ifrs 9

TRANSCRIPT

November 2009

IAS Plus website

We have had morethan 8 millionvisits to ourwww.iasplus.comwebsite. Our goal is to be the mostcomprehensivesource of newsabout internationalfinancial reporting onthe Internet. Pleasecheck in regularly.

The headlines

• New classification and measurementrequirements for financial assets.

• New criteria for amortised cost measurement.• New measurement category – fair value through

other comprehensive income.• Impairment assessment only for amortised cost

assets.

• No more available-for-sale assets.• No more held-to-maturity assets and tainting

rules.• No more embedded derivatives in financial

assets.• No more unquoted equity investments

measured at cost less impairment.

IFRS centres of excellence

AmericasNew York Robert Uhl [email protected] Robert Lefrancois [email protected]

Asia-PacificHong Kong Stephen Taylor [email protected] Bruce Porter [email protected]

Europe-AfricaCopenhagen Jan Peter Larsen [email protected] Andreas Barckow [email protected] Graeme Berry [email protected] Veronica Poole [email protected] Laurence Rivat [email protected]

IFRS global officeGlobal IFRS leaderKen [email protected]

IAS Plus Update.IFRS 9 Financial Instruments

Background

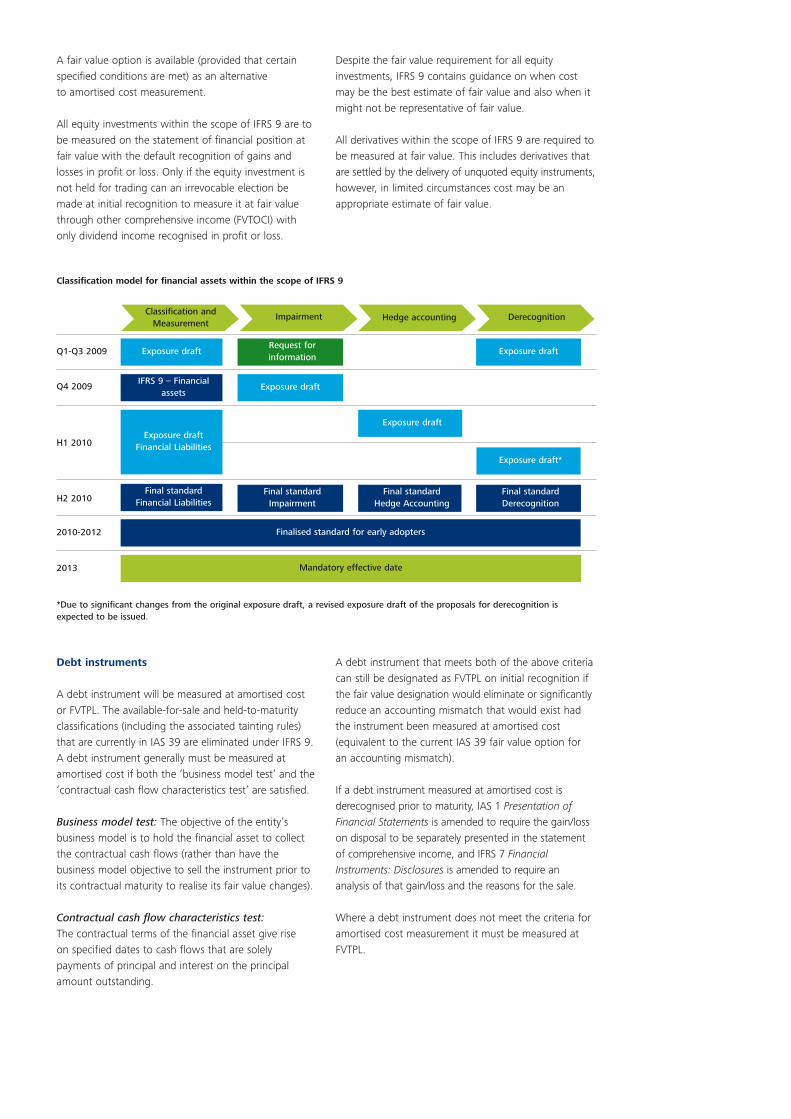

On 12 November 2009, the International AccountingStandards Board (IASB) issued IFRS 9 FinancialInstruments. This Standard introduces new requirementsfor the classification and measurement of financialassets and is effective from 1 January 2013 with earlyadoption permitted.

The exposure draft for this Standard included bothfinancial assets and financial liabilities within its scope,however, due to concerns raised with the proposals forfinancial liabilities the scope was restricted to onlyfinancial assets.

