ifrs for smes - world banksiteresources.worldbank.org/extcenfinrepref/resources/4152117... ·...

TRANSCRIPT

1

International Financial Reporting Standards

IFRS for SMEsIFRS Foundation-World Bank

26–27 May 2011

Kiev, Ukraine

Copyright © 2010 IFRS Foundation.

All rights reserved.

2The IFRS for SMEs

Topic 3.1(a)

Section 21 Provisions and

Contingencies

Section 28 Employee Benefits

Michael Wells

3The IFRS for SMEs

Section 21

Provisions & Contingencies

4Section 21 – Scope

• Section 21 applies to accounting &

reporting of provisions, contingent

liabilities & contingent assets

except those provisions covered by

other sections including:

– leases (Section 20). However, Section 21 covers onerous operating leases

– construction contracts (Section 23)– employee benefit obligations (Sec. 28)– income tax (Section 29)

5Section 21 – Provisions

Provisions are liabilities of uncertain timing or amount.

A liability is a present obligation…

A present obligation may be either

–legal (binding contract or statutory requirement)

–constructive (derives from an entity’s actions which the entity has no realistic alternative to settling)

6Section 21 – Examples provisions

• Ex 1*: Waste from A’s factory

contaminated the groundwater. Lawsuit:

local community seek compensation for

damages to health from contamination.

A acknowledges wrongdoing. Court is

deciding extent of the compensation.

Lawyers expect ruling in +2 yrs &

compensation in the range of

CU1,000,000 to CU30,000,000.

* see example 1 in Module 21 of the IFRS Foundation training material

7Section 21 – Examples provisions continued

• Ex 2*: Waste from A’s factory contaminated the groundwater. Required by law to restore the environment. Estimates restoration cost between 1,000,000 & 15,000,000. Unsure of period to complete restoration.

• Ex 3*: A manufacturer gives warranties to the purchasers of its goods. Warranty = make good, by repair or replacement, manufacturing defects that become apparent within 3 years of sale.

*see example with the same number in Module 21 of the IFRS Foundation training material

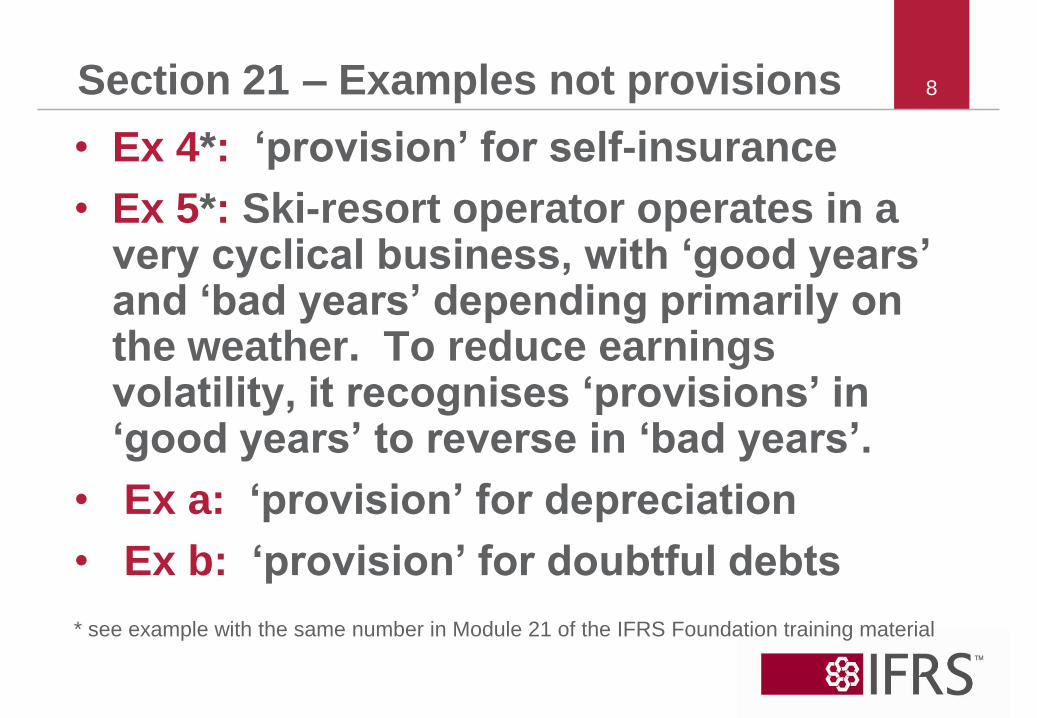

8Section 21 – Examples not provisions

• Ex 4*: ‘provision’ for self-insurance

• Ex 5*: Ski-resort operator operates in a very cyclical business, with ‘good years’ and ‘bad years’ depending primarily on the weather. To reduce earnings volatility, it recognises ‘provisions’ in ‘good years’ to reverse in ‘bad years’.

• Ex a: ‘provision’ for depreciation

• Ex b: ‘provision’ for doubtful debts

* see example with the same number in Module 21 of the IFRS Foundation training material

9

Section 21 – Example constructive

oblig.

• Ex 12*: Waste from A’s factory

contaminated the groundwater. A is not

required by law to restore the

contaminated environment & there is no

court case. However, in the reporting

period the entity publicly announced that

it would restore the contaminated

environment within the next 12 months.

* see example 12 in Module 21 of the IFRS Foundation training material

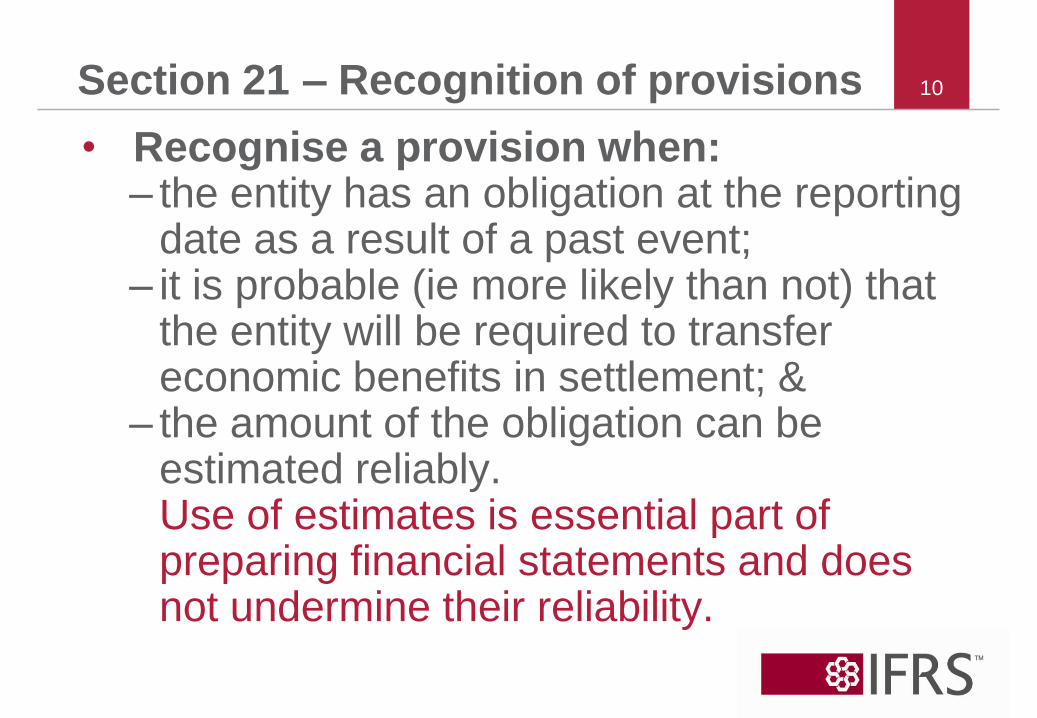

10Section 21 – Recognition of provisions

• Recognise a provision when:– the entity has an obligation at the reporting

date as a result of a past event;– it is probable (ie more likely than not) that

the entity will be required to transfer economic benefits in settlement; &

– the amount of the obligation can be estimated reliably.Use of estimates is essential part of preparing financial statements and does not undermine their reliability.

