ifrs institute webcast - visualwebcaster.com

TRANSCRIPT

1

IFRS Institute Webcast

Financial statementFinancial statement presentation andrelated-party disclosures

June 13, 2012

2

Administrative

CPE regulations require online participants take part in online questions. Participants are required to respond to a minimum of four questions in order to be eligible for CPE credit.q p q g

Results will be reviewed in aggregate and may be published as a “pulse survey” of the marketplace in the aggregate. Please note that no responses will be tracked back to any individual or organization.

Send questions via the “Ask a Question” button.

Help Desk: 1-877-398-1471 or outside the United States at 1-954-969-3342

© 2012 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 26440NSS

1

3

Today’s presenters

Paul MunterAudit PartnerU.S. International Financial Reporting Standards (IFRS) Professional Practice Leader

Brian HecklerPartnerAccounting Advisory Services

Kevin BoglegManaging DirectorAccounting Advisory Services

© 2012 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 26440NSS

2

4

Learning objectivesg jBy completing this module, you should beable to:

1) Understand the basic financial statement presentation requirements under IFRS and differences to U.S. GAAP

2) Understand the differences between the requirements under IAS 7 Statement of Cash Flows and U.S. GAAP

3) Explain the requirements of IAS 24Related-Party Disclosures.

5

Presentation offinancial statementsIAS 1 P t ti f Fi i l St t tIAS 1 Presentation of Financial Statements

6

Complete set of financial statements

a) Statement of financial position

b) Statement of comprehensive income

c) Statement of changes in equity

d) Statement of cash flows

e) Notes

f) Statement of financial position as at the beginning of the earliest comparative period whenf) Statement of financial position as at the beginning of the earliest comparative period when an entity restates comparative information, if material, following a:

Change in accounting policy

Correction of an error

Reclassification of items in the financial statements.

U.S. GAAP Difference

© 2012 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 26440NSS

5

7

Knowledge check 1

Which of the following statements is correct?

A. In order to be in compliance with the requirements under IAS 1, a reporting entity needs to prepare at least one year of comparative financial information.

B. In order to be in compliance with the requirements under IAS 1, a reporting entity needs to prepare at least two years of comparative financial information.

C. Similar to U.S. GAAP, there is no requirement under IFRS for inclusion of comparative financial information.

D. The IFRS presentation requirements are identical with those under SEC Regulation S-X Art. 3 General Instructions as to Financial Statements.

© 2012 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 26440NSS

6

8

Knowledge check 1 – Debrief: Correct answer is A

A. Correct, In order to be in compliance with the requirements under IAS 1, a reporting entity needs to prepare at least one year of comparative financial information.p p y p

B. Incorrect

C. Incorrect

D. Incorrect

© 2012 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 26440NSS

7

9

Other components of financial reports

Not within scope of IFRSs, but often presented outside financial statements:

– Financial review by management

Performance

Financial position

– Environmental reports, value-added statements, etc.

IASB issued a document on “Management Commentary” which is not required for entities IASB issued a document on Management Commentary which is not required for entities to be in compliance with IFRS but provides recommendations (similar to MD&A) on issues management may want to discuss

© 2012 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 26440NSS

8

10

Identification of financial statements

Must be clearly identified and distinguished from other information in annual report

Required disclosures:

– Name of entity

– Separate, individual, or consolidated financial statements

– Annual reporting date or reporting period

– Presentation currencyPresentation currency

– Level of rounding

© 2012 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 26440NSS

9

11

Compliance with IFRS

“Explicit and unreserved statement of compliance”

Disclose application of standards or interpretations before effective date

Inappropriate accounting treatments not rectified by additional disclosure

© 2012 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 26440NSS

10

12

Statement of financial position: Current/noncurrent

Present assets and liabilities on face of the Statement of Financial Position as:

– Current/noncurrent

– Broadly in order of liquidity (when reliable and more relevant)

Deferred tax assets and liabilities are noncurrent

© 2012 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 26440NSS

11

13

Statement of financial position: Current/noncurrent (continued)

Assets current if: Liabilities current if:

