ies webinar: energy outlook, q2 market intelligence update

TRANSCRIPT

Q2 2015 Energy Market Outlook

Energy Prices and Market Intelligence Q2 Update June 2, 2015

Presenter: Jonathan Lee, Sr Energy Market Intelligence Manager, Ecova

Wholesale natural gas prices are hovering near two and a half year lows as natural gas production soars.

− As the nation increases its reliance on natural gas-fired electric generation, wholesale gas prices will play an even bigger role in the direction of electric prices.

Fundamental Drivers – Bulls and Bears

• Summer Weather: El Niño impacting summer temperature forecasts. If forecasts hold, excessive natural gas cooling demand may be limited.

• Natural Gas Production, Storage: Production continues to operate near a record pace, which has helped drive the amount of gas in storage to a surplus compared to last year and the 5-year average. Another strong storage replenishment year could push supplies above 4,000 Bcf.

• Power Sector Demand: Natural gas expected to temporarily equal coal during parts of 2015.

• LNG Exports: Five LNG export facilities will be in various construction stages during Q2 2015.

Regional Electric Outlook:

– California: Persistent drought conditions have reduced hydro output and placed more reliance on natural gas and renewable generation.

– Midwest: Coal plant retirements hit their peak in 2015, which has impacted capacity pricing.

ENERGY MARKET INTELLIGENCE

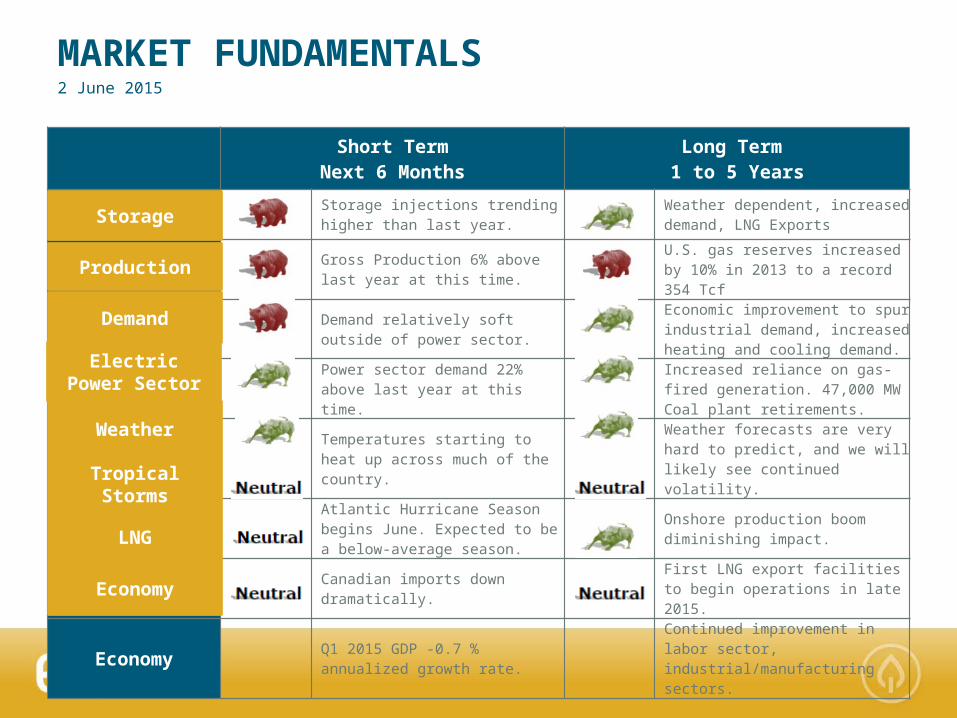

Short TermNext 6 Months

Long Term 1 to 5 Years

Storage Storage injections trending higher than last year.

Weather dependent, increased demand, LNG Exports

Production Gross Production 6% above last year at this time.

U.S. gas reserves increased by 10% in 2013 to a record 354 Tcf

Demand Demand relatively soft outside of power sector.

Economic improvement to spur industrial demand, increased heating and cooling demand.

Electric Power Sector

Power sector demand 22% above last year at this time.

Increased reliance on gas-fired generation. 47,000 MW Coal plant retirements.

Weather

Temperatures starting to heat up across much of the country.

Weather forecasts are very hard to predict, and we will likely see continued volatility.

Tropical Storms

Atlantic Hurricane Season begins June. Expected to be a below-average season.

Onshore production boom diminishing impact.

LNG

Canadian imports down dramatically.

First LNG export facilities to begin operations in late 2015.

Economy

Q1 2015 GDP -0.7 % annualized growth rate.

Continued improvement in labor sector, industrial/manufacturing sectors.