New requirements for classification and measurementof financial liabilities, derecognition of financialinstruments, impairment and hedge accounting areexpected to be added to IFRS 9 in 2010 as illustrated inthe timetable. As a result, IFRS 9 will eventually be acomplete replacement for IAS 39 Financial Instruments:Recognition and Measurement.

An early adopter of IFRS 9 continues to apply IAS 39 for other accounting requirements for financialinstruments within its scope that are not covered byIFRS 9 (e.g. classification and measurement of financialliabilities, recognition and derecognition of financialassets and financial liabilities, impairment of financialassets, hedge accounting, etc.).

Summary of proposals

All recognised financial assets that are currently in thescope of IAS 39 will be measured at either amortisedcost or fair value.

A debt instrument (e.g. loan receivable) that (1) is heldwithin a business model whose objective is to collect thecontractual cash flows and (2) has contractual cash flowsthat are solely payments of principal and interest on theprincipal amount outstanding generally must be measuredat amortised cost. All other debt instruments must bemeasured at fair value through profit or loss (FVTPL).

*Due to significant changes from the original exposure draft, a revised exposure draft of the proposals for derecognition isexpected to be issued.

Q1-Q3 2009

Q4 2009

H1 2010

H2 2010

2010-2012

2013

Classification andMeasurement

Impairment Hedge accounting Derecognition

Exposure draftRequest forinformation

IFRS 9 – Financialassets

Exposure draft Financial Liabilities

Final standard Financial Liabilities

Finalised standard for early adopters

Mandatory effective date

Exposure draft

Final standardImpairment

Exposure draft

Exposure draft*

Final standardHedge Accounting

Exposure draft

Final standardDerecognition

A fair value option is available (provided that certainspecified conditions are met) as an alternative to amortised cost measurement.

All equity investments within the scope of IFRS 9 are tobe measured on the statement of financial position atfair value with the default recognition of gains andlosses in profit or loss. Only if the equity investment isnot held for trading can an irrevocable election bemade at initial recognition to measure it at fair valuethrough other comprehensive income (FVTOCI) withonly dividend income recognised in profit or loss.

Despite the fair value requirement for all equityinvestments, IFRS 9 contains guidance on when costmay be the best estimate of fair value and also when itmight not be representative of fair value.

All derivatives within the scope of IFRS 9 are required tobe measured at fair value. This includes derivatives thatare settled by the delivery of unquoted equity instruments,however, in limited circumstances cost may be anappropriate estimate of fair value.

Debt instruments

A debt instrument will be measured at amortised costor FVTPL. The available-for-sale and held-to-maturityclassifications (including the associated tainting rules)that are currently in IAS 39 are eliminated under IFRS 9.A debt instrument generally must be measured atamortised cost if both the ‘business model test’ and the‘contractual cash flow characteristics test’ are satisfied.

Business model test: The objective of the entity’sbusiness model is to hold the financial asset to collectthe contractual cash flows (rather than have thebusiness model objective to sell the instrument prior toits contractual maturity to realise its fair value changes).

Contractual cash flow characteristics test: The contractual terms of the financial asset give riseon specified dates to cash flows that are solelypayments of principal and interest on the principalamount outstanding.

A debt instrument that meets both of the above criteriacan still be designated as FVTPL on initial recognition ifthe fair value designation would eliminate or significantlyreduce an accounting mismatch that would exist hadthe instrument been measured at amortised cost(equivalent to the current IAS 39 fair value option for an accounting mismatch).

If a debt instrument measured at amortised cost isderecognised prior to maturity, IAS 1 Presentation ofFinancial Statements is amended to require the gain/losson disposal to be separately presented in the statementof comprehensive income, and IFRS 7 FinancialInstruments: Disclosures is amended to require ananalysis of that gain/loss and the reasons for the sale.

Where a debt instrument does not meet the criteria foramortised cost measurement it must be measured atFVTPL.

Classification model for financial assets within the scope of IFRS 9

Yes YesYes**

No

No No

Yes

* Dividend income that represents a return on investment is presented in profit or loss.** The hedge accounting provisions of IAS 39 remain applicable to derivatives designated in effective hedge relationships.*** Reclassification required when and only when an entity changes its business model for managing its financial assets.

***

No

Yes

Yes

Yes

No

No

No

Is the entire financial asset an equity investment?

FVTOCI* FVTPL Amortised Cost

Is the equity investment held for trading?

