ifrs update 2013 - deloitte · pdf filefinancial instruments ... chapter 1 objective chapter 2...

TRANSCRIPT

IFRS Update 2013Highlighting the key issues

28 November 2013

© 2013 Deloitte Accountants B.V.2

Dingeman Manschot

Ralph ter Hoeven

© 2013 Deloitte Accountants B.V.

Agenda

3

• Introduction

• Developments in accounting

• Conceptual framework project

• Financial instruments project

• Revenue recognition project

• Leases project

• Platform changes 2013 – 2014

• Conclusions

© 2013 Deloitte Accountants B.V.

Testvraag

‘We moeten zo snel als mogelijk zien af te

komen van IFRS.’

Bent u eens met deze stelling?

a) Eens

b) Oneens

4

Introduction

© 2013 Deloitte Accountants B.V.

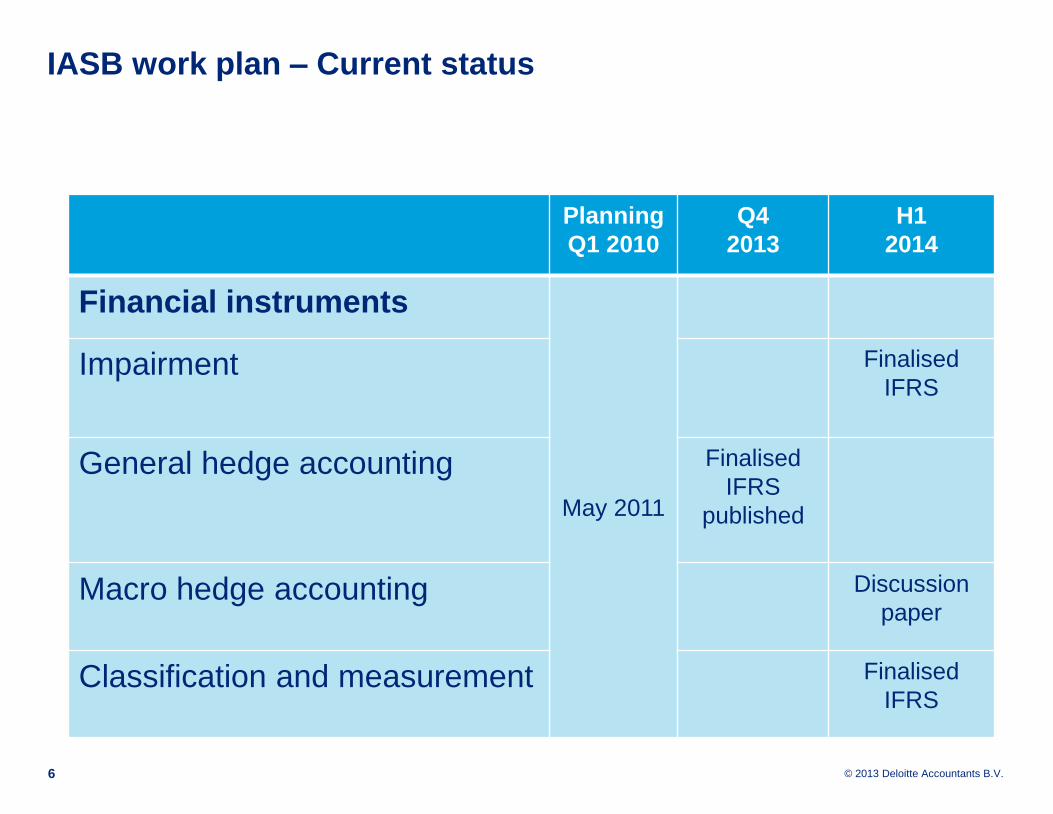

IASB work plan – Current status

Planning

Q1 2010

Q4

2013

H1

2014

Financial instruments

May 2011

Impairment Finalised

IFRS

General hedge accounting Finalised

IFRS

published

Macro hedge accounting Discussion

paper

Classification and measurement Finalised

IFRS

6

© 2013 Deloitte Accountants B.V.

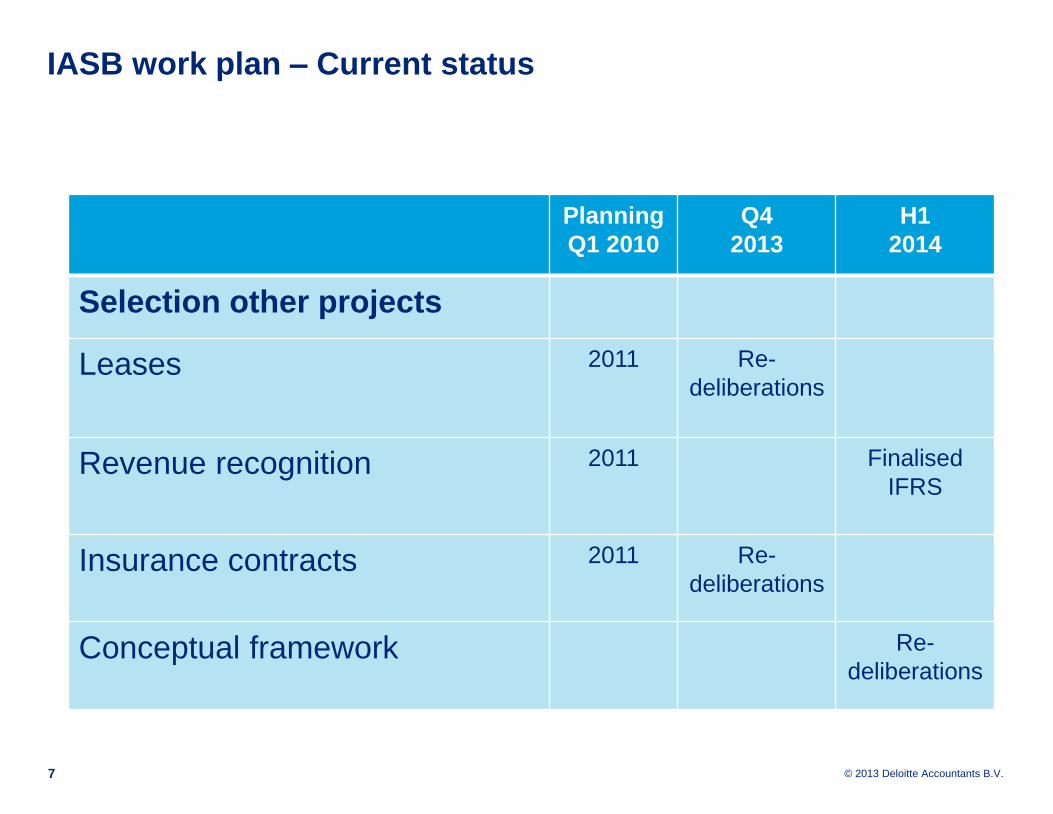

IASB work plan – Current status

Planning

Q1 2010

Q4

2013

H1

2014

Selection other projects

Leases 2011 Re-

deliberations

Revenue recognition 2011 Finalised

IFRS

Insurance contracts 2011 Re-

deliberations

Conceptual framework Re-

deliberations

7

Developments in accounting

© 2013 Deloitte Accountants B.V.

EU-Accounting Directive

9

Financial statements for financial years beginning on 1 January

2016 or during the calendar year 2016

EU-Accounting Directive 2013/34/EU

The new accounting directive is

adopted by the European

Parliament and the Council of the

European Union

© 2013 Deloitte Accountants B.V.

EU-Accounting Directive

10

‘Annual financial statements should

be prepared on a prudent basis’

‘Introduction of micro-undertakings’

‘Increase of size criteria’

‘No option to implement IFRS for SMEs’

© 2013 Deloitte Accountants B.V.

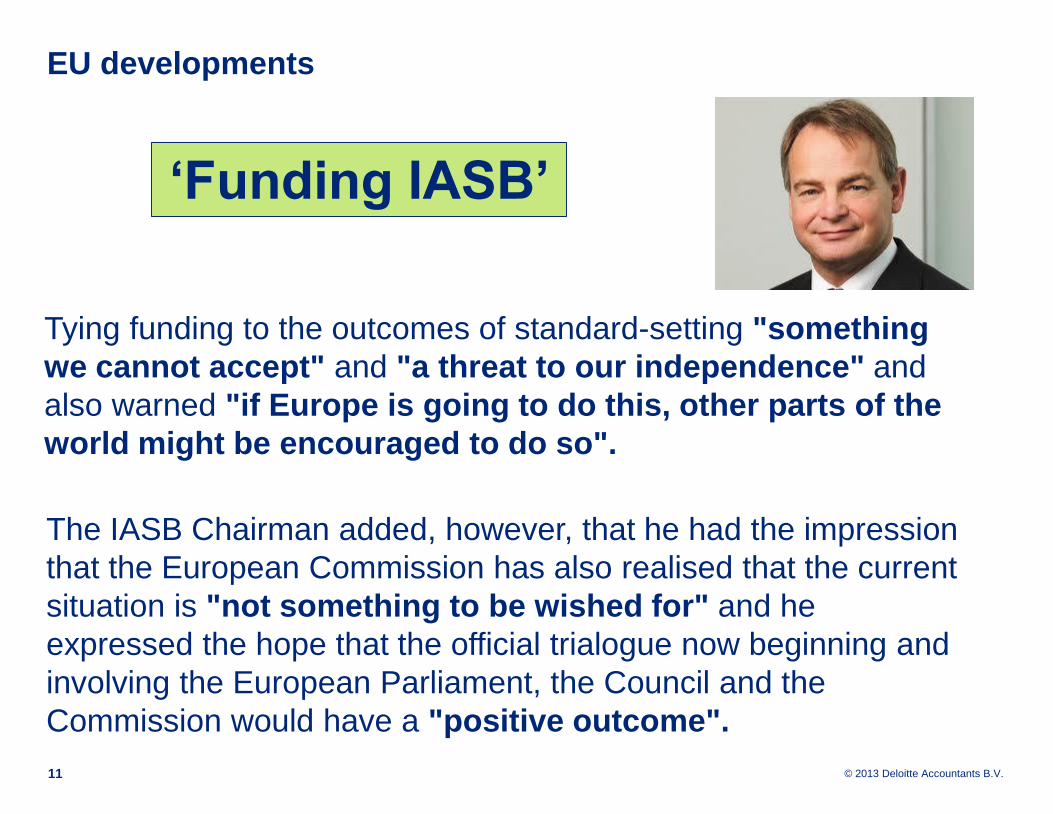

EU developments

11

Tying funding to the outcomes of standard-setting "something

we cannot accept" and "a threat to our independence" and

also warned "if Europe is going to do this, other parts of the

world might be encouraged to do so".

‘Funding IASB’

The IASB Chairman added, however, that he had the impression

that the European Commission has also realised that the current

situation is "not something to be wished for" and he

expressed the hope that the official trialogue now beginning and

involving the European Parliament, the Council and the

Commission would have a "positive outcome".

© 2013 Deloitte Accountants B.V.

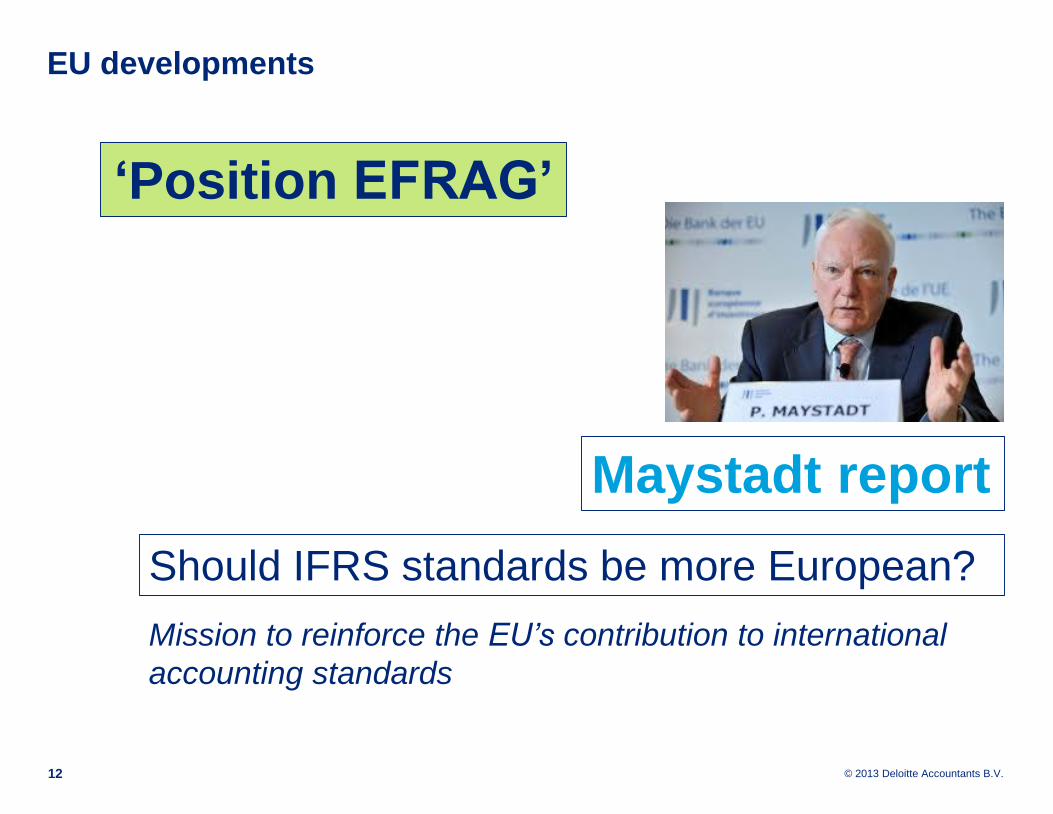

EU developments

12

Maystadt report

Should IFRS standards be more European?

Mission to reinforce the EU’s contribution to international

accounting standards

‘Position EFRAG’

© 2013 Deloitte Accountants B.V.

Vraag

‘Wie betaalt, bepaalt’.

Bent u eens met deze stelling?

a) Eens

b) Oneens

13

© 2013 Deloitte Accountants B.V.

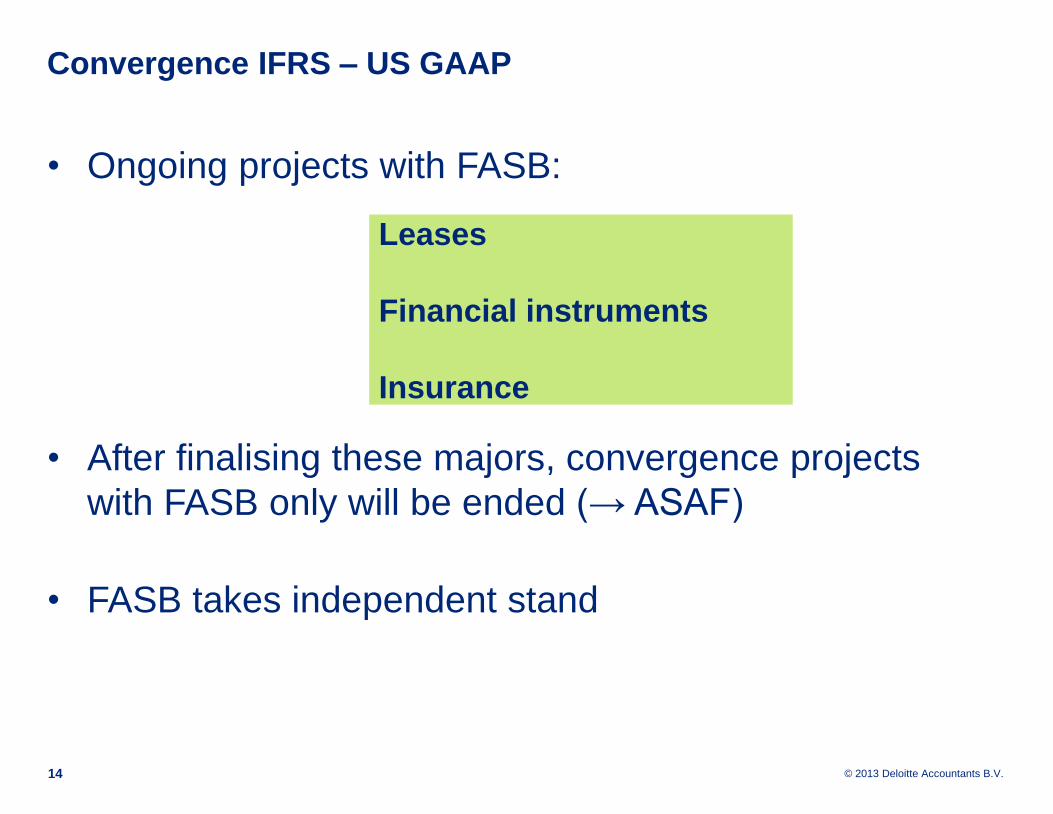

Convergence IFRS – US GAAP

14

• Ongoing projects with FASB:

• After finalising these majors, convergence projects

with FASB only will be ended (→ ASAF)

• FASB takes independent stand

Leases

Financial instruments

Insurance

© 2013 Deloitte Accountants B.V.

Disclosure

15

‘Cutting clutter’

© 2013 Deloitte Accountants B.V.16

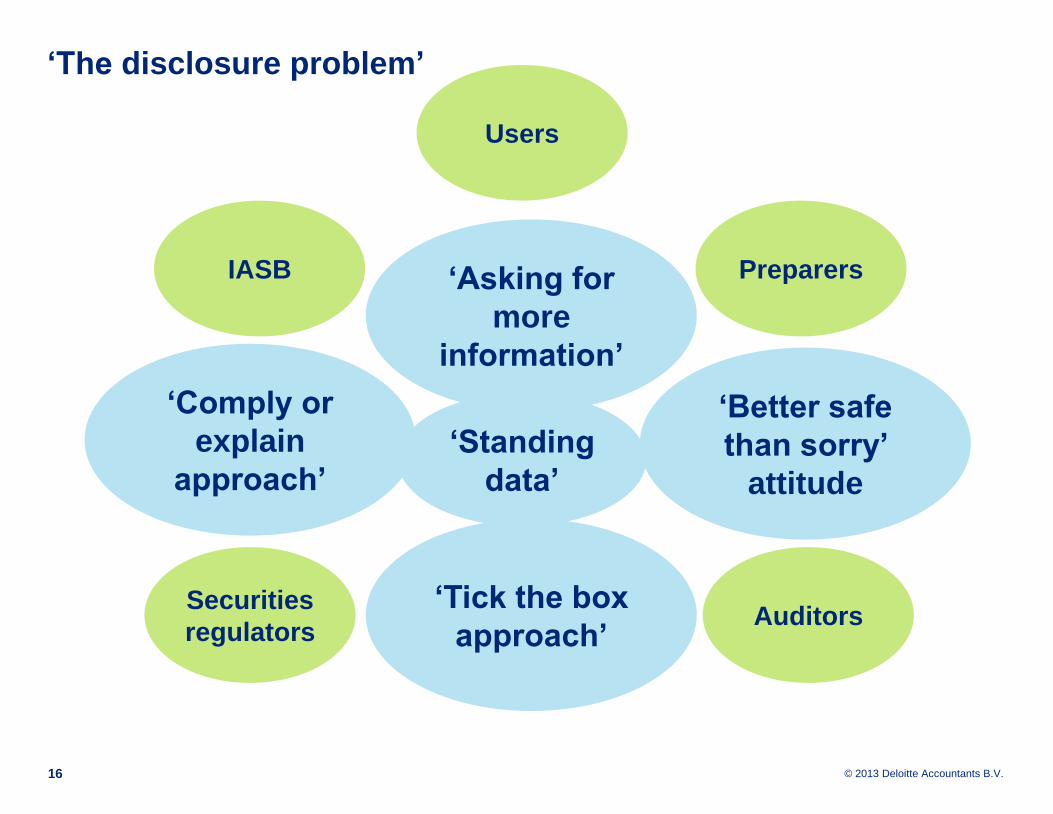

‘The disclosure problem’

‘Better safe

than sorry’

attitude

‘Asking for

more

information’

‘Comply or

explain

approach’

‘Tick the box

approach’

IASB

AuditorsSecurities

regulators

Preparers

Users

‘Standing

data’

© 2013 Deloitte Accountants B.V.

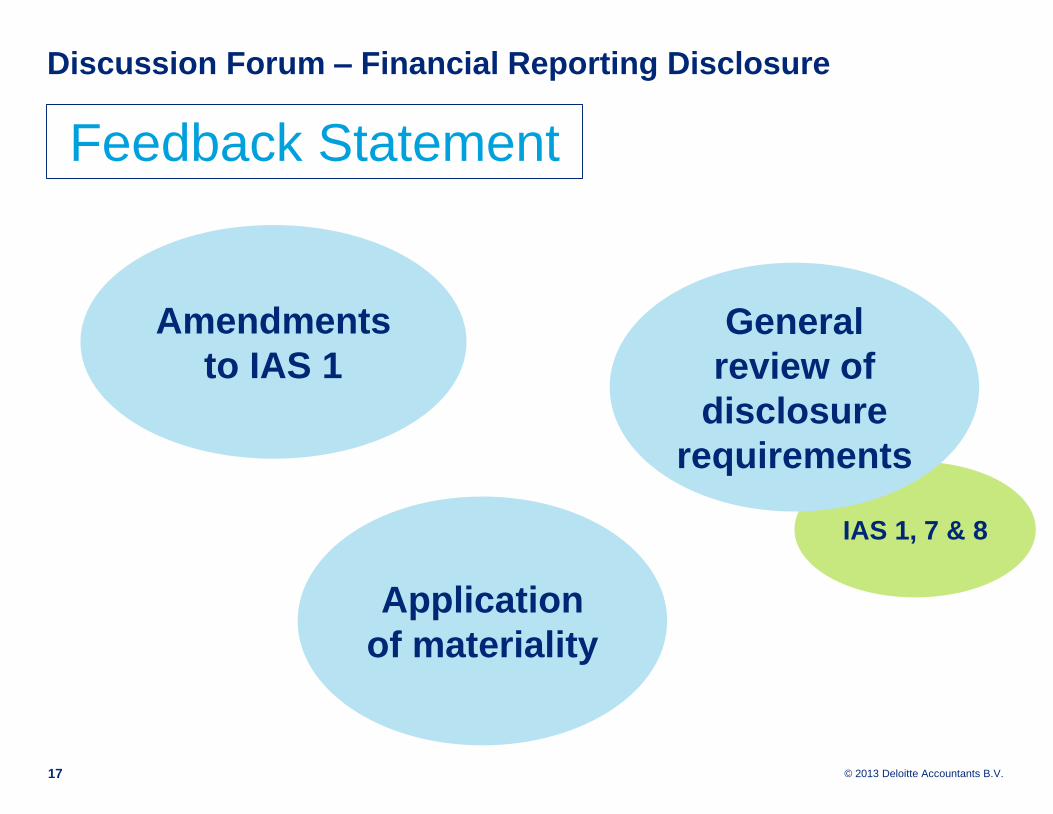

Discussion Forum – Financial Reporting Disclosure

17

Feedback Statement

Amendments

to IAS 1

Application

of materiality

IAS 1, 7 & 8

General

review of

disclosure

requirements

© 2013 Deloitte Accountants B.V.