MARKET FUNDAMENTALS 2 June 2015

Storage

Production

Demand

Electric Power Sector

Weather

Tropical Storms

LNG

Economy

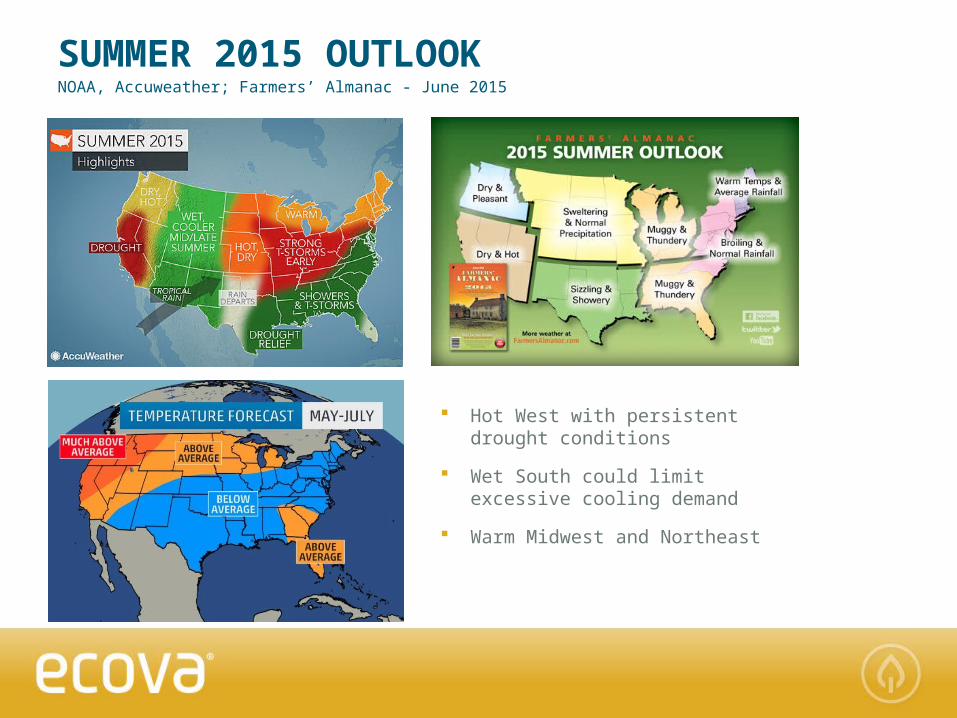

SUMMER 2015 OUTLOOKNOAA, Accuweather; Farmers’ Almanac - June 2015

Hot West with persistent drought conditions

Wet South could limit excessive cooling demand

Warm Midwest and Northeast

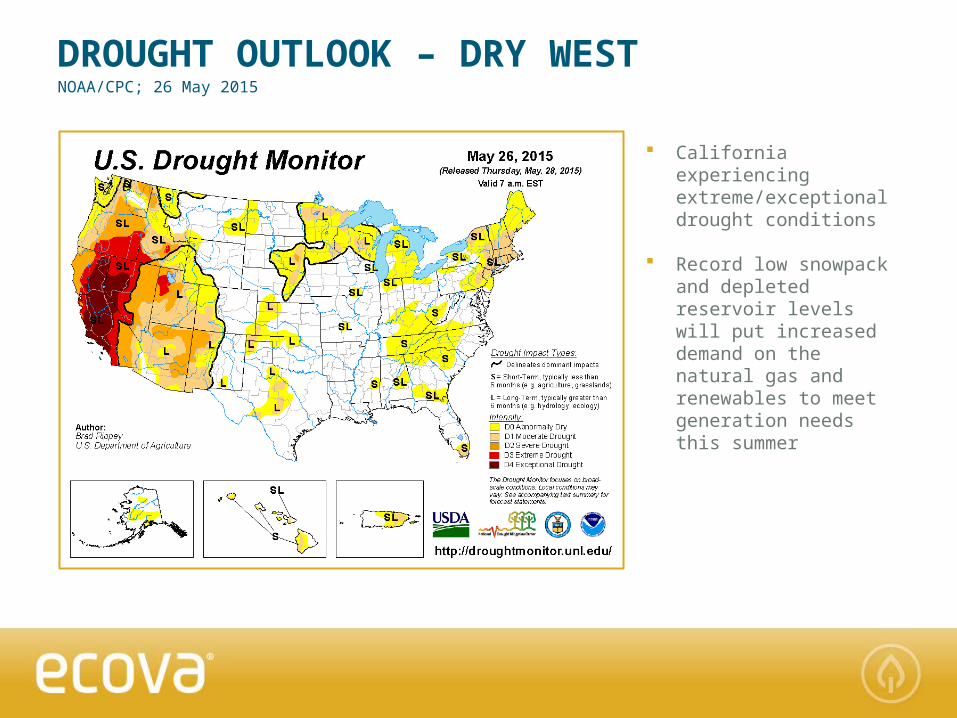

DROUGHT OUTLOOK – DRY WEST

California experiencing extreme/exceptional drought conditions

Record low snowpack and depleted reservoir levels will put increased demand on the natural gas and renewables to meet generation needs this summer

NOAA/CPC; 26 May 2015

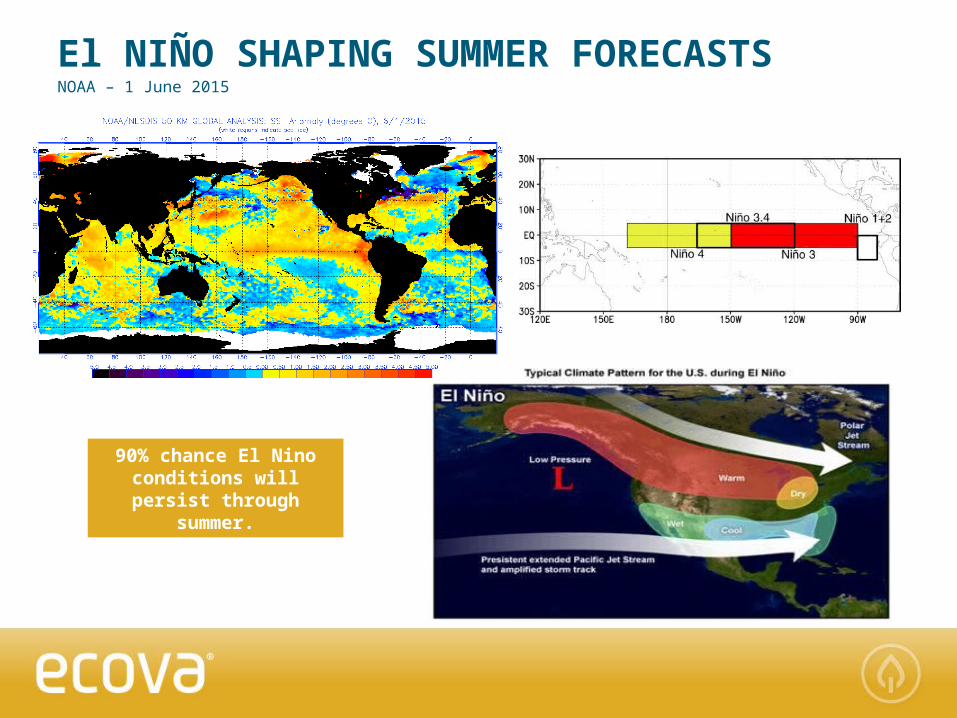

El NIÑO SHAPING SUMMER FORECASTSNOAA – 1 June 2015

90% chance El Nino conditions will persist

through summer.

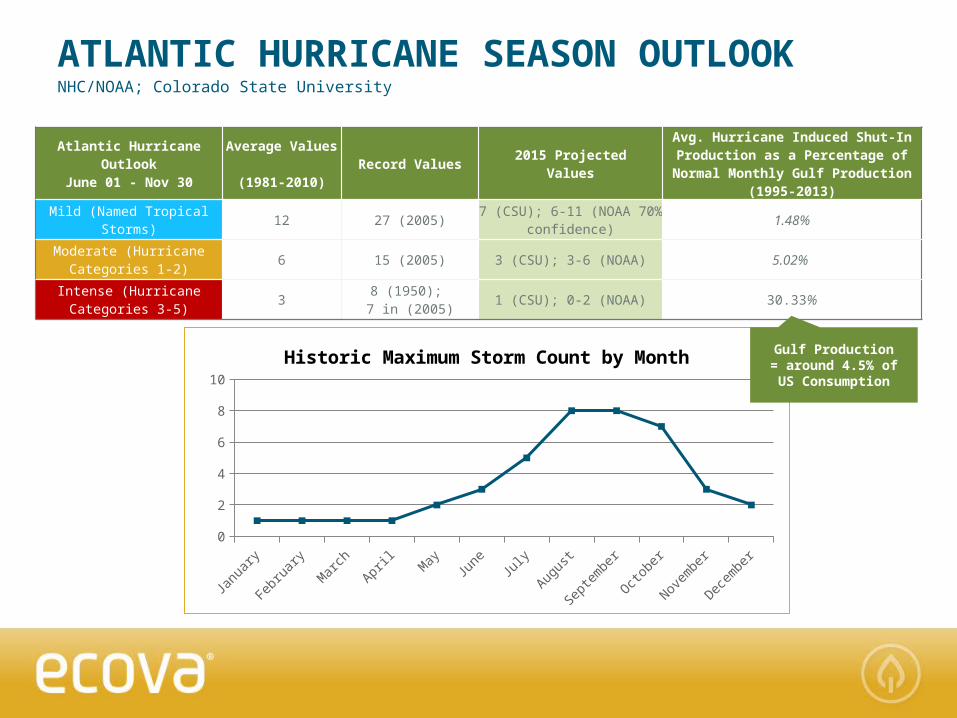

ATLANTIC HURRICANE SEASON OUTLOOKNHC/NOAA; Colorado State University

Atlantic Hurricane Outlook

June 01 - Nov 30

Average Values

(1981-2010)Record Values

2015 Projected Values

Avg. Hurricane Induced Shut-In Production as a Percentage of

Normal Monthly Gulf Production (1995-2013)

Mild (Named Tropical Storms)

12 27 (2005) 7 (CSU); 6-11 (NOAA 70% confidence)

1.48%

Moderate (Hurricane Categories 1-2)

6 15 (2005) 3 (CSU); 3-6 (NOAA) 5.02%

Intense (Hurricane Categories 3-5)

3 8 (1950); 7 in (2005)

1 (CSU); 0-2 (NOAA) 30.33%

Janu

ary

Febru

ary

Mar

chApr

ilM

ayJu

ne July

Augus

t

Septe

mbe

r

Octob

er

Novem

ber

Decem

ber

0123456789

Historic Maximum Storm Count by Month Gulf Production = around 4.5% of US Consumption