Has the entity irrevocably designated the equity investmentas at fair value through other comprehensive income?

Has the entity invoked the fair value option to reduce an accounting measurement mismatch?

Are the contractual cash flows of the financial asset solely payments of principal and interest on the principal outstanding?

Is the entire financial asset a stand alone derivative?

Is the financial asset held with the business model objective of collecting its contractual cash flows?

Business model test

IFRS 9 introduces a business model test that requires anentity to assess whether its business objective for a debtinstrument is to collect the contractual cash flows ofthe instrument as opposed to realising its fair valuechange from sale prior to its contractual maturity. This isdetermined at a higher level than the individual financialinstrument level (e.g. portfolio or business unit level).This is not based on management’s intent for individualinstruments.

The Standard acknowledges that an entity may havedifferent business units that are managed differently.For example, an entity may have a retail bankingbusiness where the objective is to collect thecontractual cash flows of loan assets and an investmentbanking business where the objective is to realise fairvalue changes through the sale of loan assets prior totheir maturity. In this case, assuming that the financialinstruments give rise to cash flows that are payments ofprincipal and interest (see cash flow characteristic testbelow), in the retail banking business they may qualifyfor amortised cost measurement even if similar financialinstruments in the investment banking business do not.Instruments that would meet the existing held fortrading definition in IAS 39 would be measured atFVTPL as they are not held to collect the contractualcash flows of the instrument.

Although the objective of an entity’s business model maybe to hold financial assets in order to collect contractualcash flows, the entity need not hold all of those assetsuntil maturity. Thus an entity’s business model can be tohold financial assets to collect contractual cash flowseven when sales of financial assets occur. For example,an entity’s assessment that it holds investments tocollect their contractual cash flows is still valid even ifthey would sell the investments to fund capitalexpenditure. However, if more than an infrequentnumber of sales are made out of a portfolio, the entityneeds to assess whether and how such sales areconsistent with an objective of collecting contractualcash flows.

The original proposals in the exposure draft would haveprevented an asset acquired at a discount reflectingincurred credit losses (‘distressed debt’) from beingmeasured at amortised cost because it did not pass thebusiness model test. The Standard takes a differentapproach, potentially allowing distressed debt to pass thebusiness model test if the business model for the holderis to collect the contractual cash flows on the debt.

Contractual cash flow characteristics test

The requirement in IFRS 9 to assess the contractual cashflow characteristics of a financial asset has beenadapted from a similar approach applied in the IFRS forSmall and Medium-sized Entities recently issued by theIASB. The concept is that only instruments withcontractual cash flows of principal and interest onprincipal (hereafter referred to as “principal andinterest”) may qualify for amortised cost measurement.The Standard describes interest as consideration for thetime value of money and the credit risk associated withthe principal outstanding during a particular period oftime. Therefore, an investment in a convertible loannote would not qualify because of the inclusion of theconversion option which is not deemed to representpayments of principal and interest.

This criterion will permit amortised cost measurementwhen the cash flows on a loan are entirely fixed (e.g. afixed interest rate loan or zero coupon bond), or whereinterest is floating (e.g. a GBP loan where interest iscontractually linked to GBP LIBOR), or combination offixed and floating (e.g. where interest is LIBOR plus afixed spread).

Other examples provided in the Standard of instrumentsthat satisfy this criterion include:

• a variable rate instrument with a stated maturity datethat permits the borrower to choose to pay three-month LIBOR for a three-month term or one-monthLIBOR for a one-month term;

• a fixed term variable market interest rate bond wherethe variable interest rate is capped; and

• a fixed term bond where the payments of principaland interest are linked to an unleveraged inflationindex of the currency in which the instrument isissued.

Examples of instruments that do not satisfy this criterioninclude:

• a bond that is convertible into equity instruments ofthe issuer; and

• a loan that pays an inverse floating interest rate (e.g. 8% minus LIBOR).

IFRS 9 contains application guidance and furtherexamples illustrating the application of this criterion.

Embedded derivatives

IFRS 9 does not retain IAS 39’s concept of anembedded derivative for hybrid contracts if the hostcontract is a financial asset within the scope of IFRS 9.Consequently, embedded derivatives that would havebeen separately accounted for at FVTPL under IAS 39because they were not closely related to the financialasset host will no longer be separated. Instead, thecontractual cash flows of the financial asset areassessed in their entirety and the asset as a whole ismeasured at FVTPL if any of its cash flows do notrepresent payments of principal and interest asdescribed by the Standard.