Vraag

Verwacht u dat het aantal disclosures

daadwerkelijk af zal nemen in de toekomst?

a) Ja

b) Nee

18

Conceptual framework project

© 2013 Deloitte Accountants B.V.

Conceptual framework

20

Building a conceptual

framework

© 2013 Deloitte Accountants B.V.

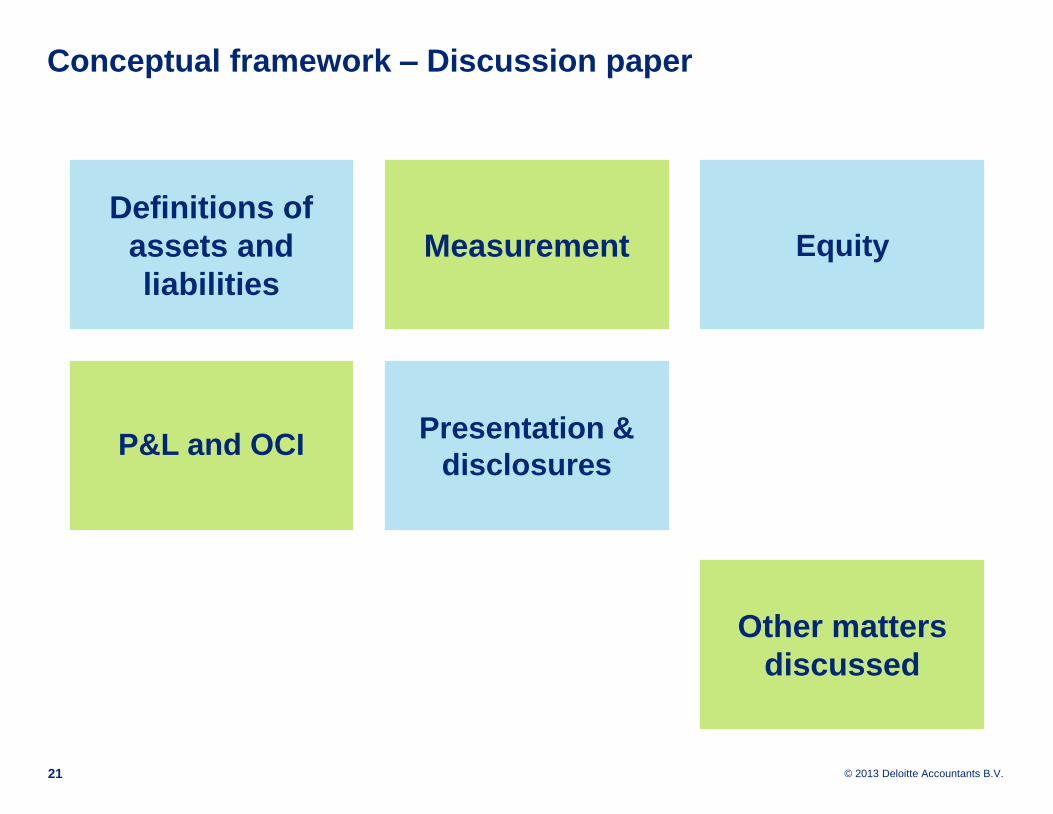

Conceptual framework – Discussion paper

21

Definitions of

assets and

liabilities

Measurement Equity

P&L and OCIPresentation &

disclosures

Other matters

discussed

Financial instruments project

© 2013 Deloitte Accountants B.V.

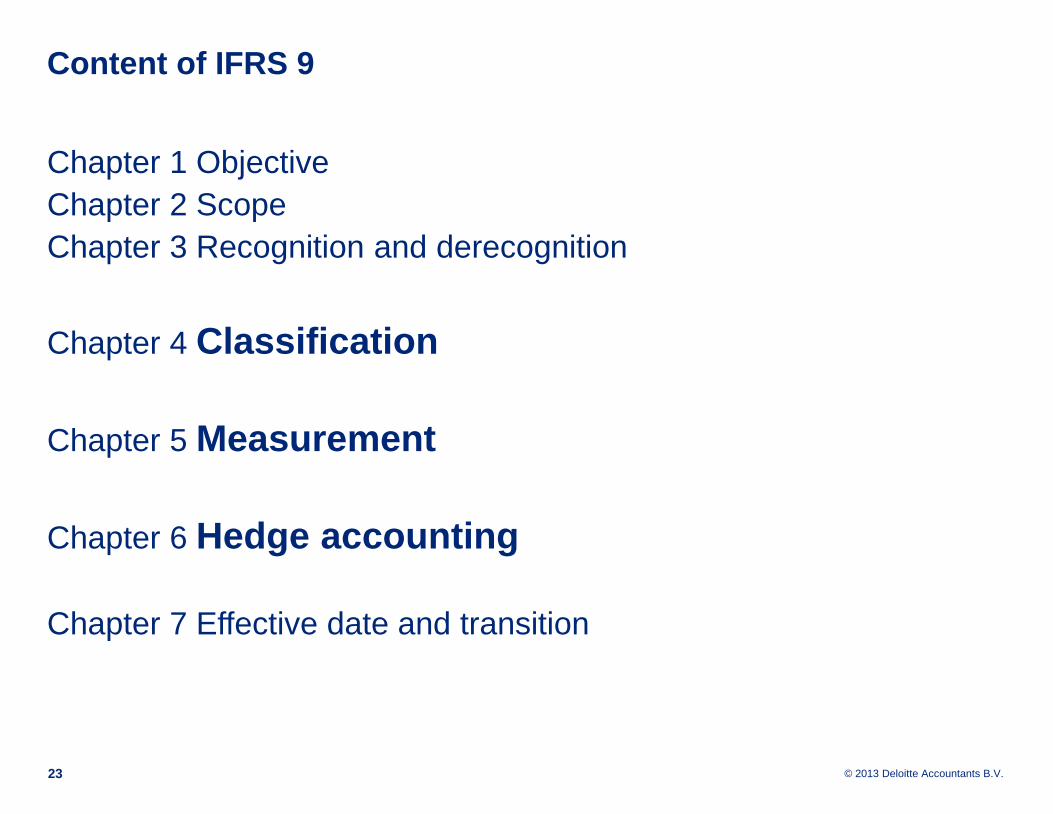

Content of IFRS 9

23

Chapter 1 Objective

Chapter 2 Scope

Chapter 3 Recognition and derecognition

Chapter 4 Classification

Chapter 5 Measurement

Chapter 6 Hedge accounting

Chapter 7 Effective date and transition

© 2013 Deloitte Accountants B.V.

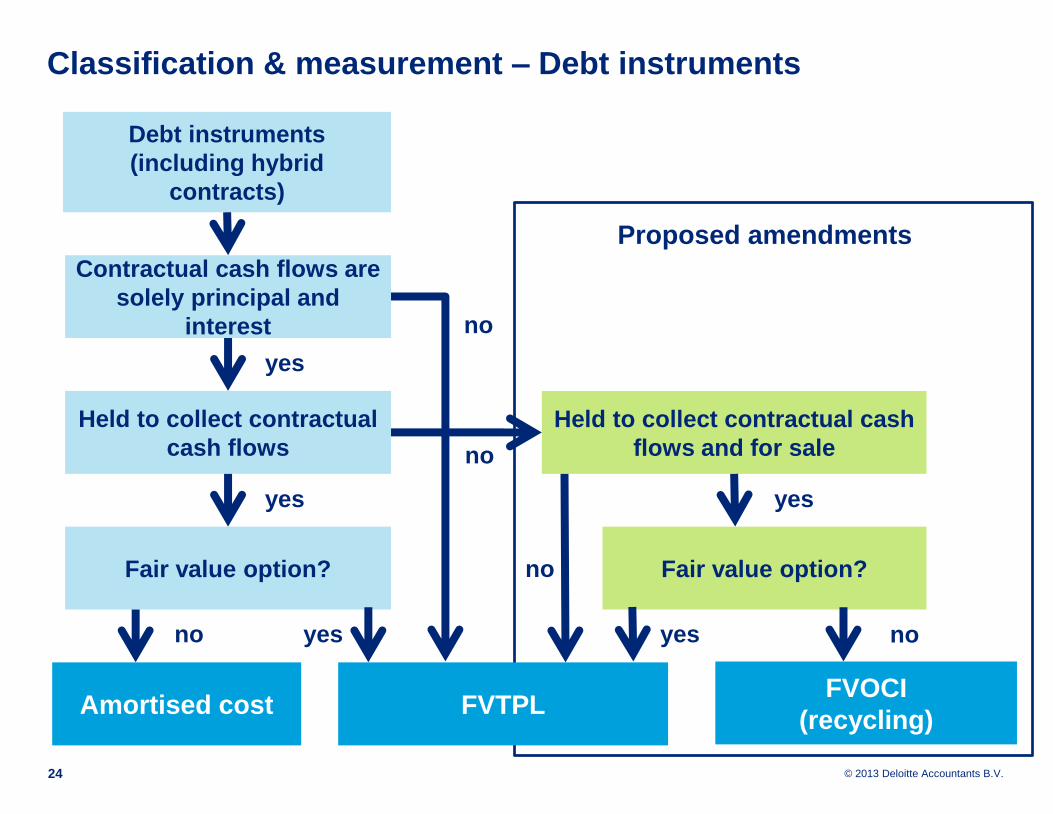

Classification & measurement – Debt instruments

24

Debt instruments

(including hybrid

contracts)

Contractual cash flows are

solely principal and

interest

Held to collect contractual

cash flows

Fair value option?

Amortised costFVOCI

(recycling)

Fair value option?

Held to collect contractual cash

flows and for sale

yes

yes

yes

no

yesno

no

yes

no

no

Proposed amendments

FVTPL

© 2013 Deloitte Accountants B.V.

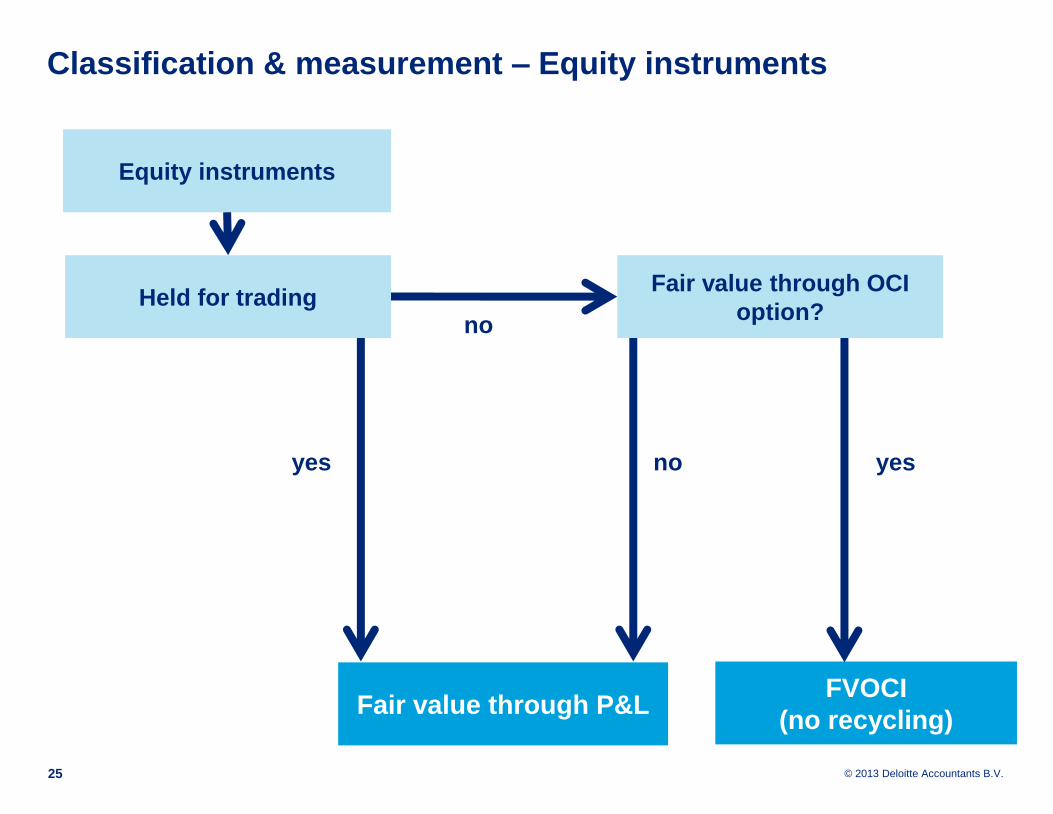

Classification & measurement – Equity instruments

25

Equity instruments

Held for tradingFair value through OCI

option?

FVOCI

(no recycling)

yes no yes

no

Fair value through P&L

© 2013 Deloitte Accountants B.V.

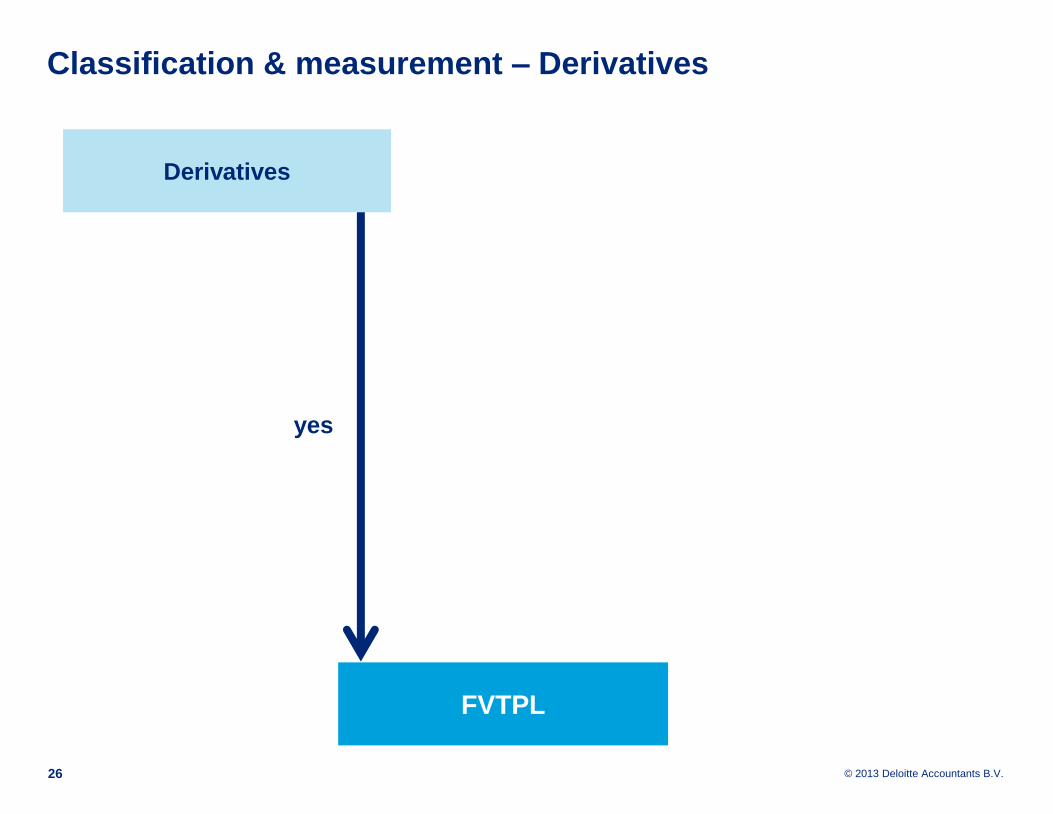

Classification & measurement – Derivatives

26

Derivatives

yes

FVTPL

© 2013 Deloitte Accountants B.V.

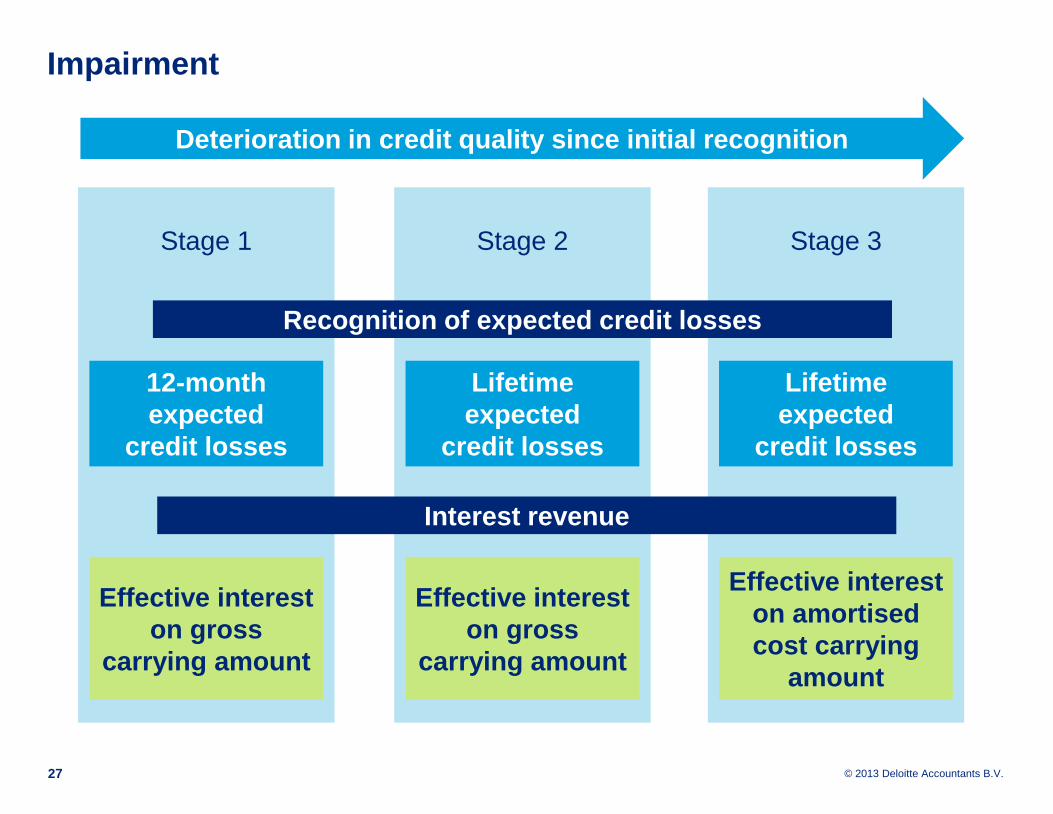

Impairment

27

Stage 1 Stage 2 Stage 3

Deterioration in credit quality since initial recognition

12-month

expected

credit losses

Lifetime

expected

credit losses

Lifetime

expected

credit losses

Effective interest

on gross

carrying amount

Effective interest

on gross

carrying amount

Effective interest

on amortised

cost carrying

amount

Interest revenue

Recognition of expected credit losses

© 2013 Deloitte Accountants B.V.

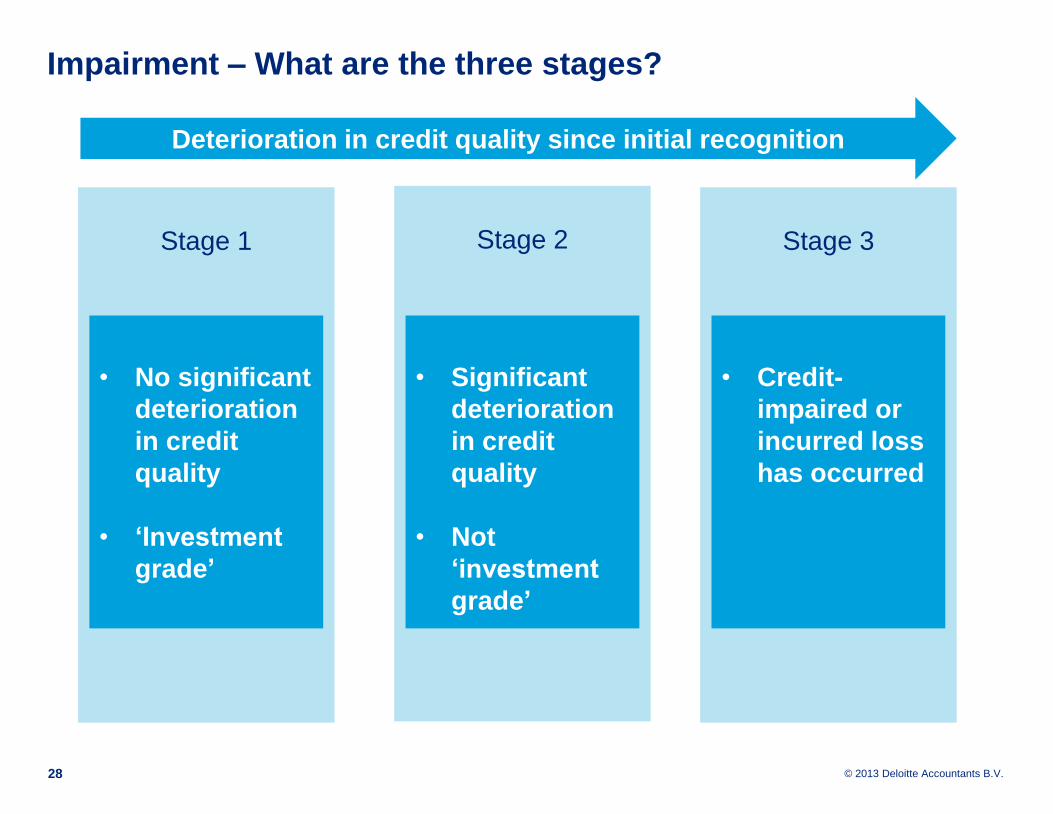

Impairment – What are the three stages?

28

Stage 1 Stage 2 Stage 3

Deterioration in credit quality since initial recognition

• No significant

deterioration

in credit

quality

• ‘Investment

grade’

• Significant

deterioration

in credit

quality

• Not

‘investment

grade’

• Credit-

impaired or

incurred loss

has occurred

© 2013 Deloitte Accountants B.V.

