ifrs 10 consolidated financial statements · pwc slide 5 2012 ifrs update 2012 ability to use power...

TRANSCRIPT

IFRS 10 Consolidated Financial Statements

2012

www.pwc.co.uk

Agenda

Introduction

What is control?

Power

• Relevant activities

PwC

• Ability to direct relevant activities

Variable returns

Questions

Slide 220122012 IFRS Update

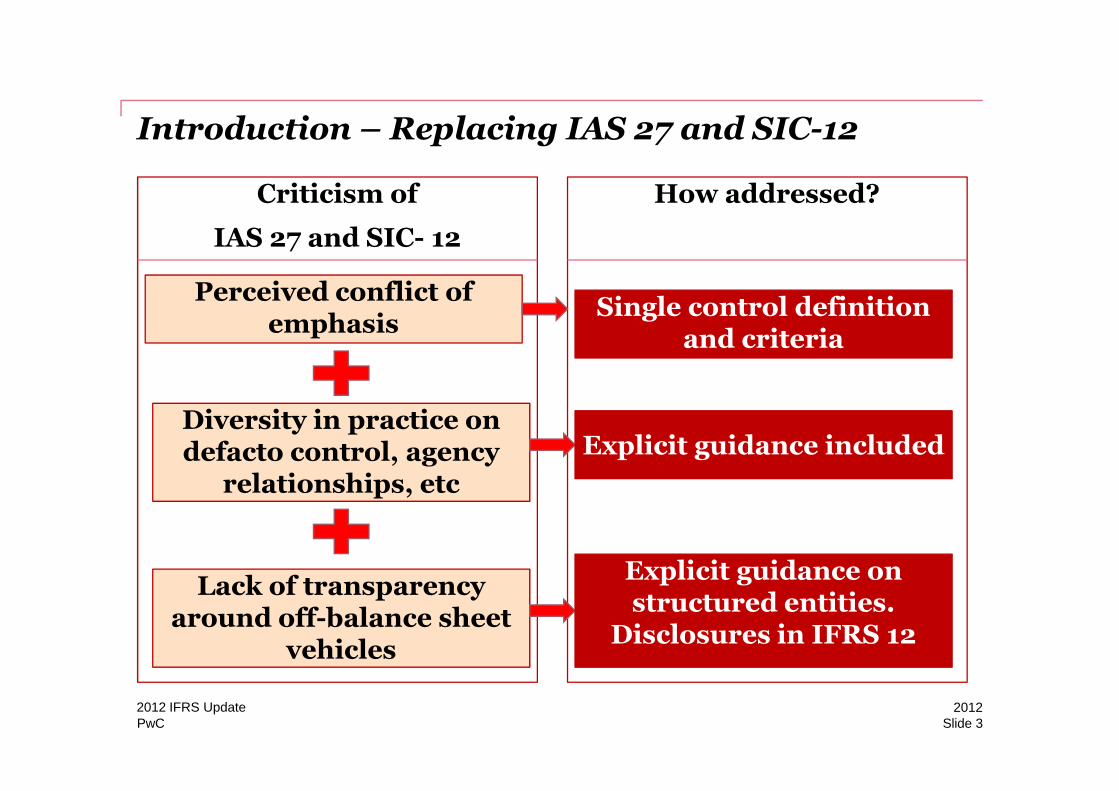

Introduction – Replacing IAS 27 and SIC-12

Criticism of

IAS 27 and SIC- 12

How addressed?

Perceived conflict of emphasis

Single control definition and criteria

PwC Slide 320122012 IFRS Update

Diversity in practice on defacto control, agency

relationships, etc

Lack of transparency around off-balance sheet

vehicles

Explicit guidance included

Explicit guidance on structured entities.

Disclosures in IFRS 12

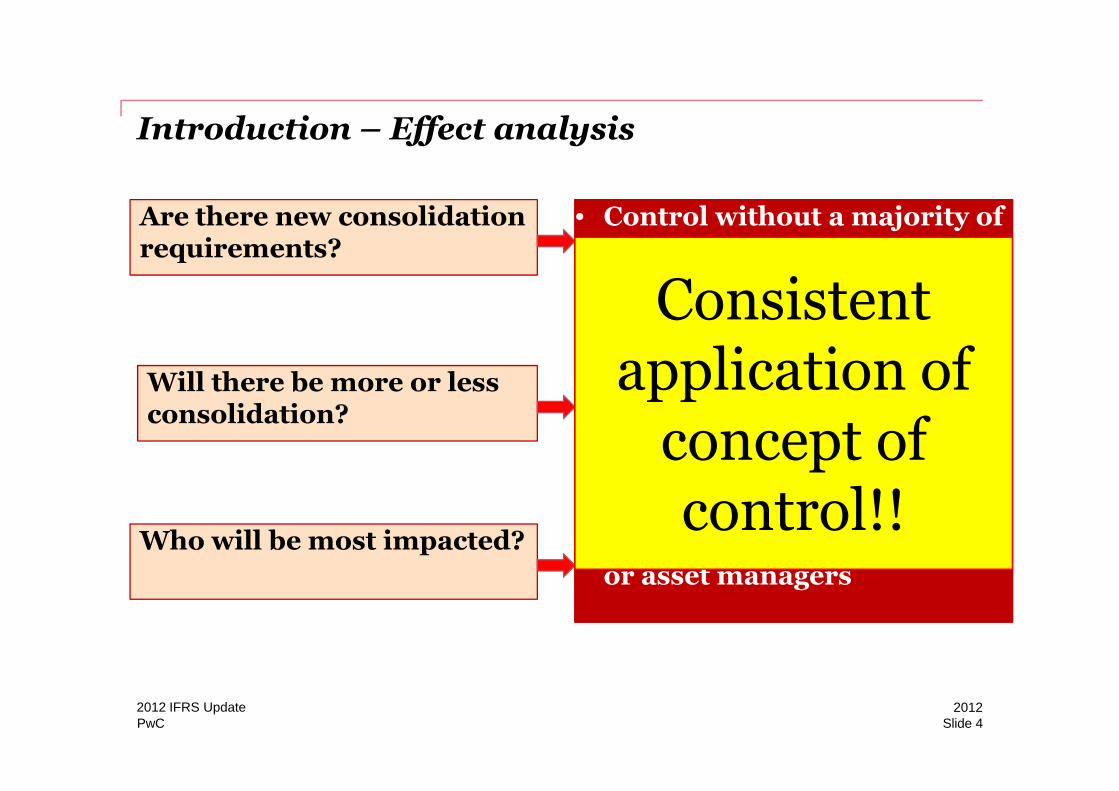

Introduction – Effect analysis

Are there new consolidation requirements?

Will there be more or less

• No new concepts introduced. Builds on existing control guidance.

• Adds additional context and application guidance

• Most consolidation decisions may be unaffected

• May result in more consolidation or de-consolidation depending on

• Control without a majority of voting rights

• Structured entities – Banks and financial institutions

Consistent application of

PwC Slide 420122012 IFRS Update

Will there be more or less consolidation?

Who will be most impacted?

application guidance

• IFRS 10 will change the way control is assessed – focus on all three elements of control

consolidation depending on bright lines applied under IAS 27/SIC 12

• Will result in more appropriate consolidation

• Potential voting rights

• Agency relationships – Fund or asset managers

application of concept of control!!