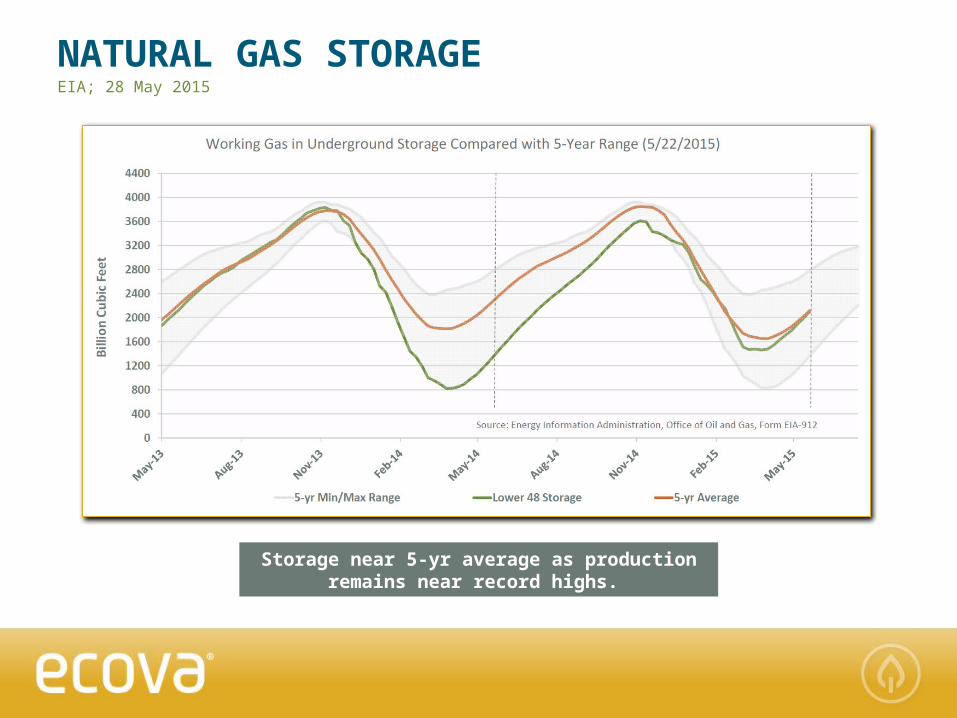

NATURAL GAS STORAGEEIA; 28 May 2015

Storage near 5-yr average as production remains near record highs.

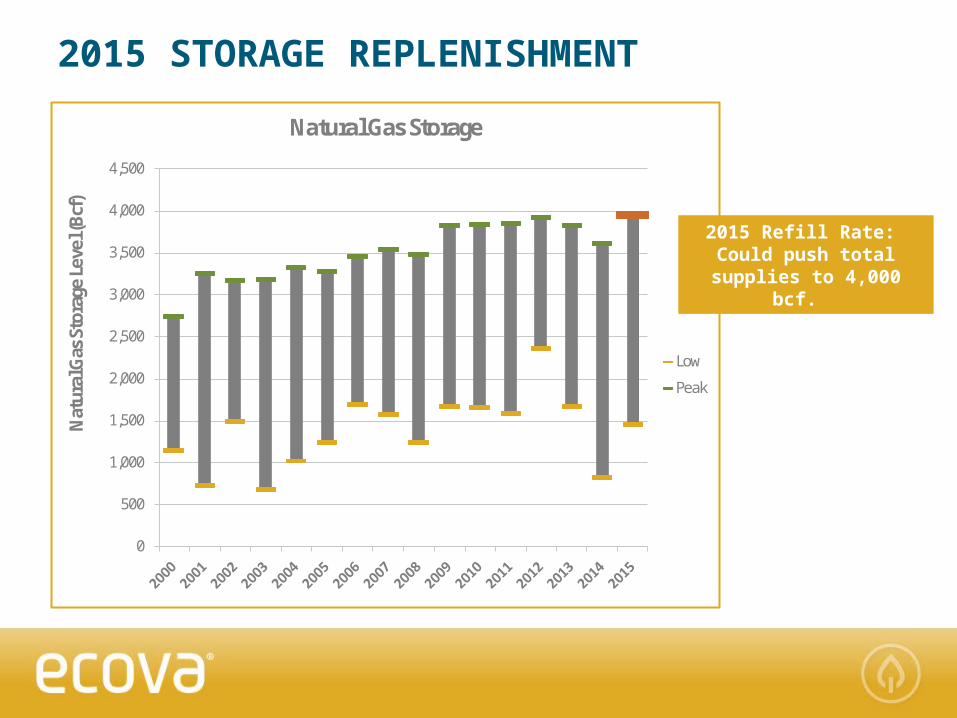

2015 STORAGE REPLENISHMENT

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

Nat

ural

Gas

Sto

rage

Leve

l (Bc

f)

Natural Gas Storage

Low

Peak

2015 Refill Rate: Could push total

supplies to 4,000 bcf.

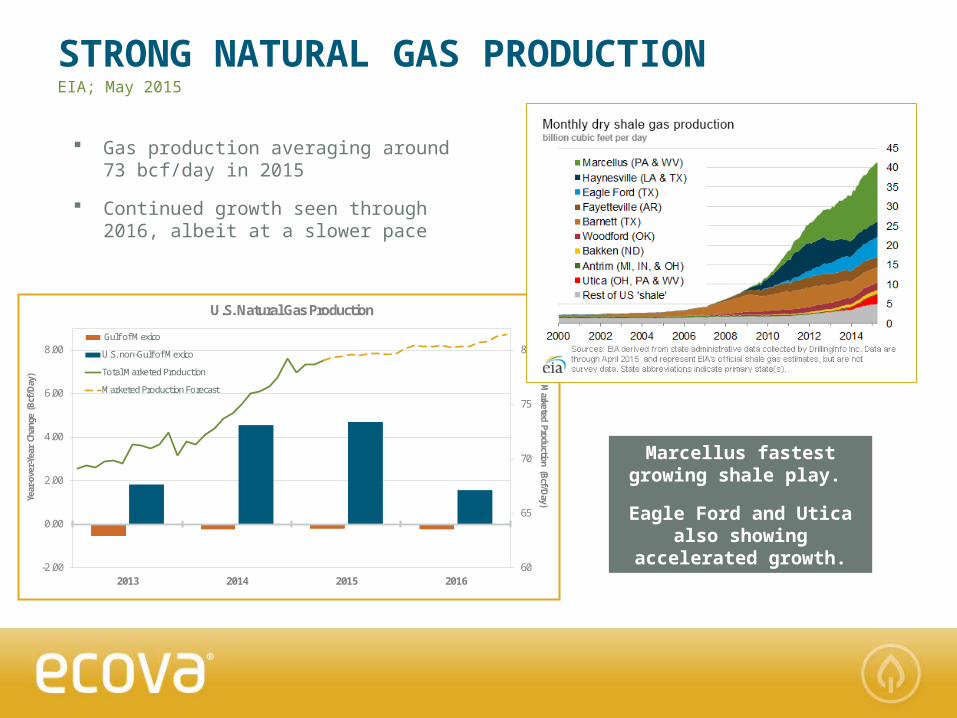

STRONG NATURAL GAS PRODUCTIONEIA; May 2015

60

65

70

75

80

-2.00

0.00

2.00

4.00

6.00

8.00

2013 2014 2015 2016

Marketed Production (Bcf/D

ay)Year

-ove

r-Ye

ar C

hang

e (B

cf/D

ay)

U.S. Natural Gas Production

Gulf of Mexico

U.S. non-Gulf of Mexico

Total Marketed Production

Marketed Production Forecast

Gas production averaging around 73 bcf/day in 2015

Continued growth seen through 2016, albeit at a slower pace

Marcellus fastest growing shale play.

Eagle Ford and Utica also showing

accelerated growth.