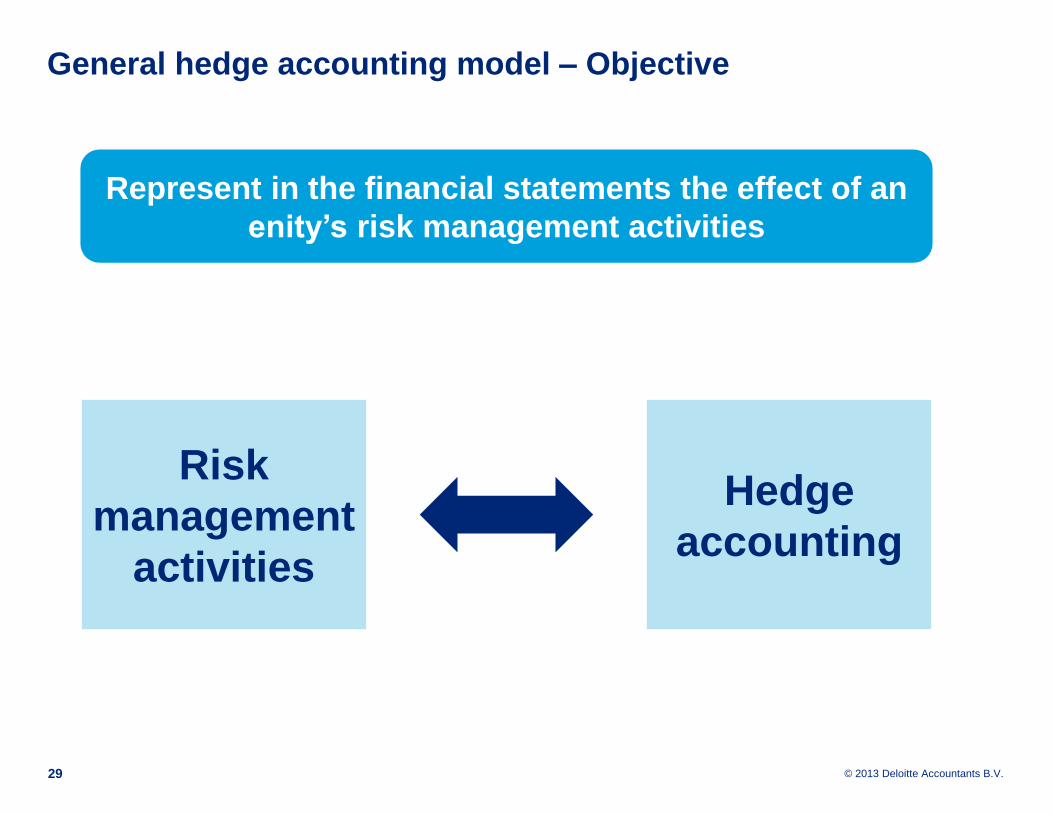

General hedge accounting model – Objective

29

Represent in the financial statements the effect of an

enity’s risk management activities

Risk

management

activities

Hedge

accounting

© 2013 Deloitte Accountants B.V.

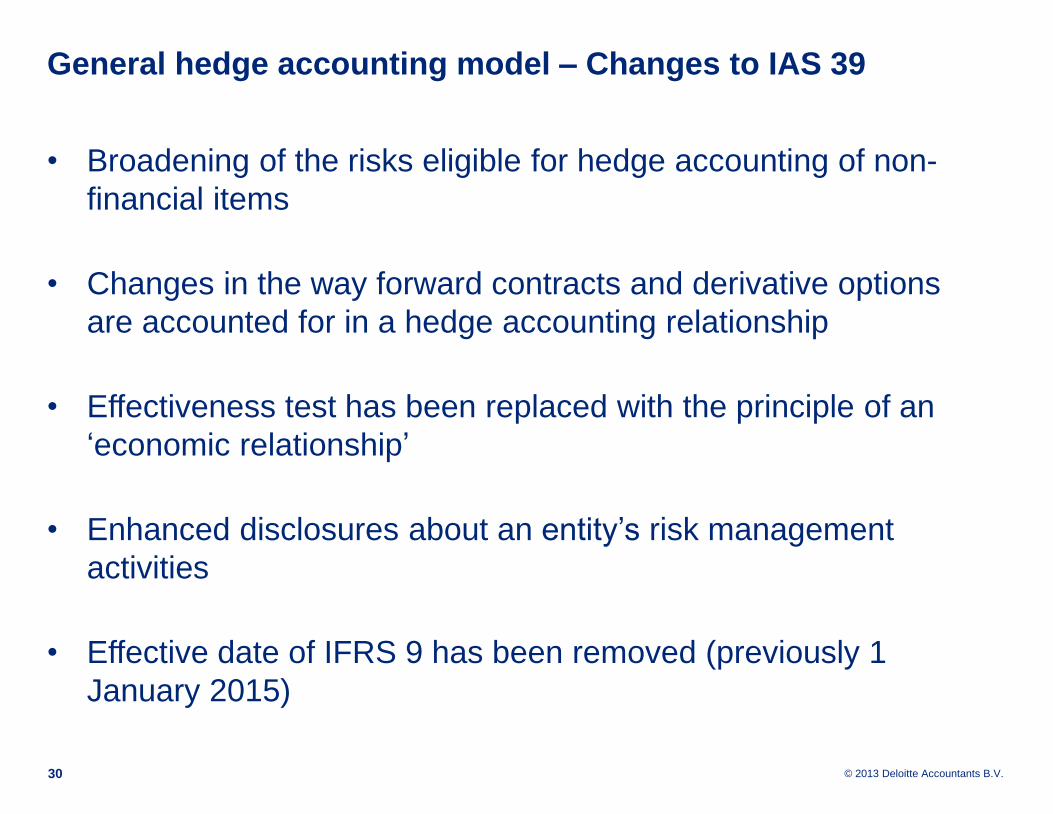

General hedge accounting model – Changes to IAS 39

• Broadening of the risks eligible for hedge accounting of non-

financial items

• Changes in the way forward contracts and derivative options

are accounted for in a hedge accounting relationship

• Effectiveness test has been replaced with the principle of an

‘economic relationship’

• Enhanced disclosures about an entity’s risk management

activities

• Effective date of IFRS 9 has been removed (previously 1

January 2015)

30

Revenue recognition project

© 2013 Deloitte Accountants B.V.

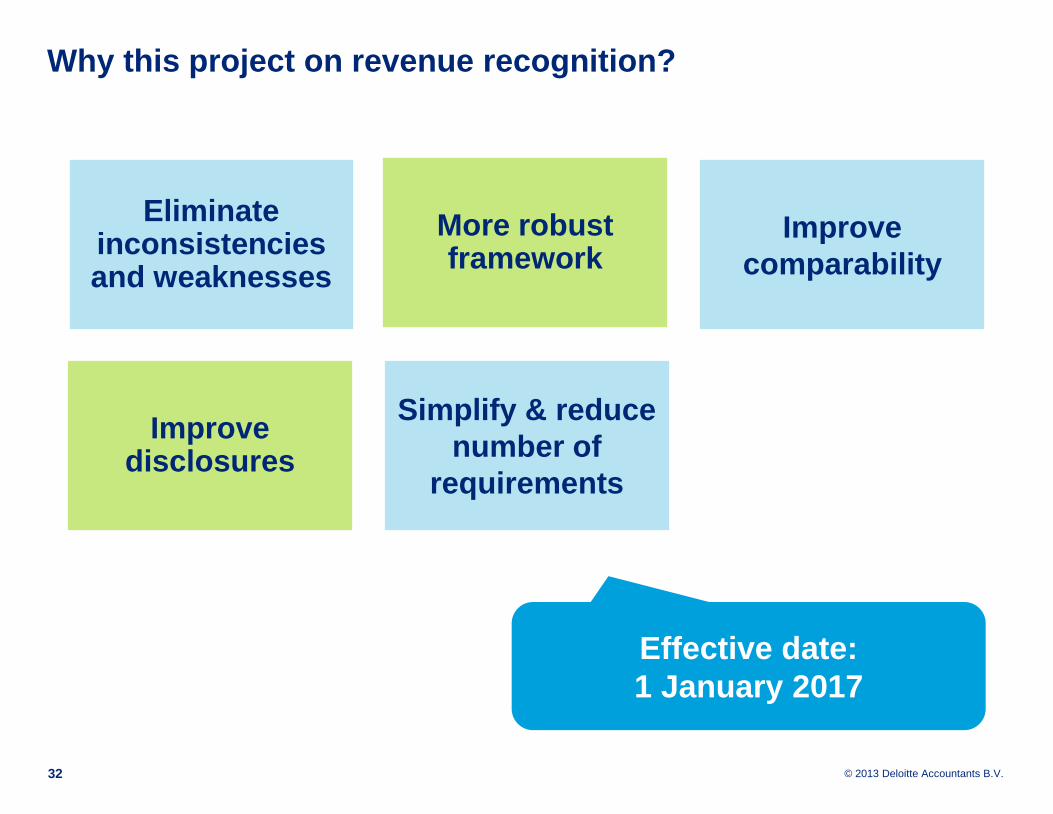

Why this project on revenue recognition?

32

Eliminate inconsistencies and weaknesses

More robust framework

Improve

comparability

Improve disclosures

Simplify & reduce

number of

requirements

Effective date:

1 January 2017

© 2013 Deloitte Accountants B.V.

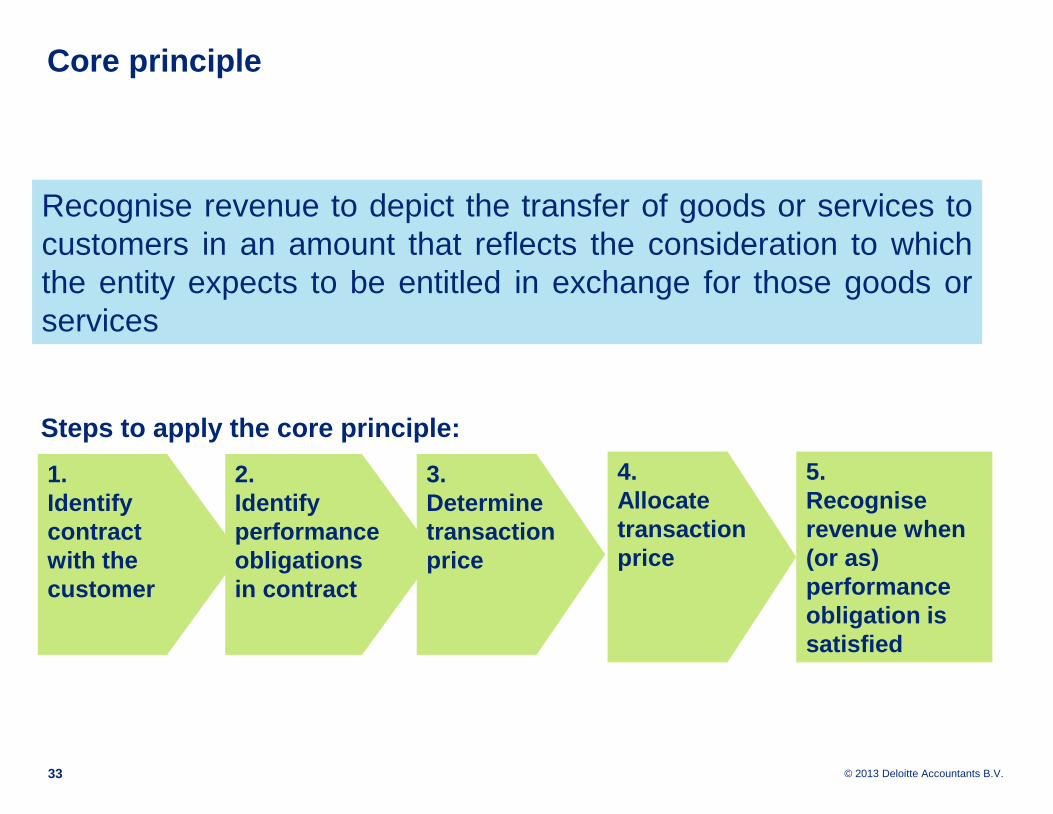

Core principle

33

Recognise revenue to depict the transfer of goods or services to

customers in an amount that reflects the consideration to which

the entity expects to be entitled in exchange for those goods or

services

Steps to apply the core principle:

1.

Identify

contract

with the

customer

2.

Identify

performance

obligations

in contract

3.

Determine

transaction

price

4.

Allocate

transaction

price

5.

Recognise

revenue when

(or as)

performance

obligation is

satisfied

© 2013 Deloitte Accountants B.V.

Understanding the core approach

34

Contract

with

customer

Deliver

equipment

Provide

training

services

Provide

ongoing

services

Provide

warranty

€ 100

€ 5

€ 4

€ 1

When

delivered

When

performed

When

provided

When

provided

1. Identify

the contract

2. Identify

performance

obligations

3. Determine

transaction

price

4. Allocate

transaction

price

5. Recognise

revenue when /

as performance

obligation is

satisfied

© 2013 Deloitte Accountants B.V.

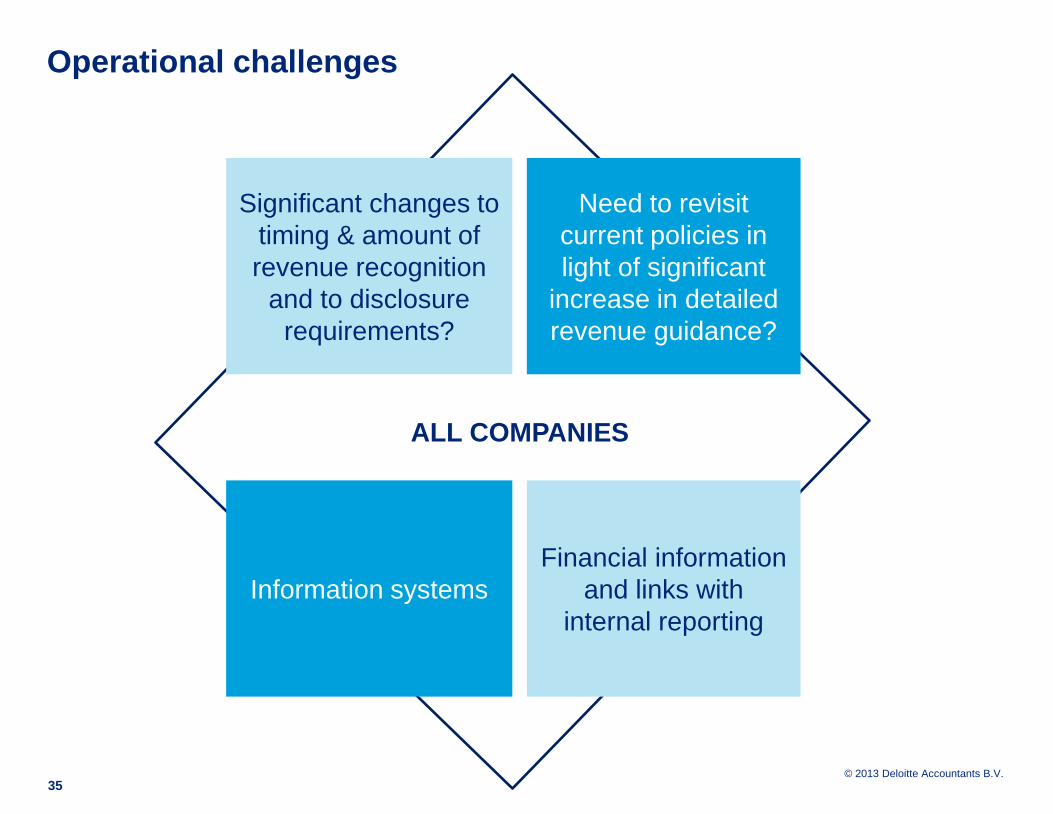

Operational challenges

35

Significant changes to

timing & amount of

revenue recognition

and to disclosure

requirements?

Need to revisit

current policies in

light of significant

increase in detailed

revenue guidance?

Information systems

Financial information

and links with

internal reporting

ALL COMPANIES

Leases project

© 2013 Deloitte Accountants B.V.37

© 2013 Deloitte Accountants B.V.

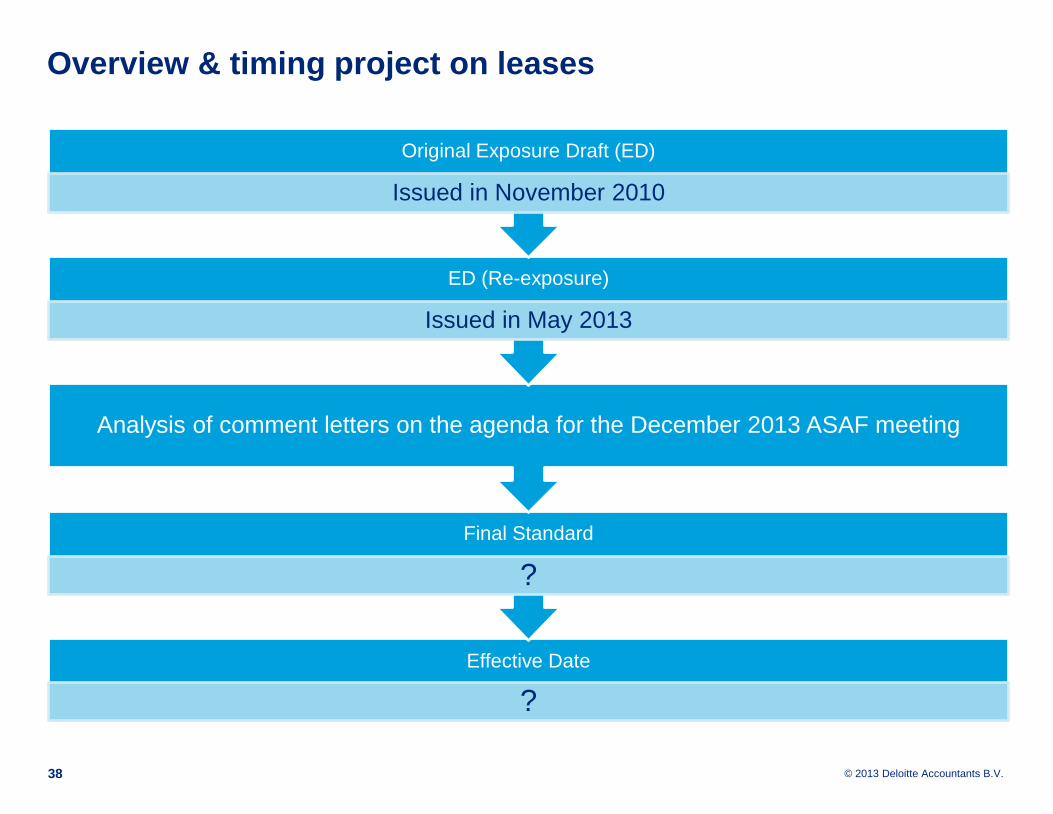

Overview & timing project on leases

Effective Date

?

Final Standard

?

Analysis of comment letters on the agenda for the December 2013 ASAF meeting

ED (Re-exposure)

Issued in May 2013

Original Exposure Draft (ED)

Issued in November 2010

38

© 2013 Deloitte Accountants B.V.

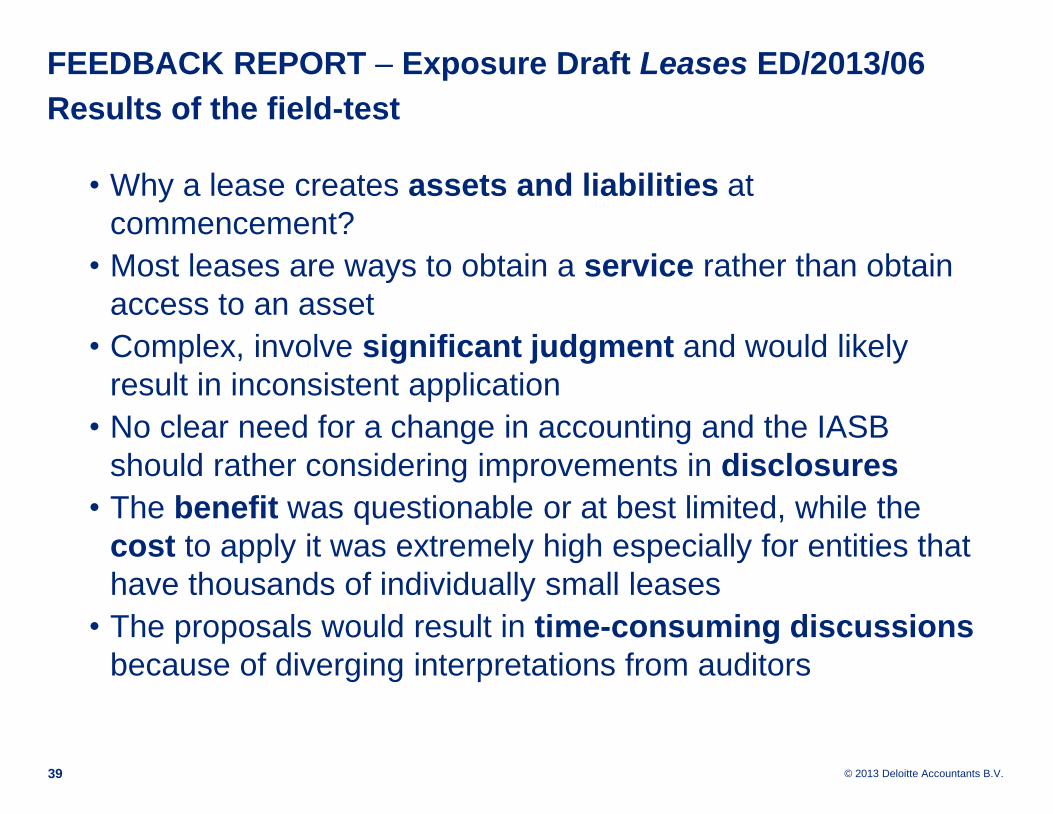

FEEDBACK REPORT – Exposure Draft Leases ED/2013/06

Results of the field-test

39

• Why a lease creates assets and liabilities at

commencement?

• Most leases are ways to obtain a service rather than obtain

access to an asset

• Complex, involve significant judgment and would likely

result in inconsistent application

• No clear need for a change in accounting and the IASB

should rather considering improvements in disclosures

• The benefit was questionable or at best limited, while the

cost to apply it was extremely high especially for entities that

have thousands of individually small leases

• The proposals would result in time-consuming discussions

because of diverging interpretations from auditors

© 2013 Deloitte Accountants B.V.