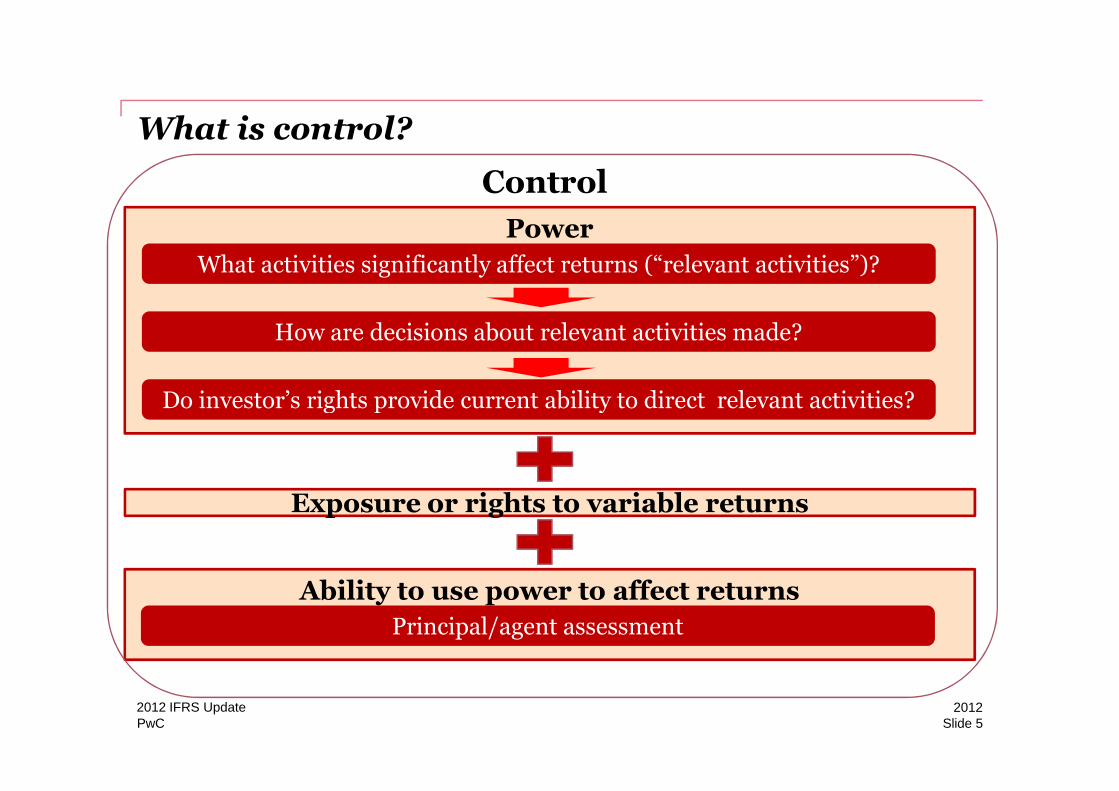

What is control?

Power

What activities significantly affect returns (“relevant activities”)?

How are decisions about relevant activities made?

Do investor’s rights provide current ability to direct relevant activities?

Control

PwC Slide 520122012 IFRS Update

Ability to use power to affect returns

Do investor’s rights provide current ability to direct relevant activities?

Principal/agent assessment

Exposure or rights to variable returns

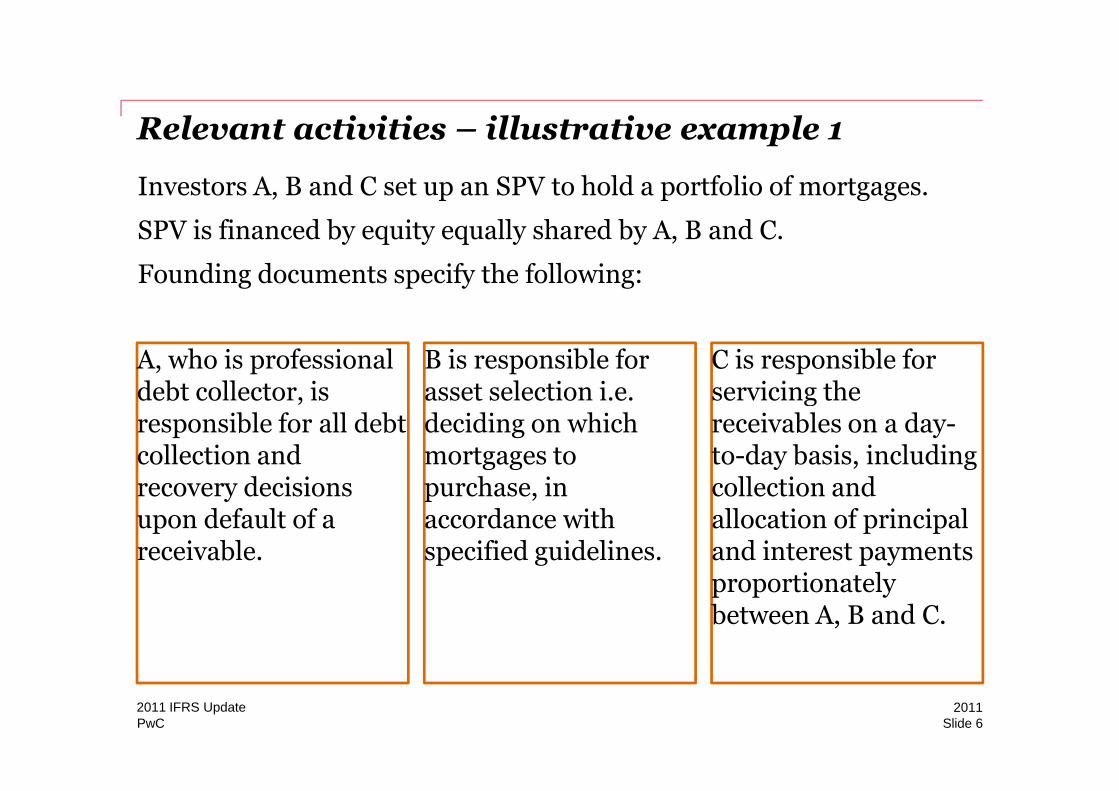

Relevant activities – illustrative example 1

A, who is professional debt collector, is

B is responsible for asset selection i.e.

C is responsible for servicing the

Investors A, B and C set up an SPV to hold a portfolio of mortgages.

SPV is financed by equity equally shared by A, B and C.

Founding documents specify the following:

PwC

debt collector, is responsible for all debt collection and recovery decisions upon default of a receivable.

asset selection i.e. deciding on which mortgages to purchase, in accordance with specified guidelines.

servicing the receivables on a day-to-day basis, including collection and allocation of principal and interest payments proportionately between A, B and C.

20112011 IFRS UpdateSlide 6

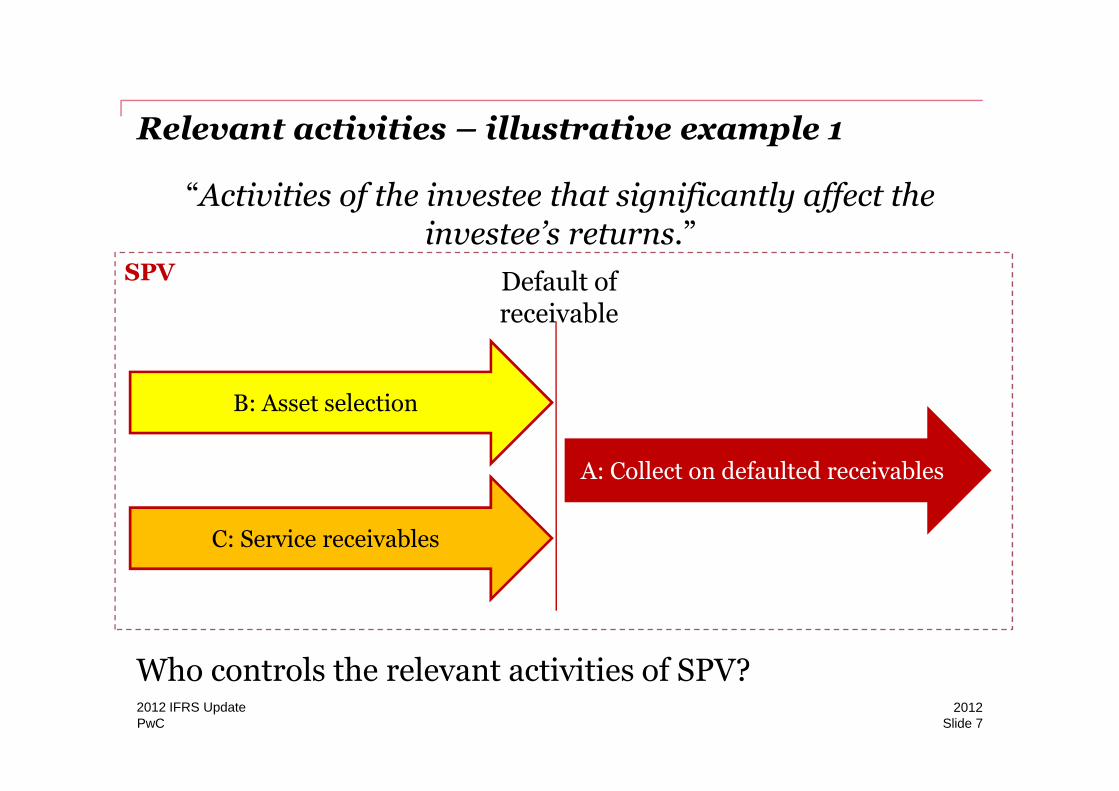

Relevant activities – illustrative example 1

“Activities of the investee that significantly affect the investee’s returns.”

