icici jan 17 issue sachincontent.icicidirect.com/moneymanagermagazine/january_2018.pdf · repairs...

TRANSCRIPT

72

Shilpa KumarMD & CEO

ICICI Securities Ltd.

At the onset, let me start by wishing

you a Very Happy New Year!

2017 was an eventful year on many

fronts. The year began with

a d j u s t m e n t s r e l a t e d t o

demonetization and ended with

s imi la r e f fo r ts to accus tom

ourselves with the Goods and

Service Tax. Both events are an

important economic landmark. We

look a t 2018 w i th renewed

optimism. We believe it to be the

year of stabilization as various steps

taken by the government may start

bearing fruit in CY18. With potential

government policies in place,

private sector's balance sheet

repairs and mending of banking

sector, private sector investments can accelerate in the year ahead. All

these factors are likely to resurrect India's GDP growth.

Indian nominal GDP growth seems to have bottomed out and is poised

for long term structural growth on account of enduring reforms such as

demonetization, GST, Insolvency and Bankruptcy code (IBC), etc.

Although adjustments to reforms have taken a toll on the nominal GDP

(9.3% in H1FY18) in the short-term, realization of long term advantages

will start mainly from FY19.

GST collections thus far are below our estimate. Lower than expected

GST collections (and thus, lower indirect taxes) would be an overhang

on fiscal deficit financing. GST collections would need to match

comparable indirect tax revenues to ensure zero revenue loss under the

new system. However, complete clarity is yet to emerge on the

implication of initial GST collection from official sources. A possible

ICICIdirect Money Manager January 20181

encouraging aspect to future collections is the implementation of

interstate e-way bill system on goods valued above Rs. 50000 with

effect from February 1, 2018. E-way bill implementation in states under

the previous system (pre-GST) had helped boost tax revenues by

15-20%.

We expect RBI to maintain status quo on benchmark rates for most of

year 2018, though we believe there is still scope of lower lending rates in

the banking system. Lower credit cost in terms of lower provisioning,

re-pricing of deposits at lower rates and structural reforms like lower

cash to GDP ratio, increased digital transactions, increase in merchant

discount rate (MDR) rates expected to cut losses, benchmarking of

lending rates to marginal cost lending rate (MCLR) is likely to provide

scope for further rate transmission.

Government's “Housing for All by 2022” scheme is expected to be a key

catalyst in economic recovery. We believe Housing for All scheme will

revive the economy with 250+ sectors forward and backward linkages.

Beside this, it would result in huge employment generation.

For CY18, we expect that the key driving force for the market would be

earnings recovery, which would be backed by a rise in asset turn

thereby improving the RoCE profile. We remain positive on Equity.

However for personal investments, it is important to follow a strict asset

allocation strategy that is backed by your goals and investment

objectives. It is important that you allocate your capital into both equity

(for growth) and debt (to provide stability). The start of the year is an

opportune time to work on your financial plan and an asset allocation

strategy.

Our message remains the same - 'Keep investing and stay invested for

your l i fe goals. ' Through this magazine and our website

www.icicidirect.com we want to make an earnest attempt to partner

with you in setting and achieving your financial goals. Give us an

opportunity to serve you, walk into any of your Neighborhood Financial

Superstore and talk to us.

As we head into 2018, one of the foremost questions that we would like answered is how will the markets perform and the trend going forward. Will it have the same robustness as last year or get better or are there some surprises in store.

In our New Year edition of ICICIdirect Money Manager, we put together a detail account of investment outlook 2018. Some of the leading experts in the industry put forth their views on last year's financial review, expectations from different asset classes in the upcoming year, key risks in the market today on micro and macro level. All in all, through this edition, we try to answer one common question, “How should you position your investment portfolio for the year 2018?”

While it is important to know the market expectations, the information needs to be used in tandem with our own financial goals and investment objectives. These investment objectives should in turn define the asset allocation. An asset allocation strategy defines how much one need to invest in diverse assets like equity, debt, gold etc. It is a great time to start or review your financial plan and define an appropriate asset allocation strategy.

With a fresh year ahead, set clear, concise financial goals and make a plan to put finances into shape. Give yourself adequate time to list down your priorities. Make investments that fit your risk appetite and that are linked to your goals.

In order to give you more in-depth take on the markets, we bring to you the fundamental, technical and derivatives market outlook 2018 from our internal team of research experts. Our research team also presents the performance review of different categories of mutual funds, along with the outlook for near future. So read on, stay updated and tuned. Do write us your feedback at [email protected] and share your thoughts.

Team ICICIdirect Money Manager wishes you a happy New Year.

Your magazine is now also available on www.magzter.com, a digital newsstand.

ICICIdirect Money Manager January 2018

Editor & Publisher : Abhishake Mathur, CFA

Editorial Board : Sameer Chavan, CWM®, Pankaj Pandey

CMEditorial Team : Nithyakumar VP CFP , Sachin Jain, Research Team

Coordinating Editor : Namrata Lonkar

2

ICICIdirect Money Manager January 2018

MD Desk ...................................................................................................1

Editorial ....................................................................................................2

Contents ...................................................................................................3

News ........................................................................................................4

Stock ideas: Greenply Industries & Gujarat Gas .....................................5

Fundamental Outlook 2018 ........................................................................13

Technical Outlook 2018 .............................................................................24

Derivatives strategy for 2018 .....................................................................30

Flavour of the Month 2017 was an eventful year on many fronts. As we step into a new fiscal,three experts from the industry share their viewpoints on CY17 and expectations from CY18................................................................34

Ask Our PlannerOur financial planner answers personal finance queries to help you build a substantial portfolio more easily...............................................47

Mutual Fund Analysis It's time to remain constructive in balanced funds and maintain stability in the portfolio. Check these top three funds recommended by our research team............................................................................50

This month on iCommunityTake a look at the latest activities on our unique information platform- iCommunity (for January 2018)............................................................59

Equity Model Portfolio................................................................................60

Quiz Time .................................................................................................64

Prime Numbers ........................................................................................65

3

India's oil consumption in 2017 expanded at the slowest pace in four years as a surprise ban on high-value currency notes and a new national sales tax weakened the economy. The nation's consumption of petroleum products rose 2 percent to about 200 million tons, the Oil Ministry's Petroleum Planning and Analysis Cell said Wednesday. That's the slowest since 2013, when demand grew 1.7 percent while global oil prices averaged about $109 a barrel, almost double last year's level. The cash ban and the new tax hit truckers the hardest, affecting demand for diesel as they are the largest consumers of the fuel in India.

Courtesy: Financial Express

India's oil consumption hits a rough patch, demand growth weakest since 2013 as economy slows

'India largest market for freelancers'

India is the largest freelancer market with 10 million people freelancing, according to PayPal.Freelancers in India, on an average, earn about Rs. 19 lakh per year, according to a new survey by global digital payments giant PayPal.“Of the surveyed freelancers, 41% have witnessed very fast growth in through the past 12 months, with 80% of them working with international as well as domestic clients,” the report said.The survey, conducted with 500 Indian freelancers, found that they were below the age of 40 and predominantly men.

Courtesy: The Hindu

ICICIdirect Money Manager January 2018

The December quarter performance of Tata Consultancy Servicec was without surprises or shocks. But investors may feel relieved given the possibility that the country's largest software exporter may show better revenue growth in dollar terms for the current fiscal compared with the previous two.

In addition, a stronger momentum in the digital segment is a bright spot amid subdued trend in banking, financial services and insurance (BFSI) verticals, which contributed over one-third to the total revenue. While the momentum in revenue seems to be reviving, the company is yet to restore the operating margin (EBIT margin) back to its target range of 26-28 per cent.

Courtesy: Economic Times

TCS topline shows signs of revival

Budget bonanza: Govt likely to do away with dividend distribution tax

The finance ministry is likely to do away with the dividend distribution tax (DDT) in the upcoming Union Budget. At present, if a company gives dividend to its shareholders, it has to pay DDT of 20.36 per cent (15 per cent plus surcharge and cess)."It is expected that Budget 2018 may propose a withdrawal of DDT and return to the classic system of dividend taxation, that is, dividend income to be taxed at the hands of the recipient shareholders," said SonuIyer, partner and leader, India region people advisory services, EY.

Courtesy: Business Standard

4

STOCK IDEAS

ICICIdirect Money Manager January 2018

Greenply Industries – MDF division to drive future growth…

Company Background

Incorporated in 1984, Greenply Industries (GIL) is a leading p layer in the o rgan ised plywood and medium density fibreboard (MDF) market. The company has a strong pan-India presence and has a d i s t r ibu to r and s tock i s t strength of 1656 and 841 in the plywood and MDF segments, respectively. This strong brand presence helps it to increase its market penetration in this highly fragmented wood panel industry. In 2014, the company de-merged its decorative b u s i n e s s c o m p r i s i n g laminates and allied products into Greenlam Industries, mainly to focus on its plywood and MDF business.