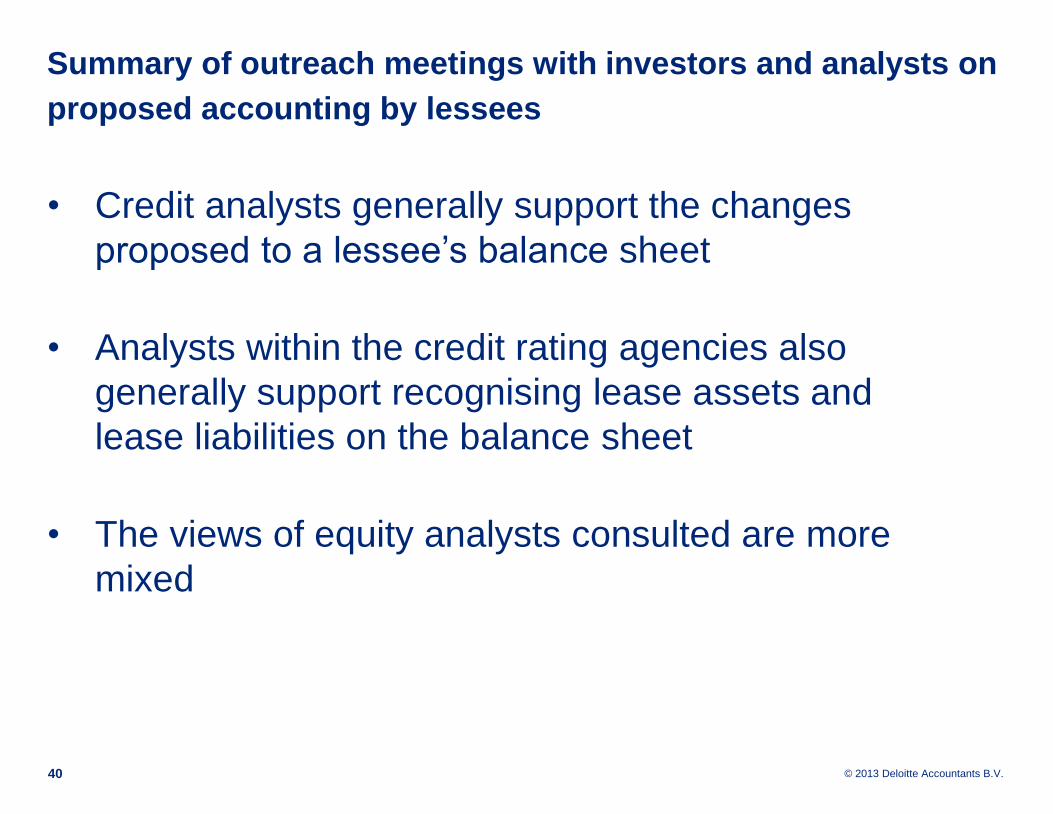

Summary of outreach meetings with investors and analysts on

proposed accounting by lessees

40

• Credit analysts generally support the changes

proposed to a lessee’s balance sheet

• Analysts within the credit rating agencies also

generally support recognising lease assets and

lease liabilities on the balance sheet

• The views of equity analysts consulted are more

mixed

© 2013 Deloitte Accountants B.V.

Vraag

Bent u voor het opnemen van leases op de

balans?

a) Ja

b) Nee

41

© 2013 Deloitte Accountants B.V.

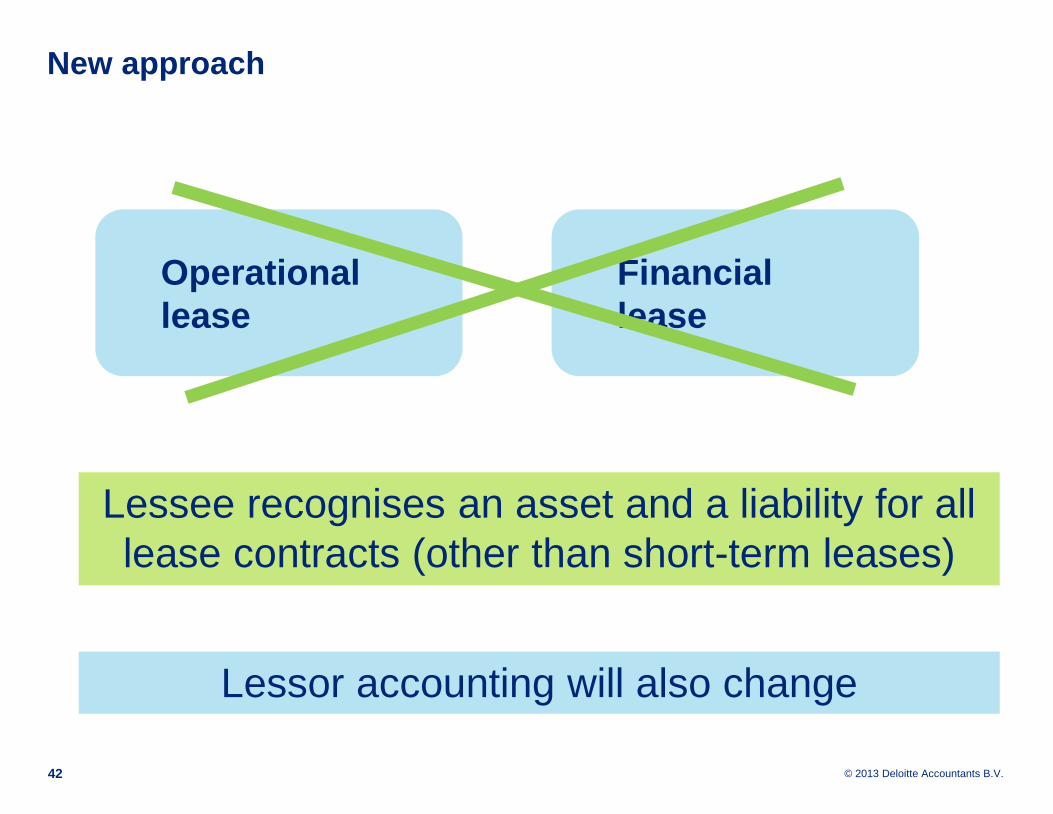

New approach

Financial

lease

Operational

lease

42

Lessee recognises an asset and a liability for all

lease contracts (other than short-term leases)

Lessor accounting will also change

© 2013 Deloitte Accountants B.V.

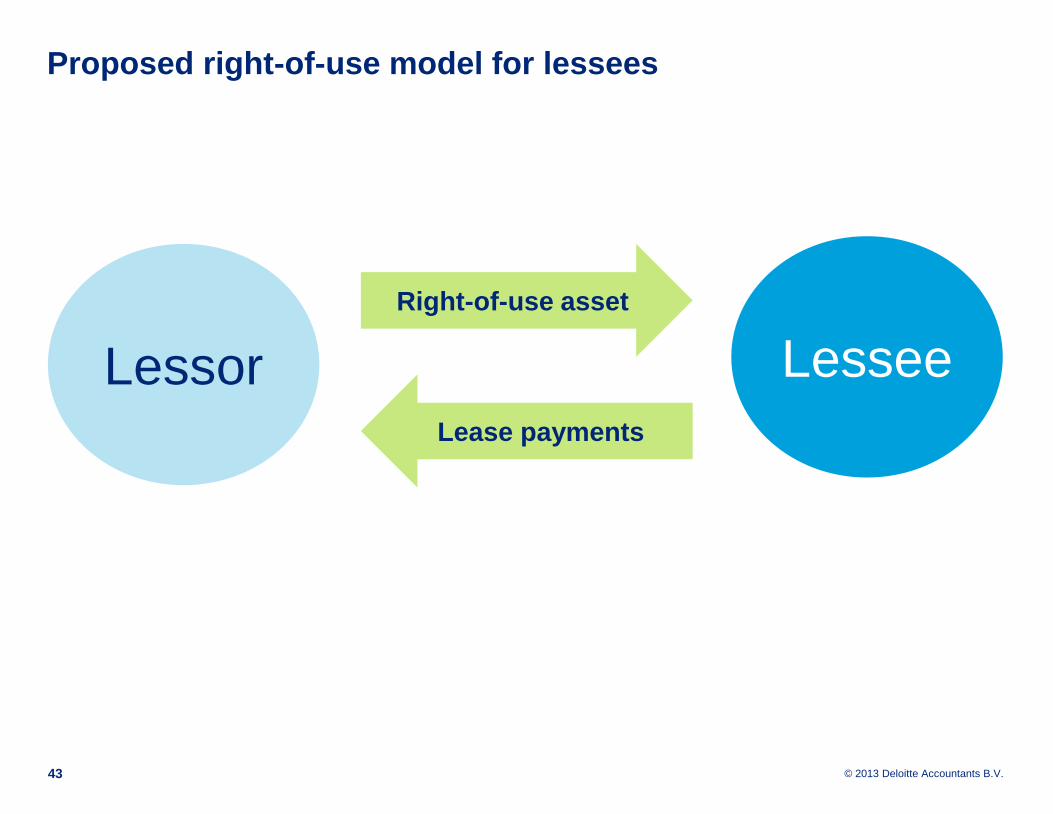

Proposed right-of-use model for lessees

43

Lessor Lessee

Right-of-use asset

Lease payments

© 2013 Deloitte Accountants B.V.

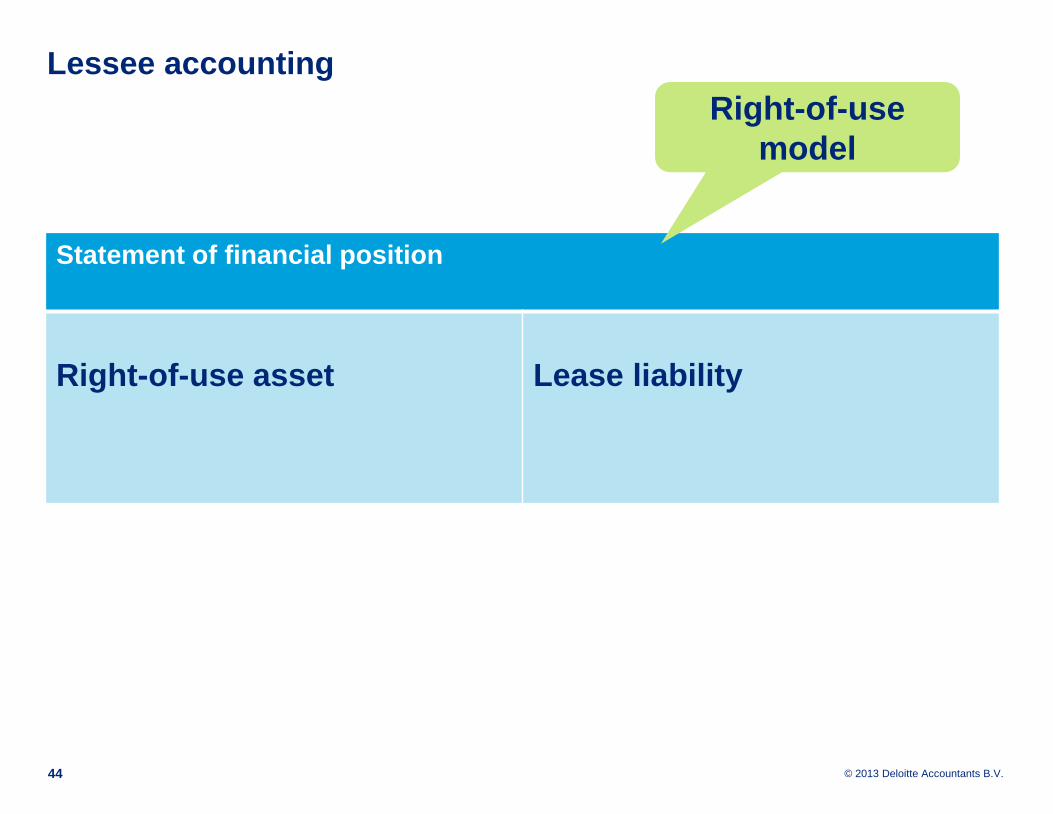

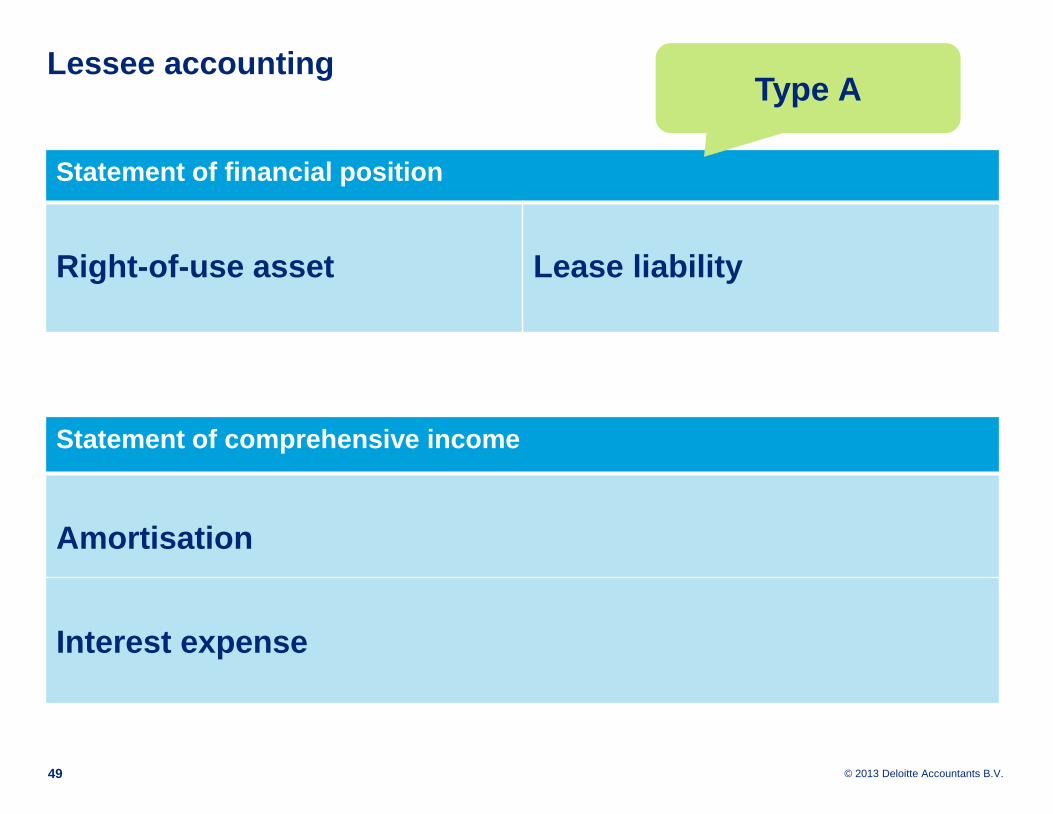

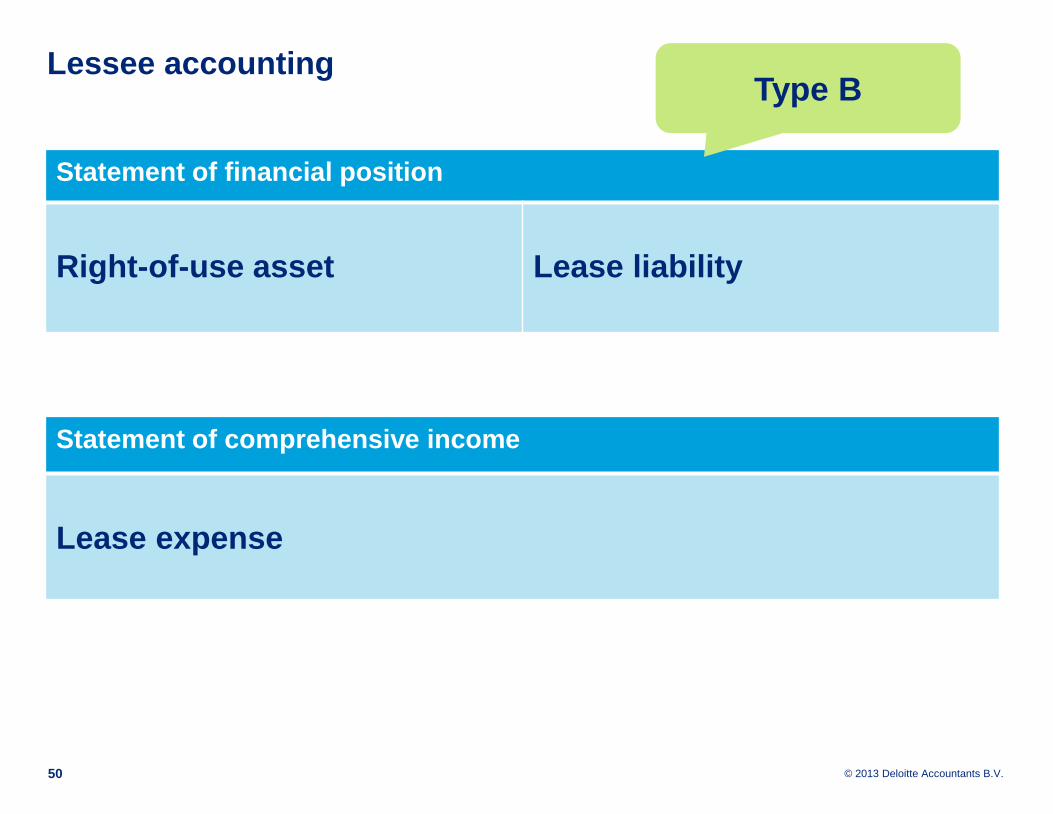

Lessee accounting

Statement of financial position

Right-of-use asset Lease liability

44

Right-of-use

model

© 2013 Deloitte Accountants B.V.

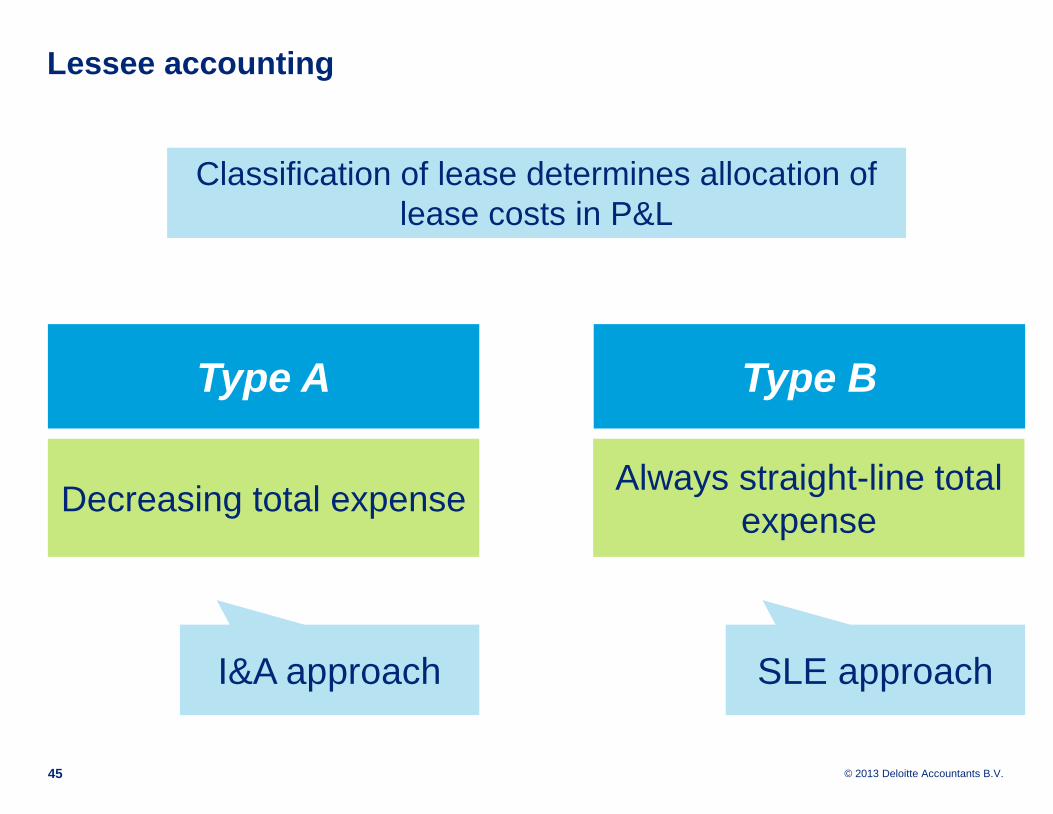

Lessee accounting

45

Type A Type B

Always straight-line total

expenseDecreasing total expense

Classification of lease determines allocation of

lease costs in P&L

I&A approach SLE approach

© 2013 Deloitte Accountants B.V.

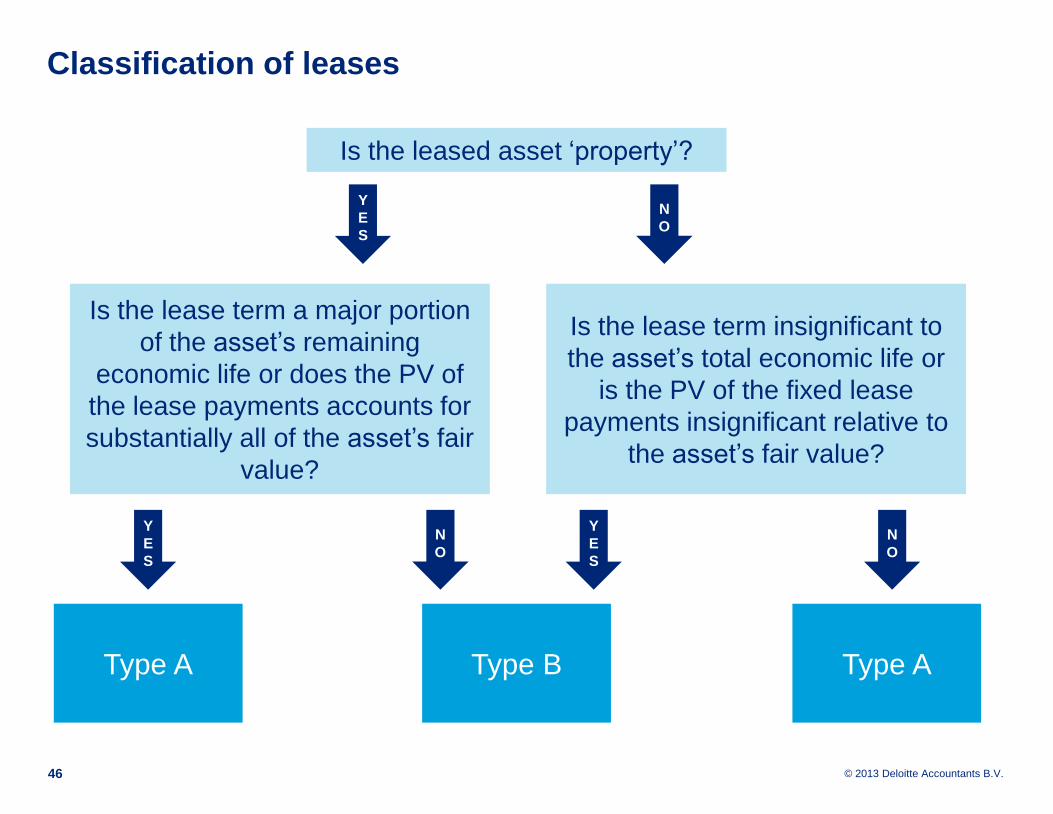

Classification of leases

46

Is the leased asset ‘property’?

Y

E

S

N

O

Is the lease term a major portion

of the asset’s remaining

economic life or does the PV of

the lease payments accounts for

substantially all of the asset’s fair

value?