Default of receivable

B: Asset selection

SPV

PwC

A: Collect on defaulted receivables

C: Service receivables

B: Asset selection

Who controls the relevant activities of SPV?

Slide 720122012 IFRS Update

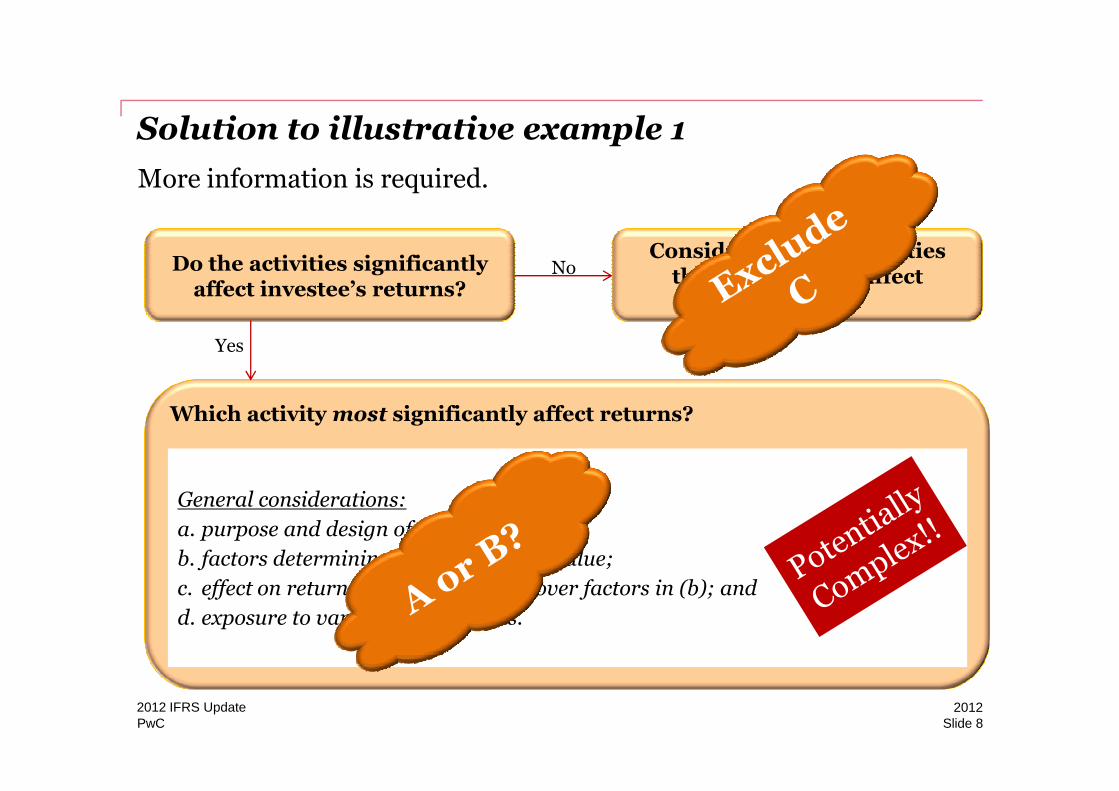

Solution to illustrative example 1

Do the activities significantly affect investee’s returns?

Consider only the activities that significantly affect

returns.

No

Yes

More information is required.

PwC Slide 820122012 IFRS Update

Which activity most significantly affect returns?

General considerations:

a. purpose and design of investee;

b. factors determining profit, revenue , value;

c. effect on returns of decision power over factors in (b); and

d. exposure to variability of returns.