As IFRS 9 only applies to financial assets in the scopeof IAS 39, the requirement to assess contractualarrangements for non-closely related embeddedderivatives still applies to all hybrid contracts with afinancial liability host and non-financial host contractsthat are outside the scope of IAS 39.

Non-recourse lending

When debt instruments are non-recourse, i.e. thelender’s claim is limited to specific assets of theborrower, it will be necessary to consider whether theloan only represents contractual cash flows that arepayments of principal and interest. The Standardrequires an entity to look through to the underlyingassets or cash flows to make this determination. If theterms of the loan give rise to any other cash flows orlimit the cash flows in a manner inconsistent withpayments representing principal and interest the loancannot be measured at amortised cost.

For example, an entity that is developing an investmentproperty may issue a fixed rate bond whose terms statethat the principal and interest on the bond arerepayable solely from the sale proceeds of thedevelopment property and without recourse to theissuing entity. Such a bond would fail the ‘contractualcash flow characteristics test’ because the underlyingasset to which the bond is contractually linked does nothave cash flow characteristics of principal and interest.

Contractually linked instruments

Where the receipts under an asset are paid by the issuerin order of priority over other multiple contractuallylinked instruments the Standard has specific conditionsfor the cash flows of such instruments to be regardedas payments of principal and interest. An examplewould be tranched notes issued from a special purposeentity set up to collateralise debt obligations wherepayments on the tranches are prioritised resulting ineach tranche being relatively more senior or moresubordinate to other tranches.

A tranche will only be regarded as containing paymentsof principal and interest (and therefore potentiallyeligible for amortised cost measurement) if all thefollowing criteria are met:

• Firstly, the tranche must only have cash flowscharacteristics that are solely payments of principaland interest on the principal outstanding (e.g. theinterest rate is not linked to, say, a commodity index).

• Secondly, the underlying pool of instruments held bythe entity issuing the tranche must contain one ormore financial assets whose contractual cash flowsare only payments of principal and interest. Theunderlying pool of instruments can contain otherinstruments, such as derivatives, but these must onlyreduce the cash flow variability of the pool ofinstruments held whose contractual cash flows aresolely payments of principal and interest or align thefixed or floating nature of the interest rate, foreigncurrency risk, or timing differences of the cash flowsof the tranches and the cash flows of the underlyingpool of financial instruments. Where derivatives areused to reduce the cash flow variability of instrumentsin the pool, the combined cash flows must give riseto payments of principal and interest for thiscondition to be satisfied.

• Thirdly, the exposure to credit risk in the underlyingpool of financial instruments inherent in the tranche isequal to or lower than the exposure to credit risk ofthe underlying pool of financial instruments.

To make this assessment the entity has to look throughuntil it can identify the pool of instruments that arecreating, rather than passing through, the cash flows.

In cases where the underlying pool of instruments canchange, all possible permitted instruments must beconsidered as part of this assessment. For example, ifthe pool of instruments at initial recognition of thetranche does not include written credit derivatives, butthe pool of instruments could include these in thefuture, then the tranche is not eligible for amortisedcost measurement.

When it is impracticable to assess the underlying poolof instruments the test is deemed to fail and thetranche must be measured at FVTPL.

Reclassifications

For debt instruments not designated at FVTPL under thefair value option, reclassification is required betweenFVTPL and amortised cost, or vice versa, if the entity’sbusiness model objective for its financial assets changesso that its previous model no longer applies. Forexample, reclassification from amortised cost to fairvalue might be required when a financial services firmdecides to shut down its retail mortgage business and itno longer accepts new business and is activelymarketing its mortgage loan portfolio for sale.

When a reclassification is required it is applied from firstday of the first reporting period following the change inbusiness model. The Standard expects reclassificationsto occur very infrequently.

Fair value option

An entity may irrevocably elect on initial recognition tomeasure a financial asset at FVTPL if that designationeliminates or significantly reduces an accountingmismatch had the financial asset been measured atamortised cost.

For example, an entity may hold a fixed rate loanreceivable that it commercially hedges with an interestrate swap, with matching terms, that swaps the fixedrate to a floating rate. Assuming the conditions foramortised cost measurement are met, measuring theloan asset at amortised cost would create ameasurement mismatch with the interest rate swapheld at FVTPL. In this case the loan receivable could bedesignated at FVTPL under the fair value option toreduce the measurement mismatch that arises frommeasuring the loan at amortised cost.