Y

E

S

N

O

Type A

Is the lease term insignificant to

the asset’s total economic life or

is the PV of the fixed lease

payments insignificant relative to

the asset’s fair value?

N

O

Y

E

S

Type AType B

© 2013 Deloitte Accountants B.V.

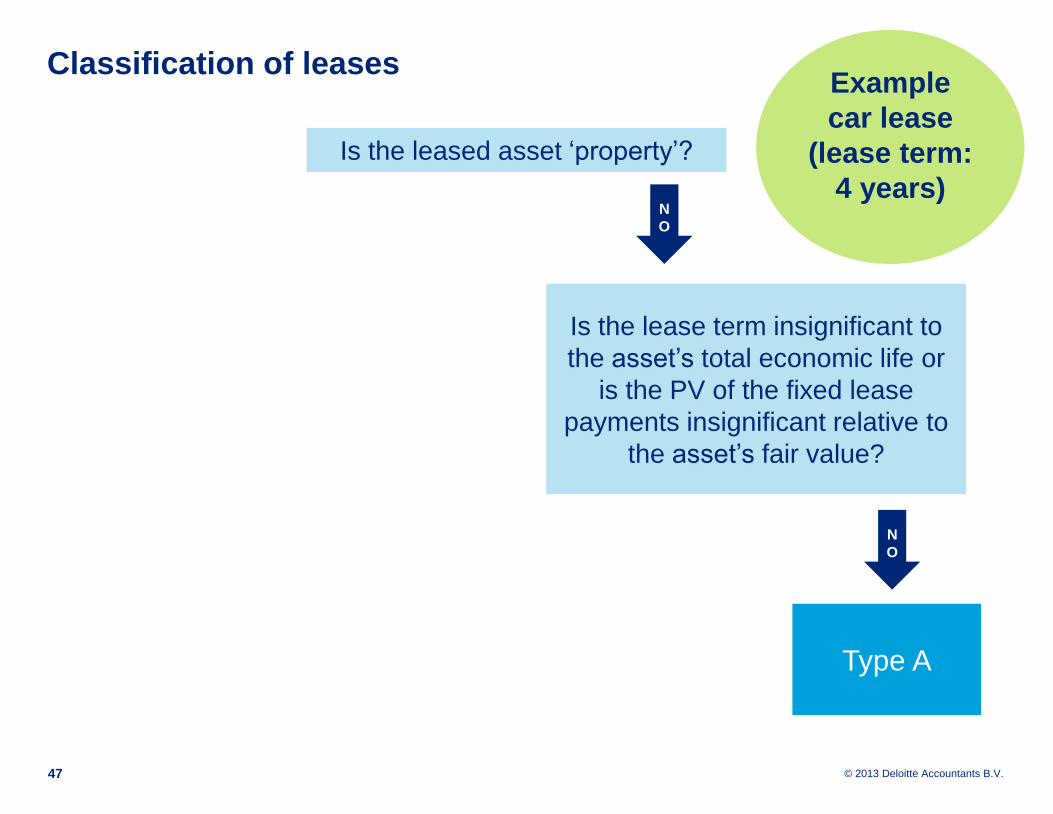

Classification of leases

47

Is the leased asset ‘property’?

N

O

Is the lease term insignificant to

the asset’s total economic life or

is the PV of the fixed lease

payments insignificant relative to

the asset’s fair value?

N

O

Type A

Example

car lease

(lease term:

4 years)

© 2013 Deloitte Accountants B.V.

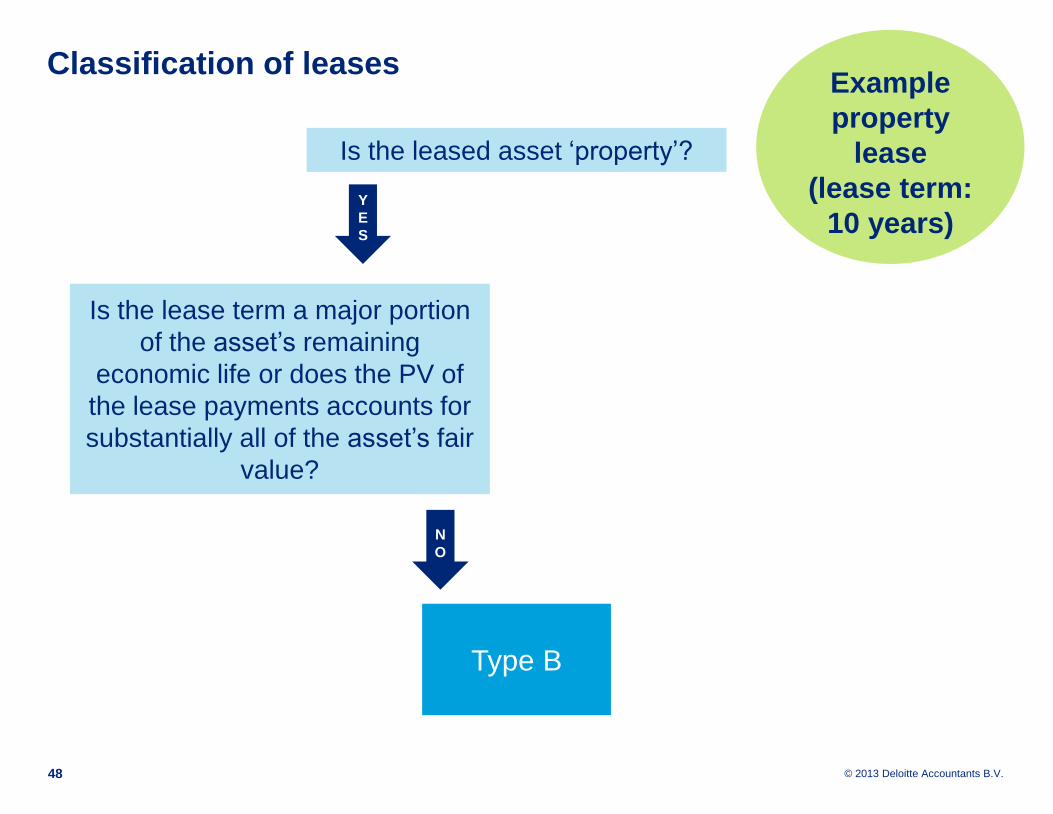

Classification of leases

48

Is the leased asset ‘property’?

Y

E

S

Is the lease term a major portion

of the asset’s remaining

economic life or does the PV of

the lease payments accounts for

substantially all of the asset’s fair

value?

N

O

Type B

Example

property

lease

(lease term:

10 years)

© 2013 Deloitte Accountants B.V.

Lessee accounting

Statement of financial position

Right-of-use asset Lease liability

Statement of comprehensive income

Amortisation

Interest expense

49

Type A

© 2013 Deloitte Accountants B.V.

Lessee accounting

Statement of financial position

Right-of-use asset Lease liability

Statement of comprehensive income

Lease expense

50

Type B

© 2013 Deloitte Accountants B.V.

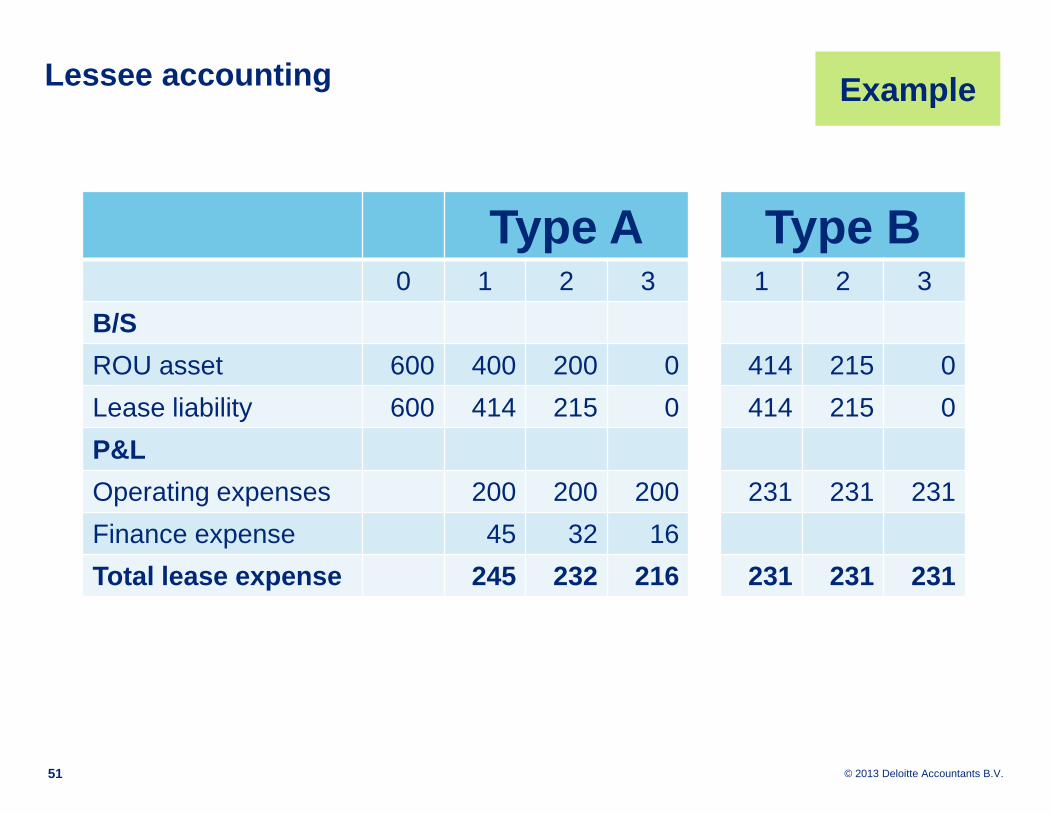

Lessee accounting

51

Type A Type B0 1 2 3 1 2 3

B/S

ROU asset 600 400 200 0 414 215 0

Lease liability 600 414 215 0 414 215 0

P&L

Operating expenses 200 200 200 231 231 231

Finance expense 45 32 16

Total lease expense 245 232 216 231 231 231

Example

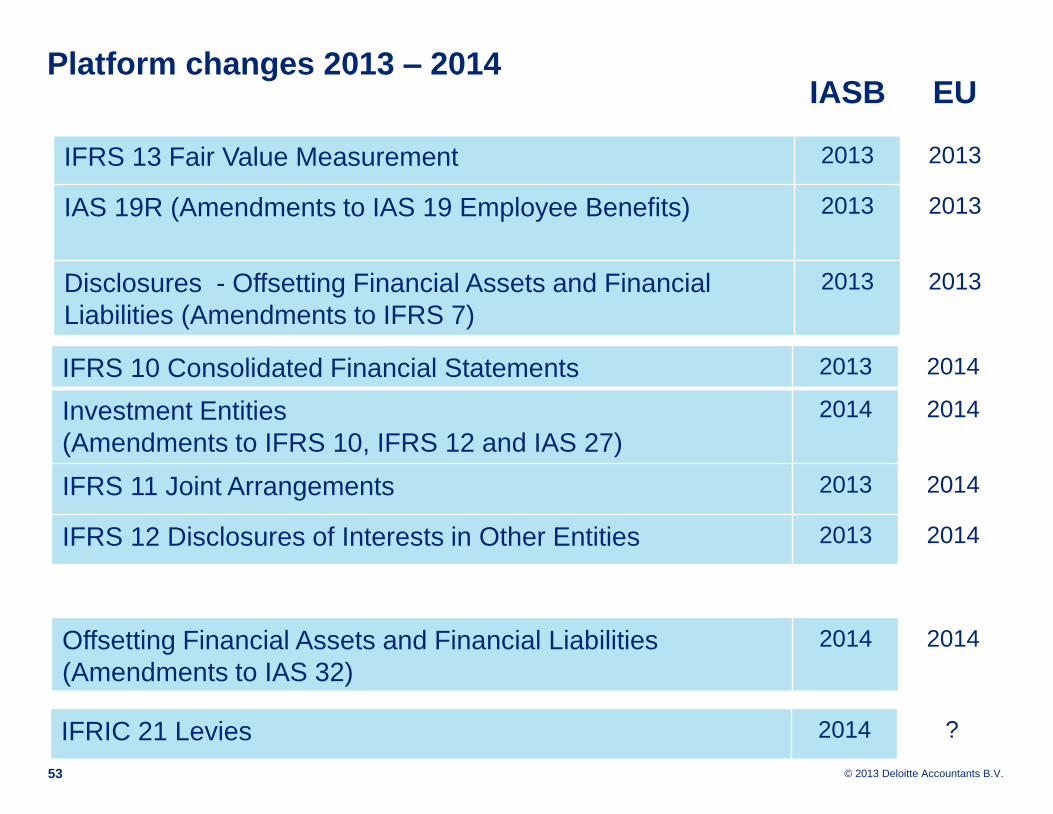

Platform changes 2013 – 2014

© 2013 Deloitte Accountants B.V.

IASB EU

IFRS 13 Fair Value Measurement 2013 2013

IAS 19R (Amendments to IAS 19 Employee Benefits) 2013 2013

Disclosures - Offsetting Financial Assets and Financial

Liabilities (Amendments to IFRS 7)

2013 2013

53

IFRIC 21 Levies 2014 ?

Offsetting Financial Assets and Financial Liabilities

(Amendments to IAS 32)

2014 2014

Platform changes 2013 – 2014

IFRS 10 Consolidated Financial Statements 2013 2014

Investment Entities

(Amendments to IFRS 10, IFRS 12 and IAS 27)

2014 2014

IFRS 11 Joint Arrangements 2013 2014

IFRS 12 Disclosures of Interests in Other Entities 2013 2014

IFRS 13

Fair value measurement

© 2013 Deloitte Accountants B.V.

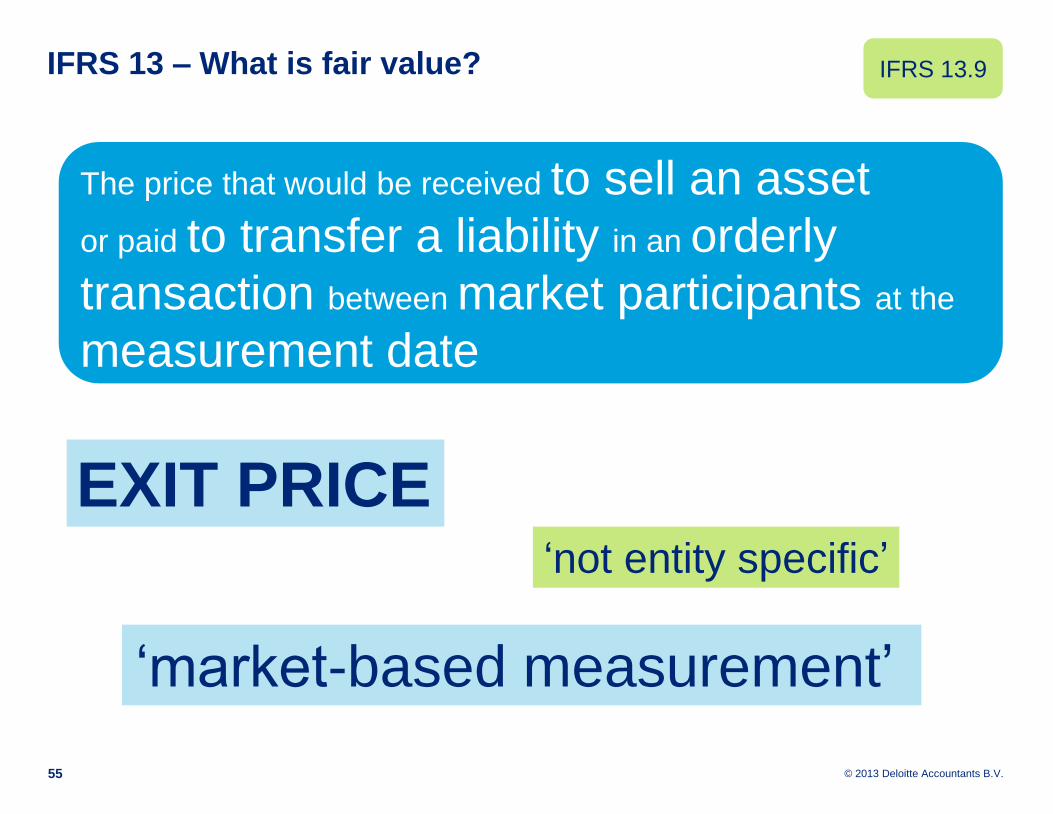

IFRS 13 – What is fair value?

55

The price that would be received to sell an asset

or paid to transfer a liability in an orderly

transaction between market participants at the

measurement date

‘not entity specific’

‘market-based measurement’

IFRS 13.9

EXIT PRICE

© 2013 Deloitte Accountants B.V.

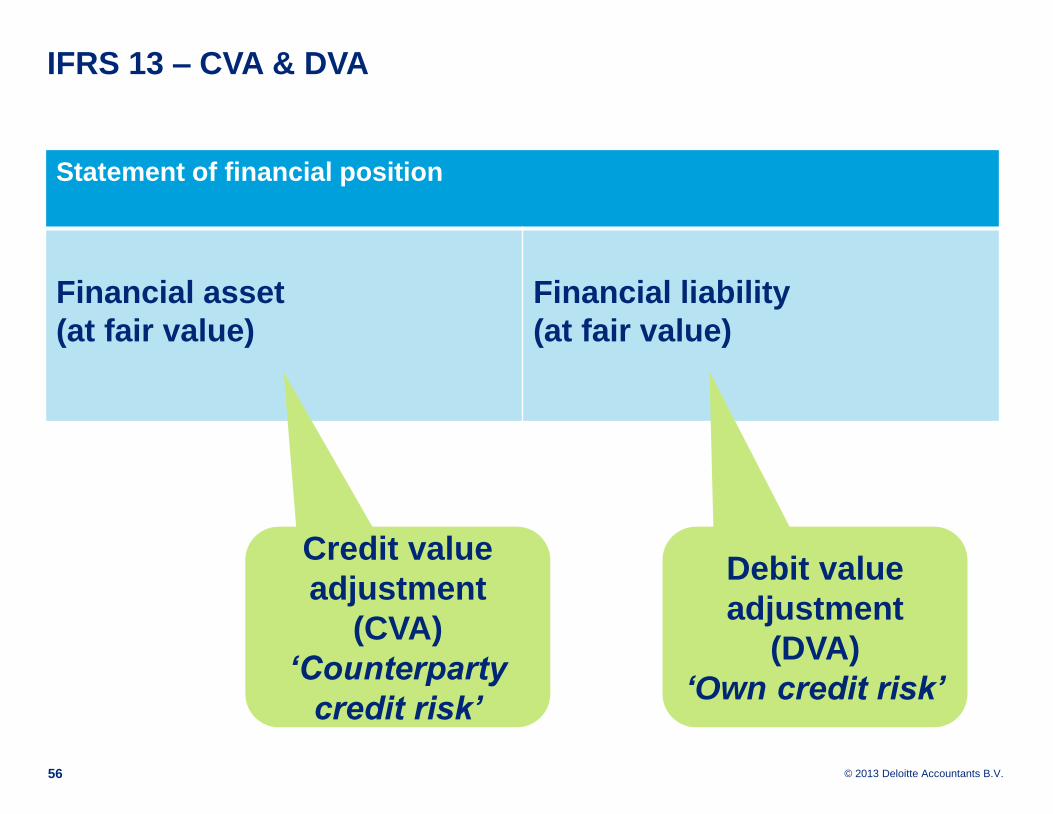

IFRS 13 – CVA & DVA

Statement of financial position

Financial asset

(at fair value)

Financial liability

(at fair value)

56

Credit value

adjustment

(CVA)

‘Counterparty

credit risk’

Debit value

adjustment

(DVA)

‘Own credit risk’

© 2013 Deloitte Accountants B.V.

Vraag

Was u reeds op de hoogte van de

problematiek rond CVA en DVA?

a) Ja

b) Nee

57

© 2013 Deloitte Accountants B.V.

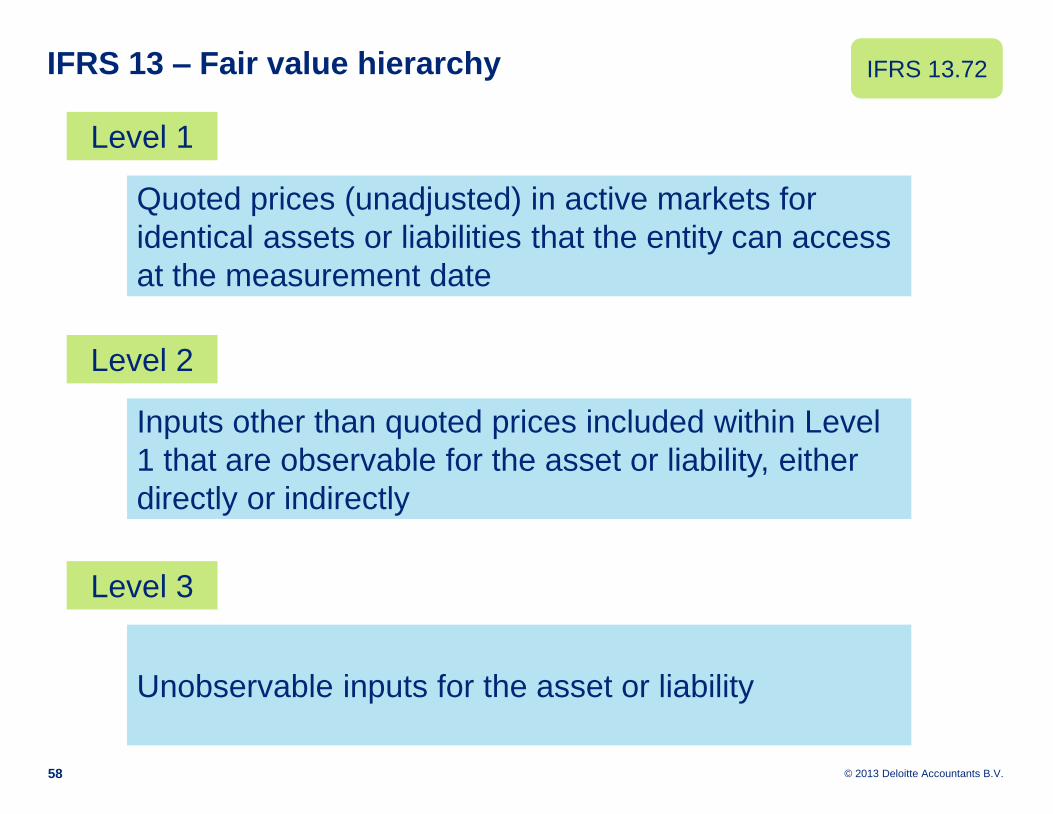

IFRS 13 – Fair value hierarchy

58

IFRS 13.72

Quoted prices (unadjusted) in active markets for

identical assets or liabilities that the entity can access

at the measurement date

Inputs other than quoted prices included within Level

1 that are observable for the asset or liability, either

directly or indirectly

Unobservable inputs for the asset or liability

Level 1

Level 2

Level 3

© 2013 Deloitte Accountants B.V.