– Involved in normal operating cycle

– Held primarily for trading purposes

– Expected to be realized within 12 months

– Cash or a cash equivalent

– Involved in normal operating cycle

– Held primarily for trading purposes

– Due to be settled within 12 months

– No unconditional right to defer settlement for at least12 th12 months

All other assets and liabilities are noncurrent

Loans due within 12 months classified as noncurrent if have current ability and expectation to refinance for at least 12 months after reporting date

– Post-balance sheet “cures” or refinancings do not result in noncurrent classification

© 2012 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 26440NSS

12

14

Statement of comprehensive income

All items of income and expense recognized in a period are presented in one or two statements:

– Single statement of comprehensive income

– Separate (but consecutive) income statement and statement of comprehensive income

Statement of comprehensive income includes components of other comprehensive income

Total comprehensive income presented

Changes in equity:

– All nonowner changes in equity presented in the same one or two statements noted above

– Owner changes in equity presented in the statement of changes in equity (not included in the statements above)

© 2012 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 26440NSS

13

IASB/FASB issued amendments to presentation of OCI in June 2011

15

Statement of comprehensive income: Presentation

Analysis of expenses (face or notes): Nature or function

If classification based on function, additional information required:

– Depreciation/amortization

– Employee benefits expense

Separate disclosure of nature and amount of material items of income and expense (face or notes)

U.S. GAAP Difference

No extraordinary items

Other disclosures

Components of other comprehensive income segregated between:

– Items to be recycled to P&L (e.g., unrealized gain/loss on AFS financial assets, cash flow hedges)

© 2012 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 26440NSS

14

g )

– Items not recycled to P&L (e.g., remeasurement gain/loss on postretirement benefit plan, revaluation surplus on PPE, gain/loss on equity securities classified as FVTOCI under IFRS 9)

16

Knowledge check 2

Which of the following statements is correct?

A. IFRS requires that expenses be presented by function.

B. IFRS has detailed industry-specific guidance regarding the presentation of line items in the statement of comprehensive income.

C. Reporting entities which have transitioned from U.S. GAAP to IFRS have an option to stick to the presentation format they used under U.S. GAAP.

D IFRS id ti t t b ith t f ti i th t t tD. IFRS provides an option to present expenses by either nature or function in the statement of comprehensive income.

© 2012 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 26440NSS

15

17

Knowledge check 2 – Debrief: correct answer is D

A. Incorrect

B. Incorrect

C. Incorrect

D. Correct, IFRS provides an option to present expenses by either nature or function in the statement of comprehensive income.

