icecap february 2011 global market outlook

TRANSCRIPT

7/21/2019 IceCap February 2011 Global Market Outlook

http://slidepdf.com/reader/full/icecap-february-2011-global-market-outlook 1/8

Our view on global investment markets:

February 2011: The Long Bond Con

Keith Dicker, CFA

Chief Investment Officer

www.IceCapAssetManagement.com

First publication June 2010

7/21/2019 IceCap February 2011 Global Market Outlook

http://slidepdf.com/reader/full/icecap-february-2011-global-market-outlook 2/8

2

“Con man” is a term for Confidence Man – in his usual role, the con

man does something to gain someone’s trust or confidence and then

when the person is least expecting it, the con man steals some formof wealth from the unsuspecting victim.

There are two types of cons – the short con and the long con. The

short con refers to a theft that occurs relatively quickly, like the card

game on the street corner.

The long con however is much more elaborate and requires more skill

and patience. To pull off a successful long con, the con man needs

help from other con men as well as many months of preparation.

The key difference between the two is the potential payout. While

the short con steals dollar bills from his victims, the long con is

looking for a 7 figure payday.

The greatest long cons to come out of Hollywood naturally include

the 1973 Oscar winning “The Sting” featuring a young Robert Redford

and Paul Newman, as well as the 1988 hit “Dirty Rotten Scoundrels”

supported by Steve Martin & Michael Caine.

Unfortunately for the World, today we are also experiencing another

long con and it’s in the bond market. This is a very dangerous con and

the victims have no idea it is occurring.

Redford & Newman excelled at this game

22www.IceCapAssetManagement.com

February 2011: The Long Bond Con

The Debt Bomb

Much has already been written about the debt problem that exists in

the World today. This is a good thing. Everyone should be made awarethat the entire Western World has been living beyond its means and

that the time has come for everyone to pull up their socks, pants and

knickers and become fiscally prudent. While the Americans, British,

Irish, Spanish and the Greeks discovered the hard way that they can no

longer use their house as an ATM to withdraw cash at will – others

including Canadians and Australians are not that far off from

potentially experiencing déjà vu.

A little bit of debt is a good thing. Otherwise, you’d have to pay 100%cash down for your car, scooter or house – and unless you are an

investment banker with Goldman Sachs, most people seldom find an

extra $200,000 sleeping in the bottom of their pocket. This is where

the banks step in and provide a vital service for the World’s economy.

The unfortunate part of this story is that banks are also profit seeking

companies which incentivizes them to lend, lend and then lend some

more – it’s fair to say this kind act is a part of their DNA (why else

would they lead people to financial ruin?). What makes thisunfortunate is that banks the World over have provided easy access to

credit and therefore encouraged people to borrow, borrow, borrow so

that they can spend, spend, spend.

While individuals have started to pay down their debt, the fiscal

management skills of most governments is (and we’ll try to say this

7/21/2019 IceCap February 2011 Global Market Outlook

http://slidepdf.com/reader/full/icecap-february-2011-global-market-outlook 3/8

3

The tipping point

33www.IceCapAssetManagement.com

politely) – crap. It’s a fact that politicians do not spend their money,

they much prefer to spend your money and lots of it. At the same

time, politicians are not particularly fond of raising taxes either – this

act has been a time-proven strategy of how not to be re-elected.

The result is that year-after-year-after-year, the difference between

what they have spent and what they have collected from taxes is

negative, resulting in one big fiscal deficit. Subsequently, the only way

for countries to continue to provide the services to which we have

become accustomed is to borrow money each year.

For an individual, this is equivalent to receiving a salary of $100,000/year, but then to turn around and spend $110,000. Repeat

the insanity again the following year and the year after that. The

tipping point is reached when the banks no longer answer your phone

call for more loans. The outcome is simple, either you learn how to

make more money, or you dramatically change your spendthrift ways.