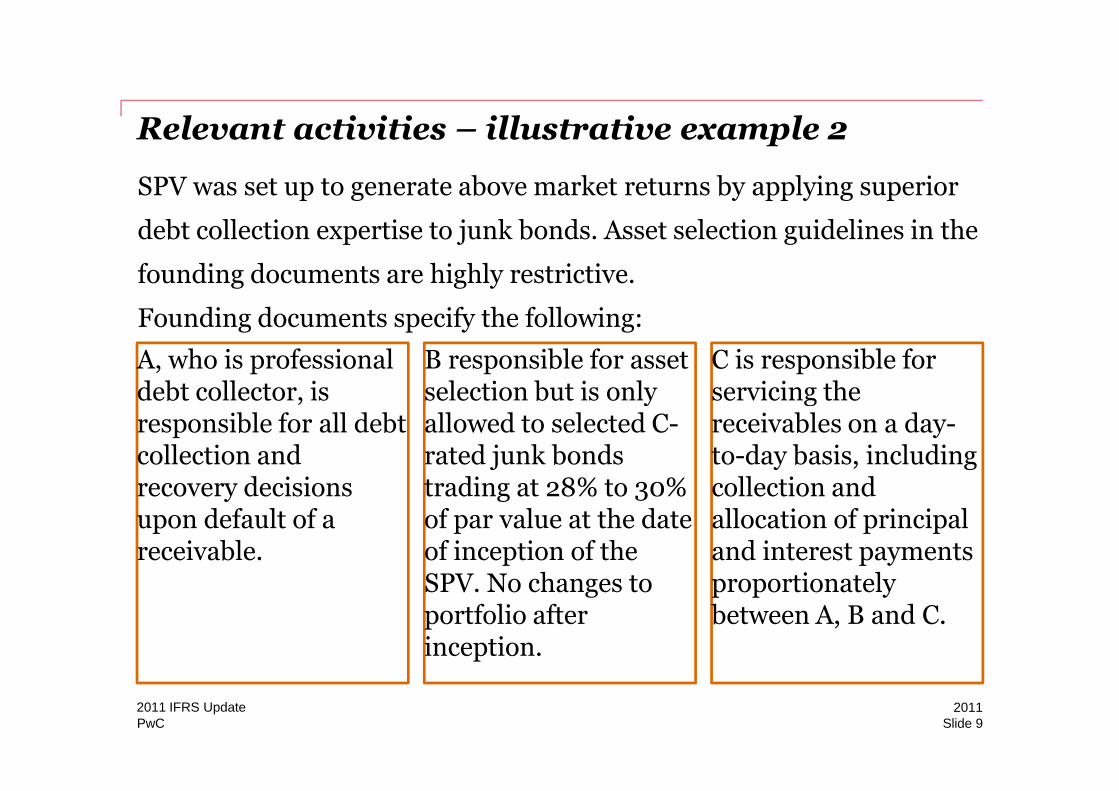

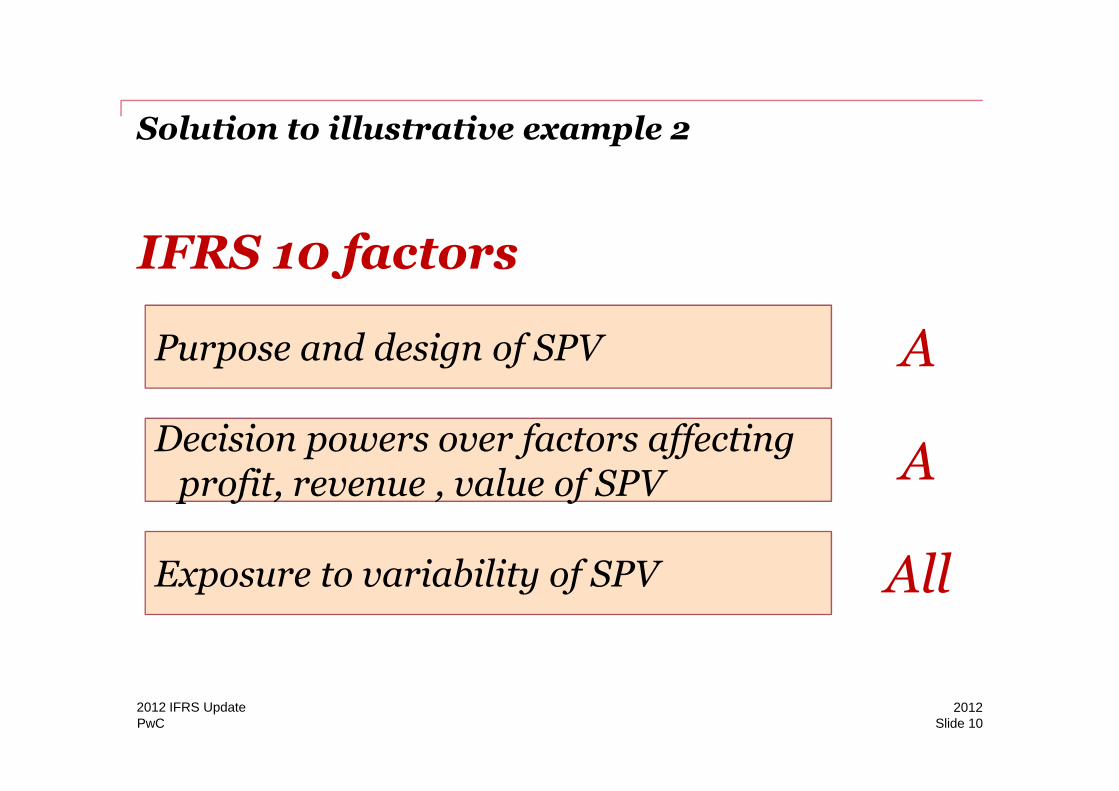

Relevant activities – illustrative example 2

A, who is professional debt collector, is

B responsible for asset selection but is only

C is responsible for servicing the

SPV was set up to generate above market returns by applying superior

debt collection expertise to junk bonds. Asset selection guidelines in the

founding documents are highly restrictive.

Founding documents specify the following:

PwC

debt collector, is responsible for all debt collection and recovery decisions upon default of a receivable.

selection but is only allowed to selected C-rated junk bonds trading at 28% to 30% of par value at the date of inception of the SPV. No changes to portfolio after inception.

servicing the receivables on a day-to-day basis, including collection and allocation of principal and interest payments proportionately between A, B and C.

20112011 IFRS UpdateSlide 9

Solution to illustrative example 2

Purpose and design of SPV A

IFRS 10 factors

PwC20122012 IFRS Update

Slide 10

Decision powers over factors affecting profit, revenue , value of SPV

Exposure to variability of SPV

A

All

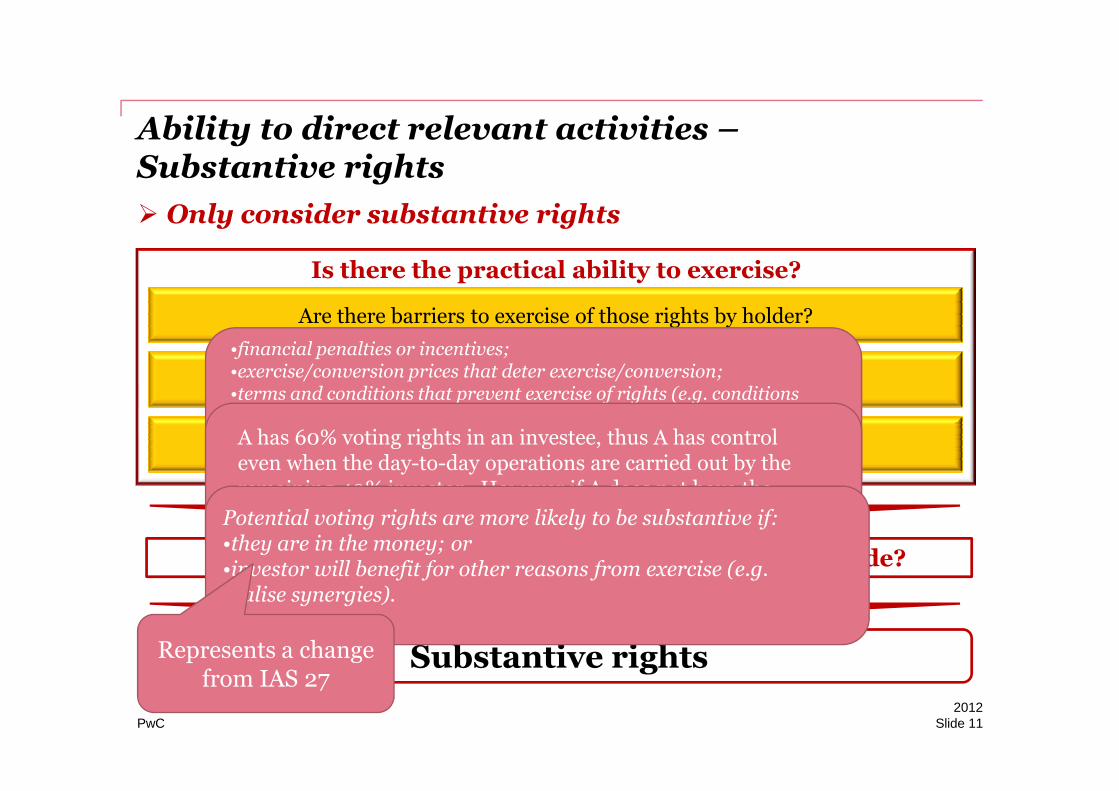

Ability to direct relevant activities –Substantive rights

Is there the practical ability to exercise?

Are there barriers to exercise of those rights by holder?

Do practical mechanisms exist for collective exercise of rights?

� Only consider substantive rights

•financial penalties or incentives;•exercise/conversion prices that deter exercise/conversion;•terms and conditions that prevent exercise of rights (e.g. conditions

PwC Slide 112012

Is the right exercisable when decisions need to be made?

Yes

Substantive rights

Yes

Will the holder benefit from the exercise of those rights?

•terms and conditions that prevent exercise of rights (e.g. conditions that narrowly limit timing of exercise); •the lack of an explicit, reasonable mechanism through which holders can exercise their rights; •inability to obtain information needed to exercise rights;

A has 60% voting rights in an investee, thus A has control even when the day-to-day operations are carried out by the remaining 40% investor. However if A does not have the ability to exercise that voting right, A does not have control.Potential voting rights are more likely to be substantive if:

•they are in the money; or •investor will benefit for other reasons from exercise (e.g. realise synergies).