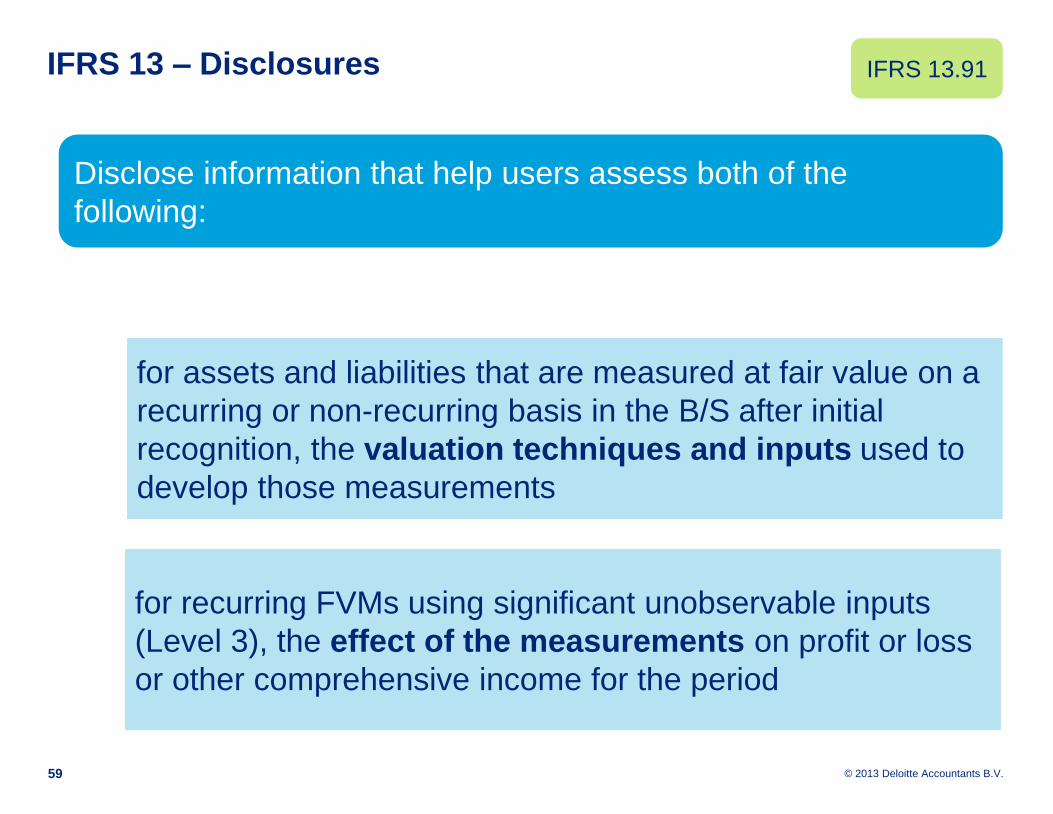

IFRS 13 – Disclosures

59

IFRS 13.91

Disclose information that help users assess both of the

following:

for assets and liabilities that are measured at fair value on a

recurring or non-recurring basis in the B/S after initial

recognition, the valuation techniques and inputs used to

develop those measurements

for recurring FVMs using significant unobservable inputs

(Level 3), the effect of the measurements on profit or loss

or other comprehensive income for the period

© 2013 Deloitte Accountants B.V.

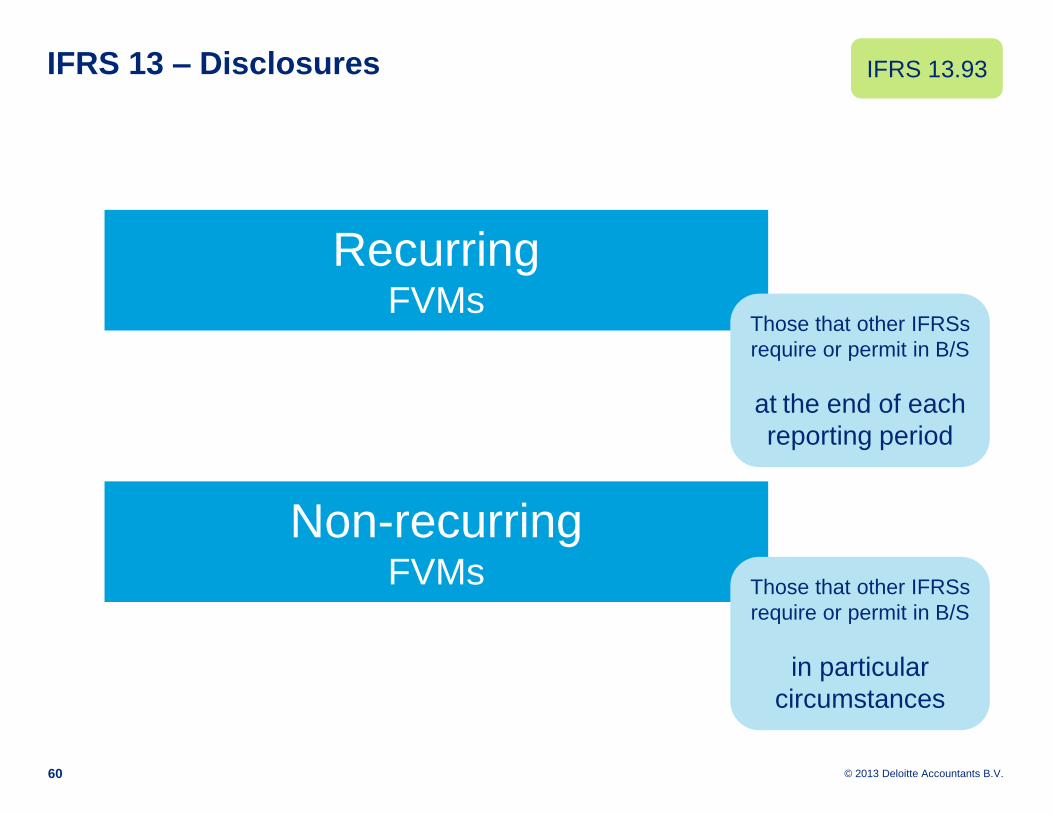

IFRS 13 – Disclosures

60

IFRS 13.93

RecurringFVMs

Non-recurringFVMs

Those that other IFRSs

require or permit in B/S

at the end of each

reporting period

Those that other IFRSs

require or permit in B/S

in particular

circumstances

© 2013 Deloitte Accountants B.V.

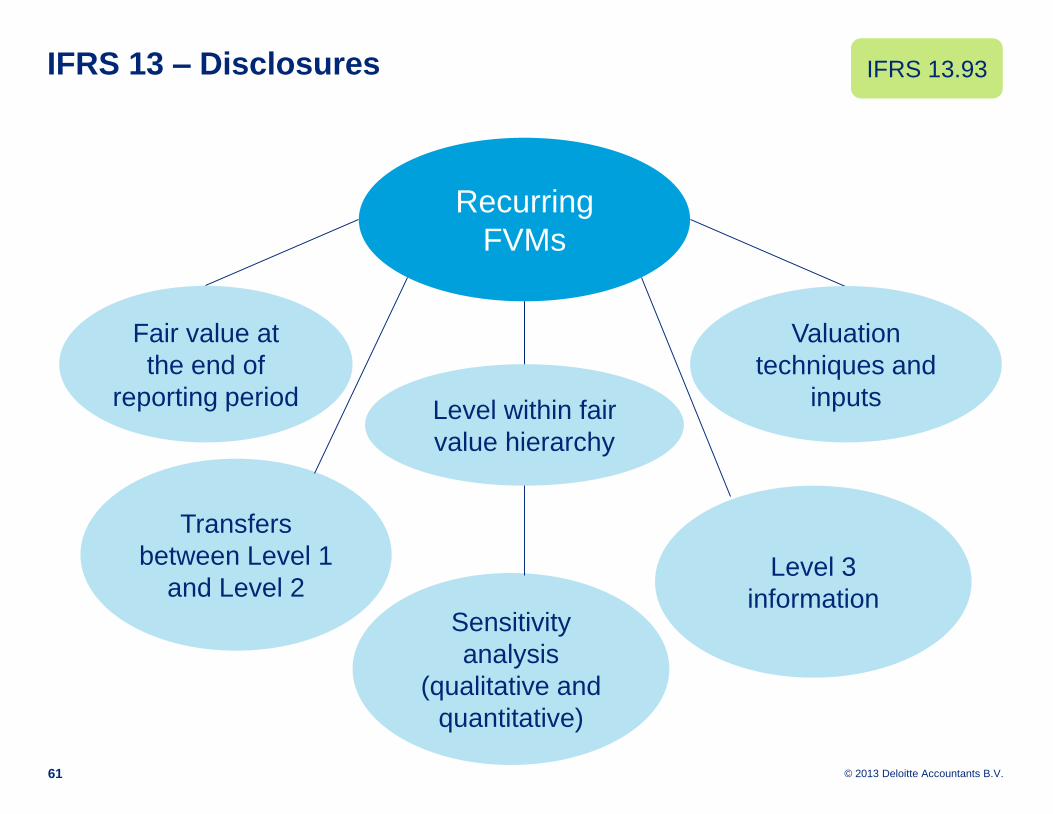

IFRS 13 – Disclosures

Recurring

FVMs

Fair value at

the end of

reporting period

Valuation

techniques and

inputs

Transfers

between Level 1

and Level 2Level 3

information

61

IFRS 13.93

Sensitivity

analysis

(qualitative and

quantitative)

Level within fair

value hierarchy

© 2013 Deloitte Accountants B.V.

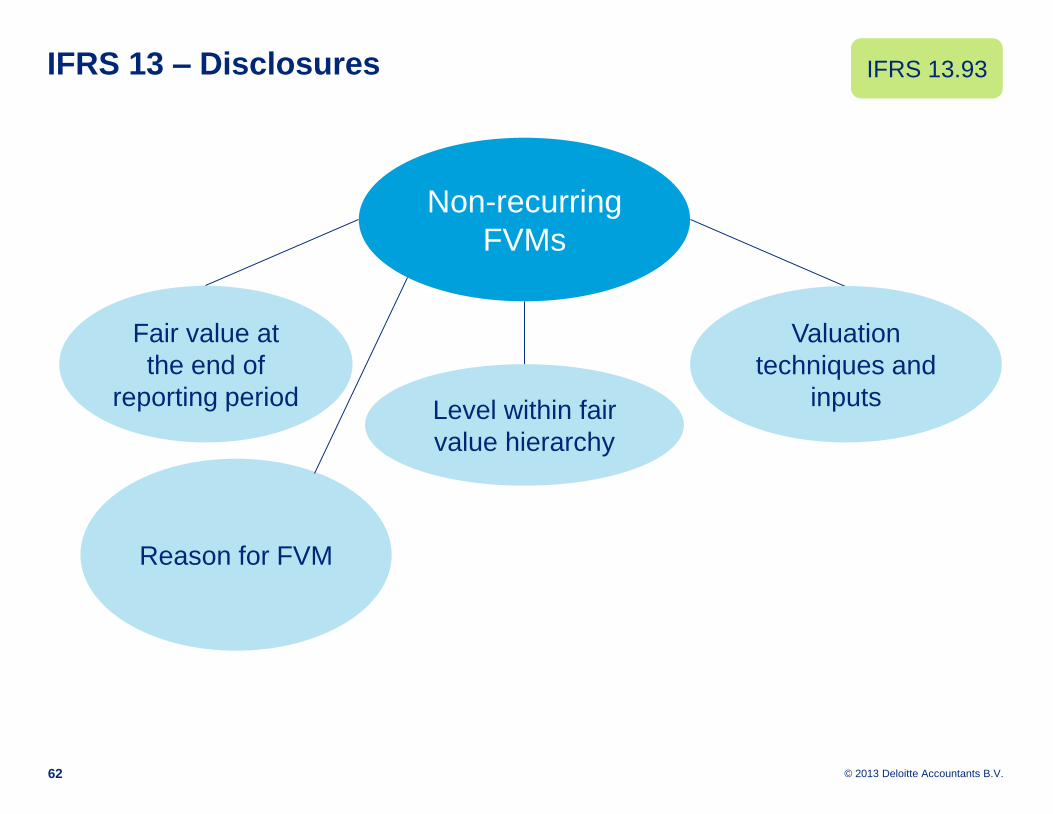

IFRS 13 – Disclosures

Non-recurring

FVMs

Fair value at

the end of

reporting period

Valuation

techniques and

inputs

Reason for FVM

62

IFRS 13.93

Level within fair

value hierarchy

© 2013 Deloitte Accountants B.V.

IFRS 13 – Disclosures

FV in notes

only

Valuation

techniques and

inputs

63

IFRS 13.93

Level within fair

value hierarchy

© 2013 Deloitte Accountants B.V.

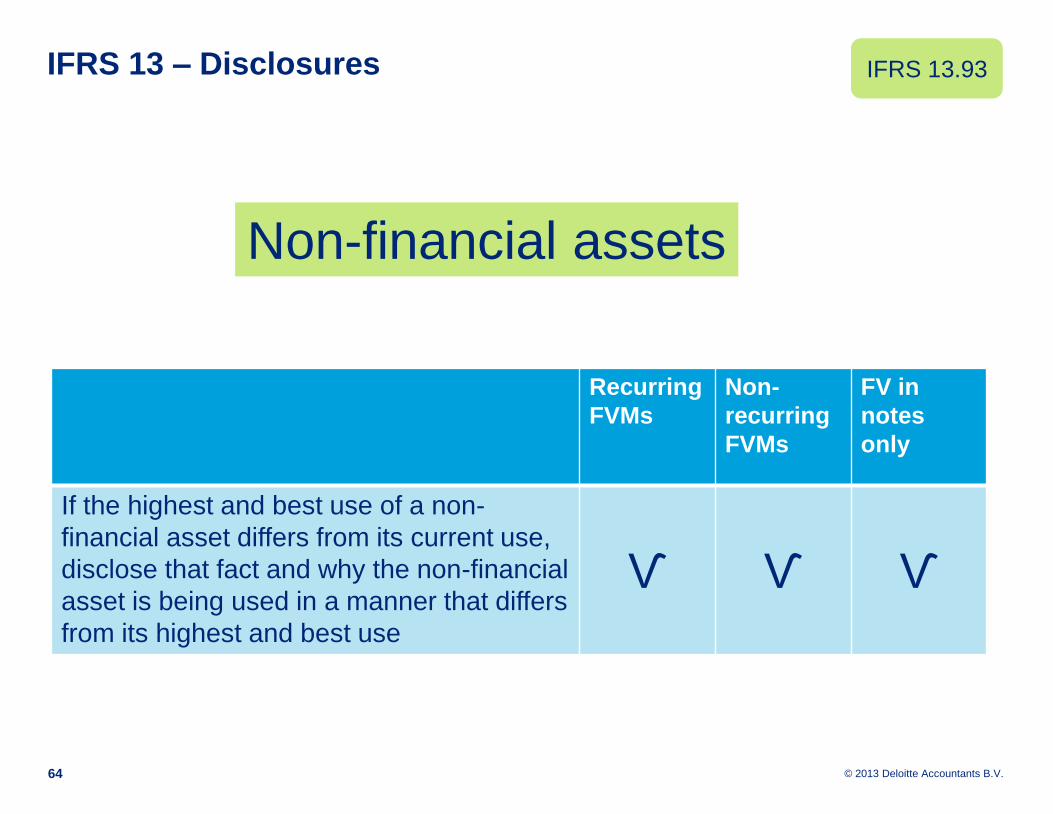

IFRS 13 – Disclosures

64

Recurring

FVMs

Non-

recurring

FVMs

FV in

notes

only

If the highest and best use of a non-

financial asset differs from its current use,

disclose that fact and why the non-financial

asset is being used in a manner that differs

from its highest and best use

Ѵ Ѵ Ѵ

IFRS 13.93

Non-financial assets

Offsetting financial assets

and financial liabilities

© 2013 Deloitte Accountants B.V.

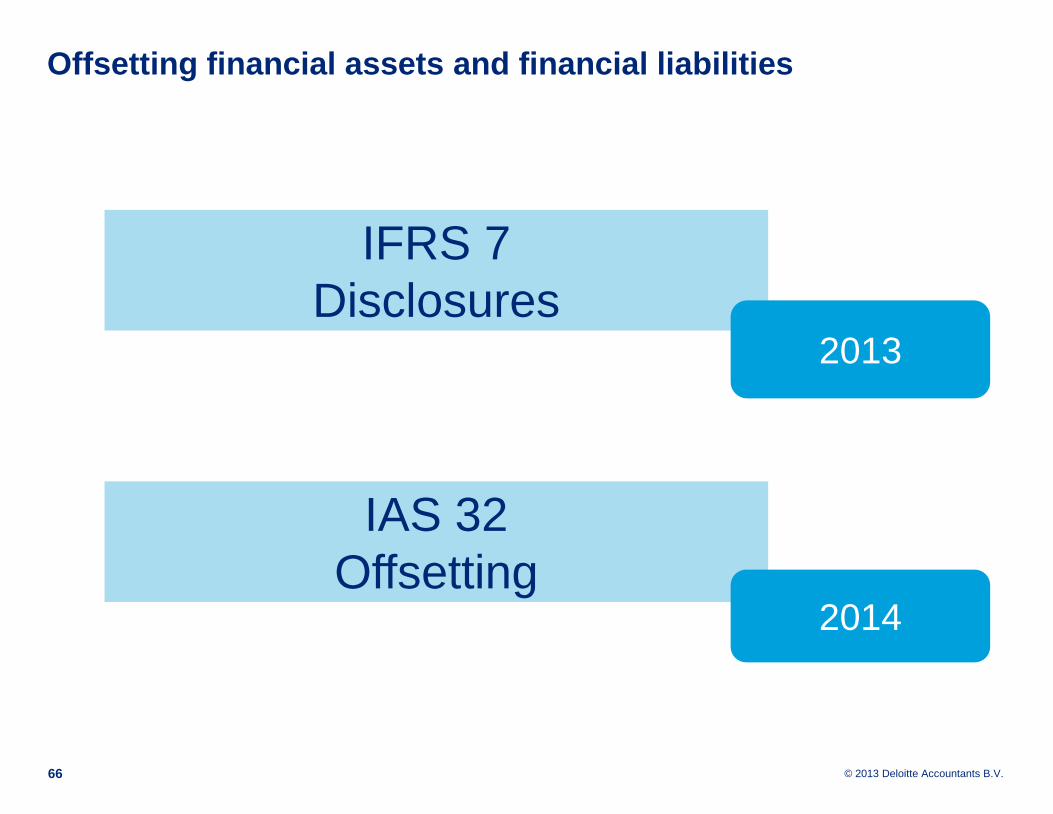

Offsetting financial assets and financial liabilities

66

IFRS 7

Disclosures

IAS 32

Offsetting

2013

2014

© 2013 Deloitte Accountants B.V.

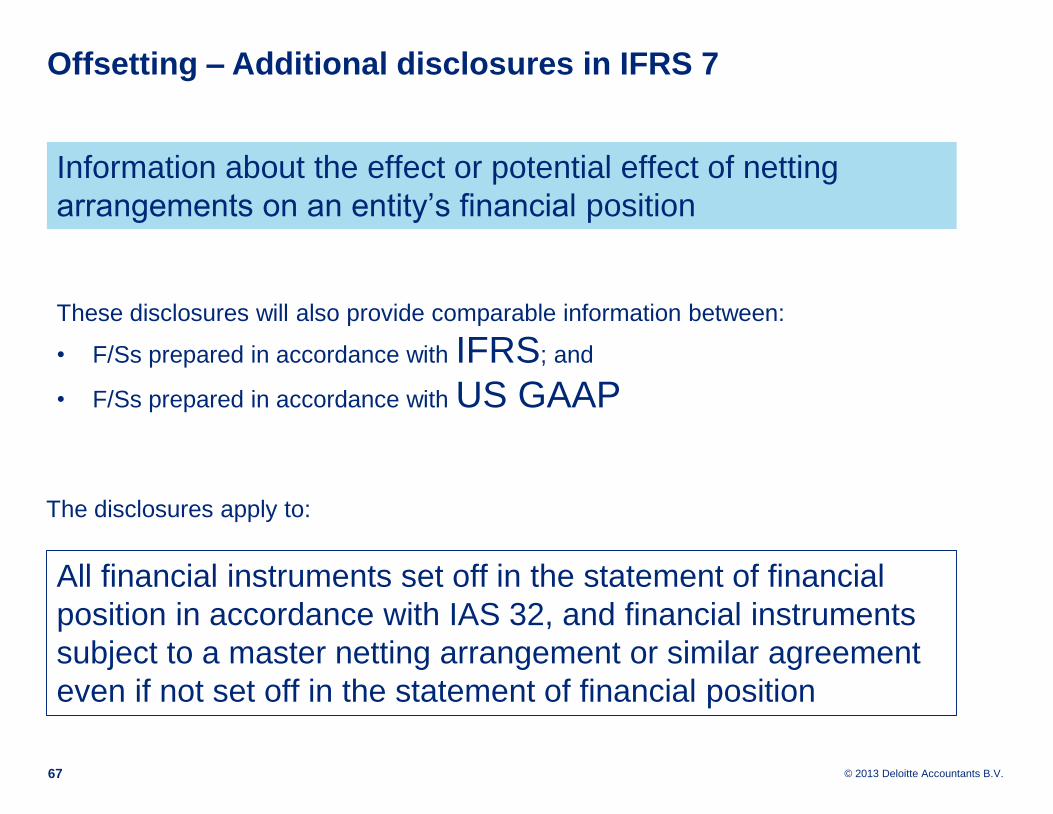

Offsetting – Additional disclosures in IFRS 7

67

Information about the effect or potential effect of netting

arrangements on an entity’s financial position

These disclosures will also provide comparable information between:

• F/Ss prepared in accordance with IFRS; and

• F/Ss prepared in accordance with US GAAP

All financial instruments set off in the statement of financial

position in accordance with IAS 32, and financial instruments

subject to a master netting arrangement or similar agreement

even if not set off in the statement of financial position

The disclosures apply to:

© 2013 Deloitte Accountants B.V.