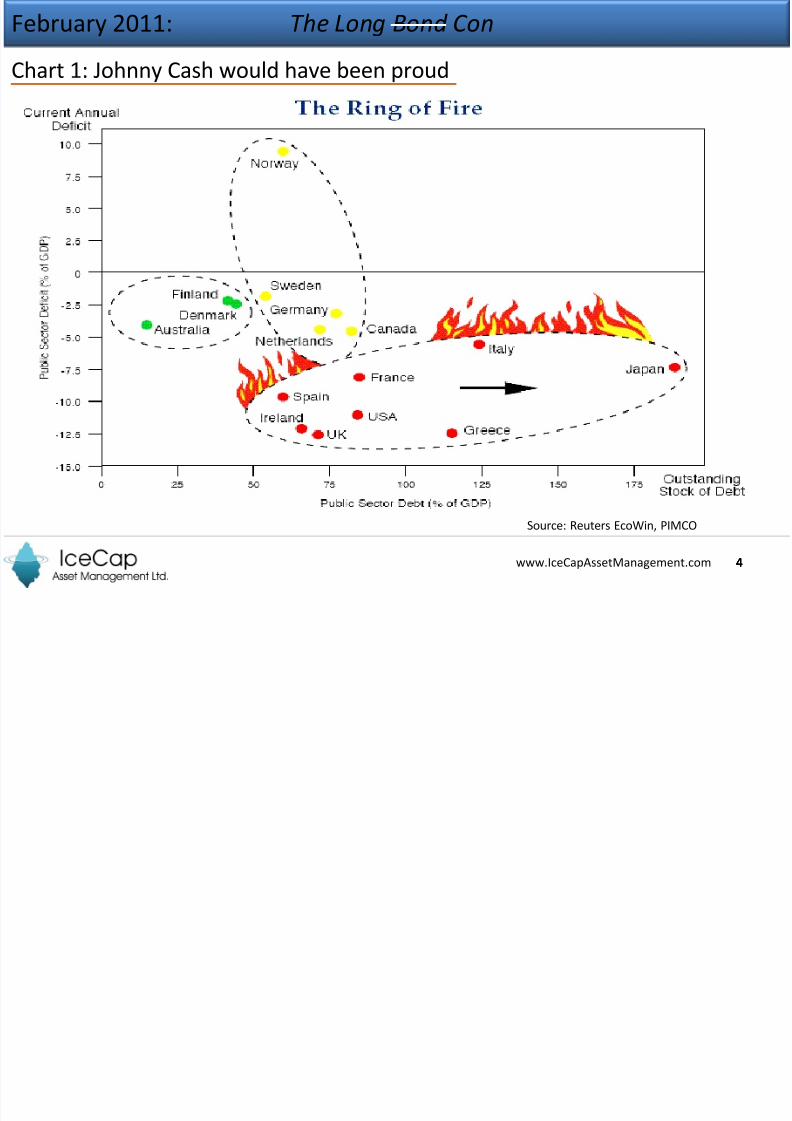

Countries are no different (see Chart 1 on next page). Most have been

growing their fiscal deficits for years with no restraints in sight. The

result has been astronomical growth in outstanding debt. The day of reckoning should have occurred a few years ago; the only saving grace

was low interest rates. The very same low interest rates that allowed

individuals to borrow recklessly were also available for countries to

grow recklessly – the difference being...well, there are no differences.

Sooner or later, countries will also have to face the Reaper and repay

their debts.

This is where the Long Con comes in to play. Central bankers in the US,

Europe, Britain and Japan (and hopefully at least a few elected

government representatives) fully understand that some day they’ll

have to pay back the debt they owe. They also know that it is virtually

impossible to fix their deficit overnight, and therefore the amount of

money they need to borrow continues to increase. The result is that

the only way out of the mess is to try to keep the cost of borrowing as

low as possible for as long as possible.

The con therefore is to keep short-term rates as close to zero as

possible, while printing money to keep longer-term interest rates as

low as possible.