11

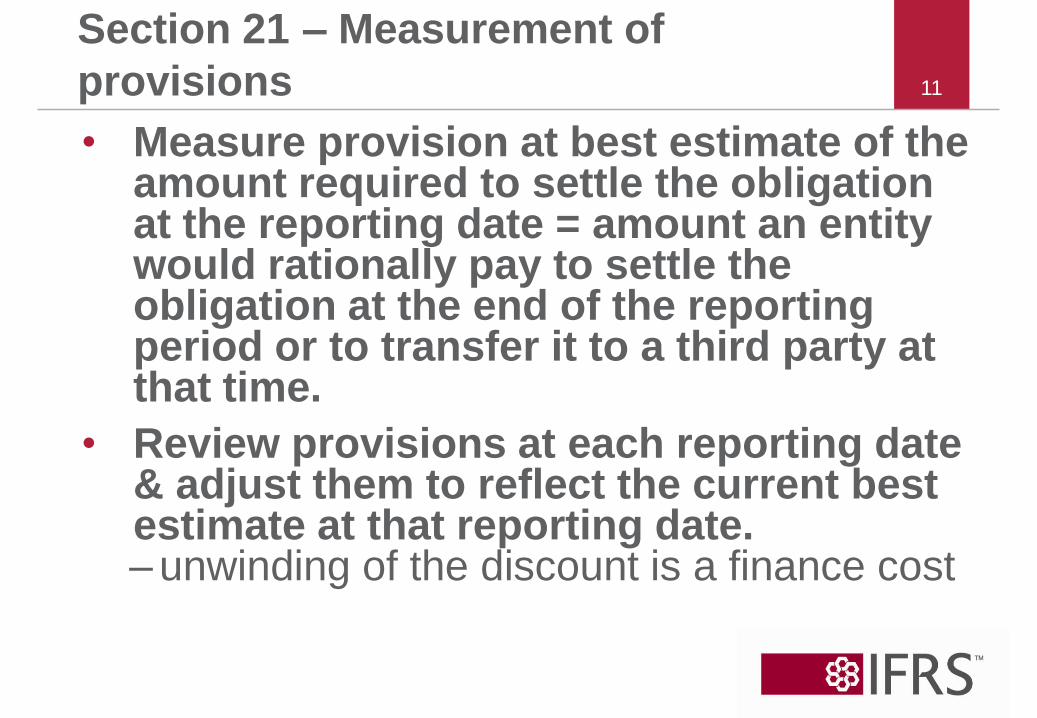

Section 21 – Measurement of

provisions

• Measure provision at best estimate of the amount required to settle the obligation at the reporting date = amount an entity would rationally pay to settle the obligation at the end of the reporting period or to transfer it to a third party at that time.

• Review provisions at each reporting date & adjust them to reflect the current best estimate at that reporting date.– unwinding of the discount is a finance cost

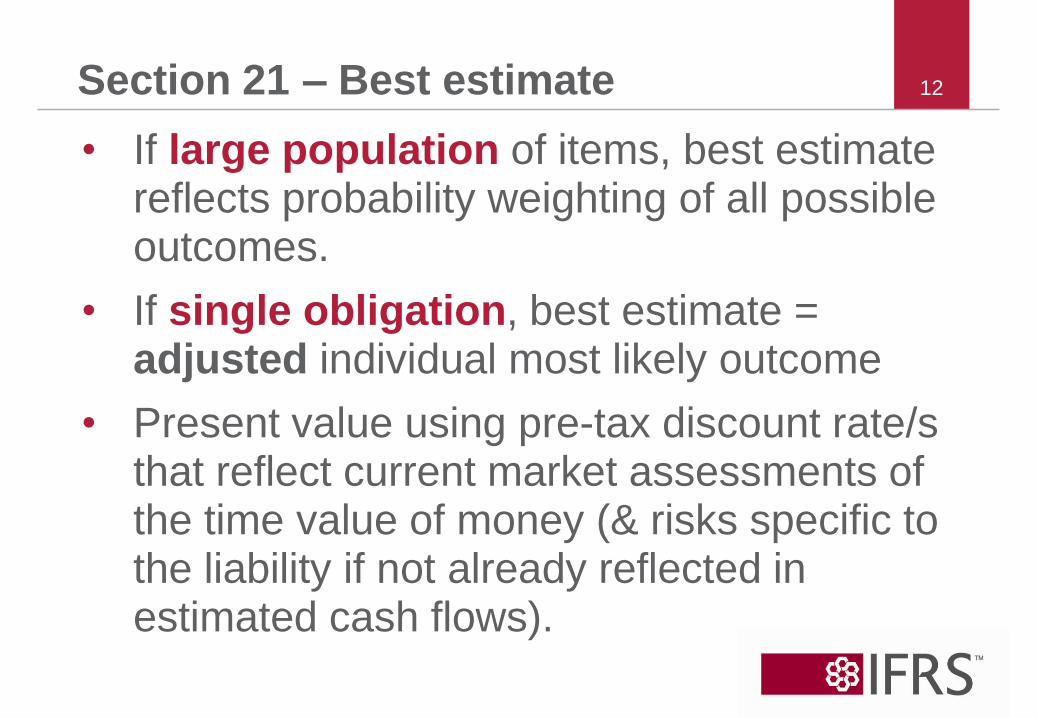

12Section 21 – Best estimate

• If large population of items, best estimate reflects probability weighting of all possible outcomes.

• If single obligation, best estimate = adjusted individual most likely outcome

• Present value using pre-tax discount rate/s that reflect current market assessments of the time value of money (& risks specific to the liability if not already reflected in estimated cash flows).

13Section 21 – Examples measurement

• Ex 14*: A has 1,000 units of a product sold with active warranties (ie A will repair defects found up to 6 months after sale).

Probabilities & repair cost: major defect = 5% chance of CU400 repair; minor defect = 20% chance of CU100 repair; 75% chance of no defects.

• Best estimate (expected value) = CU40,000Calculation: (75% x 1,000 units x nil) + (20% x 1,000

units x CU100) + (5% x 1,000 units x CU400)

* see example 14 in Module 21 of the IFRS Foundation training material

14Section 21 – Examples measurement

• Ex 15*: Personal injury lawsuit brought by customer. Lawyers estimate 30% chance compensation = CU2,000,000 & 70% chance = CU300,000. Ruling expected in 2 years. Discount rate = 4% per year (ie 2-year government bonds = 5% less 1% risks specific to liability).

Individual most likely outcome = CU300,000. Because only other possible outcome is higher, the best estimate to settle the obligation at 31/12/20X1 will be higher than PV of the most likely outcome of CU300,000, eg PV of CU810,000 at 4% = ±CU748,890

* see example 15 in Module 21 of the IFRS Foundation training material

15Section 21 – Example remeasurement

• Ex 25*: Provision for a lawsuit = CU40,000 at 31/12/20X1 & remeasured to CU90,000 at 31/12/20X2. CU3,000 of the increase = unwinding of the discount & the remainder is for better information becoming available.