© 2012 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 26440NSS

16

18

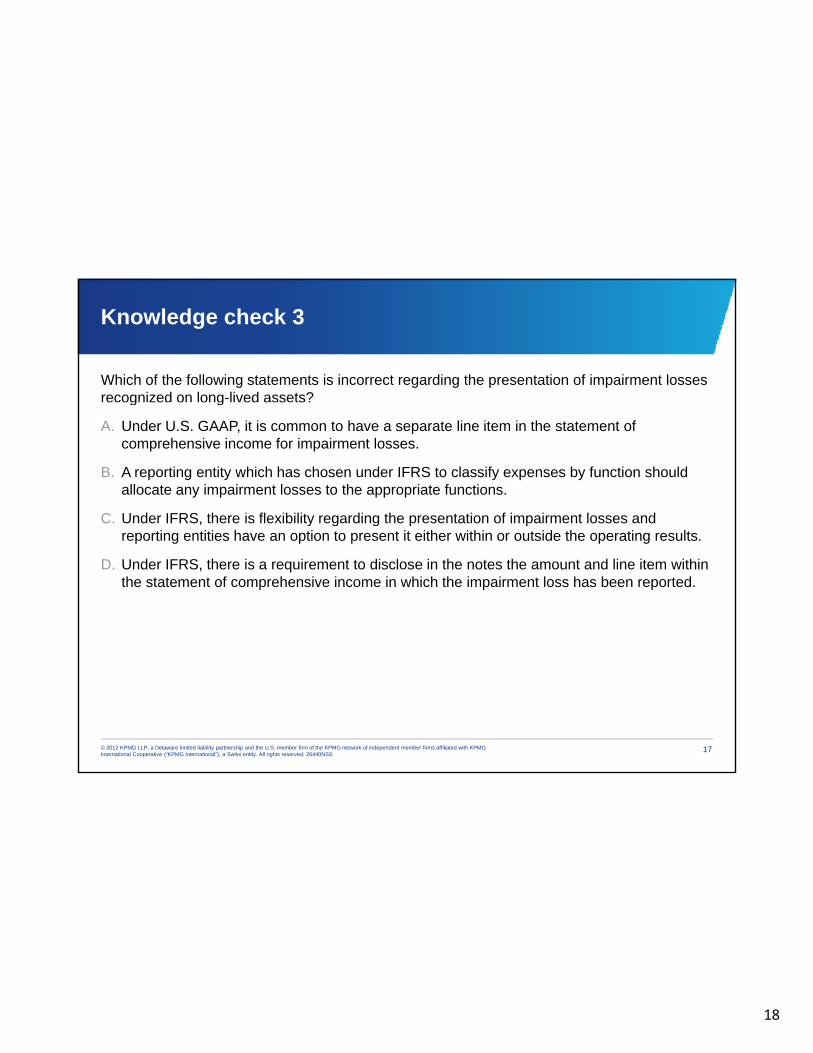

Knowledge check 3

Which of the following statements is incorrect regarding the presentation of impairment losses recognized on long-lived assets?g g

A. Under U.S. GAAP, it is common to have a separate line item in the statement of comprehensive income for impairment losses.

B. A reporting entity which has chosen under IFRS to classify expenses by function should allocate any impairment losses to the appropriate functions.

C. Under IFRS, there is flexibility regarding the presentation of impairment losses and y g greporting entities have an option to present it either within or outside the operating results.

D. Under IFRS, there is a requirement to disclose in the notes the amount and line item within the statement of comprehensive income in which the impairment loss has been reported.

© 2012 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 26440NSS

17

19

Knowledge check 3 – Debrief: correct answer is C

Incorrect

Incorrect

Correct, Impairment losses would be included in operating results.

Incorrect

© 2012 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 26440NSS

18

20

The future of financial statement presentation

The IASB and FASB initiated a joint project on financial statement presentation to address users’ concerns that existing requirements permit too many alternative types of g q p y yppresentation and that information is highly aggregated and inconsistently presented

In October 2008, the Boards published the Discussion Paper Preliminary Views on Financial Statement Presentation

Staff draft of Exposure Draft Financial Statement Presentation was published on July 1, 2010 reflecting the Boards’ cumulative tentative decisions

During October 2010 meeting, Boards decided to focus on the highest priority projects

– Unclear when, if at all, deliberations will resume

© 2012 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 26440NSS

19

21

Proposed classification and presentation

Summary of proposed format

Statement of financial positionStatement of comprehensive

income Statement of cash flowsStatement of financial position income Statement of cash flows

Business section:

Operating category

– Operating finance subcategory

Investing category

Business section:

Operating category

– Operating finance subcategory

Investing category

Business section:

Operating category

Investing category

Income taxes section Financing section:

Debt category

Financing section:

Debt category Debt category Debt category

Equity category

Discontinued operations section Multicategory transaction section Multicategory transaction section

Financing section:

Debt category

Equity category

Income taxes section Income taxes section

© 2012 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 26440NSS

20

q y g y

Discontinued operations section,net of tax

Discontinued operations section

Other comprehensive income section,net of tax

22

The future of financial statement presentation

Financial statement presentation – Other comprehensive income

In June 2011 the IASB and FASB issued amendments to the presentation of items of– In June 2011, the IASB and FASB issued amendments to the presentation of items of other comprehensive income:

Items of profit or loss and items of other comprehensive income must be presented either as:

One combined statement of comprehensive income, or

Two consecutive statements: income and other comprehensive incomep

IASB requirement to present separately items in OCI that will and will not be reclassified subsequently to profit or loss

Mandatory for annual periods beginning on or after July 1, 2012, early adoption permitted