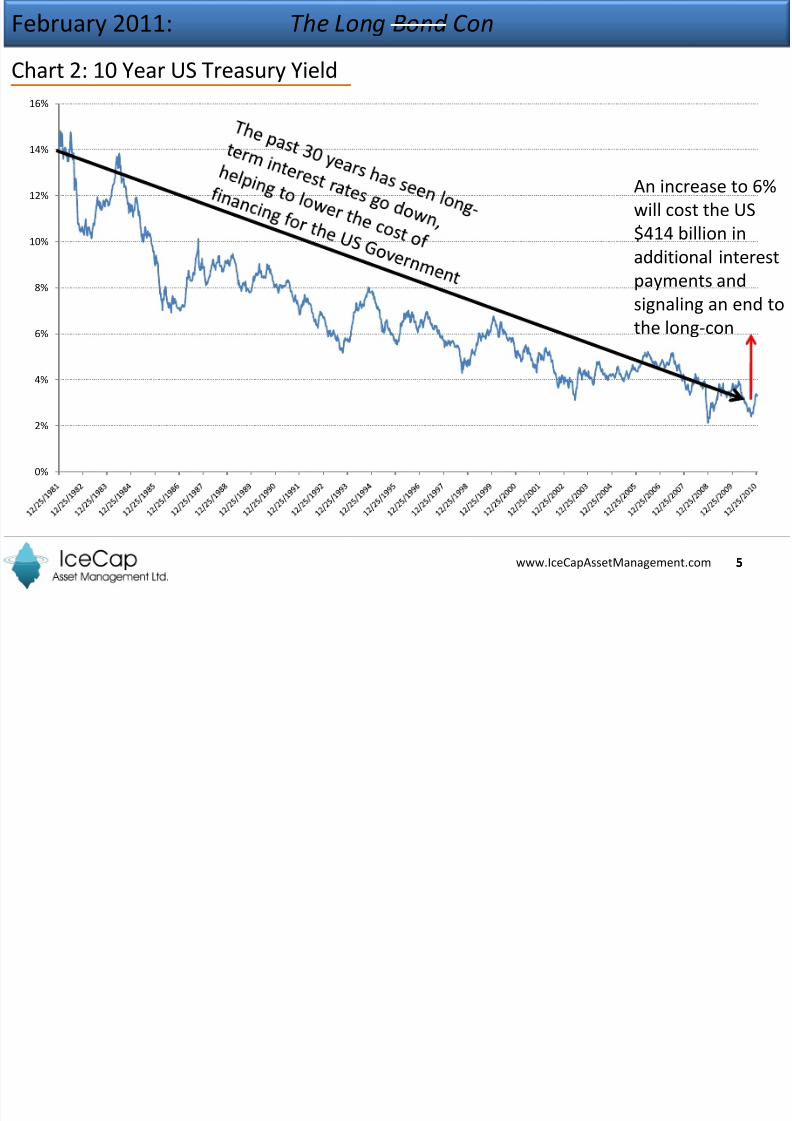

To understand the financial benefit, let’s simplify the numbers. The US

is currently paying about $414 billion/year in interest. Yes, $414 billion

– you can buy a lot of Cosmopolitan magazines with that much money.

The obligation to pay $414 billion is based upon a borrowing rate of

2.99%. What keeps people awake at night is the following question –

what happens if interest rates increase from 2.99% to 4.5%, or what if

they double to 6% (see chart 2 on page 5)? All else being equal, the

math is pretty easy as the interest paid increases to $621 billion and$828 billion respectively.

We can all be excused for being stunned by these large numbers,

however the key point to remember is that everyone, and every

country has a tipping point – a critical moment when something has to

change. The potential for long term interest rates to rise substantially

has pushed many countries to the tipping point.