The increase of CU50,000 will be recognised as an expense in the determination of the entity’s profit or loss for the year ended 31/12/20X2– CU3,000 = finance cost– CU47,000 = change in estimate

* see example 25 in Module 21 of the IFRS Foundation training material

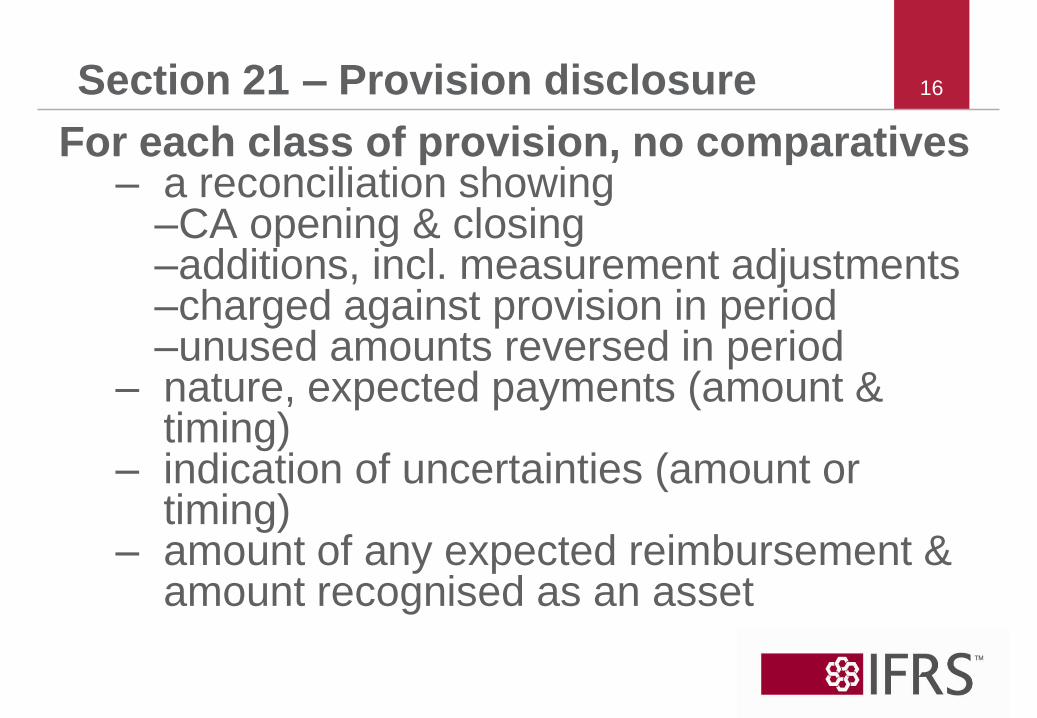

16Section 21 – Provision disclosure

For each class of provision, no comparatives– a reconciliation showing

–CA opening & closing–additions, incl. measurement adjustments –charged against provision in period–unused amounts reversed in period

– nature, expected payments (amount & timing)

– indication of uncertainties (amount or timing)

– amount of any expected reimbursement & amount recognised as an asset

17Section 21 – contingent liabilities

A contingent liability is either:

(i) a possible but uncertain obligation; or

(ii) a present obligation that is not

recognised because it fails the

recognition criteria in paragraph 21.4.

18Section 21 – Contingent liabilities

Do not recognise a contingent liability as a liability (except contingent liabilities of an acquiree in a business combination).

Contingent liabilities are disclosed unless the possibility of an outflow of resources is remote.

When an entity is jointly and severally liable for an obligation, the part of the obligation that is expected to be met by other parties is treated as a contingent liability.

19

Section 21 – Example contingent

liability

• Ex 29*: Community is seeking compensation from A for damages to their health as a result of contamination believed to be caused by A’s plant.

It is doubtful whether A is the source of the contamination because

–many entities operate in the same area producing similar waste & it is unclear which entity is the source of the leak

–A has taken precautions to avoid leaks & is vigorously defending the case.

* see example 29 in Module 21 of the IFRS Foundation training material

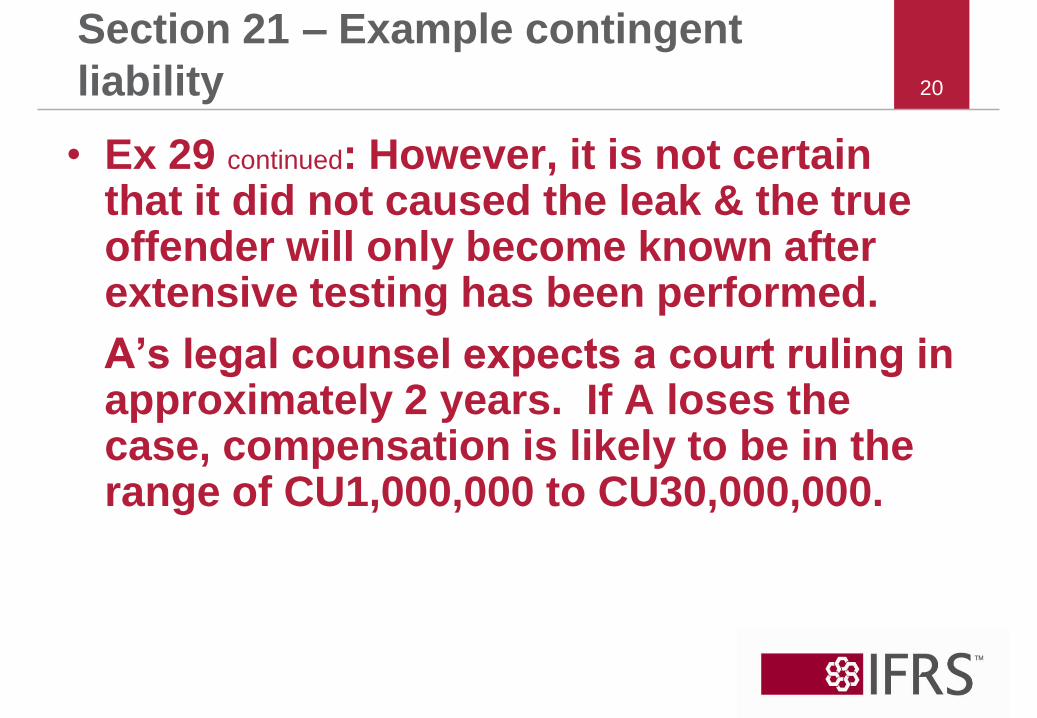

20

Section 21 – Example contingent

liability

• Ex 29 continued: However, it is not certain that it did not caused the leak & the true offender will only become known after extensive testing has been performed.

A’s legal counsel expects a court ruling in approximately 2 years. If A loses the case, compensation is likely to be in the range of CU1,000,000 to CU30,000,000.

21

Section 21 – Example contingent

liability

• Ex 29 continued:

It may be uncertain whether the entity has

a present obligation—this is the matter

being determined by the court.

– if taking account of all of the available

evidence, it is probable that the entity will

successfully defend the court case then

the entity has a possible obligation &

hence a contingent liability.

22Section 21 – Contingent liab disclosure

• For each class of contingent liability unless the possibility of any outflow is remote, disclose, a brief description of the nature of the contingent liability and, when practicable:– estimate of its financial effect (measured

like a provision); – indication of uncertainties of amount or

timing; &– possibility of any reimbursement.

• If impracticable to make one or more of these disclosures, that fact shall be stated.