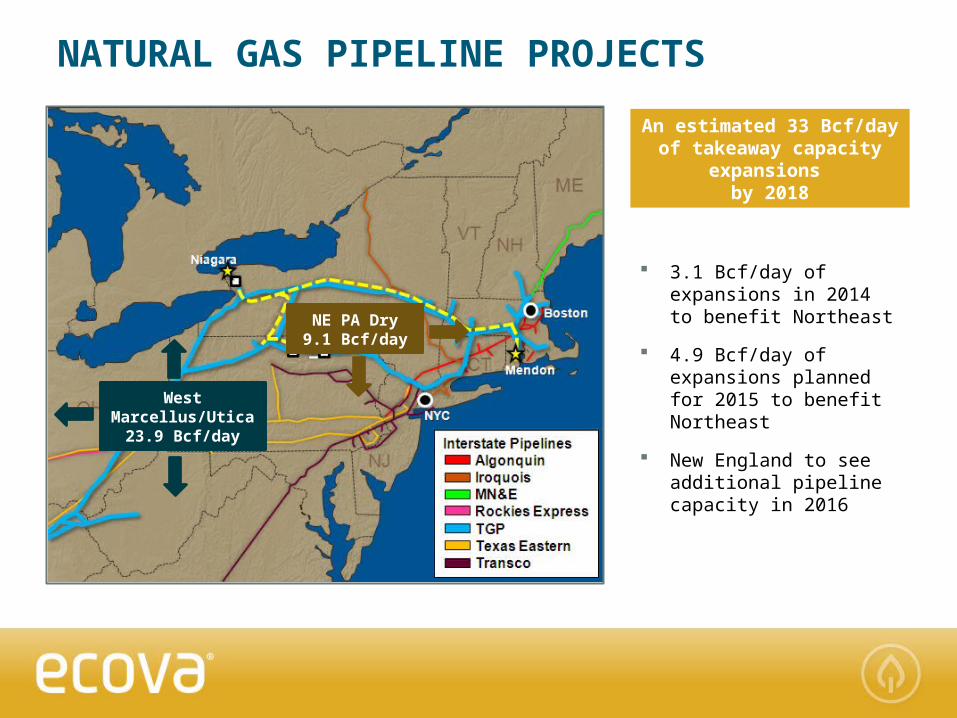

NATURAL GAS PIPELINE PROJECTS

NE PA Dry9.1 Bcf/day

West Marcellus/Utica

23.9 Bcf/day

An estimated 33 Bcf/day of takeaway capacity

expansions by 2018

3.1 Bcf/day of expansions in 2014 to benefit Northeast

4.9 Bcf/day of expansions planned for 2015 to benefit Northeast

New England to see additional pipeline capacity in 2016

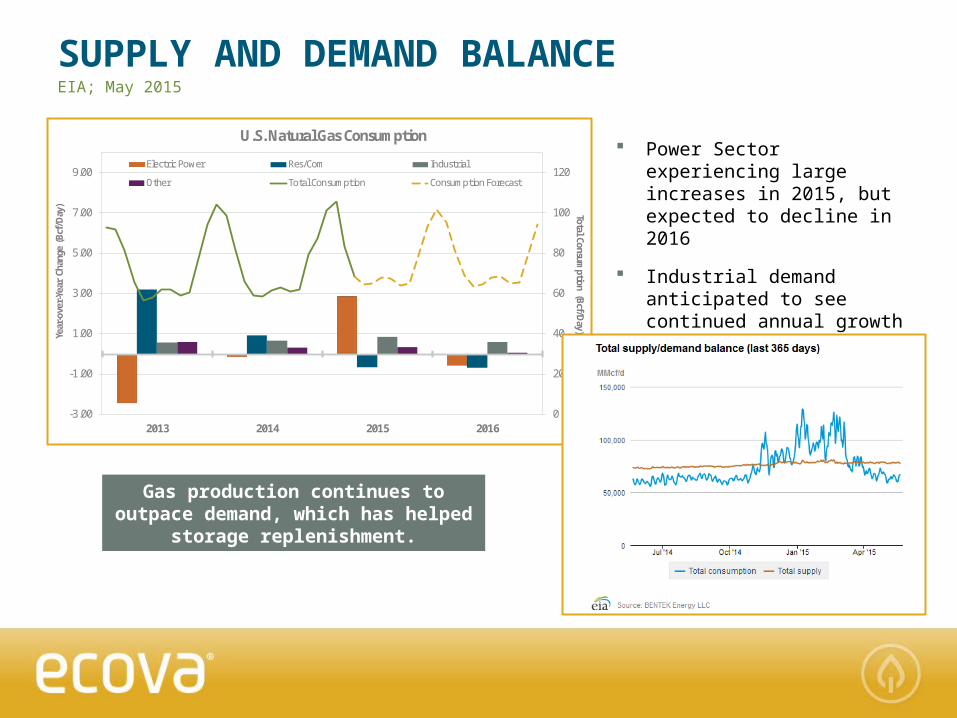

SUPPLY AND DEMAND BALANCE

Gas production continues to outpace demand, which has

helped storage replenishment.

Power Sector experiencing large increases in 2015, but expected to decline in 2016

Industrial demand anticipated to see continued annual growth

EIA; May 2015

0

20

40

60

80

100

120

-3.00

-1.00

1.00

3.00

5.00

7.00

9.00

2013 2014 2015 2016

Total Consumption (Bcf/D

ay)

Year

-ove

r-Ye

ar C

hang

e (B

cf/D

ay)

U.S. Natural Gas Consumption

Electric Power Res/Com Industrial

Other Total Consumption Consumption Forecast

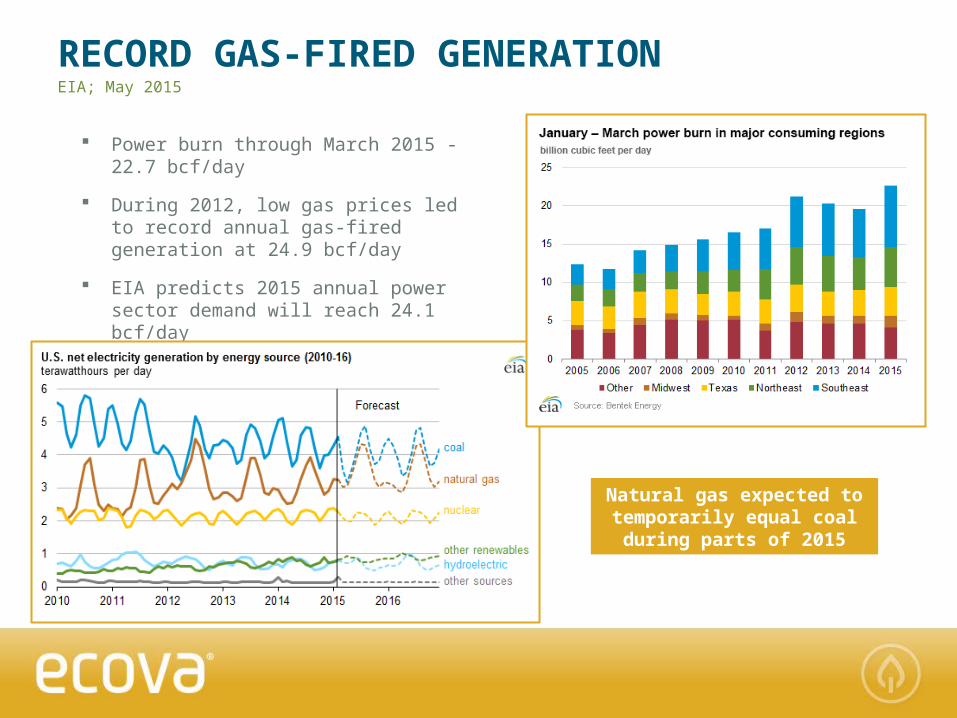

RECORD GAS-FIRED GENERATIONEIA; May 2015

Power burn through March 2015 - 22.7 bcf/day

During 2012, low gas prices led to record annual gas-fired generation at 24.9 bcf/day