Financial statement presentation – Discontinued operations

© 2012 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 26440NSS

21

– Joint project to establish a common definition of discontinued operations and require common disclosures

Project on hold until completion of the highest priority projects

23

Statement of cash flowsIAS 7 St t t f C h FlIAS 7 Statement of Cash Flows

24

Statement of cash flows

Statement of Cash FlowsStatement of Cash Flows

Operating FinancingInvesting

Principal revenue Acquisition and disposal of Activities that result in

changes in the size and

© 2012 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 26440NSS

23

generating and other activities that are not investing or financing

long-term assets and other investments not included in

cash equivalents

changes in the size and composition of the equity capital and borrowings of

the entity

25

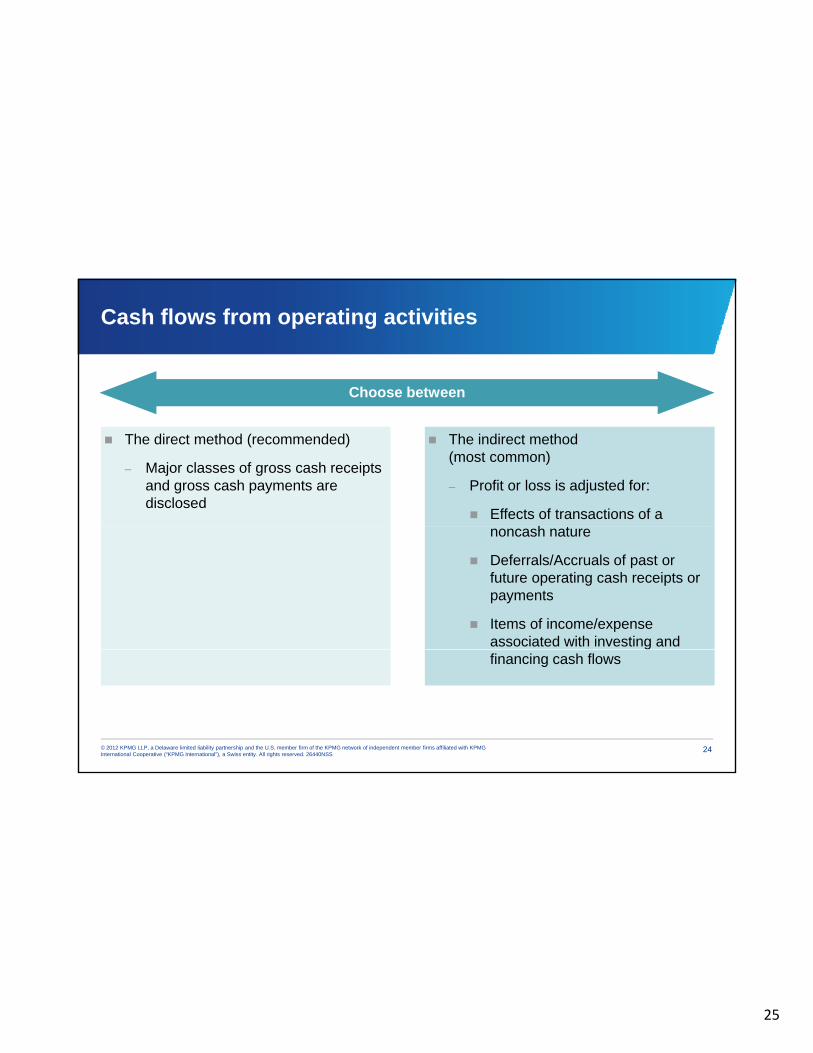

Cash flows from operating activities

Choose between

The direct method (recommended)

– Major classes of gross cash receipts and gross cash payments are disclosed

The indirect method (most common)

– Profit or loss is adjusted for:

Effects of transactions of a hnoncash nature

Deferrals/Accruals of past or future operating cash receipts or payments

Items of income/expense associated with investing and

© 2012 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 26440NSS

24

financing cash flows

26

Key points

Definition of cash and cash equivalents

Classification of transactions into different categories: operating, investing, and financial activities

Cash flow items in majority of cases reported gross

Foreign currency transactions

Separate reporting of:

U.S. GAAP Difference

– Interest and dividends paid and received

– Income taxes

– Acquisition and disposal of business units

© 2012 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 26440NSS

25

27

Knowledge check 4

Which of the following statements is correct regarding the statement of cash flows presentation requirements?p q

A. IFRS and U.S. GAAP are completely converged.

B. There are some significant differences, particularly for financial institutions, regarding the presentation requirements under IFRS versus U.S. GAAP.