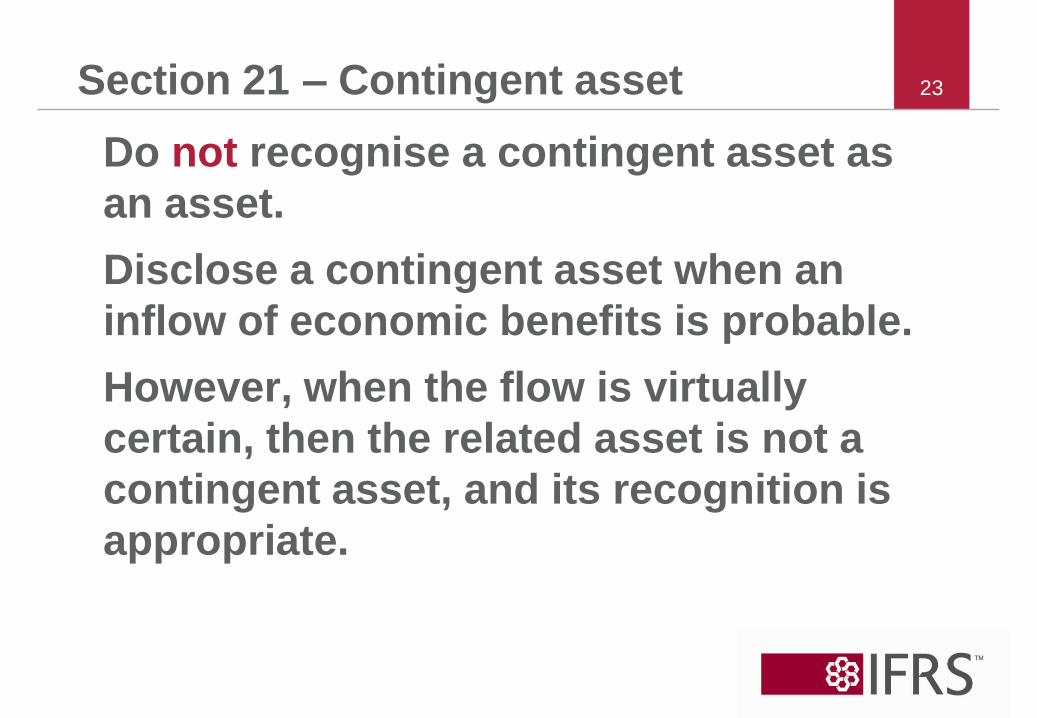

23Section 21 – Contingent asset

Do not recognise a contingent asset as

an asset.

Disclose a contingent asset when an

inflow of economic benefits is probable.

However, when the flow is virtually

certain, then the related asset is not a

contingent asset, and its recognition is

appropriate.

24

Section 21 – Contingent asset

disclosure

• If an inflow of economic benefits is probable (more likely than not) but not virtually certain, disclose: – a description of the nature of the

contingent assets at the end of the reporting period, and

– when practicable without undue cost or effort, an estimate of their financial effect (measured using the principles set out for measuring provisions).

• If it is impracticable to make this disclosure, that fact shall be stated.

25Section 21 – Prejudicial disclosures

• In extremely rare cases, disclosure of some or all of the information required by para’s 21.14–21.16 can be expected to prejudice seriously the position of the entity in a dispute with other parties on the subject matter of the provision, C liab. or C asset.

• In such cases, need not disclose the information, but must disclose the general nature of the dispute, together with the fact that, & reason why, the information has not been disclosed.

• Note: no recognition & measurement exemption for provisions.

26The IFRS for SMEs

Section 28

Employee Benefits

27Section 28 – Scope

Employee benefits (EBs) are all forms of

consideration given by an entity in

exchange for service rendered by

employees, including directors and

management.

Section 28 applies to all EBs, except for

share-based payment transactions, which

are covered by Section 26 Share-based

Payment.

28

Section 28 – Types of employee

benefits

• 4 types of EBs:

– short-term employee benefits

– post-employment benefits

– other long-term employee benefits

– termination benefits

And equity compensation (see Section 26)

29

Section 28 – General recognition

criteria

• Recognise cost of EBs to which

employees have become entitled for

service rendered to entity in reporting

period

– liability, after deducting amounts that

have been paid. Asset if prepaid EB

expense

– expense, unless another section requires

cost included in asset (for example

inventories or PP&E)

30

Section 28 – Short-term employee

benefits

• Short-term employee benefits (S/TEBs)

are wholly due within 12 months after the

end of the period in which the employees

render the related service (hereafter 12

month limitation).

– but excludes termination benefits.

31

Section 28 – Short-term employee

benefits

• Examples of S/TEBs include:– wages, salaries & social security contrib;– S/T compensated absences (paid annual

leave & paid sick leave) for absences expected to occur within 12 month limitation;

– profit-sharing & bonuses payable within 12 month limitation; &

– non-monetary benefits (such as medical care, housing, cars and free or subsidised goods or services) for current employees.

32Section 28 – Measurement of S/TEBs

• Measure S/TEBs that meet general

recognition criteria (above)

– at the undiscounted amount expected to

be paid

33Section 28 – Examples S/TEBs

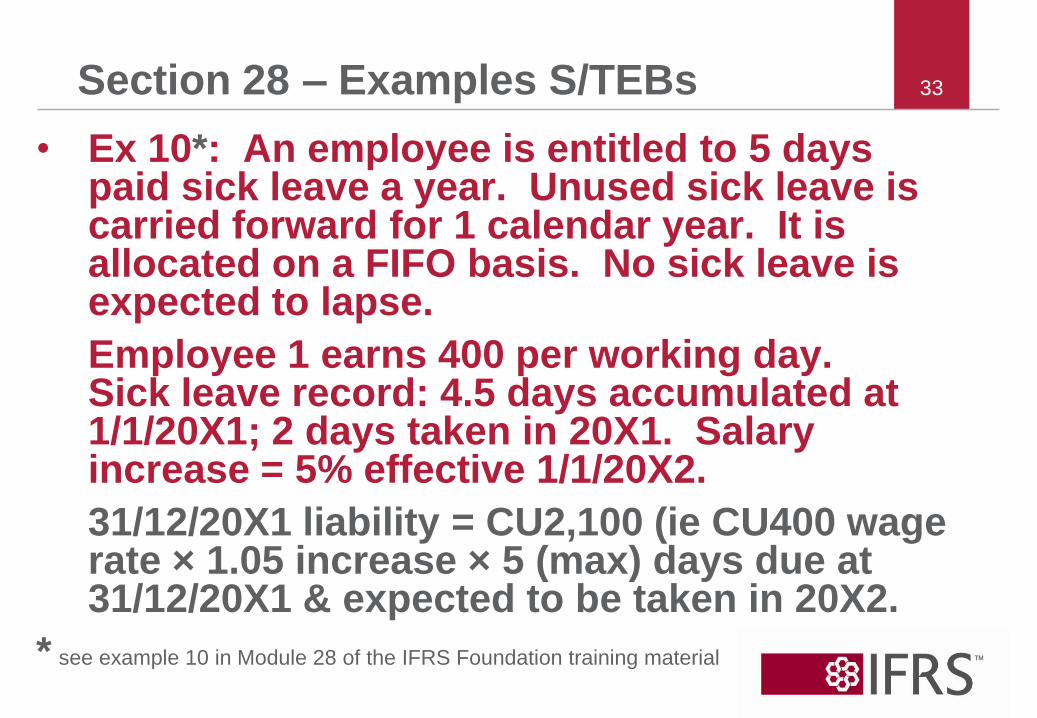

• Ex 10*: An employee is entitled to 5 days paid sick leave a year. Unused sick leave is carried forward for 1 calendar year. It is allocated on a FIFO basis. No sick leave is expected to lapse.

Employee 1 earns 400 per working day. Sick leave record: 4.5 days accumulated at 1/1/20X1; 2 days taken in 20X1. Salary increase = 5% effective 1/1/20X2.

31/12/20X1 liability = CU2,100 (ie CU400 wage rate × 1.05 increase × 5 (max) days due at 31/12/20X1 & expected to be taken in 20X2.