Equity investments

Under IFRS 9 all equity investments held must bemeasured at fair value. The current exemption in IAS 39that requires unquoted equity investments to bemeasured at cost less impairment where fair valuation isnot sufficiently reliable is not available under the newStandard. However, IFRS 9 does contain guidance onwhen cost might be the best estimate of fair value ofan unquoted equity investment that is difficult to valuebecause of little or no timely or relevant information.It also gives examples of when cost will not berepresentative of fair value such as when there hasbeen a significant change in the performance of theinvestee compared with budgets, plans or milestones.

Gains and losses arising on equity investments arerecognised in profit or loss (i.e. they are measured atFVTPL) unless the entity irrevocably designates at initialrecognition that they should be recognised in othercomprehensive income (i.e. designating them as atFVTOCI). Designation at FVTOCI is not permitted if theequity investment is held for trading.

If the equity investment is designated as at FVTOCI thenall gains or losses (except dividend income) arerecognised in other comprehensive income without anysubsequent reclassification to profit or loss (although atransfer of the cumulative gain within equity ispermitted). Dividend income is recognised in profit orloss in accordance with IAS 18 Revenue.

Designation as at FVTOCI means that the currentrequirements in IAS 39 to perform an assessment ofimpairment and to reclassify cumulative fair value gainsor losses on disposal no longer apply because all fairvalue movements other than dividend income remainpermanently in equity.

As a consequential amendment, IFRS 7 is amended torequire extensive disclosures regarding investments inequity instruments designated as at FVTOCI, includingwhy an entity has chosen to designate as at FVTOCI.

Derivatives

Under IFRS 9, all derivatives within its scope must bemeasured at fair value; therefore similar to the changesregarding equity investments described above, the newStandard removes the requirement to measure at costderivatives that are linked to and will result in thedelivery of an unquoted equity investment where fairvalue is not sufficiently reliable. However, IFRS 9describes in certain limited cases where cost maybeacceptable as a best estimate of fair value.

Impact of IFRS 9

In some cases IFRS 9 will result in more financial assetsat fair value, in others less. The impact will depend onwhat types of financial asset an entity holds, how it hasclassified them previously, and what choices it makesunder the new classification model.

One of the most significant changes will be the ability to measure some debt instruments (e.g. investments ingovernment and corporate bonds) at amortised costwhich under IAS 39 would in many cases have beenmeasured at fair value if quoted in an active market.Other instruments, such as asset-backed securities (e.g. some cash-collateralised debt obligations) andservice concession receivables, that may under IAS 39have been measured entirely at amortised cost or asavailable-for-sale will more likely be measured at FVTPL.

Hybrid financial assets with separated embeddedderivatives at FVTPL (e.g. synthetic-collateralised debtobligations) will instead by measured at FVTPL in theirentirety.

Assets that are currently classified as held-to-maturityare likely to continue to be measured at amortised costas they are held to collect the contractual cash flowsand often give rise to only payments of principal andinterest. However, the current tainting rules andrestrictions from applying hedge accounting for interestrate risk or prepayment risk that apply to held-to-maturityassets will be removed.

The elimination of the available-for-sale category andthe requirement for all equity investments to bemeasured at fair value removes the multiple impairmentmethodologies that currently exist in IAS 39 (asillustrated in the table on the next page). IFRS 9 onlyrequires impairment assessment for financial assetsmeasured at amortised cost. The rules on impairingamortised cost assets remain unchanged at this stage,but they are potentially subject to change under theproposals in the IASB’s exposure draft FinancialInstruments: Amortised Cost and Impairment, issued inNovember 2009, which proposes an ‘expected loss’approach to impairment measurement.

Impact of IFRS 9

More

Less More

• Quoted equity (FVTPL).• Government and corporate bonds held to sell prior to maturity (to realise fair value changes).

Balance sheet volatility

• Trade receivable.• Derivatives.• Held for trading Instruments.

• Government and corporate bonds held to collect contractual cash flows.

• Quoted equity (elected to FVTOCI).

• Unquoted equity previously held at cost (FVTPL).• Certain tranched notes.

• Unquoted equity previously held at cost (elected to FVTOCI).

P&L

vola

tilit

y

Effective date, comparative information andtransition

The effective date of IFRS 9 is for annual periodsbeginning on or after 1 January 2013, with earlyadoption permitted.

The Standard is required to be applied retrospectively.However, the business model assessment is to be madeat the date of initial application (which is the date whenan entity first applies IFRS 9). Also, designation as atFVTPL or FVTOCI, or de-designation of financialinstruments that were previously designated as atFVTPL, is to be made on the basis of the facts andcircumstances that existed at the date of initialapplication.