Over the past two decades, GIL has g rown s ign i f i can t l y resulting in 26% market share in the organised plywood market and 30% market share in the domestic MDF industry. Furthermore, the company's strong brand presence and a well entrenched distribution network have helped GIL to evolve with changing times and cater to rising customer

expectations. Moreover, to support its growth, GIL has b u i l t f o u r p l y w o o d manufacturing facilities across the country with total capacity of 32.4 MSM (million square metre) and an MDF facility with capacity of 1,80,000 CBM. With MDF demand on the rise, the company is undertaking a greenfield expansion to build an MDF facility in Andhra Pradesh w i th an annua l capacity of 3,60,000 CBM. Also, i t is expanding i ts plywood capacity by 40% to 46 MSM.

Investment Rationale

MDF facil ity expected to be commissioned by July, 2018…

GIL is setting up a new MDF facility in Andhra Pradesh with a capacity of 360,000 CBM entailing a capex of | 750 crore (already spent | 530 crore till Q2FY18). Construction is in full swing while the management is aiming to commission the plant three months ahead of schedule in July, 2018. It plans to operate the plant at 60% capacity utilisation in FY19E. The new plant will cater to

5

ICICIdirect Money Manager January 2018

STOCK IDEAS

southern demand (30% of G I L ' s M D F s a l e s ) . T h e company would export the remaining portion. It is aiming at full utilisation by FY22E. With the commissioning of the new MDF plant, we expect, GIL's MDF revenues to grow robustly at 33.5% CAGR to | 1134.6 crore over FY17-20E.

New plywood capacity to be operational by Q3FY19E…

GIL is expanding its plywood capacity due to capacity constraints at its existing units. It is setting up a facility in UP with a manufacturing capacity of 13.5 MSM, which would take its total capacity to 45.9 MSM. It plans to spend ~| 125 crore and wou ld manu fac tu re premium plywood at the plant. The plant is expected to come on stream by Q3FY19E. GIL is also setting up a decorative veneer unit in Gujarat that is a l s o e x p e c t e d t o b e commissioned by Q3FY19E. To e n s u r e r a w m a t e r i a l security, the company has also set up a veneer unit in Gabon. Currently, three production lines are operational while the remaining three would be operational by December, 2017. Reduction in GST rates

from 28% to 18% coupled with the expected implementation of the E-way bill by April 1, 2018 would result in a quicker shift from unorganised to o r g a n i s e d p l a y e r s . C o n s e q u e n t l y , t h e management expects 12-15% revenue CAGR in the plywood division in the next two years. We expect plywood revenues to grow at 12.4% CAGR to | 1658.2 crore in FY18E-20E.

MDF division - future growth engine!!!

We remain positive on GIL as t h e s h a r e o f o r g a n i s e d plywood players (currently 30% of plywood market) is set to expand with GST rate cut, higher brand aspirations and GIL's strong brand presence. GIL's strategy of capex across p r o d u c t s e g m e n t s l i k e plywood, MDF and decorative veneer bode well for the company's future growth. Consequently, we expect topline, bottomline to grow at 19.8%, 19.4% to | 2842.3 c r o r e , | 2 2 9 . 8 c r o r e , respectively, in FY17-20E. We continue to maintain our BUY rating on the stock with a revised target price of | 425 (~22x FY20E EPS).

6

ICICIdirect Money Manager January 2018

STOCK IDEAS

Stock Data

Key Financials

Valuations Summary

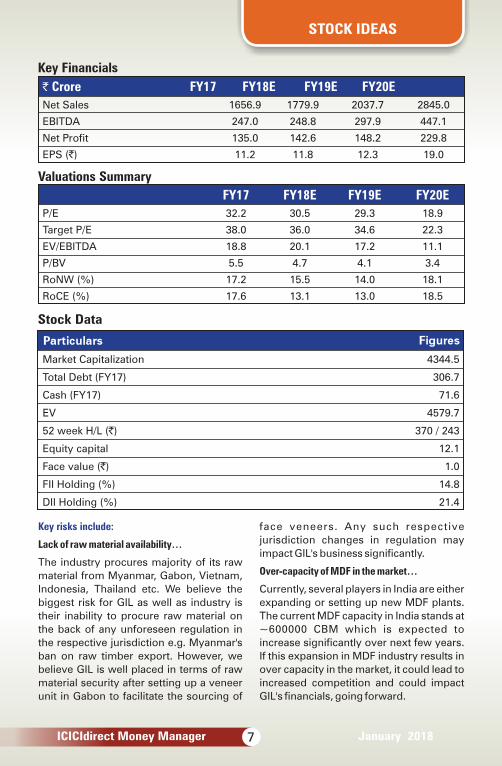

` Crore FY17 FY18E FY19E FY20E

Net Sales 1656.9 1779.9 2037.7 2845.0

EBITDA 247.0 248.8 297.9 447.1

Net Profit 135.0 142.6 148.2 229.8

EPS (`) 11.2 11.8 12.3 19.0

FY17 FY18E FY19E FY20E

P/E 32.2 30.5 29.3 18.9

Target P/E 38.0 36.0 34.6 22.3

EV/EBITDA 18.8 20.1 17.2 11.1

P/BV 5.5 4.7 4.1 3.4

RoNW (%) 17.2 15.5 14.0 18.1

RoCE (%) 17.6 13.1 13.0 18.5

Market Capitalization 4344.5

Total Debt (FY17) 306.7

Cash (FY17) 71.6

EV 4579.7

52 week H/L (`) 370 / 243

Equity capital 12.1

Face value (`) 1.0

FII Holding (%) 14.8

DII Holding (%) 21.4

7

Key risks include:

Lack of raw material availability…

The industry procures majority of its raw

material from Myanmar, Gabon, Vietnam,

Indonesia, Thailand etc. We believe the

biggest risk for GIL as well as industry is

their inability to procure raw material on

the back of any unforeseen regulation in

the respective jurisdiction e.g. Myanmar's

ban on raw timber export. However, we

believe GIL is well placed in terms of raw

material security after setting up a veneer

unit in Gabon to facilitate the sourcing of

face veneers. Any such respective

jurisdiction changes in regulation may

impact GIL's business significantly.

Over-capacity of MDF in the market…

Currently, several players in India are either

expanding or setting up new MDF plants.

The current MDF capacity in India stands at

~600000 CBM which is expected to

increase significantly over next few years.

If this expansion in MDF industry results in

over capacity in the market, it could lead to

increased competition and could impact

GIL's financials, going forward.

ICICIdirect Money Manager January 2018

STOCK IDEAS

ANALYST CERTIFICATION We /I, Deepak Purswani, CFA MBA (Finance), Vaibhav Shah, MBA (Finance); Research Analysts, authors and the names subscribed to this report, hereby certify that all of the views expressed in this research report accurately reflect our views about the subject issuer(s) or securities. We also certify that no part of our compensation was, is, or will be directly or indirectly related to the specific recommendation(s) or view(s) in this report.

Terms & conditions and other disclosures:ICICI Securities Limited (ICICI Securities) is a full-service, integrated investment banking and is, inter alia, engaged in the business of stock brokering and distribution of financial products. ICICI Securities Limited is a Sebi registered Research Analyst with Sebi Registration Number – INH000000990. ICICI Securities is a wholly-owned subsidiary of ICICI Bank which is India's largest private sector bank and has its various subsidiaries engaged in businesses of housing finance, asset management, life insurance, general insurance, venture capital fund management, etc. (“associates”), the details in respect of which are available on www.icicibank.com.

ICICI Securities is one of the leading merchant bankers/ underwriters of securities and participate in virtually all securities trading markets in India. We and our associates might have investment banking and other business relationship with a significant percentage of companies covered by our Investment Research Department. ICICI Securities generally prohibits its analysts, persons reporting to analysts and their relatives from maintaining a financial interest in the securities or derivatives of any companies that the analysts cover.

The information and opinions in this report have been prepared by ICICI Securities and are subject to change without any notice. The report and information contained herein is strictly confidential and meant solely for the selected recipient and may not be altered in any way, transmitted to, copied or distributed, in part or in whole, to any other person or to the media or reproduced in any form, without prior written consent of ICICI Securities. While we would endeavour to update the information herein on a reasonable basis, ICICI Securities is under no obligation to update or keep the information current. Also, there may be regulatory, compliance or other reasons that may prevent ICICI Securities from doing so. Non-rated securities indicate that rating on a particular security has been suspended temporarily and such suspension is in compliance with applicable regulations and/or ICICI Securities policies, in circumstances where ICICI Securities might be acting in an advisory capacity to this company, or in certain other circumstances.