EIA predicts 2015 annual power sector demand will reach 24.1 bcf/day

Natural gas expected to temporarily equal coal during parts of 2015

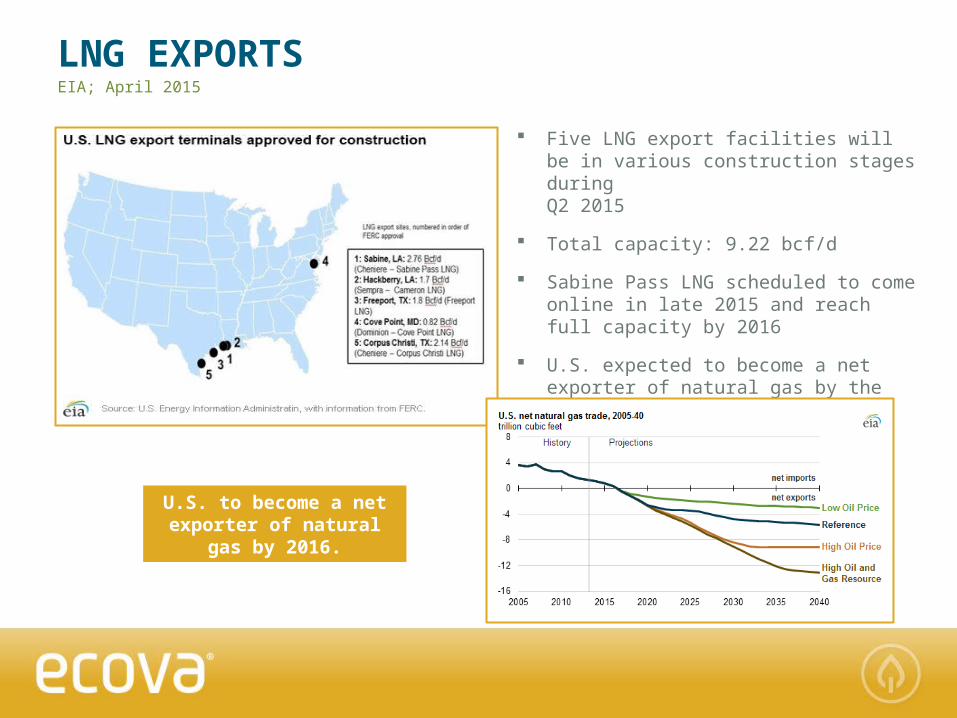

LNG EXPORTSEIA; April 2015

Five LNG export facilities will be in various construction stages during Q2 2015

Total capacity: 9.22 bcf/d

Sabine Pass LNG scheduled to come online in late 2015 and reach full capacity by 2016

U.S. expected to become a net exporter of natural gas by the end of 2016

U.S. to become a net exporter of natural

gas by 2016.