February 2011: The Long Bond Con

7/21/2019 IceCap February 2011 Global Market Outlook

http://slidepdf.com/reader/full/icecap-february-2011-global-market-outlook 4/8

4

Chart 1: Johnny Cash would have been proud

444www.IceCapAssetManagement.com

Source: Reuters EcoWin, PIMCO

February 2011: The Long Bond Con

7/21/2019 IceCap February 2011 Global Market Outlook

http://slidepdf.com/reader/full/icecap-february-2011-global-market-outlook 5/8

5

0%

2%

4%

6%

8%

10%

12%

14%

16%

Chart 2: 10 Year US Treasury Yield

555www.IceCapAssetManagement.com

An increase to 6%

will cost the US

$414 billion in

additional interest

payments andsignaling an end to

the long-con

February 2011: The Long Bond Con

7/21/2019 IceCap February 2011 Global Market Outlook

http://slidepdf.com/reader/full/icecap-february-2011-global-market-outlook 6/8

6

Core Inflation

The ability to objectively assess the credibility of any profession lies

within the skill (or willingness) to make fun of yourself. It ’s a given that

lawyers, doctors, mechanics and teachers all have a chuckle about

their misgivings while enjoying their end-of-week drinks – this is

perfectly healthy. In the investment World, and more specifically

within the imaginary World of economics, this ability has gone AWOL.

The reason for this unexcused absence of sanity – core inflation. Let us

explain.

The financial services industry bombards us with data on a daily,

weekly, monthly, quarterly and annual basis. If that isn’t enough, wehave CNBC blaring every second of the day. Some of the data is quite

important and market moving, while other data is useless.

Probably one of the most important data points released is the

monthly CPI (Consumer Price Index) report. This data tells us if the

price of stuff is going up or down. If prices are going down, stocks and

bonds act silly. If prices are going up, stocks and bonds also act silly.

With all of this silliness happening, you just knew someone would try

to act like an adult and try to restore some common sense to thesituation. The problem is, the adult turned out to be an economist

who never ever had end-of-the-week drinks with his co-workers. This

defiant act allowed him to conjure the most silly economic data of all –

“core” inflation.

The objective of core inflation is to produce a monthly number that

would put a stop to all of the silliness in the stock and bond markets.

Happy hour should be mandatory

February 2011: The Long Bond Con

666www.IceCapAssetManagement.com

However, the only silliness that now exists is the method of calculating

“core” inflation. To arrive at this magical number, economists have

decided to eliminate from the calculation any input that actually

fluctuates. This will ensure the World (and CNBC) will report a stable

number each month. If that isn’t enough, they have even decided to

report inflation to the 3rd decimal point – you can’t make that up.

The result? In the USA housing prices, energy prices and food prices

are all eliminated from the Core CPI report. Does this make sense? Of

course not. I’m pretty confident that every American can tell you that

their heating and grocery bills are paid with real money on a regular

basis. If gas hits $4 per gallon, inflation is definitely present.

The silliness is even sillier in Japan as they have decided to exclude, get

ready for this, “sushi” from some of their inflation calculations. Yes,

you can’t make that up either.

Many products and services in the Western World have not seen price

increases and this is reflected in the “core” inflation data. Without a

doubt, economists and central bankers happily drift off to sleep every

night with this data under their pillow. Meanwhile, everyone else onthe planet is awake worried about higher energy prices and higher

food prices. In the real World, inflation is very much alive and it is

affecting the quality of life for many.

7/21/2019 IceCap February 2011 Global Market Outlook

http://slidepdf.com/reader/full/icecap-february-2011-global-market-outlook 7/8

7

Hope has never been a good strategy

February 2011: The Long Bond Con

777www.IceCapAssetManagement.com

How is this related to the Long Con

Let’s not forget – the World’s economy is at a critical juncture; saddled

with 0% interest rates, money printing by central banks and

uncontrollable fiscal deficits. There are only two outcomes possible:

1) A return to a normal economy

2) Or something very different

Central banks have already demonstrated that they can keep short-

term interest rates very low for a very long time. The con that keeps

long-term rates low is the real game to watch. An unsuccessful

outcome will have the undesirable effect of seeing the cost to borrow

skyrocket, with the net effect being a decline in your standard of living.

The irony is that if long-term rates continue to rise, the Federal

Reserve and the European Central Bank will be forced to buy even

more long-term bonds in an effort to keep long-term rates lower (yes,

QE3 may be here before you know it). This effort to keep rates down is

equivalent to holding a basketball underneath water – at some point

your arms grow tired and the ball will explode upwards, exactly the

same way long-term rates will react to continued interference by

central banks.