Represents a change from IAS 27

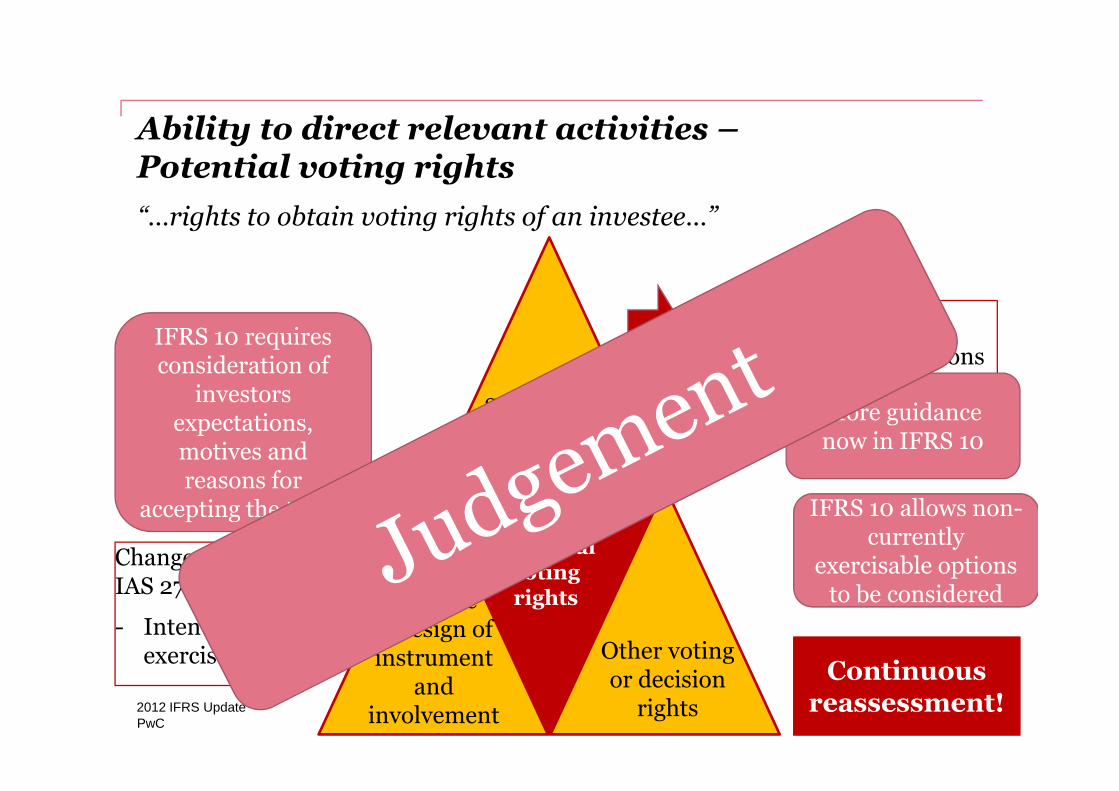

Ability to direct relevant activities –Potential voting rights

Substantive

“…rights to obtain voting rights of an investee…”

Changes from IAS 27:

- in/out of money options

- timing of exercise

IFRS 10 requires consideration of

investors

PwC Slide 1220122012 IFRS Update

Substantive or

protective?

Purpose & design of instrument

and involvement

Other voting or decision

rights

Potential voting rights

- timing of exercise

Changes from IAS 27:

- Intention to exercise

Continuous reassessment!

More guidance now in IFRS 10

IFRS 10 allows non-currently

exercisable options to be considered

investors expectations, motives and reasons for

accepting the terms

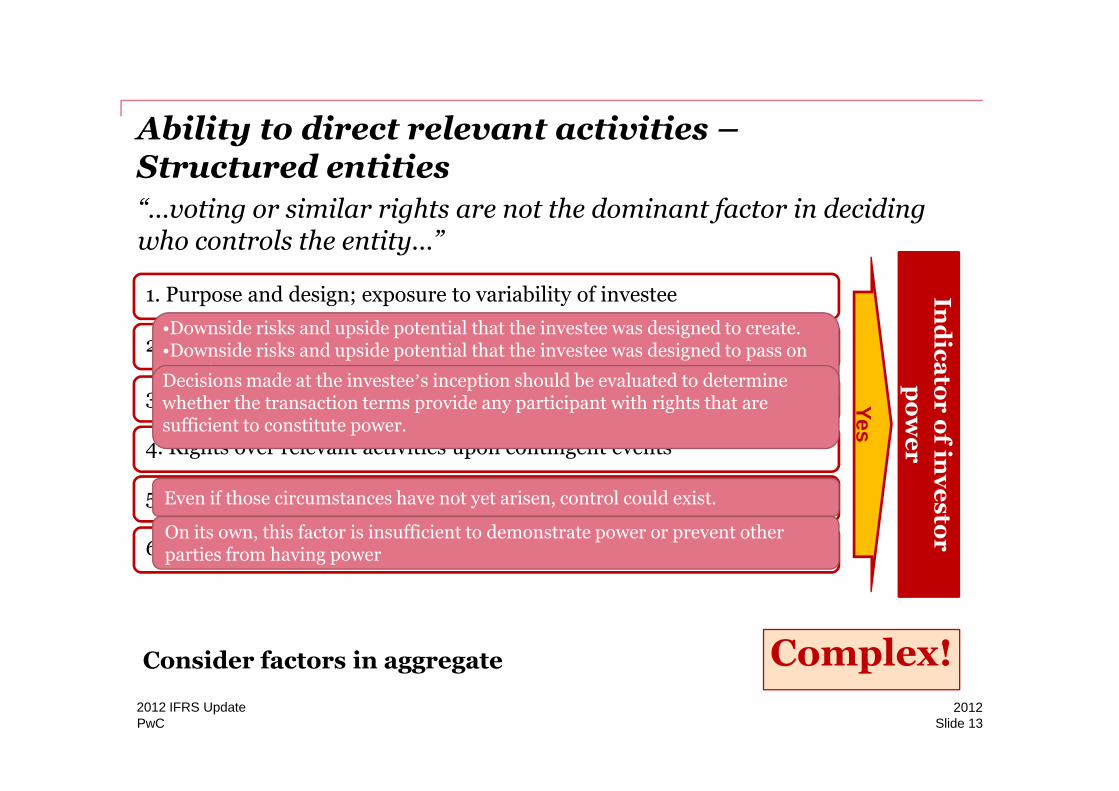

Ability to direct relevant activities –Structured entities

1. Purpose and design; exposure to variability of investee

2. Involvement at inception; inception decisions that provide power

3. Contracts providing rights over closely-related activities

Indicator of in

vestor

power

“…voting or similar rights are not the dominant factor in deciding who controls the entity…”

•Downside risks and upside potential that the investee was designed to create. •Downside risks and upside potential that the investee was designed to pass onto other parties in the transaction.

•Whether the investor is exposed to those risks and upside potential. Decisions made at the investee’s inception should be evaluated to determine whether the transaction terms provide any participant with rights that are

PwC Slide 1320122012 IFRS Update

3. Contracts providing rights over closely-related activities

4. Rights over relevant activities upon contingent events

5. Commitment to ensure investee operates as designed

6. Other factors

Indicator of in

vestor

power

Yes

Consider factors in aggregate Complex!

•Whether the investor is exposed to those risks and upside potential. whether the transaction terms provide any participant with rights that are sufficient to constitute power.

Even if those circumstances have not yet arisen, control could exist.

On its own, this factor is insufficient to demonstrate power or prevent other parties from having power

Variable returns

“…investor’s returns from its involvement have the potential to vary as a result of the investee’s performance…”

• Many possible forms, e.g.

� Dividends

� Servicing fees

Could be positive or negative

PwC Slide 1420122012 IFRS Update

� Servicing fees

� Tax benefits

� Economies of scale

• Assessment made based on the substance of the arrangement regardless of legal form of returns

Variable returns – Absorber vs. contributor

• For assessing exposure to variable returns – consider instruments that absorb variability (e.g. shares) of investee’s performance

• Contributors of variability (e.g. debtors) are irrelevant.

• Assessment can get complex

PwC Slide 1520122012 IFRS Update

• Assessment can get complex

• Swap/derivative contracts

• Leasing arrangements ( Residual value guarantees, extensions option)

• Shareholder being a creditor to the investee

Complex – Please consult!

Key points

• Control comprises all of power, exposure to variable returns, and the ability to use power to influence returns

• Relevant activities significantly affect investee’s returns

� Consider power over relevant activities only.