* see example 10 in Module 28 of the IFRS Foundation training material

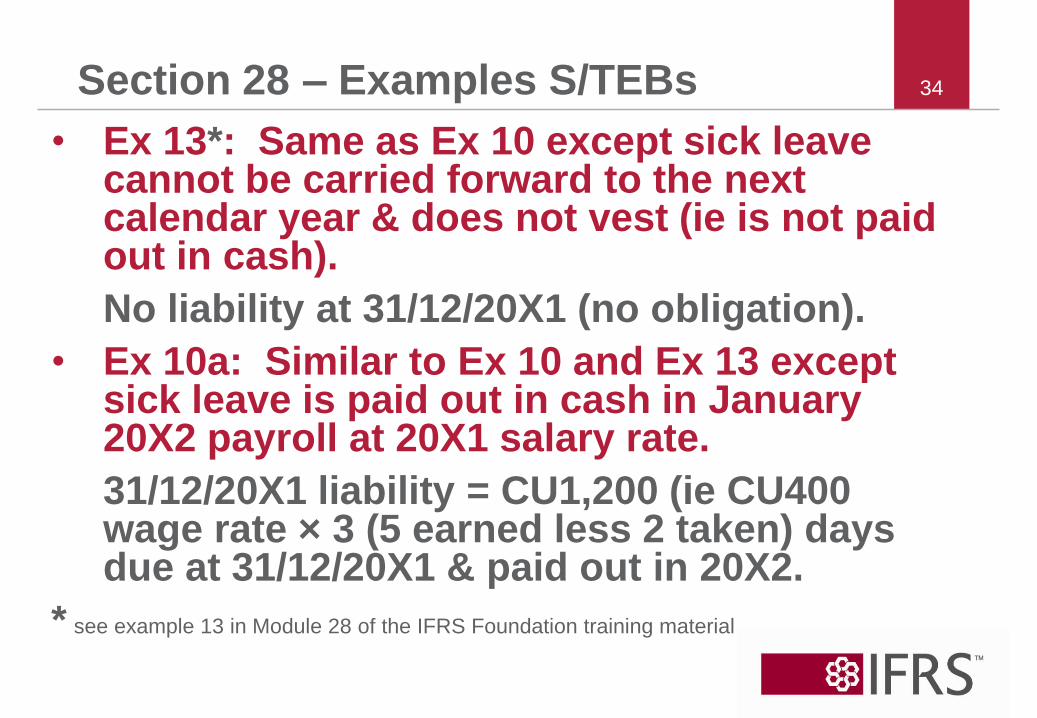

34Section 28 – Examples S/TEBs

• Ex 13*: Same as Ex 10 except sick leave cannot be carried forward to the next calendar year & does not vest (ie is not paid out in cash).

No liability at 31/12/20X1 (no obligation).

• Ex 10a: Similar to Ex 10 and Ex 13 except sick leave is paid out in cash in January 20X2 payroll at 20X1 salary rate.

31/12/20X1 liability = CU1,200 (ie CU400 wage rate × 3 (5 earned less 2 taken) days due at 31/12/20X1 & paid out in 20X2.

* see example 13 in Module 28 of the IFRS Foundation training material

35Section 28 – Examples S/TEBs

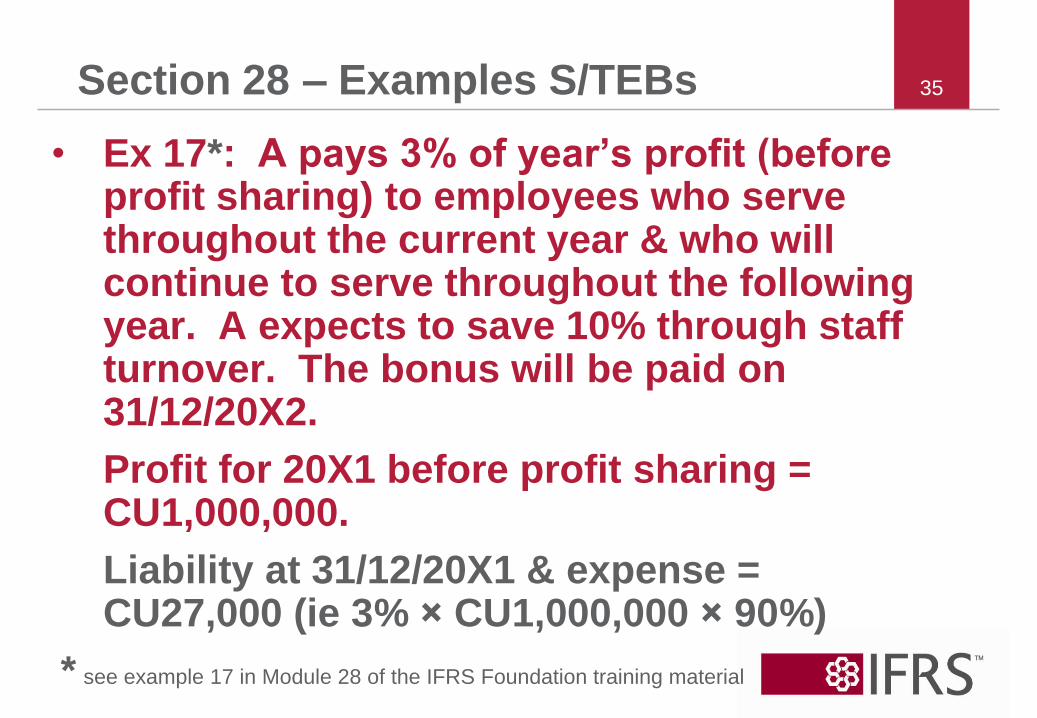

• Ex 17*: A pays 3% of year’s profit (before profit sharing) to employees who serve throughout the current year & who will continue to serve throughout the following year. A expects to save 10% through staff turnover. The bonus will be paid on 31/12/20X2.

Profit for 20X1 before profit sharing = CU1,000,000.

Liability at 31/12/20X1 & expense = CU27,000 (ie 3% × CU1,000,000 × 90%)

* see example 17 in Module 28 of the IFRS Foundation training material

36Section 28 – Post-employment benefits

• Post-employment benefits (PEBs) are

employee benefits (other than

termination benefits) that are payable

after the completion of employment

• Examples of PEBs include

– retirement benefits, such as pension

– other PEBs, such as post-employment

life insurance and post-employment

medical care

37Section 28 – Post-employment benefits

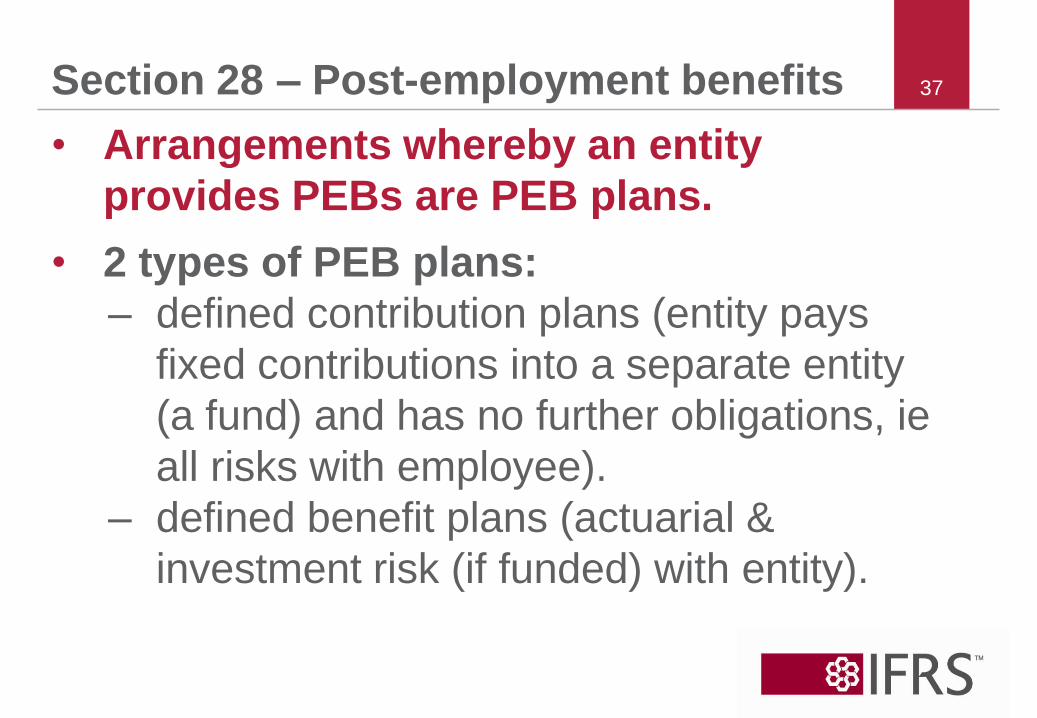

• Arrangements whereby an entity

provides PEBs are PEB plans.