This report is based on information obtained from public sources and sources believed to be reliable, but no independent verification has been made nor is its accuracy or completeness guaranteed. This report and information herein is solely for informational purpose and shall not be used or considered as an offer document or solicitation of offer to buy or sell or subscribe for securities or other financial

instruments. Though disseminated to all the customers simultaneously, not all customers may receive this report at the same time. ICICI Securities will not treat recipients as customers by virtue of their receiving this report. Nothing in this report constitutes investment, legal, accounting and tax advice or a representation that any investment or strategy is suitable or appropriate to your specific circumstances. The securities discussed and opinions expressed in this report may not be suitable for all investors, who must make their own investment decisions, based on their own investment objectives, financial positions and needs of specific recipient. This may not be taken in substitution for the exercise of independent judgment by any recipient. The recipient should independently evaluate the investment risks. The value and return on investment may vary because of changes in interest rates, foreign exchange rates or any other reason. ICICI Securities accepts no liabilities whatsoever for any loss or damage of any kind arising out of the use of this report. Past performance is not necessarily a guide to future performance. Investors are advised to see Risk Disclosure Document to understand the risks associated before investing in the securities markets. Actual results may differ materially from those set forth in projections. Forward-looking statements are not predictions and may be subject to change without notice.

ICICI Securities or its associates might have managed or co-managed public offering of securities for the subject company or might have been mandated by the subject company for any other assignment in the past twelve months.

ICICI Securities or its associates might have received any compensation from the companies mentioned in the report during the period preceding twelve months from the date of this report for services in respect of managing or co-managing public offerings, corporate finance, investment banking or merchant banking, brokerage services or other advisory service in a merger or specific transaction.

ICICI Securities or its associates might have received any compensation for products or services other than investment banking or merchant banking or brokerage services from the companies mentioned in the report in the past twelve months.

ICICI Securities encourages independence in research report preparation and strives to minimize conflict in preparation of research report. ICICI Securities or its associates or its analysts did not receive any compensation or other benefits from the companies mentioned in the report or third party in connection with preparation of the research report. Accordingly, neither ICICI Securities nor Research Analysts and their relatives have any material conflict of interest at the time of publication of this report.

It is confirmed that Deepak Purswani, CFA MBA (Finance), Vaibhav Shah, MBA (Finance); Research Analysts of this report have not received any compensation from the companies mentioned in the report in the preceding twelve months.

Compensation of our Research Analysts is not based on any specific merchant banking, investment banking or brokerage service transactions.

ICICI Securities or its subsidiaries collectively or Research Analysts or their relatives do not own 1% or more of the equity securities of the Company mentioned in the report as of the last day of the month preceding the publication of the research report.

Since associates of ICICI Securities are engaged in various financial service businesses, they might have financial interests or beneficial ownership in various companies including the subject company/companies mentioned in this report.

It is confirmed that Deepak Purswani, CFA MBA (Finance), Vaibhav Shah, MBA (Finance); Research Analysts do not serve as an officer, director or employee of the companies mentioned in the report.

ICICI Securities may have issued other reports that are inconsistent with and reach different conclusion from the information presented in this report.

Neither the Research Analysts nor ICICI Securities have been engaged in market making activity for the companies mentioned in the report.

We submit that no material disciplinary action has been taken on ICICI Securities by any Regulatory Authority impacting Equity Research Analysis activities.

This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution, publication, availability or use would be contrary to law, regulation or which would subject ICICI Securities and affiliates to any registration or licensing requirement within such jurisdiction. The securities

described herein may or may not be eligible for sale in all jurisdictions or to certain category of investors. Persons in whose possession this document may come are required to inform themselves of and to observe such restriction.

8

ICICIdirect Money Manager January 2018

STOCK IDEAS

Gujarat Gas - Price hike to support healthy margins…

Company Background

Gujarat Gas (GG) is one of the

Ind ia ' s la rgest p layer in

industrial gas segment and city

gas distribution (CGD) with a

dominant presence in Gujarat.

It caters to the gas demand of

~3000 industrial consumers,

~5 lakh CNG vehicles and ~12

lakh households in Gujarat.

Total volumes in FY17 were at

5 . 4 m m s c m d w i t h t h e

industrial and retail segments

contributing ~68% of total

volumes.

Investment Rationale

Profitable growth to continue

on account price hikes...

The company has announced

price hikes for its industrial

customers in the month of

December, which were due for

a considerable period of time.

For industrial units in Morbi,

prices have been hiked by |

2 . 5 / s c m t o | 2 7 . 9 / s c m ,

whereas for other industrial

units, prices have been hiked

by | 2.6/scm to | 29.2/scm. In

the near term, the company

has been witnessing a dip in

gross margins on account of

rise in LNG prices (input costs)

and no price hike for industrial

customers mainly on account

of state elections. However, the

current price hikes will help the

company to restore its healthy

margins in the range of | 7-

7.5/scm. Going ahead, better

gas sourcing arrangements

and relatively stable LNG

prices will enable the company

t o m a i n t a i n i t s

competitiveness.

Volume growth to remain

stable, going ahead

For H1FY18, the company

reported volume growth of

1 5 % Yo Y w i t h a v e r a g e

volumes at 5.9 mmscmd.

External factors like Gujarat

floods and GST transition

phase had some impact on

industrial volumes in the

previous quarter (Q2FY18).

However, we believe volumes

will come back on track in

coming quarters. Currently,

industrial volumes contribute

~70% of Gujarat Gas' total

sales volumes. Going ahead,

the company expects the share

9

ICICIdirect Money Manager January 2018

STOCK IDEAS

to reduce to ~60% over the

long term given the relatively

higher growth of CNG and

domestic PNG segment. In lieu

of the same, the company is

aiming to set up 200 CNG

stations in coming years.

Overall, we believe increase in

both CNG as well as industrial

PNG demand will drive Gujarat

G a s ' v o l u m e g r o w t h

momentum. Vo lumes in

FY18E, FY19E are estimated at

6 mmscmd, 6.8 mmscmd,

respectively.

Rapid expansion in CGD to

puts Gujarat Gas in sweet

spot

With its expanding presence

across several districts in

Gujarat and relatively low gas

prices, Gujarat Gas is set to

benefit, going ahead, from

volume growth in CNG, and

industrial retail segment. We

believe the company's strong

CGD network offers good

demand potential due to lower

C N G , r e s i d e n t i a l P N G

penetration and increased

usage of natural gas for

industrial volumes. We now

value Gujarat Gas at 25x FY19E

EPS of | 40 on the back of

better visibility on earnings

growth. We have a BUY rating

with a target price of | 1000.

Valuations Summary

Key Financials

` Crore FY16 FY17 FY18E FY19E

Net Sales 6105.9 5093.0 5989.3 7155.2

EBITDA 725.2 749.0 930.5 1195.2

Net Profit 178.6 223.1 342.7 550.7

EPS (`) 13.0 16.2 24.9 40.0

FY16 FY17 FY18E FY19E

P/E 71.2 57.0 37.1 20.7

Target P/E 69.4 55.5 36.2 25.0

EV / EBITDA 20.7 20.0 16.1 12.2

P/BV 7.6 6.9 6.8 5.5

RoNW 11.8 13.6 18.3 24.0

RoCE 12.4 12.3 16.0 21.1

10

ICICIdirect Money Manager January 2018

STOCK IDEAS

Stock Data

Key risks include:

Disruption in gas supplies

Gujarat Gas receives more

than 80% of the current gas

supplies from GAIL. Any

n e g a t i v e c h a n g e i n t h e

allocation of gas to GG would

have an impact on the earnings

estimates and valuations of the

company.

Currency Risk

GG's supply contracts for the

purchase of gas are mostly

denominated in US dollars

while the company supplies to

customers in Indian rupees.

Hence, any sharp depreciation

in the Indian rupee will have a

short-term negative impact on

earnings of the company, as it

will be difficult for GG to pass

on the increase in raw material

costs to customers.

Market Capitalization (` crore) 11399.9

Debt (` crore) 2350.9

Cash and Cash Equivalent (` crore) 62.1

EV (` crore) 15010.4

52 Week High / Low (`) 973 / 500

Equity Capital 137.7

Face Value (`) 10.0

11

ICICIdirect Money Manager January 2018

STOCK IDEAS

ANALYST CERTIFICATION We /I, Mayur Matani, MBA and Akshay Gavankar, PGDM) Research Analysts, authors and the names subscribed to this report, hereby certify that all of the views expressed in this research report accurately reflect our views about the subject issuer(s) or securities. We also certify that no part of our compensation was, is, or will be directly or indirectly related to the specific recommendation(s) or view(s) in this report.