• Consider only substantive rights

PwC

• Consider only substantive rights

• Structured entities are not controlled by voting rights

� Potentially complex consolidation analysis

• Contributors of variability are not exposed to variable returns

20122012 IFRS UpdateSlide 16

Questions

PwC20122012 IFRS Update

Slide 17

IFRS 11 - Classification of joint arrangements

www.pwc.co.uk

Agenda

Principles of classification

Focus on ‘other facts and circumstances’

PwC

Case studies

Slide 192012 IFRS Update

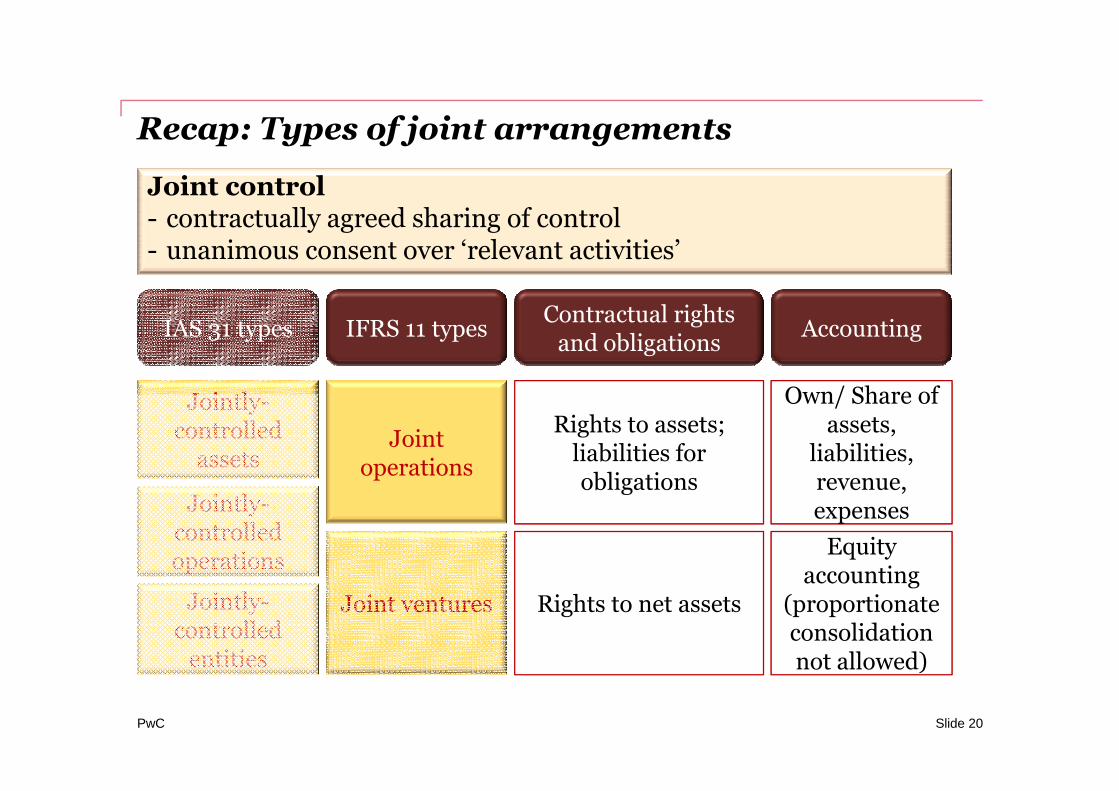

Recap: Types of joint arrangements

IAS 31 types IFRS 11 typesContractual rights and obligations

Accounting

Jointly- Own/ Share of

Joint control- contractually agreed sharing of control - unanimous consent over ‘relevant activities’

PwC

Jointly-controlled

assets

Jointly-controlled operations

Jointly-controlled entities

Joint operations

Joint ventures

Rights to assets; liabilities for obligations

Rights to net assets

Own/ Share of assets,

liabilities, revenue, expenses

Equity accounting

(proportionate consolidation not allowed)

Slide 20

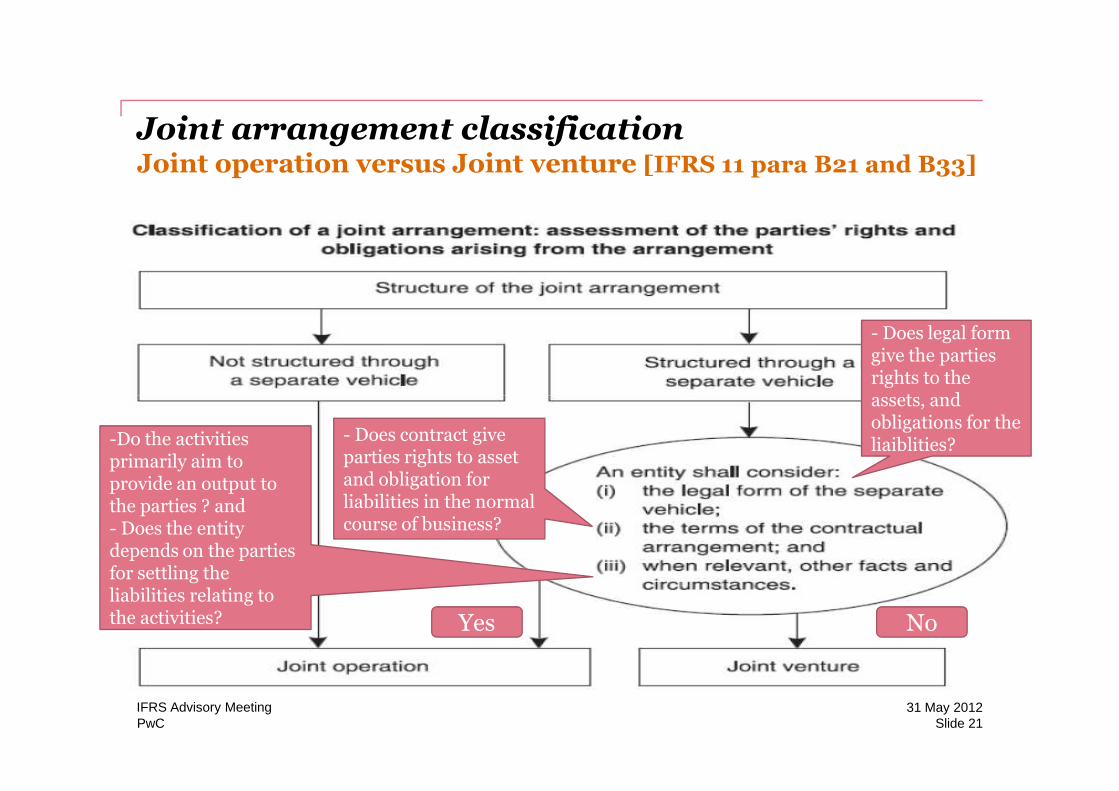

Joint arrangement classificationJoint operation versus Joint venture [IFRS 11 para B21 and B33]

- Does legal form give the parties rights to the assets, and

PwC

-Do the activities primarily aim to provide an output to the parties ? and- Does the entity depends on the parties for settling the liabilities relating to the activities?

assets, and obligations for the liaiblities?

- Does contract give parties rights to asset and obligation for liabilities in the normal course of business?

Slide 2131 May 2012IFRS Advisory Meeting

Yes No

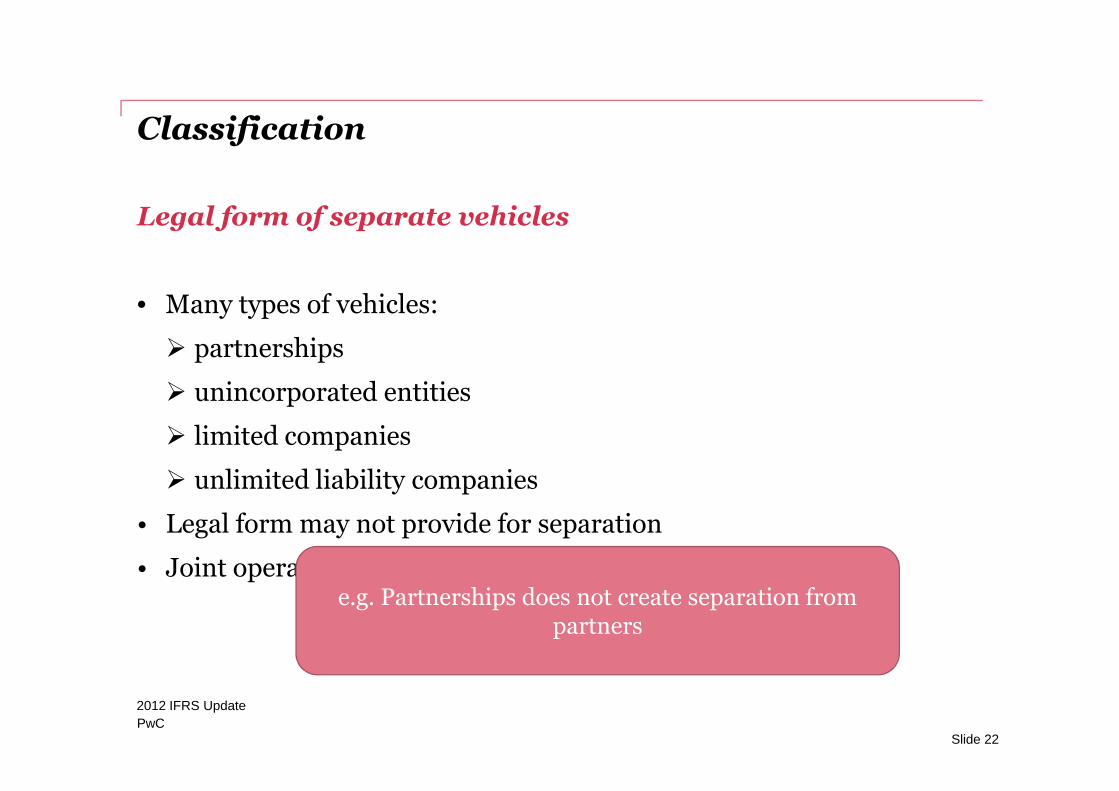

Classification

Legal form of separate vehicles

• Many types of vehicles:

� partnerships

� unincorporated entities

PwC

� unincorporated entities

� limited companies

� unlimited liability companies

• Legal form may not provide for separation

• Joint operations if no legal separation

2012 IFRS Update

Slide 22

e.g. Partnerships does not create separation from partners

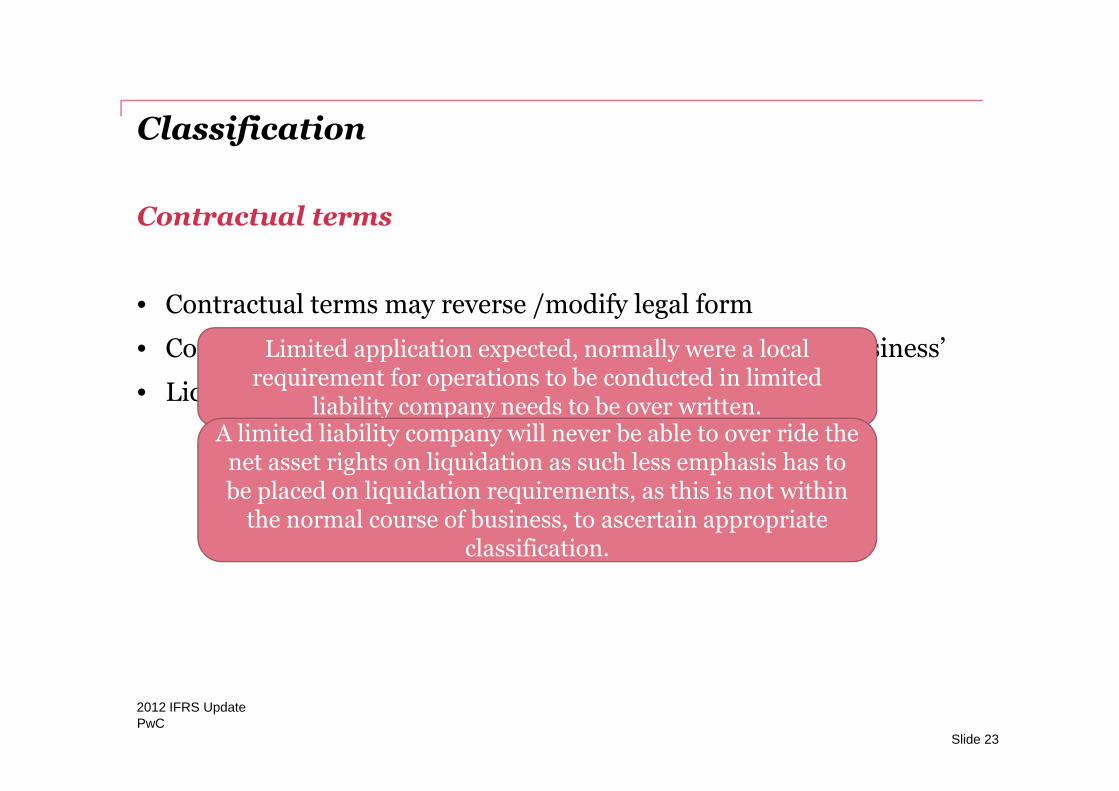

Classification

Contractual terms

• Contractual terms may reverse /modify legal form

• Consider only rights and obligations in ‘normal course of business’

• Liquidation and bankruptcy rights less relevant

Limited application expected, normally were a local requirement for operations to be conducted in limited

liability company needs to be over written.

PwC

• Liquidation and bankruptcy rights less relevant

2012 IFRS Update

Slide 23

liability company needs to be over written.A limited liability company will never be able to over ride the net asset rights on liquidation as such less emphasis has to be placed on liquidation requirements, as this is not within

the normal course of business, to ascertain appropriate classification.

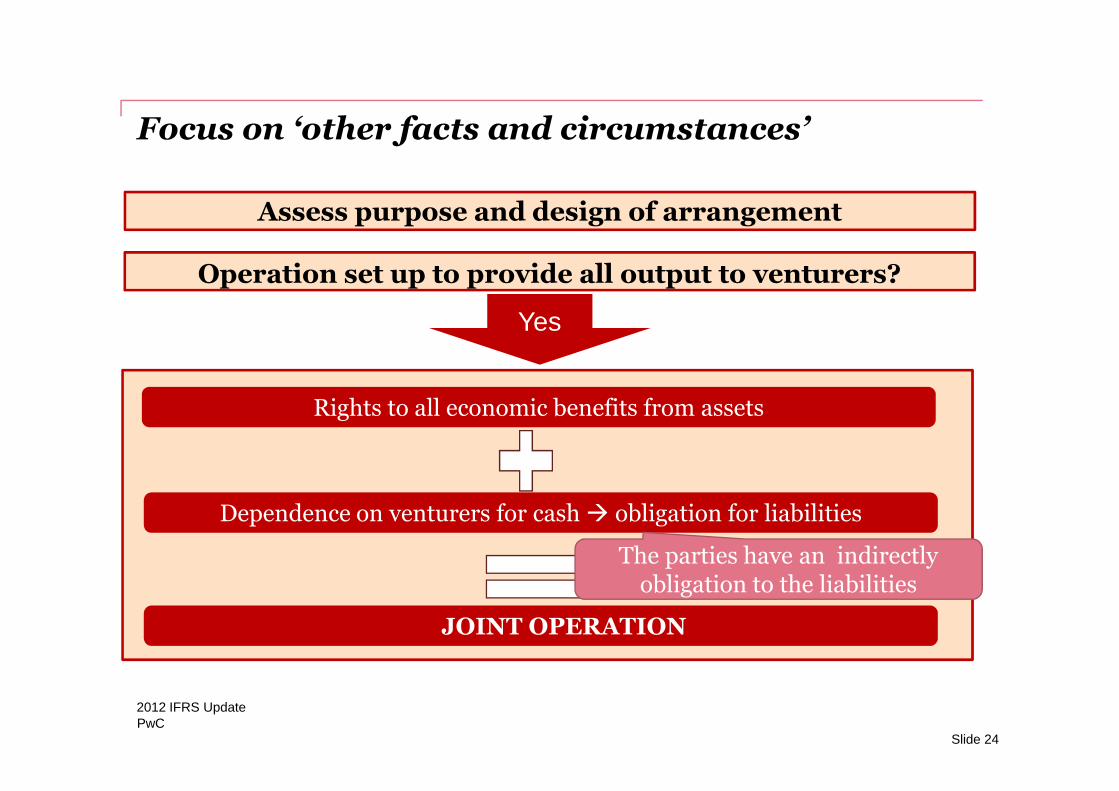

Focus on ‘other facts and circumstances’

Assess purpose and design of arrangement

Operation set up to provide all output to venturers?