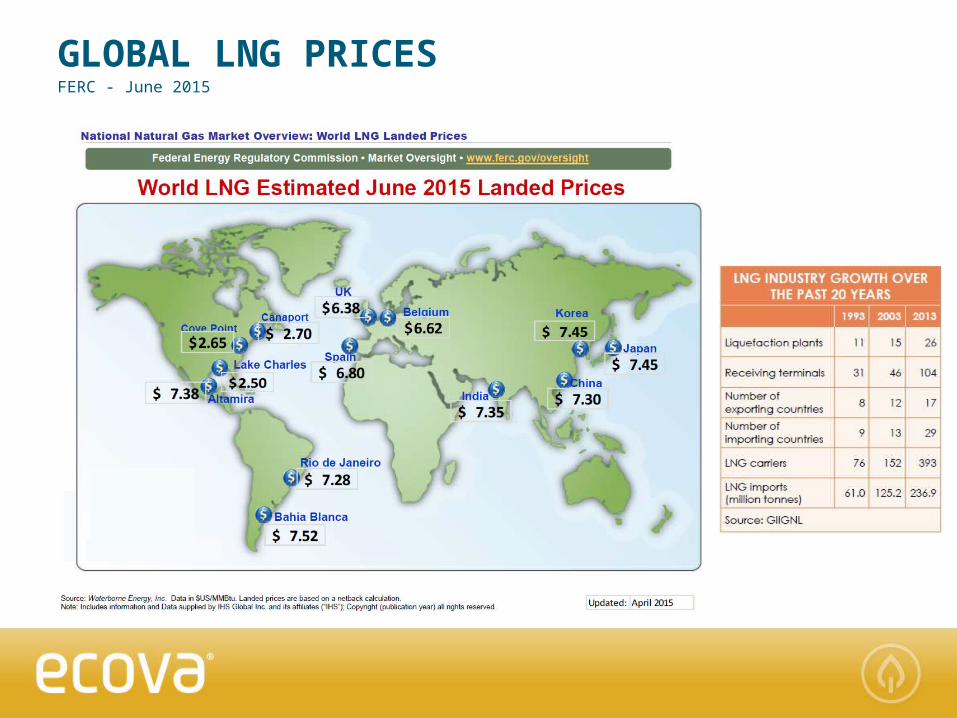

GLOBAL LNG PRICESFERC - June 2015

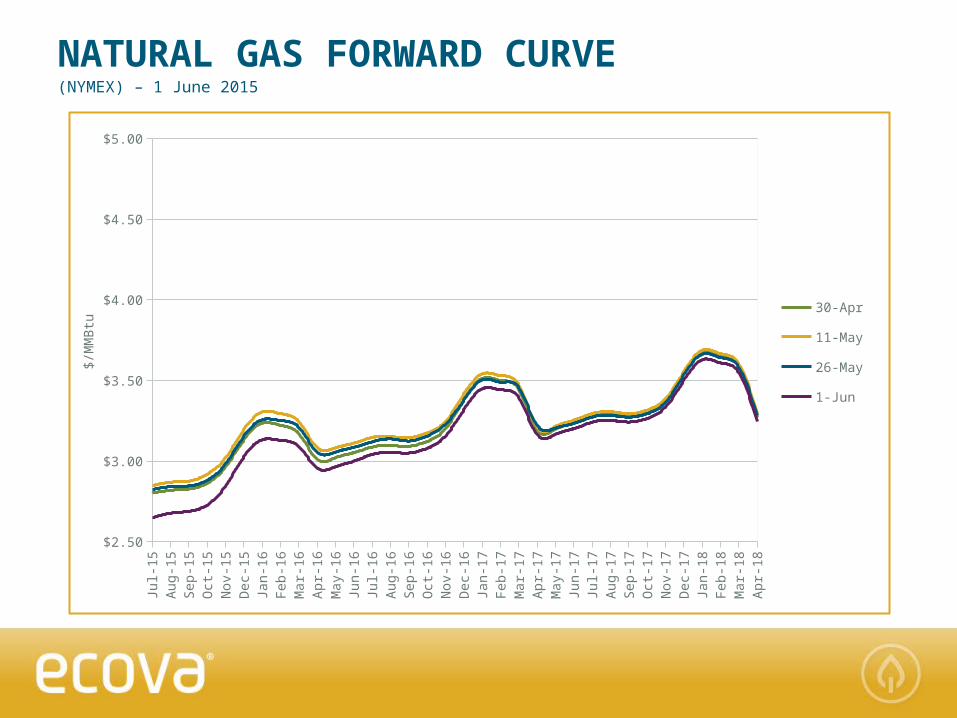

NATURAL GAS FORWARD CURVE(NYMEX) – 1 June 2015

Natural Gas Curve Remains Near Lowest

Level Since 2012

Jul-

15

Aug-1

5Sep-1

5O

ct-1

5N

ov-1

5D

ec-

15

Jan-1

6Fe

b-1

6M

ar-

16

Apr-

16

May-1

6Ju

n-1

6Ju

l-16

Aug-1

6Sep-1

6O

ct-1

6N

ov-1

6D

ec-

16

Jan-1

7Fe

b-1

7M

ar-

17

Apr-

17

May-1

7Ju

n-1

7Ju

l-17

Aug-1

7Sep-1

7O

ct-1

7N

ov-1

7D

ec-

17

Jan-1

8Fe

b-1

8M

ar-

18

Apr-

18

$2.50

$3.00

$3.50

$4.00

$4.50

$5.00

30-Apr

11-May

26-May

1-Jun

$/M

MB

tu

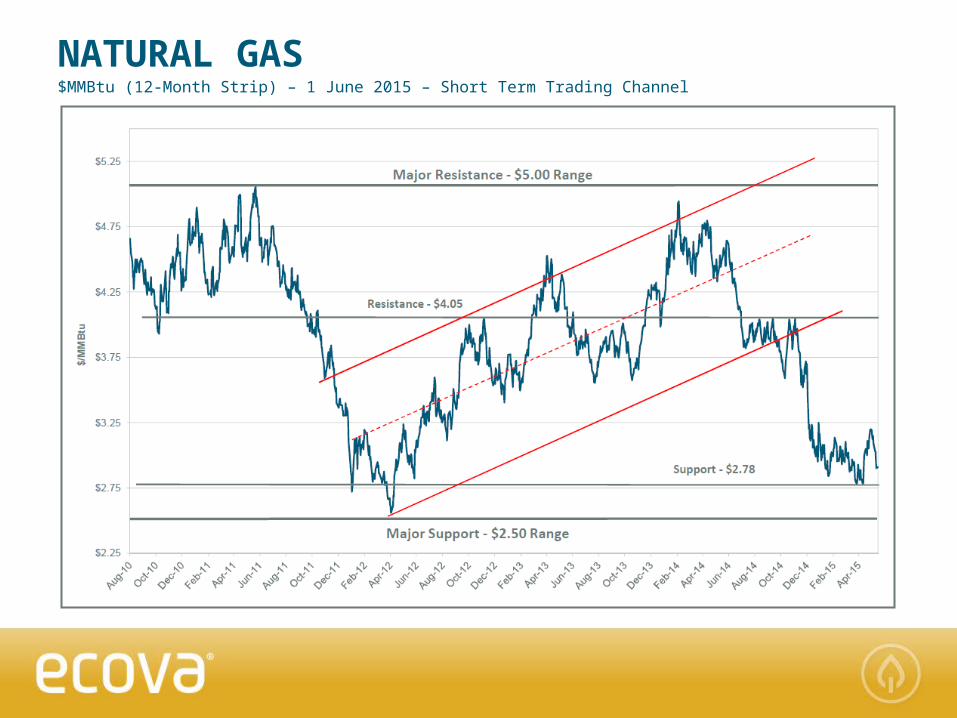

NATURAL GAS$MMBtu (12-Month Strip) – 1 June 2015 – Short Term Trading Channel

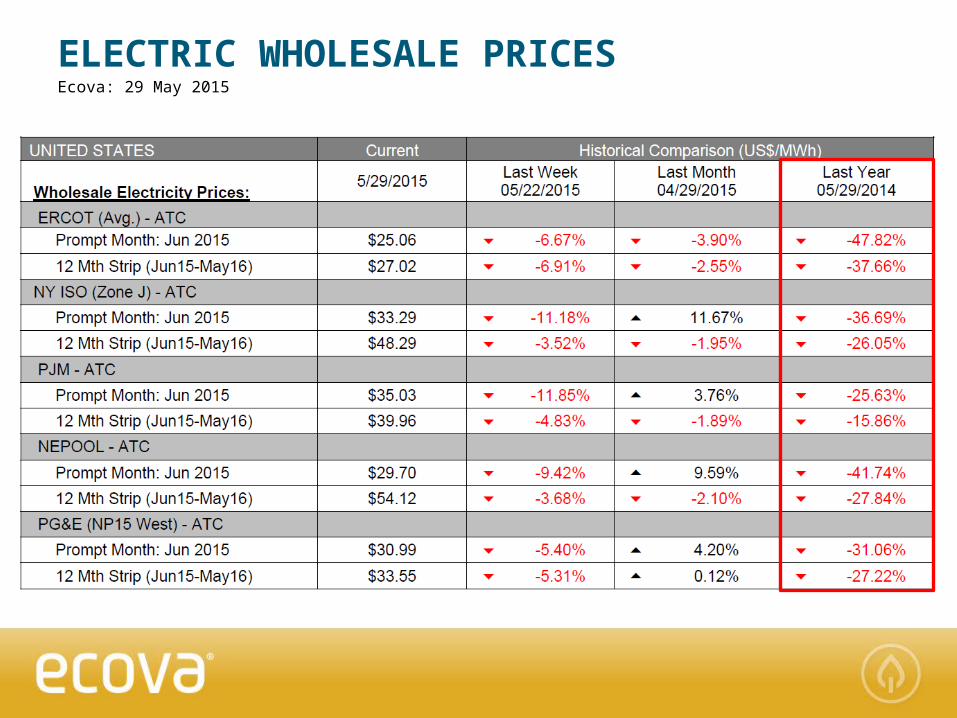

ELECTRIC WHOLESALE PRICESEcova: 29 May 2015

Jan-

12

Apr-1

2

Jul-1

2

Oct-1

2

Jan-

13

Apr-1

3

Jul-1

3

Oct-1

3

Jan-

14

Apr-1

4

Jul-1

4

Oct-1

4

Jan-

15

Apr-1

5$25

$35

$45

$55

$65

$75

$85

$95 ERCOT AVG NY ISO J PJM NEPOOL PG&E NP15 W

Pri

ce p

er

MW

h

WHOLESALE ELECTRICITY$MWh (12-Month Strip) – 29 May 2015

CA and ERCOT lowest level since 2012

NYISO, NEPOOL, and PJM lower, but winter reliability risks still priced in

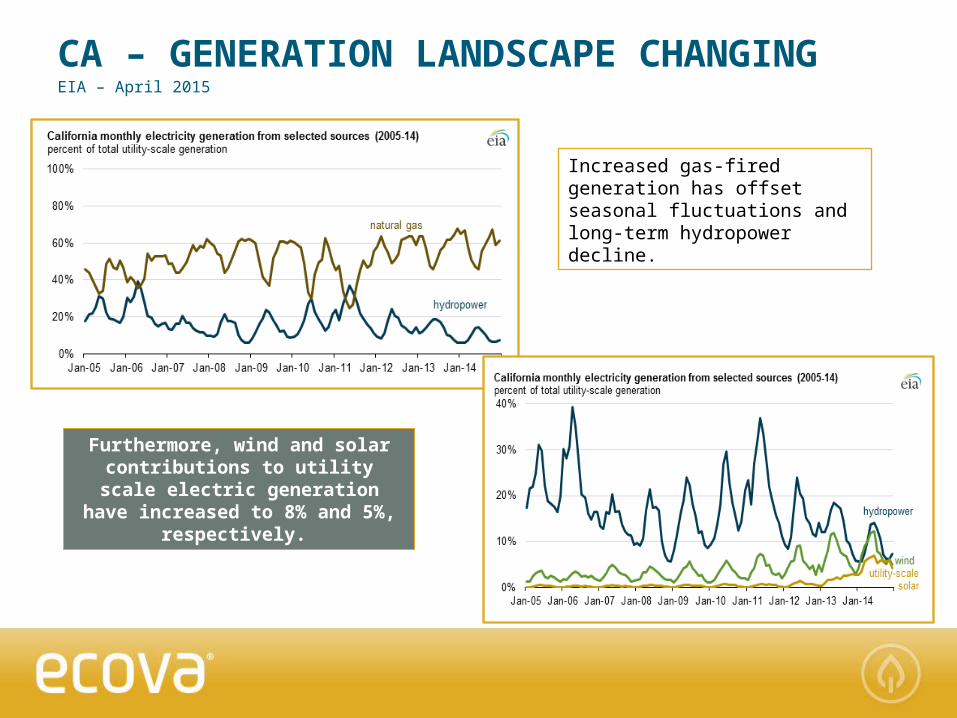

CA – GENERATION LANDSCAPE CHANGINGEIA – April 2015

Increased gas-fired generation has offset seasonal fluctuations and long-term hydropower decline.

Furthermore, wind and solar contributions to utility scale

electric generation have increased to 8% and 5%,

respectively.