Terms & conditions and other disclosures:ICICI Securities Limited (ICICI Securities) is a full-service, integrated investment banking and is, inter alia, engaged in the business of stock brokering and distribution of financial products. ICICI Securities Limited is a Sebi registered Research Analyst with Sebi Registration Number – INH000000990. ICICI Securities is a wholly-owned subsidiary of ICICI Bank which is India's largest private sector bank and has its various subsidiaries engaged in businesses of housing finance, asset management, life insurance, general insurance, venture capital fund management, etc. (“associates”), the details in respect of which are available on www.icicibank.com.

ICICI Securities is one of the leading merchant bankers/ underwriters of securities and participate in virtually all securities trading markets in India. We and our associates might have investment banking and other business relationship with a significant percentage of companies covered by our Investment Research Department. ICICI Securities generally prohibits its analysts, persons reporting to analysts and their relatives from maintaining a financial interest in the securities or derivatives of any companies that the analysts cover.

The information and opinions in this report have been prepared by ICICI Securities and are subject to change without any notice. The report and information contained herein is strictly confidential and meant solely for the selected recipient and may not be altered in any way, transmitted to, copied or distributed, in part or in whole, to any other person or to the media or reproduced in any form, without prior written consent of ICICI Securities. While we would endeavour to update the information herein on a reasonable basis, ICICI Securities is under no obligation to update or keep the information current. Also, there may be regulatory, compliance or other reasons that may prevent ICICI Securities from doing so. Non-rated securities indicate that rating on a particular security has been suspended temporarily and such suspension is in compliance with applicable regulations and/or ICICI Securities policies, in circumstances where ICICI Securities might be acting in an advisory capacity to this company, or in certain other circumstances.

This report is based on information obtained from public sources and sources believed to be reliable, but no independent verification has been made nor is its accuracy or completeness guaranteed. This report and information herein is solely for informational purpose and shall not be used or considered as an offer document or solicitation of offer to buy or sell or subscribe for securities or other financial instruments. Though disseminated to all the customers simultaneously, not all customers may receive this report at the same time. ICICI Securities will not treat recipients as customers by virtue of their receiving this report. Nothing in this report constitutes investment, legal, accounting and tax advice or a representation that any investment or strategy is suitable or appropriate to your specific circumstances. The securities discussed and opinions expressed in this report may not be suitable for all investors, who must make their own investment decisions, based on their own investment objectives, financial positions and needs of specific recipient. This may not be taken in substitution for the exercise of independent judgment by any recipient. The recipient should independently evaluate the investment risks. The value and return on investment may vary because of changes in interest rates, foreign exchange rates or any other reason. ICICI Securities accepts no liabilities whatsoever for any loss or damage of any kind arising out of the use of this report. Past performance is not necessarily a guide to future performance. Investors are advised to see Risk Disclosure Document to understand the risks associated before investing in the securities markets. Actual results may differ materially from those set forth in projections. Forward-looking statements are not predictions and may be subject to change without notice.

ICICI Securities or its associates might have managed or co-managed public offering of securities for the subject company or might have been mandated by the subject company for any other assignment in the past twelve months.

ICICI Securities or its associates might have received any compensation from the companies mentioned in the report during the period preceding twelve months from the date of this report for services in respect of managing or co-managing public offerings, corporate finance, investment banking or merchant banking, brokerage services or other advisory service in a merger or specific transaction.

ICICI Securities or its associates might have received any compensation for products or services other than investment banking or merchant banking or brokerage services from the companies mentioned in the report in the past twelve months.

ICICI Securities encourages independence in research report preparation and strives to minimize conflict in preparation of research report. ICICI Securities or its associates or its analysts did not receive any compensation or other benefits from the companies mentioned in the report or third party in connection with preparation of the research report. Accordingly, neither ICICI Securities nor Research Analysts and their relatives have any material conflict of interest at the time of publication of this report.

It is confirmed that Mayur Matani, MBA and Akshay Gavankar, PGDM Research Analysts of this report have not received any compensation from the companies mentioned in the report in the preceding twelve months.

Compensation of our Research Analysts is not based on any specific merchant banking, investment banking or brokerage service transactions.

ICICI Securities or its subsidiaries collectively or Research Analysts or their relatives do not own 1% or more of the equity securities of the Company mentioned in the report as of the last day of the month preceding the publication of the research report. ,

Since associates of ICICI Securities are engaged in various financial service businesses, they might have financial interests or beneficial ownership in various companies including the subject company/companies mentioned in this report.

It is confirmed that Mayur Matani, MBA and Akshay Gavankar, PGDM. Research Analysts do not serve as an officer, director or employee of the companies mentioned in the report.

ICICI Securities may have issued other reports that are inconsistent with and reach different conclusion from the information presented in this report.

Neither the Research Analysts nor ICICI Securities have been engaged in market making activity for the companies mentioned in the report.

We submit that no material disciplinary action has been taken on ICICI Securities by any Regulatory Authority impacting Equity Research Analysis activities.

This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution, publication, availability or use would be contrary to law, regulation or which would subject ICICI Securities and affiliates to any registration or licensing requirement within such jurisdiction. The securities described herein may or may not be eligible for sale in all jurisdictions or to certain category of investors. Persons in whose possession this document may come are required to inform themselves of and to observe such restriction.

report and information herein is solely for informational purpose and shall not be used or considered as an offer document or solicitation of offer to buy or sell or subscribe for securities or other financial instruments. Though disseminated to all the customers simultaneously, not all customers may receive this report at the same time. ICICI Securities will not treat recipients as customers by virtue of their receiving this report. Nothing in this report constitutes investment, legal, accounting and tax advice or a representation that any investment or strategy is suitable or appropriate to your specific circumstances. The securities discussed and opinions expressed in this report may not be suitable for all investors, who must make their own investment decisions, based on their own investment objectives, financial positions and needs of specific recipient. This may not be taken in substitution for the exercise of independent judgment by any recipient. The recipient should independently evaluate the investment risks. The value and return on investment may vary because of changes in interest rates, foreign exchange rates or any other reason. ICICI Securities accepts no liabilities whatsoever for any loss or damage of any kind arising out of the use of this report. Past performance is not necessarily a guide to future performance. Investors are advised to see Risk Disclosure Document to understand the risks associated before investing in the securities markets. Actual results may differ materially from those set forth in projections. Forward-looking statements are not predictions and may be subject to change without notice.

ICICI Securities or its associates might have managed or co-managed public offering of securities for the subject company or might have been mandated by the subject company for any other assignment in the past twelve months.

ICICI Securities or its associates might have received any compensation from the companies mentioned in the report during the period preceding twelve months from the date of this report for services in respect of managing or co-managing public offerings, corporate finance, investment banking or merchant banking, brokerage services or other advisory service in a merger or specific transaction.

ICICI Securities or its associates might have received any compensation for products or services other than investment banking or merchant banking or brokerage services from the companies mentioned in the report in the past twelve months.

12

FUNDAMENTAL OUTLOOK2018

ICICIdirect Money Manager January 2018

Investment Outlook 2018

Pankaj Pandey,Head-Research,ICICIdirect

CY 17 was a remarkable year for equities as liquidity across the globe ensured that it was the most favored asset class. Back home in India, the story was no different as Sensex delivered a handsome 29% return, aided further by the falling yields which led to decline in cost of capital and consequent expansion of P/E multiples. Amid all these, the year was also marked by one-offs such as Demonetisation and implementation of GST, which temporarily led to a down tick in corporate earnings and GDP growth.