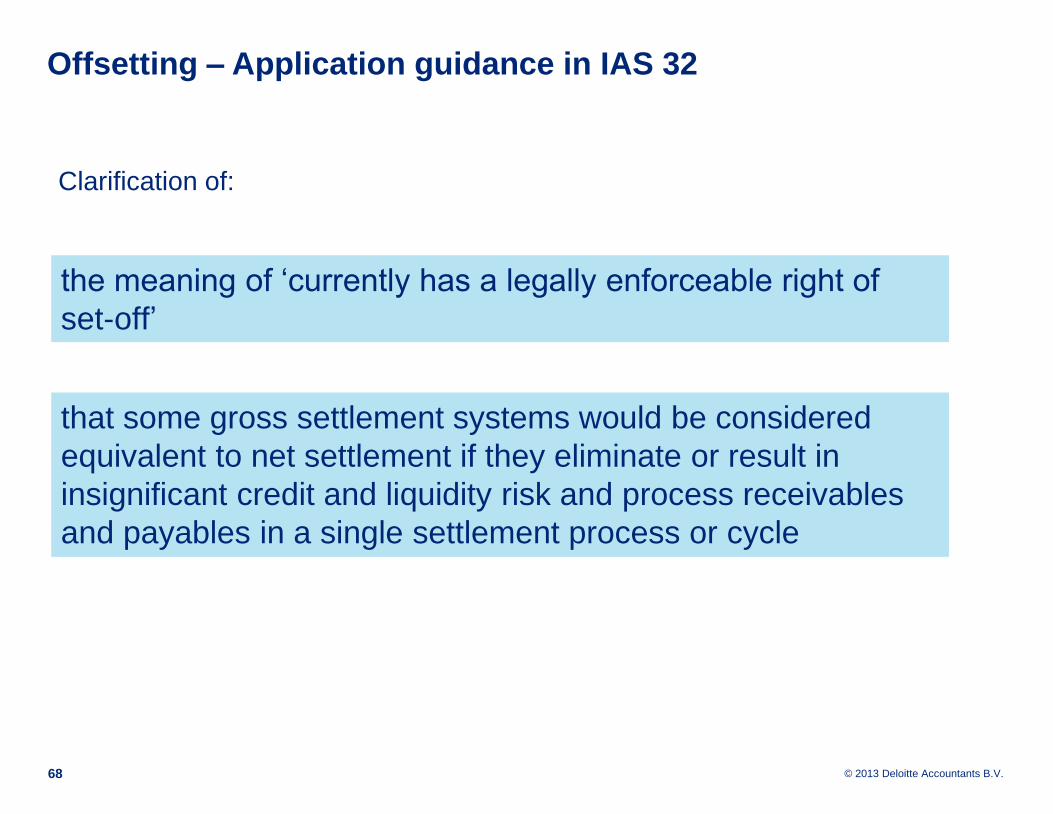

Offsetting – Application guidance in IAS 32

68

the meaning of ‘currently has a legally enforceable right of

set-off’

that some gross settlement systems would be considered

equivalent to net settlement if they eliminate or result in

insignificant credit and liquidity risk and process receivables

and payables in a single settlement process or cycle

Clarification of:

© 2013 Deloitte Accountants B.V.

Vraag

Was u reeds op volledig op de hoogte van

deze nieuwe in 2013 vereiste disclosures?

a) Ja

b) Nee

69

IFRS 10 Consolidated

financial statements

© 2013 Deloitte Accountants B.V.

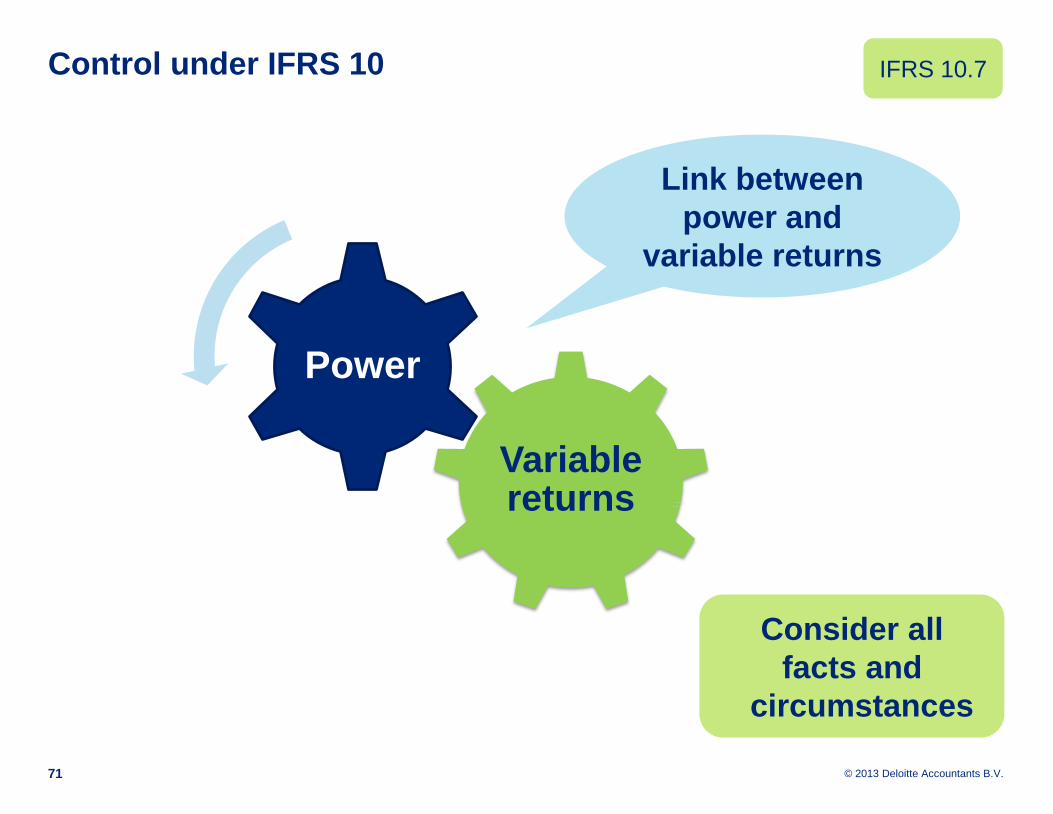

Control under IFRS 10

Variablereturns

Power

Link between

power and

variable returns

IFRS 10.7

71

Consider all

facts and

circumstances

© 2013 Deloitte Accountants B.V.

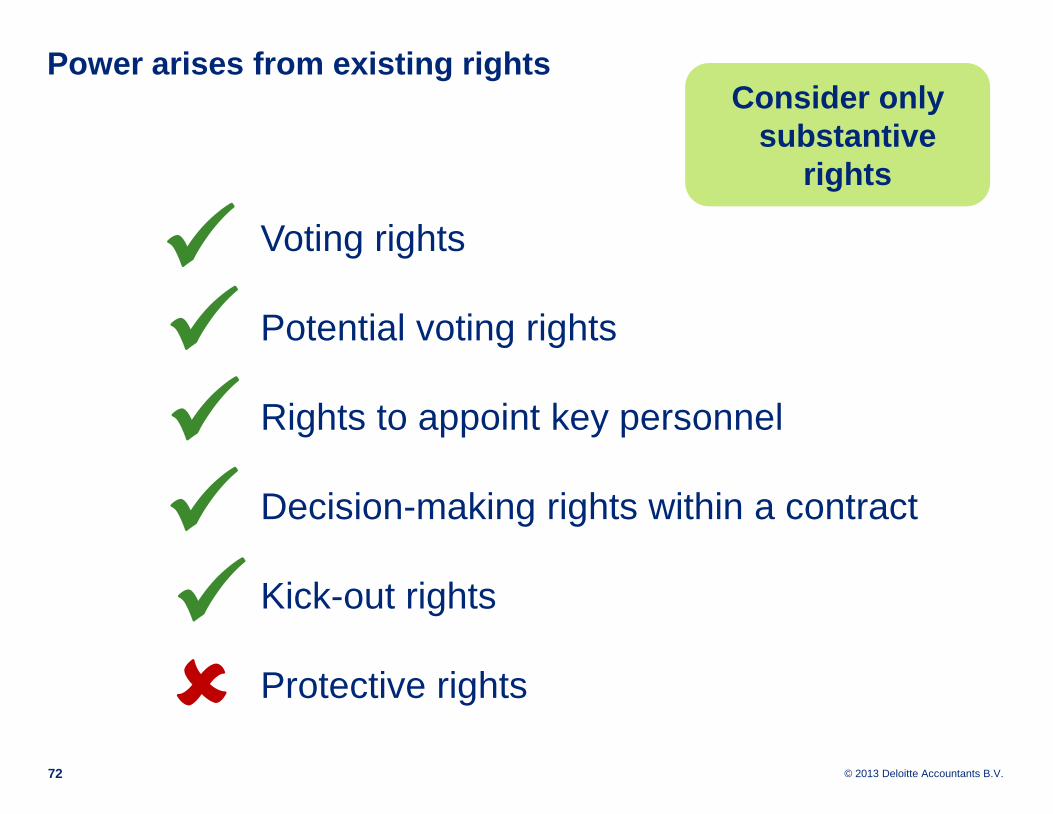

Power arises from existing rights

Voting rights

Potential voting rights

Rights to appoint key personnel

Decision-making rights within a contract

Kick-out rights

Protective rights

72

Consider only

substantive

rights

© 2013 Deloitte Accountants B.V.

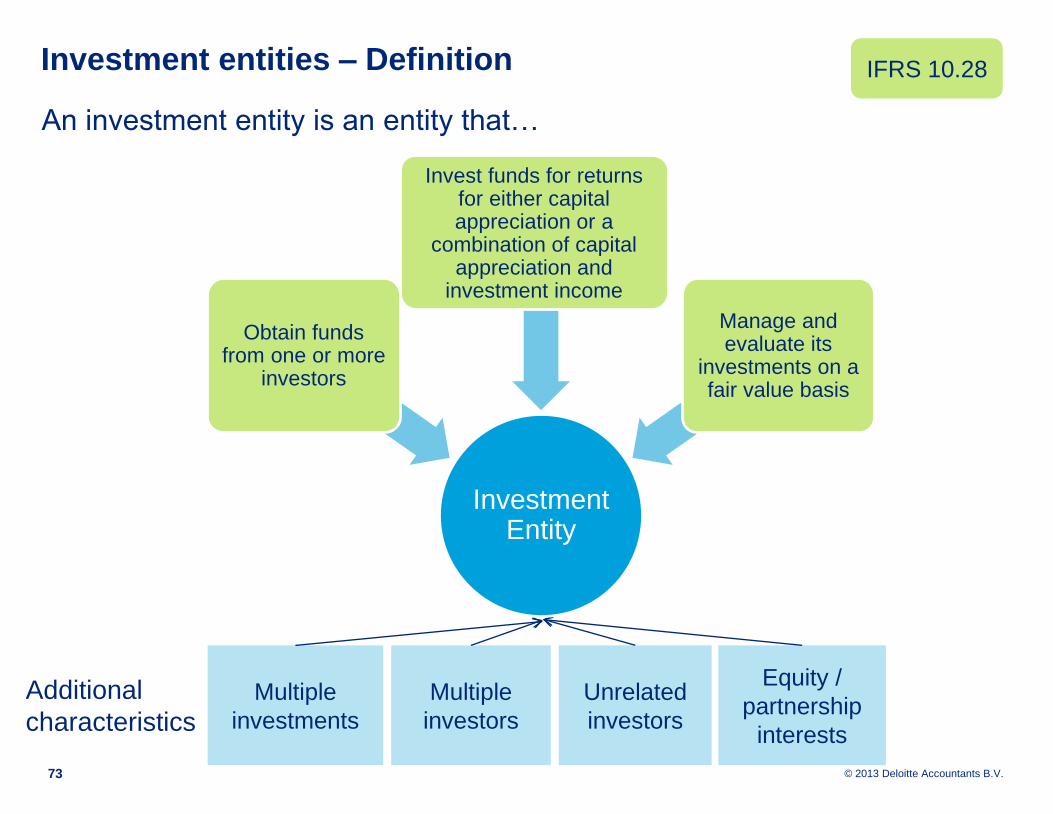

Investment entities – Definition

73

An investment entity is an entity that…

Multiple

investments

Multiple

investors

Equity /

partnership

interests

Additional

characteristicsUnrelated

investors

Investment Entity

Obtain funds from one or more

investors

Invest funds for returns for either capital appreciation or a

combination of capital appreciation and

investment income

Manage and evaluate its

investments on a fair value basis

IFRS 10.28

© 2013 Deloitte Accountants B.V.

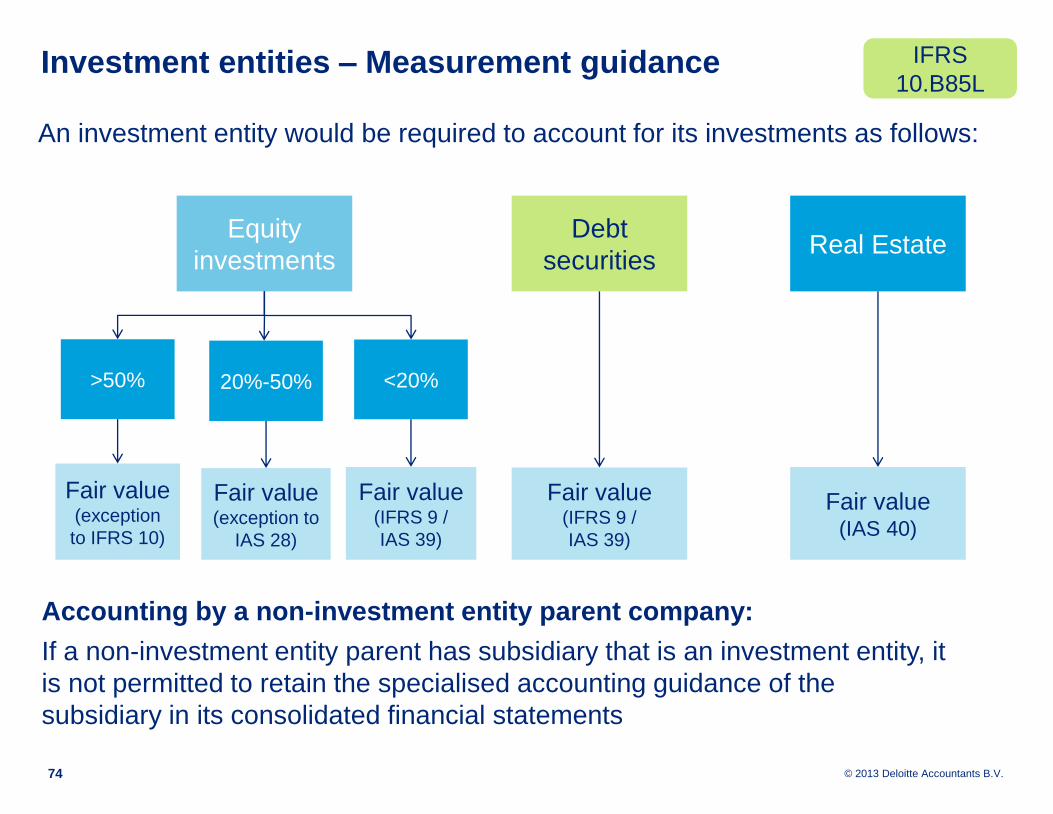

An investment entity would be required to account for its investments as follows:

74

Accounting by a non-investment entity parent company:

If a non-investment entity parent has subsidiary that is an investment entity, it

is not permitted to retain the specialised accounting guidance of the

subsidiary in its consolidated financial statements

Equity

investments

Debt

securitiesReal Estate

>50% 20%-50% <20%

Fair value(exception

to IFRS 10)

Fair value(exception to

IAS 28)

Fair value(IFRS 9 /

IAS 39)

Fair value(IFRS 9 /

IAS 39)

Fair value(IAS 40)

Investment entities – Measurement guidance IFRS

10.B85L

IFRS 11 Joint arrangements

© 2012 Deloitte Accountants B.V.IFRS Update 2012

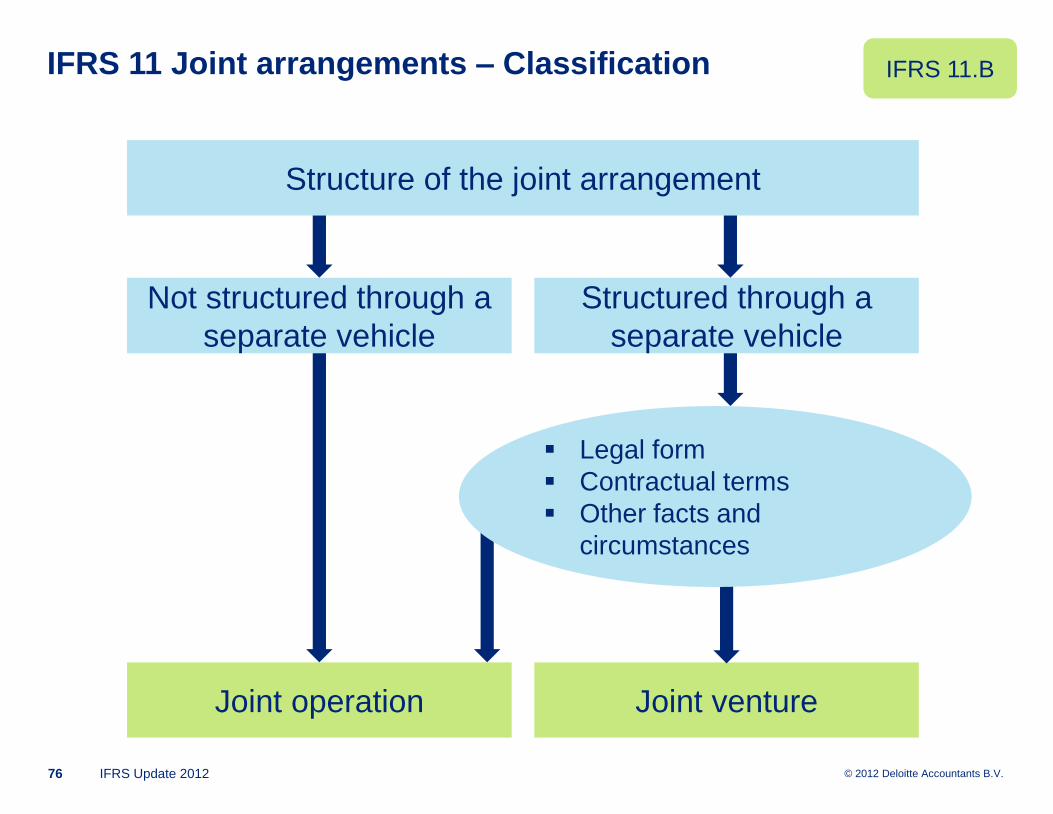

IFRS 11 Joint arrangements – Classification

76

Structure of the joint arrangement

Not structured through a

separate vehicle

Structured through a

separate vehicle

Joint operation Joint venture

Legal form

Contractual terms

Other facts and

circumstances

IFRS 11.B

© 2012 Deloitte Accountants B.V.IFRS Update 2012

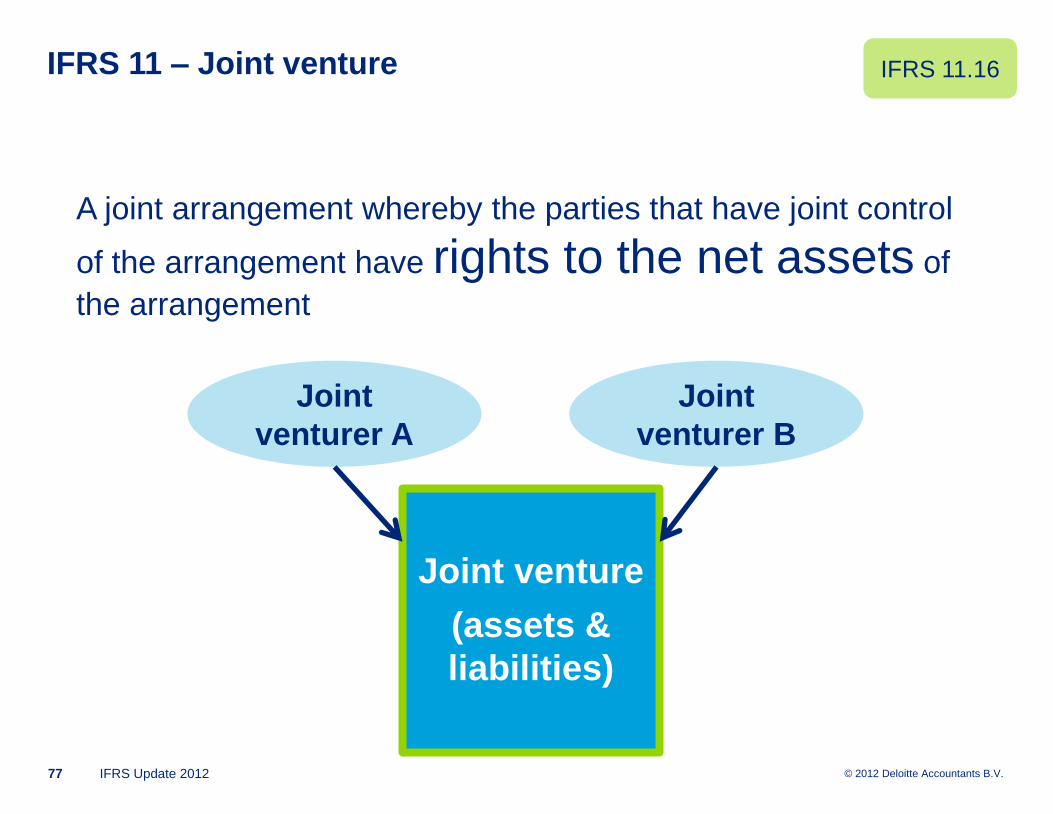

IFRS 11 – Joint venture

77

IFRS 11.16

A joint arrangement whereby the parties that have joint control

of the arrangement have rights to the net assets of

the arrangement

Joint venture

(assets &

liabilities)

Joint

venturer A

Joint

venturer B

© 2012 Deloitte Accountants B.V.IFRS Update 2012

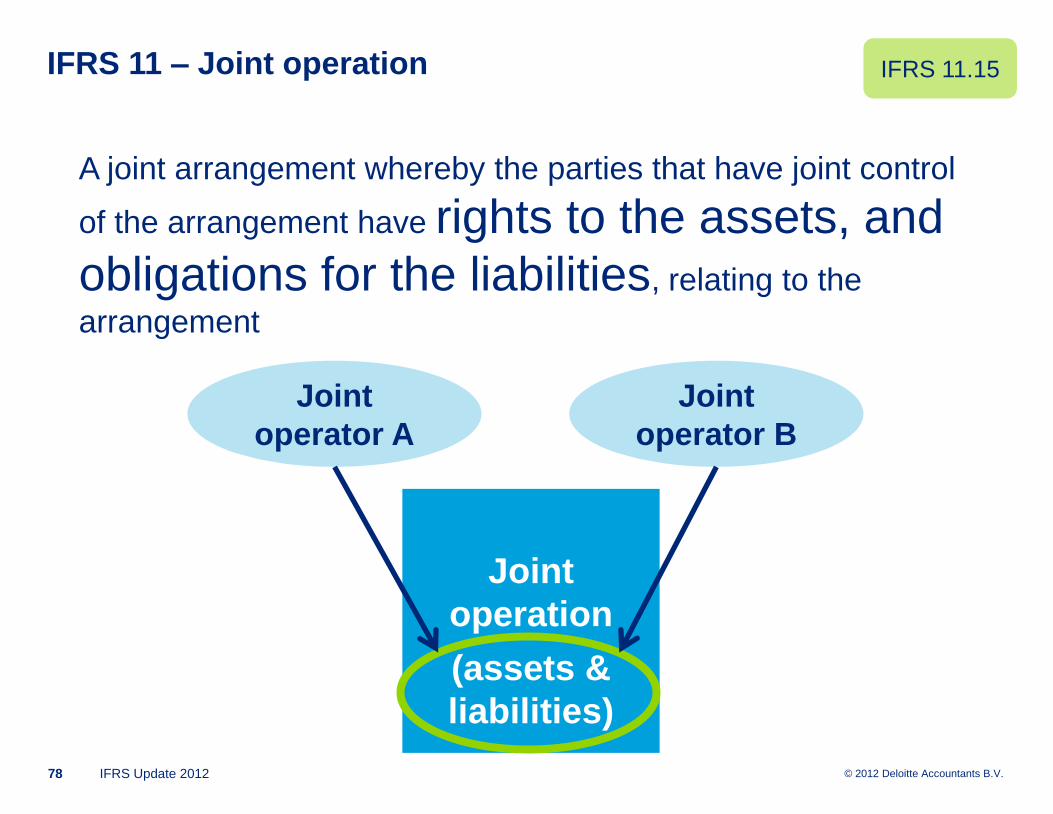

IFRS 11 – Joint operation

78

IFRS 11.15

A joint arrangement whereby the parties that have joint control

of the arrangement have rights to the assets, and

obligations for the liabilities, relating to the

arrangement

Joint

operation

(assets &

liabilities)

Joint

operator A

Joint

operator B

© 2013 Deloitte Accountants B.V.