• 2 types of PEB plans:

– defined contribution plans (entity pays

fixed contributions into a separate entity

(a fund) and has no further obligations, ie

all risks with employee).

– defined benefit plans (actuarial &

investment risk (if funded) with entity).

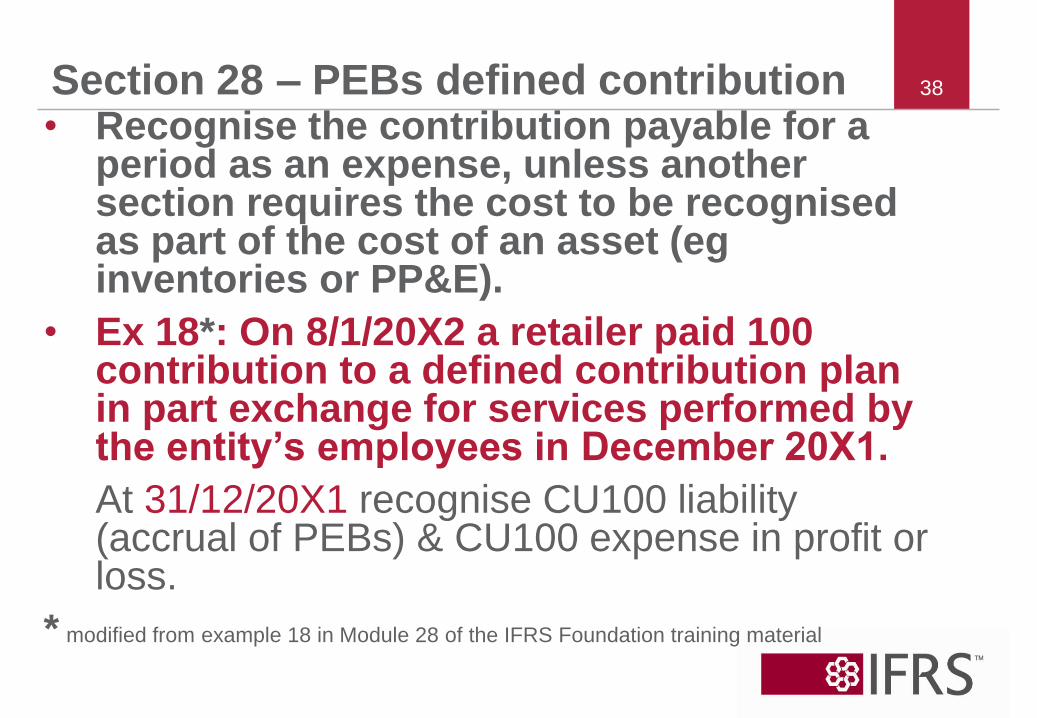

38Section 28 – PEBs defined contribution• Recognise the contribution payable for a

period as an expense, unless another section requires the cost to be recognised as part of the cost of an asset (eg inventories or PP&E).

• Ex 18*: On 8/1/20X2 a retailer paid 100 contribution to a defined contribution plan in part exchange for services performed by the entity’s employees in December 20X1.

At 31/12/20X1 recognise CU100 liability (accrual of PEBs) & CU100 expense in profit or loss.

* modified from example 18 in Module 28 of the IFRS Foundation training material

39Section 28 – PEBs defined benefit plans

• Apply general recognition principle,

recognise:

– a liability for its obligations under defined

benefit plans net of plan assets—its

‘defined benefit liability’ (see

paragraphs 28.15–28.23).

– the net change in that liability during the

period as the cost of its defined benefit

plans during the period (see paragraphs

28.24–28.27).

40Section 28 – Defined benefit liability

• Measure defined benefit liability at net of:– PV of defined benefit obligation (DBO)– FV of plan assets (if any) out of which

the obligations are to be settled directly– paragraphs 11.27–11.32 provide

guidance on fair value measurement).

• If PV of DBO < FV of plan assets, plan has a surplus. Recognise surplus as asset only to extent recoverable through reduced future contributions or through refunds from the plan.

41Section 28 – Defined benefit obligation (DBO)

• PV of DBO reflects estimated amount of

benefit that employees have earned in

return for their service in the current &

prior periods

– including benefits that are not yet vested

– including the effects of benefit formulas

that give employees greater benefits for

later years of service (eg final salary).

• Significant judgements in measuring

DBO include actuarial assumptions.

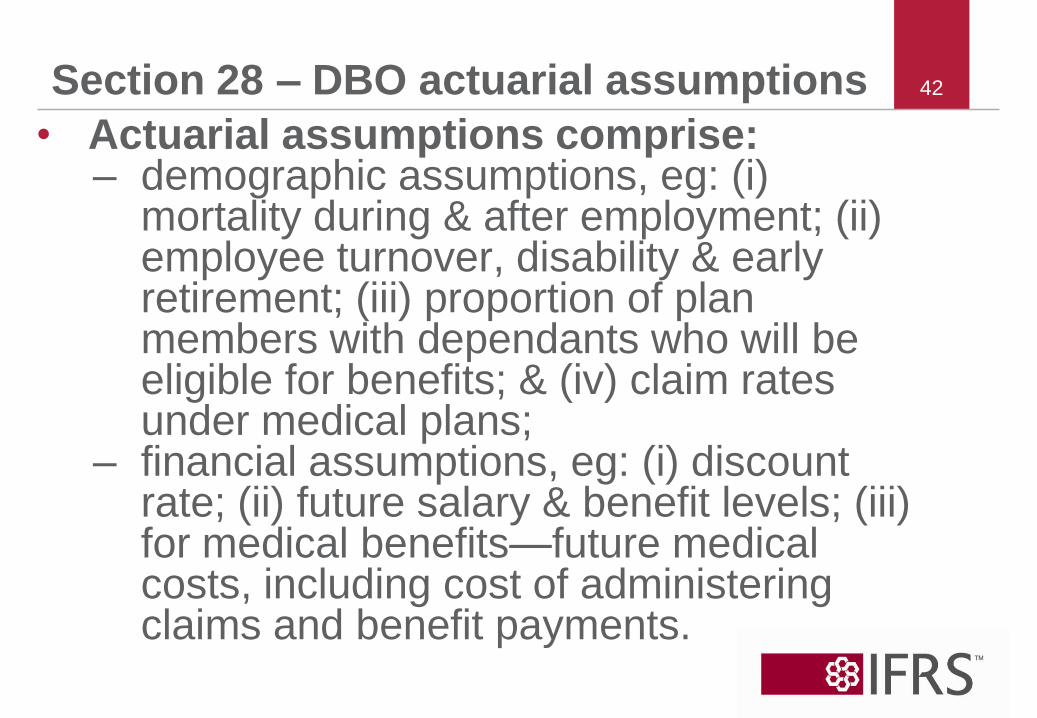

42Section 28 – DBO actuarial assumptions

• Actuarial assumptions comprise:– demographic assumptions, eg: (i)

mortality during & after employment; (ii) employee turnover, disability & early retirement; (iii) proportion of plan members with dependants who will be eligible for benefits; & (iv) claim rates under medical plans;

– financial assumptions, eg: (i) discount rate; (ii) future salary & benefit levels; (iii) for medical benefits—future medical costs, including cost of administering claims and benefit payments.