C. The requirements to prepare and present a statement of cash flows are completely different between U.S. GAAP and IFRS.

D. Under IFRS, income taxes paid or received have to be allocated to cash flows from operating, investing, and financing activities respectively and separately.

© 2012 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 26440NSS

26

28

Knowledge check 4 – Debrief: correct answer is B

A. Incorrect

B. Correct, there are some significant differences, particularly for financial institutions, regarding the presentation requirements under IFRS versus U.S. GAAP.

C. Incorrect

D. Incorrect

© 2012 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 26440NSS

27

29

Related-party disclosuresIAS 24 R l t d P t Di lIAS 24 Related-Party Disclosures

30

IAS 24 Objective

“To ensure that an entity’s financial statements contain the disclosures necessary to draw attention to the possibility that its financial position and profit or loss may have been affected p y p p yby the existence of related parties and by transactions and outstanding balances, including commitments, with such parties.” (IAS 24.1)

© 2012 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 26440NSS

29

31

Definition of “a related party”

1) A person or a close member of that person’s family is related to a reporting entity if that person has control, joint control or significant influence, or is a member of the key p , j g , ymanagement personnel or the reporting entity or of a parent of the reporting entity.

2) An entity is related to the reporting entity if any of the following conditions applies:

They are members of the same group

One entity is an associate or joint venture of the other entity

B th titi j i t t f th thi d t Both entities are joint ventures of the same third party

One entity is a joint venture of a third party and the other an associate

The entity is a postemployment benefit plan for the benefit of employees of either the reporting entity or an entity related to the reporting entity

An entity is controlled or jointly controlled by a person identified in #1) above

© 2012 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 26440NSS

30

A person having control or joint control over the reporting entity has significant influence over the entity or is a member of key management

32

Related-party disclosures include:

Relationships between a parent and its subsidiaries

Key management personnel compensation by category

Related-party transactions – minimum disclosure includes:

The amount of the transactions

Th f di b l The amount of outstanding balances

Provisions for doubtful debts

The expense recognized during the period in respect of bad or doubtful debts due from related parties