Unfortunately, the World today is truly a small place, and the cheap

money being produced in the Western World is being exported to

emerging markets resulting in a gasoline-on-fire effect for their

economies. The result? Significantly higher food and energy prices.

And there you have it; the identification of the con man should be no

surprise to anyone – it is the central banks of the United States, the

European Union, Japan and Britain. The con is to keep long-term rates

as low as possible, the victims in this case are everyone on the planet

who will inevitably be exposed to sky rocketing rates at some point. In

Hollywood, we all cheered for Robert Redford and Paul Newman to

pull off the con. In today’s World, let’s all pray that Bernanke and

Trichet are not able to accomplish the same feat.

European Credit Crisis

IceCap has written about the malaise of the European banking system

and sovereign debt crisis now on several occasions. Our view has not

changed.

While Egypt has certainly (and justifiably so) dominated the news, the

European financial crisis continues. Next up is Portugal, who despite

their heroic attempts to calm markets will require a bailout within

hours. There is also a concern that the outcome of the upcoming Irish

election may place strains on their “agreement” to accept their

bailout. Belgium is also on the list – as are the original perpetrators –

the Greeks.

While this may all sound confusing, the only fact investors need to

understand is that each bailout is a financial transaction to ensure

bond investors do not lose any of their money. The other salient point

is that the bond investors being saved are mostly other European

banks. The bailouts have effectively become a transfer of wealth from

the tax payers to the banks. While many believe all is fine in Europe

these days, we think otherwise.

7/21/2019 IceCap February 2011 Global Market Outlook

http://slidepdf.com/reader/full/icecap-february-2011-global-market-outlook 8/8

8

Kick the can

88www.IceCapAssetManagement.com

The Arab World

The speed of which events are sweeping across north Africa, the

Middle East (and now China) has caught everyone off guard. The

suggestion that both Tunisia and Egypt would have kicked-out out their

dictators over a 3 week period would have been laughed at by the

World’s elite if it hadn’t happened.

Understandably, chaos and havoc is escalating within the region –

however, chaos and havoc of a different kind is happening at the

Pentagon. The Americans have been involved in the Middle East for a

long time and have established allies of varying degrees, most notably

with Egypt and Bahrain. The point we make is that those who believe

these events are either “over” or don’t affect them may be dearly

wrong. The blueprint for how the game is played is changing and

worse still, no one will know the rules or the players until the dust has

settled.

Whereas financial markets have decided to shrug-off the news, energy

and agricultural commodities are rising. We do not know the eventual

outcome, however we do acknowledge (and respect) that the

probability of oil supplies being disrupted are considerably highertoday than 8 weeks ago. The same can be said for various food

commodities. The point we make, is that the complacency shown by

the stock market may be misplaced and should be monitored closely.

Our Strategy

In previous publications, we have detailed the dangerous balancing act

being orchestrated by the central banks and governments. On one side

of the axis we see the real economy which remains at stall speed,

while the other side is drugged up on unprecedented monetary and

fiscal stimuli; the most recent addition being the $850 billion tax

package in the US and the European bailout of Portugal.

The “dangerous” part of this act is the deteriorating fiscal deficit of

much of the developed world. The Americans will now have an

accumulated fiscal deficit of about 96% of GDP, a level that has not

been seen for over 65 years – now that’s progress! The can has been

kicked down the road for another year, and we only hope the private

sector is able to pull its weight once the governments are unable to

continue with their money printing and spending ways.

As a result, the game or con has squarely shifted to the bond market

and more specifically longer-term bonds. While main stream media

are very capable of reporting rioting in Tunisia, Greece and Spain – we

look forward to see how they handle rioting in the bond market should

governments fail to get a grip on reality.

Our strategy hasn’t changed that much, we continue to hold gold inour portfolios. This strategy will provide insurance and protection

against being burned by wayward government policies, while we

remain cognizant of the desire for stock markets to go higher. Our

growth strategies are focused on the commodity related strategies in

both our stock and commodity portfolios. Agricultural commodity ETFs

continue to trend higher and this obviously makes us and our clients

happy.

February 2011: The Long Bond Con