Rights to all economic benefits from assets

Yes

PwC

Rights to all economic benefits from assets

Dependence on venturers for cash � obligation for liabilities

JOINT OPERATION

Slide 24

2012 IFRS Update

The parties have an indirectly obligation to the liabilities

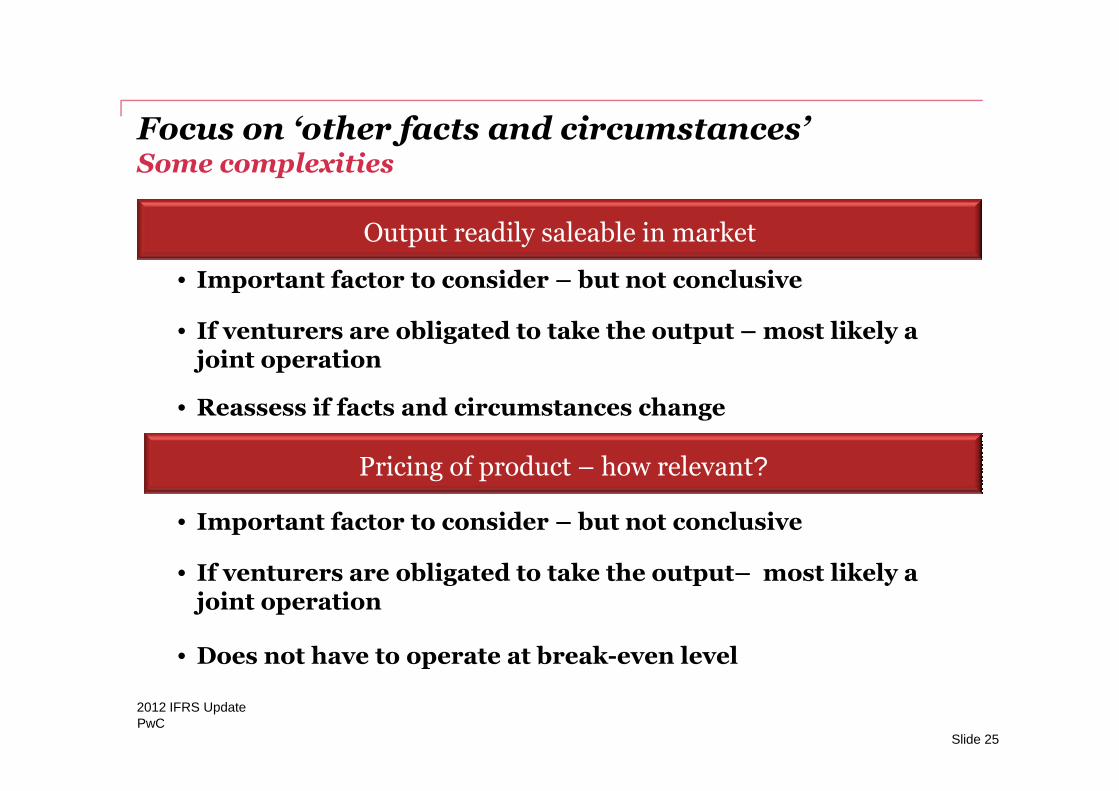

Focus on ‘other facts and circumstances’ Some complexities

Output readily saleable in market

• Important factor to consider – but not conclusive

• If venturers are obligated to take the output – most likely a joint operation

• Reassess if facts and circumstances change

PwC2012 IFRS Update

Slide 25

• Reassess if facts and circumstances change

Pricing of product – how relevant?

• Important factor to consider – but not conclusive

• If venturers are obligated to take the output– most likely a joint operation

• Does not have to operate at break-even level

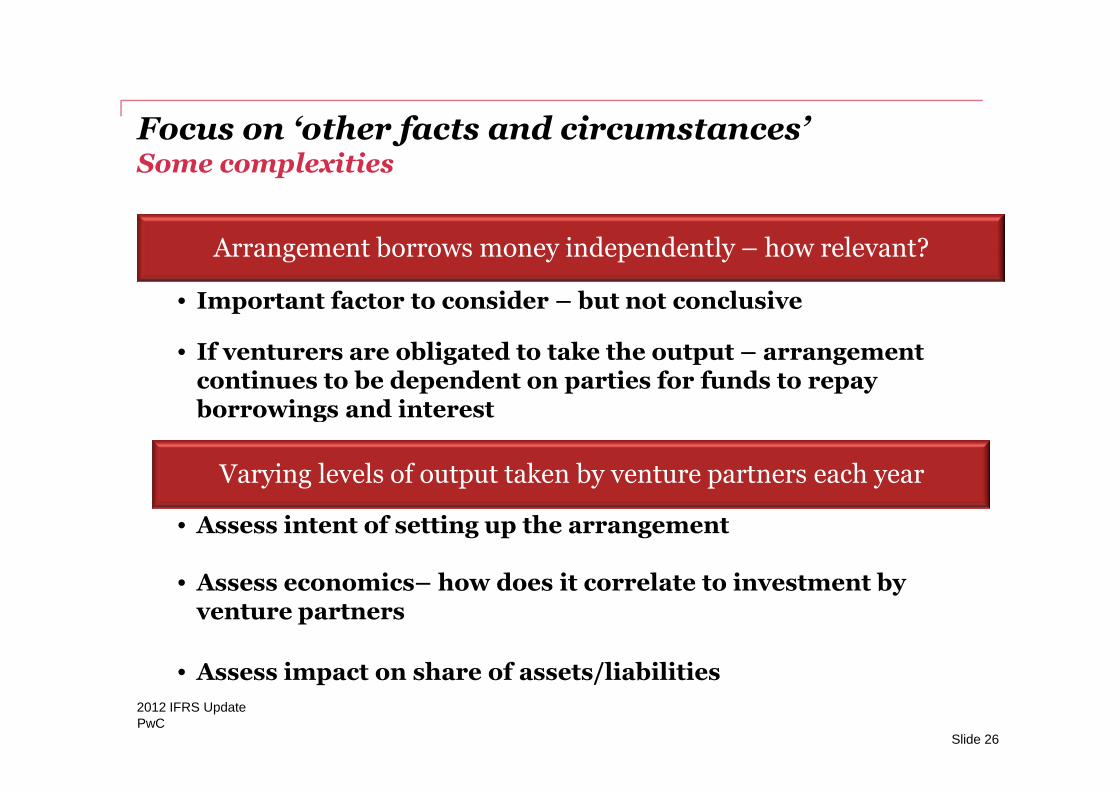

Focus on ‘other facts and circumstances’ Some complexities

Arrangement borrows money independently – how relevant?

• Important factor to consider – but not conclusive

• If venturers are obligated to take the output – arrangement continues to be dependent on parties for funds to repay borrowings and interest

PwC2012 IFRS Update

Slide 26

borrowings and interest

Varying levels of output taken by venture partners each year

• Assess intent of setting up the arrangement

• Assess economics– how does it correlate to investment by venture partners

• Assess impact on share of assets/liabilities

Key learning points

Classification is key to accounting for joint arrangements

Assess purpose and design for ‘other facts and circumstances’

PwC2012 IFRS Update

Slide 27

If venturers are obligated to take the output - pricing of output, ability to sell to third parties and borrowings are less relevant

When facts and circumstances change, re-assess classification.

Questions

© 2012 PwC. All rights reserved. Not for further distribution without the permission of PwC. "PwC" refers to the network of member firms of PricewaterhouseCoopers International Limited (PwCIL), or, as the context requires, individual member firms of the PwC network. Each member firm is a separate legal entity and does not act as agent of PwCIL or any other member firm. PwCIL does not provide any services to clients. PwCIL is not responsible or liable for the acts or omissions of any of its member firms nor can it control the exercise of their professional judgment or bind them in any way. No member firm is responsible or liable for the acts or omissions of any other member firm nor can it control the exercise of another member firm's professional judgment or bind another member firm or PwCIL in any way.

The training was brought to you by PwC’s Business School.

The content of this presentation is based on the current status of International Financial Reporting Standards (IFRS), its exposure drafts, interpretations and best practice. The information, comments and material presented in this document are provided for information purposes only and are not to be used or considered as specific advice to account for transactions. When determining the proper accounting treatment the specific circumstances of each entity or transaction need to be taken into account. The presentation is not addressing all possible technical aspects and does not claim to be complete or exhaustive.

PricewaterhouseCoopers (PwC) will not accept any liability related to the information provided in this presentation and its interpretation. This document may not be reproduced in whole or part or made available without prior written consent of PwC.