A financial asset or financial liability designated as atFVTPL under existing IAS 39 on the basis of anaccounting mismatch can only be retained if theaccounting mismatch continues to exist at the date ofinitial application. If the accounting mismatch does notexist at the date of initial application then the previouslydesignated fair value option must be revoked. An entitymay also choose to revoke its previous designation of afinancial asset or financial liability as at FVTPL if it hadpreviously been designated due to an accountingmismatch.

In cases where retrospective application is not practicalor requires hindsight, other practical expedients otherthan full retrospective application are required.

Entities adopting the new Standard with an initialapplication date before 1 January 2012 will be exemptfrom the requirement to restate prior periods. A similarexemption is also included as a consequentialamendment in IFRS 1 First-time Adoption ofInternational Financial Reporting Standards to providefirst-time adopters the same allowance.

In October 2009, the IASB tentatively agreed that earlyadopters of any phase of the project to replace IAS 39before its effective date will also be required to adoptearlier phases of the project but are not required toadopt later phases before their effective dates. Basedon these tentative conclusions, an entity that earlyadopts this revised classification and measurementstandard for financial assets would not be required toearly adopt later additions to IFRS 9 in respect ofclassification and measurement of financial liabilities,derecognition of financial instruments, impairment orhedge accounting.

Financial liabilities

The scope of the original exposure draft for thisStandard included both financial assets and financialliabilities. Comments received from respondents to theexposure draft raised concerns about the requirementfor financial liabilities with cash flow characteristics thatdo not represent payments solely of principal andinterest to be measured at FVTPL in their entirety due tothe resulting fair value movements due to own creditrisk being recognised in profit or loss. This compares tocurrent IAS 39 when in many instances suchinstruments would only be partially measured at FVTPL,being an embedded derivative, with a host contractfinancial liability measured at amortised cost. Financialliabilities were therefore scoped out of IFRS 9 at thisstage to allow further consideration of the treatment ofsuch instruments. An entity early adopting IFRS 9 as itcurrently stands would continue to apply the existingrequirements in IAS 39 for classification andmeasurement of financial liabilities. New requirementsfor accounting for financial liabilities are expected to beissued in 2010.

Financial asset IAS 39 classification Impairment testingrequired?

IFRS 9 classification Impairment testingrequired?

Debt instruments Available-for-sale Yes Amortised cost Yes

Loan and receivable Yes FVTPL No

Held-to-maturity Yes

FVTPL No

Equity investments Available-for-sale Yes FVTOCI No

Cost less impairment Yes FVTPL No

FVTPL No

Changes in the requirement to test financial assets for impairment

For more information on Deloitte Touche Tohmatsu, please access our website at www.deloitte.com

Deloitte provides audit, tax, consulting, and financial advisory services to public and private clients spanning multiple industries.With a globally connected network of member firms in 140 countries, Deloitte brings world-class capabilities and deep local expertiseto help clients succeed wherever they operate. Deloitte’s 150,000 professionals are committed to becoming the standard of excellence.

Deloitte’s professionals are unified by a collaborative culture that fosters integrity, outstanding value to markets and clients,commitment to each other, and strength from cultural diversity. They enjoy an environment of continuous learning, challengingexperiences, and enriching career opportunities. Deloitte’s professionals are dedicated to strengthening corporate responsibility,building public trust, and making a positive impact in their communities.

Deloitte refers to one or more of Deloitte Touche Tohmatsu, a Swiss Verein, and its network of member firms, each of which is a legally separate and independent entity. Please see www.deloitte.com/about for a detailed description of the legal structure ofDeloitte Touche Tohmatsu and its member firms.

This publication contains general information only and is not intended to be comprehensive nor to provide specific accounting,business, financial, investment, legal, tax or other professional advice or services. This publication is not a substitute for suchprofessional advice or services, and it should not be acted on or relied upon or used as a basis for any decision or action that mayaffect you or your business. Before making any decision or taking any action that may affect you or your business, you shouldconsult a qualified professional advisor.

Whilst every effort has been made to ensure the accuracy of the information contained in this publication, this cannot be guaranteed,and neither Deloitte Touche Tohmatsu nor any related entity shall have any liability to any person or entity that relies on theinformation contained in this publication. Any such reliance is solely at the user’s risk.

© Deloitte Touche Tohmatsu 2009. All rights reserved.

Designed and produced by The Creative Studio at Deloitte, London. 953A