43Section 28 – DBO valuation method

• Measure DBO using projected unit credit method (PUC). However, if undue cost or effort use simplified calculation.

• Under simplified calculation:– ignore estimated future salary increases; – ignore future service of current

employees (ie assume closure of the plan for existing as well as any new employees); &

– ignore possible in-service mortality of current employees (however, consider mortality after service (ie life expectancy)).

44Section 28 – DBO PUC valuation method

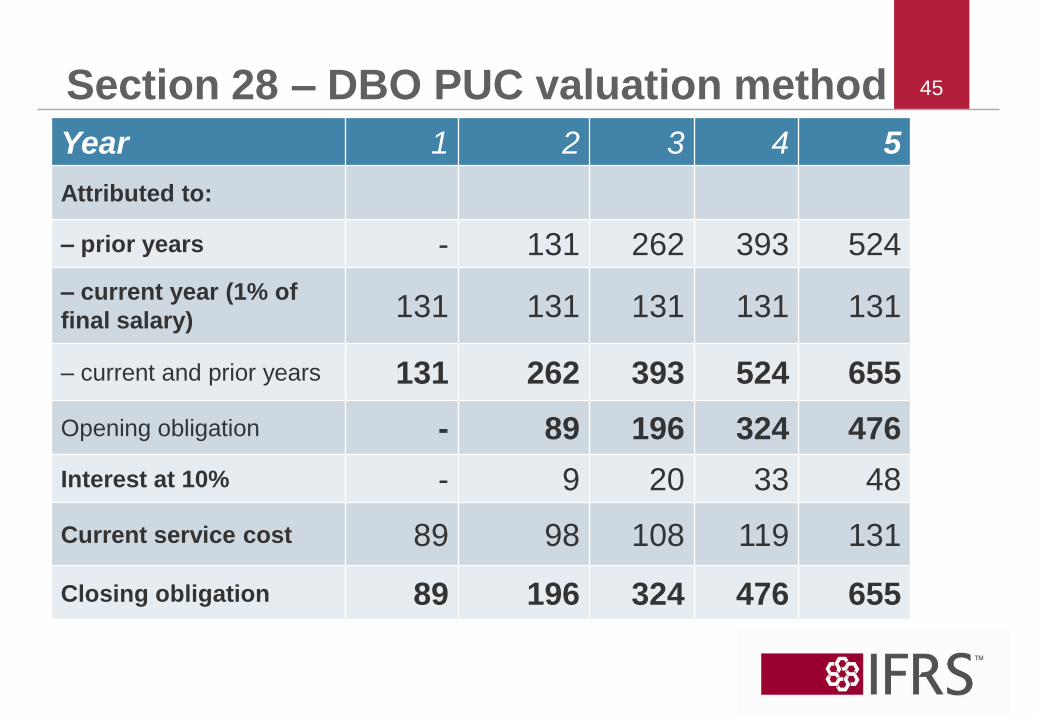

• Ex 30*: Lump sum benefit payable on retirement = 1% of final salary for each year of service. Salary in Y1 = 10,000 (increase at 7% pa). Discount rate = 10% pa. Employee expected to retire at end of Y5.

• Shows how the obligation builds up: – assuming that there are no changes in

actuarial assumptions. – for simplicity, this example assumes

employee will stay until end of Y5.

* see example 30 in Module 28 of the IFRS Foundation training material

45Section 28 – DBO PUC valuation method

Year 1 2 3 4 5

Attributed to:

– prior years - 131 262 393 524

– current year (1% of

final salary)131 131 131 131 131

– current and prior years 131 262 393 524 655

Opening obligation - 89 196 324 476

Interest at 10% - 9 20 33 48

Current service cost 89 98 108 119 131

Closing obligation 89 196 324 476 655

46Section 28 – DBO PUC valuation method

• Notes on PUC calculations:

Current service cost is the present value of

benefit attributed to the current year eg Y1—

CU131 × 1/(1.1)4 = CU131 ÷ 0.683013 =

CU89.47

The closing obligation is the present value

of benefit attributed to current and prior

years.

47Section 28 – DBO simplified method

• Ex 33*: Same as Ex 30, except use

simplified method of calculation.

* see example 33 in Module 28 of the IFRS Foundation training material

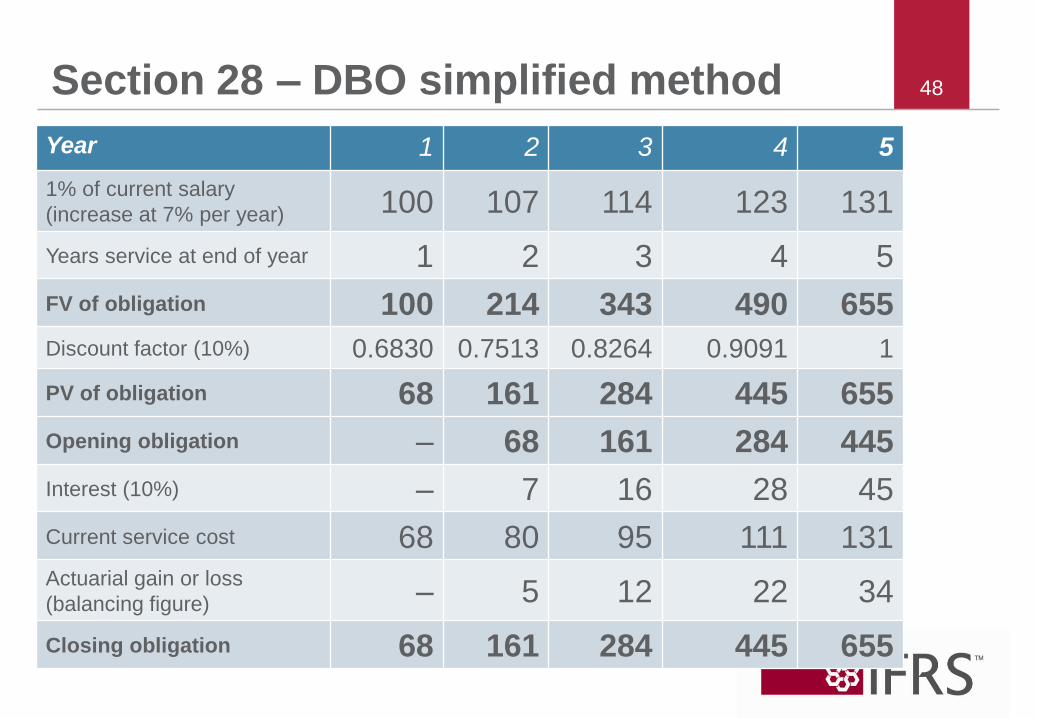

48Section 28 – DBO simplified method

Year 1 2 3 4 5

1% of current salary

(increase at 7% per year) 100 107 114 123 131

Years service at end of year 1 2 3 4 5

FV of obligation 100 214 343 490 655

Discount factor (10%) 0.6830 0.7513 0.8264 0.9091 1

PV of obligation 68 161 284 445 655

Opening obligation – 68 161 284 445

Interest (10%) – 7 16 28 45

Current service cost 68 80 95 111 131

Actuarial gain or loss

(balancing figure) – 5 12 22 34

Closing obligation 68 161 284 445 655

49Section 28 – DBO simplified method

• Notes on simplified method calculations

Current service cost = PV of benefit attributed to the current year– Calculation Y1: CU100 salary × 1/(1.1)4

= CU68.30

Closing obligation = PV of benefit attributed to current & prior years– Calculation Y1: CU100 × 1 year’s service

÷ 1/(1.1)4 = CU68.30

50Section 28 – Defined benefit expense

• Recognise net change in defined benefit liability in the period (other than benefits paid to employees or contributions from the employer) as the cost of its defined benefit plans during the period.