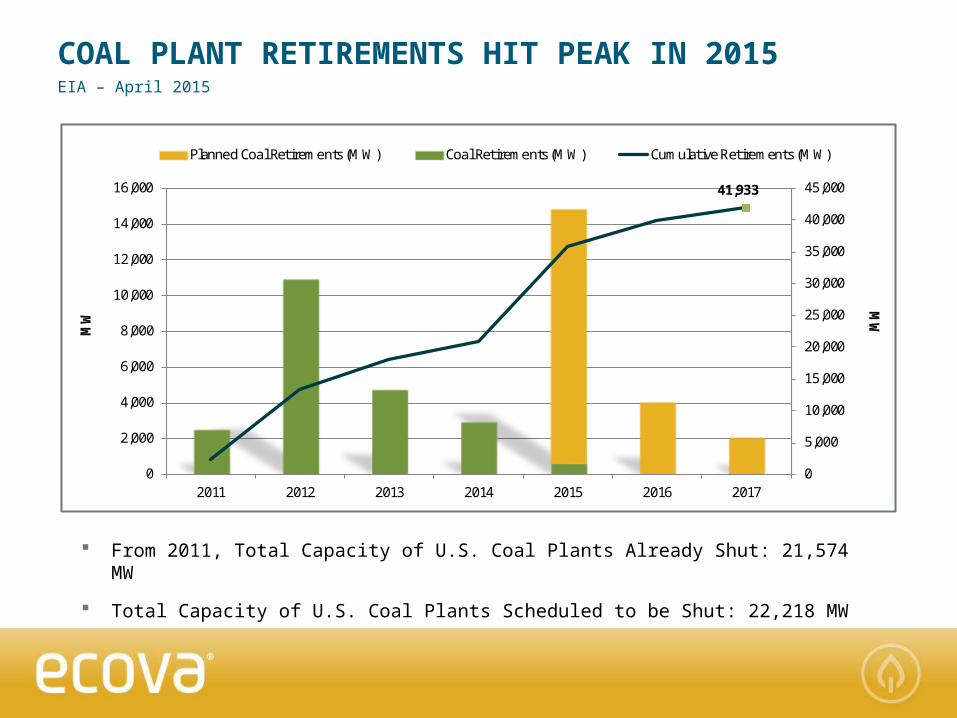

COAL PLANT RETIREMENTS HIT PEAK IN 2015EIA – April 2015

From 2011, Total Capacity of U.S. Coal Plants Already Shut: 21,574 MW

Total Capacity of U.S. Coal Plants Scheduled to be Shut: 22,218 MW

41,933

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

2011 2012 2013 2014 2015 2016 2017

MW

MW

Planned Coal Retirements (MW) Coal Retirements (MW) Cumulative Retirements (MW)

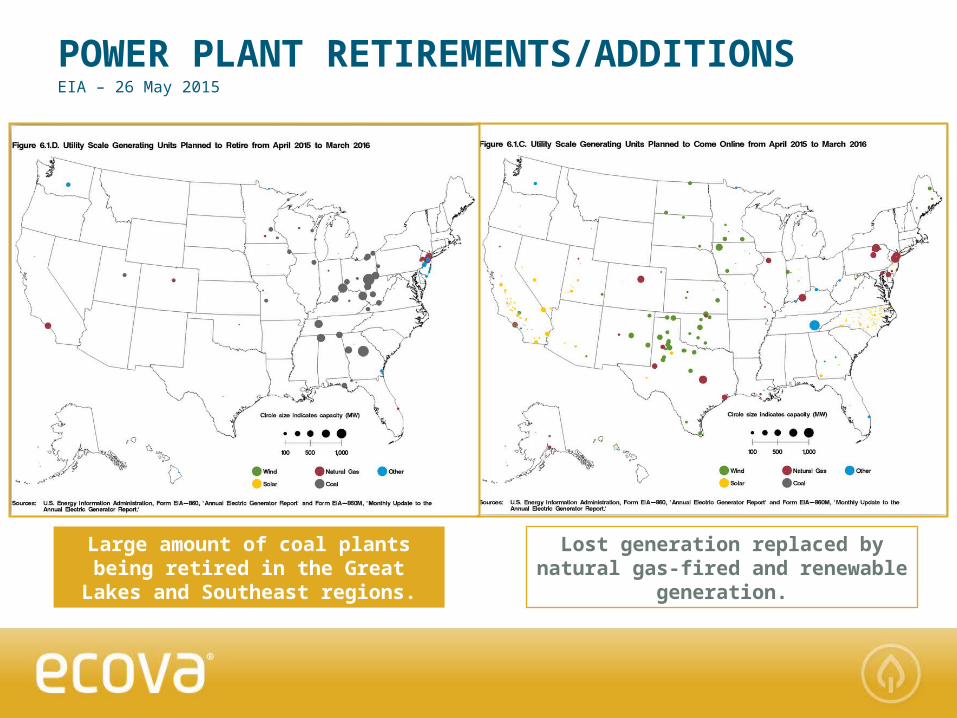

POWER PLANT RETIREMENTS/ADDITIONSEIA – 26 May 2015

Large amount of coal plants being retired in the Great Lakes

and Southeast regions.

Lost generation replaced by natural gas-fired and renewable

generation.

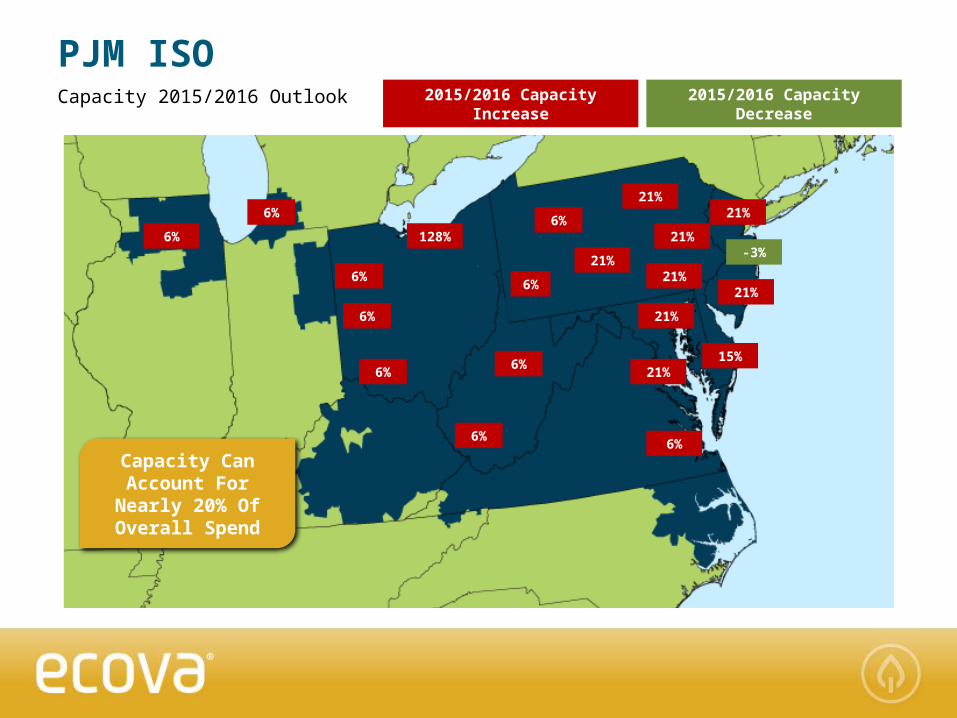

PJM ISO

6%

2015/2016 Capacity Increase

2015/2016 Capacity Decrease

6%6%

128%

6%

6%

6%

6%

6%

6%

21%

21%

6%

21%

21%

21%21%

21%

15%21%

-3%

Capacity Can Account For

Nearly 20% Of Overall Spend

Capacity 2015/2016 Outlook

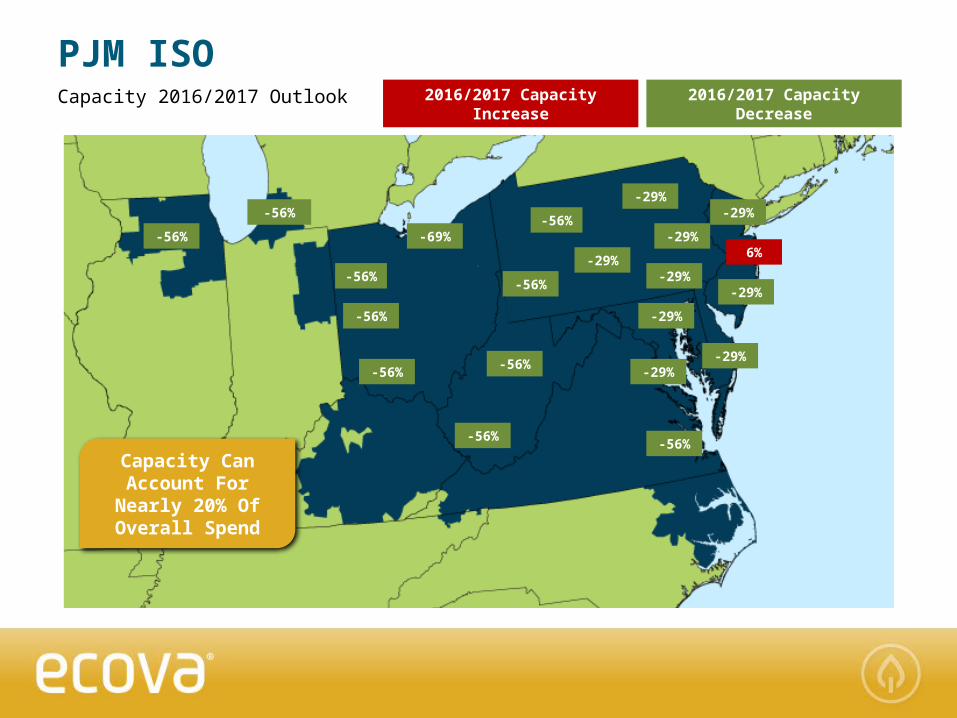

Capacity 2016/2017 Outlook

-56%

2016/2017 Capacity Increase

2016/2017 Capacity Decrease

-56%

-56%-

69%

-56%

-56%

-56%

-56%

-56%

-56%

-29%

-29%

-56%

-29%

-29%

-29%

-29%

-29%

-29%-

29%

6%

Capacity Can Account For

Nearly 20% Of Overall Spend

PJM ISO

MISO CAPACITY2015/2016 Auction Clearing Price Overview - April 2015

Ameren Illinois will experience a significant increase in capacity rates in 15/16