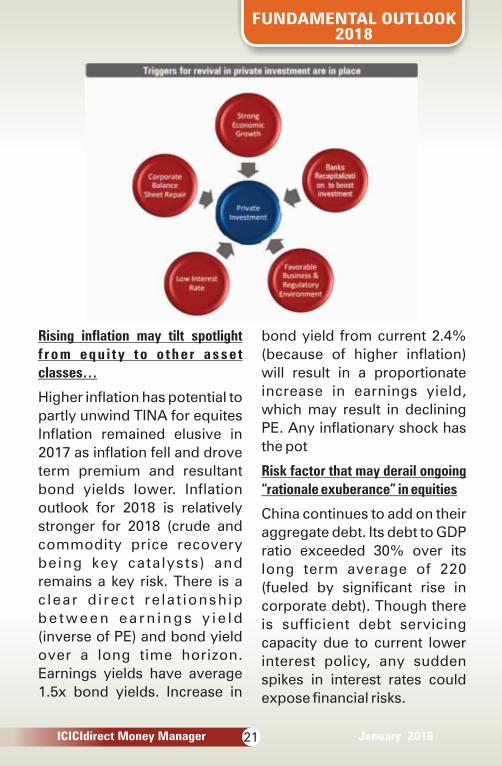

Government to lead capex, its p o l i c i e s t o b r e a k p r i v a t e investment jinx… Based on our bottom up approach, in f ras t ructure investment may jump up to Rs .48 lakh c rore led by housing, roads and railways in

the next five years, which i m p l i e s 1 0 % C A G R i n infrastructure spending in the next five years. Hence, we expect infrastructure spending as percentage of GDP to inch up to 6.0% in the next five years vs. 5.6% in the previous f i ve years . In our v iew, inc reased in f ras t ruc ture spending may inch up GDP growth rate by 80 to 100 bps. Government's “Housing for All b y 2 0 2 2 ” s c h e m e ( t o t a l

Source: ICICIdirect.com Research

13

FUNDAMENTAL OUTLOOK2018

ICICIdirect Money Manager January 2018

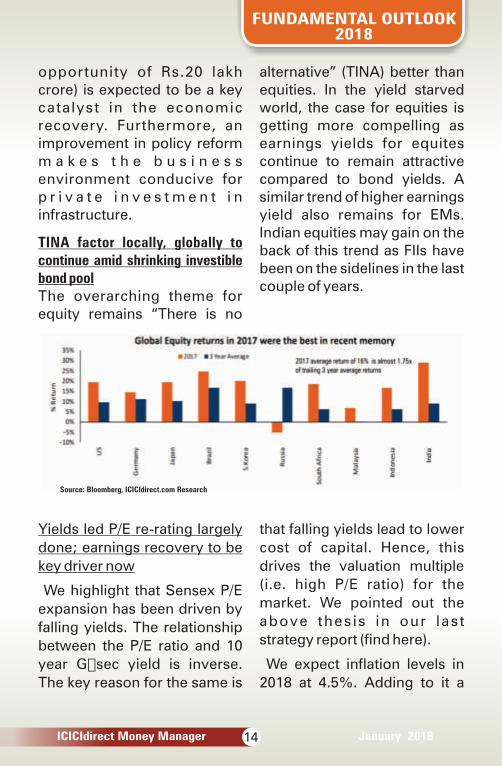

TINA factor locally, globally to continue amid shrinking investible bond poolThe overarching theme for equity remains “There is no

opportunity of Rs.20 lakh crore) is expected to be a key catalyst in the economic recovery. Furthermore, an improvement in policy reform m a k e s t h e b u s i n e s s environment conducive for p r i v a t e i n v e s t m e n t i n infrastructure.

alternative” (TINA) better than equities. In the yield starved world, the case for equities is getting more compelling as earnings yields for equites continue to remain attractive compared to bond yields. A similar trend of higher earnings yield also remains for EMs. Indian equities may gain on the back of this trend as FIIs have been on the sidelines in the last couple of years.

Source: Bloomberg, ICICIdirect.com Research

Yields led P/E re-rating largely

done; earnings recovery to be

key driver now

We highlight that Sensex P/E

expansion has been driven by

falling yields. The relationship

between the P/E ratio and 10

year G�sec yield is inverse.

The key reason for the same is

that falling yields lead to lower

cost of capital. Hence, this

drives the valuation multiple

(i.e. high P/E ratio) for the

market. We pointed out the

above thes is in our last

strategy report (find here).

We expect inflation levels in

2018 at 4.5%. Adding to it a

14

FUNDAMENTAL OUTLOOK2018

ICICIdirect Money Manager January 2018

normalized real interest rate of

175 bps and further 75-100 bps

markup for 10 year G-sec, we

expect the 10 year G-sec yield

to hover close to 7-7.25%

(similar to current levels).

Therefore, we believe much of

the yield based re�rating is

largely done.

However, going ahead, the key

driving force for the market

would be earnings recovery

(earnings CAGR of 17.4% in

FY17-20), which will largely be

the function of improving

c a p a c i t y u t i l i s a t i o n a t

corporate level (currently at

five year low).

Sensex RoCE to expand as utilization levels of India Inc improve

=Ex-financials, Sensex RoCE is expected to expand 220 bps in FY17-20E to 24.7% by FY20E vs. 22.5% in FY17, leading to earnings CAGR of 11% over FY17-20E

=Improvement is envisaged on account of higher sweating of assets and consequent better asset turnovers coupled with operational leverage benefits in terms of improved EBITDA margin profile

15

FUNDAMENTAL OUTLOOK2018

ICICIdirect Money Manager January 2018

For financials; core RoAs are

expected to improve gradually

to 3.3% in FY20E vs. 3.1% in

FY17 primarily tracking a

revival of credit growth.

C o n s e q u e n t l y, B F S I i s

expected to report a robust

33% earnings CAGR over

FY17�20E.

Measuring Nifty fair value:

SoTP methodology intersects

P/E valuation at 11,725

We have tried to evolve 2018

Index target based on bottoms

up approach by using a sum of

the parts (SoTP) evaluation of

individual index constituents

T h e r a t i o n a l e o f s u c h

methodology stems from the

fact that over the period of

time, companies, within the

index, with presence in various

verticals/businesses have

witnessed value unlocking and

in such case the concept of

SoTP captures the value in a

better way than purely P/E

based valuations (especially

for businesses where earnings

are yet to mature). Moreover,

we also note that superior

b u s i n e s s e s , e x h i b i t i n g

consistent RoCEs, within the

index now command higher

valuat ions, whi le certain

businesses within the index

continue to trade at/below

average index multiple .

It should be noted that our

Sensex target implies target

P/E of 18x on average of FY19

and FY20 earnings(i.e. 1x PEG),

which is on the higher end of

historical average P/E of

16�17x commanded by the

market. However, we highlight

that improving RoCE is a better

metric than PE dissonance

during an economic upturn.

16

FUNDAMENTAL OUTLOOK2018

ICICIdirect Money Manager January 2018

GST collections yet to stabilize

GST collections thus far are below our estimate, and we suspect below the revenue neutral rate required. Lower than expected GST collections (and thus, lower indirect taxes) would be an overhang on fiscal deficit financing. In absence of off icial estimates for the targeted col lect ions, we arrived at a revenue neutral figure of GST collections by working backwards from combined FY17 indirect tax revenues of the Central and State governments. GST collections would need to match comparable indirect tax revenues to ensure zero revenue loss under the new system.

Income tax collections boosted

Demonetisation-impacted H2FY17 saw a rise of 16% in direct tax collections YoY. In comparison, H1FY17 (six m o n t h s b e f o r e demonetisation) had recorded a 9% YoY growth over the comparable period. Apart from crackdown on black money, voluntary income declaration s c h e m e s , i n c r e a s e i n

surcharges for higher income slabs (above Rs.50 lakh and Rs.1 crore) and fear of action from authorities seem to have p r o v i d e d a b o o s t t o co l l ec t ions . In te rms o f p e r s o n a l i n c o m e t a x collections, the government managed to rake in Rs.3.5 lakh crore from individual tax payers in FY17, a rise of 21% YoY from FY16 collection of Rs.2.9 lakh crore. The total number of tax returns filed by individual assesses during FY17 was 5.43 crore, up 17.3% YoY. 1.26 crore new taxpayers (i.e. return filers and non-filers making tax payments) were added to the tax base

Corporate tax rates to decline gradually as near term fisc is challenged…

The Finance Minister in his previous Budget 2015 had made clear his intention to cut corpora te taxes to 25% gradually over a period to e n c o u r a g e f o r e i g n investments and jobs. In this direction, the government in the last Budget reduced the tax rate for companies with an annual turnover up to Rs.50 crore to 25% to promote

17

FUNDAMENTAL OUTLOOK2018

ICICIdirect Money Manager January 2018

MSME and encourage firms to migrate to the company format.

However, in the coming Budget, there is little room for the government to reduce corporate tax rates as clarity is yet to emerge on GST revenue collections. With the phasing out of major profit linked deductions like accelerated depreciation, SEZ, area based deductions, etc., and plugging loopholes in the direct tax systems, the government can g r a d u a l l y b r i n g d o w n corporate taxes to the desired levels of 25% over a period of time

We expect the fiscal deficit for FY17�18 at 3.4% of GDP, 20 bps above the targeted fiscal deficit of 3.2%. For FY17�18, disinvestment receipts have been budgeted at Rs.72,500 crore. However, we expect the same at Rs.1,08,000 crore on account of significant stake stales, buybacks in Q4FY18 . We b e l i e v e t h e e x c e s s proceeds from disinvestment of Rs.35,500 crore are likely to provide significant cushion to the government to meet the fiscal target for FY17�18.