• Recognise cost either (accounting policy) – entirely in profit or loss as an expense, or – partly in profit or loss & partly as an item

of OCI (only actuarial gains & losses can be in OCI)

unless part of the cost of an asset (eg see Section 17 PP&E).

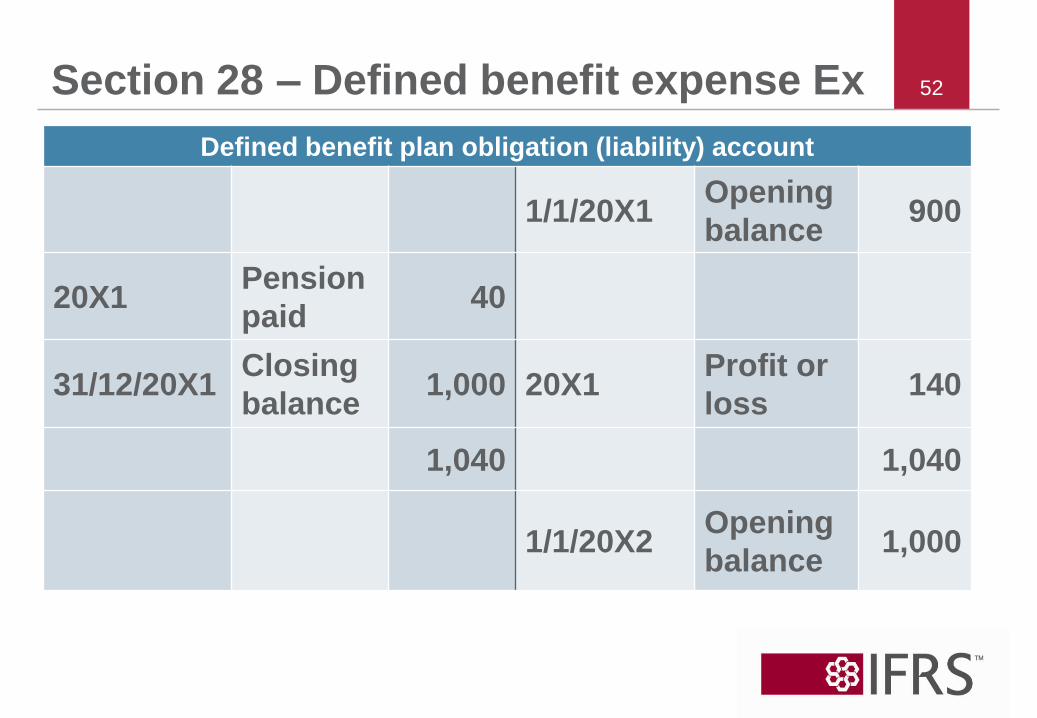

51Section 28 – Defined benefit expense Ex

• Ex 39*: A recognises actuarial gains & losses in profit or loss. Employees promised a pension of 0.2% of final salary for each year of service. The pension is payable from the age of 65. The plan is unfunded.

At 31/12/20X1 CA of the plan obligation = CU1,000 (20X0: CU900).

In 20X1 A paid pensions of CU40 to its past employees.

* see example 39 in Module 28 of the IFRS Foundation training material

52Section 28 – Defined benefit expense Ex

Defined benefit plan obligation (liability) account

1/1/20X1Opening

balance900

20X1Pension

paid40

31/12/20X1Closing

balance1,000 20X1

Profit or

loss140

1,040 1,040

1/1/20X2Opening

balance1,000

53Section 28 – Defined benefit expense Ex

• Ex 42*: Same as Ex 39 except recognises

all actuarial gains & losses in OCI.

CU50 of the cost of the defined benefit

plan for 20X1 is attributable to actuarial

losses.

• Recognise CU140 expense for 20X1 as

follows:

– CU50 in OCI (ie actuarial gains & losses)

– CU90 (the remainder) in profit or loss.

* see example 42 in Module 28 of the IFRS Foundation training material

54Section 28 – Defined benefit expense Ex

• Ex 40*: Same as Ex 39 except plan is

funded

– in 20X1 fund paid pensions of CU40 to

past employees & entity contributed

CU110 to the fund.

– at 31/12/20X1 FV of plan assets =

CU980 (20X0: CU890).

* see example 40 in Module 28 of the IFRS Foundation training material

55Section 28 – Defined benefit expense Ex

Funded defined benefit plan (liability) account

1/1/20X1Opening

balance10(a)

20X1Increase

funding 110

31/12/20X1Closing

balance20(b) 20X1

Profit or

loss120(c)

130 130

1/1/20X2Opening

balance20

(a) CU900 obligation less CU890 plan assets

(b) CU1,000 obligation less CU980 plan assets

(c) balancing figure

56

Section 28 – Other long-term employee

benefits

• Other long-term employee benefits

(OL/TEBs) are employee benefits (other

than post-employment benefits &

termination benefits) that are not wholly

due within 12 months after the end of the

period in which the employees render

the related service.

57Section 28 – OL/TEBs

• Examples of OL/TEBs include:– long-term compensated absences, eg

long-service or sabbatical leave– long-service benefits– long-term disability benefits – profit-sharing & bonuses payable + 12

months after the end of the period in which the employees render the related service

– deferred compensation paid + 12 months after the end of the period in which it is earned

58Section 28 – OL/TEBs

• Recognise a liability for OL/TEBs

measured at the net of:

– PV of the benefit obligation

– FV of plan assets (if any) out of which the

obligations are to be settled directly.

• Expense recognition is same as post-

employment defined benefit plan

– can choose to recognise actuarial gains

& losses in OCI)

59Section 28 – Termination benefits

• Termination benefits are employee

benefits payable as a result of either:

– an entity’s decision to terminate an

employee’s employment before the

normal retirement date, or

– an employee’s decision to accept

voluntary redundancy in exchange for

those benefits.

60Section 28 – Termination benefits

• Termination benefits include

commitments by legislation, by

contractual or other agreements with

employees or their representatives or by

a constructive obligation based on

business practice, custom or a desire to

act equitably, to make payments (or

provide other benefits) to employees

when it terminates their employment.

61

Section 28 – Recognition &

measurement

• Recognise termination benefits as a liability & an expense only when the entity is demonstrably committed either:– to terminate the employment of an

employee before the normal retirement date, or

– to provide termination benefits as a result of a firm voluntary redundancy offer.

• measure at best estimate of expenditure that would be required to settle the obligation at reporting date (PV if > 12 months).

62Section 28 – EBs disclosures

• PEBs have extensive disclosures.

• S/TEBs Section 28 does not specify disclosures

• For each category OL/TEBs & termination benefits: the nature of the benefit, the amount of its obligation and the extent of funding at the reporting date.

© 2010 IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK | www.ifrs.org

63Questions or comments?

Expressions of individual views by

members of the IASB and its staff

are encouraged.

The views expressed in this

presentation are those of the

presenter.

Official positions of the IASB on

accounting matters are determined

only after extensive due process

and deliberation.

64

This presentation may be modified from time to time. The latest version may be downloaded from:

http://www.ifrs.org/Conferences+and+Workshops/IFRS+for+SMEs+Train+the+trainer+workshops.htm

The accounting requirements applicable to small and medium-sized entities (SMEs) are set out in the International Financial Reporting Standard (IFRS) for SMEs, which was issued by the IASB in July 2009.

The IFRS Foundation, the authors, the presenters and the publishers do not accept responsibility for loss caused to any person who acts or refrains from acting in reliance on the material in this PowerPoint presentation, whether such loss is caused by negligence or otherwise.