GDP Per capita (Thousand 2000 Yuan)

Source: NBS, IHS

Real GDP growth vs Real GDP per capita

Northeast Central Coast West

61

© 2014 IHS

China’s regions over the 1990-99 period

0

4

8

12

16

20

0 5 10 15 20 25 30 35 40 45 50 55Real

GDP

gro

wth

, CAG

R 19

90-9

9 (P

erce

nt)

1990 Real GDP Per capita (Thousand 2000 Yuan)

Source: NBS, IHS

Real GDP growth vs Real GDP per capita

Northeast Central Coast West

62

© 2014 IHS

China’s regions over the 2000-09 period

0

4

8

12

16

20

0 5 10 15 20 25 30 35 40 45 50 55Real

GDP

gro

wth

, CAG

R 20

00-0

9 (P

erce

nt)

2000 Real GDP Per capita (Thousand 2000 Yuan)

Source: NBS, IHS

Real GDP growth and Real GDP per capita

Northeast Central Coast West

63

© 2014 IHS

China’s regions over the 2007-13 period

0

4

8

12

16

20

0 5 10 15 20 25 30 35 40 45 50 55

Real

GDP

gro

wth

, CAG

R 20

07-1

3 (P

erce

nt)

2007 Real GDP Per capita (Thousand 2000 Yuan)

Source: NBS, IHS

Real GDP growth and Real GDP per capita

Northeast Central Coast West

64

© 2014 IHS

Regional growth vs. GDP per capita level

6

7

8

9

10

11

12

13

14

0 7 14 21 28

Real

GDP

gro

wth

, CAG

R (P

erce

nt)

Real GDP Per capita (Thousand 2000 Yuan)

Real GDP per capita growth and Real GDP per capita

Source: NBS, IHS

65

Northeast Central Coast West National

1980,1980-89 1990,1990-99 2000, 2000-09 2007, 2007-13

© 2014 IHS

Coastal provinces no longer China’s hub for economic growth

0

2

4

6

8

10

12

14

16

1980-1985 1985-1990 1990-1995 1995-2000 2000-2005 2005-2010 2010-2015 2015-2020

Coast Central Northeast West National

GDP per capita (Thousand yen)

Source: NBS, IHS

Real GDP per capita, compound annual growth rate (percent) Real GDP per capita, compound annual growth rate (percent)

Source: NBS, IHS

66

© 2014 IHS

Real GDP per capita in coastal regions is still above the rest of China

0

10

20

30

40

50

60

70

80

1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 2020

Coast Central Northeast West National

Real GDP per capita (Thousand 2000 Yuan)

Source: NBS, IHS

67

© 2014 IHS

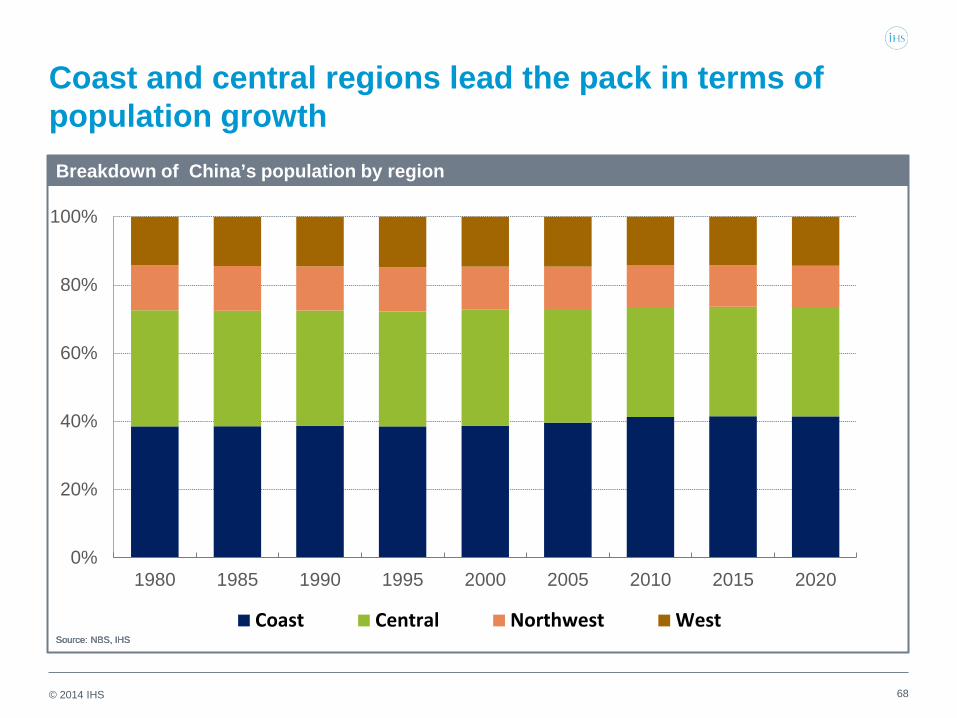

Coast and central regions lead the pack in terms of population growth

0%

20%

40%

60%

80%

100%

1980 1985 1990 1995 2000 2005 2010 2015 2020

Coast Central Northwest West

Population share

Source: NBS, IHS

GDP per capita (Thousand yen)

Source: NBS, IHS

Real GDP per capita, compound annual growth rate (percent) Breakdown of China’s population by region

Source: NBS, IHS

68

© 2014 IHS

Western provinces progressively becoming China’s most dynamic consumer markets

0

2

4

6

8

10

1996-2001 2001-06 2006-11 2011-16 2016-21Coast Central Northeast West National

GDP per capita (Thousand yen)

Source: NBS, IHS

Real consumption per capita, compound annual growth rate (percent) GDP per capita (Thousand yen)

Source: NBS, IHS

Real GDP per capita, compound annual growth rate (percent) Real consumption per capita, compound annual growth rate (percent)

Source: NBS, IHS

69

© 2014 IHS 70

Breakdown of China’s GDP by region

55.8% 25.0%

10.5%

8.7%

Coast Central Northeast West

Nominal GDP (1996)

Source: NBS, IHS

55.4% 24.4%

11.6%

8.6%

Coast Central Northeast West

Nominal GDP (2013)

Source: NBS, IHS

© 2014 IHS 71

Breakdown of China’s private consumption by region

51.1%

27.2%

10.8%

10.9%

Coast Central Northeast West

Nominal private consumption (1996)

Source: NBS, IHS

54.8%

25.3%

10.3%

9.6%

Coast Central Northeast West

Nominal private consumption (2013)

Source: NBS, IHS

© 2014 IHS

IHS Customer Care: • Americas: +1 800 IHS CARE (+1 800 447 2273); [email protected] • Europe, Middle East, and Africa: +44 (0) 1344 328 300; [email protected] • Asia and the Pacific Rim: +604 291 3600; [email protected]

© 2014 IHS. No portion of this report may be reproduced, reused, or otherwise distributed in any form without prior written consent, with the exception of any internal client distribution as may be permitted in the license agreement between client and IHS. Content reproduced or redistributed with IHS permission must display IHS legal notices and attributions of authorship. The information contained herein is from sources considered reliable but its accuracy and completeness are not warranted, nor are the opinions and analyses which are based upon it, and to the extent permitted by law, IHS shall not be liable for any errors or omissions or any loss, damage or expense incurred by reliance on information or any statement contained herein. For more information, please contact IHS at Customer Care (see phone numbers and email addresses above). All products, company names or other marks appearing in this publication are the trademarks and property of IHS or their respective owners.