Indian nominal GDP growth seems to have bottomed out and is poised for long term structural growth on account of enduring reforms such as d e m o n e t i s a t i o n , G S T, Insolvency and Bankruptcy code (IBC), etc. Although reforms have taken a toll on the nominal GDP (9.3% in H1FY18) in the short�term, realisation of long term advantages will start mainly from FY19. Private consumption (PFCE), the backbone of India's GDP, is expected to continue its steady growth momentum due to an increase in disposable income.

Traction in disposable income & state pay commission to drive consumption…

Agri loan waiver and increase in disposable income are expected to provide support to f o o d & b e v e r a g e s c o n s u m p t i o n a n d b a s i c h o u s i n g n e e d s , w h i c h contribute 45% to PFCE. Also, robust growth in consumption of clothing & footwear (7% of P F C E ) , t r a n s p o r t & communication (18%) among others are expected to lead to i m p r o v e m e n t i n p r i v a t e consumption growth.

18

FUNDAMENTAL OUTLOOK2018

ICICIdirect Money Manager January 2018

Source: RBI, Mospi, Government of India, media articles, ICICIdirect.com Research

After the central government's

implementation of Seventh

Pay Commission, states are

also likely to follow suit by

i n c r e a s i n g e x p e n d i t u r e

towards salaries and pension.

Some of the states have

already announced the budget

for incremental salaries and

wages. Initial figures suggest

the release of incremental

Rs.70,000 crore from some of

major states. This can go up to

R s . 2 l a k h c r o r e w i t h

implementation across all

states. We expect expenditure

of states on salaries and wages

to increase sharply at 19.3% in

FY19E.

Also, HRA dues to the tune of

Rs.30000 crore and Rs.10000

crore for teachers in UGC

funded un ivers i t i es and

colleges, respectively, lined up

for payment between H2FY18

and FY19E is likely to increase

the quantum of GFCE. As

salaries and wages constitutes

65% of the GFCE, hike in the

s a m e w o u l d s t i m u l a t e

consumption over the next

couple of years. Hence, we

expect the GFCE to increase at

12.6% and 14.8% in FY18E and

FY19E, respectively.

Source: RBI, Mospi, Government of India, media articles, ICICIdirect.com Research

19

FUNDAMENTAL OUTLOOK2018

ICICIdirect Money Manager January 2018

Real interest rate within RBI range,

to maintain status quo on Repo rate

RBI has indicated to maintain

real interest rate in the range of

1.25%-2.00%. RBI earlier said

the equilibrium real interest

rate in India was 1.5�2.0% but

it subsequently brought down

the range to 1.25%

We have tried to analyse the

future rate action by RBI with

real rate assumption of 1.75%

and average inflation range for

year 2018 at 4.25% to 4.75%

We expect RBI to maintain

status quo on repo rate at 6.0%

during CY18. While we do not

expect a further rate cut, we

also do not expect a reversal in

the interest rate cycle in the

near future

The recent up move in G-sec

yield with 10 year yield moving

t o 7 . 3 0 % i s m o r e o f a

r e t r a c e m e n t o f b u l l i s h

positioning as investors adjust

from a declining rate cycle to a

prolonged status quo phase in

benchmark rates. Considering

the 10 Year G-Sec yield spread

over repo at 100-125bps, we

expect 10 year G-Sec yield to

trade in the range of 7.0%-

7.25%

Scope for banking system to lower

rates remains…deposit repricing

effect still at play

Whi le we expect RB I to

m a i n t a i n s t a t u s q u o o n

benchmark rates for most of

year 2018, we believe there is

still scope of lower lending

rates in the banking system.

Lower credit cost in terms of

lower provisioning, repricing

of deposits at lower rates and

structural reforms like lower

cash to GDP ratio, increased

digital transactions, increase in

merchant discount rate (MDR)

rates expected to cut losses,

benchmarking of lending rates

to marginal cost lending rate

(MCLR) provide scope for

further rate transmission. We

estimate scope of further

reduction of 40 bps in the

banking system in a gradual

m a n n e r p a r t i c u l a r l y i n

c o r p o r a t e l e n d i n g r a t e .

{assumed 40 bps = 20 bps

from deposits + 15 bps from

provisions + 5 bps from lower

opex}

20

FUNDAMENTAL OUTLOOK2018

ICICIdirect Money Manager January 2018

Rising inflation may tilt spotlight

f rom equ i t y to o the r asse t

classes…

Higher inflation has potential to

partly unwind TINA for equites

Inflation remained elusive in

2017 as inflation fell and drove

term premium and resultant

bond yields lower. Inflation

outlook for 2018 is relatively

stronger for 2018 (crude and

commodity price recovery

being key catalysts) and

remains a key risk. There is a

c lear d i rect re la t ionship

b e t w e e n e a r n i n g s y i e l d

(inverse of PE) and bond yield

over a long time horizon.

Earnings yields have average

1.5x bond yields. Increase in

bond yield from current 2.4%

(because of higher inflation)

will result in a proportionate

increase in earnings yield,

which may result in declining

PE. Any inflationary shock has

the pot

Risk factor that may derail ongoing

“rationale exuberance” in equities

China continues to add on their

aggregate debt. Its debt to GDP

ratio exceeded 30% over its

long term average of 220

(fueled by significant rise in

corporate debt). Though there

is sufficient debt servicing

capacity due to current lower

interest policy, any sudden

spikes in interest rates could

expose financial risks.

21

FUNDAMENTAL OUTLOOK2018

ICICIdirect Money Manager January 2018

Sectoral Outlook:

- We are positive on sectors like

auto (volume driven operating

leverage benefit &increasing

share of premium) , banking

(PSU banks' return potential),

c a p i t a l g o o d s , c e m e n t

(demand fromrural, Individual

House Builder (IHB) segment

and government led infra

p r o j e c t s ) , c o n s u m e r

discretionary (India's shifting

preference towards premium

products and increas ing

penetration of the electrical

goods, asset light model, cash

surplus status of companies),

FMCG (increasing demand

22

FUNDAMENTAL OUTLOOK2018

ICICIdirect Money Manager January 2018

from rural India, structural

r e fo rms ) , i n f r as t ruc tu re

(government's renewed focus

on sector, “Housing for All by

2022”scheme, historic road

building program), logistics

(implementation of the e-way

bill) , media, retail (Incremental

benefit of the shift from

unorganised to organized) and

telecom (data usage adoption

- We are neutral on defensives

l i k e I T ( t r a n s i t i o n o f I T

landscape from traditional to

digital, client IT spending

pattern towards emerging

technologies) , textiles and

apparels, pharma (post GST

r e c o v e r y , n o r m a l i z e d

emerging markets currency

volatility and new product

launches) , power, real estate

(optimist ic on affordable

h o u s i n g s e g m e n t a m i d

government's policy push,

improvement in fundamental

drivers such as sales volumes)

, metals and mining (stable

rea l i za t ions and hea l thy

demand prospects) , oil and

gas (sharp run-up in stock

prices, steady volume led

growth expected)

23

TECHNICAL OUTLOOK 2018

ICICIdirect Money Manager January 2018

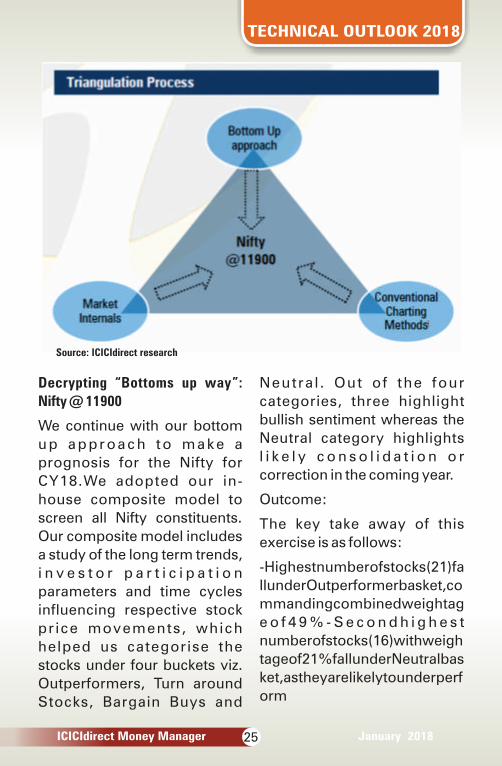

Triangulation reaffirms faith in Bulls

As 2017 draws to an end with>20% gain on domestic indices, a common question that an investor is pondering upon is “Is a significant correction in sight?” or “Are we at a tipping point,which would converge into a mega bull rally for the next couple of years?” Hence, we have centered our“Market Strategy2018” report around the above questions in order to gauge what is in store for equities in CY18.