© 2012 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 26440NSS

31

33

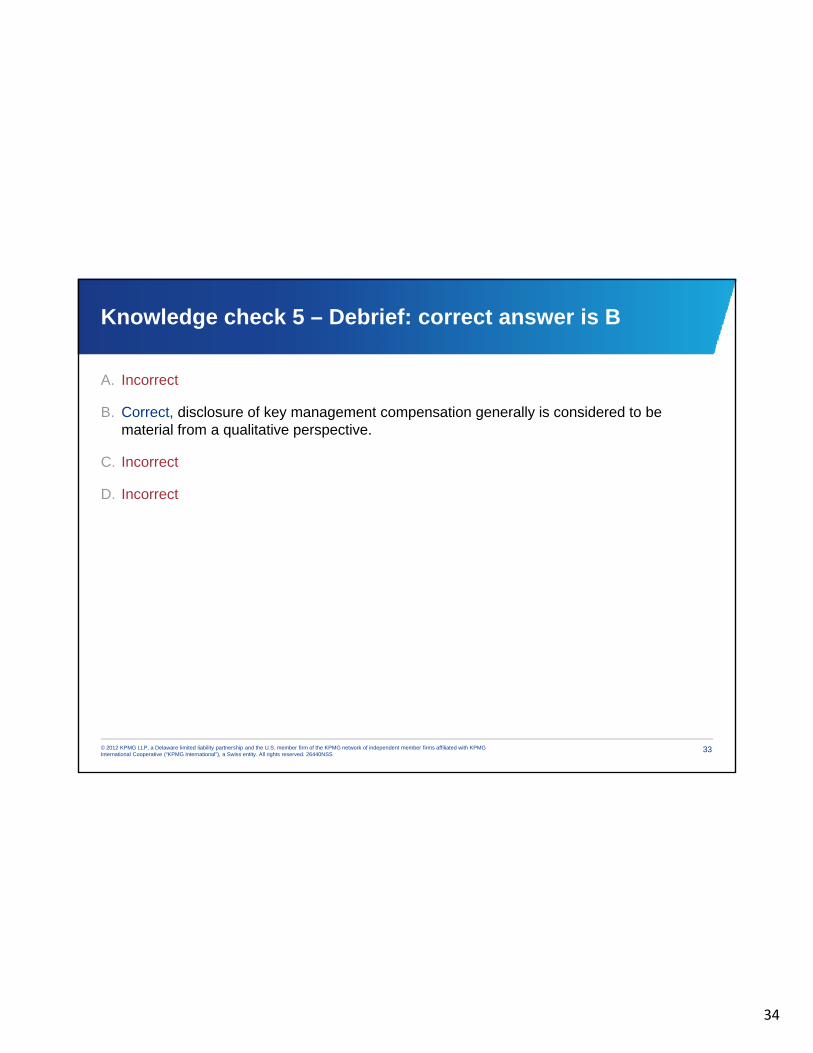

Knowledge check 5

Which of the following statements is correct regarding the disclosure requirements for key management compensation?g p

A. There is no requirement to disclose key management compensation.

B. Disclosure of key management compensation generally is considered to be material from a qualitative perspective.

C. There is no requirement to categorize different elements of key management compensation (for example, distinguish between short-term benefits and postemployment ( g ybenefits).

D. A qualitative discussion around the key features of the compensation arrangements usually is sufficient.

© 2012 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 26440NSS

32

34

Knowledge check 5 – Debrief: correct answer is B

A. Incorrect

B. Correct, disclosure of key management compensation generally is considered to be material from a qualitative perspective.

C. Incorrect

D. Incorrect

© 2012 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 26440NSS

33

35

Practical considerations

Changes to financial statement presentations may impact an organization’s financial systems and processes:g y p

New accounting disclosure and recognition requirements may result in more detailed presentation of information and/or new data elements or fields to be recorded and information to be calculated on a different basis.

Reporting packs may need to be modified to gather additional disclosure information from branches oradditional disclosure information from branches or subsidiaries operating on a standard general ledger package or collect information from subsidiaries that use different financial accounting packages.

© 2012 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 26440NSS

34

36

Practical considerations

Assessment and planning:

Accounting disclosure and information gap analysis

Complexity assessment

Initial adoption alternatives – IFRS 1

Industry/competitor assessment

Other company-wide initiatives and projects Other company wide initiatives and projects

Analysis of existing resource capabilities

Training requirements

Impact on investments, foreign subsidiaries, and overseas operations

Investor and analyst communications

© 2012 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 26440NSS

35

Project team structure and work plan

Entire organization involvement – not just an accounting issue

Ensure buy-in from auditors on decisions and interpretations made by management

37

KPMG Institutes and Training

About the KPMG IFRS Institute

The KPMG IFRS Institute, part of the KPMG Institute Network, has been created as an open forum where board and audit committee members, executives, management, stakeholders, academia, and government representatives can share knowledge, gain insight, and access thought leadership about the evolving global financial reporting environment. To visit the IFRS Institute, go to www.kpmginstitutes.com/ifrs-institute.

Executive EducationExecutive Educationwww.ExecEd.kpmg.comGroup Live, Instructor-Led CPE Credit accounting courses, seminars, workshops and update conferences for corporate accountants and financial executives.

© 2012 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 26440NSS

36

38

The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity. Although we endeavor to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act upon such information without appropriate professional advice after a thorough examination of the particular situation.

© 2012 KPMG LLP, a Delaware limited liability partnership and© 2012 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 26440NSS

The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG International.