Vraag

Heeft u al analyses verricht om na te gaan

wat de gevolgen zijn van toepassing van

IFRS 10 en IFRS 11?

a) Ja

b) Nee

79

IFRIC 21 Levies

© 2013 Deloitte Accountants B.V.

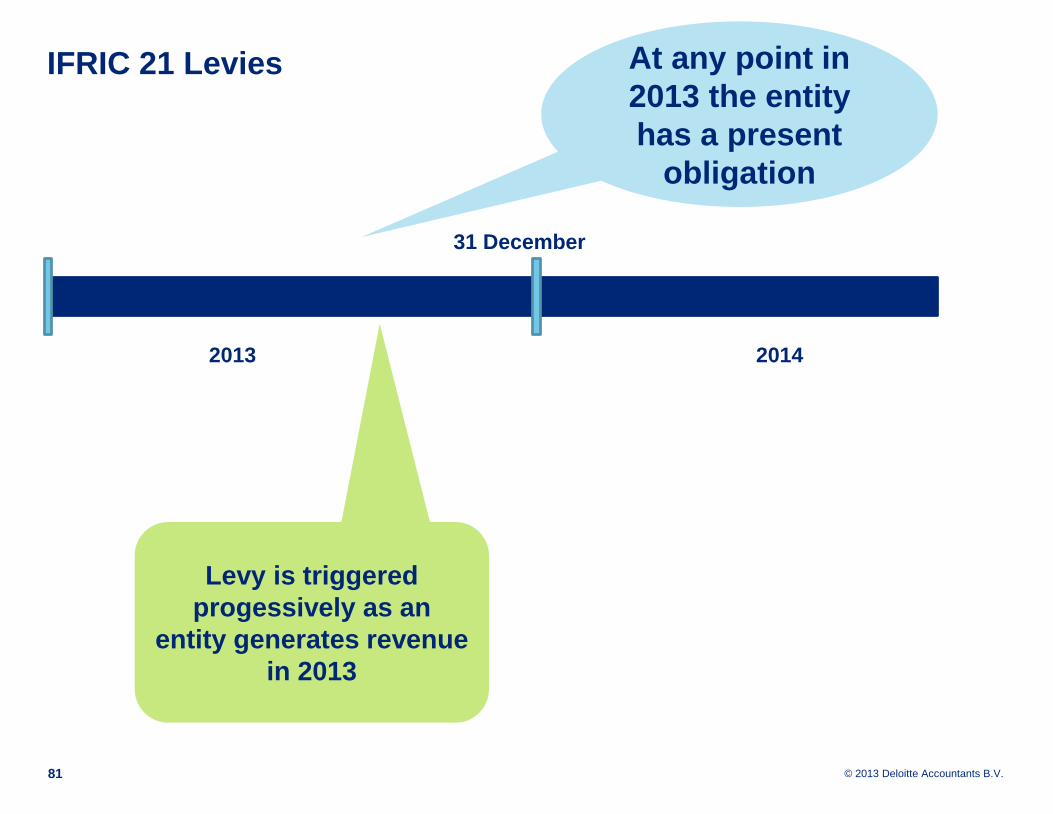

IFRIC 21 Levies

81

2013

31 December

2014

At any point in

2013 the entity

has a present

obligation

Levy is triggered

progessively as an

entity generates revenue

in 2013

© 2013 Deloitte Accountants B.V.

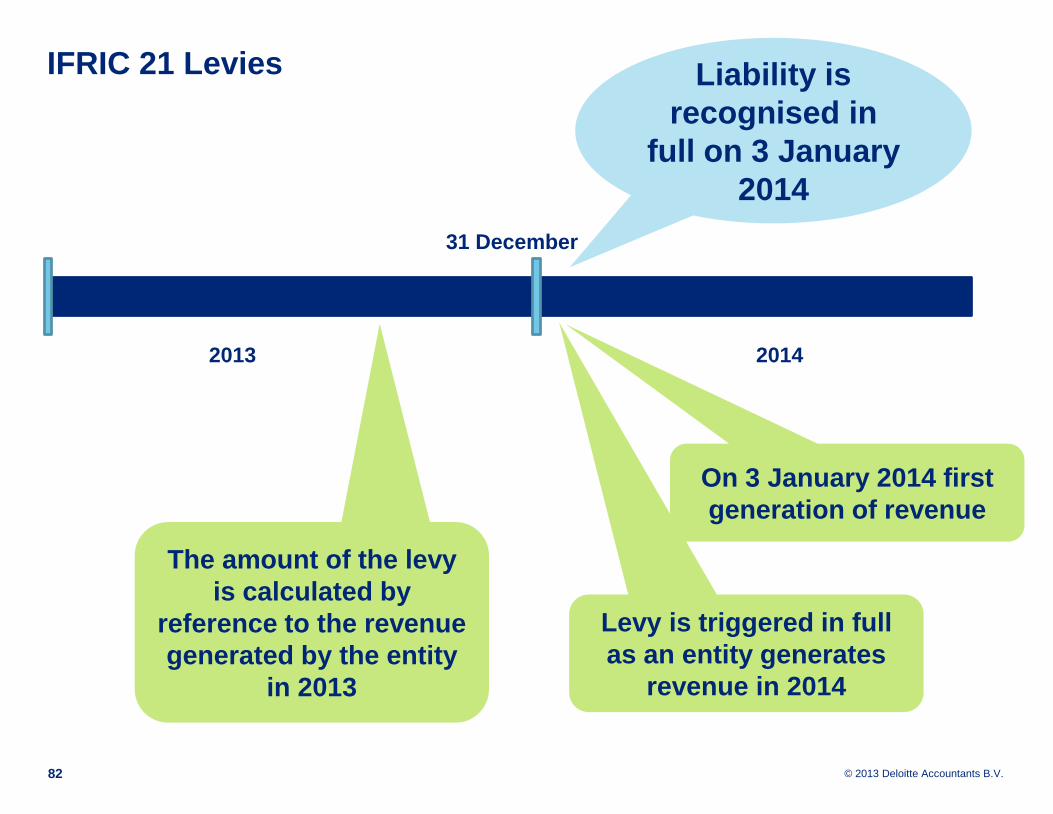

IFRIC 21 Levies

82

2013

31 December

2014

The amount of the levy

is calculated by

reference to the revenue

generated by the entity

in 2013

Levy is triggered in full

as an entity generates

revenue in 2014

Liability is

recognised in

full on 3 January

2014

On 3 January 2014 first

generation of revenue

© 2013 Deloitte Accountants B.V.

IFRIC 21 Levies

83

2013

31 December

2014

The amount of the levy

is calculated by

reference to the

amounts in the financial

statements at the end of

2013

Levy is triggered in full if

an entity operates as a

bank on 1 January 2014

Liability is

recognised in

full on 1 January

2014

IAS 19R Employee benefits

© 2013 Deloitte Accountants B.V.

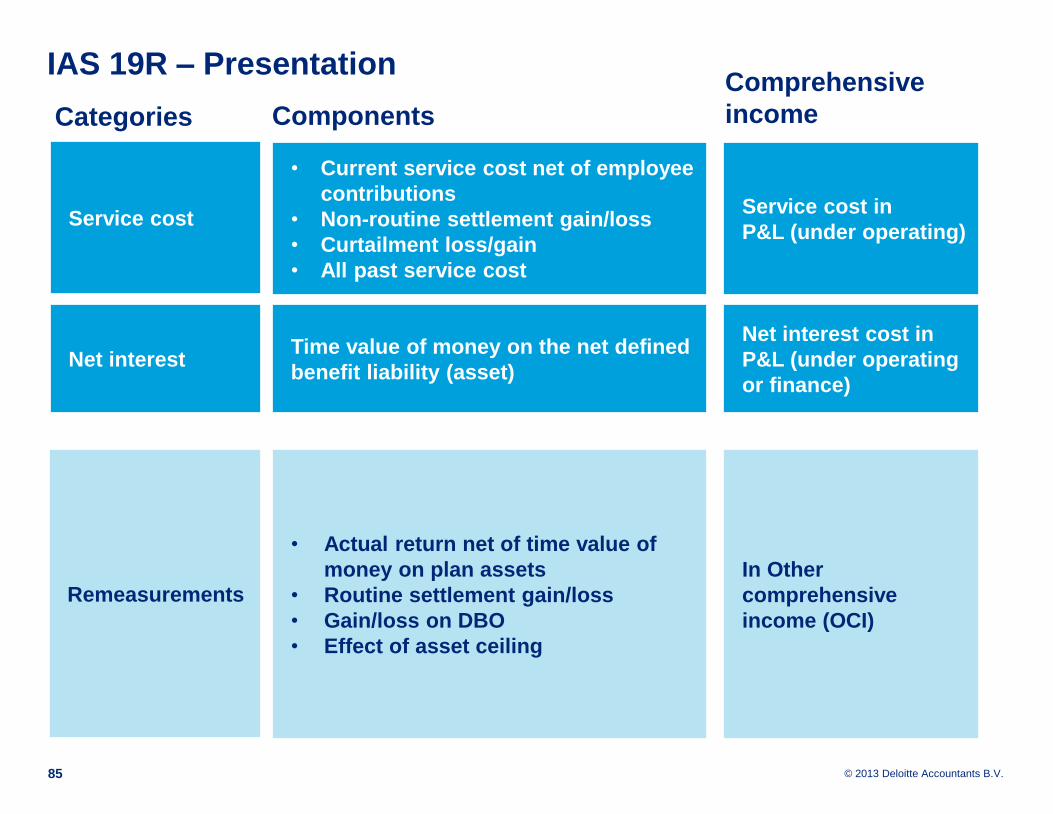

IAS 19R – Presentation

85

Categories Components

Comprehensive

income

Service cost

• Current service cost net of employee

contributions

• Non-routine settlement gain/loss

• Curtailment loss/gain

• All past service cost

Service cost in

P&L (under operating)

Net interestTime value of money on the net defined

benefit liability (asset)

Net interest cost in

P&L (under operating

or finance)

Remeasurements

• Actual return net of time value of

money on plan assets

• Routine settlement gain/loss

• Gain/loss on DBO

• Effect of asset ceiling

In Other

comprehensive

income (OCI)

© 2013 Deloitte Accountants B.V.

IAS 19R – Objective of disclosures

Information

that

Explains the

characteristics of

and risks

associated with its

defined benefit

plans

Identifies and

explains the

amounts in the

F/S’s arising

from its defined

benefit plans

Describes how its

defined benefit

plans may affect

the amount,

timing and

uncertainty of the

entity’s future

cash flows

86

IAS 19.135

© 2013 Deloitte Accountants B.V.

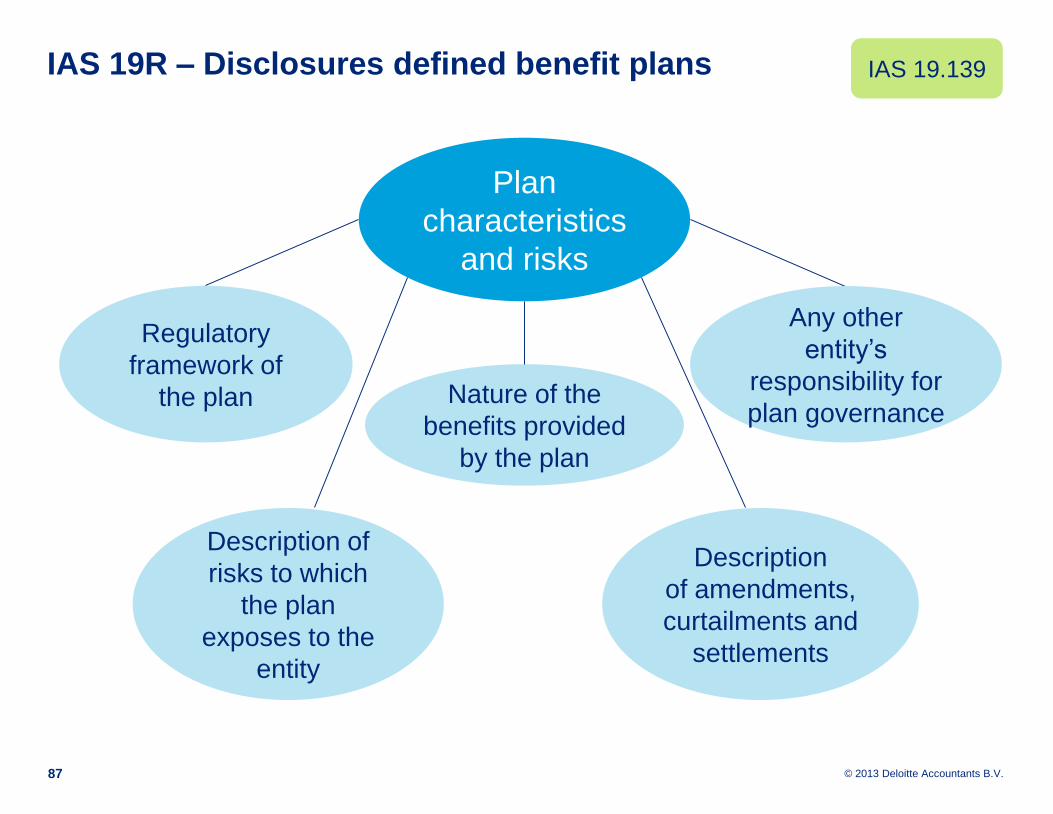

IAS 19R – Disclosures defined benefit plans

Plan

characteristics

and risks

Regulatory

framework of

the plan Nature of the

benefits provided

by the plan

Any other

entity’s

responsibility for

plan governance

Description of

risks to which

the plan

exposes to the

entity

Description

of amendments,

curtailments and

settlements

87

IAS 19.139

© 2013 Deloitte Accountants B.V.

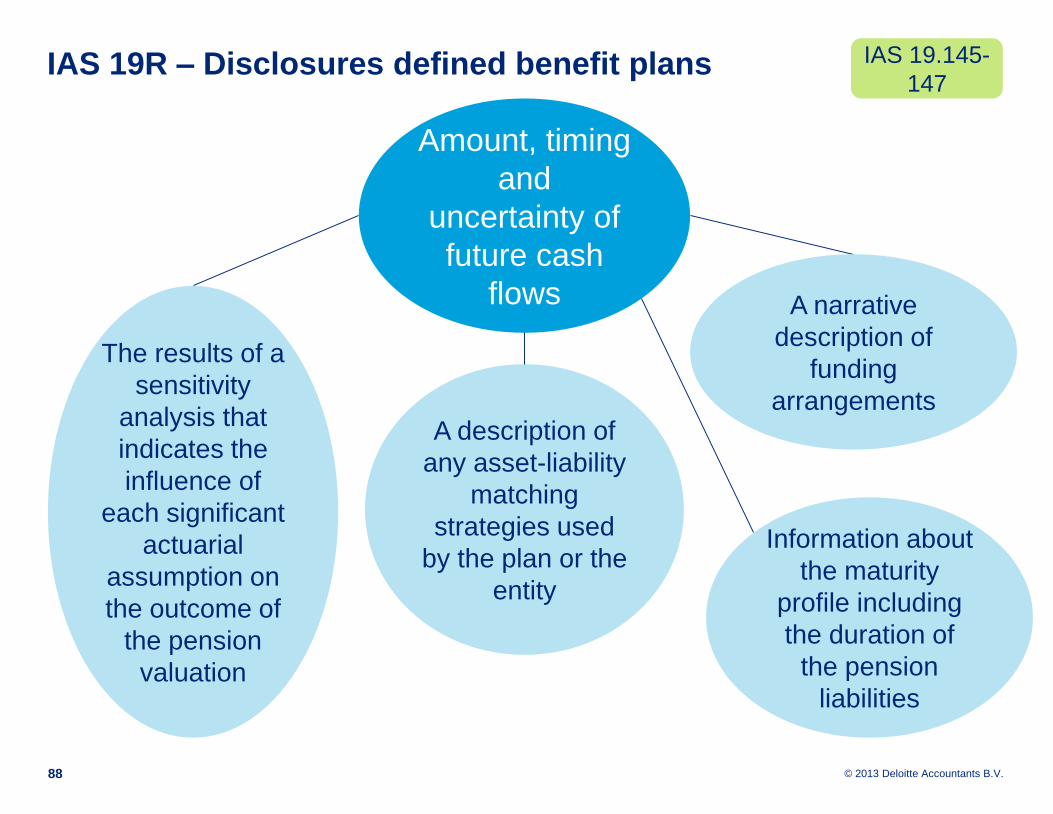

IAS 19R – Disclosures defined benefit plans

Amount, timing

and

uncertainty of

future cash

flows

The results of a

sensitivity

analysis that

indicates the

influence of

each significant

actuarial

assumption on

the outcome of

the pension

valuation

A description of

any asset-liability

matching

strategies used

by the plan or the

entity

A narrative

description of

funding

arrangements

88

IAS 19.145-

147

Information about

the maturity

profile including

the duration of

the pension

liabilities

© 2013 Deloitte Accountants B.V.

IAS 19R – Disclosures defined benefit plans

Multi-employer

plans

The extent to

which the entity

is liable for

other entities’

obligations

Qualitative

information about

agreed

deficit/surplus

allocation on

wind-up or

withdrawal

A narrative

description of

funding

arrangements

(method used to

determine the

entity’s rate of

contributions and

any minimum

funding

requirements

89

IAS 19.148

© 2013 Deloitte Accountants B.V.

IAS 19R – Application problems

• Discount rate (IFRIC)

• Employee contributions (Amendment to IAS 19R)

• Liability ceiling

90

‘Handreiking voor de toepassing

van IAS 19R in de Nederlandse

pensioensituatie’

Conclusions

© 2013 Deloitte Accountants B.V.

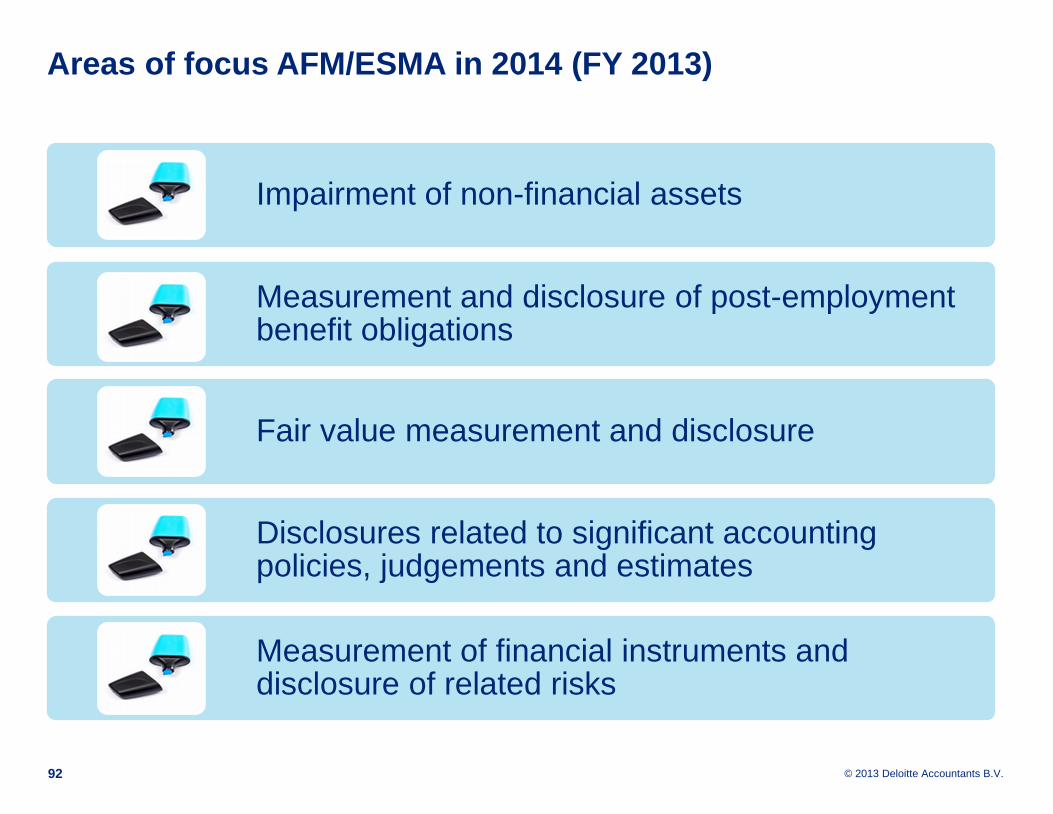

Areas of focus AFM/ESMA in 2014 (FY 2013)

Impairment of non-financial assets

Measurement and disclosure of post-employment benefit obligations

Fair value measurement and disclosure

Disclosures related to significant accounting policies, judgements and estimates

Measurement of financial instruments and disclosure of related risks

92