Dharmesh Shah,Head-Technical analysis, ICICIdirect

WeinitiatedaTriangulationpro

cessinascertainingthewayah

eadformarketsthatpencilsina)

bottomupapproach,b)conve

ntionalchartingmethodsandc

)marketinternals.Alloutcome

sreaffirmthatbullswillprevaili

nCY18whereintheNiftyisexpe

ctedtoreturn14%withapotent

ialtargetof11900overthenext

12-15months.

Apartfromtheabove,wealsod

ecipheredinterestingobserva

tionsthatinclude:

> Mega t rend ana lys is

highlights multifold rallies

over the next few years and

m i n o r c o r r e c t i o n s

accompanied by i t that

should be utilized as an

i n c r e m e n t a l b u y i n g

opportunity

>Dissecting 'unconventional/

unloved' ideas (both large

and mid/small caps) for beta

c a p t u r i n g . I n c a s e o f

unconventional ideas we

have constructed in-house

sectoral indices that have

eventually helped us pick

stocks from those baskets.

F o r u n l o v e d s t o c k s ,

observation of cycles across

a longer time frame and back

testing it have also thrown up

interesting ideas across the

spectrum

Onlydownsiderisktoourprog

nosisiselongatedtimecorrecti

onwithlimitedpricedamageas

wedonotexpecttheNiftytosus

tainbelow9400levels.

24

TECHNICAL OUTLOOK 2018

ICICIdirect Money Manager January 2018

Source: ICICIdirect research

Decrypting “Bottoms up way”:

Nifty @ 11900

We continue with our bottom

up approach to make a

prognosis for the Nifty for

CY18.We adopted our in-

house composite model to

screen all Nifty constituents.

Our composite model includes

a study of the long term trends,

i n v e s t o r p a r t i c i p a t i o n

parameters and time cycles

influencing respective stock

pr ice movements, which

helped us categorise the

stocks under four buckets viz.

Outperformers, Turn around

Stocks, Bargain Buys and

Neutra l . Out of the four

categories, three highlight

bullish sentiment whereas the

Neutral category highlights

l i k e l y c o n s o l i d a t i o n o r

correction in the coming year.

Outcome:

The key take away of this

exercise is as follows:

-Highestnumberofstocks(21)fa

llunderOutperformerbasket,co

mmandingcombinedweightag

e o f 4 9 % - S e c o n d h i g h e s t

numberofstocks(16)withweigh

tageof21%fallunderNeutralbas

ket,astheyarelikelytounderperf

orm

25

TECHNICAL OUTLOOK 2018

ICICIdirect Money Manager January 2018

-Eightindexconstituentswith18

%weightagehaveapproached

price,timewisematurityofcorre

ction&settobeginfreshuptrend

-Fivestockscarryingweightagef

12%arewitnessingastructural

Source: Bloomberg, ICICI Direct.com Research

Mega trends: Are we at a tipping

point?

The Sensex witnessed two

m e g a t r e n d s s i n c e i t s

inception. Between 1979 and

1992,theindexgained40timeso

ver13yearswhi lethe2003-

08rallygainedseventimesinma

g n i t u d e . W h i l e t h e 2 0 0 3 -

08rallywasbornoutofa11yearb

e a r p h a s e ( 1 9 9 2 -

2003),thecurrentbullmarket,w

hichcommencedfrom2013low

s,wasprecededbysixyearsof

underperformance (2008-

14whentheactualbreakoutocc

urred)

Source: Bloomberg, ICICI Direct.com Research

26

TECHNICAL OUTLOOK 2018

ICICIdirect Money Manager January 2018

Technically,wewanttopresenta

casethatinvestorsshouldfocus

onlongtermtrendsandbenefitfr

omthemratherthanworryingab

outshort term a berrations as

e v i d e n t f r o m h i s t o r i c a l

evidence.Anempiricalevidenc

egivesusconfidencethatthecur

rentbullmarketinIndiaisstillina

nearlystageandisl ikely to

extend over then extfourt of

I've years. Therefore, were

commend utilizing any inter

media tecorrections as a

n i n c r e m e n t a l b u y i n g

opportunity.

General Elections: Bulls charge…

The year 2018 being a pre-

election year wil l have a

s i g n i f i c a n t b e a r i n g o n

sentiments in equity markets. It

has been observed tha t

benchmark ind ices have

performed relatively well in

pre-election year. Hence,

historical evidence suggest

that there are unlikely to be

large drawdowns in CY18.

Source: Bloomberg, ICICI Direct.com Research

Gold ($1264): Bullion to extend

its time correction, upsides

capped at $1400...

= Gold prices have gained

almost 10% during CY17 on

the back of weakness in the US

dollar and increased global

geopolitical tensions. Despite

the up move, gold prices

remained in a broad range of

$1400-1050 in the last four

years.

= Going forward, we expect

gold prices to continue the

c u r r e n t c o r r e c t i v e

econsolidation. Prices, after 11

years of stupendous rally from

$252 to $1921, have been in a

27

TECHNICAL OUTLOOK 2018

ICICIdirect Money Manager January 2018

corrective trend in the last six

year while retracing 50% of the

previous rally. We expect

prices to remain in the time

wise consolidation phase

while upsides look capped

around the $1400 region, as it

is the higher band of the last

four years consolidation and

the 38.2% retracement of the

entire decline from 2011 peak

of $1921 to 2015 bottom of

$1046 levels.

Source: Bloomberg, ICICI Direct.com Research

B r e n t ( $ 6 3 . 8 0 ) : T i m e w i s e

consolidation to extend...

=WeexpectBrentcrudepricest

oshifttheirtradingrangehigher

whileconsolidatinginarangego

inginto2018.Theupsidelooksc

appedaround$70levelsasitisth

econfluenceoffollowingtechni

calparameters:

>Price parity with previous

2016 rally from $ 31 to $ 58 as

projected from the 2017 low of

$ 43 projects upside towards $

70 levels

>The previous yearly high of

2015 is placed around $ 70

levels

=Declinesinoilpricesarelikelyt

o b e a n c h o r e d a t ~ $ 5 0 -

52beingthe61.8%retracement

ofpastfivemonthsrally($44-

64)placedat$52andvalueofther

isingtrendlineconnectingyearl

ylowsof2016($27)and2017($4

4)

28

TECHNICAL OUTLOOK 2018

ICICIdirect Money Manager January 2018

=To sum up, Brent prices are

expected to remain in a

broader trading range of $50-

72 amid lack of structural turn

around on long term charts

Source: Bloomberg, ICICI Direct.com Research

US$INR (64.05): Rupee likely to

appreciate to 62…

=Fromayearlyperspective,the

USDINRpairformedabearishen

gulfingcandlethisyear,hintinga

tatemporaryhalttotherupeede

preciationtrajectorythatbeena

majorthemesinceCY11.

=WeexpecttheUSDINRpairto

depreciatein2018andheadtow

ardsthemajorsupportarea

s e e n n e a r t h e 6 2 . 4 0 -

62.00region,whichistheconflu

enceof:i)61.8%Fibonacciexten

sionofdeclinefrom2013 high to

2014lowextendedfrom2016hi

gh,andii)61.8%Fibonacciexten

sionofdeclinefrom68.87to63.9

2extendedfrom65.89.

=Havingsaidthat,wedonotfor

eseethepairsustainingbelow62

-62.00rangenextyear,aspolicy

divergencebetweentheFederal

ReserveandotherG7centralban

ksshouldkeepthedollarsupport

edagainsttheG7basket

=Thepairhasmajorresistancei

nthecomingyeararound66.50l

evelsbeingtheconfluenceofthe

breakdownareaofMarch2017a

ndthe61.8%retracementofthe

2017downmove.

29

DERIVATIVES STRATEGYFOR 2018

ICICIdirect Money Manager January 2018

Rational exuberance to drive Nifty higher for target of 11700…

Amit GuptaHead - Derivatives Research,ICICI Securities

Since the commencement

of rate hike by the US Fed in

2015, equity markets have

constantly outperformed

other key asset classes like

gold and bonds. This has

triggered strong inflows into

equities at the expense of

other key asset classes like

bond and gold. S&P is likely

to clock strong positive

returns in 2018, as the Fed is

expected to deliver two or

three rate hikes in 2018,

which is likely to keep the

underperformance trend of

bonds, gold intact (caveat

being deflation shock).Easy

financial conditions coupled

with subdued volatility and

robust sent iment f rom

corporates, individuals to

cont inue to thrus t US

equities higher.

The decline in standard

dev ia t ion (SD) o f S&P

returns was seen in 2016

when SD declined from 4%

to 3%. In the Nifty, it was

seen in 2017 when SD of

Nifty returns fell from 5% to

3%. We believe 2018 would

be the year in which SD of

Nifty returns could witness a

further decline from 3% to

1.5% following S&P pattern.