Potential impact to pricing between $7.00 - $9.00/MWh

Jump largely due to the retirement of coal-plants in the region

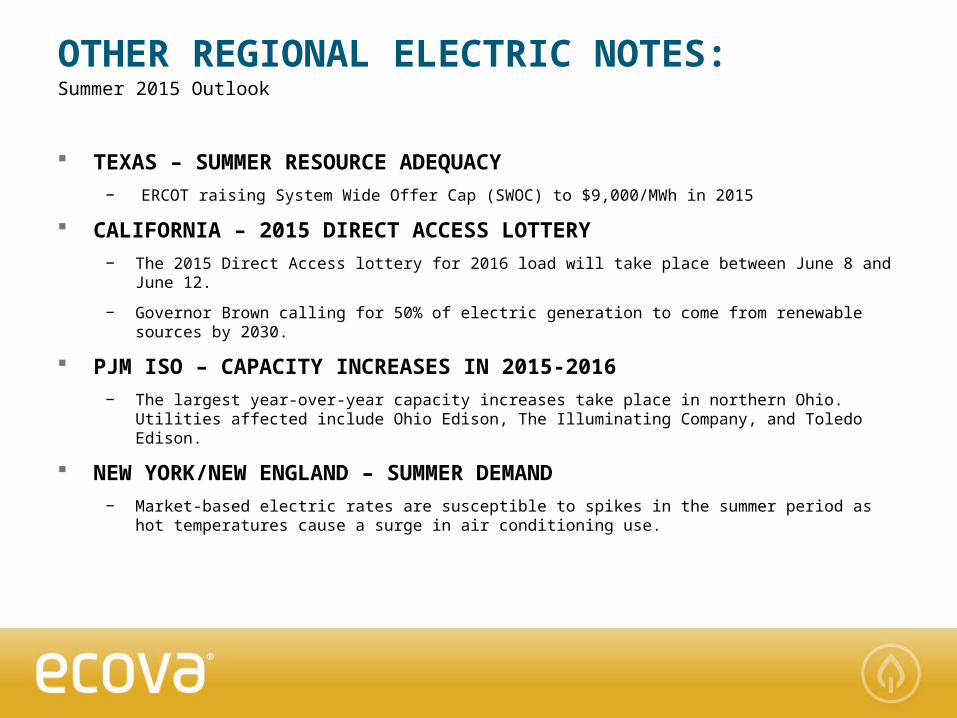

OTHER REGIONAL ELECTRIC NOTES:Summer 2015 Outlook

TEXAS – SUMMER RESOURCE ADEQUACY− ERCOT raising System Wide Offer Cap (SWOC) to $9,000/MWh in 2015

CALIFORNIA – 2015 DIRECT ACCESS LOTTERY− The 2015 Direct Access lottery for 2016 load will take place between June 8 and June 12.

− Governor Brown calling for 50% of electric generation to come from renewable sources by 2030.

PJM ISO – CAPACITY INCREASES IN 2015-2016− The largest year-over-year capacity increases take place in northern Ohio. Utilities affected

include Ohio Edison, The Illuminating Company, and Toledo Edison.

NEW YORK/NEW ENGLAND – SUMMER DEMAND− Market-based electric rates are susceptible to spikes in the summer period as hot

temperatures cause a surge in air conditioning use.

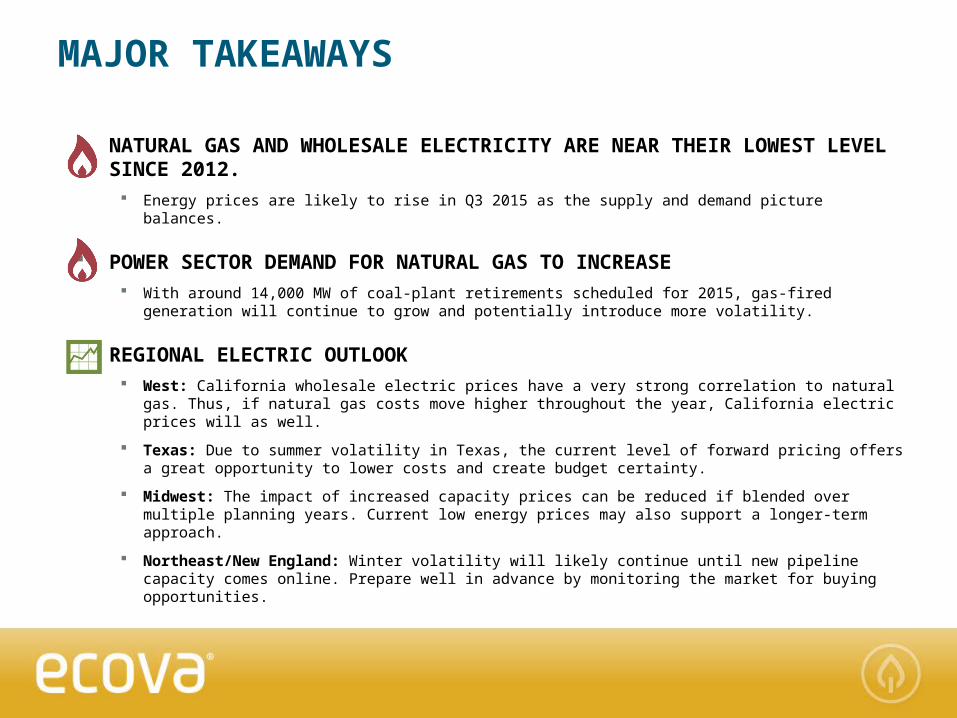

NATURAL GAS AND WHOLESALE ELECTRICITY ARE NEAR THEIR LOWEST LEVEL SINCE 2012.

Energy prices are likely to rise in Q3 2015 as the supply and demand picture balances.

POWER SECTOR DEMAND FOR NATURAL GAS TO INCREASE With around 14,000 MW of coal-plant retirements scheduled for 2015, gas-fired generation will

continue to grow and potentially introduce more volatility.

REGIONAL ELECTRIC OUTLOOK West: California wholesale electric prices have a very strong correlation to natural gas. Thus,

if natural gas costs move higher throughout the year, California electric prices will as well.

Texas: Due to summer volatility in Texas, the current level of forward pricing offers a great opportunity to lower costs and create budget certainty.

Midwest: The impact of increased capacity prices can be reduced if blended over multiple planning years. Current low energy prices may also support a longer-term approach.

Northeast/New England: Winter volatility will likely continue until new pipeline capacity comes online. Prepare well in advance by monitoring the market for buying opportunities.

MAJOR TAKEAWAYS

INSIDE ENERGY & SUSTAINABILITY WEBINARS

Tap into Water Saving Opportunities – June 25th at 11a PST

Questions, comments, suggestions? [email protected]

ENERGY PRICE HUB

Ecova’s all-in-one resource page for market intelligence and timely energy insights http://www.ecova.com/news-media/energy-price-hub.aspx

RELATED RESOURCES

Q&A

Thank you!