Hence, we believe the Nifty

should be able to post near

17% return in the coming

year.

30

DERIVATIVES STRATEGYFOR 2018

ICICIdirect Money Manager January 2018

Source: Bloomberg, ICICIdirect.com Research

June 2018, 9700 Put writing further strengthens view of strong support near these levels

= The action happened not only in 2017 Put strike but also in June 2018 Put strike where premiums were shorted in a n t i c i p a t i o n o f l i m i t e d downsides in the market

= The 9700 Put of June 2018 is still witnessing writing. This also started when the Nifty was near 9700. This strengthens the view that strong support for the market is close to these levels.

While the US Fed has started its unwinding of balance sheet, ECB and BoJ are likely to c o n t i n u e w i t h t h e i r Q E

programme. Together, they will continue to push US$100 billion of QE till June 2018. Even after this, BoJ is likely to continue with its US$60 billion QE run rate. Hence, the central bank liquidity picture is likely to remain positive in 2018. A positive liquidity environment bodes well for risk assets like equities

Equity ETF in US clocked record inflow

ETFs in US have outgrown actively managed MFs. On a consolidated basis, strong inflow is seen in equity ETF. As per the latest data for 2017, equi ty based ETFs have received almost double the record inflows seen in 2016.

31

DERIVATIVES STRATEGYFOR 2018

ICICIdirect Money Manager January 2018

This suggests preference for equity remains

Volatility to remain lower in equities

Cross asset volatility is likely to remain low. In equity markets more specifically, volatility has been moving in sync not only for India and EMs but also the developed markets. With chances of any major risk shock remaining benign, volatility across equity markets is likely to remain low

Bond market f lows taking a breather

At the start of the year, as the reflation trade eased, EM bonds saw strong buying i n t e r e s t i n H 1 o f 2 0 1 7 . However, in H2 of 2017, as growth picked up pace in most Ems, the inflows in bonds tapered off. Additionally, the decidedly hawkish centrals banks of the US & Europe kept yields higher. This reduced the spread between developed markets and EMs. As a result, the alpha from EM bond portfolio has reduced. FIIs are using the equity route for EMs as GDP growth and EPS expansion remains intact for most Ems. Hence, in 2018, EM

equites should continue to see strong inflows even if bond m a r k e t i n f l o w s r e m a i n subdued.

Major currencies have appreciated

At the start of the year, on fears o f “r e f l a t i o n t r a d e ” E M currencies were looking weak. However during the year, as the EM's continued to post robust growth, their currency and forex reserves positions improved. The usual suspect “Current account deficit”, also improved for most key EM's. Hence as we look into 2018, the EM currency basket seems substantially resilient (when compared in the last couple of years). With the commodity recovery story intact in midst of strong macro environment, EM's are set to deliver strong & s y n c h r o n i s e d p r i c e performance in 2018.

Equity corrections have reduced

Since the last few years the steady flows in the equity markets have restricted the equity downsides. Certain m a j o r d o w n s i d e s h a v e become on account of events like US rate hike, Election jitters in Euro.

32

DERIVATIVES STRATEGYFOR 2018

ICICIdirect Money Manager January 2018

Source: Bloomberg, ICICIdirect.com Research

Stocks witnessing accumulation pattern- Quant Picks for 2018

Source: Bloomberg, ICICIdirect.com Research

33

FLAVOUR OF THE MONTH

Investment Outlook 2018

ICICIdirect Money Manager January 2018

2017was a remarkable year for equities on both national and global fronts. While

Sensex delivered 29% returns, gold prices gained almost 10% amongst other

categories that offered positive returns in CY17. Will the good run continue for

2018? We asked a panel of industryexperts for their views on the year ahead and

also a look back on 2017. Let's take a look:

2018 India Equity Market Outlook –

On Your Mark, Get Set, 2019?

2018 will mark the fourth year

of the Modi Government in

office and the penultimate year

before the general elections

scheduled for April-May 2019.

With the Dec 2017 state

election victories for the

BJP/NDA in Gujarat and

Himachal Pradesh, markets

may heave a sigh of relief.

H o w e v e r, t h e q u e s t i o n

remains: Will the government

stick to the path of economic

reforms, or focus on politics

(read populism), before 2019?

We would place our bets on

reforms, and we base this on a

number of factors including –

(i) 19 out of 29 states in India

are now under BJP/NDA rule

potentially making it easier for

the ruling party to bring about

its reforms, (ii) several reforms

are on the anvil including

improvements to the Direct

Tax Code, e-way bill, real-

estate sector, banking sector

among others, (iii) the reform

agenda has been recognized

globally - India has jumped 30

spots in the World Bank's Ease

of Doing Business ranking, (iv)

stellar foreign inflows this year,

both FDI (+US$ 54.7bn till Oct-

end) and FPI (+US$ 8.5bn till

Nov-end), on the back of

reforms.

The Government reforms over

the past couple of years could

Anup Maheshwari,Executive Vice President and CIO- Equities, DSP BlackRock

34

FLAVOUR OF THE MONTH

ICICIdirect Money Manager January 2018

2018 India Equity Market Outlook –

On Your Mark, Get Set, 2019?

2018 will mark the fourth year

of the Modi Government in

office and the penultimate year

before the general elections

scheduled for April-May 2019.

With the Dec 2017 state

election victories for the

BJP/NDA in Gujarat and

Himachal Pradesh, markets

may heave a sigh of relief.

H o w e v e r, t h e q u e s t i o n

remains: Will the government

stick to the path of economic

reforms, or focus on politics

(read populism), before 2019?

We would place our bets on

reforms, and we base this on a

number of factors including –

(i) 19 out of 29 states in India

are now under BJP/NDA rule

potentially making it easier for

the ruling party to bring about

its reforms, (ii) several reforms

are on the anvil including

improvements to the Direct

Tax Code, e-way bill, real-

estate sector, banking sector

among others, (iii) the reform

agenda has been recognized

globally - India has jumped 30

spots in the World Bank's Ease

of Doing Business ranking, (iv)

stellar foreign inflows this year,

both FDI (+US$ 54.7bn till Oct-

end) and FPI (+US$ 8.5bn till

Nov-end), on the back of

reforms.

The Government reforms over

the past couple of years could

broadly be broken into three

main categories: a) Crackdown

on black money b) Financial

inclusion through Aadhaar and

Jan Dhan bank accounts and c)

Direct benefit transfer (DBT) of

subsidies. These are critical

long term structural reforms in

our view, the benefits of which

will be realized over the next

few years. And as we had

anticipated, these caused near

term pain to growth and

earnings.

However, this did not stop

Indian equities from rallying

sharply in 2017 - up ~36% in

USD terms or ~28% in INR

terms. The obvious question

has been on high valuations

and its sustainability. We think

this run up has been a part of

the broader EM rally and that

35

FLAVOUR OF THE MONTH

ICICIdirect Money Manager January 2018

India is not an outlier. Markets

are certainly at a high but

valuations are not. An earnings

catch-up could certainly help

sustain these valuations. We

expect corporate earnings to

see a broad based recovery in

FY19 and FY20. Along with the

positive base effect, a mix of

global cyclicals (metals), autos,

oil marketing companies and

banks may be the key drivers

for this.

After hitting a low of 5.7% in Q1

FY18, GDP growth recovered

to 6.3% in Q2 FY18, and we

expect the upward trend to

continue. With demonetization

behind us, implementation of ththe 7 pay commission along

with the higher government

spending on the rural segment

could help support demand.

This should benefit consumer

facing companies like staples,

consumer durables and other

under-penetrated sub sectors

which will also benefit from

initiatives on “Housing for All”

and “Power for All”.

On the investment front,

private sector capex may

remain subdued as corporates

continue to operate at lower

util izations of ~70%. For

reference, ~80% utilization

was the threshold for new

capex growth last time around.

However, new capex may be

r e p l a c e d b y i n o r g a n i c

acquisition of existing idle

capacities spurred by sales

through the National Company

Law Tribunal (NCLT). The onus

will then likely lie on the

G o v e r n m e n t t o d r i v e

investments. If private capex

does revive however, it is likely

to be swift, given the inherent

efficiencies of the private

sector.

Flows: We expect domestic

flows (led by mutual funds) to

continue to outpace foreign

flows for the fourth year in a

row in 2018, as India is finally

w i t n e s s i n g a s h i f t f r o m

physical to financial savings

which looks more structural.

EMs have seen equity inflows

of ~60 billion in 2017 so far

which is after four years of net

outflows from EMs. Global

p o r t f o l i o m a n a g e r s a r e

36

FLAVOUR OF THE MONTH

ICICIdirect Money Manager January 2018

underweight EM equities,

l e a v i n g m o r e r o o m f o r